Private Federated Learning Without a Trusted Server: Optimal Algorithms for Convex Losses

Abstract

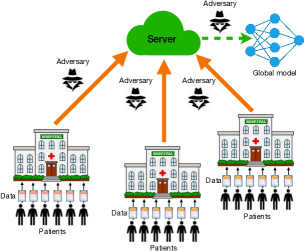

This paper studies federated learning (FL)—especially cross-silo FL—with data from people who do not trust the server or other silos. In this setting, each silo (e.g. hospital) has data from different people (e.g. patients) and must maintain the privacy of each person’s data (e.g. medical record), even if the server or other silos act as adversarial eavesdroppers. This requirement motivates the study of Inter-Silo Record-Level Differential Privacy (ISRL-DP), which requires silo ’s communications to satisfy record/item-level differential privacy (DP). ISRL-DP ensures that the data of each person (e.g. patient) in silo (e.g. hospital ) cannot be leaked. ISRL-DP is different from well-studied privacy notions. Central and user-level DP assume that people trust the server/other silos. On the other end of the spectrum, local DP assumes that people do not trust anyone at all (even their own silo). Sitting between central and local DP, ISRL-DP makes the realistic assumption (in cross-silo FL) that people trust their own silo, but not the server or other silos. In this work, we provide tight (up to logarithms) upper and lower bounds for ISRL-DP FL with convex/strongly convex loss functions and homogeneous (i.i.d.) silo data. Remarkably, we show that similar bounds are attainable for smooth losses with arbitrary heterogeneous silo data distributions, via an accelerated ISRL-DP algorithm. We also provide tight upper and lower bounds for ISRL-DP federated empirical risk minimization, and use acceleration to attain the optimal bounds in fewer rounds of communication than the state-of-the-art. Finally, with a secure “shuffler” to anonymize silo messages (but without a trusted server), our algorithm attains the optimal central DP rates under more practical trust assumptions. Numerical experiments show favorable privacy-accuracy tradeoffs for our algorithm in classification and regression tasks.

1 Introduction

Machine learning tasks often involve data from different “silos” (e.g. cell-phone users or organizations such as hospitals) containing sensitive information (e.g. location or health records). In federated learning (FL), each silo (a.k.a. “client”) stores its data locally and a central server coordinates updates among different silos to achieve a global learning objective (Kairouz et al., 2019). One of the primary reasons for the introduction of FL was to offer greater privacy (McMahan et al., 2017). However, storing data locally is not sufficient to prevent data leakage. Model parameters or updates can still reveal sensitive information (e.g. via model inversion attacks or membership inference attacks) (Fredrikson et al., 2015; He et al., 2019; Song et al., 2020; Zhu & Han, 2020).

Differential privacy (DP) (Dwork et al., 2006) protects against privacy attacks. Different notions of DP have been proposed for FL. The works of Jayaraman & Wang (2018); Truex et al. (2019); Noble et al. (2022) considered central DP (CDP) FL, which protects the privacy of silos’ aggregated data against an external adversary who observes the final trained model.111We abbreviate central differential privacy by CDP. This is different than the concentrated differential privacy notion in Bun & Steinke (2016), for which the same abbreviation is sometimes used in other works. There are two major issues with CDP FL: 1) it does not guarantee privacy for each specific silo; and 2) it does not guarantee data privacy when an adversarial eavesdropper has access to other silos or the server. To address the first issue, McMahan et al. (2018); Geyer et al. (2017); Jayaraman & Wang (2018); Gade & Vaidya (2018); Wei et al. (2020a); Zhou & Tang (2020); Levy et al. (2021); Ghazi et al. (2021) considered user-level DP (a.k.a. client-level DP). User-level DP guarantees privacy of each silo’s full local data set. This is a practical notion for cross-device FL, where each silo/client corresponds to a single person (e.g. cell-phone user) with many records (e.g. text messages). However, user-level DP still suffers from the second critical shortcoming of CDP: it allows silo data to be leaked to an untrusted server or to other silos. Furthermore, user-level DP is less suitable for cross-silo FL, where silos are typically organizations (e.g. hospitals, banks, or schools) that contain data from many different people (e.g. patients, customers, or students). In cross-silo FL, each person has a record (a.k.a. “item”) that may contain sensitive data. Thus, an appropriate notion of DP for cross-silo FL should protect the privacy of each individual record (“item-level DP”) in silo , rather than silo ’s full aggregate data.

Another notion of DP is local DP (LDP) (Kasiviswanathan et al., 2011; Duchi et al., 2013). While central and user-level DP assume that people trust all of the silos and the server, LDP assumes that individuals (e.g. patients) do not trust anyone else with their sensitive data, not even their own silo (e.g. hospital). Thus, LDP would require each person (e.g. patient) to randomize her report (e.g. medical test results) before releasing it (e.g. to their own doctor/hospital). Since patients/customers/students usually trust their own hospital/bank/school, LDP may be unnecessarily stringent, hindering performance/accuracy.

In this work, we consider a privacy notion called inter-silo record-level differential privacy (ISRL-DP), which requires that all of the communications of each silo satisfy (item-level) DP; see Fig. 1. By the post-processing property of DP, this also ensures that the the broadcasts by the server and the global model are DP. Privacy notions similar or identical to ISRL-DP have been considered in Truex et al. (2020); Huang et al. (2020); Huang & Gong (2020); Wu et al. (2019); Wei et al. (2020b); Dobbe et al. (2020); Zhao et al. (2020); Arachchige et al. (2019); Seif et al. (2020); Liu et al. (2022). We provide a rigorous definition of ISRL-DP in Definition 2 and Appendix B.

Why ISRL-DP? ISRL-DP is the natural notion of DP for cross-silo FL, where each silo contains data from many individuals who trust their own silo but may not trust the server or other silos (e.g., hospitals in Fig. 1). The item-level privacy guarantee that ISRL-DP provides for each silo (e.g. hospital) ensures that no person’s record can be leaked. In contrast to central DP and user-level DP, the protection of ISRL-DP is guaranteed even against an adversary with access to the server and/or other silos (e.g. hospitals). This is because each silo’s communications are DP with respect to their own data records and cannot leak information to any adversarial eavesdropper. On the other hand, since individuals (e.g. patients) trust their own silo (e.g. hospital), ISRL-DP does not require individuals to randomize their own data reports (e.g. health records). Thus, ISRL-DP leads to better performance/accuracy than local DP by relaxing the strict local DP requirement. Another benefit of ISRL-DP is that each silo can set its own item-level DP budget depending on its privacy needs; see Appendix H and also Liu et al. (2022); Aldaghri et al. (2021).

In addition, ISRL-DP can be useful in cross-device FL without a trusted server: If the ISRL privacy parameters are chosen sufficiently small, then ISRL-DP implies user-level DP (see Appendix C). Unlike user-level DP, ISRL-DP does not allow data to be leaked to the untrusted server/other users.

Another intermediate trust model between the low-trust local model and the high-trust central/user-level models is the shuffle model of DP (Bittau et al., 2017; Cheu et al., 2019). In this model, a secure shuffler receives noisy reports from the silos and randomly permutes them before the reports are sent to the untrusted server.222Assume that the reports can be decrypted by the server, but not by the shuffler Erlingsson et al. (2020a); Feldman et al. (2020b). An algorithm is Shuffle Differentially Private (SDP) if silos’ shuffled messages are CDP; see Definition 3. Fig. 2 summarizes which parties are assumed to be trustworthy (from the perspective of a person contributing data to a silo) in each of the described privacy notions.

Problem setup: Consider a FL setting with silos, each containing a local data set with samples:333In Appendix H, we consider the more general setting where data set sizes and ISRL-DP parameters may vary across silos, and the weights on each silo’s loss in 2 may differ (i.e. ). for . In each round of communication , silos download the global model and use their local data to improve the model. Then, silos send local updates to the server (or other silos, in peer-to-peer FL), who updates the global model to . For each silo , let be an unknown probability distribution on a data universe (i.e. ). Let Given a loss function , define silo ’s local objective as

| (1) |

where is a parameter domain. Our goal is to find a model parameter that performs well for all silos, by solving the FL problem

| (2) |

while maintaining the privacy of each silo’s local data. At times, we will focus on empirical risk minimization (ERM), where is silo ’s local objective. Thus, in the ERM case, our goal is to solve , while maintaining privacy. When takes the form 1 (not necessarily ERM), we may refer to the problem as stochastic convex optimization (SCO) for emphasis. For ERM, we make no assumptions on the data; for SCO, we assume the samples are drawn independently. For SCO, we say problem 2 is “i.i.d.” or “homogeneous” if and , The excess risk of an algorithm for solving 2 is , where and the expectation is taken over both the random draw of and the randomness of . For ERM, the excess empirical risk of is , where the expectation is taken solely over the randomness of . Thus, a fundamental question in FL is about the minimum achievable excess risk while maintaining privacy. In this work, we specifically study the following questions for FL with convex and strongly convex loss functions:444Function is -strongly convex () if and all sub-gradients . If is convex.

Question 1. What is the minimum achievable excess risk for solving 2 with inter-silo record-level DP? Question 2. With a trusted shuffler (but no trusted server), can the optimal central DP rates be attained?

Contributions: Our first contribution is a complete answer to Question 1 when silo data is i.i.d.: we give tight upper and lower bounds in Section 2. The ISRL-DP rates sit between the local DP and central DP rates: higher trust allows for higher accuracy. Further, we show that the ISRL-DP rates nearly match the optimal non-private rates if , where is the ISRL-DP parameter (“privacy for free”). As a corollary of our analysis, we also derive tight upper and lower bounds for FL algorithms that satisfy both ISRL-DP and user-level DP simultaneously, which could be useful in cross-device settings where (e.g. cell phone) users don’t trust the server or other users with their sensitive data (e.g. text messages): see Section D.3.5.

Second, we give a complete answer to Question 1 when is an empirical loss in Section 4.555ERM is a special case of the FL problem 2: if is the empirical distribution on , then . While (Girgis et al., 2021) provided a tight upper bound for the (non-strongly) convex case, we use a novel accelerated algorithm to achieve this upper bound in fewer communication rounds. Further, we obtain matching lower bounds. We also cover the strongly convex case.

Third, we give a partial answer to Question 1 when silo data is heterogeneous (non-i.i.d.), providing algorithms for smooth that nearly achieve the optimal i.i.d. rates in Section 3. For example, if is -strongly convex and -smooth, then the excess risk of our algorithm nearly matches the i.i.d. lower bound up to a multiplicative factor of . Our algorithm is significantly more effective (in terms of excess risk) than existing ISRL-DP FL algorithms (e.g. Arachchige et al. (2019); Dobbe et al. (2020); Zhao et al. (2020)): see Appendix A for a thorough discussion of related work.

Fourth, we address Question 2 in Section 5: We give a positive answer to Question 2 when silo data is i.i.d. Further, with heterogeneous silo data, the optimal central DP rates are nearly achieved without a trusted server, if the loss function is smooth. We summarize our results in Fig. 3.

1.1 Preliminaries

Differential Privacy: Let and be a distance between databases. Two databases are -adjacent if . DP ensures that (with high probability) an adversary cannot distinguish between the outputs of algorithm when it is run on adjacent databases:

Definition 1 (Differential Privacy).

Let A randomized algorithm is -differentially private (DP) (with respect to ) if for all -adjacent data sets and all measurable subsets , we have

| (3) |

Definition 2 (Inter-Silo Record-Level Differential Privacy).

Let , , . A randomized algorithm is -ISRL-DP if for all and all -adjacent silo data sets , the full transcript of silo ’s sent messages satisfies 3 for any fixed settings of other silos’ messages and data.

Definition 3 (Shuffle Differential Privacy (Bittau et al., 2017; Cheu et al., 2019)).

A randomized algorithm is -shuffle DP (SDP) if for all -adjacent databases and all measurable subsets , the collection of all uniformly randomly permuted messages that are sent by the shuffler satisfies 3, with .

Notation and Assumptions: Let be the norm and denote the projection operator. Function is -Lipschitz if , A differentiable function is -smooth if its derivative is -Lipschitz. If is -smooth and -strongly convex, denote its condition number by . For differentiable (w.r.t. ) , we denote its gradient w.r.t. by . Write if such that Write if for some parameters . Assume the following throughout:

Assumption 1.

-

1.

is closed, convex, and , .

-

2.

is -Lipschitz and convex for all . In some parts of the paper, we assume is -strongly convex.

-

3.

for all .

-

4.

In each round , a uniformly random subset of silos is available to communicate with the server, where are independent random variables with .

In Assumption 1 part 4, the network determines : it is not a design parameter. This assumption is more general (and realistic for cross-device FL (Kairouz et al., 2019)) than most (DP) FL works, which usually assume or is deterministic. On the other hand, in cross-silo FL, typically all silos can reliably communicate in each round, i.e. (Kairouz et al., 2019).

2 Inter-Silo Record-Level DP FL with Homogeneous Silo Data

In this section, we provide tight (up to logarithms) upper and lower bounds on the excess risk of ISRL-DP algorithms for FL with i.i.d. silo data. For consistency of presentation, we assume that there is an untrusted server. However, our algorithms readily extend to peer-to-peer FL (no server), by having silos send private messages directly to each other and perform model updates themselves.

2.1 Upper Bounds via Noisy Distributed Minibatch SGD

We begin with our upper bounds, obtained via Noisy Distributed Minibatch SGD (MB-SGD): In each round , all available silos receive from the server and send noisy stochastic gradients to the server: where and are drawn uniformly from (and then replaced). The server averages these reports and updates . After rounds, a weighted average of the iterates is returned: with With proper choices of , , , and , we have:

Theorem 2.1 (Informal).

Let .

Then

Noisy MB-SGD

is -ISRL-DP. Moreover:

1. If is convex, then

| (4) |

2. If is -strongly convex, then

| (5) |

The first terms in each of 4 and 5 ( for convex and for strongly convex) are bounds on the uniform stability (Bousquet & Elisseeff, 2002) of Noisy MB-SGD. We use these uniform stability bounds to bound the generalization error of our algorithm. Our stability bound for in Lemma D.2 is novel even for . The second terms in 4 and 5 are bounds on the empirical risk of the algorithm. We use Nesterov smoothing (Nesterov, 2005) to extend our bounds to non-smooth losses. This requires us to choose a different stepsize and from Bassily et al. (2019) (for ), which eliminates the restriction on the smoothness parameter that appears in (Bassily et al., 2019, Theorem 3.2).666In (Bassily et al., 2019), the number of iterations is denoted by , rather than . Privacy of Noisy MB-SGD follows from the Gaussian mechanism (Dwork & Roth, 2014, Theorem A.2), privacy amplification by subsampling (Ullman, 2017), and advanced composition (Dwork & Roth, 2014, Theorem 3.20) or moments accountant (Abadi et al., 2016, Theorem 1). See Section D.2 for the detailed proof.

2.2 Lower Bounds

We provide excess risk lower bounds for the case , establishing the optimality of Noisy MB-SGD for two function classes: ; and . We restrict attention to distributions satisfying Assumption 1, part 3. The -ISRL-DP algorithm class contains all sequentially interactive algorithms and all fully interactive, -compositional (defined in Section D.3) algorithms.777Sequentially interactive algorithms can query silos adaptively in sequence, but cannot query any one silo more than once. Fully interactive algorithms can query each silo any number of times. See (Joseph et al., 2019) for further discussion. If is sequentially interactive or -compositional, write . The vast majority of DP algorithms in the literature are -compositional. For example, any algorithm that uses the strong composition theorems of (Dwork & Roth, 2014; Kairouz et al., 2015; Abadi et al., 2016) for its privacy analysis is -compositional: see Section D.3.2. In particular, Noisy MB-SGD is -compositional, hence it is in .

Theorem 2.2 (Informal).

Let

, , and . Then:

1. There exists a and a distribution such that for , we have:

2. There exists a -smooth and distribution such that for , we have

Further, if , then the above lower bounds hold with .

The lower bounds for are nearly tight888Up to logarithms, a factor of , and for strongly convex case–a factor of . If , then the ISRL-DP algorithm that outputs any attains the matching upper bound by Theorem 2.1. The first term in each of the lower bounds is the optimal non-private rate; the second terms are proved in Section D.3.4. In particular, if , then the non-private term in each bound is dominant, so the ISRL-DP rates match the respective non-private rates, resulting in “privacy for free” (Nemirovskii & Yudin, 1983). The ISRL-DP rates sit between the rates for LDP and CDP: higher trust allows for higher accuracy. For example, for , the LDP rate is (Duchi et al., 2013), and the CDP rate is (Bassily et al., 2019).

Theorem 2.2 is more generally applicable than existing LDP and CDP lower bounds. When , ISRL-DP is equivalent to LDP and Theorem 2.2 recovers the LDP lower bounds (Duchi et al., 2013; Smith et al., 2017). However, Theorem 2.2 holds for a wider class of algorithms than the lower bounds of (Duchi et al., 2013; Smith et al., 2017), which were limited to sequentially interactive LDP algorithms. When , ISRL-DP is equivalent to CDP and Theorem 2.2 recovers the CDP lower bounds (Bassily et al., 2019).

Obtaining our more general lower bounds under the more complex notion of ISRL-DP is challenging. The lower bound approaches of (Duchi et al., 2013; Smith et al., 2017; Duchi & Rogers, 2019) are heavily tailored to LDP and sequentially interactive algorithms. Further, the applicability of the standard CDP lower bound framework (e.g. (Bassily et al., 2014; 2019)) to ISRL-DP FL is unclear.

In light of these challenges, we take a different approach to proving Theorem 2.2: We first analyze the central DP guarantees of when silo data sets are shuffled in each round, showing that CDP amplifies to . We could not have concluded this from existing amplification results (Erlingsson et al., 2020b; Feldman et al., 2020b; Balle et al., 2019; Cheu et al., 2019; Balle et al., 2020) since these results are all limited to sequentially interactive LDP algorithms and . Thus, we prove the first privacy amplification by shuffling bound for fully interactive ISRL-DP FL algorithms. Then, we apply the CDP lower bounds of Bassily et al. (2019) to , the “shuffled” version of . This implies that the shuffled algorithm has excess population loss that is lower bounded as in Theorem 2.2. Finally, we observe that the i.i.d. assumption implies that and have the same expected population loss. Note that our proof techniques can also be used to obtain ISRL-DP lower bounds for other problems in which a CDP lower bound is known.

3 Inter-Silo Record-Level DP FL with Heterogeneous Silo Data

Consider the non-i.i.d. FL problem, where takes the form 1 for some unknown distributions on , . The uniform stability approach that we used to obtain our i.i.d. upper bounds does not work in this setting.999Specifically, Lemma D.1 in Appendix D does not apply without the i.i.d. assumption. Instead, we directly minimize

by modifying Noisy MB-SGD as follows:

1. We draw disjoint batches of

local samples without replacement from each silo

and set . Thus,

stochastic gradients are independent across iterations, so our bounds apply to .

2. We use acceleration (Ghadimi & Lan, 2012) to increase the convergence rate.

3. To provide ISRL-DP, we re-calibrate and

apply parallel composition (McSherry, 2009).

After these modifications, we call the resulting algorithm One-Pass Accelerated Noisy MB-SGD. It is described in Algorithm 1. In the strongly convex case, we use a multi-stage implementation of One-Pass Accelerated Noisy MB-SGD (inspired by (Ghadimi & Lan, 2013)) to further expedite convergence: see Section E.1 for details.

Carefully tuning step sizes, , and yields:

Theorem 3.1 ( case).

Let be

-smooth for all

Assume . Then One-Pass Accelerated Noisy MB-SGD is -ISRL-DP. Moreover, if , then:

1. For convex , we have

| (6) |

2. For -strongly convex with , we have

| (7) |

Remarkably, the bound 7 nearly matches the optimal i.i.d. bound 5 up to the factor . In particular, for well-conditioned loss functions, our algorithm achieves the optimal i.i.d. rates even when silo data is arbitrarily heterogeneous. The gap between the bound 6 and the i.i.d. bound 4 is . Closing the gaps between the non-i.i.d. upper bounds in Theorem 3.1 and the i.i.d. lower bounds in Theorem 2.2 is left as an open problem. Compared to previous upper bounds, Theorem 3.1 is a major improvement: see Appendix A for details.

In Section E.2, we provide a general version (and proof) of Theorem 3.1 for . If but is sufficiently large or silo heterogeneity sufficiently small, then the same bounds in Theorem 3.1 hold with replaced by . Intuitively, the case is harder when data is highly heterogeneous, since stochastic estimates of will have larger variance. In Lemma E.3 (Section E.2), we use a combinatorial argument to bound the variance of stochastic gradients.

4 Inter-Silo Record-Level DP Federated ERM

In this section, we provide an ISRL-DP FL algorithm, Accelerated Noisy MB-SGD, with optimal excess empirical risk. The difference between our proposed algorithm and One-Pass Accelerated Noisy MB-SGD is that silo now samples from with replacement in each round: see line 6 in Algorithm 1. This allows us to a) amplify privacy via local subsampling and advanced composition/moments accountant, allowing for smaller ; and b) run more iterations of our algorithm to better optimize . These modifications are necessary for obtaining the optimal rates for federated ERM. We again employ Nesterov smoothing (Nesterov, 2005) to extend our results to non-smooth .

Theorem 4.1 (Informal).

Let .

Then, there exist algorithmic parameters such that

Algorithm 1 is -ISRL-DP and:

1. If is convex, then

| (8) |

2. If is -strongly convex then

| (9) |

See Section F.1 for the formal statement and proof. With non-random , Girgis et al. (2021) provides an upper bound for (non-strongly) convex ISRL-DP ERM that nearly matches the one we provide in 8. However, Algorithm 1 achieves the upper bounds for convex and strongly convex loss in fewer rounds of communication than (Girgis et al., 2021): see Section F.1 for details. In Section F.2, we get matching lower bounds, establishing the optimality of Algorithm 1 for ERM.

5 Shuffle DP Federated Learning

Assume access to a secure shuffler and fix . In each round , the shuffler receives reports from active silos (we assume here for concreteness), draws a uniformly random permutation of , , and then sends to the server for aggregation. When this shuffling procedure is combined with ISRL-DP Noisy Distributed MB-SGD, we obtain:

Theorem 5.1 (i.i.d.).

Let

.

Then there are choices of algorithmic parameters such that Shuffled

Noisy MB-SGD is -SDP. Moreover:

1. If is convex, then

2. If is -strongly convex, then

See Section G.1 for details and proof. When , the rates in Theorem 5.1 match the optimal central DP rates (Bassily et al., 2019), and are attained without a trusted server. Thus, with shuffling, Noisy MB-SGD is simultaneously optimal for i.i.d. FL in the inter-silo and central DP models.

If silo data is heterogeneous, then we use a shuffle DP variation of One-Pass Accelerated Noisy MB-SGD, described in Section G.2, to get:

Theorem 5.2 (Non-i.i.d.).

Assume is -smooth . Let . Then, there is an -SDP variation of One-Pass Accelerated Noisy MB-SGD such that for , we have:

1. If is convex, then

| (10) |

2. If is -strongly convex with , then

| (11) |

The bound 11 matches the optimal i.i.d., central DP bound (Bassily et al., 2019) up to . Hence, if is not ill-conditioned, then 11 shows that it is not necessary to have either i.i.d. data or a trusted server to attain the optimal CDP rates. See Section G.2 for proof and the case.

6 Numerical Experiments

We validate our theoretical findings with three sets of experiments. Our results indicate that ISRL-DP MB-SGD yields accurate, private models in practice. Our method performs well even relative to non-private Local SGD, a.k.a. FedAvg (McMahan et al., 2017), and outperforms ISRL-DP Local SGD for most privacy levels. Appendix I contains details of experiments, and additional results.101010We also describe the ISRL-DP Local SGD baseline in Appendix I.

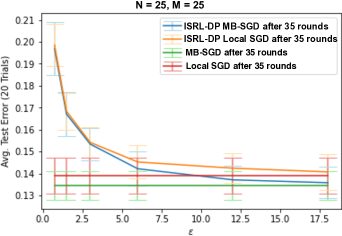

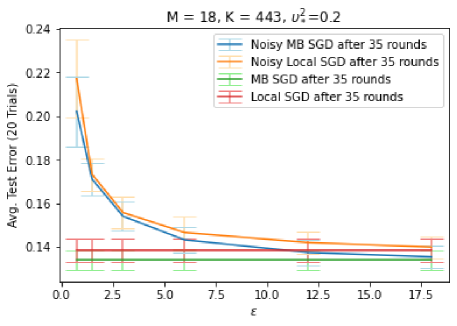

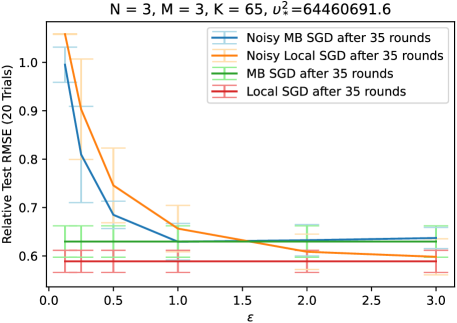

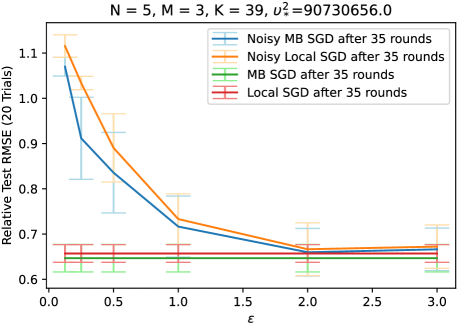

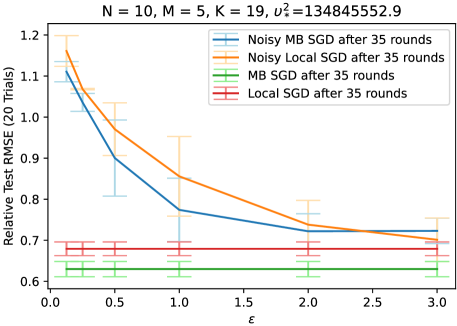

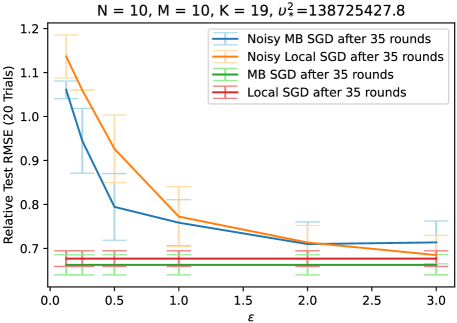

Binary Logistic Regression with MNIST: Following (Woodworth et al., 2020b), we consider binary logistic regression on MNIST (LeCun & Cortes, 2010). The task is to classify digits as odd or even. Each of 25 odd/even digit pairings is assigned to a silo (). Fig. 4 shows that ISRL-DP MB-SGD outperforms (non-private) Local SGD for and outperforms ISRL-DP Local SGD.

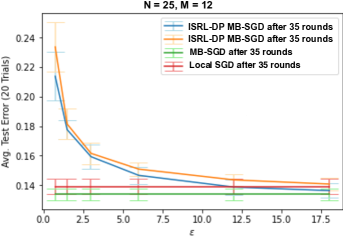

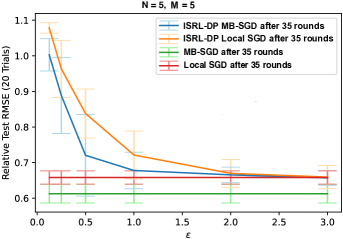

Linear Regression with Health Insurance Data: We divide the data set (Choi, 2018) () into silos based on the level of the target: patient medical costs. Fig. 5 shows that ISRL-DP MB-SGD outperforms ISRL-DP Local SGD, especially in the high privacy regime . For , ISRL-DP MB-SGD is in line with (non-private) Local SGD.

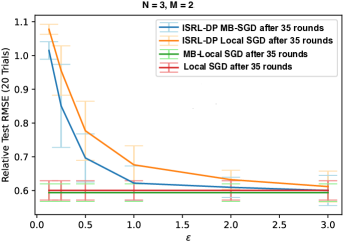

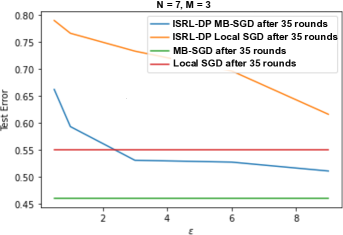

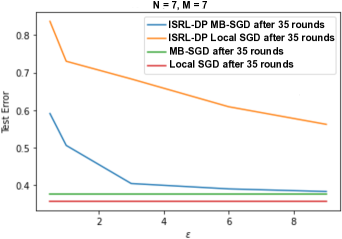

Multiclass Logistic Regression with Obesity Data: We train a softmax regression model for a -way classification task with an obesity data set (Palechor & de la Hoz Manotas, 2019). We divide the data into heterogeneous silos based on the value of the target variable, obesity level, which takes values: Insufficient Weight, Normal Weight, Overweight Level I, Overweight Level II, Obesity Type I, Obesity Type II and Obesity Type III. As shown in Fig. 6, our algorithm significantly outperforms ISRL-DP Local SGD by across all privacy levels.

7 Concluding Remarks and Open Questions

This paper considered FL without a trusted server and advocated for inter-silo record-level DP (ISRL-DP) as a practical privacy notion in this setting, particularly in cross-silo applications. We provided optimal ISRL-DP algorithms for convex/strongly convex FL in both the i.i.d. and ERM settings when all clients are able to communicate. The i.i.d. rates sit between the rates for the stringent “no trust” local DP and relaxed “high trust” central DP notions, and allow for “privacy for free” when . As a side result, in Appendix D.3.5, we established the optimal rates for cross-device FL with user-level DP in the absence of a trusted server. Additionally, we devised an accelerated ISRL-DP algorithm to obtain state-of-the-art upper bounds for heterogeneous FL. We also gave a shuffle DP algorithm that (nearly) attains the optimal central DP rates for (non-i.i.d.) i.i.d. FL. An open problem is to close the gap between our i.i.d. lower bounds and non-i.i.d. upper bounds: e.g. can in 7 be removed? Also, when , are our upper bounds tight? Finally, what performance is possible for non-convex ISRL-DP FL?

Acknowledgments

This work was partly supported by a gift from the USC-Meta Center for Research and Education in AI and Learning. AL thanks Xingyu Zhou for helpful feedback on our lower bound proofs.

References

- Abadi et al. (2016) Martin Abadi, Andy Chu, Ian Goodfellow, H. Brendan McMahan, Ilya Mironov, Kunal Talwar, and Li Zhang. Deep learning with differential privacy. Proceedings of the 2016 ACM SIGSAC Conference on Computer and Communications Security, Oct 2016. doi: 10.1145/2976749.2978318. URL http://dx.doi.org/10.1145/2976749.2978318.

- Agarwal et al. (2012) Alekh Agarwal, Peter L. Bartlett, Pradeep Ravikumar, and Martin J. Wainwright. Information-theoretic lower bounds on the oracle complexity of stochastic convex optimization. IEEE Transactions on Information Theory, 58(5):3235–3249, 2012. doi: 10.1109/TIT.2011.2182178.

- Aldaghri et al. (2021) Nasser Aldaghri, Hessam Mahdavifar, and Ahmad Beirami. Feo2: Federated learning with opt-out differential privacy. arXiv preprint arXiv:2110.15252, 2021.

- Arachchige et al. (2019) Pathum Chamikara Mahawaga Arachchige, Peter Bertok, Ibrahim Khalil, Dongxi Liu, Seyit Camtepe, and Mohammed Atiquzzaman. Local differential privacy for deep learning. IEEE Internet of Things Journal, 7(7):5827–5842, 2019.

- Asi et al. (2021) Hilal Asi, Vitaly Feldman, Tomer Koren, and Kunal Talwar. Private stochastic convex optimization: Optimal rates in l1 geometry. In International Conference on Machine Learning, pp. 393–403. PMLR, 2021.

- Balle et al. (2019) Borja Balle, James Bell, Adria Gascón, and Kobbi Nissim. The privacy blanket of the shuffle model. In Annual International Cryptology Conference, pp. 638–667. Springer, 2019.

- Balle et al. (2020) Borja Balle, Peter Kairouz, Brendan McMahan, Om Dipakbhai Thakkar, and Abhradeep Thakurta. Privacy amplification via random check-ins. 33, 2020.

- Bassily et al. (2014) Raef Bassily, Adam Smith, and Abhradeep Thakurta. Private empirical risk minimization: Efficient algorithms and tight error bounds. In 2014 IEEE 55th Annual Symposium on Foundations of Computer Science, pp. 464–473. IEEE, 2014.

- Bassily et al. (2019) Raef Bassily, Vitaly Feldman, Kunal Talwar, and Abhradeep Thakurta. Private stochastic convex optimization with optimal rates. In Advances in Neural Information Processing Systems, 2019.

- Bittau et al. (2017) Andrea Bittau, Ulfar Erlingsson, Petros Maniatis, Ilya Mironov, Ananth Raghunathan, David Lie, Mitch Rudominer, Ushasree Kode, Julien Tinnes, and Bernhard Seefeld. Prochlo: Strong privacy for analytics in the crowd. In Proceedings of the Symposium on Operating Systems Principles (SOSP), pp. 441–459, 2017.

- Bousquet & Elisseeff (2002) Olivier Bousquet and André Elisseeff. Stability and generalization. The Journal of Machine Learning Research, 2:499–526, 2002.

- Bun & Steinke (2016) Mark Bun and Thomas Steinke. Concentrated differential privacy: Simplifications, extensions, and lower bounds. In Proceedings, Part I, of the 14th International Conference on Theory of Cryptography - Volume 9985, pp. 635–658, Berlin, Heidelberg, 2016. Springer-Verlag. ISBN 9783662536407. doi: 10.1007/978-3-662-53641-4_24. URL https://doi.org/10.1007/978-3-662-53641-4_24.

- Chen et al. (2018) Yi-Ruei Chen, Amir Rezapour, and Wen-Guey Tzeng. Privacy-preserving ridge regression on distributed data. Information Sciences, 451:34–49, 2018.

- Cheu et al. (2019) Albert Cheu, Adam Smith, Jonathan Ullman, David Zeber, and Maxim Zhilyaev. Distributed differential privacy via shuffling. In Annual International Conference on the Theory and Applications of Cryptographic Techniques, pp. 375–403. Springer, 2019.

- Cheu et al. (2021) Albert Cheu, Matthew Joseph, Jieming Mao, and Binghui Peng. Shuffle private stochastic convex optimization. arXiv preprint arXiv:2106.09805, 2021.

- Choi (2018) Miri Choi. Medical insurance charges data. 2018. URL https://www.kaggle.com/mirichoi0218/insurance.

- Den Hollander (2012) Frank Den Hollander. Probability theory: The coupling method. 2012.

- Dobbe et al. (2020) Roel Dobbe, Ye Pu, Jingge Zhu, Kannan Ramchandran, and Claire Tomlin. Customized local differential privacy for multi-agent distributed optimization, 2020.

- Duchi & Rogers (2019) John Duchi and Ryan Rogers. Lower bounds for locally private estimation via communication complexity. In Conference on Learning Theory, pp. 1161–1191. PMLR, 2019.

- Duchi et al. (2013) John C. Duchi, Michael I. Jordan, and Martin J. Wainwright. Local privacy and statistical minimax rates. In 2013 IEEE 54th Annual Symposium on Foundations of Computer Science, pp. 429–438, 2013. doi: 10.1109/FOCS.2013.53.

- Dwork & Roth (2014) Cynthia Dwork and Aaron Roth. The Algorithmic Foundations of Differential Privacy. 2014.

- Dwork et al. (2006) Cynthia Dwork, Frank McSherry, Kobbi Nissim, and Adam Smith. Calibrating noise to sensitivity in private data analysis. In Theory of cryptography conference, pp. 265–284. Springer, 2006.

- Erlingsson et al. (2020a) Úlfar Erlingsson, Vitaly Feldman, Ilya Mironov, Ananth Raghunathan, Shuang Song, Kunal Talwar, and Abhradeep Thakurta. Encode, shuffle, analyze privacy revisited: Formalizations and empirical evaluation. arXiv preprint arXiv:2001.03618, 2020a.

- Erlingsson et al. (2020b) Ulfar Erlingsson, Vitaly Feldman, Ilya Mironov, Ananth Raghunathan, Kunal Talwar, and Abhradeep Thakurta. Amplification by shuffling: From local to central differential privacy via anonymity, 2020b.

- Feldman & Vondrak (2019) Vitaly Feldman and Jan Vondrak. High probability generalization bounds for uniformly stable algorithms with nearly optimal rate. In Alina Beygelzimer and Daniel Hsu (eds.), Proceedings of the Thirty-Second Conference on Learning Theory, volume 99 of Proceedings of Machine Learning Research, pp. 1270–1279, Phoenix, USA, 25–28 Jun 2019. PMLR. URL http://proceedings.mlr.press/v99/feldman19a.html.

- Feldman et al. (2020a) Vitaly Feldman, Tomer Koren, and Kunal Talwar. Private stochastic convex optimization: optimal rates in linear time. In Proceedings of the 52nd Annual ACM SIGACT Symposium on Theory of Computing, pp. 439–449, 2020a.

- Feldman et al. (2020b) Vitaly Feldman, Audra McMillan, and Kunal Talwar. Hiding among the clones: A simple and nearly optimal analysis of privacy amplification by shuffling, 2020b.

- Fredrikson et al. (2015) Matt Fredrikson, Somesh Jha, and Thomas Ristenpart. Model inversion attacks that exploit confidence information and basic countermeasures. In Proceedings of the 22nd ACM SIGSAC Conference on Computer and Communications Security, pp. 1322–1333, 2015.

- Gade & Vaidya (2018) Shripad Gade and Nitin H Vaidya. Privacy-preserving distributed learning via obfuscated stochastic gradients. In 2018 IEEE Conference on Decision and Control (CDC), pp. 184–191. IEEE, 2018.

- Geyer et al. (2017) Robin C. Geyer, Tassilo Klein, and Moin Nabi. Differentially private federated learning: A client level perspective. CoRR, abs/1712.07557, 2017. URL http://arxiv.org/abs/1712.07557.

- Ghadimi & Lan (2012) Saeed Ghadimi and Guanghui Lan. Optimal stochastic approximation algorithms for strongly convex stochastic composite optimization i: A generic algorithmic framework. SIAM Journal on Optimization, 22(4):1469–1492, 2012. doi: 10.1137/110848864. URL https://doi.org/10.1137/110848864.

- Ghadimi & Lan (2013) Saeed Ghadimi and Guanghui Lan. Optimal stochastic approximation algorithms for strongly convex stochastic composite optimization, ii: Shrinking procedures and optimal algorithms. SIAM Journal on Optimization, 23(4):2061–2089, 2013. doi: 10.1137/110848876. URL https://doi.org/10.1137/110848876.

- Ghazi et al. (2021) Badih Ghazi, Ravi Kumar, and Pasin Manurangsi. User-level private learning via correlated sampling. arXiv preprint arXiv:2110.11208, 2021.

- Girgis et al. (2021) Antonious Girgis, Deepesh Data, Suhas Diggavi, Peter Kairouz, and Ananda Theertha Suresh. Shuffled model of differential privacy in federated learning. In Arindam Banerjee and Kenji Fukumizu (eds.), Proceedings of The 24th International Conference on Artificial Intelligence and Statistics, volume 130 of Proceedings of Machine Learning Research, pp. 2521–2529. PMLR, 13–15 Apr 2021. URL https://proceedings.mlr.press/v130/girgis21a.html.

- Hardt et al. (2016) Moritz Hardt, Ben Recht, and Yoram Singer. Train faster, generalize better: Stability of stochastic gradient descent. In Maria Florina Balcan and Kilian Q. Weinberger (eds.), Proceedings of The 33rd International Conference on Machine Learning, volume 48 of Proceedings of Machine Learning Research, pp. 1225–1234, New York, New York, USA, 20–22 Jun 2016. PMLR. URL http://proceedings.mlr.press/v48/hardt16.html.

- He et al. (2019) Zecheng He, Tianwei Zhang, and Ruby B Lee. Model inversion attacks against collaborative inference. In Proceedings of the 35th Annual Computer Security Applications Conference, pp. 148–162, 2019.

- Huang & Gong (2020) Zonghao Huang and Yanmin Gong. Differentially private ADMM for convex distributed learning: Improved accuracy via multi-step approximation. arXiv preprint:2005.07890, 2020.

- Huang et al. (2020) Zonghao Huang, Rui Hu, Yuanxiong Guo, Eric Chan-Tin, and Yanmin Gong. DP-ADMM: ADMM-based distributed learning with differential privacy. IEEE Transactions on Information Forensics and Security, 15:1002–1012, 2020.

- Jayaraman & Wang (2018) Bargav Jayaraman and Lingxiao Wang. Distributed learning without distress: Privacy-preserving empirical risk minimization. Advances in Neural Information Processing Systems, 2018.

- Joseph et al. (2019) Matthew Joseph, Jieming Mao, Seth Neel, and Aaron Roth. The role of interactivity in local differential privacy. In 2019 IEEE 60th Annual Symposium on Foundations of Computer Science (FOCS), pp. 94–105. IEEE, 2019.

- Kairouz et al. (2015) Peter Kairouz, Sewoong Oh, and Pramod Viswanath. The composition theorem for differential privacy, 2015.

- Kairouz et al. (2019) Peter Kairouz, H. Brendan McMahan, Brendan Avent, Aurélien Bellet, Mehdi Bennis, Arjun Nitin Bhagoji, Keith Bonawitz, Zachary Charles, Graham Cormode, Rachel Cummings, Rafael G. L. D’Oliveira, Salim El Rouayheb, David Evans, Josh Gardner, Zachary Garrett, Adrià Gascón, Badih Ghazi, Phillip B. Gibbons, Marco Gruteser, Zaid Harchaoui, Chaoyang He, Lie He, Zhouyuan Huo, Ben Hutchinson, Justin Hsu, Martin Jaggi, Tara Javidi, Gauri Joshi, Mikhail Khodak, Jakub Konečný, Aleksandra Korolova, Farinaz Koushanfar, Sanmi Koyejo, Tancrède Lepoint, Yang Liu, Prateek Mittal, Mehryar Mohri, Richard Nock, Ayfer Özgür, Rasmus Pagh, Mariana Raykova, Hang Qi, Daniel Ramage, Ramesh Raskar, Dawn Song, Weikang Song, Sebastian U. Stich, Ziteng Sun, Ananda Theertha Suresh, Florian Tramèr, Praneeth Vepakomma, Jianyu Wang, Li Xiong, Zheng Xu, Qiang Yang, Felix X. Yu, Han Yu, and Sen Zhao. Advances and open problems in federated learning. arXiv preprint:1912.04977, 2019.

- Kamath (2020) Gautam Kamath. Cs 860: Algorithms for private data analysis, 2020. URL http://www.gautamkamath.com/CS860notes/lec5.pdf.

- Karimireddy et al. (2020) Sai Praneeth Karimireddy, Satyen Kale, Mehryar Mohri, Sashank Reddi, Sebastian Stich, and Ananda Theertha Suresh. SCAFFOLD: Stochastic controlled averaging for federated learning. In Hal Daumé III and Aarti Singh (eds.), Proceedings of the 37th International Conference on Machine Learning, volume 119 of Proceedings of Machine Learning Research, pp. 5132–5143. PMLR, 13–18 Jul 2020.

- Kasiviswanathan et al. (2011) Shiva Prasad Kasiviswanathan, Homin K Lee, Kobbi Nissim, Sofya Raskhodnikova, and Adam Smith. What can we learn privately? SIAM Journal on Computing, 40(3):793–826, 2011.

- Khaled et al. (2019) Ahmed Khaled, Konstantin Mishchenko, and Peter Richtárik. Better communication complexity for local SGD. arXiv preprint, 2019.

- Koloskova et al. (2020) Anastasia Koloskova, Nicolas Loizou, Sadra Boreiri, Martin Jaggi, and Sebastian Stich. A unified theory of decentralized SGD with changing topology and local updates. In Hal Daumé III and Aarti Singh (eds.), Proceedings of the 37th International Conference on Machine Learning, volume 119 of Proceedings of Machine Learning Research, pp. 5381–5393. PMLR, 13–18 Jul 2020.

- LeCun & Cortes (2010) Yann LeCun and Corinna Cortes. MNIST handwritten digit database. 2010. URL http://yann.lecun.com/exdb/mnist/.

- Lei et al. (2017) Lihua Lei, Cheng Ju, Jianbo Chen, and Michael I Jordan. Non-convex finite-sum optimization via scsg methods. In Proceedings of the 31st International Conference on Neural Information Processing Systems, pp. 2345–2355, 2017.

- Levy et al. (2021) Daniel Levy, Ziteng Sun, Kareem Amin, Satyen Kale, Alex Kulesza, Mehryar Mohri, and Ananda Theertha Suresh. Learning with user-level privacy. arXiv preprint arXiv:2102.11845, 2021.

- Li et al. (2020) Xiang Li, Kaixuan Huang, Wenhao Yang, Shusen Wang, and Zhihua Zhang. On the convergence of FedAvg on non-iid data. In 8th International Conference on Learning Representations, ICLR 2020, Addis Ababa, Ethiopia, April 26-30, 2020, 2020. URL https://openreview.net/forum?id=HJxNAnVtDS.

- Liu & Talwar (2019) Jingcheng Liu and Kunal Talwar. Private selection from private candidates. In Proceedings of the 51st Annual ACM SIGACT Symposium on Theory of Computing, pp. 298–309, 2019.

- Liu et al. (2022) Ziyu Liu, Shengyuan Hu, Zhiwei Steven Wu, and Virginia Smith. On privacy and personalization in cross-silo federated learning. arXiv preprint arXiv:2206.07902, 2022.

- Lobel & Ozdaglar (2010) Ilan Lobel and Asuman Ozdaglar. Distributed subgradient methods for convex optimization over random networks. IEEE Transactions on Automatic Control, 56(6):1291–1306, 2010.

- Lowy & Razaviyayn (2021) Andrew Lowy and Meisam Razaviyayn. Output perturbation for differentially private convex optimization with improved population loss bounds, runtimes and applications to private adversarial training. arXiv preprint:2102.04704, 2021.

- Ma et al. (2018) Xu Ma, Fangguo Zhang, Xiaofeng Chen, and Jian Shen. Privacy preserving multi-party computation delegation for deep learning in cloud computing. Information Sciences, 459:103–116, 2018.

- McMahan et al. (2017) Brendan McMahan, Eider Moore, Daniel Ramage, Seth Hampson, and Blaise Aguera y Arcas. Communication-efficient learning of deep networks from decentralized data. In Artificial Intelligence and Statistics, pp. 1273–1282. PMLR, 2017.

- McMahan et al. (2018) Brendan McMahan, Daniel Ramage, Kunal Talwar, and Li Zhang. Learning differentially private recurrent language models. In International Conference on Learning Representations (ICLR), 2018. URL https://openreview.net/pdf?id=BJ0hF1Z0b.

- McSherry (2009) Frank D McSherry. Privacy integrated queries: an extensible platform for privacy-preserving data analysis. In Proceedings of the 2009 ACM SIGMOD International Conference on Management of data, pp. 19–30, 2009.

- Murtagh & Vadhan (2016) Jack Murtagh and Salil Vadhan. The complexity of computing the optimal composition of differential privacy. In Theory of Cryptography Conference, pp. 157–175. Springer, 2016.

- Nedic et al. (2017) Angelia Nedic, Alex Olshevsky, and Wei Shi. Achieving geometric convergence for distributed optimization over time-varying graphs. SIAM Journal on Optimization, 27(4):2597–2633, 2017.

- Nemirovskii & Yudin (1983) Arkadii Semenovich Nemirovskii and David Borisovich Yudin. Problem Complexity and Method Efficiency in Optimization. 1983.

- Nesterov (2005) Yurii Nesterov. Smooth minimization of non-smooth functions. Mathematical programming, 103(1):127–152, 2005.

- Noble et al. (2022) Maxence Noble, Aurélien Bellet, and Aymeric Dieuleveut. Differentially private federated learning on heterogeneous data. In International Conference on Artificial Intelligence and Statistics, pp. 10110–10145. PMLR, 2022.

- Palechor & de la Hoz Manotas (2019) Fabio Mendoza Palechor and Alexis de la Hoz Manotas. Dataset for estimation of obesity levels based on eating habits and physical condition in individuals from colombia, peru and mexico. Data in brief, 25:104344, 2019.

- Papernot & Steinke (2021) Nicolas Papernot and Thomas Steinke. Hyperparameter tuning with renyi differential privacy, 2021.

- Seif et al. (2020) Mohamed Seif, Ravi Tandon, and Ming Li. Wireless federated learning with local differential privacy. In 2020 IEEE International Symposium on Information Theory (ISIT), pp. 2604–2609, 2020. doi: 10.1109/ISIT44484.2020.9174426.

- Smith et al. (2017) Adam Smith, Abhradeep Thakurta, and Jalaj Upadhyay. Is interaction necessary for distributed private learning? In 2017 IEEE Symposium on Security and Privacy (SP), pp. 58–77, 2017. doi: 10.1109/SP.2017.35.

- Song et al. (2020) Mengkai Song, Zhibo Wang, Zhifei Zhang, Yang Song, Qian Wang, Ju Ren, and Hairong Qi. Analyzing user-level privacy attack against federated learning. IEEE Journal on Selected Areas in Communications, 38(10):2430–2444, 2020. doi: 10.1109/JSAC.2020.3000372.

- Stich (2019) Sebastian U. Stich. Unified optimal analysis of the (stochastic) gradient method. arXiv preprint:1907.04232, 2019.

- Touri & Gharesifard (2015) Behrouz Touri and Bahman Gharesifard. Continuous-time distributed convex optimization on time-varying directed networks. In 2015 54th IEEE Conference on Decision and Control (CDC), pp. 724–729, 2015. doi: 10.1109/CDC.2015.7402315.

- Truex et al. (2019) Stacey Truex, Nathalie Baracaldo, Ali Anwar, Thomas Steinke, Heiko Ludwig, Rui Zhang, and Yi Zhou. A hybrid approach to privacy-preserving federated learning. In Proceedings of the 12th ACM Workshop on Artificial Intelligence and Security, pp. 1–11, 2019.

- Truex et al. (2020) Stacey Truex, Ling Liu, Ka-Ho Chow, Mehmet Emre Gursoy, and Wenqi Wei. LDP-Fed: federated learning with local differential privacy. In Proceedings of the Third ACM International Workshop on Edge Systems, Analytics and Networking, pp. 61–66. Association for Computing Machinery, 2020. ISBN 9781450371322.

- Ullman (2017) Jonathan Ullman. CS7880: rigorous approaches to data privacy, 2017. URL http://www.ccs.neu.edu/home/jullman/cs7880s17/HW1sol.pdf.

- Wang et al. (2017) D Wang, M Ye, and J Xu. Differentially private empirical risk minimization revisited: Faster and more general. In Proc. 31st Annual Conference on Advances in Neural Information Processing Systems (NIPS 2017), 2017.

- Wei et al. (2020a) Kang Wei, Jun Li, Ming Ding, Chuan Ma, Hang Su, Bo Zhang, and H Vincent Poor. User-level privacy-preserving federated learning: Analysis and performance optimization. arXiv preprint:2003.00229, 2020a.

- Wei et al. (2020b) Kang Wei, Jun Li, Ming Ding, Chuan Ma, Howard H Yang, Farhad Farokhi, Shi Jin, Tony QS Quek, and H Vincent Poor. Federated learning with differential privacy: Algorithms and performance analysis. IEEE Transactions on Information Forensics and Security, 15:3454–3469, 2020b.

- Woodworth et al. (2020a) Blake Woodworth, Kumar Kshitij Patel, Sebastian Stich, Zhen Dai, Brian Bullins, Brendan Mcmahan, Ohad Shamir, and Nathan Srebro. Is local SGD better than minibatch SGD? In International Conference on Machine Learning, pp. 10334–10343. PMLR, 2020a.

- Woodworth et al. (2020b) Blake E Woodworth, Kumar Kshitij Patel, and Nati Srebro. Minibatch vs local sgd for heterogeneous distributed learning. In H. Larochelle, M. Ranzato, R. Hadsell, M. F. Balcan, and H. Lin (eds.), Advances in Neural Information Processing Systems, volume 33, pp. 6281–6292. Curran Associates, Inc., 2020b. URL https://proceedings.neurips.cc/paper/2020/file/45713f6ff2041d3fdfae927b82488db8-Paper.pdf.

- Wu et al. (2019) Nan Wu, Farhad Farokhi, David Smith, and Mohamed Ali Kaafar. The value of collaboration in convex machine learning with differential privacy, 2019.

- Yuan & Ma (2020) Honglin Yuan and Tengyu Ma. Federated accelerated stochastic gradient descent. In H. Larochelle, M. Ranzato, R. Hadsell, M. F. Balcan, and H. Lin (eds.), Advances in Neural Information Processing Systems, volume 33, pp. 5332–5344. Curran Associates, Inc., 2020. URL https://proceedings.neurips.cc/paper/2020/file/39d0a8908fbe6c18039ea8227f827023-Paper.pdf.

- Zhao et al. (2020) Yang Zhao, Jun Zhao, Mengmeng Yang, Teng Wang, Ning Wang, Lingjuan Lyu, Dusit Niyato, and Kwok-Yan Lam. Local differential privacy based federated learning for internet of things. IEEE Internet of Things Journal, 2020.

- Zhou & Tang (2020) Yaqin Zhou and Shaojie Tang. Differentially private distributed learning. INFORMS Journal on Computing, 32(3):779–789, 2020.

- Zhu & Han (2020) Ligeng Zhu and Song Han. Deep leakage from gradients. In Federated learning, pp. 17–31. Springer, 2020.

Appendix

To ease navigation, we provide a high-level table of contents for this Appendix:

Contents

Appendix A: Thorough Discussion of Related Work

Appendix B: Rigorous Definition of Inter-Silo Record-Level DP

Appendix C: Relationships Between Notions of DP

Appendix H: ISRL-DP Upper Bounds with Unbalanced Data and Differing Silo Privacy Needs

Appendix I: Numerical Experiments: Details and Additional Results

Appendix J: Limitations and Societal Impacts

Appendix A Thorough Discussion of Related Work

Federated Learning: In the absence of differential privacy constraints, federated learning (FL) has received a lot of attention from researchers in recent years. Among these, the most relevant works to us are (Koloskova et al., 2020; Li et al., 2020; Karimireddy et al., 2020; Woodworth et al., 2020a; b; Yuan & Ma, 2020), which have proved bounds on the convergence rate of FL algorithms. From an algorithmic standpoint, all of these works propose and analyze either Minibatch SGD (MB-SGD), FedAvg/Local SGD (McMahan et al., 2017), or an extension or accelerated/variance-reduced variation of one of these (e.g. SCAFFOLD (Karimireddy et al., 2020)). Notably, Woodworth et al. (2020b) proves tight upper and lower bounds that establish the near optimality of accelerated MB-SGD for the heterogeneous SCO problem with non-random in a fairly wide parameter regime. Lobel & Ozdaglar (2010); Touri & Gharesifard (2015); Nedic et al. (2017) provide convergence results with random connectivity graphs. Our upper bounds describe the effect of the mean of on DP FL.

DP Optimization: In the centralized setting, DP ERM and SCO is well-understood for convex and strongly convex loss functions (Bassily et al., 2014; Wang et al., 2017; Bassily et al., 2019; Feldman et al., 2020a; Lowy & Razaviyayn, 2021; Asi et al., 2021).

Tight excess risk bounds for local DP SCO were provided in Duchi et al. (2013); Smith et al. (2017).

A few works have also considered Shuffle DP ERM and SCO. Girgis et al. (2021); Erlingsson et al. (2020a) showed that the optimal CDP convex ERM rate can be attained in the lower trust (relative to the central model) shuffle model of DP. The main difference between our treatment of shuffle DP and Cheu et al. (2021) is that our results are much more general than Cheu et al. (2021). For example, Cheu et al. (2021) does not consider FL: instead they consider the simpler problem of stochastic convex optimization (SCO). SCO is a simple special case of FL in which each silo has only sample. Additionally, Cheu et al. (2021) only considers the i.i.d. case, but not the more challenging non-i.i.d. case. Further, Cheu et al. (2021) assumes perfect communication (), while we also analyze the case when and some silos are unavailable in certain rounds (e.g. due to internet issues). Note that our bounds in Theorem 5.1 recover the results in Cheu et al. (2021) in the special case considered in their work.

DP Federated Learning: More recently, there have been many proposed attempts to ensure the privacy of individuals’ data during and after the FL process. Some of these have used secure multi-party computation (MPC) (Chen et al., 2018; Ma et al., 2018), but this approach leaves users vulnerable to inference attacks on the trained model and does not provide the rigorous guarantee of DP. Others (McMahan et al., 2018; Geyer et al., 2017; Jayaraman & Wang, 2018; Gade & Vaidya, 2018; Wei et al., 2020a; Zhou & Tang, 2020; Levy et al., 2021; Ghazi et al., 2021; Noble et al., 2022) have used user-level DP or central DP (CDP), which rely on a trusted third party, or hybrid DP/MPC approaches (Jayaraman & Wang, 2018; Truex et al., 2019). The work of (Jayaraman & Wang, 2018) proves CDP empirical risk bounds and high probability guarantees on the population loss when the data is i.i.d. across silos. However, ISRL-DP and SDP are not considered, nor is heterogeneous (non-i.i.d.) FL. It is also worth mentioning that (Geyer et al., 2017) considers random but does not prove any bounds.

Despite this progress, prior to our present work, very little was known about the excess risk potential of ISRL-DP FL algorithms, except in the two extreme corner cases of and . When , ISRL-DP and CDP are essentially equivalent; tight ERM (Bassily et al., 2014) and i.i.d. SCO (Bassily et al., 2019; Feldman et al., 2020a) bounds are known for this case. In addition, for LDP i.i.d. SCO when and , (Duchi et al., 2013) establishes the minimax optimal rate for the class of sequentially interactive algorithms and non-strongly convex loss functions. To the best of our knowledge, all previous works examining the general ISRL-DP FL problem with arbitrary either focus on ERM and/or do not provide excess risk bounds that scale with both and , making the upper bounds provided in the present work significantly tighter. Furthermore, none of the existing works on ISRL-DP FL provide lower bounds or upper bounds for the case of random . We discuss each of these works in turn below:

(Truex et al., 2020) gives a ISRL-DP FL algorithm, but no risk bounds are provided in their work.

The works of (Huang et al., 2020) and (Huang & Gong, 2020) use ISRL-DP ADMM algorithms for smooth convex Federated ERM. However, the utility bounds in their works are stated in terms of an average of the silo functions evaluated at different points, so it is not clear how to relate their result to the standard performance measure for learning (which we consider in this paper): expected excess risk at the point output by the algorithm. Also, no lower bounds are provided for their performance measure. Therefore, the sub-optimality gap of their result is not clear.

(Wu et al., 2019, Theorem 2) provides an -ISRL-DP ERM bound for fixed of for -strongly convex, -smooth with condition number and is an average of The additive term is clearly problematic: e.g. if , then the bound becomes trivial. Ignoring this term, the first term in their bound is still looser than the bound that we provide in Theorem 4.1. Namely, for , our bound in part 2 of Theorem 4.1 is tighter by a factor of and does not require -smoothness of the loss. Additionally, the bounds in (Wu et al., 2019) require “large enough” and do not come with communication complexity guarantees. In the convex case, the ISRL-DP ERM bound reported in (Wu et al., 2019, Theorem 3) is difficult to interpret because the unspecified “constants” in the upper bound on are said to be allowed to depend on .

(Wei et al., 2020b, Theorems 2-3) provide convergence rates for smooth convex Polyak-Łojasiewicz (a generalization of strong convexity) ISRL-DP ERM, which are complicated non-monotonic functions of Since they do not prescribe a choice of it is unclear what excess loss and communication complexity bounds are attainable with their algorithm.

(Dobbe et al., 2020) proposes a ISRL-DP Inexact Alternating Minimization Algorithm (IAMA) with Laplace noise; their result (Dobbe et al., 2020, Theorem 3.11) gives a convergence rate for smooth, strongly convex ISRL-DP FL of order ignoring smoothness and strong convexity factors, where is a parameter that is only upper bounded in special cases (e.g. quadratic objective). Thus, the bounds given in (Dobbe et al., 2020) are not complete for general strongly convex loss functions. Even in the special cases where a bound for is provided, our bounds are tighter. Assuming that and (for simplicity of exposition) that parameters are the same across silos, (Dobbe et al., 2020, Theorem 3.11) implies taking to ensure -ISRL-DP. The resulting convergence rate is then which does not scale with and is increasing with Also, the dependence of their rate on the dimension is unclear, as it does not appear explicitly in their theorem.111111Note that in order for their result to be correct, by (Bassily et al., 2014) when , their bound must scale at least as unless their bound is trivial (). Ignoring this issue, the dependence on and in the bound of (Dobbe et al., 2020) is still looser than all of the excess loss bounds that we provide in the present work.

(Zhao et al., 2020) and (Arachchige et al., 2019) apply the ISRL-DP FL framework to Internet of Things, and (Seif et al., 2020) uses noisy (full-batch) GD for ISRL-DP wireless channels in the FL (smooth strongly convex) ERM setting. The bounds in these works do not scale with the number of data points , however (only with the number of silos ). Therefore, the bounds that we provide in the present work are tighter, and apply to general convex FL problems besides wireless channels and Internet of Things.

Appendix B Rigorous Definition of Inter-Silo Record-Level DP

Recall:

Definition 4.

(Differential Privacy) Let A randomized algorithm is -DP if for all -adjacent data sets and all measurable subsets , we have

| (12) |

If 12 holds for all measurable subsets , then we denote this property by . An -round fully interactive randomized algorithm for FL is characterized in every round by local silo functions called randomizers () and an aggregation mechanism. (See below for an example that further clarifies the terminology used in this paragraph.) The randomizers send messages , to the server or other silos. The messages may depend on silo data and the outputs of silos’ randomizers in prior rounds.121212We assume that is not dependent on () given and ; that is, the distribution of is completely characterized by and . Therefore, the randomizers of cannot “eavesdrop” on another silo’s data, which aligns with the local data principle of FL. We allow for to be empty/zero if silo does not output anything to the server in round . Then, the server (or silos, for peer-to-peer FL) updates the global model. We consider the output of to be the transcript of all silos’ communications: i.e. the collection of all messages . Algorithm is -ISRL-DP if for all silos , the full transcript is -DP, for any fixed settings of the other silos’ messages and data. More precisely:

Definition 5.

(Inter-Silo Record-Level Differential Privacy) Let , . A randomized algorithm is -ISRL-DP if for all silos and all -adjacent ,

where and .

Example clarifying the terminology used in the definition of ISRL-DP given above: Assume all silos are available in every round and consider to be the minibatch SGD algorithm, , where for drawn randomly from . Then the randomizers of silo are its stochastic gradients: for drawn randomly from . Note that the output of these randomizers depends on , which is a function of previous stochastic gradients of all silos . The aggregation mechanism outputs by simply averaging the outputs of silos’ randomizers: . We view the output of to be the transcript of all silos’ communications, which in this case is the collection of all stochastic minibatch gradients . Note that in practice, the algorithm does not truly output a list of gradients, but rather outputs that is some convex combination of the iterates , which themselves are functions of . However, by the post-processing property of DP (Dwork & Roth, 2014, Proposition 2.1), the privacy of will be guaranteed if the silo transcripts are DP. Thus, here we simply consider the output of to be the silo transcripts. Clearly, minibatch SGD is not ISRL-DP. To make it ISRL-DP, it would be necessary to introduce additional randomness to make sure that each silo’s collection of stochastic gradients is DP, conditional on the messages and data of all other silos. For example, Noisy MB-SGD is a ISRL-DP variation of (projected) minibatch SGD.

Appendix C Relationships between notions of DP

C.1 ISRL-DP is stronger than CDP

Assume is -ISRL-DP. Let be adjacent databases in the CDP sense; i.e. there exists a unique such that Then for all , , , so the conditional distributions of and given are identical for all Integrating both sides of this equality with respect to the joint density of shows that (unconditional equality of distributions). Hence the full transcript of silo is (unconditionally) -CDP for all A similar argument (using the inequality 3 instead of equality) shows that silo ’s full transcript is unconditionally -CDP. Therefore, by the basic composition theorem for DP (Dwork & Roth, 2014), the full combined transcript of all silos is -CDP, which implies that is -CDP.

Conversely, -CDP does not imply -ISRL-DP for any . This is because a CDP algorithm may send non-private updates to the server and rely on the server to randomize, completely violating the requirement of LDP.

C.2 ISRL-DP Implies User-Level DP for small

Precisely, we claim that if is -ISRL-DP then is user-level DP; but conversely -user-level DP does not imply -ISRL-DP for any . The first part of the claim is due to group privacy (see (Kamath, 2020, Theorem 10) ) and the argument used above in Section C.1 to get rid of the “conditional”. The second part of the claim is true because a user-level DP algorithm may send non-private updates to the server and rely on the server to randomize, completely violating the requirement of ISRL-DP.

Therefore, if and , then any -ISRL-DP algorithm also provides a strong user-level privacy guarantee.

Appendix D Proofs and Supplementary Material for Section 2

D.1 Pseudocode of Noisy MB-SGD

We present pseudocode for Noisy MB-SGD in Algorithm 2:

D.2 Proof of Theorem 2.1

We begin by proving Theorem 2.1 for -smooth and then extend our result to the non-smooth case via Nesterov smoothing (Nesterov, 2005). We will require some preliminaries. We begin with the following definition from (Bousquet & Elisseeff, 2002):

Definition 6.

(Uniform Stability) A randomized algorithm is said to be -uniformly stable (w.r.t. loss function ) if for any pair of adjacent data sets , we have

In our context, . The following lemma, which is well known, allows us to easily pass from empirical risk to population loss when the algorithm in Question 1s uniformly stable:

Lemma D.1.

Let be -uniformly stable w.r.t. convex loss function . Let be any distribution over and let Then the excess population loss is upper bounded by the excess expected empirical loss plus :

where the expectations are over both the randomness in and the sampling of Here we denote the empirical loss by and the population loss by for additional clarity, and

Proof.

The next step is to bound the uniform stability of Algorithm 2.

Lemma D.2.

Let be convex, -Lipschitz, and -smooth loss for all Let . Then under Assumption 3, Noisy MB-SGD with constant stepsize and averaging weights is -uniformly stable with respect to for . If, in addition is -strongly convex, for all then Noisy MB-SGD with constant step size and any averaging weights is -uniformly stable with respect to for (assuming ).

Proof of Lemma D.2.

The proof of the convex case extends techniques and arguments used in the proofs of (Hardt et al., 2016, Theorem 3.8), (Feldman & Vondrak, 2019, Lemma 4.3), and (Bassily et al., 2019, Lemma 3.4) to the ISRL-DP FL setting; the strongly convex bound requires additional work to get a tight bound. For now, fix the randomness of Let be two data sets, denoted for for all and similarly for , and assume Then there is a unique and such that For , denote the -th iterates of Algorithm 2 on these two data sets by and respectively. We claim that

| (13) |

for all We prove the claim by induction. It is trivially true when Suppose 13 holds for all Denote the samples in each local mini-batch at iteration by (dropping the for brevity). Assume WLOG that First condition on the randomness due to minibatch sampling and due to the Gaussian noise, which we denote by . Also, denote (for ) and . Then by the same argument used in Lemma 3.4 of (Bassily et al., 2019), we can effectively ignore the noise in our analysis of step of the algorithm since the same (conditionally non-random) update is performed on and , implying that the noises cancel out. More precisely, by non-expansiveness of projection and gradient descent step for (see Lemma 3.7 in (Hardt et al., 2016)), we have

where is a realization of the random variable that counts the number of times index occurs in worker ’s local minibatch at iteration (Recall that we sample uniformly with replacement.) Now is a sum of independent Bernoulli( random variables, hence Then using the inductive hypothesis and taking expected value over the randomness of the Gaussian noise and the minibatch sampling proves the claim. Next, taking expectation with respect to the randomness of implies

since the are i.i.d. with Then Jensen’s inequality and Lipschitz continuity of imply that for any

completing the proof of the convex case.

Next suppose is -strongly convex. The proof begins identically to the convex case. We condition on , , and as before and (keeping the same notation used there) get for any

We will need the following tighter estimate of the non-expansiveness of the gradient updates to bound the first term on the right-hand side of the inequality above:

Lemma D.3.

(Hardt et al., 2016) Let be -strongly convex and -smooth. Assume Then for any we have

Note that is -smooth and -strongly convex and hence so is . Therefore, invoking Lemma D.3 and the assumption as well as Lipschitzness of yields

Next, taking expectations over the (with mean ), the minibatch sampling (recall ), and the Gaussian noise implies

One can then prove the following claim by an inductive argument very similar to the one used in the proof of the convex part of Lemma D.2: for all

where The above claim implies that

Finally, using the above bound together with Lipschitz continuity of and Jensen’s inequality, we obtain that for any

This completes the proof of Lemma D.2. ∎

Next, we will bound the empirical loss of Noisy MB-SGD (Algorithm 2). We will need the following two lemmas for the proof of Lemma D.6 (and hence Theorem 2.1):

Lemma D.4.

(Projection lemma) Let be a closed convex set. Then for any

Lemma D.5.

(Stich, 2019) Let , let and be non-negative step-sizes such that for all for some parameter . Let and be two non-negative sequences of real numbers which satisfy

for all Then there exist particular choices of step-sizes and averaging weights such that

where In fact, we can choose and as follows:

We give the excess empirical risk guarantee of ISRL-DP MB-SGD below:

Lemma D.6.

Let be -strongly convex (with for convex case), -Lipschitz, and -smooth in for all where is a closed convex set in s.t. for all

Let .

Then Noisy MB-SGD (Algorithm 2) with attains the following empirical loss bounds as a function of step size and the number of rounds:

1. (Convex) For any and , , we have

2. (Strongly Convex) There exists a constant stepsize such that if , then

| (14) |

Proof.

First, condition on the random and consider as fixed. Let be any minimizer of , and denote the average of the i.i.d. Gaussian noises across all silos in one round by Note that by independence of the and hence Then for any , conditional on we have that

| (15) |

where we used Lemma D.4 in the first inequality, -strong convexity of (for ) and the fact that is independent of the gradient estimate and mean zero in the next inequality, and the fact that is -Lipschitz for all in the last inequality (together with independence of the noise and the data again).

Now we consider the convex () and strongly convex () cases separately.

Convex () case: Re-arranging Section D.2, we get

and hence

by taking total expectation and using . Then for , the average iterate satisfies:

Plugging in finishes the proof of the convex case.

Strongly convex () case: Recall from Section D.2 that

| (16) |

for all (upon taking expectation over ). Now, Section D.2 satisfies the conditions for Lemma D.5, with sequences

and parameters

Then Lemma D.5 and Jensen’s inequality imply

Finally, plugging in and completes the proof. ∎

We are now prepared to prove Theorem 2.1 in the -smooth case:

Theorem D.1.

Let be

-smooth

in for all .

Assume , choose and Then Algorithm 2 is -ISRL-DP. Moreover, there are choices of such that

Algorithm 2 achieves the following excess loss bounds:

1. If is convex, then setting

yields

| (17) |

2. If is -strongly convex, then setting yields

| (18) |

Proof.

Privacy: By independence of the Gaussian noise across silos, it suffices to show that transcript of silo ’s interactions with the server is DP for all (conditional on the transcripts of all other silos). WLOG consider . By the advanced composition theorem (Theorem 3.20 in (Dwork & Roth, 2014)), it suffices to show that each of the rounds of the algorithm is -ISRL-DP, where (we used the assumption here) and First, condition on the randomness due to local sampling of the local data point (line 4 of Algorithm 2). Now, the sensitivity of each local step of SGD is bounded by by -Lipschitzness of Thus, the standard privacy guarantee of the Gaussian mechanism (see (Dwork & Roth, 2014, Theorem A.1)) implies that (conditional on the randomness due to sampling) taking suffices to ensure that round (in isolation) is -ISRL-DP. Now we invoke the randomness due to sampling: (Ullman, 2017) implies that round (in isolation) is -ISRL-DP. The assumption on ensures that , so that the privacy guarantees of the Gaussian mechanism and amplification by subsampling stated above indeed hold. Therefore, with sampling, it suffices to take to ensure that round (in isolation) is -ISRL-DP for all and hence that the full algorithm ( rounds) is -ISRL-DP.

Excess loss: 1. First suppose is merely convex (). By Lemma D.2, Lemma D.1, and Lemma D.6, we have:

for any . Choosing implies

Finally, one verifies that the prescribed choice of yields 17.

2. Now suppose is -strongly convex. Then for the used in the proof of Lemma D.6 and , we have

by Lemma D.6, Lemma D.2, and Lemma D.1. Hence 18 follows by our choice of . ∎

We use Theorem D.1 to prove Theorem 2.1 via Nesterov smoothing (Nesterov, 2005), similar to how (Bassily et al., 2019) proceeded for CDP SCO with non-strongly convex loss and . That is, for non-smooth , we run ISRL-DP Noisy MB-SGD on the smoothed objective (a.k.a. -Moreau envelope) , where is a design parameter that we will optimize for. The following key lemma allows us to easily extend Theorem D.1 to non-smooth :

Lemma D.7 (Nesterov (2005)).

Let be convex and -Lipschitz and let . Then the -Moreau envelope satisfies:

1. is convex, -Lipschitz, and -smooth.

2. ,

Now let us re-state the precise version of Theorem 2.1 before providing its proof:

Theorem D.2 (Precise version of Theorem 2.1).

Let and choose , Then Algorithm 2 is -ISRL-DP. Further, there exist choices of such that running Algorithm 2 on yields:

1. If is convex, then setting

yields

| (19) |

2. If is -strongly convex, then setting yields

| (20) |

Proof.

Privacy: ISRL-DP is immediate from post-processing (Dwork & Roth, 2014, Proposition 2.1), since we already showed that Algorithm 2 (applied to ) is ISRL-DP.

Excess risk: We have

by part 2 of Lemma D.7. Moreover, by part 1 of Lemma D.7 and Theorem D.1, we have:

for convex , and

for -strongly convex . Thus, choosing such that and such that completes the proof. ∎

D.3 Lower Bounds for ISRL-DP FL: Supplemental Material and Proofs

This section requires familiarity with the notation introduced in the rigorous definition of ISRL-DP in Appendix B.

D.3.1 -Compositionality

The -ISRL-DP algorithm class contains all sequentially interactive and fully interactive, -compositional algorithms.

Definition 7 (Compositionality).

Let be an -round -ISRL-DP FL algorithm with data domain . Let denote the minimal (non-negative) parameters of the local randomizers selected at round such that is -DP for all and all For , we say that is -compositional if If such is an absolute constant, we simply say is compositional.

Definition 7 is an extension of the definition in Joseph et al. (2019) to .

D.3.2 Algorithms whose Privacy follows from Advanced Composition Theorem are -Compositional

Suppose is -ISRL-DP by the advanced composition theorem (Dwork & Roth, 2014, Theorem 3.20). Then

and for any . Assume without loss of generality: otherwise the privacy guarantee of is essentially meaningless (see Remark D.1). Then , so that is -compositional. Note that even if , would still be compositional, but the constant may be larger than .

D.3.3 Example of LDP Algorithm that is Not Compositional

This example is a simple modification of Example 2.2 in (Joseph et al., 2019) (adapted to our definition of compositionality for ). Given any , set and let be the standard basis for Let and For all let be the randomized response mechanism that outputs with probability and otherwise outputs a uniformly random element of Note that is -DP, hence -DP for any . Consider the -round algorithm in Algorithm 3, where

Since each silo’s data is only referenced once and is -DP, we have and is -DP. However, , so that is not -compositional.

Also, note that our One-Pass Accelerated Noisy MB-SGD is only -compositional for , since for this algorithm. Thus, substituting the that is used to prove the upper bounds in Theorem 3.1 (see Section E.2) and plugging into Theorem 2.2 explains where the non-i.i.d. lower bounds in Fig. 3 come from.

D.3.4 Proof of Theorem 2.2

First, let us state the complete, formal version of Theorem 2.2, which uses notation from Appendix B:

Theorem D.3 (Complete Version of Theorem 2.2).

Let

, and . Suppose that in each round , the local randomizers are all -DP, for , .

Then:

1. There exists a and a distribution such that for , we have:

2. There exists a -smooth and distribution such that for , we have

Further, if , then the above lower bounds hold with .

Before we proceed to the proof of Theorem 2.2, we recall the simpler characterization of ISRL-DP for sequentially interactive algorithms. A sequentially interactive algorithm with randomizers is -ISRL-DP if and only if for all , is -DP for all . In what follows, we will fix for all . We now turn to the proof.

Step 1: Privacy amplification by shuffling. We begin by stating and proving the amplification by shuffling result that we will leverage to obtain Theorem 2.2:

Theorem D.4.

Let such that and Assume that in each round, the local randomizers are -DP for all with . Assume . If is -compositional, then assume and denote ; if instead is sequentially interactive, then assume and denote Let be the same algorithm as except that in each round , draws a random permutation of and applies to instead of . Then, is -CDP, where and . In particular, if , then Note that for sequentially interactive ,

To the best of our knowledge, the restriction on is needed to obtain in all works that have analyzed privacy amplification by shuffling (Erlingsson et al., 2020b; Feldman et al., 2020b; Balle et al., 2019; Cheu et al., 2019; Balle et al., 2020), but these works focus on the sequentially interactive case with , so the restriction amounts to (or The non-sequential -compositional part of Theorem D.4 will follow as a corollary (Corollary D.1 ) of the following result which analyzes the privacy amplification in each round:

Theorem D.5 (Single round privacy amplification by shuffling).

Let and let be an -DP local randomizer for all and where is an arbitrary set. Given a distributed data set and , consider the shuffled algorithm that first samples a random permutation of and then computes where Then, is -CDP, where

| (21) |

and In particular, if then

| (22) |

Further, if , then setting implies that

| (23) |

and , which is in if we assume

We sometimes refer to the algorithm as the “shuffled algorithm derived from the randomizers ” From Theorem D.5, we obtain:

Corollary D.1 (-round privacy amplification for -compositional algorithms).

Let be an -round -ISRL-DP and -compositional algorithm such that and where is an arbitrary set. Assume that in each round, the local randomizers are -DP for , where , , and Then, the shuffled algorithm derived from (i.e. is the composition of the shuffled algorithms defined in Theorem D.5) is -CDP, where and where In particular, if is compositional, then .

Proof.

Let and Then the (central) privacy loss of the full -round shuffled algorithm is bounded as

where the three (in)equalities follow in order from the Advanced Composition Theorem (Dwork & Roth, 2014), 23 in Theorem D.5, and -compositionality of combined with the assumption . Also, by the Advanced Composition Theorem, where by Theorem D.5. Hence In particular, if is compositional, then , so . ∎

Remark D.1.