thmTheorem \newsiamthmlemLemma \newsiamthmpropProposition \newsiamthmcorCorollary \newsiamremarkremRemark \newsiamremarkdefiDefinition \headersCardinality Minimization, Constraints, and Regularization: A SurveyA. M. Tillmann, D. Bienstock, A. Lodi, and A. Schwartz

Cardinality Minimization, Constraints, and Regularization: A Survey††thanks: June 17, 2021; August 5, 2022.

Abstract

We survey optimization problems that involve the cardinality of variable vectors in constraints or the objective function. We provide a unified viewpoint on the general problem classes and models, and give concrete examples from diverse application fields such as signal and image processing, portfolio selection, or machine learning. The paper discusses general-purpose modeling techniques and broadly applicable as well as problem-specific exact and heuristic solution approaches. While our perspective is that of mathematical optimization, a main goal of this work is to reach out to and build bridges between the different communities in which cardinality optimization problems are frequently encountered. In particular, we highlight that modern mixed-integer programming, which is often regarded as impractical due to commonly unsatisfactory behavior of black-box solvers applied to generic problem formulations, can in fact produce provably high-quality or even optimal solutions for cardinality optimization problems, even in large-scale real-world settings. Achieving such performance typically draws on the merits of problem-specific knowledge that may stem from different fields of application and, e.g., shed light on structural properties of a model or its solutions, or lead to the development of efficient heuristics; we also provide some illustrative examples.

keywords:

sparsity, cardinality constraints, regularization, mixed-integer programming, signal processing, portfolio optimization, regression, machine learning90-02, 90C05, 90C06, 90C10, 90C11, 90C26, 90C30, 90C33, 90C59, 90C90, 62J07, 68T99, 94A12, 91G10

1 Introduction

The cardinality of variable vectors occurs in a plethora of optimization problems, in either constraints or the objective function. In the following, we attempt to describe the broad landscape of such problems with a general emphasis on continuous variables. This restriction serves as a natural distinguishing feature from a myriad of classical operations research or combinatorial optimization problems, where “cardinality” typically appears in the form of minimizing or limiting the number of some objects associated with (non-auxiliary, i.e., structural) binary decision variables. Cardinality restrictions on general variables are thus of a decidedly different flavor, and also require different modeling and solution techniques than those immediately available in the binary case.

The general classes of problems we are interested in can be formalized as follows:

-

•

Cardinality Minimization Problems

(-min()) -

•

Cardinality-Constrained Problems

(-cons(, , )) -

•

Regularized Cardinality Problems

(-reg(, ))

where we use (the so-called “-norm”), , , and . The set in any of these problems can be used to impose further constraints on . For simplicity, we will usually simply write out the constraints rather than fully state the corresponding set ; e.g., we may write -cons(, , ) instead of -cons(, , ).

Most concrete problems we will discuss belong to one of these three classes, although we will also encounter variations and extensions. Indeed, very similar problems may arise in very different fields of application, sometimes resulting in some methodology being reinvented or researchers being generally unaware of relevant results and developments from seemingly disparate communities. Moreover, the incomplete transfer of knowledge between different disciplines may prevent progress in the resolution of some problems that could strongly benefit of new approaches for similar problems, developed with completely different applications in mind. With this document, we hope to provide a useful roadmap connecting several disciplines and offering an overview of the many different computational approaches that are available for cardinality optimization problems. Note that a similar overview was given a couple of years ago in [351], but with a much more limited scope of cardinality problems and their aspects than we consider here (albeit discussing the related case of semi-continuous variables in more detail, in particular associated perspective reformulations, which we mostly skip). Moreover, significant advances have been achieved in just these past few years, which we include in this survey.

To emphasize the cross-disciplinary nature of many of the cardinality optimization problem classes and to provide a clear reference point for members of different communities to recognize their own problem of interest in this survey, we will group our overview of various concrete such problems according to the respective application areas and point out overlaps and differences. The solution methods we shall discuss cover both exact and heuristic approaches; our own mathematical programming perspective tends to favor exact models and algorithms that can provide provable guarantees on solution quality, a stance that appears to be less commonly taken in practical applications. This is “a feature, not a bug” of the present paper—we hope to bring across that in many cases, mixed-integer programming (MIP) offers an attractive alternative to widely-used heuristic methods. Generally, a typical first step in that direction is experimenting with off-the-shelf solvers to tackle basic MIP formulations. Depending on the application, this may already work very well, especially when solution quality is more important than speed. Importantly, MIP solvers also provide certifiable error bounds of the computed solution w.r.t. the optimum if terminated prematurely (e.g., when imposing a runtime limit), in contrast to many heuristic methods without general quality guarantees that are commonly employed in various applications. Moreover, improvement to optimality is often not hopeless and can be achieved either by simply allowing more solving time, or by improving the underlying mathematical model formulation and/or incorporating knowledge of the problem at hand into the MIP solver. Thus, as subsequent steps to substantially improve speed and scalability of MIP approaches, it is worth revisiting the model and guiding or enhancing the MIP solver by customizing existing (and/or adding new problem-specific) algorithmic components—a fact we will document with some examples.

We organize the subsequent discussion as follows: In the remainder of this introductory section, we will clarify some relationships between the main problem classes and fix our notation. Then, in Section 2, we describe the most common different realizations of the above problems -min(), -cons(, , ), and -reg(, ) as they occur in diverse fields like signal processing, compressed sensing, portfolio optimization, and machine learning; some further related problems are also discussed. In Section 3, we summarize exact modeling techniques (in particular, mixed-integer linear and nonlinear programming) and algorithmic approaches from the literature, and provide some exemplary numerical experiments to illustrate how the sometimes unsatisfactory performance of general-purpose models and MIP solvers may be significantly improved by some advanced modeling tricks and, especially, by integrating problem-specific knowledge and heuristic methods. This is followed in Section 4 by reviewing the plethora of proposed relaxations, regularization, and heuristic schemes, including popular -norm and atomic norm minimization as well as greedy methods. Finally, in Section 5, we address scalability aspects of exact and approximate/heuristic algorithms, and then conclude the paper in Section 6.

Moreover, Table 1 provides an alternative overview meant to facilitate navigating this document if one is primarily interested in one specific problem. Since this paper covers too many different problems to provide such an overview for all of them, we do so exemplarily for three of the most-widely used problems, and note that the pointers to topics and locations given for these should also be helpful for many other related problems as well. Specifically, Table 1 covers -min(), -cons(, , ), and -reg(, ), which will be formally introduced first in Section 2.1 in the context of signal processing, but also appear in virtually all other application areas, and can be seen as the “base problems” for various related variants and extensions.

| problem | location | information |

|---|---|---|

| -min() | Sect. 3.2 | exact solution methods, mostly based on mixed-integer programming |

| Sect. 4.1 | -surrogate problem BPDN() and solution approaches, e.g., homotopy methods, ADMM, and smoothing techniques | |

| Sect. 4.3 | heuristics based on nonconvex approximations (but only considering related constraints) | |

| Sect. 4.5 | other heuristics such as subspace pursuit | |

| -cons(, , ) | Sect. 3.3 | exact solution methods, mostly based on mixed-integer programming |

| Sect. 4.1 | -surrogate problem LASSO() and solution approaches, e.g., a spectral projected gradient method and smoothing techniques | |

| Sect. 4.4 | heuristics based on nonconvex formulations | |

| Sect. 4.5 | other heuristics such as iterative hard-thresholding and matching pursuit | |

| -reg(, ) | Sect. 3.4 | theoretical discussion of the general problem -reg(, ), some exact solution methods for special cases, possibilities for -reg(, ) |

| Sect. 4.1 | -surrogate problem -LS() and solution approaches, e.g., iterative soft-thresholding and semismooth Newton methods | |

| Sect. 4.4 | heuristics based on nonconvex reformulations | |

| Sect. 4.5 | other heuristics such as iterative hard-thresholding |

1.1 Relationships Between Main Problem Classes

At least in some communities, it appears to be folklore knowledge that problems belonging to the classes -min(), -cons(, , ), or -reg(, ) can sometimes be equivalent in the sense that they share optimal solutions under certain assumptions on the cardinality, constraint and regularization parameters. Indeed, the fact that in widely-used surrogate models like -norm problems, such equivalences always hold for the right parameter choices (cf. Section 4.1), might mislead one to presume the same is true for the -based problems. However, this is generally not the case. We formalize (non-)equivalence statements for the three main classes of cardinality problems in the following result, where we let be the typical slight variation of the cardinality minimization problem that most naturally relates to the other problem classes; to simplify notation, we also abbreviate -cons, and -reg.

Proposition 1.

Let , , , and .

-

1.

If is an optimal solution of -reg, then it also optimally solves -cons for and -min() for . The reverse implications are not true in general.

-

2.

If all optimal solutions of -cons have the same cardinality , then they all also solve -min() for . The equal-cardinality assumption cannot be dropped in general.

-

3.

If all optimal solutions of -min() have the same function value , then they all also solve -cons for . The equal-value assumption cannot be dropped in general.

Proof 1.1.

First, let solve -reg. Then, for all with , it holds that , and for all with , we have which shows that solves both -cons and -min() as claimed. To show that the reverse implications do not hold in general, consider the case and with

Then, in particular, optimally solves both -cons and -min(); -cons is solved by with and -cons by with . Thus, the optimal value of -reg as a function of is

For , the solution to -reg is , for , both and are optimal, and for , only is. This means that cannot by recovered by -reg for any , which concludes the proof of statement 1.

We skip the straightforward proofs of the positive statements in 2 and 3. To show that these implications are not true without the respective assumptions, let and first consider . Then, any with optimally solves -cons, but not -min() unless . Now, let . Then, and are both optimal for -min(), but does not solve -cons.

Note that points 2 and 3 of Proposition 1 imply equivalence of -cons and -min(), for the appropriate values of and , in case of solution uniqueness, which is often an important desideratum (e.g., for signal reconstruction). However, the parameter values that yield such an equivalence are typically not known a priori.

1.2 Notation

We let denote the set of nonnegative real numbers. For a natural number , we abbreviate . The complement of a set is denoted by . The cardinality of a vector is denoted as , where is its support (i.e., index set of nonzero entries). The standard -norm (for ) of a vector is defined as , and . For a matrix , denotes is Frobenius norm, and its -th column. For a set and a vector or matrix , and denote the vector restricted to indices in or the column-submatrix induced by , respectively. We use to denote an all-ones vector, and to denote the identity matrix, of appropriate dimensions. A superscript denotes transposition (of a vector or matrix). A diagonal matrix build from a vector is denoted by , and conversely, extracts the diagonal of a matrix as a vector. For vectors , we sometimes abbreviate (i.e., for all ) as , extending the standard interval notation to vectors.

2 Prominent Cardinality Optimization Problems

Cardinality optimization problems (COPs, for short) abound in several different areas of application, such as medical imaging (e.g., X-ray tomography), face recognition, wireless sensor network design, stock-picking, crystallography, astronomy, computer vision, classification and regression, interpretable machine learning, or statistical data analysis, to name but a few. In this section, we highlight the most prominent realizations of such problems. To facilitate “mapping” concrete problems to concrete applications, we structure the section according to the three broad fields in which cardinality optimization problems are encountered most frequently: signal and image processing, portfolio optimization and management, and high-dimensional statistics and machine learning; further related COPs and extensions are gathered in a final subsection. Along these lines, a first broad overview of applications is provided in Figure 1.

2.1 Signal and Image Processing

In the broad field of signal processing, it has been found that signal sparsity can be exploited beneficially in several tasks, e.g., to remove noise from image or audio data or to reduce the amount of measurements needed to faithfully reconstruct signals from observations. In particular, the advent of compressed sensing (see [184] for a thorough introduction) has sparked a tremendous interest in several core cardinality optimization problems in the past 15 years or so.

At first, the focus was on reconstruction from linear measurements (), but research quickly also expanded to different nonlinear settings. We will discuss the respective fundamental sparse recovery tasks in Sections 2.1.1 and 2.1.2 below; Section 2.1.3 covers important generalizations of the main sparsity concept.

Before we get started, a brief remark on the measurement matrices seems in order: In signal processing applications, is typically not fully generic but assumes certain forms and properties arising from an underlying physical measurement model or setup. Also, much of the theory for efficient solvability (see, e.g., Section 4.1.1) relies on properties of that hold with high probability for certain random matrices. Thus, in signal processing and, in particular, compressed sensing, one often encounters matrices such as Fourier transforms, Gaussian or Bernoulli matrices—sometimes combined with binary masks to blot out random entries, or otherwise modified. In contrast, we note that in other areas of application for the problems introduced in the following (or related tasks), the matrix is often comprised of observational data (e.g., in finance, regression or machine learning), which is typically unstructured and rarely beholden to specific probability distributions. This distinction may be partially responsible for the many different approaches found across disciplines.

2.1.1 Sparse Recovery From Linear Measurements

The fundamental sparse recovery problem takes the form111The decision version of -min() and variants with other linear constraints than equality is also called minimum number of relevant variables in linear systems (MinRVLS) [9] or minimum weight solution to linear equations [195].

| (-min()) |

where with (w.l.o.g.) , and . Its variant allowing for noise in the linear measurements is usually deemed more realistic (although real-world applications for the above noise-free setting do exist) and can be formulated as

| (-min()) |

with some that is often derived from statistical properties of the noise in applications. The assumption excludes the otherwise trivial all-zero solution. Depending on noise models and application contexts, the -norm in the constraint may be replaced by the -norm (e.g., when the noise is impulsive, cf. [168]), by the -norm (in case of uniform quantization noise or for sparse linear discriminant analysis, cf. [80, 89], respectively), or possibly by general -(quasi-)norms for some .

An alternative to cardinality minimization seeks to optimize data fidelity within a prescribed sparsity level of the signal vector to be reconstructed, i.e., typically,

| (-cons(, , )) |

This problem is often also referred to as subset selection or feature selection, see, e.g., [292, 55], and plays an important role in many regression and machine learning tasks (see also Section 2.3). Here, as for -min(), the -norm term is often rewritten equivalently as to ensure differentiability (in with ) and simplify derivative notation; variants employing other norms also exist. The special case with orthogonal yields a sparse version of the standard denoising problem, where one seeks to “clean up” a noisy version of the target signal (in case , cf. [165]), often incorporating an orthogonal basis transformation ( but orthogonal, as in, e.g., [154, 153, 279]). Going beyond orthogonal bases, i.e., utilizing sparse representability w.r.t. more general —such as overcomplete dictionaries, see Section 2.1.3 below—can further improve denoising capabilities, e.g., in image processing, see, for instance, [165] and references therein.

By its respective definition, -min() requires (approximate) knowledge of the noise level , and for -cons(, , ), the user must specify the allowed sparsity level . Since in practice it may be unclear how to choose either or appropriately, the regularization approach

| (-reg(, )) |

has also been thoroughly investigated. Note that this problem is also particularly suitable to situations where the noise has limited variance (but its level is unknown), and a sparse solution (of unknown cardinality) is sought. Here, the regularization parameter controls the tradeoff between sparsity of the solution and data fidelity. While this model has the potential advantage of being unconstrained, it is similarly unclear how to “correctly” choose in most applications. In general, there are many different approaches to obtain regularization, sparsity or residual error-bound parameters that work well for an application at hand, including homotopy schemes and cross-validation techniques.

A fundamental question from the signal processing perspective is that of uniqueness of the recovery problem solution. In particular, for the basic reconstruction problem -min(), uniqueness can be characterized by means of a matrix parameter called the spark (see [206, 151, 356]), which is defined as the smallest number of linearly dependent columns, i.e.,

| (-min()) |

Indeed, all -sparse signals are respective unique optimal solutions of -min() if and only if , see [151, 210] or [256, Thm. 1.1]. The spark is also known as the girth of the matroid defined over the column index set, cf. [315], and it is also important in other fields, e.g., in the context of tensor decompositions [254, 250, 405] (by relation to the so-called “Kruskal rank” ) or matrix completion [408]. When working in the binary field , the spark problem amounts to computing the minimum (Hamming) distance of a binary linear code, which—along with the strongly related problem of maximum-likelihood decoding—has been treated extensively in the coding theory community, see, e.g., the structural and polyhedral results and LP and MIP techniques discussed in [326, 404, 169, 243, 27, 238, 325] and references therein.

Another connection to coding theory is found by relating the cardinality-minimization problem -min() to an error-correction perspective in decoding applications (see, e.g., [97]): Suppose a message is encoded using a linear code with full column-rank as , but a corrupted version is received. If the unknown transmission error is sufficiently sparse, recovering the true message can be formulated as . Using a left-nullspace matrix for , multiplying from the left by yields . Now, the sparse error vector can be obtained by solving -min(), and once is known, it remains to solve for (which is trivial since has full column-rank) to recover the original message.

Finally, for all problems defined above, several variants with additional constraints on the variables have been considered in the literature—in particular, nonnegativity constraints (), more general variable bounds ( for with , ), or integrality constraints. The case of complex-valued variables has also been investigated in compressed sensing and sparse signal recovery problems; nevertheless, for simplicity, we stick to the real-valued setting throughout this paper unless explicitly stating otherwise.

2.1.2 Sparse Recovery From Nonlinear Measurements

While compressed sensing concentrates on reconstructing sparse signals from linear measurements, analogous tasks have also been investigated for certain kinds of nonlinear observations. In particular, the classical optics problem of phase retrieval [368] has been demonstrated to benefit from sparsity priors as well, see, e.g., [298, 340]. The (noise-free) sparse phase retrieval problem may be stated as

| (-min()) |

where, generally, (often a Fourier matrix) and is also allowed to take on complex values; here, denotes the component-wise absolute value. Naturally, noise-aware variants exist for this type of problem as well (and are arguably more realistic than the idealized problem above), as do cardinality-constrained analogues; for brevity, we do not list them explicitly. Also, instead of the “magnitude-only” measurement model , the squared-magnitude (again, evaluated component-wise) is often used. Typical further constraints impose nonnegativity or a priori information on the signal support, e.g., restricting the solution nonzeros to certain index ranges. To achieve solution uniqueness up to a global phase factor in phase retrieval, oversampling (i.e., ) is necessary in general.

It is worth mentioning that sparse phase retrieval using squared-magnitude measurements can also be viewed as a special case of what has been termed quadratic compressed sensing [341], where the linear measurements are replaced by quadratic ones , , with symmetric positive semi-definite matrices . The most general form of cardinality minimization problem with a (single) quadratic constraint can be stated as

| (-min()) |

where is symmetric positive (semi-)definite, and . Extensions to multiple quadratic constraints as in quadratic compressed sensing are conceivable as well. A problem of this type is considered in the context of sparse filter design [377, 376], namely

with a positive definite matrix . Note that -min() can also be rewritten in this form:

Here, however, is rank-deficient (for with ), resulting in unboundedness of the feasible set in certain directions.

A cardinality minimization problem of the form -min(, , ) was considered in [177], combining nonconvex “modulus” constraints and noise-aware linear measurement constraints. Various related approaches to exploit the concept of sparsity in the context of direction-or-arrival estimation, sensor array or antenna design have also been investigated, see, e.g., [345, 218, 399, 217]; however, here, the true cardinality is typically replaced by an -norm surrogate (cf. Section 4.1), and group sparsity models (cf. Section 2.4.3) may be used instead of standard vector sparsity.

2.1.3 Generalized Sparsity Models

In the problems considered thus far, the vector is assumed to be sparse itself, or to be well approximated by a sparse one. While this basic sparsity model proved adequate and was successfully utilized in numerous examples, in different practical applications, a more general approach is called for, as the signal may not be (approximately) sparse directly. Thus, it often makes sense to admit sparse representations with respect to a given matrix (called dictionary), i.e., with a sparse coefficient vector . Sometimes, taking as a certain basis matrix (e.g., a discrete cosine transform or wavelet basis) can already work quite well, and generally, overcompleteness in the dictionary—i.e., having more columns than rows—allows for even sparser representations and further applications. For instance, loosely related to the decoding problem outlined earlier, [380] considers face recognition by identifying a new (vectorized) image as a sparse linear combination of elements from a large dictionary of partially occluded/corrupted images taken under varying illumination, which can be modeled as

where is an error vector. (This problem generalizes to the “robust PCA” problem of decomposing a matrix into a sparse and a low-rank part, see, e.g., [95].) Moreover, importantly, a suitable dictionary can be learned from data to enhance representability for certain signal or image classes, see Section 2.3. Thus, in principle, for a (fixed) dictionary , one can replace by and by in all of the problems from Sections 2.1.1 and 2.1.2.

The above approach is sometimes called the synthesis sparsity model, since the signal is “synthesized” from a few columns of . The alternative cosparsity (or analysis) model instead presumes that is sparse for some matrix with , see, e.g., [166, 301, 239, 337, 149]. Thus, the respective analysis-variants of the models discussed earlier can be obtained by simply replacing by ; the measurement part (e.g., or ) remains unchanged. Clearly, this constitutes an immediate generalization of the respective synthesis-variant—note that the two variants become equivalent when is a basis, since then, one can substitute by throughout the respective problem and arrive back at the synthesis model form—and hence offers some more flexibility.

The cosparsity viewpoint has been employed, for instance, in discrete tomography (see, e.g., [142] for a cosparsity minimization problem with linear projection equations and box constraints) and image segmentation (see, e.g., [348] treating a so-called discretized Potts model or [233, 77] for one-dimensional “jump-penalized” least-squares segmentation, both of which amount to minimization of an -norm data fidelity term with cosparsity-regularization), where is taken as a discrete gradient or finite-differences operator. Further applications include, for example, audio denoising, see, e.g., [196].

2.2 Portfolio Optimization and Management

Quadratic programs (QPs) with cardinality constraints rather than a cardinality objective play a crucial role in financial applications, in particular, portfolio optimization, see, e.g., [63, 101, 194, 290, 52]. Broadly speaking, in portfolio selection (or portfolio management), one seeks to find (or update, resp.) a low-risk/high-return composition of assets from a given universe, e.g., the constituents of a stock-market index like the S&P500. Here, cardinality constraints serve the purpose of reducing the cost and complexity of management of the resulting portfolio. These problems are usually formulated in the general form

| (-cons(, , )) |

where the symmetric positive (semi-)definite matrix is the (possibly scaled) covariance matrix of the assets and is the vector of expected returns. If the focus is on achieving a low risk (volatility) profile, the return-maximization term is sometimes replaced by a minimum-return constraint . Similarly, the risk term can be replaced by a maximum-risk constraint . The system subsumes commonly encountered variables bounds (in particular, prohibits short-selling) as well as further constraints such as (when, as is usual, represents allocation percentages) or minimum-investment constraints222Minimum-investment constraints have the form , and so are not, technically, linear constraints. The associated variables are often referred to as semi-continuous (see, e.g., [351]). With standard modeling techniques to formalize the cardinality constraints (see, e.g., [63, 52]), however, they can be linearized; e.g., using with , a minimum-investment constraint simply becomes ; see also Section 3.3.1. (e.g., to prevent positions that incur more transaction fees than they are expected to earn back). There are also portfolio selection problems with linear objectives, see, e.g., the summary provided in [105].

Since is symmetric positive semidefinite, the above problem is convex except for the cardinality constraint. Variants of these kinds of models have been considered that include a further quadratic regularization term in the objective and/or diagonal-matrix extraction (i.e., separating into a positive semidefinite and a diagonal part) as a kind of preprocessing step; see [52] for a recent overview.

Moreover, note that -cons(, , ) is a special case of the above general problem, as it can be rewritten as

However, the matrix is again rank-deficient here for the matrices usually considered in sparse recovery applications. In fact, by exploiting the fact that a symmetric positive semidefinite rank- matrix can be decomposed as with some (think Cholesky factorization), [52] show that -cons(, , ) can conversely be rewritten to resemble -cons(, , ), albeit with an additional linear term in the objective and retaining the other (linear) constraints.

It is worth mentioning that, in a spirit similar to sparse PCA (see the next subsection for a definition), the covariance matrix in real-world portfolio selection problems is sometimes replaced by a low-rank estimate, e.g., from truncating the singular-value decomposition of the obtained with the data, cf. [52, 406].

2.3 High-Dimensional Statistics and Machine Learning

Cardinality aspects also play an important role in various applications in machine learning and data science; for clarity, we break down the following discussion into topical subsections.

2.3.1 Sparse Regression, Feature Selection, and Principle Component Analysis

The problems -min() or -cons(, , ) are often referred to as sparse regression, being cardinality-considerate versions of classical linear regression (ordinary least-squares). Another problem from statistical estimation that is related to -min() seeks to find sparse regressors with a constraint on the maximal absolute correlation between predictors and the corresponding residual; this can be formulated as the so-called discrete Dantzig selector [284]:

| (-min()) |

As mentioned earlier (cf. Section 2.1), the problem -cons(, , ) is also known as subset selection or feature selection, see, e.g., [292, 55]. Beyond sparse regression, feature selection is, in fact, a vital part of various machine learning problems: Wherever a model of some kind is to be trained to perform inference/prediction tasks, from simple regression to complex neural networks, the (input) features are typically selected manually and can be numerous. Thus, integrating a sparsity component to automatically detect relevant features has become a staple in reducing the computational burden and sharpen model interpretability; see also Section 2.3.2 below.

Furthermore, QPs with cardinality constraints are not only important in finance (cf. Section 2.2), but are also encountered in feature extraction methods. In particular, the well-known sparse principal component analysis (PCA) problem (see, e.g., [410, 130, 271, 144, 49]) is usually defined as

| (-cons(, , )) |

Clearly, sparse PCA is related to -cons(, , ), albeit with nonconvex objective—note that earlier, we discussed a minimization problem, but in sparse PCA, we maximize a quadratic term. Also, here, the quadratic equation introduces further nonconvexity, but may, in fact, be relaxed to its convex counterpart in an equivalent reformulation, see [271, Lemma 1]. Generalizing the constraint to with a symmetric positive semidefinite matrix , one obtains the sparse linear discriminant analysis (LDA) problem, see, e.g., [296]. The sparse PCA problem is also taken up in [262], which presents mixed-integer SDP formulations and an approximate mixed-integer LP formulation, compare their strength to other formulations and analyze their theoretical and practical performance. Similarly, [145] considers the interesting related problem of sparse PCA with global support. Here the goal is, given an covariance matrix , to compute an matrix (with typically much smaller than ) with orthonormal columns, so as to maximize , but subject to having at most nonzero rows. The columns of can thus be viewed as a set of -sparse principle components of with common global support.

2.3.2 Classification

Cardinality constraints have also been employed in other machine learning tasks, and are often introduced to improve interpretability of learned classification or prediction models. We already mentioned the feature selection problem -cons(, , ). Another example is the sparse version of support vector machines (SVMs) for (binary) classification, which can be stated as333Note that we slightly abuse notation by referring to the sparse SVM problem class as -cons(, , ), since the cardinality constraint only involves but not . Nevertheless, clearly, there is no requirement that a cardinality constraint involves all variables of a problem under consideration, although this is typically the case in the problems we discuss here.

| (-cons(, , )) |

where . Here, is one of several possible convex empirical loss functions (w.r.t. input data points with associated labels ) that is minimized by training the classifier hyperplane . Similarly to the portfolio selection problem treated in [52], an optional regularization term with —called ridge or Tikhonov penalty—can be used to ensure strong convexity and thus existence of a unique optimal solution, see, e.g., [57].

The idea of “interpretability by sparsity” can also be found in recent approaches to train oblique decision trees for (multi-class) classification. While standard decision trees split data inputs at tree nodes according to a single feature (e.g., follow the left branch if , and the right branch otherwise, with tree leaves yielding the predicted class for the input feature vector ), more powerful splits use hyperplanes whose coefficients are obtained via training the model. At least for small tree-depths, one can compute optimal decision trees (in the sense of classification accuracy w.r.t. the chosen task and training/testing data sets) with mixed-integer programming, cf., e.g., [54]. To retain the clear interpretability of univariate splits, one can restrict the cardinality of the vectors used at split nodes of the classification tree being learned, so each path through the tree represents a series of decisions based on a few features each.

2.3.3 Dictionary Learning

In connection with sparse coding in signal and, in particular, image processing, dictionary learning (DL) problems have received considerable attention over the past years. Indeed, the observation that certain signal classes admit sparse approximate representations w.r.t. some basis or overcomplete “dictionary” matrix (see, e.g., [310, 165, 272]) was an important motivation for the intense research on sparse recovery techniques. Following this understanding that signals are not necessarily sparse themselves but may be sparsely approximated w.r.t. a dictionary (i.e., not is sparse but with small), it was soon realized that while some fixed dictionaries may work reasonably well, better results can be achieved by adapting the dictionary to the data. Thus, the goal of DL is to train suitable dictionaries on the datasets of interest for a concrete application at hand. Example applications include image denoising and inpainting (see, e.g., [165, 274, 272]) or simultaneous dictionary learning and signal reconstruction from noisy linear or nonlinear measurements (see, e.g., [272, 357]). Possible basic formulations of the task to algorithmically learn suitable matrices on the basis of large collections of training signals are

or

usually additionally constraining the columns of to be unit-norm in order to avoid scaling ambiguities. Here, all training signals , , are sparsely encoded as w.r.t. the same dictionary . Unsurprisingly, dictionary learning is also NP-hard in general (and hard to approximate) [355], and no general-purpose exact solution methods are known. Instead, algorithms are typically of a greedy nature or employ alternating minimization/block coordinate descent, iteratively solving easier subproblems obtained by fixing all but one group of variables, see, for instance, [310, 6, 273]. In particular, many such schemes involve classical sparse recovery problems like, e.g., -min() or -cons(, , ) as frequent subproblems, so any progress regarding solvability of those problems can also directly impact many dictionary learning algorithms. Such DL schemes work reasonably well in practice, and may even be extended to simultaneously learn a dictionary for sparse coding and reconstructing the sparse signals, from linear or nonlinear (noisy) measurements, see, e.g., [357]. Also, note that, as in compressed sensing and especially for -min() and similar problems, the -norm is often replaced by its -surrogate, cf. Section 4.1. However, apart from occasional results demonstrating convergence to stationary points of the typically nonconvex DL models, hardly any success guarantees are known for such methods in general.

For special cases, researchers have nevertheless considered the question of dictionary identifiability, i.e., whether the true underlying dictionary can be uniquely reconstructed (up to trivial sign, scale and permutation ambiguities) from measurements along with sparse signals forming the columns of . Thus far, results are relatively scarce and mostly yield probabilistic guarantees (typically for certain algorithms) under arguably strong assumptions on the dictionary and/or assuming support locations and entry values of follow some probability distributions. For instance, [344, 349, 350] investigate the case in which is a basis (square, invertible matrix) and measurements are noiseless, [14, 5, 336] consider noisy measurements and overcomplete but incoherent dictionaries, [28] does so without incoherence requirements, and [21] treats the noise-free case with overcomplete and a less restrictive “semi-random” model for the supports of . In [329], success guarantees and error bounds are derived for the case of unitary bases and with certain spectral bound properties that hold with high probability under common probability distribution models for its support/entires. The paper [343] relates DL to the geometrical notion of combinatorial rigidity of subspace incidence systems and provides a classification of several DL guarantees from this viewpoint, along with some new identifiability results. Deterministic recovery conditions are even less common; an early example is [7], which establishes non-probabilistic identifiability at the cost of potentially exponential sample complexity. More recently, [61] avoids probabilistic arguments as well as the inherent intractability of DL and, assuming only a certain norm bound, shows that and can be approximated up to bounded small violations of the presumed number of dictionary columns and sparsity level of those in .

2.3.4 Rank Minimization and Low-Rank Matrix Completion

A problem related to DL that, in fact, generalizes -min(), is the affine rank minimization problem , where is a linear map. Clearly, if is further constrained to be diagonal, the problem reduces to finding the sparsest vector in an affine subspace, i.e., -min(). We refer to [330] for interesting theoretical analyses of this problem and references to various applications from system identification and control to collaborative filtering. Another sparsity-related problem that received attention to due its successful application to the “Netflix problem”—in a nutshell, obtaining good predictions for recommendation systems based on limited (user rating/preference) observations—is that of low-rank matrix completion. Here, the most basic problem seeks a matrix that approximates a given matrix as well as possible under a rank constraint . Rank constraints for matrices are related to cardinality constraints for vectors; indeed, if has rank , this means that only of its singular values are nonzero. Thus, using the singular-value decomposition , a rank constraint on can be expressed as , . In matrix completion, the usual objective is , whence it is clearly always optimal to have of rank equal to (provided ); then, it is common practice to directly split as with and and handle the rank constraint implicitly by construction. However, the problem has also been viewed as rank minimization under linear constraints, for which the rank can then be modeled semialgebraically, which gives rise to a semidefinite relaxation that is exact under certain conditions, see [129]. Inductive or interpretable matrix completion aims at enhancing interpretability of the reasons for recommendations by substituting (or , or both) by with a known “feature matrix” , so that linear combinations of these features yield , and then enforcing the rank constraint by restricting the cardinality of the coefficient vectors of these linear combinations to some , or restricting the selection of features to , respectively; see [56] and references therein.

2.3.5 Clustering

Finally, it is worth mentioning that the term “cardinality constraint” is also sometimes used with a slightly different meaning. A particular example is cardinality-constrained (-means) clustering, where one seeks to partition a set of data-points into clusters, minimizing the inter-cluster Euclidean distances (to the cluster center). Here, one could restrict the number of clusters to be considered by an upper cardinality bound ; however, it is trivially optimal to always use the maximal possible number of clusters. Then, one can in fact directly incorporate the knowledge that one will have clusters into the problem formulation in other ways (see, e.g., [332]), similarly to the rank constraint in matrix completion we saw above. The cardinality of the clusters themselves may then also be restricted (e.g., to balance the partition to clusters of equal sizes), which ultimately yields cardinality equalities w.r.t. sets of cluster-assignment variables; as these are typically binary variables, this type of cardinality constraint is again different from our focus here (cf. beginning of Section 1).

2.4 Miscellaneous Related Problems and Extensions

The various classes of cardinality optimization problems discussed up to now can be generalized and extended in different directions. In this section, we briefly point out some of these connections.

2.4.1 “Classical” Combinatorial Optimization Problems

As mentioned earlier, corresponds to the girth of the vector matroid defined over the column subsets of ; cf. [315] for details on matroid theory and terminology. Thus, is a special case of the more general problem

where if and zero otherwise (i.e., is the characteristic vector of ). Moreover, recall that, when considered over the binary field , the spark problem coincides with the problem of determining the minimum distance of a binary linear code, cf. Section 2.1.1 and the references given there; this amounts to the binary-matroid girth problem. The girth of a matroid equals the cogirth of the associated dual matroid . Moreover, cocircuits of (i.e., circuits of ) correspond exactly to the complements of hyperplanes of , so

where is the complement of w.r.t. the matroid’s ground set. Note that in the case of vector matroids, the cogirth is known as cospark (cf. [97]) and can be written as

similarly to the spark, it appears in recovery and uniqueness conditions for analysis signal models and decoding, see, e.g., [97, 301]. The spark and cospark can thus also be interpreted as dual problems, since for any whose columns span the nullspace of .

In fact, constitutes a special case of the more general minimum number of unsatisfied linear relations (MinULR) problem, where for and , one seeks to minimize the number of violated relations in an infeasible system , with representing all sorts of linear relations; see [8, 9]. MinULR is also known by the name minimum irreducible infeasible subsystem cover (MinIISC), and is a well-investigated combinatorial problem; the same holds for its complementary problem maximum feasible subsystem (MaxFS), which seeks to find a cardinality-maximal feasible subsystem of , cf. [8, 10, 322]. Problems like MinULR play an important role in infeasibility analysis of linear systems, e.g., when analyzing demand satisfiability in gas transportation networks [236, 235]. Note that for the inhomogeneous equation , MinULR can be rephrased via

and thus can be seen as a weighted version of -min(), with weights zero for the -variables in the objective. Conversely, -min() can also be rephrased as a special case of MaxFS (or MinULR, of course), see, e.g., [234]. Using a diagonal (and thus, effectively, binary) weight matrix within the -term obviously yields special cases of the analysis formulations that generalize to for some matrix . To the best of our knowledge, it has not yet been investigated if and how results on (or involving) the spark from the signal processing context might aid the solution of discrete optimization problems by means of the connections laid out above or by exploiting “hidden” spark-like subproblems such as, e.g., in Proposition 2 below.

Finally, countless problems from combinatorial optimization and operations research applications seek to minimize (or restrict) “the number of something”, which is naturally formulated as cardinality minimization w.r.t. non-auxiliary (structural) binary decision vectors under broad general or highly problem-specific constraints. Classical examples are the standard packing/partitioning/covering problems

with , respectively, and ; see, e.g., [73] and textbooks like [251]. We do not delve into these kinds of problems here, since our focus is on handling the cardinality of continuous variable vectors.

2.4.2 Matrix Sparsification and Sparse Nullspace Bases

Another related combinatorial optimization problem essentially extends the idea of sparse representations from vectors to matrices: For a given matrix (w.l.o.g. with ), the Matrix Sparsification problem is given by

| (MS) |

where counts the nonzeros of a matrix , extending the common “-norm” from vectors to matrices. The problem is polynomially equivalent to that of finding a sparsest basis for the nullspace of a given matrix, by arguments similar to the aforementioned “duality” relation between spark and cospark. This Sparsest Nullspace Basis problem can be formally stated as

| (SNB) |

(recall that for an matrix with full row-rank , the nullspace has dimension ). MS and SNB have been studied quite extensively from the combinatorial optimization perspective, see, e.g., [287, 1, 122, 199, 163]; [208] provides a nice overview of their equivalence relation and associated complexity results, and also establishes some connections to compressed sensing.

Exact solution of the problems MS and SNB, as well as certain approximate versions, are known to be NP-hard tasks, see [287, 122, 208, 354, 355]. Connections to matroid theory reveal an optimal greedy method for matrix sparsification that sparsifies a given by solving a sequence of subproblems; the scheme can be described compactly as follows (cf. [163, 208]):

-

1.

Initialize (empty matrix).

-

2.

For , find a that is linearly independent of the rows of and minimizes , and update .

The final minimizes and has full rank , i.e., is indeed a solution of MS.

It turns out that the first of the above subproblems amounts exactly to a spark computation, i.e., a problem of the form -min():

Proposition 2.

The first subproblem in the above greedy MS algorithm can be solved as a spark problem.

Proof 2.1.

The first subproblem can be written as , which we recognize as . In light of the earlier discussion, this is polynomially equivalent to , where is such that is a basis for its nullspace (cf. [356, Lemma 3.1]). In particular, a solution to can be retrieved from a solution to as the unique solution to , i.e., (recall that with full column-rank ).

In [208], the authors show that the subproblems of the greedy MS algorithm can, in principle, each be solved by means of sequences of problems of the form , i.e., MinULR w.r.t. . An ongoing work by the present first author pursues a different strategy, aiming at leveraging the relation to the spark problem without resorting to breaking down each subproblem of the greedy scheme into many further subproblems (which are still NP-hard, too). So far, the literature apparently only describes a handful of (combinatorial) heuristics for MS or SNB, see [287, 122, 50, 104] and some further references gathered in [354].

Finally, it is interesting to note that matrix sparsification can also be interpreted as a special dictionary learning task: The columns of the given matrix correspond to the “training signals” and to the sought dictionary that enables sparse representations. Two crucial differences to the usual applications of DL are that MS requires to be a basis (rather than the common overcomplete dictionary) and the stricter accuracy requirements w.r.t. the obtained sparse representations (i.e., , whereas in signal/image processing, one is typically satisfied with, or even desires, only). To the best of our knowledge, the relationship between MS and DL has not yet been explored in either direction.

2.4.3 Group-/Block-Sparsity

Another extension of the sparsity concept in signal processing and learning leads to group- (or block-)sparsity models: Here, the prior is not sparsity of the full variable vector, but sparsity w.r.t. groups of variables, i.e., whole blocks of variables are simultaneously treated as “off” (zero) or “on” (all group members are nonzero; may also mean that at least one member is nonzero). This perspective can be useful in many signal processing applications like simultaneous sparse approximation or multi-task compressed sensing/learning (e.g., [361, 347, 167]), dictionary learning for image restoration (e.g., [403]), neurological imaging or bioinformatics (e.g., [320]), and may offer additional interpretability due to identification of the respective active groups. For instance, in a feature selection context, one may have several (disjoint or overlapping) groups of related features along with knowledge that features within a group are either all irrelevant or all have combined explanatory value together. A typical formulation would then read, e.g.,

where is a known group structure (collection of index subsets). The group-cardinality constraint is represented by here, ensuring that the computed solution has support restricted to the union of a selection of at most groups. In [147], the extension of cardinality constraints to group sparsity is introduced via the concept of affine sparsity constraints (ASC), and structural properties of systems of ASCs are studied. For more details and practical application references, intractability results and relaxation properties, we refer to [26, 228, 36] and references therein.

3 Exact Models and Solution Methods

The cardinality problems described in the previous section are all NP-hard in general, and are often also very hard to solve approximately. On the one hand, samples of such intractability results cover, in particular, -min() [195, 8, 9, 355], -min() [302], cardinality-constrained QPs [63], sparse PCA [360], -reg(, ) [306], and generalized variants (with other norms or sparsity-inducing penalty functions) of some such problems [114], as well as related problems such as matroid (co-)girth and (co-)spark [246, 366, 360, 356], MinULR/MaxFS [8, 9], and matrix sparsification [287, 354, 208]. On the other hand, there are a few examples of polynomially solvable special cases in the literature that involve certain sparsity patterns or combinatorial properties of the matrix , see, e.g., [140] for -cons(, , ) and [198, 356] for compressed sensing sparse recovery.

Thus, polynomial-time exact solution algorithms generally cannot exist unless PNP, which justifies the extensive efforts to devise practically efficient approximate (heuristic) methods; see Section 4 below. Unfortunately, despite there being numerous success guarantees under certain conditions on the matrix (and optimal solution sparsity and uniqueness) for most algorithms proposed in the literature, the strongest such conditions are typically themselves NP-hard to evaluate exactly or approximately; see, for instance, corresponding results on , the nullspace property, and the restricted isometry property (RIP) [360, 375].

Nevertheless, in light of the impressive improvements in modern solvers over the last decades, it is still worth investigating exact solution approaches for the different cardinality optimization problems. Here, we focus on reformulations as mixed-integer linear and nonlinear programs (MIPs and MINLPs, for short), accompanying structural results, and specialized solution techniques and solver components for the considered problems. As mentioned earlier, satisfactory results may already be achievable with off-the-shelf software applied to generic models; depending on the concrete problem/application, scalability and performance can then often be further improved by exploiting problem-specific knowledge in the solving process.

We begin with describing different approaches to model the cardinality of a variable vector, see Section 3.1. Subsequently, we will provide overviews of both general-purpose and problem-specific modeling and exact solution techniques, followingour broad classification into cardinality minimization or constrained problems (Sections 3.2 and 3.3, resp.) and cardinality-regularized optimization tasks (Section 3.4).

3.1 Modeling Cardinality

Typically, cardinality terms are modeled using binary indicator variables that effectively encode whether an original problem variable is zero or nonzero. This can be done in a linear fashion when the problem variables are (explicitly or implicitly) bounded, see Section 3.1.1, or via nonlinear constraints of the complementarity type, see Section 3.1.2. It is also possible to employ a bilinear replacement technique (again using binary auxiliary variables), or to model cardinality using continuous auxiliary variables and nonlinear constraints, see Section 3.1.3.

3.1.1 Exploiting (Auxiliary) Variable Bounds

The classical approach to model the cardinality of a continuous variable vector in a MI(NL)P is by introducing big-M constraints and auxiliary binary variables that encode whether a continuous variable is zero or nonzero. More precisely, we can rewrite as provided that

with being a sufficiently large constant. Here, if , the big-M constraint forces , while in case of , no restriction is imposed upon ; conversely, if , then cannot be set to zero and therefore must be equal to , so indeed counts the nonzero entries of . Note that , is still possible, so generally, we only have . Nevertheless, equality obviously holds at least in optimal points of cardinality minimization problems, and bounding from above still correctly represents a cardinality constraint w.r.t. . Therefore, we may refer to as the cardinality of for simplicity.

From a theoretical standpoint, for problems with unbounded variables, it might not be possible to define sufficiently large bounds within MIP or even MINLP representations, see [224, 328]. In practice, appropriate bounds (or constants ) may also not be available a priori. While theoretical bounds based on encoding lengths of the data may exist (see, e.g., [212]), they are impractically huge. Similarly, using arbitrary large values will, generally, introduce numerical instability (in floating-point arithmetic). Indeed, supposing a solver works with a numerical tolerance of, say, (the typical default tolerance of linear programming (LP) solvers), a value of, e.g., can render the model invalid numerically: For instance, one might then have , which the solver counts as zero due to its tolerance settings, but then the big-M constraints read and no longer correctly enforce .

Generally, it is well known that a big-M approach may lead to weak relaxations, which can significantly slow down the solving process of (branch-and-bound) algorithms, see, e.g., [42] and also the example later in Section 3.2.1. Nonetheless, it is a simple and flexible approach that still may work reasonably well, and is therefore often tried in a first effort. The general big-M modeling paradigm can be refined by using individual lower and upper bound constants for each variable. In particular, if bounds are part of the original problem, with , we can replace the above big-M box constraint by

with . Individual bounds and for each could also be derived from the data by considering the minimal and maximal values each variable may attain while retaining overall feasibility. Given that it is not unusual that a MI(NL)P formulation of a COP requires considerable computational effort to be solved to provable optimality, it may indeed be worth spending some time to tighten a valid big-M model by computing individual bounds via

where the set symbolizes further constraints possibly required to keep these problems bounded—e.g., could be a level-set of the objective function w.r.t. a known (sub-)optimal value, cf. [42]. In fact, especially in the context of solving MI(NL)Ps with a branch-and-bound algorithm, one may even consider adaptively tightening the bounds by incorporating information on, e.g., the optimal support size or objective function value obtained along the way. Should these bound-computation problems turn out to be impractically hard to solve to optimality themselves, relaxations could be employed to still provide improved valid bounds, see, e.g., [42].

Some examples for problem-specific derivations of variable bounds can be found in Sections 3.2 and 3.3 below. Note also that in some problems, variables may be scaled arbitrarily, in which case can feasibly be set to any positive value, and that it may even be possible to not explicitly include the variables in a problem—see the discussion of models and methods for -min() and -min() in Section 3.2. Section 3.2.1 also provides an illustrative example which, in particular, shows the benefits of good choices of the constant .

3.1.2 Complementarity-Type Formulations

A conceptually different possibility to model the cardinality and/or support couples auxiliary binary variables to the continuous variables by means of (nonlinear) complementarity(-type) constraints:

Here, again implies , so for all feasible points . In optimal solutions of cardinality minimization problems, integrality of and holds automatically, so can always be relaxed to , see, e.g., [170]. Figure 2 illustrates the effects of the auxiliary variables here compared to the big-M formulation. Note also that complementarity-type constraints as above do not (implicitly) assume boundedness of the -variables—a potential advantage over the big-M approach, albeit at the cost of linearity.

Constraints like are related to the class of equilibrium constraints, cf. [270], and can also be interpreted as specially-ordered set constraints of type 1 (SOS-1 constraints) [60], since only one out of a group of variables—here, a pair —may be nonzero. Modern MIP solvers can exploit this structural knowledge in certain ways (e.g., for bound-tightening), so it may be worth informing a solver of this explicitly in addition to another employed formulation, as done, e.g., in [55]. Specialized branching schemes for SOS-1 or complementarity constraints were discussed, e.g., in [32, 135].

Note also that these complementarity-type constraints are bilinear and can therefore be relaxed using McCormick envelopes [286], a relaxation-by-linearization technique that actually is an exact reformulation for bounded and : Introducing auxiliary variables to replace each bilinear term and additional linear constraints , , , and ensures equivalence of the original and the extended problem in this case. However, in the special case in which the bilinear terms are associated with complementarity constraints deriving from cardinality, the McCormick envelopes do not add anything to the big-M reformulation above.

The paper [170] describes various ways to reformulate the complementarity-type constraints. Because complementarity constraints are usually defined for nonnegative variables, the above variant is called half-complementarity constraints there. A variant with classical full complementarity constraints can easily be obtained by splitting the variable into its nonnegative and nonpositive parts, respectively. Moreover, [170] discusses four equivalent nonlinear reformulations. The motivating problem of that paper is of the form -min(), though most of the theoretical results on optimality conditions of the nonlinear reformulations were developed for the more general problem class -reg(, ) with and continuously differentiable functions , , and .

The very recent work [394] introduced a branch-and-cut algorithm to solve general linear programs with complementarity constraints (LPCCs) to global optimality. In contrast, the previous work [170] was largely concerned with computing stationary solutions. The LPCC viewpoint offers a quite flexible modeling paradigm with a host of diverse applications (see, e.g., those surveyed in [227]), including, in particular, -min() and -cons(, , ) for polyhedral feasible sets , cf. [170, 86]. For an overview of related earlier works on exact methods for (certain subclasses of) LPCCs or strongly related problems, see [394] and the many references therein. We would like to mention explicitly the interesting minimax/Benders decomposition approach of [226] that was extended to convex QPs with complementarity constraints in [25], and the quite extensive research into polyhedral aspects—i.e., cutting planes—in [135, 136, 138, 346, 294, 252, 137, 253, 248, 178, 179, 180]; the last three references also consider overlapping cardinality constraints (formulated as complementarity or SOS-1 constraints) and other MIP solver components like branching rules for corresponding LPCCs. It is also worth mentioning that convex quadratic constraints, as they appear in -min() and similar problems, can be recast as second order cone (SOC) constraints. These have also been studied extensively, often with a particular focus on deriving cutting planes for (mixed-integer) SOC programs, see, e.g., [214, 334, 159, 47, 367, 295, 100, 20, 187, 185, 186] and references therein.

3.1.3 Further Ways to Model Cardinality

Another alternative to model cardinality is considered in [53] (see also [52]): Here, the auxiliary binary variables are linked to in the same way as before, i.e., they essentially encapsulate the logical constraint that if , then shall hold as well. (Indeed, “” is a special case of an indicator constraint, and the reformulations discussed here can be applied to more general such constraints, see, e.g., [42, 72] for detailed discussions.) The key observation then is that one can replace by throughout the problem formulation; indeed, any then only contributes444Note that, however, would then in principle be possible even if . While this does not influence feasibility or the optimal solution value in the sense of the original formulation, it needs to be considered when extracting the optimal solution. There, the corresponding can w.l.o.g. be set to zero. [53, 52] propose to add a ridge regularization term to the objective for algorithmic reasons, which automatically enforces that indeed implies in an optimal solution. to a constraint or the objective if . The resulting mixed-integer nonlinear problems considered in [53, 52] are solved by an outer-approximation scheme that is shown to often work more efficiently than using black-box MINLP solvers. The general technique is well-known and quite broadly applicable, cf. [161, 181]. The main idea is a decomposition of the problem that allows for repeatedly solving an outer problem involving only the binary variables , and an inner problem that can be solved efficiently (for a fixed ) and provides subgradient cuts (i.e., linear inequalities based on the subgradient of the inner problem, which can be seen as a convex function in ) that refine the outer problem. Note that the same arguments as for (half-)complementarity constraints would allow to linearize various constraints (e.g., linear inequalities) in the context of the replacement-reformulation technique mentioned earlier (replacing by directly as suggested in [53, 52]), which seems to not have been tried out yet.

Interestingly, it is also possible to exactly model the cardinality of a vector using only continuous auxiliary variables, along with certain (nonlinear) constraints. For instance, [395] show that

Similar but more complicated reformulations for cardinality constraints () can be found in, e.g., [222] (see also Sections 3.3 and 4.4), though it seems unclear whether those might be helpful in a cardinality minimization context.

3.2 Cardinality Minimization

The generic cardinality minimization problem -min() can be reformulated using auxiliary binary variables with any of the techniques of the previous subsection.

The big-M approach has been applied in [75, 291] to -min(), for , as well as the corresponding cardinality-constrained and -regularized problems in a unified fashion; see also references therein for partial earlier treatments, e.g., of -min() in [242]. While the resulting mixed-integer (linear or nonlinear) problems were solved with an off-the-shelf MIP solver in [75], [291] demonstrated (for ) that considerable runtime improvements can be achieved if the usual LP-relaxations that form the standard backbone of modern MIP solvers are replaced by problem-specific other relaxations, involving the -norm as a proxy for sparsity, that admit very fast first-order solution algorithms (see Section 4.1 for an overview of many such methods). Both these works apparently employ a simple heuristic to select the big-M constant: starting with (a least-squares estimate of the maximum amplitude of -sparse solutions), accept the computed optimal solution if and restart otherwise with increased to .

As indicated in the previous subsection, we may consider computing individual bounds on each variable (and locally tightening them within a branch-and-bound solving process). As an example, let us consider , with the usual assumption that (and ). For -min(), we then know that the optimal value is at most (since there exists an invertible submatrix of ); thus, for each , we could consider

However, these problems may be as hard to solve to optimality as the original problem, so one may want to consider relaxations, and one might also encounter unboundedness (even though the original problem is bounded) which may be non-trivial to circumvent. In particular, suppose we use a complementarity reformulation of the cardinality constraint here:

( analogously). Then, one could employ known relaxations of complementarity constraints (see Section 3.1 and, in particular, Section 4.4) to obtain valid values for and —or detect subproblem unboundedness—by solving the respective relaxations. Alternatively, boundedness provided, we may combine the big-M selection heuristic from [75] outlined earlier with the bound-computation problems: For any , let and be diagonal matrices with the bounds already computed for variables on their respective diagonals, and let . Then, to compute a lower bound for (analogously for an upper bound), we can solve

| s.t. | |||

repeatedly with increased as long as the solution satisfies any of the big-M constraints with equality. Note that the above problem is an LP and therefore efficiently solvable in practice; for bound validity, we do not need to retain the integrality of . Note also that we could easily integrate possible lower bounds on the optimal cardinality into either of the above problems by means of the inequality . Depending on the problem, such bounds may be available a priori; e.g., for -min(), we trivially know that any solution must have at least two nonzero entries unless is a scaled version of a column of (which can easily be checked).

Another example can be found in [376], which considers a big-M mixed-integer QP (MIQP) reformulation of -min(), with positive definite. There, individual bounds and for each are derived from the data and even turn out to have closed-form expressions:

Note that the feasible set of -min() extends infinitely in certain directions if is rank-deficient (i.e., only semi-definite). In particular, this is the case for the correspondingly reformulated problem -min() in the usual setting with , . Then, as for -min(), boundedness of the bound-computation problems has to be ensured explicitly, for which a cardinality constraint again seems the natural choice, and relaxation offers ways to circumvent intractability issues.

As alluded to earlier, some problems allow reformulations or specialized models that can avoid the need for a big-M or complementarity/bilinear cardinality formulation. For -min() and -min(), [234] proposed a branch-and-cut algorithm that exploits a reformulation of these problems as MaxFS instances. For instance, (with ) can be transformed into reduced row-echelon form via Gaussian elimination, yielding an equivalent system ; a minimum-support solution for this can be found by finding a maximum feasible subsystem of the infeasible system . A characterization of minimally infeasible subsystems (the complements of maximal feasible subsystems) by means of the so-called alternative polyhedron (cf. [201, 319]) then yields a binary IP model with exponentially many constraints that are separated and added to the model dynamically within a branch-and-bound solver framework; see [234, 322, 10] for the details. At the time of publication, this branch-and-cut method could only solve rather small instances to optimality. The scheme also incorporates several heuristics for the MaxFS (or MinIISC) problem, adapted to the resulting special instances, with one noteworthy conclusion being that the common -norm minimization approach may not be the best choice.

For the problem -min(), i.e., computing , note that any feasible vector lies in the nullspace of a matrix and, therefore, can be scaled arbitrarily without compromising its feasibility or affecting its -norm. Thus, every value works in a big-M cardinality modeling approach. Spark computation is discussed in detail in [356]; in particular, a formulation with was employed and—utilizing additional auxiliary binary variables to model the nontriviality constraint —the resulting MIP was given as

| (1) |

see also analogous MIP models and/or exact algorithms for the cospark, i.e., vector matroid cogirth problem, in [119, 247, 13]. Here, only one of the -variables can become , and implies , thus ensuring and also eliminating sign symmetry (if , then also ). Moreover, by exploiting relations to matroid theory, [356] proposed the following pure binary IP model for the spark computation problem -min():

| (2) |

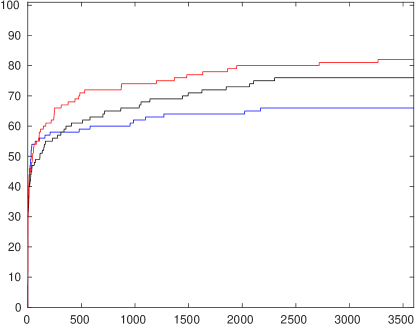

where . This formulation avoids an explicit representation of altogether, at the cost of having an exponential number of constraints. Nevertheless, these constraints can be separated in polynomial time by a simple greedy method, and [356] devises a problem-specific branch-and-cut method combining the above model (1) with dynamic generation of the inequalities from (2) (and some other valid inequalities), and incorporating dedicated heuristics, propagation and pruning rules as well as a branching scheme. Using numerical experiments detailed in [356] as an example, Figure 3 illustrates a key point we wish to emphasize for COPs in general—namely, that (on average) dedicated solvers can solve more instances more quickly than by simply plugging a compact model into a general-purpose MIP solver, and prove better quality guarantees in cases that took unreasonably long to solve to optimality.

A binary IP formulation analogous to (2) can also be given for -min(), based on the following result (we omit its straightforward proof):

Lemma 3.

A set is a (inclusion-wise minimal) feasible support for w.r.t. if and only if for all (maximal) infeasible supports .

This IP then reads

| (3) |

In fact, Lemma 3 and (3) extend directly to -min(); however, in contrast to the spark case (2), the separation problem for the inequalities in (3) w.r.t. maximal infeasible supports can be shown to be generally NP-hard [359]. The approach is strongly related to the model from [234] discussed earlier, which essentially splits the support into that of the positive and negative parts of , respectively. This split seems to have some structural advantages w.r.t. greedy separation heuristics, even though the underlying IP has (roughly) twice as many variables due to the transformation to MaxFS/MinIISC.

Note that one can also make use of the spark IP formulation, and (with slight modifications) the solver from [356], to tackle -min(): While -min(, ) searches for the overall smallest circuit of the vector matroid induced by the columns of , -min() can be viewed as seeking the smallest circuit of the vector matroid over that mandatorily contains the right-hand-side column (see also [119]). Thus, -min() is equivalent to

| (4) | ||||

| s.t. |

i.e., the covering-type inequalities hold for all complements of bases of the matroid over the columns of that contain . Indeed, it can easily be seen that bases containing the -th column of correspond to infeasible supports (w.r.t. ) from Lemma 3 once that column is removed. While these infeasible supports are not necessarily maximal (there could be columns of that are linearly dependent on the ones contained in the basis and thus could be included in a linear combination without changing infeasibility), the separation problem can still be solved by a greedy method, unlike for the covering inequalities corresponding to maximal infeasible supports. We will explore big-M selection and the approach to solve -min() via (4) a bit further as an illustrative example in Section 3.2.1 below.

Besides tightening big-M bounds as discussed earlier, it has been shown in several cardinality minimization applications that standard (general-purpose) branch-and-bound MIP solvers can be improved significantly by exploiting problem-specific heuristics and relaxations (or methods tailored to the specific structure of the relaxations encountered in the process of solving the MIPs), see, e.g., [291, 377, 376, 356]. Of course, this also holds for certain mixed-integer nonlinear programming (MINLP) formulations. An example is the efficient heuristic providing high-quality starting solutions for the exact branch-and-cut scheme (including specialized cuts and branching rules) for -min(, , ) recently proposed in [177].

A general impression, which may be gleaned from all the MIP efforts in the aforementioned references is that finding good or even optimal solutions is often possible with dedicated heuristics (including running MIP solvers for a limited amount of time), but that proving optimality is hard not only in theory but also in practice.

Finally, we point out that cardinality minimization problems could also be solved by means of a sequence of cardinality-constrained problems with for , until the first feasible subproblem is found (indicating minimality of the respective cardinality level); of course, one could also apply, e.g., binary search in this context. Depending on the concrete constraints, since this sequential approach leaves the possibility to choose an arbitrary objective function, one could simplify the feasible set by moving parts of it into the objective—for instance, -min() could be tackled by solving -cons(, , ) for until the first subproblem with optimal objective value of at most was found.

3.2.1 An Illustrative Example

Since (4) appears to be novel, we adapted the spark-specific code from [356] to this variant in order to, in the following, provide an illustrative example on how heavily exploiting problem-specific knowledge can significantly improve the performance of exact solvers versus black-box models. The following example consists of the matrix from instance 67 from [356] (a binary parity-check matrix of a rate- WRAN LDPC code) and a right-hand side , where has nonzero components with positions drawn uniformly at random and entries drawn i.i.d. from the standard normal distribution. The (modified) spark code is implemented using the open-source MIP solver SCIP [192], which we also employ as a black-box solver for the standard big-M formulation of -min(), i.e.,

| (5) |