Zeroth-Order Methods for Convex-Concave Minmax Problems: Applications to Decision-Dependent Risk Minimization

Abstract

Min-max optimization is emerging as a key framework for analyzing problems of robustness to strategically and adversarially generated data. We propose a random reshuffling-based gradient free Optimistic Gradient Descent-Ascent algorithm for solving convex-concave min-max problems with finite sum structure. We prove that the algorithm enjoys the same convergence rate as that of zeroth-order algorithms for convex minimization problems. We further specialize the algorithm to solve distributionally robust, decision-dependent learning problems, where gradient information is not readily available. Through illustrative simulations, we observe that our proposed approach learns models that are simultaneously robust against adversarial distribution shifts and strategic decisions from the data sources, and outperforms existing methods from the strategic classification literature.

1 Introduction

The deployment of learning algorithms in real-world scenarios necessitates versatile and robust algorithms that operate efficiently under mild information structures. Min-max optimization has been used as a tool ensure robustness in variety of domains e.g. robust optimization [BTEGN09], robust control [HÅBB13], to name a few. Recently, min-max optimization has emerged as a promising framework for framing problems of algorithmic robustness against adversaries [GPAM+14, SKL17, MMS+17], strategically generated data [DRS+18, BHK20], and distributional shifts in dynamic environments [YLMJ21].

Despite this, recent works in machine learning and robust optimization on designing and analyzing stochastic algorithms for min-max optimization problems have largely operated on a number of assumptions that preclude their application to a broad range of real-world problems e.g., access to first-order oracles that provide exact gradients [YKH20, NSH+19, JNJ20] or restrictive structural assumptions such as strong convexity [LLC+20, WBMR20, SBDG21]. Moreover, the developed theory is often not well-aligned with the practical implementation of these algorithms in real-world machine learning applications. For example, [BSG20] propose zeroth-order methods for convex-concave problems but the proposed algorithm may not be suitable for machine learning applications where the objective function is a sum of large numbers of component functions (depending on the size of dataset). Indeed, in order to compute the gradient estimate at any iteration Beznosikov et al requires perturbing all the functions which might not be suitable/possible for many applications. Furthermore, stochastic gradient methods are often used with random reshuffling (without replacement) in practice, yet their theoretical performance is usually characterized under the assumption of uniform sampling with replacement [Bot09, JNN19].

In this work, we do away with these assumptions and formulate a gradient-free (zeroth-order), random reshuffling-based algorithm with non-asymptotic convergence guarantees under mild structural assumptions on the underlying min-max objective. Our convergence guarantees are established by balancing the bias and variance of the zeroth-order gradient estimator [BLM18], using coupling-based arguments to analyze the correlations between iterates due to the random reshuffling procedure [JNN19], and exploiting the recent connections between the Optimistic Gradient Descent Ascent (OGDA) and Proximal Gradient algorithms [MOP20b].

One of the primary problem areas in which such an algorithm becomes necessary is in learning from strategically generated or decision-dependent data, a classical problem in operations research (see, e.g., [HBT18] and references therein). This problem has garnered a lot of attention of late in the machine learning community under the name \sayperformative prediction [PZMDH20, MPZ21, BHK20] due to the growing recognition that learning algorithms are increasingly dealing with data from strategic agents. In such problems, assuming access to the response map of strategic agents is often too restrictive, and the introduction of agent’s strategic responses into a convex loss function can often result in non-convex objectives.

As an example of such a decision-dependent problem, consider a scenario in which a ride-sharing platform seeks to devise an adaptive pricing strategy which is responsive to changes in supply and demand. The platform observes the current supply and demand in the environment and adjusts the price to increase the supply of drivers (and potentially decrease the demand) as needed. Drivers, however, have the ability to adjust their availability, and can strategically create dips in supply to trigger price increases. Such gaming has been observed in real ride-share markets (see, e.g., [Ham19, You19]) and results in negative externalities like higher prices for passengers. Importantly, in this situation, the platform does not observe precisely the decision making process of the drivers, only their strategically generated availability, and must learn to optimize through these agents’ responses. This lack of precise knowledge regarding the data generation process, and the reactive nature of the data, motivate the use of game theoretic abstractions for the decision problem, as well as algorithms for finding solutions in the absence of full information.

Previous work analyzing this problem studies this phenomenon through the lens of risk minimization in which the data distribution is decision-dependent, and seeks out settings in which the decision maker can optimize the decision-dependent risk [MPZ21]. These works, however, do not account for model misspecification in their analysis. In particular, if the data generation model is incorrect, the performance of the optimal solution returned by their training methods may potentially degrade rapidly, something we explore in our experiments.

We show that the decision-dependent learning (performative prediction) problem can be robustified by taking a distributional robustness perspective on the original problem. Moreover, we show that, under mild assumptions, the distributionally robust decision-dependent learning problem can be transformed to a min-max problem and hence our zeroth-order random reshuffling algorithm can be applied. The gradient-free nature of our algorithm is important for applications where data is generated by strategic users that one must query; in these scenarios, the decision-maker is unlikely to access the best response map (data generation mechanism) of the strategic users, and hence will lack access to precise gradients.

Contributions.

In this paper, we analyze the class of convex-concave min-max problems given by

| (1) |

where , , and has the finite-sum structure given by , where denote individual loss functions. This formulation is ubiquitous in machine learning applications, where the overall loss objective is often the average of the loss function evaluated over each data point in a dataset.

The contributions of this paper can be summarized as follows.

-

I)

We propose an efficient zeroth-order random reshuffling-based OGDA algorithm for a convex-concave min-max optimization problem, without assuming any other structure on the curvature of the min-max loss (e.g., strong convexity or strong concavity). We provide (to our knowledge) the first non-asymptotic analysis of OGDA algorithm with random reshuffling and zeroth-order gradient information.

-

II)

As an important application, we formulate the Wasserstein distributionally robust learning with decision-dependent data problem as a constrained finite-dimensional, smooth convex-concave min-max problem of the form (1). In particular, we consider the setting of learning from strategically generated data, where the goal is to fit a generalized linear model, and where an ambiguity set is used to capture model misspecification regarding the data generation process. This setting encapsulates a distributionally robust version of the recently introduced problem of strategic classification [HMPW16]. We show that this problem, under mild assumptions on data generation model and the ambiguity set, can be transformed into a convex-concave min-max problem to which our algorithm applies.

-

III)

We complement the theoretical contributions of this paper by presenting illustrative numerical examples.

2 Related Work

Our work draws upon the existing literature on zeroth-order methods for min-max optimization problems, decision-dependent learning (performative prediction), and distributionally robust optimization.

Zero-Order Methods for Min-Max Optimization.

Zeroth-order methods provide a computationally efficient method for applications in which first-order or higher-order information is inaccessible or impractical to compute, e.g., when generating adversarial examples to test the robustness of black-box machine learning models [LLC+20, LCK+20, CZS+17, IEAL18, TTC+19, LLW+19, AH17]. Recently, Liu et al. and others [LLC+20, GJZ18, WBMR20] provided the first non-asymptotic convergence bounds for zeroth-order algorithms, based on analysis methods for gradient-free methods in convex optimization [NS17]. However, these works assume that the min-max objective is either strongly concave in the maximizing variable [LLC+20, WBMR20] or strongly convex [GJLJ17] in the minimizing variable, an assumption that fails to hold in many applications [DRS+18, YLMJ21]. In contrast, the zeroth-order algorithm presented in this work provides non-asymptotic guarantees under the less restrictive assumption that the objective function is convex-concave. In particular, we present the first (to our knowledge) zeroth-order variant of the Optimistic Gradient Ascent-Descent (OGDA) algorithm [MOP20b, MOP20a].

In single-variable optimization problems, first-order stochastic gradient descent algorithms are empirically observed to converge faster when random reshuffling (RR, or sampling without replacement) is deployed, compared to sampling with replacement [RR11, Bot09]. Although considerably more difficult to analyze theoretically, gradient-based RR methods have recently been shown to enjoy faster convergence when the underlying objective function is convex [Sha16, JNN19, MKR21, HS19, SS19, GOP21, RGP20]. Recently, these theoretical results have been extended to first-order methods for convex-concave min-max optimization problems [YLMJ21]; in this paper, we further extend these results to the case of zero-order algorithms. Specifically, we present the first (to our knowledge) non-asymptotic convergence rates for zeroth-order random reshuffling min-max optimization algorithms.

Distributionally Robust Optimization.

Distributionally Robust Optimization (DRO) seeks to find solutions to optimization problems (e.g., supervised learning tasks) robust against changes in the data distribution between training and test time [MMS+17, YLMJ21]. These distributional differences may arise due to imbalanced data, sample selection bias, or adversarial perturbations or deletions [CSSL09, MMS+17], and are often modeled as min-max optimization problems, in which the classifier and an adversarial noise component are respectively modeled as the minimizer and maximizer of a common min-max loss objective [Bag05, BBC10, GMT14, GYdH15, RM19]. In particular, the noise is assumed to generate the worst possible loss corresponding to a bounded training data distribution shift, with the bound given by either the -divergence or Wasserstein distance. [YLMJ21, BTHW+13, ND16, HNSS18, SAEK15]. While this work considers adversarial noise in generated data, largely in a worst-case context, it has yet to capture strategically generated data wherein a data source generates data via a best response mapping.

Strategic Classification and Performative Prediction.

Strategic classification [HMPW16, DRS+18, KTS+19, SBKK20] and performative prediction [PZMDH20, MDPZH20, MPZ21, DX20] concern supervised learning problems in which the training data distribution shifts in response to the deployed classifier or predictor more generally. This setting naturally arises in machine learning applications in which the selection of the deployed classifier either directly changes the training data (e.g., decisions based on credit scores, such as loan approvals, themselves change credit scores), or prompts the data source to artificially alter their attributes (e.g. withdrawals during bank runs spur worried clients to make more withdrawals) [PZMDH20, MDPZH20, MPZ21]. Here, the learner accesses only perturbed features representing the strategic agents’ best responses to a deployed classifier, and not the true underlying features [DRS+18]. This is a recently introduced formulation to machine learning; the results in this body of literature (to our knowledge) have not introduced the concept of robustness to model misspecification or the data generation process, in the same manner as we capture in this work.

3 Preliminaries

Recall that in this paper, we consider the class of convex-concave min-max problems given by:

| (2) |

where , , and , where denote individual loss functions. For convenience, we denote .

Assumption 3.1.

The following statements hold:

-

(i)

The sets and are convex and compact.

-

(ii)

The functions are convex in for each , concave in for each , and -Lipschitz and -smooth in (which implies that , by definition, also possesses the same properties).

For ease of exposition, we denote , , , and define the operators , for each , by:

| (3) |

Observe that under Assumption 3.1, , and and each are monotone111A function is called monotone if for all .. Finally, we define the gap function associated with the loss by

| (4) |

where denotes any min-max saddle point of the overall loss , and denotes any feasible point. This gap function allows us to measure the convergence rate of our proposed algorithm. To this end, we define the -optimal saddle-point of (2) as follows.

Definition 3.1 (-optimal saddle point solution).

A feasible point is said to be an -optimal saddle-point solution of (2) if

4 Algorithms and Performance

In this section we introduce a gradient-free version of the well-studied Optimistic Gradient Descent Ascent (OGDA) algorithm, and give finite time rates showing that it can efficiently find the saddle point in constrained convex-concave problems.

4.1 Zero-Order Gradient Estimates

In our zero-order, random-reshuffling based variant of the OGDA algorithms, we use the one-shot randomized gradient estimator in [Spa97, FKM05, GJZ18, LLC+20]. In particular, given the current iterate and a query radius , we sample a vector uniformly from unit sphere (i.e. ), and define the zeroth-order estimator of the min-max loss to be:

Properties of this zeroth-order estimator, derived in [BLM18], are reproduced as Proposition A.4 in Appendix A.1.

4.2 Optimistic Gradient Descent Ascent with Random Reshuffling (OGDA-RR)

In this subsection, we formulate our main algorithm, Optimistic Gradient Descent Ascent with Random Reshuffling (OGDA-RR). In each epoch , the algorithm generates a uniformly random permutation of independently of any other randomness, and fixes a query radius and search direction . (Note: query radii only depends on epoch indices , and not on sample indices). For each index , we compute the OGDA-RR update as follows:

| (5) |

After repeating this process for epochs, the algorithm returns the step-size-weighted average of the iterates, . Roughly, the weighting described in Theorem 4.1 below optimally balances the bias and variance of the zero-order gradient estimator in Section 4.1.

Theorem 4.1.

Let denote the objective function in the constrained min-max optimization problem given by (1), and let denote any saddle point of . Fix . Suppose Assumption 3.1 holds, and the number of epochs , step sizes sequence , and query radii sequence satisfy:

for some initial step size , initial query radius , parameter , and constant:

Then the iterates generated by the OGDA-RR Algorithm (Alg. 1) satisfy:

Remark.

Note that our OGDA-RR algorithm is more computationally efficient than Alg. 2 in [YLMJ21], even if one replaces the gradient estimates with true gradient values. This is because Alg. 2 in [YLMJ21] requires inner loop iterations to approximate a proximal point update. Here, we avoid this restriction by exploiting the recent perspective that the OGDA update is a perturbed proximal point update [MOP20a, MOP20b]. For more details, see Appendix A.2 for the proof of Theorem 4.1.

5 Applications to Decision-Dependent DRO

In this section we discuss a novel convex-concave min-max reformulation of a class of decision-dependent distributional robust risk minimization problems, which reflects the need for learning classifiers that are simultaneously robust to strategic data sources and adversarial model-specification. In particular, we present a distributionally robust formulation of strategic classification [DRS+18] with generalized linear loss, a semi-infinite optimization problem that can be reformulated to a finite-dimensional convex-concave min-max problem.

Strategic classification is an emerging paradigm in machine learning which attempts to “close the loop"— i.e., account for data (user) reaction at training time—while designing classifiers to be deployed in strategic environments in the real world, where deploying naïve classifier (designed ignoring the distribution shift) can be catastrophic. Modeling the exact behavior of such strategic interactions is very complex, since the decision-maker (learner) does not have access to the strategic users’ preferences and hence lacks access to their best response function. To overcome this difficulty, we use a natural model for these strategic behaviors that has been exploited in Dong et. al.(2018), and then impose robustness conditions (in the form of an ambiguity set on the decision-dependent data distribution) to capture model misspecification. To facilitate the discussion, we provide a primer on decision-dependent DRO in the next subsection.

5.1 Primer on decision-dependent distributionally robust optimization

Consider a generalized linear problem, where the goal is to estimate the parameter , which is assumed to be a compact set, by solving the following convex optimization program:

where is a smooth convex function and the tuple is sampled from an unknown distribution , often approximated by the empirical distribution of a set of observed data. The generalized linear model encompasses a wide range of machine learning formulations [MN19].

A distributionally robust generalized linear problem, on the other hand, minimizes the worst case expectation over an uncertainty set in the space of probability measures. This setup can be envisioned as a game between a learning algorithm and an adversary. Based on parameters chosen by the learning algorithm, the adversary then picks a probability measure from the uncertainty set which maximizes the risk for that choice of parameter:

where . Typically is chosen as a Wasserstein ball around the empirical distribution of a set of observed data points, , sampled independently from the data distribution . Then, for any the uncertainty set is given by .

A critique of the above problem formulation is that the underlying data distribution is considered fixed, while in many strategic settings underlying data distribution will depend on the classifier parameter . Decision-dependent supervised learning aims to tackle such distribution shifts. When specialized to the generalized linear model, the problem formulation becomes:

where . In this work, we take a step forward and work with the distributionally robust decision-dependent generalized linear model, defined as:

| (6) |

where and . Here, the dependence of on the choice of classifier is captured by its inclusion in . To describe decision-dependent distribution shifts , we restrict our focus to the setting of strategic classification. The following subsection formalizes our setting.

5.2 Model for strategic response

Below, we denote the data points sampled from true distribution by where is a unknown, underlying distribution. For ease of presentation, we associate each data point index with an agent. For each agent , let denote its utility function that a strategic agent seeks to maximize. In other words, when a classifier parametrized by is deployed, the agent responds by reporting , defined as:

Note that we allow different agent to have different utility function.

We now impose the following assumptions on the utility functions; these are crucial for ensuring guaranteed convergence of our proposed algorithms.

Assumption 5.1.

For each agent , define , where satisfies:

-

(i)

for all ;

-

(ii)

is convex on ;

-

(iii)

is positive homogeneous222A function is positive homogenous of degree r if for any scalar and we have of degree ;

-

(iv)

Its convex conjugate is -Lipschitz and -smooth on .

As is pointed out in Dong et. al. (2018), a large class of functions satisfy the requirements posited in Assumption 5.1. For example, for any arbitrary norm and any the function is a candidate. Note that these assumptions are not very restrictive and capture a large variety of practical scenarios [DRS+18]. A natural consequence of the above modeling paradigm is that . To wit, the agents act strategically only if their true label is . This is a reasonable setting for many real world applications [DRS+18]. We now present a technical lemma which will be helpful in subsequent presentation.

Lemma 5.2 (Dong et. al. (2018)).

Under Assumption 5.1, for each agent , the set of best responses is finite and bounded. The function is convex. To wit, for any : where

Against the preceding backdrop, we now present the convex-concave min-max reformulation of the Wasserstein Distributionally Robust Strategic Classification (WDRSC) problem.

5.3 Reformulation of the WDRSC Problem

The WDRSC problem formulation contains two main components—the strategic component that accounts for a distribution shift in response to the choice of classifier , and the adversarial component that accounts for the uncertainty set . As per the modeling assumptions described in Section 5.2, we have and for all . We now impose certain restrictions on the adversarial component that would enable us to reformulate the WDRSC problem as a convex-concave min-max optimization problem. Crudely speaking, we allow adversarial modifications on features for all data points, but adversarial modifications on labels only when the true label is .

For the distributionally robust strategic classification problem, we consider a specific form of uncertainty set that allows us to reformulate the infinite-dimensional optimization problem as a finite-dimensional convex-concave min-max problem. As described above, in our formulation, the features of a given data point can be perturbed strategically if , but not if . On top of the strategic perturbations we also consider the adversarial perturbations to the data points. Specifically, we also assume that the adversary can perturb both the features and label of a data point if , but can only perturb the features and not the label if . A rigorous exposition of this restriction is deferred to Appendix B.1. Under these assumptions, we now present a convex-concave min-max reformulation of the WDRSC problem.

Theorem 5.3.

Let the strategic behavior of the agents be governed in accordance with Assumption 5.1. Suppose is convex and -smooth. In addition, suppose is non-decreasing. Then the WDRSC problem (6) can be reformulated into the following convex-concave min-max problem:

| (7) | ||||

where for any , we have concisely written as .

The proof of Theorem 5.3 is presented in Appendix B.2.

Remark.

The non-decreasing assumption on the map is not overly restrictive; in fact, it is satisfied by the logistic regression model in supervised learning (see Appendix C).

Remark.

Note that we can convert the smooth convex-concave minmax problem (7) into a non-smooth convex minimization problem by explictly taking maximization over . But we refrain from doing as it has been observed [YLMJ21] that solving the smooth minimax optimization problem is faster than solving the non-smooth problem. In fact, we have presented an experimental study in Appendix C which corroborates this observation.

Throughout the rest of this paper, we denote the min-max objective in (7) by .

6 Empirical Results

In this section we deploy zeroth-order OGDA algorithm with random reshuffling to solve the convex concave reformulation of WDRSC as presented in (7). We point out that in order to solve (7), the zeroth-order method should only be applied to estimate the gradient with respect to . This is because the gradient with respect to other variables, namely , can be exactly computed. Specifically, to compute derivative with respect to the designer must know the best response function which is often not available and it can only be queried.

We now present some illustrations of the empirical performance of our proposed algorithm, as well as empirical justification for solving the WDRSC problem over existing prior approaches to strategic classification.

6.1 Experimental Setup

Our first set of empirical results uses synthetic data to illustrate the effectiveness of our algorithms. The datasets used in this section are constructed as follows: the ground truth classifier and features are sampled as and , for each , while the ground truth labels are given by for each , where . We use with . The first five of the features are chosen to be strategic. In all experiments, we take and . Each strategic agent has a utility function given by:

| (8) |

where denote the perturbation “power" of agent . For simplicity, we assume all agents are homogeneous, in the sense that for all ; in practice, one need not impose this assumption. Given this utility function, the best response of agents takes the form:

| (9) |

where, in our simulations, we fix . We reemphasize that our algorithm does not use the value of in any of its computations. For purposes of illustration, we focus on the performance of the following algorithms:

-

(A-I)

Zeroth-order optimistic-GDA with random reshuffling (see Algorithm 1),

-

(A-II)

Zeroth-order optimistic-GDA without random reshuffling (see Appendix C),

-

(A-III)

Zeroth-order stochastic-GDA with random reshuffling (see Appendix C),

-

(A-IV)

Zeroth-order stochastic-GDA without random reshuffling (see Appendix C).

and we evaluate the proposed algorithms and model formulation on two criteria:

- (i)

-

(ii)

Accuracy: Given a data set , the accuracy of a classifier is measured as . Under this criterion we compare the accuracy under different perturbations for different classifiers ;

To compute suboptimality, we first compute a true min-max saddle point via a first order gradient based algorithm (namely, GDA). All experiments were run using Python 3.7 on a standard MacBook Pro laptop (2.6 GHz Intel Core i7 and 16 GB of RAM).

6.2 Results

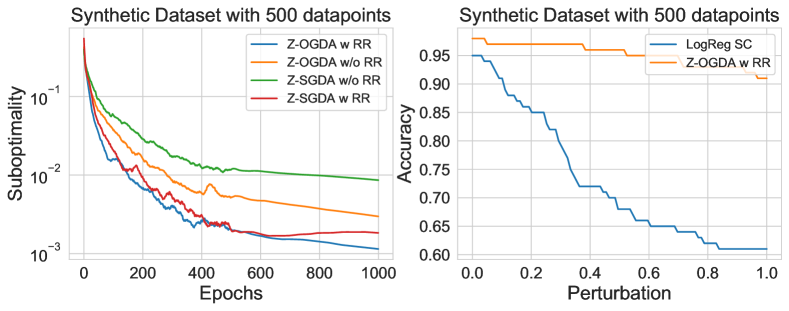

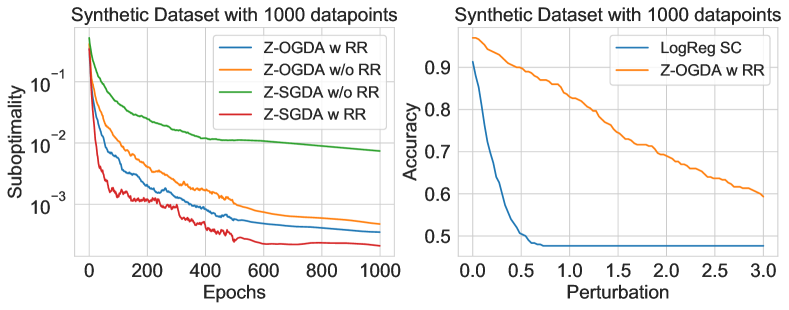

Simulation results presented in Figure (1(a))-(1(b)) show that our proposed algorithm (i.e. (A-I)) outperforms algorithms without reshuffling (i.e. (A-II) and (A-IV)). However, its performance resembles that of zeroth-order stochastic-GDA with random reshuffling. More experimental studies need to be conducted to more conclusively determine whether (A-I) outperforms (A-III), or vice versa. In fact , there has been no theoretical investigations even for the first order stochastic-GDA algorithm with random reshuffling; this is an interesting future direction to explore.

In Figure 1, we also compare the robustness of the classifier obtained by using Algorithm (A-I) with that obtained from prior work on solving probems of strategic classification trained with (referred as LogReg SC in Figure 1). As expected, due to the formulation, the performance of the classifier obtained via (A-I) degrades gracefully even when subject to large perturbations, while the performance of existing approaches to strategic classification degrades rapidly. Further numerical results on synthetically generated and real world datasets are given in Appendix C.

7 Conclusion

This paper presents the first (to our knowledge) non-asymptotic convergence rates for a gradient-free stochastic min-max optimization algorithm with random reshuffling. Our theoretical results, established for smooth convex-concave min-max objectives, do not require any additional, restrictive structural assumptions to hold. As a concrete application, we reformulate a distributionally robust strategic classification problem as a convex-concave min-max optimization problem that can be iteratively solved using our method. Empirical results on synthetic and real datasets demonstrate the efficiency and effectiveness of our algorithm, as well as its robustness against adversarial distributional shifts and strategic behavior of the data sources. Immediate directions for future work include establishing convergence results for the random-reshuffling based Stochastic Gradient Descent Ascent (SGDA-RR) algorithm, as well as performing more extensive experimental studies to better understand the empirical performance of our algorithm.

Acknowledgements

Research supported by NSF under grant DMS 2013985 “THEORINet: Transferable, Hierarchical, Expressive, Optimal, Robust and Interpretable Networks”. Chinmay Maheshwari, Chih-Yuan Chiu and S. Shankar Sastry were also supported in part by U.S. Office of Naval Research MURI grant N00014-16-1- 2710.

References

- [AH17] Charles Audet and Warren Hare. Derivative-free and blackbox optimization. Springer, 01 2017.

- [Bag05] J. A. Bagnell. Robust supervised learning. In AAAI, volume 2, pages 714–719, 2005.

- [BBC10] Dimitris Bertsimas, David Brown, and Constantine Caramanis. Theory and applications of robust optimization. SIAM Review, 53, 10 2010.

- [BHK20] Gavin Brown, Shlomi Hod, and Iden Kalemaj. Performative prediction in a stateful world. arXiv preprint arXiv:2011.03885, 2020.

- [BLM18] Mario Bravo, David Leslie, and Panayotis Mertikopoulos. Bandit learning in concave N-person games. In Proceedings of the 32nd International Conference on Neural Information Processing Systems, NIPS’18, page 5666–5676, Red Hook, NY, USA, 2018.

- [Bot09] L. Bottou. Curiously fast convergence of some stochastic gradient descent algorithms. In Proceedings of the Symposium on Learning and Data Science, Paris, 2009.

- [BSG20] Aleksandr Beznosikov, Abdurakhmon Sadiev, and Alexander Gasnikov. Gradient-free methods with inexact oracle for convex-concave stochastic saddle-point problem. ArXiv, 2020.

- [BTEGN09] Aharon Ben-Tal, Laurent El Ghaoui, and Arkadi Nemirovski. Robust optimization. Princeton university press, 2009.

- [BTHW+13] A. Ben-Tal, D. D. Hertog, A. D. Waegenaere, B. Melenberg, and G. Rennen. Robust solutions of optimization problems affected by uncertain probabilities. Manag. Sci., 59:341–357, 2013.

- [CSSL09] Joaquin Candela, Masashi Sugiyama, Anton Schwaighofer, and Neil D. Lawrence. Dataset Shift in Machine Learning. The MIT Press, 2009.

- [CZS+17] P. Chen, Huan Zhang, Yash Sharma, Jinfeng Yi, and Cho-Jui Hsieh. ZOO: Zeroth-Order Optimization-based Black-box Attacks to Deep Neural Networks Without Training Substitute Models. Proceedings of the 10th ACM Workshop on Artificial Intelligence and Security, 2017.

- [DRS+18] Jinshuo Dong, Aaron Roth, Zachary Schutzman, Bo Waggoner, and Zhiwei Steven Wu. Strategic classification from revealed preferences. In Proceedings of the 2018 ACM Conference on Economics and Computation, EC ’18, page 55–70, New York, NY, USA, 2018. Association for Computing Machinery.

- [DX20] Dmitriy Drusvyatskiy and Lin Xiao. Stochastic optimization with decision-dependent distributions. arXiv, 2020.

- [FKM05] Abraham D. Flaxman, Adam Tauman Kalai, and H. Brendan McMahan. Online convex optimization in the bandit setting: Gradient descent without gradient. In Proceedings of the Sixteenth Annual ACM-SIAM Symposium on Discrete Algorithms, SODA ’05, page 385–394, USA, 2005. Society for Industrial and Applied Mathematics.

- [GJLJ17] Gauthier Gidel, Tony Jebara, and Simon Lacoste-Julien. Frank-wolfe algorithms for saddle point problems. In Proceedings of the 20th International Conference on Artificial Intelligence and Statistics, volume 54 of Proceedings of Machine Learning Research, pages 362–371, Fort Lauderdale, FL, USA, 20–22 Apr 2017. PMLR.

- [GJZ18] Xiang Gao, B. Jiang, and S. Zhang. On the information-adaptive variants of the ADMM: An iteration complexity perspective. Journal of Scientific Computing, 76:327–363, 2018.

- [GMT14] Virginie Gabrel, Cécile Murat, and Aurélie Thiele. Recent advances in robust optimization: An overview. European Journal of Operational Research, 235(3):471–483, 2014.

- [GOP21] Mert Gürbüzbalaban, A. Ozdaglar, and P. Parrilo. Why random reshuffling beats stochastic gradient descent. Math. Program., 186:49–84, 2021.

- [GPAM+14] Ian Goodfellow, Jean Pouget-Abadie, Mehdi Mirza, Bing Xu, David Warde-Farley, Sherjil Ozair, Aaron Courville, and Yoshua Bengio. Generative adversarial nets. In Z. Ghahramani, M. Welling, C. Cortes, N. Lawrence, and K. Q. Weinberger, editors, Advances in Neural Information Processing Systems, volume 27, 2014.

- [GYdH15] Bram L. Gorissen, Ihsan Yanikoglu, and Dick den Hertog. A practical guide to robust optimization. Omega, 53(C):124–137, 2015.

- [HÅBB13] Martin Hast, Karl Johan Åström, Bo Bernhardsson, and Stephen Boyd. Pid design by convex-concave optimization. In 2013 European Control Conference (ECC), pages 4460–4465. IEEE, 2013.

- [Ham19] Isobel Hamilton. Uber drivers are reportedly colluding to trigger surge prices because they say the company is not paying them enough. Business Insider, June 14, 2019.

- [HBT18] Lars Hellemo, Paul I Barton, and Asgeir Tomasgard. Decision-dependent probabilities in stochastic programs with recourse. Computational Management Science, 15(3):369–395, 2018.

- [HMPW16] Moritz Hardt, Nimrod Megiddo, Christos Papadimitriou, and Mary Wootters. Strategic classification. In Proceedings of the 2016 ACM Conference on Innovations in Theoretical Computer Science, ITCS ’16, page 111–122, New York, NY, USA, 2016. Association for Computing Machinery.

- [HNSS18] Weihua Hu, Gang Niu, Issei Sato, and Masashi Sugiyama. Does distributionally robust supervised learning give robust classifiers? In Jennifer Dy and Andreas Krause, editors, Proceedings of the 35th International Conference on Machine Learning, volume 80 of Proceedings of Machine Learning Research, pages 2029–2037. PMLR, 10–15 Jul 2018.

- [HS19] Jeff Z. HaoChen and S. Sra. Random shuffling beats SGD after finite epochs. In ICML, 2019.

- [IEAL18] Andrew Ilyas, Logan Engstrom, Anish Athalye, and Jessy Lin. Black-box adversarial attacks with limited queries and information. In Jennifer Dy and Andreas Krause, editors, Proceedings of the 35th International Conference on Machine Learning, volume 80 of Proceedings of Machine Learning Research, pages 2137–2146. PMLR, 10–15 Jul 2018.

- [JNJ20] Chi Jin, Praneeth Netrapalli, and Michael I. Jordan. What is local optimality in nonconvex-nonconcave minimax optimization? In ICML, 2020.

- [JNN19] Prateek Jain, Dheeraj M. Nagaraj, and Praneeth Netrapalli. SGD without replacement: sharper rates for general smooth convex functions. In ICML, 2019.

- [KTS+19] M. Khajehnejad, Behzad Tabibian, B. Schölkopf, A. Singla, and M. Gomez-Rodriguez. Optimal Decision Making Under Strategic Behavior. ArXiv, abs/1905.09239, 2019.

- [LCK+20] Sijia Liu, Pin-Yu Chen, Bhavya Kailkhura, Gaoyuan Zhang, Alfred O. Hero III, and Pramod K. Varshney. A primer on zeroth-order optimization in signal processing and machine learning: Principals, recent advances, and applications. IEEE Signal Processing Magazine, 37(5):43–54, 2020.

- [Lee13] John M. Lee. Introduction to Smooth Manifolds. Springer Science+Business Media New York, 2013.

- [LLC+20] Sijia Liu, Songtao Lu, Xiangyi Chen, Yao Feng, Kaidi Xu, Abdullah Al-Dujaili, Mingyi Hong, and Una-May O’Reilly. Min-max optimization without gradients: Convergence and applications to adversarial ML. In Proceedings of the 37th International Conference on Machine Learning, volume 119 of Proceedings of Machine Learning Research, pages 6282–6293. PMLR, 13–18 Jul 2020.

- [LLW+19] Yandong Li, Lijun Li, Liqiang Wang, Tong Zhang, and Boqing Gong. NATTACK: learning the distributions of adversarial examples for an improved black-box attack on deep neural networks. In arXiv, 2019.

- [MDPZH20] Celestine Mendler-Dünner, Juan Perdomo, Tijana Zrnic, and Moritz Hardt. Stochastic optimization for performative prediction. In Advances in Neural Information Processing Systems, volume 33, pages 4929–4939, 2020.

- [MKR21] Konstantin Mishchenko, Ahmed Khaled, and Peter Richtárik. Random reshuffling: Simple analysis with vast improvements, 2021.

- [MMS+17] Aleksander Madry, Aleksandar Makelov, Ludwig Schmidt, Dimitris Tsipras, and Adrian Vladu. Towards deep learning models resistant to adversarial attacks. ArXiv, 06 2017.

- [MN19] Peter McCullagh and John A Nelder. Generalized Linear Models. Routledge, 2019.

- [MOP20a] Aryan Mokhtari, A. Ozdaglar, and S. Pattathil. A Unified Analysis of Extra-gradient and Optimistic Gradient Methods for Saddle Point Problems: Proximal Point Approach. In AISTATS, 2020.

- [MOP20b] Aryan Mokhtari, A. Ozdaglar, and S. Pattathil. Convergence Rate of O(1/k) for optimistic gradient and extragradient methods in smooth convex-concave saddle point problems. SIAM J. Optim., 30:3230–3251, 2020.

- [MPZ21] John Miller, Juan Perdomo, and Tijana Zrnic. Outside the echo chamber: Optimizing the performative risk. arXiv preprint arXiv:2102.08570, 2021.

- [ND16] Hongseok Namkoong and John C Duchi. Stochastic gradient methods for distributionally robust optimization with f-divergences. In D. Lee, M. Sugiyama, U. Luxburg, I. Guyon, and R. Garnett, editors, Advances in Neural Information Processing Systems, volume 29, 2016.

- [Nes14] Yurii Nesterov. Introductory Lectures on Convex Optimization: A Basic Course. Springer Publishing Company, Incorporated, 1 edition, 2014.

- [NS17] Yurii Nesterov and Vladimir Spokoiny. Random gradient-free minimization of convex functions. Found. Comput. Math., 17(2):527–566, April 2017.

- [NSH+19] Maher Nouiehed, Maziar Sanjabi, Tianjian Huang, J. Lee, and Meisam Razaviyayn. Solving a class of non-convex min-max games using iterative first order methods. In NeurIPS, 2019.

- [PZMDH20] Juan Perdomo, Tijana Zrnic, Celestine Mendler-Dünner, and Moritz Hardt. Performative prediction. In Proceedings of the 37th International Conference on Machine Learning, volume 119 of Proceedings of Machine Learning Research, pages 7599–7609. PMLR, 13–18 Jul 2020.

- [RGP20] Shashank Rajput, Anant Gupta, and Dimitris Papailiopoulos. Closing the convergence gap of SGD without replacement. arXiv e-prints, page arXiv:2002.10400, February 2020.

- [RM19] Hamed Rahimian and Sanjay Mehrotra. Distributionally robust optimization: A review. In SIAM, 08 2019.

- [RR11] Benjamin Recht and Christopher Ré. Parallel stochastic gradient algorithms for large-scale matrix completion. Mathematical Programming Computation, 5, 04 2011.

- [Rud76] Walter Rudin. Principles Of Mathematical Analysis. McGraw-Hill, Inc., 1976.

- [RW21] Benjamin Recht and Stephen Wright. Optimization for Data Analysis. Cambridge University Press, 1 edition, 2021.

- [SAEK15] Soroosh Shafieezadeh-Abadeh, Peyman Mohajerin Esfahani, and D. Kuhn. Distributionally robust logistic regression. In NeurIPS, 2015.

- [SBDG21] Abdurakhmon Sadiev, Aleksandr Beznosikov, Pavel Dvurechensky, and Alexander Gasnikov. Zeroth-Order Algorithms for Smooth Saddle-Point Problems. ArXiv, 2021.

- [SBKK20] Pier Giuseppe Sessa, Ilija Bogunovic, M. Kamgarpour, and A. Krause. Learning to play sequential games versus unknown opponents. ArXiv, abs/2007.05271, 2020.

- [Sha16] O. Shamir. Without-Replacement Sampling for Stochastic Gradient Methods. In NIPS, 2016.

- [SKL17] Jacob Steinhardt, Pang Wei Koh, and Percy Liang. Certified defenses for data poisoning attacks. In Proceedings of the 31st International Conference on Neural Information Processing Systems, NIPS’17, page 3520–3532, Red Hook, NY, USA, 2017.

- [Spa97] J. Spall. A one-measurement form of simultaneous perturbation stochastic approximation. Autom., 33:109–112, 1997.

- [SS19] Itay Safran and O. Shamir. How good is SGD with random shuffling? ArXiv, abs/1908.00045, 2019.

- [TTC+19] Chun-Chen Tu, Pai-Shun Ting, P. Chen, Sijia Liu, Huan Zhang, Jinfeng Yi, Cho-Jui Hsieh, and Shin-Ming Cheng. AutoZOOM: autoencoder-based zeroth order optimization method for attacking black-box neural networks. In AAAI, 2019.

- [WBMR20] Z. Wang, K. Balasubramanian, Shiqian Ma, and Meisam Razaviyayn. Zeroth-order algorithms for nonconvex minimax problems with improved complexities. ArXiv, abs/2001.07819, 2020.

- [YKH20] Junchi Yang, Negar Kiyavash, and Niao He. Global convergence and variance reduction for a class of nonconvex-nonconcave minimax problems. In Advances in Neural Information Processing Systems, volume 33, pages 1153–1165, 2020.

- [YLMJ21] Yaodong Yu, Tianyi Lin, Eric V. Mazumdar, and Michael I. Jordan. Fast distributionally robust learning with variance reduced min-max optimization. ArXiv, abs/2104.13326, 2021.

- [You19] Soo Youn. Uber, Lyft drivers coordinate to manipulate surge pricing at Virginia airport over pay concerns: Report. ABC News, May 18, 2019.

Appendix A Results for the Proof of Theorem 4.1

A.1 Lemmas for Theorem 4.1

First, we list some fundamental facts regarding projections onto convex, compact subsets of an Euclidean space. Below, for any fixed convex, compact subset , we denote the projection operator onto by for each . Note that is well-defined (i.e., exists and is unique) for each , if were convex and compact.

We begin by summarizing some fundamental properties of the projection operator .

Proposition A.1.

Let be compact and convex, and fix arbitrarily. Then:

Proof.

From [Nes14], Lemma 3.1.4 (see also [RW21], Lemma 7.4), we have:

Adding the two expressions and rearranging terms, we obtain:

as given in the first claim. The Cauchy Schwarz inequality then implies:

If , then the second claim becomes , which is clearly true. Otherwise, dividing both sides above by gives the second claim. ∎

Lemma A.2.

Let be a compact, convex subset of , and consider the update , where . Then, for each :

Proof.

Note that:

By definition of , and optimality conditions for the projection operator:

Substituting back, we obtain:

Rearranging and dividing by gives the claim in the lemma. ∎

Next, we state the properties of the mean and variance of the zeroth-order gradient estimator defined in Section LABEL:subsec:_Zeroth-Order_Gradient_Estimates ([BLM18], Lemma C.1). Below, we define the -smoothed loss function by , where denotes the ()-dimensional unit sphere in , denotes the -dimensional unit open ball in , and denotes the continuous uniform distribution over a set. Similarly, we define by , for each . We further define and . Finally, we use to denote the volume of a set in dimensions.

Proposition A.3.

Let and . Then the following holds:

| (10) | ||||

| (11) | ||||

| (12) | ||||

| (13) |

Proof.

First, to establish (10), observe that since and for each , , and :

| (14) | ||||

where (14) follows because Stokes’ Theorem (see, e.g., Lee, Theorem 16.11 [Lee13]) implies that:

The equality (10) now follows by observing that the surface-area-to-volume ratio of is .

Below, we present technical lemmas that allow us to analyze the convergence rate of the correlated iterates in our random reshuffling-based OGDA Algorithm (Alg. 1).

Let denote the permutations drawn from epoch 0 to epoch , and let and denote the iterates obtained at epoch , when the permutations and are used for the epoch , respectively. Moreover, let denote the distribution of under , and for let denote the distribution of with conditioned on the event .

We use the -Wasserstein distance between probability distributions on , defined below, to characterize the distance between and . This is used in the coupling-based techniques employed to establish non-asymptotic convergence results for our random reshuffling algorithm. Note the difference between the -Wasserstein distance for probability distributions on , and the Wasserstein distance on associated with a metric , defined in Appendix B.2 (Definition B.1).

Definition A.1 (-Wasserstein distance between distributions on ).

Let be probability distributions over with finite -th moments, for some , and let denote the set of all couplings (joint distributions) between and . The -Wasserstein distance between and , denoted , is defined by:

The following proposition characterizes the 1-Wasserstein distance as a measure of the gap between Lipschitz functions of random variables.

Proposition A.4 (Kantorovich Duality).

If are probability distributions over with finite second moments, then:

where .

Using [YLMJ21, Lemma C.2], we now bound the difference between the unbiased gap and the biased gap using the Wasserstein metric.

Lemma A.5.

Let denote a saddle point of the min-max optimization problem (2). Then, for each and , the iterates of the OGDA-RR algorithm satisfy:

Proof.

Since and are independently generated permutations of , the iterates and are i.i.d. Thus, we have:

and thus:

| (16) | ||||

| (17) | ||||

| (18) | ||||

| (19) |

where (16) follows by properties of the conditional expectation on and the fact that and are independent, (17) follows from the fact that is Lipschitz, (18) follows from Proposition A.4, and (19) follows from the fact that for any two probability distributions . ∎

The next lemma bounds the difference in the iterates and (assuming, as before, that were fixed and identical for both sequences.)

Lemma A.6.

Denote, with a slight abuse of notation, and . Then:

Proof.

Our proof strategy is to bound the differences between zeroth-order and first-order OGDA updates, and between the OGDA and proximal point updates. To this end, we define:

By the triangle inequality:

| (20) | ||||

Observe that bounding the fourth term is equivalent to bounding the second term, and bounding the fifth term is equivalent to bounding the first term.

To bound the first term on the right hand side, we use Proposition A.3 to conclude that:

| (21) |

For the second term, we use the -Lipschitzness of , for each to conclude that:

| (22) |

For the third term, we observe that if , then:

| (23) |

On the other hand, if , then:

so we have:

| (24) | ||||

| (25) | ||||

| (26) |

so . Here, (24) follows from the definitions of and , as well as Proposition A.1, while (25) holds because the monotonicity of , for each , implies that . Putting together (21), (22), (23), (26), we have:

where the indicator returns 1 if the given event occurs, and 0 otherwise.

Since , we can iteratively apply the above inequality to obtain that, for any and epoch and :

∎

Remark.

In the theorems and lemmas below, we will be concerned with the case where and have the following specific relationship. Let denote the set of all random permutations over the set . For each , let denote the map that swaps, for each input permutation , the -th and -th entries. For each , define the map as follows:

Intuitively, performs a single swap such that the -th position of the permutation is . Clearly, if is a random permutation (i.e., selected from a uniform distribution over ), then has the same distribution as . Based on this construction, we have and . This gives a coupling between and . Since and differ by at most two entries, by iteratively applying Lemma A.6, we have:

as claimed.

Lemma A.7.

If for each , the iterates of the OGDA-RR algorithm satisfy, for each :

where is a constant independent of the sequences and .

Proof.

The iterates of the OGDA-RR algorithm are given by:

| (27) |

where we have defined:

First, by applying Lemma A.2 we have:

| (28) | ||||

Below, we proceed to bound the inner product terms on the right-hand-side of (28). First, we bound :

| (29) | ||||

Note that the final inequality follows by applying Young’s inequality, and noting that is -Lipschitz. Next, we bound :

| (30) | ||||

where the first equality above follows by applying Proposition A.3, (10), and we have used the shorthand . (Recall that ) Next, we upper bound each of the three quantities in (30). First, by Proposition A.3, (11), we have:

| (31) |

with as given in Lemma A.7. Meanwhile, the law of iterated expectations can be used to bound the second quantity:

| (32) |

and we can upper-bound the third quantity as shown below. By using the compactness of and the continuity of , we have:

| (33) |

and using (31) and the bound for each given in (33), we have:

| (34) |

Substituting (34) back into (33), we have:

| (35) |

where is a constant independent of the sequences and . The quantities and can be similarly bounded. Substituting (31), (32), (35) back into (30), and substituting (30) and (29) into (28), we find that:

In particular, since by assumption for each , then:

∎

Finally, to bound the step size terms above, we require the following lemma, which follows from standard calculus arguments.

Lemma A.8.

A.2 Proof of Theorem 4.1

Proof.

(Proof of Theorem 4.1) By applying Lemma A.7 (note that , for each ) and using convex-concave nature of (refer Proposition 1 in [MOP20b]), for each , we have:

| (36) |

Meanwhile, Lemma A.5, Proposition A.4 (Kantorovich Duality), and Lemma A.6 imply that:

Substituting back into (36), we have:

| (37) |

We can now sum the above telescoping terms across the -th epoch, as shown below:

Meanwhile, we have for each , :

where the final inequality follows from Proposition A.3, (12). We can upper bound in a similar fashion. Substituting back into (37), we have:

| (38) | ||||

where .

Appendix B Wasserstein Distributionally Robust Strategic Classification

B.1 Model of Adversary

In this subsection, we formally define our model for the adversary, and the uncertainty set of distributions for the resulting strategically and adversarially perturbed data. For better exposition, in this section we summarize the various distributions used in the main article in Table 1 below.

| Notation | Explanation |

|---|---|

| Unknown underlying distribution | |

| Unknown underlying distribution strategically perturbed by | |

| Empirical distribution of strategically perturbed data | |

| An element of uncertainty set | |

| Conditional distribution of adversarially generated data given data point |

The WDRSL problem formulation contains two main components—the strategic component that accounts for the distribution shift in response to the choice of classifier , and the adversarial component, which accounts for the uncertainty set . As per the modeling assumptions put forth in Section 5.2, we have and for all . For the sake of brevity, we shall use in place of for all .

As per the standard formulation of distributionally robust optimization, we restrict to be a Wasserstein neighborhood of (the empirical distribution of strategic responses ), i.e., we set for some . However, to ensure that the min-max problem reformulated from the WDRSC problem is convex-concave, we further require the adversary to modify the label of an data point in the empirical distribution only when the true label is , although they are still always allowed to modify the feature . As a consequence, this imposes some restrictions on the conditional distribution of , as generated by the adversary, given a data point in the empirical distribution. In particular:

By definition of conditional distributions, we obtain that any distribution can be expressed as the average of the conditional distribution . That is,

Below, we formally state the restriction described above.

Assumption B.1.

We assume that and for all . As a direct result, the uncertainty set is characterized as:

| (40) |

In the following subsection, we reformulate the WDRSC problem with a generalized linear model and with the uncertainty set defined in (40).

B.2 Proof of Theorem 5.3

The proof takes inspirations from [SAEK15, Theorem 1]. First, we define the Wasserstein distance between distributions on with cost function ; note that this is different from the -Wasserstein distance between probability distributions on defined in Appendix A.1.

Definition B.1.

(Wasserstein distance between distributions on with cost Function ) Let be probability distributions over with finite second moments, and let denote the set of all couplings (joint distributions) between and . Given a metric on , we define:

In Theorem 6 and in our proof below, we use the cost function , with a fixed constant , for each and .

Proof.

(Proof of Theorem 5.3) Fix a . Note that . For any , let . We first analyze the inner supremum term, i.e.

Here, denotes the set of all joint distributions that couple and . Since the marginal distribution of is discrete, such couplings are completely determined by the conditional distribution of given for each . That is:

where for any , is a Dirac delta distribution with its support at point .

We introduce some notations. Let and . Let’s introduce two distributions and such that

Due to the constraint (40), we have at every . This implies:

With a slight abuse of notation, we denote , and . The optimization problem of concern then simplifies to:

| s.t. | |||

First, we rewrite the inequality constraint above as follows. Recall that:

Hence,

| s.t. | |||

Now, we can use duality to reformulate the infinite-dimensional optimization problem into a finite-dimensional problem:

which is equivalent to:

We now invoke [YLMJ21, Lemma A.1], which claims that for any and :

We now have:

In the above presented optimization problem we can conclude that:

To further simplify the expression, note that:

so the overall objective can be written as:

We claim that the minimax objective above is convex is . There are mainly two cases to analyze:

-

1.

Case I (): We have as per the strategic classification model. Therefore is a linear function. For every , we claim that the mapping is convex. Indeed, the assumption that is convex and the observation that is affine in ensures the convexity.

-

2.

Case II (): We know from Lemma 5.2 that is convex in . Moreover, the convexity of and the assumption that is non-decreasing ensures that is convex for every .

This concludes the proof.

∎

Appendix C Details on experimental study

Code used to reproduce the results in the main paper is available at https://drive.google.com/drive/folders/1spuB3R6vEU2AqaXxAxeeXo9z5QMVdtdl?usp=sharing

C.1 Algorithms

In our experiments, we compare the OGDA-RR algorithm (Alg. 1) with three other zeroth-order algorithms—Optimistic Gradient Descent Ascent with Sampling with Replacement (OGDA-WR), Stochastic Gradient Descent Ascent with Random Reshuffling (SGDA-RR), and Stochastic Gradient Descent Ascent with Sampling with Replacement (SGDA-WR)—characterized by the update equations (42), (43), (44), respectively. For convenience, we have reproduced (5), the update equation for the OGDA-RR algorithm (Algorithm 1), as (41) below:

| (41) | ||||

| (42) | ||||

| (43) | ||||

| (44) |

where the indices and are as defined in Algorithms 2, 3, and 4.

C.2 Additional Experimental Results

In this section, we present more experimental findings, on both synthetic and real-world datasets, that reinforces the utility of the proposed algorithm. In all experimental results throughout this subsection, we take , and .

C.2.1 Experimental Study On Synthetic Datasets

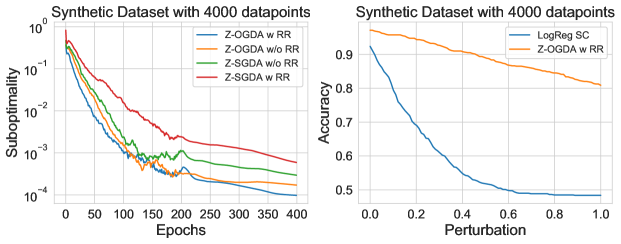

Figure 2 compares the performance of (A-I)-(A-IV) on a synthetic dataset (whose generating process is the same as that described in Section 6), with 4000 training points and 800 test points. Our proposed algorithm performs better empirically compared to most of its counterparts. Moreover, the proposed classifier, (A-I), is significantly more robust than a classifier obtained without considering adversarial perturbations. Note, however, that we cannot make any conclusive claims yet, because of the inherent randomness in these algorithms. Indeed, even if we fix the initialization, then there are two sources of randomness—the construction of the zeroth-order gradient estimator, and the sampling process that generates the data points.

To illustrate the variability in these algorithms’ performance, we run each algorithm repeatedly on a data set with 500 synthetically generated data points, using the same initialization, and present confidence interval plots with standard deviations for the resulting performance (Figure 3). On average, our proposed algorithm (A-I) outperforms the other algorithms (A-II)-(A-IV). It is also interesting to point out that the performance of algorithms with random reshuffling is generally higher, and fluctuate less, compared to the performance of algorithms without random reshuffling.

We now illustrate the performance of our algorithm on two real-world data sets—the \sayGiveMeSomeCredit dataset 333This dataset can be found at https://www.kaggle.com/c/GiveMeSomeCredit, and the \sayPorto Bank data set444This dataset can be found at https://archive.ics.uci.edu/ml/datasets/bank+marketing.

C.2.2 Experimental Study on Credit Dataset

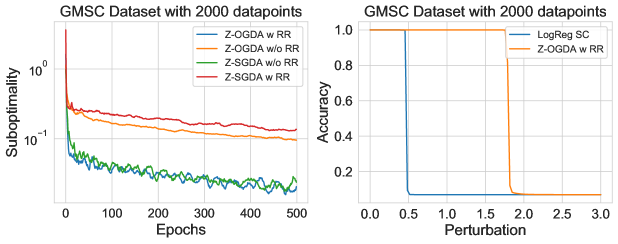

In modern times, banks use machine learning to determine whether or not to finance a customer. This process can be encoded into a classification framework, by using features such as age, debt ratio, monthly income to classify a customer as either likely or unlikely to default. However, those algorithms generally do not account for strategic or adversarial behavior on the part of the agents.

To illustrate the effect of our algorithm on datasets of practical significance, we deploy our algorithms on the \sayGiveMeSomeCredit(GMSC) dataset, while assuming that the underlying features are subject to strategic or adversarial perturbations. We use a subset of the dataset of size 2000 with balanced labels. In Figure 4, we compare the empirical performance of our algorithm (A-I) with that of (A-II)-(A-IV). The left pane shows that (A-I) performs well, and the right pane illustrates that our classifier is significantly more robust to adversarial perturbations in data, compared to the strategic classification-based logistic regression algorithm developed recently in the literature [DRS+18].

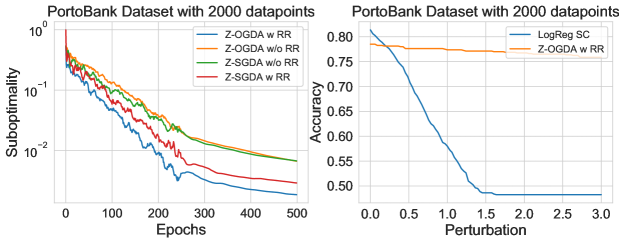

C.2.3 Experimental Study on Porto-Bank Dataset

Next, we present empirical results obtained by applying our algorithm to the \sayPorto-Bank dataset, which describes marketing campaigns of term deposits at Portuguese financial institutions. The classification task in this scenario aims to predict whether a customer with given features (eg. age, job, marital status etc.) would enroll for term deposits.

In Figure 5, we present the performance of our proposed algorithm (A-I) on the Porto-Bank dataset. For ease of illustration, we consider a subset of the dataset with 2000 training data points, 800 test data points, and balanced labels. In Figure 5, we compare the empirical performance of our algorithm (A-I) with that of (A-II)-(A-IV). The left pane shows that (A-I) performs well, while the right pane illustrates that our classifier is significantly more robust to adversarial perturbations in data, compared to the strategic classification-based logistic regression developed recently in the literature [DRS+18].

C.2.4 Effect of on sample complexity

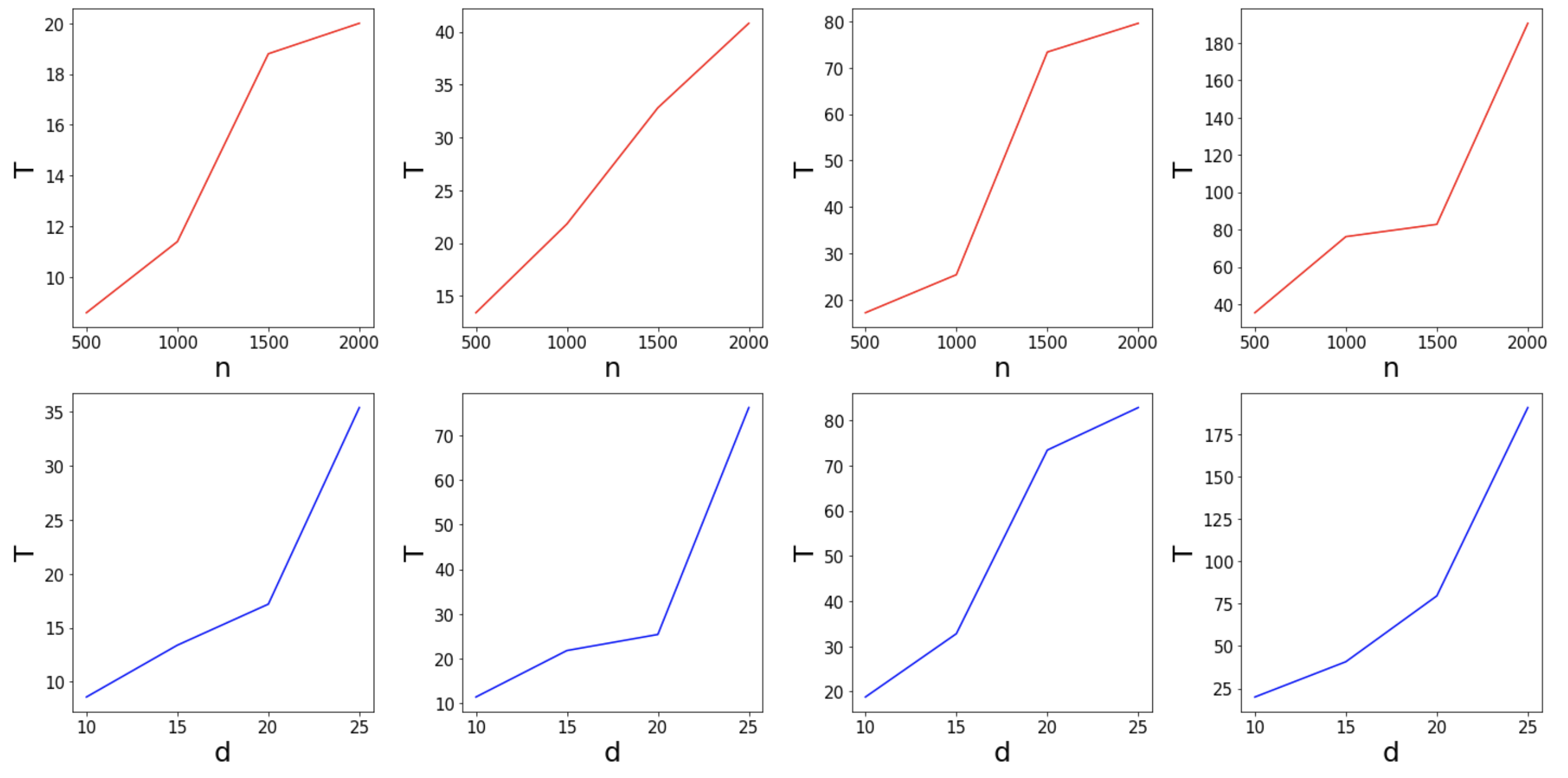

In this part, we demonstrate the empirical results that corroborates the theoretical dependence of sample complexity on . For this purpose, we use synthetic dataset which is generated as per the method described in Section 6.1. Here we work in the setting where and . We fix the suboptimality to and compute the number of samples required in each of the settings of and so that the iterates reach the suboptimality. We present the results in Figure 6.

C.3 Logistic regression as a Generalized linear model

The goal in logistic regression is to maximize the log-likelihood of the conditional probability of (the label) given (the feature). In this model, it is assumed that:

This implies that:

Given a data point the logistic loss is log-likelihood of observing given . For any and :

Now, the log-likelihood is given by:

The goal is to maximize the log likelihood, which is equivalent to minimizing the negative log likelihood. Thus the logistic regression minimizes the following loss:

where . If , then the above loss becomes:

Otherwise, if , then the above loss becomes . Thus, the above loss is equivalent to .