Random feature neural networks learn Black-Scholes type PDEs without curse of dimensionality

Abstract

This article investigates the use of random feature neural networks for learning Kolmogorov partial (integro-)differential equations associated to Black-Scholes and more general exponential Lévy models. Random feature neural networks are single-hidden-layer feedforward neural networks in which only the output weights are trainable. This makes training particularly simple, but (a priori) reduces expressivity. Interestingly, this is not the case for Black-Scholes type PDEs, as we show here. We derive bounds for the prediction error of random neural networks for learning sufficiently non-degenerate Black-Scholes type models. A full error analysis is provided and it is shown that the derived bounds do not suffer from the curse of dimensionality. We also investigate an application of these results to basket options and validate the bounds numerically.

These results prove that neural networks are able to learn solutions to Black-Scholes type PDEs without the curse of dimensionality. In addition, this provides an example of a relevant learning problem in which random feature neural networks are provably efficient.

1 Introduction

A fundamental problem in science and engineering is to infer an unknown input-output relation from data. In recent years (artificial) neural networks have become an important tool to address such problems in complex, high-dimensional situations. Neural networks have shown a strikingly efficient computational performance in an enormous range of applications and impressive progress has also been made regarding the theoretical and mathematical foundations of neural network-based methods.

In many situations additional a priori information about the unknown input-output relation is available and the problem amounts to learning the solution of a partial differential equation (PDE) or, for instance in a financial context, an expectation of a stochastic process. Examples of applications of neural networks in this area can be found e.g. in Han et al. (2018), E et al. (2017), Sirignano and Spiliopoulos (2018), Huré et al. (2020), Buehler et al. (2019), Cuchiero et al. (2020). We refer to the surveys Ruf and Wang (2020), Beck et al. (2020), Germain et al. (2021) for an overview of the numerous recent applications of neural network-based learning in the context of PDEs, stochastic processes and finance. There has also been important progress regarding the theoretical and mathematical foundations of neural network-based methods in this area, see again the surveys mentioned above for an overview. Many of these recent mathematical results prove that deep neural networks are able to approximate solutions to various classes of PDEs without the curse of dimensionality, see, for instance, Elbrächter et al. (2018), Grohs et al. (2018), Hutzenthaler et al. (2020), Reisinger and Zhang (2019), Laakmann and Petersen (2021), Kutyniok et al. (2019), Gonon and Schwab (2021b). In some articles then a learning problem is considered and such approximation error bounds are combined with generalization error bounds in order to prove that the empirical risk-minimizing deep neural network is capable of overcoming the curse of dimensionality for learning solutions to certain PDEs, see e.g. Berner et al. (2020), Carmona and Laurière (2019). In practice, the neural network that minimizes the empirical risk needs to be calculated approximately, which is typically achieved using a variant of the stochastic gradient descent algorithm. This introduces a further error component, the optimization error, which has remained challenging to analyze mathematically for general neural networks. As a consequence, in the context of PDEs there have been no results in the literature so far which address all three error components and explain mathematically the success of neural networks at learning solutions to high-dimensional PDEs. In this work such an explanation is provided by proving that neural networks are capable of learning solutions to certain PDEs without the curse of dimensionality. This is achieved by considering neural networks in which only certain weights are trainable and the remaining parameters are generated randomly, as we will now describe in more detail.

We investigate the capabilities of random (feature) neural networks Huang et al. (2006), Rahimi and Recht (2008), Rahimi and Recht (2009) as a learning method in the context of certain Kolmogorov PDEs. Random neural networks are feedforward neural networks with a single hidden layer and the property that the parameters of the hidden layer are randomly initialized and then fixed. Hence, only the parameters of the output layer can be trained. The non-convex optimization problem that needs to be solved in order to train a standard neural network reduces to a convex optimization problem here. This simplifies both training in practice and theoretical analysis. On the other hand, allowing only parts of the parameters to be trained reduces the approximation capabilities and so, at least a priori, it is not clear if random neural networks still have any of the powerful approximation properties of general deep neural networks. In several other contexts these questions have been addressed and learning (or prediction/test) error bounds for random features or random neural networks have been proved (see for instance Rahimi and Recht (2008), Rudi and Rosasco (2017), Carratino et al. (2018), Mei and Montanari (2019), Mei et al. (2021) and the references therein), but not in the context of PDEs. This is precisely the subject of this article. We investigate these questions for the problem of learning an unknown function from a class of Kolmogorov PDEs, which include the Black-Scholes PDE as a special case. These partial (integro-)differential equations, which are also referred to as (non-local) PDEs, arise for instance in the context of option pricing in exponential Lévy models, see e.g. Cont and Tankov (2004), Eberlein and Kallsen (2019) and the references therein.

The main results of this article prove that, indeed, random neural networks are capable of learning non-degenerate Black-Scholes type PDEs without the curse of dimensionality. We provide a full error analysis, i.e., bounds on the approximation error, the generalization (or estimation) error and the optimization error. For each of these error components we obtain polynomial convergence rates which do not depend on the dimension of the underlying PDE and constants which grow at most polynomially in .

Thus, the article contributes to the literature in several aspects. Firstly, it provides for the first time a neural network-based algorithm for learning Kolmogorov PDEs for which a full error analysis (covering all three error components) is available and which does not suffer from the curse of dimensionality. The solution to the PDE can be learnt on a full hypercube from observational data even without knowing the parameters of the PDE. Secondly, it provides an example of a practically relevant learning problem in which random features are provably efficient. Finally, the techniques developed in the article may also be helpful for the theoretical analysis of more general neural network-based learning methods in future works.

Neural networks with randomly sampled weights already appear in Barron’s work Barron (1992), Barron (1993). The random sampling-based dimension-independent convergence rates obtained there were also extended to the larger class of “generalized Barron functions” in E et al. (2020), E et al. (2019), E and Wojtowytsch (2020), see also Berner et al. (2021, Section 4.2). For further related results and extensions we refer, for instance, to Barron and Klusowski (2018), Siegel and Xu (2020), Caragea et al. (2020) and the references therein. In all these results, the random sampling procedure is an intermediate step to establish the existence of neural network weights and obtain approximation bounds. This does not yield a constructive sampling procedure in general, since the random sampling distribution depends on the unknown target function. In contrast, in the random features approach Rahimi and Recht (2009), Rahimi and Recht (2008) considered here the distribution from which the random weights are sampled is chosen a priori and does not depend on the target function.

Numerical methods for partial (integro-)differential equations associated to univariate and certain multivariate exponential Lévy models were developed, e.g., in Cont and Voltchkova (2005), Farkas et al. (2007), Matache et al. (2004), Hilber et al. (2009). In a high-dimensional setting, when the parameters of the PDE are known and the solution of the PDE needs to be evaluated at a single point, then Monte Carlo methods are able to approximate the solution of the PDE without the curse of dimensionality. In contrast, here we consider a more challenging situation, which includes both the problem of evaluating the solution of the PDE on a full hypercube by a numerical method and the problem of learning the solution of the PDE from observed values. In the latter situation, in particular, the true parameters of the PDE are unknown.

The remainder of the article is structured as follows. Section 2 introduces random neural networks and provides a general approximation result. In Section 3 we build on this result to provide random neural network approximation bounds for a class of convolutional functions and then specialize to the case of partial (integro-)differential equations or (non-local) PDEs associated to exponential Lévy models. Section 4 introduces the learning problem, provides error bounds for different learning methods (regression, constrained regression and stochastic gradient descent) and develops an application to basket option pricing. These results are then applied in Section 5 to prove that random neural networks are capable of learning Black-Scholes type PDEs without the curse of dimensionality. The paper concludes with a numerical experiment to validate the obtained bounds.

1.1 Notation

In most parts of the article we will consider the dimension as fixed, but we will work out explicitly the dependence of all constants on . In Sections 3.2 and 5 we will consider a family of models indexed by and thus appears explicitly in the notation there.

Throughout, denotes the Euclidean norm on or (the appropriate space will always be clear from the context). For we denote the Euclidean ball by . All random variables are defined on a probability space and we write for the -norm on . For we use the notation .

2 Random neural networks: preliminary results

In this section we recall the definition of random (feature) neural networks and provide a general approximation result. Such networks will be used to learn an unknown target function.

A random neural network is a feedforward neural network with one hidden layer and randomly generated hidden weights. More specifically, let , let be i.i.d. random variables, let be i.i.d. -valued random vectors, assume that and are independent and for an -valued random vector consider the (random) function

| (2.1) |

where is a fixed activation function. Throughout the article we will consider random neural networks with the ReLU activation function given by for . The random variables and will be referred to as the (random) hidden weights of the neural network and as the vector of output weights.

To approximate an unknown function the (random) hidden weights are considered as fixed and only the output vector can be trained. Thus, the goal is to find such that the expected uniform approximation error is small.

Approximation properties of such random neural networks have been studied for instance in Huang et al. (2006), Rahimi and Recht (2008), Rudi and Rosasco (2017) and most recently in Gonon et al. (2020). Theorem 2.1 below is a novel approximation result for sufficiently regular functions, which will be crucial for the results in Section 3. The result and parts of the proof of Theorem 2.1 are similar to Gonon et al. (2020, Theorem 1); however in Gonon et al. (2020, Theorem 1) a more general Hilbert space setting and more general sampling distributions are considered. In contrast, Theorem 2.1 works under stronger hypotheses and employs Rademacher complexity-based techniques to obtain a uniform error bound instead of an -error bound.

More specifically, in what follows we make the following assumptions on the distribution of the hidden weights of the random neural network (2.1):

-

•

the distribution of has a strictly positive Lebesgue-density on and

-

•

the distribution of has a strictly positive Lebesgue-density on .

In this situation, the following random neural network approximation result holds.

Theorem 2.1.

Let , let and assume there exists such that

| (2.2) |

for all . Suppose that

| (2.3) |

for all and

| (2.4) |

is finite. Then there exists an -valued, -measurable random vector such that

| (2.5) |

Moreover, for .

Remark 2.2.

The proof of Theorem 2.1 is based on several ingredients: firstly, (2.2) is used to derive an integral representation for (see (2.10)). This representation is related to the Radon-wavelet integral representation (as used in Maiorov and Meir (2000)) and representations in Barron (1992), Barron (1993), Klusowski and Barron (2018). Secondly, the output weights are selected based on an “importance sampling procedure” (see (2.11)). This matches the distribution of the random weights (which is chosen a priori and does not depend on ) with the function in the integral representation for (see (2.10)). Thirdly, Rademacher complexity-based techniques (Bartlett and Mendelson (2003), Boucheron et al. (2013), Ledoux and Talagrand (2013)) are employed to bound the -error between the random neural network and the target function on the hypercube . The first two ingredients were also used in the proof of Gonon et al. (2020, Theorem 1).

Proof.

First, let us point out that for any -valued random vector the mapping is -measurable by Aliprantis and Border (2006, Lemma 4.51).

We now proceed in two steps. The first step consists in deriving an integral representation of based on (2.2), as in Gonon et al. (2020). From this integral representation we construct the output weights based on an importance sampling procedure. The second step then uses Rademacher complexities to estimate the expected -error.

Step 1: By considering separately the cases and , one obtains for any the identity

| (2.6) |

Inserting , multiplying by , integrating over , employing the representation (2.2) and using Fubini’s theorem (which can be applied due to (2.3)) hence yields for any that

| (2.7) | ||||

Changing variables in the integral and using that for and we have then shows for all that

| (2.8) |

From the fact that and are elements of one obtains and and hence we can represent

| (2.9) | ||||

Combining (2.8) and (2.9) we obtain for all

| (2.10) |

with

for . Define for the function

and choose the random vector as

| (2.11) |

The estimate

| (2.12) |

then proves the claimed bound on for .

Step 2: We now use the representation (2.10) to prove (2.5) for the choice of made in (2.11). To this end, first notice that for any we have by the choice of and by the integral representation (2.10)

Therefore, letting for and , we have

| (2.13) |

Let by i.i.d. Rademacher random variables which are independent of and . Symmetrization (see e.g. Boucheron et al. (2013)) and (2.13) then yields

| (2.14) |

For , we let . Then is bounded, is a contraction and hence independence and Ledoux and Talagrand (2013, Theorem 4.12) yield

| (2.15) | ||||

Now for each we use Jensen’s inequality and the fact that to estimate

| (2.16) | ||||

Inserting this in (2.15) and using first Jensen’s inequality and subsequently the fact that are identically distributed yields

| (2.17) | ||||

From the bound (2.12) we obtain

| (2.18) | ||||

Combining this with (2.14) and (2.17) yields

| (2.19) | ||||

which completes the proof. ∎

Remark 2.3.

With some additional work the weight distributions in Theorem 2.1 could also be allowed to have compact support as in Gonon et al. (2020, Theorem 1). However, in the results below (for instance in Theorem 3.1) such weight distributions would require much more restrictive assumptions on the unknown function and thus we do not pursue this direction here.

Corollary 2.4.

3 Random neural network approximation bounds

In this section we use random neural networks to approximate functions with a convolutional structure. In Section 3.1 we derive approximation error bounds with explicit dependence on the dimension . These results are then applied in Section 3.2 in the context of exponential Lévy models, which include the Black-Scholes model as a special case.

3.1 Bounds for convolutional functions

Consider a function given by for an -valued random vector and a function . Assume that the characteristic function of satisfies the following bound: there exists such that

| (3.1) |

Examples of functions of this type include expectations (respectively option prices) and associated solutions to PDEs in (exponential) Lévy models with non-degenerate Gaussian component, see Section 3.2 below.

We now approximate by a random neural network and analyze the approximation error. As above the randomly generated hidden weights are not trainable and the goal is to find such that the expected uniform approximation error is small. The output weight vector may be chosen depending on , i.e., it is a -measurable random variable.

Our goal is to obtain approximation error bounds in which the dependence on the dimension is fully explicit. To achieve this we need more specific assumptions on the distributions from which the hidden weights and are drawn. Recall that denotes the Lebesgue-density of and denotes the density of . We will assume below that is the density of a multivariate -distribution for some and that has at most polynomial decay, that is, there exists a polynomial such that

| (3.2) |

This hypothesis is satisfied, for instance, by Student’s -distribution.

These assumptions allow us to obtain explicit control of the normalizing constant of the weight distribution .

Theorem 3.1.

Let and let . Suppose and has density satisfying (3.2). Then there exist and an absolute constant such that for any of the form with and satisfying (3.1) the following random neural network approximation result holds: there exists an -valued, -measurable random vector such that

| (3.3) |

The constant only depends on and the constant depends on , but it does not depend on , or .

Moreover,

| (3.4) |

for , where the constant depends on , but it does not depend on , or .

Remark 3.2.

Remark 3.3.

Hypothesis (3.1) in Theorem 3.1 is employed in the proof in order to guarantee that the constant in the error bound does not grow exponentially in the dimension . In low-dimensional situations this behaviour may not be required and hence (3.1) could be replaced by the weaker hypothesis for some , or even by the assumption that for some and sufficiently large (depending on and ). In this situation the error bound (3.3) is still valid with a different constant and an additional factor which is potentially exponential in .

Proof.

Let be of the form with and satisfying (3.1). We verify that satisfies the hypotheses of Theorem 2.1 and derive a bound for the constant in (2.4) with the claimed properties.

For we denote by the Fourier transform of given for all by . By (3.1) and Sato (1999, Proposition 2.5(xii)) the random variable has a bounded Lebesgue-density . Thus, we can write . The convolution theorem (see for instance Amann and Escher (2009, Theorem X.9.16)) hence shows that . Combining this with and (3.1) we obtain that is integrable. The Fourier inversion theorem (see for instance Amann and Escher (2009, Theorem X.9.12)) therefore yields for all that

| (3.6) |

Hence, the representation (2.2) holds for all with , . Condition (2.3) is satisfied, since (3.1) implies

Denote by the degree of , then there exist such that for all . Then for all , where . Consequently, we may use (3.2) to estimate for any

and for analogously . Therefore, and we can now use the comparison on to estimate the constant in (2.4) as

with , , .

We now insert the density and use the estimate for to obtain

| (3.7) | ||||

with , . Denote by a random variable with a -distribution. Then the last line in (3.7) can be rewritten in terms of , yielding

| (3.8) | ||||

On the other hand, where is a -dimensional standard normal random vector. Hence, has a -distribution and thus

Combining this with (3.8) and the upper and lower bounds for the gamma function (see, e.g., Gonon et al. (2019, Lemma 2.4)) we obtain

| (3.9) | ||||

with . Now clearly

| (3.10) |

and

| (3.11) | ||||

because and hence and for all with . Combining this with (3.9) we have therefore proved that

| (3.12) | ||||

with .

Altogether, the hypotheses of Theorem 2.1 are satisfied and hence there exists an -valued, -measurable random vector such that the error bound (2.5) holds. Inserting (3.12) yields

| (3.13) | ||||

Hence, the -error estimate (3.3) follows with

where we recall that , , the constants and only depend on and , are given by (3.10) and (3.11), respectively.

To prove the upper bound on we insert the bound from Theorem 2.1, then (3.1) and (3.2) can be used to estimate similarly as before for

with , . In the last two steps we used that the maximum is attained for and we applied the lower bound for the gamma function as in (3.9). The hypothesis implies and therefore

by a similar reasoning as used to argue that in (3.11) is finite. Hence, the bound on follows with . This completes the proof. ∎

We now show that an analogous approximation result holds when the assumption is replaced by the assumptions that satisfies a Lipschitz-condition and admits certain moments.

Here we call increasing if for any with for all it holds that for all . Furthermore, we denote .

Proposition 3.4.

Proof.

Let and denote . Set . Then for we estimate

The truncated function is integrable and

Therefore, the result follows from Theorem 3.1 and the triangle inequality. ∎

Remark 3.5.

Let us now explain how Proposition 3.4 could be applied. In the case of exponential Lévy models we would choose for . Hence, if is -Lipschitz-continuous, then (3.14) is satisfied with for . Consequently, if we choose for some , then

with , and where the last step holds if the number of nodes satisfies the condition (which is, however, exponential in ). Furthermore,

is finite under exponential moment hypotheses on . Therefore, from (3.15) and Markov’s inequality we obtain

| (3.16) |

3.2 Bounds for non-degenerate Lévy models

In this section we apply Theorem 3.1 to prove that random neural networks are capable of overcoming the curse of dimensionality in the numerical approximation of solutions to partial (integro-)differential equations (also referred to as (non-local) PDEs) associated to exponential Lévy models with a non-degenerate Gaussian component. This includes the Black-Scholes PDE as a special case. We refer to Cont and Tankov (2004), Eberlein and Kallsen (2019) for background on exponential Lévy models and their applications in financial modelling and, e.g., to Sato (1999) for an extensive treatment of Lévy processes.

For each we consider a payoff function and a Lévy process with characteristic triplet satisfying for some . We define the shifted drift vector given by for . We now consider the partial (integro-)differential equation

| (3.17) |

for , where we write for . The (non-local) PDE (3.17) is the Kolmogorov PDE for the exponential Lévy model associated to . By Sato (1999, Theorem 25.17) the exponential Lévy process is a martingale if (and only if) . In this case, is the price at time of an option with payoff at maturity when price of the underlying at time is . Furthermore, if the jump-measure vanishes (), then (3.17) is the Black-Scholes PDE.

We now show that can be approximated by random neural networks without the curse of dimensionality. To achieve this, the weights of the random neural networks are generated as follows: let and for each let by i.i.d. -distributed -valued random vectors independent of the i.i.d. random variables which have a strictly positive Lebesgue-density of at most polynomial decay (see (3.2)). For we write and .

Theorem 3.6.

Let , . For each assume the payoff function satisfies and , the characteristic triplet of the Lévy process satisfies for all

| (3.18) |

assume and suppose is an at most polynomially growing solution to the PDE (3.17). Then there exist constants such that for any there exists an -valued, -measurable random vector such that the random neural network

| (3.19) |

satisfies the approximation bound

| (3.20) |

Proof.

Let , and for . Then Proposition 3.9 below shows that .

Furthermore, by the Lévy-Khintchine representation (see for instance Sato (1999, Theorem 8.1) or Applebaum (2009, Theorem 1.2.14 and Theorem 1.3.3)) we have with

| (3.21) |

In particular,

since the integrability property guarantees that and are indeed -integrable for any . This and (3.18) show that for all

| (3.22) |

Theorem 3.1 hence shows that there exist , and an -valued, -measurable random vector such that the random neural network satisfies

| (3.23) |

Thus, we obtain

with and . This proves (3.20) and the statement, since in Theorem 3.1 does not depend on or and hence the constants are the same for all . ∎

Remark 3.7.

Theorem 3.6 also holds if we directly assume instead of considering the PDE (3.17). For instance in the context of mathematical finance many quantities of interest (such as option prices or “greeks”) are defined in terms of such expectations. In particular, in this situation the hypothesis is not required (in Theorem 3.6 this hypothesis is implicit in the assumption ).

The integrability hypothesis is more restrictive, but currently it can not be avoided in the proof of Theorem 3.1. The hypothesis is satisfied e.g. for butterfly or binary options. More general payoffs can be incorporated by truncation (which is often possible without affecting the price significantly) or potentially by employing Fourier representations as in Carr and Madan (1999) instead of (3.6).

Remark 3.8.

The proof of Theorem 3.6 employs the “Feynman-Kac representation” from Proposition 3.9 below. Proposition 3.9 is essentially a consequence of the results from Barles et al. (1997). For the readers’ convenience we provide a proof of Proposition 3.9 and make explicit how it can be obtained from Barles et al. (1997). Related results and further references can be found, for instance, in Pham (1998), Cont and Voltchkova (2005), Cont and Voltchkova (2006, Proposition 3.3), Glau (2016).

Proposition 3.9.

Suppose is an at most polynomially growing solution to the PDE (3.17) and is bounded. Then for all it holds that .

Proof.

Let and . Firstly, the assumptions on imply that and a straightforward calculation shows that satisfies the (non-local) PDE

| (3.24) |

for . Set and for write

| (3.25) | ||||

Now if and is a global maximum point of , then and . Thus, (3.24) implies

| (3.26) | ||||

This and Barles et al. (1997, Lemma 3.3) show that is a viscosity subsolution of (3.24) in the sense of Barles et al. (1997). Similarly, one argues that is also a viscosity supersolution to (3.24). Barles et al. (1997, Theorem 3.5) hence shows that for all we have (see also the proof of Gonon and Schwab (2021b, Corollary 5.4)) where is the unique solution to ,

where is a Poisson random measure on with intensity , is an independent -dimensional standard Brownian motion and . Note that the assumption for some guarantees that the function in Barles et al. (1997, Theorem 3.5) can be chosen so that it satisfies the required boundedness hypothesis. Hence, by the Lévy-Itô-decomposition (see for instance Sato (1999, Theorem 19.2) or Applebaum (2009, Theorem 2.4.16)) we obtain that has the same distribution as . Thus, we have proved the representation and therefore for all , with ,

∎

4 Learning by random neural networks

In this section we use random neural networks to learn functions of the type considered in Section 3.1. In Section 4.1 we formulate the considered learning problem. In Sections 4.2, 4.3, 4.4 we then provide bounds on the prediction error that arises when is learnt by means of regression, constrained regression and stochastic gradient descent, respectively. In Sections 4.5 we will then apply these results to obtain prediction error bounds for random neural networks applied to learning option prices in certain non-degenerate models.

4.1 Formulation of the learning problem

Let and suppose that we are given i.i.d. -valued random variables (the data) which are independent of . Let be the target function (which we will assume to be of the form specified in Section 3.1) and suppose that

| (4.1) |

for -a.e. , that is, is the regression function. This encompasses two important situations:

-

•

Learning from noisy observations: We observe the unknown function (the solution to a PDE or market prices of options) at data points up to some additive noise. Thus, in this situation we suppose , , for i.i.d. random variables which are independent of and satisfy .

-

•

Solving PDEs by learning: Solving linear Kolmogorov PDEs with affine coefficients has been formulated as a learning problem in Berner et al. (2020). The setting considered here also covers this type of learning problem.

The target function is considered unknown and is to be learnt from the data using random neural networks. To do this, we recall that minimizes

| (4.2) |

among all measurable functions . Thus, to learn from the data one aims at finding a minimizer of

| (4.3) |

is the empirical version of (4.2). In the situation considered here we know from Section 3 that can be approximated well by random neural networks and so we learn by minimizing only over this class of functions, i.e. by minimizing over neural networks with random weights and trainable (see Section 2). This leads to the optimization problem

| (4.4) |

for a suitable set of -valued, -measurable random vectors. The measurability requirement incorporates the fact that are generated randomly and then fixed and hence the trainable weights may depend on .

Having solved (4.4), the learning algorithm then returns the (random) function

as our approximation for . To evaluate the learning performance of the random features regression algorithm we need to bound the (squared) learning error (or prediction error)

| (4.5) |

where has the same distribution as and is independent of .

4.2 Regression

Consider first the case . In this case computing (4.4) amounts to a simple least squares optimization. Hence can be calculated explicitly by solving

| (4.6) |

where is the -random matrix with entries and is the -dimensional random vector with for , .

Thus, there is no additional “optimization error” component in this case and we can directly bound the prediction error (4.5) by combining the approximation error estimates from Section 3 with a result from Györfi et al. (2002).

The trained neural network will be capped at a level by applying the truncation , .

Theorem 4.1.

Remark 4.2.

Theorem 4.1 bounds the square-root of the prediction error by . This matches, up to constants, the error bound obtained in the seminal work Barron (1994) for general “Barron functions”. In Barron (1994) all parameters of the network are trainable and the neural network estimator is defined via empirical risk minimization over a constrained parameter set. However, the optimization error, which arises when the neural network estimator is calculated based e.g. on the stochastic gradient descent algorithm, is not addressed in Barron (1994). In contrast, in our situation the class of considered functions is smaller, but the neural network estimator can be directly calculated by solving the linear system (4.6). Hence, the bound in Theorem 4.1 captures the full training error.

Proof.

Firstly, for fixed , we consider the function class , (in Györfi et al. (2002) the same symbol is used for these two sets) and let . Then is an -dimensional vector space and hence Györfi et al. (2002, Theorem 11.3) implies that

| (4.8) | ||||

where is the law of under and .

For any , the minimization problem for can be solved explicitly and we obtain , where is a solution to the linear system (4.6) with fixed to . A solution always exists (see for instance Stoer and Bulirsch (2002, Chapter 4.8.1)) and, e.g. by choosing the solution given in terms of the pseudo-inverse matrix as , it is possible to write for a measurable function and select in such a way that .

4.3 Constrained regression

In the next result we consider a constrained regression estimator, i.e., in (4.4) is calculated with a smaller set of potential weights . This leads to a different bound than in Theorem 4.1, but for instance for the same rate is achieved.

Set . Computing (4.4) now corresponds to a constrained regression problem

| (4.10) |

The solution to (4.10) is given explicitly as follows: coincides with the solution to the unconstrained problem (4.6) with minimal norm in case satisfies . Otherwise is given explicitly as

| (4.11) |

with a non-negative -measurable random variable111This means that once the data and the random weights have been sampled/observed (i.e. conditionally on these) is just a constant. such that . The two cases can be summarized by setting in the first case and interpreting the inverse in (4.11) as a pseudo-inverse, then is given by (4.11) in both cases.

We now provide a bound on the prediction error for random neural networks with parameters learned according to (4.10).

Theorem 4.3.

Remark 4.4.

Theorem 4.3 shows that the prediction error is of order . Thus, the error bound decays more quickly than the bound that was obtained in the seminal work Rahimi and Recht (2009), where high-probability bounds were obtained for random neural networks trained by constrained regression in a classification setting (). The reason for this faster rate is that we use the mean-square loss here. This allows to write due to (4.1). For -Lipschitz loss functions the bound can be deduced (see Rahimi and Recht (2009, Lemma 2)), which leads to an approximation error of order instead of .

Thus, we are concerned here with a slightly different setting, but our proof of the “estimation error” (or generalization error) component is based on similar arguments as the proof in Rahimi and Recht (2009).

Proof.

Firstly, (4.1) and independence imply

| (4.13) | ||||

and analogously for any . Thus, we calculate

| (4.14) | ||||

where we used (4.10) and in the last step.

Consider the first term in the right hand side of (4.14). Theorem 3.1 (c.f. also Remark 3.2) guarantees that there exists an -valued, -measurable random vector such that

| (4.15) |

where we used that . Furthermore, (3.4) shows that -a.s. the weight vector satisfies . Hence, it follows that and so the decomposition (4.14) can be applied with .

For the second term in the right hand side of (4.14) we let denote the solution to (4.10) for fixed to . The random variable can be written as for a measurable function (in fact, for the strictly decreasing function , where are with fixed to ). Then from the formula (4.11) it is clear that for a measurable function and . Furthermore, we write for the measurable function with (which exists, since is -measurable) and . Then by independence

| (4.16) | ||||

We now fix , consider for , the random variables and let denote i.i.d. Rademacher random variables independent of all other random variables. Employing symmetrization (see for instance (Boucheron et al., 2013, Lemma 11.4)) we obtain

| (4.17) |

In the next step we denote by the vector with components , and rewrite . Then we use the triangle inequality, Jensen’s inequality and independence to estimate

| (4.18) | ||||

where is the Frobenius norm on . Denoting by the Frobenius (matrix) inner product on and using independence and we obtain

Employing an analogous argument for the second term in the right hand side of (4.18) (now with the standard inner product on ) yields

| (4.19) | ||||

Using and inserting the bound (4.19) in (4.17) we obtain

| (4.20) | ||||

Employing the bound

| (4.21) |

we estimate using the Minkowski integral inequality and the triangle inequality

The second term in the right hand side of (4.20) can be bounded similarly with (4.21). Inserting this and (4.20) in (4.16) yields

| (4.22) | ||||

Recall that has a multivariate -distribution , hence where and are independent. Thus, . Using that and we may thus deduce from (4.22) that

| (4.23) | ||||

with not depending on , or . Combining (4.23) with (4.14) and (4.15) we obtain

| (4.24) |

∎

4.4 Stochastic gradient descent

For the most common choices of the solution to the optimization problem (4.4) can be obtained by solving the system of linear equations (4.6) or (4.11), respectively. There may nevertheless be situations in which one is interested in solving (4.4) using a stochastic gradient descent method (e.g. when comparing the performance of different learning methods in an experiment). Therefore, we will briefly discuss optimization of (4.10) by stochastic gradient descent here and combine our error bound in Theorem 4.3 with the stochastic gradient descent optimization error bound from Shamir and Zhang (2013).

To this end, let denote the set within which we look for an optimizer, let be the orthogonal projection onto , for write for the -valued random vector with components , , let denote the number of stochastic gradient descent iterations, let denote the batch size and let denote i.i.d. random variables each having a uniform distribution on and independent of . Then, starting with , we iteratively compute

| (4.25) |

where for . The parameter vector is then used for the random neural network, i.e., is the learned function approximating . The next proposition provides a bound on the prediction error.

Proposition 4.5.

Let , and . Suppose and has density satisfying (3.2). Suppose is of the form with and satisfying (3.1). Assume that , -a.s. and . Let for and with , as in Theorem 3.1 and , not depending on or .

Then there exist such that

| (4.26) | ||||

The constant only depends on and the constants depend on , , but they do not depend on , , or .

Remark 4.6.

The first two terms in the error bound in (4.26) are as in the bound (4.12) in Theorem 4.3, whereas the last term in (4.26) is due to the stochastic gradient descent optimization. The rate of convergence to of this last error term as a function of could be further improved, e.g., by using a more refined optimization scheme (based on averaging) than (4.25), see for instance Shamir and Zhang (2013). However, for our purposes the bound in Proposition 4.5 suffices as this bound already proves that the overall error does not suffer from the curse of dimensionality.

Proof.

Let be as in Theorem 3.1, let be the -valued, -measurable random vector satisfying (3.3) (see Theorem 3.1) and let be as in Theorem 4.3.

By independence and (4.1) we obtain (as in (4.13)-(4.14) in the proof of Theorem 4.3)

| (4.27) | ||||

where we used (4.10) and (as established in the proof of Theorem 4.3) in the last step. The first expectation in the right hand side of (4.27) has been bounded in (4.15) in the proof of Theorem 4.3. For the second expectation we may proceed analogously as in (4.16): we use the same notation as in (4.16) and, in addition, write for the output of the stochastic gradient descent algorithm with fixed to . Then independence yields

| (4.28) | ||||

Now we can compare (4.27) and (4.28) to (4.14) and (4.16) in the proof of Theorem 4.3. We see that the decomposition (4.27) yields the same error terms as in Theorem 4.3 plus the additional term .

Therefore, Theorem 4.3 shows that

| (4.29) | ||||

We now analyze the last term. Write for the output of the stochastic gradient descent algorithm and for the solution to (4.10) when . From the updating scheme it is clear that there exists a measurable function such that . Furthermore (as argued in the proof of Theorem 4.3), for a measurable function and . Thus, we may use independence to write

| (4.30) |

where for . Consider as fixed now and write for the vector with , . Let , . Then , and hence is a (global) minimizer of in . Write and recall

| (4.31) |

with . Independence implies . Furthermore, is convex and the Minkowski integral inequality and independence yield

| (4.32) | ||||

where in the last two inequalities we used the estimate . Shamir and Zhang (2013, Theorem 2) hence implies that

Inserting this in (4.30) and using independence yields

| (4.33) | ||||

Employing Minkowski’s integral inequality we estimate

| (4.34) | ||||

Recall that , where and are independent. Therefore and one obtains analogously to (4.34) the estimate . Inserting this into (4.34) and (4.33) and estimating yields

| (4.35) | ||||

with and where we used , . Combining this with (4.29) yields (4.26), as claimed. ∎

4.5 Application to basket option pricing

As a first application of the results derived in Sections 4.2–4.4 we consider the problem of learning prices of basket put options in certain “non-degenerate” models.

Suppose that is the market price of a put option with strike written on a basket of assets. Assume that, up to some additive noise, these market prices are “generated” from an unknown, non-degenerate stochastic model. This means that we assume

where are i.i.d. random variables, is a -valued random vector and are non-negative weights. Assume that , and are independent of . We think of as the value at time of a price process (for which is a martingale measure).

The goal is to learn the pricing function from the observed market prices .

This fits into the framework introduced above (see Section 4.1) if we let and consider as the observed realizations of the i.i.d. random variables so that also is the realization of . We assume that is distributed uniformly on and are independent of . Then the option pricing function is indeed the regression function (4.1) and we obtain the following corollary. Recall that has the same distribution as and is independent of .

Corollary 4.7.

Let , , and be constants which do not depend on or . Suppose and has density satisfying (3.2). Assume that the -valued random vector satisfies for all . Then there exists such that the prediction error bound

| (4.36) |

holds and there exist such that for any the prediction error bounds

| (4.37) | ||||

| (4.38) |

hold. The constants do not depend on , or .

Remark 4.8.

The proof of Corollary 4.7 shows that does not depend on . Hence, by choosing it can always be guaranteed that is not empty.

Remark 4.9.

The hypothesis is inherited from Theorem 3.1. In Theorem 3.1 this hypothesis guarantees that the constants do not grow exponentially in the dimension . In the situation here and so this hypothesis could be relaxed considerably: it could be replaced by the assumption for some , or even by the assumption that for some and sufficiently large (depending on and ).

Proof.

Firstly, by assumption we have , -a.s. and satisfies for that

with and . Hence, -a.s. with for . Furthermore, , satisfies (3.1), and for all . Thus, the hypotheses of Theorem 4.1 with are satisfied and so, using -a.s., we obtain that there exist and such that the prediction error bound (4.7) holds. Hence (4.36) follows with .

Next we prove (4.37). To this end, notice and let be as in Theorem 3.1. Then Theorem 4.3 proves that for any satisfying there exists a constant such that the prediction error bound (4.12) holds. The proof actually shows that the same constant can be chosen for all in the specified range. Thus, (4.37) follows with and .

Furthermore, Proposition 4.5 proves that there exists such that (4.26) holds. Setting we obtain (4.38).

In these results we proved that the constants depend on , , , , but they do not depend on , or , hence it follows that do not depend on , or .

∎

5 Learning Black-Scholes type PDEs

In this section we apply the results from Section 4 to prove that random neural networks are capable of learning Black-Scholes type partial (integro-)differential equations (also referred to as (non-local) PDEs) without the curse of dimensionality. More specifically, we consider the problem of learning solutions to Kolmogorov PDEs associated to exponential Lévy-processes, which includes the Black-Scholes PDE as a special case. The learning methods used to tackle this problem are random neural networks trained by (constrained) regression or stochastic gradient descent. By combining the results from Theorems 3.6, 4.1, 4.3 and from Proposition 4.5 we obtain bounds on the prediction error. The dependence on the dimension in these bounds is explicit and at most polynomial, whereas the bounds decay at polynomial rate in the number of samples and the network size (and the number of stochastic gradient descent iterations ). Hence, the number of samples, hidden nodes of the network and gradient steps required to achieve a prescribed prediction accuracy grows at most polynomially in and . This means that random neural networks are capable of learning solutions to such Kolmogorov PDEs without the curse of dimensionality.

For the reader’s convenience we introduce in Section 5.1 in detail again all the objects relevant to the discussion. Section 5.2 then contains the prediction error bounds for Black-Scholes type PDEs. We conclude in Section 5.3 with a numerical experiment.

5.1 Formulation of the learning problem for PDEs

We again put ourselves in the situation studied in Section 3.2 and consider for each the partial (integro-)differential equation

| (5.1) |

for , where is a “payoff” function and is the characteristic triplet of a Lévy process , we write , , for the shifted drift vector and we assume for some . Furthermore, we recall the notation for .

The (non-local) PDE (5.1) is the Kolmogorov PDE for the exponential Lévy model associated to , see Section 3.2 for further interpretation and a discussion on the relation to option pricing and the assumption on . If , then (5.1) is the Black-Scholes PDE.

Let and suppose we are given i.i.d. -valued random variables , with the property that

| (5.2) |

for -a.e. , that is, is the regression function. We are interested in learning on the set . This encompasses two particularly relevant situations.

Example 5.1.

Suppose that the solution of the PDE can be observed at points . The observations are not perfect, but perturbed by some additive noise. The goal is to learn the solution of the PDE on the entire set from these noisy observations. This situation is captured in our setting with for , where are i.i.d. random variables independent of .

Example 5.2.

A different situation of interest arises when neural networks are employed as a solution method for the PDE (5.1) in the way proposed in Berner et al. (2020) for a related setting. Let be i.i.d. random variables uniformly distributed on and independent of and let for . Then one may show using the Feynman-Kac formula (see Proposition 3.9) that

for -a.e. and hence is indeed the regression function (5.2). Thus, in this situation we have formulated the problem of solving the PDE (5.1) on as a statistical learning problem with data points , .

In order to learn the unknown function from the data we employ a random neural network. Recall from Section 2 that a random neural network is a single-hidden-layer feedforward neural network in which the hidden weights are randomly generated and then considered fixed and only the output-layer weight vector can be trained. The weights of the random neural networks are generated as follows: let , for each let be i.i.d. -valued random vectors and let be i.i.d. random variables. Assume that is -distributed and has a strictly positive Lebesgue-density of at most polynomial decay (see (3.2)). For each we assume that , and are independent. For we write and . If hidden nodes are used, the random neural network employed for learning is then given by

| (5.3) |

where is an -valued, -measurable random vector which needs to be chosen. The (squared) learning error (or prediction error) is given by

| (5.4) |

where has the same distribution as and is independent of and .

Learning by then amounts to selecting an -valued (random) vector that minimizes the prediction error. may be chosen depending on the random weights and the data . We consider three choices:

-

•

is chosen as , where

(5.5) for . Note that can be calculated explicitly by solving a system of linear equations (see Section 4.2).

-

•

is chosen as , where

(5.6) for . Recall that can be calculated explicitly by solving a system of linear equations (see Section 4.3).

-

•

is chosen as , where is computed using the stochastic gradient descent algorithm as introduced in Section 4.4.

Remark 5.3.

As pointed out above, training of random neural networks can be performed by solving a system of linear equations (see (4.6) in Section 4.2 and (4.11) in Section 4.3). There may nevertheless be situations in which one is interested in training a random neural network using a stochastic gradient descent method (e.g. a performance comparison in an experiment). This is the reason why we also analyze optimization by stochastic gradient descent here.

5.2 Learning error bounds

With these preparations (see Section 5.1) we now use the results from Sections 3 and 4 to prove that can be learnt using random neural networks without the curse of dimensionality.

Corollary 5.4.

Let , , . Assume that for each the payoff function satisfies and , the characteristic triplet of the Lévy process satisfies for all

| (5.7) |

assume that , -a.s. and suppose is an at most polynomially growing solution to the PDE (5.1).

-

(i)

Assume for all that and for all . Then there exist constants such that for any the prediction error of random neural network regression satisfies

(5.8) -

(ii)

Assume for all that . Then there exist such that for any , there exist such that for any the random neural network trained by constrained regression with parameter satisfies

(5.9) -

(iii)

Consider the same situation as in (ii). Then, in addition, there exist constants such that for any the random neural network trained by stochastic gradient descent for steps with learning rate for and with as in (ii) satisfies

(5.10)

Remark 5.5.

Each of these statements can be translated directly into a statement on the number of samples and hidden nodes required to guarantee a prescribed learning error of precision at most . For instance, in the case of regression (corresponding to the bound (5.8)) we see that there exist constants such that for all , at most weights and samples suffice to guarantee

| (5.11) |

This follows from (5.8) by choosing , and where is a constant such that for all .

Proof.

For fixed let and for . Then Proposition 3.9 shows that and, as argued in the proof of Theorem 3.6, the characteristic function of satisfies the bound (3.22).

Proof of (i): Theorem 4.1 hence implies that there exist and such that

| (5.12) | ||||

with and . This proves (i), since and in Theorem 4.1 do not depend on , or .

Proof of (ii): Let and be as in Theorem 3.1, choose , and let , . Then satisfies and hence Theorem 4.3 shows that there exists such that

| (5.13) |

From the proof of Theorem 4.3 (with here) the constant is given by

and hence with . Thus, (5.13) yields

| (5.14) |

with and . As shown in the above results (and visible from the explicit expressions available for these constants) neither nor the constants depend on , or . Hence, the constants do not depend on or . This proves (ii).

Proof of (iii): Let , , , be as in the proof of (ii) and let , . Applying Proposition 4.5 with and using the estimate provided in the proof of (ii) (see (5.13) and (5.14)) for the first two terms in (4.26) we obtain that there exists such that

| (5.15) |

The constant was given explicitly in the proof and we deduce that with . Combining this with (5.15) proves (5.10) with , . By the same reasoning as above do not depend on or . This proves (iii). ∎

5.3 Numerical example

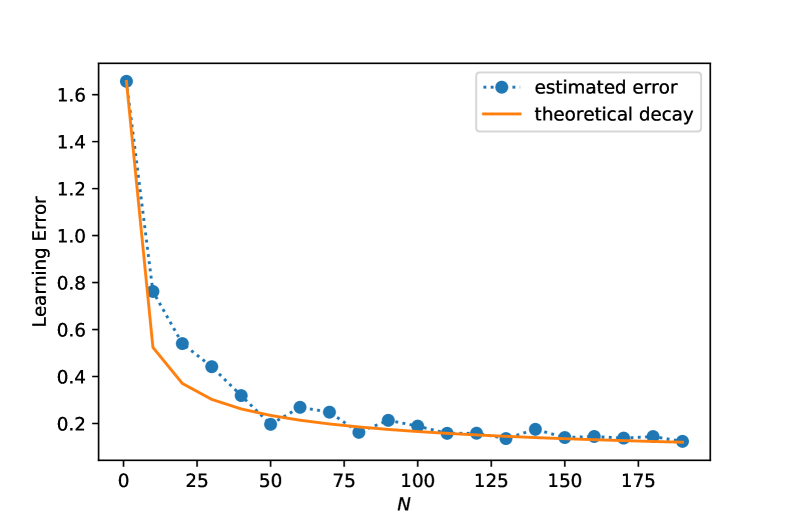

In this section we consider a numerical example in which the solution to (5.1) is learnt from noisy observations. We fix , and generate training data points for our experiment. The goal is then to learn based only on these data points, i.e. without using any knowledge about the underlying PDE or its parameters. This is achieved by employing neural networks with randomly generated hidden weights, as explained in detail in Section 5.1.

For the unknown PDE we choose the pricing PDE for a max-call option in a -dimensional Black-Scholes model with equal correlations among the assets. Thus, we fix , choose as initial value for the PDE and let be given for by for and . Furthermore, , and the parameter values are chosen as , , . The strike is chosen as (which corresponds to expressing prices in units of the “actual” strike). From the solution with on one can also directly obtain the solution for other values of (e.g. ) on the set by using . For our experiment we now select and generate the -th data point as follows: we randomly uniformly sample on and then use a Monte Carlo simulation with sample paths to calculate an approximate value of . is then defined as this approximate value and corresponds to a noisy observation of at . By using this procedure for we generate data points (the training data).

The goal is now to learn the solution to (5.1) based only on these (noisy) observations. To achieve this we use random neural networks as described in Section 5.1. We consider different choices for the number of hidden nodes . For the weight distributions we choose and let have a Student’s -distribution with degrees of freedom (i.e. and is the density of a -distribution with degrees of freedom). Unconstrained regression is employed to fit the output weights (see (5.5)), resulting in an output weight vector and a random neural network approximation (see (5.3)) to .

Then we generate test samples according to the same procedure that we used for the training data above. Based on these training data points we calculate the squared error . The error is an estimate of the prediction error (see (5.4), (5.8) and recall that the Monte Carlo price is an unbiased estimate of ). Figure 1 displays for different choices of the number of hidden nodes, namely, . The figure also displays the function , where is chosen as .

The theoretical results from Corollary 5.4 show that, for large, the theoretical prediction error decays at least as when increases. The numerical results here reproduce this behaviour for the estimated prediction error . This can be seen from Figure 1, where the estimated error matches closely the function .

This numerical experiment also indicates that the integrability and smoothness assumptions in Corollary 5.4 can potentially be relaxed. More specifically, the payoff considered in the example here does not satisfy the hypothesis and for the chosen parameters the matrix does not satisfy (5.7), since the smallest eigenvalue of is smaller than and hence any eigenvector of corresponding to this eigenvalue satisfies for any . Nevertheless, the numerical results suggest that Corollary 5.4(i) is still valid in this situation. While Theorem 2.1 may be used to establish the -decay in also without the hypotheses and (5.7), these hypotheses were needed in the proof of Theorem 3.1 (and propagate to Corollary 5.4) in order to guarantee that the constant in the error bound does not grow exponentially in . The numerical experiment and the choice indicates non-exponential constants also here and hence it may be possible to relax these assumptions by taking a different approach than the one that was used in the proof of Theorem 3.1.

References

- Aliprantis and Border (2006) C. D. Aliprantis and K. C. Border. Infinite dimensional analysis. Springer, Berlin, 2006. ISBN 978-3-540-32696-0; 3-540-32696-0.

- Amann and Escher (2009) H. Amann and J. Escher. Analysis. III. Birkhäuser, Basel, 2009. ISBN 978-3-7643-7479-2; 3-7643-7479-2. doi: 10.1007/978-3-7643-7480-8. URL https://doi.org/10.1007/978-3-7643-7480-8.

- Applebaum (2009) D. Applebaum. Lévy processes and stochastic calculus, volume 116 of Cambridge Studies in Advanced Mathematics. Cambridge University Press, Cambridge, second edition, 2009. ISBN 978-0-521-73865-1. doi: 10.1017/CBO9780511809781. URL https://doi.org/10.1017/CBO9780511809781.

- Barles et al. (1997) G. Barles, R. Buckdahn, and E. Pardoux. Backward stochastic differential equations and integral-partial differential equations. Stochastics Stochastics Rep., 60(1-2):57–83, 1997. ISSN 1045-1129. doi: 10.1080/17442509708834099. URL https://doi.org/10.1080/17442509708834099.

- Barron (1992) A. R. Barron. Neural net approximation. In Yale Workshop on Adaptive and Learning Systems, volume 1, pages 69–72, 1992.

- Barron (1993) A. R. Barron. Universal approximation bounds for superpositions of a sigmoidal function. IEEE Trans. Inform. Theory, 39(3):930–945, 1993. ISSN 0018-9448. doi: 10.1109/18.256500. URL https://doi.org/10.1109/18.256500.

- Barron (1994) A. R. Barron. Approximation and estimation bounds for artificial neural networks. Machine Learning, 14:115–133, 1994.

- Barron and Klusowski (2018) A. R. Barron and J. M. Klusowski. Approximation and estimation for high-dimensional deep learning networks. Preprint, arXiv 1809.03090, 2018.

- Bartlett and Mendelson (2003) P. L. Bartlett and S. Mendelson. Rademacher and Gaussian complexities: Risk bounds and structural results. Journal of Machine Learning Research, 3(3):463–482, 2003.

- Beck et al. (2020) C. Beck, M. Hutzenthaler, A. Jentzen, and B. Kuckuck. An overview on deep learning-based approximation methods for partial differential equations. Preprint, arXiv 2012.12348, 2020.

- Berner et al. (2020) J. Berner, P. Grohs, and A. Jentzen. Analysis of the generalization error: empirical risk minimization over deep artificial neural networks overcomes the curse of dimensionality in the numerical approximation of Black-Scholes partial differential equations. SIAM J. Math. Data Sci., 2(3):631–657, 2020. doi: 10.1137/19M125649X. URL https://doi.org/10.1137/19M125649X.

- Berner et al. (2021) J. Berner, P. Grohs, G. Kutyniok, and P. Petersen. The modern mathematics of deep learning. Preprint, arXiv 2105.04026, 2021.

- Boucheron et al. (2013) S. Boucheron, G. Lugosi, and P. Massart. Concentration Inequalities: A Nonasymptotic Theory of Independence. OUP Oxford, 2013.

- Buehler et al. (2019) H. Buehler, L. Gonon, J. Teichmann, and B. Wood. Deep hedging. Quant. Finance, 19(8):1271–1291, 2019. ISSN 1469-7688. doi: 10.1080/14697688.2019.1571683. URL https://doi.org/10.1080/14697688.2019.1571683.

- Caragea et al. (2020) A. Caragea, P. Petersen, and F. Voigtlaender. Neural network approximation and estimation of classifiers with classification boundary in a barron class. Preprint, arXiv 2011.09363, 2020.

- Carmona and Laurière (2019) R. Carmona and M. Laurière. Convergence analysis of machine learning algorithms for the numerical solution of mean field control and games: I - the ergodic case. To appear in SIAM Journal on Numerical Analysis (SINUM), July 2019. URL https://arxiv.org/abs/1907.05980.

- Carr and Madan (1999) P. Carr and D. Madan. Option valuation using the fast fourier transform. Journal of Computational Finance, 2:61–73, 1999.

- Carratino et al. (2018) L. Carratino, A. Rudi, and L. Rosasco. Learning with sgd and random features. In Advances in Neural Information Processing Systems, volume 31, 2018. URL https://proceedings.neurips.cc/paper/2018/file/741a0099c9ac04c7bfc822caf7c7459f-Paper.pdf.

- Cont and Tankov (2004) R. Cont and P. Tankov. Financial Modelling with Jump Processes. Chapman & Hall/CRC, 2004.

- Cont and Voltchkova (2005) R. Cont and E. Voltchkova. Integro-differential equations for option prices in exponential lévy models. Finance and Stochastics, 9:299–325, 2005.

- Cont and Voltchkova (2006) R. Cont and E. Voltchkova. A Finite Difference Scheme for Option Pricing in Jump Diffusion and Exponential Lévy Models. SIAM Journal on Numerical Analysis, 43(4):1596–1626, 2006.

- Cuchiero et al. (2020) C. Cuchiero, W. Khosrawi, and J. Teichmann. A generative adversarial network approach to calibration of local stochastic volatility models. Risks, 8(4):101, 2020.

- E and Wojtowytsch (2020) W. E and S. Wojtowytsch. On the banach spaces associated with multi-layer relu networks: Function representation, approximation theory and gradient descent dynamics. Preprint, arXiv 2007.15623, 2020.

- E et al. (2017) W. E, J. Han, and A. Jentzen. Deep learning-based numerical methods for high-dimensional parabolic partial differential equations and backward stochastic differential equations. Communications in Mathematics and Statistics, 5(4):349–380, 2017.

- E et al. (2019) W. E, C. Ma, and L. Wu. A priori estimates of the population risk for two-layer neural networks. Commun. Math. Sci., 17(5):1407–1425, 2019.

- E et al. (2020) W. E, C. Ma, S. Wojtowytsch, and L. Wu. Towards a mathematical understanding of neural network-based machine learning: what we know and what we don’t. Preprint, arXiv 2009.10713, 2020.

- Eberlein and Kallsen (2019) E. Eberlein and J. Kallsen. Mathematical finance. Springer Finance. Springer, Cham, 2019.

- Elbrächter et al. (2018) D. Elbrächter, P. Grohs, A. Jentzen, and C. Schwab. DNN Expression Rate Analysis of High-dimensional PDEs: Application to Option Pricing. Technical Report 2018-33, Seminar for Applied Mathematics, ETH Zürich, Switzerland, 2018. URL https://www.sam.math.ethz.ch/sam_reports/reports_final/reports2018/2018-33.pdf. (to appear in Constr. Approx. (2021)).

- Farkas et al. (2007) W. Farkas, N. Reich, and C. Schwab. Anisotropic stable Lévy copula processes—analytical and numerical aspects. Math. Models Methods Appl. Sci., 17(9):1405–1443, 2007.

- Germain et al. (2021) M. Germain, H. Pham, and X. Warin. Neural networks-based algorithms for stochastic control and pdes in finance. Preprint, arXiv 2101.08068, 2021.

- Glau (2016) K. Glau. Classification of Lévy processes with parabolic Kolmogorov backward equations. Theory Probab. Appl., 60(3):383–406, 2016.

- Gonon and Schwab (2021a) L. Gonon and C. Schwab. Deep ReLU network expression rates for option prices in high-dimensional, exponential Lévy models. Preprint, arXiv 2101.11897, to appear in Finance Stoch., 2021a.

- Gonon and Schwab (2021b) L. Gonon and C. Schwab. Deep relu neural network approximation for stochastic differential equations with jumps. Preprint, arXiv 2102.11707, 2021b.

- Gonon et al. (2019) L. Gonon, P. Grohs, A. Jentzen, D. Kofler, and D. Šiška. Uniform error estimates for artificial neural network approximations for heat equations. Technical Report 2019-61, Seminar for Applied Mathematics, ETH Zürich, Switzerland, 2019. URL https://www.sam.math.ethz.ch/sam_reports/reports_final/reports2019/2019-61.pdf. to appear in IMA J. Num. Anal.

- Gonon et al. (2020) L. Gonon, L. Grigoryeva, and J.-P. Ortega. Approximation bounds for random neural networks and reservoir systems. Preprint, arXiv 2002.05933, 2020.

- Grohs et al. (2018) P. Grohs, F. Hornung, A. Jentzen, and P. von Wurstemberger. A proof that artificial neural networks overcome the curse of dimensionality in the numerical approximation of Black-Scholes partial differential equations. To appear in Memoirs of the American Mathematical Society; arXiv:1809.02362, page 124 pages, 2018.

- Györfi et al. (2002) L. Györfi, M. Kohler, A. Krzyżak, and H. Walk. A distribution-free theory of nonparametric regression. Springer Series in Statistics. Springer-Verlag, New York, 2002. ISBN 0-387-95441-4. doi: 10.1007/b97848. URL https://doi.org/10.1007/b97848.

- Han et al. (2018) J. Han, A. Jentzen, and W. E. Solving high-dimensional partial differential equations using deep learning. Proceedings of the National Academy of Sciences, 115(34):8505–8510, 2018.

- Hilber et al. (2009) N. Hilber, N. Reich, C. Schwab, and C. Winter. Numerical methods for Lévy processes. Finance and Stochastics, 13:471–500, 2009.

- Huang et al. (2006) G.-B. Huang, L. Chen, and C.-K. Siew. Universal approximation using incremental constructive feedforward networks with random hidden nodes. Trans. Neur. Netw., 17(4):879–892, July 2006. ISSN 1045-9227. doi: 10.1109/TNN.2006.875977. URL https://doi.org/10.1109/TNN.2006.875977.

- Huré et al. (2020) C. Huré, H. Pham, and X. Warin. Deep backward schemes for high-dimensional nonlinear PDEs. Math. Comp., 89(324):1547–1579, 2020.

- Hutzenthaler et al. (2020) M. Hutzenthaler, A. Jentzen, T. Kruse, T. A. Nguyen, and P. von Wurstemberger. Overcoming the curse of dimensionality in the numerical approximation of semilinear parabolic partial differential equations. Proc. A., 476(2244):630–654, 2020.

- Klusowski and Barron (2018) J. M. Klusowski and A. R. Barron. Approximation by combinations of ReLU and squared ReLU ridge functions with and controls. IEEE Trans. Inform. Theory, 64(12):7649–7656, 2018. ISSN 0018-9448. doi: 10.1109/tit.2018.2874447. URL https://doi.org/10.1109/tit.2018.2874447.

- Kutyniok et al. (2019) G. Kutyniok, P. Petersen, M. Raslan, and R. Schneider. A theoretical analysis of deep neural networks and parametric PDEs. arXiv:1904.00377, page 43 pages, 2019.

- Laakmann and Petersen (2021) F. Laakmann and P. Petersen. Efficient approximation of solutions of parametric linear transport equations by ReLU DNNs. Adv. Comput. Math., 47(1):Paper No. 11, 2021. ISSN 1019-7168. doi: 10.1007/s10444-020-09834-7. URL https://doi.org/10.1007/s10444-020-09834-7.

- Ledoux and Talagrand (2013) M. Ledoux and M. Talagrand. Probability in Banach Spaces. Springer Berlin Heidelberg, 2013.

- Maiorov and Meir (2000) V. E. Maiorov and R. Meir. On the near optimality of the stochastic approximation of smooth functions by neural networks. Adv. Comput. Math., 13(1):79–103, 2000. ISSN 1019-7168. doi: 10.1023/A:1018993908478. URL https://doi.org/10.1023/A:1018993908478.

- Matache et al. (2004) A.-M. Matache, T. von Petersdorff, and C. Schwab. Fast deterministic pricing of options on Lévy driven assets. M2AN Math. Mod. and Num. Anal., 38:37–71, 2004. doi: http://dx.doi.org/10.1051/m2an:2004003.

- Mei and Montanari (2019) S. Mei and A. Montanari. The generalization error of random features regression: Precise asymptotics and double descent curve. Preprint, arXiv 1908.05355, 2019.

- Mei et al. (2021) S. Mei, T. Misiakiewicz, and A. Montanari. Generalization error of random features and kernel methods: hypercontractivity and kernel matrix concentration. Preprint, arXiv 2101.10588, 2021.

- Pham (1998) H. Pham. Optimal stopping of controlled jump diffusion processes: a viscosity solution approach. J. Math. Systems Estim. Control, 8(1):27 pp. 1998. ISSN 1052-0600.

- Rahimi and Recht (2008) A. Rahimi and B. Recht. Random features for large-scale kernel machines. In Advances in Neural Information Processing Systems, pages 1177–1184, 2008.

- Rahimi and Recht (2009) A. Rahimi and B. Recht. Weighted sums of random kitchen sinks: Replacing minimization with randomization in learning. In D. Koller, D. Schuurmans, Y. Bengio, and L. Bottou, editors, Advances in Neural Information Processing Systems, volume 21, pages 1313–1320. Curran Associates, Inc., 2009. URL https://proceedings.neurips.cc/paper/2008/file/0efe32849d230d7f53049ddc4a4b0c60-Paper.pdf.

- Reisinger and Zhang (2019) C. Reisinger and Y. Zhang. Rectified deep neural networks overcome the curse of dimensionality for nonsmooth value functions in zero-sum games of nonlinear stiff systems. arXiv:1903.06652, page 34 pages, 2019.

- Rudi and Rosasco (2017) A. Rudi and L. Rosasco. Generalization properties of learning with random features. In Advances in Neural Information Processing Systems, pages 3215–3225, 2017.

- Ruf and Wang (2020) J. Ruf and W. Wang. Neural networks for option pricing and hedging: a literature review. Preprint, 2020.

- Sato (1999) K.-I. Sato. Lévy processes and infinitely divisible distributions. Cambridge University Press, 1999.

- Shamir and Zhang (2013) O. Shamir and T. Zhang. Stochastic gradient descent for non-smooth optimization: Convergence results and optimal averaging schemes. In S. Dasgupta and D. McAllester, editors, Proceedings of the 30th International Conference on Machine Learning, volume 28 of Proceedings of Machine Learning Research, pages 71–79, Atlanta, Georgia, USA, 17–19 Jun 2013. PMLR. URL http://proceedings.mlr.press/v28/shamir13.html.

- Siegel and Xu (2020) J. W. Siegel and J. Xu. Approximation rates for neural networks with general activation functions. Neural Networks, 128:313–321, 2020. ISSN 0893-6080. doi: https://doi.org/10.1016/j.neunet.2020.05.019. URL https://www.sciencedirect.com/science/article/pii/S0893608020301891.

- Sirignano and Spiliopoulos (2018) J. Sirignano and K. Spiliopoulos. DGM: A deep learning algorithm for solving partial differential equations. J. Comput. Phys., 375:1339–1364, 2018. ISSN 0021-9991. doi: 10.1016/j.jcp.2018.08.029. URL https://doi.org/10.1016/j.jcp.2018.08.029.

- Stoer and Bulirsch (2002) J. Stoer and R. Bulirsch. Introduction to numerical analysis, volume 12 of Texts in Applied Mathematics. Springer-Verlag, New York, third edition, 2002. ISBN 0-387-95452-X. doi: 10.1007/978-0-387-21738-3. URL https://doi.org/10.1007/978-0-387-21738-3.