Robust Inference for High-Dimensional Linear Models

via Residual Randomization

Abstract

We propose a residual randomization procedure designed for robust Lasso-based inference in the high-dimensional setting. Compared to earlier work that focuses on sub-Gaussian errors, the proposed procedure is designed to work robustly in settings that also include heavy-tailed covariates and errors. Moreover, our procedure can be valid under clustered errors, which is important in practice, but has been largely overlooked by earlier work. Through extensive simulations, we illustrate our method’s wider range of applicability as suggested by theory. In particular, we show that our method outperforms state-of-art methods in challenging, yet more realistic, settings where the distribution of covariates is heavy-tailed or the sample size is small, while it remains competitive in standard, “well behaved” settings previously studied in the literature.

1 Introduction

The Lasso (Tibshirani, 1996) and its variants are typically used to estimate the coefficients of a linear model in the high-dimensional setting where the number of covariates, , is larger than the number of samples, . The Lasso has been shown to possess many desirable theoretical properties and has proven fruitful in applications across nearly all scientific domains (Bühlmann & Van De Geer, 2011). This widespread use has recently generated much interest in procedures for performing inference using Lasso estimates.

However, for parameters which are zero or nearly zero, the Lasso point estimates may have an irregular distribution, and naïvely constructing confidence intervals typically results in invalid inference. To overcome these difficulties, various procedures have been proposed. Wasserman & Roeder (2009) and Meinshausen et al. (2009) both used sample splitting procedures to form valid -values. Zhang & Zhang (2014), Van de Geer et al. (2014), and Javanmard & Montanari (2014) proposed the desparsified and debiased Lasso, which adds a one step correction to the Lasso estimate. The resulting estimate is not sparse, but under certain conditions, it has asymptotically negligible bias. The debiased/desparsified estimate is asymptotically normal and can be used for inference.

An alternative approach for inference in high-dimensional linear models is the bootstrap. Chatterjee & Lahiri (2011) proposed a residual bootstrap procedure for the adaptive Lasso (Zou, 2006). One crucial requirement with this approach is the “beta-min” condition, which requires the non-zero parameters to be large enough in absolute value (i.e., much larger than ). This condition can be overly restrictive in cases where the primary aim is to test null hypotheses on the significance of regression coefficients of the form . To circumvent this problem, Dezeure et al. (2017) and Zhang & Cheng (2017) both proposed bootstrap procedures based on the desparsified Lasso (Van de Geer et al., 2014), which are capable of performing simultaneous inference over a set of parameters in the linear model; i.e., for all . Zhang & Cheng (2017) proposed bootstrapping the linearized part of the desparsified Lasso with a Gaussian multiplier bootstrap, while Dezeure et al. (2017) proposed using either a wild bootstrap or a residual bootstrap procedure for the entire estimator.

The above procedures are typically obtained under strong regularity conditions on covariates and require i.i.d. sub-Gaussian errors. Therefore, they may perform poorly in more realistic settings where is relatively small, the covariates and errors are non-Gaussian and/or heavy-tailed, or have complex structures, such as heterogeneity or clustering.

In contrast, randomization methods (Fisher et al., 1935; Pitman, 1937; Kempthorne, 1952) are non-parametric and typically exact in finite samples, which makes them robust (Lehmann & Romano, 2006, Chapter 15). Randomization procedures leverage structure in the data for testing and inference —e.g., permutation tests exploit exchangeability through permuting the data—and rely less on analytical assumptions or asymptotic arguments.

We show that a robust alternative for inference in high-dimensional linear models is possible through the use of residual randomization, which was first proposed by Freedman & Lane (1983a, b) as an extension of Fisher’s randomization test. Residual randomization builds a test that is exact in the idealized case where the true errors are known, and remains asymptotically valid when using regression residuals in lieu of the true errors. Recently, Toulis (2019) extended the original residual randomization procedure to include complex error structures (e.g., clustered errors), and showed that the procedure is asymptotically valid and empirically effective in the low-dimensional setting where is fixed and grows, including settings with heterogeneity and clustering. Toulis (2019) also proposed an extension to the high-dimensional setting (different than the one we propose), but did not give any theoretical guarantees.

1.1 Contributions

In this paper, we propose a novel residual randomization procedure for conducting hypothesis tests and computing confidence intervals for parameters in a high-dimensional linear model. In Section 2.3, we define a class of oracle tests that are exact for finite samples. However, these oracle tests are infeasible, and so we develop an approximate implementation for each test in the class. Broadly speaking, our procedure selects a specific test from the class for which the approximate but feasible test is close to the oracle. Thus, we explicitly prioritize controlling the empirical size of the test. Our procedure is specifically designed to be robust to small sample sizes and non-Gaussianity in both covariates and errors. This is in contrast to previous procedures that prioritize testing power and shorter confidence intervals.

We show theoretically that our procedure is valid even when the covariates and errors are sub-Weibull as opposed to the sub-Gaussian condition previously required in the literature. We also show that our procedure is sound when the errors have clustered dependence. Indeed, we see empirically that our residual randomization method is comparable to state-of-art methods in “well behaved” high-dimensional benchmarks and is superior in more complex settings, e.g., when is small, the covariates are non-Gaussian, or the errors are heavy-tailed or heterogeneous.

2 Methodology

2.1 Setup

Throughout we let and denote the vector -norm and matrix -norm, respectively. For any positive integer , we let . For , let denote the th row and denote the th column. We let denote the th standard basis; i.e., a vector whose th element is and all other elements are .

We assume that the data are generated from the linear model

| (1) |

where are the linear coefficients, are the covariates, and is the vector of (unobservable) errors. Thus, corresponds to the covariates for the th observation and corresponds to the th covariate. Let denote the sparsity of such that .

In contrast to previous work which requires sub-Gaussian covariates and errors, we allow and to follow sub-Weibull() distributions. Sub-Weibull random variables are a class of distributions with tails of the form (Kuchibhotla & Chakrabortty, 2018; Vladimirova et al., 2020). The class of sub-Gaussian and sub-exponential distributions can be obtained as a subclass by setting equal to and , respectively. However, when , the tails can be heavier than sub-exponential. Finally, we also assume that are drawn i.i.d., and and are uncorrelated so that .

We propose a procedure to test linear hypotheses of the form

| (2) |

for some and ; we then invert the test to form confidence intervals. The form in (2) includes many hypotheses of interest; e.g., setting and implies , setting and implies . In Remark 2 we briefly discuss how the procedure can be generalized to tests of the form where and . This would allow for simultaneous inference as in Zhang & Cheng (2017) and Dezeure et al. (2017).

2.2 Residual Randomization

Following the framework of Toulis (2019), we require two key constructs: (1) A set of linear maps such that , conditional on ; and (2) An invariant , where for all and any finite . We emphasize that all the test we propose is conditional on .

Given these two definitions, if we can find a test statistic, , such that under , then we can compare the observed value of with to test . Indeed, conditioned on and (or alternatively and ), the random variable

| (3) |

is uniform over the set . Thus, can be used as a -value and rejecting the null hypothesis when yields a hypothesis test with exact size 111We describe a one sided test, but a two-sided test could be similarly defined. (save for the discreteness in which can be easily remedied by adding uniform noise to or increasing ). We consider the following three invariances for the distribution of .

Exchangeability: If all elements of are exchangeable, then could be all permutation matrices. This includes the standard setting with i.i.d. errors.

Sign Symmetry: If for all , then could be all diagonal matrices with on the diagonal. This allows for heteroskedastic errors where may depend on , but is symmetric around conditional on .

Clustered Exchangeability: In many cases, the data can be partitioned into disjoint clusters, such that exchangeability is only reasonable within a cluster; e.g., to model country-specific effects in users of an online platform; should then be the set of within-cluster permutations. This generalizes exchangeability, but we will keep the two settings distinct.

In the low-dimensional setting, where , Toulis (2019) considered tests of the form and used the test statistic , where is the least squares estimate of , and set the invariant . Since , under the null hypothesis that ,

| (4) |

Thus, given the true errors , we could form an exact -value as in Eq. (3). In practice, is unknown so one would instead use the residuals, , or the restricted residuals, , where is the restricted OLS estimates under . In this case, the test is approximate, but as shown in Toulis (2019), it can attain the correct size asymptotically.

Remark 1

The robustness properties of residual randomization can be deduced from (3). Specifically, the performance of the test does not depend on the distribution of the errors. Similarly, regularity conditions on are not needed because the test is conditioned on . Finally, the decision of the test remains invariant to monotone transformations of , and so the test remains robust to rescaling of the data. In our experiments, we demonstrate that the robustness properties of the exact test (using the true errors) are also inherited by the approximate procedure using the residuals.

2.3 High-Dimensional Residual Randomization

In the high-dimensional setting, where , the OLS estimate is ill-defined and the low-dimensional residual randomization method cannot be directly applied. In this section, we propose adjustments appropriate for the high-dimensional setting and show that this test can be further optimized for robustness.

Instead of the OLS estimator, we use a version of the debiased Lasso (Javanmard & Montanari, 2014) which corrects for the regularization bias by adding a term proportional to the subgradient of the objective at the Lasso solution , where is the penalty parameter. When it is obvious, we will simply write instead of . Appropriate values of are problem dependent, and we give theoretically sufficient choices in Section 3.

Specifically, for some , we use the estimator

| (5) |

To form the high-dimensional test statistic, we replace in (4) with :

| (6) |

Setting , this yields

| (7) | ||||

For some fixed and any , comparing to

| (8) |

for all would yield an exact test as described in (3) under the null, since . When the null hypothesis does not hold such that , under weak conditions, will be bounded at a rate of . However, contains an additional term which will grow as leading to rejection of the null hypothesis.

This procedure could be applied for any .222 If , then the distribution over would be a point mass. Nonetheless some randomization procedure for breaking ties could be used to maintain exact size. In (13), letting will prevent such an from being feasible. Thus, in contrast to the low-dimensional setting, in the high-dimensional setting, we have not just a single test, but a class of tests indexed by , all of which are exact under the null hypothesis. For any , we call this the oracle randomization distribution. Since all oracle tests are exact, a good rule of thumb would be to select the matrix , which gives the test with the most power, or alternatively, which—when inverted—yields the shortest confidence intervals. In some sense, this is the motivation behind Zhang & Cheng (2017) and Dezeure et al. (2017) setting as an estimate of , albeit for a bootstrap procedure which is not exact. As suggested by the Gauss-Markov theorem, this should asymptotically give the shortest confidence intervals.

However, since we do not have access to or , we cannot directly use any of these oracle tests. Thus, we use the following invariant with being the residuals from the Lasso regression:

| (9) | ||||

For any , we refer to the resulting distribution—when selecting uniformly from —as the attainable randomization distribution, because it only involves quantities which we can directly access and compute. The oracle (8) and attainable (9) distributions share the same second term, but differ in their first terms and . Thus, each attainable distribution no longer retains the exact size that its corresponding oracle test enjoys. In particular, selecting an attainable test based on minimizing its oracle’s confidence interval length may result in poor finite sample performance.

Instead of prioritizing short confidence intervals, we prioritize the correct size of the test by selecting to minimize the distance between the attainable test and its corresponding oracle test. Indeed, in Section 3 we show that the Wasserstein-1 distance between the oracle and attainable distributions is upper bounded by

| (10) |

Roughly speaking, regulates the difference between the means of the attainable and oracle distributions, while is the cost of using residuals instead of the true errors. Intuitively, one would expect (and we confirm empirically) that prioritizing the minimization of over has a larger effect on the accuracy of the attainable test’s -value. Towards this end, we upweight the first term by setting and select which minimizes:

| (11) |

While (11) can be solved using a linear program solver, for computational convenience, instead of directly optimizing (11) with respect to , we instead solve

| (12) |

where

| (13) | ||||

The problem in (13) is the CLIME (Cai et al., 2011) problem, and we solve it using the fastclime package (Pang et al., 2014). In Section 3 we show that, for any , using , where is a minimizer of (12), ensures that the selected attainable and oracle distributions converge.

To select , Javanmard & Montanari (2014) solve a problem with the same constraint as (13), but instead minimize the for all , which—similar to Zhang & Cheng (2017) and Dezeure et al. (2017)—prioritizes shorter confidence intervals. When it is sparse, the inverse covariance of can be consistently estimated by solving (13) (Cai et al., 2011). In that case the residual randomization procedure should still produce asymptotically efficient confidence intervals and would be asymptotically equivalent to the other procedures. However, in finite samples, we see empirical improvements in robustness. We detail our procedure in Algorithm 1, which produces a -value for testing the null hypothesis that .

Remark 2

Thus far, we have assumed a 1-dimensional hypothesis test. However, similar to Zhang & Cheng (2017) and Dezeure et al. (2017), this can generalized be to testing several null-hypotheses simultaneously. In particular, one might instead use

| (14) |

and the corresponding invariant

| (15) |

We focus on the -dimensional case for expositional clarity.

2.4 Confidence Intervals

To form a univariate confidence interval for , we invert the hypothesis test for (Rosenbaum, 2003). In particular, for we can compute the distribution of and set and to the and quantiles. Finally, to invert the level two-sided test we select such that . This is equivalent to the confidence interval for :

| (16) |

Note that as opposed to the multiplier bootstrap confidence intervals proposed by Zhang & Cheng (2017), the confidence intervals in (16) may be asymmetric because they are produced from the attainable randomization distribution, which may be asymmetric. This is similar to the procedure proposed by Dezeure et al. (2017).

3 Main Results

Let denote the oracle randomization distribution of in (8) conditional on and when is selected uniformly from . Let denote the attainable distribution; i.e., the distribution of in (9) when is chosen uniformly from . As the notation implies, both and depend on and are random distributions with respect to . We give a finite sample characterization of the Wasserstein-1 distance between these two random distributions under certain assumptions, and we show that the distance goes to with probability going to . All proofs are given in the supplement.

We first state Lemma 1 which, as mentioned in Section 2.3 shows that the distance between the oracle and attainable distributions can be decomposed into the estimation error of as well as two terms which, roughly speaking, regulate the difference in means and variance.

Lemma 1

For any , let denote the Wasserstein-1 distance between the oracle randomization distribution and attainable randomization distributions. Then,

| (17) | ||||

where is the uniform distribution over in .

We now provide conditions under which the two terms in (17) can be controlled for the selected by (13) and (12). Condition 1 requires that the tails of and be sub-Weibull and bounds certain moments of the observed covariates. In Condition 1, denotes the Orlicz norm of with and is the joint Orlicz norm.

Condition 1 (Covariates)

Suppose that are generated i.i.d. with mean and covariance . Let and denote the largest and smallest eigenvalues of . Suppose each element of is sub-Weibull() and the de-correlated covariates are jointly sub-Weibull() with

| (18) |

We also define

| (19) | ||||

We assume the high-dimensional regime where and both grow and can be much larger than . Condition 2 also implicitly restricts the 2-norm of and through . In particular, we require to scale linearly with the condition number of . We will also require so that is in the feasible set of (13) for some with probability tending to .

Condition 2 (Sample Size)

Suppose

| (20) |

and

| (21) | ||||

for some constant which only depends on .

We now give conditions on the set of group actions, .

Condition 3 (Exchangeability)

Let where is the set of all matrices corresponding to a permutation of such that (i) for some and equal-sized disjoint sets, and (ii) for all , and for all , .

Condition 4 (Sign Symmetry)

Let where is the set of all diagonal matrices containing only such that there is an equal number of positive and negative ’s.

Condition 5 (Cluster Exchangeability)

Suppose there exist disjoint sets with and such that are exchangeable, but may otherwise be dependent. That is, , where is the set of all block diagonal matrices where the block is a permutation matrix satisfying Condition 3.

In Conditions 3, 4, and 5 we implicitly assume that is even to simplify the analysis; when is odd, the last observation may be discarded. A more subtle requirement is that we do not assume the support of the randomization distribution is over all possible maps in either , , or . These sets grow exponentially in . Instead, we consider the more practical scenario where is fixed with respect to . This is similar to using the bootstrap or a Monte Carlo procedure with a number of draws that may be increased when a better approximation is desired, but in general stays fixed with . Condition 5 also implicitly requires that since if all clusters have size because there would be only sub-matrix which satisfies Condition 3 for each .

Given the conditions on the covariates and group actions, we now state Lemma 2 and 3, which show that the two terms in Lemma 1 can be controlled.

Lemma 3

Corollary 1

Corollary 1 implies that using any procedure that can produce an estimate such that is sufficient for showing that the oracle and attainable distributions converge in Wasserstein distance. For concreteness, we consider two settings and apply existing results on Lasso estimation. However, other estimators (i.e., SCAD or best subset selection) can also be used as long as attains the correct rate. First, we consider Lasso estimates when is sub-Weibull() as in Kuchibhotla & Chakrabortty (2018) who require some additional assumptions summarized in Condition 6 that follows. We also consider the setting of Belloni et al. (2016) who require sub-Gaussian covariates and errors, but allow for clustered error dependence.

Condition 6 (Lasso with sub-Weibull errors)

Suppose is sub-Weibull() with . Suppose that

| (26) |

where

| (27) | ||||

Furthermore, suppose that the Lasso penalty term is set such that

| (28) |

and in addition to Condition 2

| (29) |

where and is a constant only depending on .

Theorem 1 (Sub-Weibull Errors and Covariates)

Recall in Condition 5 with clustered errors, denotes the number of clusters, where each cluster has size . Then, Theorem 2, presented below, combines Corollary 1 with the results of Belloni et al. (2016) on Lasso estimates under clustered errors. In particular, they propose the Cluster-Lasso procedure and show that its performance depends on a term which measures the within-cluster dependence:

| (31) |

where and denotes the th covariate and th observation in the th cluster which have been adjusted by their respective cluster means. Under complete independence , and the rate in Theorem 2 recovers the rate under independent errors. In the worst case, however, , so that each cluster is essentially one observation. It is worth noting that Belloni et al. (2016) allow cluster dependence in both covariates and errors; however, we allow for dependent errors but still require the covariates to be i.i.d. For completeness, we include the assumptions of Belloni et al. (2016) in the supplement.

Theorem 2 (Clustered Errors)

Remark 3

4 Numerical Experiments

We compare nominal confidence intervals (CIs) over 1000 trials of BLPR (Liu et al., 2017), HDI (Dezeure et al., 2017), DLASSO (Javanmard & Montanari, 2014)333https://web.stanford.edu/ montanar/sslasso/code.html, SILM (Zhang & Cheng, 2017) and residual randomization (RR) with and . We slightly modified SILM to output marginal confidence intervals and ensure that the modified variance estimator does divide by if the support of the estimated is . Additional details are in the supplement, and the code is available at: https://github.com/atechnicolorskye/rrHDI.

In each setting, we sample random with rows drawn i.i.d. from either (N1) ; (G1) ; (N2) with ; (NT) for ; (GT) for ; or (WB) each element is a centered Weibull with scale and shape .

We sample the errors from (N1) ; (G1) ; (N2) with ; (WB) a centered Weibull with scale and shape ; (HN) normal with ; or (HM) with . The exchangeable settings exclude the heteroskedastic cases of HN and HM; the symmetric settings exclude G1 and WB.

For a fair comparison, we have HDI use wild bootstrap for the symmetric settings. Also, apart from SILM, empirical performance is generally not affected by the scale of the covariates; however, in certain settings SILM performed very poorly when the covariates were not standardized. Thus, we standardize the covariates to benefit SILM.

For each setting, we draw with or active (i.e., non-zero) coordinates drawn from the Rademacher distribution and set the remaining inactive coordinates to 0. We arrange entries in in such that there is one active entry between two inactive entries (isolated), one active between an active entry and an inactive entry (adjacent), and one active entry between two other active entries (sandwiched). We also use the same scheme for the inactive variables. We then set .

To obtain , we solve (13) to up to iterations using fastclime (Pang et al., 2014) which starts with and uses warm starts to progressively shrink . We further select via (12) by using a grid search over the values used by fastclime with . Empirically, a larger value of generally results in better coverage, but comes at the expense of confidence interval length; broadly speaking though, we see that for , the performance of the proposed procedure is fairly insensitive to the value of .

Since in practice we do not know the appropriate Lasso tuning parameter a priori, for the residual randomization procedure we employ the Square-Root Lasso (Belloni et al., 2011) implemented in RPtests (Shah & Buhlmann, 2017) to obtain estimates for . We follow (Zhang & Cheng, 2017) and rescale by as a finite-sample correction. For all settings, we use group actions/bootstrap resamples.

In Figures 1 and 2 we show the empirical coverage and the confidence interval length for the active variables when for exchangeable and symmetric errors respectively. In the supplement, we provide corresponding figures for the inactive variables as well as results for .

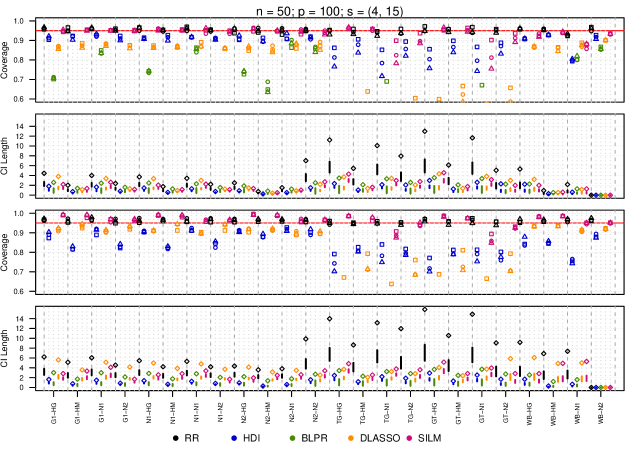

Among the competing methods, SILM performs the best, and has generally satisfactory performance across all settings except the Toeplitz case and the setting with Weibull covariates for . For , HDI generally outperforms DLASSO, but when , HDI’s performance decreases drastically. Generally, BLPR performs the worst and when has coverage less than . All the competing methods perform poorly when the covariates have Toeplitz covariance. The sandwich coordinates typically have the lowest coverage and the isolated coordinates typically have empirical coverage closest to the nominal rate.

In contrast, we see that RR nearly obtains the nominal 95% coverage regardless of exchangeability or sign symmetry, and across all experimental configurations. This remarkable stability can be explained by our selection procedure for and the general properties of randomization tests (see Introduction and Remark 1). At the same time, RR typically yields larger interval lengths. While the interval length from RR is generally longer than the competing methods, this is especially true when the covariates have Toeplitz covariance. We posit that this is because solving (13) for poorly conditioned sample covariances can yield large and thus results in larger confidence intervals.

In the supplement, we show the empirical coverage for the inactive coordinates with as well as all coordinates when . For , the results are qualitatively similar to the results for ; RR almost always has the best empirical coverage followed by SILM, HDI, DLASSO, and then BLPR. However, all methods (including RR) generally perform less well; in particular, in contrast to the case, there are some settings where RR does not attain nominal coverage. For the inactive variables when and , all procedures except BLPR typically achieve (or exceed) nominal coverage.

Table 1 gives the average computation time (in seconds) required for each of the procedures with , . We form a confidence interval for each of the 300 coordinates using group actions/bootstrap resamples. Unsurprisingly, RR requires more computational effort than competing procedures that appeal to asymptotic limiting distributions (BLPR and DLASSO). However, the computational effort is comparable to the resampling-based methods in our experiments (HDI and SILM).

| Method | BLPR | HDI | DLASSO | SILM | RR |

| Time (s) | 18.9 | 374.2 | 11.2 | 61.1 | 135.1 |

5 Discussion

The theoretical guarantees coupled with the excellent empirical performance suggest that residual randomization is an appealing alternative for robust inference in high-dimensional linear models. Across a wide range of settings, it attains nominal coverage even when is small or the errors are heavy tailed. Of course, this does not come for free, as we observe that the confidence intervals produced are generally larger than those produced by competing methods—especially when there is strong cross-correlation in covariates. Nonetheless, we believe that in most practical applications slightly larger confidence intervals is a small price to pay in exchange for better, more robust coverage.

While the procedure is asymptotically valid for any fixed , one practical concern is specifying a tuning parameter when selecting . If is too small, this may result in degraded empirical performance; however, the simulations show that there is a threshold of for which our procedure performs well across all settings. This threshold seems to coincide with a point at which the length of our confidence intervals become insensitive to increasing . Thus, this threshold can be well approximated—at least via heuristics.

Nonetheless, in Section 3 of the supplement, we describe an alternative procedure which also performs well empirically and is also asymptotically valid when an upper bound on in (19) is known.

Several questions may be fruitful to pursue in the future. First, to form confidence intervals, we require control of . However, it would be interesting to investigate residual randomization procedures which only require small in-sample prediction error; i.e., . This would allow testing individual coordinates of without assuming stringent restricted eigenvalue or irrepresentability conditions. There are additional advantages of the residual randomization framework which could be further exploited methodologically. For example, we primarily focused on selecting , but one could also use the observed covariates to select specific invariances which optimize certain test properties.

Acknowledgments

This work was completed in part with resources provided by the University of Chicago Research Computing Center.

References

- Belloni et al. (2011) Belloni, A., Chernozhukov, V., and Wang, L. Square-root lasso: pivotal recovery of sparse signals via conic programming. Biometrika, 98(4):791–806, 2011. ISSN 0006-3444. doi: 10.1093/biomet/asr043. URL https://doi.org/10.1093/biomet/asr043.

- Belloni et al. (2016) Belloni, A., Chernozhukov, V., Hansen, C., and Kozbur, D. Inference in high-dimensional panel models with an application to gun control. Journal of Business & Economic Statistics, 34(4):590–605, 2016.

- Bickel & Freedman (1981) Bickel, P. J. and Freedman, D. A. Some asymptotic theory for the bootstrap. The annals of statistics, pp. 1196–1217, 1981.

- Bickel & Freedman (1983) Bickel, P. J. and Freedman, D. A. Bootstrapping regression models with many parameters. Festschrift for Erich L. Lehmann, pp. 28–48, 1983.

- Bühlmann & Van De Geer (2011) Bühlmann, P. and Van De Geer, S. Statistics for high-dimensional data: methods, theory and applications. Springer Science & Business Media, 2011.

- Cai et al. (2011) Cai, T., Liu, W., and Luo, X. A constrained minimization approach to sparse precision matrix estimation. J. Amer. Statist. Assoc., 106(494):594–607, 2011. ISSN 0162-1459. doi: 10.1198/jasa.2011.tm10155. URL https://doi.org/10.1198/jasa.2011.tm10155.

- Chatterjee & Lahiri (2011) Chatterjee, A. and Lahiri, S. N. Bootstrapping lasso estimators. J. Amer. Statist. Assoc., 106(494):608–625, 2011. ISSN 0162-1459. doi: 10.1198/jasa.2011.tm10159. URL https://doi.org/10.1198/jasa.2011.tm10159.

- Dezeure et al. (2017) Dezeure, R., Bühlmann, P., and Zhang, C.-H. High-dimensional simultaneous inference with the bootstrap. TEST, 26(4):685–719, 2017. ISSN 1133-0686. doi: 10.1007/s11749-017-0554-2. URL https://doi.org/10.1007/s11749-017-0554-2.

- Fisher et al. (1935) Fisher, R. A. et al. The design of experiments. The design of experiments., (2nd Ed), 1935.

- Freedman & Lane (1983a) Freedman, D. and Lane, D. A nonstochastic interpretation of reported significance levels. Journal of Business & Economic Statistics, 1(4):292–298, 1983a.

- Freedman & Lane (1983b) Freedman, D. A. and Lane, D. Significance testing in a nonstochastic setting. In A Festschrift for Erich L. Lehmann, Wadsworth Statist./Probab. Ser., pp. 185–208. Wadsworth, Belmont, CA, 1983b.

- Javanmard & Montanari (2014) Javanmard, A. and Montanari, A. Confidence intervals and hypothesis testing for high-dimensional regression. The Journal of Machine Learning Research, 15(1):2869–2909, 2014.

- Kempthorne (1952) Kempthorne, O. The design and analysis of experiments. 1952.

- Kuchibhotla & Chakrabortty (2018) Kuchibhotla, A. K. and Chakrabortty, A. Moving beyond sub-gaussianity in high-dimensional statistics: Applications in covariance estimation and linear regression. arXiv preprint arXiv:1804.02605, 2018.

- Lehmann & Romano (2006) Lehmann, E. L. and Romano, J. P. Testing statistical hypotheses. Springer Science & Business Media, 2006.

- Liu et al. (2017) Liu, H., Xu, X., and Li, J. J. A bootstrap lasso+ partial ridge method to construct confidence intervals for parameters in high-dimensional sparse linear models. arXiv preprint arXiv:1706.02150, 2017.

- Lopes (2014) Lopes, M. E. A residual bootstrap for high-dimensional regression with near low-rank designs. In Proceedings of the 27th International Conference on Neural Information Processing Systems - Volume 2, NIPS’14, pp. 3239–3247, Cambridge, MA, USA, 2014. MIT Press.

- Meinshausen et al. (2009) Meinshausen, N., Meier, L., and Bühlmann, P. -values for high-dimensional regression. J. Amer. Statist. Assoc., 104(488):1671–1681, 2009. ISSN 0162-1459. doi: 10.1198/jasa.2009.tm08647. URL https://doi.org/10.1198/jasa.2009.tm08647.

- Pang et al. (2014) Pang, H., Liu, H., and Vanderbei, R. The fastclime package for linear programming and large-scale precision matrix estimation in r. Journal of Machine Learning Research, 15(14):489–493, 2014. URL http://jmlr.org/papers/v15/pang14a.html.

- Pitman (1937) Pitman, E. J. Significance tests which may be applied to samples from any populations. Supplement to the Journal of the Royal Statistical Society, 4(1):119–130, 1937.

- Rosenbaum (2003) Rosenbaum, P. R. Exact confidence intervals for nonconstant effects by inverting the signed rank test. The American Statistician, 57(2):132–138, 2003.

- Shah & Buhlmann (2017) Shah, R. and Buhlmann, P. RPtests: Goodness of Fit Tests for High-Dimensional Linear Regression Models, 2017. URL https://CRAN.R-project.org/package=RPtests. R package version 0.1.4.

- Tibshirani (1996) Tibshirani, R. Regression shrinkage and selection via the lasso. J. Roy. Statist. Soc. Ser. B, 58(1):267–288, 1996. ISSN 0035-9246. URL http://links.jstor.org/sici?sici=0035-9246(1996)58:1<267:RSASVT>2.0.CO;2-G&origin=MSN.

- Toulis (2019) Toulis, P. Life after bootstrap: Residual randomization inference in regression models. arXiv preprint arXiv:1908.04218, 2019.

- Van de Geer et al. (2014) Van de Geer, S., Bühlmann, P., Ritov, Y., Dezeure, R., et al. On asymptotically optimal confidence regions and tests for high-dimensional models. The Annals of Statistics, 42(3):1166–1202, 2014.

- Vladimirova et al. (2020) Vladimirova, M., Girard, S., Nguyen, H., and Arbel, J. Sub-weibull distributions: Generalizing sub-gaussian and sub-exponential properties to heavier tailed distributions. Stat, 9(1):e318, 2020.

- Wasserman & Roeder (2009) Wasserman, L. and Roeder, K. High-dimensional variable selection. Ann. Statist., 37(5A):2178–2201, 2009. ISSN 0090-5364. doi: 10.1214/08-AOS646. URL https://doi.org/10.1214/08-AOS646.

- Zhang & Zhang (2014) Zhang, C.-H. and Zhang, S. S. Confidence intervals for low dimensional parameters in high dimensional linear models. J. R. Stat. Soc. Ser. B. Stat. Methodol., 76(1):217–242, 2014. ISSN 1369-7412. doi: 10.1111/rssb.12026. URL https://doi.org/10.1111/rssb.12026.

- Zhang & Cheng (2017) Zhang, X. and Cheng, G. Simultaneous inference for high-dimensional linear models. J. Amer. Statist. Assoc., 112(518):757–768, 2017. ISSN 0162-1459. doi: 10.1080/01621459.2016.1166114. URL https://doi.org/10.1080/01621459.2016.1166114.

- Zou (2006) Zou, H. The adaptive lasso and its oracle properties. J. Amer. Statist. Assoc., 101(476):1418–1429, 2006. ISSN 0162-1459. doi: 10.1198/016214506000000735. URL https://doi.org/10.1198/016214506000000735.