Discrete potential mean field games: duality and numerical resolution111This work was supported by a public grant as part of the Investissement d’avenir project, reference ANR-11-LABX-0056-LMH, LabEx LMH, and by the FIME Lab (Laboratoire de Finance des Marchés de l’Energie), Paris.

Abstract

We propose and investigate a general class of discrete time and finite state space mean field game (MFG) problems with potential structure. Our model incorporates interactions through a congestion term and a price variable. It also allows hard constraints on the distribution of the agents. We analyze the connection between the MFG problem and two optimal control problems in duality. We present two families of numerical methods and detail their implementation: (i) primal-dual proximal methods (and their extension with nonlinear proximity operators), (ii) the alternating direction method of multipliers (ADMM) and a variant called ADM-G. We give some convergence results. Numerical results are provided for two examples with hard constraints.

Key-words:

mean field games, dynamic programming, Kolmogorov equation, duality theory, primal-dual optimization, ADMM, ADM-G.

AMS classification:

49N80, 49N15, 90C25, 91A16, 91A50.

1 Introduction

The class of mean field game (MFG) problems was introduced by J.-M. Lasry and P.-L. Lions in [34, 35, 36] and M. Huang, R. Malhamé, and P. Caines in [33] to study interactions among a large population of agents. The agents of the game optimize their own dynamical system with respect to a criterion; the criterion is parameterized by some endogenous coupling terms. These coupling terms are linked to the collective behavior of all agents and thus induce an interaction between them. It is assumed that an isolated agent has no impact on the coupling terms and that all agents are identical. At a mathematical level, MFGs typically take the form of a system of coupled equations: a dynamic programming equation (characterizing the optimal behavior of the agents), a Kolmogorov equation (describing the distribution of the agents), and coupling equations.

In this work we study a class of discrete time and finite state space mean field games with potential structure. The dynamical system of each agent is a Markov chain, with controlled probability transitions. Few publications deal with fully discrete models; in a seminal work, D. Gomes, J. Mohr, and R. R. Souza [25] have studied the existence of a Nash equilibrium via a fixed point approach and investigated the long-term behavior of the game. The proof relies on a monotonicity assumption for the congestion term. In [31], in a similar setting, the convergence of the fictitious play algorithm is established. In addition [31] proves the convergence of a discrete mean field game problem (with an entropic regularization of the running cost) toward a continuous first-order mean field game.

Potential (also called variational) MFGs are coupled systems which can be interpreted as first-order conditions of two control problems in duality whose state equations are respectively a Kolmogorov equation and a dynamic programming equation. The primal problem (involving the Kolmogorov equation) can be interpreted as a stochastic optimal control problem with cost and constraints on the law of the state and the control. Its numerical resolution is thus of interest beyond the context of MFGs.

Framework.

In our model, the agents interact with each other via two coupling terms: a congestion variable and a price variable . The congestion is linked to the distribution of the agents via the subdifferential of a proper convex and l.s.c. potential . The price is linked to the joint law of states and controls of the agents via the subdifferential of a proper convex and l.s.c. potential . A specificity of our discrete model is that the potentials and can take the value and thus induce constraints on the distribution of the agents, referred to as hard constraints. In the continuous case, four classes of variational MFGs can be identified. Our model is general enough to be seen as the discrete counterpart of these four cases. Case 1: MFGs with monotone congestion terms ( is differentiable, ). The first variational formulation was given in [35] and has been widely studied in following works [8, 14, 16, 37, 38]. Case 2: MFGs with density constraints ( has a bounded domain, ). These models are of particular interest for describing crowd motions. The coupling variable has there an incentive role. The reader can refer to [16, 37, 41, 42]. Case 3: MFGs with Cournot interactions (, is differentiable). In this situation, each agent optimally chooses a quantity to be sold at each time step of the game. Interactions with the other players occur through the gradient of which maps the mean strategy (the market demand) to a market price. See for example [10, 27, 28, 29, 30]. Case 4: MFGs with price formation (, has a bounded domain). These models incorporate a hard constraint on the demand. The price variable is the associated Lagrange multiplier and has a incentive role. We refer to [26].

The first part of the article is devoted to the theoretical analysis of the MFG system. We first introduce a potential problem, shown to be equivalent to a convex problem involving the Kolmogorov equation via a change of variable, similar to the one widely employed in the continuous setting (e.g. in [6]). Under a suitable qualification condition, we establish a duality result between this problem and an optimal control problem involving the dynamic programming equation. We show the existence of solutions to these problems and finally we show the existence of a solution to the MFG system. A uniqueness result is proved (when and are differentiable).

The second part of the article is devoted to the numerical resolution of the MFG system. We focus on two families of methods: primal-dual methods and augmented Lagrangian methods. These two classes exploit the duality structure discussed above and can deal with hard constraints. They have already been applied to continuous MFGs, see for example the survey article [3]. Primal-dual methods have been applied to stationary MFGs with hard congestion terms in [13] and to time-dependent MFGs in [12]. In a closely related setting, [21] applies a primal-dual method to solve a discretized optimal transport problem. Augmented Lagrangian methods have been applied to MFGs in [5] and to MFGs with hard congestion terms in [8]. Other methods exploiting the potential structure have been investigated in the literature, they are out of the scope of the current article. Let us mention the Sinkhorn algorithm [7]. The fictitious play method has been investigated in various settings: [23] shows the connection between the fictitious play method and the Frank-Wolfe algorithm in a discrete and potential setting; [15] considers a continuous setting, with a non-convex potential.

Let us emphasize that the above references all deal with interaction terms depending on the distribution of the states of the agents; very few publications are concerned by interactions through the controls (see [2]). The present work is the first to address methods for “Cournot” mean field games.

Contributions.

Let us comment further on the families of methods under investigation and our contributions. The primal-dual algorithms that we have implemented were introduced by A. Chambolle and T. Pock [17] and applied to mean field games in [13]. A novelty of our work is also to show that the extension of primal-dual methods of [18], involving nonlinear proximity operators (based on Bregman divergences), can also be used to solve MFGs. The augmented Lagrangian method that we have implemented is applied to the dual problem (involving the dynamic programming equation), as originally proposed in [6] for optimal transportation problems. As in [6], we have actually implemented a variant of the augmented Lagrangian method, called alternating direction method of multipliers (ADMM). The method was introduced by R. Glowinski and A. Marroco [24] and studied by D. Gabay and B. Mercier [22]. It relies on a successive minimization of the augmented Lagrangian function. One of the main limitations of ADMM is that when the number of involved variables is greater or equal to three, as it is the case for our problem, convergence is not granted. A novelty of our work is to consider a variant of ADMM, the alternating direction method with Gaussian back substitution (ADM-G), introduced in [32]. At each iteration of this method, the ADMM step is followed by a Gaussian back substitution step. Convergence is ensured. The practical implementation of the additional step turns out to be inexpensive in our framework.

The last contribution of this work is to propose and solve numerically two hard constraints problems: a congestion mean field game problem and a “Cournot” mean field game. Following our analysis we define a notion of residuals allowing us to compare the empirical convergence of each method in a common setting.

Organization of the article.

The article is organized as follows. In section 2 we provide the main notations, the mean field game system under study and the underlying individual player problem. In section 3 we formulate a potential problem and perform the announced change of variable. In section 4 we form a dual problem and we establish a duality result. In section 5 we provide our main results: existence and uniqueness of a solution to the mean field game. In section 6 we provide a detailed implementation of the primal-dual proximal algorithms, ADMM and ADM-G, and we give theoretical convergence results when possible. In section 7 we present numerical results for two concrete problems. We provide outputs obtained for each method: errors, value function, equilibrium measure, mean displacement, congestion, demand and price.

2 Discrete mean field games

2.1 Notation

Sets.

Let denote the duration of the game. We set and . Let denote the state space. We set

For any finite set , we denote by the finite-dimensional vector space of mappings from to . For any finite set and linear operator , we denote the adjoint operator satisfying the relation

All along the article, we make use of the following spaces:

Convex analysis.

For any function , we denote

The subdifferential of is defined by

By convention, if . Note also that if and only if , where is the Fenchel transform of , defined by

Note that the subdifferential and Fenchel transforms of , , and (introduced in the next paragraph) are considered for fixed values of the time and space variables.

We denote by the indicator function of (without specifying the underlying vector space). For any subset , we denote by the indicator function of . For any , we denote by the normal cone to at ,

We set if .

Nemytskii operators.

Given two mappings and , we call Nemytskii operator the mapping defined by

We will mainly use this notation in order to avoid the repetition of time and space variables, for example, we will write instead of .

All along the article, we will transpose some notions associated with to the Nemytskii operator . When and , we define the domain of by

We define by where is the Fenchel transform of with respect to the second variable.

2.2 Coupled system

Data and assumption.

We fix an initial distribution and four maps: a running cost , a potential price function , a potential congestion cost , and a displacement cost ,

The following convexity assumption is in force all along the article. Note that we will later make use of an additional qualification assumption (Assumption 4.1).

Assumption 2.1 (Convexity).

For any , the maps , , and are proper, convex and lower semicontinuous. In addition .

Coupled system.

The unknowns of the MFG system introduced below are denoted . They can be described as follows:

-

and are the coupling terms of the MFG: is a congestion term incurred by agents located at at time and is a price variable

-

denotes the probability transition from to , for agents located at at time

-

denotes the proportion of agents located at at time

-

is the value function of the agents.

For any , we define the individual cost ,

Given , we denote

We aim at finding a quintuplet such that for any ,

| (MFG) |

Heuristic interpretation.

-

The dynamical system of each agent is a Markov chain controlled by , with initial distribution : for any ,

(1) Given the coupling terms , the individual control problem is

(2) The equations (MFG,i-ii) are the associated dynamic programming equations: given , if and satisfy these equations, then is a solution to (2). The reader can refer to [9, Chapter 7] for a detailed presentation of the dynamic programming approach for the optimal control of Markov chains.

-

Given , denote by the probability distribution of , that is, . Then is obtained by solving the Kolmogorov equation (MFG,iii). In the limit when the number of agents tends to , the distribution coincides with the empirical distribution of the agents.

-

Finally, the equations (MFG,iv-v) link the coupling terms and to the distribution of the agents and their control .

In summary: given a solution to (MFG), the triplet is a solution to the mean field game

Potential problem.

The next section of the article will be dedicated to the connection between the coupled system and the potential problem (P), introduced page P. We provide here a stochastic formulation of (P) as an optimal control problem of a Markov chain, which has its own interest:

where is a controlled Markov satisfying (1).

Remark 2.2.

-

At any time , it is possible to encode constraints on the transitions of the agents located at by defining in such a way that is strictly included into . An example will be considered in Section 7.

-

If and are differentiable, then their subdifferentials are singletons and thus the coupling terms and are uniquely determined by and through the equations (MFG,iv-v).

2.3 Further notation

We introduce now two linear operators, and . They will allow to bring out the connection between the coupled system and the potential problem. The operator and its adjoint are given by

The operator and its adjoint are given by

We can now reformulate the dynamic programming equations of the coupled system (MFG,i-ii) as follows:

3 Potential problem and convex formulation

3.1 Perspective functions

Given a proper l.s.c. and convex function with bounded domain, we define the perspective function (following [39, Section 3]) by

Lemma 3.1.

The perspective function is proper, convex, l.s.c. and its domain is given by For any , we have

| (3) |

where .

Proof.

The proof is a direct application of [11, Lemmas 1.157, 1.158] when has a bounded domain. In this case the recession function of is the indicator function of zero. ∎

Lemma 3.2.

Let . Then if and only if

Proof.

Direct application of [20, Proposition 2.3]. ∎

3.2 Potential problem

We define the following criterion

and the following potential problem (recall that is the solution to the Kolmogorov equation (MFG,iii), given ):

| (P) |

The link between the mean field game system (MFG) and the potential problem (P) will be exhibited in Section 5. Notice that Problem (P) is not convex. Yet we can define a closely related convex problem, whose link with (P) is established in Lemma 3.3.

We denote by the perspective function of with respect to the third variable. By Lemma 3.1 the function is proper convex and l.s.c. for any . We define

In the above definition, is the Nemytskii operator of , that is, for any ,

We consider now the following convex problem:

| (P̃) |

where is defined by

Lemma 3.3.

Proof.

Step 1: . Let be such that . Let

| (4) |

for any . Then is feasible for problem (P̃) and

| (5) |

for any . Indeed by definition of , if then (5) holds and if then and (5) still holds. It follows that and consequently, .

Step 2: . Let be such that and let be such that

| (6) |

for all . Then (5) is satisfied and is feasible for (P). Thus , and consequently, .

Step 3: non-empty and bounded sets of solutions. Since is l.s.c. with non-empty bounded domain, it reaches its minimum on its domain. Then the set of solutions to (P) is non-empty and bounded. Now let be a solution to (P) and let be given by (4). We have that

thus we deduce that the set of solutions to (P̃) is non-empty. It remains to show that the set of solutions to (P̃) is bounded. Let be a solution to (P̃). The Kolmogorov equation implies that , for any . By Lemma 3.1, we have , which implies that . ∎

4 Duality

We show in this section that Problem (P̃) is the dual of an optimization problem, denoted (D), itself equivalent to an optimal control problem of the dynamic programming equation, problem (D̃). For this purpose, we introduce a new assumption (Assumption 4.1), which is assumed to be satisfied all along the rest of the article.

4.1 Duality result

The dual problem is given by

| (D) |

Note that the above kind of dynamic programming equation involves inequalities (and not equalities as in (MFG,i)).

We introduce now a qualification condition, which will allow to prove the main duality result of the section. For any and we define the solution to the following perturbed Kolmogorov equation

| (7) |

We also define, for any ,

| (8) |

Assumption 4.1 (Qualification).

There exists such that for any in with , there exists such that

| (9) |

Remark 4.2.

Assume that and are non-empty sets. Then in this case, Assumption 4.1 is satisfied if there exists such that

Remark 4.3 (Mean field game planning problem and optimal transport).

Theorem 4.4.

Proof.

The primal problem (P̃) can formulated as follows:

| () |

where the maps and and the operator are defined by

| (10) |

We next prove that the qualification condition

is satisfied. This is equivalent to show the existence of such that for any , with , there exists satisfying

This is a direct consequence of Assumption 4.1. Therefore, we can apply the Fenchel-Rockafellar theorem (see [40, Theorem 31.2]) to problem (). It follows that the following dual problem has the same value as () and possesses a solution:

| () |

It remains to calculate , , and . For any , we define

We then define

| (11) |

For any we have by Lemma 3.1 that

The adjoint operator is given by

It follows that

Moreover, It follows that (D) and () are equivalent, which concludes the proof of the theorem. ∎

4.2 A new dual problem

We introduce in this section a new optimization problem, equivalent to (D). We define the mapping which associates with the solution to the dynamic programming equation

| (12) |

We define the following problem

| (D̃) | ||||

Note that the above dual criterion is of similar nature as the dual criterion in [19, Remark 2.3].

Lemma 4.5.

Proof.

Conversely, let be feasible for (D). Let . Now we claim that , for any (this is nothing but a comparison principle for our dynamic programming equation). The proof of the claim relies on a monotonicity property of . Given and , we say that if , for all . Since has its domain included in , we have

Using the above property, it is easy to prove the claim by backward induction. It follows that and finally, val(D̃) val(D). Thus the two problems have the same value.

The other claims of the lemma are then easy to verify. ∎

Lemma 4.6.

For any , the map is concave.

Proof.

Let . Given , consider the Markov chain defined by

By the dynamic programming principle, we have

The criterion to be minimized in the above equality is affine with respect to , thus it is concave. The infimum of a family of concave functions is again concave, therefore, is concave with respect to . ∎

As a consequence of the above Lemma, the criterion is concave.

5 Connection between the MFG system and potential problems

The connection between the MFG system and the potential problems can be established with the help of seven conditions, which we introduce first. We say that and satisfy the condition (C1) if for any ,

where . We say that the conditions (C2-C7) are satisfied if

We show in the next lemma that the conditions (C1-C7) are necessary and sufficient optimality conditions for () and ().

Lemma 5.1.

Proof.

Let and . We define the two quantities and as follows:

By Theorem 4.4, and are respectively solutions of () and () if and only if . Then we have the following decomposition

where

for any . By the Fenchel-Young inequality,

Then if and only if

| (13) |

By Lemma 3.2 we have that (C1) holds if and only if and it is obvious that (C2-C7) holds if and only if . Then the conditions (C1-C7) hold if and only if (13) holds, which concludes the proof. ∎

Proposition 5.2.

Proof.

For any , we define the set of controls satisfying

if and

if , for any . Note that for any , we have , for any . We have now the following converse property to Proposition 5.2.

Proposition 5.3.

Let and be respectively solutions to () and (). Let and let . Then is a solution to (MFG).

Proof.

By Lemma 4.5, is a solution to (D). The pairs and are solutions to () and ()), respectively, therefore they satisfy conditions (C1-C7), by Lemma 5.1. Equations (MFG,iii-v) are then obviously satisfied. By definition, satisfies (MFG,i). Finally, (MFG,ii) is satisfied, by condition (C1) and by definition of the set . It follows that is solution to (MFG). ∎

Since the existence of solutions to () and () has been established in Lemmas 3.3 and 4.5, we have the following corollary.

Corollary 5.4.

There exists a solution to (MFG).

We finish this section with a uniqueness result.

Proposition 5.5.

Proof.

It follows from Proposition 5.2 that is a solution to () and that and are solutions to (). Thus by Lemma 5.1, the conditions (C3) and (C4) are satisfied, both for and and for and , which implies that and . It further follows that .

If moreover is strictly convex for any then the minimal argument in (MFG,ii) is unique, which implies that and finally that . ∎

6 Numerical methods

In this section we investigate the numerical resolution of the problems () and (). We investigate different methods: primal-dual proximal algorithms, ADMM and ADM-G. For all methods, it is assumed that the computation of the prox operators (defined below) of , and are tractable. Note that for the method involving the Kullback-Leibler distance in Subsubsection 6.2.2, the prox of is replaced by a stightly more complex optimization problem.

We explain in the Appendix A how to calculate the prox of (and the nonlinear proximator based on the entropy function) in the special case where is linear on its domain. We explain in Section 6.4 how to recover a solution to (MFG).

6.1 Notations

Let be a subset of , let denote its closure. Let . Assume that the following assumption holds true.

Assumption 6.1.

The set is convex and the map is continuous and 1-strongly convex on . There exists an open subset containing such that can be extended to a continuous differentiable function on .

We define then the Bregman distance by

If is the Euclidean distance , then .

Given a l.s.c., convex and proper function , we define its proximal operator as follows:

For any non-empty, convex and closed , we define the projection operator of on by

Finally, we denote for any .

6.2 Primal-dual proximal algorithms

In this subsection we present the primal-dual algorithms proposed by A. Chambolle and T. Pock in [17] and [18]. For the sake of simplicity, we denote by the primal variable and by the dual variable . The primal-dual algorithms rely on the following saddle-point problem

| (14) |

which is equivalent to problem () (defined in the proof of Theorem 4.4). Let and be two subsets of and , respectively. Let and let satisfy Assumption 6.1.

For any and for any we define:

Iteration ,

(15)

Then we define the following algorithm.

Theorem 6.2.

Let be such that , where denotes the operator norm of (for the Euclidean norm). Assume that and . Assume that the iteration (15) is well-defined, that is, the minimal arguments in (i) and (iii) exist. Let denote the sequence generated by the algorithm. For any we set

| (16) |

Let . Then the following holds:

- 1.

- 2.

Proof.

Remark 6.3.

Lemma 6.4.

Let . Then , where is the cardinal of the set .

Proof.

For any , we have

We have and , which concludes the proof. ∎

6.2.1 Euclidean distance

Now we explicit the update rule (15) in the case where and are both equal to the Euclidean distance and defined on and respectively. In this situation (i,15) and (iii,15) can be expressed via proximal operators:

| (19) |

Now we detail the computation of the proximal steps in the above algorithm.

Primal step.

Dual step.

Remark 6.5.

An alternative formulation of the primal problem (avoiding the decoupling and ) is as follows:

where

This formulation may have numerical advantages since the operator has a smaller norm than . In full generality, there is however no analytic form for the proximal operator of the that would be based on the proximal operators of and . Therefore we do not explore any further this formulation.

6.2.2 Kullback-Leibler divergence

In this section we slightly modify the Euclidean framework above. Instead of considering a Euclidean distance in (i,15), we consider an entropy based Bregman distance called Kullback-Leibler divergence. Let us define

For any , we define

| (22) |

with the convention that . Then, given and , we have

where

| (23) |

As can be easily verified, the map is -strongly convex on . The domain of is not contained in in general (as required by Theorem 6.2), however is not -strongly convex on . This is a minor issue, since any solution to (14) lies in , thus we can replace by without modifying the solution set to the problem.

Compared to the Subsection 6.2.1, the computations of (21) still hold. The projection step (20) is now replaced by

| (24) |

6.3 ADMM and ADM-G

We now present ADMM and ADM-G. Introducing the variables

| (25) |

and recalling the definition of and (see the proof of Theorem 4.4), the problem (D) can be written as follows:

| (26) |

Remark 6.6.

Let . The Lagrangian and augmented Lagrangian associated with problem (26) are defined by

| (27) | ||||

when evaluated at . Note that their definition is different from the one introduced in (14).

We define an ADMM step which consists in the updates of , and via three successive minimization steps and in the update of via a gradient ascent step of the augmented Lagrangian:

Iteration ,

(28)

6.3.1 ADMM

The ADMM method is given by Algorithm 2.

Unlike in [6] this algorithm does not reduce to ALG2, thus we have no theoretical guarantee about the convergence. But as we will see in subsection 6.3.2, convergence results are available for ADM-G. The relation (28,i) is given by

The relation (28,ii) can be written under a proximal form,

for any . The relation (28, iii) can be written as a projection step

| (29) |

6.3.2 ADM-G

We explicit now the implementation of the ADM-G algorithm introduced in [32]. To fit their framework we define

with appropriate dimensions, so that the constraint of problem (26) writes . We define

Then we have

Theorem 6.7.

Proof.

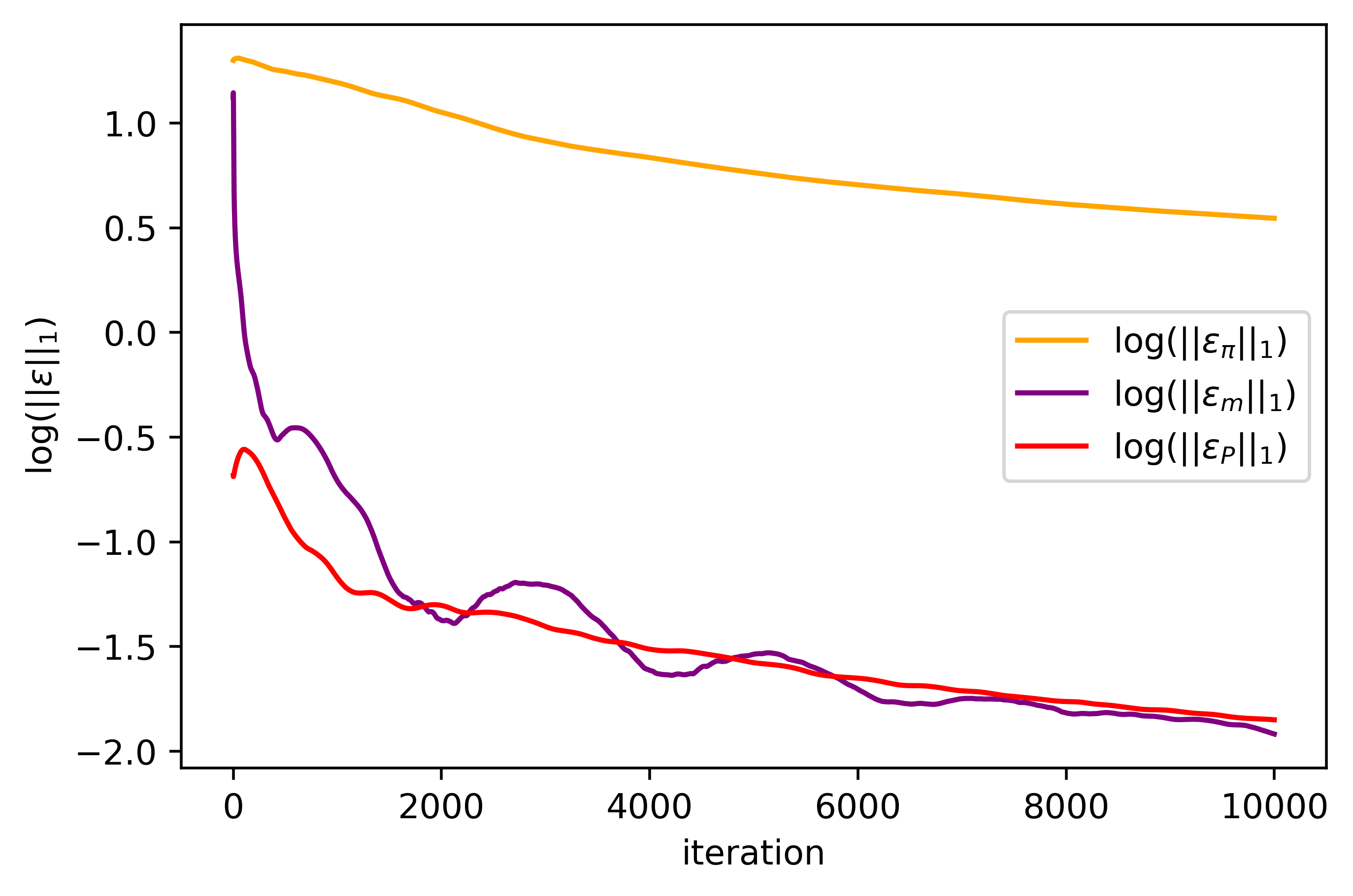

6.4 Residuals

Let and denote the two sequences generated by a numerical method. Let us consider

| (32) |

It was shown in Proposition 5.3 that if for some , and are solutions to () and (), then is a solution to (MFG).

Therefore, we look the sequence as a sequence of approximate solutions to (MFG). Note that (MFG,i) is exactly satisfied, by construction. We consider the residuals defined as follows, in order to measure the satisfaction of the remaining relations in the coupled system:

for all . If the residuals are null, then is a solution to (MFG). The errors are then defined as the norms of , , , and .

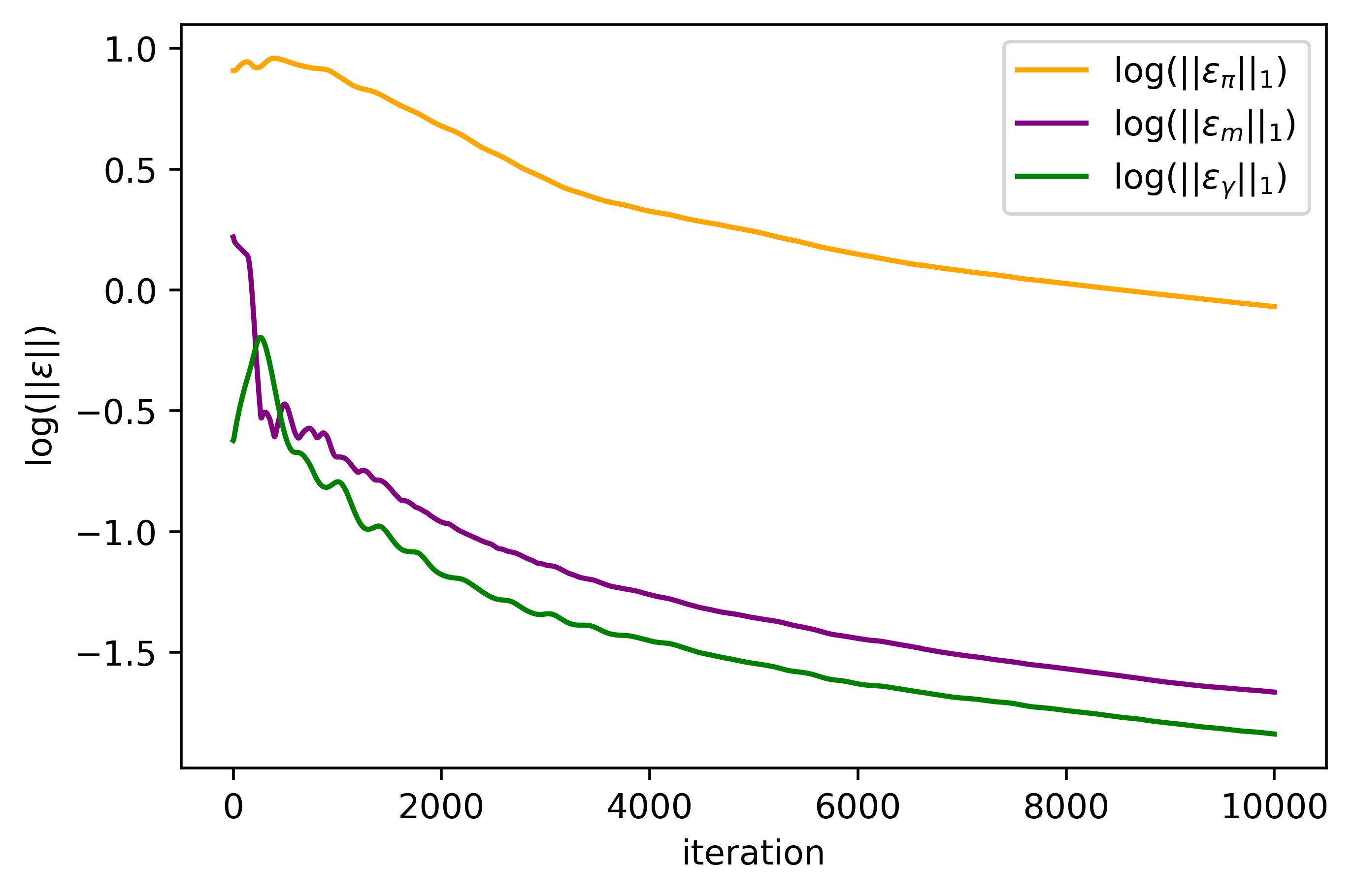

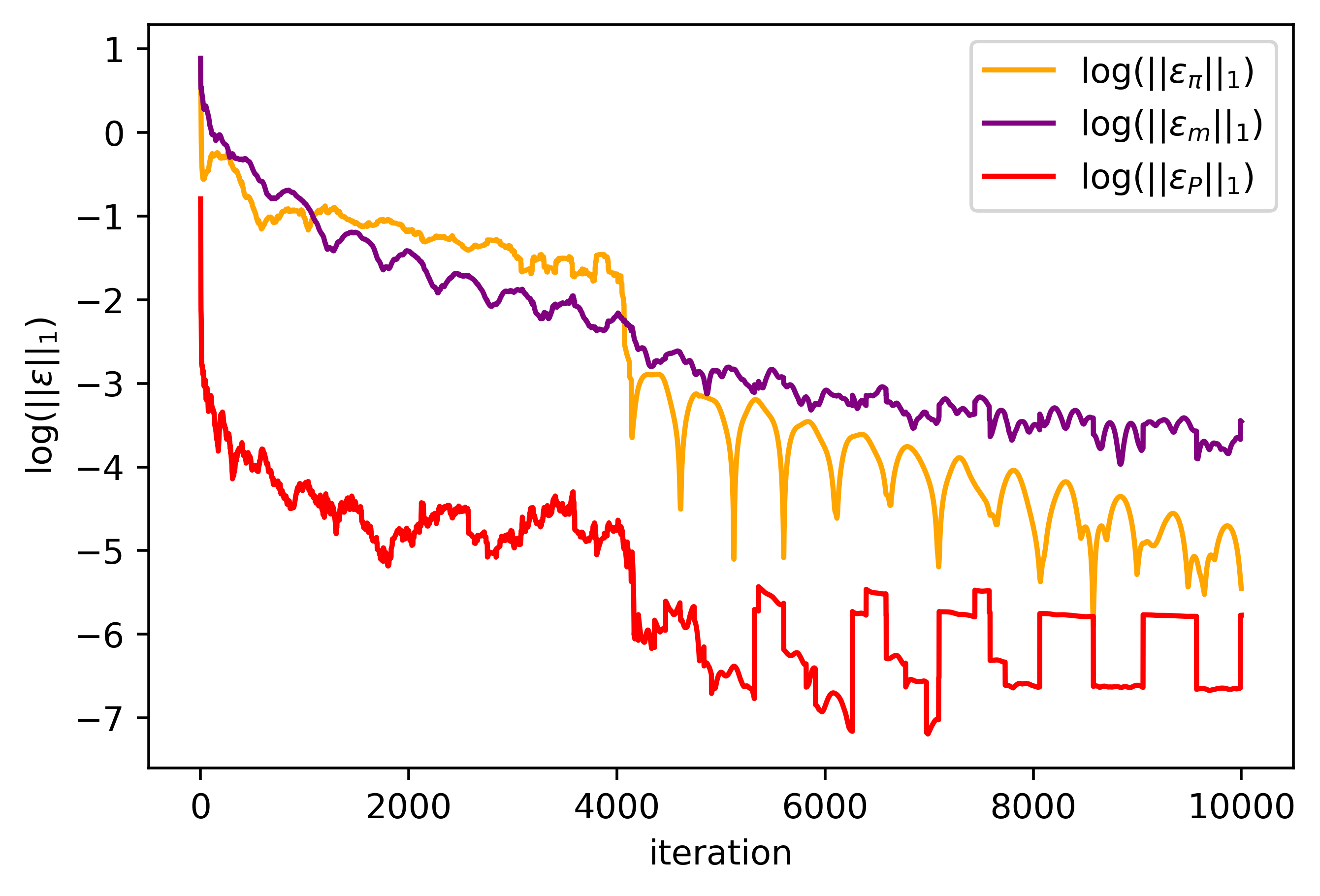

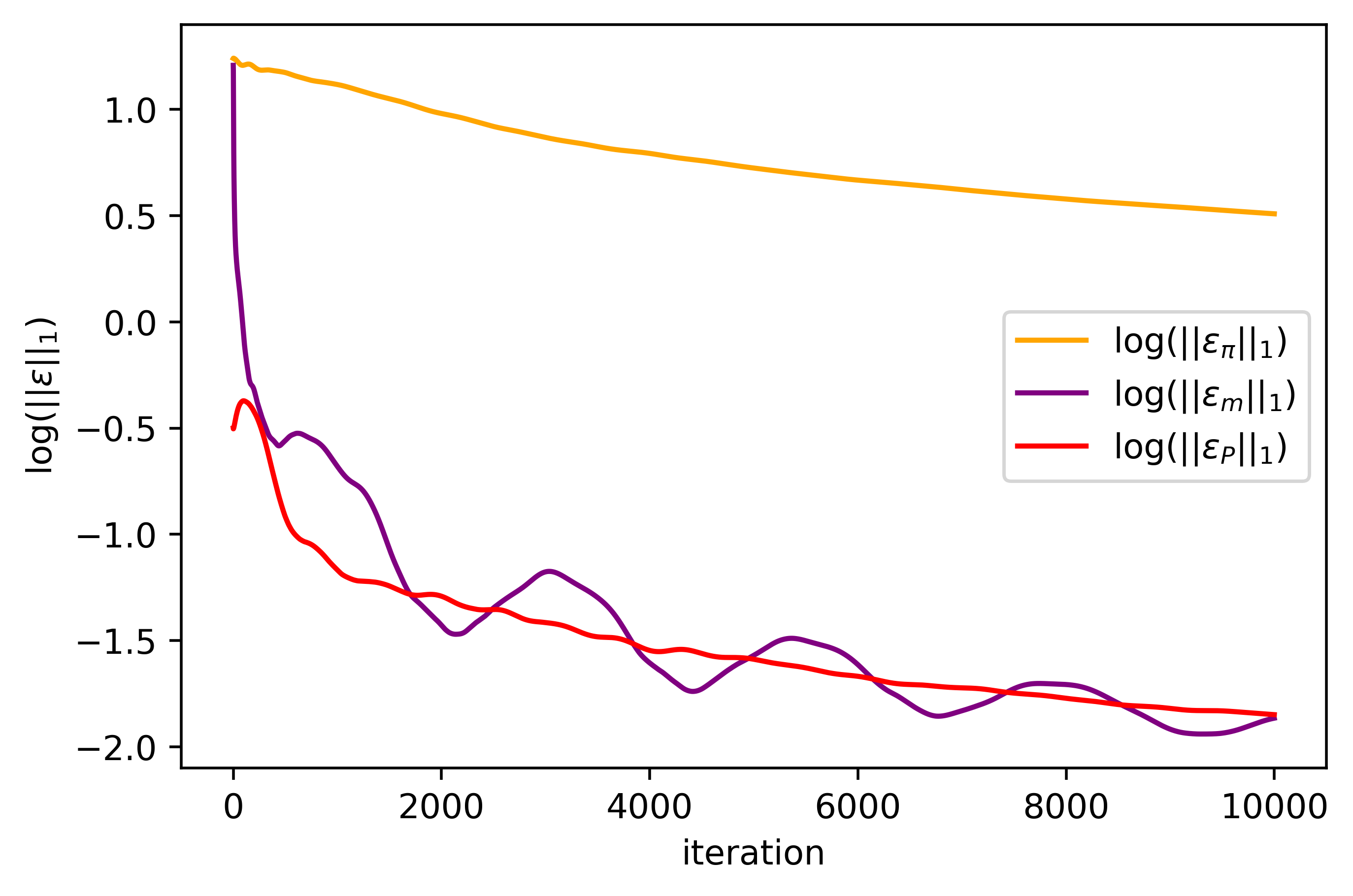

Remark 6.9.

In the following numerical section 7, we plot residuals for ADMM, ADMG, Chambolle-Pock and Chambolle-Pock-Bregman algorithms. The difference in nature of the convergence results (ergodic versus classical) makes the performance comparison between different methods delicate:

- •

-

•

Following Theorem 6.7, we plot the sequence of residuals for ADM-G and ADMM.

7 Numerical Results

In this section we provide two problems that we solve with the algorithms presented in the previous section. We set and we define two scaling coefficients and . We solve two instances of the following scaled system:

| (MFGΔ) |

One can show that this system is connected to two optimization problems of very similar nature as Problems () and (), which can be solved as described previously. For both examples, is defined by

| (33) |

where . Since is linear with respect to , we can interpret as displacement cost from state to state that is fixed (in opposition to the displacement cost induced by that depends on the price). In Appendix A the reader can find detailed computations of the Euclidean projection (20) (Subsection A.1) and the computation of (24) (Subsection A.2) for this particular choice of running cost . The notion of residuals that we use in the following is adapted from Section 6.4 to the scaled system (MFGΔ). In all subsequent graphs, the state space is represented by and the set of time steps by .

7.1 Example 1

In our first example, we take and . We consider a potential of the form , where

| (34) |

and where is given by

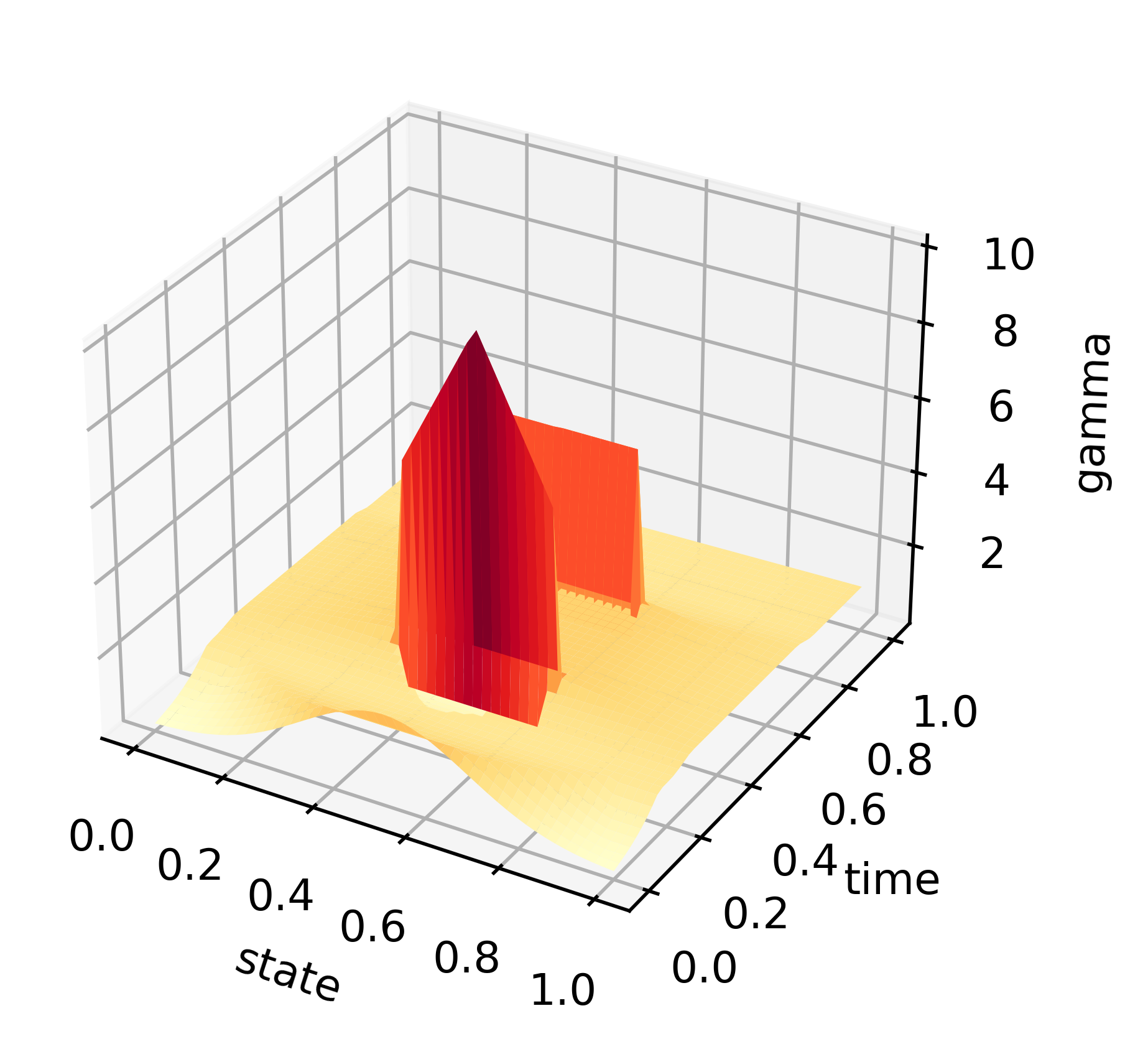

for any . We refer to as the soft congestion term and to as the hard congestion term.

We call narrow region the set of points for which and we call spacious region the set of points for which . In this situation the state of an agent represents its physical location on the interval . Each agent aims at minimizing the displacement cost induced by and avoids congestion as time evolves from time to . The congestion term is linked to by the following relation (see Remark 2.2):

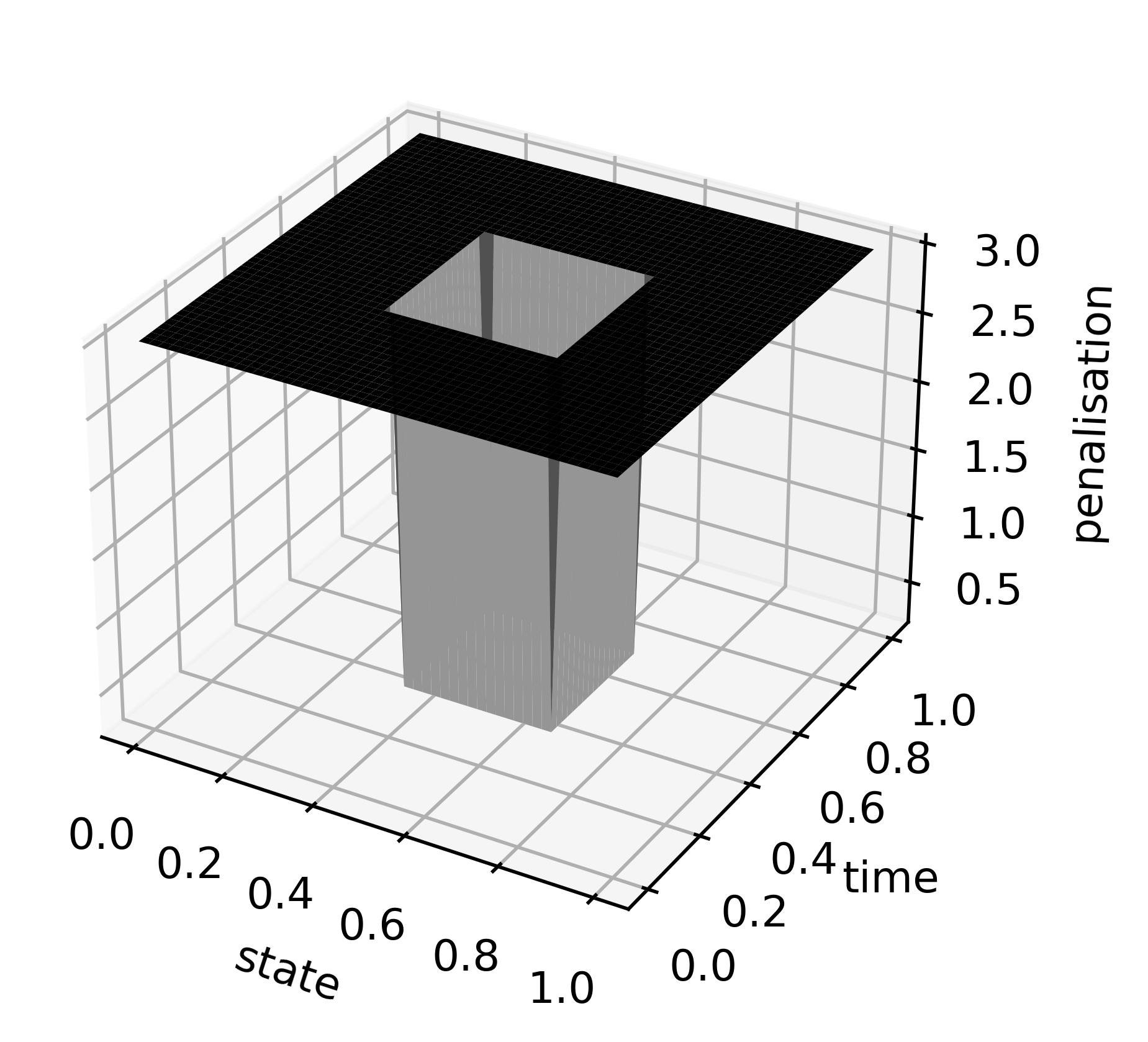

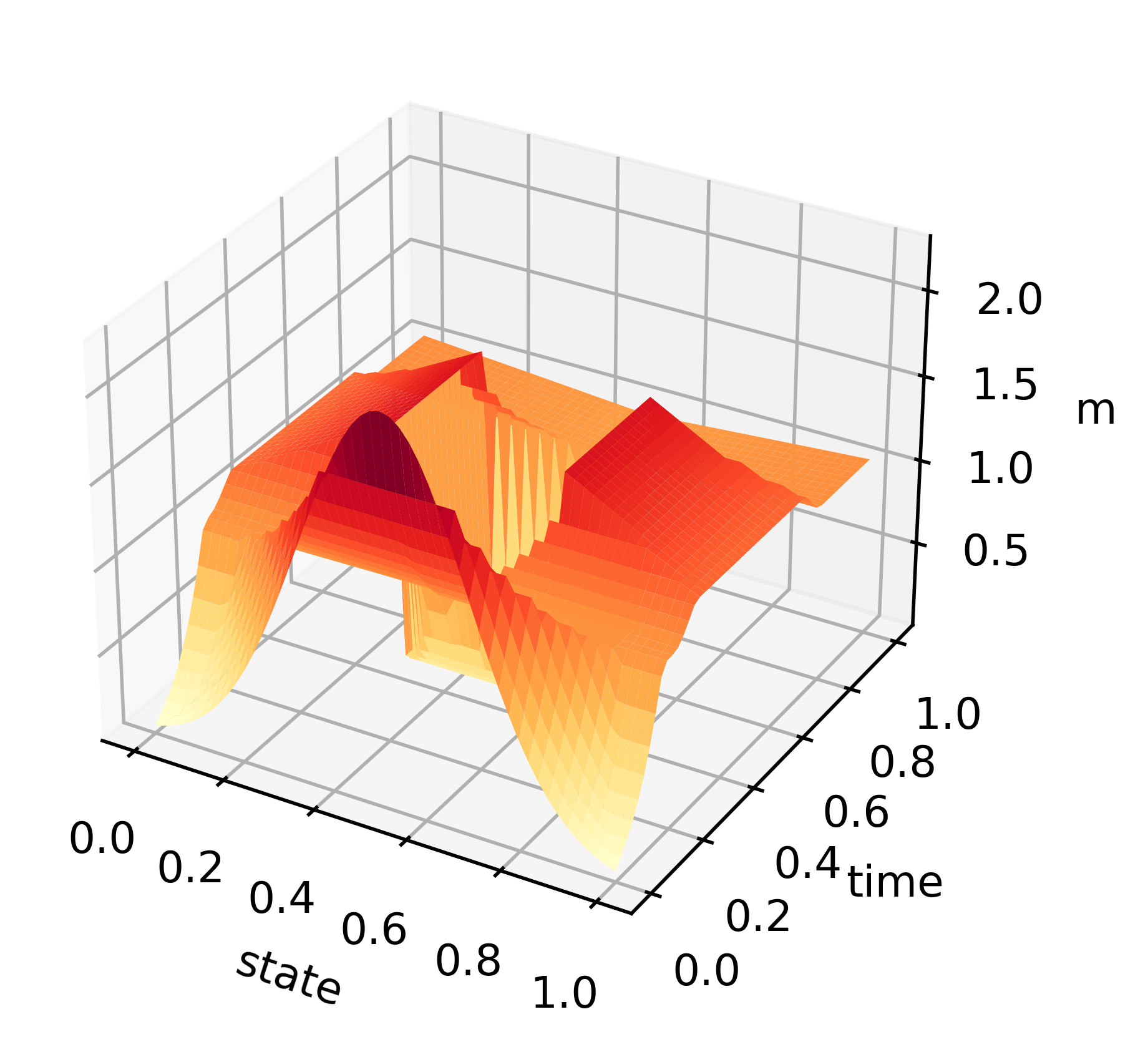

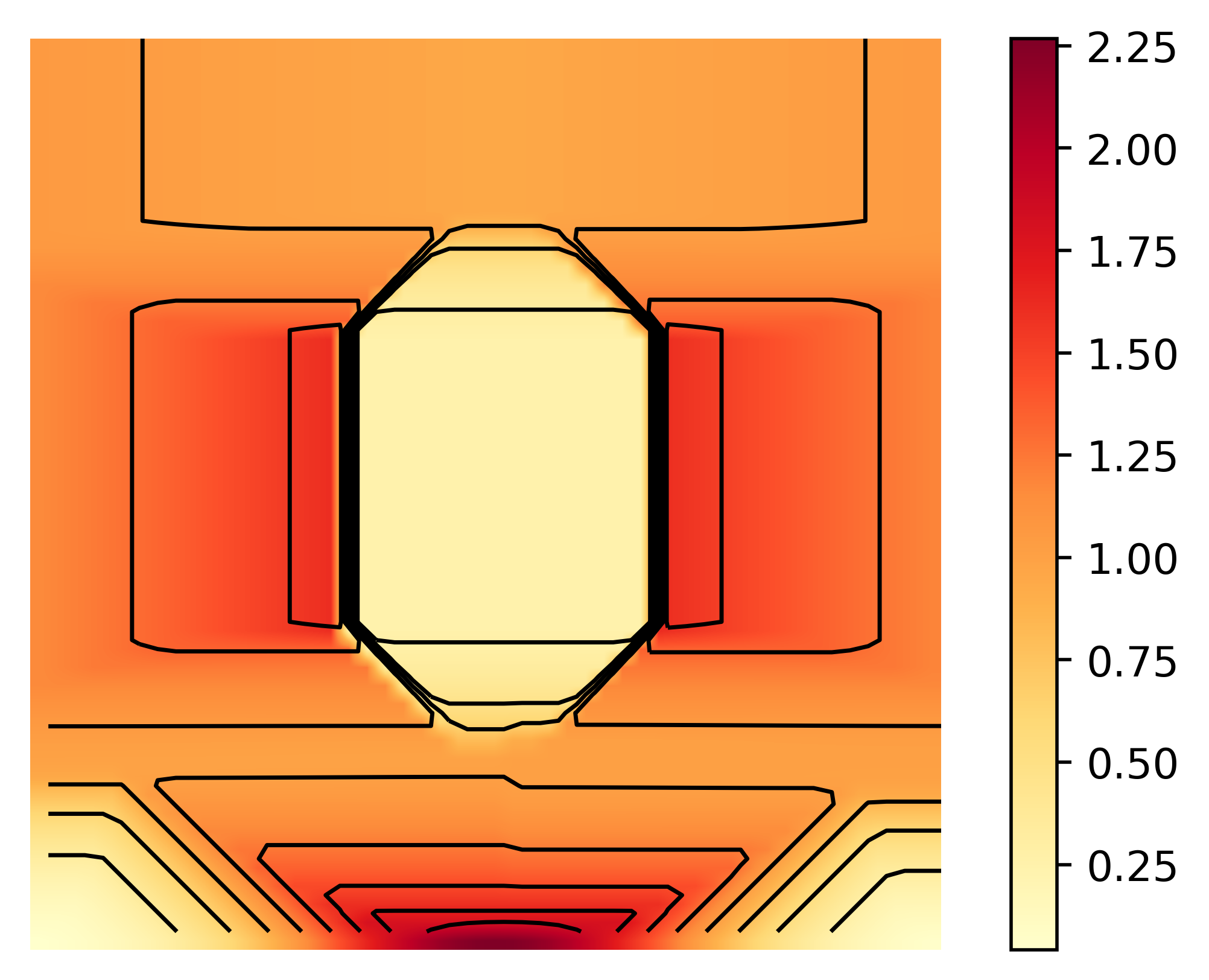

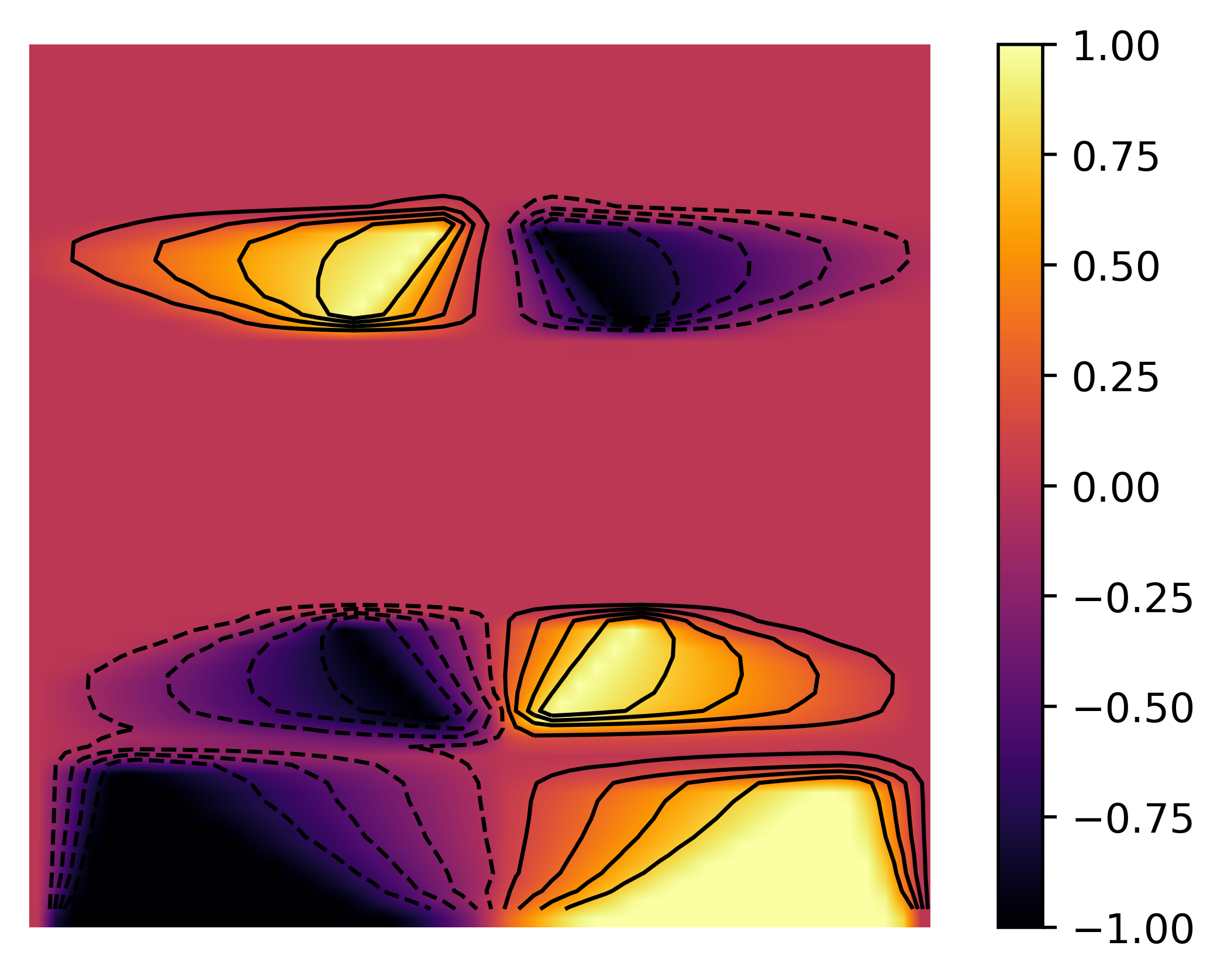

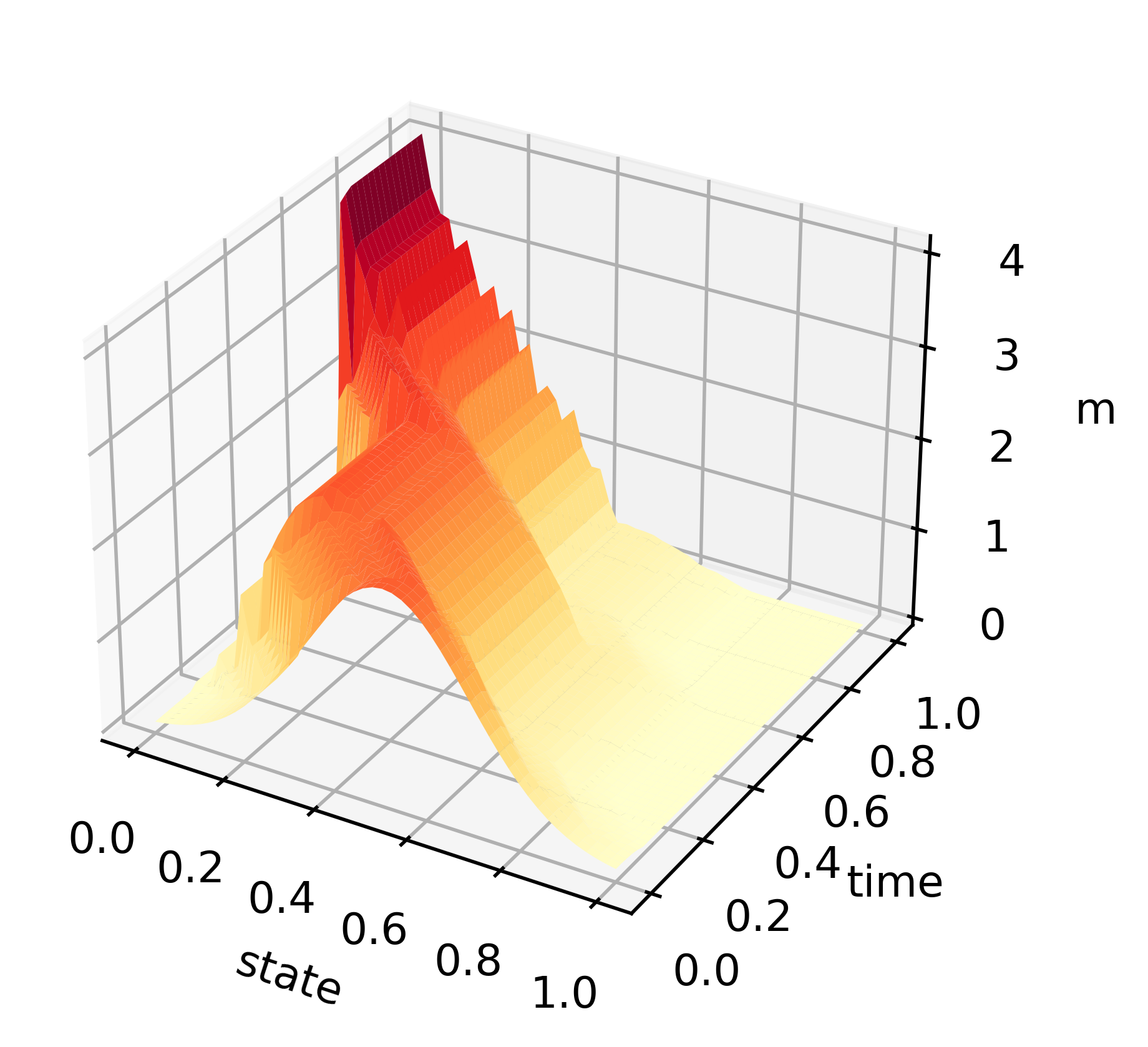

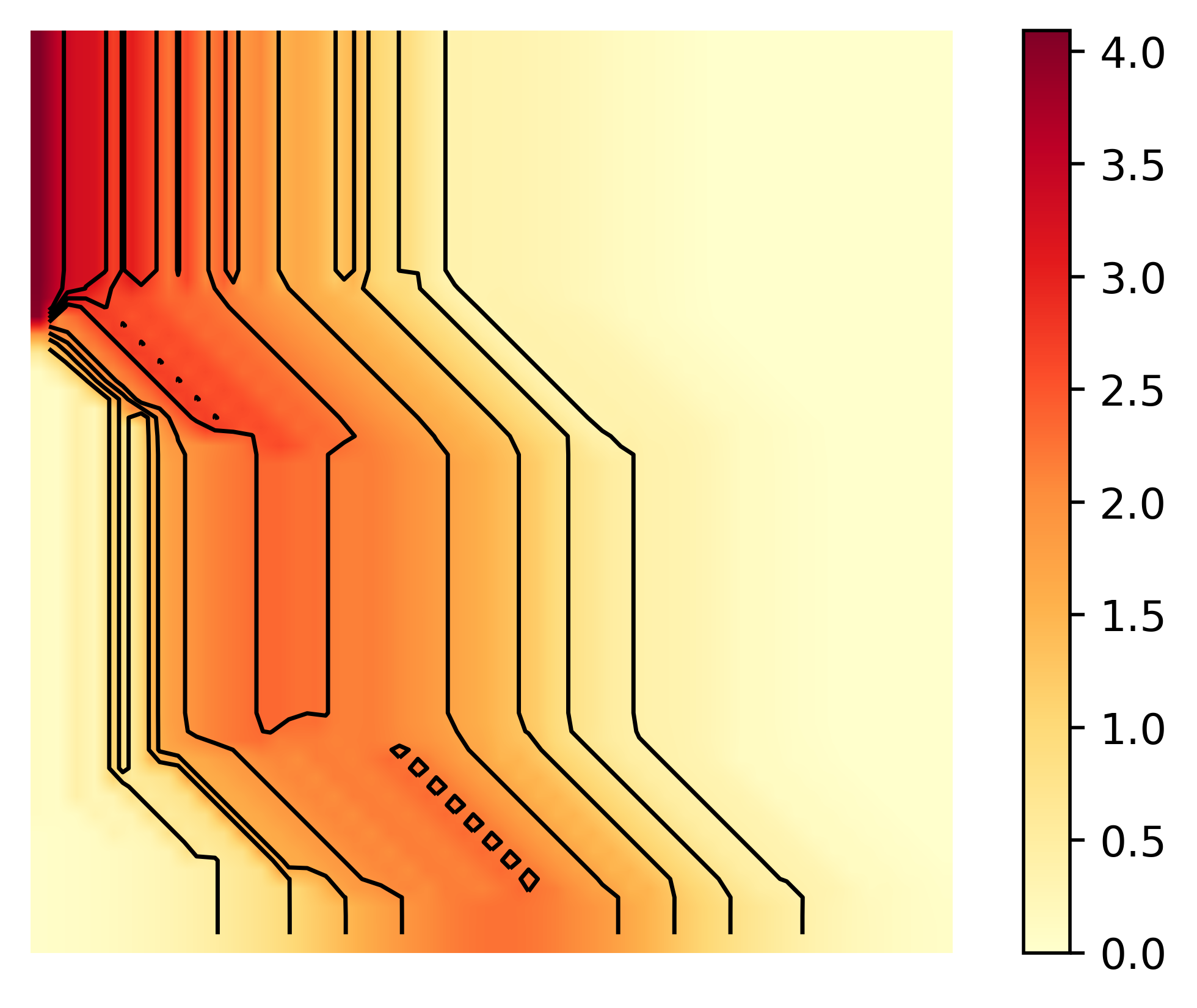

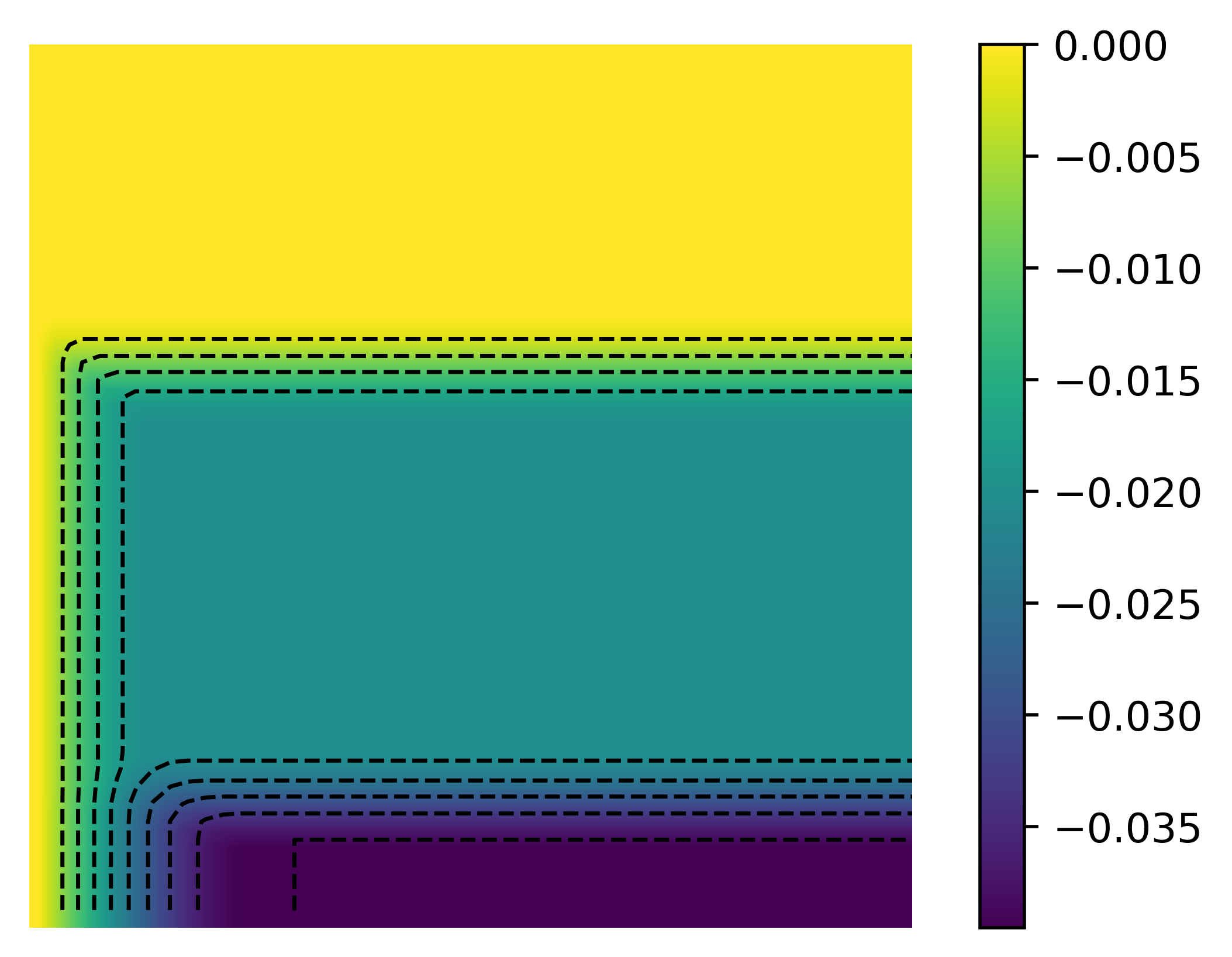

As shown on the graphs below, we have two regimes at equilibrium: in the spacious regions plays the role of a classical congestion term and . In the narrow region the constraint is binding, is such that the constraint is satisfied at the equilibrium and is maximal for the dual problem.

(a) Measure , 3d plot

(a) Measure , 3d plot

(b) Measure , contour plot

(b) Measure , contour plot

(c) Mean displacement , 3d plot

(c) Mean displacement , 3d plot

(d) Mean displacement , contour plot

(d) Mean displacement , contour plot

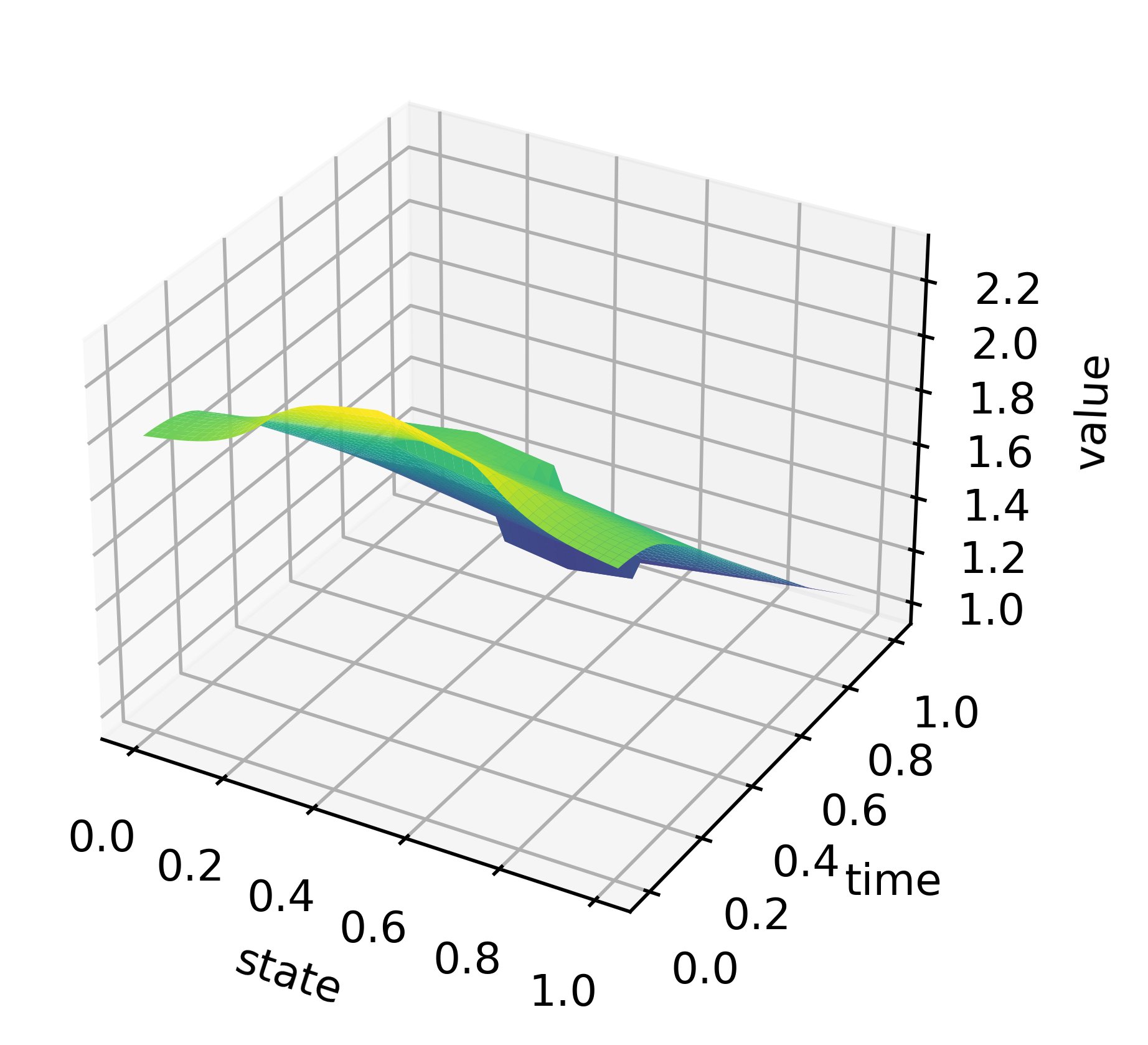

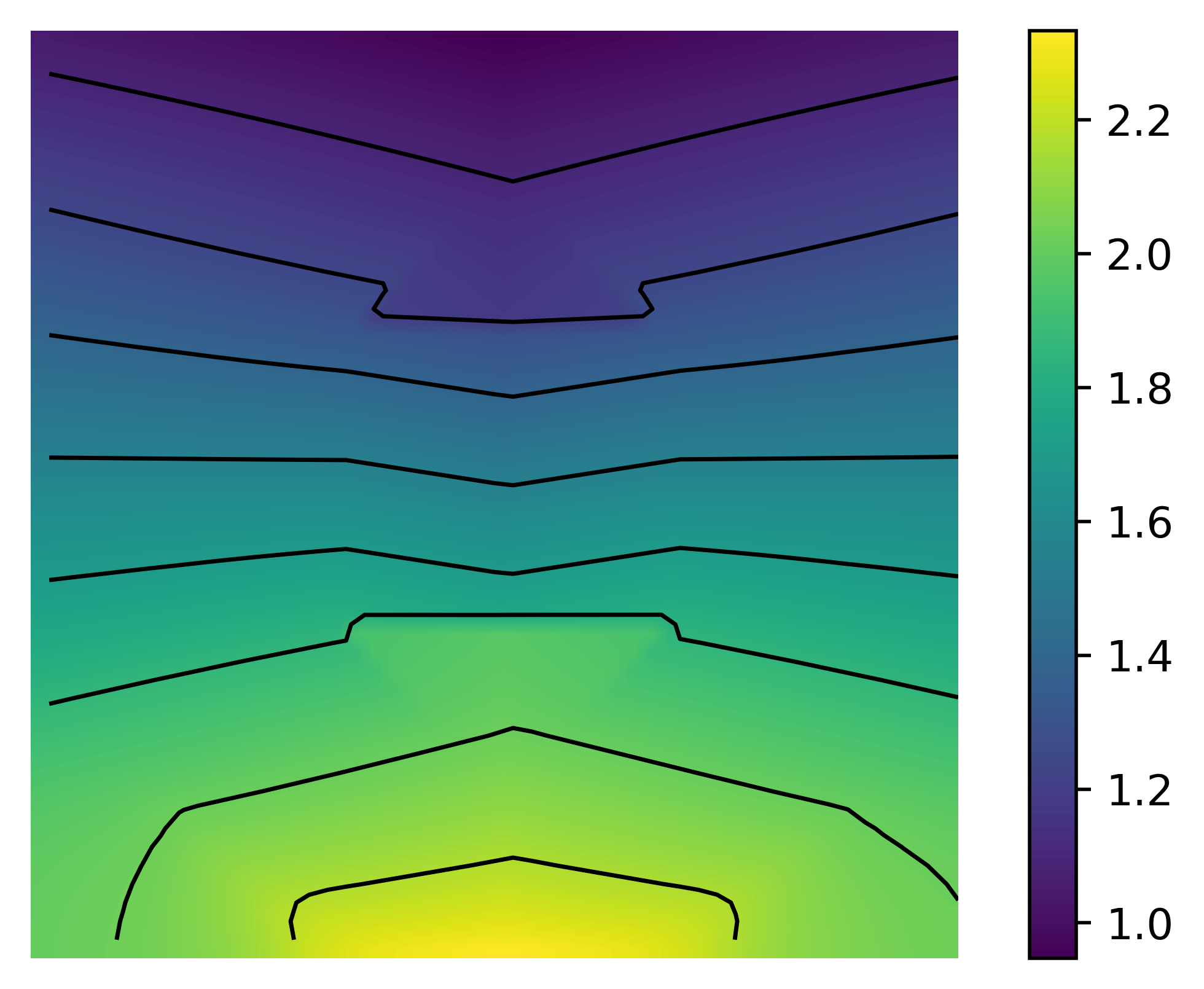

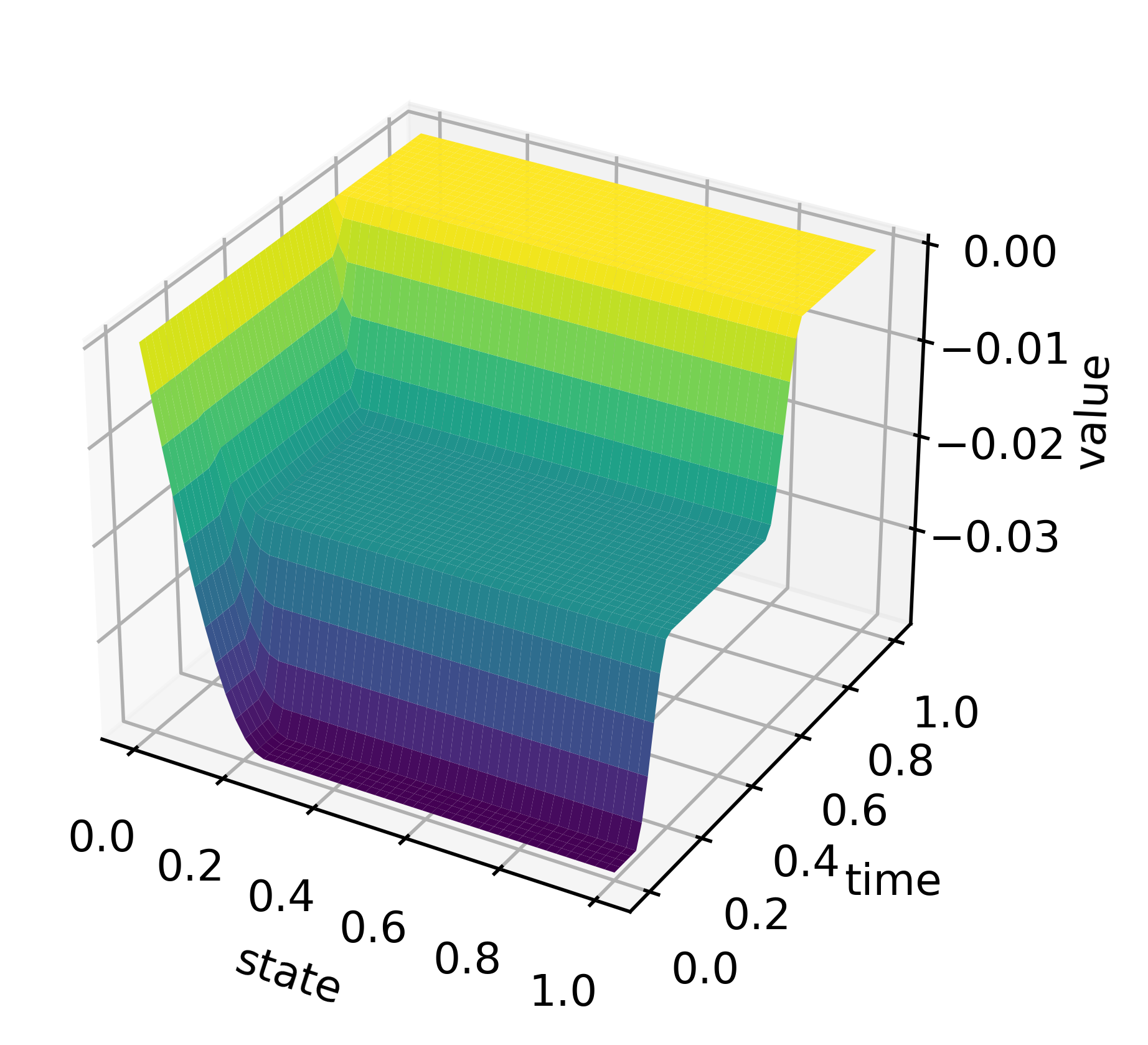

(e) Value function , 3d plot

(e) Value function , 3d plot

(f) Value function , contour plot

(f) Value function , contour plot

(g) Congestion , 3d plot

(g) Congestion , 3d plot

(h) Congestion , contour plot

Figure 2: Solution of Example 1

(h) Congestion , contour plot

Figure 2: Solution of Example 1

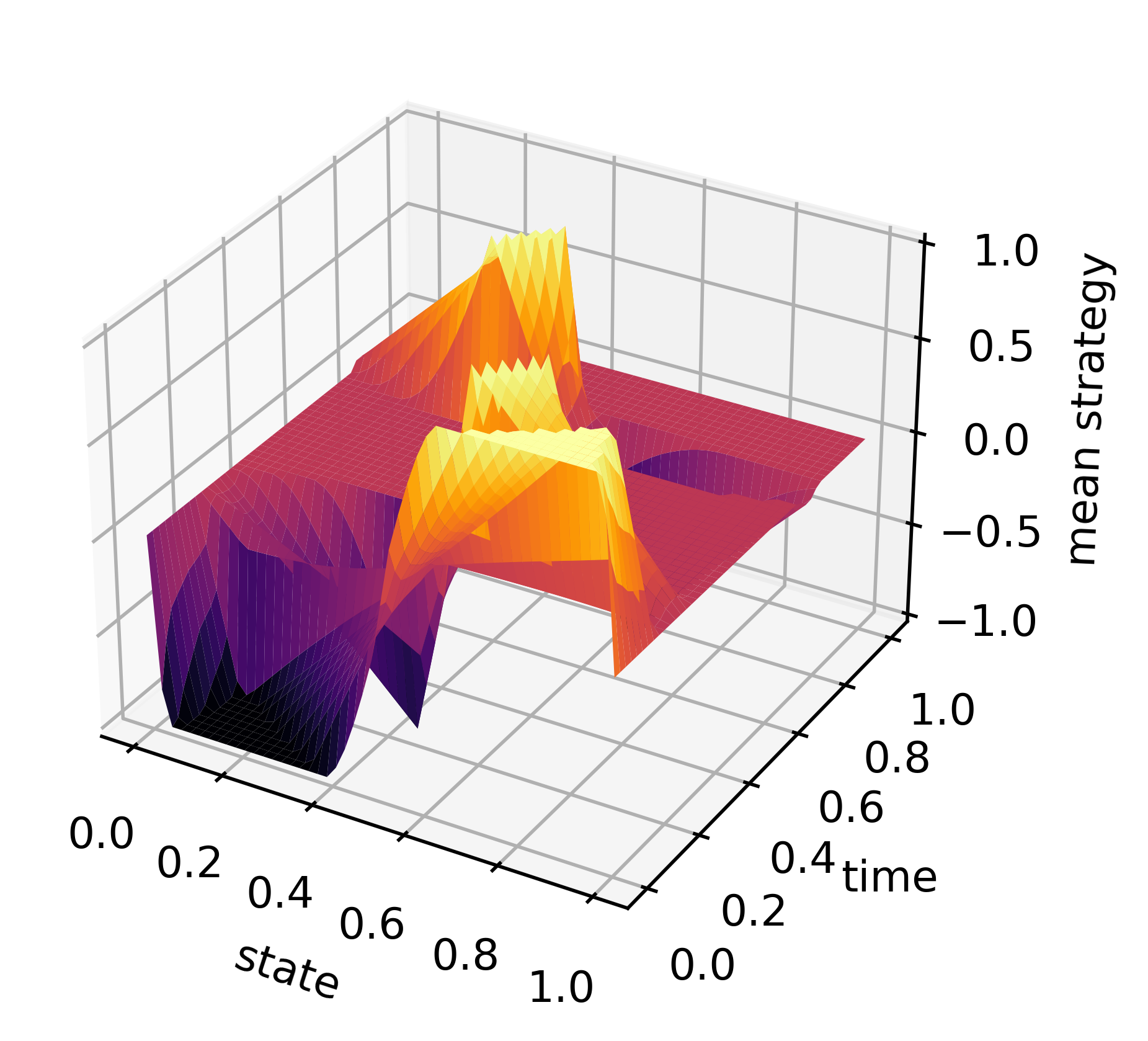

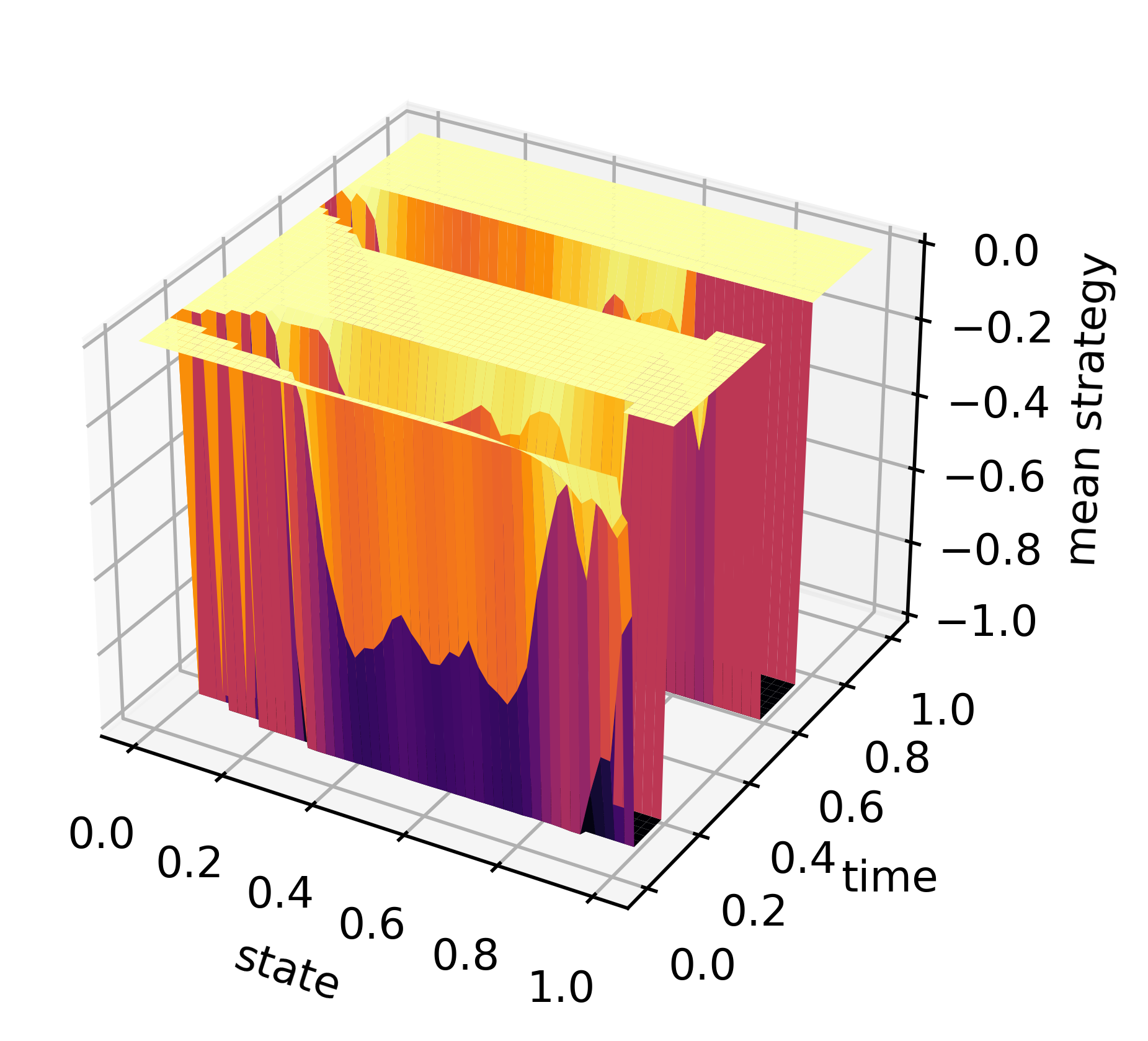

We give a representation of the solution to the mean field system in Figure 2. Since it is hard to give a graphical representation of , we give instead a graph of the mean displacement , defined by

For each variable, a 3D representation of the graph and a 2D representation of the contour plots are provided. For the contour plots, the horizontal axis corresponds to the state space and the vertical axis to the time steps (to be read from the bottom to the top).

Let us comment the results. We start with the interpretation of the measure and the mean displacement . At the beginning of the game, the distribution of players is given by the initial condition . Then the players spread since they are in the spacious region to avoid congestion.

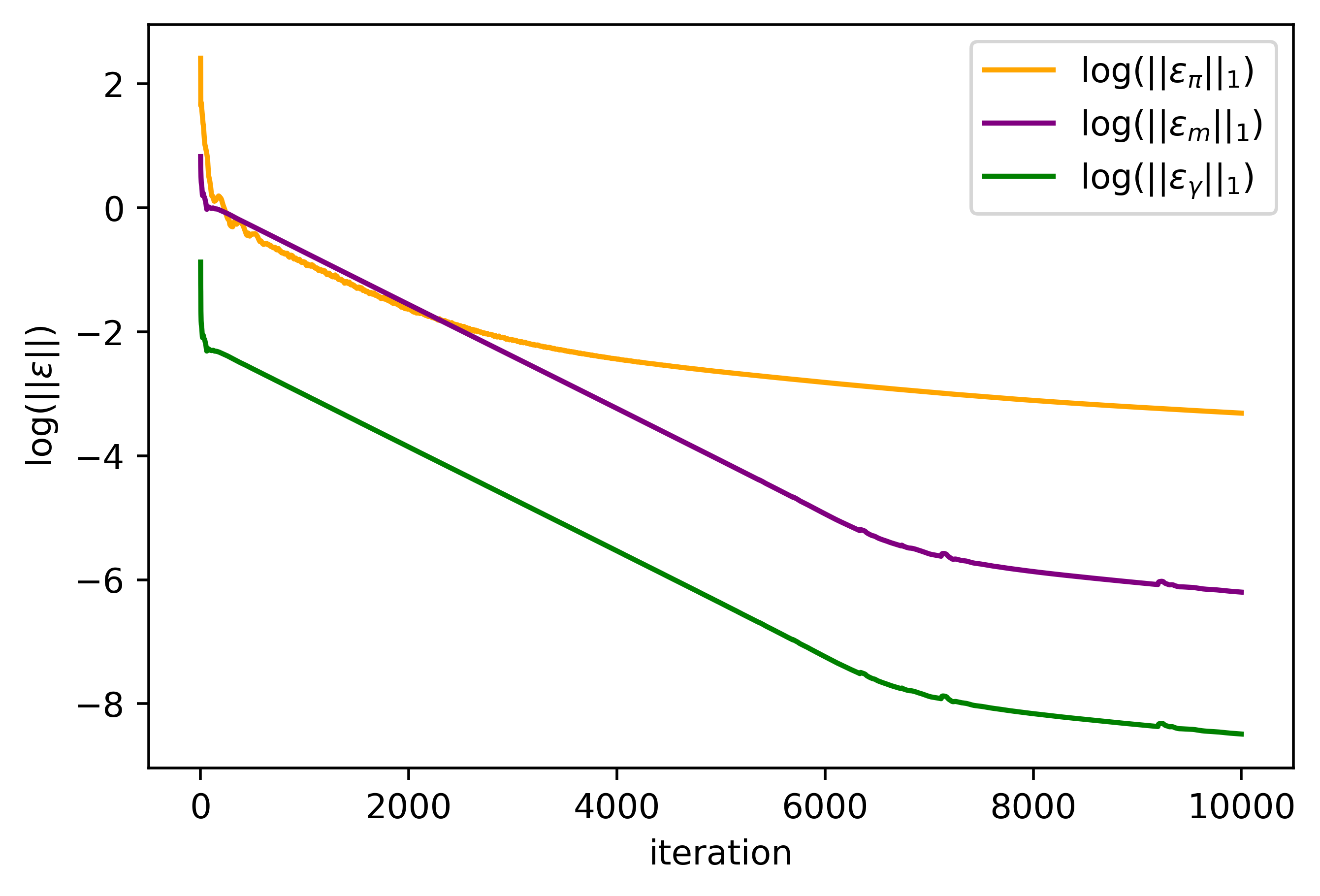

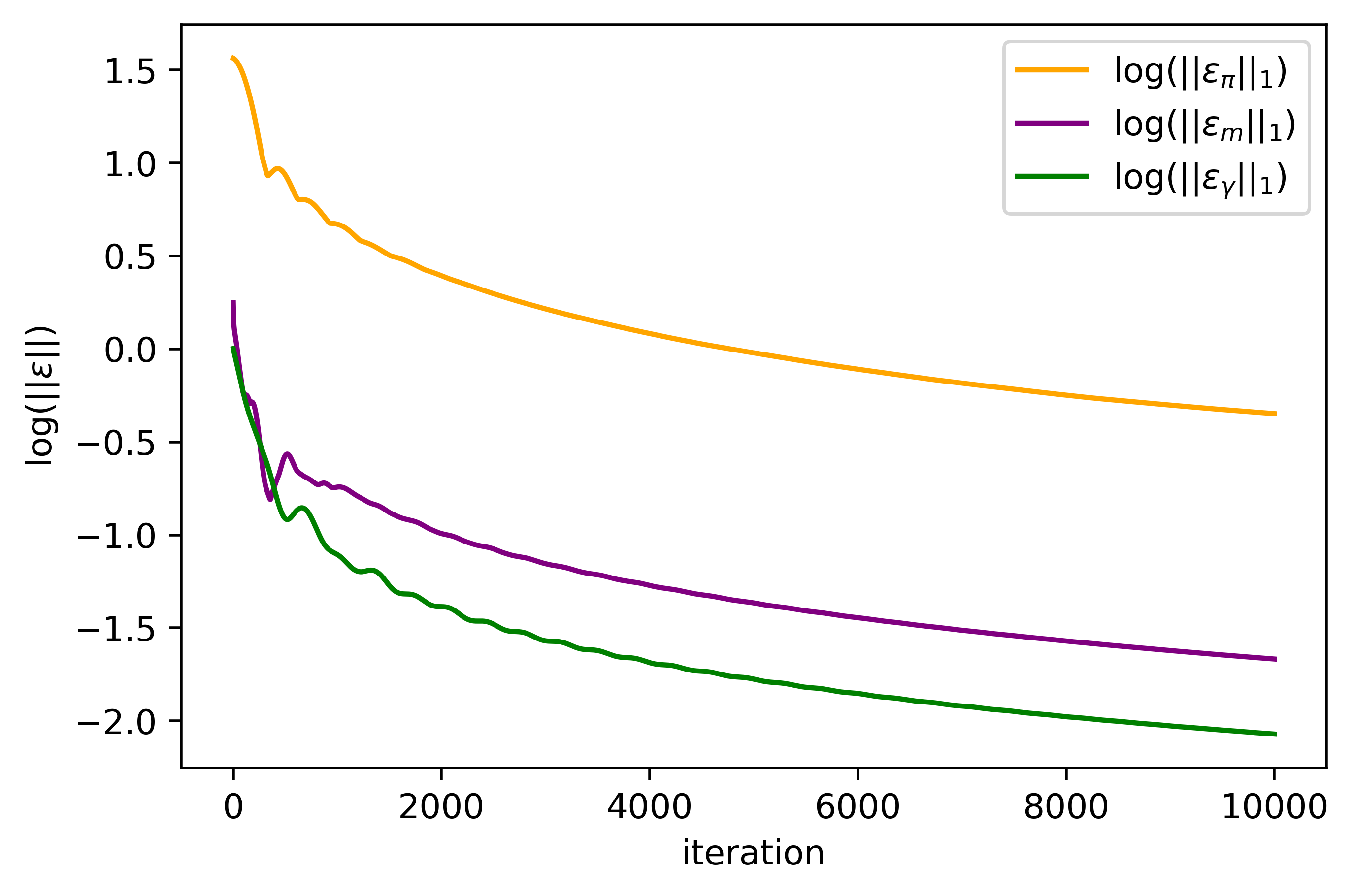

Convergence results

(a) ADMM

(a) ADMM

(b) ADMG

(b) ADMG

(c) Chambolle-Pock

(c) Chambolle-Pock

(d) Chambolle-Pock-Bregman

Figure 3: Errors plots for Example 1

Figure 4 shows the evolution of the error terms in function of the iterations. The execution time of each algorithm is given in the following table.

Chambolle-Pock

Chambolle-Pock-Bregman

ADMM

ADM-G

Time (s)

1600

1300

2000

2000

Figure 4: Execution time of each algorithm for Example 1, with

(d) Chambolle-Pock-Bregman

Figure 3: Errors plots for Example 1

Figure 4 shows the evolution of the error terms in function of the iterations. The execution time of each algorithm is given in the following table.

Chambolle-Pock

Chambolle-Pock-Bregman

ADMM

ADM-G

Time (s)

1600

1300

2000

2000

Figure 4: Execution time of each algorithm for Example 1, with

Thus the mean displacement is negative on the left (black region) and positive on the right (yellow region), around . The distribution becomes uniform after some time. In a second phase, the agents move again towards the border of the state space, anticipating the narrow region. They start their displacement before entering into the narrow region due to their limited speed and displacement cost. Then we are in a stationary regime (purple region), the mean displacement is null and the mass does not vary until the end of the narrow region. At the end of the narrow region, the agents spread again along the state axis and the distribution becomes uniform.

We now interpret the value and the congestion . The value function has to be interpreted backward in time. At the end of the game, the terminal condition imposes that the value is equal to the congestion. Since the congestion is positive and accumulates backward in the value function (which can be seen in the dynamic programming equation), the value function increases backward in time. At the end and at the beginning of the narrow region we observe irregularities in the value function due to the irregularities of the congestion term . But the impact on the value function is limited due to the trade-off between the variables and in the dual problem. At the beginning of the game the value function is higher at the middle of the space because of the initial distribution of players that are accumulated at this point. The congestion term is high enough at the beginning of the narrow region to ensure that the constraint on the distribution of players is satisfied at this point. Then is high enough at the end of the narrow region to ensure that the constraint on the distribution of players is satisfied for all time indices . At the exception of these two moments, plays the role of a classical congestion term.

7.2 Example 2

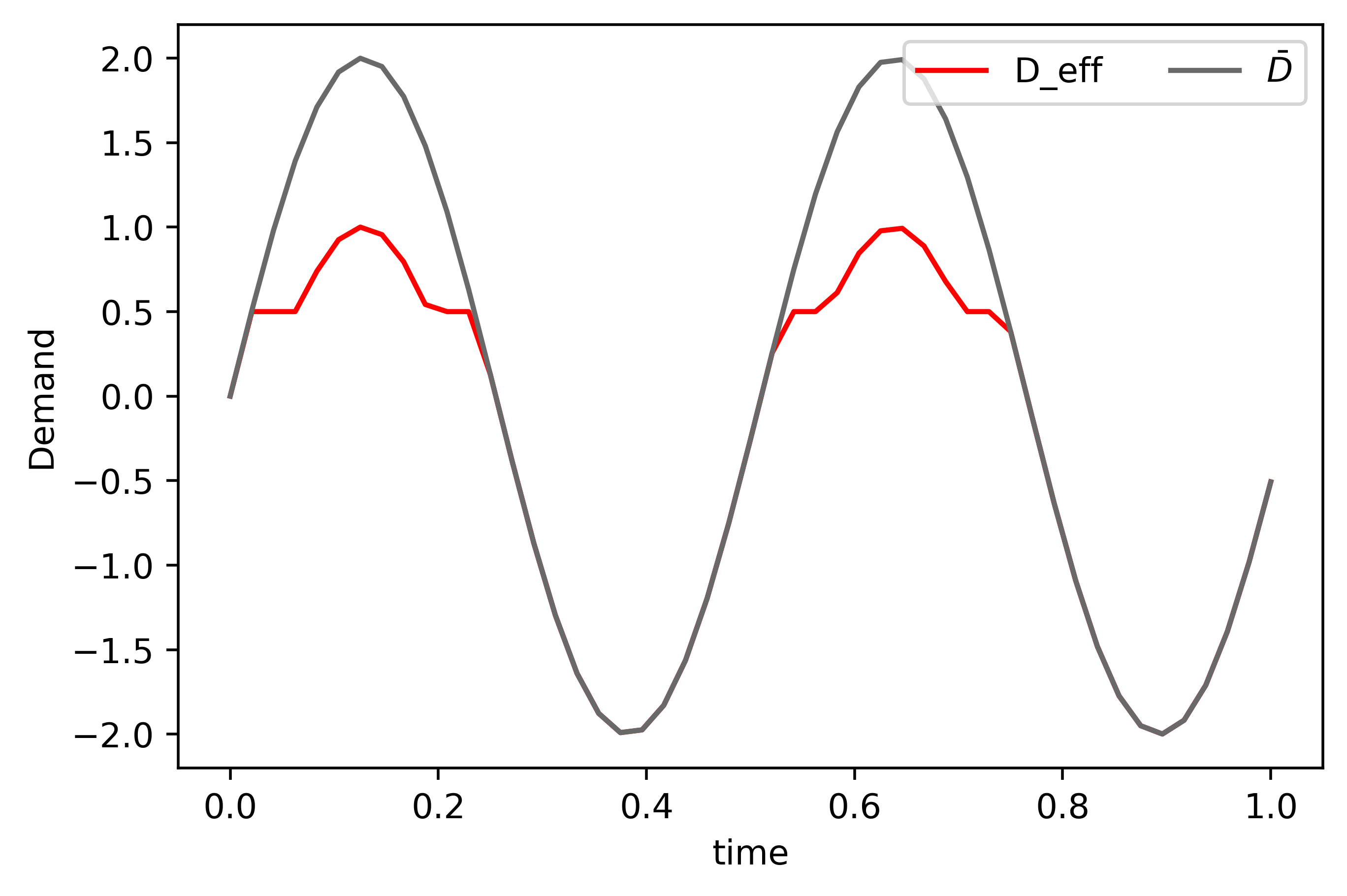

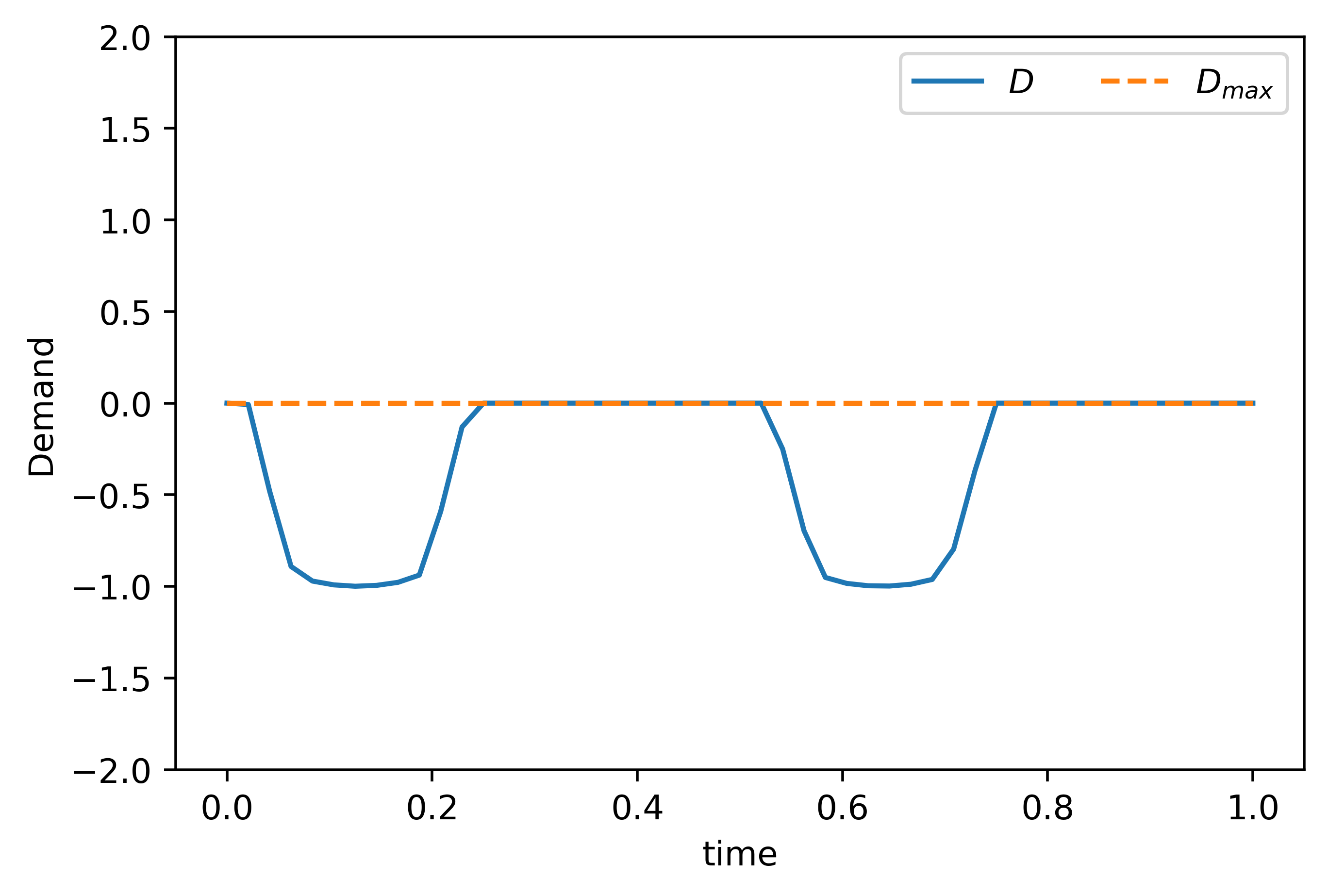

Here we assume that . In this situation the state of an individual agent represents a level of stock. We set ; it represents the quantity bought in order to “move” from to . Therefore the variable (used in the primal problem) is the average quantity which is bought; it has to be understood as a demand, since at equilibrium,

We define the potential , where

The potential is the sum of a convex and differential term with full domain and a convex non-differentiable term . The quantity is a given exogenous quantity which represent a net demand (positive or negative) to be satisfied by the agents. In this example for any and .

Market equilibrium

(a) Exogenous quantity and effective demand

(a) Exogenous quantity and effective demand

(b) Maximal aggregated demand and demand

(b) Maximal aggregated demand and demand

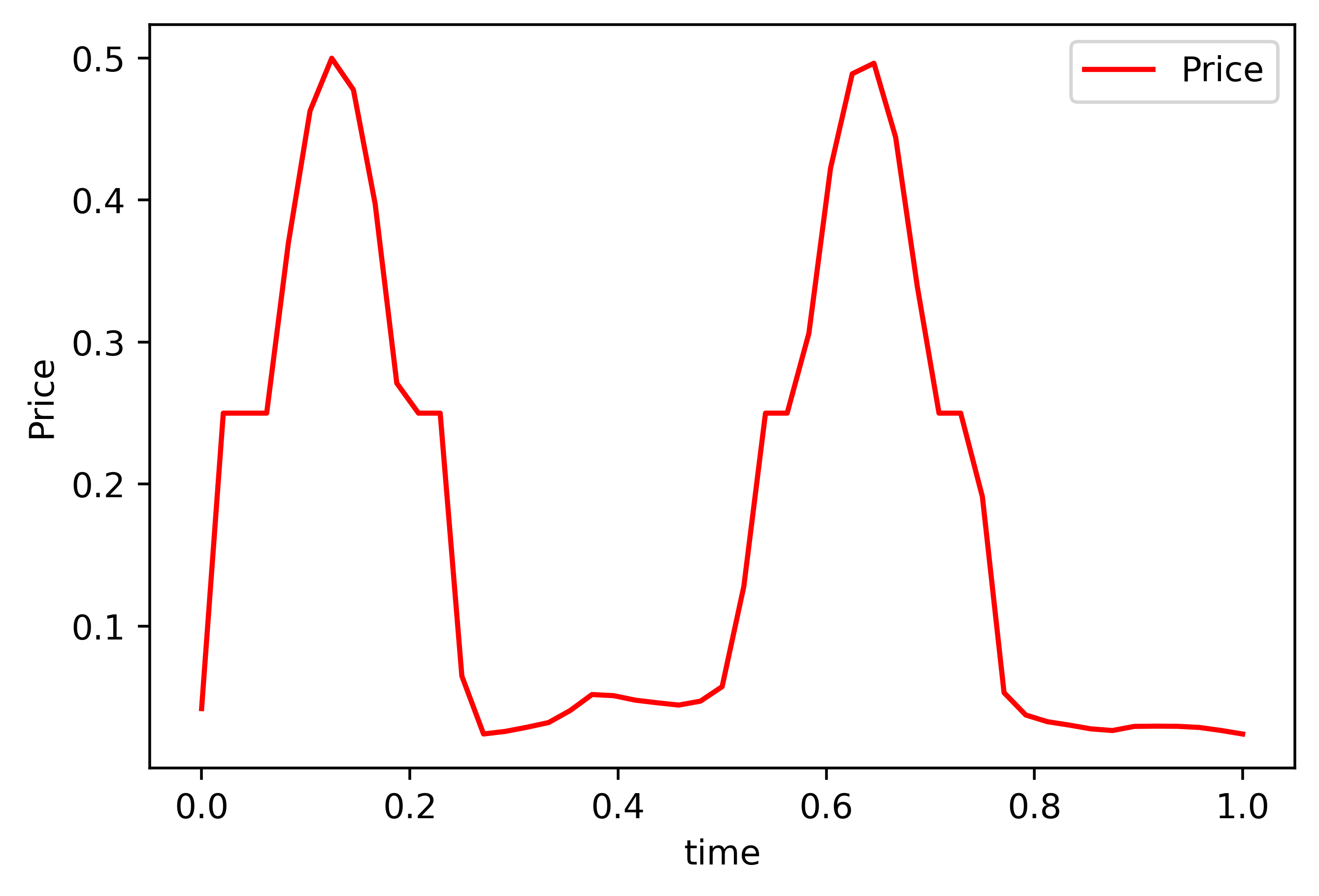

(c) Price

(c) Price

In this situation each agent faces a price and chooses to increase or deplete her stock. The price mechanism is given by

where is called the effective demand and follows two regimes.

(a) Measure , 3d plot

(a) Measure , 3d plot

(b) Measure , contour plot

(b) Measure , contour plot

(c) Mean displacement , 3d plot

(c) Mean displacement , 3d plot

(d) Mean displacement , contour plot

(d) Mean displacement , contour plot

(e) Value function , 3d plot

(e) Value function , 3d plot

(f) Value function , contour plot

Figure 6: Solution of Example 2

(f) Value function , contour plot

Figure 6: Solution of Example 2

When the constraint on the demand is not binding, we are in a soft regime, the price plays the role of a classical price term and is given by . The quantity is an exogenous quantity which can be positive or negative. If the quantity , the exogenous quantity is interpreted as being a demand and the agents have an incentive to deplete their stock to satisfy this demand. If , the exogenous quantity is interpreted as being a supply. In the absence of a hard constraint, the agents would have interest to increase their stock to absorb this supply. When the constraint on the demand is binding, we are in a hard regime and the price plays the role of an adjustment variable so that the constraint is satisfied and is maximal for the dual problem.

In the case where it is not profitable to buy or sell, we have that and thus . This situation occurs when the quantity , since the hard constraint prevents the agents from buying on the market. On the graph this corresponds to the case where the red and the black curves coincide.

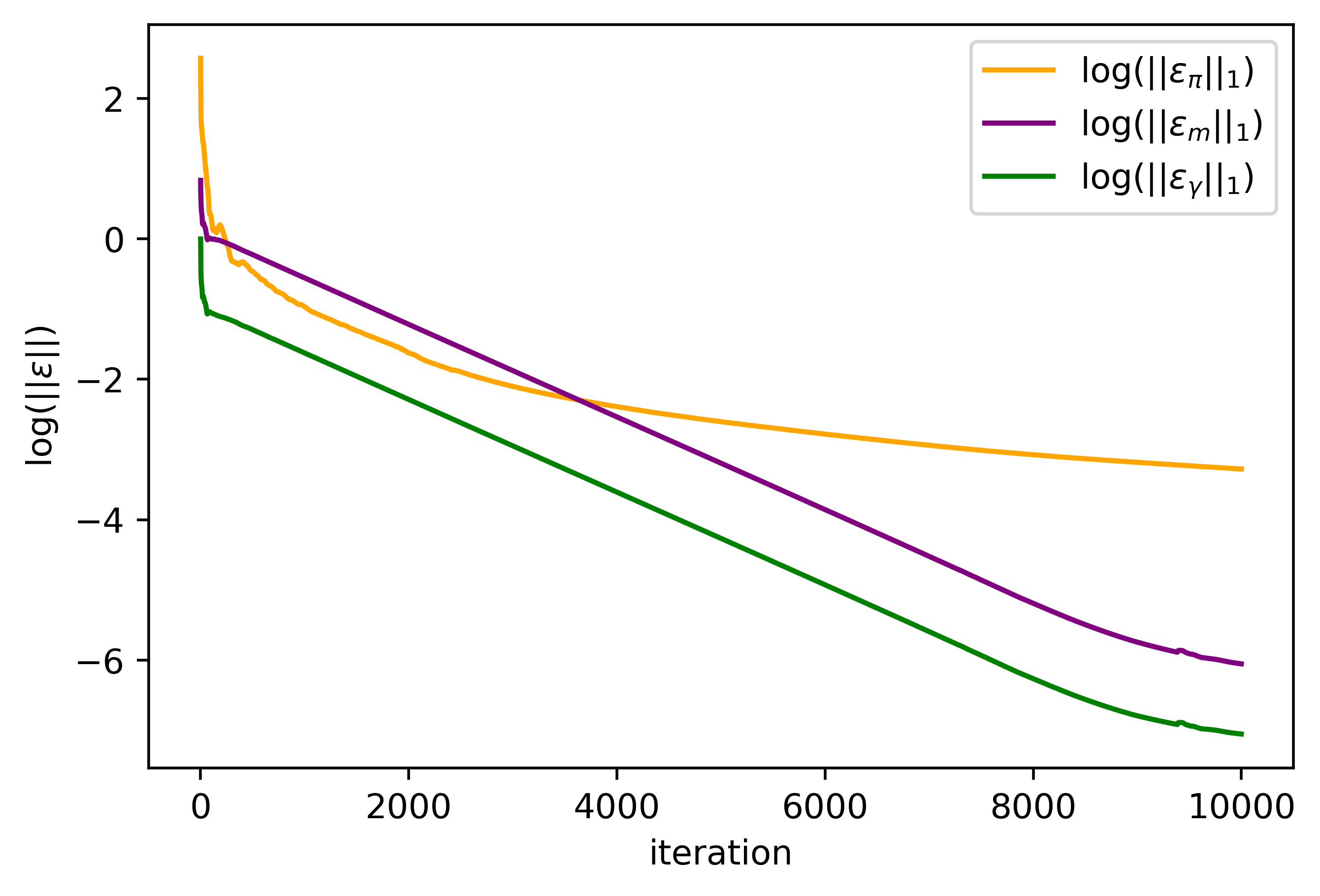

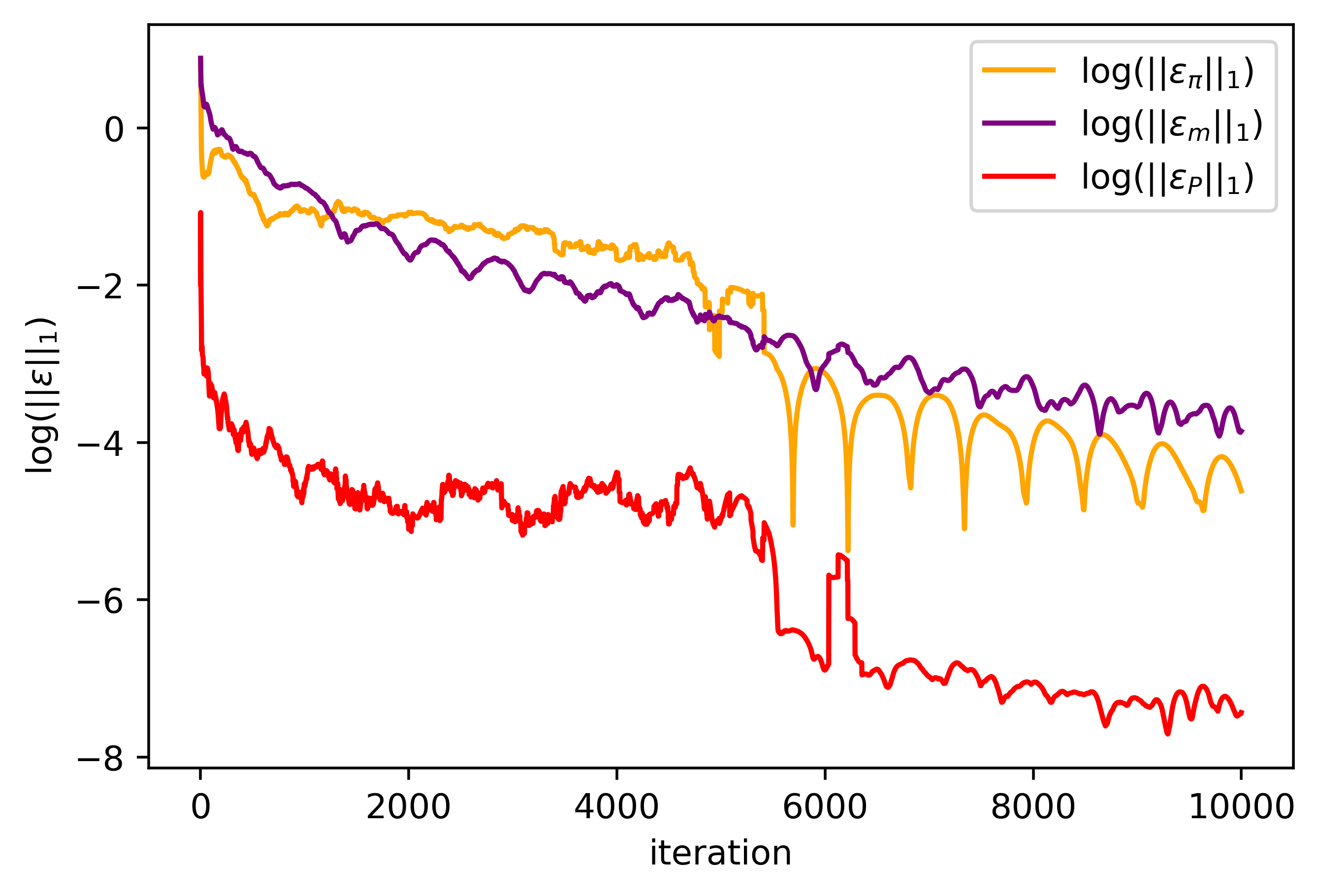

Convergence results

(a) ADMM

(a) ADMM

(b) ADMG

(b) ADMG

(c) Chambolle-Pock

(c) Chambolle-Pock

(d) Chambolle-Pock-Bregman

Figure 7: Errors plots for Example 2

The execution time of each algorithm is given in the following table.

Chambolle-Pock

Chambolle-Pock-Bregman

ADMM

ADM-G

Time (s)

1700

1300

2200

2200

Figure 8: Execution time of each algorithm for Example 2 and

(d) Chambolle-Pock-Bregman

Figure 7: Errors plots for Example 2

The execution time of each algorithm is given in the following table.

Chambolle-Pock

Chambolle-Pock-Bregman

ADMM

ADM-G

Time (s)

1700

1300

2200

2200

Figure 8: Execution time of each algorithm for Example 2 and

When we observe that the red curve is lower than the black curve meaning that a certain amount (given by the blue curve on the following graph) of the demand has been satisfied by the agents. Three effects prevent the agents from fully satisfying the demand: their level of stock, their trading cost and their depletion speed limitation.

At the optimum we observe that the demand is indeed below the threshold , meaning that the constraint is satisfied. We now comment the measure , the mean displacement and the value function . For a given initial distribution of the level of stock, we observe that the measure is shifted to the left with time. This means that the agents deplete their stocks with time. This is consistent with the mean displacement where we observe two regimes: either the agents choose to sell as much as possible or the agents choose not to sell on average. The value function can be interpreted backward. At the end of the game the value is null due to the terminal condition. Then the higher the level of stock, the lower the value function that is to say the value function is increasing in time and decreasing in space. This comes from the definition of and the constraint , which implies that the price is positive.

Appendix A Appendix

We detail here the calculation of the projection on and the non-linear proximity operator in (24), for a running cost of the form

The adaptation to the case where is defined by (33) is straightforward.

A.1 Projection on

We detail the computation of , as it appears in (20) and (29). First notice that the projection is decoupled in space and time, then for any and , we need to compute

where . The corresponding problem is

| (35) |

For any , the solution of the inner minimization problem is given by

Then replacing into (35), the minimization problem is now given by

where . It is now relatively easy to minimize . Let us sort the sequence , that is, let us consider such that . It is obvious that the function is strictly convex and polynomial of degree 2 on each of the intervals , ,…, and . One can identify on which of these intervals a stationary point of exists, by evaluating , for all . Then one can obtain an analytic expresison of the (unique) stationary point , which minimizes . Finally, we have .

A.2 Entropic proximity operator

Here we detail the computation of the solution to (24). For notational purpose we set and . By definition of the running cost , we have that

Problem (24) writes

| subject to: |

To find the solution, we define the following Lagrangian with associated multipliers :

For any , a saddle point of the Lagrangian is given by the following first order conditions,

| (36) |

Case 1: . At time we have that . For any we have that and and by a direct computation we have that

| (37) |

where .

Case 2: . At time we have that . For any we have by a direct computation

| (38) |

where

References

- [1] Yves Achdou, Fabio Camilli, and Italo Capuzzo-Dolcetta. Mean field games: numerical methods for the planning problem. SIAM Journal on Control and Optimization, 50(1):77–109, 2012.

- [2] Yves Achdou and Ziad Kobeissi. Mean field games of controls: Finite difference approximations, 2020.

- [3] Yves Achdou and Mathieu Laurière. Mean Field Games and Applications: Numerical Aspects, pages 249–307. Springer International Publishing, Cham, 2020.

- [4] Heinz H. Bauschke and Patrick L. Combettes. Convex analysis and monotone operator theory in Hilbert spaces, volume 408. Springer, 2011.

- [5] J.-D. Benamou and G. Carlier. Augmented Lagrangian methods for transport optimization, mean field games and degenerate elliptic equations. Journal of Optimization Theory and Applications, 167(1):1–26, 2015.

- [6] Jean-David Benamou and Yann Brenier. A computational fluid mechanics solution to the Monge-Kantorovich mass transfer problem. Numerische Mathematik, 84(3):375–393, 2000.

- [7] Jean-David Benamou, Guillaume Carlier, Simone Di Marino, and Luca Nenna. An entropy minimization approach to second-order variational mean-field games. Mathematical Models and Methods in Applied Sciences, 29(08):1553–1583, 2019.

- [8] Jean-David Benamou, Guillaume Carlier, and Filippo Santambrogio. Variational mean field games. In Active Particles, Volume 1, pages 141–171. Springer, 2017.

- [9] J. Frédéric Bonnans. Convex and Stochastic Optimization. Universitext Series. Springer-Verlag, 2019.

- [10] J. Frédéric Bonnans, Saeed Hadikhanloo, and Laurent Pfeiffer. Schauder estimates for a class of potential mean field games of controls. Applied Mathematics & Optimization, 83(3):1431–1464, 2021.

- [11] J. Frédéric Bonnans and Alexander Shapiro. Perturbation analysis of optimization problems. Springer Science & Business Media, 2000.

- [12] Luis Briceño-Arias, Dante Kalise, Ziad Kobeissi, Mathieu Laurière, A. Mateos González, and Francisco J. Silva. On the implementation of a primal-dual algorithm for second order time-dependent mean field games with local couplings. ESAIM: Proceedings and Surveys, 65:330–348, 2019.

- [13] Luis M. Briceno-Arias, Dante Kalise, and Francisco J. Silva. Proximal methods for stationary mean field games with local couplings. SIAM Journal on Control and Optimization, 56(2):801–836, 2018.

- [14] Pierre Cardaliaguet, P. Jameson Graber, Alessio Porretta, and Daniela Tonon. Second order mean field games with degenerate diffusion and local coupling. Nonlinear Differential Equations and Applications NoDEA, 22(5):1287–1317, 2015.

- [15] Pierre Cardaliaguet and Saeed Hadikhanloo. Learning in mean field games: The fictitious play. ESAIM: Control, Optimisation and Calculus of Variations, 23(2):569–591, 2017.

- [16] Pierre Cardaliaguet, Alpár R. Mészáros, and Filippo Santambrogio. First order mean field games with density constraints: pressure equals price. SIAM Journal on Control and Optimization, 54(5):2672–2709, 2016.

- [17] Antonin Chambolle and Thomas Pock. A first-order primal-dual algorithm for convex problems with applications to imaging. Journal of mathematical imaging and vision, 40(1):120–145, 2011.

- [18] Antonin Chambolle and Thomas Pock. On the ergodic convergence rates of a first-order primal–dual algorithm. Mathematical Programming, 159(1):253–287, 2016.

- [19] Y.T. Chow, W. Li, S. Osher, and W. Yin. Algorithm for Hamilton–Jacobi equations in density space via a generalized Hopf formula. Journal of Scientific Computing, 80(2):1195–1239, 2019.

- [20] Patrick L. Combettes. Perspective functions: Properties, constructions, and examples. Set-Valued and Variational Analysis, 26(2):247–264, 2018.

- [21] Matthias Erbar, Martin Rumpf, Bernhard Schmitzer, and Stefan Simon. Computation of optimal transport on discrete metric measure spaces. Numerische Mathematik, 144(1):157–200, 2020.

- [22] Daniel Gabay and Bertrand Mercier. A dual algorithm for the solution of nonlinear variational problems via finite element approximation. Computers & mathematics with applications, 2(1):17–40, 1976.

- [23] Matthieu Geist, Julien Pérolat, Mathieu Laurière, Romuald Elie, Sarah Perrin, Olivier Bachem, Rémi Munos, and Olivier Pietquin. Concave utility reinforcement learning: the mean-field game viewpoint. arXiv preprint arXiv:2106.03787, 2021.

- [24] Roland Glowinski and Americo Marroco. Sur l’approximation, par éléments finis d’ordre un, et la résolution, par pénalisation-dualité d’une classe de problèmes de dirichlet non linéaires. ESAIM: Mathematical Modelling and Numerical Analysis-Modélisation Mathématique et Analyse Numérique, 9(R2):41–76, 1975.

- [25] Diogo A. Gomes, Joana Mohr, and Rafael Rigao Souza. Discrete time, finite state space mean field games. Journal de mathématiques pures et appliquées, 93(3):308–328, 2010.

- [26] Diogo A. Gomes and Joao Saude. A mean-field game approach to price formation. Dynamic Games and Applications, pages 1–25, 2020.

- [27] P. Jameson Graber and Alain Bensoussan. Existence and uniqueness of solutions for Bertrand and Cournot mean field games. Applied Mathematics & Optimization, pages 1–25, 2015.

- [28] P. Jameson Graber, Vincenzo Ignazio, and Ariel Neufeld. Nonlocal Bertrand and Cournot mean field games with general nonlinear demand schedule. Journal de Mathématiques Pures et Appliquées, 148:150–198, 2021.

- [29] P. Jameson Graber and Charafeddine Mouzouni. Variational mean field games for market competition. In PDE models for multi-agent phenomena, pages 93–114. Springer, 2018.

- [30] P. Jameson Graber, Alan Mullenix, and Laurent Pfeiffer. Weak solutions for potential mean field games of controls. Nonlinear Differential Equations and Applications NoDEA, 28(5):1–34, 2021.

- [31] Saeed Hadikhanloo and Francisco J Silva. Finite mean field games: fictitious play and convergence to a first order continuous mean field game. Journal de Mathématiques Pures et Appliquées, 132:369–397, 2019.

- [32] Bingsheng He, Min Tao, and Xiaoming Yuan. Alternating direction method with gaussian back substitution for separable convex programming. SIAM Journal on Optimization, 22(2):313–340, 2012.

- [33] Minyi Huang, Roland P. Malhamé, and Peter E. Caines. Large population stochastic dynamic games: closed-loop McKean-Vlasov systems and the Nash certainty equivalence principle. Communications in Information & Systems, 6(3):221–252, 2006.

- [34] Jean-Michel Lasry and Pierre-Louis Lions. Jeux à champ moyen. i–le cas stationnaire. Comptes Rendus Mathématique, 343(9):619–625, 2006.

- [35] Jean-Michel Lasry and Pierre-Louis Lions. Jeux à champ moyen. ii–horizon fini et contrôle optimal. Comptes Rendus Mathématique, 343(10):679–684, 2006.

- [36] Jean-Michel Lasry and Pierre-Louis Lions. Mean field games. Japanese journal of mathematics, 2(1):229–260, 2007.

- [37] Alpár Richárd Mészáros and Francisco J. Silva. A variational approach to second order mean field games with density constraints: the stationary case. Journal de Mathématiques Pures et Appliquées, 104(6):1135–1159, 2015.

- [38] Adam Prosinski and Filippo Santambrogio. Global-in-time regularity via duality for congestion-penalized mean field games. Stochastics, 89(6-7):923–942, 2017.

- [39] R. Tyrrell Rockafellar. Level sets and continuity of conjugate convex functions. Transactions of the American Mathematical Society, 123(1):46–63, 1966.

- [40] R. Tyrrell Rockafellar. Convex analysis, volume 36. Princeton university press, 1970.

- [41] Filippo Santambrogio. A modest proposal for MFG with density constraints. Networks & Heterogeneous Media, 7(2):337–347, 2012.

- [42] Filippo Santambrogio. Crowd motion and evolution PDEs under density constraints. ESAIM: Proceedings and Surveys, 64:137–157, 2018.