A Numerical Approach to Pricing Exchange Options under Stochastic Volatility and Jump-Diffusion Dynamics

A Numerical Approach to Pricing Exchange Options under Stochastic Volatility and Jump-Diffusion Dynamics

Abstract.

We consider a method of lines (MOL) approach to determine prices of European and American exchange options when underlying asset prices are modelled with stochastic volatility and jump-diffusion dynamics. As the MOL, as with any other numerical scheme for PDEs, becomes increasingly complex when higher dimensions are involved, we first simplify the problem by transforming the exchange option into a call option written on the ratio of the yield processes of the two assets. This is achieved by taking the second asset yield process as the numéraire. We also characterize the near-maturity behavior of the early exercise boundary of the American exchange option and analyze how model parameters affect this behavior. Using the MOL scheme, we conduct a numerical comparative static analysis of exchange option prices with respect to the model parameters and investigate the impact of stochastic volatility and jumps to option prices. We also consider the effect of boundary conditions at far-but-finite limits of the computational domain on the overall efficiency of the MOL scheme. Toward these objectives, a brief exposition of the MOL and how it can be implemented on computing software are provided.

Key words and phrases:

Exchange options, Jump diffusion processes, Method of lines, Put-call transformation, Stochastic volatility1. Introduction

We investigate the pricing of European and American exchange options written on assets with prices driven by stochastic volatility and jump-diffusion (SVJD) dynamics. The earliest analysis of European exchange options was that of Margrabe (1978) who, by noting that the European exchange option price is linear homogeneous in the stock prices, transformed the problem to the classical European call option pricing problem which was then solved using the method of Black and Scholes (1973). Bjerskund and Stensland (1993) considered a similar approach in pricing American exchange options in a pure diffusion setting. They suggested that by choosing one of the stocks as the numéraire, the American exchange option pricing problem may be simplified to the problem of pricing an American call or put option. Bjerskund and Stensland (1993) refer to this technique as the put-call transformation.

With well-established evidence pointing to the deficiencies of the geometric Brownian motion in accurately modelling asset price returns, there has since been a movement to study option prices (including exchange options) under alternative asset price models.111The empirical literature addressing the limitations of the Black and Scholes (1973) is extremely rich and will not be reviewed here. Instead, we invite the reader to consult Bakshi, Cao, and Chen (1997), Duffie, Pan, and Singleton (2000), Cont (2001), Andersen, Benzoni, and Lund (2002), Chernov et al. (2003), Eraker, Johannes, and Polson (2003), Kou (2008), and the references therein. Cheang, Chiarella, and Ziogas (2006), Cheang and Chiarella (2011), Caldana et al. (2015), Cufaro-Petroni and Sabino (2018), and Ma, Pan, and Wang (2020) analyzed European exchange options when asset prices are modelled using jump-diffusion processes. Antonelli and Scarlatti (2010), Alòs and Rheinlander (2017), and Kim and Park (2017) priced European exchange options where underlying assets are driven by stochastic volatility models. Cheang and Chiarella (2011) also considered the case of American exchange options in their analysis. More recently, Cheang and Garces (2020), derived analytical representations for the European and American exchange option prices assuming that stock prices are modelled using a pair of Bates stochastic volatility and jump-diffusion dynamics. Among the aforementioned investigations, those of Cheang, Chiarella, and Ziogas (2006) and Alòs and Rheinlander (2017) priced exchange options using the put-call transformation approach. Fajardo and Mordecki (2006) also used a similar transformation, which they called the “dual market method”, to price options (including perpetual exchange options) when underlying prices are driven by Lévy processes. The others priced exchange options under the equivalent martingale measure (EMM) corresponding to the money market account.

The addition of both stochastic volatility and jump-diffusion precludes the availability of closed-form solutions (in the sense of the Black-Scholes or the Margrabe formulas) for exchange option prices, hence we resort to a numerical approximation of exchange option prices. Our main contributions toward this objective are as follows:

-

(1)

We extend the Bjerskund and Stensland (1993) strategy for valuing American exchange options in a pure-diffusion setting into the SVJD framework. This analysis also extends the closely related dual market approach of Fajardo and Mordecki (2006) for Lévy processes to accommodate stochastic volatility. To the best of our knowledge, not much focus has been placed on the use of the put-call transformation technique to pricing finite maturity American options in the stochastic volatility and jump-diffusion settings. As such, we aim to discuss how this technique can be applied to pricing exchange options with such asset price dynamics. Although we focus on exchange options only, as Fajardo and Mordecki (2006) notes, the approach is just as useful when pricing derivatives with homogeneous payoff functions.

-

(2)

In the simplified framework, we investigate the behavior of the early exercise boundary of the American exchange option near maturity, thereby extending the analysis of Chiarella and Ziogas (2009) for American calls under jump-diffusion. We also study analytically and numerically how some key model parameters, namely the dividend yields and the jump parameters, affect the behavior of the early exercise boundary.

-

(3)

We give a detailed discussion of a method of lines (MOL) scheme to numerically determine the price of exchange options, expressed in units of the second asset yield process, and the joint transition density function of the underlying state variables in the SVJD framework.

- (4)

-

(5)

As alternatives to the often assumed boundary condition for the behavior of option prices at high volatility levels (e.g. Clarke and Parrott 1999; Chiarella et al. 2009), we consider Venttsel boundary conditions for the far-but-finite limits of the computational domain and their impact on option prices and the performance of the MOL algorithm.

-

(6)

Using MOL-generated prices, we investigate how stochastic volatility and jumps in the asset prices affect option prices. Furthermore, we conduct an extensive numerical comparative static analysis to see how key model parameters affect the exchange option prices and the early exercise boundary.

As such, this paper serves as a numerical complement to the work of Cheang and Garces (2020) who focused more on the analytical aspects of pricing exchange options under SVJD dynamics.

In this analysis, pricing takes place under the EMM corresponding to setting the second asset yield process as the numéraire. Under , we find that the the no-arbitrage price of the European exchange option can be written as a function of only the asset yield ratio and the instantaneous variance . Furthermore, we verify an early exercise representation of the discounted American exchange option price, which can also be written as a function of only and . The pricing integro-partial differential equations for European and American exchange options, as well as the associated boundary conditions, under this measure are then derived.

The pricing IPDEs are then solved using the method of lines. The method of lines is a numerical method to solve PDEs which consists of discretizing the equation in all but one variable resulting to a sequence or system of ODEs in the remaining continuous variable. Schiesser and Griffiths (2009) provide a general exposition on the method, but for applications in option and fixed income instrument pricing, the time-discrete MOL, expertly discussed by Meyer (2015), has gained particular traction.222The time-discrete MOL involves discretizing the PDE in all but one spatial variable, as opposed to most applications where time is left as the continuous variable (see Schiesser and Griffiths 2009). This approach is also known as Rothe’s method or the horizontal MOL. This type of MOL has been applied to pricing American put options in the Black-Scholes framework (Meyer and van der Hoek 1997), put options under jump-diffusion dynamics (Meyer 1998), call options under stochastic volatility (Adolfsson et al. 2013; Chiarella and Ziveyi 2013), call options under Bates SVJD (Chiarella et al. 2009), American options with SV and stochastic interest rates (Kang and Meyer 2014), American options under a regime-switching GBM (Chiarella et al. 2016), and spread options under pure-diffusion dynamics (Chiarella and Ziveyi 2014). It is particularly useful for approximating American option prices as the algorithm can be easily adjusted to accommodate unknown free boundaries. It is also attractive for financial applications as the option delta and gamma are calculated as part of the algorithm with no additional computational cost. However as with any numerical technique for solving PDEs, the MOL becomes highly complex the more spatial variables are involved. In this paper, we thus use the put-call transformation technique in an effort to simplify the MOL approximation of the exchange option price.

While the succeeding analysis focuses on exchange options written on stocks, one may consider exchange options written on other assets such as indices and foreign currencies. For foreign currencies, in particular, the dividend yields are replaced by risk-free interest rates in the domestic and foreign money markets. Siegel (1995) explains how exchange options can be used to estimate the “implicit beta” between an underlying stock and a given market index. The exchange option framework may be adapted to investigate real options (Kensinger 1988; Carr 1995), outperformance options (Cheang and Chiarella 2011)333Cheang and Chiarella (2011) assumed that only one asset price process had jumps while the other was modelled as a pure-diffusion process. Quittard-Pinon and Randrianarivony (2010) discuss in greater detail the European exchange option pricing problem under a similar model specification., energy market options (surveyed in Benth and Zdanowicz 2015), and the option to enter/exit an emerging market (Miller 2012), among others. Ma, Pan, and Wang (2020) provide additional examples of financial contracts which can be priced under the exchange option framework.

The rest of the paper is organized as follows. Section 2 describes the SVJD model for the asset prices and the stochastic variance and discusses construction of the measure . In Section 3, we derive the pricing IPDE for the European and American exchange options. Section 4 discusses the behavior of the early exercise boundary near the expiry of the American exchange option. Section 5 explains the MOL algorithm for the solution of the pricing IPDE, the results of which are shown in Section 6. Section 7 concludes the paper. The focus of this paper is on the numerical implementation, hence we only briefly describe the proof of some technical results shown here and instead refer to (Garces and Cheang 2020) as it focuses on the probabilistic and analytical representation of exchange option prices under this framework.

2. Asset Price Dynamics and the Put-Call Transformation

In this section, we discuss the model specification for the underlying stock prices. We assume that the financial market consists of a risk-free money market account and two risky assets over a finite time period . We also let be the maturity of the exchange option. The dynamics of the asset prices are discussed below.

Let be a probability space equipped with a filtration satisfying the usual conditions. Let , , and be standard -Brownian motions with instantaneous correlations given by and , for Denote by the correlation matrix of the random vector . Let () be the counting measure associated to a marked Poisson process with -local characteristics .444See Runggaldier (2003) for more details. Underlying is a sequence of ordered pairs where is the “mark” of the th occurrence of an event that occurs at a non-explosive time . The marks are i.i.d. real-valued random variables with non-atomic density . Associated to the event times, we define a Poisson counting process given by where is the indicator function.

We assume that the counting measures are independent of the Brownian motions and of each other. Henceforth, we assume that is the natural filtration generated by the Brownian motions and the counting measures, augmented with the collection of -null sets.

Denote by and the price processes of two assets that pay a constant dividend yield of and , respectively, per annum. As stock prices may jump, we let and denote the stock prices prior to any jumps occurring at time . Let be the instantaneous variance process that governs the volatility of both stock price processes. We assume that the dynamics of the stock prices and the instantaneous variance satisfy the stochastic differential equations

| (1) | ||||

| (2) |

Here, is the mean jump size of the price of asset under , and , , , , and are positive constants. It is also assumed that .

We refer to this model as the proportional stochastic volatility and jump-diffusion (SVJD) model. While there is only one variance processes feeding into the diffusion component of each of the asset prices, the degree of influence the stochastic volatility process has on the asset price dynamics is governed by the proportionality coefficients and .555In contrast, Cheang and Garces (2020) assume one variance process for each asset price. However, their analytical representations require that the asset price processes are uncorrelated with each other and with the variance processes. The current model specification allows such dependence structure. In turn, the dynamics of the stochastic volatility process, modelled by a CIR square-root process, is dictated by the speed of mean reversion , the long-run variance , and the volatility of volatility .

As described above, the model features a common instantaneous variance process and independent jump terms for each asset. The individual jump processes may be taken to model idiosyncratic risk factors in each asset that cause sudden changes in returns.666In contrast, Cheang and Chiarella (2011) introduced an additional compound Poisson process appearing in both asset return processes which capture macroeconomic shocks or systematic risk factors which may introduce sudden jumps in returns. Although extremely rare, it is possible that jumps for both stocks arrive at the same time, representing market shocks or sudden events that may affect both assets. In addition, the common variance process models systematic market volatility or volatility at the macroeconomic level. As such, individual asset prices may provide feedback to each other via the correlation between the diffusion components and the dependence on a common stochastic volatility.

The price process of the money market account is denoted by , with for , where is the (constant) risk-free interest rate.

In this paper, we assume that the dividend yields, the risk-free rate, the parameters , , , , and , the jump the intensities and jump-size densities are constant through time, but the analysis can be extended to the case where these parameters are deterministic functions of time.

We require the following assumption on the parameters of the variance process and the correlation parameters to ensure that remains strictly positive and finite for all under and any other probability measure equivalent to (Andersen and Piterbarg 2007; Cheang and Garces 2020).

Assumption 1.

The parameters , , and and the correlation coefficients and satisfy (Feller condition) and , .

Straightforward calculations using Itô’s Lemma for jump-diffusions show that equation (1) admits a solution of the form

for , . Assumption 1 and the non-explosion assumption on the point processes imply that the integrals and summation that appear above are well-defined. It also follows that -a.s. for all , and hence either asset can be used as a numéraire.

Instead of , we take , the second asset yield process, as the numéraire and define the probability measure , such that the first asset yield process and the money market account, when discounted by , are martingales under . With the second asset yield process as the numéraire, the discounted price of any other asset with price process is defined by .

Next, we discuss the construction of . The following standard proposition specifies the form of the Radon-Nikodým derivative .

Proposition 2.1.

Suppose is a vector of -adapted processes and let be constants. Define the process by

| (3) | ||||

and suppose that is a strictly positive -martingale such that for all . Then is the Radon-Nikodým derivative of some probability measure and the following hold:777The Radon-Nikodým derivative can be used to characterize any probability measure equivalent to as parameterized by the vector process and the constants . We assume that are constant to preserve the time-homogeneity of the intensity and the jump size distribution. As the market under the SVJD is generally incomplete, one can construct multiple equivalent martingale measures consistent with the no-arbitrage assumption.

-

(1)

Under , the vector process has drift ;

-

(2)

has intensity , under ; and

-

(3)

The mgf of under is given by ,

We now specify the parameters of so that is an EMM corresponding to the numéraire . Let and , where and be the first asset yield process and the money market account when discounted using the second stock’s yield process. We will refer to as the asset yield ratio process. If we choose , , and as

| (4) | ||||

| (5) | ||||

| (6) |

where and , then and are -martingales on .888This assertion can be proved using Itô’s Lemma on and and eliminating the resulting drift term as required by the martingale representation for jump-diffusion processes (see Runggaldier 2003, Theorem 2.3).

With this choice of parameters for , the dynamics of becomes

| (7) |

where is a -Wiener process. The choice of preserves the structure of the instantaneous variance as a square-root process. Assumption 1 ensures that this process is strictly positive and finite -a.s.

Under , satisfies the equation

| (8) | ||||

where we define with standard -Wiener processes and and .999In view of Proposition 2.1, we note that . Lastly, we note that the instantaneous correlation between the -Brownian motions and is given by .

3. The Exchange Option Pricing IPDE

Now we derive the integro-partial differential equation (IPDE) for the price of an exchange option written on and . Denote by the price of a European exchange option whose terminal payoff is given by where . A rearrangement of terms expresses the discounted terminal payoff as

Let denote the discounted European exchange option price. Then, assuming that no arbitrage opportunities exist, is given by

| (9) | ||||

In other words, the price at any time of the European exchange option measured in units of the second asset yield process is the -expectation of the terminal payoff measured in units of the second asset yield process (Geman, El Karoui, and Rochet 1995). From the last equation, we also note that the terminal payoff is variable only in the asset yield ratio . Thus, we assume that the discounted European exchange option price is represented by the process and so

| (10) |

Thus we have shown that, by taking the second asset yield process as the numéraire asset, the exchange option pricing problem is equivalent to pricing a European call option on the asset yield price ratio with maturity date and strike price . If we choose as the numéraire, then the problem simplifies to the valuation of a put option written on the asset yield ratio .

The following technical assumption is required to implement Itô’s formula for jump-diffusion processes.

Assumption 2.

For , is (at least) twice-differentiable in and and differentiable in with continuous partial derivatives.

The following proposition provides the IPDE that characterizes the discounted European exchange option price. This result can be proved using Itô’s formula for jump-diffusion processes and employing usual martingale arguments (see Cheang and Garces 2020, Appendix 2).

Proposition 3.1.

The price at time of the European exchange option is given by

| (11) |

where , satisfying Assumption 2, is the solution of the terminal value problem

| (12) | ||||

| (13) |

with and the IPDE operator defined as

| (14) | ||||

where is the expectation with respect to the r.v. () under the measure . Note that all partial derivatives are evaluated at .

Let be the price at time of an American exchange option written on and . After a rearrangement of terms, standard theory on American option pricing (see e.g. Myneni 1992) dictates that the discounted American exchange option price is given by

| (15) | ||||

where the supremum is taken over all -stopping times . From here, we see that the change of numéraire reduces the problem to pricing an American call option on the asset yield price ratio , similar to our observation for the European exchange option. The price of the American exchange option also hedges against the exchange option payoff in the sense that for all and

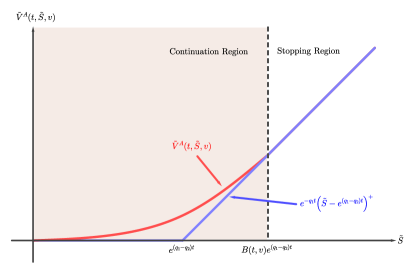

Before prescribing additional boundary conditions to IPDE (12) for the American exchange option, we first define the continuation and stopping regions, denoted by and , respectively, that divide the domain of IPDE (12). These regions are given by

| (16) | ||||

Denote by and the stopping and continuation regions at a fixed .

For the American exchange option, there exists a critical stock price ratio such that the stopping and continuation regions can be written as

| (17) | ||||

(Broadie and Detemple 1997; Touzi 1999).101010Mishura and Shevchenko (2009) analyzed, in further detail, the properties of the exercise region of the finite-maturity American exchange option in a pure diffusion setting. In the same setting, Villeneuve (1999) established the nonemptiness of exercise regions of American rainbow options, which include spread and exchange options as special cases. For a fixed and , the early exercise boundary and the continuation and stopping regions are illustrated in Figure 1. It is known that in the continuation region the American exchange option behaves like its live European counterpart, and so satisfies IPDE (12) for .

We require value-matching and smooth-pasting conditions on IPDE (12) to elliminate arbitrage opportunities and to ensure that and are both continuous across the early exercise boundary . Specifically, the required value-matching condition is

| (18) |

and the smooth-pasting conditions are

| (19) | ||||

Therefore, is a solution to IPDE (12) over the domain , , . The IPDE has terminal and boundary conditions

| (20) | ||||

value-matching condition (18) and smooth-pasting condition (19).

The American exchange option price can be decomposed into the sum of the discounted European exchange option price and an early exercise premium.

Proposition 3.2.

Suppose Assumption 2 also holds for . Assume further that the smooth pasting conditions (19) across the early exercise boundary hold. Then can be expressed as

| (21) |

where is the discounted European exchange option price given by equation (10) and is the early exercise premium given by

where is the indicator function, is the event and

Note that all partial derivatives in are all evaluated at .

Proof.

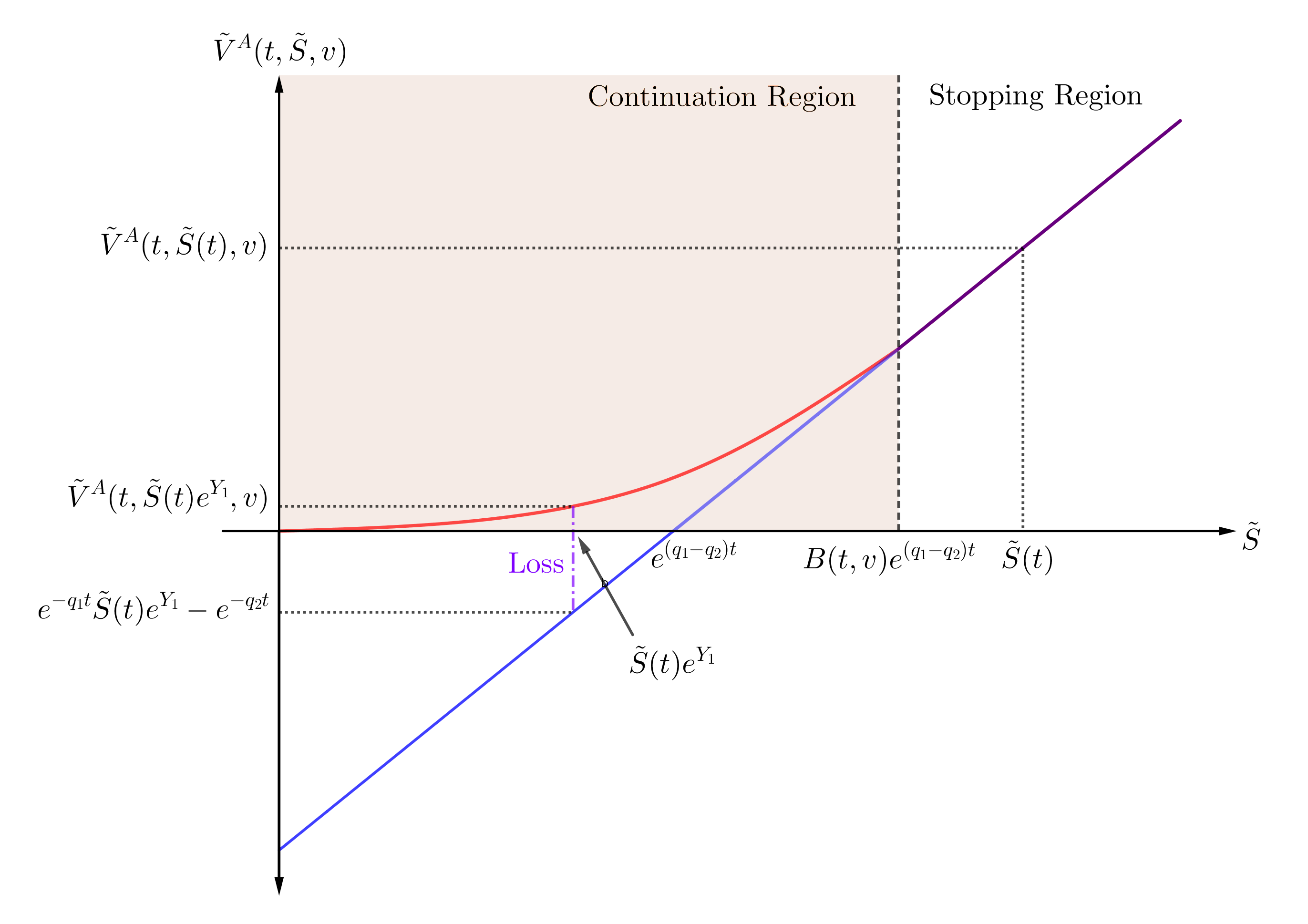

The early exercise premium can be decomposed into a diffusion component (the positive term) and a jump component (the negative terms). However, unlike the early exercise premium derived by Cheang, Chiarella, and Ziogas (2013) for an American call option under SVJD dynamics, our early exercise premium representation contains two jump terms. This is because has two sources of jumps: the jumps in the price of the first asset and the jumps in the numéraire. Nonetheless, the interpretation remains the same: the diffusion term captures the discounted expected value of cash flows due to dividends when asset prices are in the stopping region and the jump terms capture the rebalancing costs incurred by the holder of the American exchange option when a jump instantaneously occurs in the price of either asset, causing to jump back into the continuation region immediately after the option is exercised.111111In this situation, the investor is unable to adjust the decision to exercise in response to the instantaneous jump in asset prices and is therefore vulnerable to the rebalancing cost described earlier. A similar phenomenon in the context of consumption-investment problems with transaction costs in a Lévy-driven market is explored in greater technical detail by De Vallière, Kabanov, and Lépinette (2016). Figure 2 illustrates the loss (captured by the difference in option value and the exercise value) incurred by the option holder when the asset yield ratio jumps back into the continuation region due to a jump, by a factor , in the price of the first asset. A similar graphical analysis holds if the price of the numéraire asset instantaneously jumps instead of the price of the first asset (in this case, the new asset yield ratio is ).

Recall that is a solution of the homogeneous IPDE (12) over the restricted domain , , and subject to the value-matching condition (18), the smooth-pasting condition (19), and boundary conditions (20). Following Jamshidian (1992) and Chiarella and Ziogas (2004), the restriction on the domain can be removed by adding the appropriate inhomogeneous term to the IPDE such that the equation holds for all . The inhomogeneous IPDE corresponding to our analysis is presented in the following proposition. This analysis requires that and its first-order partial derivative with respect to are continuous, but the value-matching and smooth-pasting conditions are sufficient to meet this requirement.

Proposition 3.3.

The discounted American exchange option price is a solution to the inhomogeneous IPDE

| (22) |

where the inhomogeneous term is given by

| (23) | ||||

where and are the pdfs of and , respectively, under , and . This equation is to be solved for , subject to terminal and boundary conditions (20).

Proof.

Observe that for all , the equation

holds. Equation (LABEL:eqn-PutCall-InhomogeneousTerm) is obtained by expanding the negative term in the above equation with the functional form of in the stopping region and using the and to rewrite the expectations as integrals. ∎

4. Limit of the Early Exercise Boundary at Maturity

When implementing numerical schemes to solve for the American exchange option price, it is important to know the behavior of the critical asset price ratio associated to the early exercise boundary of the American exchange option immediately before the option matures (i.e. as ). Doing so provides a terminal condition for the unknown early exercise boundary that can be used in conjunction with the terminal condition on the discounted American exchange option price. The next proposition presents the limit of the early exercise boundary, which we obtain following the method of Chiarella and Ziogas (2009).

Proposition 4.1.

The limit is a solution of the equation

| (24) |

Proof.

See Appendix A ∎

Equation (24) must be solved implicitly for , which can be done using standard root-finding techniques. From our analysis, we find that the limit is dependent on the asset dividend yields and , the jump intensities and , and the jump size densities and . These dependencies highlight the influence of jumps in asset prices on the limiting behavior of the early exercise boundary.121212This is in contrast to the proposition of Carr and Hirsa (2003), in their analysis of the one-asset American put option where the log-price is driven by a Lévy process, that the limit of the early exercise boundary is only dependent on the dividend yield and the risk-free rate. We note further that equation (24) does not depend on the instantaneous variance since the option payoff is independent of . However, equation (24) is true for all . In fact, is constant with respect to .

In the absence of jumps (i.e. when ), the limit reduces to . This is consistent with the result of Broadie and Detemple (1997) for American exchange options in the pure diffusion case. In the pure diffusion case, if , implying that the early exercise boundary many not be continuous in at maturity. When jumps are present, the analysis of continuity becomes more complicated, as shown below.

First, we present some conditions under which equation (24) has a solution.

Proposition 4.2.

Suppose and are given and let and be continious probability density functions. The equation

| (25) |

has a unique solution if . Furthermore, if and only if

and the limit of the early exercise boundary is .

Proof.

See Appendix B ∎

An immediate result from Proposition 4.2 is a condition for the continuity of at maturity.

Proposition 4.3.

Suppose . For any fixed , is continuous at maturity if

| (26) |

Proof.

In other words, if the dividend yield of the first asset exceeds that of the second asset by the amount given by the right-hand side of (26), then the early exercise boundary is continuous at maturity.

We briefly discuss the behavior of with respect to changes in . Note that , so when decreases, increases. In particular, for a given , there exists such that . If decreases, then increases away from zero, thereby moving the unique zero of to some other number such that . In other words, the solution of equation (25) increases without bound, and consequently , as . Thus, when the first asset bears no dividend yield, it is not optimal to exercise the American exchange option early or at least immediately prior to the option maturity.

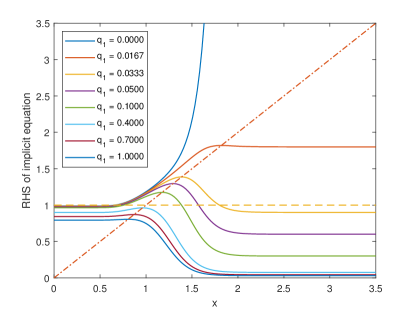

We give a numerical illustration of the aforementioned properties in the case of when the jump size random variables and have normal distributions and , respectively, under . The integrals in equation (25) can then be expressed in terms of the standard normal distribution. Figure 3 shows the behavior of the right-hand side of equation (25), which we denote by , for increasing values of given this specific distribution of jump sizes and fixed parameters , , , and . We observe that, except for when , the behavior of is generally the same for any value . That is, it increases up until some value of , then eventually decreases to . The graph of eventually crosses the line, indicating the solution of equation (25). However, if , then the graph of never crosses the line, implying that there is no solution exists for (25) and that the equation will only be satisfied by taking the limit as , giving an infinite early exercise boundary . We also note that as increases farther from , eventually falls below unity. One can also formulate the difference in (26) in terms of the standard normal distribution

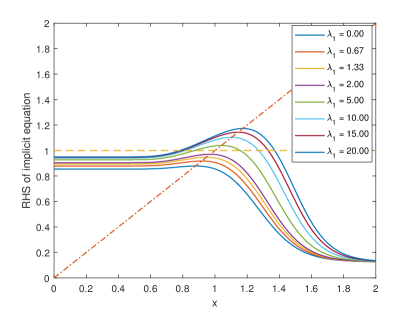

A comparative static analysis of with respect to the jump intensities and can also be conducted. We note that

as was established in the proof of Proposition 4.2. With the same arguments as above, these inequalities imply that are non-decreasing with and . This is graphically illustrated by Figure 4, where we once again plot the right-hand side of equation (25) for various values of . In this example, we set and (chosen such that below and above unity are illustrated), with the value of all other jump parameters chosen similarly to those for Figure 3. A similar illustration can also be generated for a comparative static analysis with respect to .

The response of the early exercise boundary limit at maturity with respect to the jump intensities is indeed expected. As discussed in the previous section, there is a nonzero probability that asset prices may jump back into the continuation region immediately after exercise, resulting to losses for the option holder. The option holder is thus more conservative in opting for early exercise and is willing to exercise early only when the asset yield ratios are higher compared to the no-jump case. This is so that even if the asset yield jumps downward, it is less likely to move all the way back in to the continuation region thereby reducing risk on the investor’s end.

5. Method of Lines Implementation

Here, we discuss the MOL algorithm to numerically solve the IPDEs for the discounted European and American exchange option prices and the joint transition density function (tdf) of the asset yield ratio and the variance process under . For convenience, the terminal value problem is transformed into an initial value problem involving the time to maturity . We also denote the discounted exchange option prices by , where and . We first discuss the MOL for the European exchange option (which is also applicable to the joint tdf) and present the required adjustments for the approximation of the unknown exercise boundary for the American exchange option. We conclude this section with a discussion of alternative boundary conditions at the far boundary of .

It has been observed that MOL performs as competitively, if not more efficiently, compared to other methods such as componentwise splitting methods, numerical integration with the joint tdf, Monte Carlo techniques, and full finite difference schemes (Chiarella et al. 2009; Chiarella and Ziveyi 2013; Kang and Meyer 2014, among others). This is mainly due to the ability of the MOL to calculate the option delta and gamma to any desired accuracy with no considerable additional computational effort. To illustrate the accuracy and efficiency of the MOL, we compare the MOL American exchange option prices to prices generated by the Longstaff and Schwartz (2001) least-squares Monte Carlo (LSMC) algorithm, a simple and popular simulation-based method for valuing early exercise options.131313The LSMC algorithm only simulates the optimal exercise strategy and is unable to estimate the early exercise boundary. For a simulation-based method for approximating the early exercise frontier, see Ibáñez and Zapatero (2004). More recently, Bayer, Tempone, and Wolfers (2020) proposed a new simulation-based method that estimates exercise rates of randomized exercise strategies, an optimization problem which they show is equivalent to the original optimal stopping formulation.

5.1. MOL Approximation of the IPDE and the Riccati Transform Method

With the new notation introduced in this section, we find that the discounted European exchange option price satisfies

| (27) | ||||

This equation is to be solved for , , and subject to the initial condition

We also impose the following (asymptotic) boundary conditions on (27):

| (28) |

The first boundary condition implies that the option becomes worthless for very small values of (i.e. when the price of the first asset dominates that of the second asset). The second boundary condition implies that the option delta becomes insensitive to changes in the asset yield ratio when it is sufficiently large. The third boundary condition means that the option price is insensitive to changes in the instantaneous variance for sufficiently large values of .

For computational purposes, the infinite domains for and are truncated to and , respectively, with some suitably chosen and . We consider the partition of with uniform width and the partition of , also with uniform size . Denote by the approximate solution of (27) at the time line and variance line , and let be the approximation of the option delta.

We then use finite difference quotients to discretize equation (27) in all variables but . For the time derivative, a backward difference approximation is used following Meyer and van der Hoek (1997),

The approximation is only first-order accurate for the first two time steps, but for all subsequent time steps, a second-order approximation is used. Using such a scheme improves the accuracy of the method of lines algorithm. The second-order partial derivatives in are approximated using central difference quotients

We use an upwinding difference approximation for ,

This approximation is only first-order accurate, but it helps keep the finite difference approximation in stable as the coefficients of the second-order partial derivatives vanish as and it improves the performance of the iterative method used in the method of lines algorithm (Chiarella et al. 2009; Meyer 2015).

At the last variance line , we invoke the asymptotic boundary condition (28) in . The boundary condition can be approximated by

| (29) |

and a forward difference approximation of this implies that . Differentiating with respect to , we also find that .

The integral terms must also be approximated at each time and variance line. Assuming that and under , the integrals, which we denote by and , can be approximated using Gauss-Hermite quadrature,

where and are the weights and abscissas of the Gauss-Hermite quadrature scheme with integration points. The parameters and are also approximated using Gauss-Hermite quadrature.

The MOL approximation of equation (27) at and is therefore

| (30) | ||||

where the coefficients are obtained by comparing (LABEL:eqn-MOLEu-IPDE-Approx2) to (27) after substituting the finite difference and integral approximations (see Appendix C).

As the source term of equation (LABEL:eqn-MOLEu-IPDE-Approx2) at each depends on , , and , none of which are available at the current variance line, and involves integrals based on , the sequence of equations (LABEL:eqn-MOLEu-IPDE-Approx2) represents a system of coupled second-order integral-ordinary differential equations. To this end, we employ a nested two-level iterative scheme in conjunction with the Riccati transform approach of Meyer and van der Hoek (1997), as was done by Chiarella et al. (2009). In the first iteration level, referred to as integral term iterations, the integral terms are approximated using the latest available values of the option price. This enables us to treat (LABEL:eqn-MOLEu-IPDE-Approx2) as a second-order ODE which can then be solved using the Riccati transform method in the second iteration level, referred to as the variance line iterations.

The two-stage iterative process and the Riccati transform solution of equation (LABEL:eqn-MOLEu-IPDE-Approx2) is shown in Algorithm 1. The succeeding discussions aim to clarify certain details of the algorithm.

Let and be the iteration counters for the integral term and variance line iterations, respectively, and let and be the th iterates of and , replacing with when we refer to their counterparts in the integral term iterations. “Previous” iterates will be denoted with a superscript or . The Riccati transform method requires that the computational -domain be partitioned with a mesh . Note that this mesh may not necessarily have a uniform width. In view of boundary conditions (28), it is known that and .

In each integral term iteration, and are computed using previous iteration values of . But since is available only at the mesh points for , the summands required for and are linearly interpolated or extrapolated. The integrals are computed only once per integral term iteration and are not recomputed during the variance line iterations.

We now discuss what transpires in the general th variance line iteration.

At , equation (LABEL:eqn-MOLEu-IPDE-Approx2) is not solved directly. Instead, we apply the quadratic extrapolation formulas

| (31) | ||||

to approximate the option price and delta at the first variance line.141414Provided that the Feller condition is satisfied, the quadratic extrapolation combined with the MOL approach produces a consistent approximation of the pricing equation as (Chiarella et al. 2009, Appendix).

For , equation (LABEL:eqn-MOLEu-IPDE-Approx2) is transformed into a system of first-order ODEs

| (32) | ||||

where , , and . The corresponding Riccati transformation is given by

| (33) |

where and are solutions of the initial value problems

| (34) | ||||

with . System (34) is integrated using the trapezoidal rule starting at until . This process is referred to as the forward sweep. Once and have been determined, the equation

is integrated using the trapezoidal rule starting at . The starting point is calculated using the boundary condition and the above equation. The option price can be recovered using the Riccati transform (33). The reverse sweep concludes after calculating and for all .

The process at the last variance line is similar to that for , except that the coefficients , , and must be adjusted in view of equations (42).

The variance line iterations terminate once the convergence criterion

| (35) |

is satisfied. Otherwise, the current iterates are stored as previous iterates and the next variance line iteration commences. If (35) is met, then and are stored as and and the current integral term iteration continues. The convergence criterion may also include the option delta, if a more stringent criterion is desired.

Now back at the current integral term iteration, criterion (35) is checked again using and . If it is not satisfied, then the current iterates are stored as previous iterates and the next integral term iteration commences. At this point, and are recalculated and another pass of variance line iterations commences. Otherwise, the integral term iterations terminate and the latest iterates and are taken to be the solutions and at the th time step. The algorithm then proceeds to the next time step.

As seen above, the MOL algorithm naturally computes the option price , the option delta , and the option gamma . The option gamma profile can be stored by computing with the second equation in (32) after computing and in the reverse sweep.

The MOL algorithm discussed above can also be used to approximate the joint transition density function of the log-asset yield ratio and the variance . The joint tdf is known to satisfy the backward Kolmogorov equation

| (36) | ||||

for , , and . Equation (36) is to be solved subject to the initial condition , where is the Dirac delta function, and boundary conditions , , and . It is assumed here that the values of the state variables at maturity are constant.

5.2. Adjustments for the American Exchange Option Price

The MOL algorithm discussed above has to be slightly adjusted to determine the unknown early exercise boundary during the forward sweep. For convenience, we continue to denote the discounted American exchange option price by . Then also satisfies (27), subject to the same initial condition. However, this equation must be solved over the restricted domain , , and , where us the unknown early exercise boundary. For , the option price is known analytically as . In addition to the usual boundary conditions and we also impose smooth-pasting condition . A suitable initial condition for the early exercise boundary is , where is a solution of equation (24), and let be the approximation of the boundary at and .

The MOL approximation of the American exchange option at and is also given by equation (LABEL:eqn-MOLEu-IPDE-Approx2) with coefficients (41) for and (42) for . Thus, in this section, we highlight how the Riccati transform method in the previous section is modified to solve for the early exercise boundary. We assume that is chosen such that for all . Algorithm 2 shows the modified MOL algorithm.

In each of the variance line iterations, the and are estimated using the quadratic extrapolation formulas (31). For each , the forward sweep of system (34) via the trapezoidal rule starts at in the direction of increasing . The main difference is that for the American exchange option, the sign of the function

| (37) |

is monitored at each . Equation (37) arises from combining the smooth-pasting condition and the Riccati transform equation. The initial value is . The forward sweep stops at the index at which first becomes negative; i.e. is the first index such that . The approximation of the early exercise boundary at this iteration, which we denote by , is estimated to be the zero of the cubic spline interpolant through the points that occurs in between and . This zero is numerically solved using any standard root finding algorithm.

Once has been determined, the reverse sweep for is then carried out over the interval . Since is not part of the regular mesh, the trapezoidal rule is first applied over , where the required values of , , , , and are linearly interpolated from values at and , which were determined as part of the forward sweep. Once has been calculated, the reverse sweep can continue over along the regular mesh. For , it is known that . The value of can be calculated using the Riccati transform equation.

The same process applies at the last variance line, except that a recalculation of the coefficients of the Riccati system according to equation (42) is required before commencing the forward sweep.

Once the convergence criterion is satisfied at both iteration levels, the final iterates are then stored as the solution at the th time step.151515The convergence criterion can also include the early exercise boundary. The algorithm then proceeds to the next time step.

5.3. Venttsel Boundary Conditions at

The choice of boundary conditions for equation (27) affects the quality of the MOL approximation obtained using the algorithms discussed above. In most financial applications, the initial condition is usually dictated by the type of instrument being priced. However, articulating boundary conditions in the spatial variables is not as straightforward since the equation may be degenerate at certain points of the boundary or the domain may be unbounded. The problem considered in this paper struggles with both issues.

The pricing equation (27) is degenerate when or . As such, the structure of the IPDE determines whether conditions at these boundaries should be independently imposed or if the equation itself should naturally hold at these boundaries. Chiarella et al. (2009) consider this issue in more detail, with the aid of the Fichera function for degenerate equations, for the closely related American call option under SVJD dynamics and justify the use of quadratic extrapolation for the solution of the pricing equation along the first variance line .161616Such an analysis was also done by Kang and Meyer (2014) for American calls under stochastic volatility and stochastic interest rates. Meyer (2015) provides a discussion of the Fichera theory applied to common financial problems. They showed that equation (27) is expected to hold when provided that the Feller condition is satisfied. This implies that no independent condition is required at that point. On the other hand, we allow the dynamics of to dictate the boundary condition at . From (8), if the process starts at zero, then it will stay at zero, implying that the option becomes worthless throughout its life. This motivates the choice of the first boundary condition in (28).

For the MOL algorithm, we truncated the infinite and domains. As such, boundaries must be prescribed at the far boundaries and . For the Riccati transform method to work in the European case, the boundary condition at must be equivalent to a scalar equation in and , and this is attained through the second condition in (28) when approximated as (although there may be alternatives to this). In the American case, no such condition is required since we already have the smooth-pasting and value-matching conditions at the free boundary, which is assumed to be less than . Hence, we only need to consider boundary conditions at .

As an alternative to the boundary condition , we consider Venttsel boundary conditions derived from the pricing equation.171717We do not seek to formally define Venttsel boundary conditions in this paper. The reader is referred to Meyer (2015, Section 1.2.3) for a discussion of Venttsel boundary conditions in the context of financial pricing problems. Following the theory of Venttsel boundary conditions in Meyer (2015), we find that the equation

| (38) | ||||

is an admissible Venttsel condition at provided that . Equation (38) is equivalent to the assumption that the option delta and vega are insensitive to the instantaneous variance for when the variance level is sufficiently large. Another Venttsel condition is given by

| (39) | ||||

which resembles the pricing equation when volatility is constant at . Whichever Venttsel boundary condition is chosen, the equation must be solved subject to boundary conditions in and .

In the MOL implementation, the adoption of either Venttsel condition implies a change in the coefficients of equation (LABEL:eqn-MOLEu-IPDE-Approx2) at . For equation (38), we employ a backward difference approximation of . This is appropriate in view of the upwinding difference approximation for the other variance lines as this Venttsel condition requires that . The usual discretization is employed for . Once the coefficients of equation (LABEL:eqn-MOLEu-IPDE-Approx2) have been updated, the Riccati solution for the last variance line can proceed as outlined in Section 5.1.

The impact of these Venttsel conditions on the performance of the MOL algorithm is explored in the succeeding sections.

6. Numerical Results and Discussion

| Asset Price | Stoch. Vol. | Jumps | Mesh Sizes | ||||

|---|---|---|---|---|---|---|---|

| 0.50 | 2.00 | 5.00 | 5.00 | ||||

| 0.05 | 0.56 | 0.20 | 4.00 | ||||

| 0.03 | 0.00 | 2.00 | |||||

| 0.50 | 0.40 | 2.00 | 30 | ||||

| 0.50 | 0.50 | 0.20 | 25 | ||||

| 0.50 | 0.05 | 0.00 | 140 | ||||

| 20 | |||||||

In this section, we present numerical approximations of the discounted European and American exchange option prices, the early exercise boundary, the discounted early exercise premium, and the joint tdf generated using the MOL algorithm discussed in the previous section. These results were obtained using the parameter values enumerated in Table 1, although in Section 6.2, we investigate how the option prices and the early exercise boundary change in response to alternative model parameter values.181818Model parameter values used in this paper are similar to those used by Chiarella et al. (2009), although additional parameters are used to accommodate the second asset. The values of and were chosen so that the exercise boundary is discontinuous at maturity, thereby highlighting the impact of jumps in asset prices. The chosen means of the jump size variables and are zero, indicating that upward and downward jumps in asset prices are equally likely to occur. We also assume that they have equal standard deviations.191919Less emphasis on the jump size distribution concentrates the analysis on the effect of the jump intensities. Alternative jump size distributions may be considered as well, although the form of the density function dictates the quadrature formula for approximating the integral terms. Correlations among Wiener processes are initially assumed to be positive, although the effect of negative correlations is also be explored in Section 6.2.

All source codes were implemented using MATLAB on an x64-based personal computer with an Intel Core™i7-10710U CPU with 1.10GHz, 1608 MHz, 6 cores, 12 logical processors, and 8GB RAM. Due to hardware constraints, modest mesh sizes for , , and (or ) are used, although as seen in Table 2 below, the MOL does not require too many time steps to converge. The computational domain for was divided into three intervals, , , and , which was then subdivided using 20, 80, and 40 mesh points, respectively. This allows for a more precise approximation of the early exercise boundary as it tends to occur near . Despite the use of relatively few mesh points, convergence was attained for all MOL implementations with parameters reported in Table 1 and the alternative values explored in Section 6.2.

All option prices, option deltas, and price differences presented in this section are in their discounted form, i.e. they are expressed in units of the second asset yield. As such, prices and price differences may be more pronounced if the exchange option is written on highly priced underlying assets.

6.1. MOL Approximation of Exchange Option Prices and the Joint TDF

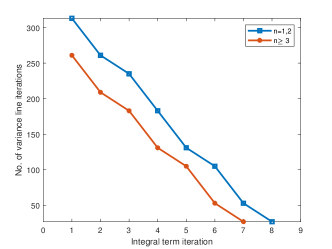

Figure 5 shows the typical convergence pattern of the integral term and variance line iterations for the MOL approximation of the European and American exchange option in the th time step. It has been observed that the convergence behavior is the same for both types of exchange options. However, we note a decrease in the number of integral term iterations required on and after the third time step, signifying the effect of adopting a second-order backward difference approximation for the time derivative for on the efficiency of the computation. The number of variance line iterations generally decreases as the integral line iterations continue. Chiarella et al. (2009) reported that the number of variance line iterations required drastically increases as the number of mesh points in increases, but we were unable to replicate this phenomenon due to hardware constraints. While the convergence behavior is the same for both European and American cases, a typical MOL pass yields a computing time for the American exchange option that is almost double that required for the European case. In a sample implementation, the European and American cases were completed in 74.4492 and 152.5094 seconds, respectively.

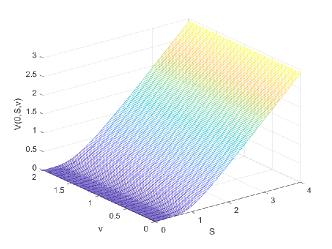

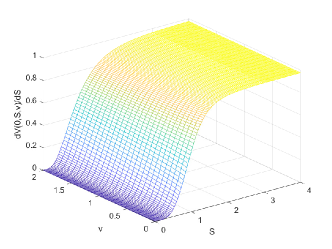

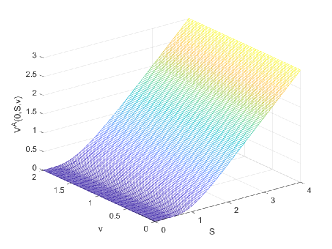

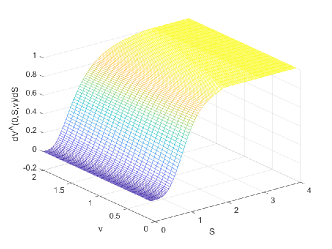

Figure 6 shows the approximation of the discounted European exchange option price and delta against and at (or ), the start of the life of the option. Similar to ordinary European call options, the delta of the European exchange option is steepest when the asset yield ratio is close to .

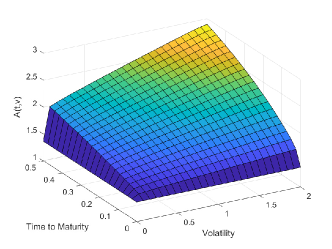

Figures 7 and 8 show the MOL approximations of the early exercise surface, the discounted American exchange option price, and the American exchange option delta at time-to-maturity (or time ). Figure 7 shows that the early exercise boundary at is constant with respect to since the option payoff is independent of as discussed in Section 4. The figure also illustrates that the is an increasing function of . As expected from the put-call transformation technique, the American and European exchange option price profiles, when expressed in terms of the asset yield ratio, behave in a similar manner to their ordinary call option counterparts.

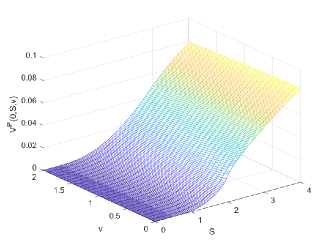

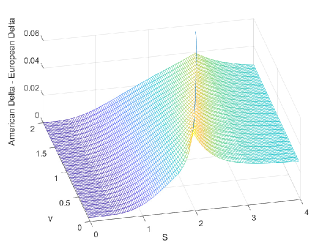

The price and delta profiles of the European and American exchange options appear to behave similarly in and , but the difference is emphasized when we compute the early exercise premium . Figure 9 shows the discounted early exercise premium surface in the asset yield ratio and variance at . For a fixed , the premium is increasing in . On closer inspection, the early exercise premium has an inflection which can be confirmed to occur at the early exercise boundary . This is also where the difference in American and European deltas peaks. This implies that the premium increases the fastest as the asset yield ratio approaches the exercise boundary from the left.

| Method of Lines | [LS] Monte Carlo | |||||

| Price | 95% CI | |||||

| 0.500 | 0.015447 | 0.015441 | 0.015440 | 0.000015 | 0.000012 | 0.000032 |

| 0.625 | 0.039076 | 0.039108 | 0.039112 | 0.000622 | 0.004355 | 0.008093 |

| 0.750 | 0.077450 | 0.077521 | 0.077530 | 0.004084 | 0.003621 | 0.004546 |

| 0.875 | 0.130851 | 0.130953 | 0.130966 | 0.018030 | 0.017121 | 0.018939 |

| 1.000 | 0.198052 | 0.198179 | 0.198194 | 0.058294 | 0.056785 | 0.059803 |

| 1.500 | 0.565205 | 0.565367 | 0.565382 | 0.499905 | 0.499602 | 0.500208 |

| 2.000 | 1.016076 | 1.016183 | 1.016189 | 0.999884 | 0.999481 | 1.000286 |

| 2.500 | 1.500852 | 1.500875 | 1.500869 | 1.500207 | 1.499520 | 1.500893 |

| 3.000 | 2.000000 | 2.000000 | 2.000000 | 1.999870 | 1.999284 | 2.000457 |

| 3.500 | 2.500000 | 2.500000 | 2.500000 | 2.499871 | 2.499129 | 2.500612 |

| 4.000 | 3.000000 | 3.000000 | 3.000000 | 2.999690 | 2.998935 | 3.000445 |

| 2.6622 | 2.6626 | 2.6605 | - | - | - | |

| Comp Time (s) | 194.5725 | 332.1941 | 522.4031 | - | - | |

In Table 2, we compare MOL prices for American exchange options to those generated by the Longstaff and Schwartz (2001) least-squares Monte Carlo algorithm. The LSMC algorithm was implemented using time steps and 10,000 scenarios (half of which are antithetic variates). For the simulation approach, first-order Euler-Maruyama discretizations of the asset yield and instantaneous variance processes were used. The LSMC algorithm requires knowledge of the second asset price process since it serves as a (stochastic) discount factor for pricing options under , so was also simulated with initial value .202020By assuming that , the MOL prices are then expressed in monetary units rather than in units of the second asset yield process.

The exercise policy generated by the LSMC is sub-optimal as it approximates the American option by its Bermudan counterpart, and so the prices produced by the algorithm are lower bounds of the “true” American option price (Longstaff and Schwartz 2001). We are able to verify this property for the parameters used, with MOL prices being consistently higher than point estimates for the price from the LSMC algorithm. We note however that the discrepancy is larger especially for when the option is deeply out-of-the-money, but this is most likely due to the slow convergence of the Monte Carlo method, a phenomenon that was also observed in a similar analysis by Chiarella and Ziveyi (2014). For smaller values of , the regression step is also ill-conditioned, which most likely contributed to the discrepancy as well. MOL and LSMC prices for deeply out-of-the-money options are nonetheless consistent with (28). For higher values of , the MOL prices fall within the 95% confidence interval calculated using the LSMC approach.

Also, it takes substantially longer to estimate a complete profile of American option prices using the LSMC algorithm compared to the MOL. Having to simulate sample paths for the second asset price process means the appeal of the put-call transformation in reducing the dimensionality of the problem is lost in the simulation approach. The MOL is also far more efficient than the LSMC algorithm, since in one implementation of the MOL, we are able to estimate the option price, the delta, the gamma, and the early exercise boundary. The MOL also requires substantially fewer time steps to converge. By increasing the number of basis functions used in the regression and the number of simulations decreases the gap between the LSMC point estimate and the “true” option price, but doing so increases the computation time (Stentoft 2004). We report however that increasing the number of time steps does not drastically diminish the discrepancy between MOL and LSMC prices for lower asset yield ratios. In particular, when and the LSMC prices when are and , respectively, which are still far below the MOL prices.212121The LSMC algorithm was also implemented for a smaller number of exercise times, and , but it produced prices and confidence intervals which fall completely below the MOL price for all values of considered. Average computation times for and time steps in the LSM algorithm are 4,582.9s and 4,949.9s, respectively.

A complete comparison of the relative efficiency and accuracy of these two methods remains to be seen, since both methods have numerous sources of error, including (but not limited to) the discretization scheme for the simulation of state variables or the discretization of partial derivatives, truncation of infinite domains, the choice of mesh sizes and partition points in all variables, boundary conditions for the IPDE, numerical integration scheme, and the choice of basis functions for regression. Nonetheless, for the parameter values and assumptions reported for this numerical experiment, the results we obtained are reasonably comparable.

6.2. Numerical Comparative Statics

In this section, we investigate how the discounted American and European exchange option prices and the early exercise boundary time profile change in response to changes in the model parameters. This analysis covers three components: (1) the effect of the correlations between the Wiener processes in the asset price and variance processes, (2) the effect of asset price jump intensities, and (3) the effect of the variance process parameters, namely the mean reversion rate , volatility of volatility , and the market price of volatility . The analysis of option price differencesat (or ) are shown with respect to the asset yield ratio as this highlights how the early exercise boundary influences the comparative statics of the American exchange option. In all subsequent analyses, option prices and the early exercise boundary are shown for (the long-term variance ) and parameter values in Table 1 except for those which were varied in the numerical experiment. Prices and the early exercise boundary were generated using the method of lines discussed in the previous sections.

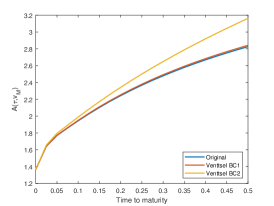

Figure 10 shows the effect of the model parameters on the early exercise boundary. In all panels except for the fourth, we note that all boundary curves start at the limit at maturity () as calculated using the method in Section 4 ( for the parameters in Table 1). This is expected as the limit depends only on the dividend yields and the jump parameters, and not on diffusion and variance parameters. The results of the numerical comparative statics are enumerated below.

-

•

The exercise boundary is lowest when both asset prices are positively correlated to the variance process, and is highest when the assets have opposing directions of correlation with the variance process. The boundaries generated when the correlations are zero or are both negative are similar, but are consistently higher than the positive correlation case.

-

•

A negative correlation between the asset prices also generates a consistently higher boundary curve than when or , the latter generating the smallest values.

-

•

The boundary curve pivots upward when the gap between and increases, although the effect is symmetric whether it is asset 1 or 2 that has a greater proportionality coefficient.

-

•

The early exercise boundary is not as sensitive to the rate of mean reversion and the market price of volatility compared to the diffusion coefficients. The differences are more pronounced when the option is far from maturity.

-

•

Changing the value of produces negligible changes in the boundary curve and is thus not shown here. This is somewhat contrary to the results of Chiarella et al. (2009) who found that the impact of stochastic volatility on the free boundary for ordinary American call options is more pronounced for higher values of . Our conclusions may be due to the way volatility affects both the numerator and denominator of the asset yield ratio. Thus, there is a possibility that an increase in one asset price due to more volatile volatility may be canceled out by the same phenomenon in the other asset price.

As discussed in Section 4, increasing the jump intensities and introduces upward shifts in the early exercise boundary (as opposed to the upward pivots as seen in the other simulations). If no jumps occur in both asset prices (i.e. when both asset prices are modelled as correlated stochastic volatility processes), the boundary at maturity is and the entire curve lies much lower than when at least one of the asset prices has jumps. While it is not shown in Figure 10, the impact of the jump intensities is symmetric in the sense that, for example, the same boundary curve is generated when and when . It is also expected that changing the jump size density parameters (in our case, the mean and variance of the normal distribution governing and ) will also introduce upward or downward shifts in the boundary curve as these also directly affect the limit of the boundary at maturity. A similar effect may also be observed when assuming a different distribution for the jump sizes, e.g. the double exponential jumps assumed by Kou (2002).

We now proceed to numerical comparative statics on the discounted European and American prices. Here, we display the difference when the price generated after modifying a given parameter is subtracted from the option price solved with the parameters in Table 1. A common observation is that price differences vanish for deeply in-the-money American exchange options because of the value-matching condition. The point at which the price differences meet the baseline is the exercise boundary, which is more clearly explicated in Figure 10. In contrast, the price differences for deeply in-the-money European options dissipate more slowly, if at all as can be seen in some simulations.

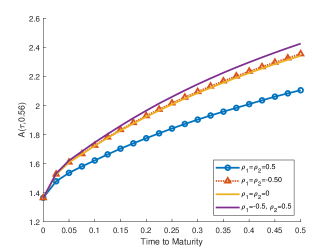

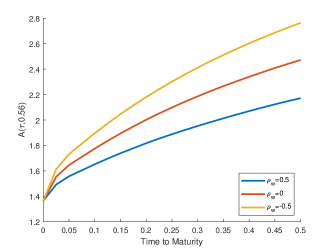

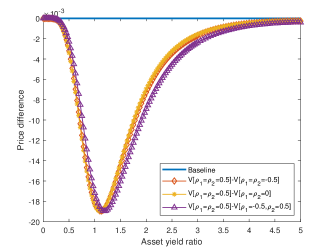

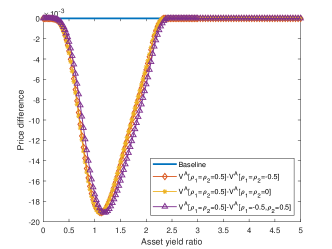

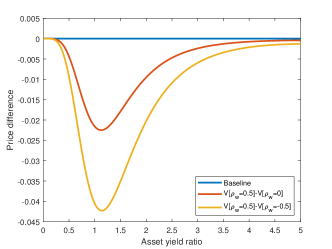

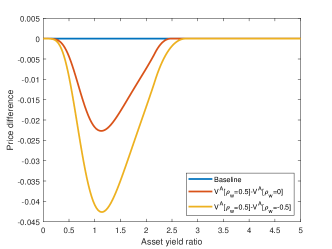

Figures 11 and 12 show the effect of the correlation coefficients on the discounted exchange option prices. In these simulations, we find that deviating from the default correlations in Table 1 resulted to higher MOL prices for both types of options. However, the price differences do not vary drastically between assumed alternative values for correlations with the Wiener process in the variance process. In contrast, price differences between cases are more pronounced when the correlation between the asset prices is changed. In particular, both types of options are more expensive when the asset prices are negatively correlated to each other, as there is a higher tendency for larger spreads between the prices of the two assets. From Figure 12, option prices are lowest when the assets are positively correlated with each other. In both analyses, the price differences are maximal when the options are at-the-money.

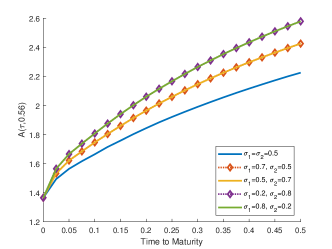

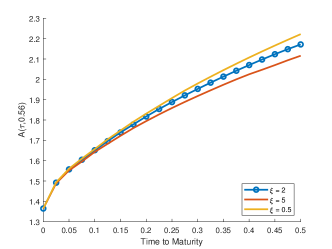

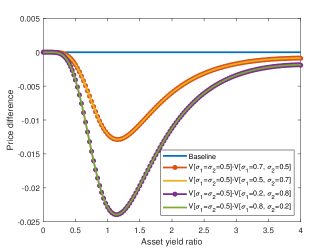

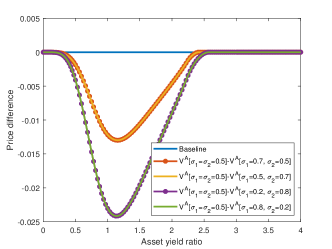

Option prices also tend to increase when the gap between the proportionality coefficients and in the diffusion term of the asset price dynamics increases, as indicated by Figure 13. Similar to the analysis on the early exercise boundary, it does not matter which asset is more sensitive to the instantaneous variance as the effect on option prices is symmetric. We note however that there is a noticeable price difference for deeply in-the-money European options.

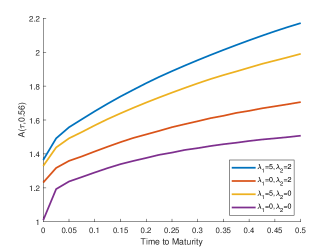

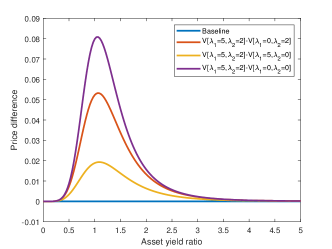

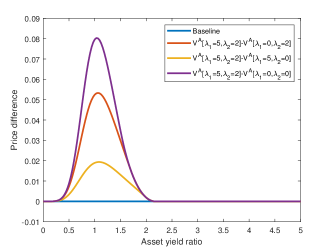

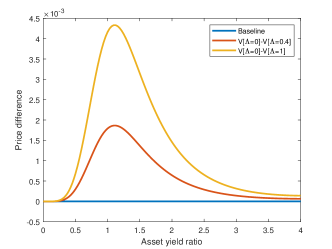

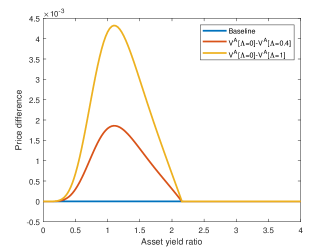

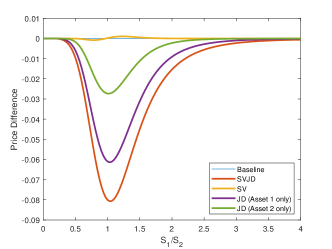

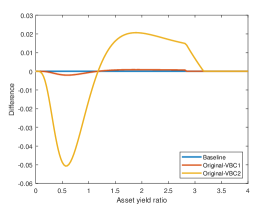

Figure 14 shows how the jump intensity rates affect the discounted exchange option prices. The baseline reference, where it is possible for both assets prices to jump, is priced the highest. The largest difference is observed between the baseline and the stochastic volatility case, where neither asset price jumps. While it is not shown here, we also observe the same symmetry in how and affect option prices, as was observed for the early exercise boundary. In the comparative static analysis presented in this section, changing the jump intensities result in the largest differences in option prices, reaching up to 0.08 when the option is at-the-money. The magnitude of differences may be affected, however, by the other choices for the jump size distribution and/or its parameters.

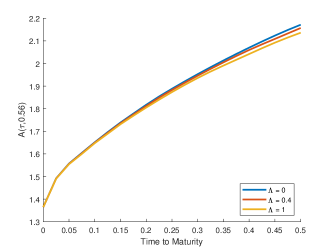

Figures 15, 16, and 17 exhibit the price differences resulting from varying the values of the stochastic volatility parameters. From Figure 15, it can be seen that increasing the rate of mean reversion tends to decrease the discounted exchange option prices. The same conclusion can be drawn for the market price of volatility, although there is a slight price difference even when the European option is deep in-the-money.

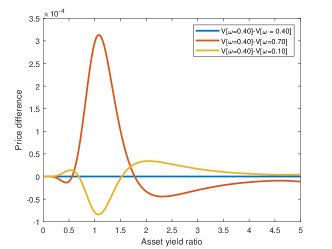

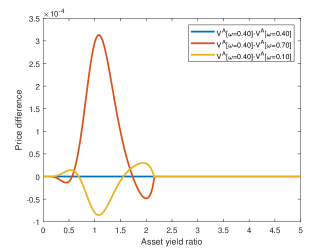

As seen from Figure 17, however, the effect of the volatility of volatility is less straightforward. Increasing (relative to the default ) results to prices which are lower when the option is near-the-money but higher when the option is either deeply out-of-the-money or in-the-money. The reverse is true for when the volatility of volatility is decreased. There also seems to be a noticeable difference for deeply-in-the-money European exchange options.

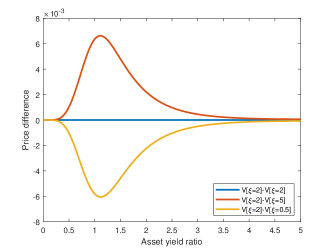

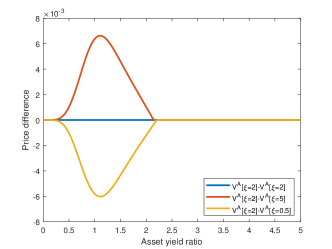

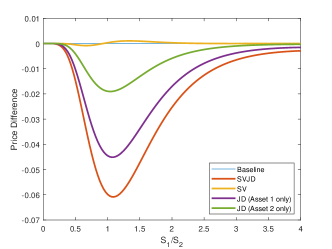

The next numerical experiment is concerned with assessing the impact of stochastic volatility and jumps to the discounted price of European exchange options. The base prices correspond to the pure diffusion case, for which a formula has been provided by Margrabe (1978). For simplicity, we assume no dividend yields for both assets. Furthermore, since the variance process is mean-reverting, we assume that the constant volatility for the pure diffusion case is for asset , as was done by Chiarella and Ziveyi (2013). The stochastic volatility case was simulated by setting the jump intensities to zero, but these were subsequently allowed to have nonzero values eventually building up to the default SVJD case. When exactly one of the jump intensities was equal to zero, it was assumed that this asset is driven by stochastic volatility dynamics whereas the other asset had both stochastic volatility and jumps. Here, we focus only on the European case, since as exhibited in the previous numerical experiments the American case behaves similarly, except for when the asset yield ratio exceeds the exercise boundary where the price differences vanish. Cases for a negative and a positive correlation between asset price processes are considered.

As seen in Figure 18, stochastic volatility prices are slightly higher than the constant volatility case when the option is out-of-the-money, but are lower when the option is in-the-money. This observation is consistent with the numerical results of Heston (1993) and Chiarella et al. (2009) for options on a single asset. The addition of jumps by allowing nonzero jump intensities generated higher option prices irrespective of the moneyness of the option, with the highest prices attained when both assets have SVJD dynamics. We find that price differences eventually vanish for large enough asset price ratios in the positive correlation case, but the differences persist in the negative correlation case (at least within the assumed range of values for the asset price ratio). In both positive and negative correlation cases, the SV and SVJD option prices converge to the Margrabe price when the option is deeply out-of-the-money. In contrast to the results of Chiarella et al. (2009), who found that the price differences invert from positive to negative (and vice versa) depending on the moneyness of the option, we find that price differences are consistently negative when jumps are involved. This may be attributed to how the jump and stochastic volatility parameters are chosen and the possibility that jumps may dominate stochastic volatility in terms of contributions to the overall variance in asset prices.

6.3. Effect of Alternative Boundary Conditions at

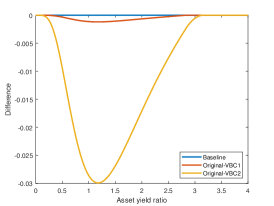

The final numerical experiment explores how MOL approximations of option prices and the early exercise boundary are affected by the use of Venttsel boundary conditions. Figure 19 shows the early exercise boundary, American option price, and American delta computed for each Venttsel boundary condition (38) and (38) using parameters values in Table 1. For the option price and delta, we exhibit the differences at and when compared to the base case that uses (29). As can be seen from the graphs, there is very little difference in the MOL approximations when either (29) or (38) is used. This is rather surprising as (38) is notably simpler than when (29) is applied to (27), which still contains second-order derivatives in . We furthermore note that the computation time when (38) is active is shorter than when (29) is used, indicating that using the Venttsel boundary condition may be computationally more efficient while delivering the similar results. The differences in option price and delta are much more pronounced when (39) is used, particularly when the option is at-the-money. Using boundary condition (39) also results to a much larger approximation of the early exercise boundary at compared to when either (29) or (38) is used.

We end this section with a disclaimer that these observations and conclusions were made for the specific parameter values we assumed in Table 1 and the modifications thereof introduced in each numerical experiment. We anticipate that the insights explored here may still hold for other parameter values or when a full calibration exercise with respect to actual data is implemented, but these conclusions might no longer be true in general.

7. Concluding Remarks

This paper discusses the application of Bjerskund and Stensland’s put-call transformation technique in pricing European and American exchange options under stochastic volatility and jump-diffusion dynamics. This technique allows us to reduce the number of dimensions in the main problem and write the option price and the associated IPDE as a function of time, the asset yield ratio, and the instantaneous variance level. With the inhomogeneous form of the IPDE for the American exchange option, we were also able to analyze the behavior of the early exercise boundary near maturity. It was found that the limit of the boundary at maturity is strongly influenced by the magnitude of the difference between asset dividend yields and the jump component of each asset price process. The numerical implementation in this paper complements the integral representations of the exchange option prices obtained by Garces and Cheang (2020) using Fourier and Laplace transforms.

Given the reduction in dimensions, we then formulate a method of lines algorithm to numerically solve the option pricing IPDE, thereby detailing and extending the method presented by Chiarella et al. (2009). As noted by researchers who have applied the MOL in option pricing, this method is particularly useful as it naturally computes for the option delta and gamma and minimal adjustments are required to calculate the free boundary associated with American options. While for simplicity our implementation uses constant parameter values, Algorithms 1 and 2 can easily be extended to parameters that are deterministic functions of time. However, adding more stochastic elements will result to a higher number of dimensions in the MOL implementation, which will then require additional iteration levels (see Kang and Meyer 2014, for example). As reported in previous work (Chiarella et al. 2009; Chiarella and Ziveyi 2013; Kang and Meyer 2014, among others), the MOL performs just as efficiently, if not more, than Monte Carlo simulations, numerical integration, and other numerical methods for solving IPDEs and PDEs, such as finite difference methods, componentwise splitting methods, and sparse grid approaches. Our numerical analysis in Section 5 confirms that the MOL indeed performs more efficiently to the Longstaff and Schwartz (2001) Monte Carlo approach.Algorithms 1 and 2 and the accompanying discussion in Section 5 can be easily modified and implemented to accommodate other payoff structures or underlying asset price dynamics.

Using the MOL approach, we were also able to assess the impact of the model parameters on the exchange option prices and the early exercise boundary. We find that the jump intensities have substantial impact on option prices as it is able to shift the early exercise boundary curves upward and generate the largest price differences relative to the default prices computed using parameters in Table 1. We also find the correlation parameters and the volatility constants of proportionality have a considerable impact, while the parameters of the variance process have the least impact. The presence of stochastic volatility and or jumps in one or both assets also has a considerable effect on option prices when the asset prices are positively or negatively correlated with one another. We note however that these conclusions are true for the specific set of parameter values used in the numerical approximation and may not hold in full generality. A complete analytical comparative static analysis remains to be seen in literature, but nonetheless we have shown that jumps and stochastic volatility have considerable impact on option prices and the early exercise boundary.

Our analysis also showed that 38 at the far variance boundary is a plausible alternative to the often-used vanishing vega assumption, producing comparable results with less computational time. We note however that the choice of boundary conditions is strongly affected by the calibration of model parameters. Specifically, if calibration yields parameters which violate either the Feller condition or the condition for the viability of Venttsel boundary condition 38, then alternative conditions must be imposed on the boundary of the computational domain.

A formal convergence analysis of the MOL is also an issue to be investigated in future work, although the algorithm we presented converges for all reported parameter values. An application of the put-call transformation transformation and/or the MOL in pricing multi-asset derivatives under other asset price model specifications (e.g. Lévy processes, regime switching models) is also a topic that we aim to explore in future studies. In a future study, we also aim to see how the MOL can be extended when pricing takes place in the risk-neutral world (i.e. the second asset price then becomes a separate spatial variable) or when additional risk factors are included, such as multi-factor stochastic volatility (Christoffersen, Heston, and Jacobs 2009) and stochastic interest rates.

Disclosure Statement

The authors report no potential conflict of interest arising from the results of this paper.

References

- Adolfsson et al. (2013) Adolfsson, Thomas, Carl Chiarella, Andrew Ziogas, and Jonathan Ziveyi. 2013. “Representation and Numerical Approximation of American Option Prices under Heston Stochastic Volatility Dynamics.” Quantitative Finance Research Center Research Paper 327, University of Technology Sydney .

- Alòs and Rheinlander (2017) Alòs, Elisa, and Thorstein Rheinlander. 2017. “Pricing and hedging Margrabe options with stochastic volatilities.” Economic Working Papers 1475, Department of Economics and Business, Universitat Pompeu Fabra .