Credit Spread Approximation and Improvement using Random Forest Regression

a: Université de Limoges, LAPE, 5 rue Félix Eboué, 87031 Limoges Cedex, France

b: JPLC SASU, 54 avenue de la Révolution, 87000 Limoges, France

Draft. Not edited.

Please do not circulate.

Abstract

Credit Default Swap (CDS) levels provide a market appreciation of companies’ default risk. These derivatives are not always available, creating a need for CDS approximations. This paper offers a simple, global and transparent CDS structural approximation, which contrasts with more complex and proprietary approximations currently in use. This Equity-to-Credit formula (E2C), inspired by CreditGrades, obtains better CDS approximations, according to empirical analyses based on a large sample spanning 2016-2018. A random forest regression run with this E2C formula and selected additional financial data results in an 87.3% out-of-sample accuracy in CDS approximations. The transparency property of this algorithm confirms the predominance of the E2C estimate, and the impact of companies’ debt rating and size, in predicting their CDS.

Keywords: Risk Analysis; Finance; Structural Model; Random Forests; Credit Default Swaps

1 Introduction

The ability to accurately apprehend companies’ credit risk is at the core of financial professionals’ concerns and an extensive branch of literature is dedicated to this matter (e.g. Merton,, 1974; Black and Cox,, 1976; Vasicek,, 1987; Finger et al.,, 2002). Since the mid-nineties, the uncertainty regarding an obligor’s capacity to fulfill its contractual duty can be insured by a derivative, the Credit Default Swap. However, not all firms have actively traded CDS, leading to the development of estimations. Merton, (1974) was the first to define a relationship between a company’s probability of default and its capital structure. He used the option pricing framework to relate the three balance sheet segments, i.e. asset, debt and equity. Black and Cox, (1976) added the possibility for a default to occur prior to maturity. But numerous approximations were developed in the private sector when these derivatives started to be traded. For obvious reasons, many of these models are highly proprietary and are not accessible to researchers.

Despite being developed by practitioners, the CreditGrades model (Finger et al.,, 2002) is available for use to everyone. This formula relies on companies’ asset values dynamic modeled with a diffusion process and a default barrier that can be crossed prior to maturity as in Black and Cox, (1976). Overall, academics have focused on strengthening the definitions of some variables of the CreditGrades model to improve its accuracy. For instance Zhou, 2001b takes into account market changes using a jump-diffusion process. Sepp, (2006) makes the model even more complex assuming that the firm’s asset value process follows a double-exponential jump-diffusion and that the variance of the firm’s assets return is stochastic. Another extension of the CreditGrades model, using implied (and not historical) volatilities to take into account both equities volatilities and leverage, is proposed by Stamicar and Finger, (2006). More recently, Escobar et al., (2012) have offered a multivariate extension of the CreditGrades model under the assumption of stochastic variance and correlation among the companies’ assets. Credit Default Swap is a topic of interest in much recent operational research literature (Guarin et al.,, 2011; Tomohiro,, 2014; Cont and Minca,, 2016; Chalamandaris and Vlachogiannakis,, 2018; Koutmos,, 2018; Irresberger et al.,, 2018), but in practice, models for traded CDS spreads tend not to be popular among portfolio managers. Although the aforementioned models provide very close approximations (e.g. Imbierowicz and Cserna,, 2008), they remain prohibitively complex.

In this paper, our aim is to develop an intuitive, accurate and open-access instrument to approximate CDS spreads, intended for use by credit market practitioners or as a reliable proxy for researchers. We first provide an elementary formula, called Equity-to-Credit (E2C henceforth), comparable to the CreditGrades model in terms of accuracy. We then further improve the precision of this straightforward formula using machine learning tools, which have become more prevalent in the financial sector.

The first contribution of this paper is the development of a concise and broad-based approximation assessing credit spreads. The Equity-to-Credit formula which we develop is a pared-down elementary equation inspired by RiskMetrics Group’s CreditGrades model (Finger et al.,, 2002). The formula relies on two main mathematical concepts: the reflection principle and Gauss’s inequality. The probability of default is based on the reflection principle and its symmetrical property. Its upper bound is specified with Gauss’s inequality which is a refinement of Chebyshev’s inequality, converted to a conservative equality following Roy’s “principle of safety first” (Roy,, 1952). We obtain a simple and transparent credit approximation which only depends on leverage, equity volatility and standard debt recovery parameters, assessed on a conservative setting and CreditGrades parameterization.

We then use the CreditGrades model as a comparative basis to empirically assess the E2C formula’s reliability in the second part of this paper. More specifically, both models’ results are confronted to the actual CDS. The E2C formula proves to be more correlated and a better regressor than the alternative model. In addition, a comparison is performed gathering data by buckets of senior unsecured debt rating and industrial sectors. The analysis is done with medians and truncated means, both proving in favor of the E2C formula. Consistently with the existing literature, our 2016-2018 sample confirms that structural models generally underpredict actual CDS spreads. Rodrigues and Agarwal, (2011) reach the same conclusions for three structural models including the CreditGrades model. Moreover, we notice that both the E2C and the CreditGrades models yield lesser underestimations for riskier companies’ spreads, in line with Teixeira, (2007). Notably, the E2C returns closer estimates for the financial sector where CreditGrades, and Merton models more generally, are traditionally poor.

By construction, some parameters influencing credit spreads are missing from structural models such as our E2C. Therefore, our second contribution in this paper is an improvement of our CDS approximation accuracy, taking into account selected complementary features. We suggest the use of a supervised learning algorithm which allows the treatment of a multivariate universe, composed of the E2C and a limited number of chosen variables. The E2C formula being only based on equity information, a credit derivatives index is set as a time-specific independent variable. Company-specific variables are then added, such as credit ratings, size, industrial sector, and geographical location.

Its intelligibility and its ability to handle reasonable sample sizes were the main reasons driving our choice of the random forest regression algorithm (Breiman,, 2001). The purpose is to average multiple randomly bootstrapped decision trees (“bagging”, in Breiman,, 1996) built with subsets of the features randomly chosen at each node. Once the hyper-parameters are tuned, the algorithm is parallelized to decrease computation time. The main result is an 87.3% out-of-sample accuracy which emphasizes the power of this machine learning algorithm and our database to approximate CDS spreads.

In addition, this algorithm’s choices are easily accessible through the transparency of its decisions at each split, displaying the feature it chooses in order to reduce the error. This allows us to evaluate each feature’s contribution in predicting the CDS spreads, using two methods. First, we measure the improvement brought by a specific selected variable at each node. Then, the importance of the variable is measured by how much it decreases the model accuracy when this feature is randomly permuted. This two-pronged evaluation confirms that our E2C formula is the main variable selected by the decision trees when approximating the CDS. Additionally, it underlines the next best source of improvements as the company’s credit rating and its size.

The remainder of this paper is organized as follows. In the next section, we present the main steps to build our E2C formula. We then confirm that the accuracy provided by the E2C is at least as good as its closest parent’s. Finally, the approximation accuracy is improved using random forest regressions on the E2C and other independent variables.

2 The E2C Formula

In this section, we present the main steps to build the E2C formula, leading to an elementary CDS approximation equation. The stock price is defined as an additive stochastic process, such that:

We assume that the stock price varies by a random amount of standard deviation per time unit. Where stands for a level of volatility and a symmetric standard random variable: has zero mean and unit variance but is not necessarily assumed a normal distribution. Hence, the expected value and the variance of the stock price process are E[] = and Var() = .

Once the prices’ path model is defined, we derive the probability for a bankruptcy to occur. In this kind of model, the failure happens if the stock price reaches a certain level. For obvious economic reasons, it is set at zero. Therefore, we look for the probability that a stock price reaches zero at any time prior to a certain maturity .

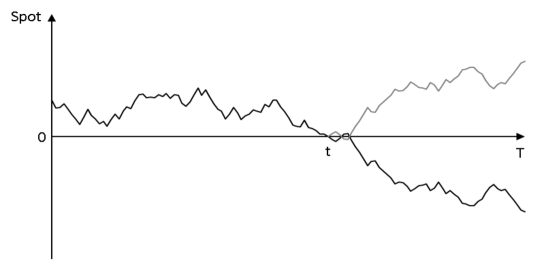

Knowing that the process starts at , the probability of reaching at any time is measured. According to the reflection principle (Lévy,, 1940, see Figure 1 below), if the zero value is reached before , each possible path ending positively has a symmetric counterpart ending negatively from this point until . In other words, if the drift is null, the number of all paths reaching zero is exactly twice the number of paths terminating below zero.

Hence,

According to symmetry:

| (1) |

The idea above is closely related to the barrier concept introduced by Black and Cox, (1976) which assesses the first time a firm’s asset value drops below a certain time-dependent barrier.

To define this probability boundary and for simplicity, we note a random variable corresponding to . The boundary could be estimated with Chebyshev’s well-known over-conservative inequality (1867), . However, a lesser-known refinement developed by Gauss, (1821) (or more recently, in Perks,, 1947) allows to sharpen Chebyshev’s boundary by a factor on the condition that is unimodal with a mode . This assumption is correct regarding our model with . Applying Gauss’s inequality to our main equation 1, we get:

For simplicity and economic sense, we get rid of the inequality operator based on the paper of Roy, (1952). Following his “principle of safety first” and a conservative objective, we maximize our upper bound. It has a financial sense therefore to conclude:

Dividing this probability by the time horizon, we define the hazard rate .

| (2) |

Using R as the asset specific recovery rate, we model the credit approximation as:

| (3) |

Next, we derive a closed-form expression for the volatility parameter based on the CreditGrades assumptions, and focusing on the downside evolution of the stock price. In fact, in this asymmetric approach which is presented in Appendix A, the above equation 3 is still valid with a “downside delta” , and is justified by reconsidering the Gauss inequality on only one side of the distribution.

Much research has been done on the link between bankruptcies, assets, debts and equities, notably by Merton, (1974) and Black and Cox, (1976). A company defaults if a certain level of insolvency is reached. In line with the assumption of the CreditGrades approach, we apprehend this level, or default barrier, as the remaining amount of the firm’s assets in the case of default, corresponding to the recovery value received by the debt holders. We note this amount , where is the average recovery on the debt and the firm’s debt-per-share.

To keep the simplest expression consistent with the definition of (such that the asset value when ), we write . With being the equity volatility, the equity and asset volatilities are related as follows:

Then, as such is not constant, we anchor it by emphasizing its downside boundary values:

-

•

At , , therefore,

-

•

If the default occurs, thus, , hence,

And we retain for the average of these values, using the geometric average as we are dealing with magnitudes. In addition, it is indifferent whether the average is squared or the squared values are averaged.

Hence,

And, as

We get:

where is the ratio “debt to enterprise market value” of the company, also known as the Market-Adjusted Debt (MAD) ratio. The final credit approximation222The hazard rate is null when the debt is null, which is another property from the use of a geometric average. is computed replacing this result in equation 3.

| (4) |

The above formula is thereafter referred to as the Equity-to-Credit (E2C) formula. The E2C is computed using both market and balance sheet inputs – on the one hand the current stock price and its volatility, and on the other hand the company’s debt-per-share. The debt-per-share is computed following the CreditGrades method, further detailed in Appendix A. With regard to the volatilities, for each company, both historical and implied ones are extracted for different maturities. The historical volatilities are computed over 30, 60, 120, 200, 260 and 360 days and the implied volatilities correspond to 3, 6, 12, 18 and 24 months options maturities. After a few tests, we retain the implied volatilities for strikes of put options “out of the money” by 0.5 standard deviation. For robustness, the E2C’s volatility parameter is defined as the median of all the above available volatilities. In general, recovery rates of traded CDS are set at 0.4 corresponding to the developed market average. However, being conservative, we set it at 0.3, as some practitioners do and as it is commonly attributed to emerging markets. After some empirical tests, the RiskMetrics team chose an of 0.5 for their model. Hence, knowing that the CreditGrades parameterization is relevant for our equation, we calibrate our model with and .

The equation presented in this section is very intuitive as the variables’ impact is consistent with market specialists’ expectations. This credit spread approximation is an increasing function of the debt and the corresponding stock volatility. On the other end, when the share value increases, the spread value decreases.

3 E2C and CreditGrades Models Comparison

3.1 Data and Softwares

Our panel data sample is a blend of market and fundamental reports information over 308 listed companies from 27 countries (of which 12 are gathered in a single Eurozone group)333Country (number of Firms per Country) list: Australia (14), Canada (5), Denmark (2), Eurozone (78), Great Britain (22), Hong Kong (6), India (3), Japan (22), Malaysia (1), New Zealand (2), Norway (2), Singapore (1), South Korea (8), Sweden (3), United States (139).. Each company belongs to one of the following ten major sectors: basic material, communications, consumer cyclical, consumer non-cyclical, energy, financial, industrial and utilities444Technology and diversified sectors are not displayed, they only respectively count 8 and 2 companies on average.. The data set spans weekly, every Friday over three years (i.e. 155 dates), from 2016-02-03 until 2018-12-28, and is based entirely on Bloomberg L. P. data.

Data preparation and handling is entirely conducted in Python 3.6 (Python Software Foundation, 2016), relying on the packages “numpy” by Van Der Walt et al., (2011), “pandas” by McKinney, (2010) and for visual outputs on “matplotlib” by Hunter and Dale, (2007). Linear regressions are performed with Stata 13.0 (2013). Moreover, we use “sci-kit learn” by Pedregosa et al., (2011) for the random forest and the “randomForest” R package by Liaw and Wiener, (2002) to confirm the results.

3.2 Basic Analysis

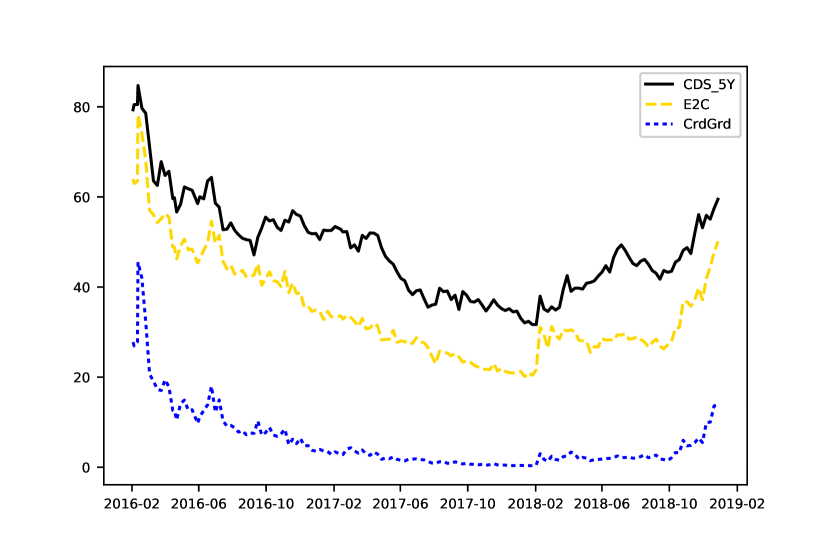

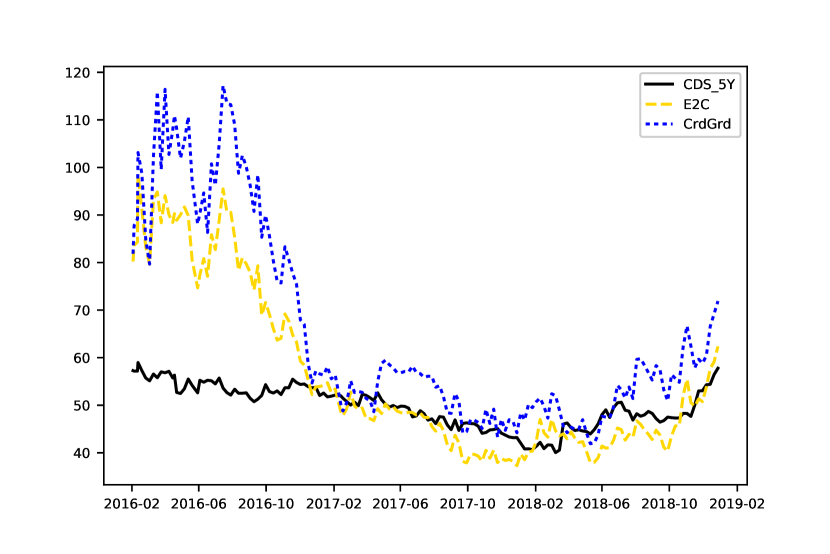

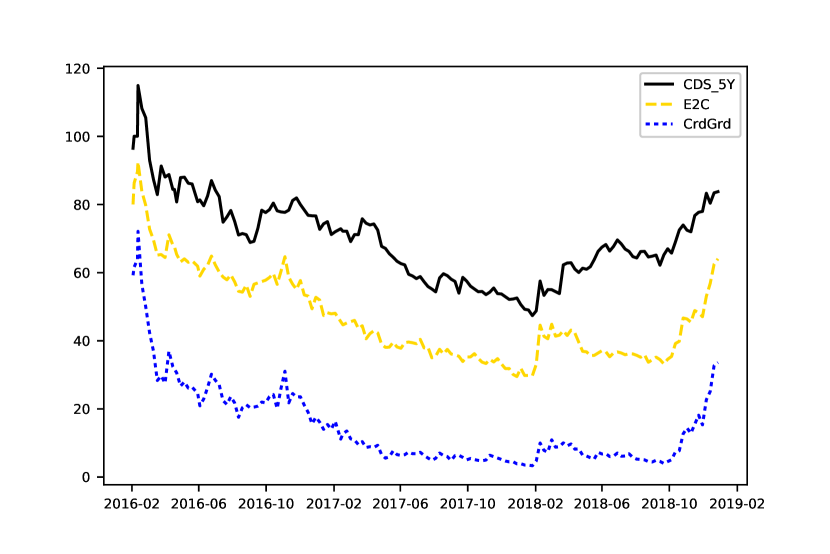

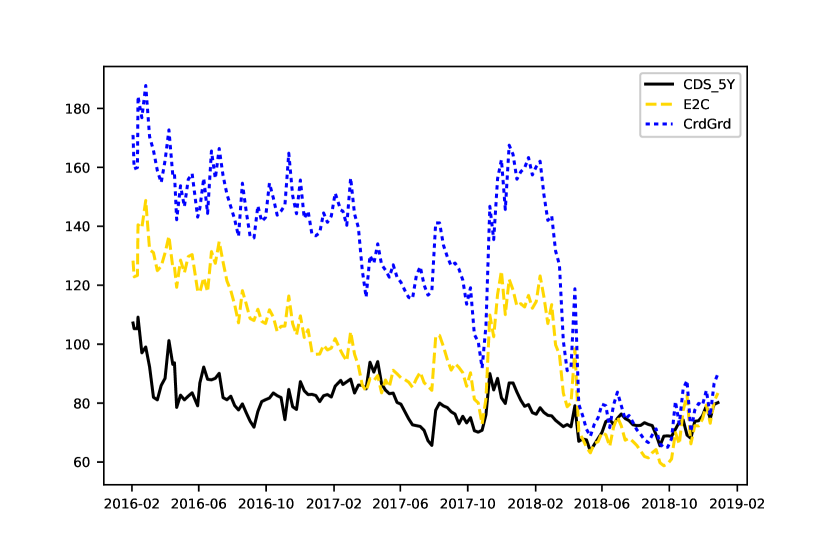

Based on the data sample defined above, we compare the two CDS spreads approximations obtained by our E2C formula, i.e. equation 4, and the CreditGrades version defined by RiskMetrics Group. This version requires the use of the Cumulative Normal distribution and logarithm functions, and an additional parameter which stands for the standard deviation of the global recovery rate ( according to the RiskMetrics paper, 2002). To convert the CreditGrades survival probabilities to spreads, we define the maturity years. All other parameters are set as those defined previously for the E2C. We analyze the 5-year CDS against the E2C equation defined above, and against the CreditGrades estimate , where is the hazard rate implied by CreditGrades (described in Appendix B).

According to the descriptive tables available in Appendix B, the E2C and CreditGrades outputs are relatively close to one another and more importantly to the 5-year CDS. Both approximations have a lower median and are slightly more volatile than the actual CDS. A comparative table of the quality of the CDS approximations at a country level produced by each of these models is available in Table B.2. Moreover, the E2C’s density function shape is closer to the CDS, as it is more right-skewed and leptokurtic than the one obtained with CreditGrades. We also notice, for all curves, a higher heterogeneity between companies than within. Finally, we compute the averages of each firm’s correlation over time and of each date’s correlation over all firms. In both correlation tables, E2C is highly correlated to CreditGrades with a coefficient around 90%. Above all, E2C is more correlated to the 5-year CDS than CreditGrades between companies and through time. Across the board, our approximation shows conclusive results.

We further study the predictivity of these equations with econometric techniques. According to the appropriate testing555In both cases, panel (fixed-effects) models are chosen over pooled OLS. The null hypothesis of homoscedasticity of the Breusch and Pagan Lagrangian multiplier test is rejected. Then, we perform a test of overidentifying restrictions (similar to Hausman test, with ) on our model which includes time-variant variables. The result indicates that the fixed-effects model should be preferred over the random-effects model., we handle both regressions (CDS onto E2C and onto CreditGrades) with fixed-effects models. Thus, both company-specific characteristics and time must be taken into account. In the summarized results below (Table 1), we highlight the , and in particular the along with the fixed-effects model.

| CDS_5y | CDS_5y | |

| E2C | 0.637∗∗∗ | |

| (203.81) | ||

| CrdGrd | 0.671∗∗∗ | |

| (162.29) | ||

| constant | 58.16∗∗∗ | 44.41∗∗∗ |

| (103.7) | (61.26) | |

| 47476 | 47476 | |

| -within | 0.468 | 0.358 |

| -between | 0.796 | 0.618 |

| -overall | 0.692 | 0.543 |

| t statistics in parentheses | ||

| ∗ , ∗∗ , ∗∗∗ | ||

With an over 10 points of percentage above the CreditGrades regression, the E2C formula is shown to approximate the CDS with globally more reliability than CreditGrades.

3.3 Rating and Sectorial Analyses

Finally, we focus on two universes in which firms’ repartition is overall well balanced: unsecured senior debt ratings and industrial sectors. The E2C results are compared, along with those of CreditGrades, to the actual CDS spreads using two methods. The basic averages being exposed to outliers, we firstly choose to compare their medians. The second method compares the truncated means, where averages are computed after having dropped the extreme 10% top and bottom points. For the sake of visualization, we summarize our results below in Figures 2 and 6.

3.3.1 Debt Rating Comparison

Our dataset is composed of senior unsecured debt ratings provided by Standard & Poor’s and Moody’s. Unfortunately, their rating scales are different, and their ratings for specific firms and dates might be different. This issue is overcome through the following guidelines: if both agencies provide the same grades (based on the comparison scale in Santos,, 2008), the corresponding grade is chosen; if only one agency gives a grade, this grade is selected; and if the grades are different, still being conservative, the worst one is kept. Our sample includes no AAA grades and too few AA, therefore we group them in a global A bucket. Furthermore, too little data for firms rated below B is available in our sample, so we remove them for this comparison.

In all cases, the E2C formula provides a closer median to the CDS than CreditGrades, with the exception of the double-B grade for which E2C and CreditGrades medians are almost alike. Regarding the truncated mean, E2C is indubitably better for the single B and comparable for single A and triple-B. These positive results are strengthened by the measures of accuracy shown in Appendix B, Table B.5. Additionally, we find that these structural models do not underestimate spreads for riskier companies (cf. Teixeira,, 2007).

3.3.2 Industrial Sector Comparison

The firms are classified among ten major sectors (introduced in the above data section, 3.1). The sectoral comparisons are displayed below based on the same metrics.

Except for utilities and financial, we reach the same conclusions as Rodrigues and Agarwal, (2011)666Their study includes the CreditGrades model., Lardic and Rouzeau, (1999) and Eom et al., (2004) who emphasized that structural models generally underpredict the observed credit spreads, at least for low levels of risks. Indeed, it is hard to define and calibrate a meaningful process for the firms’ asset values (Schönbucher,, 2003). Those are generally modeled following continuous diffusion paths, and thus are prevented from reaching the default barrier in very short time-spans, as may conceivably occur in reality. Zhou’s work (1997; ) overcame this issue by introducing a jump-diffusion process, at the cost of further complexity (cf. Section 1). In addition, credit spreads bear residual agency and covenant risks, which are not shared by equity. Regarding the median, it is clear that in every case, the E2C formula approximates the CDS spreads at least as well as CreditGrades. The E2C approximations are clearly superior for basic materials, communications, consumer cyclical and non-cyclical, energy and industrial. Almost identical conclusions are reached computing the truncated mean. E2C results are unquestionably better for basic materials, communications, industrial, utilities and financial. The latter is particularly interesting as it is a key sector where CreditGrades, and more generally “Merton” models, are traditionally poor. These encouraging charts are confirmed by the measures of accuracy shown in Table B.6 of Appendix B. We now know, at least with these samples, that our simple estimation is at least as good as CreditGrades in almost all of the above cases.

After the positive statistics of section 3.2, the above detailed analysis in terms of rating and sector confirms the satisfactory level of accuracy of the E2C formula with regards to the CreditGrades model. We therefore provide credit market practitioners with an equation which is slightly better than its closest parent, the CreditGrades model, while surpassing it in terms of intuitiveness and clarity.

The period studied in this paper (2016-2018) was overall characterized by low volatilities and highly expansive monetary policies, limiting our assessment of the E2C formula’s reaction to changes in the volatility regime. However, we performed an OLS analysis at dates of higher volatility within our data sample. We chose to match the lower bound of the 3-month VIX volatility index777Which is steadier than the VIX index. during the 2007-2008 financial crisis, which was at 20%; a threshold888As robustness check, the volatility analysis was performed for above the mean and at the 75% quantile, obtaining the same results. exceeded 20 times out of our 155 dates (i.e. 6078 observations). The results available in Table B.7 (Appendix B) show a stable accuracy for E2C even when the market is more volatile999Table B.7 (Appendix B) provides corresponding results for CreditGrades as well..

4 Approximation Improved by Random Forests

4.1 Sample Construction

The previous positive results give us ground to use and test our approximation further. More precisely, we look to improve our CDS approximation using the simple E2C formula and some additional input variables, and the actual CDS spreads are thereafter used as labels to train supervised learning algorithms. As usual, the original sample is split between training and test sets; and the results are checked with traditional error-squared metrics.

We suppose that the major part of the CDS approximation should be explained by the E2C formula, which is based on equity information. But CDS are evolving on a different market and thus are not only company-dependent but also correlated to the overall credit market. Therefore, we add the most liquid Investment Grade CDS index, the IG CDX101010As robustness check, the Itraxx & HY CDX indexes and the VIX 3-month volatility index were set as independent variables; various combinations led to similar results., which evolves through time but is not company-dependent. The default likelihood of a debtor is qualitatively and quantitatively assessed by a credit rating agency and disclosed with a credit rating grade. Obviously, the grade level should have an impact on the corresponding CDS spread. Companies’ size should also matter, being related to a level of importance and liquidity and linked to a stability concept, thus being integrated in CDS levels. This latter independent variable is measured by the market capitalization. It is worth noting that debt ratings and size are company-specific but not strongly time-dependent. Finally, companies’ industrial sectors and geographical locations111111The currencies stands as proxy for geographical locations. are included as easily accessible additional variables which satisfy the same criteria.

Before running our algorithms, we perform light features engineering. According to LeCun, (2012), “to efficiently perform a basic machine learning algorithm, it is fundamental to pre-process the data, reduce dimensions and extract hand-crafted, domain specific features”. First, points with one or more missing data are removed (8% of our data sample), leaving 47,476 observations. Incidentally, random forests are generally robust to numerical instabilities, so there is no need to remove multicollinearity and features with little variance. There is also no need for monotone functions such as centering, scaling or Box-Cox transformations, to which random forests are invariant. The second step in feature engineering concerns the handling of three non-numeric polytomous variables, i.e. countries, industrial sectors, and debt ratings. We perform a label encoding for the unsecured debt ratings, which are an ordinal variable. However, countries and industrial sectors are plain non-ordinal categorical values, which we handle with one-hot encoding121212As usual, for each binary variable group, the dummies with the fewest observations (here, “CTRY_MYR” and “INDUSTRIES_DIVERSIFIED”) are removed. (if countries and industrial sectors were converted through label encoding, artificial relationships between the values would be enforced, whereas creating dummy variables dilutes the features’ strength). After a short presentation of our metrics, we run the algorithms on 4 independent variables and 23 dummy variables.

The in-sample set is built by randomly removing 20% of the companies and 20% of the dates. This method leaves us with an out-of-sample standing for 36% of the whole dataset. The approximation accuracy is assessed using a well-known econometric measure, the R-squared131313. Other distance-related metrics, such as the relative absolute and squared errors, deliver the same conclusions.

4.2 Random Forest Regressions

4.2.1 Algorithm Description

An efficient algorithm minimizes both the bias and the variance. Generally, decision trees deliver a low bias but are, by construction, prone to overfit. Therefore, ensemble methods (Opitz and Maclin,, 1999) running multiple trees are appropriate for relevant predictions. Specifically, we choose a meta-algorithm called bootstrap aggregating (or “bagging”, in Breiman,, 1996) which builds multiple trees from a training set’s sample, randomly drawn with replacement. Bagging contributes to reducing the variance and avoiding overfitting. In the process known as random forest algorithm, developed by Breiman, (2001), this property is reinforced by the random selection, at each node, of a subset of the features used for splitting. Earlier work on random forests had also been launched at Bell Laboratories by Ho, (1995, 1998). This random subset might slightly increase the bias along with the decrease in variance (bias-variance tradeoff).

Random forests have recently been used within the fields of economics and finance (Nyman and Ormerod,, 2016; Khaidem et al.,, 2017; Tanaka et al.,, 2016; Behr and Weinblat,, 2017; Yeh et al.,, 2012). The validity of the use of random forests among a wide choice of learning algorithms has been studied, and confirmed, by Fernandez-Delgado et al., (2014). Brummelhuis and Luo, (2017) further verify this use in the context of CDS proxy construction.

Even though recent machine learning research is more oriented toward deep learning algorithms (Badrinarayanan et al.,, 2017; Sun et al.,, 2018; Sangineto et al.,, 2018), recent papers in applied machine learning have shown that the outputs of deep learning and ensemble based methods are comparable, at least for reasonable sample sizes. An argument in favor of deep learning is its marginally better accuracy (Ahmad et al.,, 2017) although random forests have in some cases outperformed neural networks (Liu et al.,, 2013; Rodriguez-Galiano et al.,, 2015; Krauss et al.,, 2017). However, our own priority in this paper is to keep our methods as simple and above all as understandable as possible, leading us to strongly lean in favor of random forests. Beyond performing an internal cross-validation, random forests require less parameter tuning (Ahmad et al.,, 2017). As far as transparency goes, random forests are also preferable to neural networks, which are often considered to be black boxes (although see Shwartz-Ziv and Tishby,, 2017, for a recent improvement).

While random forests are generally run with unpruned classification and regression trees (CARTs, in Breiman et al.,, 1984), limiting the trees’ depth is an option. This has no negative impact in terms of overfitting, and has the positive result of contributing to faster computation. Consequently, we set a maximum depth to the trees, and choose to run them in parallel for further speed. The following is a brief explanation of the random forest algorithm, based on the notations of Hastie et al., (2009). At step 1(b), we shortly present a decision trees algorithm.

-

1.

for b= 1 to B:

-

(a)

draw a bootstrap subset from the original dataset.

-

(b)

grow a decision tree using the following process:

-

i.

use a greedy algorithm seeking the splitting feature among a randomly selected subset of the features () and split point that solve:

-

ii.

once the best fit found, partition the data in two regions (, )

-

iii.

repeat (i) on each resulting region until a leaf node in all the branches of the tree is found, or the maximum depth is reached.

-

i.

-

(a)

-

2.

output the ensemble of trees .

Thereafter, the prediction on a new point from the OS is made using the function:

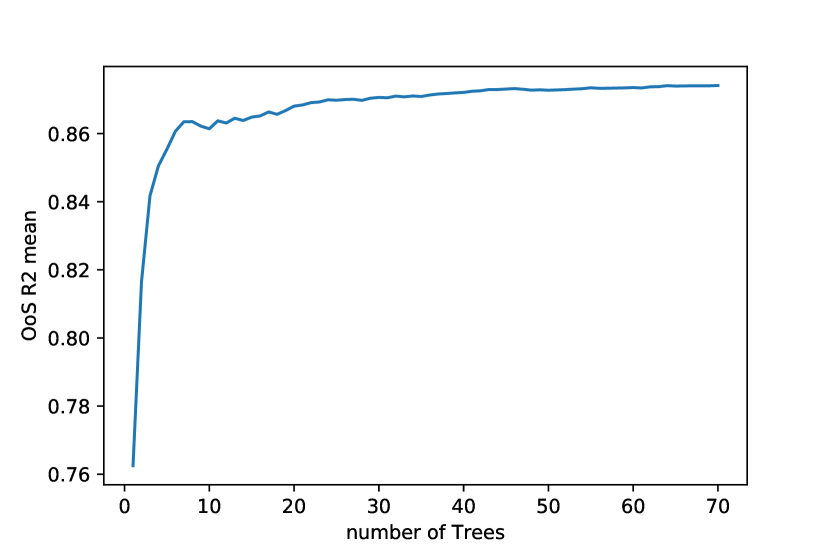

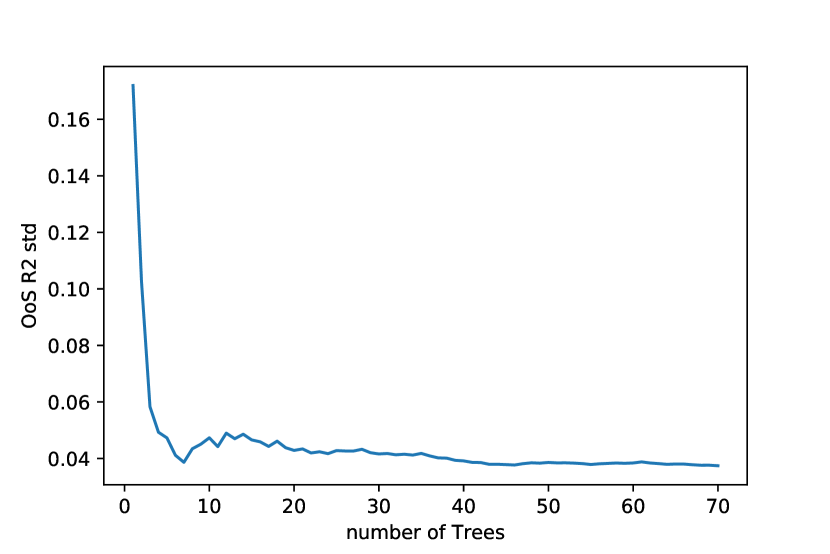

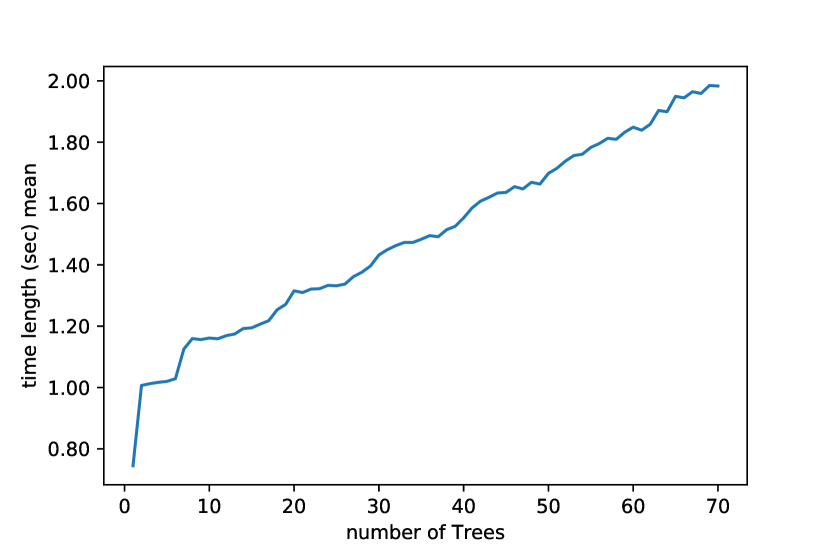

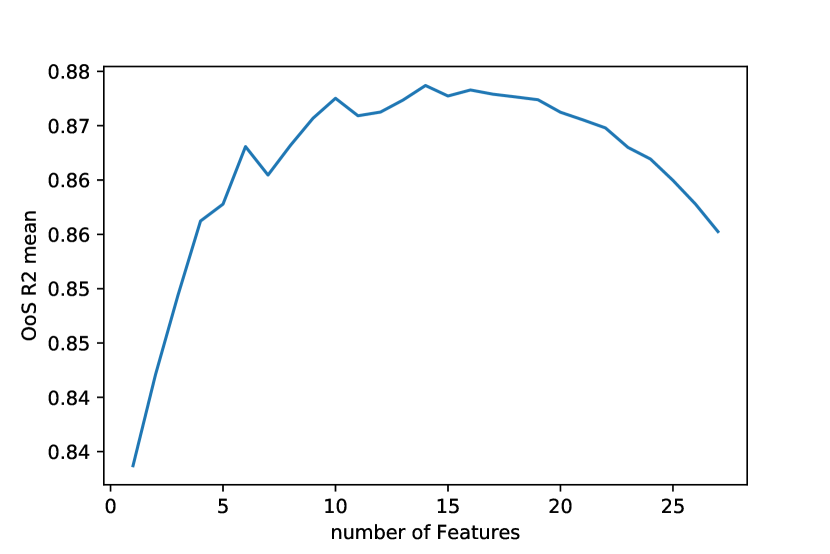

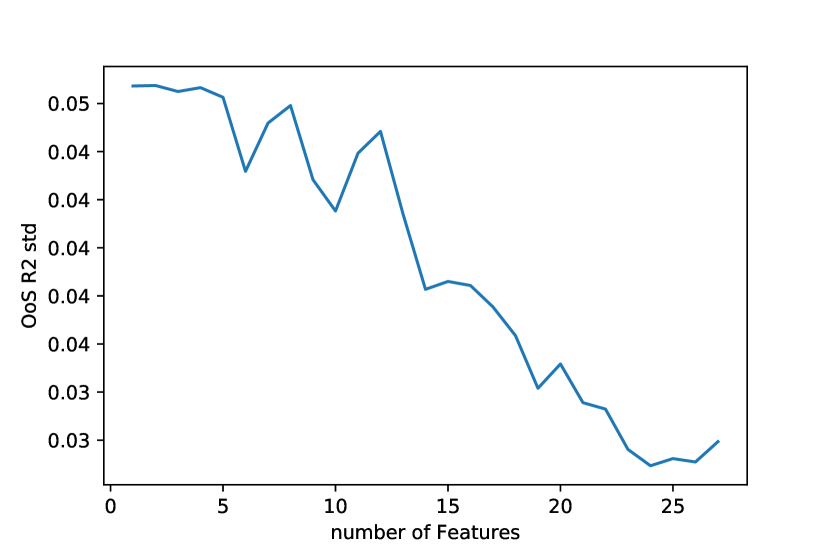

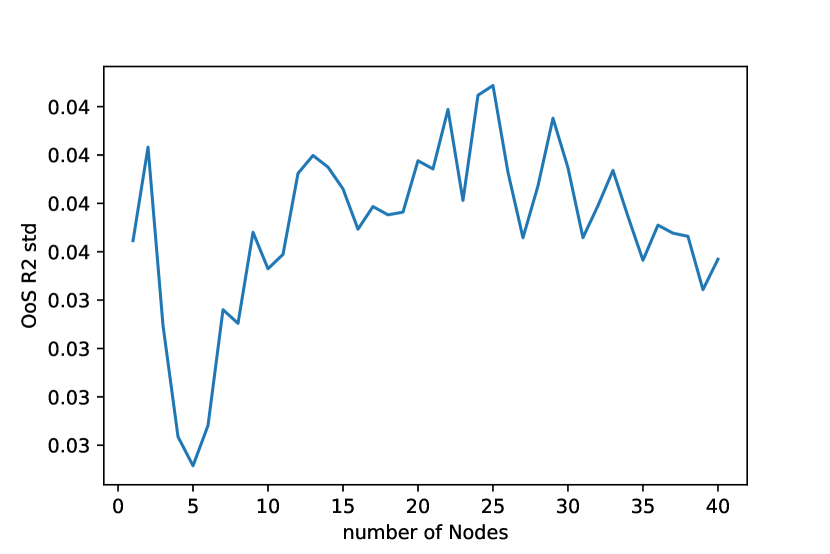

Random forests require to set at least two hyper-parameters. First of all, we determine the number of random trees we want the algorithm to run. While more trees reduce the variance, we choose as usual in function of accuracy constrained by the time of computations. Figure 14 summarizes various criteria supporting our decision.

Thereafter the chosen number of random trees is set at 50. Secondly, we set the number of features randomly selected at each node. According to Breiman, (2001), having categorical and dummy variables, should be set at two or three times . This parameter is thus set at 15, a number additionally confirmed by Figure 15, maximizing the averaged accuracy while minimizing its variance.

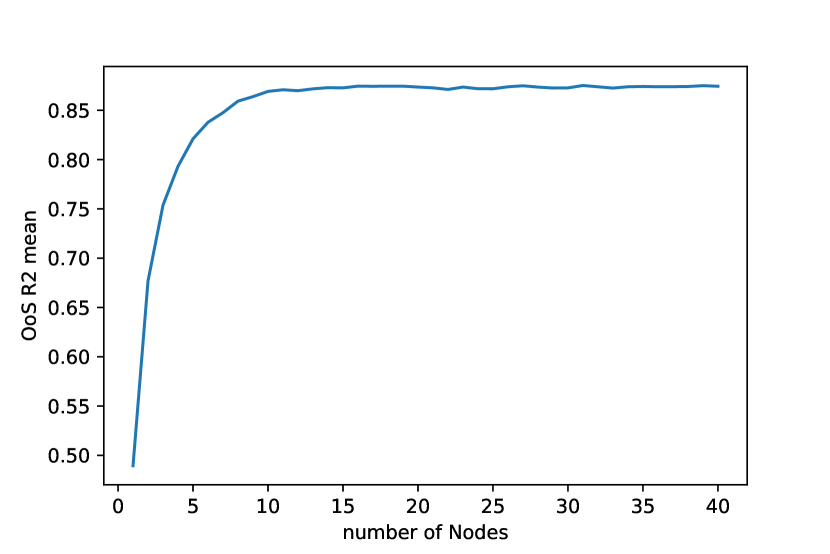

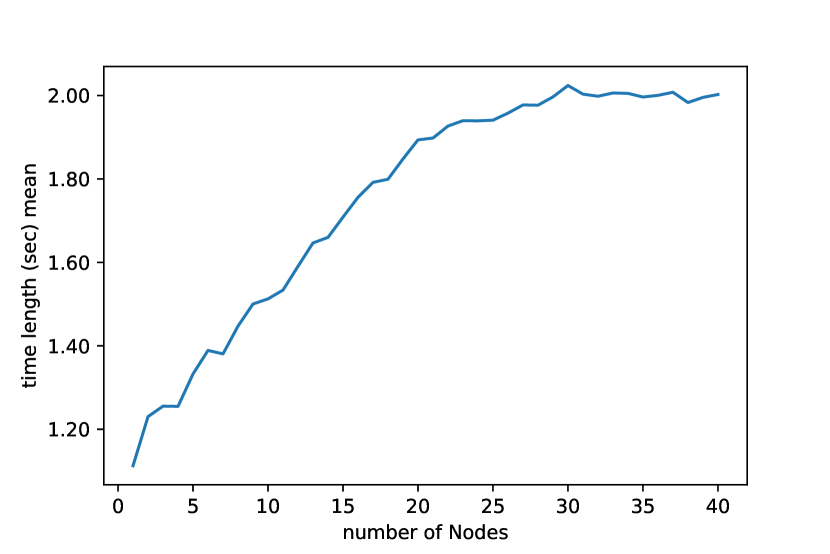

Based on Figure 16 and on the concept that pruning can correct potential remaining overfitting, we notice that beyond a sufficient number of nodes the accuracy remains the same. In addition, it leads to quicker computations. Thus we expand the trees’ depth until 15 nodes.

In a nutshell, we launch 50 arbitrary decision trees, each one randomly checking 15 features at each node and having a 15 nodes depth. With this parameters setting, we end up with an 87.3% out-of-sample , see Table 2.141414As a comparison, we obtained close results using a gradient boosting regression (Friedman,, 2001) – another algorithm based on decision trees. For the sake of brevity, we do not report these results here. They are, however, available upon request to the authors.

| IS Mean (Std) | OoS Mean (Std) | |

| 99.2% (0.06%) | 87.3% (3.86%) |

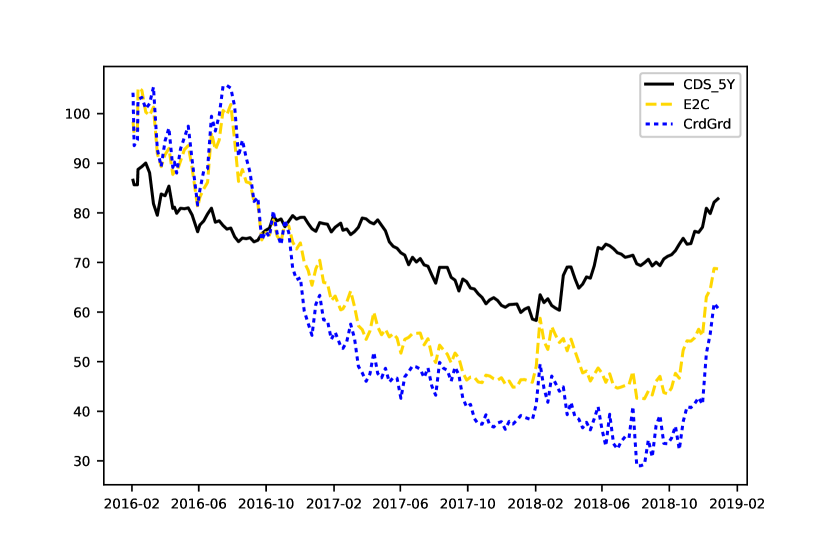

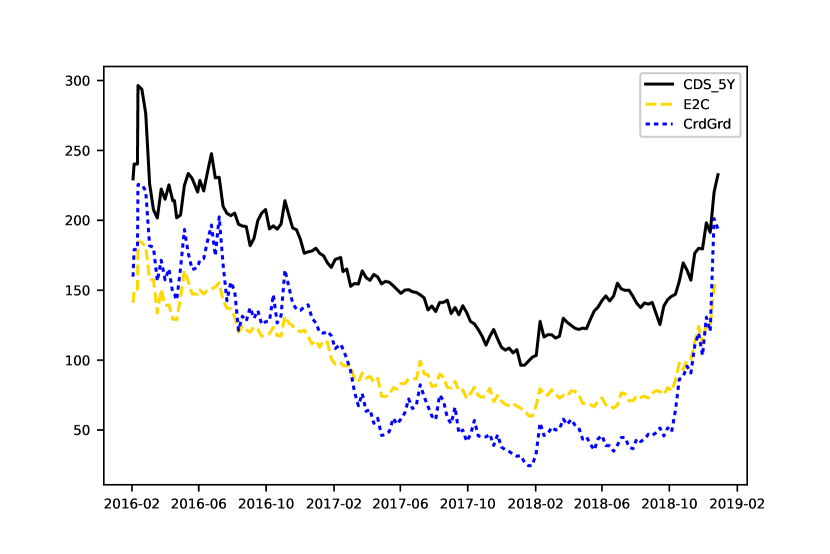

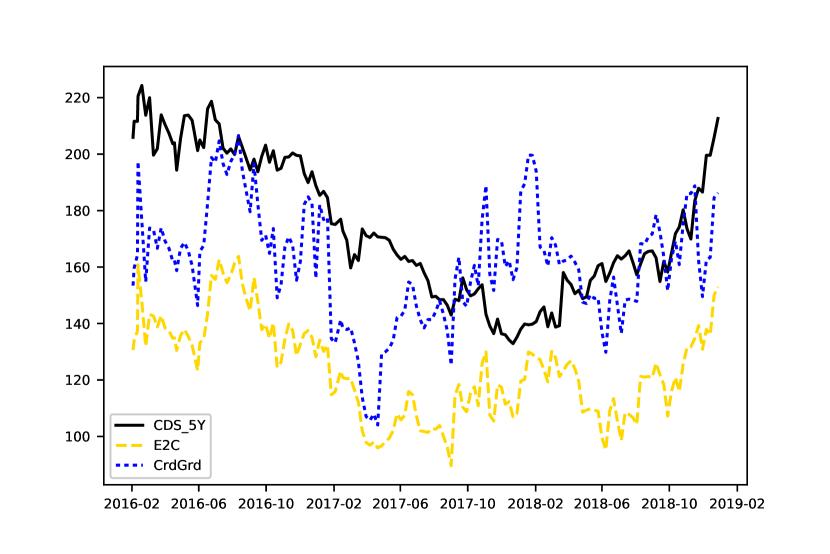

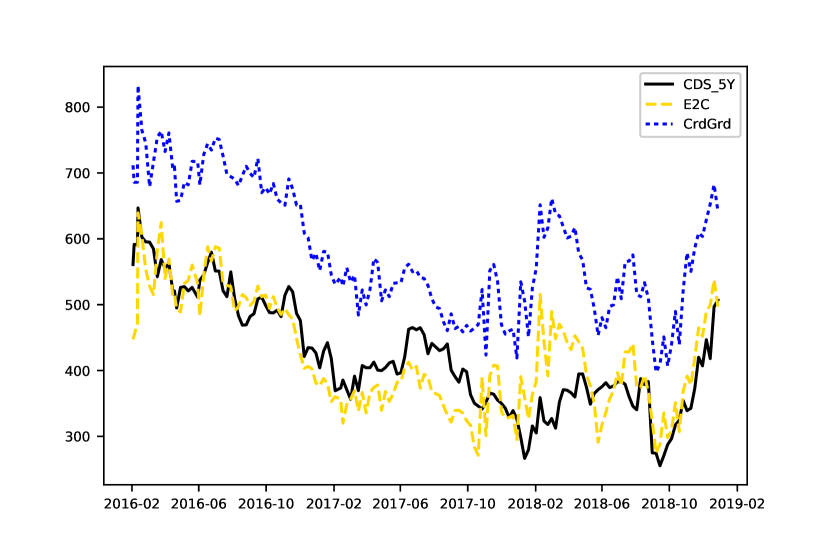

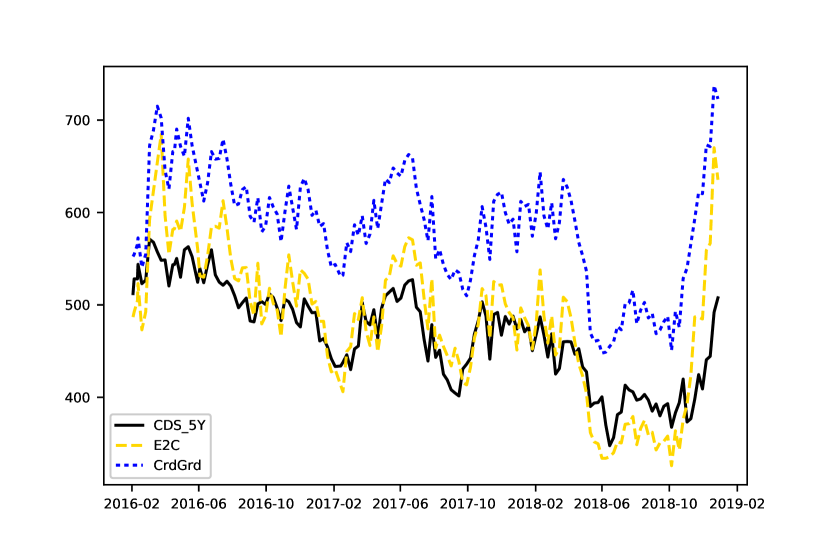

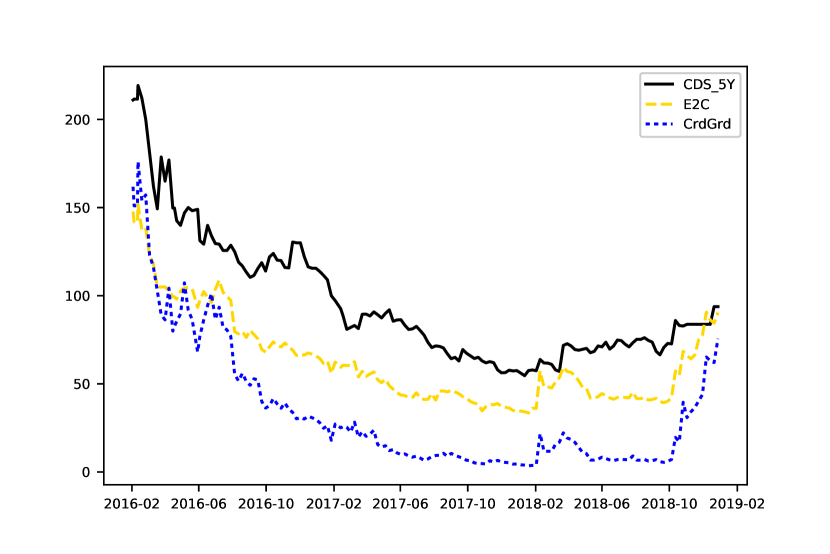

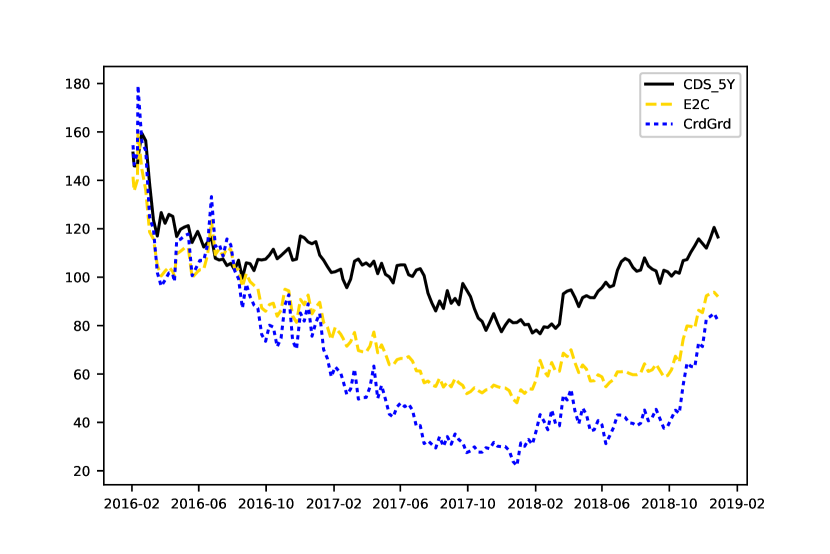

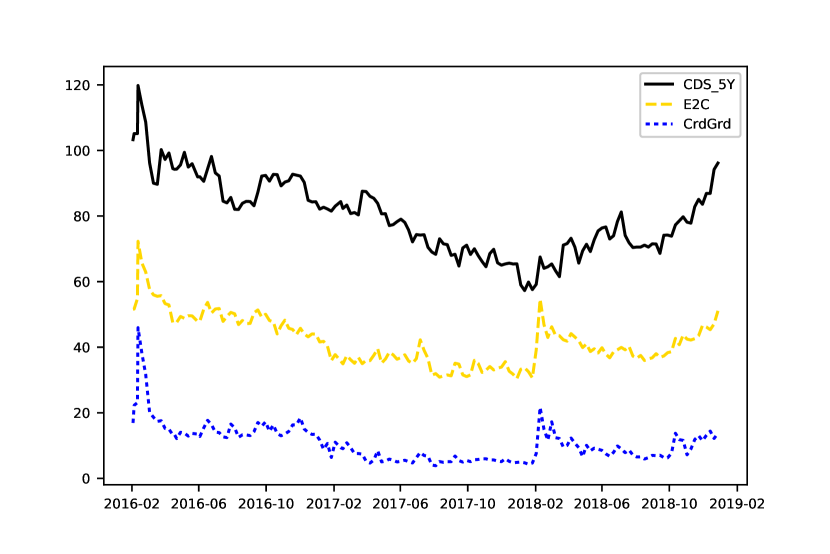

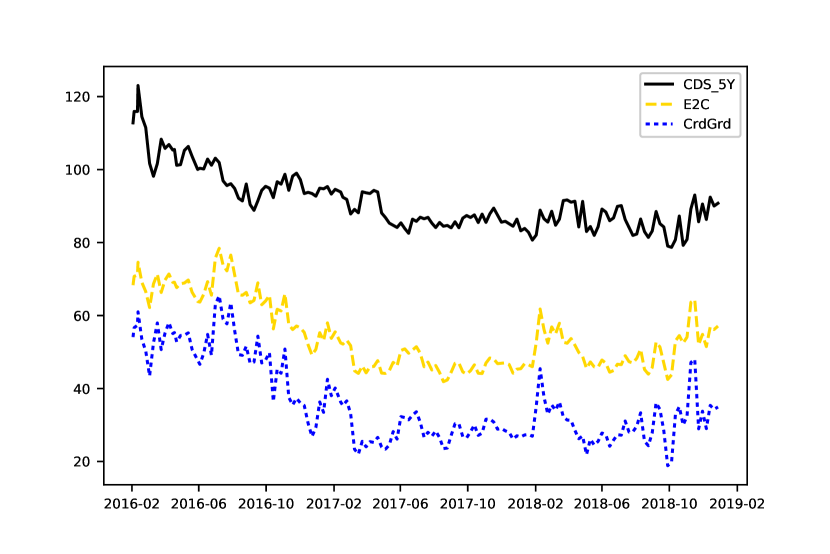

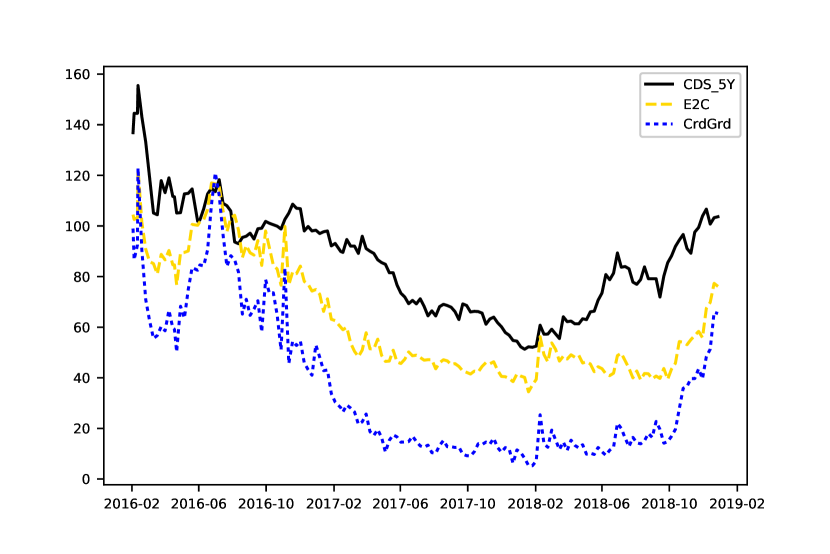

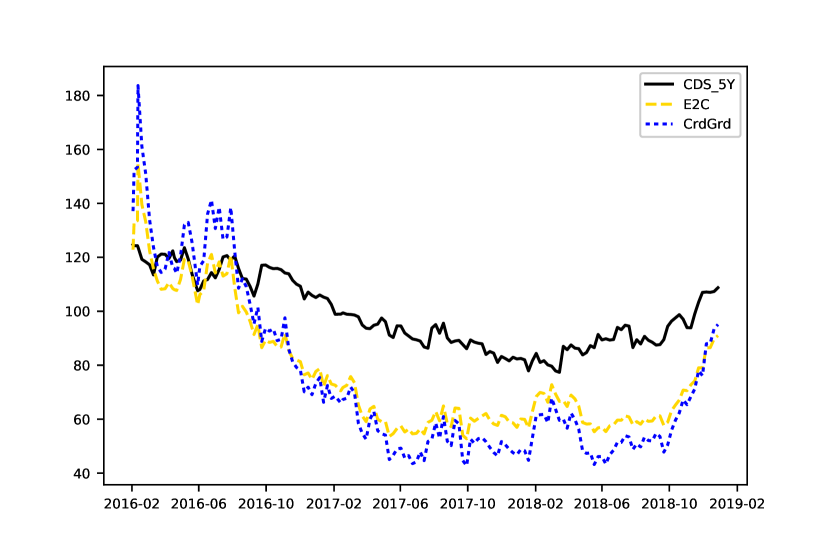

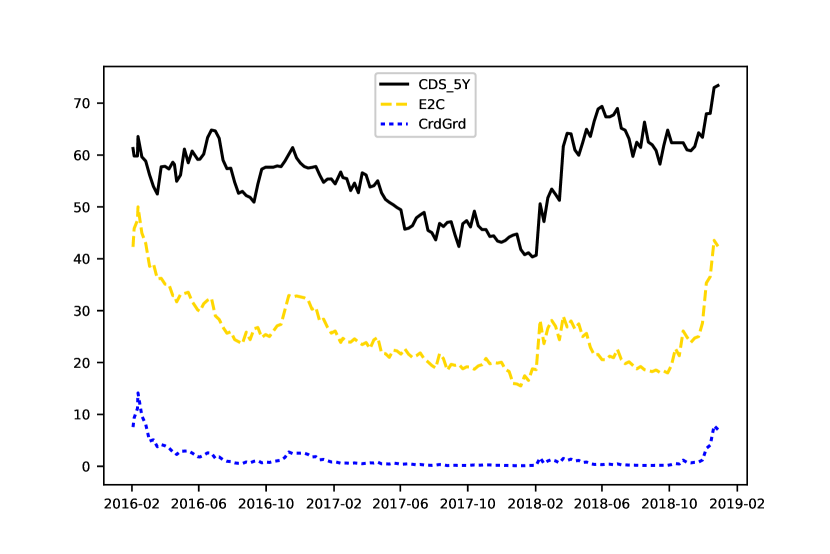

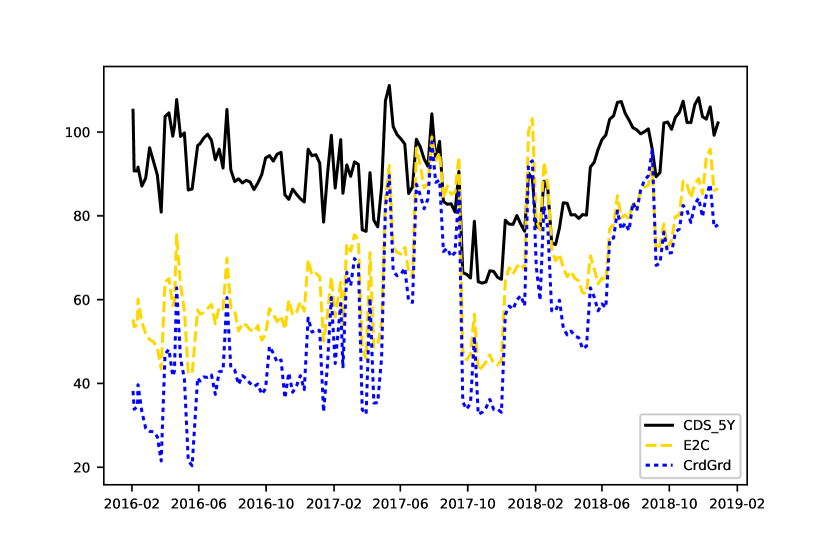

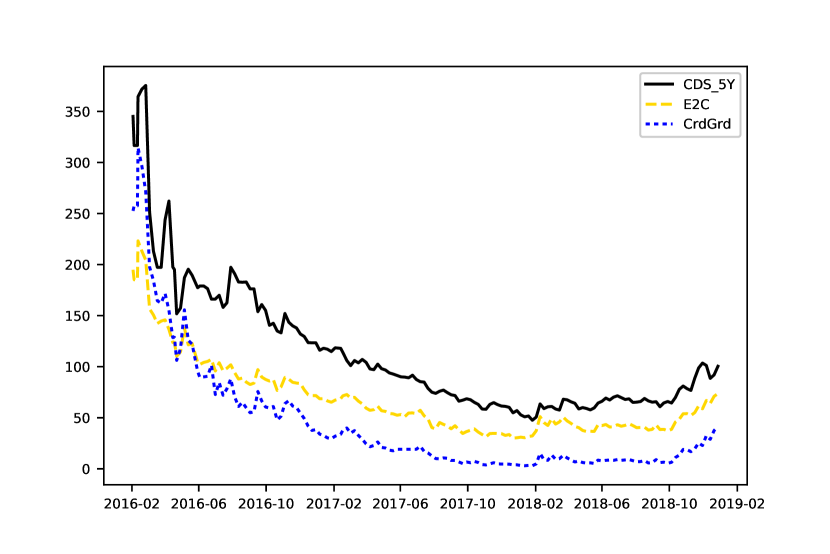

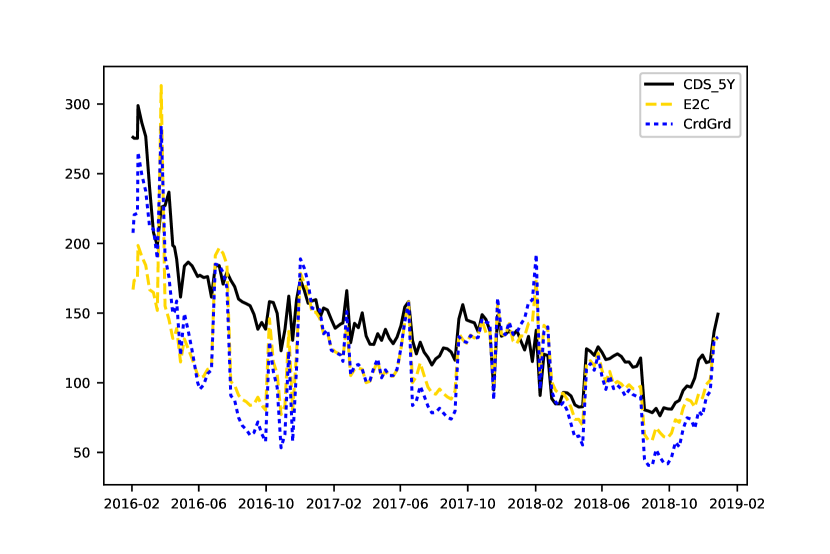

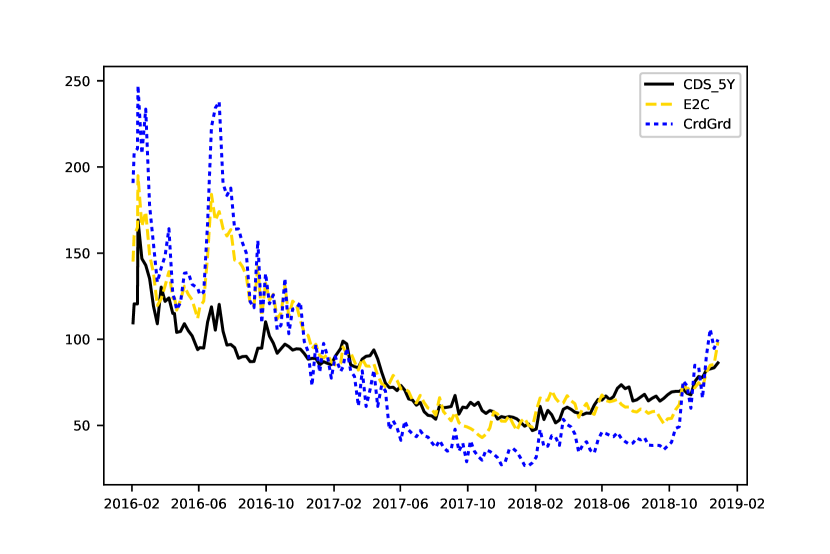

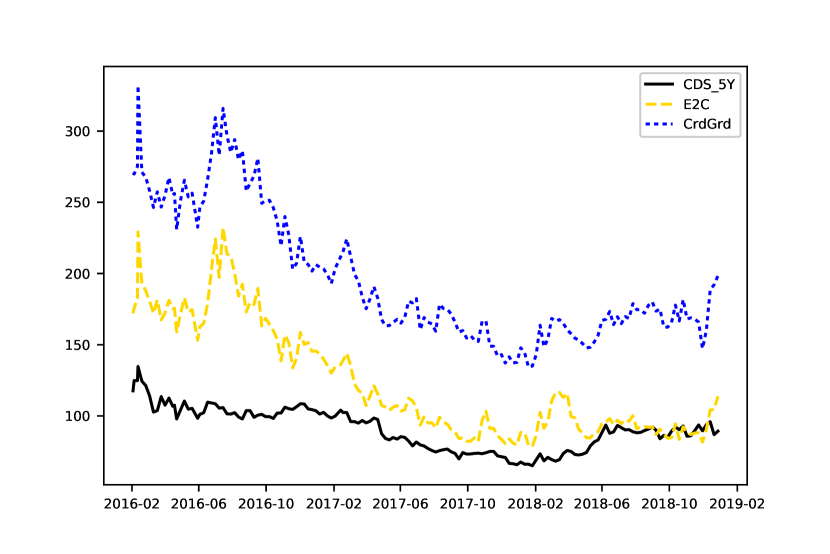

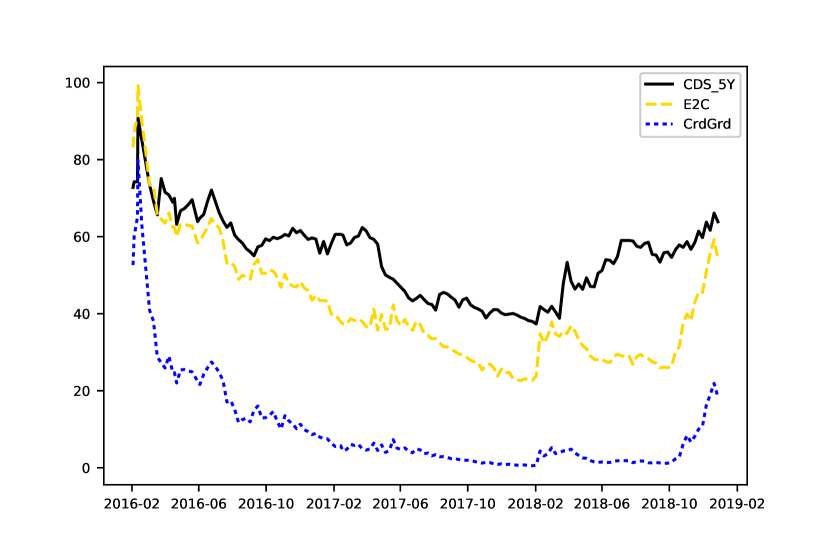

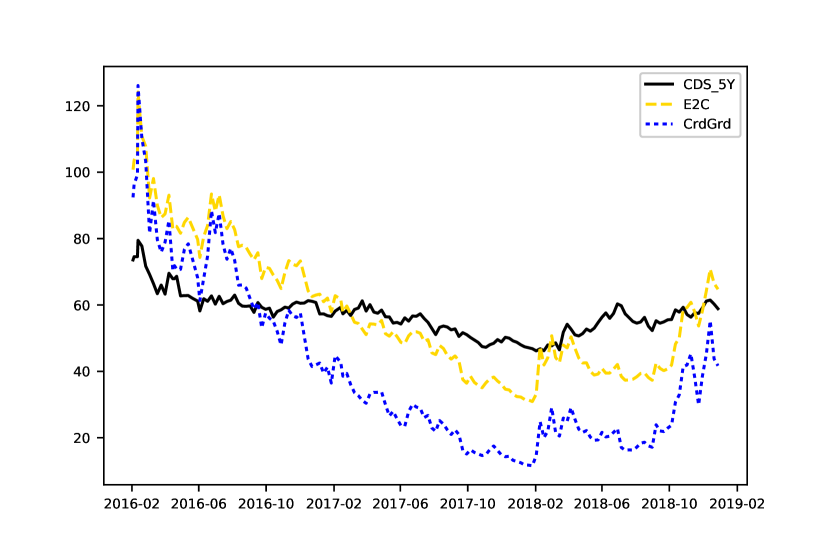

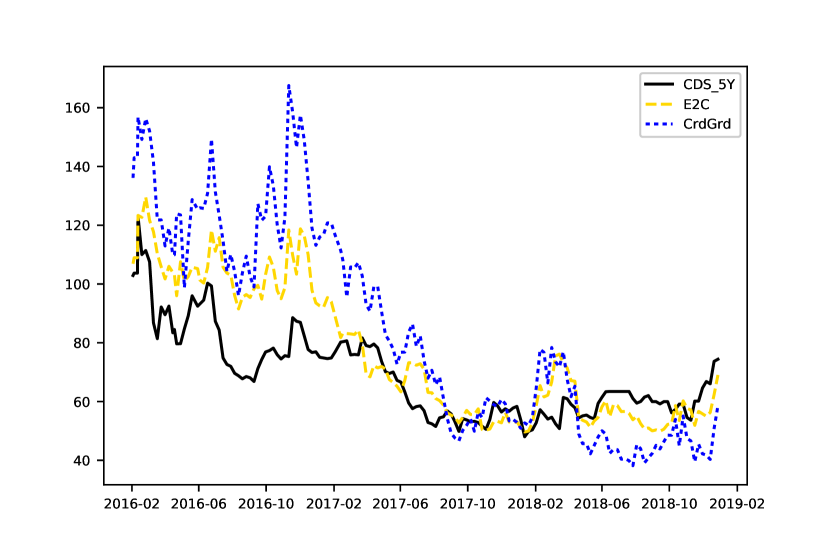

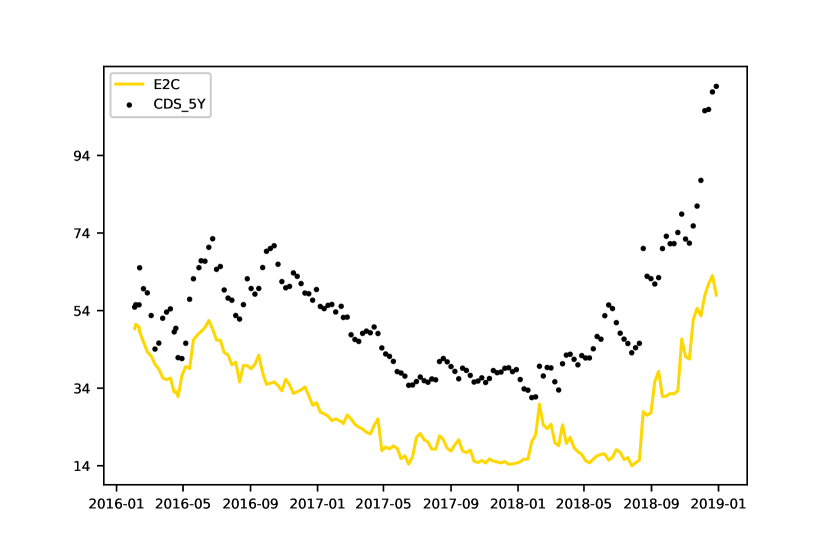

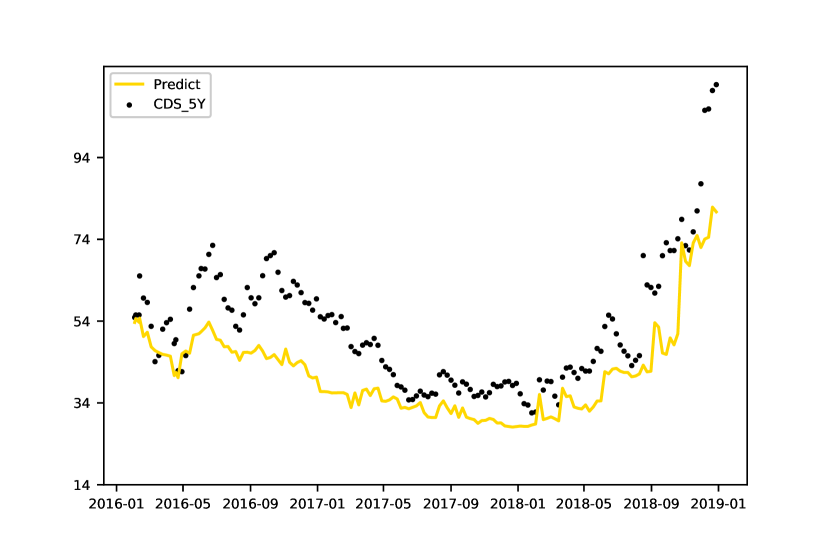

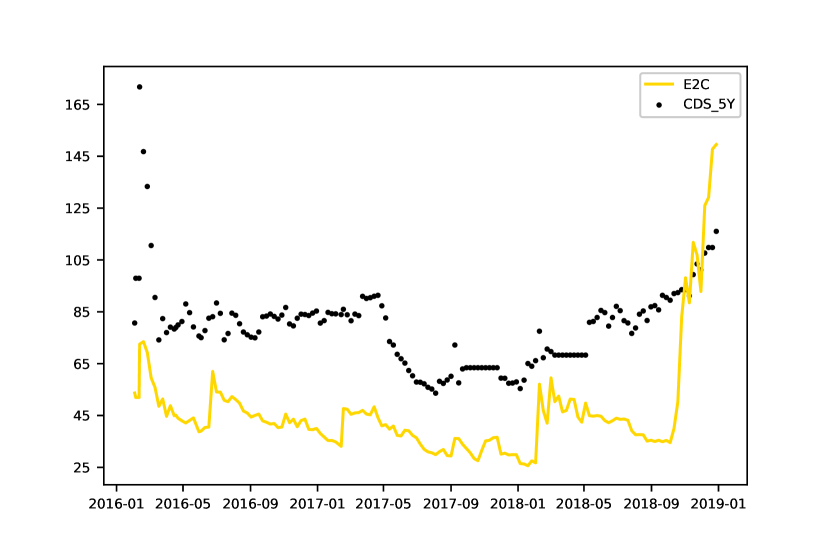

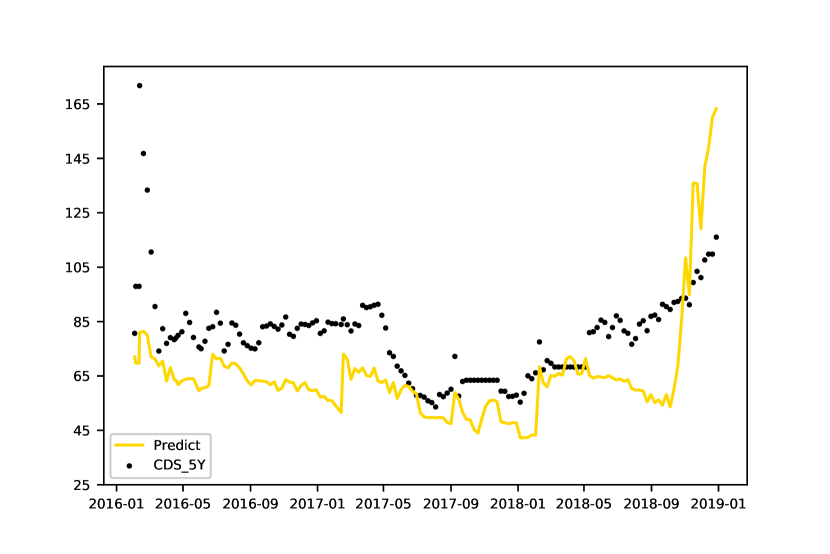

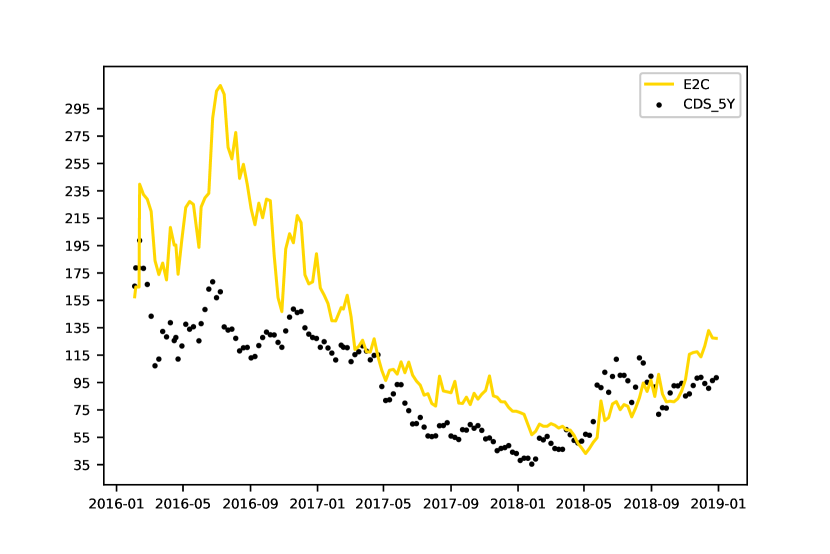

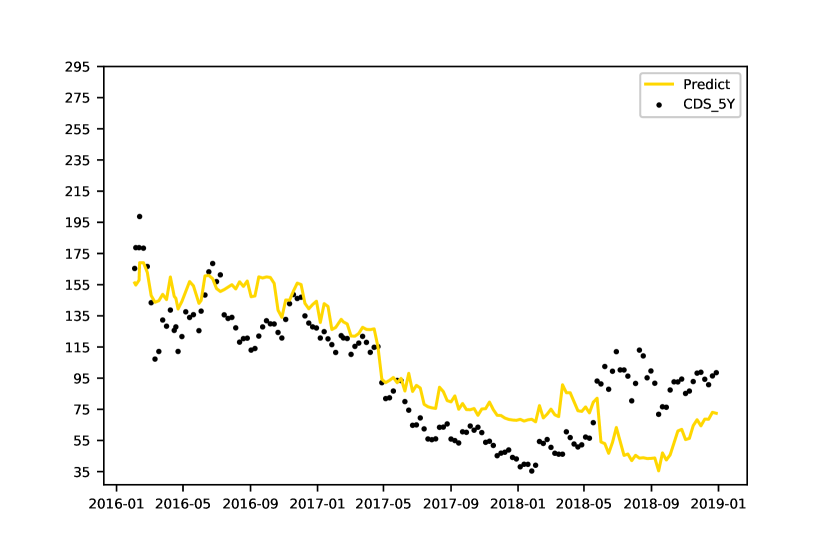

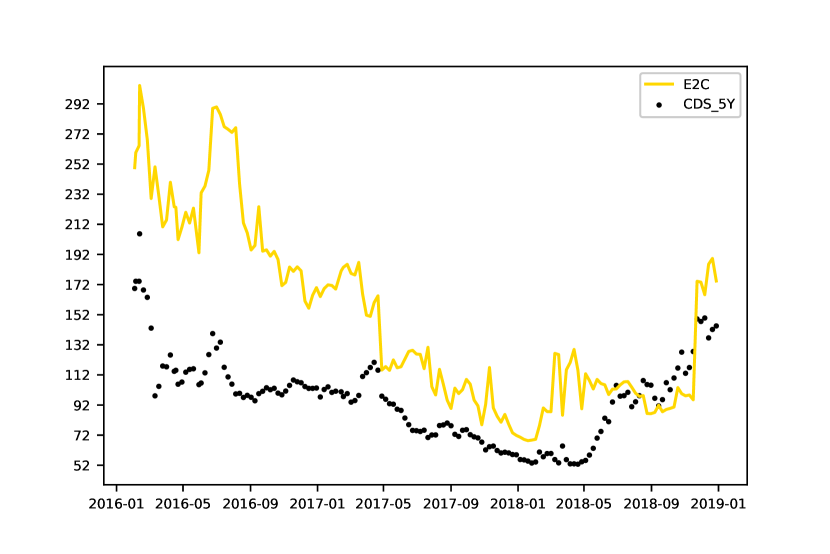

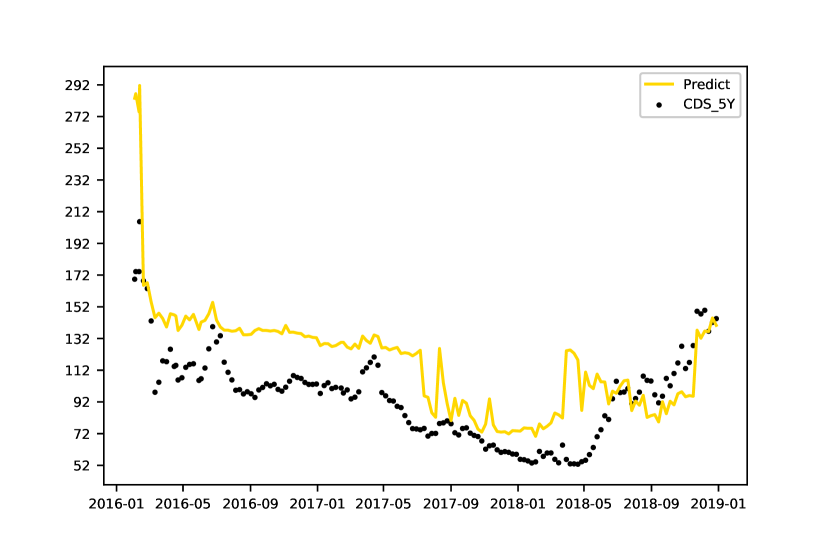

These out-of-sample results are illustrated for 10 companies chosen randomly, see Figure 17. On these graphs, the black points stand for the 5y CDS benchmarks. The yellow line stands for the sole E2C on the left-hand side and the predicted results using random forest on all features on the right-hand side.

The graphs on the left-hand side present an already satisfactory approximation of the 5-year CDS using only the E2C equation. However, it is clear on the right-hand-side graphs that the use of a random forest algorithm on a multivariate sample (including the E2C) provides a significantly improved prediction. Training a random forest with these easy-to-access variables is thus a worthwhile process. As robustness check, we ran the random forest algorithm on the same multivariate set-up, removing one sector at a time. Similar levels of accuracy were reached (cf. Appendix C, Table C.1).

4.2.2 Verification of Feature Importance

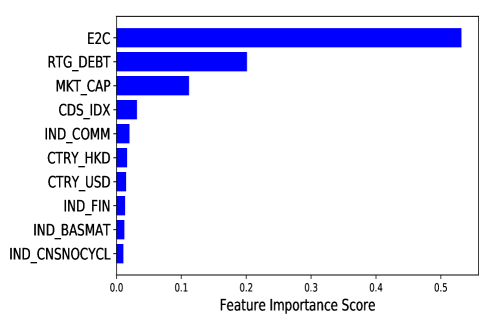

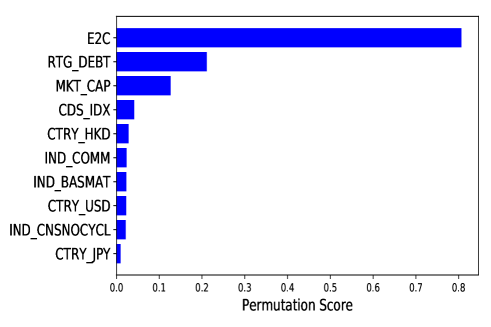

The use of a random forest algorithm has been justified above with reference to the results obtained. However, it has an additional property worth noting – its transparency which gives access to a quantified measure of each variable’s importance. This allows us to assess the individual contribution of the variables (including the E2C) in the improvement obtained with the random forest. The contribution of each feature in predicting the response can be assessed using two methods. Firstly, a method called feature importance, which empirically highlights whether the trees are frequently consulted by a specific feature weighted by the enhancement it brings. At each node, the improvement brought by a specific selected variable is computed comparing the residual sum of squares before and after splitting. In other words, this method counts, for each tree, the number of times a data sample passes through a node whose decision is based on a specific feature, times the improvement it carries. Then, the total contribution of the variable is averaged over all trees. Secondly, we measure the variable importance by how much it decreases the model accuracy (averaged over all trees) when this feature is randomly permuted. More specifically, this method computes, for each feature, the mean square error151515As usual, on the out-of-bag samples. without permutation and compares it to the permuted one. Then, the subtraction is averaged over all random trees and normalized. For instance, for a feature A, we get:

Shuffling a variable is similar in linear regressions to setting a coefficient as null. Consequently, we expect important variables’ to be significantly lower in the scrambled cases than in the genuine ones, leading to a high . In addition, this method does not affect the values’ distribution, because variables are just permuted. Moreover, this second metric is useful to distinguish the importance among correlated variables. We display these features’ importance measures in the bar charts below, the first method being on the left-hand side. Only the ten most important variables (according to our measures) are shown in Figure 21.

These bar charts confirm that the E2C is by far the main variable contributing to our improved approximation of the CDS161616CreditGrades as substitute for E2C, while providing the same R-squared and being the main feature, is a less dominant variable in this set-up.. Beyond the E2C, the inclusion of debt ratings and market capitalizations also clearly improves the model. In a sample with a high heterogeneity between companies, it is encouraging to observe that the random forest highlights company-specific variables such as the two listed above.

5 Conclusion

In this paper, we develop an instrument which is both intuitive and accurate to approximate CDS spreads. It relies on an elementary formula, called E2C, and on random forest regressions learning from a small data set.

Our first step in reaching this goal is the analysis of the cornerstone concepts driving structural models for Credit Default Swaps. Most of this analysis is closely related to the CreditGrades method, but the specificity of our equation rests on the use of fewer parameters and a more elementary formula. Upon verification, the E2C provides at least as accurate an approximation of the CDS as the CreditGrades model does, and in fact outperforms in certain predictions for firms grouped by debt ratings or industrial sectors.

Furthermore, we provide a protocol using random forest regressions to correct some remaining issues with accuracy found in all models such as the E2C or CreditGrades. This supervised learning algorithm allows the inclusion of a few additional widely-available financial data as independent variables, to complement the E2C. We detail the steps from the sample pre-processing to the final hyper-parameter setting. The use of the random forest algorithm culminates in an 87.3% out-of-sample accuracy in our CDS approximations. This method remains simple among non-linear supervised algorithms, and has the added benefit of transparency, which allows an evaluation of the relative importance of our variables. Beyond confirming the impact of debt rating and company size on CDS, this transparency highlights the predominance of the E2C as a reliable predictor among all other variables.

Financial practitioners and researchers have long had to balance precision against transparency in their selection of CDS spreads approximations. The E2C formula we offer in this paper goes a long way toward resolving that tension; as it generally outstrips the accuracy of the CreditGrades model while being more intuitive and straightforward. Furthermore, by conducting random forest regressions on a multivariate universe including our E2C, we obtain an outstandingly reliable and accessible CDS estimation.

Although our sample covers a large number of companies, industries and countries, we suggest that additional insights may be uncovered with historical data covering a longer time-span. CDS maturity is also not considered in this paper and is left for future research, possibly starting from the exploration of other mathematical “concentration inequalities” for the formula’s upper bound.

References

- Ahmad et al., (2017) Ahmad, M. W., Mourshed, M., and Rezgui, Y. (2017). Trees vs neurons: Comparison between random forest and ann for high-resolution prediction of building energy consumption. Energy and Buildings, 147:77–89.

- Badrinarayanan et al., (2017) Badrinarayanan, V., Kendall, A., and Cipolla, R. (2017). Segnet: A deep convolutional encoder-decoder architecture for image segmentation. IEEE Transactions on Pattern Analysis and Machine Intelligence, 39:2481 – 2495.

- Behr and Weinblat, (2017) Behr, A. and Weinblat, J. (2017). Default patterns in seven eu countries: A random forest approach. International Journal of the Economics of Business, 24(2):181.

- Black and Cox, (1976) Black, F. and Cox, J. (1976). Valuing corporate securities: Some effects of bond indenture provisions. Journal of Finance, 31:351–367.

- Breiman, (1996) Breiman, L. (1996). Bagging predictors. Machine Learning, 24:123–140.

- Breiman, (2001) Breiman, L. (2001). Random forests. Machine Learning, 45:5–32.

- Breiman et al., (1984) Breiman, L., Friedman, J., Stone, C. J., and Olshen, R. A. (1984). Classification and Regression Trees.

- Brummelhuis and Luo, (2017) Brummelhuis, R. and Luo, Z. (2017). Cds rate construction methods by machine learning techniques. pages 1–51.

- Chalamandaris and Vlachogiannakis, (2018) Chalamandaris, G. and Vlachogiannakis, N. (2018). Are financial ratios relevant for trading credit risk? evidence from the cds market. Annals of Operations Research, 266:395–440.

- Chebyshev, (1867) Chebyshev, P. L. (1867). Des valeurs moyennes. Journal de mathématiques pure et appliqués, 12:177–184.

- Cont and Minca, (2016) Cont, R. and Minca, A. (2016). Credit default swaps and systemic risk. Annals of Operations Research, 247:523–547.

- Eom et al., (2004) Eom, Y. H., Helwege, J., and Huang, J.-Z. (2004). Structural models of corporate bond pricing: An empirical analysis. The Review of Financial Studies, 17:499–544.

- Escobar et al., (2012) Escobar, M., Arian, H., and Seco, L. (2012). Creditgrades framework within stochastic covariance models. Journal of Mathematical Finance, 2:303–314.

- Fernandez-Delgado et al., (2014) Fernandez-Delgado, M., Cernadas, E., Barro, S., and Amorim, D. (2014). Do we need hundreds of classifiers to solve real world classification problems? Journal of Machine Learning Research, 15:3133–3181.

- Finger et al., (2002) Finger, C. C., Lardy, J. P., Finkelstein, V., Pan, G., Ta, T., and Tierney, J. (2002). CreditGrades. Technical report, RiskMetrics Group.

- Foundation, (2016) Foundation, P. S. (2016). Python 3.6.0 documentation.

- Friedman, (2001) Friedman, J. H. (2001). Greedy function approximation: A gradient boosting machine. The Annals of Statistics, 29(5):1189–1232.

- Gauss, (1821) Gauss, C. F. (1821). Theoria combinationis observationum erroribus minimus obnoxiae (pars prior). Gauss Werke, 4:3–26.

- Guarin et al., (2011) Guarin, A., Liu, X., and Ng, W. L. (2011). Enhancing credit default swap valuation with meshfree methods. European Journal of Operational Research, 214:805–813.

- Hastie et al., (2009) Hastie, T., Tibshirani, R., and Friedman, J. (2009). The Elements of Statistical Learning. Second edition.

- Ho, (1995) Ho, T. K. (1995). Random decision forests. In Proceedings of the third international conference on Document analysis and recognition, pages 278–282.

- Ho, (1998) Ho, T. K. (1998). The random subspace method for constructing decision forests. IEEE Transactions on Pattern Analysis and Machine Intelligence, 20:832–844.

- Hunter and Dale, (2007) Hunter, J. and Dale, D. (2007). The matplotlib users guide. Technical report, R Cran.

- Imbierowicz and Cserna, (2008) Imbierowicz, B. and Cserna, B. (2008). How efficient are credit default swap markets? an empirical study of capital structure arbitrage based on structural pricing model. SSRN Electronic Journal.

- Irresberger et al., (2018) Irresberger, F., Weiss, G., Gabrysch, J., and Gabrysch, S. (2018). Liquidity tail risk and credit default swap spreads. European Journal of Operational Research, 269:1137–1153.

- Khaidem et al., (2017) Khaidem, L., Saha, S., and Dey, S. R. (2017). Predicting the direction of stock market prices using random forest. Applied Mathematical Finance, pages 1–20.

- Koutmos, (2018) Koutmos, D. (2018). Interdependencies between cds spreads in the european union: Is greece the black sheep or black swan? Annals of Operations Research, 266:441–498.

- Krauss et al., (2017) Krauss, C., Do, X. A., and Huck, N. (2017). Deep neural networks, gradient-boosted trees, random forests: Statistical arbitrage on the s&p 500. European Journal of Operational Research, 259:689–702.

- Lardic and Rouzeau, (1999) Lardic, S. and Rouzeau, E. (1999). Implementing merton’s model on the french corporate bond market. In AFFI Conference.

- LeCun, (2012) LeCun, Y. (2012). Learning invariant feature hierarchies. Lecture Notes in Computer Science (including subseries Lecture Notes in Artificial Intelligence and Lecture Notes in Bioinformatics) 7583 LNCS, PART 1.

- Lévy, (1940) Lévy, P. (1940). Sur certains processus stochastiques homogènes. Compositio Mathematica, 7:283–339.

- Liaw and Wiener, (2002) Liaw, A. and Wiener, M. (2002). Classification and regression by randomforest. R News, 2(3):18–22.

- Liu et al., (2013) Liu, M., Wang, M., Wang, J., and Li, D. (2013). Comparison of random forest, support vector machine and back propagation neural network for electronic tongue data classification: Application to the recognition of orange beverage and chinese vinegar. Sensors and Actuators B: Chemical, 177:970–980.

- McKinney, (2010) McKinney, W. (2010). Data structures for statistical computing in python. Proceedings of the ninth Python in science conference, 445:51–56.

- Merton, (1974) Merton, R. (1974). On the pricing of corporate debt: The risk structure of interest rates. Journal of Finance, 29:449–470.

- Nyman and Ormerod, (2016) Nyman, R. and Ormerod, P. (2016). Predicting economic recessions using machine learning algorithms.

- Opitz and Maclin, (1999) Opitz, D. and Maclin, R. (1999). Popular ensemble methods: An empirical study. Journal of Artificial Intelligence Research, 11:169–198.

- Pedregosa et al., (2011) Pedregosa, F., Varoquaux, G., Gramfort, A., Michel, V., Thirion, B., Grisel, O., Blondel, M., Prettenhofer, P., Weiss, R., Dubourg, V., Vanderplas, J., Passos, A., Cournapeau, D., Brucher, M., Perrot, M., and Duchesnay, E. (2011). Scikit-learn: Machine learning in python. Journal of Machine Learning Research, 12:2825–2830.

- Perks, (1947) Perks, W. (1947). A simple proof of gauss’s inequality. Journal of the Staple Inn Actuarial Society, 7(1):38–41.

- Rodrigues and Agarwal, (2011) Rodrigues, M. and Agarwal, V. (2011). The performance of structural models in pricing credit spreads. Midwest Finance Association 2012 Annual Meetings Paper, pages 1–26.

- Rodriguez-Galiano et al., (2015) Rodriguez-Galiano, V., M.Sanchez-Castillo, M.Chica-Olmo, and M.Chica-Rivas (2015). Machine learning predictive models for mineral prospectivity: An evaluation of neural networks, random forest, regression trees and support vector machines. Ore Geology Reviews, 71:804–818.

- Roy, (1952) Roy, A. D. (1952). Safety first and the holding of assets. Econometrica, 20:431–449.

- Sangineto et al., (2018) Sangineto, E., Nabi, M., Culibrk, D., and Sebe, N. (2018). Self paced deep learning for weakly supervised object detection. IEEE Transactions on Pattern Analysis and Machine Intelligence, PP:1–1.

- Santos, (2008) Santos, K. (2008). Corporate credit ratings: a quick guide.

- Schönbucher, (2003) Schönbucher, P. J. (2003). Credit derivatives pricing models.

- Sepp, (2006) Sepp, A. (2006). Extended creditgrades model with stochastic volatility and jumps. Wilmott Magazine, pages 50–62.

- Shwartz-Ziv and Tishby, (2017) Shwartz-Ziv, R. and Tishby, N. (2017). Opening the black box of deep neural networks via information.

- Stamicar and Finger, (2006) Stamicar, R. and Finger, C. C. (2006). Incorporating equity derivatives into the creditgrades model. Journal of Credit Risk, 2(1):3–29.

- StataCorp, (2013) StataCorp (2013). Stata 13.

- Sun et al., (2018) Sun, Y., Yen, G. G., and Yi, Z. (2018). Evolving unsupervised deep neural networks for learning meaningful representations. IEEE Transactions on Evolutionary Computation, PP:1–1.

- Tanaka et al., (2016) Tanaka, K., Kinkyo, T., and Hamori, S. (2016). Random forests-based early warning system for bank failures. Economics Letters, 148:118–121.

- Teixeira, (2007) Teixeira, J. C. A. (2007). An empirical analysis of structural models of corporate debt pricing. Applied Financial Economics, 17(14):1141–1165.

- Tomohiro, (2014) Tomohiro, A. (2014). Bayesian corporate bond pricing and credit default swap premium models for deriving default probabilities and recovery rates. Journal of the Operational Research Society, 65:454–465.

- Vasicek, (1987) Vasicek, O. A. (1987). Probability of loss on loan portfolio. KMV Corporation.

- Walt et al., (2011) Walt, S. V. D., Colbert, S., and Varoquaux, G. (2011). The numpy array: a structure for efficient numerical computation. Computing in Science & Engineering, 13:22–30.

- Yeh et al., (2012) Yeh, C. C., Lin, F., and Hsu, C. Y. (2012). A hybrid kmv model, random forests and rough set theory approach for credit rating. Knowledge-Based Systems, 33:166–172.

- Zhou, (1997) Zhou, C. (1997). A jump-diffusion approach to modeling credit risk and valuing defaultable securities. In Finance and Economics Discussion Papers 1997/15.

- (58) Zhou, C. (2001a). An analysis of default correlations and multiple defaults. Review of Financial Studies, 14(2).

- (59) Zhou, C. (2001b). The term structure of credit spreads with jump risk. Journal of Banking & Finance, 25:2015–2040.

Appendices

Appendix A

Modified “one-sided” approach to the Gauss Inequality

A result similar to Gauss’s inequality gives, for any random variable with a decreasing density for negative values:

Then, from the reflection principle for an unbiased stock evolution from the current price:

and

Hence,

Expressing the stock evolution in independent steps:

And this last conditional expectation is proxied by the geometric average of the downside boundary values of a Black-Cox/CreditGrades type model of the firm.

Debt-per-Share Evaluation

According to CreditGrades, the financial debt amount is determined splitting companies in two categories, banking and non-banking firms.

-

•

Banking Sector \@mathmargin0pt

-

•

Non-Banking Sector \@mathmargin0pt

To develop a little further the choice for banks, we highlight that banks deposits are not part of financial leverage, thus excluded from the debt-per-share. In fine, many financial statements items should be assessed on a case-by-case basis171717ST Borrowings, and both Other ST and LT Liabilities contain many other items which in fact should be weighted 0% into the debt-per-share calculations, ranging from accounts payables and accrued expenses to repos, securities lending of regulated broker-dealer or securities subsidiaries, …, leading to a laborious analysis. For the sake of simplification, CreditGrades chose to include in its debt-per-share computations the consolidated Long Term Borrowings. , the minority interests and the prefered equities are balance sheet data, thus are given in fundamental report currency. To match with the current stock price and the current market capitalization, we convert them to the stock price currency. Finally, the debt-per-share is defined as follow:

Note that is capped at 50% of , is capped at 50% of and is floored at 10% of . Moreover, the weightings of and the cap and floor levels are inspired by CreditGrades (2002).

Appendix B

CreditGrades formula

Descriptive Statistics Tables

| Des Stat | CDS_5Y | E2C | CrdGrd |

| No. of obs. | 47476 | 47476 | 47476 |

| No. of firms | 308 | 308 | 308 |

| No. of periods | 155 | 155 | 155 |

| Mean | 137.4 | 124.5 | 138.7 |

| Std-overall | 230.2 | 236.5 | 268.5 |

| Std-between | 202.2 | 202.8 | 249.4 |

| Std-within | 120.3 | 129.4 | 107.4 |

| Min | 12.9 | 1.4 | 0 |

| q(25%) | 46 | 26 | 1.1 |

| q(50%) | 71.6 | 50.6 | 18.6 |

| q(75%) | 132.3 | 115.5 | 135.6 |

| Max | 4491.1 | 4444.9 | 2246.9 |

| Skew | 7.3 | 5.5 | 2.9 |

| Kurt | 86.3 | 44.1 | 9.2 |

| 5y CDS | E2C | CrdGrd | |||||

| Obs. | mean | std | mean | std | mean | std | |

| Australia | 2170 | 88.9 | 45.3 | 34.4 | 22.6 | 15.1 | 27.6 |

| Britain | 3402 | 94.8 | 89.4 | 59.6 | 112.8 | 44.8 | 138.8 |

| Canada | 775 | 318.1 | 275.2 | 376.5 | 518.2 | 373.9 | 458.1 |

| Denmark | 280 | 88.2 | 49.6 | 112.6 | 70.2 | 277.4 | 220 |

| Eurozone | 12061 | 103.2 | 208.1 | 102.2 | 139.1 | 119.7 | 194.5 |

| Hong Kong | 930 | 191.9 | 181.9 | 63.2 | 90.8 | 63.1 | 134.8 |

| India | 465 | 180 | 47.4 | 326.3 | 193.9 | 433.3 | 251.5 |

| Japan | 3410 | 50.9 | 36.1 | 110.8 | 101 | 147.4 | 200.6 |

| Malaysia | 155 | 107.3 | 33.7 | 46.3 | 75 | 46.2 | 102 |

| New Zealand | 310 | 80.2 | 33.7 | 40 | 31.9 | 26.7 | 36.2 |

| Norway | 310 | 41.2 | 19.1 | 50 | 36.2 | 24.5 | 47.1 |

| Singapore | 155 | 57.2 | 9.4 | 8.2 | 4.1 | 0 | 0 |

| South Korea | 1240 | 73.7 | 22.7 | 90.9 | 57.7 | 180.1 | 235.8 |

| Sweden | 465 | 86.2 | 39 | 50.1 | 20.3 | 18.1 | 22.5 |

| United States | 21348 | 180.9 | 284.9 | 155.4 | 303 | 167.3 | 326 |

| Correl | CDS_5Y | E2C | CrdGrd |

|---|---|---|---|

| CDS_5Y | 100% | 66.7% | 62.3% |

| E2C | 66.7% | 100% | 92.7% |

| CrdGrd | 62.3% | 92.7% | 100% |

| Correl | CDS_5Y | E2C | CrdGrd |

|---|---|---|---|

| CDS_5Y | 100% | 85% | 76.3% |

| E2C | 85% | 100% | 89.6% |

| CrdGrd | 76.3% | 89.6% | 100% |

| RMSE | MAPE | MASE | |||||

| Obs. | E2C | CrdGrd | E2C | CrdGrd | E2C | CrdGrd | |

| A | 11396 | 55 | 132 | 0.72 | 1.44 | 16.1 | 31.2 |

| BBB | 17581 | 61 | 124 | 0.56 | 1.06 | 12.9 | 22.5 |

| BB | 5360 | 98 | 214 | 0.47 | 0.76 | 9.6 | 15.2 |

| B | 3637 | 260 | 265 | 0.39 | 0.49 | 6.2 | 6.6 |

| RMSE | MAPE | MASE | |||||

| Obs. | E2C | CrdGrd | E2C | CrdGrd | E2C | CrdGrd | |

| Basic Materials | 3285 | 62 | 89 | 0.49 | 0.77 | 6.2 | 9 |

| Communication | 4907 | 54 | 77 | 0.48 | 0.78 | 9.4 | 12.9 |

| Consumer Cyclical | 7232 | 70 | 105 | 0.59 | 0.99 | 11.2 | 16.5 |

| Consumer Non-Cyclical | 5616 | 81 | 108 | 0.53 | 0.88 | 9.9 | 11.7 |

| Energy | 2227 | 101 | 133 | 0.37 | 0.68 | 4.8 | 5.9 |

| Financial | 6346 | 127 | 267 | 0.85 | 2.06 | 15.8 | 34.9 |

| Industrial | 4425 | 51 | 75 | 0.61 | 1.01 | 7.7 | 10.4 |

| Utilities | 2540 | 77 | 154 | 0.647 | 1.279 | 13.8 | 22.1 |

RMSE: Root Mean-Square Error

MAPE: Mean Absolute Percentage Error

MASE: Mean Absolute Scaled Error

Consistent with section 3.3, we removed the 10% top and bottom points.

Volatility Regime Tests

Model 1:

Model 2:

Where is a dummy variable, defined as 1 if VIX 3-month volatility index 20.

| CDS_5y | CDS_5y | |

| E2C | 0.8097∗∗∗ | 0.8096∗∗∗ |

| (326.36) | (289.22) | |

| VOL | 1.8482 | |

| (0.93) | ||

| E2C*VOL | -0.0002 | |

| (-0.04) | ||

| constant | 36.5921∗∗∗ | 36.3731∗∗∗ |

| (55.19) | (51.13) | |

| 47476 | 47476 | |

| 0.6917 | 0.6917 | |

| t statistics in parentheses | ||

| ∗ , ∗∗ , ∗∗∗ | ||

| CDS_5y | CDS_5y | |

| CrdGrd | 0.6319∗∗∗ | 0.6163∗∗∗ |

| (237.69) | (212.11) | |

| VOL | -6.3372∗ | |

| (-2.58) | ||

| CrdGrd*VOL | 0.0922∗∗∗ | |

| (12.83) | ||

| constant | 49.7583∗∗∗ | 50.6751∗∗∗ |

| (61.92) | (59.21) | |

| 47476 | 47476 | |

| 0.5434 | 0.5451 | |

| t statistics in parentheses | ||

| ∗ , ∗∗ , ∗∗∗ | ||

Appendix C

Random Forests Robustness Tests

| In-Sample | Out-of-Sample | ||||

| Removed Sector | Remaining Obs. | mean (%) | std (%) | mean (%) | std (%) |

| Basic Materials | 41753 | 99.3 | 0.06 | 84 | 7.16 |

| Communication | 39990 | 99.2 | 0.07 | 87 | 3.55 |

| Consumer Cyclical | 36795 | 99.4 | 0.05 | 85.6 | 5.26 |

| Consumer Non-Cyclical | 39129 | 99.2 | 0.08 | 85.1 | 6.51 |

| Energy | 43245 | 99.3 | 0.07 | 86.9 | 4.54 |

| Financial | 37791 | 99.3 | 0.07 | 87.5 | 4.33 |

| Industrial | 40328 | 99.3 | 0.06 | 86 | 4.91 |

| Utilities | 42780 | 99.2 | 0.07 | 85.9 | 4.37 |