Machine Learning for Variance Reduction in Online Experiments

Abstract

We consider the problem of variance reduction in randomized controlled trials, through the use of covariates correlated with the outcome but independent of the treatment. We propose a machine learning regression-adjusted treatment effect estimator, which we call MLRATE. MLRATE uses machine learning predictors of the outcome to reduce estimator variance. It employs cross-fitting to avoid overfitting biases, and we prove consistency and asymptotic normality under general conditions. MLRATE is robust to poor predictions from the machine learning step: if the predictions are uncorrelated with the outcomes, the estimator performs asymptotically no worse than the standard difference-in-means estimator, while if predictions are highly correlated with outcomes, the efficiency gains are large. In A/A tests, for a set of 48 outcome metrics commonly monitored in Facebook experiments the estimator has over 70% lower variance than the simple difference-in-means estimator, and about 19% lower variance than the common univariate procedure which adjusts only for pre-experiment values of the outcome.

1 Introduction

While sample sizes are typically larger for online experiments than traditional field experiments, the desired minimum detectable effect sizes may be small, and the outcome variables of interest may be heavy-tailed. Even with quite large samples, statistical power may be low. Variance reduction methods play a key role in these settings, allowing for precise inferences with less data (Deng et al., 2013; Taddy et al., 2016; Xie and Aurisset, 2016). One common technique involves ”adjusting” the simple difference-in-means estimator to account for covariate imbalances between the test and control groups (Deng et al., 2013; Lin, 2013), with the magnitude of the adjustment depending on both the magnitude of those imbalances, and the correlation between the covariates and the outcome of interest. If covariates are highly correlated with the outcome, then the treatment effect estimator’s variance will decrease substantially.

Performing this adjustment procedure with the pre-experiment values of the outcome variable itself as the covariate can greatly reduce confidence interval (CI) width, if the outcome exhibits high autocorrelation. A natural question is how to adjust for multiple covariates, which may have a complicated nonlinear relationship with the outcome variable. Using many covariates in a machine learning (ML) model, it may be possible to develop a proxy highly correlated with the outcome variable and hence generate further variance reduction gains. This raises both statistical and scalability issues, however, as it is unclear how traditional justifications for linear regression adjustment with a fixed number of covariates translate to the case of general, potentially very complex ML methods, and it may not be scalable to generate new predictions every time an experiment’s results are queried.

This paper makes three contributions. First, we propose an easy-to-implement and practical estimator which can take full advantage of ML methods to perform regression adjustment across a potentially large number of covariates, and derive its asymptotic properties. We name the procedure MLRATE, for “machine learning regression-adjusted treatment effect estimator”. MLRATE uses cross-fitting (e.g. Athey and Wager (2020); Chernozhukov et al. (2018); Newey and Robins (2018)), which simplifies the asymptotic analysis and guarantees that the “naive” CIs which do not correct for the ML estimation step are asymptotically valid. We also ensure robustness of the estimator to poor quality predictions from the ML stage, by including those ML predictions as a covariate in a subsequent linear regression step. Our approach is agnostic or model-free in two key respects—we do not assume that the ML model converges to the truth, and in common with Lin (2013), in the subsequent linear regression step we do not assume that the true conditional mean is linear. Second, we demonstrate that the method works well for online experiments in practice. Across a variety of metrics, the estimator reduces variance in A/A tests by around 19% on average relative to regression adjustment for pre-experiment outcomes only. Some metrics see variance reduction of 50% or more. Variance reduction of this magnitude can amount to the difference between experimentation being infeasibly noisy and being practically useful. Third, we sketch how the computational considerations involved in implementing MLRATE at scale can be surmounted.

2 Outcome prediction for variance reduction

2.1 Setup & motivation

The data consist of a vector of covariates , an outcome variable , and a binary treatment indicator . The treatment is assigned randomly and independently of the covariates. For observations , the vector is drawn iid from a distribution . To motivate our main estimator and illustrate some of the central ideas, first consider a “difference-in-difference”-style estimator, where we train an ML model predicting from , and then compute the difference between the test and control group averages of . If we treat the estimated ML model as non-random and ignore its dependence on the sample, the resulting estimator has the same expectation as the usual difference-in-means estimator where we compute the difference between the test and control group averages of . This is because and are independent, and hence . Furthermore, if is a good predictor of , then will exceed , and the difference-in-difference estimator based on averages of will be lower variance than the difference-in-means estimator based on averages of .

MLRATE differs in two main respects from the heuristic argument above. First, instead of directly subtracting the ML predictions from the outcome , we include them as a regressor in a subsequent linear regression step. This guarantees robustness of the estimator to poor, even asymptotically inconsistent predictions: regardless of how bad the outcome predictions from the ML step are, MLRATE has an asymptotic variance no larger than the difference-in-means estimator. Second, we use cross-fitting to estimate the predictive models, so that the predictions for every observation are generated by a model trained only on other observations. This allows us to control the randomness in the ML function ignored in the argument above. We derive the asymptotic distribution of this regression-adjusted estimator, and show that the usual, “naive” CIs for the average treatment effect (ATE), which ignore the randomness generated by estimating the predictive models, are in fact asymptotically valid. Thus asymptotically the ML step can only increase precision, and introduces no extra complications in computing CIs.

2.2 Related work

Our work is closely related to the large literature on semiparametric statistics and econometrics, in which low-dimensional parameters of interest are estimated in the presence of high-dimensional nuisance parameters Bickel (1982); Robinson (1988); Newey (1990); Tsiatis (2007); Van der Laan and Rose (2011); Wager et al. (2016). A common approach in this literature appeals to Donsker conditions and empirical process theory to control the randomness generated by the estimation error in the nuisance function Andrews (1994); Van Der Vaart and Wellner (1996); Van der Vaart (2000); Kennedy (2016). This approach is less appealing in this context, as it would greatly restrict the kind of ML methods that could be used for the prediction step (Chernozhukov et al., 2018), and hence the variance reduction attainable. The idea of instead using sample-splitting in semiparametric problems—estimating nuisance parameters on one subset of data and evaluating them on another—dates back at least to Bickel (1982), with subsequent contributions by Schick (1986); Klaassen (1987); Bickel et al. (1993), among others. More recent applications of this idea, also referred to as “cross-fitting”, include Chernozhukov et al. (2018); Athey and Wager (2020); Belloni et al. (2012); Zheng and van der Laan (2011). This paper is especially similar in spirit to “double machine-learning” (Chernozhukov et al., 2018), which combines sample-splitting with the use of Neyman-orthogonal scores, which have the property of being insensitive to small errors in estimating the nuisance function. Although the results of Chernozhukov et al. (2018) do not directly carry over to our setting, we use similar arguments to establish our results. A second strand of related literature concerns “agnostic” regression adjustment, which delivers consistent estimates of the average treatment estimate even when the regression model is misspecified Yang and Tsiatis (2001); Freedman (2008); Lin (2013); Guo and Basse (2020); Cohen and Fogarty (2020). The procedure described in Cohen and Fogarty (2020) is particularly relevant, as it shares the same structure of first estimating nonlinear models and then calibrating them in a linear regression step, although in contrast to their work we use sample-splitting to allow for a very general class of nonlinear ML models. A third strand of the literature considers improving estimator precision in the context of large-scale online experiments Chapelle et al. (2012); Deng et al. (2013); Coey and Cunningham (2019); Xie and Aurisset (2016).

Relative to these literatures, our contribution is to describe an estimator which i) delivers substantial variance reduction when good ML predictors of the outcome variable are available, and ii) performs well in the presence of poor-quality predictions, even allowing for predictive models which never converge to the truth with infinite data. In particular, MLRATE is guaranteed to never perform worse, asymptotically, than the difference-in-means estimator, even with arbitrarily poor predictions. In contrast to low-dimensional regression adjustment, we give formal statistical guarantees on inference even when complex ML models are used to predict outcomes; in contrast to double-ML, as applied to randomized experiments, our proposed estimator need not be semiparametrically efficient, but allows for inconsistent estimates of the nuisance parameters. Finally, this methodology is practical and computationally efficient enough to be deployed at large scale, and we show with Facebook data that MLRATE can deliver substantial additional variance reduction beyond the existing state-of-the-art commonly used in practice, of linear regression adjustment for pre-experiment covariates (Deng et al., 2013; Xie and Aurisset, 2016).

2.3 Estimation and inference with MLRATE

The linear regression-adjusted estimator of the ATE is the OLS estimate of in the regression

| (2.1) |

where is the average of over all . The covariates may be multivariate, but are of fixed dimension that does not grow with the sample size. The analysis in Lin (2013) establishes that the OLS estimator for is a consistent and asymptotically normal estimator of the ATE , and the robust, Huber-White standard errors are asymptotically valid. In contrast to this setting, we wish to capture complex interactions and nonlinearities in the relationship between the outcome and covariates, and allow for a vector of covariates with dimension potentially increasing with the sample size. To this end, we propose the following procedure. We assume throughout that is evenly divisible by , to simplify notation.

Section 2.4 proves the statistical validity of this estimation and inference procedure. Note that if the cross-fitted, random functions were replaced by a single, fixed function , MLRATE reduces to the standard linear regression-adjusted estimator. Instead the relation between the covariates and the outcome is itself estimated from the data. Intuitively this should help with variance reduction, as the estimated proxy may be highly correlated with , but with the challenge that the dependence of the ’s on the data complicates the analysis of the statistical properties of the treatment effect estimator . Our main technical result assuages this concern, showing that the asymptotic distribution of is not impacted and thus it is a consistent, asymptotically normal estimator of the ATE. CIs with level percent are given in the usual way by , where is the CDF of the standard normal distribution.

Remark 2.1.

The chief purpose of cross-fitting is to avoid bias from overfitting. With sufficiently flexible ML models, in-sample predictions would be close to the outcomes . The linear regression step would then amount to adjusting for the outcome variable itself, which is correlated with the treatment, and this may introduce severe attenuation bias into estimates of the treatment effect. By generating predictions only on out-of-sample data, we ensure the adjustment covariate is independent of the treatment.

Remark 2.2.

In online experiments, only a subset of users are typically assigned to any given experiment. To maximize training data and minimize compute costs, an equally valid variation on the above is to perform the cross-fitting ML step once, using data from all users, whereas the linear regression step must occur separately for every experiment of interest, using only the users in that experiment.

Remark 2.3.

Alternatively, one may estimate a single ML model entirely on pre-experiment data. For an experiment starting at time , we may train a model predicting time outcomes from time covariates, and then use that model to predict time outcomes from time covariates. Those model predictions can then be treated as any other covariate, as they are entirely a function of pre-experiment data, and the results of (Lin, 2013) apply. Although simpler, this approach suffers from the drawbacks that it requires some history of the outcome metric to exist even pre-experiment, and that the predictive model may perform worse if the relationship between covariates and outcomes changes over time.

Remark 2.4.

The choice of does not affect the asymptotic distribution of the estimator, although it may matter in finite samples. As Chernozhukov et al. (2018) note, in cross-fitting applications involving estimating high-dimensional nuisance functions with small samples, larger values of (e.g. or 5) may perform better. Much larger values of may be unattractive, however, given diminishing returns in model performance and the extra compute cost. In the simulations and empirical examples in Section 3 we show that good performance is achievable even with the low computation choice of .

We now sketch the main technical result. Beyond standard regularity conditions, the main assumption is that for each split , the estimated functions converge to some in the sense that . This condition is quite weak in two aspects: On the one hand, it only requires convergence of the to , and not convergence at a particular rate. Such consistency results are available for many common ML algorithms, including random forests (see Athey et al. (2019) and references therein), gradient boosted decision trees (Biau and Cadre, 2021), deep feedforward neural nets (Farrell et al., 2021), and regularized linear regression in some asymptotic regimes (Knight and Fu, 2000). On the other hand, we allow the ML modelling step to be misspecified and inconsistent: there is no requirement that , although a poorly-specified ML model may limit the variance reduction obtained. Allowing for inconsistent estimators is an especially important advantage in the presence of high-dimensional covariates, as in such settings there is no general guarantee that ML estimators will be consistent if the number of covariates grows faster than , due to the curse of dimensionality (Stone, 1982).

To make explicit the dependence on the ’s, we denote MLRATE by . We denote by the linear regression adjustment estimator as in (2.1) where we adjust for the covariate . This latter estimator is infeasible as is unknown, but we prove in Theorem 2.1 below that the two estimators are asymptotically equivalent, i.e. . Deriving the asymptotic distribution of is straightforward, and from this equivalence we conclude that shares the same asymptotic distribution.

2.4 The asymptotic behavior of MLRATE

Define the covariate vector as a function of an arbitrary (possibly random) function , , and define for . We adopt the notation .111If the input function is random, the quantity is also a random variable. If it is a deterministic function , then is the same as the expectation . In what follows, matrix norms refer to the operator norm, and denotes the minimum eigenvalue of the symmetric matrix . Recall that given the assumption of equally-sized splits, . All proofs are in the Appendix.

Assumption 2.1.

i) . ii) For all , the estimated functions belong to a vector space of functions with probability one, with satisfying for some . iii) . iv) For each , converges to some function in the sense that . v) .

Condition i) is a standard assumption in randomized controlled trials, while conditions ii) and iii) are standard boundedness requirements. Condition iv) is the convergence assumption discussed above. Condition v) can be motivated with reference to the scientific question at hand: restricting attention only to adjustment functions which exhibit nontrivial variation with respect to the value of the covariate is unlikely to hurt the amount of variance reduction achieved.

The following proposition ensures that the inverse of exists for all .

Proposition 2.1.

Given Assumption 2.1, .

Define

| (2.2) |

and

| (2.3) |

These are the sample and population OLS coefficients, from the regression of on . We also define the corresponding quantities for the limiting function ,

| (2.4) |

and

| (2.5) |

The key intermediate step in deriving the asymptotic distribution of MLRATE is the following result, which states that the distribution of , centered around the random variable , is asymptotically equivalent to that of , centered around .

Proposition 2.2.

Under Assumption 2.1,

Having established Proposition 2.2, we turn to the limiting distribution of MLRATE. This is not quite immediate: the estimator is defined as the coefficient on in the regression of on a constant, , , and . By contrast, Proposition 2.2 concerns the regression of on a constant, , , and . To conclude the argument we write MLRATE in terms of the coefficients from the latter regression, and apply Proposition 2.2. MLRATE, , can be written as

| (2.6) |

We also define , the corresponding quantity using the unknown :

| (2.7) |

The ATE satisfies

| (2.8) |

Here denotes the -th entry of ; and are similarly defined. To see why (2.8) hold, note that holds for any function : this is essentially a restatement of the observation that regardless of the particular covariate we adjust for, the regression-adjusted estimator will still be consistent for the ATE Yang and Tsiatis (2001); Tsiatis et al. (2008). This argument resembles the idea of Neyman orthogonality (Neyman (1959); Chernozhukov et al. (2018)), where the estimate of the parameter of interest is not heavily influenced by an undesirable estimate of the nuisance function.

We now state our main theorem, which asserts that the randomness from the ML function fitting step in MLRATE does not affect its asymptotic distribution.

Theorem 2.1.

Given Theorem 2.1, the problem of finding the asymptotic distribution of MLRATE reduces to finding the asymptotic distribution of . The latter, summarized in the following proposition, can be established by standard asymptotic arguments, and is already known in the literature.222See, for example, equation (10) in Yang and Tsiatis (2001). Note that there is a small typo in that display: it should read instead of . Define , , , and . For notational convenience, below we use to denote for each .

Proposition 2.3.

If , , and , then , where

| (2.9) |

Putting together the previous results, we arrive at the asymptotic distribution for MLRATE, which is asymptotically normal and centered around the ATE .

Corollary 2.1.

Under Assumption 2.1, , where

| (2.10) |

It follows directly from this corollary that the asymptotic variance of MLRATE is smaller than variance of the simple difference-in-means estimator by the amount

Thus ML regression adjustment, like ordinary linear regression adjustment Yang and Tsiatis (2001); Lin (2013), cannot reduce asymptotic precision. For some intuition about the determinants of variance reduction, consider the special case where (i.e. the slope of the best-fitting linear relationship between and does not vary from test to control groups), and . The unadjusted, difference-in-means estimator has asymptotic variance . The relative efficiency of the adjusted estimator, , equals . If , regression adjustment shrinks CIs by ; with a correlation of 0.8, they are 40% smaller.

The following proposition shows that the sample analog of (2.10) is a consistent estimator of the asymptotic variance, and it can thus be used to construct asymptotically valid CIs.

Proposition 2.4.

3 Simulations & empirical results

We now validate MLRATE in practice, on both simulated data, and real Facebook user data. These two validation exercises serve complementary purposes: simulations allow us to verify that the CIs’ empirical coverage is indeed close to their nominal coverage for the data generating process of our choice, while the Facebook data gives an indication of the magnitude of variance reduction that can be expected in practice. All computation is done on an internal cluster, on a standard 64GB ram machine.

Our simulated data generating process has 10,000 iid observations and 100 covariates distributed as . The outcome variable is , where is the Friedman function and the treatment effect function is (Friedman, 1991; Nie and Wager, 2020). The treatment indicator is , and the error term is . Treatment is independent of covariates and the error term, and the error term is independent of the covariates. This data generating process involves non-trivial complexity, with nonlinearities and interactions in the baseline outcome, many extraneous covariates that do not affect outcomes, and heterogeneous treatment effects correlated with some covariates. We find the ATE by Monte Carlo integration, and compute the average number of times the MLRATE CIs contain this ATE, over 10,000 simulation repetitions, as well as 95% CIs for this coverage percentage. Both in these simulations and the subsequent analysis of Facebook data, we choose gradient boosted regression trees (GBDT) and elastic net regression as two examples of ML prediction procedures in MLRATE, with scikit-learn’s implementation Pedregosa et al. (2011). Moreover, we choose splits for cross-fitting.

| MLRATE-GBDT | MLRATE-Elastic Net | Unadjusted | |

| CI Coverage (%) | |||

| Relative CI Width | 0.62 | 0.86 | 1.00 |

Table 1 shows the simulation results. “CI Coverage” displays the average coverage percentage rate over the 10,000 simulations, and the CI width for these estimated coverage rates. “Relative CI Width” displays the CI width for each method divided by the simple difference-in-means CI width (“Unadjusted”), averaged over the 10,000 simulations. Empirical coverage is close to the nominal coverage for all three estimators, with the CIs for empirical coverage including the nominal rate. Both the GBDT and elastic net versions of MLRATE demonstrate efficiency gains over the difference-in-means estimator. As might be expected given the highly nonlinear dependence of the outcomes on covariates, GBDT performs substantially better than the linear, elastic net model: on average across simulations, the MLRATE-GBDT CIs are 62% the width of the unadjusted CIs, whereas the analogous figure for the elastic net CIs is 86%. Also of interest is the comparison to the semiparametric efficiency bound (Newey, 1994; Hahn, 1998), which can be calculated explicitly for this data generating process: despite the fact that MLRATE is agnostic, and does not assume consistency of the ML procedure employed, the MLRATE-GBDT CIs are only 11.3% wider than those implied by the semiparametric efficiency bound.

The variance reduction numbers above are of course dependent on the particular data generating process specified in the simulation. To get a better sense of the magnitudes of variance reduction one might expect in practice, we evaluate the estimator on 48 real metrics used in online experiments run by Facebook, capturing a broad range of the most commonly consulted user engagement and app performance measurements. We focus on A/A tests in this evaluation rather than A/B tests run in production. This is because the true effect is unknown in the latter, which makes it impossible to evaluate the coverage properties of the CI. Because treatments in online experiments are typically subtle and are unlikely to greatly change the relationship between outcomes and covariates, the magnitude of variance reduction will likely be very similar in A/B tests.

For each outcome metric, we select a random sample of approximately 400,000 users, and simulate an A/A test by assigning a treatment indicator for each user, drawn from a Bernoulli(0.5) distribution. The features used in the ML model vary for each metric and consist of the pre-experiment values of the metric, as well as the pre-experiment values of other metrics that have been grouped together as belonging to the same product area. There are between 20 and 100 other such metrics, with the exact number depending on the outcome metric in question. Outcome values are calculated as the sum of the daily values over a period of one week, and the features values are calculated as the sum of the daily values over the three weeks leading up to the experiment start date.

For each metric, we calculate variances and CI width for four estimators of the ATE: The difference-in-means estimator; A univariate linear regression adjustment procedure of equation (2.1) where the only covariate is the pre-experiment value of the outcome metric (for simplicity, we denote it by ‘LinInteract’); And MLRATE-GBDT/Elastic Net with all available pre-experiment metrics used as features.

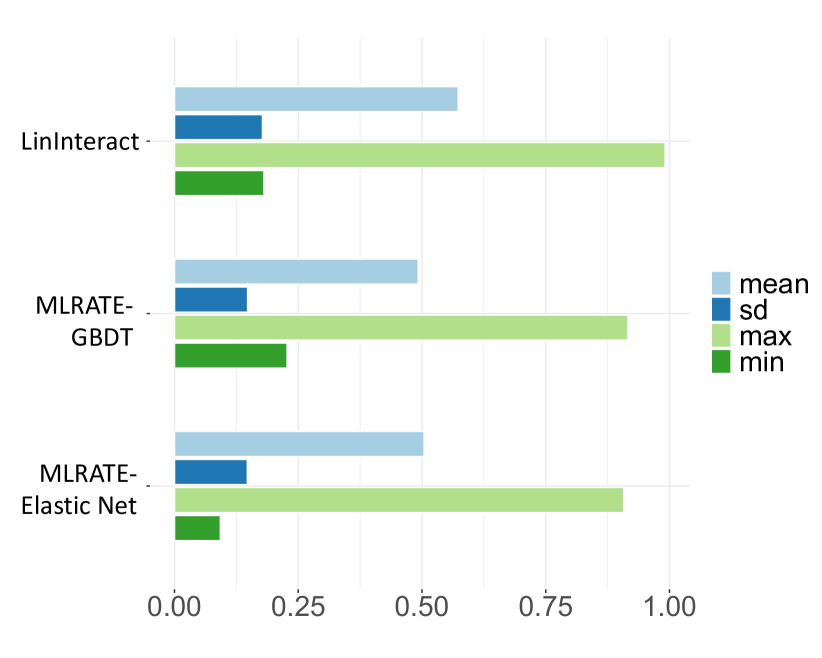

Figure 1(a) shows that LinInteract substantially outperforms the simple difference-in-means estimator, and MLRATE delivers additional gains still. Unlike in the simulated data generating process above, MLRATE-GBDT and MLRATE-Elastic Net perform similarly. The variance reduction relative to the difference-in-means estimator is 72 - 74% on average across metrics, and relative to LinInteract is 19%. The corresponding figures for reduction of the average CI width are 50 - 51%, and 11 - 12%, respectively. Alternatively, to achieve the same precision as the MLRATE-GBDT estimator, the difference-in-means estimator would require sample sizes on average 5.44 times as large on average across metrics and the univariate procedure would require sample sizes 1.56 times as large.

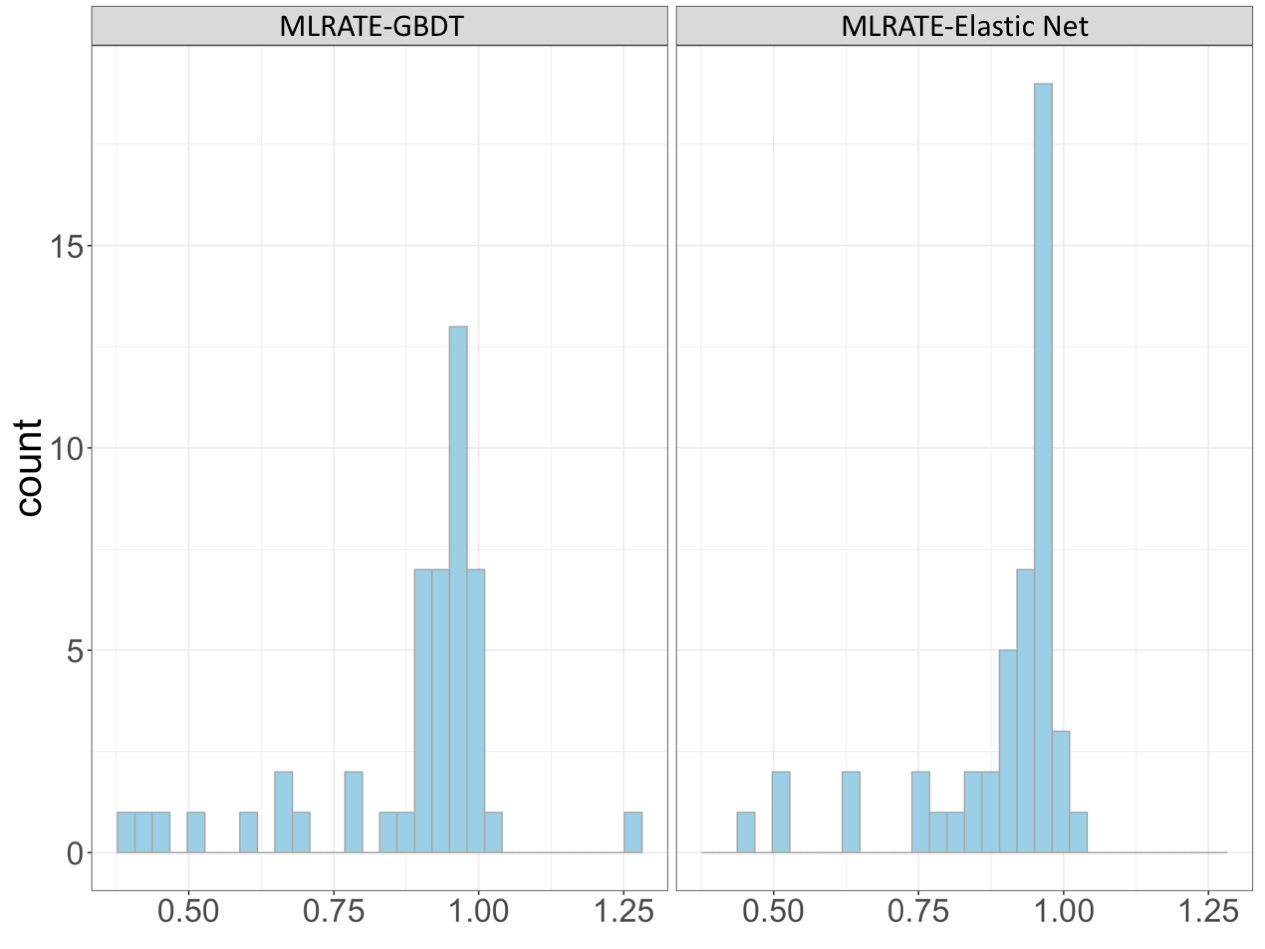

Figure 1(b) displays the metric-level distribution of CI widths relative to the univariate adjustment case. There is substantial heterogeneity in performance across metrics: for some, ML regression adjustment delivers only quite modest gains relative to univariate adjustment, while for others, it drastically shrinks CIs. This is natural given the variety of metrics in the analysis: some, especially binary or discrete outcomes, may benefit more from more sophisticated predictive modelling, whereas for others simple linear models may perform well. For some metrics, CIs are shrunk by half or more, which may be the difference between experimentation for those metrics being practical and not. As in the simulations, the coverage rates for ML regression adjusted CIs for these metrics are close to the nominal level. For the metric experiencing the largest variance reduction gains from MLRATE—where one might be the most concerned with coverage—we find an average coverage rate of 94.90% over 10,000 simulated A/A tests, where each simulated A/A test is carried out on a 10% subsample drawn at random with replacement from the initial user dataset.

We remark that we design our evaluation to give a realistic sense of the potential variance reduction gains that can be attained with minimal effort and common software implementations of standard ML algorithms. In fact, the supervised learning models we use in this analysis–GBDT and elastic net regression–are deliberately simple, and the training data sample sizes of around 400,000 observations are not especially large by the standards of online A/B tests. The input features to the models are not heavily preprocessed: they are typically raw logged metric values, as opposed to, say, embeddings generated by a prior ML layer. Moreover, as already mentioned in remark 2.4, we always choose the number of splits instead of treating it as a hyperparameter and tuning for better performance. We expect that with more sophisticated supervised learning techniques (e.g. deep, recurrent neural networks with transfer learning across metrics), larger datasets, and better choice of through cross-validation, the precision gains could be considerably greater still.333In Figure 1(b), one metric in the GBDT case has substantially larger variance than the univariate adjustment case, indicating that the default GBDT fit performs quite poorly on this sample. Larger sample sizes or more customized ML modeling will have the benefit of attenuating such anomalies.

In the simulations and the empirical study above, the dimension of the covariates is not large compared to the sample size. However, our algorithm applies equally to the high-dimensional regime. In many high-dimensional applications, Assumption 2.1 can be easily satisfied, and our theory fully extends to this case.

4 Implementation

The key guiding principle for selecting features for the ML model is that we can use any variables independent of treatment assignment. Thus any variable extracted before the experiment start is eligible. This simple rule facilitates collaboration with engineering and data science partners familiar with forecasting: they can freely apply their domain expertise to engineer features and build predictive models for specific metrics, without concerns about statistical validity as long as the cross-fitting step in MLRATE is enforced.

The ML step in MLRATE means that the analyst can err on the side of inclusivity in deciding what features to use, as irrelevant features will tend to be omitted from the fitted model. In contrast to Deng et al. (2013), for example, we are automatically learning the one ‘feature’ () that has the best predictive power instead of restricting ourselves to a particular pre-experiment feature, thus allowing for greater overall variance reduction. Moreover, this method is highly scalable as the ML step does not need to be performed once per experiment. Once predictions have been generated for a given metric, they can be used to improve precision for all experiments starting after the period used for feature construction.

For real-world applications, the linear regression step in MLRATE, which ensures non-inferiority relative to the difference-in-means estimator, is an important safeguard. There may be no guarantee in practice that the predictive models produced by modeling teams will always be well-calibrated, and without the linear regression layer this non-inferiority guarantee need not hold.

Finally, we note that an additional “censoring” step may be useful when the metric has substantial mass close to zero, reducing computation cost without significantly affecting estimation accuracy. After training the models , instead of regression adjustment using , define for some pre-determined threshold , where is the hard-thresholding operator Then one can perform regression adjustment with in place of , with the same statistical theory applying. Small values of will cause small efficiency losses, but can greatly reduce the computation cost on the linear regression when is large.444Covariance computations need only be explicitly performed on users with either non-zero metric values or a non-zero regressor (users with both values equal to zero can be separately accounted for). As such, the compute costs of these queries can end up being approximately linear in the number of non-truncated users when the outcome metric is sparse.

5 Conclusion

MLRATE is a scalable methodology that allows ML algorithms to be used for variance reduction, while still giving formal statistical guarantees on consistency and CI coverage. Of particular practical importance is the methodology’s robustness to the ML algorithm used, both in the sense that the ML algorithm used need not be consistent for the truth, and in the sense that no matter how bad the ML predictions are, MLRATE has asymptotic variance no larger than the difference-in-means estimator. Our application to Facebook data demonstrates variance reduction gains using pre-experiment covariates and even simple predictive algorithms. We expect that more sophisticated predictive algorithms, and incorporating other covariates into this framework–for example, generating user covariates by synthetic-control inspired strategies that incorporate contemporaneous data on outcomes for individuals outside the experiment–could lead to more substantial efficiency gains still.

Appendix A Proof of Proposition 1

For any (deterministic) , we have

where denotes the Kronecker product,

Therefore, any eigenvalue of is the product of one eigenvalue of and one eigenvalue of . It’s easy to verify from Assumption 1 that all eigenvalues of and are nonnegative and bounded. Thus, we only need to show , .

Through some calculations, one can find out that

which leads to

On the other hand, can be deduced from . By combining the above two inequalities, we conclude the proof.

Appendix B Proof of Proposition 2

For compactness we may write the random variables as and as . Similarly for any observation we write as and as . We are only interested in convergence in probability, so we can assume that the inverse matrices in the definition of and exist, as this happens with probability approaching 1 according to Lemma E.2. We have where

and

Similarly, where

and

We can write . We show that and . From the definitions of and above, we have If

-

1.

-

2.

-

3.

-

4.

,

then as desired. Similarly we write as

If

-

5.

-

6.

-

7.

-

8.

then as desired. We complete the proof in 8 steps by showing statements 1 - 8 above.

Step 1.

We apply Lemma E.3 by letting . Consequently, Step 1 amounts to verifying the conditions of Lemma E.3. In fact, these conditions are guaranteed by Lemma E.1 as well as the following fact: For each ,

| (B.1) |

We now prove (B.1). Define , and note that conditional on the data in , the function is non-random, and the are mean zero matrices, uncorrelated across observations in . With slight abuse of notation, we use to denote expectations conditional on the observations with indices belonging to the set . For any ,

| (B.2) | ||||

| (B.3) | ||||

| (B.4) | ||||

| (B.5) |

If the RHS of (B.5) is , we can use Lemma 6.1 of Chernozhukov et al. (2018) to conclude that is as required. Some calculations give

| (B.6) |

Then Also

| (B.7) | ||||

| (B.8) | ||||

| (B.9) | ||||

| (B.10) |

where the second-to-last line follows because as is a vector space. We conclude from (B.6) that the RHS of (B.5) is .

Step 2.

By the Cauchy-Schwarz inequality,

| (B.11) |

As , the second term on the RHS is by Markov’s inequality. Also for , , and by Markov’s inequality the first term on the RHS is also .

Step 3.

By the central limit theorem, is asymptotically normal. By the delta method and invertibility of , is also, and hence its norm is .

Step 4.

We show that for any , , from which the result follows. By Cauchy-Schwarz,

As has finite second moment by assumption, it remains to show the first term on the RHS is . We have

| (B.12) |

From Lemma 6.1 in Chernozhukov et al. (2018), the first term on the RHS in (B.12) is and by the convergence assumption on , the second term is too.

Step 5.

By the continuous mapping theorem it suffices to show that

From the argument in Step 1, both and are for all , and hence and are both for all . The other entries in the matrix are straightforwardly .

Step 6.

This follows from Step 8 and the fact that by Chebyshev’s inequality, .

Step 7.

is invertible by assumption.

Step 8.

The reasoning here is similar to Step 1. For any and , define , and note that conditional on the data in , the are mean zero matrices, uncorrelated across observations in . Then

Because , the RHS of (B) is . We use Lemma 6.1 of Chernozhukov et al. (2018) to conclude that is also , from which the result follows.

Appendix C Proof of Theorem 1

We have

| (C.1) | ||||

| (C.2) | ||||

| (C.3) |

where

| (C.4) |

and

| (C.5) |

Proposition 1 has established that . Moreover

| (C.6) |

and

| (C.7) |

We show and are to conclude. In fact

| (C.8) |

This is because

-

•

from Proposition 1;

-

•

from the LLN and the same logic bounding (B.12) above;

-

•

from the CLT and the fact that has all eigenvalues bounded away from 0;

-

•

again from bounding argument applied to (B.12).

Similarly,

| (C.9) |

which results from the following facts:

-

•

;

-

•

from the same reasoning applied to bound (B.1);

-

•

due to convergence of to , continuity of , and the continuous mapping theorem;

-

•

from the CLT.

Combining the above arguments, we conclude that .

Appendix D Proof of Proposition 4

We first show that . We have

| (D.1) |

By the same logic as in Step 1 of the proof of Proposition 1, for each ,

and so . Since , it follows that . Similarly . Hence . Also, by Proposition 1,

| (D.2) |

and by continuity of and the continuous mapping theorem,

| (D.3) |

Consequently . By the continuous mapping theorem, we conclude that .

Appendix E Proof of auxiliary lemmas

Lemma E.1.

Given Assumption 1,

Proof.

Since the number of splits is bounded, we only need to verify for any ,

Below we’ll prove

| (E.1) |

The other terms can be derived in the similar manner.

First, since as , we know that for any subsequence of , it further has a subsequence , such that a.s. as . Our next step is to prove

| (E.2) |

as .

For notational simplicity, define . Since are independent conditioned on , for any we have

Furthermore,

| (E.3) |

Our goal is now to derive the limit in the last term so that we can infer the limiting distribution of .

First, we conduct the Taylor expansion

Here

Thus

| (E.4) |

First, with probability 1,

| (E.5) |

Next, we bound . In fact,

This means

where ,

.

On the one hand,

On the other hand, by Markov’s inequality,

Combining the above two bounds, we deduce that

Thus with probability 1, .

Finally we plug the above into (E.3) and conclude that

This implies that converges in distribution to a centered normal random variable with variance , and (E.2) follows.

Finally, since for any subsequence of , it further has a subsequence such that (E.2) holds, it can only be the case that (E.1) is true.

∎

Lemma E.2.

The following hold with probability tending to 1:

| (E.6) |

| (E.7) |

Proof.

Lemma E.3.

Let be sequences of random real symmetric matrices of fixed dimension. Assume that with probability 1, , and . Moreover, assume that

If in addition,

then

Proof.

Define the event

Then . Now on , according to a Neumann series expansion,

Here , and we have on

| (E.8) |

Here we use the fact that on

Similar expansions hold for , and , and we define , and accordingly. Using some simple algebra, we deduce that on ,

where

For any ,

| (E.9) |

Combining the fact that , we only need to prove that each of the rest of the terms on the the RHS of (E.9) has limit 0.

First, follows from our assumption. For , observe that where

We bound the limit of as follows: For any , there exists such that , . According to our assumption, there further exists such that for all , . Therefore for all ,

The above argument implies that . Similarly we have . Thus

Now we proceed to bound the limit of . In fact we have

In the last inequality we utilize (E.8). Combining our assumptions, we have

Similarly

We conclude our proof. ∎

References

- Andrews (1994) Andrews, D. W. (1994). Empirical process methods in econometrics. Handbook of econometrics, 4 2247–2294.

- Athey et al. (2019) Athey, S., Tibshirani, J. and Wager, S. (2019). Generalized random forests. The Annals of Statistics, 47 1148–1178.

- Athey and Wager (2020) Athey, S. and Wager, S. (2020). Policy learning with observational data.

- Belloni et al. (2012) Belloni, A., Chen, D., Chernozhukov, V. and Hansen, C. (2012). Sparse models and methods for optimal instruments with an application to eminent domain. Econometrica, 80 2369–2429.

- Biau and Cadre (2021) Biau, G. and Cadre, B. (2021). Optimization by gradient boosting. In Advances in Contemporary Statistics and Econometrics. Springer, 23–44.

- Bickel (1982) Bickel, P. J. (1982). On adaptive estimation. The Annals of Statistics 647–671.

- Bickel et al. (1993) Bickel, P. J., Klaassen, C. A., Bickel, P. J., Ritov, Y., Klaassen, J., Wellner, J. A. and Ritov, Y. (1993). Efficient and adaptive estimation for semiparametric models, vol. 4. Johns Hopkins University Press Baltimore.

- Chapelle et al. (2012) Chapelle, O., Joachims, T., Radlinski, F. and Yue, Y. (2012). Large-scale validation and analysis of interleaved search evaluation. ACM Transactions on Information Systems (TOIS), 30 1–41.

- Chernozhukov et al. (2018) Chernozhukov, V., Chetverikov, D., Demirer, M., Duflo, E., Hansen, C., Newey, W. and Robins, J. (2018). Double/debiased machine learning for treatment and structural parameters. The Econometrics Journal, 21.

- Coey and Cunningham (2019) Coey, D. and Cunningham, T. (2019). Improving treatment effect estimators through experiment splitting. In The World Wide Web Conference.

- Cohen and Fogarty (2020) Cohen, P. L. and Fogarty, C. B. (2020). No-harm calibration for generalized oaxaca-blinder estimators.

- Deng et al. (2013) Deng, A., Xu, Y., Kohavi, R. and Walker, T. (2013). Improving the sensitivity of online controlled experiments by utilizing pre-experiment data. In Proceedings of the sixth ACM international conference on Web search and data mining.

- Farrell et al. (2021) Farrell, M. H., Liang, T. and Misra, S. (2021). Deep neural networks for estimation and inference. Econometrica, 89 181–213.

- Freedman (2008) Freedman, D. A. (2008). On regression adjustments to experimental data. Advances in Applied Mathematics, 40 180–193.

- Friedman (1991) Friedman, J. H. (1991). Multivariate adaptive regression splines. The annals of statistics 1–67.

- Guo and Basse (2020) Guo, K. and Basse, G. (2020). The generalized oaxaca-blinder estimator. arXiv preprint arXiv:2004.11615.

- Hahn (1998) Hahn, J. (1998). On the role of the propensity score in efficient semiparametric estimation of average treatment effects. Econometrica 315–331.

- Kennedy (2016) Kennedy, E. H. (2016). Semiparametric theory and empirical processes in causal inference. In Statistical causal inferences and their applications in public health research. Springer, 141–167.

- Klaassen (1987) Klaassen, C. A. (1987). Consistent estimation of the influence function of locally asymptotically linear estimators. The Annals of Statistics 1548–1562.

- Knight and Fu (2000) Knight, K. and Fu, W. (2000). Asymptotics for lasso-type estimators. Annals of statistics 1356–1378.

- Lin (2013) Lin, W. (2013). Agnostic notes on regression adjustments to experimental data: Reexamining freedman’s critique. The Annals of Applied Statistics, 7 295–318.

- Newey (1990) Newey, W. K. (1990). Semiparametric efficiency bounds. Journal of applied econometrics, 5 99–135.

- Newey (1994) Newey, W. K. (1994). The asymptotic variance of semiparametric estimators. Econometrica: Journal of the Econometric Society 1349–1382.

- Newey and Robins (2018) Newey, W. K. and Robins, J. R. (2018). Cross-fitting and fast remainder rates for semiparametric estimation. arXiv preprint arXiv:1801.09138.

- Neyman (1959) Neyman, J. (1959). Optimal asymptotic tests of composite hypotheses. Probability and statistics 213–234.

-

Nie and Wager (2020)

Nie, X. and Wager, S. (2020).

Quasi-Oracle Estimation of Heterogeneous Treatment Effects.

Biometrika.

Asaa076.

https://doi.org/10.1093/biomet/asaa076 - Pedregosa et al. (2011) Pedregosa, F., Varoquaux, G., Gramfort, A., Michel, V., Thirion, B., Grisel, O., Blondel, M., Prettenhofer, P., Weiss, R., Dubourg, V. et al. (2011). Scikit-learn: Machine learning in python. The Journal of Machine Learning Research, 12 2825–2830.

- Robinson (1988) Robinson, P. M. (1988). Root-n-consistent semiparametric regression. Econometrica: Journal of the Econometric Society 931–954.

- Schick (1986) Schick, A. (1986). On asymptotically efficient estimation in semiparametric models. The Annals of Statistics 1139–1151.

- Stone (1982) Stone, C. J. (1982). Optimal global rates of convergence for nonparametric regression. The annals of statistics 1040–1053.

- Taddy et al. (2016) Taddy, M., Lopes, H. F. and Gardner, M. (2016). Scalable semiparametric inference for the means of heavy-tailed distributions. arXiv preprint arXiv:1602.08066.

- Tsiatis (2007) Tsiatis, A. (2007). Semiparametric theory and missing data. Springer Science & Business Media.

- Tsiatis et al. (2008) Tsiatis, A. A., Davidian, M., Zhang, M. and Lu, X. (2008). Covariate adjustment for two-sample treatment comparisons in randomized clinical trials: a principled yet flexible approach. Statistics in medicine, 27 4658–4677.

- Van der Laan and Rose (2011) Van der Laan, M. J. and Rose, S. (2011). Targeted learning: causal inference for observational and experimental data. Springer Science & Business Media.

- Van der Vaart (2000) Van der Vaart, A. W. (2000). Asymptotic statistics. Cambridge University Press.

- Van Der Vaart and Wellner (1996) Van Der Vaart, A. W. and Wellner, J. A. (1996). Weak convergence. In Weak convergence and empirical processes. Springer, 16–28.

- Wager et al. (2016) Wager, S., Du, W., Taylor, J. and Tibshirani, R. J. (2016). High-dimensional regression adjustments in randomized experiments. Proceedings of the National Academy of Sciences, 113 12673–12678.

- Xie and Aurisset (2016) Xie, H. and Aurisset, J. (2016). Improving the sensitivity of online controlled experiments: Case studies at netflix. In Proceedings of the 22nd ACM SIGKDD International Conference on Knowledge Discovery and Data Mining.

- Yang and Tsiatis (2001) Yang, L. and Tsiatis, A. A. (2001). Efficiency study of estimators for a treatment effect in a pretest–posttest trial. The American Statistician, 55 314–321.

- Zheng and van der Laan (2011) Zheng, W. and van der Laan, M. J. (2011). Cross-validated targeted minimum-loss-based estimation. In Targeted Learning. Springer, 459–474.