The link between Bitcoin and Google Trends attention

Abstract

This paper shows that Bitcoin is not correlated to a general uncertainty index as measured by the Google Trends data of Castelnuovo and Tran, (2017). Instead, Bitcoin is linked to a Google Trends attention measure specific for the cryptocurrency market. First, we find a bidirectional relationship between Google Trends attention and Bitcoin returns up to six days. Second, information flows from Bitcoin volatility to Google Trends attention seem to be larger than information flows in the other direction. These relations hold across different sub-periods and different compositions of the proposed Google Trends Cryptocurrency index.

Keywords: Cryptocurrencies; Google Trends; transfer entropy ; market attention

JEL codes: G01; G14

1 Introduction

Since its creation in 2009, Bitcoin has gained a growing attention among investors, researchers and policy makers. The first advocates were libertarians critical to the global financial crisis of 2008. These investors saw blockchain as a mechanism to bypass the traditional financial system, which was severely criticized as its lax regulation was deemed to lead to the crisis. A second wave of Bitcoin enthusiasts were speculators, who saw in Bitcoin (and in newly minted cryptocurrencies) high-yield investment opportunities. A third wave of market participants were financial institutions, which aimed to introduce blockchain technology in their industry and offer investors more secure platforms for cryptoinvestment. At the same time, governments begun to worry about the potential negative effects of cryptocurrencies. Several countries have been introducing regulations (e.g., tax laws, anti-money laundering/anti-terrorism financing laws. See Global Legal Research Center, (2018)) and issuing warnings about the high risk of this type of investment (Martin, , 2021). Finally, a fourth wave of cryptocurrency market players currently taking place, is related to the so-called Central Bank Digital Currencies (Fernández-Villaverde et al., , 2020). For a detailed review on the evolution and current state of research on cryptocurrencies, we refer to Corbet et al., (2019) and Bariviera and Merediz-Solà, (2021), among others.

At the same time, the increasing digitalization of the economy has left a digital footprint that, in certain way, reveals preferences, tastes, or consumption habits. Given that cryptocurrencies are digitally native assets, investors tend to gather market information mainly through the internet (social networks, specialized forums, etc.). Specifically, Google searches tend to signal investors’ attention. Urquhart, (2018) is one of the earliest papers to relate cryptocurrency’s market attention with Google Trends, finding that realized volatility, volume and returns influence future search for the term ’Bitcoin’. Subsequently, Shen et al., (2019) point out that the number of tweets is a significant driver of Bitcoin trading volume and realized volatility.

Other researchers have used news-based uncertainty indices to assess the impact of uncertainty on Bitcoin. Demir et al., (2018) finds that the Economic Policy Uncertainty (EPU) index is negatively associated with Bitcoin daily returns. Walther et al., (2019), using a GARCH-MIDAS framework, finds that Global Real Economic Activity fares well in cryptocurrency volatility forecasting. In a similar vein, Fang et al., (2020) reports a significant impact of News Implied Volatility (NVIX) on long-term cryptocurrency volatility. Meanwhile, Aysan et al., (2019) detects significant predictive power of the Geopolitical Risk (GPR) index for both Bitcoin returns and volatility. More recently, Lucey et al., (2021) uses weekly data to construct cryptocurrency uncertainty indices based on a variety of news pieces from LexisNexis Business database. The authors carry out a historical decomposition and relate their cryptocurrency uncertainty indices to major economic and political events.

The aim of the present paper is to explore to what extent investors’ attention to the cryptocurrency market is captured by a set of keywords as measured by Google Trends. Compared to Twitter (where access is limited in time) or to LexisNexis (a subscription-based service), Google Trends is freely available. In addition, Google Trends is simple to obtain and potentially reflects the attention of a broader profile of investors.

Overall, our contribution to the literature is as follows. First, we construct a Google Trends cryptocurrency index to capture market attention. Second, we find that the Google Trends Uncertainty (GTU) index proposed by Castelnuovo and Tran, (2017) does not prove useful in reflecting cryptocurrency market attention. Third, we show that there are important information flows from Google Trends to the cryptocurrency market and viceversa, reflecting a recurring dialog between the market attention and investors’ interests. Finally, cryptocurrency market attention is well captured by a handful of keywords such as Bitcoin, BTC, blockchain, crypto, cryptocurrency.

2 Construction of Google Trends Cryptocurrency index

Following Castelnuovo and Tran, (2017), we update their Google Trends Uncertainty (GTU) index over the period 2015-2021. In addition, we construct a Google Trends Cryptocurrency (GTC) index, using a set of cryptocurrency-oriented keywords. It is reasonable to postulate that cryptocurrency investors gather information mainly through the internet. Even though there are several search engines (e.g., Google, Yahoo, Bing, Ask), Google clearly dominates the market. According to Johnson, (2021) the worldwide search market share of Google is 86.6%. Thus Google Trends could be used as a reliable measure for online searches.

The keywords that constitute our GTC index are selected using a bibliometric analysis of scientific papers in line with Merediz-Solà and Bariviera, (2019). The full set is composed by 38 keywords. In order to check the robustness of our results, we reduce the number of keywords, leaving only the ones that we consider more closely related to Bitcoin economics, while dropping more technical words such as ’hash’, ’hard fork’, ’proof of work’, etc. The list of the full set of keywords, as well as the three subsets of keywords of the index are detailed in the appendix. After obtaining the daily Google Trend index for each keyword, we compute the arithmetic mean for all the keywords, constituting the daily GTC index.

3 Methods

We measure information linkages between Bitcoin and market attention by means of Shannon Transfer Entropy (for details, see Dimpfl and Peter, (2013, 2018)). Shannon Transfer Entropy is a flexible, non-parametric method designed to overcome some of the limitations of Granger causality (the assumed linearity assumption).

Transfer Entropy is a measure based on the Kullback-Liebler distance of transition probabilities, and allows not only to determine the direction of information flows, but more importantly to quantify the strength of those flows.

Let consider two processes and , with marginal probability distributions and , and joint probability distribution , the Shannon transfer entropy (TE) can be defined as:

| (1) |

where is a measure of the information conveyed from to . Considering that TE could be a biased estimator of the information transfer, Marschinski and Kantz, (2002) proposed a modified metric, by removing the information produced by shuffled realization of the explanatory process as:

| (2) |

The Effective Transfer Entropy (ETE) shows not only the direction, but also the quantity of information transmited from one process to the other.

4 Empirical Analysis

4.1 Data

This paper uses daily data on Google Trends and Bitcoin prices. We calculate the Google Trends Uncertainty (GTU) index using the keywords of Castelnuovo and Tran, (2017), as well as our Google Trends Cryptocurrency (GTC) index proposed in Section 2. Bitcoin daily data is used to compute the logarithmic return and Parkinson, (1980) volatility111We also computed Garman and Klass, (1980) volatility. Although not displayed in the paper due to space considerations, results are similar.. For replication purposes, data used in this paper is available online along this paper.

We focus mainly on Bitcoin, since cryptocurrency market linkages (both in returns and volatilities) have become very strong in recent years (Aslanidis et al., , 2021).

The empirical results of this section are obtained using the GTC index with five keywords (Subset 2), but they are robust to a different selection of keywords. For details of the different selection of keywords, see the appendix.

4.2 Results

We explore by means of Transfer Entropy, the information exchange between the Bitcoin market and the Google Trends uncertainty (GTU) index. We use first differences of the Google Trends data to ensure stationarity. Table 1 shows that information flows between Bitcoin and GTU are not statistically significant, which indicates a detachment of cryptocurrencies from the general macroeconomic environment. This result is in line with previous findings (Corbet et al., (2018) and Aslanidis et al., (2019)), who report that major cryptocurrencies are rather isolated from traditional assets such as gold, stocks or bonds. Notice our finding is robust to a selection of different lag lengths, as observed in Figure 2.

| Direction | TE | ETE | Std.Err. | p-value |

|---|---|---|---|---|

| GTU→Return | 0.0036 | 0.0000 | 0.0013 | 0.2267 |

| Return→GTU | 0.0036 | 0.0006 | 0.0014 | 0.5067 |

| GTU→Volatility | 0.0022 | 0.0000 | 0.0013 | 0.6067 |

| Volatility →GTU | 0.0031 | 0.0004 | 0.0015 | 0.4967 |

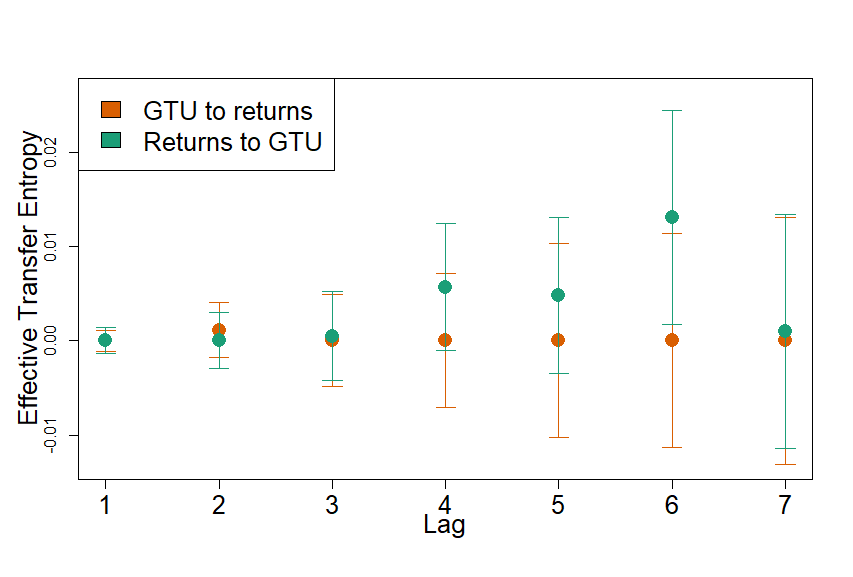

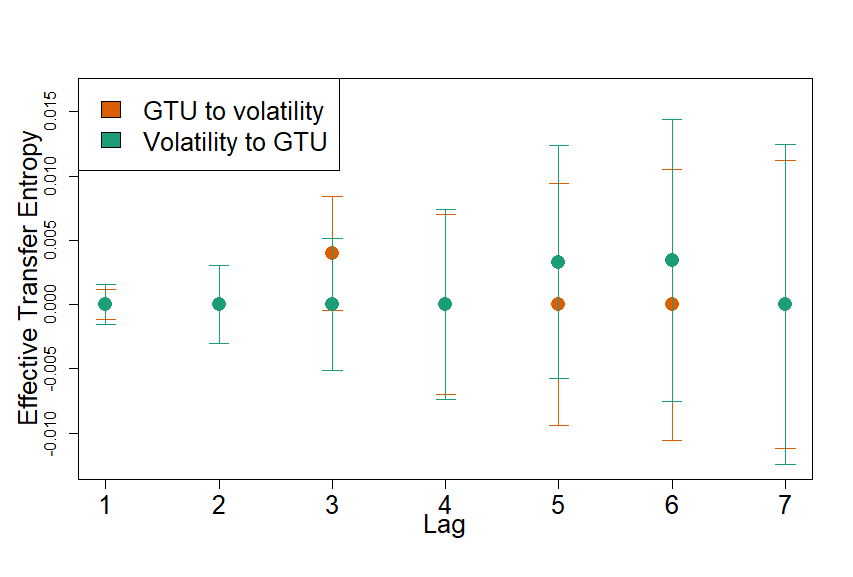

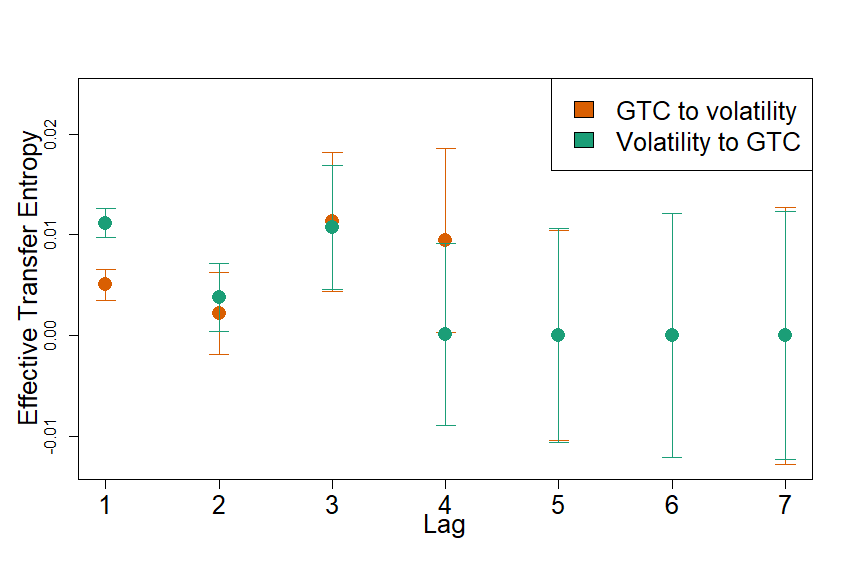

A different picture emerges, however, when analyzing Bitcoin returns/volatility with respect to the Google Trends Cryptocurrency (GTC) index. Table 2 displays the results of Transfer Entropy using just the first lag. As seen, there is a reciprocal flow of information between Bitcoin and GTC. We observe that the amount of information emitted and received between Bitcoin returns and market attention is similar. However, there is more information leaked from Bitcoin volatility to GTC than in the other direction.

Another important result is that the interdependence between GTC and returns is significant for up to six days (see Figure 3). On the contrary, the transfer of information between Bitcoin volatility and GTC holds strong for up to three days. This implies that news are absorbed by the market, although large price swings produce stronger market attention during several days.

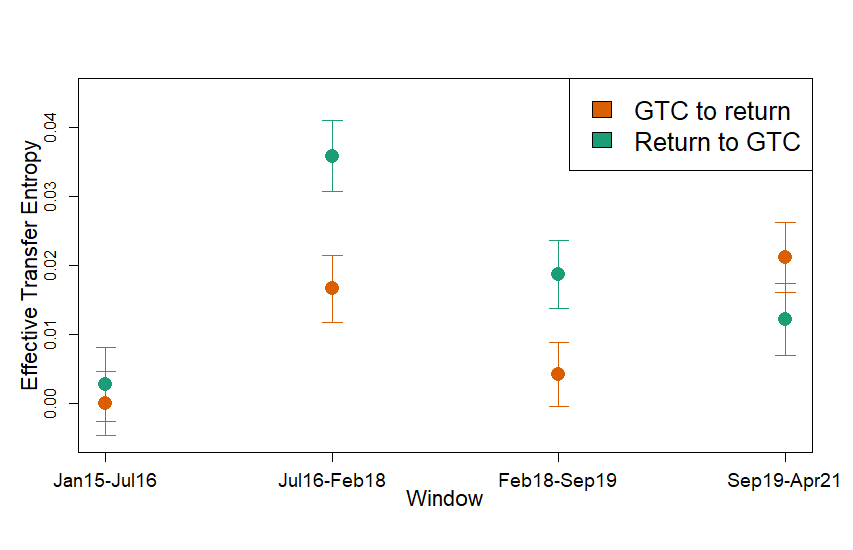

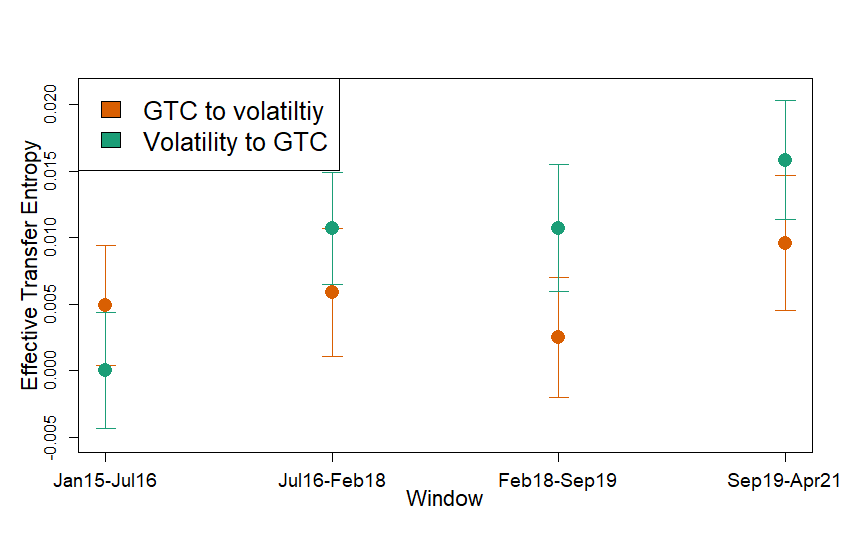

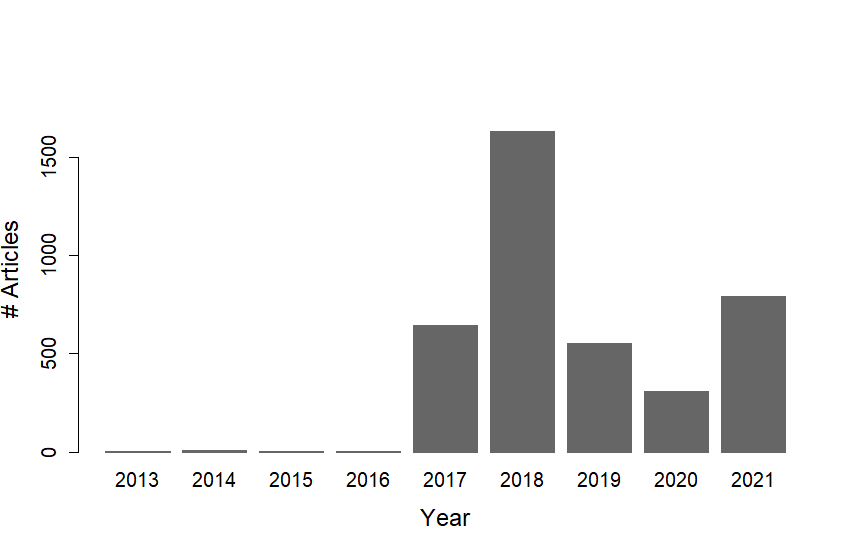

To analyze the information transfer over time, we divide our sample into four non-overlapping windows of 575 observations each. Results of ETE using the first lagged value of the variables are reported in Figure 4. We observe that in the first window (from January 2015 to July 2016) there is no information transfer between returns or volatilities and GTC. We should recall that until 2016 there was less public knowledge of cryptocurrencies. It was precisely in 2017 when Bitcoin price rose from $ 800 to $ 20000, and cryptocurrencies begun gaining attention in social networks and mainstream newspapers. Figure 5 clearly shows that since 2017 prestigious sources such as Dow Jones Newswires, MarketWatch, The Wall Street Journal, and Barron’s have been publishing articles within the subject ‘Cryptocurrency Markets’ (Factiva, , 2021). News made cryptocurrencies popular, encouraging high-yield seeking investors to gather information about this new type of financial asset, generating this “dialog” between online searches and cryptocurrency market profitability and risk metrics.

| Direction | TE | ETE | Std.Err. | p-value |

|---|---|---|---|---|

| GTC →Return | 0.0098 | 0.0058 | 0.0015 | 0.0025 |

| Return →GTC | 0.0121 | 0.0079 | 0.0013 | 0.0000 |

| GTC →Volatility | 0.0083 | 0.0051 | 0.0015 | 0.0100 |

| Volatility →GTC | 0.0155 | 0.0111 | 0.0014 | 0.0000 |

5 Conclusion

We confirm that the cryprocurrency market is rather detached from the general macroeconomic environment as proxied by the Google Trends Uncertainty data Castelnuovo and Tran, (2017). Instead, the proposed Google Trends Cryptocurrency index conveys important information flows to (and receives feedback from) the cryptocurrency market.

Information transfer between Google Trends and daily returns is found to be bidirectional and to last for up to six days. As for Bitcoin volatility news are more rapidly absorbed, as the significance of information flows vanishes after three days. Another worth noting result is that information flows from Bitcoin volatility to Google Trends data are larger than vice versa.

When analyzing data in temporal sub-samples, we detect that information flows are not significant at the start of our sample (January 2015-July 2016), but become so after 2016. This could be explained by the greater attention and consolidation of the cryptocurrency market as an alternative investment vehicle.

Our results are robust to different composition of the Google Trends Cryptocurrency (GTC) index, to different lag lengths, and sub-periods.

Recent moves by investment banks into cryptocurrencies (e.g., Morgan Stanley, Goldman Sachs) and the approval of Bitcoin ETFs in Canada show institutional interest in the market is gaining momentum. More recently, the Settlements, (2021) started a consultative process to gather opinions on the possibility of commercial banks holding Bitcoin and other digital assets. Although our research does not detect any relationship between Bitcoin and the general macroeconomy, the institutionalization of cryptocurrencies could make their way into the traditional financial ecosystem. Overall, our research has important implications for fund management and policy making, as it provides important information for portfolio design and rebalancing.

References

- Aslanidis et al., (2019) Aslanidis, N., Bariviera, A. F., and Martinez-Ibañez, O. (2019). An analysis of cryptocurrencies conditional cross correlations. Finance Research Letters, 31:130–137.

- Aslanidis et al., (2021) Aslanidis, N., Bariviera, A. F., and Perez-Laborda, A. (2021). Are cryptocurrencies becoming more interconnected? Economics Letters, 199:109725.

- Aysan et al., (2019) Aysan, A. F., Demir, E., Gozgor, G., and Lau, C. K. M. (2019). Effects of the geopolitical risks on Bitcoin returns and volatility. Research in International Business and Finance, 47(September 2018):511–518.

- Bariviera and Merediz-Solà, (2021) Bariviera, A. F. and Merediz-Solà, I. (2021). Where do we stand in cryptocurrencies economic research? a survey based on hybrid analysis. Journal of Economic Surveys, 35(2):377–407.

- Castelnuovo and Tran, (2017) Castelnuovo, E. and Tran, T. D. (2017). Google it up! a google trends-based uncertainty index for the united states and australia. Economics Letters, 161:149–153.

- Corbet et al., (2019) Corbet, S., Lucey, B., Urquhart, A., and Yarovaya, L. (2019). Cryptocurrencies as a financial asset: A systematic analysis. International Review of Financial Analysis, 62(June 2018):182–199.

- Corbet et al., (2018) Corbet, S., Meegan, A., Larkin, C., Lucey, B., and Yarovaya, L. (2018). Exploring the dynamic relationships between cryptocurrencies and other financial assets. Economics Letters, 165:28 – 34.

- Demir et al., (2018) Demir, E., Gozgor, G., Lau, C. K. M., and Vigne, S. A. (2018). Does economic policy uncertainty predict the Bitcoin returns? An empirical investigation. Finance Research Letters, 26:145–149.

- Dimpfl and Peter, (2013) Dimpfl, T. and Peter, F. J. (2013). Using transfer entropy to measure information flows between financial markets. Studies in Nonlinear Dynamics and Econometrics, 17(1):85–102.

- Dimpfl and Peter, (2018) Dimpfl, T. and Peter, F. J. (2018). Analyzing volatility transmission using group transfer entropy. Energy Economics, 75(C):368–376.

- Factiva, (2021) Factiva (2021). Dow jones factiva database. https://professional.dowjones.com/factiva/. Accessed: 2021-05-20.

- Fang et al., (2020) Fang, T., Su, Z., and Yin, L. (2020). Economic fundamentals or investor perceptions? The role of uncertainty in predicting long-term cryptocurrency volatility. International Review of Financial Analysis, 71(39):101566.

- Fernández-Villaverde et al., (2020) Fernández-Villaverde, J., Sanches, D., Schilling, L., and Uhlig, H. (2020). Central bank digital currency: Central banking for all? Review of Economic Dynamics.

- Garman and Klass, (1980) Garman, M. B. and Klass, M. J. (1980). On the estimation of security price volatilities from historical data. The Journal of Business, 53(1):67–78.

- Global Legal Research Center, (2018) Global Legal Research Center (2018). Regulation of Cryptocurrency Around the World. The Law Library of Congress, 5080(June).

- Johnson, (2021) Johnson, J. (2021). Online search usage - statistics & facts. https://www.statista.com/topics/1710/search-engine-usage/. Accessed: 2021-05-20.

- Lucey et al., (2021) Lucey, B. M., Vigne, S. A., Yarovaya, L., and Wang, Y. (2021). The cryptocurrency uncertainty index. Finance Research Letters, (March):102147.

- Marschinski and Kantz, (2002) Marschinski, R. and Kantz, H. (2002). Analysing the information flow between financial time series. The European Physical Journal B - Condensed Matter and Complex Systems, 30(2):275–281.

- Martin, (2021) Martin, K. (2021). Cryptocurrency holders take on central banks at their peril. https://www.ft.com/content/2b94acc4-cfbb-466c-bf8a-09a5106c750b. Accessed: 2020-05-30.

- Merediz-Solà and Bariviera, (2019) Merediz-Solà, I. and Bariviera, A. F. (2019). A bibliometric analysis of bitcoin scientific production. Research in International Business and Finance, 50:294–305.

- Parkinson, (1980) Parkinson, M. (1980). The Extreme Value Method for Estimating the Variance of the Rate of Return. The Journal of Business, 53(1):61–65.

- Settlements, (2021) Settlements, B. f. I. (2021). Prudential treatment of cryptoasset exposures.

- Shen et al., (2019) Shen, D., Urquhart, A., and Wang, P. (2019). Does twitter predict Bitcoin? Economics Letters, 174:118–122.

- Urquhart, (2018) Urquhart, A. (2018). What causes the attention of Bitcoin? Economics Letters, 166:40–44.

- Walther et al., (2019) Walther, T., Klein, T., and Bouri, E. (2019). Exogenous drivers of Bitcoin and Cryptocurrency volatility – A mixed data sampling approach to forecasting. Journal of International Financial Markets, Institutions and Money, 63:101133.

Appendix A Sets of words to construct the Google Trends Cryptocurrency Attention (GTC) Index

| Full set | AES256 | crypto crash | miner | Mount Gox |

|---|---|---|---|---|

| altcoin | cryptocurrency | minted | Mt Gox | |

| anonymity | cryptography | public key | Mt. Gox | |

| Bitcoin | digital assets | ripple | private key | |

| block producer | distributed ledger | satoshi | Proof of Authority | |

| blockchain | ethereum | soft fork | Proof of Burn | |

| BTC | hard fork | stablecoin | Proof of Stake | |

| coin | hash | tether | Proof of Work | |

| consensus | hashing | token | ||

| crypto | ICO | virtual currency | tether | |

| Subset 1 | anonymity | crypto | miner | token |

| Bitcoin | cryptocurrency | minted | private key | |

| blockchain | ICO | public key | Proof of Work | |

| BTC | cryptography | ripple | ||

| coin | ethereum | satoshi | ||

| consensus | hash | stablecoin | ||

| Subset 2 | Bitcoin | crypto | ethereum | tether |

| blockchain | cryptocurrency | ripple | ||

| BTC | cryptography | satoshi | ||

| Subset 3 | Bitcoin | BTC | cryptocurrency | |

| blockchain | crypto |