- CI

- confidence interval

- OLS

- ordinary least squares

- CLT

- central limit theorem

- IV

- instrumental variables

- ATE

- average treatment effect

- RCT

- randomized control trial

- VAM

- value-added model

- LAN

- locally asymptotically normal

- DiD

- difference-in-differences

- OVB

- omitted variables bias

- FWL

- Frisch-Waugh-Lovell

- TWFE

- two-way fixed effects

- EW

- easiest-to-estimate weighting

- CW

- easiest-to-estimate common weighting

Contamination Bias in Linear Regressions††thanks: Contact: paul.goldsmith-pinkham@yale.edu, peter_hull@brown.edu, and mkolesar@princeton.edu. We thank Alberto Abadie, Jason Abaluck, Isaiah Andrews, Josh Angrist, Tim Armstrong, Kirill Borusyak, Kyle Butts, Clément de Chaisemartin, Peng Ding, Len Goff, Jin Hahn, Xavier D’Haultfœuille, Simon Lee, Bernard Salanié, Pedro Sant’Anna, Tymon Słoczyński, Isaac Sorkin, Jonathan Roth, Jacob Wallace, Stefan Wager, and numerous seminar participants for helpful comments. Hull acknowledges support from National Science Foundation Grant SES-2049250. Kolesár acknowledges support by the Sloan Research Fellowship and by the National Science Foundation Grant SES-22049356. Mauricio Cáceres Bravo, Jerray Chang, William Cox, and Dwaipayan Saha provided expert research assistance. An earlier draft of this paper circulated under the title “On Estimating Multiple Treatment Effects with Regression”.

0.2cm0.2cm

We study regressions with multiple treatments and a set of controls that is flexible enough to purge omitted variable bias. We show that these regressions generally fail to estimate convex averages of heterogeneous treatment effects—instead, estimates of each treatment’s effect are contaminated by non-convex averages of the effects of other treatments. We discuss three estimation approaches that avoid such contamination bias, including the targeting of easiest-to-estimate weighted average effects. A re-analysis of nine empirical applications finds economically and statistically meaningful contamination bias in observational studies; contamination bias in experimental studies is more limited due to idiosyncratic effect heterogeneity.

1 Introduction

Consider a linear regression of an outcome on a vector of treatments and a vector of flexible controls . The treatments are assumed to be as good as randomly assigned conditional on the controls. For example, may indicate the assignment of individuals to different interventions in a stratified randomized control trial (RCT), with the randomization protocol varying across some experimental strata indicators in . Or, in an education value-added model (VAM), might indicate the matching of students to different teachers or schools with including measures of student demographics and lagged achievement which yield a credible selection-on-observables assumption. The regression might also be the first stage of an instrumental variables (IV) regression leveraging the assignment of multiple decision-makers (e.g. bail judges) indicated in , which is as-good-as-random conditional on some controls . These sorts of regressions are widely used across many fields in economics.111Prominent RCTs where randomization probabilities vary across strata include Project STAR [141] and the RAND Health Insurance Experiment [146]. Prominent VAM examples include studies of teachers [134, 110], schools [93, 88, 150], and healthcare institutions [87, 124]. Prominent “judge IV” examples include [140, 145, 117].

This paper shows that such multiple-treatment regressions generally fail to estimate convex weighted averages of heterogeneous causal effects, and discusses solutions to this problem. The problem may be surprising given an influential result in [89], showing that regressions on a single binary treatment and flexible controls estimate a convex average of treatment effects whenever is conditionally as good as randomly assigned. We show that this result does not generalize to multiple treatments: regression estimates of each treatment’s effect are generally contaminated by a non-convex average of the effects of other treatments. Thus, the regression coefficient for a given treatment arm incorporates the effects of all arms.

We first derive a general characterization of such contamination bias in multiple-treatment regressions.222Our use of the term “contamination” follows [160], and differs from its use in some analyses of clinical trials [[, e.g.]]keoghbrown07 to describe settings where members of one treatment group receive the treatment of another group—what economists typically call “non-compliance”. Our “bias” terminology refers to an implication of our result: if a given treatment has constant effects, but the other treatment effects are heterogeneous, the regression estimand is inconsistent for the given treatment effect. We show the core problem by focusing on the special case of a set of mutually exclusive treatment indicators, though our characterization applies even when the treatments are not restricted to be binary or mutually exclusive. To separate the problem from the typical challenge of omitted variables bias (OVB), we assume a best-case scenario where the covariate parametrization is flexible enough to include the treatment propensity scores (e.g., with a linear covariate adjustment, we assume that the propensity scores are linear in the covariates). This condition holds trivially if the only covariates are strata indicators. Under these conditions, we show that the regression coefficient on each treatment identifies a convex weighted average of its causal effects plus a contamination bias term given by a linear combination of the causal effects of other treatments, with weights that sum to zero. Thus, each treatment effect estimate will generally incorporate the effects of other treatments, unless the effects are uncorrelated with the contamination weights. Since these weights sum to zero some are necessarily negative—further complicating the interpretation of the coefficients.

Contamination bias arises because regression adjustment for the confounders in is generally insufficient for making the other treatments ignorable when estimating a given treatment’s effect, even when this adjustment is flexible enough to avoid OVB. To see this intuition clearly, suppose the only controls are strata indicators. OVB is avoided when the treatments are as good as randomly assigned within strata. But because the treatments enter the regression linearly, the [89] result implies that the causal interpretation of a given treatment’s coefficient is only guaranteed when its assignment depends linearly on both the strata indicators and the other treatment indicators. With mutually exclusive treatments, this condition fails because the dependence is inherently nonlinear—the probability of assignment to a given treatment is zero if an individual is assigned to one of the other treatments, regardless of their stratum, but strata indicators affect the treatment probability otherwise. Such dependence generates contamination bias.333This issue is distinct from the [122, 121] critique of using regression to analyze randomized trials, which concerns estimation, not identification.

Contamination bias also arises under an alternative “model-based” identifying assumption that—rather than making assumptions on the treatment’s “design” (i.e. propensity scores)—posits that the covariate specification spans the conditional mean of the potential outcome under no treatment, . In a linear model with unit and time fixed effects, this reduces to the parallel trends restriction often used in difference-in-differences (DiD) and event study regressions. It is common for to include multiple indicators in such settings—for example, the leads and lags relative to a treatment adoption date used to support the parallel trends assumption or estimate treatment effect dynamics.444Alternatively may indicate multiple contemporaneous treatments, as in certain “mover” regressions. We show that replacing the restriction on propensity scores in our characterization with an assumption on generates an additional issue: the own-treatment weights are negative whenever the implicit propensity score model used by the regression to partial out the covariates and the other treatments fits probabilities greater than one. This result shows that the negative weighting and contamination bias issues documented previously in the context of two-way fixed effects regressions [[, e.g.,]]goodman2021difference, sun2021estimating, de2020aer, de2020two, callaway2021difference, borusyak2021revisiting,wooldridge2021mundlak,hull2018movers are more general—and conceptually distinct—problems.555Our analysis also relates to issues with interpreting multiple-treatment IV estimates [96, 138, 139, 129, 142, 99]. Negative weighting arises because regressions leveraging model-based restrictions on may fit treatment probabilities exceeding one. Contamination bias arises because additive covariate adjustments don’t account for the non-linear dependence of a given treatment on the other treatments and covariates. This generates a different form of propensity score misspecification: a non-zero fitted probability of a given treatment, even when one of the other treatments is known to be non-zero.666While our results are framed in the context of a causal model, we show how analogous results apply to descriptive regressions which seek to estimate averages of conditional group contrasts without assuming a causal framework—as in studies of outcome disparities across multiple racial or ethnic groups, studies of regional variation in healthcare utilization or outcomes, or studies of industry wage gaps.

We then discuss three solutions to the contamination bias problem, and their trade-offs. These solutions apply when the propensity scores are non-degenerate, such as in an RCT or other “design-based” regression specification.777Solving the contamination bias problem under model-based identification approaches requires either targeting subpopulations of the treated or applying substantive restrictions on the conditional means of potential outcomes under treatment. We do not explore this case as it has already been studied extensively in the DiD context [[, e.g.]]de2020two, sun2021estimating, callaway2021difference,borusyak2021revisiting,wooldridge2021mundlak. First, a conceptually principled solution is to adapt approaches to estimating the average treatment effect (ATE) of a conditionally ignorable binary treatment to the multiple treatment case [[, e.g.]]cattaneo10, chernozhukov2018double,ChNeSi21, GrPi22. For example, one could run a regression that includes interactions between the treatments and demeaned controls, or combine such regression with inverse propensity score weighting for doubly-robust estimation. Such ATE estimators work well under strong overlap of the covariate distribution for units in each treatment arm. But they may be imprecise under limited overlap or be outright infeasible with overlap failures—common scenarios in observational studies [113].

This practical consideration motivates an alternative approach: estimating a weighted average of treatment effects, as regression does in the binary treatment case, while avoiding the contamination bias of multiple-treatment regressions. We derive the weights that are easiest to estimate, in the sense of minimizing a semiparametric efficiency bound under homoskedasticity. These easiest-to-estimate weights are always convex. They also coincide with the implicit linear regression weights when the treatment is binary (i.e. the [89] case), formalizing a virtue of regression adjustment. In the multiple treatment case, the easiest-to-estimate weighting can be implemented by a simple second solution: a linear regression which restricts estimation to the individuals who are either in the control group or the treatment group of interest. While trivial to implement, effects estimated using these one-treatment-at-a-time regressions are not directly comparable, since the weighting is treatment-specific. The third solution we discuss is to impose common weights across treatments in our optimization; we show how these weights can be implemented using a weighted regression approach. We give guidance for how researchers can gauge the extent of contamination bias in practice and implement these solutions in a new R and Stata package, multe.888The packages are avaiable at CRAN and https://github.com/gphk-metrics/stata-multe, respectively.

We study the empirical relevance of contamination bias in nine applications: six RCTs with stratified randomization and three observational studies of racial disparities. We find economically and statistically meaningful contamination bias in several of these applications. Notably, the largest contamination bias is found in the observational studies while the smallest is bias is found in the experimental studies. In a detailed analysis of one of the experiments (the Project STAR trial) we show that the lack of contamination bias reflects limited correlation between treatment effects and contamination weights and small variation in the contamination weights, rather than limited effect heterogeneity. This analysis highlights the importance of conducting contamination bias diagnostics, particularly in observational studies where propensity score variation may cause large variability in the contamination weights.

We structure the rest of the paper as follows. Section 2 illustrates contamination bias in a simple stylized setting. Section 3 characterizes the general problem, and discusses connections to previous analyses. Section 4 three solutions, and gives guidance for measuring and avoiding contamination bias in practice. Section 5 illustrates these tools using nine applications. Section 6 concludes. Appendix A collects all proofs and extensions. Appendix B discusses the connection between our contamination bias characterization and that in the DiD literature. Details on the applications and additional exhibits are given in Appendices C and D.

2 Motivating Example

We build intuition for the contamination bias problem in two simple examples. We first review how regressions on a single randomized binary treatment and binary controls identify a convex average of heterogeneous treatment effects. We then show how this result fails to generalize when we introduce an additional treatment arm. We base these examples on a stylized version of the Project STAR experiment, which we return to as an application in Section 5.1. The simple structure of these examples helps isolate the core mechanisms of contamination bias. Later sections consider non-experimental settings with richer control specifications, both theoretically and empirically.

2.1 Convex Weights with One Randomized Treatment

Consider the regression of an outcome on a single treatment indicator , a single binary control , and an intercept:

| (1) |

By definition, is a mean-zero regression residual that is uncorrelated with and . For example, analysing the Project STAR trial, [141] primarily studied the effect of small class size on the test scores of kindergartners indexed by . Project STAR randomized students to classes within schools, with the fraction of students assigned to small classes varying by school due to the varying number of total students in each school. To account for this, [141] included school fixed effects as controls. Such specifications are often found in stratified RCTs with varying treatment assignment rates across a set of pre-treatment strata. If we imagine two such strata, demarcated by a binary indicator , then eq. 1 corresponds to a stylized two-school version of a Project STAR regression.

We wish to interpret the coefficient in terms of the causal effects of on . For this we use potential outcome notation, letting denote the test score of student when . Individual ’s treatment effect is then given by , and we can write realized achievement as . Since treatment assignment is random within schools, is conditionally independent of potential outcomes given : .

[89] showed that regression coefficients like identify a convexly-weighted average of within-strata ATEs. In our Project STAR example, this result shows that:

| (2) |

gives a convex weighting scheme, and is the ATE in school . Thus, in our example the coefficient identifies a weighted average of school-specific small classroom effects across the two schools.

Equation 2 can be derived by applying the Frisch-Waugh-Lovell (FWL) Theorem. The multivariate regression coefficient can be written as a univariate regression coefficient from regressing onto the population residual from regressing onto and a constant:

| (3) |

where we substitute the potential outcome model for in the second equality. Since is binary, the propensity score is linear and the residual is mean independent of (not just uncorrelated with it): . Therefore,

| (4) |

The first equality in eq. 4 follows from the law of iterated expectations, the second equality follows by the conditional random assignment of and the third equality uses . Hence, the first summand in eq. 3 is zero. Analogous arguments show that

where gives the conditional variance of the small-class treatment within schools. Since , it follows that we can write the second summand in eq. 3 as

proving the representation of in eq. 2.

The key fact underlying this derivation is that the residual from the auxiliary regression of the treatment on the other regressors is mean-independent of . By the FWL theorem, treatment coefficients like can always be represented as in eq. 3 even without this property. We next show, however, that the remaining steps in the derivation of eq. 2 fail when an additional treatment arm is included. This failure can be attributed to the fact that the auxiliary FWL regression delivers a treatment residual that is uncorrelated with—but not mean-independent of—the other regressors. The lack of mean independence leads to an additional term in the expression for the regression coefficient.

2.2 Contamination Bias with Two Randomized Treatments

In reality, Project STAR randomized students to three mutually exclusive conditions within schools: a control group with a regular class (), a treatment that reduced class size (), and a treatment that introduced full-time teaching aides (). We incorporate this extension of our stylized example by considering a regression of student achievement on a vector of two treatment indicators, , where indicates assignment to treatment . We continue to include a constant and the school indicator as controls, yielding the regression

| (5) |

The observed outcome is now given by , with and denoting the potentially heterogeneous effects of a class size reduction and introduction of a teaching aide, respectively. As before, we analyze this regression by assuming is conditionally independent of the potential achievement outcomes given the school indicator : .

To analyze the coefficient on , we again use the FWL theorem to write

| (6) |

where again denotes a population residual, but now from regressing on , a constant, and . Unlike before, this residual is uncorrelated with but not mean-independent of the remaining regressors because the dependence between and is non-linear. When , must be zero regardless of the value of (because they are mutually exclusive) while if the mean of does depend on unless the treatment assignment is completely random. Thus, in general, .

Because does not coincide with a conditionally de-meaned , we can not generally reduce eq. 6 to an expression involving only the effects of the first treatment arm, . It turns out that we nevertheless still have , as in eq. 4, since the auxilliary regression residuals are still uncorrelated with any individual characteristic like .999To see this, note that in the auxiliary regression we can partial out and the constant from both sides to write . Thus, is a linear combination of residuals which, per eq. 4, are both uncorrelated with . It follows that . The regression thus does not suffer from OVB. However, we do not generally have . Instead, simplifying eq. 6 by the same steps as before leads to the expression

| (7) |

as a generalization of eq. 2. Here can be shown to be non-negative and to average to one, similar to the weight in eq. 2. Thus, if not for the second term in eq. 7, would similarly identify a convex average of the conditional ATEs . But precisely because , this second term is generally present: is generally non-zero, complicating the interpretation of by including the conditional effects of the other treatment .

The second contamination bias term in eq. 7 arises because the residualized small class treatment is not conditionally independent of the second full-time aide treatment within schools, despite being uncorrelated with by construction. This can be seen by viewing as the result of an equivalent two-step residualization. First, both and are de-meaned within schools: and where gives the propensity score for treatment . Second, a bivariate regression of on is used to generate the residuals . When the propensity scores vary across the schools (i.e. ), the relationship between these residuals varies by school, and the line of best fit between and averages across this relationship. As a result, the line of best fit does not isolate the conditional (i.e. within-school) variation in : the remaining variation in will tend to predict within schools, making the contamination weight non-zero.

2.3 Illustration and Intuition

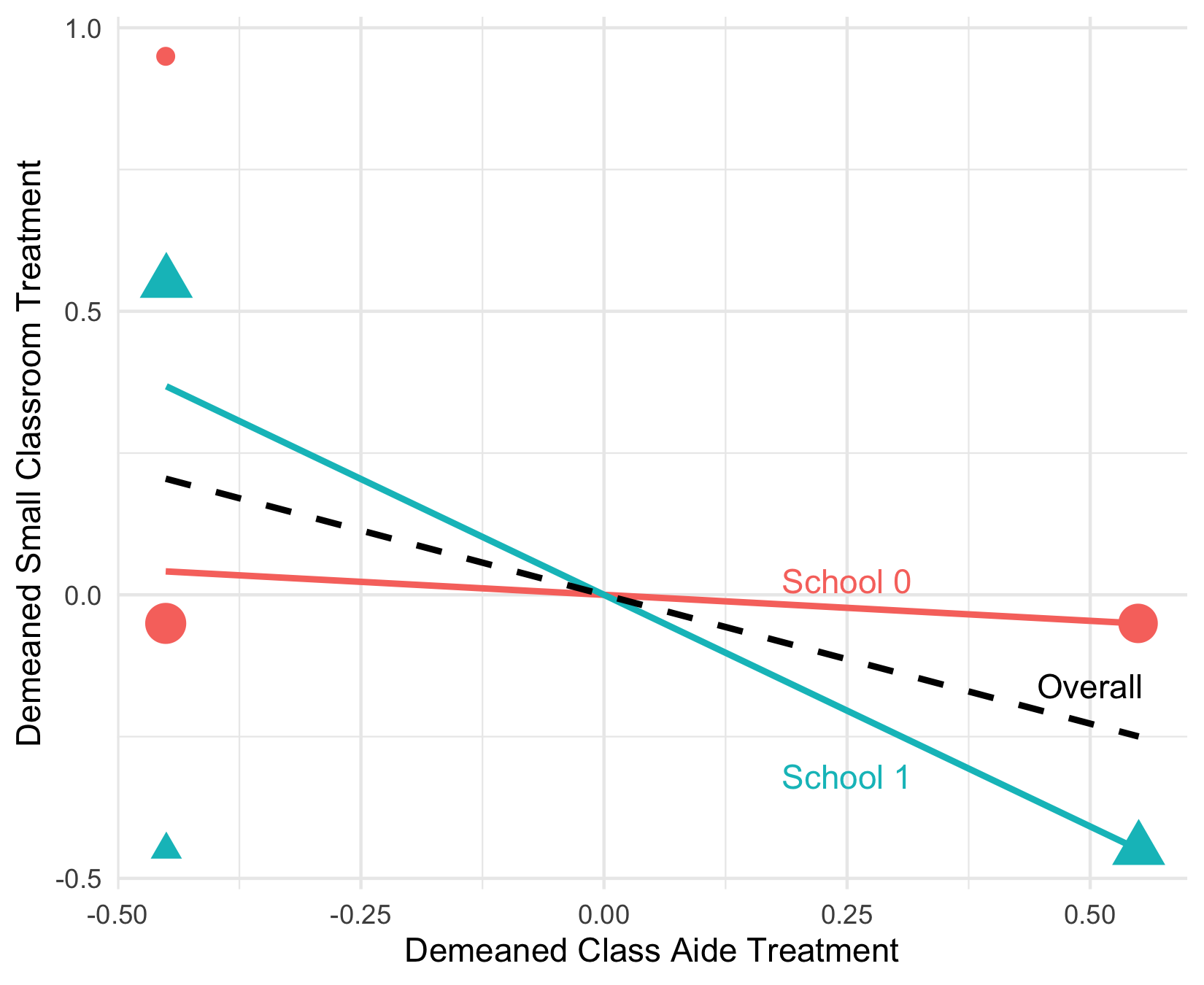

A simple numerical example helps make the contamination bias problem concrete. Suppose in the previous setting that school (indicated by ) assigned only 5 percent of the students to the small classroom treatment, with 45 percent of the students assigned to the full-time aide treatment and the rest assigned to the control group. In school (indicated by ), there was a substantially larger push for students to be placed into treatment groups with 45 percent of students assigned to a small classroom, 45 percent assigned to a classroom with a full-time aide, and only 10 percent assigned to the control group. Therefore, and while . Suppose that the schools have the same number of students, so that . It then follows from the above formulas that and .

As reasoned above, the contamination weights are non-zero here because the within-school correlation between the residualized treatments, and , is heterogeneous: in school it is about , so that the value of the demeaned class aide treatment is only weakly predictive of the small classroom treatment, while in school it is highly predictive with correlation . Figure D.1 in Appendix D illustrates this graphically, showing that because the overall regression of on averages over these two correlations, the regression residuals are predictive of the value of the class aide treatment.

To illustrate the potential magnitude of bias in this example, suppose that classroom reductions have no effect on student achievement (so ), but that the effect of a teaching aide varies across schools. In school the aide is highly effective, , (which may be the reason for the higher push in this school to place students into treatment groups) but in school , the aide has no effect, . By eq. 7, the regression coefficient on the first treatment identifies

Thus, in this example, a researcher would conclude that small classrooms have a sizable negative effect on student achievement—equal in magnitude to around half of the true teaching aide effect in school —despite the true small-classroom effect being zero for all students. This treatment effect coefficient can be engineered to match an arbitrary magnitude and sign by varying the heterogeneity of the teaching aide effects across schools.

To build further intuition for eq. 7, it is useful to consider two cases where the contamination bias term is zero. First, note that since regression residuals are by construction uncorrelated with the included regressors, . Therefore, . If the average effects of the teaching aide treatment are constant across the two schools, , then is constant, and this covariance is zero such that contamination bias disappears. More generally, when the average teaching aide treatment effects across schools exhibit idiosyncratic variation, in the sense that they have a weak covariance with the contamination weights across schools, the contamination bias term will be small.

Second, consider the case where and are independent conditional on —such as when the small classroom and teacher aid interventions are independently assigned within schools, in contrast to the previously assumed mutual exclusivity of these treatments. In this case the conditional expectation will be linear, since and are unrelated given , and will thus be identified by the auxiliary regression of on , , and a constant. Consequently, the residuals will coincide with . The coefficient on in eq. 5 can therefore be shown to be equivalent to the previous eq. 2, identifying the same convex average of . This case highlights that dependence across treatments is necessary for the contamination bias to arise.

3 General Problem

We now derive a general characterization of the contamination bias problem, in regressions of an outcome on a -dimensional treatment vector and flexible transformations of a control vector . We focus on the case of mutually exclusive indicators for values of an underlying treatment (with the indicator omitted). We extend the characterization to a general (i.e. potentially non-binary) in Section A.1.

We suppose the effects of on are estimated by a partially linear model:

| (8) |

where and are defined as the minimizers of expected squared residuals :

| (9) |

for some linear space of functions . This setup nests linear covariate adjustment by setting , in which case eq. 8 gives a linear regression of on , , and a constant. The setup also allows for more flexible covariate adjustments—such as by specifying to be a large class of “nonparametric” functions [[, e.g.]]robinson88.

Two examples highlight the generality of this setup:

Example 1 (Multi-Armed RCT).

is a vector of mutually-exclusive indicators for experimental strata, within which is randomly assigned to individuals . is linear.

Example 2 (Two-Way Fixed Effects).

indexes panel data, with a fixed set of units observed over periods . where and denote the underlying unit and period, and includes unit and period indicators. contains indicators for leads and lags relative to a deterministic treatment adoption date, (with at least one lead excluded to prevent collinearity).

Example 1 nests the motivating RCT example in Section 2, allowing for an arbitrary number of experimental strata in and multiple treatment arms in . Example 2 shows that our setup can also nest the kind of regressions considered in a recent literature on DiD and related regression specifications [[, e.g.]]goodman2021difference,hull2018movers, sun2021estimating, de2020aer,de2020two,callaway2021difference, borusyak2021revisiting,wooldridge2021mundlak. We elaborate on the connections to this literature in Appendix B by considering general two-way fixed effects (TWFE) specifications with non-random treatments. These include specifications with multiple static treatment indicators, as in “mover regressions” that leverage over-time transitions, as well as dynamic event study specifications.101010Some papers in this DiD literature study issues we do not consider, such as when researchers fail to include indicators for all relevant treatment states. This specification of will generally add bias terms to our decomposition of , below. Similarly, we do not consider multicollinearity issues like in [101] by implicitly assuming a unique solution to eq. 9. For event studies this means we assume some units are never treated, with .

As a first step towards characterizing the treatment coefficient vector, we solve the minimization problem in eq. 9. Let denote the residuals from projecting onto the control specification, with elements . It follows from the projection theorem [[, e.g.]Theorem 11.1]vdv98 that

| (10) |

Applying the FWL theorem, each treatment coefficient can be written where is the residual from regressing on . Letting denote the projection of onto the space , we may write these residuals as .

3.1 Causal Interpretation

We now consider the interpretation of each treatment coefficient in terms of causal effects. Let denote the potential outcome of unit when . Observed outcomes are given by where is a vector of treatment effects with elements . We denote the conditional expectation of the vector of treatment effects given the controls by , so that is the conditional ATE for the th treatment. We let denote the vector of propensity scores, so that . Our characterization of contamination bias doesn’t require the propensity scores to be bounded away from and and in fact allows them to be degenerate, i.e. for all . This is the case in Example 2, since is a non-random function of . We return to practical questions of propensity score support in Section 4.

We make two assumptions to interpret in terms of the effects . First, we assume mean-independence of the potential outcomes and treatment, conditional on the controls:

Assumption 1.

for all .

A sufficient condition for this assumption is that the treatment is randomly assigned conditional on the controls, making it conditionally independent of the potential outcomes:

| (11) |

Such conditional random assignment appears in Example 1. In Example 2, where treatment is a non-random function of the unit and time indices in , Assumption 1 holds trivially.

Second, we assume is specified such that that one of two conditions holds:

Assumption 2.

Let and recall . Either

| (12) |

for all , or

| (13) |

The first condition requires the covariate adjustment to be flexible enough to capture each treatment’s propensity score. For example, with a linear specification for , eq. 12 requires the propensity scores to be linear in [[, cf. eq. (30) in]]AnKr99handbook. This condition holds trivially in Example 1, since is a vector of indicators for groups within which is randomly assigned. When this condition holds, the projection of the treatment onto the covariates coincides with the vector of propensity scores, and the projection residuals coincide with the conditionally demeaned treatment vector .

In Example 2, with being a deterministic function of unit and time indices and including unit and time fixed effects, eq. 12 fails because the propensity scores are binary—they cannot be captured by a linear combination of the TWFEs. However, eq. 13 is satisfied by a parallel trends assumption: that the average untreated potential outcomes are linear in the unit and time effects. We elaborate on this setup in Appendix B.111111Identification based on eq. 12 can be seen as “design-based” in that it only restricts the treatment assignment process. Identification based on eq. 13 can be seen as “model-based” in that it makes no assumptions on the treatment assignment process but specifies a model for the unobserved untreated potential outcomes.

Under either condition in Assumption 2, the specification of controls is flexible enough to avoid OVB. To see this formally, suppose all treatment effects are constant: for all . This restriction lets us write , where is a vector collecting the constant effects. The only source of bias when regressing on and controls is then the unobserved variation in the untreated potential outcomes . But it follows from the definition of in eq. 10 that there is no such OVB when Assumption 2 holds; the coefficient vector identifies the constant effects:

Here the first line uses the fact that because is a vector of projection residuals, and the second line uses the law of iterated expectations and Assumption 1. Under eq. 12, , so that the term in braces is zero by another application of the law of iterated expectations: . It is likewise zero under eq. 13 since is by definition of projection orthogonal to any function in such that . Hence, OVB is avoided in the constant-effects case so long as either the propensity scores or the untreated potential outcomes are spanned by the control specification. Versions of this robustness property have been previously observed in, for instance, [155].

When treatment effects are heterogeneous but contains a single treatment indicator, identifies a weighted average of the conditional effects . Specifically, since by the previous argument we still have , it follows from eq. 10 that

| (14) |

where the second equality uses iterated expectations and the identity . Under eq. 12, , so the weights further simplify to . This extends the [89] result to a general control specification; versions of this extension appear in, for instance, [91], [92, Chapter 3.3], and [94].

This result provides a robustness rationale for estimating the effect of a single as-good-as-randomly assigned treatment with a partially linear model (8): so long as the specification of is rich enough to make eq. 12 hold, will identify a convex average of heterogeneous treatment effects. In Section 4 we will derive another rationale for targeting in this model, showing that the weights minimize the semiparametric efficiency bound (conditional on the controls) for estimating some weighted-average treatment effect.

Our first proposition shows that with multiple treatments, the interpretation of becomes more complicated because of contamination bias:

Proposition 1.

Under Assumptions 1 and 2, the treatment coefficients in (8) identify

| (15) |

where, recalling that gives the projection of onto the space ,

with and . Furthermore, if eq. 12 holds, .

Proposition 1 shows that the coefficient on in eq. 8 is a sum of two terms. The first term is a weighted average of conditional ATEs , with own treatment weights that average to one—generalizing the characterization of the single-treatment case, eq. 14. The expression for implies that these weights are convex if the implicit linear probability model used to compute fits probabilities that lie below one, . The second term is a weighted average of treatment effects for other treatments , with contamination weights that average to zero. Because the contamination weights are zero on average, they must be negative for some values of the controls unless they are all identically zero.121212Proposition 1 complements an algebraic result in [[], Section 7.1]chatto_zubiz_2021, which shows that the regression estimator of can be written in terms of weighted sample averages of outcomes among units in different treatment arms (regardless of whether Assumptions 1 and 2 hold). In contrast, our analysis interprets regression estimands in terms of weighted averages of conditional ATEs under a broad class of identifying assumptions. In a finite-population setting, [86] show that identifies matrix-weighted averages of individual treatment effect vectors ; however, they do not discuss the interpretation of the estimand. This is the case when the implicit linear probability model correctly predicts that if .

Hence, if the linear probability model is correctly specified, i.e. for some vector and , the contamination weights are zero and the own treatment weights are positive. This is the analog of condition (12) if we interpret as a binary treatment of interest and as a specification for the controls. In other words, the assignment of treatment must be additively separable between and . However, with mutually exclusive treatments, this won’t be the case unless treatment assignment is unconditionally random. In particular, since must equal zero if the unit is assigned to one of the other treatments regardless of the value of , under correct specification it must be the case that for all elements of . This in turn implies that the assignment of treatment doesn’t depend on , which is impossible unless the propensity score is constant.

Thus, misspecification in the linear probability model will generally yield nonsensical fitted probabilities that generate non-zero contamination weights . Furthermore, if the misspecification also yields fitted probabilities , we will have negative own treatment weights. The last part of Proposition 1 shows that such nonsensible predictions are ruled out if eq. 12 holds.

We make four further remarks on our general characterization of contamination bias:

Remark 1.

Since the contamination weights are mean zero, we may write the contamination bias term as . Thus, the treatment coefficient does not suffer from contamination bias if the contamination weights are uncorrelated with the conditional ATEs . This is trivially true if the other treatments are homogeneous, i.e. when . More generally, contamination bias will be small if the contamination weight exhibits weak covariance with the conditional ATEs. Since , this is the case when (i) the factors influencing treatment effect heterogeneity are largely unrelated to the factors influencing the treatment assignment process in the sense that is close to zero, (ii) the contamination weights display limited variability, and/or (iii) treatment effect heterogeneity in the other treatments is limited.

Remark 2.

Since the weights in eq. 15 are functions of the variances and covariances and , they are identified and can be used to further characterize each coefficient. For example, the contamination bias term can be bounded by the identified contamination weights and bounds on the heterogeneity in conditional ATEs .

Remark 3.

The results in Proposition 1 are stated for the case when are mutually exclusive treatment indicators. In Section A.1 we relax this assumption to allow for combinations of non-mutually exclusive treatments (either discrete or continuous). In this case, the own-treatment weights may be negative even if eq. 12 holds.

Remark 4.

While we derived Proposition 1 in the context of a causal model, an analogous result follows for descriptive regressions that do not assume potential outcomes or impose Assumption 1. Consider, specifically, the goal of estimating an average of conditional group contrasts with a partially linear model eq. 8 and replace condition (13) with an assumption that . The steps that lead to Proposition 1 then show that such regressions also generally suffer from contamination bias: the coefficient on a given group indicator averages the conditional contrasts across all other groups, with non-convex weights. Furthermore, the weights on own-group conditional contrasts are not necessarily positive. These sorts of conditional contrast comparisons are therefore not generally robust to misspecification of the conditional mean, .

3.2 Implications

Proposition 1 shows that treatment effect heterogeneity can induce two conceptually distinct issues in flexible regression estimates of treatment effects. First, with either single or multiple treatments, there is a negative weighting of a treatment’s own effects when projecting the treatment indicator onto other treatment indicators and covariates yields fitted values exceeding one, i.e. when . This issue is relevant in various DiD regressions and related approaches which rely on a model of untreated potential outcomes that ensures eq. 13 holds (e.g. parallel trends assumptions) but which potentially misspecify the assignment model in eq. 12. Although the recent DiD literature focuses on TWFE regressions, Proposition 1 shows such negative weighing can arise more generally—such as when researchers allow for linear trends, interacted fixed effects, or other extensions of the basic parallel trends model. None of these alternative specifications for are in general flexible enough to capture the degenerate propensity scores and hence ensure that .

Second, in the multiple treatment case, there is a potential for contamination bias from other treatment effects—regardless of which condition in Assumption 2 holds. This form of bias is relevant whenever one uses an additive covariate adjustment, no matter how flexibly the covariates are specified. Versions of this problem have been noted in, for example, the [160] analysis of DiD regressions with treatment leads and lags or the [130] analysis of mover regressions (see Appendix B).131313The negative weights issue raised in [114] (when ), and the related issue that own-treatment weights may be negative in [160] and [115] (when ), arise because the treatment probability is not linear in the unit and time effects. If eq. 12 holds with , Proposition 1 shows estimates a convex combination of treatment effects. This covers the setting considered in Theorem 1(iv) in [95]. In their Comment 2, [95] say that “the sum of the weights [used in Theorem 1(iv)] is one, although some of the weights may be negative”. Proposition 1 shows these weights are, in fact, non-negative. Proposition 1 shows such contamination bias arises much more broadly, however.

The characterization in Proposition 1 also relates to concerns in interpreting multiple-treatment IV estimates with heterogeneous effects [96, 138, 139, 129, 142, 99]. This connection comes from viewing eq. 8 as the second stage of an IV model estimated by a control function approach; in the linear IV case, for example, can be interpreted as giving the residuals from a first-stage regression of on a vector of valid instruments . In the single-treatment case, the resulting coefficient has an interpretation of a weighted average of conditional local average treatment effects under the appropriate first-stage monotonicity condition [131]. But as in Proposition 1 this interpretation fails to generalize when includes multiple mutually-exclusive treatment indicators: each combines the local effects of treatment with a non-convex average of the effects of other treatments.

Finally, Proposition 1 has implications for single-treatment IV estimation with multiple instruments and flexible controls if the first stage has the form of eq. 8, where now is interpreted as the treatment and gives the vector of instruments. Proposition 1 shows that the first-stage coefficients on the instruments will not generally be convex weighted average of the true first-stage effects . Because of this non-convexity, the regression specification may fail to satisfy the effective monotonicity condition even when is always positive: the cross-instrument contamination of causal effects may cause monotonicity violations, even when specifications with individual instruments do not. This issue is distinct from previous concerns over monotonicity failures in multiple-instrument designs [151, 120, 153, 149], which are generally also present in such just-identified specifications. It is also distinct from concerns about insufficient flexibility in the control specification when monotonicity holds unconditionally [100].

This new monotonicity concern may be especially important in “examiner” IV designs, which exploit the conditional random assignment to multiple decision-makers. Many studies leverage such variation by computing average examiner decision rates, often with a leave-one-out correction, and use this “leniency” measure as a single instrument with linear controls. These IV estimators can be thought of as implementing versions of a jackknife IV estimator [90], based on a first stage that uses examiner indicators as instruments, similar to eq. 8. Proposition 1 thus raises a new concern with these IV analyses when controls (such as time fixed effects) are needed to ensure ignorable treatment assignment.

4 Solutions

We now discuss three solutions to the contamination bias problem raised by Proposition 1, each targeting a distinct causal parameter. First, in Section 4.1, we discuss estimation of unweighted ATEs. The other two solutions, discussed in Section 4.2, estimate weighted averages of individual treatment effects using an easiest-to-estimate weighting (EW) scheme in that the weights minimize the semiparametric efficiency bound for estimating weighted ATEs under homoskedasticity. If the weights are allowed to vary across treatments, the EW scheme for each treatment is recovered by estimating the partially linear model in eq. 8 but in a sample restricted to individuals in the control group and to those receiving treatment . If the weights are constrained to be common across treatments, this leads to a weighted regression estimator. In Section 4.3, we outline our proposed guidance to researchers in measuring contamination bias and applying these solutions.

Implementing the first solution requires strong overlap (i.e. that treatment propensity scores are bounded away from zero and one) while the other two solutions are not well-defined if the propensity score is fully degenerate. Solutions allowing for degenerate propensity scores require either targeting subpopulations of treated observations or adding substantive restrictions on conditional means of treated potential outcomes (beyond eq. 13, which only restricts untreated potential outcomes). We refer readers to [115, 160, 102, 101, 166] for such solutions in the context of DiD regressions.

4.1 Estimating Average Treatment Effects

Many estimators exist for the ATE of binary treatments—see [133] and [85] for reviews. Several of these approaches extend naturally to multiple treatments: including matching on covariates or the propensity score, inverse propensity score weighting, interacted regression, or doubly-robust methods (see, among others, [104], [107], and [126]). Here we summarize the last two approaches.

For the interacted regression solution, we adapt the implementation for the binary treatment case discussed in [133, Section 5.3] to multiple treatments. Specifically, consider the specification:

| (16) |

where , and we continue to define and the functions as minimizers of . When consists of linear functions, eq. 16 specifies a linear regression of on , , a constant, and the interactions between each treatment indicator and the demeaned control vector . Define for , so that . If Assumption 1 holds and is furthermore rich enough to ensure for then . Moreover, for , such that the regression identifies both the unconditional and conditional ATEs.

The added interactions in eq. 16 ensure that each treatment coefficient is determined only by the outcomes in treatment arms with and , avoiding the contamination bias in Proposition 1. Demeaning the in the interactions ensures they are appropriately centered to interpret the coefficients on the uninteracted as ATEs.

Estimation of eq. 16 is conceptually straightforward for parametric . In particular, if consists of linear functions, one simply estimates

| (17) |

by ordinary least squares (OLS), where is the sample average of the covariate vector. More generally, to increase the plausibility of the key assumption that , one may constrain only by nonparametric smoothness assumptions. Given a sequence of basis functions , such as polynomials or splines, one then approximates with a linear combination of the first terms, with increasing with the sample size, thus tailoring the model complexity to data availability. Given a choice of , estimation and inference can proceed exactly as in the parametric case; the only difference is that the baseline covariates in eq. 17 are replaced by the basis vector and is replaced by the sample average of this expansion. This estimator has been studied in the binary treatment case by [106] and [132], with the latter providing a detailed analysis of how to choose and the former showing that this sieve estimator achieves the semiparametric efficiency bound under strong overlap: it is impossible to construct another regular estimator of the ATE with smaller asymptotic variance.

An attractive alternative approach combines the interacted regression with inverse propensity score weighting. Instead of using OLS to estimate eq. 16 one uses weighted least squares, weighting observations by the inverse of some estimate of the propensity score (see, e.g., [156, 165, 158]). An advantage of this approach is that it is doubly-robust: the estimator is consistent so long as either the propensity score estimator is consistent or the outcome model is correct (i.e. ). A recent literature shows how the double-robustness property, when combined with cross-fitting, reduces the sensitivity of the ATE estimate to overfitting or regularization bias in estimating the nuisance functions and . Cross-fitting also allows for using more flexible methods to approximate and , including modern machine learning methods [[, see, e.g.]]chernozhukov2018double,ceinr22,ChNeSi21.

Either approach should work reliably in stratified RCTs and other settings with strong overlap. But under weak overlap, when propensity scores are not bounded away from zero and one, all of these ATE estimators may be imprecise and have poor finite-sample behavior. This is not a shortcoming of the specific estimator; indeed, [137] show that identification of the ATE is irregular under weak overlap and that it is not possible to estimate it at a -rate. When overlap fails entirely, with some propensity scores obtaining values of zero or one, the ATE is no longer point-identified. These results formalize the intuition that it is difficult or impossible to reliably estimate the counterfactual outcomes for units with extreme propensity scores.141414One approach to limited overlap is trimming: i.e., dropping observations with extreme propensity scores [112, 113, 167]. As with the estimators we derive next, trimming estimators shift the estimand from ATE to easier-to-estimate weighted averages of conditional ATEs. Such extreme propensity scores are common in observational settings. The solutions we discuss next downweight these difficult-to-estimate counterfactuals to address this practical challenge.

4.2 Easiest-to-Estimate Averages of Treatment Effects

Suppose in a sample of observations we wish to estimate a weighted average of conditional potential outcome contrasts , where , is a -dimensional contrast vector with elements , and is some weighting scheme.151515In a slight abuse of notation relative to Section 3, the weights here are not required to average to one. Instead, we scale the estimand by the sum of the weights, . We focus on two specifications for the contrast vector, leading to two alternatives to estimating the ATE using eq. 16. First, for separately estimating the effect of each treatment , we set , and set the remaining entries of to . The contrast of interest then becomes , the weighted ATE of treatment across different strata. Second, we specify so as to allow us to simultaneously contrast the effects of all treatments—we discuss this further below. For each contract vector , we find the easiest-to-estimate weighting (EW) scheme that leads to the smallest possible standard errors under homoskedasticity.

This optimization problem has four motivations. The first is a robustness motivation: a researcher would like to estimate a given contrast as preceisely as possible, at least under the benchmark of constant treatment effects, while being robust to the possibility that the effects are heterogeneous. While the optimization problem does not impose convexity it turns out that the EW scheme is convex. Hence, the resulting estimand retains an interpretation of identifying a convex average of conditional contrasts when treatment effects are heterogeneous while avoiding the contamination bias displayed by the regression estimator per Proposition 1. This robustness property presumably underlies the popularity of regression as a tool for estimating the effect of a binary treatment: the regression estimator is efficient under homoskedasticity and constant treatment effects while, by the [89] result, retaining a causal interpretation under heterogeneous effects.161616There are at least two ways to motivate the interest in convex weights. First, ensures the estimand captures average effects for some well-defined (and characterizable) subpopulation. Second, it prevents what [159] call a sign-reversal: that if has the same sign for all ( or ), then the estimand will also have this sign. [100] call such estimands “weakly causal”.

Second, the EW scheme can be seen as giving a bound on the information available in the data: if the scheme nonetheless yields overly large standard errors, inference on other treatment effects (such as the unweighted ATE) as least as uninformative. Computing the EW standard errors thus reveals whether informative conclusions (regardless of how one specifies the treatment effect of interest) are only possible under additional assumptions or with the aid of additional data. If the EW scheme yields small standard errors even though the standard errors for, say, the unweighted ATE are large, one can conclude that the data is informative about some treatment effects—even if it is not informative about the unweighted average.

In fact, our solution below shows that in the binary treatment case the EW scheme is exactly the same as the weights used by regression. To illustrate the second justification in this special case, recall that the treatment weights are proportional to the conditional variance of treatment, , which tend to zero as tends to zero or one. Regression thus downweights observations with extreme propensity scores where the estimation of counterfactual outcomes is difficult, avoiding the poor finite-sample behavior of ATE estimators under weak overlap and allowing regression to be informative even in cases when it is not possible to precisely estimate the unweighted ATE. More generally, since under binary treatment regression gives the EW scheme, it establishes the extent to which internally valid and informative inference for any causal effect are possible with the data at hand.

Third, the EW scheme can be viewed as offering an intermediate point along a particular robustness-precision “possibility frontier”. The ATE estimator based on the interacted specification in eq. 16 lies on one end of this frontier, being the most robust to treatment effect heterogeneity (i.e. retaining a clear interpretation regardless of the form of or how it relates to the propensity scores). But this robustness comes at the potential cost of imprecision and non-standard inference under weak overlap. The regression estimator based on eq. 8 lies on the other end of the frontier: it is likely to be precise even when overlap is weak (and is efficient under homoskedasticity if the partly linear model in eq. 8 is correct, such that treatment effects are constant). But this precision comes at the cost of contamination bias under heterogeneous treatment effects. The EW scheme lies in between these extremes, purging contamination bias and retaining good performance under weak overlap by giving up explicit control over the treatment effect weighting, letting it be data-determined.171717There are other approaches to resolving the robustness-precision tradeoff, such as seeking precise estimates subject to the weights remaining “close” to one, or placing some restrictions on the form of effect heterogeneity, in contrast to leaving it completely unrestricted as we do here (see [148] for an example of this approach in an IV setting). We leave these alternatives to future research.

Finally, while the derivation of the EW scheme is motivated by statistical precision concerns, the resulting estimand can be seen as identifying the impact of a policy that manipulates the treatment via a particular incremental propensity score intervention. We discuss this interpretation in Remark 6 below.

We derive the EW scheme in two steps. First, we establish a precision benchmark—a semiparametric efficiency bound—for estimation of a given weighted average of treatment effects under the idealized scenario that the propensity score is known. Second, we determine which weights minimize the semiparametric efficiency bound. We discuss estimation when the propensity score is not known in Section 4.3.

The following proposition establishes the first step of our derivation:

Proposition 2.

Suppose eq. 11 holds in an i.i.d. sample of size , with known non-degenerate propensity scores . Let . Consider the problem of estimating the weighted average of contrasts

where the weighting function and contrast vector are both known. Suppose the weighting function satisfies , and that the second moments of and are bounded. Then, conditional on the controls , the semiparametric efficiency bound is almost-surely given by

| (18) |

As formalized in the Section A.2 proof, establishes the lower bound on the asymptotic variance of any regular estimator of under the idealized case of known propensity scores.181818The efficiency bound for the population analog has an additional term, , reflecting the variability of the conditional average contrast. The variance-minimizing weights for thus depend on the nature of treatment effect heterogeneity. By focusing on , we avoid this term, which allows us give the characterization in eq. 19 without any assumptions about heterogeneity in treatment effects.

To establish the second step, we minimize eq. 18 over . Simple algebra shows that the EW scheme is (up to an arbitrary constant) given by

| (19) |

Note that this weighting scheme delivers convex weights, , even though convexity was not imposed in the optimization. Hence, there is no cost in precision if we restrict attention to convex weighted averages of conditional ATEs.

When the contrast vector is selected to estimate the weighted average effect of a particular treatment , a corollary to Proposition 2 is that regression weights are the easiest-to-estimate:

Corollary 1.

For some , let be a vector with elements if , if , and otherwise. Suppose that the conditional variance of relevant potential outcomes is homoskedastic: . Then the variance-minimizing weighting scheme is given by , where

| (20) |

Per eq. 14, the weighting coincides with the weighting of conditional ATEs from the partially linear model (8) when it is fit only on observations with , provided .191919This follows since the propensity score in the subsample is given by , so that in eq. 20 equals the conditional variance of the treatment indicator times the probability of being in the subsample. When the treatment is binary, this simply amounts to running a regression on the binary treatment indicator with an additive covariate adjustment.

Corollary 1 thus gives a precision justification for estimating the effect of any given treatment by a partially linear regression with an additive covariate adjustment in the subsample with under a homoskedasticity benchmark, complementing the robustness motivation discussed earlier.202020As usual, homoskedasticity is a tractable baseline: the arguments in favor of OLS following Corollary 1 can be extended to favor a (feasible) weighted least squares regression when is consistently estimable. To estimate the effects of all treatments one can run such regressions, restricting the sample to one treatment arm and the control group.

This precision justification builds on earlier results in [112, Corollary 5.2] (a working paper version of [113]) and [144, Corollary 1] who show, in the context of a binary treatment, that the weighting minimizes the asymptotic variance of a particular class of inverse propensity score weighted estimators. Our Corollary 1 extends the property to all regular estimators, as well as to multiple treatments.

Remark 5.

The one-treatment-at-a-time regression can also be motivated as a direct solution to contamination bias in the partially linear regression in eq. 8. In particular, as discussed in Section 3.1, contamination bias arises because the implicit linear probability model incorrectly imposes additive separability between and . To solve this issue, one can include interactions between the controls and . This is analogous to the interacted regression in eq. 16, except we exclude the interaction . Running this regression is equivalent to the one-treatment-at-a-time regression.212121To see this, observe that the coefficient on is unchanged if we don’t demean the controls and if we replace with . That is, if we regress onto , , and the interactions for . The regressor matrix is block-diagonal: is non-zero iff and the remaining regressors are nonzero iff . Hence, the coefficient on can equivalently be computed by regressing onto and in the sample with .

Remark 6.

The population analog of the estimand implied by the weighting in Corollary 1, , also identifies the effect of a particular marginal policy intervention. Consider the effects of a class of policies indexed by a scalar that restrict treatments to by increasing the propensity score of treatment to and setting .222222With multiple treatments, policy relevance of any contrast only involving two treatments will generally require the policy to restrict the number of treatments to preclude flows in and out of multiple treatment states. For instance, the ATE gives the effect of comparing two policies: one makes only treatment available, while the other makes only treatment available. Then the marginal effect of the increasing the policy intensity per unit treated at is given by [[, see]for derivation and discussion]ZhOp22. Thus, the weights identify the marginal policy effect if they correspond to the derivative . This is approximately the case for policies under which individuals with more extreme propensity scores are less likely to exhibit a behavioral response, which as argued in [135] is the case for many policies. If the treatment is binary to begin with, [168] show that the approximation is exact for policies that increase the log odds of a treatment by a constant —such as by increasing the intercept in a logit model for treatment.

A shortcoming of the EW scheme in Corollary 1 is that it is treatment-specific, precluding comparisons of the weighted-average effects across treatments.232323Formally, for treatments and , we estimate the weighted averages and . Because the weights and differ, the difference between these estimands cannot generally be written as a convex combination of conditional treatment effects . This critique also applies to the own-treatment weights in Proposition 1. Thus even without contamination bias one may find the implicit multiple-treatment regression weighting deficient. This issue is especially salient when the control group is arbitrarily chosen, such as in teacher VAM regressions which omit an arbitrary teacher from estimation and seek causal comparisons across all teachers.

We thus turn to the question of how Proposition 2 can be used to select the easiest-to-estimate weighting scheme which allows for simultaneous comparisons across all treatment arms. Suppose that the contrast of interest is drawn at random from a given marginal treatment distribution , so that with probability and with the same probability.242424Formally, we draw two treatments at random from the given marginal distribution, discarding the draw if the two treatments are equal. Let denote this distribution over the (now random) contrasts. If the researcher wishes to report an accurate contrast estimate but needs to commit to a weighting scheme before knowing the contrast of interest, it is optimal to minimize the expected variance

Minimizing this expression over is equivalent to minimizing eq. 18 with , which yields eq. 19 with this contrast specification as the optimal weighting. Thus, the optimal weights are proportional to . Specializing to the homoskedastic case leads to the following result:

Corollary 2.

Let denote the distribution over possible contrast vectors such that . Suppose that for all . Then the weighting scheme minimizing the average variance bound is given by:

The easiest-to-estimate common weighting (CW) scheme generalizes the intuition behind the single binary treatment (Corollary 1), placing higher weight on covariate strata where the treatments are evenly distributed, and putting less weight on strata with limited overlap. When the treatment is binary, , the ’s do not matter and the CW scheme reduces to that in Corollary 1: . With multiple treatments, however, the weights remain the same for every treatment—allowing for simultaneous comparisons across all treatment pairs .

There are two natural choices for the marginal treatment probabilities . First, if one is equally interested in all contrasts, one can set . This uniform probability scheme was previously proposed by [143]; our characterization in terms of optimizing a semiparametric efficiency bound is, to our knowledge, novel. Second, if more common treatments are of greater interest, we may set to equal to the empirical treatment probabilities . Treatment arms that have low prevalence would then have little impact on the weighting. This weighting targets precise estimation of contrasts involving more common treatments at the expense of contrasts involving less common treatments. We use this choice in our empirical applications in Section 5. In Section 4.3 below, we show how to implement the CW scheme using a weighted regression approach.

4.3 Practical Guidance in Measuring and Avoiding Contamination Bias

A researcher interested in estimating the effects of multiple mutually exclusive treatments with regression can use Proposition 1 to measure the extent of contamination bias in their estimates. When the propensity score is not fully degenerate, they can further compute one the alternative estimators discussed in the previous subsections. Here we provide practical guidance on both procedures, which we illustrate empirically in the next section.

For simplicity, we focus on the case where is linear and eq. 8 is estimated by OLS. We assume Assumption 1 and both conditions in Assumption 2 hold, such that all propensity scores and potential outcome conditional expectation functions are linearly spanned by the controls . These conditions hold, for example, when contains a set of mutually exclusive group indicators. When is unrestricted, the recommendations in this section would require non-parametric approximations for analogous to those discussed in Section 4.1.

Under this setup, we can decompose the OLS estimator from the uninteracted regression

| (21) |

to obtain a sample analog of the decomposition in Proposition 1. To this end, note that the own-treatment and contamination bias weights in Proposition 1 are identified by the linear regression of on the residuals . Specifically, is given by the th element of the matrix , which can be estimated by its sample analog where is the sample residual from an OLS regression of on and a constant and is a matrix collecting these sample residuals. The th element of estimates the weight that observation puts on the th treatment effect in the th treatment coefficient. For this is an estimate of the own-treatment weight in Proposition 1; for this is an estimate of a contamination weight.

Under linearity, the th conditional ATE may be written as , where and are coefficients in the interacted regression specification

| (22) |

Estimating eq. 22 by OLS yields estimates . For each observation , we stack the set of conditional ATE estimates in a vector .

Using the OLS normal equations, we then obtain a sample analog of the population decomposition in Proposition 1:

| (23) |

The first term estimates the own-treatment effect components, , while the second term estimates the contamination bias components, . If the contamination bias term is large for some , it suggests the estimate of the th treatment effect is substantially impacted by the effects of other treatments. Researchers can also compare the first term of eq. 23 to other weighted averages of own-treatment effects, including the ones discussed next, to gauge the impact of the regression weighting .252525When the covariates are not saturated, it is possible that the estimated weighting function is not positive-definite for some or all . In particular, the diagonal elements of need not all be positive. However, it is guaranteed that the diagonal of sums to one and the non-diagonal weights sum to zero, since .

Further analysis of the estimated weights can shed more light on the regression estimates in . For example, the contamination weights for can be plotted against the treatment effect estimates to visually assess the sources of contamination bias. Low bias may arise from limited treatment effect heterogeneity, small contamination weights, or a low correlation between the two.

Implementing the alternative estimators is also straightforward under the linearity assumptions. First, estimating eq. 17 by OLS yields estimates of the unweighted ATEs . The estimates are numerically equivalent to , where and are OLS estimates of eq. 22.

The second alternative is to estimate the uninteracted regression,

| (24) |

among observations assigned either to treatment or the control group, , for each . These one-treatment-at-a-time regressions estimate the EW scheme from Corollary 1.

The third solution is to estimate the CW scheme from Corollary 2. If the propensity scores were known, one could run a weighted regression of onto and a constant, with each observation weighted by . When the weights are unknown, we replace with its estimate

| (25) |

where denotes estimated propensity scores. We then regress on , weighting by . In our applications below we estimate the propensity scores using a multinomial logit model. When the weights are uniform, this estimator reduces to the estimator studied in [143]. The resulting estimator can be written as

| (26) |

When the treatment is binary and is obtained via a linear regression, this weighted regression estimator coincides with the usual (unweighted) regression estimator that regresses onto and .262626To see this, note that in this case , so that , where the second equality uses the least-squares normal equations and . Proposition 3 in Appendix A shows that the estimator is efficient in the sense that it achieves the semiparametric efficiency bound for estimating .272727Similar to the discussion in Section 4.1, it may be attractive to consider a version of that combines the propensity score weighting with a regression adjustment using an estimate of ; we leave detailed study of such an approach to future research.

Remark 7.

Under homoskedasticity, the second and third solutions yield estimates with smaller asymptotic variance than the estimator of the unweighted ATE. These gains in precision are achieved by changing the estimand to a different convex average of conditional treatment effects. In particular, covariate values where the propensity score is close to zero for some will be effectively discarded. In practice, explicitly plotting the treatment weights and may help to identify the types of individuals who are downweighted by these solutions, and to assess the variation in these weights. Plotting them against treatment effect estimates can help visually assess the extent to which differences in weighting schemes drive differences in between estimates. In particular, the difference between the ATE and any weighted ATE estimand of the effect of treatment with weights , normalized such that is given by . Thus, if the own treatment weights display only a weak covariance with own treatment effect, the weighting will have little effect on the estimand. This is analogous to the observation in Remark 1 that contamination bias reflects the covariance between the contamination weights and treatment effects of the other treatments.

5 Applications

5.1 Project STAR Application

We first illustrate our framework for analyzing and addressing contamination bias with data from Project STAR, as studied in [141]. The Project STAR RCT randomized 11,600 students in 79 public Tennessee elementary schools to one of three types of classes: regular-sized (20–25 students), small (target size 13–17 students), or regular-sized with a teaching aide. The proportion of students randomized to the small class size and teaching aide treatment varied over schools, due to school size and other constraints on classroom organization. Students entering kindergarten in the 1985–1986 school year participated in the experiment through the third grade. Other students entering a participating school in grades 1–3 during these years were similarly randomized between the three class types. We focus on kindergarten effects, where differential attrition and other complications with the experimental analysis are minimal.282828Students in regular-sized classes were randomly reassigned between classrooms with and without a teaching aide after kindergarten, complicating the interpretation of the aide effect in later grades. The randomization of students entering the sample after kindergarten was also complicated by the uneven availability of slots in small and regular-sized classes [141].

| A. Treatment effect estimates | |||||

| Own | ATE | EW | CW | ||

| (1) | (2) | (3) | (4) | (5) | |

| Small | |||||

| Aide | |||||

| Number of controls | 77 | ||||

| Sample size | 5,868 | ||||

B. Contamination bias estimates Worst-Case Bias Bias Negative Positive (1) (2) (3) Small class size 0.155 -1.654 1.670 (0.160) (0.185) (0.187) Teaching aide -0.183 -1.529 1.530 (0.149) (0.176) (0.177)

-

•

Notes: Panel A gives estimates of small class and teaching aide treatment effects for the Project STAR kindergarten analysis. Col. 1 reports estimates from a partially linear model in eq. 21, col. 2 reports the own-treatment component of the decomposition in eq. 23, col. 3 reports the interacted regression estimates based on eq. 17, col. 4 reports estimates based on the EW scheme using one-treatment-at-a-time regressions in eq. 24, and col 5 uses the CW scheme based on eq. 25. Panel B gives the contamination bias component of the decomposition in eq. 23 in col. 1, while cols. 2 and 3 reports the smallest (largest) possible contamination bias from reordering the conditional ATEs to be as negatively (positively) correlated with the cross-treatment weights as possible. Robust standard errors are reported in parentheses. Robust standard errors that assume the propensity scores are known are reported in square brackets.

Column 1 of Panel A in Section 5.1 reports estimates of kindergarten treatment effects in a sample of 5,868 students initially randomized to the small class size and teaching aide treatments. Specifically, we estimate the partially linear regression (eq. 21) where is student ’s test score achievement at the end of kindergarten, are indicators for the initial experimental assignment to a small kindergarten class and a regular-sized class with a teaching aide, respectively, and is a vector of school fixed effects. We follow [141] in computing as the average percentile of student ’s math, reading, and word recognition score on the Stanford Achievement Test in the experimental sample. As in the original analysis [141, column 6 of Table V, panel A], we obtain a small class size effect of 5.36 with a heteroskedasticity-robust standard error of 0.78 and a teaching aide effect of 0.18 (standard error: 0.72).292929Our sample and estimates are very similar to—but not exactly the same as—those in [141]. We use heteroskedasticity-robust (non-clustered) standard errors throughout this analysis, since the randomization of students to classrooms is at the individual leve.

As discussed in Section 2, treatment assignment probabilities vary across the schools indicated by the fixed effects in . If treatment effects also vary across schools in a way that covaries with the contamination weights , we expect the estimated effect of small class sizes to be partly contaminated by the effect of teaching aides (and vice versa). Panel B reports the contamination bias part of the decomposition in eq. 23, which appears minimal for both treatment arms.

It is useful to decompose the contamination bias further into the standard deviation of the school-specific treatment effect , standard deviation of the contamination weights, and their correlation, as discussed in Remark 1. Figure D.2 in Appendix D does this graphically, plotting estimates of the school-specific treatment effects against the contamination weights for . As can be seen from Figure D.2, the variability of school-specific treatment effects is substantial: Adjusting for estimation error, we estimate the standard deviation of to be 11.0 for the small class treatment and of 9.1 for the aide treatment.303030We adjust for estimation error by subtracting the average squared standard error from the empirical variance of the treatment effect estimates and taking the square root. Both standard deviations are an order of magnitude larger than the standard errors in Section 5.1. On the other hand, the standard deviations for the contamination weights for the small class and aide treatment are only moderate: and , respectively. Moreover, the correlation between the conditional treatment effects and the contamination weights is weak: for the small class effect estimate and for the aide effect estimate. The moderate variation in the contamination weights coupled with weak correlation between the weights and the treatment effects explains why the contamination bias is small, even though the treatment effects vary substantially across schools.

Had the experimental design been such that the contamination weights strongly correlate with the treatment effects, sizable contamination bias could have resulted. To illustrate this, we compute worst-case (positive and negative) weighted averages of the estimated by re-ordering them across the computed cross-treatment weights . This exercise highlights potential scenarios in which the randomization strata happened to have been highly correlated with the effect heterogeneity. Columns 2 and 3 in panel B of Section 5.1 show that both bounds on possible contamination bias are an order of magnitude larger than the actual contamination bias: for the small class size treatment and for the teaching aide treatment.313131The point estimates and standard errors in Columns 4 and 5 in Section 5.1 do not account for the fact that the re-ordering is based on estimates of rather than the true treatment effects. This biases the reported estimates away from zero. The reported estimates and associated confidence intervals can be interpreted as giving an upper bound for the worst-case contamination bias. Overall, for both treatments, the underlying heterogeneity in this setting makes substantial contamination bias possible even though actual contamination bias turns out to be relatively small.