Accurate Shapley Values for explaining tree-based models

Salim I. Amoukou Tangi Salaün Nicolas J.B. Brunel

University Paris Saclay LaMME Stellantis Quantmetry University Paris Saclay, ENSIIE LaMME Quantmetry

Abstract

Shapley Values (SV) are widely used in explainable AI, but their estimation and interpretation can be challenging, leading to inaccurate inferences and explanations. As a starting point, we remind an invariance principle for SV and derive the correct approach for computing the SV of categorical variables that are particularly sensitive to the encoding used. In the case of tree-based models, we introduce two estimators of Shapley Values that exploit the tree structure efficiently and are more accurate than state-of-the-art methods. Simulations and comparisons are performed with state-of-the-art algorithms and show the practical gain of our approach. Finally, we discuss the limitations of Shapley Values as a local explanation. These methods are available as a Python package.

1 Introduction

The increasing use of Machine Learning (ML) models in industry, business, sciences, and society has brought the interpretability of these models to the forefront of ML research. As ML models are often considered as black-box models, there is a growing demand from scientists, practitioners, and citizens for tools that can provide insights into important variables in predictions or identify biases for specific individuals or sub-groups. Standard global importance measures like permutation importance measures (Breiman,, 2001) are insufficient for explaining individual or local predictions, and new methodologies are being developed in the active field of Explainable AI (XAI).

In this context, various local explanations have been proposed, focusing on model-agnostic methods that can be applied to the most successful ML models, such as ensemble methods like random forests and gradient boosted trees, as well as deep learning models. Some of the most widely used methods are the Partial Dependence Plot (Friedman,, 2001), Individual Conditional Expectation (Goldstein et al.,, 2015), and local feature attributions such as Local Surrogate (LIME) (Ribeiro et al.,, 2016). These techniques enable better understanding of the predictions made by a model for individual cases, providing transparency and trust in the ML models’ decision-making processes. To achieve the same objective, Shapley Values (Shapley,, 1953), a concept developed primarily in Cooperative Game Theory, has been adapted for XAI to evaluate the ”fair” contribution of a variable to a prediction (Strumbelj and Kononenko,, 2010; Lundberg and Lee,, 2017). Shapley Values (SV) are widely used to identify important variables at both local and global levels. As remarked by Lundberg et al., (2020); Covert et al., 2020b , a lot of importance measures aim at analyzing the behavior of a prediction model based on features by removing variables and considering reduced predictors. Typically, for any group of variables , with any subset and reference distribution , the reduced predictor is defined as:

| (1) |

where is the conditional distribution . Other SV can be defined with the marginal probabilities but their interpretation is different (Heskes et al.,, 2020; Janzing et al.,, 2020; Chen et al.,, 2020). There are still active debates on using or not conditional probabilities (Frye et al.,, 2020). This work focuses only on conditional SV, as estimating them poses significant challenges. The SV for explaining the prediction have been introduced in (Lundberg and Lee,, 2017) and are based on a cooperative game with value function . For any group of variables and , we denote the set and we introduce a straightforward generalization of the SV for coalition as

| (2) |

This definition of the Shapley Value serves as a generalization of the classical SV for a single variable. By considering the singleton for , we retrieve the standard definition for feature . In the following section, we show how this definition arises naturally when measuring the impact of a group of variables , particularly in the case of categorical variables.

We propose solutions for computing and estimating the Shapley Values (SV). We focus solely on tree-based models due to their reduced computational cost and easier statistical handling. We demonstrate that the current state-of-the-art algorithm for tree-based models, TreeSHAP (Lundberg et al.,, 2020), is highly biased when features are dependent. Consequently, we introduce statistically principled estimators to improve the estimation of the SV. Additionally, we address the theoretical computation of SV for categorical variables when using standard encodings, which motivates the use of equation 2. Specifically, we show that the true SV of a categorical variable is different from the sum of SVs of encoded variables, as generally used. Moreover, using the sum of encoded variables as the SV of a categorical variable provides incorrect estimates of all SVs in the model and leads to spurious interpretations. This is currently the only way to handle categorical variables with TreeSHAP, and we therefore highlight the correct method for computing the SV of encoded variables and implement it using our estimators. Our contributions, which reduce bias in SV estimation, are implemented in a Python package.

The paper is structured as follows. In the next section, we derive invariance principles for SV under reparametrization or encoding, which is particularly useful for dealing with categorical variables. In section 3, we introduce two estimators of reduced predictors and SV. In section 4, we highlight the improvement over dependent TreeSHAP. Finally, we discuss the reliability of SV in providing local explanations.

2 Coalition and Invariance for Shapley Values

In this section, we present a unifying property of invariance for the Shapley Values of continuous and categorical variables. The property states that the explanation provided by a variable should not depend on the way it is encoded in a model. This invariance property provides a natural way of computing the SV of categorical variables based on the notion of coalition and the general definition given in equation 2. This is especially useful in our case, as we are also interested in the discretization of continuous variables to facilitate the estimation of Shapley Values and enhance their stability, which we will discuss in Section 3.

2.1 Invariance under reparametrization for continuous variables

In equation 2, there is no restriction on the dimension of . We assume that the variables are vector-valued, i.e., where . We further assume that each variable is transformed with a diffeomorphism . We introduce the transformed variables and the reparametrized model defined by , i.e., where . Generally, we cannot relate the predictor learned from the real dataset to the predictor learned from the transformed dataset where is the label to predict. Estimation procedures are not invariant with respect to reparametrization, which means we obtain different predictors after ”diffeomorphic feature engineering”: . Consequently, we focus only on the impact of reparametrization on explanations, and we show below that the Shapley Values are invariant under reparametrization.

Proposition 2.1.

Let and its reparametrization, then we have , and :

| (3) |

The proof can be found in the Supplementary Material. This identity indicates that the information provided by each feature in the explanation is independent of any encoding, as mentioned by Owen and Prieur, (2017); Covert et al., 2020a . The SV primarily depends on the dependence structure of the features. Therefore, the Shapley Values of a feature remains the same after diffeomorphic transformation , we have . Suppose a variable is separated into correlated variables , for instance, by discretizing a feature. As and carry the same information, we may ask whether the SV of the group of features is equal to the SV of . In the next section, we provide an affirmative answer to this question.

2.2 Invariance for encoded categorical variable

In the remainder of the paper, we use to denote continuous predictive variables, to denote categorical variables and to denote the output of interest. While there are numerous encodings for a categorical variable with modalities , we focus on two popular methods: One-Hot-Encoding (OHE) and Dummy Encoding (DE). These methods introduce indicator variables such that if , otherwise. In contrast to the continuous case, introducing indicator variables changes the number of ”players” in the game defined for computing the Shapley Value. This change has significant consequences on the computation of the SV for all variables in the model. Hence, the widely adopted practice of summing the SV of indicator variables to compute the SV of is generally not justified and false. To benefit from a similar invariance result as Proposition 2.1, we need to deal with the coalition of indicators and use the general expression of SV introduced in equation 2. For the sake of simplicity, we assume that the model uses only the two variables , where and is a categorical variable. The efficiency property of SV gives the decomposition

| (4) |

where denotes the law of . To establish the link between the SV of the indicator variables and the SV of the variable , we introduce additional notations. We focus on the Dummy Encoding (DE) without loss of generality. The variables are defined on , and their distribution is the image probability of induced by the transformation . The initial predictor is reparametrized as a function such that . The function is not completely defined for all and is only defined -almost everywhere because of the deterministic dependence . Consequently, we need to extend to the whole space by setting as soon as . For the predictor , we can compute the SV of and obtain the following decomposition thank to the efficiency property of SV,

| (5) |

where are the SV of the variable computed with distribution and model . Note that

As a result, we have

| (6) |

In general, we have , because the SV depends on the number of variables and they are not calculated using the same quantities. We show in the next proposition that where is computed with equation 2 and corresponds to the Shapley Values of the coalition of the variables .

Proposition 2.2.

Given a predictor and its reparametrization using Dummy Encoding such that , we have

| (7) |

where is the SV of when the variables are considered as a single variable. We refer to Supplementary Material for detailed derivations. In general, for cooperative games, the SV of a coalition with is different from the sum of individual SV . We note that we can compute two different SV for when we use the reparametrized predictor : and . These two SV are different in general as they involve different numbers of variables and different conditional expectations. Proposition 2.2 shows that we should prefer as it is equal to the SV of in the original model .

2.3 Coalition or Sum: numerical comparisons

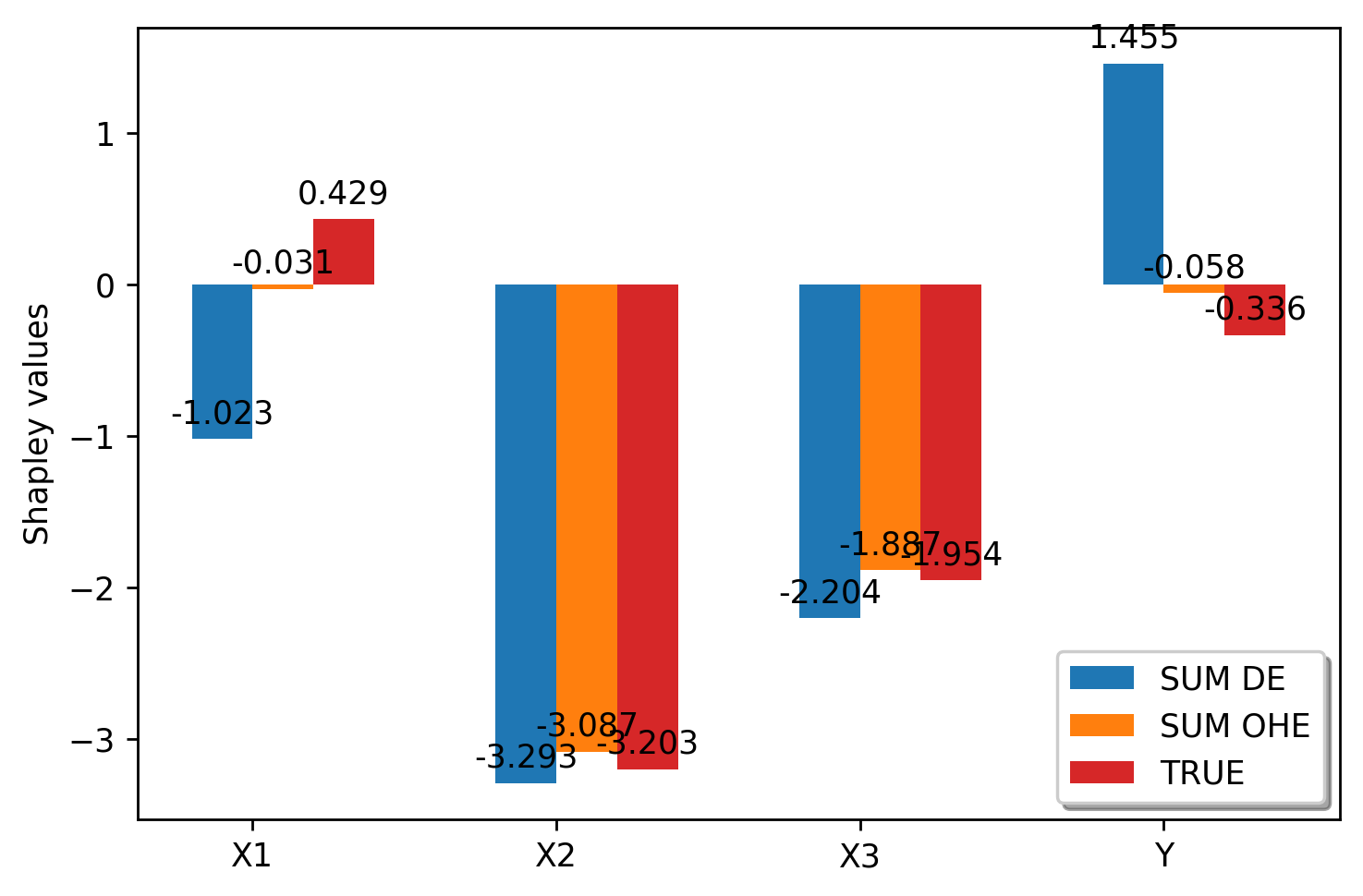

We give numerical examples illustrating the differences between coalition or sum on the corresponding explanations. We consider a linear predictor , with 1 categorical and 3 continuous variables , defined as with and , . The values of the parameters used in our experiments are found in the Supplementary Material. In figure 1, we remark that the SV change dramatically w.r.t the encoding. The sign changes given the encoding (DE or OHE) and is often different from the sign of the true SV of without encoding. We can also note important differences in the SV of the quantitative variable .

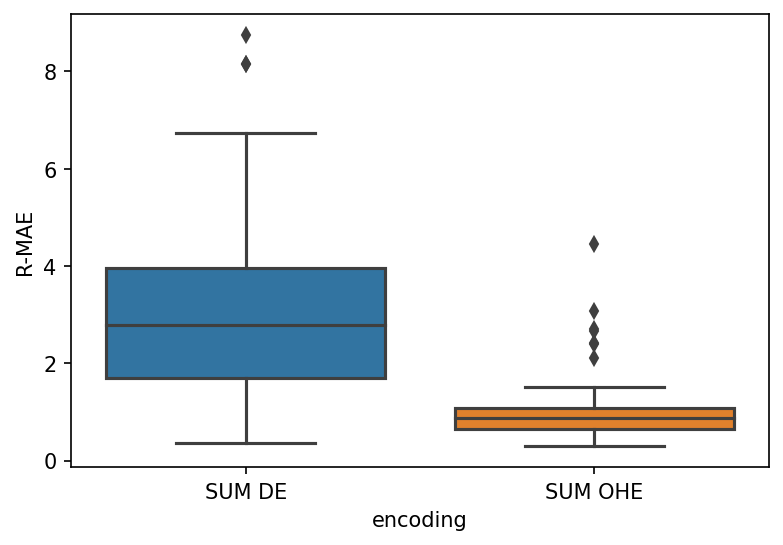

To quantify the global difference of the different methods, we compute the relative absolute error (R-AE) of the SV defined as:

| (8) |

We compute the SV of 1000 new observations. We observe in figure 2 that the differences can be huge for almost all samples (DE is much worse than OHE in this example). Thus, we highly recommend using the coalition as it is consistent with the true SV contrary to the sum. More examples on real datasets can be found in the Supplementary Material.

3 Shapley Values for tree-based models

The computation of Shapley Values (SV) faces two main challenges: the combinatorial explosion with coalitions to consider and the estimation of conditional expectations . Current approaches rely on several approximations and sampling procedures that assume independence (Lundberg and Lee,, 2017; Covert and Lee,, 2020). More recently, some methods propose to model the joint distribution of features with a gaussian distribution or vine copula to draw samples from the conditional distributions (Aas et al.,, 2020, 2021). Other methods, such as (Williamson and Feng,, 2020), train one model for each selected subset of variables, which is accurate but computationally costly. However, their final objective differs from ours since we are interested in local estimates and exact computations (i.e., no sampling of the subsets). To achieve this, we focus on tree-based models, as exploited by Lundberg et al., (2020) for deriving an algorithm (TreeSHAP) for exact computation of SV, where we can compute all the terms (no sampling of the subsets ) and the estimation of the conditional expectations is simplified. After briefly presenting the limitations of TreeSHAP, we introduce two new estimators that use the tree structure. For simplicity, we consider a single tree and not an ensemble of trees (Random Forests, Gradient Tree Boosting, etc.), as extending our estimators to these more complex models is straightforward through linearity.

3.1 Algorithms for computing Conditional Expectations and the Tree SHAP algorithm

We consider a tree-based model defined on (categorical variables are one-hot encoded). We have where represents a leaf. The leaves form a partition of the input space, and each leaf can be written as with . Alternatively, we write the leaf with the decision path perspective: a leaf is defined by a sequence of decision based on variables . For each node in the path of the leaf , is the variable used to split, and the region defined by the split value is either or . The leaf can be rewritten as

| (9) |

The crucial point is to identify the set of leaves compatible with the condition . We can partition the leaf according to a coalition as with and . Thus, for each condition the set of compatible leaves of is

and the reduced predictor has the simple expression

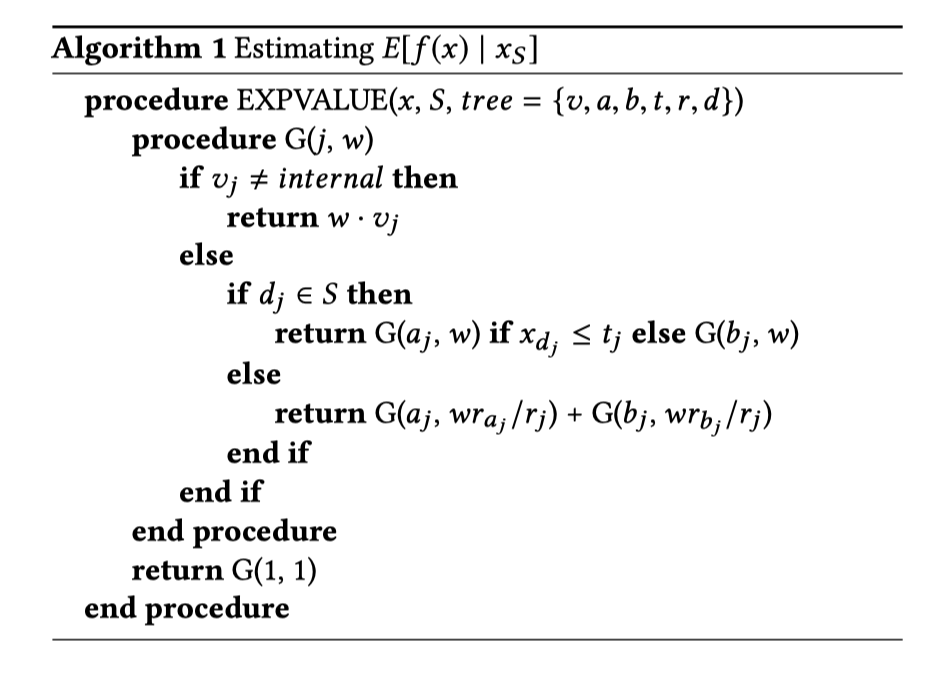

where the probability is computed under the law of the features . If we have a model for , we can derive the conditional law and directly evaluate the conditional probabilities. For instance, when , we can compute exactly the conditional probabilities . In general, deriving conditional probabilities can be challenging, but assumptions about the factorization of the distribution can accelerate the computation. In (Lundberg et al.,, 2020), the authors introduce a recursive algorithm (TreeSHAP with path-dependent feature perturbation, Algorithm 1) that assumes that the probabilities for every compatible leaf can be factored with the decision tree, which simplifies the computation as

| (10) |

with if , and 1 otherwise. The underlying assumption in (10) is that we have a Markov property defined by the path in the tree, see the algorithm description in the Supplementary Material. However, as we will demonstrate in our simulations, this assumption is too strong and leads to a high estimation bias. We denote and as the estimators of the reduced predictor and Shapley Values using the estimator (10). Therefore, we propose two estimators that do not rely on the factorization of .

3.2 Statistical Estimation of Conditional Expectations

Discrete case. To address the statistical problem of estimating the probabilities from a given dataset , where , without assuming any density or prior knowledge about as done in Aas et al., (2020, 2021), we first consider the case where all variables are categorical. This allow us to estimate directly. A straightforward estimation is based on , which is the number of observations in such that , and , which is the number of observations in leaf of that satisfy the condition . An accurate estimation of the conditional probability can be obtained by computing the ratio of these two terms as

| (11) |

Estimating the conditional probabilities becomes more challenging when the variables are continuous. A common approach is to use kernel smoothing estimators (Nadaraya,, 1964). However, this method has several drawbacks, such as a low convergence rate in high dimensions and the need to derive and select appropriate bandwidths, which can add complexity and instability to the estimation procedure. To address these issues, we propose a simple approach based on quantile-discretization of the continuous variables. This technique is commonly used for easing model explainability, particularly in tree-based models, as shown in (Bénard et al., 2021b, ). Binning observations can also help to stabilize the reduced predictors and Shapley Values, thus improving the robustness of the explanation (Alvarez-Melis and Jaakkola,, 2018).

In our experiments, we use a simple approach to discretize continuous variables into quantiles, where each feature is encoded with indicator variables . Let denote the empirical -th quantile of feature using dataset , and let and . We define if falls into the interval . To compute the Shapley Values of a given feature , we use the coalition of its indicator variables as defined in Proposition 2.2. Then, we define the Discrete reduced predictor denoted by as

| (12) |

and the corresponding estimator of the SV is denoted . Although the discretization of continuous variables leads to some loss of information, it is often negligible in terms of performance when using tree-based models, as shown in the Supplementary Material. With only quantiles, the input space is divided into a fine grid of cells, which provides a rich representation of the data. However, this is also a limitation, as the number of cells increases rapidly with and the number of categories per variable, leading to high variance for cells with low frequencies. Therefore, we propose an alternative estimator that leverages the leaf information provided by the decision tree, allowing for faster SV computation.

Continuous and mixed-case. Instead of discretizing the variables, we use the leaves of the estimated trees. Essentially, we replace the conditions by . This change introduces a bias, but it aims at improving the variance during estimation. We introduce the Leaf-based estimator as

| (13) |

where is an estimate of the conditional probability, and is a normalizing constant. The definition of every probability estimate is

where is the number of observations of in the leaf , and is the number of observations of satisfying the conditions . Another interpretation of this estimator is that it projects the partition of the tree along the direction defined by the variables . This results in a projected tree that only considers the variables , which is then used to estimate the conditional probability . It is important to note that the probability estimates do not necessarily sum up to one as we are not conditioning on the same event, i.e.,

Therefore, we introduce a normalizing constant to ensure the probabilities are correctly normalized. This normalizing constant is defined as

The Leaf-based reduced predictor (13) can be computed for continuous and categorical variables, and hence we can compare it with in order to evaluate its bias. In both cases, the main challenge is the computation of , for every coalition . We show in the next section how the computational complexity of the SV is drastically reduced. Indeed, when we consider the leaf , we only have to compute the SV for variables, which corresponds to the variables used for splitting in the leaf , and not for all the variables.

Bias analysis. Before employing the two proposed estimators to calculate the Shapley Values, we first analyze the bias of these estimators. When the variables are discrete, it is obvious that the discrete estimator is consistent. However, in the case of the leaf estimator , we analyze its bias with respect to the true reduced predictor below.

The control of the blue term is well established, and its rate of convergence is known. Recently, Grunewalder, (2018) (Proposition 3.2) shows that if , with , then .

The second term depends on the quality of the partition obtained from the tree. The intuition behind the effectiveness of tree-based models is that they group observations with similar conditional laws in each cell. Indeed, one of the assumptions to prove the consistency of tree-based models is that the variation of the conditional law is zero in each leaf, i.e., for all and , we have (Scornet et al.,, 2015; Meinshausen and Ridgeway,, 2006; Elie-Dit-Cosaque and Maume-Deschamps,, 2022), or alternatively, show that the diameter of the leaves tends to 0 (Györfi et al.,, 2002). The latter ensures that the probability varies slightly as we move within a given cell if admits a continuous density. Therefore, if the diameter of the leaves tends to 0 as generally assumed for partition-based estimator (Györfi et al.,, 2002), the leaf estimator is consistent.

3.3 Fast Algorithm for Shapley Values with the Leaf estimator

Here, we focus on the computational efficiency offered by the Leaf estimator. It is well-known that the computation of the Shapley Values has exponential complexity, as we need to compute different coalitions for each observation. However, with the Leaf estimator , we can reduce the complexity to being exponential in the depth of the tree in the worst case, instead of being exponential in the total number of variables . This is very interesting, as the depth of the tree is rarely above 10 in practice, while can be very large, spanning different orders of magnitude. The idea is to split the original game into the sum of smaller games, as described by the following proposition.

Proposition 3.1.

Consider a tree-based model , and let be the set of variables used along the path to leaf . For any observation and variable , we can decompose its Shapley value into the sum of cooperative games defined on each leaf as follows

| (14) |

where is a reweighted version of the Shapley Value of the cooperative game with players and value function .

Therefore, to compute the Shapley Values, we propose calculating them leaf by leaf using equation 14. In this approach, the computation of the Shapley Values for the variables is performed by summing over cooperative games (leaves), each having a number of variables lower than or equal to , which is the maximum depth of the tree. As a result, the computational complexity is in the worst cases. To improve the computational efficiency, we introduce the Multi-Games algorithm which leverages on Proposition 3.1. This algorithm is linear in the number of observations and can handle a large number of variables. However, its complexity is still higher than that of TreeSHAP (Lundberg et al.,, 2020), which is polynomial with . The algorithm is described below, and we use the notations and .

Remark: This algorithm is highly parallelizable, as it can be vectorized to compute the Shapley values for multiple observations simultaneously.

4 Comparison of the estimators

To compare the different estimators, we need a model where conditional expectations can be calculated exactly. If then is also multivariate gaussian with explicit mean vector and covariance matrix; see Supplementary Material. Note that we do not include any comparisons with KernelSHAP as our main goal is to improve upon TreeSHAP which is the state-of-the-art for tree-based models. In addition, most implementation of KernelSHAP is based on the marginal distribution as its aims to be model-agnostic.

Experiment 1. In the first experiment, we consider a dataset with generated by a linear regression model with following a multivariate Gaussian distribution with mean vector and covariance matrix , where and . The response variable is , where is a vector of coefficients. We trained a RandomForest on and obtained an MSE of . The parameters used for the training can be found in the Supplementary Material. Since the law of is known, we can compute the exact Shapley Values (SV) of using a Monte Carlo estimator (MC).

We aim to compare the true Shapley Value with the Shapley Value estimated by the different methods , where the can be SHAP, Leaf, or D. To quantify the differences between these estimators, we consider two evaluation metrics. Firstly, we compute the Relative Absolute Error (R-AE) as defined in equation (8). Secondly, we measure the True Positive Rate (TPR) to evaluate whether the ranking of the top highest and lowest Shapley Values is preserved across different estimators.

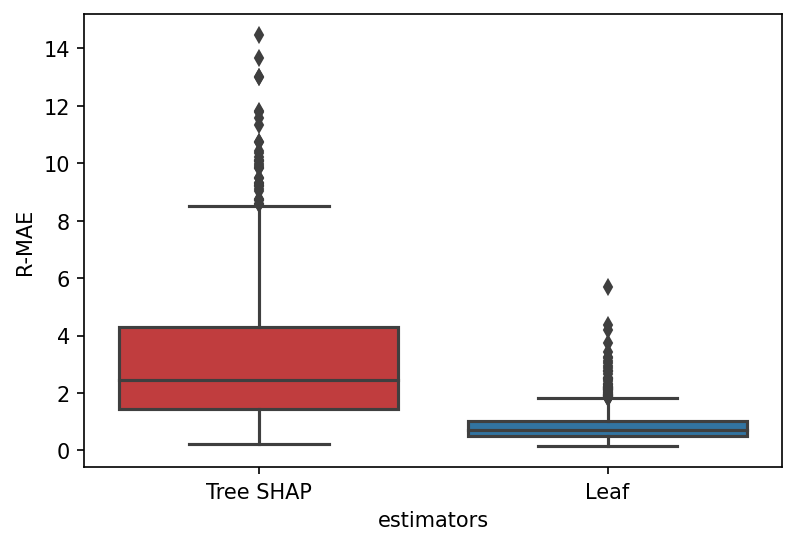

In figure 3, we compute the SV , on a new dataset of size 1000 generated by the synthetic model. We observe that the estimator is more accurate than TreeSHAP by a large margin. TreeSHAP has an average R-AE and TPR while Leaf estimator gets R-AE and TPR.

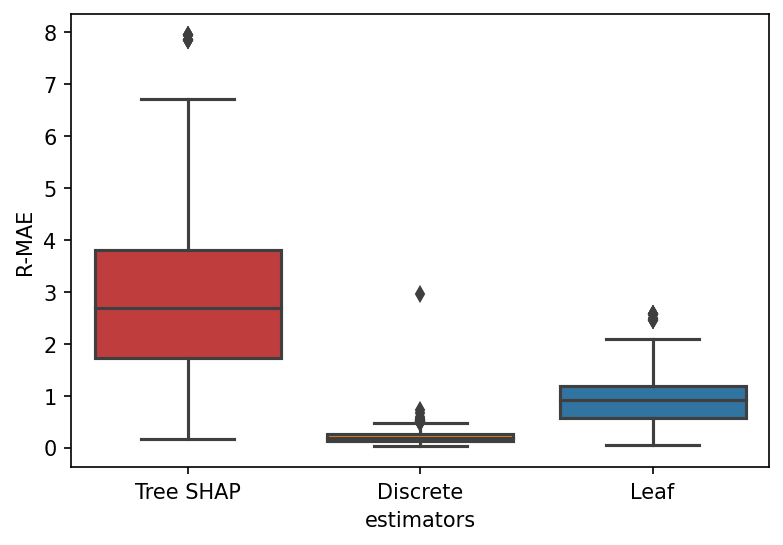

In figure 3, we compare the SV of the Discrete unbiased estimator , TreeSHAP and Leaf estimator with the True , where f was trained on the discretized version of . As demonstrated in figure 4, the Discrete estimator also outperforms TreeSHAP by a significant margin.

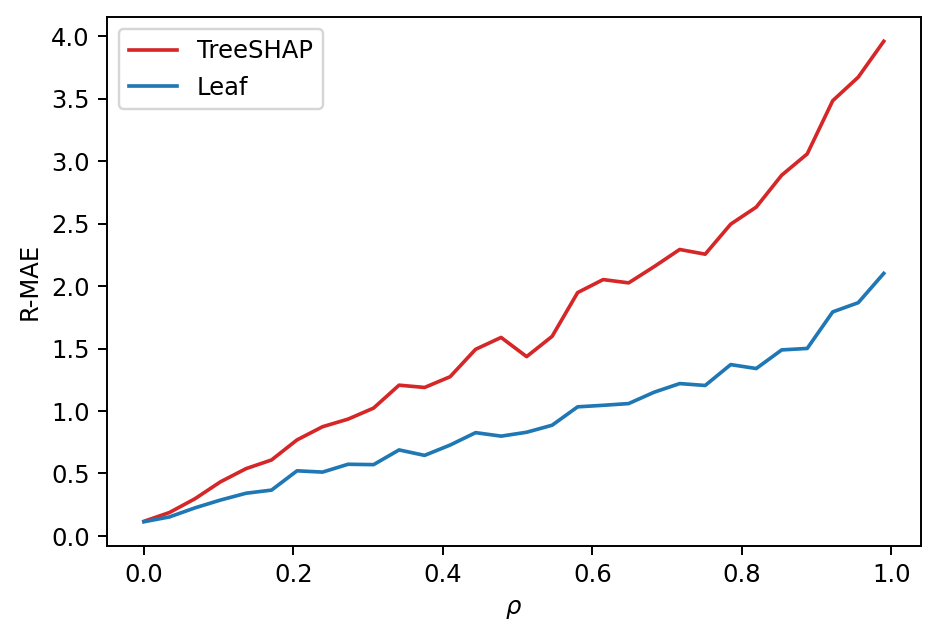

Experiment 2. Here, we investigate the impact of feature dependence on the performance of the different estimators. We utilize the toy model from Experiment 1, but we vary the correlation coefficient from 0 to 0.99, representing increasing positive correlations among the features. As shown in Figure 5, TreeSHAP performs well when the features are independent (), but it is outperformed by Leaf as the dependence between the features increases.

Furthermore, we conduct a runtime comparison of computing SV with Leaf and TreeSHAP on three datasets with different shapes: Boston , Adults , and a toy linear model , where is the number of observations and p is the number of variables. We trained XGBoost with default parameters on these datasets and computed the SV of observations for Adults, the toy model, and observations for Boston. As expected, as shown in Table 1, TreeSHAP is much faster than the Leaf estimator. This difference in runtime can be partly explained by the Leaf estimator having to go through all the data for each leaf, whereas TreeSHAP uses the information stored in the trees. However, the Leaf estimator is not very affected by the dimension of the variables, as it succeeds in computing the SV when in a reasonable time.

| DataSETS | Leaf | Tree SHAP |

|---|---|---|

| A (p=12) | 1 min 4 s ± 1.73 s | 3.33 s ± 39.9 ms |

| B (p=13) | 8.82 s ± 204 ms | 129 ms ± 6.91 ms |

| t (p=500) | 1min 5s ± 1.73 s | 101 ms ± 4.54 ms |

5 Discussion and Future works

We have demonstrated that the current implementation of Shapley Values can lead to unreliable explanations due to biased estimators or inappropriate handling of categorical variables. To address these issues, we have proposed new estimators and provided a correct method for handling categorical variables. Our results show that even in simple models, the difference between the state-of-the-art (TreeSHAP) and proposed methods can be significant. Despite the growing interest in trustworthy AI, the impact of these inaccuracies in explanations is not well understood. One reason for this may be the difficulty in systematically and quantitatively evaluating the quality of an explanation, as it depends on the law of the data, which can be difficult to approximate. Furthermore, such analyses may be influenced by confirmation bias.

We also believe that the quality of estimates is not the only drawback of SV. In fact, we demonstrate in Proposition 5.1 that SV explanations are not local explanations, but remain global, even in simple linear models.

Proposition 5.1.

Let us assume that we have , independent Gaussian features, and a linear predictor defined as:

Even if we choose an observation such that and the predictor only uses , the SV of is not necessarily zero. Indeed,

The proof is in the Supplementary Material. Proposition 5.1 highlights that the SV are not a truly local measures, but rather have a global effect. This occurs because when calculating the SV for or , we also consider subsets that do not contain . By marginalizing and changing the sign of , we use the other linear model not used for the given observation. Such findings pose significant challenges in the interpretation of SV, and we believe that they are often overlooked due to the lack of precision and understanding of Shapley Values in practice.

References

- Aas et al., (2020) Aas, K., Jullum, M., and Løland, A. (2020). Explaining individual predictions when features are dependent: More accurate approximations to shapley values.

- Aas et al., (2021) Aas, K., Nagler, T., Jullum, M., and Løland, A. (2021). Explaining predictive models using shapley values and non-parametric vine copulas. arXiv preprint arXiv:2102.06416.

- Alvarez-Melis and Jaakkola, (2018) Alvarez-Melis, D. and Jaakkola, T. S. (2018). On the robustness of interpretability methods. arXiv preprint arXiv:1806.08049.

- (4) Bénard, C., Biau, G., Da Veiga, S., and Scornet, E. (2021a). Sirus: Stable and interpretable rule set for classification. Electronic Journal of Statistics, 15(1):427–505.

- (5) Bénard, C., Biau, G., Veiga, S., and Scornet, E. (2021b). Interpretable random forests via rule extraction. In International Conference on Artificial Intelligence and Statistics, pages 937–945. PMLR.

- Breiman, (2001) Breiman, L. (2001). Random forests. Machine learning, 45(1):5–32.

- Chen et al., (2020) Chen, H., Janizek, J. D., Lundberg, S., and Lee, S.-I. (2020). True to the model or true to the data? arXiv preprint arXiv:2006.16234.

- Covert and Lee, (2020) Covert, I. and Lee, S. (2020). Improving kernelshap: Practical shapley value estimation via linear regression. CoRR, abs/2012.01536.

- (9) Covert, I., Lundberg, S., and Lee, S. (2020a). Understanding global feature contributions through additive importance measures. CoRR, abs/2004.00668.

- (10) Covert, I., Lundberg, S., and Lee, S.-I. (2020b). Explaining by removing: A unified framework for model explanation. arXiv preprint arXiv:2011.14878.

- Dua and Graff, (2017) Dua, D. and Graff, C. (2017). UCI machine learning repository.

- Elie-Dit-Cosaque and Maume-Deschamps, (2022) Elie-Dit-Cosaque, K. and Maume-Deschamps, V. (2022). Random forest estimation of conditional distribution functions and conditional quantiles. Electronic Journal of Statistics, 16(2):6553–6583.

- Friedman, (2001) Friedman, J. H. (2001). Greedy function approximation: A gradient boosting machine. Ann. Statist., 29(5):1189–1232.

- Frye et al., (2020) Frye, C., de Mijolla, D., Begley, T., Cowton, L., Stanley, M., and Feige, I. (2020). Shapley explainability on the data manifold. arXiv preprint arXiv:2006.01272.

- Goldstein et al., (2015) Goldstein, A., Kapelner, A., Bleich, J., and Pitkin, E. (2015). Peeking inside the black box: Visualizing statistical learning with plots of individual conditional expectation. Journal of Computational and Graphical Statistics, 24(1):44–65.

- Grunewalder, (2018) Grunewalder, S. (2018). Plug-in estimators for conditional expectations and probabilities. In International Conference on Artificial Intelligence and Statistics, pages 1513–1521. PMLR.

- Györfi et al., (2002) Györfi, L., Kohler, M., Krzyżak, A., and Walk, H. (2002). A distribution-free theory of nonparametric regression, volume 1. Springer.

- Heskes et al., (2020) Heskes, T., Sijben, E., Bucur, I. G., and Claassen, T. (2020). Causal shapley values: Exploiting causal knowledge to explain individual predictions of complex models. In Larochelle, H., Ranzato, M., Hadsell, R., Balcan, M., and Lin, H., editors, Advances in Neural Information Processing Systems 33: Annual Conference on Neural Information Processing Systems 2020, NeurIPS 2020, December 6-12, 2020, virtual.

- Janzing et al., (2020) Janzing, D., Minorics, L., and Blöbaum, P. (2020). Feature relevance quantification in explainable ai: A causal problem. In International Conference on Artificial Intelligence and Statistics, pages 2907–2916. PMLR.

- Lundberg et al., (2020) Lundberg, S. M., Erion, G., Chen, H., DeGrave, A., Prutkin, J. M., Nair, B., Katz, R., Himmelfarb, J., Bansal, N., and Lee, S.-I. (2020). From local explanations to global understanding with explainable ai for trees. Nature Machine Intelligence, 2(1):2522–5839.

- Lundberg and Lee, (2017) Lundberg, S. M. and Lee, S.-I. (2017). A unified approach to interpreting model predictions. In Guyon, I., Luxburg, U. V., Bengio, S., Wallach, H., Fergus, R., Vishwanathan, S., and Garnett, R., editors, Advances in Neural Information Processing Systems 30, pages 4765–4774.

- Meinshausen and Ridgeway, (2006) Meinshausen, N. and Ridgeway, G. (2006). Quantile regression forests. Journal of Machine Learning Research, 7(6).

- Nadaraya, (1964) Nadaraya, E. A. (1964). On estimating regression. Theory of Probability & Its Applications, 9(1):141–142.

- Owen and Prieur, (2017) Owen, A. B. and Prieur, C. (2017). On shapley value for measuring importance of dependent inputs. SIAM/ASA Journal on Uncertainty Quantification, 5(1):986–1002.

- Ribeiro et al., (2016) Ribeiro, M. T., Singh, S., and Guestrin, C. (2016). ” why should i trust you?” explaining the predictions of any classifier. In Proceedings of the 22nd ACM SIGKDD international conference on knowledge discovery and data mining, pages 1135–1144.

- Scornet et al., (2015) Scornet, E., Biau, G., and Vert, J.-P. (2015). Consistency of random forests. The Annals of Statistics, 43(4):1716–1741.

- Shapley, (1953) Shapley, L. S. (1953). Greedy function approximation: A gradient boosting machine. Contribution to the Theory of Games, 2:307–317.

- Strumbelj and Kononenko, (2010) Strumbelj, E. and Kononenko, I. (2010). An efficient explanation of individual classifications using game theory. Journal of Machine Learning Research, 11:1–18.

- Williamson and Feng, (2020) Williamson, B. D. and Feng, J. (2020). Efficient nonparametric statistical inference on population feature importance using shapley values.

Supplementary Material:

Accurate Shapley Values for explaining tree-based models

Appendix A Proof of Proposition 3.1: Decomposition of the original game into the sum of smaller game

Proposition A.1.

Consider a tree-based model , and let be the set of variables used along the path to leaf . For any observation and variable , we can decompose its Shapley value into the sum of cooperative games defined on each leaf as follows

| (15) |

where is a reweighted version of the Shapley Value of a cooperative game with players and value function .

Proof.

By definition, we have for the variable

If and , we have

| (16) |

Therefore, can be rewrite as:

∎

Appendix B Proof of SV invariance for transformed continuous variables

Proposition B.1.

Let and its reparametrization, then we have , and :

Proof.

It is a direct application of the change of variables formula. If is the joint density of , the transformed variable has density . We have

The computation of the reduced predictor is straightforward

The equality of Shapley Values directly results from the equality of reduced predictors.

∎

Appendix C Proof of SV invariance for encoded categorical variables

Proposition C.1.

Given a predictor and its reparametrization using Dummy Encoding such that , we have

| (17) |

We recall the expression of the SV of the two variables and . The roles of variables are symmetric, and the categorical or quantitative nature of the variable does not have any impact on the computation of the SV, as demonstrated below. Let’s consider an observation , then

| (20) |

Proof.

Let’s consider the Dummy Encoding (DE) without loss of generality, then the observation is reparametrized as , and by construction of , such that . By taking the coalition of or considering them as a single variable, we have

| (21) |

Using the fact that

we have

We also have

Consequently, we have

We can recognize that we have exactly . We can derive similarly that . ∎

Proposition C.2.

If , then is also multivariate gaussian with mean and covariance matrix equal:

Appendix D Proof of the limitation of SV as local explanation

Proposition D.1.

Let us assume that we have , and a linear predictor defined as:

| (22) |

Even if we choose an observation such that and the predictor only uses , the SV of is not necessarily zero.

Proof.

| (23) | ||||

| (24) |

The second term is zero. Indeed,

Because, if we condition on the event with

| because | ||||

∎

The first term of 3.3 is the classic marginal contribution of SV in linear model.

Therefore,

The computation of is obtained by symmetry.

Appendix E Relation between the Algorithm 1 (TreeSHAP with path-dependent) and

In section 3.1, we have said that the recursive algorithm 1 introduced in Lundberg et al., (2020) and shows in figure 2 assumes that the probabilities can be factored with the decision tree as:

| (25) |

with if , and 1 otherwise.

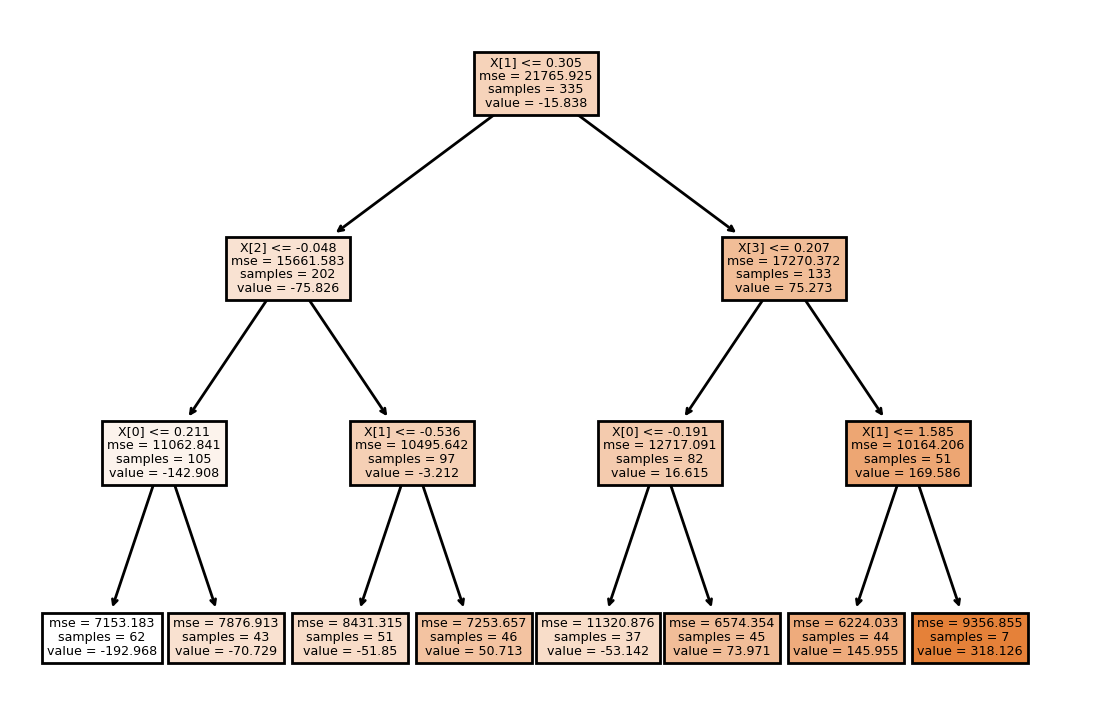

To show the link between between and the Algorithm 1, we choose an observation and compute where is the tree in the left of figure 6. is comptatible with Leaf , we denote the value of each leaf respectively.

The output of the algorithm is on step 4, and its corresponds to:

| Step | Calculus |

|---|---|

| 0 | G(0, 1) |

| 1 | G(1, 202/335) + G(8, 133/335) |

| 2 | G(5, 202/335) + G(9, 88/335) + G(12, 51/335) |

| 3 | G(6,(202/335)*(51/97)) + G(7,(202/335)*(46/97)) + G(11,82/335) + G(13,44/335) |

| + G(14,7/335) | |

| 4 | -(202/335)*(51/97)*51,85 + (202/335)*(46/97)*50,713 + (82/335)*73,971 |

| + (44/335)*145,955 + (7/335)*318,126 | |

| 5 | = 41.98 |

Appendix F Additional experiments

F.1 Impact of quantile discretization

The table below shows the impact of discretization on the performance of a Random Forest on UCI datasets.

| Dataset | Breiman’s RF | q=2 | q=5 | q=10 | q=20 |

|---|---|---|---|---|---|

| Authentification | 0.0002 | 0.08 | 0.002 | 0.0005 | 0.0004 |

| Diabetes | 0.17 | 0.23 | 0.18 | 0.18 | 0.18 |

| Haberman | 0.32 | 0.35 | 0.30 | 0.32 | 0.30 |

| Heart Statlog | 0.10 | 0.10 | 0.10 | 0.10 | 0.10 |

| Hepastitis | 0.13 | 0.15 | 0.14 | 0.14 | 0.13 |

| Ionosphere | 0.02 | 0.07 | 0.03 | 0.02 | 0.02 |

| Liver Disorders | 0.23 | 0.32 | 0.27 | 0.25 | 0.24 |

| Sonar | 0.07 | 0.09 | 0.07 | 0.07 | 0.07 |

| Spambase | 0.01 | 0.14 | 0.03 | 0.02 | 0.01 |

| Titanic | 0.13 | 0.15 | 0.14 | 0.14 | 0.13 |

| Wilt | 0.007 | 0.15 | 0.03 | 0.02 | 0.02 |

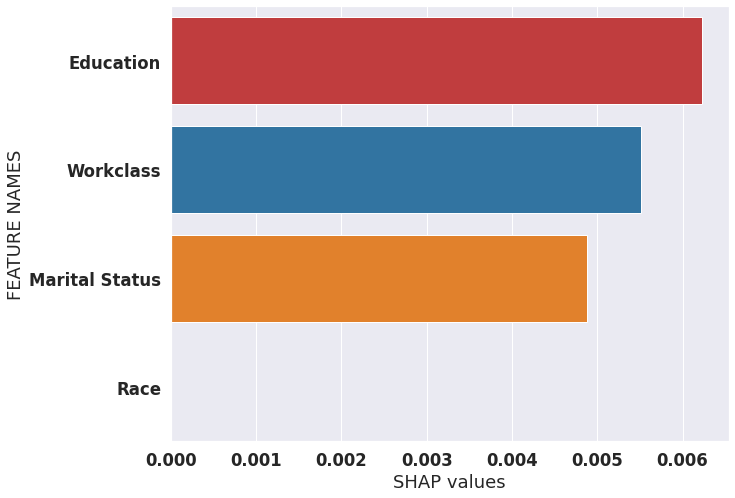

F.2 The differences between Coalition and sum on Census Data

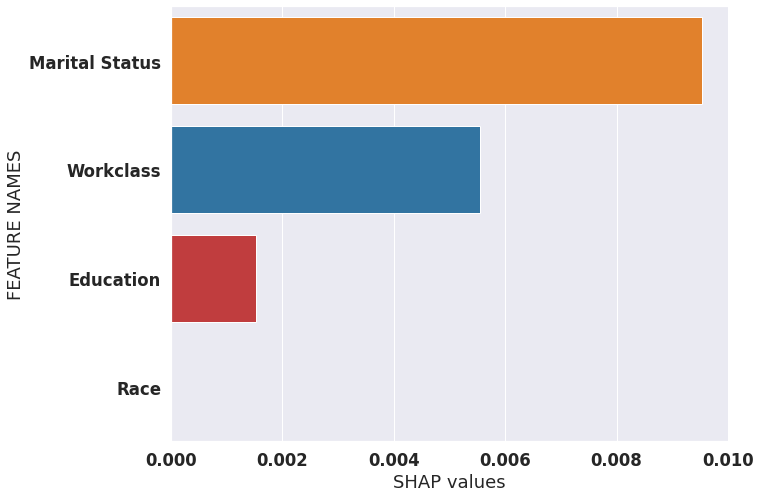

We use UCI Adult Census Dataset Dua and Graff, (2017). We keep only 4 highly-predictive categorical variables: Marital Status, Workclass, Race, Education and use a Random Forest which has a test accuracy of . We compare the Global SV by taking the coalition or sum of the modalities. Global SV are defined as .

In figure 7, we see differences between the global SV with coalition and sum with N=5000. The ranking of the variables changes, e.g. Education goes from important with sum to not important with the coalition. We also compute the proportion of order inversion over N=5000 observations choose randomly. The ranking of variables is changed in of the cases. Note that this difference may increase or diminish depending on the data.

Appendix G EXPERIMENTAL SETTINGS

All our experiments are reproducible and can be found on the github repository Active Coalition of Variables, https://github.com/salimamoukou/acv00

A.1 Toy model of Section 2.3

Recall that the model is a linear predictor with categorical variables define as with and , .

For the experiments in Figure 1 and 2, we set . We use a random matrices generated from a Wishart distribution. The covariance matrices are:

, ,

for respectively.

The coefficients are and the selected observation in figure 1 values is

A.2 Toy model of Section 4

The data are generated from a linear regression with , , , with , is the identity matrix, is all-ones matrix and a linear predictor . for the continuous case and d=3, for the discrete case.

We used the decision tree of sklearn trained on with the defaults parameters. The Mean Squared Error (MSE) are MSE for the continuous case and MSE for the discrete case.