Laurent Condat \Emaillaurent.condat@kaust.edu.sa and \NamePeter Richtárik

\addrKing Abdullah University of Science and Technology (KAUST), Thuwal 23955-6900, Saudi Arabia

MURANA: A Generic Framework for

Stochastic Variance-Reduced Optimization

Abstract

We propose a generic variance-reduced algorithm, which we call MUltiple RANdomized Algorithm (MURANA), for minimizing a sum of several smooth functions plus a regularizer, in a sequential or distributed manner. Our method is formulated with general stochastic operators, which allow us to model various strategies for reducing the computational complexity. For example, MURANA supports sparse activation of the gradients, and also reduction of the communication load via compression of the update vectors. This versatility allows MURANA to cover many existing randomization mechanisms within a unified framework, which also makes it possible to design new methods as special cases.

keywords:

convex optimization, distributed optimization, randomized algorithm, stochastic gradient, variance reduction, communication, sampling, compression1 Introduction

We consider the estimation of the model , for some , arising as the solution of the optimization problem

| (1) |

for some , where each convex function is -smooth, for some , i.e. is nonexpansive, and is a proper, closed, convex function (Bauschke and Combettes, 2017), whose proximity operator

is easy to compute, for any (Parikh and Boyd, 2014; Condat et al., 2022a). We introduce

and we suppose that is -strongly convex, for some , i.e. is convex. Since the problem (1) is strongly convex, exists and is unique.

In a distributed client-server setting, is the number of parallel computing nodes, with an additional master node communicating with these nodes. Communication between the master and nodes is often the bottleneck, so that it is desirable to reduce the amount of communicated information, in comparison with the baseline approach, where vectors of are sent back and forth at every iteration.

In a non-distributed setting, is, for instance, the number of data points contributing to some training task; it is then desirable to avoid scanning the entire dataset at every iteration.

1.1 Randomized optimization algorithms

To formulate our algorithms, we will make use of several sources of randomness of the form

| (2) |

where is the iteration counter, is the model estimate converging to the desired solution , is a control variate converging to , and is a shorthand notation to denote a random realization of a stochastic process with expectation , so that is a random unbiased estimate of the vector . Although we adopt this notation as if were a random operator, its argument does not always have to be known or computed. For instance, if

is not needed when the output is . This means that in (2), is not computed in that case; this is the key reason why randomness makes it possible to decrease the overall complexity. The distribution of the random variable is not needed, and that is why we lighten the notations by omitting to write the underlying probability space structure. Indeed, we only need to know a constant such that, for every ,

| (3) |

where the norm is the 2-norm and denotes the expectation. Thus, if tends to , not only does tend to , but the variance tends to as well. Hence, in a step like in (2), will converge to and everything will work out so that the algorithm converges to the exact solution .

That is, the proposed algorithm will be variance reduced (Gower et al., 2020). In recent years, variance-reduced algorithms like SAGA (Defazio et al., 2014) or SVRG (Johnson and Zhang, 2013; Zhang et al., 2013; Xiao and Zhang, 2014) have become the reference for finite-sum problems of the form (1) since they converge to the exact solution but can be times faster than standard proximal gradient descent, which is typically a huge improvement. Variance reduction with the control variate is akin to an error-feedback mechanism, see Condat et al. (2022c) for a recent discussion on this relationship.

1.2 Communication bottleneck in distributed and federated learning

In the age of big data, there has been a shift towards distributed computations, and modern hardware increasingly relies on the power of uniting many parallel units into a single system. Training large machine learning models critically relies on distributed architectures. Typically, the training data is distributed across several workers, which compute, in parallel, local updates of the model. These updates are then sent to a central server, which performs aggregation and then broadcasts the updated model back to the workers, to proceed with the next iteration. But communication of vectors between machines is typically much slower than computation, so communication is the bottleneck. This is even more true in the modern machine learning paradigm of federated learning (Konečný et al., 2016; McMahan et al., 2017; Kairouz et al., 2021; Li et al., 2020), in which a global model is trained in a massively distributed manner over a network of heterogeneous devices, with a huge number of users involved in the learning task in a collaborative way. Communication can be costly, slow, intermittent and unreliable, and for that reason the users ideally want to communicate the minimum amount of information. Moreover, they also do not want to share their data for privacy reasons.

Therefore, compression of the communicated vectors, using various sketching, sparsification, or quantization techniques (Alistarh et al., 2017; Wen et al., 2017; Wangni et al., 2018; Albasyoni et al., 2020; Basu et al., 2020; Dutta et al., 2020; Sattler et al., 2020; Xu et al., 2021), has become the approach of choice. In recent works (Tang et al., 2019; Liu et al., 2020; Philippenko and Dieuleveut, 2020; Gorbunov et al., 2020b), double, or bidirectional, compression is considered; that is, not only the vectors sent by the workers to the server, but also the model updates broadcast by the server to all workers, are compressed.

Our proposed algorithm MURANA accommodates for model or bidirectional compression using the operators ; see Section 2.1.

1.3 A generic framework

Unbiased stochastic operators with conic variance, like in (3), allow to model a wide range of strategies: they can be used

-

(i)

for sampling, i.e. to select a subset of functions whose gradient is computed at every iteration, like in SAGA or SVRG, as mentioned above;

-

(ii)

for compression; in addition to the idea of communicating each vector only with some small probability, we can mention as example the rand-k operator, which sends out of elements, chosen at random and scaled by , of its argument vector;

-

(iii)

to model partial participation in federated learning, with each user participating in a fraction of the communication rounds only.

That is why we formulate MURANA with this type of operators, which have all these applications, and many more.

1.4 Contributions

We propose MUltiple RANdomized Algorithm (MURANA) – a generic template algorithm with several several sources of randomness that can model a wide range of computation, communication reduction strategies, or both at the same time (e.g. by composition, see Proposition 2.2). MURANA is variance reduced: it converges to the exact solution whatever the variance, which can be arbitrarily large. MURANA generalizes DIANA (Mishchenko et al., 2019; Horváth et al., 2019) in several ways and encompasses SAGA (Defazio et al., 2014) and loopless SVRG (Hofmann et al., 2015; Kovalev et al., 2020) as particular cases; we also give minibatch versions for them. Thus, our main contribution is to present these different algorithms within a unified framework, which allows us to derive convergence guarantees with weakened assumptions.

2 Proposed framework: MURANA

2.1 Three sources of randomness

We define . We first introduce the first set of stochastic operators, , for every and . In particular, we assume that there is a constant such that for every ,

| (4) |

For every and , and at two different iteration indexes are independent random variables. However, they can have different laws since only their first and second order statistics matter, as expressed in (4). Note that and with can be dependent, so should be viewed as a whole joint random process; this is needed for sampling or partial participation, for instance, where indexes in are chosen at random; see Proposition 2.1 below.

Next, we introduce the second set of stochastic operators, , with same properties: for every , , ,

| (5) |

for some constant , and same dependence properties with respect to and as the . and can be dependent, and we will see this in the particular case of DIANA, where .

Finally, we introduce the third set of stochastic operators, , which will be applied to the model updates. For every and ,

| (6) |

for some constant . The operators are mutually independent and independent from all operators and .

To analyze MURANA, we need to be more precise than just specifying the marginal gain . So, we introduce the average gain and the offset , such that, for every and , ,

| (7) |

We can assume that , since (7) is satisfied with replaced by and by , by convexity of the squared norm. In other words, without further knowledge, one can set and . But the convergence rate will depend on , not , and the smaller , the better. Thus, whenever is much smaller than , it is important to exploit this knowledge. In addition, having allows to take larger stepsizes and have better constants in the convergence rates of the algorithms.

In particular, if the operators are mutually independent, the variance of the sum is the sum of the variances, and we can set and . Another case of interest is the sampling setting:

Proposition 2.1 (Marginal and average gains of sampling).

This property was proved in Qian et al. (2019), but with different notations, so we give a new proof in Appendix A, for sake of completeness.

Thus, in Proposition 2.1, can be as large as , but we always have .

Furthermore, the stochastic operators can be composed, which makes it possible to combine random activation with respect to and compression of the vectors themselves, for instance:

Proposition 2.2 (Marginal and average gains of composition).

Let and be stochastic operators such that, for every and ,

for some , , , . Then for every and ,

| (9) | ||||

| (10) |

Thus, the marginal gain of is .

If, in addition, the operators are mutually independent, then for every , , we get

| (11) |

Thus, the average gain of the in that case is and their offset is .

2.2 Proposed algorithms: MURANA and MURANA-D

We propose the MUltiple RANdomized Algorithm (MURANA), described in Algorithm 1, as an abstract mathematical algorithm without regard to the execution architecture, or equivalently, as a sequential algorithm. We also explicitly write MURANA as a distributed algorithm in a client-server architecture, with explicit communication steps, as Algorithm 2, and call it MURANA-D.

If , where denotes the identity, and , MURANA with reverts to standard proximal gradient descent, which iterates:

This baseline algorithm evaluates the full gradient at every iteration, which requires gradient calls. If every gradient call has linear complexity , the complexity is per iteration, which is typically much too large.

Thus, the three sources of randomness in MURANA are typically used as follows: the operators are used to save computation, by using much less than , possibly even only 1, gradient calls per iteration, and/or decreasing the communication load by compressing the vectors sent by the nodes to the master for aggregation. The operators control the variance-reduction process, during which each variable learns the optimal gradient along the iterations, using the available computed information. In a distributed setting, the operators are used for compression during broadcast, in which the server communicates the model estimate to all nodes, at the beginning of every iteration.

When for every and , we recover the recently proposed DIANA method of Mishchenko et al. (2019); Horváth et al. (2019) as a particular case of MURANA-D, but generalized here in several ways, see in Section 3. In MURANA, we have more degrees of freedom than in DIANA: the stochastic gradient , which is an unbiased estimate of and is used to update the model , is obtained from the output of the operators , whereas the control variates learn the optimal gradients using the output of the operators . We can think of L-SVRG, see below in Section 5, which has these two, different and decoupled, mechanisms: the random choice of the activated gradient at every iteration and the random decision of taking a full gradient pass. Thus, MURANA is a versatile template algorithm, which covers many diverse tools spread across the literature of randomized optimization algorithms in a single umbrella.

2.3 Convergence results

We define , , and we denote by the conditioning of .

Theorem 2.3 (Linear convergence of MURANA).

In MURANA, suppose that and , and set and . Choose . Set . Suppose that

| (12) |

Set . Define the Lyapunov function, for every ,

| (13) |

Then, for every , we have , where

| (14) |

Thus, MURANA converges linearly with rate , in expectation; in particular, for every , . In addition, if MURANA is initialized with , for every , we have

| (15) |

In Theorem 2.3, we have

so that

Maximizing this term, which appears in the rate , with respect to yields , so that the best choice for is

Thus, we can provide a simplified version of Theorem 2.3 as follows:

Corollary 2.4.

In MURANA, suppose that and . Choose . Set . Suppose that

| (16) |

Then, using defined in (13), with and , we have, for every , , where

| (17) |

Therefore, if is fixed and , the asymptotic complexity of MURANA to achieve -accuracy is

| (18) |

iterations.

Proof 2.5.

In the conditions of Corollary 2.4, if we set , we have:

Thus, to balance the two constants and , we can choose , so that

Another choice is , so that

3 Particular case: DIANA

When , for every and , and , MURANA-D reverts to DIANA, shown as Algorithm 3 (in the case , i.e. full participation). DIANA was proposed by Mishchenko et al. (2019) and generalized (with ) by Horváth et al. (2019). It was then further extended (still with ) to the case of compression of the model during broadcast by Gorbunov et al. (2020b), where it is called ‘DIANA with bi-directional quantization’; this corresponds to here, and we still call the algorithm DIANA in this case. An extension to was made by Gorbunov et al. (2020a), who performed a unified analysis of a large class of non-variance-reduced and variance-reduced SGD-type methods under strong quasi-convexity. An analysis in the convex regime was performed by Khaled et al. (2020).

However, to date, DIANA was studied for independent operators only. Even in this case, our following results are more general than existing ones. For instance, in Theorem 1 of Horváth et al. (2019), all functions are supposed to be strongly convex, whereas we only require their average to be strongly convex; this is a significantly weaker assumption.

Thus, we generalize DIANA to arbitrary operators , to the presence of a regularizer , and to possible randomization, or compression, of the model updates. As a direct application of Corollary 2.4 with , we have:

Theorem 3.1 (Linear convergence of DIANA).

In DIANA, suppose that and . Choose . Set . Suppose that

Define the Lyapunov function, for every ,

| (19) |

Then, for every , we have , where

| (20) |

Therefore, if is fixed and , the complexity of DIANA to achieve -accuracy is

| (21) |

iterations.

3.1 Partial participation in DIANA

We make use of the possibility of having dependent stochastic operators and we use the composition of operators , like in Proposition 2.2, with the being sampling operators like in Proposition 2.1. This yields DIANA-PP, shown as Algorithm 3. Since DIANA-PP is a particular case of DIANA with such composed operators, we can apply Theorem 3.1, with , the marginal gain of the composed operators here, equal to , , :

Theorem 3.2 (Linear convergence of DIANA-PP).

In DIANA-PP, suppose that the are mutually independent and set . Suppose that and . Choose . Set . Suppose that

Define the Lyapunov function, for every ,

| (22) |

Then, for every , we have , where

| (23) |

Therefore, if is fixed and , the asymptotic complexity of DIANA-PP to achieve -accuracy is

| (24) |

iterations.

To summarize, DIANA is the particular case of DIANA-PP with full participation, i.e. . Its convergence with general, possibly dependent, operators , is established in Theorem 3.1. DIANA-PP is more general than DIANA, since it allows for partial participation, but its convergence is established in Theorem 3.2 only when the operators are mutually independent.

4 Particular case: SAGA

When , for every and , and these operators are set as dependent sampling operators like in Proposition 2.1, and , MURANA becomes Minibatch-SAGA, shown as Algorithm 4. We have , , and we set and . Minibatch-SAGA is SAGA (Defazio et al., 2014) if and proximal gradient descent if , so Minibatch-SAGA interpolates between these two regimes for . This algorithm was called ‘minibatch SAGA with -nice sampling’ by Gower et al. (2021), with their being our , but studied only with . It was called ‘q-SAGA’ by Hofmann et al. (2015) with their being our , but studied only with all functions strongly convex. Thus, the following convergence results are new, to the best of our knowledge.

As an application of Corollary 2.4, we have:

Theorem 4.1 (Linear convergence of Minibatch-SAGA).

Set and choose . Set . In Minibatch-SAGA, suppose that

Define the Lyapunov function, for every ,

| (25) |

Then, for every , we have , where

| (26) |

Therefore, if , the asymptotic complexity of Minibatch-SAGA to achieve -accuracy is iterations and gradient calls, since there are gradient calls per iteration.

On a sequential machine without any memory access concern, is the best choice, but a larger might be better on more complex architectures with memory caching strategies, or under more specific assumptions on the functions (Gazagnadou et al., 2019; Gower et al., 2019).

Let us state the convergence result for SAGA, as the particular case in Theorem 4.1:

Corollary 4.2 (linear convergence of SAGA).

Choose . In SAGA, suppose that

Define the Lyapunov function, for every ,

| (27) |

Then, for every , we have , where

| (28) |

Therefore, if , the asymptotic complexity of SAGA to achieve -accuracy is iterations or gradient calls, since there is 1 gradient call per iteration.

In this result (and in the other ones as well), instead of first choosing , one can choose directly and set accordingly, such that . This yields:

Corollary 4.3 (linear convergence of SAGA).

In SAGA, suppose that

Set . Define the Lyapunov function, for every ,

Then, for every , we have , where

In Theorem 5.6 of Bach (2021), Bach gives a rate for SAGA with of . Let us see how our results with the flexible constant make it possible to understand these constants and improve upon them. is not allowed in Corollaries 4.2 and 4.3. So, let us invoke Theorem 2.3, which is more general than Corollary 2.4, with , , , , , . We choose and , so that . Then we get a rate , which is slightly better but almost the same as above, since . Now, keeping the same value of and choosing , Corollary 4.2 yields a rate , which is better, since . On the other hand, choosing in Corollary 4.3 yields , so that , which is again better, since . Thus, and , and every value in between, are uniformly better choices in SAGA than , according to our analysis.

5 Particular case: L-SVRG

Like SAGA, SVRG (Johnson and Zhang, 2013; Zhang et al., 2013) (sometimes called prox-SVRG (Xiao and Zhang, 2014) if ) is a variance-reduced randomized algorithm, well suited to solve (1), since it can be up to times faster than proximal gradient descent.

Recently, the loopless-SVRG (L-SVRG) algorithm was proposed by Hofmann et al. (2015) and later rediscovered by Kovalev et al. (2020). L-SVRG is similar to SVRG, but with the outer loop of epochs replaced by a coin flip performed in each iteration, designed to trigger with a small probability, e.g. , the computation of the full gradient of . In comparison with SVRG, the analysis of L-SVRG is simpler and L-SVRG is more flexible; for instance, there is no need to know to achieve the complexity. In SVRG and L-SVRG, in addition to the full gradient passes computed once in a while, two gradients are computed at every iteration. A minibatch version of L-SVRG, with instead of 1 gradients picked at every iteration, was called “L-SVRG with -nice sampling” by Qian et al. (2021), see also Sebbouh et al. (2019); we call it Minibatch-L-SVRG, shown as Algorithm 5.

Minibatch-L-SVRG is a particular case of MURANA, with the , , set as dependent sampling operators like in Proposition 2.1, and , . Thus, like for Minibatch-SAGA, we have and . Let . The mappings are all copies of the same random operator , defined by

We have and we set . We also set ; these variables are not stored in Minibatch-L-SVRG, but are computed upon request. Hence, as an application of Corollary 2.4, we get:

Theorem 5.1 (Linear convergence of Minibatch-L-SVRG).

Set and choose . Set . In Minibtach-L-SVRG, suppose that

Define the Lyapunov function, for every ,

| (29) |

Then, for every , we have , where

| (30) |

For instance, with , , so that , and , we have ; since , this is slightly better but very similar to the rate given in Theorem 5 of Kovalev et al. (2020).

Therefore, if , the asymptotic complexity of Minibatch-L-SVRG to achieve -accuracy is iterations and gradient calls, since there are gradient calls per iteration in expectation. This is the same as Minibatch-SAGA if .

6 Particular case: ELVIRA (new)

It is a pity not to use the full gradient in L-SVRG to update , when it is computed. And even with , which means the full gradient computed at every iteration, L-SVRG does not revert to proximal gradient descent. We correct these drawbacks by proposing a new algorithm, called ELVIRA, shown as Algorithm 6. The novelty is that whenever a full gradient pass is computed, it is used just after to update the estimate of the solution.

ELVIRA is a particular case of MURANA as follows: , , and the are set like in Minibatch-L-SVRG. The depend on the and are set as follows: if the full gradient is not computed, are sampling operators like in Proposition 2.1, Minibatch-L-SVRG and Minibatch-SAGA. Otherwise, the are set to the identity.

We have and we set . Moreover, . For instance, if and , we have , instead of with L-SVRG. Like in L-SVRG, we set ; these variables are not stored and are computed upon request.

Hence, as an application of Corollary 2.4, we get:

Theorem 6.1 (Linear convergence of ELVIRA).

Set and choose . Set . In ELVIRA, suppose that

Define the Lyapunov function, for every ,

| (31) |

Then, for every , we have , where

| (32) |

For instance, with , and , we have , like for L-SVRG. But for and a given , the interval for is slightly larger in ELVIRA than in L-SVRG. In other words, for a given , one can choose a larger value of , yielding a smaller rate .

Therefore, if , the complexity of ELVIRA is iterations and gradient calls, since there are gradient calls per iteration in expectation. If in addition , the complexity becomes iterations and gradient calls.

So, the asymptotic complexity of ELVIRA is the same as that of Minibatch-L-SVRG, and it has the same low-memory requirements. But in practice, one can expect ELVIRA to be a bit faster, because its variance is strictly lower. This is illustrated by experiments in Appendix D. ELVIRA reverts to proximal gradient descent if or .

7 Conclusion

We have proposed a general framework for iterative algorithms minimizing a sum of functions by making calls to unbiased stochastic estimates of their gradients, and featuring variance-reduction mechanisms learning the optimal gradients. Our generic template algorithm MURANA allows us to study existing algorithms and design new ones within a unified analysis. Sampling among functions, compression of the vectors sent in both directions in distributed settings, e.g. by sparsification or quantization, as well as partial participation of the workers, which are of utmost importance in modern distributed and federated learning settings, are all features covered by our framework. In future work, we plan to exploit our findings to design new algorithms tailored to specific applications, and to investigate the following questions:

-

1.

Can we relax the strong convexity assumption and still guarantee linear convergence of MURANA? For instance, in Condat et al. (2022c), linear convergence of DIANA under a Kurdyka–Łojasiewicz assumption has been proved.

-

2.

Can we relax the unbiasedness assumption of the stochastic estimation processes? In Condat et al. (2022c), a new class of possibly biased and random compressors is introduced, and linear convergence of DIANA with them is proved.

-

3.

Can we prove last-iterate convergence as well as a sublinear rate for MURANA when the problem is convex but not strongly convex? And in the nonconvex setting?

-

4.

Can we extend the setting of stochastic gradients with variance-reduction mechanisms to other algorithms than proximal gradient descent, like primal–dual algorithms for optimization problems involving several nonsmooth terms (Combettes and Pesquet, 2021; Condat et al., 2022a, b)? An approach of this type has been proposed in Salim et al. (2022), based on another proof technique with the Lagrangian gap, and it would be interesting to combine the two approaches. For instance, can we derive an algorithm like MURANA-D for decentralized optimization, and not only for the client-server setting, similar to the DESTROY algorithm in Salim et al. (2022)?

References

- Albasyoni et al. (2020) A. Albasyoni, M. Safaryan, L. Condat, and P. Richtárik. Optimal gradient compression for distributed and federated learning. arXiv:2010.03246, 2020.

- Alistarh et al. (2017) D. Alistarh, D. Grubic, J. Li, R. Tomioka, and M. Vojnovic. QSGD: Communication-efficient SGD via gradient quantization and encoding. In Proc. of 31st Conf. Neural Information Processing Systems (NIPS), pages 1709–1720, 2017.

- Bach (2021) F. Bach. Learning theory from first principles. Draft of a book, version of Sept. 6, 2021, 2021.

- Basu et al. (2020) D. Basu, D. Data, C. Karakus, and S. N. Diggavi. Qsparse-Local-SGD: Distributed SGD With Quantization, Sparsification, and Local Computations. IEEE Journal on Selected Areas in Information Theory, 1(1):217–226, 2020.

- Bauschke and Combettes (2017) H. H. Bauschke and P. L. Combettes. Convex Analysis and Monotone Operator Theory in Hilbert Spaces. Springer, New York, 2nd edition, 2017.

- Combettes and Pesquet (2021) P. L. Combettes and J.-C. Pesquet. Fixed point strategies in data science. IEEE Trans. Signal Process., 69:3878–3905, 2021.

- Condat et al. (2022a) L. Condat, D. Kitahara, A. Contreras, and A. Hirabayashi. Proximal splitting algorithms for convex optimization: A tour of recent advances, with new twists. SIAM Review, 2022a. to appear.

- Condat et al. (2022b) L. Condat, G. Malinovsky, and P. Richtárik. Distributed proximal splitting algorithms with rates and acceleration. Frontiers in Signal Processing, 1, January 2022b.

- Condat et al. (2022c) L. Condat, K. Yi, and P. Richtárik. EF-BV: A unified theory of error feedback and variance reduction mechanisms for biased and unbiased compression in distributed optimization. arXiv:2205.04180, 2022c.

- Defazio et al. (2014) A. Defazio, F. Bach, and S. Lacoste-Julien. SAGA: A fast incremental gradient method with support for non-strongly convex composite objectives. In Proc. of 28th Conf. Neural Information Processing Systems (NIPS), pages 1646–1654, 2014.

- Dutta et al. (2020) A. Dutta, E. H. Bergou, A. M. Abdelmoniem, C. Y. Ho, A. N. Sahu, M. Canini, and P. Kalnis. On the discrepancy between the theoretical analysis and practical implementations of compressed communication for distributed deep learning. In Proc. of AAAI Conf. Artificial Intelligence, pages 3817–3824, 2020.

- Gazagnadou et al. (2019) N. Gazagnadou, R. Gower, and J. Salmon. Optimal mini-batch and step sizes for SAGA. In Proc. of 36th Int. Conf. Machine Learning (ICML), volume PMLR 97, pages 2142–2150, 2019.

- Gorbunov et al. (2020a) E. Gorbunov, F. Hanzely, and P. Richtárik. A unified theory of SGD: Variance reduction, sampling, quantization and coordinate descent. In Proc. of 23rd Int. Conf. Artificial Intelligence and Statistics (AISTATS), 2020a.

- Gorbunov et al. (2020b) E. Gorbunov, D. Kovalev, D. Makarenko, and P. Richtárik. Linearly converging error compensated SGD. In Proc. of 34th Conf. Neural Information Processing Systems (NeurIPS), 2020b.

- Gower et al. (2019) R. M. Gower, N. Loizou, X. Qian, A. Sailanbayev, E. Shulgin, and P. Richtárik. SGD: General analysis and improved rates. In Proc. of 36th Int. Conf. Machine Learning (ICML), volume PMLR 97, pages 5200–5209, 2019.

- Gower et al. (2020) R. M. Gower, M. Schmidt, F. Bach, and P. Richtárik. Variance-reduced methods for machine learning. Proc. of the IEEE, 108(11):1968–1983, November 2020.

- Gower et al. (2021) R. M. Gower, P. Richtárik, and F. Bach. Stochastic quasi-gradient methods: Variance reduction via Jacobian sketching. Math. Program., 188:135–192, July 2021.

- Hofmann et al. (2015) T. Hofmann, A. Lucchi, S. Lacoste-Julien, and B. McWilliams. Variance reduced stochastic gradient descent with neighbors. In Proc. of 29th Conf. Neural Information Processing Systems (NIPS), pages 1509–1519, 2015.

- Horváth et al. (2019) S. Horváth, D. Kovalev, K. Mishchenko, S. Stich, and P. Richtárik. Stochastic distributed learning with gradient quantization and variance reduction. arXiv:1904.05115, 2019.

- Johnson and Zhang (2013) R. Johnson and T. Zhang. Accelerating stochastic gradient descent using predictive variance reduction. In Proc. of 27th Conf. Neural Information Processing Systems (NIPS), pages 315–323, 2013.

- Kairouz et al. (2021) P. Kairouz et al. Advances and open problems in federated learning. Foundations and Trends in Machine Learning, 14(1–2), 2021.

- Khaled et al. (2020) A. Khaled, O. Sebbouh, N. Loizou, R. M. Gower M., and P. Richtárik. Unified analysis of stochastic gradient methods for composite convex and smooth optimization. arXiv:2006.11573, 2020.

- Konečný et al. (2016) J. Konečný, H. B. McMahan, F. X. Yu, P. Richtárik, A. T. Suresh, and D. Bacon. Federated learning: Strategies for improving communication efficiency. Paper arXiv:1610.05492, presented at the NIPS Workshop on Private Multi-Party Machine Learning, 2016.

- Kovalev et al. (2020) D. Kovalev, S. Horváth, and P. Richtárik. Don’t jump through hoops and remove those loops: SVRG and Katyusha are better without the outer loop. In Proc. of 31st Int. Conf. Algorithmic Learning Theory (ALT), volume PMLR 117, pages 451–467, 2020.

- Li et al. (2020) T. Li, A. K. Sahu, A. Talwalkar, and V. Smith. Federated learning: Challenges, methods, and future directions. IEEE Signal Processing Magazine, 3(37):50–60, 2020.

- Liu et al. (2020) X. Liu, Y. Li, J. Tang, and M. Yan. A double residual compression algorithm for efficient distributed learning. In Proc. of 23rd Int. Conf. Artificial Intelligence and Statistics (AISTATS), volume PMLR 108, pages 133–143, 2020.

- McMahan et al. (2017) H. Brendan McMahan, Eider Moore, Daniel Ramage, Seth Hampson, and Blaise Agüera y Arcas. Communication-efficient learning of deep networks from decentralized data. In Proc. of 20th Int. Conf. Artificial Intelligence and Statistics (AISTATS), 2017.

- Mishchenko et al. (2019) K. Mishchenko, E. Gorbunov, M. Takáč, and P. Richtárik. Distributed learning with compressed gradient differences. arXiv:1901.09269, 2019.

- Parikh and Boyd (2014) N. Parikh and S. Boyd. Proximal algorithms. Foundations and Trends in Optimization, 3(1):127–239, 2014.

- Philippenko and Dieuleveut (2020) C. Philippenko and A. Dieuleveut. Bidirectional compression in heterogeneous settings for distributed or federated learning with partial participation: tight convergence guarantees. arXiv:2006.14591, 2020.

- Qian et al. (2019) X. Qian, A. Sailanbayev, K. Mishchenko, and P. Richtárik. MISO is making a comeback with better proofs and rates. arXiv:1906.01474, June 2019.

- Qian et al. (2021) X. Qian, Z. Qu, and P. Richtárik. L-SVRG and L-Katyusha with arbitrary sampling. Journal of Machine Learning Research, 22(112):1–47, 2021.

- Richtárik and Takáč (2016) P. Richtárik and M. Takáč. Parallel coordinate descent methods for big data optimization. Math. Program., 156:433–484, 2016.

- Salim et al. (2022) A. Salim, L. Condat, K. Mishchenko, and P. Richtárik. Dualize, split, randomize: Fast nonsmooth optimization algorithms. Journal of Optimization Theory and Applications, 2022. to appear.

- Sattler et al. (2020) F. Sattler, S. Wiedemann, K.-R. Müller, and W. Samek. Robust and communication-efficient federated learning from non-i.i.d. data. IEEE Trans. Neural Networks and Learning Systems, 31(9):3400–3413, 2020.

- Sebbouh et al. (2019) O. Sebbouh, N. Gazagnadou, S. Jelassi, F. Bach, and R. Gower. Towards closing the gap between the theory and practice of SVRG. In Proc. of 33rd Conf. Neural Information Processing Systems (NeurIPS), 2019.

- Tang et al. (2019) H. Tang, C. Yu, X. Lian, T. Zhang, and J. Liu. Doublesqueeze: Parallel stochastic gradient descent with double-pass error-compensated compression. In Proc. of Int. Conf. Machine Learning (ICML), pages 6155–6165, 2019.

- Wangni et al. (2018) J. Wangni, J. Wang, J. Liu, and T. Zhang. Gradient sparsification for communication-efficient distributed optimization. In Proc. of 32nd Conf. Neural Information Processing Systems (NeurIPS), pages 1306–1316, 2018.

- Wen et al. (2017) W. Wen, C. Xu, F. Yan, C. Wu, Y. Wang, Y. Chen, and H. Li. TernGrad: Ternary gradients to reduce communication in distributed deep learning. In Proc. of 31st Conf. Neural Information Processing Systems (NIPS), pages 1509–1519, 2017.

- Xiao and Zhang (2014) L. Xiao and T. Zhang. A proximal stochastic gradient method with progressive variance reduction. SIAM J. Optim., 24(4):2057–2075, 2014.

- Xu et al. (2021) H. Xu, C.-Y. Ho, A. M. Abdelmoniem, A. Dutta, E. H. Bergou, K. Karatsenidis, M. Canini, and P. Kalnis. GRACE: A compressed communication framework for distributed machine learning. In Proc. of 41st IEEE Int. Conf. Distributed Computing Systems (ICDCS), 2021.

- Zhang et al. (2013) L. Zhang, M. Mahdavi, and R. Jin. Linear convergence with condition number independent access of full gradients. In Proc. of 27th Conf. Neural Information Processing Systems (NIPS), 2013.

Appendix A Proof of Proposition 2.1

The first statement with the value of follows from

Let us establish the second statement with the values of and . We start with the identity, where denotes expectation with respect to the random set :

By computing the expectations on the right hand side, we finally get:

Appendix B Proof of Proposition 2.2

We have, for every and ,

where the bar denotes conditional expectation, so that and

so that Hence,

Moreover, for every , ,

so that

Thus, if the are mutually independent,

so that

Appendix C Proof of Theorem 2.3

Let us place ourselves in the conditions of Theorem 2.3. We define and . We have .

Let . We have, conditionally on , and : . Thus, using also (6) and the fact that ,

Thus, with ,

| (33) |

Moreover, using nonexpansiveness of the proximity operator and the fact that ,

We have . So, using (7),

where we used the fact that for every vectors , , , where . Now, we will use the fact that and the Peter–Paul inequality, according to which, for every and , . Thus,

where we used the fact that if the constant in front of is negative, we can ignore this term, whereas if it positive, we have to upper bound it.

In addition,

By -strong convexity of , is monotone, so that . Also, by cocoercivity of the gradient, for every , . So,

Hence, using the definition of ,

and, by combination with (33),

On the other hand, conditionally on , , and , we have, for every ,

Thus, with ,

Thus, conditionally on , , and ,

By definition of , , so that the last term above is zero and

where

Since , we have .

Finally, iterating the tower rule on the conditional expectations, we have, for every ,

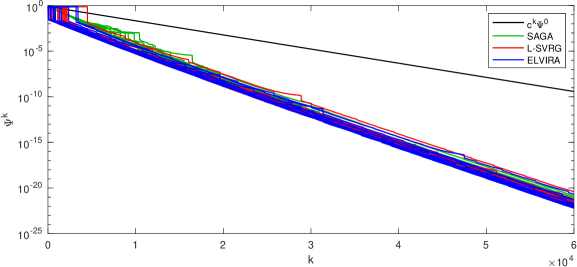

Appendix D Experiments

We compare SAGA, L-SVRG and ELVIRA on the same synthetic problem of minimizing over the average of functions , with ; that is, Problem (1) with . Every function is quadratic: for some matrix of size and vector , all made of independent random values drawn from the uniform distribution in , with . Since , none of the is strongly convex, but their average is -strongly convex, with . Every is -smooth, with . We choose so that the 2 terms in the rate are equal and and we set in the 3 algorithms. In L-SVRG and ELVIRA, and . Then the Lyapunov function is the same for the 3 algorithms, as well as the rate . We show the upper bound in black in Figure 1. The solutions and were computed to machine precision by running SAGA with iterations. The value of with respect to is shown in Figure 1 for the 3 algorithms, for 15 different runs of each algorithm. We can observe that the algorithms converge linearly, as proved by our convergence results, with an empirical convergence rate better than the upper bound. The 3 algorithms have rather similar convergence profiles, with convergence slightly slower for SAGA, ELVIRA performing best, with less choppy curves, and L-SVRG in between. The convergence is shown with respect to the iteration index , but we should keep in mind that SAGA has 1 gradient evaluation per iteration, whereas in average L-SVRG and ELVIRA have 3. But SAGA needs to store all the vectors , while L-SVRG and ELVIRA do not need such memory occupation.