Semiparametric inference on Gini indices of two semicontinuous populations under density ratio models

Meng Yuan, Pengfei Li and Changbao Wu111Meng Yuan is doctoral student, Pengfei Li is Professor and Changbao Wu is Professor, Department of Statistics and Actuarial Science, University of Waterloo, Waterloo ON N2L 3G1,Canada (E-mails: m33yuan@uwaterloo.ca, pengfei.li@uwaterloo.ca and cbwu@uwaterloo.ca).

The Gini index is a popular inequality measure with many applications in social and economic studies. This paper studies semiparametric inference on the Gini indices of two semicontinuous populations. We characterize the distribution of each semicontinuous population by a mixture of a discrete point mass at zero and a continuous skewed positive component. A semiparametric density ratio model is then employed to link the positive components of the two distributions. We propose the maximum empirical likelihood estimators of the two Gini indices and their difference, and further investigate the asymptotic properties of the proposed estimators. The asymptotic results enable us to construct confidence intervals and perform hypothesis tests for the two Gini indices and their difference. We show that the proposed estimators are more efficient than the existing fully nonparametric estimators. The proposed estimators and the asymptotic results are also applicable to cases without excessive zero values. Simulation studies show the superiority of our proposed method over existing methods. Two real-data applications are presented using the proposed methods.

Keywords: Density ratio model, zero-excessive data, empirical likelihood, equality test.

1 Introduction

The Gini index, first proposed by Gini (1912), has been widely used to measure population inequality. In economic studies, it is an important measure of income or wealth inequality among individuals or households in a particular population (Wang et al., 2016; Peng, 2011). In life expectancy studies, it is used to describe the concentration of survival times and to evaluate inequality among people in the target population (Bonetti et al., 2009; Lv et al., 2017). The index is closely related to the Lorenz curve (Lorenz, 1905), a widely used measure for the size distribution of income or wealth. It is the ratio of the area between the Lorenz curve and the 45-degree line to the area under the 45-degree line. Hence, the Gini index ranges from 0 to 1, with 0 indicating perfect equality and 1 for extreme inequality.

Study variables such as income and survival time are often modelled by using a positive continuous distribution. One important scenario in applications is that there are two related populations, each containing a sizeable zero values for the study variable. The inferential problems can be on the Gini index for each population separately or the difference of the two Gini indices. The scenario is quite common in practice but efficient inferential procedures are not available in the existing literature.

In this paper, we propose new semiparametric inference procedures for the Gini indices of two semicontinuous populations. Specifically, suppose that we have two independent samples from two related populations with values of the study variable generated from the following mixture models:

| (1) |

where is the zero proportion in population , is the sample size for sample , is an indicator function, and is the cumulative distribution function (CDF) of the positive observations in sample . For population , the Gini index can be equivalently defined (David, 1968) as

| (2) |

where is the expected absolute difference of for two randomly selected units from population and is the expectation of population . Our discussions in this paper focus on statistical inferences on , , and . It is worth mentioning that although our results are presented for cases where the two populations contain excess zeros for the study variable, the proposed methods and the theoretical results are also applicable to cases without excess zeros, i.e., in model (1). In addition, inferences on a general function of and can also be conducted. See Section 2 for further discussion.

Samples with positive outcomes only, i.e., in model (1), are common in studies of family income or wealth or a country’s gross domestic products (Gastwirth, 1972; Cowell, 2011). For instance, all the household incomes are positive in the 1997 Family and Income and Expenditure Survey conducted by the Philippine Statistics Authority. More details can be found in Section 4. Samples with a mixture of excess zero values and skewed positive outcomes, i.e., in model (1), naturally arise in studies of expenditure data and health cost data (Zhou & Tu, 1999; Zhou & Tu, 2000; Zhou & Cheng, 2008). For example, Zhou & Cheng (2008) presented a dataset from the assessment of inpatient charges (see Section 4), and most patients with uncomplicated hypertension had no hospitalization and therefore zero costs. This paper systematically studies both cases ( and ) in a unified framework via model (1).

Many studies of the Gini index have applied nonparametric methods. For example, point estimators of , , and and their asymptotic variance estimation have been discussed in Hoeffding (1948), Anand (1983), Ogwang (2000), Giles (2004), Modarres & Gastwirth (2006), Yitzhaki (1991), Karagiannis & Kovacevic (2000), and Davidson (2009). See Wang & Zhao (2016) for a detailed review. Qin et al. (2010) and Peng (2011) used the empirical likelihood (EL) method (Owen, 2001) to construct confidence intervals (CIs) for the index. More recently, Wang et al. (2016) derived the jackknife EL (JEL). Peng (2011) and Wang & Zhao (2016) compared two Gini indices of independent or correlated populations using the EL method and the JEL method, respectively.

Fully nonparametric methods are robust to potential model misspecifications on the ’s. However, these methods ignore the characteristics common to the two samples and/or the relation between the two populations, which have been shown to be useful for more efficient statistical inferences; see, for instance, the studies on the strengths of lumber produced in Canada in different years (Chen & Liu, 2013; Cai et al., 2017; Cai & Chen, 2018) and biomarkers for the diagnosis of disease in case and control groups (Yuan et al., 2020, 2021).

To combine the information from the two samples without making risky parametric distributional assumptions, we model the CDFs of the positive observations and in model (1) via a density ratio model (DRM) (Anderson, 1979; Qin, 2017). Let be the probability density function of , . The DRM postulates that

| (3) |

where is the vector of unknown parameters and with being a -dimensional, prespecified, nontrivial basis function. Note that the baseline distribution is completely unspecified, which allows the DRM to embrace many distributions that are commonly used in the study of the Gini index (Moothathu, 1985, 1989, 1990). For example, when , the DRM includes two log-normal distributions with the same variance with respect to the log-scale, two Pareto distributions with the same scale parameter, and two chi-square distributions with different degrees of freedom; when , the DRM includes two exponential distributions with different rates. The DRM is closely related to the well-studied logistic regression (Qin & Zhang, 1997) and is broader than the Cox proportional hazard model (Jiang & Tu, 2012).

The DRM has served as a useful and flexible inferential platform for many statistical problems, including quantile and quantile-function estimation (Chen & Liu, 2013; Yuan et al., 2021; Chen et al., 2021), receiver operating characteristic analysis (Qin & Zhang, 2003; Chen et al., 2016; Yuan et al., 2021), hypothesis-testing problems (Fokianos et al., 2001; Cai et al., 2017), and data integration (Qin et al., 2015; Yuan et al., 2021). Recently, the DRM has been used for semicontinuous data. For example, Wang et al. (2017) and Wang et al. (2018) developed EL ratio (ELR) statistics for testing the homogeneity of distributions and the equality of population means, respectively. Yuan et al. (2020) proposed estimators of linear functionals of two semicontinuous populations. To the best of our knowledge, inferential procedures for two Gini indices , and their difference have not been explored under the mixture model (1) and the DRM (3). This paper aims to fill this void.

Our contributions can be summarized as follows. We first propose the maximum EL estimators (MELEs) of , , and under models (1) and (3). Using techniques from U-statistics and V-statistics, we derive the asymptotic normality of the MELEs of , , and and show that their asymptotic variances are smaller than those of nonparametric estimators. These asymptotic results are used to construct Wald-type CIs for , , and and obtain a Wald-type statistic for testing . The proposed methods and asymptotic results are applicable to both and in model (1). Extensive simulation studies and applications to two real datasets demonstrate the advantages of our proposed methods over existing ones. Software for implementing the proposed methods and Qin & Zhang (1997)’s goodness-of-fit test for the DRM assumption in (3) has been developed in R and is available from the authors upon request.

The rest of the paper is organized as follows. In Section 2, we propose the MELEs of , , and and study their asymptotic properties under the assumed semiparametric density ratio model. We construct CIs and conduct hypothesis tests on , , and based on the theoretical results. Results from simulation studies are presented in Section 3, and applications to two real-world datasets are given in Section 4. We conclude the paper with a discussion in Section 5. Proofs and technical details and additional simulation results are provided in the Supplementary Material.

2 Main Results

Let and be the (random) numbers of zero observations and positive observations, respectively, in each sample . It follows that for . Without loss of generality, we assume that the first observations in group , , are positive, and the remaining observations are 0. Let be the total (fixed) sample size, i.e., .

2.1 The MELEs of and

In this section, we develop the EL function and present the MELEs of and . Based on the two samples from model (1), the full likelihood function is given by

| (4) |

which is the product of two likelihood components: one from the number of zero observations and the other from the positive observations.

Following the EL principle (Owen, 2001) and with the help of the DRM (3), we use the combined sample to model via

| (5) |

where for and . The model for in (5) and the DRM (3) together imply that

| (6) |

To ensure that both and are CDFs, the feasible ’s must satisfy the following set of constraints:

| (7) |

where .

Let . Substituting (5) and (6) into (4) and taking the logarithm, we obtain the empirical log-likelihood function of as

| (8) |

where

Here is the binomial log-likelihood function corresponding to the zero observations, and represents the empirical log-likelihood function associated with the positive observations. The MELE of is then defined as

subject to the constraints in .

With the form of given in (8), it can be checked that the MELE of has a closed form expression given by

and the MELE of is then denoted as

| (9) |

Following Cai et al. (2017), the estimator can be obtained by maximizing the following dual empirical log-likelihood function without any constraints:

| (10) |

where is a random variable. That is, . Once the is obtained, the MELEs of the ’s are computed as

| (11) |

With the MELEs and , the MELE of and for as specified in (5)–(6) can be computed as

| (12) |

2.2 Asymptotic properties of MELEs

In this section, we study the asymptotic properties of the MELEs . We use , , and to denote the true values of , , and , respectively. Let and

where denotes the expectation operator with respect to , and refers to a random variable from the distribution .

The asymptotic results in this section are developed under the following regularity conditions.

-

C1:

As the total sample size goes to infinity, for some constant .

-

C2:

The two CDFs and satisfy the DRM (3) with the true parameter , and for all in a neighborhood of the true value .

-

C3:

The components of are continuous and stochastically linearly independent.

-

C4:

The moments and exist for all in a neighborhood of the true value .

Condition C1 indicates that both and go to infinity at the same rate. For simplicity, and convenience of presentation, we write and assume that it is a constant. This does not affect our technical development. Condition C2 guarantees the existence of the moment generating function of in a neighborhood of and therefore all its finite moments. Condition C3 is an identifiability condition. Conditions C2 and C3 together imply that is positive definite and the quadratic approximation of the dual empirical log-likelihood function is applicable. Conditions C1–C4 guarantee that the linear approximations of and can be used.

The following theorem establishes the asymptotic normality of the MELEs .

Theorem 1.

Assume that for and Conditions C1–C4 are satisfied. As the total sample size ,

in distribution with the asymptotic variance-covariance matrix

| (15) |

where

Note that the condition for ensures that the binomial log-likelihood function has regular properties and the quadratic approximation is applicable. Repeating all the steps in the proof of Theorem 1, we obtain a similar result for cases where for in the following theorem.

Theorem 2.

Assume that Conditions C1–C4 are satisfied. When there is no excess of zeros, i.e., for , the joint distribution of and asymptotically follows a bivariate normal distribution with mean zero and variance in (15) with being replaced by 0.

Since the proposed method utilizes more information to obtain the MELEs of Gini indices, we expect that the proposed MELEs are more efficient than fully nonparametric estimators. With the alternative form of the Gini index in (13), the fully nonparametric estimators of the two Gini indices for sample are

| (16) |

where

and is the empirical CDF of the positive observations in sample . The following theorem compares the proposed estimators MELEs and the nonparametric estimators in terms of their asymptotic variance-covariance matrices. Note that is the asymptotic variance-covariance matrix of the MELEs given in Theorem 1.

Theorem 3.

Assume that Conditions C1–C4 are satisfied.

-

(a)

For the nonparametric estimators and as , we have

in distribution, where the variance-covariance matrix

-

(b)

The two asymptotic variance-covariance matrices and satisfy

where for and

Note that is a positive semidefinite matrix, which implies that the proposed MELEs for the Gini index are at least as efficient as the nonparametric estimators. Our simulation results reported in Section 3 confirm this result. It is worth mentioning that the theorem is applicable whether or not there are excess zero values.

2.3 Inference on functions of Gini indices

Under the current setting of two samples, we may be interested in performing inference on the Gini index for only one of the samples or other functions of the two Gini indices, such as their difference. The results of Theorems 1 and 2 can be used to develop the following theorem for parameters which are a general function of the two Gini indices.

Theorem 4.

Assume the conditions of Theorem 3 hold. Let be a bivariate smooth function. As , we have in distribution with

With the results in Theorems 3 and 4, we can easily show that is no larger than the asymptotic variance of the fully nonparametric estimator . That is, utilizing the information from both samples via the DRM (3) improves the estimation of .

The general form covers many interesting functions of and . For example, when , the parameter represents the logit transformation of the Gini index ; when , the parameter refers to the difference of two Gini indices.

The variance may depend on , , and . Replacing these unknown quantities by their MELEs leads to a consistent estimator of . Together with the result in Theorem 4, we have

in distribution. Hence, is asymptotically pivotal and can be used to construct CIs and to conduct hypothesis tests on .

For ease of presentation, we use and to denote and . Then the Wald-type CI for is given by

where is the quantile of the standard normal distribution. When testing , we reject the null hypothesis if at the significance level .

3 Simulation Studies

In this section, we compare the finite-sample performance of our semiparametric methods with existing methods of inferences on the Gini indices through simulation studies. We focus on three inferential problems:

-

(1)

Point estimation for , , and ;

-

(2)

Confidence intervals on , , and ;

-

(3)

Hypothesis testing on .

We conduct the simulation studies under two distributional settings: (i) and are the CDFs of and ; and (ii) and are the CDFs of and . Here represents the chi-square distribution with degrees of freedom, and refers to the exponential distribution with the rate parameter . The proposed inference procedures under the DRM are implemented with the correctly specified , where in the setting and in the exponential setting. For each scenario, we consider two combinations of sample sizes, , , and the results are based on 2,000 Monte Carlo simulation runs.

3.1 Performance of point estimators

We start by exploring the performance of the point estimators. We consider the following three estimators:

Three combinations of are considered for the zero population proportions: , , . We evaluate the performance of a point estimator in terms of the bias and the mean squared error (MSE). Tables 1 and 2 present the simulated results for different settings.

| Bias | MSE | Bias | MSE | Bias | MSE | |||

|---|---|---|---|---|---|---|---|---|

| (100,100) | (0,0) | EMP | 5.37 | 0.74 | 7.80 | 0.62 | -2.43 | 1.29 |

| JEL | -0.39 | 0.73 | 1.57 | 0.57 | -1.96 | 1.31 | ||

| DRM | 2.06 | 0.37 | 4.18 | 0.40 | -2.13 | 0.31 | ||

| (0.3,0.3) | EMP | 6.17 | 1.19 | 6.19 | 1.21 | -0.02 | 2.35 | |

| JEL | 2.16 | 1.18 | 1.83 | 1.20 | 0.33 | 2.40 | ||

| DRM | 2.60 | 0.95 | 3.04 | 1.06 | -0.44 | 1.71 | ||

| (0.7,0.7) | EMP | 6.56 | 0.91 | 6.01 | 1.01 | 0.54 | 1.86 | |

| JEL | 4.88 | 0.91 | 4.18 | 1.01 | 0.70 | 1.89 | ||

| DRM | 2.70 | 0.79 | 2.97 | 0.91 | -0.28 | 1.56 | ||

| (300,300) | (0,0) | EMP | 1.70 | 0.23 | 2.31 | 0.19 | -0.61 | 0.40 |

| JEL | -0.22 | 0.23 | 0.23 | 0.19 | -0.45 | 0.40 | ||

| DRM | 0.66 | 0.13 | 1.12 | 0.14 | -0.46 | 0.11 | ||

| (0.3,0.3) | EMP | 2.52 | 0.39 | 1.75 | 0.41 | 0.78 | 0.79 | |

| JEL | 1.18 | 0.39 | 0.29 | 0.41 | 0.90 | 0.80 | ||

| DRM | 0.94 | 0.32 | 0.89 | 0.37 | 0.06 | 0.57 | ||

| (0.7,0.7) | EMP | 2.84 | 0.31 | 2.40 | 0.34 | 0.44 | 0.67 | |

| JEL | 2.28 | 0.31 | 1.78 | 0.34 | 0.49 | 0.67 | ||

| DRM | 1.30 | 0.27 | 1.50 | 0.31 | -0.20 | 0.55 | ||

| Bias | MSE | Bias | MSE | Bias | MSE | |||

|---|---|---|---|---|---|---|---|---|

| (100,100) | (0,0) | EMP | 4.59 | 0.81 | 5.94 | 0.86 | -1.35 | 1.59 |

| JEL | -0.42 | 0.81 | 0.95 | 0.84 | -1.37 | 1.63 | ||

| DRM | 1.55 | 0.66 | 2.82 | 0.41 | -1.27 | 0.58 | ||

| (0.3,0.3) | EMP | 4.85 | 1.09 | 3.53 | 1.10 | 1.31 | 2.14 | |

| JEL | 1.36 | 1.09 | 0.03 | 1.11 | 1.33 | 2.19 | ||

| DRM | 1.64 | 0.96 | 0.73 | 0.82 | 0.91 | 1.46 | ||

| (0.7,0.7) | EMP | 5.17 | 0.81 | 3.62 | 0.80 | 1.55 | 1.55 | |

| JEL | 3.71 | 0.81 | 2.14 | 0.80 | 1.57 | 1.58 | ||

| DRM | 1.81 | 0.73 | 1.24 | 0.65 | 0.56 | 1.20 | ||

| (300,300) | (0,0) | EMP | 1.78 | 0.28 | 1.97 | 0.27 | -0.18 | 0.57 |

| JEL | 0.11 | 0.28 | 0.30 | 0.27 | -0.19 | 0.58 | ||

| DRM | 0.76 | 0.22 | 0.96 | 0.13 | -0.20 | 0.21 | ||

| (0.3,0.3) | EMP | 1.80 | 0.37 | 1.48 | 0.36 | 0.32 | 0.73 | |

| JEL | 0.63 | 0.37 | 0.31 | 0.36 | 0.32 | 0.74 | ||

| DRM | 0.74 | 0.34 | 0.73 | 0.27 | 0.01 | 0.51 | ||

| (0.7,0.7) | EMP | 1.81 | 0.26 | 1.98 | 0.26 | -0.16 | 0.53 | |

| JEL | 1.32 | 0.26 | 1.48 | 0.26 | -0.16 | 0.54 | ||

| DRM | 0.80 | 0.24 | 0.90 | 0.22 | -0.10 | 0.43 | ||

We observe from Tables 1 and 2 that the biases of the estimators of and are acceptable for all three methods under all scenarios. The EMP estimators and always give the largest biases. When the proportions of zero values are small, i.e., or , the biases of the JEL estimators and are the smallest. The DRM estimators and have a clear advantage in terms of bias when . The performance of the EMP estimators and and the JEL estimators and is similar in terms of the MSE. The DRM estimators and give the smallest MSEs in all cases; this agrees with the result in Theorem 3. The MSEs of all the estimators decrease as moves toward or the sample size increases.

For the estimators of the difference , we find that the biases of all the estimators are relatively small in all cases. The biases of the DRM estimator are usually the smallest. The MSEs of the EMP estimator for and JEL estimator for are very close, whereas the MSEs of the DRM estimator are significantly smaller than those of the other two estimators. For instance, the MSE of is less than 25% of the MSEs of and when the simulated samples come from distributions with and .

We conducted additional simulations with and ; the results show similar patterns and are presented in the Supplementary Material.

3.2 Performance of confidence intervals

We examine and compare the performance of the following confidence intervals for the Gini indices in the simulation studies:

-

–

NA-EMP: Wald-type CIs based on the normal approximation (Qin et al., 2010);

-

–

BT-EMP: bootstrap-t CIs (Qin et al., 2010);

-

–

EL: ELR-based CIs (Qin et al., 2010);

-

–

BT-EL: bootstrap ELR-based CIs (Qin et al., 2010);

- –

- –

-

–

NA-DRM: Wald-type CIs based on the normal approximation under the DRM;

-

–

BT-DRM: bootstrap-t CIs under the DRM.

The EL method, to our best knowledge, has not been used to construct CIs for the difference of two Gini indices in the existing literature. Hence, we consider all the methods, except for EL and BT-EL, in our comparisons of the CIs for the parameter . For those calibrated by the bootstrap method, we used 1,000 nonparametric bootstrap samples drawn from the original sample with replacement.

Three combinations of are considered for the zero population proportions: , , . We evaluate the performance of a CI in terms of the coverage probability (CP) and the average length (AL). Tables 3 and 4 contain the simulated results for the CIs of and under different settings. The simulated results for the CIs of are shown in Table 5.

| (100,100) | (300,300) | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| CP | AL | CP | AL | CP | AL | CP | AL | ||

| (0,0) | NA-EMP | 93.85 | 0.100 | 94.20 | 0.092 | 94.60 | 0.059 | 94.80 | 0.054 |

| BT-EMP | 94.10 | 0.103 | 94.75 | 0.094 | 94.85 | 0.059 | 95.05 | 0.054 | |

| EL | 93.85 | 0.100 | 94.20 | 0.091 | 94.55 | 0.059 | 94.80 | 0.054 | |

| BT-EL | 94.45 | 0.103 | 95.10 | 0.095 | 94.90 | 0.059 | 94.95 | 0.054 | |

| JEL | 94.45 | 0.102 | 94.85 | 0.094 | 94.70 | 0.059 | 95.15 | 0.054 | |

| AJEL | 94.80 | 0.105 | 95.50 | 0.096 | 94.90 | 0.060 | 95.30 | 0.055 | |

| NA-DRM | 95.25 | 0.074 | 94.65 | 0.078 | 94.70 | 0.043 | 94.70 | 0.045 | |

| BT-DRM | 95.55 | 0.075 | 95.00 | 0.079 | 94.55 | 0.043 | 94.55 | 0.046 | |

| (0.3,0.3) | NA-EMP | 93.80 | 0.132 | 93.65 | 0.134 | 94.60 | 0.077 | 94.05 | 0.079 |

| BT-EMP | 95.30 | 0.135 | 94.55 | 0.137 | 95.20 | 0.077 | 94.40 | 0.079 | |

| EL | 93.75 | 0.131 | 93.65 | 0.134 | 94.60 | 0.077 | 94.00 | 0.078 | |

| BT-EL | 94.50 | 0.136 | 94.85 | 0.139 | 94.65 | 0.078 | 94.55 | 0.079 | |

| JEL | 94.45 | 0.137 | 93.80 | 0.141 | 94.50 | 0.078 | 94.55 | 0.080 | |

| AJEL | 95.35 | 0.141 | 94.20 | 0.144 | 94.80 | 0.079 | 94.80 | 0.081 | |

| NA-DRM | 95.10 | 0.120 | 94.35 | 0.130 | 95.45 | 0.070 | 94.90 | 0.076 | |

| BT-DRM | 95.75 | 0.121 | 94.65 | 0.130 | 95.25 | 0.070 | 94.65 | 0.075 | |

| (0.7,0.7) | NA-EMP | 92.20 | 0.113 | 92.95 | 0.119 | 94.90 | 0.067 | 93.90 | 0.070 |

| BT-EMP | 96.75 | 0.122 | 96.55 | 0.128 | 96.30 | 0.068 | 95.40 | 0.072 | |

| EL | 92.35 | 0.111 | 92.90 | 0.117 | 95.15 | 0.067 | 93.75 | 0.070 | |

| BT-EL | 94.70 | 0.120 | 95.30 | 0.127 | 95.75 | 0.069 | 94.55 | 0.072 | |

| JEL | 90.75 | 0.123 | 90.80 | 0.129 | 94.00 | 0.069 | 93.00 | 0.072 | |

| AJEL | 91.35 | 0.127 | 91.55 | 0.133 | 94.25 | 0.070 | 93.10 | 0.073 | |

| NA-DRM | 94.50 | 0.111 | 94.85 | 0.121 | 95.10 | 0.065 | 95.20 | 0.071 | |

| BT-DRM | 95.40 | 0.113 | 95.90 | 0.123 | 95.45 | 0.064 | 95.60 | 0.070 | |

| (100,100) | (300,300) | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| CP | AL | CP | AL | CP | AL | CP | AL | ||

| (0,0) | NA-EMP | 93.85 | 0.110 | 93.50 | 0.111 | 94.65 | 0.065 | 94.45 | 0.065 |

| BT-EMP | 94.35 | 0.115 | 94.05 | 0.115 | 94.75 | 0.065 | 94.75 | 0.065 | |

| EL | 93.90 | 0.110 | 93.50 | 0.110 | 94.65 | 0.065 | 94.55 | 0.065 | |

| BT-EL | 94.50 | 0.113 | 94.00 | 0.113 | 94.80 | 0.065 | 94.60 | 0.065 | |

| JEL | 94.35 | 0.113 | 93.90 | 0.113 | 94.90 | 0.065 | 94.55 | 0.065 | |

| AJEL | 94.95 | 0.115 | 94.35 | 0.116 | 95.10 | 0.066 | 94.75 | 0.066 | |

| NA-DRM | 94.80 | 0.100 | 94.05 | 0.079 | 93.95 | 0.059 | 95.20 | 0.045 | |

| BT-DRM | 94.45 | 0.104 | 94.75 | 0.079 | 93.65 | 0.060 | 94.95 | 0.045 | |

| (0.3,0.3) | NA-EMP | 93.55 | 0.127 | 94.25 | 0.128 | 94.55 | 0.075 | 93.45 | 0.075 |

| BT-EMP | 95.35 | 0.132 | 94.90 | 0.132 | 94.70 | 0.075 | 93.80 | 0.075 | |

| EL | 93.60 | 0.126 | 94.10 | 0.127 | 94.70 | 0.075 | 93.30 | 0.075 | |

| BT-EL | 94.75 | 0.131 | 94.85 | 0.132 | 95.05 | 0.076 | 93.70 | 0.076 | |

| JEL | 93.80 | 0.132 | 94.55 | 0.133 | 94.65 | 0.076 | 93.65 | 0.076 | |

| AJEL | 94.50 | 0.136 | 95.15 | 0.136 | 95.00 | 0.076 | 93.80 | 0.076 | |

| NA-DRM | 95.55 | 0.124 | 94.95 | 0.112 | 95.15 | 0.073 | 94.60 | 0.065 | |

| BT-DRM | 95.45 | 0.125 | 95.30 | 0.112 | 94.60 | 0.072 | 94.60 | 0.064 | |

| (0.7,0.7) | NA-EMP | 91.40 | 0.104 | 92.15 | 0.105 | 94.60 | 0.062 | 94.55 | 0.062 |

| BT-EMP | 96.30 | 0.114 | 95.70 | 0.115 | 95.85 | 0.064 | 95.50 | 0.064 | |

| EL | 92.05 | 0.102 | 92.35 | 0.102 | 94.70 | 0.062 | 94.55 | 0.062 | |

| BT-EL | 95.00 | 0.110 | 94.20 | 0.111 | 95.40 | 0.064 | 95.25 | 0.064 | |

| JEL | 90.40 | 0.114 | 91.00 | 0.114 | 94.30 | 0.064 | 93.95 | 0.064 | |

| AJEL | 90.85 | 0.117 | 91.60 | 0.118 | 94.40 | 0.064 | 94.05 | 0.064 | |

| NA-DRM | 94.65 | 0.109 | 93.90 | 0.101 | 96.10 | 0.064 | 95.40 | 0.059 | |

| BT-DRM | 95.80 | 0.109 | 95.55 | 0.102 | 95.65 | 0.062 | 95.95 | 0.058 | |

When the sample sizes are , we can see from Tables 3 and 4 that the NA-EMP and EL CIs for and tend to be narrow and have lower CPs, especially when the proportions of zero values are large, i.e., . With the help of bootstrap calibration, the BT-EMP and BT-EL CIs achieve better performance in terms of CP. However, when , the BT-EMP CIs have slight overcoverage with inflated ALs. The AJEL CIs always have the longest ALs, and the JEL CIs are only slightly shorter. Moreover, when and , the CPs of the JEL and AJEL CIs are close to the nominal level of 95%. The JEL and AJEL CIs suffer from undercoverage when . The NA-DRM CIs have the shortest ALs, and their CPs are very close to the 95% nominal level in all cases. This is strong evidence that using DRMs improves the performance of the CIs. The bootstrap calibration does little to improve the CIs: the performances of the NA-DRM and BT-DRM CIs are similar.

When the sample sizes increase to , the performance of all the CIs becomes satisfactory in terms of CP. The NA-DRM and BT-DRM CIs always have the shortest ALs, and there is little variation among the ALs of the other CIs.

Since the Gini index ranges from 0 to 1, a logit transformation may improve the performance of the CIs for and under the DRM. However, the results (reported in the Supplementary Material) show that the transformation does not provide any significant improvement.

| (100,100) | (300,300) | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| CP | AL | CP | AL | CP | AL | CP | AL | ||

| (0,0) | NA-EMP | 92.69 | 0.137 | 94.90 | 0.157 | 94.65 | 0.079 | 95.15 | 0.092 |

| BT-EMP | 92.89 | 0.139 | 94.80 | 0.161 | 94.35 | 0.080 | 95.15 | 0.092 | |

| JEL | 93.84 | 0.142 | 95.80 | 0.164 | 95.00 | 0.081 | 95.55 | 0.093 | |

| AJEL | 94.54 | 0.144 | 96.05 | 0.166 | 95.20 | 0.081 | 95.75 | 0.094 | |

| NA-DRM | 94.44 | 0.070 | 94.95 | 0.092 | 94.65 | 0.041 | 94.70 | 0.055 | |

| BT-DRM | 92.94 | 0.069 | 94.95 | 0.092 | 93.80 | 0.041 | 94.65 | 0.054 | |

| (0.3,0.3) | NA-EMP | 94.19 | 0.188 | 93.05 | 0.181 | 95.00 | 0.110 | 94.65 | 0.106 |

| BT-EMP | 94.54 | 0.191 | 93.45 | 0.184 | 95.00 | 0.110 | 94.65 | 0.106 | |

| JEL | 95.45 | 0.202 | 94.75 | 0.195 | 95.55 | 0.113 | 95.35 | 0.108 | |

| AJEL | 95.70 | 0.205 | 95.10 | 0.198 | 95.55 | 0.113 | 95.55 | 0.109 | |

| NA-DRM | 94.24 | 0.165 | 94.30 | 0.149 | 95.00 | 0.096 | 95.05 | 0.087 | |

| BT-DRM | 93.34 | 0.161 | 93.45 | 0.146 | 94.35 | 0.094 | 94.60 | 0.086 | |

| (0.7,0.7) | NA-EMP | 93.20 | 0.164 | 94.29 | 0.148 | 94.05 | 0.097 | 94.90 | 0.088 |

| BT-EMP | 93.65 | 0.170 | 94.14 | 0.153 | 94.05 | 0.098 | 94.90 | 0.089 | |

| JEL | 96.65 | 0.188 | 97.65 | 0.175 | 95.20 | 0.101 | 95.95 | 0.092 | |

| AJEL | 96.90 | 0.192 | 98.00 | 0.179 | 95.50 | 0.102 | 96.05 | 0.093 | |

| NA-DRM | 95.55 | 0.162 | 96.19 | 0.138 | 95.60 | 0.094 | 95.70 | 0.080 | |

| BT-DRM | 93.40 | 0.153 | 94.49 | 0.133 | 94.60 | 0.090 | 95.10 | 0.078 | |

We now discuss the simulation results for the CIs of the difference presented in Table 5. We observe that the NA-EMP and BT-EMP CIs have similar performance; their performance is acceptable except when the simulated samples are from distributions with and . In this case, the CPs of the NA-EMP and BT-EMP CIs are below the 95% nominal level. The JEL and AJEL CIs always have the longest ALs. They experience overcoverage in some cases, especially when the proportions of zero values are high. The BT-DRM CIs have the shortest ALs, which leads to undercoverage in some cases. The performance of the NA-DRM CIs is consistently satisfactory in terms of CP and AL.

We also conduct additional simulations with and ; the results display similar patterns and are presented in the Supplementary Material.

3.3 Performance of tests on the equality of two Gini indices

In this section, we examine the performance of our proposed semiparametric test for testing the equality of the two Gini indices, i.e., , with comparisons to other existing methods. We consider the following tests:

-

–

NA-EMP: Wald-type test based on the normal approximation of (Qin et al., 2010);

-

–

NL-EMP: Wald-type test based on the normal approximation of ;

-

–

JEL: jackknife ELR test (Wang & Zhao, 2016);

-

–

AJEL: adjusted jackknife ELR test (Wang & Zhao, 2016);

-

–

NA-DRM: Wald-type test based on the normal approximation of under the DRM;

-

–

NL-DRM: Wald-type test based on the normal approximation of under the DRM.

Several combinations of are chosen to satisfy the null hypothesis or the alternative hypothesis . The details are presented in Table 6. Tables 7 and 8 give the simulated type I error rate and simulated power of each test at the 5% significance level.

| Null hypothesis | ||||||

| (0,0.079) | (0.3,0.355) | (0.7,0.724) | (0,0) | (0.3,0.3) | (0.7,0.7) | |

| Alternative hypothesis | ||||||

| (0,0) | (0.1,0.3) | (0.4,0.65) | (0.1,0.3) | (0.3,0.45) | (0.5,0.4) | |

| 0.049 | -0.081 | -0.127 | -0.100 | -0.075 | 0.050 | |

| 0.206 | -0.323 | -0.633 | -0.418 | -0.350 | 0.251 | |

| (0,0.079) | (0.3,0.355) | (0.7,0.724) | (0,0) | (0.3,0.3) | (0.7,0.7) | ||

|---|---|---|---|---|---|---|---|

| (100,100) | NA-EMP | 5.50 | 5.00 | 7.10 | 5.55 | 4.85 | 6.90 |

| NL-EMP | 5.45 | 4.85 | 6.40 | 5.50 | 4.70 | 6.30 | |

| JEL | 4.55 | 4.05 | 3.70 | 4.85 | 3.10 | 2.70 | |

| AJEL | 4.15 | 3.85 | 3.45 | 4.45 | 2.70 | 2.40 | |

| NA-DRM | 4.90 | 5.15 | 5.15 | 5.05 | 4.70 | 5.20 | |

| NL-DRM | 4.85 | 4.80 | 4.75 | 4.95 | 4.65 | 4.95 | |

| (300,300) | NA-EMP | 5.10 | 5.70 | 5.70 | 6.15 | 5.35 | 5.55 |

| NL-EMP | 5.10 | 5.70 | 5.70 | 6.15 | 5.35 | 5.55 | |

| JEL | 4.90 | 5.35 | 5.10 | 5.70 | 4.85 | 4.20 | |

| AJEL | 4.80 | 5.20 | 4.80 | 5.55 | 4.80 | 4.00 | |

| NA-DRM | 5.05 | 4.90 | 4.90 | 5.25 | 5.30 | 5.15 | |

| NL-DRM | 5.05 | 4.85 | 4.95 | 5.25 | 5.25 | 5.05 | |

From Table 7, we observe that the type I error rates for NA-DRM are stable and close to the 5% significance level in all cases. The type I error rates for NL-DRM are similar to those for NA-DRM when the sample sizes are and smaller when . This implies that the logit transformation of the Gini indices is unnecessary for the equality test. The type I error rates for NA-EMP and NL-EMP show similar trends. When the sample sizes are and the proportions of zero values are high, NA-EMP, NL-EMP, JEL, and AJEL have either inflated or conservative type I error rates. Large sample sizes seem to improve their performance.

| (0,0) | (0.1,0.3) | (0.4,0.65) | (0.1,0.3) | (0.3,0.45) | (0.5,0.4) | ||

|---|---|---|---|---|---|---|---|

| (100,100) | NA-EMP | 30.15 | 43.45 | 78.05 | 59.65 | 38.20 | 18.50 |

| NL-EMP | 30.00 | 42.95 | 76.95 | 59.10 | 37.40 | 18.15 | |

| JEL | 28.85 | 42.90 | 75.70 | 58.00 | 33.75 | 14.90 | |

| AJEL | 28.00 | 42.05 | 74.85 | 56.95 | 32.75 | 14.00 | |

| NA-DRM | 82.60 | 58.35 | 83.20 | 80.75 | 50.05 | 23.20 | |

| NL-DRM | 82.45 | 58.05 | 82.25 | 80.45 | 49.95 | 22.05 | |

| (300,300) | NA-EMP | 67.30 | 85.80 | 99.75 | 97.00 | 79.85 | 45.90 |

| NL-EMP | 67.30 | 85.70 | 99.70 | 96.90 | 79.50 | 45.50 | |

| JEL | 66.90 | 86.10 | 99.65 | 97.10 | 79.05 | 44.70 | |

| AJEL | 66.50 | 85.85 | 99.65 | 96.85 | 78.60 | 44.05 | |

| NA-DRM | 99.95 | 95.70 | 99.85 | 99.90 | 90.75 | 56.90 | |

| NL-DRM | 99.95 | 95.70 | 99.80 | 99.90 | 90.80 | 55.75 | |

We observe from Table 8 that NA-DRM always gives the largest testing powers. The performance of NL-DRM is comparable to NA-DRM. When the true difference of the Gini indices is large, the testing powers of NA-DRM and NL-DRM are significantly larger than those of the other methods. For example, when the simulated samples are from the distributions with and , the testing powers of NA-DRM and NL-DRM are more than twice the others.

4 Real-Data Applications

In this section, we apply our proposed methods to analyze two real datasets. Each dataset can be viewed as consisting of two samples from two different populations, and we are interested in computing the point estimates as well as the construction of confidence intervals for the Gini indices and their difference. The populations for the first dataset contain a large proportions of zeros and the study variables for the second dataset are strictly positive.

The first dataset (Zhou & Cheng, 2008) is from a clinical drug utilization study of patients with uncomplicated hypertension, originally conducted by Murray et al. (2004). It consists of the inpatient charges of 483 patients by gender. We label the charges of the 282 male patients as sample 0 and those of the 201 female patients as sample 1. In most cases, uncomplicated hypertension can be controlled if the patients follow guidelines and take antihypertensive drugs regularly. If they do not need inpatient treatment, the corresponding charges are zero. There are 253 zero values (89.7%) im sample 0 and 171 (85.0%) in sample 1.

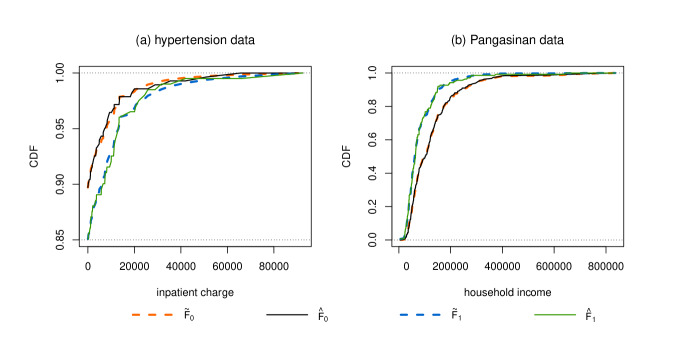

To analyze the dataset with our proposed method, we need to choose an appropriate in the DRM (3). The dataset is highly skewed to the right because of the high proportions of zero values and extra skewness in the positive inpatient charges. To balance model fit and model complexity, we choose . The goodness-of-fit test of Qin & Zhang (1997) gives a p-value of 0.563, which indicates that this is a suitable choice. Figure 1(a) shows the fitted population distribution functions and under the DRM with together with the empirical CDFs and . Clearly, the fit is adequate.

We apply the methods discussed in Sections 3.1 and 3.2 to this dataset. Table 9 presents the point estimates, and Table 10 shows the lower bound (LB), upper bound (UB), and length of the 95% CIs. The estimates of , , and for all three methods are very close. In particular, the EMP and JEL estimates are almost the same. The estimates of and are greater than 0.93, indicating the large inequality of the inpatient charge for patients with uncomplicated hypertension; the high proportion of zero values contributes to this. All the methods give similar 95% CIs for . The 95% CIs for and for NA-DRM and BT-DRM are the shortest. All the CIs for contain 0, which suggests no significant difference between the inequality of the inpatient charge for female and male patients at the 95% confidence level.

| (male) | (female) | ||

|---|---|---|---|

| EMP | 0.959 | 0.933 | 0.026 |

| JEL | 0.959 | 0.933 | 0.026 |

| DRM | 0.956 | 0.934 | 0.022 |

| (male) | (female) | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| LB | UB | Length | LB | UB | Length | LB | UB | Length | |

| NA-EMP | 0.942 | 0.977 | 0.035 | 0.902 | 0.964 | 0.062 | -0.009 | 0.062 | 0.071 |

| BT-EMP | 0.936 | 0.974 | 0.039 | 0.888 | 0.959 | 0.071 | -0.013 | 0.066 | 0.078 |

| EL | 0.941 | 0.975 | 0.034 | 0.903 | 0.961 | 0.058 | – | – | – |

| BT-EL | 0.938 | 0.976 | 0.038 | 0.897 | 0.966 | 0.068 | – | – | – |

| JEL | 0.942 | 0.980 | 0.038 | 0.904 | 0.967 | 0.063 | -0.017 | 0.069 | 0.086 |

| AJEL | 0.942 | 0.981 | 0.039 | 0.904 | 0.967 | 0.064 | -0.018 | 0.069 | 0.087 |

| NA-DRM | 0.938 | 0.974 | 0.036 | 0.906 | 0.961 | 0.056 | -0.009 | 0.054 | 0.063 |

| BT-DRM | 0.934 | 0.972 | 0.038 | 0.901 | 0.957 | 0.056 | -0.007 | 0.048 | 0.055 |

The second dataset comes from the 1997 Family and Income and Expenditure Survey conducted by the Philippine Statistics Authority; the metadata is available in the R package ineq. The province of Pangasinan is located in the Ilocos Region of Luzon. The dataset contains household incomes from different areas of Pangasinan: urban (Sample 0) and rural (Sample 1). Sample 0 has 245 observations and sample 1 has 138 observations. All the incomes are positive.

The skewness of the dataset suggests setting in the DRM (3). The goodness-of-fit test of Qin & Zhang (1997) gives a p-value 0.607. Hence, there is no strong evidence to reject the choice of . Figure 1(b) also shows that the DRM with fits the data well.

We use all the methods of Sections 3.1 and 3.2 to analyze the dataset and summarize the results in Tables 11 and 12. The EMP and JEL methods give similar estimates of , , and . The DRM estimate of is comparable to the other estimates, while the DRM estimate of is smaller than the others. Hence, the DRM estimate of is larger. All the methods give similar results for the 95% CIs for . The 95% CIs for and by NA-DRM and BT-DRM are significantly shorter than the other CIs. This is strong evidence that our method helps to utilize information across the two samples and effectively improves inference when sample sizes are small or moderate. We do not reject the hypothesis that the income inequalities of urban and rural households are the same, since all the 95% CIs for contain 0.

| (urban) | (rural) | ||

|---|---|---|---|

| EMP | 0.393 | 0.394 | -0.001 |

| JEL | 0.391 | 0.389 | 0.002 |

| DRM | 0.399 | 0.371 | 0.028 |

| (urban) | (rural) | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| LB | UB | Length | LB | UB | Length | LB | UB | Length | |

| NA-EMP | 0.354 | 0.433 | 0.079 | 0.332 | 0.455 | 0.123 | -0.074 | 0.073 | 0.146 |

| BT-EMP | 0.356 | 0.441 | 0.085 | 0.338 | 0.481 | 0.143 | -0.085 | 0.068 | 0.153 |

| EL | 0.354 | 0.433 | 0.079 | 0.333 | 0.456 | 0.123 | – | – | – |

| BT-EL | 0.353 | 0.434 | 0.080 | 0.335 | 0.455 | 0.120 | – | – | – |

| JEL | 0.356 | 0.436 | 0.081 | 0.339 | 0.466 | 0.127 | -0.083 | 0.070 | 0.153 |

| AJEL | 0.355 | 0.437 | 0.081 | 0.338 | 0.467 | 0.129 | -0.084 | 0.071 | 0.154 |

| NA-DRM | 0.361 | 0.436 | 0.075 | 0.343 | 0.399 | 0.055 | -0.003 | 0.059 | 0.062 |

| BT-DRM | 0.359 | 0.443 | 0.084 | 0.343 | 0.403 | 0.060 | -0.006 | 0.057 | 0.063 |

5 Concluding Remarks

We have proposed new semiparametric inference procedures for the Gini indices of two semicontinuous populations. Under the mixture model (1) and the DRM (3), we proposed the MELEs of the Gini indices and and established the asymptotic normality of the MELEs. Our methods are applicable whether or not there are excess zero values. We showed numerically and theoretically that our MELEs are more efficient than fully nonparametric estimators. We also explored the asymptotic properties of a general function of two Gini indices, and used the difference of the two Gini indices as an illustrating example. We used the asymptotic results to construct CIs and perform hypothesis tests for , , and . Simulation studies demonstrated that the CIs under the DRM have superior performance in terms of coverage accuracy and average length. Moreover, our method has a higher testing power than existing methods.

ELR-based CIs are range-preserving. It would be interesting to construct ELR-based CIs for Gini indices under the DRM, but the theoretical development may be technically challenging. Qin et al. (2010) investigated inference on the Gini index of a population under stratified random sampling. We could use the DRM to link the distributions of the subpopulations in all strata and then develop an inference procedure for the Gini index of the whole population. Correlated data is also of interest: Peng (2011) and Wang & Zhao (2016) compared the Gini indices of paired data. The DRM would be useful for modeling the marginal distributions of paired data and improving the efficiency of the estimation of the Gini indices. We leave these topics to future research.

References

- Anand (1983) Anand, S. (1983). Inequality and poverty in Malaysia: Measurement and decomposition. Report 9268, The World Bank.

- Anderson (1979) Anderson, J. A. (1979). Multivariate logistic compounds. Biometrika, 66, 17–26.

- Bonetti et al. (2009) Bonetti, M., Gigliarano, C., & Muliere, P. (2009). The Gini concentration test for survival data. Lifetime Data Analysis, 15, 493–518.

- Cai & Chen (2018) Cai, S. & Chen, J. (2018). Empirical likelihood inference for multiple censored samples. The Canadian Journal of Statistics, 46, 212–232.

- Cai et al. (2017) Cai, S., Chen, J., & Zidek, J. V. (2017). Hypothesis testing in the presence of multiple samples under density ratio models. Statistica Sinica, 27, 761–783.

- Chen et al. (2016) Chen, B., Li, P., Qin, J., & Yu, T. (2016). Using a monotonic density ratio model to find the asymptotically optimal combination of multiple diagnostic tests. Journal of the American Statistical Association, 111, 861–874.

- Chen et al. (2021) Chen, J., Li, P., Liu, Y., & Zidek, J. V. (2021). Composite empirical likelihood for multisample clustered data. Journal of Nonparametric Statistics, 33, 60–81.

- Chen & Liu (2013) Chen, J. & Liu, Y. (2013). Quantile and quantile-function estimations under density ratio model. The Annals of Statistics, 41, 1669–1692.

- Cowell (2011) Cowell, F. (2011). Measuring Inequality. Oxford: Oxford University Press.

- David (1968) David, H. (1968). Miscellanea: Gini’s mean difference rediscovered. Biometrika, 55, 573–575.

- Davidson (2009) Davidson, R. (2009). Reliable inference for the Gini index. Journal of Econometrics, 150, 30–40.

- Fokianos et al. (2001) Fokianos, K., Kedem, B., Qin, J., & Short, D. A. (2001). A semiparametric approach to the one-way layout. Technometrics, 43, 56–65.

- Gastwirth (1972) Gastwirth, J. L. (1972). The estimation of the Lorenz curve and Gini index. The Review of Economics and Statistics, 54, 306–316.

- Giles (2004) Giles, D. E. (2004). Calculating a standard error for the Gini coefficient: Some further results. Oxford Bulletin of Economics and Statistics, 66, 425–433.

- Gini (1912) Gini, C. (1912). Variabilità e mutabilità: contributo allo studio delle distribuzioni e delle relazioni statistiche. Bologna: Tipogr. di P. Cuppini.

- Hoeffding (1948) Hoeffding, W. (1948). A class of statistics with asymptotically normal distribution. The Annals of Mathematical Statistics, 19, 293–325.

- Jiang & Tu (2012) Jiang, S. & Tu, D. (2012). Inference on the probability as a measurement of treatment effect under a density ratio model and random censoring. Computational Statistics & Data Analysis, 56, 1069–1078.

- Karagiannis & Kovacevic (2000) Karagiannis, E. & Kovacevic, M. (2000). A method to calculate the jackknife variance estimator for the Gini coefficient. Oxford Bulletin of Economics and Statistics, 62, 119–122.

- Lorenz (1905) Lorenz, M. O. (1905). Methods of measuring the concentration of wealth. Publications of the American Statistical Association, 9, 209–219.

- Lv et al. (2017) Lv, X., Zhang, G., & Ren, G. (2017). Gini index estimation for lifetime data. Lifetime Data Analysis, 23, 275–304.

- Modarres & Gastwirth (2006) Modarres, R. & Gastwirth, J. L. (2006). A cautionary note on estimating the standard error of the Gini index of inequality. Oxford Bulletin of Economics and Statistics, 68, 385–390.

- Moothathu (1985) Moothathu, T. (1985). Distributions of maximum likelihood estimators of Lorenz curve and Gini index of exponential distribution. Annals of the Institute of Statistical Mathematics, 37, 473–479.

- Moothathu (1989) Moothathu, T. (1989). On unbiased estimation of Gini index and Yntema-Pietra index of lognormal distribution and their variances. Communications in Statistics - Theory and Methods, 18, 661–672.

- Moothathu (1990) Moothathu, T. (1990). The best estimator and a strongly consistent asymptotically normal unbiased estimator of Lorenz curve Gini index and Theil entropy index of Pareto distribution. Sankhyā: The Indian Journal of Statistics, Series B, 52, 115–127.

- Murray et al. (2004) Murray, M. D., Harris, L. E., Overhage, J. M., Zhou, X.-H., Eckert, G. J., Smith, F. E., Buchanan, N. N., Wolinsky, F. D., McDonald, C. J., & Tierney, W. M. (2004). Failure of computerized treatment suggestions to improve health outcomes of outpatients with uncomplicated hypertension: Results of a randomized controlled trial. Pharmacotherapy: The Journal of Human Pharmacology and Drug Therapy, 24, 324–337.

- Ogwang (2000) Ogwang, T. (2000). A convenient method of computing the Gini index and its standard error. Oxford Bulletin of Economics and Statistics, 62, 123–129.

- Owen (2001) Owen, A. (2001). Empirical Likelihood. New York: CRC Press.

- Peng (2011) Peng, L. (2011). Empirical likelihood methods for the Gini index. Australian & New Zealand Journal of Statistics, 53, 131–139.

- Qin (2017) Qin, J. (2017). Biased Sampling, Over-identified Parameter Problems and Beyond. Singapore: Springer.

- Qin & Zhang (1997) Qin, J. & Zhang, B. (1997). A goodness-of-fit test for logistic regression models based on case-control data. Biometrika, 84, 609–618.

- Qin & Zhang (2003) Qin, J. & Zhang, B. (2003). Using logistic regression procedures for estimating receiver operating characteristic curves. Biometrika, 90, 585–596.

- Qin et al. (2015) Qin, J., Zhang, H., Li, P., Albanes, D., & Yu, K. (2015). Using covariate-specific disease prevalence information to increase the power of case-control studies. Biometrika, 102, 169–180.

- Qin et al. (2010) Qin, Y., Rao, J., & Wu, C. (2010). Empirical likelihood confidence intervals for the Gini measure of income inequality. Economic Modelling, 27, 1429–1435.

- Wang et al. (2017) Wang, C., Marriott, P., & Li, P. (2017). Testing homogeneity for multiple nonnegative distributions with excess zero observations. Computational Statistics & Data Analysis, 114, 146–157.

- Wang et al. (2018) Wang, C., Marriott, P., & Li, P. (2018). Semiparametric inference on the means of multiple nonnegative distributions with excess zero observations. Journal of Multivariate Analysis, 166, 182–197.

- Wang & Zhao (2016) Wang, D. & Zhao, Y. (2016). Jackknife empirical likelihood for comparing two Gini indices. The Canadian Journal of Statistics, 44, 102–119.

- Wang et al. (2016) Wang, D., Zhao, Y., & Gilmore, D. W. (2016). Jackknife empirical likelihood confidence interval for the Gini index. Statistics & Probability Letters, 110, 289–295.

- Yitzhaki (1991) Yitzhaki, S. (1991). Calculating jackknife variance estimators for parameters of the Gini method. Journal of Business & Economic Statistics, 9, 235–239.

- Yuan et al. (2021) Yuan, M., Li, P., & Wu, C. (2021). Semiparametric inference of the Youden index and the optimal cut-off point under density ratio models. The Canadian Journal of Statistics. DOI 10.1002/cjs.11600.

- Yuan et al. (2020) Yuan, M., Wang, C., Lin, B., & Li, P. (2020). Semiparametric inference on general functionals of two semicontinuous populations. arXiv:2012.07092.

- Zhou & Cheng (2008) Zhou, X.-H. & Cheng, H. (2008). A computer program for estimating the re-transformed mean in heteroscedastic two-part models. Computer Methods and Programs in Biomedicine, 90, 210–216.

- Zhou & Tu (1999) Zhou, X.-H. & Tu, W. (1999). Comparison of several independent population means when their samples contain log-normal and possibly zero observations. Biometrics, 55, 645–651.

- Zhou & Tu (2000) Zhou, X.-H. & Tu, W. (2000). Interval estimation for the ratio in means of log-normally distributed medical costs with zero values. Computational Statistics & Data Analysis, 35, 201–210.

Supplementary material for

“Semiparametric inference on Gini indices of two semicontinuous populations under density ratio models”

This document of supplementary material provides further details for the paper entitled “Semiparametric inference on Gini indices of two semicontinuous populations under density ratio models”. It contains the proofs of Theorems 1–4 in the main paper and additional simulation results. The basic setting and some useful lemmas are presented in Section 1. The proofs and technical details for Theorems 1–4 are given in Sections 2–5. Section 6 contains some additional simulation results.

1 The basic setting and useful lemmas

Recall that

| (S.1) |

where is the proportion of zeros in sample , is the sample size for sample , is an indicator function, and is the cumulative distribution function (CDF) of the positive observations in sample . We link and via a density ratio model (DRM):

| (S.2) |

for the unknown parameter and with a -dimensional, prespecified, nontrivial basis function.

Recall that and are the (random) numbers of zero observations and positive observations, respectively, in sample . Clearly, , for . Without loss of generality, we assume that the first observations in group , , are positive, and the remaining observations are 0. Let be the total (fixed) sample size, i.e., .

We further let . The maximum empirical likelihood estimators (MELEs) of and respectively maximize and , where

and

with being a random variable. That is,

| (S.3) |

Once is obtained, we have

Note that , which ensures that the MELE of is a CDF. The MELEs of and for are

| (S.4) |

For convenience of presentation, we recall and introduce some notation. We use and to denote the true values of and . Let , for , and

Note that , , , and depend on and/or and . Henceforth, we use and to denote summation over the full range of data.

1.1 Alternative form of Gini index

According to David (1968), the Gini’s mean difference for sample can be equivalently expressed by

Under model (S.1), . Then can be further written as

Let and . We then have and

With the definition of and , and the MELEs of CDFs ’s in (S.4), the MELEs of and are as follows:

The MELEs of the two Gini indices are given by

| (S.5) |

1.2 Some useful lemmas

We present several useful lemmas in preparation for the proofs in Sections 2–5. The first lemma considers the expectation of summations.

Lemma 1.

Suppose that is an arbitrary vector-valued function. Let represent the expectation operator with respect to and be a random variable from . Then

Proof.

Under the DRM ( S.2),

Since and using the definitions of and , we further have

Recalling that , we have

This completes the proof.

Yuan et al. (2020) define a general parameter vector of length :

| (S.6) |

where is a given dimensional function. The MELE of is given by

| (S.7) |

The following lemmas provide the approximation of the MELE and its asymptotic property. These lemmas help to develop the asymptotic property of the MELEs of the Gini indices.

Lemma 2.

Assume that Conditions C1–C3 are satisfied and the true value for . Let be the true value of and . Then

| (S.8) |

where with

Lemma 3.

2 Proof of Theorem 1

2.1 Approximations of and

To develop the asymptotic properties of , we first find the linear approximations of and . We start with .

Recall that

The MELE is then given by

Note that is a function of , and hence we define

We then have . With the definition of and , we have

and .

By Theorem 1 of Yuan et al. (2020), we have . Applying the first-order Taylor expansion gives

| (S.9) |

Define

for and . We then rewrite as

Note that is a von Mises statistic (Mises, 1947). We denote the associated U-statistic by

According to Serfling (1980), the projection of is defined as

where . It follows from Serfling (1980, p. 190 & p. 206) that under Condition C4,

This leads to

When , is a two-sample U-statistic. Define , , and . From Theorem 12.6 in Van der Vaart (2000), we have

Since

we have

Hence,

| (S.10) | |||||

We now simplify each term in (S.10). With Lemma 1 and the definition of , we have

Hence,

Using the result in Lemma 1, we have

We move to the second term of in (S.10). Recall that

We then have

This leads to

Similarly, with the definition of , we have

Note that

Together with the result of Lemma 1, we have

For , we define the function

The approximation of is then given by

We also need the first derivative of when finding the approximation of . We take the first derivative of with respect to and evaluate the derivative at the true value . This leads to

By the law of large numbers, we have

with .

Since , we have

For ,

The expression for can be found in a similar manner:

The details are omitted here.

It can be verified that the matrix is the same as the matrix in (S.8) when we set in (S.6). According to Lemma 2, the expression in (S.9) can be further written as

| (S.12) | |||||

The remaining term is introduced by the projection of the von Mises statistic and the U-statistic when approximating .

Next, we consider the approximation of MELE . Recall that

With the definition of , the MELE can be written as

| (S.14) | |||||

Define

for . We use to denote and have

Note that is a von Mises statistic and is a two-sample U-statistic. Using the technique used to obtain the approximation of in (S.10), we have

where , , and .

Hence, is given by

where for .

Applying the first-order Taylor expansion to in (S.14) yields

With the law of large numbers, we have

with and

The expression of each element in can be found similarly to the derivation of ; we omit the details. By setting in (S.6), we can verify that the matrix is the same as the matrix in (S.8). Hence, the approximation is given by

With Lemma 2 and the natural constraint , the above approximation equation implies

| (S.15) |

where we define for .

2.2 Asymptotic properties of and

In this section, we use the approximations of and developed in Section 2.1 and the results in Lemmas 2 and 3 to derive the asymptotic properties of and .

Note that the numerators and denominators of the leading terms in (S.16) and (S.17) all have the forms in (S.7) with taking some specific forms. We define these specific as

| (S.18) |

with

| (S.19) |

Further, we define

| (S.20) |

and

| (S.21) |

Then we have

| (S.22) |

Hence, the joint limiting distribution of is determined by that of , where the are the true values of for , and

is the true value of .

Let

Applying Lemma 3, we have, as goes to infinity,

in distribution with

| (S.23) |

where and are provided in Lemma 3, and

Note that we have used the form of in (S.18) to obtain the simplified forms of , , and .

Let . Then and . Using the Delta method, we have, as ,

in distribution, where and

| (S.24) |

To finish the proof of Theorem 1, we use the forms of in (S.23) and in (S.24) to simplify . Note that

This leads to

| (S.27) |

With the fact that

we have

Hence,

| (S.29) |

3 Proof of Theorem 2

The proof of Theorem 2 is similar to that of Theorem 1. The results of Li et al. (2018) are helpful for this proof.

4 Proof of Theorem 3

We start with (a). Recall that the nonparametric estimator of the Gini index for sample is defined as

where

After some algebra, we have

| (S.31) |

where and are the sample mean and the empirical CDF based on sample .

Applying Theorem 1 of Qin et al. (2010), we have

in distribution with

| (S.32) |

where

| (S.33) |

where means the variance is taken with respect to and with defined in (S.19).

We now show that has the form claimed in (a). Note that

| (S.34) |

where indicates that the expectation is taken with respect to . After some calculus work, we can show that

| (S.35) |

For , we have under model (S.1)

where indicates that the expectation is taken with respect to . Then

| (S.36) |

With the form of in (S.19), we have

| (S.37) |

Combining (S.34)– (S.37) gives

| (S.38) | |||||

The fact that and (S.38) together imply that in (S.33) has the following form:

where in the last step, we have used the fact that .

Recall that

and

After some algebra work, we get

| (S.39) |

and

| (S.40) |

Substituting (S.39) and (S.40) into (S.32) gives the asymptotic variance as

| (S.41) |

with

Hence, has the form claimed in (a).

We now move to (b). Since , after some algebra, we find that

Together with the expression for in (S.30), it follows that

where

| (S.43) |

Let for with

Recall that

It can be verified that for ,

5 Proof of Theorem 4

The result in Theorem 4 is a direct consequence of applying the Delta method and the results in Theorems 1 and 2.

6 Additional simulation results

6.1 Results for point estimator

Tables 1 and 2 present the additional simulated results for the point estimators of the Gini indices , , and their difference under different distributional settings. The general trends are similar to those in the main paper. The DRM method always gives the smallest mean square errors (MSEs).

| Bias | MSE | Bias | MSE | Bias | MSE | |||

|---|---|---|---|---|---|---|---|---|

| (100,100) | (0.1,0.3) | EMP | 6.13 | 0.98 | 7.43 | 1.30 | -1.30 | 2.23 |

| JEL | 0.96 | 0.96 | 3.08 | 1.28 | -2.13 | 2.28 | ||

| DRM | 2.51 | 0.67 | 3.79 | 1.10 | -1.28 | 1.40 | ||

| (0.6,0.4) | EMP | 7.15 | 1.14 | 6.00 | 1.27 | 1.15 | 2.44 | |

| JEL | 4.90 | 1.14 | 2.27 | 1.27 | 2.63 | 2.49 | ||

| DRM | 2.71 | 0.94 | 3.48 | 1.18 | -0.77 | 1.98 | ||

| (300,300) | (0.1,0.3) | EMP | 1.40 | 0.31 | 2.96 | 0.41 | -1.56 | 0.72 |

| JEL | -0.33 | 0.31 | 1.51 | 0.40 | -1.83 | 0.72 | ||

| DRM | 0.75 | 0.23 | 1.38 | 0.35 | -0.63 | 0.46 | ||

| (0.6,0.4) | EMP | 2.63 | 0.38 | 1.58 | 0.43 | 1.05 | 0.80 | |

| JEL | 1.87 | 0.38 | 0.33 | 0.43 | 1.54 | 0.81 | ||

| DRM | 1.02 | 0.32 | 0.78 | 0.41 | 0.25 | 0.66 | ||

| Bias | MSE | Bias | MSE | Bias | MSE | |||

|---|---|---|---|---|---|---|---|---|

| (100,100) | (0.1,0.3) | EMP | 4.83 | 0.99 | 4.12 | 1.08 | 0.70 | 1.95 |

| JEL | 0.33 | 0.99 | 0.63 | 1.09 | -0.30 | 1.98 | ||

| DRM | 1.63 | 0.88 | 1.61 | 0.77 | 0.02 | 1.22 | ||

| (0.6,0.4) | EMP | 6.12 | 0.95 | 3.94 | 1.12 | 2.19 | 2.04 | |

| JEL | 4.17 | 0.95 | 0.95 | 1.13 | 3.22 | 2.09 | ||

| DRM | 2.34 | 0.83 | 2.09 | 0.92 | 0.25 | 1.51 | ||

| (300,300) | (0.1,0.3) | EMP | 1.52 | 0.33 | 2.26 | 0.37 | -0.75 | 0.66 |

| JEL | 0.02 | 0.33 | 1.10 | 0.36 | -1.08 | 0.67 | ||

| DRM | 0.70 | 0.29 | 0.96 | 0.25 | -0.25 | 0.40 | ||

| (0.6,0.4) | EMP | 2.03 | 0.31 | 1.26 | 0.38 | 0.77 | 0.69 | |

| JEL | 1.37 | 0.31 | 0.27 | 0.38 | 1.11 | 0.70 | ||

| DRM | 0.83 | 0.29 | 0.45 | 0.30 | 0.39 | 0.51 | ||

6.2 Results for confidence intervals

Tables 3 and 4 contain the the complete results for the confidence intervals (CIs) of and under different distributional settings. NL-DRM and BL-DRM refer to the Wald-type CIs for or using the logit transformation under the DRM and the corresponding bootstrap-t CIs. The additional results for the CIs of are shown in Table 5. Again, the general patterns are similar to those in the main paper. The NA-DRM CIs provide accurate coverage probabilities (CPs) in all situations and have shorter average lengths (ALs) than the existing nonparametric methods. Further, the bootstrap method and logit transformation do not help to improve the coverage accuracy. Hence, we recommend using the NA-DRM CI.

| (100,100) | (300,300) | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| CP | AL | CP | AL | CP | AL | CP | AL | ||

| (0,0) | NA-EMP | 93.85 | 0.100 | 94.20 | 0.092 | 94.60 | 0.059 | 94.80 | 0.054 |

| BT-EMP | 94.10 | 0.103 | 94.75 | 0.094 | 94.85 | 0.059 | 95.05 | 0.054 | |

| EL | 93.85 | 0.100 | 94.20 | 0.091 | 94.55 | 0.059 | 94.80 | 0.054 | |

| BT-EL | 94.45 | 0.103 | 95.10 | 0.095 | 94.90 | 0.059 | 94.95 | 0.054 | |

| JEL | 94.45 | 0.102 | 94.85 | 0.094 | 94.70 | 0.059 | 95.15 | 0.054 | |

| AJEL | 94.80 | 0.105 | 95.50 | 0.096 | 94.90 | 0.060 | 95.30 | 0.055 | |

| NA-DRM | 95.25 | 0.074 | 94.65 | 0.078 | 94.70 | 0.043 | 94.70 | 0.045 | |

| BT-DRM | 95.55 | 0.075 | 95.00 | 0.079 | 94.55 | 0.043 | 94.55 | 0.046 | |

| NL-DRM | 95.35 | 0.074 | 94.50 | 0.077 | 94.75 | 0.043 | 94.75 | 0.045 | |

| BL-DRM | 95.45 | 0.075 | 94.80 | 0.079 | 94.50 | 0.043 | 94.55 | 0.045 | |

| (0.1,0.3) | NA-EMP | 94.00 | 0.116 | 93.85 | 0.134 | 95.00 | 0.068 | 95.10 | 0.079 |

| BT-EMP | 94.80 | 0.119 | 95.05 | 0.137 | 95.35 | 0.068 | 95.10 | 0.079 | |

| EL | 93.90 | 0.116 | 93.95 | 0.133 | 95.00 | 0.068 | 95.05 | 0.078 | |

| BT-EL | 95.25 | 0.119 | 94.65 | 0.139 | 95.20 | 0.068 | 95.10 | 0.080 | |

| JEL | 94.70 | 0.120 | 94.00 | 0.140 | 95.25 | 0.069 | 94.65 | 0.080 | |

| AJEL | 95.25 | 0.123 | 94.60 | 0.144 | 95.40 | 0.069 | 94.80 | 0.081 | |

| NA-DRM | 93.60 | 0.099 | 94.80 | 0.128 | 94.60 | 0.058 | 95.25 | 0.075 | |

| BT-DRM | 93.95 | 0.100 | 95.25 | 0.129 | 94.55 | 0.058 | 94.95 | 0.074 | |

| NL-DRM | 93.85 | 0.099 | 95.00 | 0.128 | 94.65 | 0.058 | 95.20 | 0.075 | |

| BL-DRM | 93.65 | 0.099 | 94.95 | 0.127 | 94.55 | 0.058 | 94.85 | 0.074 | |

| (0.3,0.3) | NA-EMP | 93.80 | 0.132 | 93.65 | 0.134 | 94.60 | 0.077 | 94.05 | 0.079 |

| BT-EMP | 95.30 | 0.135 | 94.55 | 0.137 | 95.20 | 0.077 | 94.40 | 0.079 | |

| EL | 93.75 | 0.131 | 93.65 | 0.134 | 94.60 | 0.077 | 94.00 | 0.078 | |

| BT-EL | 94.50 | 0.136 | 94.85 | 0.139 | 94.65 | 0.078 | 94.55 | 0.079 | |

| JEL | 94.45 | 0.137 | 93.80 | 0.141 | 94.50 | 0.078 | 94.55 | 0.080 | |

| AJEL | 95.35 | 0.141 | 94.20 | 0.144 | 94.80 | 0.079 | 94.80 | 0.081 | |

| NA-DRM | 95.10 | 0.120 | 94.35 | 0.130 | 95.45 | 0.070 | 94.90 | 0.076 | |

| BT-DRM | 95.75 | 0.121 | 94.65 | 0.130 | 95.25 | 0.070 | 94.65 | 0.075 | |

| NL-DRM | 95.60 | 0.120 | 94.70 | 0.129 | 95.50 | 0.070 | 95.00 | 0.076 | |

| BL-DRM | 95.30 | 0.119 | 94.60 | 0.128 | 95.10 | 0.069 | 94.60 | 0.075 | |

| (0.6,0.4) | NA-EMP | 93.45 | 0.124 | 94.10 | 0.138 | 94.30 | 0.073 | 95.10 | 0.080 |

| BT-EMP | 95.85 | 0.131 | 95.00 | 0.142 | 95.55 | 0.074 | 95.10 | 0.081 | |

| EL | 94.00 | 0.123 | 94.10 | 0.137 | 94.45 | 0.073 | 95.05 | 0.080 | |

| BT-EL | 95.35 | 0.130 | 94.95 | 0.143 | 94.90 | 0.075 | 95.30 | 0.082 | |

| JEL | 92.90 | 0.133 | 94.15 | 0.145 | 93.35 | 0.075 | 94.90 | 0.082 | |

| AJEL | 93.40 | 0.137 | 94.90 | 0.149 | 93.60 | 0.075 | 95.05 | 0.083 | |

| NA-DRM | 94.60 | 0.119 | 95.05 | 0.137 | 95.30 | 0.069 | 95.15 | 0.080 | |

| BT-DRM | 94.95 | 0.120 | 95.45 | 0.137 | 95.55 | 0.069 | 94.95 | 0.078 | |

| NL-DRM | 95.00 | 0.119 | 95.25 | 0.136 | 95.60 | 0.069 | 95.15 | 0.080 | |

| BL-DRM | 94.45 | 0.116 | 94.85 | 0.134 | 95.10 | 0.068 | 94.80 | 0.078 | |

| (0.7,0.7) | NA-EMP | 92.20 | 0.113 | 92.95 | 0.119 | 94.90 | 0.067 | 93.90 | 0.070 |

| BT-EMP | 96.75 | 0.122 | 96.55 | 0.128 | 96.30 | 0.068 | 95.40 | 0.072 | |

| EL | 92.35 | 0.111 | 92.90 | 0.117 | 95.15 | 0.067 | 93.75 | 0.070 | |

| BT-EL | 94.70 | 0.120 | 95.30 | 0.127 | 95.75 | 0.069 | 94.55 | 0.072 | |

| JEL | 90.75 | 0.123 | 90.80 | 0.129 | 94.00 | 0.069 | 93.00 | 0.072 | |

| AJEL | 91.35 | 0.127 | 91.55 | 0.133 | 94.25 | 0.070 | 93.10 | 0.073 | |

| NA-DRM | 94.50 | 0.111 | 94.85 | 0.121 | 95.10 | 0.065 | 95.20 | 0.071 | |

| BT-DRM | 95.40 | 0.113 | 95.90 | 0.123 | 95.45 | 0.064 | 95.60 | 0.070 | |

| NL-DRM | 95.70 | 0.111 | 96.05 | 0.121 | 96.05 | 0.065 | 96.10 | 0.071 | |

| BL-DRM | 94.60 | 0.108 | 95.05 | 0.118 | 95.30 | 0.063 | 95.20 | 0.069 | |

| (100,100) | (300,300) | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| CP | AL | CP | AL | CP | AL | CP | AL | ||

| (0,0) | NA-EMP | 93.85 | 0.110 | 93.50 | 0.111 | 94.65 | 0.065 | 94.45 | 0.065 |

| BT-EMP | 94.35 | 0.115 | 94.05 | 0.115 | 94.75 | 0.065 | 94.75 | 0.065 | |

| EL | 93.90 | 0.110 | 93.50 | 0.110 | 94.65 | 0.065 | 94.55 | 0.065 | |

| BT-EL | 94.50 | 0.113 | 94.00 | 0.113 | 94.80 | 0.065 | 94.60 | 0.065 | |

| JEL | 94.35 | 0.113 | 93.90 | 0.113 | 94.90 | 0.065 | 94.55 | 0.065 | |

| AJEL | 94.95 | 0.115 | 94.35 | 0.116 | 95.10 | 0.066 | 94.75 | 0.066 | |

| NA-DRM | 94.80 | 0.100 | 94.05 | 0.079 | 93.95 | 0.059 | 95.20 | 0.045 | |

| BT-DRM | 94.45 | 0.104 | 94.75 | 0.079 | 93.65 | 0.060 | 94.95 | 0.045 | |

| NL-DRM | 94.90 | 0.100 | 94.10 | 0.078 | 93.95 | 0.059 | 95.25 | 0.045 | |

| BL-DRM | 94.20 | 0.103 | 94.50 | 0.079 | 93.55 | 0.059 | 94.85 | 0.045 | |

| (0.1,0.3) | NA-EMP | 93.45 | 0.119 | 94.30 | 0.128 | 95.25 | 0.070 | 94.50 | 0.075 |

| BT-EMP | 94.25 | 0.123 | 95.50 | 0.132 | 95.00 | 0.071 | 94.80 | 0.075 | |

| EL | 93.45 | 0.119 | 94.45 | 0.127 | 95.25 | 0.070 | 94.40 | 0.075 | |

| BT-EL | 94.40 | 0.122 | 95.20 | 0.131 | 95.35 | 0.071 | 94.60 | 0.076 | |

| JEL | 94.30 | 0.122 | 94.85 | 0.133 | 95.35 | 0.071 | 94.75 | 0.076 | |

| AJEL | 94.80 | 0.126 | 95.20 | 0.136 | 95.40 | 0.071 | 95.05 | 0.076 | |

| NA-DRM | 94.70 | 0.114 | 94.75 | 0.109 | 95.35 | 0.067 | 94.95 | 0.063 | |

| BT-DRM | 94.35 | 0.116 | 95.15 | 0.109 | 95.10 | 0.066 | 94.85 | 0.063 | |

| NL-DRM | 94.90 | 0.113 | 95.10 | 0.108 | 95.45 | 0.067 | 95.10 | 0.063 | |

| BL-DRM | 93.90 | 0.114 | 94.70 | 0.108 | 94.85 | 0.066 | 94.85 | 0.062 | |

| (0.3,0.3) | NA-EMP | 93.55 | 0.127 | 94.25 | 0.128 | 94.55 | 0.075 | 93.45 | 0.075 |

| BT-EMP | 95.35 | 0.132 | 94.90 | 0.132 | 94.70 | 0.075 | 93.80 | 0.075 | |

| EL | 93.60 | 0.126 | 94.10 | 0.127 | 94.70 | 0.075 | 93.30 | 0.075 | |

| BT-EL | 94.75 | 0.131 | 94.85 | 0.132 | 95.05 | 0.076 | 93.70 | 0.076 | |

| JEL | 93.80 | 0.132 | 94.55 | 0.133 | 94.65 | 0.076 | 93.65 | 0.076 | |

| AJEL | 94.50 | 0.136 | 95.15 | 0.136 | 95.00 | 0.076 | 93.80 | 0.076 | |

| NA-DRM | 95.55 | 0.124 | 94.95 | 0.112 | 95.15 | 0.073 | 94.60 | 0.065 | |

| BT-DRM | 95.45 | 0.125 | 95.30 | 0.112 | 94.60 | 0.072 | 94.60 | 0.064 | |

| NL-DRM | 95.65 | 0.123 | 95.00 | 0.111 | 95.25 | 0.073 | 94.90 | 0.064 | |

| BL-DRM | 95.25 | 0.122 | 95.15 | 0.110 | 94.45 | 0.071 | 94.55 | 0.064 | |

| (0.6,0.4) | NA-EMP | 92.70 | 0.115 | 94.05 | 0.127 | 93.65 | 0.068 | 94.30 | 0.075 |

| BT-EMP | 95.50 | 0.123 | 95.35 | 0.132 | 94.90 | 0.070 | 94.80 | 0.075 | |

| EL | 93.10 | 0.113 | 94.05 | 0.126 | 93.75 | 0.068 | 94.40 | 0.074 | |

| BT-EL | 94.30 | 0.121 | 95.20 | 0.132 | 94.15 | 0.070 | 94.75 | 0.075 | |

| JEL | 92.45 | 0.124 | 94.55 | 0.133 | 93.45 | 0.070 | 94.50 | 0.076 | |

| AJEL | 92.75 | 0.127 | 95.15 | 0.137 | 93.85 | 0.070 | 94.50 | 0.076 | |

| NA-DRM | 94.95 | 0.116 | 95.30 | 0.118 | 94.70 | 0.068 | 94.60 | 0.068 | |

| BT-DRM | 95.45 | 0.116 | 95.50 | 0.118 | 94.30 | 0.066 | 94.50 | 0.067 | |

| NL-DRM | 96.05 | 0.116 | 95.80 | 0.118 | 95.10 | 0.068 | 94.85 | 0.068 | |

| BL-DRM | 94.75 | 0.112 | 95.05 | 0.116 | 94.05 | 0.066 | 94.35 | 0.067 | |

| (0.7,0.7) | NA-EMP | 91.40 | 0.104 | 92.15 | 0.105 | 94.60 | 0.062 | 94.55 | 0.062 |

| BT-EMP | 96.30 | 0.114 | 95.70 | 0.115 | 95.85 | 0.064 | 95.50 | 0.064 | |

| EL | 92.05 | 0.102 | 92.35 | 0.102 | 94.70 | 0.062 | 94.55 | 0.062 | |

| BT-EL | 95.00 | 0.110 | 94.20 | 0.111 | 95.40 | 0.064 | 95.25 | 0.064 | |

| JEL | 90.40 | 0.114 | 91.00 | 0.114 | 94.30 | 0.064 | 93.95 | 0.064 | |

| AJEL | 90.85 | 0.117 | 91.60 | 0.118 | 94.40 | 0.064 | 94.05 | 0.064 | |

| NA-DRM | 94.65 | 0.109 | 93.90 | 0.101 | 96.10 | 0.064 | 95.40 | 0.059 | |

| BT-DRM | 95.80 | 0.109 | 95.55 | 0.102 | 95.65 | 0.062 | 95.95 | 0.058 | |

| NL-DRM | 97.05 | 0.109 | 95.75 | 0.102 | 96.75 | 0.065 | 95.95 | 0.059 | |

| BL-DRM | 94.40 | 0.104 | 94.50 | 0.098 | 95.35 | 0.061 | 95.50 | 0.057 | |

| (100,100) | (300,300) | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| CP | AL | CP | AL | CP | AL | CP | AL | ||

| (0.1,0.3) | NA-EMP | 94.45 | 0.178 | 94.55 | 0.104 | 95.20 | 0.175 | 94.69 | 0.103 |

| BT-EMP | 95.10 | 0.181 | 94.55 | 0.104 | 95.15 | 0.179 | 94.74 | 0.103 | |

| JEL | 95.45 | 0.190 | 95.15 | 0.106 | 96.40 | 0.187 | 95.15 | 0.105 | |

| AJEL | 95.60 | 0.193 | 95.25 | 0.107 | 96.60 | 0.190 | 95.25 | 0.106 | |

| NA-DRM | 94.40 | 0.146 | 95.65 | 0.085 | 94.85 | 0.138 | 94.89 | 0.080 | |

| BT-DRM | 93.45 | 0.143 | 95.10 | 0.083 | 93.80 | 0.135 | 94.34 | 0.080 | |

| (0.6,0.4) | NA-EMP | 94.60 | 0.186 | 94.30 | 0.109 | 93.84 | 0.172 | 95.00 | 0.101 |

| BT-EMP | 94.90 | 0.190 | 94.70 | 0.109 | 94.39 | 0.177 | 95.10 | 0.102 | |

| JEL | 96.25 | 0.205 | 94.90 | 0.112 | 96.85 | 0.192 | 96.30 | 0.105 | |

| AJEL | 96.40 | 0.208 | 95.00 | 0.113 | 97.10 | 0.196 | 96.40 | 0.105 | |

| NA-DRM | 95.35 | 0.175 | 95.25 | 0.102 | 95.40 | 0.150 | 95.10 | 0.088 | |

| BT-DRM | 93.95 | 0.168 | 94.05 | 0.098 | 94.59 | 0.147 | 94.75 | 0.086 | |

References

- David (1968) David, H. (1968). Miscellanea: Gini’s mean difference rediscovered. Biometrika, 55, 573–575.

- Li et al. (2018) Li, H., Liu, Y., Liu, Y., & Zhang, R. (2018). Comparison of empirical likelihood and its dual likelihood under density ratio model. Journal of Nonparametric Statistics, 30, 581–597.

- Mises (1947) Mises, R. v. (1947). On the asymptotic distribution of differentiable statistical functions. The Annals of Mathematical Statistics, 18, 309–348.

- Qin et al. (2010) Qin, Y., Rao, J., & Wu, C. (2010). Empirical likelihood confidence intervals for the Gini measure of income inequality. Economic Modelling, 27, 1429–1435.

- Serfling (1980) Serfling, R. J. (1980). Approximation Theorems of Mathematical Statistics. New York: John Wiley & Sons.

- Van der Vaart (2000) Van der Vaart, A. W. (2000). Asymptotic Statistics. New York: Cambridge University Press.

- Yuan et al. (2020) Yuan, M., Wang, C., Lin, B., & Li, P. (2020). Semiparametric inference on general functionals of two semicontinuous populations. arXiv:2012.07092.