Matrix completion with data-dependent missingness probabilities

Abstract.

The problem of completing a large matrix with lots of missing entries has received widespread attention in the last couple of decades. Two popular approaches to the matrix completion problem are based on singular value thresholding and nuclear norm minimization. Most of the past works on this subject assume that there is a single number such that each entry of the matrix is available independently with probability and missing otherwise. This assumption may not be realistic for many applications. In this work, we replace it with the assumption that the probability that an entry is available is an unknown function of the entry itself. For example, if the entry is the rating given to a movie by a viewer, then it seems plausible that high value entries have greater probability of being available than low value entries. We propose two new estimators, based on singular value thresholding and nuclear norm minimization, to recover the matrix under this assumption. The estimators involve no tuning parameters, and are shown to be consistent under a low rank assumption. We also provide a consistent estimator of the unknown function .

1. Introduction

Let be an matrix, which is only partially observed, possibly with added noise. Given an estimate of , we define its mean squared error as

| (1.1) |

where and denote the -th entries of and respectively. Given a sequence of such estimation problems, where and denote the parameter and estimator matrices of the -th problem, we call the sequence of estimators consistent if

Estimating a large matrix from a few randomly selected (and possibly noisy) entries is a common objective in many statistical problems. The basic assumption in all of the work in this area is that the matrix has either low rank or is approximately of low rank in some suitable sense. Some of the prominent applications of matrix completion include compressed sensing [12, 19, 8, 9, 10, 11], collaborative filtering [6, 42], multi-class learning [2, 40], dimension reduction [31, 46] and subspace estimation [7]. Theoretical guarantees of matrix completion under various assumptions have been worked out in [37, 17, 18, 1, 4, 28, 29, 27, 13, 26, 24, 38, 3, 43, 34]. This is only a small sampling of the huge literature on this topic. For a recent survey, see [39].

In many of the above works, it is assumed that the entries are missing uniformly at random. This may not be a realistic assumption in many applications. For example, in the classic problem of movie ratings, if a particular movie gets poor reviews, fewer numbers of viewers are expected to review it and hence the probability of missing entries corresponding to that particular movie would be higher. Work on matrix completion under the ‘missing not at random’ (MNAR) assumption is relatively sparse. Some examples include deterministic missing patterns or missing patterns that depend on the matrix, using spectral gap conditions [5], rigidity theory [44], algebraic geometry [25] and other methods [30, 41, 45]. For random but non-uniform missing patterns, a variety of statistical guarantees for procedures based on nuclear-norm penalization and other ideas are available [26, 20, 29, 9, 43, 38, 18, 17, 49, 16, 33]. However, these guarantees almost always require a careful choice of the penalty parameter (or some other parameter, such as rank) based on knowledge about the unknown matrix that is unlikely to be available. This is in contrast to the case of uniform missing pattern, where we now have many algorithms that assume no knowledge of the unknown matrix.

In the present work, we assume that the probability of an entry being revealed is a function of the value of that entry, and the revealed entries are allowed to be noisy. This frequently encountered example of missingness where a variable governs its own missingness is known as self-masking MNAR [36]. Under these assumptions, we provide an estimator of the parameter matrix based on a spectral method and prove its consistency under a low rank assumption. We also provide a second estimator based on nuclear norm minimization. This estimator performs significantly better than the spectral estimator in the absence of noise, but may not work well for noisy entries. Moreover, it is computationally expensive for large matrices. Lastly, we give estimates of the function using both methods, along with theoretical guarantees about it. Some numerical examples are worked out. The main advantage of our estimators is that they do not involve penalty parameters (or any other user-specified parameters) which have to be carefully chosen to ensure that the theoretical guarantees work out. The cost is that we have asymptotic consistency results rather than finite sample error bounds.

A recent paper that works under the setting of self-masking MNAR, but in the setting of tensor completion, is [47]. In [47], the probabilities of missingness are called ‘propensity scores’. The main difference between [47] (and similar papers) and our work is that in [47], it is assumed that the tensor of propensity scores is low-rank, while we make no such assumption. Indeed, one of the main observations in our paper, which we prove using spectral techniques reminiscent of the proof of Szemerédi’s lemma in combinatorics, is that the matrix of propensity scores is guaranteed to have an approximately low rank structure under a Lipschitz assumption on .

A natural extension of our work is to study beyond self-masking MNAR, namely, to consider examples where the process that causes the missingness of an entry depends on multiple entries of the parameter matrix and not only its value itself. Such directions are left for future research.

2. Results

2.1. The problem

Let be an matrix with all entries in the interval . Let be a function. Let be a noisy version of , modeled as a matrix with independent entries in , such that for each and . The -th entry of is revealed with probability , and remains hidden with probability , and these events occur independently. Our goal is to estimate using the observed entries of .

2.2. Modified USVT estimator

Our first proposal is an estimator of based on singular value thresholding. This is a modification of the Universal Singular Value Thresholding (USVT) estimator of [14]. The estimator is defined as follows:

-

(1)

Let be the matrix whose -th entry is if the -th entry of is revealed, and otherwise.

-

(2)

Let be the singular value decomposition of .

- (3)

-

(4)

Truncate the entries of to force them to belong to the interval . Call the resulting matrix .

-

(5)

Let be the matrix whose -th entry is if is revealed, and otherwise.

-

(6)

Repeat the above steps for the matrix instead of , to get .

-

(7)

Define a matrix as if , and otherwise.

-

(8)

Truncate the entries of to force them to be in . The resulting matrix is our estimator .

The idea behind this estimator has some similarity with the one proposed recently by Ma and Chen [33], which is also based on a two-step procedure, first estimating the matrix of missingness probabilities and then using these estimated probabilities to estimate the unknown matrix. The algorithm of Ma and Chen involves a number of user-specified parameters, whereas ours does not, which may be a desirable feature.

Note that if the entries of and are known to belong to an interval instead of , then subtracting from each entry of X and dividing by forces the entries to lie in . Then applying the above procedure, and finally multiplying the end-result by and adding , we can get the desired estimate of . The case of unknown is beyond the scope of the paper. Lastly, if , one can simply work with the transpose of to get an estimate for the transpose of .

2.3. Modified Candès–Recht estimator

Our second proposal is an estimator of based on nuclear norm minimization. This estimator works only in the absence of noise, so we assume that . Let be the matrix that minimizes nuclear norm among all matrices that are equal to at the revealed entries, and have all entries in . (Recall that the nuclear norm of a matrix , usually denoted by , is the sum of its singular values.) Hence, given a set of observed entries , our estimator is obtained by solving the optimization problem:

where

This is a small modification of the popular Candès–Recht estimator [9, 10, 11], suggested recently in [15]. The original estimator does not have the additional constraint that the entries of have to be in . This extra constraint is not problematic since this is a convex constraint. For example, it can be easily implemented in R by adding an constraint using CVXR package [21]. Moreover, from an intuitive point of view, it makes sense to add this constraint since we already know that the entries of the unknown matrix are in . This estimator is similar to the one proposed by Klopp [26], except that our method does not involve a penalty parameter.

2.4. Consistency results

We now state consistency results for the two estimators defined above. Suppose that we have a sequence of matrices , where has order , and as . Let be a sequence of random matrices with independent entries in such that for each . In other words, is a noisy version of . Let be the union of the sets of entries of all of these matrices. Let be a function such that the noisy version of an entry with true value is revealed with probability , independently of all else. Note that it is irrelevant how is defined outside , which is why we took the domain of to be this countable set.

Recall that a sequence of estimators is consistent if as , where MSE stands for the mean squared error defined in equation (1.1). We will now prove the consistencies of the two estimators defined above. The crucial assumption will be that the sequence has uniformly bounded rank. This is a version of the frequently occurring low rank assumption from the literature. In addition to that, we will need some other technical assumptions. Our first result is the following theorem, which gives a sufficient condition for the consistency of the modified USVT estimator.

Theorem 2.1.

In the above setup, suppose that the sequence has uniformly bounded rank. Let be the empirical distribution of the entries of . Suppose that for any subsequential weak limit of the sequence , there is an extension of to a Lipschitz function from into , also denoted by , which has no zeros in the support of . Then the modified USVT estimator based on is consistent.

Remark 2.2.

The statement of the above Theorem is about asymptotic behavior of MSE. However, in our proofs, we obtain some finite sample error bounds which we have omitted, with the goal of increasing the readability of the result, and also for reducing the stringency of assumptions on . In fact, the proof shows that if for some , and everywhere for some , and is a Lipschitz function with Lipschitz constant , then for any , the MSE can be upper bounded by

where is a constant depending on and , and , , and are universal constants. Such a bound reveals how the magnitude of error is dependent on the nuclear norm of parameter matrix and the Lipschitz constant of .

Remark 2.3.

Note that in many examples, such as in most recommender systems, the matrix entries can only take values in a fixed finite set. In such examples, there is no loss of generality in the assumption that has an extension that is Lipschitz and nonzero everywhere on . Also, if is continuous and nonzero everywhere in , then the condition involving the empirical distribution of the entries is redundant.

The next theorem gives the consistency of the modified Candès–Recht estimator, under the additional assumption that there is no noise.

Theorem 2.4.

In the above setup, suppose that the sequence has uniformly bounded rank, and also suppose that for each . Let be the empirical distribution of the entries of . Suppose that for any subsequential weak limit of the sequence , there is an extension of to a measurable function from into , also denoted by , such that is nonzero and continuous almost everywhere with respect to . Then the modified Candès–Recht estimator is consistent for this problem.

Remark 2.5.

We will see in numerical examples that the modified Candès–Recht estimator has superior performance. The advantage of the modified USVT estimator is twofold. First, it can be used when the matrix is very large, where using nuclear norm minimization may become infeasible due to computational cost. Second, in the presence of noise — which is often the case in practice — the modified Candès–Recht estimator may perform badly, as we will see in the simulated and real data examples.

Remark 2.6.

Often, in many MNAR examples, identifiability of parameters is an issue (see, e.g., [35]), which corresponds to the notions that there might be two sets of parameter values which yield same observations and hence, the true parameter value cannot be identified. In Theorems 2.1 and 2.4, however, the fact that we are able to approximately recover the true matrix automatically implies that identifiability is not an issue, provided that the low rank assumption holds. (That is, if there are two candidates and for the true matrix, and they both have low rank, then our estimate will be close to both and with high probability, which means that must be close to .)

2.5. Proof sketch

To prove Theorem 2.1, we first assume that converges weakly to a limit as . Let be the matrix obtained by applying entrywise to and be entrywise product of and . Let be the matrix obtained by replacing the unrevealed entries of by zero. Let be the matrix whose -th entry is if the -th entry of is revealed, and otherwise.

The main step is to show that and are also approximately low rank matrices, in the sense that and . This is proved using a spectral method, similar to the spectral proof of Szemerédi’s regularity lemma. The key idea is that a low rank matrix is approximately a block matrix after a suitable permutation of rows and columns, and therefore, applying a Lipschitz function entrywise keeps it close to a block matrix, which, in turn, is approximately low rank. Once this is established, it then follows by the standard results for USVT that if and are the estimates of and obtained by applying the USVT algorithm to and , then and with high probability (in some appropriate sense).

To prove Theorem 2.4, we first show that one can possibly permute rows and columns in each to get an limit . Next we prove there is a measurable function that is nonzero almost everywhere and converges to in cut distance almost surely subsequentially. This implies consistency of by [15, Theorem 2 and Theorem 3].

2.6. Estimating

We will now produce an estimator for the unknown function that can be used with any consistent estimator. Our procedure is motivated by the nonparametric density estimation methods available in statistics literature. It is interesting to note, if the underlying function were indeed a constant function, we have observed from simulated examples that our estimator is also close to a constant function. Hence, can be used to check if the data are MNAR or not. The estimator involves the choice of a tuning parameter , which is a positive integer, chosen by the user. Given a matrix with partially revealed entries as in Subsection 2.1, and an estimator of , the estimator of is defined as follows.

-

(1)

For , let . Note that this is a sequence of equally spaced points, starting at and going up to .

-

(2)

For each , choose uniformly at random from the interval .

-

(3)

In the interval , define to be the proportion of revealed entries among those entries of such that the corresponding entry of is in .

Note that the above procedure defines on an interval that is slightly larger than , but that should not bother us, because the domain can then be restricted to . The following theorem gives a measure of the performance of as an estimate of .

Theorem 2.7.

Suppose that is Lipschitz, with Lipschitz constant . Let be the empirical distribution of the entries of and . Then

where is a universal constant.

The above result shows that if is big, but much smaller than both and , then is close to at almost all entries of . In practice, a good rule of thumb would be to choose such that is large, but at the same time, the intervals contain substantial numbers of entries of . One can try to choose optimally using some kind of cross-validation (such as leave-one-out cross-validation), but it may be hard to prove theoretical guarantees for such methods.

Although our method of estimating has similarities with density estimation methods, the problem is quite different since the entries of the estimated matrix are not independent random variables — in fact, they may have a complicated, or even intractable, dependence structure. One might wonder if traditional nonparametric methods of estimating can still be applied here under some smoothness constraint. Such questions are left for future investigation.

2.7. Examples

In this subsection we will see how the two estimators perform in some simulated examples and two real data examples. For real data examples, one should always check whether the matrix is low-rank approximable before applying our methods. Our simulations show taking of order for estimating an matrix yields good , although we do not have a theorem to prove that. Finally, one should also check if data is noisy or not, and should apply spectral estimator when noise is present.

Example 2.8.

Consider a low rank matrix with the entries of having marginal distribution . Here, we take and . To generate such a matrix, we define , where:

-

•

For , , and the components of and are i.i.d. random variables.

-

•

, is a vector of all s, and has i.i.d entries.

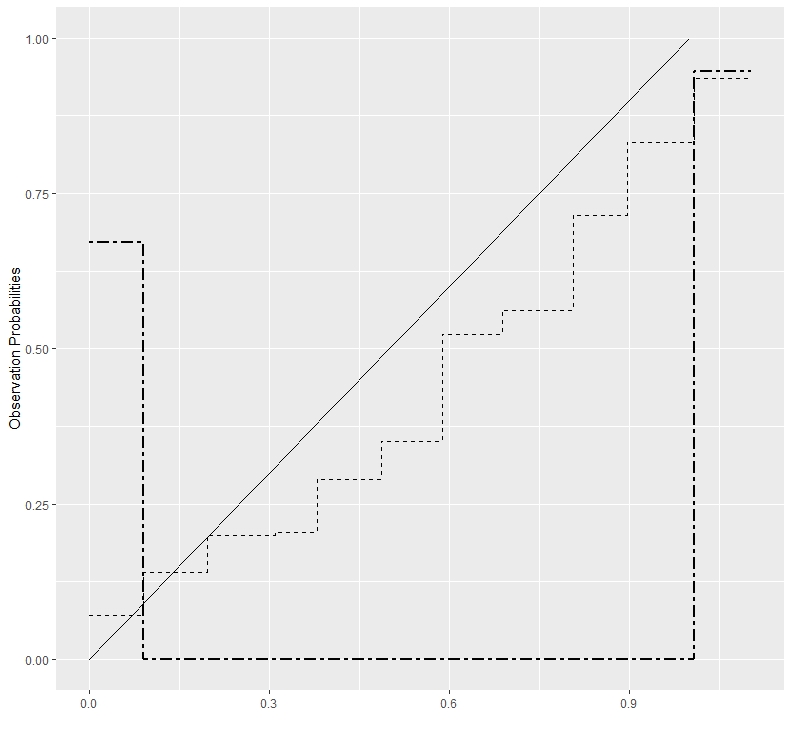

It is not difficult to see that the entries of are i.i.d. random variables. Multiplying each entry by and subtracting , we get . Then has rank with probability , and the entries of are uniformly distributed in . We take to generate missing entries, and do not add noise. To obtain the modified Candès–Recht estimator, we used code from the R package filling [48] and imposed the constraint using the CVXR package [21]. The modified USVT algorithm, being quite straightforward, was coded without the aid of existing packages.

The modified Candès–Recht estimator was able to exactly recover the true almost all the time, resulting a very small MSE of order . The modified USVT estimator performed much worse, with an unimpressive MSE of . The run-time of the modified USVT estimator was much lower than that of the modified Candès–Recht estimator: seconds versus minutes. We will see in the next example that the performance of the modified USVT estimator becomes better when is larger, accompanied by a huge gain in run-time over the other estimator. We report both our estimators and their MSEs and run-times in Table 1.

| Modified USVT | Modified Candès–Recht | |

| MSE | 0.123 | |

| Run-time | 0.31 sec | 4.08 min |

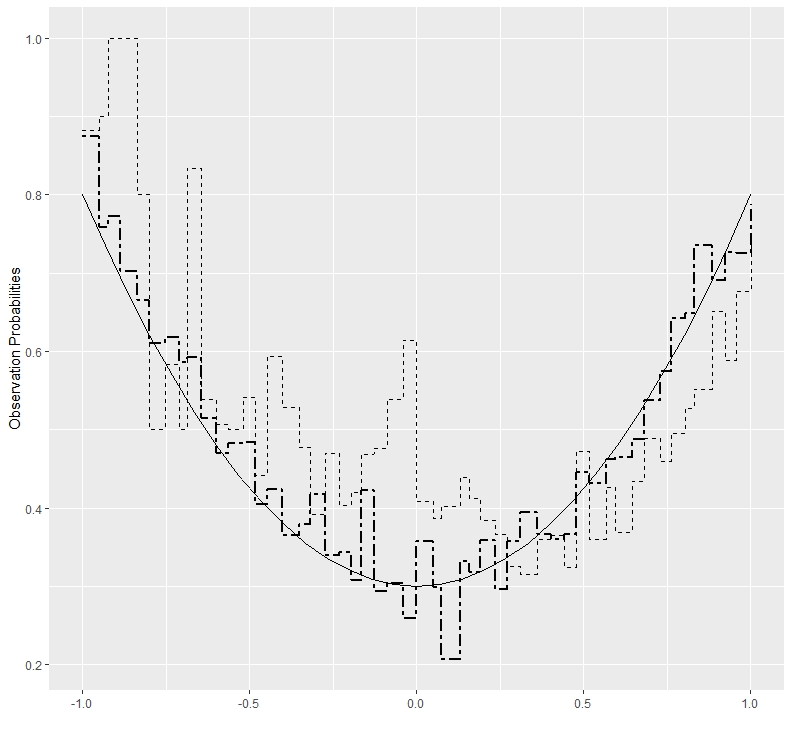

Next, for both estimators of , we estimated using the method proposed in Section 2.6, taking . The estimated ’s are shown in Figure 1. As expected, the based on the modified Candès–Recht estimator has better performance.

Example 2.9.

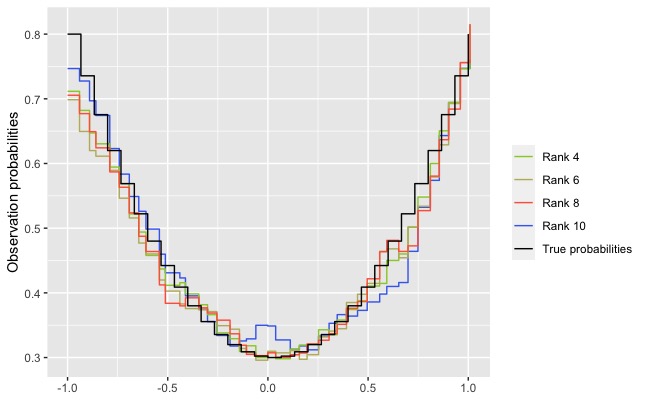

Here, we want to see how our estimator performs as we vary the rank of underlying parameter matrix. To this end, we take parameter matrix same as previous example, with and choose rank . We only report result of the modified USVT estimator, the results corresponding to modified Candés- Recht estimator varies similarly. The MSE of the estimator as we vary rank are respectively. The estimated is shown in Figure 2. We also observe our estimator performs better than the vanilla USVT algorithm developed for MCAR. A comparison of MSE of the two estimators has been given below in Table 2.

| Rank | Modified USVT | Regular USVT |

| 4 | 0.007 | 0.060 |

| 6 | 0.012 | 0.063 |

| 8 | 0.012 | 0.063 |

| 10 | 0.033 | 0.062 |

Example 2.10.

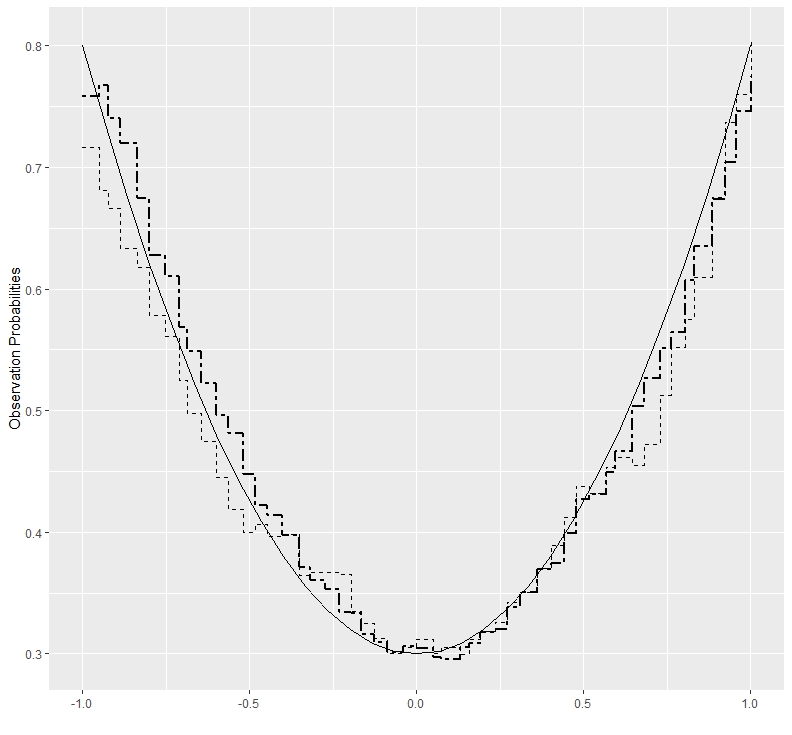

This is the same as Example 2.8, but with to show how modified USVT has significant computation time advantage over the modified Candès-Recht estimator. The MSE of the modified USVT estimator is now , and that of the modified Candès-Recht estimator is of order . So, with this larger sample size, the modified USVT estimator has reasonably good performance. The time to compute the modified USVT estimator seconds, whereas for the modified Candès–Recht estimator, it is hours. This shows that even though the latter has much better performance in terms of MSE, it may be more practical to use the former if the matrix is large. We provide the estimators of in Figure 3, taking . We report the MSEs and run-times for both estimators in Table 3.

| Modified USVT | Modified Candès–Recht | |

| MSE | 0.011 | |

| Run-time | 0.85 sec | 2.51 hrs |

A visual examination shows that both estimators perform well.

Example 2.11.

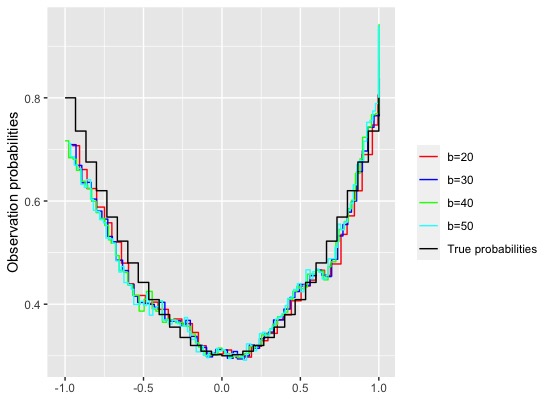

Under the same setup as before, we now show how the change of the parameter , number of bins, affect the estimate of underlying function . We choose and plot the resulting in Figure 4. There does not seem to have much difference in across different values of .

Example 2.12.

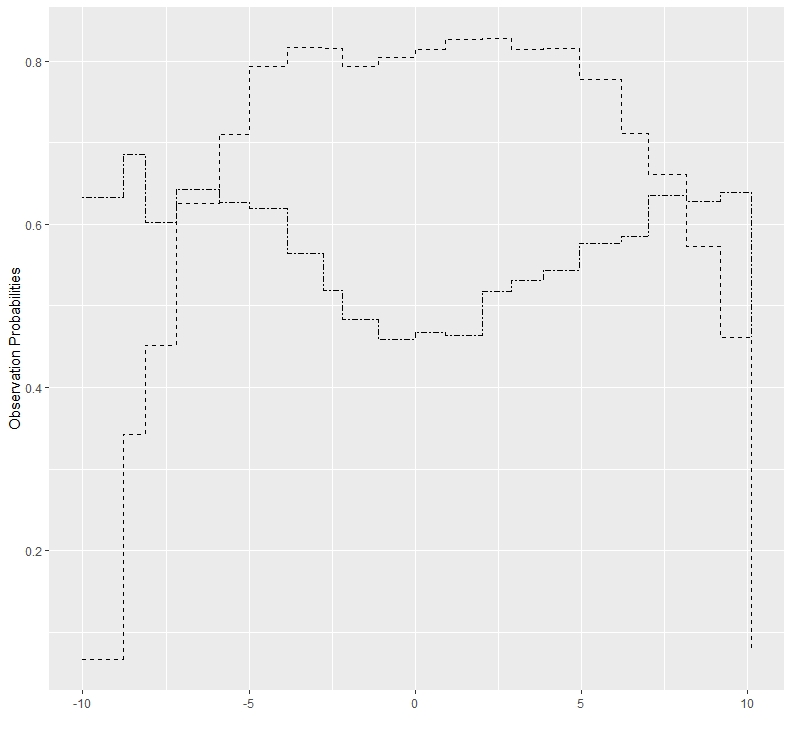

We will now show that the modified Candès–Recht estimator performs poorly under presence of noise. Here, we take and , with the marginal distribution of the entries of being , generated by the same procedure that we used to generate in Example 2.8. The noisy version of , namely , is generated as follows. For each , generate with probability and with probability . Note that . The entry is revealed with probability , and remains hidden with probability (that is, we took ). For , the MSE of modified USVT estimator turned out to be , much better than the MSE of the modified Candès–Recht estimator, which was . The estimates of based on the two methods, with , are depicted in Figure 5. The estimate based on the modified USVT method is reasonably good, even with as small as in this example. The estimate based on the modified Candès–Recht estimator, however, is completely off: It estimates to be large near and and zero everywhere in between. This is because the observed entries consist solely of zeros and ones, and coincides with at the observed values. So the estimation procedure for deduces, incorrectly, that there is no chance of observing an entry if its non-noisy value is strictly between and .

Example 2.13.

We now consider a real data example. In real data, it is not possible to compare the performance of with the ‘true ’, because we do not know what the true is (or if our model is actually valid). Still, if turns out to be substantially different than a constant function, it validates the viewpoint that entries are not missing uniformly at random. We consider the well-known Jester data [22], which consists of jokes rated by 73,421 users. The ratings are continuous values between and , entered by the users by clicking on an on-screen ‘funniness’ bar. Not every user rates every joke, so there are many missing entries. Due to the prohibitively large run-time of the modified Candès–Recht estimator, we first took a submatrix consisting of all jokes but a random sample of users. Approximately of the values were missing in this submatrix. The estimates of based on the two methods (with ) are shown in Figure 6.

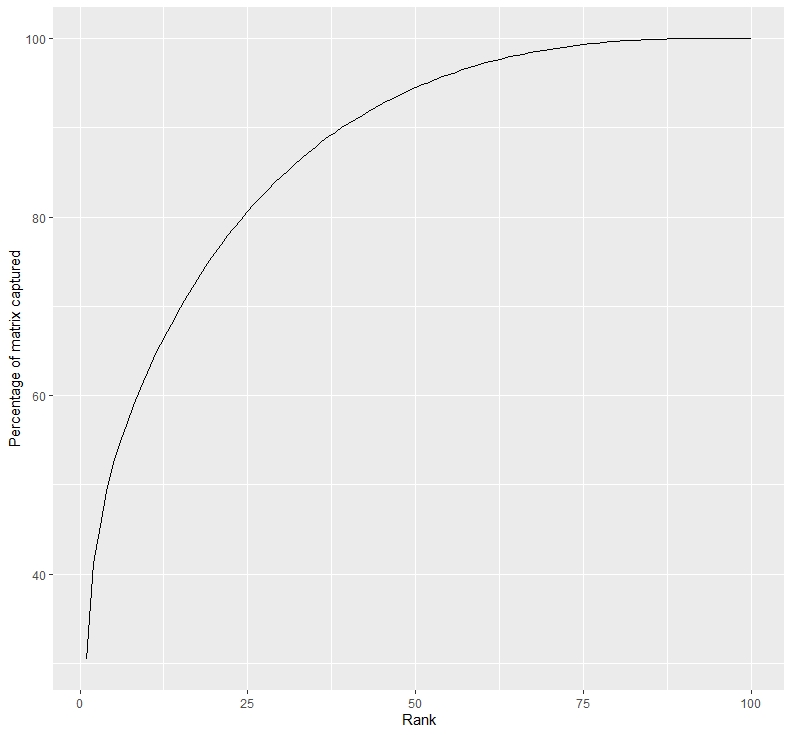

Interestingly, the two estimates are very different. We posit that this is due to the presence of noise in the observed matrix, which messes up the modified Candès–Recht estimator. Indeed, the continuous nature of the ratings makes it very unlikely that the observed matrix is without noise. This is further validated by Figure 7, where we plot the percentage of the modified Candès-Recht estimator matrix that is captured by its rank- approximation, . (The percentage is simply the sum of squares of the top singular values divided by the sum of squares of all singular values.) This figure shows that to even get within of , we need to consider a rank- approximation. Thus, is not of low rank, even approximately. This invalidates the low rank assumption of the Candès–Recht procedure, and allows us to conjecture that the given by the modified USVT estimator is a better reflection of the true , assuming that the model is correct.

Example 2.14.

We continue with the Jester data example. Assuming that the given by the modified USVT estimator reflects the true state of affairs, we ran the modified USVT method on the whole dataset. The estimated , with , is shown in Figure 8. The inverted U-shape is mysterious. It is not clear to us what may have led to this, if it is indeed close to the true , because we do not know what caused entries to be missing in this dataset.

Example 2.15.

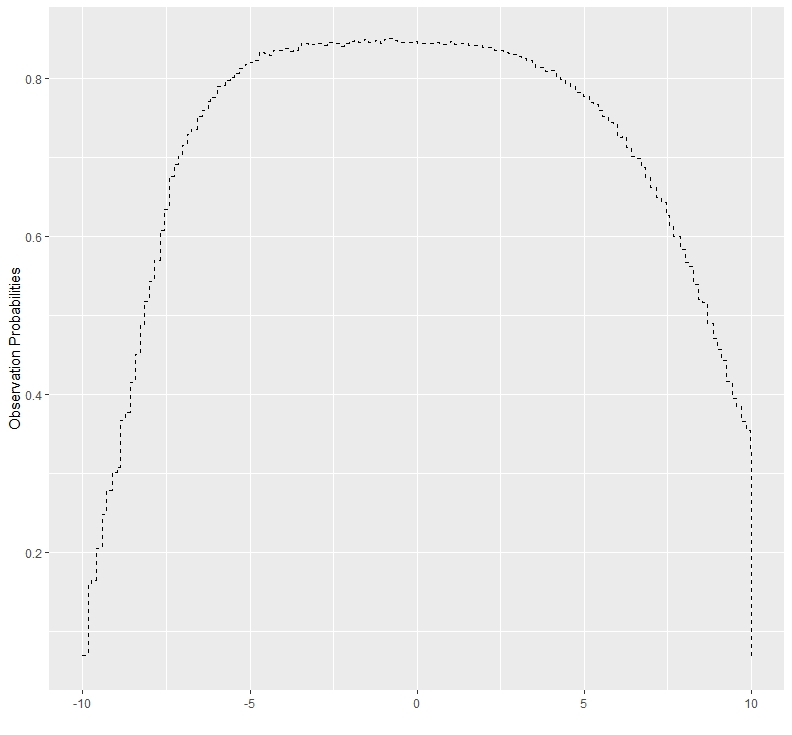

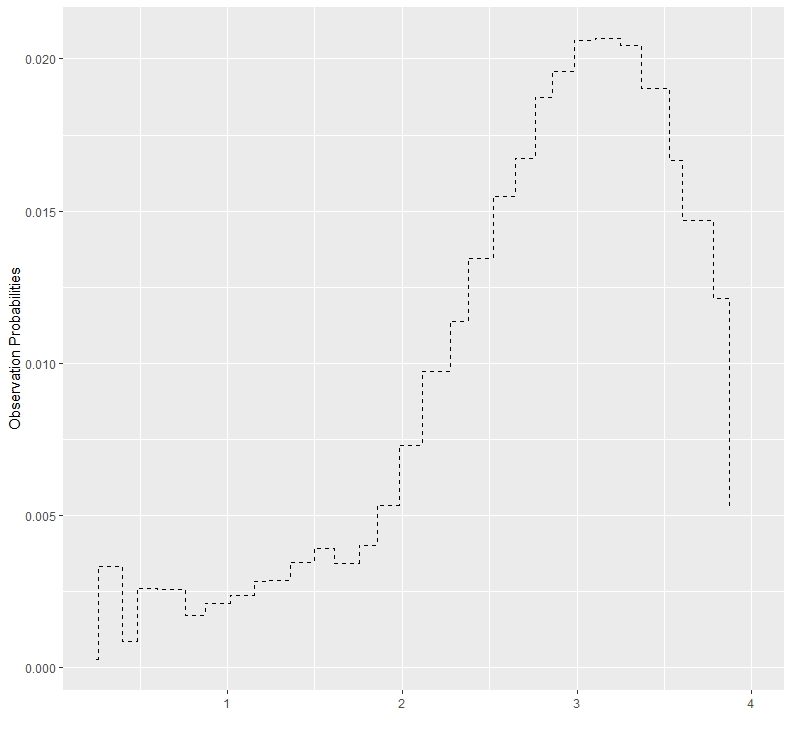

For our final example, we consider the Film Trust dataset of movie ratings [23]. This dataset consists of ratings given by users to movies, with many missing entries. The user ratings range in the set . This dataset is much sparser than the Jester data; only ratings are available, which is about percent of the total number of possible ratings. Due to the large size of the dataset, we implemented only the modified USVT algorithm. We assume that each user has a ‘true’ rating for each movie, and the observed rating, if any, is a noisy version of the true rating. The observation probability is then a function of the true rating. The estimate of , with , is plotted in Figure 9. As expected, a high rating increases the chance of the rating being available; however, there is a dip towards the end of the curve which we do not know how to explain. One possible explanation is that very highly rated movies are often classics that not many people watch and rate because they have already watched those movies before.

3. Proof of Theorem 2.4

For an matrix , define

Note that is the sum of squares of the singular values of , divided by . Given the matrix , we will also denote by the function which equals in the rectangle for each and . On the boundaries of the rectangles, we define the function is to be zero. Note that with this convention, equals the norm of the function , which will also be denoted by .

For each , let denote the group of all permutations of . Given an matrix and a measurable map , we define

| (3.1) |

where is the matrix whose -th entry is . The first key step in the proof of Theorem 2.4 is the following lemma.

Lemma 3.1.

Suppose that for each , we have a matrix of order with entries in , where as . Suppose that this sequence has uniformly bounded rank. Then there exists a subsequence and a measurable map such that as .

We will now prove Lemma 3.1. The proof closely follows the proof of [15, Theorem 1]. Let and be two positive integers. Let be a partition of and let be a partition of . The pair defines a block structure for matrices in the natural way: Two pairs of indices and belong to the same block if and only if and belong to the same member of and and belong to the same member of .

If is an matrix, let be the ‘block averaged’ version of , obtained by replacing the entries in each block (in the block structure defined by ) by the average value in that block. It is easy to see that

| (3.2) |

We need the following lemma.

Lemma 3.2.

For any matrix with entries in , and , there is a sequence of partitions of and a sequence of partitions of such that for each ,

-

(1)

is a refinement of and is a refinement of ,

-

(2)

and are bounded by , and

-

(3)

.

Proof.

Let be the singular value decomposition of , where , and some of the ’s are zero if the rank is strictly less than . Take any . Let be the largest number such that . If there is no such , let . Let

We define , , and as in the proof of [15, Lemma 4], as follows. For and , let denote the component of . Let be the largest integer multiple of that is . Let be the vector whose component is . Similarly, for , let be the largest integer multiple of that is . Finally, define . This matrix is used as a block-approximation of . As shown in [15], this sequence of partitions satisfy property (1) and (2) in the statement of the lemma. Now, using the properties of the norms noted earlier, and the facts that and , we have

Again, as in the proof of [15, Lemma 4], we obtain

Combining, we get

Now note that is constant within the blocks defined by the pair . Thus, by (3.2),

This completes the proof. ∎

We are now ready to prove Lemma 3.1.

Proof of Lemma 3.1.

Let be a uniform upper bound on the rank of . Lemma 3.2 tells us that for each and , we can find a partition of and a partition of such that

-

(1)

is a refinement of and is a refinement of ,

-

(2)

and are bounded by , and

-

(3)

.

To reduce notation, let us denote by . Following the proof of [15, Theorem 1] and passing to a subsequence if necessary, we get that for every , there exists a measurable function such that in as , where and are permutations that depend only on (and not on ). Without loss of generality, let us assume and are identity permutations for each .

By construction, the block structure for is a refinement of the block structure for . Also by construction, the value of in one of its blocks is the average value of within that block. From this, by a standard martingale argument (for example, as in the proof of [32, Theorem 9.23]) it follows that converges pointwise almost everywhere to a function as . In particular, in . We claim that in as . To show this, take any . Find so large that and . Then for any ,

Since in as and is arbitrary, this completes the proof. ∎

Henceforth, let us work in the setting of Theorem 2.4. For each , let be the random binary matrix whose -the entry is if the -th entry of is revealed, and otherwise. Then note that as functions on , , where denotes the matrix of expected values of the entries of .

Recall the cut norm on the set of matrices, as defined in [15]:

where denotes the norm of a vector . If is an matrix and is a measurable function, we define to be , where is the matrix whose -th entry is the average value of in the rectangle .

The following lemma shows that and are close in cut norm.

Lemma 3.3.

As , in probability.

Proof.

It is easy to see from the definition of cut norm that for an matrix ,

where is the operator norm of . Now take any . Using [14, Theorem 3.4], for some positive universal constants and . Hence, for large enough,

This shows that in probability as . ∎

Next, we relate the limiting empirical distribution of the entries of with the limit of as a function on . In the following, denotes Lebesgue measure on .

Lemma 3.4.

Suppose that in as a sequence of functions on . Then converges weakly to .

Proof.

Take any bounded continuous function . It is not difficult to see that

Since in and is bounded and continuous, we get

But the right side is the integral of with respect to the measure . This completes the proof. ∎

The purpose of the next lemma is to investigate the convergence of under the hypotheses of Theorem 2.4.

Lemma 3.5.

Suppose that in as a sequence of functions on . Let . Suppose that is a measurable function which is continuous almost everywhere with respect to . Then in .

Proof.

Since in , any subsequence has a further subsequence along which for -a.e. . By assumption, is continuous at for -a.e. . Combining these two observations, we get that for any subsequence, there is a further subsequence along with for -a.e. . Since , and are all taking values in , this implies that in along this subsequence. This completes the proof. ∎

As a consequence of the above lemmas, we obtain the following result.

Lemma 3.6.

Suppose that in as a sequence of functions on . Then, under the hypotheses of Theorem 2.4, there is a measurable function that is nonzero almost everywhere and in probability as .

Proof.

By Lemma 3.3, it suffices to show that for some as in the statement of the lemma. By Lemma 3.4, converges weakly to . By the hypotheses of Theorem 2.4, there is a measurable extension of to , also denoted by , which is nonzero and continuous -a.e. As noted earlier, . Therefore, by Lemma 3.5, in . It is not hard to see that this implies that . But is nonzero -a.e. Thus, we can take . ∎

We are now ready to prove Theorem 2.4.

Proof.

Suppose that is not a consistent sequence of estimators. Then, passing to a subsequence if necessary, we may assume that

| (3.3) |

Note that this condition continues to hold true if we pass to further subsequences and permute rows and columns in each , which we will do shortly. Passing to a further subsequence, and permuting rows and columns in each if necessary, we use Lemma 3.1 to get an limit of as . Then, by Lemma 3.6, there is a measurable function that is nonzero almost everywhere and in probability as . Again passing to a subsequence, we get that almost surely. But this implies, by [15, Theorem 2 and Theorem 3], that almost surely. Since the entries of and are in for all , this contradicts (3.3). ∎

4. Proof of Theorem 2.1

Without loss of generality, suppose that for each . (Otherwise, we can just transpose the matrices.) Let be a uniform upper bound on the rank of . Let be the matrix obtained by applying entrywise to . Let be the entrywise (i.e., Hadamard) product of and . Let be the matrix obtained by replacing the unrevealed entries of by zero. Let be the matrix whose -th entry is if the -th entry of is revealed, and otherwise. Note that and . Note also that the entries of and are all in .

First, let us assume that converges weakly to a limit as . Then by the hypotheses of Theorem 2.1, has an extension to a Lipschitz function on , also called , which has no zeros in the support of . Let us fix such an extension, and let denote its Lipschitz constant.

Lemma 4.1.

As , .

Proof.

Fix . It is an easy consequence of the Cauchy–Schwarz inequality that for any ,

By [15, Lemma 2], this implies that there is a block matrix with at most blocks, where depends only on and , and entries in , such that . Let be obtained by applying to entrywise. Then by the Lipschitz property of , we get

Note that just like , has at most blocks. In particular, . Therefore again by the Cauchy–Schwarz inequality,

Thus,

Since this holds for arbitrary , this completes the proof. ∎

Lemma 4.2.

As , .

Proof.

Let , , and be as in Lemma 4.2. Let be the Hadamard product of and , and be the Hadamard product of and . Then also has blocks. Moreover, since the entries of all these matrices are in , it is not hard to see that

The rest of the proof is the same as the proof of Lemma 4.1, with replaced by and replaced by . ∎

As a consequence of the above lemmas, we obtain the following result.

Lemma 4.3.

Let and be the estimates of and obtained by applying the USVT algorithm to and . Then and as .

Proof.

Let us now prove Theorem 2.1 under the simplifying assumption under which we are currently working. Let denote the modified USVT estimator. Let denote the -th element of , denote the -th element of , etc.

Since is nonzero and continuous on the support of , and the support is a compact set, there exists such that everywhere on the support of . In particular, . Since weakly, and is a closed set due to the continuity of , we get

In other words, if we let , then as .

Now take . Then

Since is obtained by truncating , the above upper bound also holds for when . But for any . Thus,

By Lemma 4.3 and our previous deduction that , the above inequality shows that in probability as . Since this is a uniformly bounded sequence of random variables, this proves the consistency of . This proves Theorem 2.1 under the simplifying assumption that converges weakly to some as . We are now ready to prove Theorem 2.1 in full generality.

Proof of Theorem 2.1.

Let be the modified USVT estimator of . Suppose that is not a consistent sequence of estimators. Passing to a subsequence if necessary, we may assume that

| (4.1) |

Note that this will continue to hold true if we pass to further subsequences. Passing to a further subsequence, we may assume that converges weakly to some . But then we already know that (4.1) is violated. This completes the proof of the theorem. ∎

5. Proof of Theorem 2.7

In this proof, will denote any universal constant, whose value may change from line to line. Let be a subinterval of . Let if the -th entry of is revealed and otherwise. Let

and let

where the right sides are declared to be zero if the corresponding sums are empty. Note that and are always in . Take some , to be chosen later. Let

| (5.1) |

Take any . There are two cases. First suppose that . Since , we have , and hence in this case, . By Markov’s inequality, the number of such is bounded above by

| (5.2) |

The second case is that . By the definition of , the number of such is at most . Combining, we get that

Now take any . Then, again, there are two cases. First, suppose that . Since , in this case we have that . Thus, by Markov’s inequality, the number of such is bounded above by (5.2). The other case is . As before, the number of such is bounded above by . Combining these two observations, we get that

| (5.3) |

We will now work under the assumption that . The final estimate will be valid even if . First, note that

Let . Then the above bound can be written as

| (5.4) |

Clearly, the above bound holds even if . Next, note that

This shows, by (5.3) and the fact that and are both in , that

| (5.5) |

Again, this bound holds even if . Combining (5.4) and (5.5), we get

| (5.6) |

Using the notation (5.1), we see that for any ,

Applying (5.6) to the interval , taking expectation over the randomness of the ’s and applying the above inequality, and then summing over , we get

Choosing gives

For , let

Then note that for any ,

Since

this completes the proof of the theorem.

Acknowledgement

S. B. thanks Debangan Dey, Samriddha Lahiry, Samyak Rajanala and Subhabrata Sen for helpful discussions. S. C.’s research was partially supported by NSF grant DMS-1855484. Lastly, we thank the two anonymous referees for their useful suggestions.

References

- Achlioptas and McSherry [2007] Dimitris Achlioptas and Frank McSherry. Fast computation of low-rank matrix approximations. Journal of the ACM (JACM), 54(2):9–es, 2007.

- Argyriou et al. [2008] Andreas Argyriou, Theodoros Evgeniou, and Massimiliano Pontil. Convex multi-task feature learning. Machine learning, 73(3):243–272, 2008.

- Azadkia [2018] Mona Azadkia. Adaptive estimation of noise variance and matrix estimation via usvt algorithm. arXiv preprint arXiv:1801.10015, 2018.

- Azar et al. [2001] Yossi Azar, Amos Fiat, Anna Karlin, Frank McSherry, and Jared Saia. Spectral analysis of data. In Proceedings of the thirty-third annual ACM symposium on Theory of computing, pages 619–626, 2001.

- Bhojanapalli and Jain [2014] Srinadh Bhojanapalli and Prateek Jain. Universal matrix completion. In International Conference on Machine Learning, pages 1881–1889. PMLR, 2014.

- Billsus and Pazzani [1998] Daniel Billsus and Michael J. Pazzani. Learning collaborative information filters. In ICML, volume 98, pages 46–54, 1998.

- Cai et al. [2021] Changxiao Cai, Gen Li, Yuejie Chi, H Vincent Poor, and Yuxin Chen. Subspace estimation from unbalanced and incomplete data matrices: statistical guarantees. The Annals of Statistics, 49(2):944–967, 2021.

- Cai et al. [2010] Jian-Feng Cai, Emmanuel J. Candès, and Zuowei Shen. A singular value thresholding algorithm for matrix completion. SIAM Journal on optimization, 20(4):1956–1982, 2010.

- Candès and Plan [2010] Emmanuel J. Candès and Yaniv Plan. Matrix completion with noise. Proceedings of the IEEE, 98(6):925–936, 2010.

- Candès and Recht [2009] Emmanuel J. Candès and Benjamin Recht. Exact matrix completion via convex optimization. Foundations of Computational mathematics, 9(6):717–772, 2009.

- Candès and Tao [2010] Emmanuel J. Candès and Terence Tao. The power of convex relaxation: Near-optimal matrix completion. IEEE Transactions on Information Theory, 56(5):2053–2080, 2010.

- Candès et al. [2006] Emmanuel J. Candès, Justin Romberg, and Terence Tao. Robust uncertainty principles: Exact signal reconstruction from highly incomplete frequency information. IEEE Transactions on information theory, 52(2):489–509, 2006.

- Carpentier et al. [2016] Alexandra Carpentier, Olga Klopp, and Matthias Löffler. Constructing confidence sets for the matrix completion problem. In Conference of the International Society for Non-Parametric Statistics, pages 103–118. Springer, 2016.

- Chatterjee [2015] Sourav Chatterjee. Matrix estimation by universal singular value thresholding. Annals of Statistics, 43(1):177–214, 2015.

- Chatterjee [2020] Sourav Chatterjee. A deterministic theory of low rank matrix completion. IEEE Transactions on Information Theory, 66(12):8046–8055, 2020.

- Cho et al. [2017] Juhee Cho, Donggyu Kim, and Karl Rohe. Asymptotic theory for estimating the singular vectors and values of a partially-observed low rank matrix with noise. Statistica Sinica, pages 1921–1948, 2017.

- Davenport et al. [2014] Mark A. Davenport, Yaniv Plan, Ewout Van Den Berg, and Mary Wootters. 1-bit matrix completion. Information and Inference: A Journal of the IMA, 3(3):189–223, 2014.

- Donoho and Gavish [2014] David Donoho and Matan Gavish. Minimax risk of matrix denoising by singular value thresholding. Annals of Statistics, 42(6):2413–2440, 2014.

- Donoho [2006] David L. Donoho. Compressed sensing. IEEE Transactions on information theory, 52(4):1289–1306, 2006.

- Foygel et al. [2011] Rina Foygel, Ruslan Salakhutdinov, Ohad Shamir, and Nathan Srebro. Learning with the weighted trace-norm under arbitrary sampling distributions. arXiv preprint arXiv:1106.4251, 2011.

- Fu et al. [2020] Anqi Fu, Balasubramanian Narasimhan, and Stephen Boyd. CVXR: An R package for disciplined convex optimization. Journal of Statistical Software, 94(14):1–34, 2020. doi: 10.18637/jss.v094.i14.

- Goldberg et al. [2001] Ken Goldberg, Theresa Roeder, Dhruv Gupta, and Chris Perkins. Eigentaste: A constant time collaborative filtering algorithm. information retrieval, 4(2):133–151, 2001.

- Guo et al. [2013] Guibing Guo, Jie Zhang, and Neil Yorke-Smith. A novel bayesian similarity measure for recommender systems. In IJCAI, volume 13, pages 2619–2625, 2013.

- Keshavan et al. [2010] Raghunandan H Keshavan, Andrea Montanari, and Sewoong Oh. Matrix completion from noisy entries. The Journal of Machine Learning Research, 11:2057–2078, 2010.

- Király et al. [2015] Franz J Király, Louis Theran, and Ryota Tomioka. The algebraic combinatorial approach for low-rank matrix completion. J. Mach. Learn. Res., 16(1):1391–1436, 2015.

- Klopp [2014] Olga Klopp. Noisy low-rank matrix completion with general sampling distribution. Bernoulli, 20(1):282–303, 2014.

- Klopp [2015] Olga Klopp. Matrix completion by singular value thresholding: sharp bounds. Electronic journal of statistics, 9(2):2348–2369, 2015.

- Koltchinskii [2011] Vladimir Koltchinskii. Von Neumann entropy penalization and low-rank matrix estimation. The Annals of Statistics, 39(6):2936–2973, 2011.

- Koltchinskii et al. [2011] Vladimir Koltchinskii, Karim Lounici, and Alexandre B. Tsybakov. Nuclear-norm penalization and optimal rates for noisy low-rank matrix completion. The Annals of Statistics, 39(5):2302–2329, 2011.

- Lee and Shraibman [2013] Troy Lee and Adi Shraibman. Matrix completion from any given set of observations. In NIPS, pages 1781–1787, 2013.

- Linial et al. [1995] Nathan Linial, Eran London, and Yuri Rabinovich. The geometry of graphs and some of its algorithmic applications. Combinatorica, 15(2):215–245, 1995.

- Lovász [2012] László Lovász. Large networks and graph limits. American Mathematical Soc., 2012.

- Ma and Chen [2019] Wei Ma and George H Chen. Missing not at random in matrix completion: The effectiveness of estimating missingness probabilities under a low nuclear norm assumption. arXiv preprint arXiv:1910.12774, 2019.

- Mazumder et al. [2010] Rahul Mazumder, Trevor Hastie, and Robert Tibshirani. Spectral regularization algorithms for learning large incomplete matrices. Journal of Machine Learning Research, 11:2287–2322, 2010.

- Miao et al. [2016] Wang Miao, Peng Ding, and Zhi Geng. Identifiability of normal and normal mixture models with nonignorable missing data. Journal of the American Statistical Association, 111(516):1673–1683, 2016.

- Mohan et al. [2018] Karthika Mohan, Felix Thoemmes, and Judea Pearl. Estimation with incomplete data: The linear case. In Proceedings of the International Joint Conferences on Artificial Intelligence Organization, 2018.

- Montanari et al. [2018] Andrea Montanari, Feng Ruan, and Jun Yan. Adapting to unknown noise distribution in matrix denoising. arXiv preprint arXiv:1810.02954, 2018.

- Negahban and Wainwright [2011] Sahand Negahban and Martin J. Wainwright. Estimation of (near) low-rank matrices with noise and high-dimensional scaling. Annals of Statistics, pages 1069–1097, 2011.

- Nguyen et al. [2019] Luong Trung Nguyen, Junhan Kim, and Byonghyo Shim. Low-rank matrix completion: A contemporary survey. IEEE Access, 7:94215–94237, 2019.

- Obozinski et al. [2010] Guillaume Obozinski, Ben Taskar, and Michael I. Jordan. Joint covariate selection and joint subspace selection for multiple classification problems. Statistics and Computing, 20(2):231–252, 2010.

- Pimentel-Alarcón et al. [2016] Daniel L Pimentel-Alarcón, Nigel Boston, and Robert D. Nowak. A characterization of deterministic sampling patterns for low-rank matrix completion. IEEE Journal of Selected Topics in Signal Processing, 10(4):623–636, 2016.

- Rennie and Srebro [2005] Jasson D. M. Rennie and Nathan Srebro. Fast maximum margin matrix factorization for collaborative prediction. In Proceedings of the 22nd international conference on Machine learning, pages 713–719, 2005.

- Rohde and Tsybakov [2011] Angelika Rohde and Alexandre B. Tsybakov. Estimation of high-dimensional low-rank matrices. Annals of Statistics, 39(2):887–930, 2011.

- Singer and Cucuringu [2010] Amit Singer and Mihai Cucuringu. Uniqueness of low-rank matrix completion by rigidity theory. SIAM Journal on Matrix Analysis and Applications, 31(4):1621–1641, 2010.

- Sportisse et al. [2020] Aude Sportisse, Claire Boyer, and Julie Josse. Imputation and low-rank estimation with Missing Not At Random data. Statistics and Computing, 30(6):1629–1643, 2020.

- Weinberger and Saul [2006] Kilian Q. Weinberger and Lawrence K. Saul. Unsupervised learning of image manifolds by semidefinite programming. International journal of computer vision, 70(1):77–90, 2006.

- Yang et al. [2021] Chengrun Yang, Lijun Ding, Ziyang Wu, and Madeleine Udell. Tenips: Inverse propensity sampling for tensor completion. In International Conference on Artificial Intelligence and Statistics, pages 3160–3168. PMLR, 2021.

- You [2020] Kisung You. filling: Matrix Completion, Imputation, and Inpainting Methods, 2020. URL https://CRAN.R-project.org/package=filling. R package version 0.2.2.

- Zhu et al. [2019] Ziwei Zhu, Tengyao Wang, and Richard J Samworth. High-dimensional principal component analysis with heterogeneous missingness. arXiv preprint arXiv:1906.12125, 2019.