Granger Causality from Quantized Measurements

Abstract

An approach is proposed for inferring Granger causality between jointly stationary, Gaussian signals from quantized data. First, a necessary and sufficient rank criterion for the equality of two conditional Gaussian distributions is proved. Assuming a partial finite-order Markov property, a characterization of Granger causality in terms of the rank of a matrix involving the covariances is presented. We call this the causality matrix. The smallest singular value of the causality matrix gives a lower bound on the distance between the two conditional Gaussian distributions appearing in the definition of Granger causality and yields a new measure of causality. Then, conditions are derived under which Granger causality between jointly Gaussian processes can be reliably inferred from the second order moments of quantized measurements. A necessary and sufficient condition is proposed for Granger causality inference under binary quantization. Furthermore, sufficient conditions are introduced to infer Granger causality between jointly Gaussian signals through measurements quantized via non-uniform, uniform or high resolution quantizers. Apart from the assumed partial Markov order and joint Gaussianity, this approach does not require the parameters of a system model to be identified. No assumptions are made on the identifiability of the jointly Gaussian random processes through the quantized observations. The effectiveness of the proposed method is illustrated by simulation results.

keywords:

Causal inference; Granger causality; quantization., ,

1 Introduction

Causal inference is the determination of the qualitative cause-and-effect (or input versus output) relationships between two or more signals over time. Sometimes these relationships are obvious beforehand, but in many critical applications they are not. For instance, in environmental monitoring the direction in which a pollutant spreads may be unknown to begin with, making it difficult to determine a priori which measurements are inputs and which are outputs. In large manufacturing plants, the root cause of alarm signals is commonly obscured by complex feedback loops. A misunderstanding of the correct causal relationships not only reduces the accuracy of the subsequently identified model, but could mislead decision-makers into poorly founded interventions.

In 1963, the econometrician C. Granger introduced a definition of causality in terms of statistical prediction [23], inspired by the work of N. Wiener [59]. A signal is said to cause another signal if at some time, the optimal expected prediction error for a future value of is reduced by knowledge of past and , as compared to if the past values only of are known. In subsequent work [26, 25], Granger proposed a looser definition in terms of conditional probabilities, whereby is said to cause if, at some time, a future and past are conditionally dependent given past ; i.e., given past , past can still influence the future of . In the case of jointly Gaussian processes under a mean-square error prediction error, the first definition coincides with the second. These definitions allow causality from to as well, which would reflect mutual coupling between the two processes as they evolve over time.

As defined above, Granger causality is a ‘non-interventionist’ notion based on signals rather than systems. This suits applications where signals can only be measured, and cannot easily be adjusted through experiments. Under linear minimum mean-square error prediction, Granger [24] and Sims [49] showed the relationship between non-causality and zeroness of parameters in the vector autoregressive and moving average representations of the processes, respectively. In [11], a connection with linear systems theory is introduced through the idea of feedback-freeness for wide-sense stationary vector random processes having a block triangular representation, which is shown to be equivalent to Granger non-causality under linear minimum mean-square error prediction. Later in [10], a more restrictive version called strong feedback free processes, having block-diagonal innovation covariance were introduced and their equivalence to strictly causal linear systems was discussed. The relation between Granger non-causality and a linear time-invariant state space representation with a star graph structure as a network topology was considered in [32], and it was shown that Granger non-causality is equivalent to the existence of such a representation. Granger causality between processes corrupted by additive noise or affected by filtering or sampling has also been investigated [50, 42, 6, 20, 51, 4].

Based on the probabilistic definition of Granger causality, non-parametric measures of causality have been proposed in terms of directed information [5, 35, 46, 47] and transfer entropy [55]. These measures are based on the Kullback-Leibler distance and take value zero iff there is no causality. Typically they also assume a finite joint Markov order for the joint process. For the special case of Gaussian processes, they generally reduce to the directed log-covariance measures introduced in [21].

In this paper, we focus on the effects of quantization on Gaussian signals. We investigate methods for inferring Granger causality between two jointly Gaussian, stationary signals using quantized measurements. Quantization serves to reduce the communication load when transmitting sensor data. In industrial systems, this facilitates efficient fault diagnosis and root-cause analysis when sensor readings exceed or drop below certain thresholds, without consuming excessive network bandwidth [31]. Quantization is also potentially important in remote environmental monitoring, where a strong causal relationship in one direction between two nearby field sensors may indicate the direction of spatial flow or movement of a population of animals, a pollutant, and so on. Quantization here reduces transmission power and prolongs battery life. Evidently, the nonlinearity introduced by the quantizers moves this problem beyond the linear systems realm of the literature above.

Our main contributions are as follows:

-

•

Assuming a partial finite-order Markov property, we introduce a causality matrix comprising joint process covariances, and show that Granger causality is characterized in terms of its rank. The basis of our analysis is a necessary and sufficient rank condition for two conditional Gaussian distributions to be identical (Theorem 5). This extends a recent result of [52, 53] on Gaussian conditional independence. To the best of our knowledge, this causality matrix has not been previously studied in the system identification or causality literature.

-

•

We present a geometric interpretation of the smallest singular value of the causality matrix which can be regarded as the distance between the two conditional Gaussian distributions appearing in the definition of Granger causality, yielding a new measure of the strength of causality.

-

•

We then consider binary quantization, employing Van Vleck’s formula [56] to express the relation between the statistics of the quantized and unquantized signals. We derive a necessary and sufficient condition to infer Granger causality between Gaussian signals from binary measurements (Theorem 1). This holds even though the variances of the unquantized signals may not be identifiable.

-

•

Next we consider multi-level quantizers and derive sufficient conditions under which Granger causality between jointly Gaussian signals can be inferred from the second order moments of their quantized versions (Theorem 3). This uses a perturbation analysis of the causality matrix introduced above, bounds on covariances of quantization error terms combined with the Eckart-Young-Mirsky approximation theorem. Exploring this result, we derive sufficient conditions for three cases:

-

a)

non-uniformly quantized measurements with finite number of quantization levels (Proposition 7),

-

b)

uniform quantization with infinitely many quantization levels (Proposition 1),

-

c)

high resolution quantization (Proposition 1).

To express the relationships between the covariances of quantized and unquantized signals, we exploit Price’s Theorem [45] introduced in information theory and Widrow and Kollár’s results [58].

-

a)

Unlike much of the literature on causal inference, e.g. [36, 49, 21], our approach does not require the statistics of the underlying Gaussian signals to be estimated, or a system model to be explicitly identified apart from the finite partial Markov order.

Preliminary versions of these results have been accepted or presented in [3, 2]. Here, we provide full proofs for the binary and non-uniform quantization cases, improving the results compared with [2], and refine our previous results on high resolution quantization in [3]. We also introduce new results on uniform quantization with infinitely many levels, and new results on the interpretation of the smallest singular value of the causality matrix as a measure of causality. Moreover, we investigate the required ergodicity properties of the quantized data to be able to estimate their covariances. Further, we present a numerical example.

The paper is organized as follows. In Section 2, we characterize Granger causality between a pair of jointly Gaussian signals in terms of the rank of a special matrix of covariances. Then we introduce an interpretation for the smallest singular value of the matrix as a measure of the strength of causality. In Section 3 we derive necessary and sufficient conditions for Granger causality using binary quantized signals. In Section 4, we investigate the effects of multi-level quantization and derive sufficient conditions for inferring Granger causality between the unquantized signals from the statistics of the quantized data. Using different techniques, we focus in Section 5 on infinite-level uniform quantization, including the high-resolution case. The empirical estimation of second order moments of the quantized processes is discussed in Section 6. Some simulation results are presented in Section 7 demonstrating the proposed methods. Section 8 concludes the paper.

Notation: Throughout this paper, we denote the random process segments by , and by . We use the conventions that when , and equals the empty sequence when or . Similarly, is the empty sequence when . When clear from context, the full sequence is written as . For a parameter , the overline and underline (, ) denote known upper and lower bounds, respectively. We also denote by the short-hand notation .

2 Granger causality investigation

Let us first begin with the definition of causality between discrete-time stochastic processes, in terms of conditional independence. Let be discrete-time random processes on the time-axis . In 1980, Granger [25] defined that does not cause if:

where denotes conditional probability measure. Otherwise, if for some there is a nonzero probability that , then causes .

In other words, causes if and only if (iff) there is a nonzero chance that at some time , the value of could still be stochastically influenced by past , even if all past values of up to time are known. If does not cause , the values of are always conditionally independent of past , given past .

Now let us assume the following:

Assumption 1 (Partial Markov-).

The random process is partially Markov of order in and , that is, .

Remark 2.

This is strictly weaker than being joint Markov for the same order , and allows the -process to potentially have a much higher-order dependence on the past. For instance, let us consider and where and are independent white noise and or are nonzero. In this example, and are joint Markov of order two while the process is partially Markov of order one. This example can easily be extended so that and are joint Markov of arbitrarily high or infinite order, while remains partial Markov-1. In other words, the partial Markov assumption gives us extra flexibility. It can also be shown that having finite partial Markov orders in each direction does not necessarily imply a finite joint Markov order, unless and are also assumed to be conditionally independent given and .

With this restriction, we define Granger causality as follows:

Definition 3 (Granger Causality).

The random process is said to not Granger cause (GC) if:

| (1) |

Otherwise, if for some there is a nonzero probability that , then is said to GC .

Remark 4.

We assess Granger causality definition from time rather than to avoid technical issues about initial conditions. Different authors have treated the initial condition differently; see e.g. [19]. In [11, 51, 6], time starts from negative infinity while Granger [25] considers the starting time . In any case, it makes no practical difference because when we infer Granger causality, we need a large number of data points.

As the conditioning term on the RHS is no longer nested (i.e. included) in that of the LHS, this is no longer a conditional independence relationship. In much of the literature e.g. [35, 47, 46], it is assumed that under non-causality the process is also Markov-, so that can be dropped from the RHS. However, finite-order partial Markovianity does not generally imply finite-order marginal Markovianity. In this paper, we do not make any a priori assumption on the Markovianity of , but show that for jointly Gaussian signals, (1) and Assumption 1 imply that is marginally Markov-, under a mild additional requirement.

For jointly Gaussian processes, it turns out that (1) can be expressed in terms of a rank condition. We first present this condition for general jointly Gaussian random vectors with joint covariance matrix . The covariance matrices between subsets of variables are denoted by matching subscripts, for instance is the cross-covariance matrix between and , while is the covariance matrix for the random vector .111For convenience we adopt this mild abuse of notation, rather than .

Theorem 5.

Let be jointly Gaussian random vectors with joint covariance matrix , and suppose that the random vector has positive definite covariance. Then the following statements are equivalent:

-

1.

The conditional distributions and are identical.

-

2.

(4) where is the dimension of the random vector .

-

3.

.

See Appendix A.

Remark 6.

The second item in this result is a variation of a recent rank formula for Gaussian conditional independence, due to Sullivant [52, 53]. Under joint Gaussianity, the positive definiteness of excludes degenerate cases where deterministic (affine) relationships exist between , and . With additional analysis, it can be shown that if is constant (requiring this positive definiteness to be relaxed), then the formula of [52, 53] for conditional independence can be recovered as a special case. However, this extension is not needed for our purposes. The third item in this result shows that if and only if conditional independence between and between immediately follow given .

Now suppose that are jointly stationary Gaussian signals satisfying Assumption 1. Further assume that they are each scalar-valued, for simplicity, and that there is never a deterministic relationship between and .

Definition 7 (Causality Matrix).

The causality matrix is defined as:

| (6) |

where , , , and . The covariances and are matrices, and is an matrix.

The causality matrix depends on the cross-covariances between and and the autocovariances of , but not on the autocovariances of . Let us first make the following assumption:

Assumption 8.

Let be jointly stationary scalar Gaussian signals satisfying Assumption 1. Further assume that there is no deterministic relationship between any of the components of at any time .

We have the following:

Theorem 9.

Suppose Assumption 8 holds.

-

i)

does not Granger cause if and only if

(7) -

ii)

If does not Granger cause , then is marginally Markov-, i.e.

(8) -

iii)

If then .

See Appendix B.

Remark 10.

A distinguishing feature of this result is that it allows Granger causality to be inferred directly from the second-order statistics of the signals, without having to analyze or fit a linear dynamical model as is often done in the literature.

Remark 11.

The assumption of no deterministic relationship between any of the components of in Theorem 9 is more relaxed than Axiom B in Granger’s paper [25] which assumes no deterministic relationship between any of the components of . For instance, the process where are independent and identically distributed is covered by Theorem 9 but not by [25]. This is a stationary random process which evolves periodically from its initial conditions. The last item in Theorem 9 does not require the assumption of no deterministic relationship between any of the component of at any time .

Remark 12.

One of the implications of the last item in Theorem 9 is that the last block column in (6) is not needed when the rank condition in (7) is evaluated, that is (7) can be replaced by . However the last block column is kept since it is used in the following Sections when sufficient conditions in terms of the smallest singular value are derived.

2.1 Measure of causality

We now introduce a geometric interpretation of the smallest singular value of the matrix introduced in Theorem 5. To do so, we consider the distance between the two conditional means of and . The distance is measured by the variance of their differences. Under the assumption of joint Gaussianity, equality of the conditional means implies equality of the conditional distributions. Hence this variance is a measure of distance between the conditional distributions. We show here that the smallest singular value of the matrix appearing in Theorem 5 gives a lower bound on this distance.

Theorem 13.

Let be jointly Gaussian random vectors with joint covariance matrix , and suppose that the random vector has positive definite covariance. Further assume that is scalar.

The variance of difference between the conditional means of distributions and is lower bounded as follows:

| (11) |

where the positive

| (12) |

mainly depends on the statistics of and does not depend on the random variable .

See Appendix C. Obviously in (13) is always positive due to the assumption on the positive definiteness of the covariance matrix of the random vector . Hence, the only way to have the lower bound zero is:

| (15) |

In this case, the matrix of interest is not full rank and Theorem 5 implies that the conditional distributions coincide. As the smallest singular value increases, the lower bound on the distance between the two conditional distributions grows.

Based on the analysis above, the smallest singular value of the causality matrix lower-bounds the distance between the two conditional Gaussian probability measures appearing in the definition of Granger causality. We interpret as a measure of the strength of Granger causality. Comparing with Geweke’s measure of causality [21], some of the properties of the measure introduced in this paper are as follows:

-

•

.

-

•

Like Geweke’s measure, if and only if does not Granger cause .

-

•

The smallest singular value has a geometric interpretation as a lower bound on the distance between the two conditional Gaussian probabilities. It is not scale-invariant while Geweke’s measure is scale-invariant, being the ratio between two conditional variances.

3 Granger causality under binary quantization

In this Section, we consider zero-mean jointly Gaussian stationary signals and passing through binary quantizers with zero thresholds. The zeroness of the mean can be checked by counting if the numbers of the values of the quantized outputs at both quantization levels are equal. Alternatively, a DC notch filter can be applied before quantization to enforce the zero mean. Note that preprocessing of data before quantization and transmission to the central data analysis point is standard, see e.g. [41]. Preprocessing occurs on signals and separately. Therefore the Granger causality between and must be assessed at a central data analysis point, using the quantized versions of both. If a mean is nonzero, this is equivalent to assuming that the respective quantizer threshold is set equal to it. The observed signals are and , respectively. We are interested in revealing whether or not Granger causes , using the statistics of the quantized signals only.

In the causality matrix defined in (6), covariances ( and ) and the variance of signal () are required. However, the variance of zero-mean Gaussian signals passed through a binary quantizer with threshold zero cannot be estimated, e.g. [39]. Hence, some of the elements of cannot be estimated.

In order to solve this issue, a modified matrix is constructed. We know that if is a nonsingular matrix, then . Let us construct a diagonal matrix where the numbers of and entries equal and , respectively. Now instead of determining the rank of the causality matrix , the rank of

| (16) |

whose elements are the cross-correlation coefficients between signals and and the auto-correlation coefficients of signals is obtained. The relation between auto-correlation coefficients of a zero-mean Gaussian signal passing through the binary quantizer with zero threshold and outputs -1 and +1 and the covariance of output of the binary quantizer can be estimated through Van Vleck’s formula [56].

Suppose that two zero-mean jointly Gaussian random variables and with correlation coefficient are quantized by binary quantizers with zero thresholds and the outputs are and , respectively:

| (17) |

It can be shown that a relation similar to Van Vleck’s formula holds between auto-/cross-correlation coefficients of the jointly Gaussian random variables and the covariances of the quantized variables as follows:

| (18) |

In fact, in order to investigate Granger causality in this Section, the elements of the causality matrix are modified to construct the matrix depending just on the correlation coefficients. The reason is that the variances of zero-mean Gaussian signals after binary quantization with the threshold zero are not identifiable. However, the rank of equals the rank of the causality matrix.

Using Theorem 9 and Remark 12, the following necessary and sufficient condition on Granger causality between signals quantized by binary quantizers can be stated:

Theorem 1.

Let satisfy Assumption 8 and be zero mean. Then does not Granger cause if and only if the matrix (16) is not full rank. The elements of the matrix are auto- and cross-correlation coefficients associated with ( and ) obtained as follows:

| (19) | ||||

| (20) | ||||

| (21) |

where and are, respectively, cross- and auto-covariance estimates of one-bit measurements observed through binary quantizers with zero thresholds and values -1 and +1.

Remark 2.

Note that the necessity and sufficiency of the result follows from the fact that (18) provides us a closed form relationship between the correlation coefficients of the unquantized signals and the covariance of their quantized versions. Thus, the correlation coefficients of zero-mean jointly Gaussian signals can be obtained. Furthermore, the rank of the causality matrix and of the matrix constructed by correlation coefficients are equal. Hence, Theorem 9 and Remark 12 imply the necessity and sufficiency on Granger causality between jointly zero-mean Gaussian, stationary random processes.

4 Inferring Granger causality using finite-level quantized data

In this Section, the impact of finite-level quantization on the inference of Granger causality between the jointly Gaussian, stationary processes and where is partially Markov of order is investigated. Using the second-order statistics of the quantized data, we construct a post-quantization matrix that mirrors the causality matrix (6) of the unquantized processes. We then show that if the difference between these two matrices is sufficiently small, then the full-rankness of implies that Granger causes (GC) . In the following Subsection, some preliminary results useful for inferring Granger causality through quantized signals are presented.

4.1 Preliminaries

Theorem 9 implies that if for some the causality matrix has full rank , then GC . The question here is whether we can infer this causal relationship from the covariances of the quantized data. To answer this question, we will use a classical result in linear algebra:

Theorem 1.

Remark 2.

Unless otherwise stated, denotes either two-norm () or Frobenius norm () in the following.

4.2 Granger causality inference under quantization

In this Subsection, the relationship between the causality matrix and its counterpart constructed by quantized signals is investigated. Using the results above, a condition to determine the rank of the causality matrix through the rank of its counterpart is derived.

4.2.1 Relationship between and

We begin with the relationship between the scalar covariances , of the unquantized signals, and , of their quantized versions, where superscript Q on a signal denotes the quantized version. For convenience, in the following we suppress time lags and use and to denote and/or . We have

| (24) |

where and denote the quantization errors of and respectively (). Now define the matrix

| (26) | ||||

| (27) |

where is defined as:

| (30) | ||||

| (32) |

which is the matrix version of the scalar relationship (24).

Theorem 3.

Denote the full-rank matrix by . If is any other matrix of the same dimensions but lower rank, then Eckart-Young-Mirsky matrix approximation Theorem (Theorem 1) states that . Conversely, if , then remains full-rank. Setting , we see that if , then is guaranteed to be full-rank. Theorem 9 then implies that GC .

Remark 4.

This result states that GC can be inferred from the statistics of the quantized data, provided that the quantization perturbation, as measured by , is smaller than , which can be taken as a measure of how far is from losing full rank. However, both sides of inequality (33) depend on the quantization schemes. We can derive a condition that compares the size of the quantization perturbation to the statistics of the unquantized processes, as follows. We know that for two matrices and of the same dimension , ([30], Problem 7.3.P16). Therefore, we have:

| (34) |

Furthermore, we know that . So if

| (35) |

then by (34) it is guaranteed to be smaller than as required. Finally, note that since , the condition (35) may be equivalently written as

| (36) |

which can be achieved with sufficiently fine quantization iff is full-rank.

Remark 5.

Note that Theorem 3 and Remark 4 hold not only for quantization but also for perturbations such as other nonlinearities or additive noise. In such cases, is the additive perturbation on the causality matrix and the smallest singular value in Theorem 3 corresponds to the matrix of covariances formed by the perturbed signals.

4.3 Granger causality under non-uniform quantization

In this Subsection we consider a general case of Granger causal inference with non-uniform, finite-level quantization. With more than two levels, we no longer have recourse to (18), which recovers the correlation coefficients of the unquantized signals from the covariances of their binary versions. Our approach here, as presented in Subsection 4.2, is to formally construct and analyze a matrix of the same form as the causality matrix (6), but in terms of the covariances of the quantized processes. As the quantized signals are not jointly Gaussian anymore, this matrix cannot be regarded as a causality matrix. We denote such a matrix by . Using the perturbations caused by quantization on the covariances of unquantized signals and the rank of the matrix , we then derive sufficient conditions to determine whether the causality matrix is full rank. Then Theorem 9 implies that Granger causes (Proposition 7).

In the following Subsection, the relation between covariances of quantized and unquantized signals is first derived, using Price’s theorem [45, 43]. Price’s theorem has been previously used in the literature to study the determination of autocorrelations and variances from data passed through quantizers or other nonlinearities [12, 39].

4.3.1 Relation between covariance of quantized and unquantized signals

For convenience, in the following jointly Gaussian random variables are denoted by and which can be and/or at different times and lags.

Let us consider two zero-mean jointly Gaussian random variables and with correlation coefficient that are quantized by non-uniform finite-level quantizers. Their quantized versions are denoted by and , respectively:

| (37) | ||||

| (38) |

where and are the number of quantization levels, ’s and ’s denote the thresholds of the quantizers and and are levels of quantizers. Note that and can be infinite. Without loss of generality, suppose that the quantizer levels are increasing ( and , ). Recall that the joint probability density function of and is as follows:

| (39) |

where and are the standard deviations of the random variables and , respectively.

Theorem 6 (Price’s Theorem).

Let and be jointly Gaussian random variables with joint probability density function and is some function such that where then

| (40) |

where is covariance between and .

Using Price’s Theorem, the covariance between quantized signals and can be obtained as follows. See Appendix D for derivation of (4.3.1):

| (41) |

Note that after quantization we do not have access to the values of correlation coefficients and of the standard deviations and (with one single subscript). In the following, we find upper bounds on and then we exploit such bounds to guarantee the causality matrix is full rank. In other words, to apply Theorem 3 for non-uniform quantized signals, the norm of , whose components are the differences between covariances of unquantized and quantized signals and as defined in (30), needs to be bounded.

4.3.2 Granger causality investigation through non-uniformly quantized signals

Let zero-mean jointly Gaussian stationary random processes and be quantized by non-uniform quantizers of the form (37) and (38) with and levels, thresholds and , and quantization levels and , respectively.

For convenience, we assume that the quantizer levels are increasing. We wish to determine whether Granger causes , using the statistics of the quantized data and .

Our approach is to use upper bounds on and to find an upper bound on the norm of . If this bound is less than , then Theorem 3 implies Granger causes . Let

| (42) | ||||

| (43) | ||||

| (44) |

where and are functions of correlation coefficient given by (4.3.1) and is given by where is the univariate Gaussian density function. The parameters and are upper bounds on and respectively, and are upper bounds on the standard deviations of and , respectively, and and are, respectively, lower bounds on the standard deviations of and .

An upper bound on in (33) is obtained as follows. We know that for , we have where and .

Note that the elements of the causality matrix are the covariances between and and the variance of and the covariances between . The maximum difference between the components of the causality matrix and the matrix can be obtained using (42)-(44) or through Appendix E. First upper bounds on and are derived as follows:

| (45) |

and

| (46) |

Using (45), (46) and Theorem 3, the following can be presented:

Proposition 7.

Let satisfy Assumption 8 and be zero mean. Suppose there exists some such that the matrix , involving covariances of the data obtained by non-uniform quantizers, is full-rank. Then Granger causes , provided that the following condition is satisfied:

| (47) |

where and are defined in (45) and (46), is the smallest singular value of and , and are defined in (42)-(44).

Remark 8.

Note that we do not make assumption on the identifiability of the second-order statistics of the unquantized jointly Gaussian signals through quantized measurements. The a priori information required to exploit Proposition 7 are the upper bounds on the cross-correlation coefficients between signal and (), the auto-correlation coefficients of at nonzero lags (), and the range of the standard deviation of ( and ).

Remark 9.

Sufficient condition (47) is useful for investigating Granger causality between jointly Gaussian signals through quantized observations. The RHS can be estimated from the quantized data available and the LHS of the condition depends on the quantizer specifications and on prior knowledge of bounds on the underlying jointly Gaussian statistics (, , and ).

Remark 10.

It can be shown that (47) is satisfied if:

| (48) |

where is the smallest singular value of the causality matrix . Note that the RHS of (48) does not depend on the quantization scheme and can be lower-bounded in terms of the prior bounds on the underlying statistics, if the underlying system is indeed causal. The difference between the LHS and RHS can be thought of as a causality margin, which we would like to be as large as possible. This can be achieved by designing quantization parameters so that the LHS is as small as possible, subject to constraints on the number of levels available. This leads to designs that may be very different from minimum mean square error (MMSE) quantizers.

Remark 11.

The approaches described in Sections 3 and 4 can be exploited for Granger causality inference of jointly Gaussian processes passing through other nonlinearities as well. Two cases can be considered. The first one is about nonlinearities whose relations between covariances or correlation coefficients of jointly Gaussian signals and second-order moments of output signals from the nonlinearity are invertible. For such situations, necessary and sufficient conditions for inferring Granger causality similar to Section 3 using Price’s Theorem and Theorem 9 can be introduced. The second cases are nonlinearities where the identifiability is not guaranteed. Sufficient conditions to infer Granger causality between the jointly Gaussian signals using approaches similar to Section 4 can be derived. In fact, first the relationship between covariances of jointly Gaussian signals and output signals from nonlinearities through Price’s Theorem can be obtained. Then bounds on the difference between covariances of jointly Gaussian signals and of the output signals from nonlinearities can be developed. And finally Theorem 3 to derive sufficient conditions can be used.

Remark 12.

If the quantizers both have a threshold and at the origin, then an alternative approach is to lump the positive and negative quantization intervals together and then apply the binary quantizer results of section 3. However, the multilevel quantization approach of this section has the advantage that the empirical

estimation of the covariances of the quantized signals is expected to become more accurate as the number of levels increases, see e.g. [54] and references therein for discussion.

We further remark that

by numerically inverting (4.3.1) and similar equations, the unquantized variances and correlation coefficients can be recovered exactly from the (co)variances of the quantized signals. In principle, causality or non-causality could then be determined from the rank of (16). However, when used on empirical estimates of the quantized signal statistics, this technique can be unreliable since it can be shown that becomes arbitrary large if the underlying correlation coefficient is sufficiently strong. This

is called the law of propagation of variance (or of statistical error); see e.g. [16] for discussion. In contrast, the approach taken in Proposition 7 does not require inverting the functions and does not suffer from such issues.

5 Granger causality using infinite-level uniformly quantized data

In this Section, Granger causality between jointly Gaussian signals is investigated when there is an infinite number of quantization levels. In the following Subsection, we focus mainly on the high resolution regime where the resolution of the quantizers is sufficiently fine, i.e. . The case of infinite-level quantization with finite resolution is explored in Appendix F.

Infinite-level quantization has been studied in control systems [18], system identification [27, 48], communications [58], etc. Although practical quantizers have a finite number of levels, in the case of input signals with unbounded support they are difficult to analyse, because of the unbounded overload regions. In contrast, infinite-level quantizers have no overload regions to complicate the analysis. If the probability mass in the overload regions is sufficiently small, then an infinite-level quantizer is a reasonable approximation.

5.1 High-resolution quantization

Recall that denote and/or at different time lags and are the corresponding quantization error terms. By analysing the infinite sums representing covariances between quantization errors and signals for sufficiently small , it is shown in Appendices I and J that the last three terms on the RHS of (24) can be expressed as follows:

| (49) | ||||

| (50) | ||||

| (51) |

where is Bachmann-Landau -notation.

Furthermore, the variance of the quantized signal can be represented as follows as shown in Appendix K:

| (52) |

In Appendix L, we show that in the high resolution regime:

| (53) |

where is the upper bound on the cross-covariance between signals and . The following result then follows immediately from Theorem 3:

Proposition 1.

Remark 2.

This result gives an explicit formula in the high-resolution regime for deciding how finely quantized and should be in order to infer causality from , which can be constructed through quantized signals available. As in the quantization perturbation bound in Theorem 3, the RHS depends on the quantization scheme. Using (36) and (5.1), we can establish a quantizer-independent one hand side as follows:

| (56) |

where .

Note the LHS suggests that plays a more critical role than . This is related to the fact that in the causality matrix , appears only in cross-covariances with , whereas also appears in auto-covariances with lag zero. Even if is coarse, the inequality can be satisfied by choosing a sufficiently fine . Conversely, if is small, would still have to be small to satisfy (56). Indeed it can be shown that for the LHS to be as small as possible, we require

, i.e. the resolution in should be exponentially finer than the resolution in . Furthermore, to improve the causality margin, the LHS can be minimized with respect to and under appropriate constraints on quantization resolution, e.g.

(which can be interpreted as the total expected bit rate in a variable-rate code for quantized and ).

6 Estimation of second-order statistics of quantized data

In this section, we establish that the auto- and cross-covariances between the quantized data can be consistently estimated, enabling the matrix to be constructed. To do so, the ergodic theorem is exploited.

First, we state the following theorem.

Theorem 1.

Let be a stationary, ergodic -variate vector process and be a measurable function . Let define an -variate vector process . Then is stationary ergodic.

See Appendix M. It follows the same line of [8] with modifications to allow vector processes. Theorem 1 implies that jointly Gaussian stationary, ergodic signals and remain stationary and ergodic after quantization ( and ). Furthermore, the Theorem implies that the products , , are also stationary and ergodic, for instance, by defining , . This enables us to exploit the Ergodic Theorem to estimate the covariance functions of the quantized signals.

Theorem 2 (Ergodic Theorem [8]).

Suppose is a strict-sense stationary and ergodic univariate process with , then almost surely and in the first mean

| (57) |

In the following, and denote and/or .

Remark 3.

The standing assumption in this Section is that the unquantized processes are ergodic. For multivariate continuous-time Gaussian processes [1] and univariate discrete-time Gaussian processes [13], it is known that ergodicity follows under stationarity if the auto- and cross-covariances vanish as the lag approaches infinity. In Appendix N, this result is extended to stationary multivariate discrete-time Gaussian processes.

6.1 Auto- and cross-covariance estimators of quantized signals with zero mean

In order to estimate the auto- and cross-covariance between quantized signals with mean zero, Theorem 2 can be used. For instance, the cross-covariance between quantized signals with mean zero and at lag can be estimated as follows. Define and note that as discussed after Theorem 1, is stationary and ergodic. Furthermore, it is clear that is finite. The following almost surely and in the first mean convergent estimator can be presented:

| (58) |

6.2 Auto- and cross-covariance estimators of quantized signals with non-zero mean

For non-zero mean quantized signals, we can still use the theorem as follows. We know that:

| (59) |

Each terms on the right hand side of (59) can be estimated through Theorem 2. Let us first mention the following theorem:

Theorem 4.

[15] Let be a Borel function, continuous at . If almost surely, then almost surely.

Using Theorem 4, with and , the following almost surely convergent estimator can be obtained:

| (60) |

7 Simulation

In this Section, numerical examples are presented to illustrate the proposed methods. We consider the following second order processes from [22]:

| (61) | ||||

| (62) |

where are assumed to be white Gaussian signals with zero mean and unit variance.

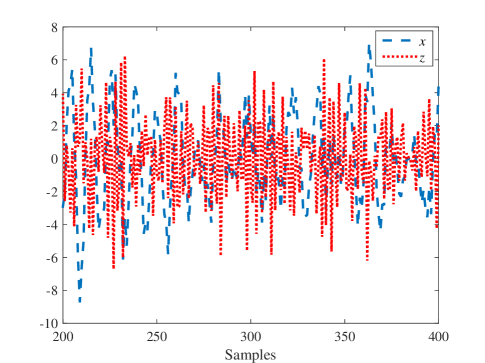

We collect samples from quantized versions of and to determine if Granger causes . The unquantized signals and are depicted in Fig. 1 to show how these signals change with each other over the period of samples . Note that we do not have access to such signals to investigate Granger causality. The process is partially Markov of order two. For noncausality cases, we change the coefficient of in (62), i.e. , to zero.

Note that empirical estimate of covariances at lag becomes less reliable when the lag approaches to the number of samples available. As a rule of thumb, it is suggested to estimate the covariances associated with at most a quarter of the number of samples () [57].

7.1 Binary quantization

In this Subsection, the signals and are quantized by binary quantizers with the thresholds zero and the quantization levels . Using the estimators of the previous Section, we estimate the smallest singular value in Theorem 1 to be 0.4697. The value is significantly different from zero. Thus, it shows that the causality matrix is full rank and therefore, Granger causes . The true smallest singular value equals 0.4807, which is close to the above-mentioned estimated value.

Now, we consider noncausality situation where the coefficient of in (62) is set to zero. In this situation, does not Granger cause . To investigate noncausality through binary quantized observations, data are collected after binary quantization and rank of the causality matrix is determined to apply Theorem 1. The smallest singular value is 0.0095 which is near zero. Hence, there is not strong evidence for the causality matrix to be full rank. We would therefore conclude that does not Granger cause .

7.2 Non-uniform finite-level quantization

We consider saturated quantizers with granular regions and associated, respectively, with and , and equal quantization intervals in the granular regions. The quantizer output is given by the lower boundary point of the corresponding cell; i.e. in the cell the value of quantizer is . If the quantizer input falls outside the granular region, the quantizer takes the value of the nearest quantizer point as described above. Let us consider that the variances are within intervals with widths 0.2 and upper bounds on auto-correlation coefficient of signal and cross-correlation between signal and are, 0.7 and 0.5, respectively.

The corresponding quantized versions of signals and with two-bit quantization depicted in Fig. 1 are shown in Fig. 2. The matrix constructed by the sample covariances of the quantized signals satisfies the sufficient condition (47), for . From Proposition 7, we conclude that Granger causes . If the true covariances of the quantized signals through (4.3.1) are used to determine the causality, the difference between the right and left hand sides of the sufficient condition of Proposition 7 is which is less than zero and it can be concluded that Granger causes .

Now let us set the coefficient of in (62) zero and calculate the sufficient condition (47). When the estimated and true covariances are used to construct the matrix , the values of are, respectively, greater than and for different values of . The values are significantly bigger than zero and we cannot conclude that Granger causes .

Now we investigate how the numbers of bits denoted by and associated with quantizers of signals and impact the determination of Granger causality using the approach given in Subsection 4.3. In Fig. 3, the sufficient condition (47), i.e. is depicted. As the numbers of bits increase, the perturbation reduces and the differences between LHS and RHS of (47) becomes more significant.

8 Conclusions

In this paper, first we showed a rank-based representation for the equality of two conditional jointly Gaussian random vectors. Assuming joint Gaussianity and a known partial Markov order, we introduce the notion of a causality matrix and show that Granger causality is equivalent to this matrix having full rank. We also introduced a geometric interpretation for the smallest singular value of the causality matrix. The smallest singular value is indeed a measure of the distance between two conditional Gaussian distribution functions appearing in the probabilistic definition of Granger causality. We exploited such an interpretation to introduce a new measure of causality.

Next a necessary and sufficient condition was proposed for assessing Granger causality under binary quantization. Furthermore, conditions under which causality can be inferred by using just the statistical properties of the quantized signals instead of estimating the statistics or model of the underlying Gaussian signals were introduced. Such conditions have been proposed for a range of quantizers including non-uniform, uniform and high resolution quantizers. Note that such an approach can be extended to other nonlinearities as well.

Future work will focus on obtaining statistical confidence intervals and convergence rates for the empirical estimators proposed here. Another open question involves relaxing the Gaussian assumption. In this case, it is likely that information-theoretic approaches based on directed information (see e.g. [5]) will prove useful. In addition, the verification of Gaussianity and determination of the unknown partial Markov order through quantized data are important topics for future study. The estimation of rank and singular values has been extensively studied in the literature, see e.g. [44, 34]. For practical use, the statistical properties of such estimators for the matrices introduced in this paper will need to be studied. We leave this as future work. A rigorous study of statistical efficiency with quantized data is beyond the scope of the current paper. However, one possible approach is to exploit results from [14] and verify its assumptions for quantized signals.

References

- [1] R.J. Adler. The Geometry of Random Fields. Wiley, London, 1981.

- [2] S. Ahmadi and G.N. Nair. Granger causality of Gaussian signals from binary or non-uniformly quantized measurements. In IFAC-PapersOnLine, pages 677–683. IFAC, 2021.

- [3] S. Ahmadi, G.N. Nair, and E. Weyer. Granger causality of Gaussian signals from quantized measurements. In 58th IEEE Conference on Decision and Control, pages 3587–3592. IEEE, 2019.

- [4] S. Ahmadi, G.N. Nair, and E. Weyer. Granger causality of Gaussian signals from noisy or filtered measurements. In IFAC-PapersOnLine, pages 506–511. IFAC, 2020.

- [5] P.O. Amblard and O.J.J. Michel. The relation between Granger causality and directed information theory: a review. Entropy, 15:113–143, 2013.

- [6] B.D.O. Anderson, M. Deistler, and J.-M. Dufour. On the sensitivity of Granger causality to errors-in-variables, linear transformations and subsampling. J. Time Ser. Anal., 40:102–123, 2019.

- [7] L.V. Benkevitch, A.E.E. Rogers, C.J. Lonsdale, R.J. Cappallo, D. Oberoi, P.J. Erickson, and K.A.V. Baker. Van Vleck correction generalization for complex correlators with multilevel quantization. arXiv:1608.04367, 2016.

- [8] L. Breiman. Probability. Society for Industrial and Applied Mathematics (SIAM), Philadelphia, 1992.

- [9] T.J.I’A. Bromwich. An Introduction to the Theory of Infinite Series. Macmillan & Co., London, 1908.

- [10] P. Caines. Weak and strong feedback free processes. IEEE Trans. Autom. Contr., 21:737–739, 1976.

- [11] P. Caines and C. Chan. Feedback between stationary stochastic processes. IEEE Trans. Autom. Contr., 20:498–508, 1975.

- [12] S. Cambanis and E. Masry. On the reconstruction of the covariance of stationary Gaussian processes observed through zero-memory nonlinearities. IEEE Trans. Inform. Theory, 24:485–494, 1978.

- [13] H. Cramér and M.R. Leadbetter. Stationary and Related Stochastic Processes: Sample Function Properties and Their Applications. Wiley, New York, 1967.

- [14] A.V. Dandawate and G.B. Giannakis. Asymptotic theory of mixed time averages and kth-order cyclic-moment and cumulant statistics. IEEE Trans. Inform. Theory, 41:216–232, 1995.

- [15] J. Davidson. Stochastic Limit Theory. Oxford University Press, New York, 1994.

- [16] E.W. Deming. Statistical Adjustment of Data. John Wiley and Sons Interscience, New York, 1948.

- [17] C. Eckart and G. Young. The approximation of one matrix by another of lower rank. Psychometrika, 1:211–218, 1936.

- [18] N. Elia and S.K. Mitter. Stabilization of linear systems with limited information. IEEE Trans. Autom. Contr., 46:1384–1400, 2001.

- [19] J.P. Florens and M. Mouchart. A note on noncausality. Econometrica, 50:583–591, 1982.

- [20] E. Florin, J. Gross, J. Pfeifer, G.R. Fink, and L. Timmermann. The effect of filtering on Granger causality based multivariate causality measures. Neuroimage, 50:577–588, 2010.

- [21] J.F. Geweke. Measurement of linear dependence and feedback between multiple time series. J. Am. Stat. Assoc., 77:304–313, 1982.

- [22] B. Gourévitch, R. Le Bouquin-Jeannés, and G. Faucon. Linear and nonlinear causality between signals: methods, examples and neurophysiological applications. Biol. Cybern., 95:349–369, 2006.

- [23] C.W.J. Granger. Economic processes involving feedback. Inf. Control, 6:28–48, 1963.

- [24] C.W.J. Granger. Investigating causal relations by econometric models and cross-spectral methods. Econometrica, 37:424–438, 1969.

- [25] C.W.J. Granger. Testing for causality: a personal viewpoint. J. Econ. Dyn. Control, 2:329–352, 1980.

- [26] C.W.J. Granger and P. Newbold. Forecasting Economic Time Series. Academic Press, New York, 1977.

- [27] F. Gustafsson and R. Karlsson. Statistical results for system identification based on quantized observations. Automatica, 45:2794–2801, 2009.

- [28] L. Guttman. Enlargement methods for computing the inverse matrix. Ann. Math. Statist., 17:336–343, 1946.

- [29] J.B. Hagen and D.T. Farley. Digital correlation techniques in radio science. Radio Sci., 8:775–784, 1973.

- [30] R.A. Horn and C.R. Johnson. Matrix Analysis. Cambridge University Press, Cambridge, 2013.

- [31] W. Hu, J. Wang, T. Chen, and S.L. Shah. Cause-effect analysis of industrial alarm variables using transfer entropies. Control Eng. Pract., 64:205–214, 2017.

- [32] M. Józsa, M. Petreczky, and M.K. Camlibel. Relationship between Granger noncausality and network graph of state-space representations. IEEE Trans. Autom. Contr., 64:912–927, 2019.

- [33] T. Kailath, A.H. Sayed, and B. Hassibi. Linear Estimation. Prentice-Hall, New Jersey, 2000.

- [34] F. Kleibergen and R. Paap. Generalized reduced rank tests using the singular value decomposition. J. Econom., 133:97–126, 2006.

- [35] I. Kontoyiannis and M. Skoularidou. Estimating the directed information and testing for causality. IEEE Trans. Inform. Theory, 62:6053–6067, 2016.

- [36] M. Laghate and D. Cabric. Learning wireless networks’ topologies using asymmetric Granger causality. IEEE J. Sel. Topics Signal Process., 12:233–247, 2018.

- [37] G. Lindgren. Stationary Stochastic Processes: Theory and Applications. Chapman and Hall/CRC, Florida, 2012.

- [38] M. Lundquist and W. Barrett. Rank inequalities for positive semidefinite matrices. Linear Algebra Appl., 248:91–100, 1996.

- [39] E. Masry and S. Cambanis. On the reconstruction of the covariance of stationary Gaussian processes observed through zero-memory nonlinearities–part II. IEEE Trans. Inform. Theory, 26:503–507, 1980.

- [40] L. Mirsky. Symmetric gauge functions and unitarily invariant norms. Quart. J. Math. Oxford, 11:50–59, 1960.

- [41] A. Moffet. JPL work on superconducting filters. In Proc. of the Interference Identification and Excision Workshop, pages 91–95, 1982.

- [42] H. Nalatore, M. Ding, and G. Rangarajan. Mitigating the effects of measurement noise on Granger causality. Physical Review E, 75:031123, 2007.

- [43] A. Papoulis. Comments on ‘An extension of Price’s theorem’ by McMahon, E. L. IEEE Trans. Inform. Theory, 11:154–154, 1965.

- [44] F. Portier and B. Delyon. Bootstrap testing of the rank of a matrix via least-squared constrained estimation. J. Am. Stat. Assoc., 109:160–172, 2014.

- [45] R. Price. A useful theorem for nonlinear devices having Gaussian inputs. IEEE Trans. Inform. Theory, 4:69–72, 1958.

- [46] C.J. Quinn, T.P. Coleman, N. Kiyavash, and N.G. Hatsopoulos. Estimating the directed information to infer causal relationships in ensemble neural spike train recordings. J. Comput. Neurosci., 30:17–44, 2011.

- [47] C.J. Quinn, N. Kiyavash, and T.P. Coleman. Directed information graphs. IEEE Trans. Inform. Theory, 61:6887–6909, 2015.

- [48] R.S. Risuleo, G. Bottegal, and H. Hjalmarsson. Identification of linear models from quantized data: a midpoint-projection approach. IEEE Trans. Autom. Contr., 65:2801–2813, 2020.

- [49] C.A. Sims. Money, income and causality. Am. Econ. Rev., 62:540–552, 1972.

- [50] V. Solo. On causality I: sampling and noise. In 46th IEEE Conference on Decision and Control, pages 3634–3639. IEEE, 2007.

- [51] V. Solo. State-space analysis of Granger-Geweke causality measures with application to fMRI. Neural Comput., 26:914–949, 2016.

- [52] S. Sullivant. Algebraic geometry of Gaussian bayesian networks. Adv. in Appl. Math., 40:482–513, 2008.

- [53] S. Sullivant. Algebraic Statistics. American Mathematical Society, Providence, 2018.

- [54] A.R. Thompson, J.M. Moran, and G.W. Swenson. Interferometry and Synthesis in Radio Astronomy. Springer, Berlin, 2017.

- [55] R. Vicente and M. Wibral. Efficient estimation of information transfer. In Directed Information Measures in Neuroscience, pages 37–58. Springer, 2014.

- [56] J.H. Van Vleck and D. Middleton. The spectrum of clipped noise. Proc. IEEE, 54:2–19, 1966.

- [57] W.W.S. Wei. Time Series Analysis: Univariate and Multivariate Methods. Pearson, New Jersey, 2005.

- [58] B. Widrow and I. Kollar. Quantization Noise: Roundoff Error in Digital Computation, Signal Processing, Control, and Communications. Cambridge University Press, Cambridge, 2008.

- [59] N. Wiener. The Theory of Prediction. McGraw-Hill, New York, 1956.

- [60] F. Zhang. The Schur Complement and Its Applications. Springer Science & Business Media, 2006.

Appendix A Proof of Theorem 5

We begin by showing that the first two items in the Theorem are equivalent.

The conditional Gaussian random vectors and have distributions as follows:

where and are conditional means and and are conditional covariances of the random vectors and , respectively. It can be shown, e.g. [33], that

| (63) | ||||

| (64) |

where

| (65) | ||||

| (66) |

In order for two Gaussian distributions to be identical, it is necessary and sufficient that they should have the same mean vector and covariance matrix. Let us begin with the equality of mean vectors (). Equating (63) and (64) and noting the positive definiteness of imply that the coefficients of linear relationship between , and appearing in must be zero. The coefficients are zero if and only if

| (67) | |||

| (68) |

Thus, if and only if (67) and (68) hold. It can be shown that if (67) and (68) are satisfied, the equality of the conditional covariance matrices and also holds. In other words, the conditional Gaussian probability density functions are equal () if and only if (67) and (68) are satisfied.

We know that a matrix is zero if and only if . Using Guttman rank additivity formula [28] for (67) and (68), we have:

| (71) | |||

| (74) |

There are two partitioned matrices whose second column is the same in the equations above. To deal with the ranks of these two matrices, let

| (77) |

Using Lemma 6 of [38], it follows:

| (82) | ||||

| (85) | ||||

| (86) |

We also have:

| (91) | ||||

| (92) |

And it follows that:

| (93) |

We can conclude that if the conditional Gaussian probability density functions are equal (), (67) and (68) are satisfied and in turn show that the rank criterion (93) holds. Therefore, one direction is proved.

In order to prove the converse, we should show that (71) and (74) are satisfied if (93) holds. Note that since is positive definite, (93) implies that both (71) and (74) hold.

Proof of item 3: Here we show that items 1 and 3 are equivalent. If item 1 in the Theorem holds, we know that (71) and (74) (and therefore (67) and (68)) are satisfied. Thus, (63) and (64) are both equal to , where is the conditional mean of given , . It follows that , where is the conditional covariance of given . This completes the proof.

Appendix B Proof of Theorem 9

We can apply Theorem 5 to (1) with , , and ,

to prove the first two parts of the Theorem.

To prove the last part, let us also define . We have:

| (94) |

where the first equality follows from the law of iterated expectations, the second equality follows from Assumption 1 and the third one is due to the assumption of the last part of the Theorem. The conditional variance of equals the conditional variance of as well. This completes the proof.

Appendix C Proof of Theorem 13

The variance of the difference between and can be upper and lower bounded using Rayleigh quotient theorem [30] as follows:

| (97) | ||||

| (100) |

where

| (103) |

, are defined in (65)-(66) and

| (104) | ||||

| (105) | ||||

| (106) |

Note that is a scalar random variable in this Theorem therefore and are column vectors. We have:

| (109) | ||||

| (110) |

where

| (113) |

Using Corollary 2.9 of [60], we have:

| (116) | ||||

| (119) |

Therefore, the lower bound on the variance between random variables and is as follows:

| (122) |

Furthermore, the smallest eigenvalue of the matrix is always positive since the matrix can be written as:

| (127) | ||||

| (133) |

and the covariance matrix of the random vector is positive definite by the assumption of the Theorem.

Now let us find a lower bound on . First note that can be expressed as follows:

| (138) |

where

| (141) |

Note that the matrix is positive definite since is positive definite. Furthermore, for a square matrix and a positive definite matrix it can be shown using the definition of eigenvalue and Rayleigh quotient theorem. Therefore, we can have:

| (144) | ||||

| (147) |

Moreover, we have:

| (151) | ||||

| (152) |

where the inequality above follows from Corollary 2.9 of [60].

Appendix D Derivation of equation (4.3.1)

Following [29, 7], we derive here the relationship between covariances of jointly Gaussian random variables quantized by two different non-uniform quantizers and correlation coefficients of the underlying jointly Gaussian random variables.

Let us consider and in Price’s Theorem. We have:

| (154) | ||||

| (155) |

where is Dirac delta function. The RHS of (40) can be written as follows:

| (156) |

Price’s Theorem implies that:

We have from the fundamental theorem of calculus:

| (157) |

Let us set which implies that:

| (158) |

Therefore, we have:

| (159) |

Thus, the covariance of quantized signals can be obtained as follows:

| (160) |

which is (4.3.1).

Appendix E Bounds on perturbation of covariances (Bounds on and )

To facilitate dealing with the integral (4.3.1) appearing in (42) and (43), an upper bound on the one-dimensional integrals can be obtained and then upper bounds on and on can be derived. In the following, we first find upper bounds on the function in integrand associated with (4.3.1) and then the integral and the maximum of the resulted upper bound are obtained to have upper bounds on and on .

For ease of notation, let us first use and to denote and/or in the following. The final bounds are presented for signal and at the end of this Section for convenience as well.

The exponential function in (4.3.1) can be bounded as follows:

| (161) | ||||

| (162) |

Let us define:

| (163) | ||||

| (164) |

where and .

Applying (161) - (164) to (4.3.1), the bounds on can be found as follows:

| (165) | |||

| (166) |

Thus the bound on is as follows:

For :

| (167) |

for :

| (168) |

In order to find the supremum of , we have to find the maximum value of its upper bounds and minimum value of its lower bounds. Note that the upper bound and the lower bound are odd functions in . Therefore, we just examine the maximum of and the minimum of for positive values of in the following.

The supremum of is as follows:

| (169) |

where

| (170) | ||||

| (171) |

For the signals and and their quantized versions, the derived bounds above can be expressed as follows. Note that

| (172) | ||||

| (173) |

where

| (174) |

can be or ,

| (175) | |||

| (176) | |||

| (177) | |||

| (178) |

and .

Appendix F Finite resolution quantization

We develop an upper bound on the norm of perturbation matrix caused by quantization and use Theorem 3 to introduce a sufficient condition to infer Granger causality between jointly Gaussian signals and using uniform quantized signals. To do so, we first derive an upper bound on the difference between covariances of quantized and unquantized signals in Appendix G. Unlike the previous Section, we use results from [58] on the cross-covariances of bivariate Gaussian random vectors that are subjected to infinite-level uniform quantization.

Proposition 1.

Let satisfy Assumption 8 and be zero mean. Suppose there exists some such that the matrix , involving covariances of the uniformly quantized data with and , is full-rank. Then Granger causes , provided that the following condition is satisfied:

| (179) | ||||

| (180) | ||||

| (181) |

where

| (182) | ||||

| (183) | ||||

| (184) |

with the Riemann zeta-function, is the smallest singular value of , and

| (185) | ||||

| (186) | ||||

| (187) | ||||

| (188) |

See Appendix H.

Remark 2.

Similar to Proposition 7, the RHS can be estimated from the quantized measurements, while the LHS can be determined a priori from the quantization parameters and the assumed bounds on the underlying signal statistics.

Remark 3.

Similar to Remark 10, we can derive the more stringent sufficient condition:

| (189) |

where the RHS no longer depends on the quantized signals.

Appendix G Bounds on quantization perturbation

First let us obtain an upper bound on the difference between covariances of quantized and of unquantized signals. Suppose that zero-mean, jointly Gaussian scalar signals and are passed through uniform quantizers with quantization intervals of length and , respectively, with infinite number of quantization intervals.

The cross-covariances of uniformly quantized bivariate Gaussian vectors are derived in [58], in the form of infinite sums.

In Appendices G.1 and G.2, it is shown that where

| (190) | ||||

| (191) | ||||

| (192) |

, (with a single subscript) denotes the standard deviation of , is the Riemann zeta-function, , and . Since a-priori known ranges of standard deviations () and of correlation coefficients are available, the intervals of , and should be valid for the entire ranges of the standard deviations and the correlation coefficients. Therefore, such variables for the upper bounds derived in (190)-(192) should be in the following intervals:

| (193) | ||||

| (194) | ||||

| (195) |

where .

In addition to cross-covariances between and and auto-covariances of , the variance of is also present in the causality matrix. Therefore, to exploit Theorem 3, the difference between the variances of and should also be derived as presented in Appendix G.3:

| (196) |

where .

G.1 Derivation of equations (190) and (191)

First let us introduce an inequality for the exponential functions appearing in covariances of quantized signals as follows:

Lemma 1.

For real :

| (197) |

Using the monotonicity of the exponential function and the fact that is always non-positive, the inequality (197) follows. Moreover the following series is absolutely convergent:

| (198) |

where is the Riemann zeta-function.

Using (197), (198) and comparison test theorem for series, it can be shown that is convergent and also converges in the region where (197) holds. Exploiting the infinite series representing derived in [58], Chapter 11, the following bound can be obtained using (197) and (198):

| (199) |

where . Furthermore, due to region of convergence of the Riemann zeta-function which is in (G.1), we have:

| (200) |

And the region of quantization intervals should be as follows:

| (201) |

to have (200). Equation (191) can be derived in a similar way.

G.2 Derivation of equation (192)

Throughout the paper, when we deal with double infinite series, convergence in Pringsheim sense [9] is considered.

Because of the absolute convergence of the Riemann zeta-function and Cauchy’s multiplication theorem, the following holds:

| (202) |

which implies that converges. Furthermore:

| (203) |

where the first inequality follows from Arithmetic Mean-Geometric Mean inequality and the second inequality is obtained by (197). Thus, using (G.2) and Comparison Test Theorem for double series [9], it can be shown that converges in the region . It can be shown that the following series is also convergent:

| (204) |

Using the order limit theorem for doubly index sequences, an upper bound can be derived as follows:

| (205) |

The covariance between quantization error terms and is expressed as follows in [58], Chapter 11:

| (206) |

For , we have:

| (207) |

where the last inequality follows from (202) and (G.2). In fact, it can be shown in a similar way to (G.2) that:

| (208) |

Note that should be chosen such that the following inequality holds for all positive integers and :

| (209) |

Hence, is as follows:

| (210) |

Note that the region of for convergence of the Riemann zeta-function is satisfied for any in (208).

G.3 Derivation of equation (196)

The variance of quantized signal can be represented as follows [58], Chapter 11:

| (211) |

Using (197), we have:

| (212) |

where due to Lemma 1 and the convergence region of the Riemann zeta-function. Furthermore, since and a-priori known range of , i.e. , is known, should be in the region of . Note that the value of in (212) should be chosen such that the upper bound on is minimized. It can be shown that the second and third terms in (212) are monotonically decreasing with respect to . Thus, should be chosen to equal in order to have a tighter bound. Substituting in (212), it can be shown that:

| (213) |

which is (196).

Appendix H Proof of Proposition 1

In order to develop a bound on the norm of quantization perturbation () to exploit Theorem 3 for the infinite-level quantized signals, the difference between elements of the causality matrix and should be first obtained. The elements of the causality matrix are the cross-covariances between and and the auto-covariances of signal . The infinity norm of is as follows:

| (214) |

An upper bound on can be derived as follows:

| (215) |

where and are obtained as follows by (190)-(192) and by replacing the standard deviations and correlation coefficients with their bounds:

| (216) | |||

| (217) | |||

| (218) | |||

| (219) |

and

| (220) | |||

| (221) |

A bound on the norm 1 can be also obtained as follows:

| (222) |

The term appearing in (215) and (H) should be replaced by its upper bound derived in (196). Moreover, note that and appearing in the norm one and infinity of depend on , , and . Such variables should be chosen such that the upper bound on () is minimized and be also in the intervals defined in (193)-(195). It can be shown that the functions and are monotonically decreasing with respect to such variables. Thus, it is sufficient to evaluate the upper bound on just for the values of , , and mentioned in the following:

| (223) | ||||

| (224) | ||||

| (225) | ||||

| (226) |

where and . Substituting such optimal values in (216) and (217) yields (180) and (181) and Theorem 3 implies Proposition 1. Note that the value of in (196) equals to in (224). Therefore, for ease of notation, is replaced by in the Proposition.

Appendix I Derivations of equations (49) and (50)

Using the comparison test theorem for infinite series, it can be shown that is absolutely convergent. The expression of is introduced in [58], Chapter 11. The series can be bounded as follows:

| (227) |

For sufficiently fine , it can be written as:

| (228) |

and (49) follows. The same method can be used to derive (50).

Appendix J Derivation of equation (51)

The covariance between quantization error terms and is as follows [58], Chapter 11:

| (229) |

It can be shown that it is convergent and a bound as follows can be obtained:

| (230) |

where the last inequality follows from Rayleigh quotient theorem. And

| (231) |

Note that since are convergent for , it can be shown that:

| (232) |

For sufficiently fine and , we have:

| (233) |

Appendix K Derivation of equation (52)

Appendix L Upper bound on in high-resolution regime

Norm infinity of the matrix can be written as follows in high resolution regime:

| (236) |

where

| (237) | ||||

| (238) | ||||

| (239) |

are obtained from (228) and (49)-(52) and is the upper bound on the cross-covariance between signals and .

For sufficiently fine , and . Hence, the dominant term between terms appearing in and is .

Furthermore, since in high-resolution regime . Therefore, the following can be stated:

| (240) |

Based on what is mentioned above, the norm one can be written as follows:

| (241) |

| (242) |

which is (5.1).

Appendix M Proof of Theorem 1

Let us first mention some definitions and make the definitions of their vector counterparts.

Definition 1 (Stationary Process).

[8] A process is said to be stationary if has the same distribution as for every ; that is, if for each :

| (243) |

for every , where the Borel field is the smallest -field of subsets of containing all finite-dimensional rectangles, denotes the space consisting of all infinite sequences of real numbers, and an -dimensional rectangle in is a set of the form

| (244) |

where are finite or infinite intervals.

Definition 2 (Invariant Set).

[8] An event is invariant if there exists such that for every :

| (245) |

Definition 3 (Ergodic Process).

[8] A stationary process is ergodic if every invariant event has probability zero or one.

The following can be defined for vector processes:

Definition 4 (Stationary Vector Process).

An -variate vector process , where , is said to be stationary if has the same distribution as for every ; that is, if for each :

| (246) |

for every , where is the corresponding Borel field.

Definition 5 (Invariant Set for Vector Processes).

An event is invariant if there exists such that for every :

| (247) |

Definition 6 (Ergodic Vector Processes).

A stationary vector process is ergodic if every invariant event has probability zero or one.

Now let us return to the proof of Theorem 1. According to Definition 4, we need to show that for every and , the following holds:

| (248) |

We know that

| (249) |

Since is a measurable function, for any there exists such that:

| (250) |

and

| (251) |

Since is stationary due to the assumption of the Theorem, the probability of the RHS’s of (250) and (M) is equal. Thus, the probability of the LHS’s of (250) and (M) is equal for any and . It implies that is a stationary vector process.

For ergodicity part of the Theorem, let us assume that is an invariant set for . Therefore, there exists such that for every :

| (252) |

Since is a measurable function, there exists for such that (252) can be written as follows:

| (253) |

Since is an invariant set for , the set is also an invariant set for . Since is ergodic and using (M), is zero or one which implies that the process is ergodic.

Appendix N Sufficient Condition for Ergodicity of Stationary Discrete-time Gaussian Vector Processes

Theorem 1.

Suppose is a stationary Gaussian vector process. If the auto- and cross-covariances vanish as the lag approaches infinity, then is ergodic.

The proof follows the same line of [13] and references therein with modifications to allow stationary discrete-time Gaussian vector processes. Let us first mention a theorem useful for the proof.

Theorem 2.

[8] Suppose is a probability space and is a field of subsets of such that the sigma-field containing is . For any and every there is a set such that

| (254) |

where is symmetric difference and defined as .

The events in the sigma-field in can be approximated in probability by finite dimensional sets. If is a probability space and , then for any , there is a finite and an event , where is the -field in , such that

| (255) |

where [37].

Now we turn to the proof. Let us assume that is an invariant set for . Define:

| (256) |

It follows from stationarity that and since is an invariant set, the following holds:

| (257) |

Theorem 2 implies that for any , there exist a finite and such that:

| (258) |

where . Using the fact that for any two random events and , yields that:

| (259) |

Now let us define

| (260) |

By stationarity, the following holds:

| (261) |

| (262) |

where the second inequality follows from the fact that for any three random events , and , .

Since the random vector process is jointly Gaussian and based on the assumption, the auto- and cross-covariances go to zero when approaches infinity, it follows that:

| (263) |

By stationarity of the random process (), it results that:

| (264) |

Equations (261), (N) and (264) and stationarity imply that:

| (265) |

and

| (266) |

Using (265) and (266), it follows that:

| (267) |

which means that is zero or one. Therefore, the stationary sequence is ergodic.