Email: kim2133@purdue.edu

Equilibrium Computation of Generalized Nash Games: A New Lagrangian-Based Approach

Abstract.

This paper presents a new primal-dual method for computing an equilibrium of generalized (continuous) Nash game (referred to as generalized Nash equilibrium problem (GNEP)) where each player’s feasible strategy set depends on the other players’ strategies. The method is based on a new form of Lagrangian function with a quadratic approximation. First, we reformulate a GNEP as a saddle point computation problem using the new Lagrangian and establish equivalence between a saddle point of the Lagrangian and an equilibrium of the GNEP. We then propose a simple algorithm that is convergent to the saddle point. Furthermore, we establish global convergence by assuming that the Lagrangian function satisfies the Kurdyka-Łojasiewicz property. A distinctive feature of our analysis is to make use of the new Lagrangian as a potential function to guide the iterate convergence. Our method has two novel features over existing approaches: (i) it requires neither boundedness assumptions on the strategy set and the set of multipliers of each player, nor any boundedness assumptions on the iterates generated by the algorithm; (ii) it leads to a Jacobi-type decomposition scheme, which, to the best of our knowledge, is the first development of a distributed algorithm to solve a general class of GNEPs. Numerical experiments are performed on benchmark test problems and the results demonstrate the effectiveness of the proposed method.

1. Introduction

We consider a generalized (continuous) Nash game (generalized Nash equilibrium problem (GNEP)) that describes a broad class of non-cooperative and simultaneous-move games, in which each player seeks to optimize her/his own objective function while subject to certain constraints that are affected by the other players’ strategies. The standard Nash game (Nash et al., 1950) is a subclass of GNEPs, as the strategic interactions among players in a Nash game are only reflected in their objective functions, not in the constraints. More specifically, the game features a set of players denoted by where each player has its own strategy . Each player has an objective function and a finite set of “coupling constraints” , both of which depend on player ’s own strategy as well as other players’ strategies . Denote all players’ strategies by a vector with dimension . The GNEP can be formally defined as a problem of simultaneously finding a solution for each of the following problem. Given other players’ strategies , each player seeks to find a strategy that solves the optimization problem:

| (1) |

where represents the “private” strategy set of player that is nonempty, closed, and convex. The feasible strategy set of each player can be represented by the parametric inequalities:

Note that the private functional constraints for are not explicitly highlighted in the paper for notational simplicity. They can be easily treated by the same way to deal with . Here , and are positive integers. The simple set is defined by , where or may be unbounded; that is, or or both.

A Nash equilibrium of the GNEP can be defined as follows.

Definition 1.

A collection of strategies is a (pure-strategy) generalized Nash equilibrium (GNE) if for every ,

i.e., is a GNE, if and only if no player has incentive to unilaterally deviate from when other players choose .

We make the following assumption on the functions throughout the paper.

Assumption 1.

For every and fixed , objective function and constraint functions , , are continuously differentiable and convex with respect to .

Note that and are possibly nonconvex with respect to some other players’ decisions , and are not necessarily shared by all players (called non-shared coupling constraints).

Under Assumption 1, Problem is known as a very general form of GNEP (Dreves et al., 2011) (We call it general GNEP in this work). In this paper, we aim to provide and analyze the first distributed primal-dual algorithm, based on a novel form of Lagrangian, to compute an equilibrium of the general GNEP, provided that equilibria of generalized Nash game exist.

We also make the following two standard assumptions; Lipschitz gradient continuity of the objective and constraint functions (smoothness) and coercivity of the objective functions.

Assumption 2 (Uniform Lipschtz gradient continuity).

For every , the gradients of and are uniformly Lipschitz continuous with constants; there exist constants such that

| (2a) | ||||

| (2b) | ||||

| (2c) | ||||

| (2d) | ||||

| In addition, for any fixed , there exist constants and such that | ||||

| (2e) | ||||

| (2f) | ||||

Here, .

Assumption 3 (Coercivity of objective function).

For every , the objective function is coercive with respect to , i.e., .

Assumption 3 implies that the level sets of the objective functions are bounded. It is well-known that coercivity assumption on the objective function is a standard assumption in nonconvex settings; see e.g., Li and Pong (2015); Boţ et al. (2019); Boţ and Nguyen (2020). However, we do not impose the coercivity assumption on the feasible strategy sets, which is in contrast to the analysis of the interior-point algorithm for solving general GNEPs in Dreves et al. (2011). In Dreves et al. (2011), the algorithm relies on the strong assumption that the feasible strategy sets of all players are bounded, i.e., where for all .

1.1. Motivating Examples

We give two practical examples that illustrate the versatility of the general GNEP model (1) and motivate to develop an efficient algorithm. We refer the readers to Facchinei and Kanzow (2010a) for more examples.

Example 1 (Power allocation in telecommunications).

This model is described in detail in Pang et al. (2008) and represents a realistic communication system subject to Quality-of-Service (QoS) constraints. There are links transmitting to different Base Stations by using different channels. Link transmits with power , and denote by the power allocation of all links. The game-theoretical model is defined by

where denotes the power gain between transmitter and receiver on the -th channel, is the noise of link on the -th channel, and is the minimum transmission rate (target rate) for link .

In this game-theoretical model, the QoS constraints are nonconvex in the other links’ decision variables, and each link has different coupling QoS constraints. Thus, this problem can be viewed as a case of the general GNEP (1). Moreover, due to the complicated coupling constraints, it is hard to compute a Nash equilibrium of the model efficiently.

Example 2 (Arrow-Debreu general equilibrium model).

This equilibrium model is introduced by Arrow and Debreu (1954) and also described as a general GNEP in Facchinei and Kanzow (2010a). There are consumers, firms, and one market player (a fictitious player) in this equilibrium model. Both consumers and firms deal with goods. The market player sets (normalized) prices for solving a market clearing problem. The -th firm maximizes its profit by deciding how much to produce , where is a production set. The -th consumer decides how much of each good to buy to maximize its utility, where is a consumption set. The GNEP is defined as the following set of problems of the three types of players:

| (2) | ||||||||

| (2) |

The first problem corresponds to firm ’s production problem, the second problem corresponds to the consumption problem of consumer , and the last problem corresponds to the market player’s problem. Here, represents the fraction of the profit of the -th production owned by consumer such that , and is an initial endowment of goods.

Definition 2 (Walrasian Equilibrium; see e.g., Jofré et al. (2007)).

A Walrasian equilibrium consists of a price vector , consumption vectors for , and production vectors for , such that

(E1) (Market Nontriviality). ,

(E2) (Utility Optimization). maximizes over s.t.

(E3) (Profit Optimization). maximizes over ,

(E4) (Market Clearing). Supplies and demands are balanced in the sense that

For any , conditions and can be expressed in terms of

where and . Note that (E4) comes out as a linear complimentarity condition on and . The above expressions lead to the idea of capturing all conditions for equilibrium, including (E4), in terms of a mapping from to : Clearly, we have

We thus see that the feasible strategy set of each player depends on the other players’ selfish decisions. Furthermore, each player’s feasible set does not depend on all other players’ decisions (i.e., non-shared coupling constraints). Hence, the Arrow-Debreu equilibrium model is a case of the general GNEPs (1).

1.2. Literature Review

The concept of GNEP was originally addressed by Debreu (1952) and Arrow and Debreu (1954) in the early 1950s, where a GNEP was called a social equilibrium problem or abstract economy. An important subclass of GNEPs, known as jointly-convex GNEPs, was first investigated by Rosen (1965) where all players share the same convex coupling constraints (i.e., ). Although early studies on GNEPs have been primarily concerned with economics, recent decades have witnessed a growing interest in the GNEP as a modeling framework and a solution concept in various application areas. Some examples include electricity market models Jing-Yuan and Smeers (1999); Contreras et al. (2004); Hobbs and Pang (2007), power allocation in telecommunications Pang et al. (2008), environmental pollution applications Krawczyk and Uryasev (2000); Breton et al. (2006), transportation systems Stein and Sudermann-Merx (2018), and mobile cloud computing Cardellini et al. (2016), to name a few.

Many approaches have been proposed to compute a GNE in the literature. A common approach is to transform a GNEP into a variational inequality (VI) and to apply algorithms designed to find a solution of a VI reformulation (see e.g., Facchinei et al. (2007); Nabetani et al. (2011); Yin et al. (2011); Kulkarni and Shanbhag (2012)). Another approach is to reformulate a GNEP into a global optimization problem using Nikaido-Isoda (NI) function and then solve the resulting optimization problem by the so-called relaxation algorithms Uryas’ev and Rubinstein (1994); Von Heusinger and Kanzow (2009b) or gradient-based algorithms Von Heusinger and Kanzow (2009a). However, the theoretical and algorithmic properties of both approaches are only established for the class of jointly-convex GNEPs. In particular, VI-based methods require the monotonicity assumption on the variational mapping that generally does not hold in general GNEPs.

The equilibrium computation of GNEPs beyond the class of jointly-convex GNEPs remains a very challenging task. This is mainly due to interdependence between each player’s strategy and some other players’ strategies through coupling constraints and potential nonconvexity of each player’s optimization problem with regard to the strategies chosen by other players. A few algorithms have indeed been proposed, including penalty-type methods Pang and Fukushima (2005); Facchinei and Kanzow (2010b), interior point algorithm Dreves et al. (2011) and augmented Lagrangian method Kanzow and Steck (2016). In all such methods, it is assumed that the extended Mangasarian-Fromovitz constraint qualification (EMFCQ), an extension of the MFCQ for infeasible points, holds with respect to for each player , at every limit point of the sequence generated by the algorithms. This MFCQ is a restrictive assumption since it is equivalent to the boundedness of the multiplier set of each player, and it cannot be justified to hold for every player in the GNEP in general due to the nature of GNEPs. More specifically, and the multipliers might occur since it is possible that from the strategic interactions among players through the coupling constraint. Thus, GNEPs may have an unbounded Lagrange multiplier set of each player.

Penalty-based algorithms reduce the GNEP to a standard Nash equilibrium problem (NEP) by penalizing coupling constraints and focus on updating the penalty parameter. In particular, the exact penalty method in Facchinei and Kanzow (2010b) results in nonsmooth subproblems, so it obtains a GNE under various differentiability assumptions on the objective functions and constraints. This lack of differentiability is a serious problem for designing efficient algorithms. To address the drawbacks of penalty-based methods, Kanzow and Steck proposed an augmented Lagrangian method in Kanzow and Steck (2016). This approach requires an algorithmic assumption that there exists a limit point of the primal sequence . However, this assumption is not clear without the compactness of each player’s private set.

Furthermore, it is noteworthy to point out that even with our coercivity assumption on the objective functions, the augmented Lagrangian (AL) algorithm in Kanzow and Steck (2016) does not guarantee that the primal sequence and/or dual sequence remains bounded. To ensure the boundedness of the sequences with the coercivity assumption, the bounded level sets of the AL functions are required. However, these level sets are typically unbounded. This is mainly related to the behavior of the multiplier sequence . Specifically, the AL method in Kanzow and Steck (2016) is of min-max dynamics (due to the increase in the dual variable) and by nature, the AL function value alternatively increases and decreases, and the dual sequence might be unbounded. Hence, the coercivity does not imply the boundedness of the primal and dual sequences in the AL algorithm. This can be illustrated by a simple example.

Example 3.

Consider the two players GNEP with :

where both players’ objective functions are coercive. We see that at the unique equilibrium (and only feasible point) given by , the gradients of the constraints are linearly dependent, and hence the MFCQ does not hold. As a result, the AL algorithm in Kanzow and Steck (2016) may generate an unbounded multiplier sequence, which results in an unbounded sequence of the AL function values and thus failure to have limit points.

In a computational perspective, a major limitation of the methods in Facchinei and Kanzow (2009); Kanzow and Steck (2016) is that they cannot be implemented in a distributed way since they need to solve subproblems represented by a large system of nonlinear equations (variational inequality) at each iteration. Thus, they are computationally expensive.

1.3. Our Contributions

The objective of this paper is to propose a new algorithmic framework for computing an equilibrium of a general GNEP under general assumptions without imposing boundedness assumptions on the generated primal and dual sequences and the (feasible) strategy sets of all players. To achieve such a goal, we introduce a novel form of Lagrangian, termed as Proximal-Perturbed Lagrangian (P-Lagrangian), and utilize a quadratic approximation of the P-Lagrangian.

The key ideas underlying our approach are as follows. First, perturbation variables are introduced to form constraints and , which can be relaxed into the objective function with Lagrange multipliers. This reformulation allows the use of as simple penalty terms and exploiting a proximal regularization on the Lagrange multipliers, which provides a strongly concave function in the multipliers. The next ingredient is to employ a quadratic approximation that is strongly convex in all the players’ strategies. This enables to simply deal with the nonconvexity of and in some , and further leads to a Jacobi-type decomposition scheme for updating primal variables at each iteration.

This paper makes the following contributions to the literature:

-

•

We introduce a new form of Lagrangian function that has a favorable structure; it is strongly concave with respect to the Lagrange multipliers, and it does not include penalty terms for handling coupling constraints. Consequently, the proposed algorithm guarantees to generate the bounded sequence of the Lagrange multipliers with the bounded primal sequence without requiring the MFCQ assumption. Moreover, this leads to an easy-to-implement algorithm by removing the computational effort in updating the penalty parameter as in Facchinei and Kanzow (2010b) and Kanzow and Steck (2016).

-

•

The proposed algorithm can deal with the nonconvexity of each player’s functions in other players’ decisions by employing a quadratic approximation of the original P-Lagrangian in . More importantly, the use of the quadratic approximation offers a Jacobi-type decomposition scheme that allows distributed simultaneous updates of primal variables, which, to the best of our knowledge, leads to the first distributed algorithm to solve general GNEPs.

-

•

We prove that our algorithm is convergent to a saddle point of P-Lagrangian under standard assumptions. In contrast to the existing methods for solving general GNEPs, our analysis does not impose any boundedness assumptions on the iterates generated by the algorithm. In particular, we do not make use of a priori assumption that a limit point of primal iterates exists, and safeguarding technique Andreani et al. (2007, 2008) to bound multiplier iterates as in Kanzow and Steck (2016). In addition, we establish the global convergence under an additional assumption that the objective and constraint functions satisfy the Kurdyka-Łojasiewicz inequality.

1.4. Notation and Outline of the Paper

Notation.

We use and to denote the -dimensional Euclidean vector space and -dimensional Euclidean vector space, respectively. For two vectors , the inner product is denoted by , and the standard Euclidean norm is denoted by . For a real scalar , we define . We use to denote the nonnegative orthant of .

Outline of the paper.

This paper is organized as follows. In section 2, we introduce the P-Lagrangian function, describe its characteristics, and reformulate the GNEP as a saddle point problem using the P-Lagrangian. Section 3 presents a distributed primal-dual algorithm based on a quadratic approximation. In Section 4, we establish convergence of the proposed algorithm. Numerical results are presented in Section 5.

2. Proximal-Perturbed Lagrangian Formulation

Before introducing Proximal-Perturbed Lagrangian (P-Lagrangian), we recall that under Assumption 1 and suitable constraint qualifications, a GNE can be characterized by the Karush-Kuhn-Tucker (KKT) conditions (see e.g., Dreves et al. Dreves et al. (2011) and Bueno et al. Bueno et al. (2019)):

The KKT conditions. Assume that a suitable constraint qualification holds. If there exists a point together with some Lagrange multipliers satisfying the KKT conditions

| (3) |

for every , then is a generalized Nash equilibrium (GNE). Here, is each player ’s Lagrangian function, and is the normal cone to at .

It is well known (Facchinei and Kanzow, 2010a, Theorem 4.6) that under the convexity assumption and a constraint qualification(CQ), the KKT conditions (3) are necessary and sufficient optimality conditions for problem . In addition, convex optimization problem is equivalent to solving the dual formulation, i.e.,

| (4) |

In general GNEP model, the set of Lagrange multipliers of each player is possibly unbounded (assuming it is nonempty) even if it satisfies the KKT conditions. This is due to the interdependency between and through the coupling constraints , . The general GNEP setting thus requires a CQ weaker than MFCQ that allows unbounded multiplier sets (e.g., Guignard CQ, cone continuity property, and constant positive linear dependence CQ); see Bueno et al. (2019) for a detailed discussion about various CQs for GNEPs. This unboundedness makes the computation of a GNE very hard, and thus boundedness of the multipliers is one of the key issues when solving GNEPs. Our motivation for introducing a new Lagrangian is to address this challenge.

This section first introduces a new form of Lagrangian that has a desirable structure for equilibrium computation. We then present a reformulation of problem (1) as a P-Lagrangian dual problem and show that computing a saddle point of the P-Lagrangian is equivalent to finding an equilibrium of the GNEP (1).

2.1. The Proximal-Perturbed Lagrangian

Motivated by the reformulation techniques in (Bertsekas and Tsitsiklis, 1989, Chapter 3.4) and (Bertsekas, 2014, Chapter 3.2), we start by transforming problem (1) into an equivalent extended formulation by introducing perturbation variables as additional constraints and letting given :

| (5) |

Obviously, for , the above extended formulation is equal to problem (1).

Noting that the reformulation (5) allows the use of as a penalty term, first consider the following partially augmented Lagrangian for every :

where and are the Lagrange multipliers associated with constraints and , respectively. is a penalty parameter. Observe that given , minimizing with respect to gives

which implies that at the unique solution . Based on this relation of and from the optimality condition for , we add a proximal term to define Proximal-Perturbed Lagrangian (P-Lagrangian):

| (6) | ||||

where is a proximal regularization parameter.

We observe that the structure of the P-Lagrangian in (6) differs from the standard augmented Lagrangian and its variants (Hestenes, 1969; Powell, 1969; Bertsekas, 2014; Birgin and Martínez, 2014, and references therein). First, it is characterized by the absence of penalty term for handling the coupling constraint . Only additional constraint is penalized with a quadratic penalty term , while the constraint is merely relaxed into the objective with the corresponding multiplier. Second, the P-Lagrangian is strongly concave in (for fixed ) and in (for fixed ) due to the presence of the negative quadratic term . Note that, as will be shown later, this quadratic term plays an important role that it does not allow for the next iterate to deviate far from when updating the multiplier via an exact maximization scheme.

2.2. Equivalence between a Saddle Point of P-Lagrangian and a GNE

Now consider the following P-Lagrangian dual problem for given :

| (7) |

Since is convex, the primal-dual solutions of problem (7), and given , can be characterized by the saddle point of the P-Lagrangian.

Definition 3.

Given , a point is said to be a (parametrized) saddle point of the Proximal-Perturbed Lagrangian for and if for every

| (8) |

for all . Here, are viewed as parameters.

We establish the equivalence between computing a saddle point of and finding an equilibrium of the GNEP (1), by proving the following two theorems.

Theorem 2.1.

Let be a saddle point of for a given and for some . Then, is an equilibrium of the GNEP (1).

Proof 2.2.

See Appendix A.1.

Theorem 2.

Proof 2.

See Appendix A.2.

3. Algorithm

In this section, we propose a simple primal-dual algorithm for computing a saddle point of based on a quadratic approximation of for every .

3.1. Motivation for Approximation of Subproblems

We begin by describing briefly why we need to consider an approximation scheme for updating . To compute a saddle point of for every , we should be able to determine a point that satisfies the following first-order optimality (or simultaneous stationarity) condition of subproblems for fixed :

It is well known (Facchinei and Pang Facchinei and Pang (2007)) that for given , computing such a stationary point is equivalent to the variational inequality (VI) problem of finding such that

where , the Cartesian product of the private strategy sets of all players, and the mapping is given by

with , and .

However, it may be difficult to compute the point using descent methods. In the GNEP setting, the monotonicity of the mapping with respect to does not hold in general (Facchinei and Kanzow, 2010a, Section 5.2) even if each component is convex in . The nonconvexity of each P-Lagrangian with respect to the other players’ variables makes it hard to preserve a descent direction for the convergence to the stationary point that satisfies all components of the variational inequality.

3.2. Construction of Quadratic Approximation Model

To overcome such a computational difficulty, we consider a monotone approximation, denoted by , to the nonmonotone mapping in . The monotone approximation of the mapping can be always chosen even if is nonmonotone (see e.g., Chung and Fuller (2010); Luna et al. (2014)). Furthermore, strongly monotone approximation mapping can be derived by replacing each player’s by a simple approximate function and then constructing an approximation .

To this end, inspired by Beck and Teboulle (2009) and Bolte et al. (2014), we first employ the following quadratic approximation in only , at a given point :

| (10) |

namely, the linearized P-Lagrangian at the point combined with quadratic proximal terms that measure the local error in the linear approximation. Here, is a proximal parameter. The term represents the gradient at a given point in other players’ strategies, and denotes the gradient of with respect to at the point .

From the conditions (2a)–(2d) in Assumption 2, we know that and have Lipschitz continuous gradients; there exist Lipschitz constants and such that

| (11a) | ||||

| (11b) | ||||

where and (see Nesterov (2012, Lemma 2)). Here, and represent and , respectively. As a direct consequence of the above Lipschitz continuity of and , (11a) and (11b) respectively, we have the well-known descent Lemma.

Lemma 1 (Bertsekas (Bertsekas, 1999, Proposition A.24)).

For and for any fixed , is Lipschitz continuous with constant . We thus have

Here, we omit fixed for notational simplicity.

Then, with the proximal parameter large enough such that , in (10) is an upper quadratic approximation of around the point with respect to and it has the following properties (see e.g., Beck and Teboulle (2009); Razaviyayn et al. (2013); Scutari et al. (2016)).

Remark 1 (Properties of ).

The approximation function with satisfies the properties:

-

(P1)

for .

-

(P2)

for .

-

(P3)

is strongly convex in all the players’ decisions with constant , i.e., for any ,

-

(P4)

is Lipschitz continuous on with some Lipschitz constant , i.e., for any ,

The properties (P1) and (P2) imply that with is a tight upper bound of around the given point . The properties (P3) and (P4) are from the structure of that is the first-order approximation of in at with quadratic term .

Given the current iterates and , since is uniformly strongly convex on , there must exist a unique minimizer at each iteration such that

It also follows from (P1) that

We can construct a (strongly) monotone approximation mapping given by

Let us now consider solving the following approximate variational inequality problem of finding :

| (12) |

It is well known ((Facchinei and Pang, 2007, Proposition 1.5.8)) that is also a solution to the system of fixed-point subproblem (or system of nonlinear projected equations) at iteration :

| (13) |

where denotes the Euclidean projection operator onto the set and is a constant.

For fixed at iteration , we use the following gradient projection to generate a sequence in inner iterations

| (14) |

equivalently,

| (15) |

Notice that the structure of allows for the inner gradient projection scheme (15) to be implemented in a distributed way since each player can update its own while keeping the current primal iterates fixed. Thus we can allow each player to choose its own step size , .

We also note that when the private strategy set of each player includes functional constraints , they are treated in the same way to handle via the P-Lagrangian. It follows that only the set remains as a simple constraint, and hence the projection onto is computationally cheap.

The following Lemma shows that the inner gradient projection scheme (15) converges to the solution of the subproblem (13) at each iteration and thus enables us to compute a point satisfying the decrease property for every during inner iterations..

Lemma 2.

Let be the unique solution to the subproblem (13) and . Let be the sequence generated by the inner gradient projection (15) with the step size for each player . Suppose that the parameter of proximal term in is chosen such that , where is the Lipschitz constant of . Then,

-

(a)

for satisfying , where , , and is the Lipschitz constant of , the sequence converges to the solution . That is,

(16) where .

-

(b)

thus, the inner gradient projection (15) can compute close to such that

(17) for every in a finite number of inner iterations.

Proof 2.

See Appendix B.

3.3. Description of Algorithm

We are ready to formally present our distributed algorithm that exploits all the features discussed. The steps of the proposed algorithm are summarized in Algorithm 1.

The main computational effort of our algorithm is involved in Step 1 to update primal iterates from to . If , by Lemma 2, we can always find a point that satisfies both conditions

| (18) |

and

| (19) |

in a finite number of inner iterations. When the descent condition (19) is satisfied, is set to . Consequently, the decrease of every value is obtained, that is,

We remark that a point satisfying the (approximate) fixed-point condition (18) does not necessarily guarantee that the descent condition (19) holds. Hence, the algorithm keeps updating the iterates until condition (19) is satisfied even after condition (18) is met, which may require many inner iterations.

The next step consists of each player updating by taking a simple minimization step (Step 2) on . This update depends on only the current iterates of the Lagrange multipliers and , but is independent of the primal variables .

After the minimization steps have been carried out, given , the multipliers are updated by exact maximization steps on . The updates of and take the explicit forms:

which can be viewed as a proximal point scheme. The multipliers are always updated whenever the corresponding is updated.

4. Convergence Analysis

In this section, we establish the convergence results of Algorithm 1. We prove that the sequence generated by Algorithm 1 converges to a saddle point of for . In particular, our analysis proceeds with the steps:

- (1)

-

(2)

We then establish the key results; the boundedness of and , followed by the boundedness of (Theorem 3).

-

(3)

With the bounded sequences, convergence to an equilibrium of the GNEP is proven; we show that any limit point of the sequence is a saddle point of (Theorem 4).

-

(4)

Finally, we establish the global convergence that the whole sequence generated by the algorithm converges to a saddle point of by assuming that the P-Langangian satisfies the Kurdyka-Łojasiewicz (KŁ) property (Theorem 5).

4.1. Key Properties of Algorithm 1

We show that the sequence can be a nonincreasing sequence. To this end, we first derive an important relation on the dual iterates and with the primal iterates that the difference of two consecutive iterates of the multipliers can be bounded by that of the primal iterates.

Lemma 3.

Let be the sequence generated by Algorithm 1. Then,

| (20) |

where is the Lipschitz constant of and is the parameter of in .

Proof 3.

See Appendix C.1

Equipped with Lemmas 2 and 3, we prove that the sequence of function values can be monotonically decreasing and convergent.

Lemma 4 (Sufficient Decrease and Convergence of ).

Suppose that Assumptions 1 and 2 hold. Let be the sequence generated by Algorithm 1. Then for , we have

where is the Lipschitz gradient constant of , is the parameter of proximal term in , and is the parameter of quadratic term in . In particular, if is chosen large enough such that , then the sequence is nonincreasing and convergent.

Proof 4.

See Appendix C.2

Next, we provide our key results that the generated sequence is bounded and asymptotic regular. The boundedness of the sequence follows by combining the above decrease property of the P-Lagrangian with the coercivity assumption on the only objective functions (Assumption 3).

Theorem 3.

Assume that there exists a GNE of the GNEP (1) satisfying the KKT conditions (3) for every . Let be the sequence generated by Algorithm 1 with the parameters set to large enough so that . Then,

-

(a)

the primal sequence is bounded;

-

(b)

the sequence of the multiplier is bounded;

-

(c)

it holds that and , and hence

(21)

Proof 3.

See Appendix C.3

4.2. Main Convergence Results

We are ready to establish our main convergence results. We first show that any limit point of the sequence produced by Algorithm 1 is a saddle point of for every .

Theorem 4 (Subsequence Convergence).

Proof 4.

See Appendix D.1

We now strengthen the above subsequence convergence result under an additional assumption that the functions satisfy the Kurdyka-Łojasiewicz (KŁ) property (see Łojasiewicz (1963) and Kurdyka (1998)): The KŁ property, along with the sufficient decrease of the P-Lagrangian and the boundedness of generated sequence, enables us to establish global convergence of the whole sequence to a saddle-point of by showing that the sequence has finite length.

Definition 4 (KŁ Property & KŁ function).

Let . Denote by the class of all concave and continuous functions , which satisfy the following conditions:

-

(i)

;

-

(ii)

is continuously differentiable () on and continuous at 0;

-

(iii)

for all

A proper and lower semicontinuous function is said to have the Kurdyka-Łojasiewicz (KŁ) property at if there exist , a neighborhood of and a function , such that

for all . The function satisfying the KŁ property at each point of dom is called a KŁ function.

Theorem 5 (Global Convergence).

Suppose that and , , , satisfy the KŁ property. Let be the sequence generated by Algorithm 1. Then the sequence has finite length, i.e.,

and the whole sequence converges to a saddle point of .

Proof 5.

See Appendix D.2

We note that verifying the KŁ property of a function might be a difficult task. However, it is well-known that semi-algebraic and real-analytic functions, which capture many applications, are classes of functions that satisfy the KŁ property; see e.g., Attouch and Bolte (2009); Attouch et al. (2010, 2013); Xu and Yin (2013); Li and Pong (2018) for an in-depth study of the KŁ functions and illustrating examples.

5. Computational Results

In this section, we present computational results to demonstrate the effectiveness of the proposed method. We conducted numerical experiments on test problems using Algorithm 1. The experiments were carried out using MATLAB (R2018a) on a laptop with a Intel Core i5-6300U CPU 2.50GHz 8GB RAM. All the test problems were taken from a library of GNEPs used in the literature Facchinei and Kanzow (2010b); Dreves et al. (2011); Kanzow and Steck (2016), and two classes of instances were considered; general GNEPs (A.1-A.10) and jointly-convex GNEPs (A.11-A.18). We refer the readers to Facchinei and Kanzow (2009) for a detailed description of the problems with data.

In the numerical test, we used the starting points listed in Facchinei and Kanzow (2010b), and the other variables’ initial points were set to for every . As for the parameters, we used fixed parameters set to and for each player’s P-Lagrangian and for all test problems. In addition, diminishing step size was simply used for every player in each problem. The stopping criterion is set as

The computational results of our algorithm for the test problems are presented in Table 1, where we used the following notations; the number of players ‘’, the number of variables ‘’, the number of constraints ‘’, starting point ‘’, total (cumulative) number of inner iterations ‘’, and computation time of CPU seconds ‘Time(s)’.

We summarize the computational results in the following:

-

(1)

Algorithm 1 was able to solve all the test problems. The experimental results show that Algorithm 1 comes out favorably in terms of the number of problems solved compared to the other methods. In particular, the exact penalty algorithm in Facchinei and Kanzow (2010b) was unable to find solutions to the problems A.2, A.7, and A.8. In addition, the interior-point algorithm in Dreves et al. (2011) and the augmented Lagrangian method in Kanzow and Steck (2016) were unable to find a GNE of the instance A.8 with starting points and , respectively. On the other hand, Algorithm 1 converges to a GNE for the three problems A.2, A.7, and A.8, starting from those points.

-

(2)

It is worth noting that Algorithm 1 converges to the same GNE from different starting points in each problem, while the exact penalty algorithm Facchinei and Kanzow (2010b) converges to different equilibria or generates unbounded sequences in some cases. This difference is because each player’s problem is convex in its own variables, and each player solves strongly convex subproblems while keeping the other players’ variables fixed. On the other hand, the exact penalty algorithm Facchinei and Kanzow (2010b) solves nondifferentiable (possible nonconvex) subproblems. This, along with sensitivity to the penalty parameters and starting points, may lead to the convergence to different equilibria or the failure of convergence.

-

(3)

Our distributed algorithm required very short CPU times to reach equilibrium for all test instances. The results confirm the efficiency of our algorithm that the computation time per iteration to solve each subproblem is significantly short for every instance. This advantage is mainly due to the Jacobi decomposition scheme for the -update with the cheap projection onto the simple set .

-

(4)

For Arrow-Debreu equilibrium problems A.10 (a-e), it is noteworthy that our problem setting is different from test problems in Facchinei and Kanzow (2009). In our setting, the production variables are added to the constraints of consumers’ problems, that is , whereas the constraints were set to in the test setting in Facchinei and Kanzow (2009). This reflects the original Arrow-Debreu model better and computational results have shown that Algorithm 1 performs well on the modified instances.

| general GNEP | Time (s) | |||||

| A.1 | 10 | 10 | 20 | 0.01 | 38 | |

| 0.1 | 36 | |||||

| 1 | 38 | |||||

| A.2 | 10 | 10 | 24 | 0.01 | 610 | 0.04 |

| 0.1 | 536 | 0.04 | ||||

| 1 | 683 | 0.05 | ||||

| A.3 | 3 | 7 | 18 | 0 | 51 | 0.01 |

| 1 | 51 | 0.01 | ||||

| 10 | 51 | 0.01 | ||||

| A.4 | 3 | 7 | 18 | 0 | 7 | |

| 1 | 7 | |||||

| 10 | 7 | |||||

| A.5 | 3 | 7 | 18 | 0 | 82 | 0.02 |

| 1 | 82 | 0.02 | ||||

| 10 | 82 | 0.02 | ||||

| A.6 | 3 | 7 | 21 | 0 | 49 | 0.02 |

| 1 | 49 | 0.02 | ||||

| 10 | 49 | 0.02 | ||||

| A.7 | 4 | 20 | 44 | 0 | 48 | 0.02 |

| 1 | 48 | 0.02 | ||||

| 10 | 48 | 0.02 | ||||

| A.8 | 3 | 3 | 8 | 0 | 45 | |

| 1 | 45 | |||||

| 10 | 45 | |||||

| A.9 (a) | 7 | 56 | 63 | 0 | 108 | 0.32 |

| A.9 (b) | 7 | 112 | 119 | 0 | 135 | 1.24 |

| A.10 (a) | 8 | 24 | 33 | 0 | 780 | 0.10 |

| A.10 (b) | 25 | 125 | 151 | 1 | 1374 | 0.67 |

| A.10 (c) | 37 | 222 | 260 | 0 | 2154 | 1.12 |

| A.10 (d) | 37 | 370 | 408 | 1 | 3251 | 1.35 |

| A.10 (e) | 48 | 576 | 625 | 1 | 4728 | 2.54 |

| jointly-convex GNEP | Time (s) | |||||

| A.11 | 2 | 2 | 2 | 0 | 12 | |

| A.12 | 2 | 2 | 4 | (2,0) | 10 | |

| A.13 | 3 | 3 | 9 | 0 | 15 | |

| A.14 | 10 | 10 | 20 | 0.01 | 38 | |

| A.15 | 3 | 6 | 12 | 0 | 145 | |

| A.16 (P=75) | 5 | 5 | 10 | 10 | 52 | 0.02 |

| A.16 (P=100) | 5 | 5 | 10 | 10 | 52 | 0.02 |

| A.16 (P=150) | 5 | 5 | 10 | 10 | 52 | 0.02 |

| A.16 (P=200) | 5 | 5 | 10 | 10 | 52 | 0.02 |

| A.17 | 2 | 3 | 7 | 0 | 9 | |

| A.18 | 2 | 12 | 28 | 0 | 114 | 0.02 |

Illustrative Examples

To see how well Algorithm 1 performs on GNEPs, we provide numerical results for three important and practical instances with graphical illustrations.

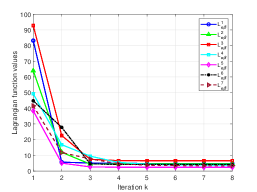

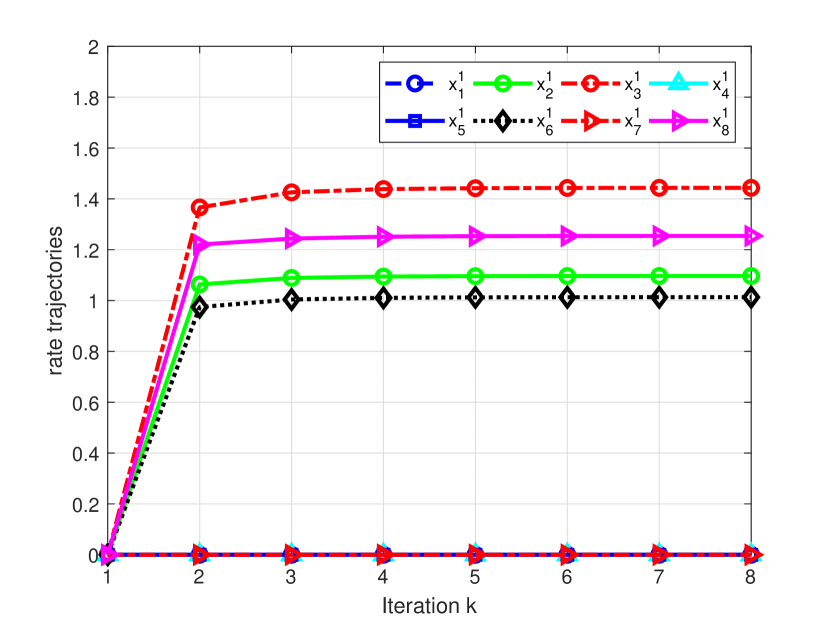

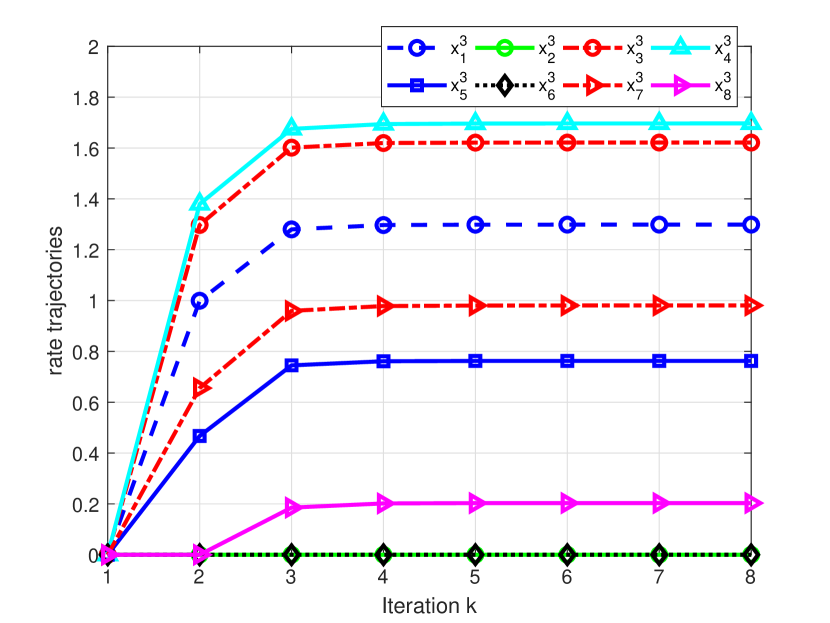

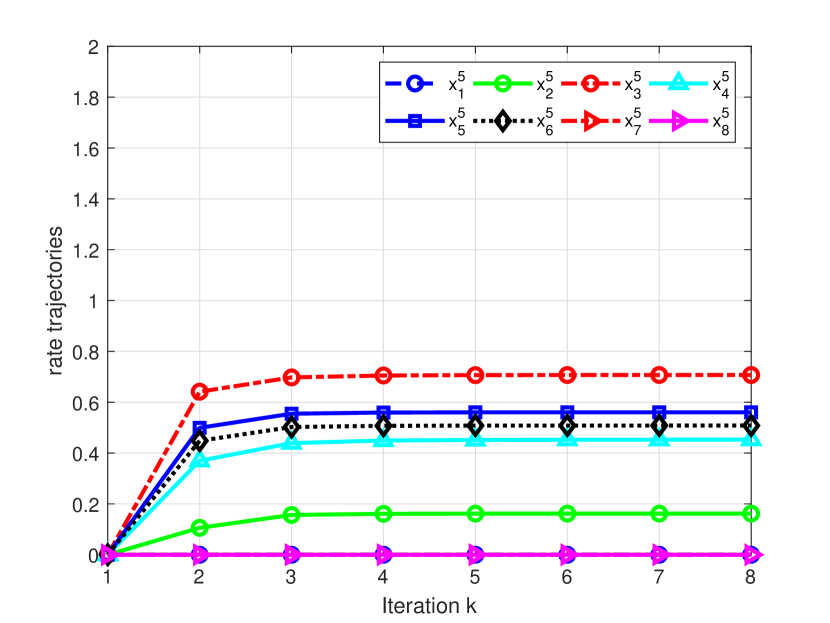

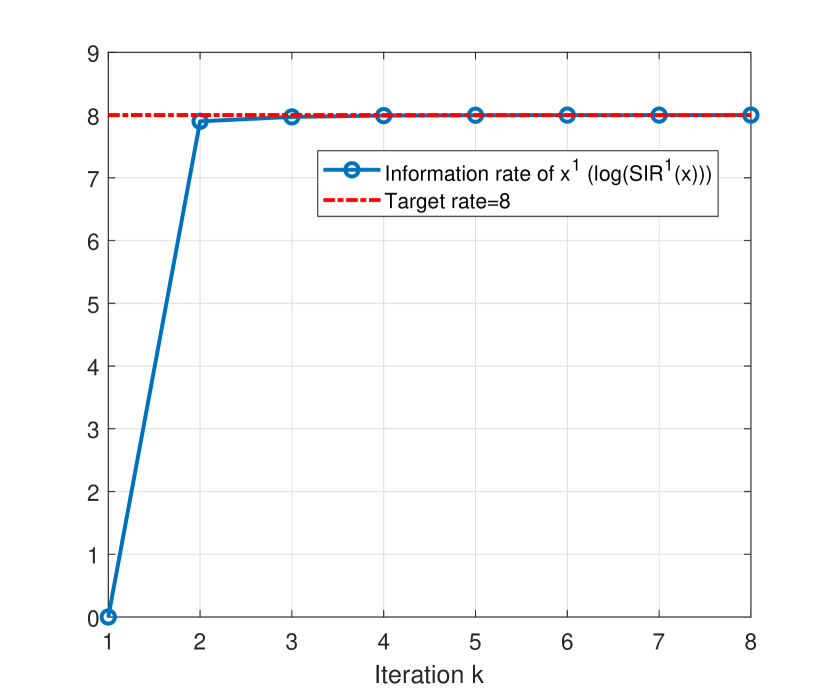

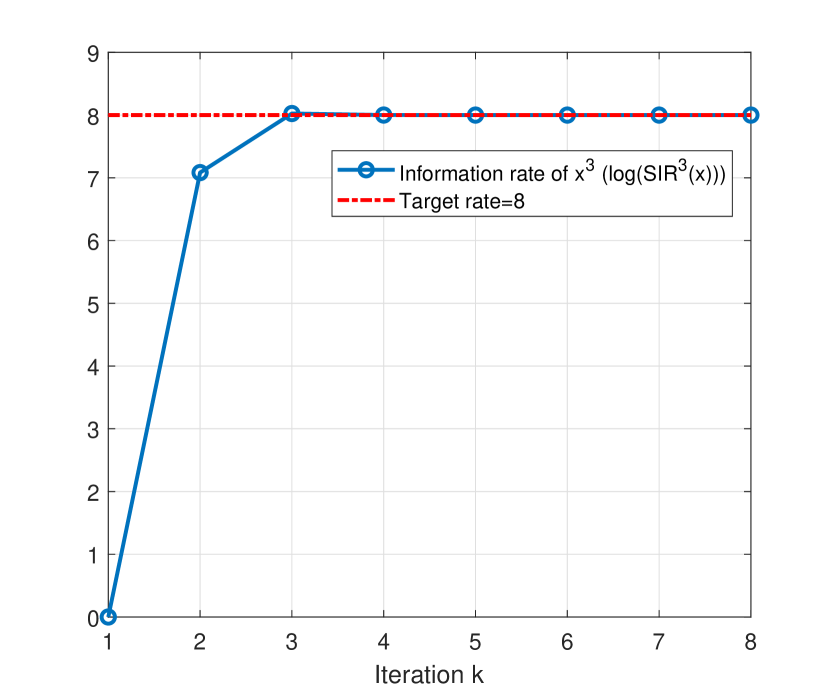

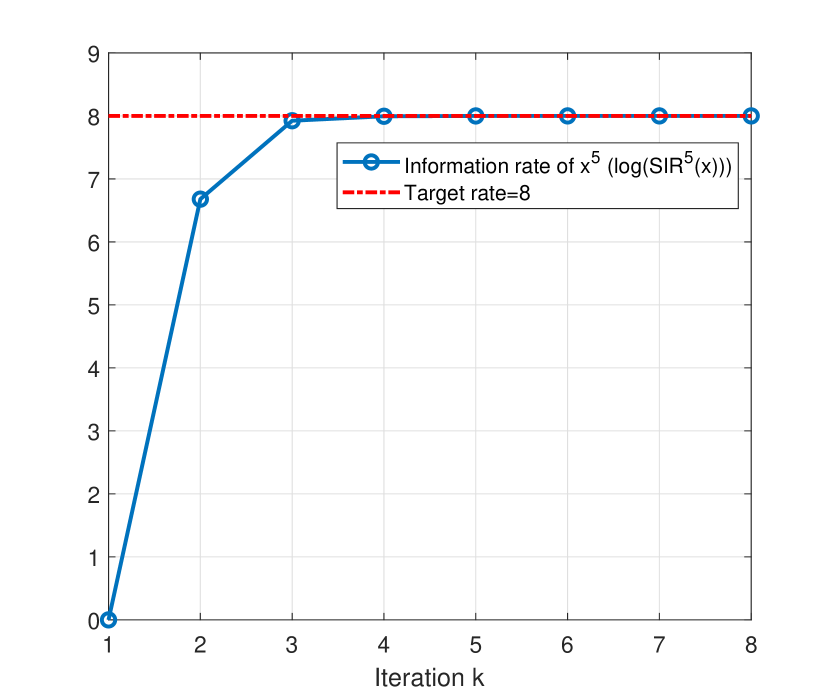

Problem A.9 (a) (Example 1 revisited, Power allocation in telecommunications)

This instance sets for all and , , for all players, and the starting point was set to . The data of coefficient is given in Facchinei and Kanzow (2009). As shown in Figure 1, the P-Lagrangian function values , , are monotonically decreasing and convergent, as expected. In addition, Figure 2 illustrates that the iterates of , , converge to a limit point satisfying the minimum target rate of 8.

Clearly, the computation time crucially depends on how the subproblems are solved efficiently. It is noteworthy that since the nonlinear coupling constraints are relaxed into the objective with the multipliers, the projection on the set can be performed efficiently, which leads to the convergence to a GNE within a significantly short CPU time of 0.32 seconds.

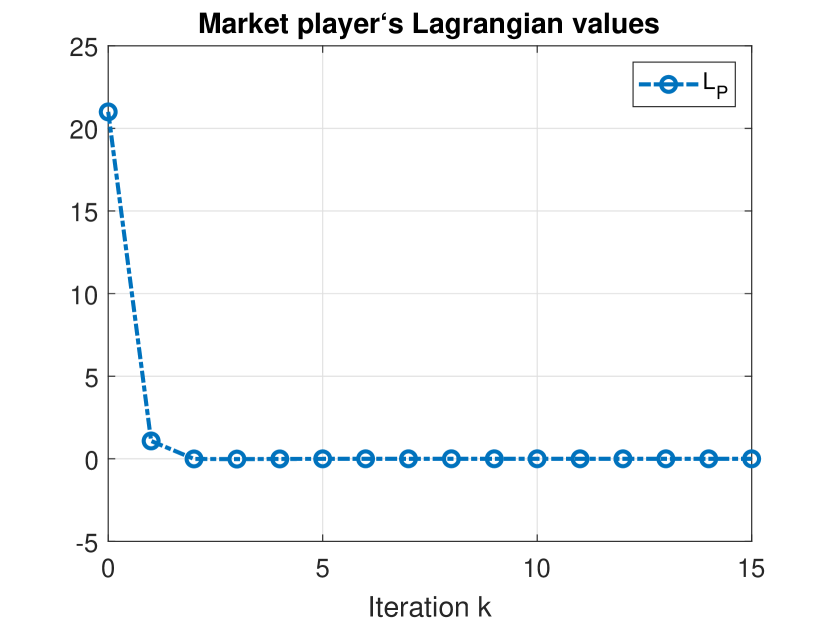

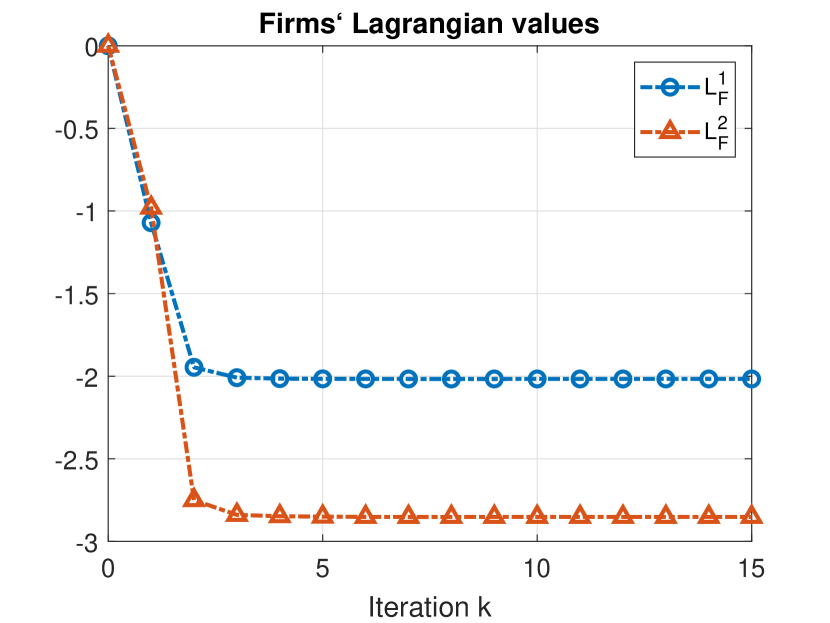

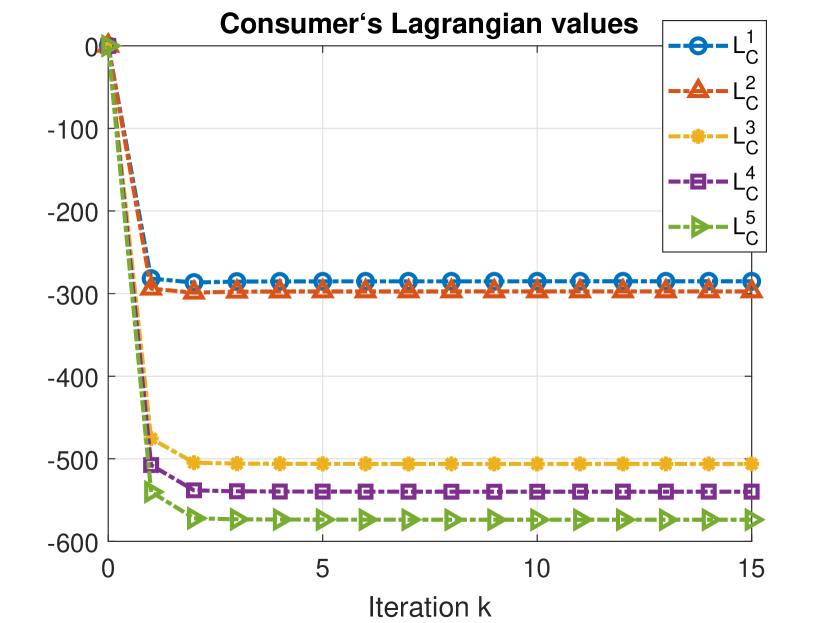

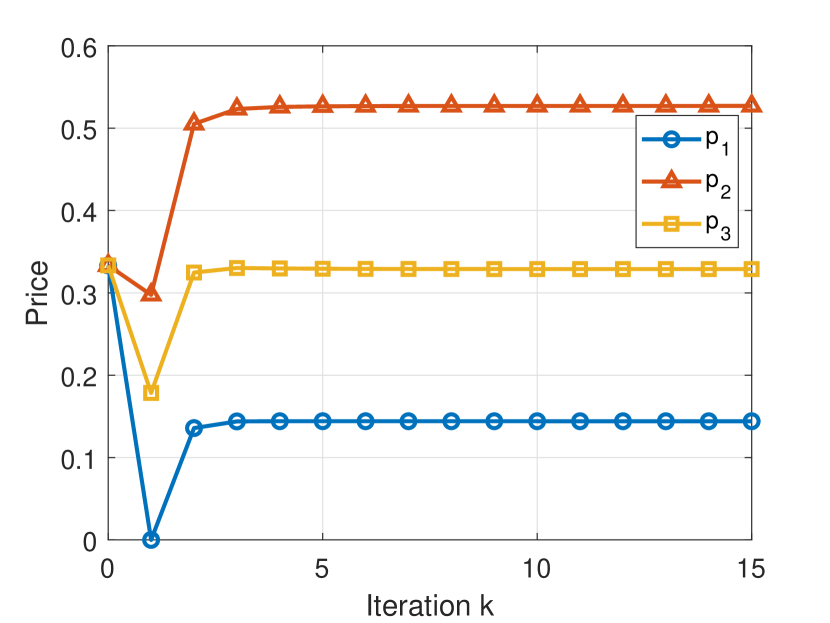

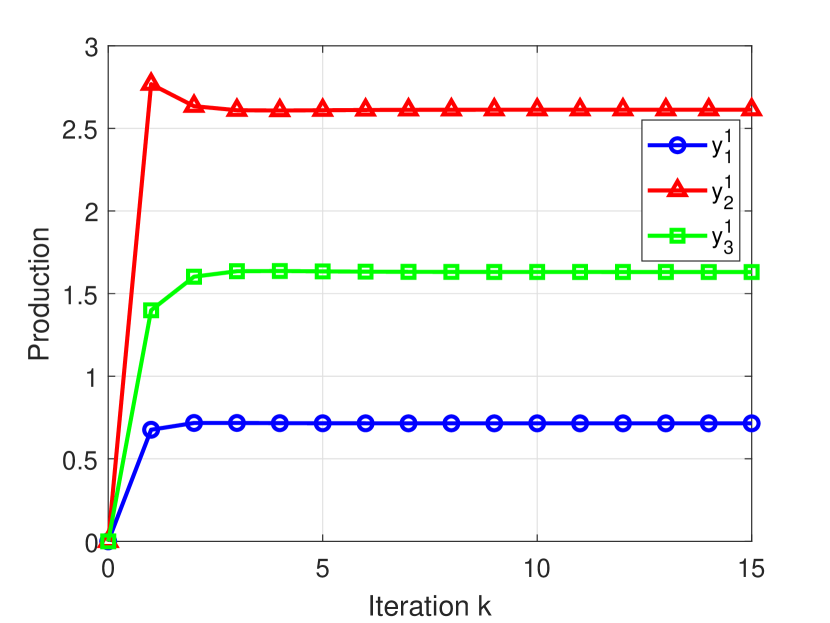

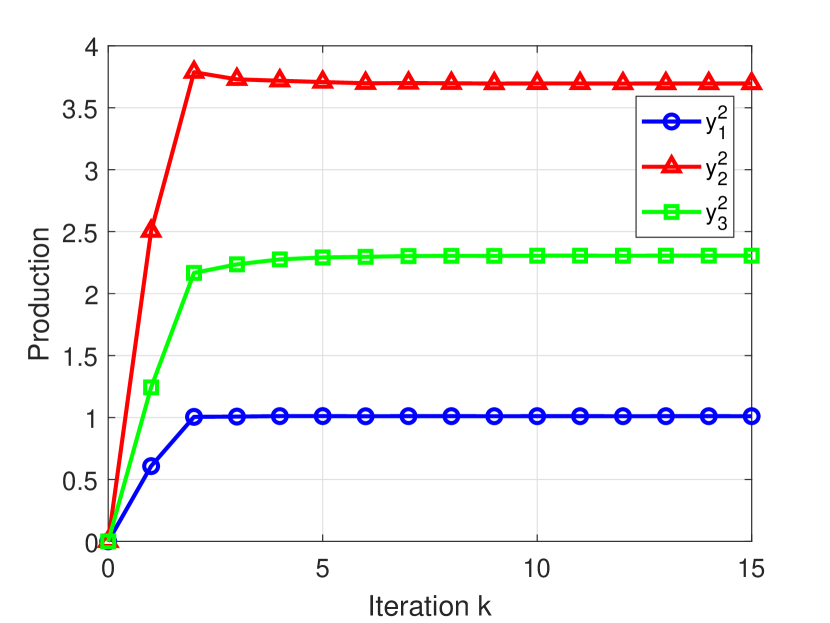

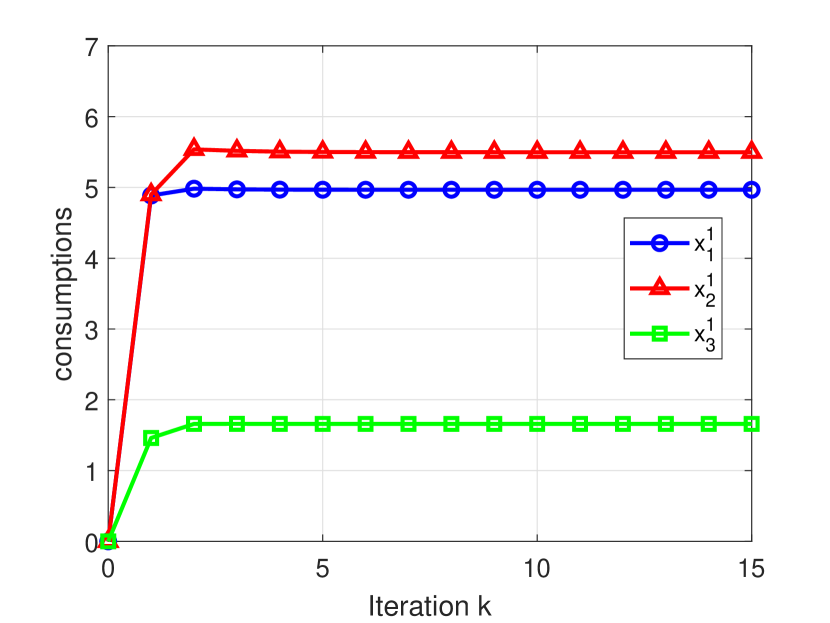

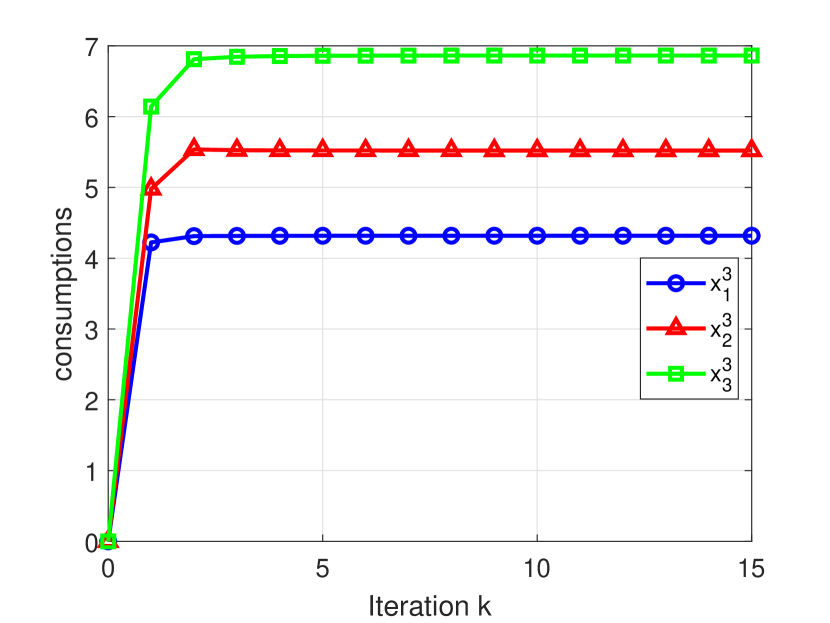

Problem A.10 (a) (Example 2 revisited, Arrow-Debreu general equilibrium model)

In this example, there are 8 players (, and one market player) and 3 goods (). The utility functions are quadratic and concave, and -th firm’s production set is defined by . The detailed data is given in Facchinei and Kanzow (2009).

The convergence results are shown in Figures 3 and 4. We see that the numerical results on this example also verifies our theoretical findings. Starting point is set to , , and . Figure 3 demonstrates that all players’ P-Langrangian values are decreasing and convergent to finite values. It can be also seen in Figure 4 that the iterates generated by Algorithm 1 converge to the equilibrium price vector that clears market as well as to the equilibrium productions and consumptions.

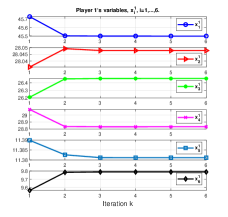

Problem A.18 (Electricity market model).

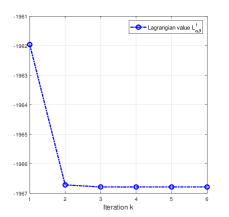

This electricity market model originally proposed by Pang and Fukushima (2005), and further discussed in Nabetani et al. (2011). There are two companies. Each company has an electricity plant in two out of three possible regions which are represented by the nodes of a graph. The goal is to maximize the profit of the company. The model has 18 variables, but we only present the reduced formulation with 12 variables. The reduction comes from the fact that both companies have plants on only 2 of the 3 nodes. We use the following abbreviations:

Player 1 has 6 variables and minimizes the objective function

and player 1 has the nonnegativity constraints, , capacity constraints

and coupling constraints .

Player 2 has 6 variables and minimizes its objective

and the nonnegativity constraints, , capacity constraints

and coupling constraints .

We only report numerical results for player 1 since player 2 has the same results. Figure 5 shows that company 1’s P-Lagrangian is convergent, and Algorithm 1 converges to a saddle-point that is a Nash equilibrium.

6. Conclusions

In this paper, we proposed a novel algorithmic framework for computing an equilibrium of generalized continuous Nash games (GNEPs) with theoretical guarantees based on the Proximal-Perturbed Lagrangian function. We have shown that the proposed method has significant advantages over existing approaches in both theoretical and computational perspectives; it does not require any boundedness assumptions and is the first development of an algorithm to solve general GNEPs in a distributed manner. The numerical results supported our theoretical findings. Possible future research is to extend our methodology to compute equilibria in stochastic Nash games with coupling constraints, which will result in a broader application domain.

The author would like to express his deep gratitude to John Birge for numerous insightful discussions and thoughtful suggestions on this work. The author would also like to thank the three anonymous reviewers for their valuable comments and suggestions that helped improve the paper.

References

- (1)

- Andreani et al. (2007) Roberto Andreani, Ernesto G Birgin, José Mario Martínez, and María Laura Schuverdt. 2007. On augmented Lagrangian methods with general lower-level constraints. SIAM Journal on Optimization 18, 4 (2007), 1286–1309.

- Andreani et al. (2008) Roberto Andreani, Ernesto G Birgin, José Mario Martínez, and Maria Laura Schuverdt. 2008. Augmented Lagrangian methods under the constant positive linear dependence constraint qualification. Mathematical Programming 111, 1-2 (2008), 5–32.

- Arrow and Debreu (1954) Kenneth J Arrow and Gerard Debreu. 1954. Existence of an equilibrium for a competitive economy. Econometrica 22 (1954), 265–290.

- Attouch and Bolte (2009) Hedy Attouch and Jérôme Bolte. 2009. On the convergence of the proximal algorithm for nonsmooth functions involving analytic features. Mathematical Programming 116, 1-2 (2009), 5–16.

- Attouch et al. (2010) Hédy Attouch, Jérôme Bolte, Patrick Redont, and Antoine Soubeyran. 2010. Proximal alternating minimization and projection methods for nonconvex problems: An approach based on the Kurdyka-Łojasiewicz inequality. Mathematics of Operations Research 35, 2 (2010), 438–457.

- Attouch et al. (2013) Hedy Attouch, Jérôme Bolte, and Benar Fux Svaiter. 2013. Convergence of descent methods for semi-algebraic and tame problems: proximal algorithms, forward–backward splitting, and regularized Gauss–Seidel methods. Mathematical Programming 137, 1-2 (2013), 91–129.

- Beck and Teboulle (2009) Amir Beck and Marc Teboulle. 2009. A fast iterative shrinkage-thresholding algorithm for linear inverse problems. SIAM Journal on Imaging Sciences 2, 1 (2009), 183–202.

- Bertsekas (1999) Dimitri P Bertsekas. 1999. Nonlinear programming. Athena scientific Belmont.

- Bertsekas (2014) Dimitri P. Bertsekas. 2014. Constrained optimization and Lagrange multiplier methods. Academic press.

- Bertsekas and Tsitsiklis (1989) Dimitri P. Bertsekas and John N Tsitsiklis. 1989. Parallel and distributed computation: numerical methods. Vol. 23. Prentice hall Englewood Cliffs, NJ.

- Birgin and Martínez (2014) Ernesto G Birgin and José Mario Martínez. 2014. Practical augmented Lagrangian methods for constrained optimization. SIAM.

- Bolte et al. (2014) Jérôme Bolte, Shoham Sabach, and Marc Teboulle. 2014. Proximal alternating linearized minimization or nonconvex and nonsmooth problems. Mathematical Programming 146, 1-2 (2014), 459–494.

- Boţ et al. (2019) Radu Ioan Boţ, Erno Robert Csetnek, and Dang-Khoa Nguyen. 2019. A proximal minimization algorithm for structured nonconvex and nonsmooth problems. SIAM Journal on Optimization 29, 2 (2019), 1300–1328.

- Boţ and Nguyen (2020) Radu Ioan Boţ and Dang-Khoa Nguyen. 2020. The proximal alternating direction method of multipliers in the nonconvex setting: convergence analysis and rates. Mathematics of Operations Research (2020).

- Breton et al. (2006) Michele Breton, Georges Zaccour, and Mehdi Zahaf. 2006. A game-theoretic formulation of joint implementation of environmental projects. European Journal of Operational Research 168, 1 (2006), 221–239.

- Bueno et al. (2019) Luis Felipe Bueno, Gabriel Haeser, and Frank Navarro Rojas. 2019. Optimality conditions and constraint qualifications for generalized Nash equilibrium problems and their practical implications. SIAM Journal on Optimization 29, 1 (2019), 31–54.

- Cardellini et al. (2016) Valeria Cardellini, Vittoria De Nitto Personé, Valerio Di Valerio, Francisco Facchinei, Vincenzo Grassi, Francesco Lo Presti, and Veronica Piccialli. 2016. A game-theoretic approach to computation offloading in mobile cloud computing. Mathematical Programming 157, 2 (2016), 421–449.

- Chung and Fuller (2010) William Chung and J David Fuller. 2010. Subproblem approximation in Dantzig-Wolfe decomposition of variational inequality models with an application to a multicommodity economic equilibrium model. Operations Research 58, 5 (2010), 1318–1327.

- Contreras et al. (2004) Javier Contreras, Matthias Klusch, and Jacek B Krawczyk. 2004. Numerical solutions to Nash-Cournot equilibria in coupled constraint electricity markets. IEEE Transactions on Power Systems 19, 1 (2004), 195–206.

- Debreu (1952) Gerard Debreu. 1952. A social equilibrium existence theorem. Proceedings of the National Academy of Sciences 38, 10 (1952), 886–893.

- Dreves et al. (2011) Axel Dreves, Francisco Facchinei, Christian Kanzow, and Simone Sagratella. 2011. On the solution of the KKT conditions of generalized Nash equilibrium problems. SIAM Journal on Optimization 21, 3 (2011), 1082–1108.

- Facchinei et al. (2007) Francisco Facchinei, Andreas Fischer, and Veronica Piccialli. 2007. On generalized Nash games and variational inequalities. Operations Research Letters 35, 2 (2007), 159–164.

- Facchinei and Kanzow (2009) Francisco Facchinei and Christian Kanzow. 2009. Penalty methods for the solution of generalized Nash equilibrium problems (with complete test problems). Sapienza University of Rome (2009).

- Facchinei and Kanzow (2010a) Francisco Facchinei and Christian Kanzow. 2010a. Generalized Nash equilibrium problems. Annals of Operations Research 175, 1 (2010), 177–211.

- Facchinei and Kanzow (2010b) Francisco Facchinei and Christian Kanzow. 2010b. Penalty methods for the solution of generalized Nash equilibrium problems. SIAM Journal on Optimization 20, 5 (2010), 2228–2253.

- Facchinei and Pang (2007) Francisco Facchinei and Jong-Shi Pang. 2007. Finite-dimensional variational inequalities and complementarity problems. Springer Science & Business Media.

- Hestenes (1969) Magnus R Hestenes. 1969. Multiplier and gradient methods. Journal of optimization theory and applications 4, 5 (1969), 303–320.

- Hobbs and Pang (2007) Benjamin F Hobbs and Jong-Shi Pang. 2007. Nash-Cournot equilibria in electric power markets with piecewise linear demand functions and joint constraints. Operations Research 55, 1 (2007), 113–127.

- Jing-Yuan and Smeers (1999) Wei Jing-Yuan and Yves Smeers. 1999. Spatial oligopolistic electricity models with Cournot generators and regulated transmission prices. Operations Research 47, 1 (1999), 102–112.

- Jofré et al. (2007) Alejandro Jofré, R Terry Rockafellar, and Roger JB Wets. 2007. Variational inequalities and economic equilibrium. Mathematics of Operations Research 32, 1 (2007), 32–50.

- Kanzow and Steck (2016) Christian Kanzow and Daniel Steck. 2016. Augmented Lagrangian methods for the solution of generalized Nash equilibrium problems. SIAM Journal on Optimization 26, 4 (2016), 2034–2058.

- Krawczyk and Uryasev (2000) Jacek B Krawczyk and Stanislav Uryasev. 2000. Relaxation algorithms to find Nash equilibria with economic applications. Environmental Modeling & Assessment 5, 1 (2000), 63–73.

- Kulkarni and Shanbhag (2012) Ankur A Kulkarni and Uday V Shanbhag. 2012. On the variational equilibrium as a refinement of the generalized Nash equilibrium. Automatica 48, 1 (2012), 45–55.

- Kurdyka (1998) Krzysztof Kurdyka. 1998. On gradients of functions definable in o-minimal structures. In Annales de l’institut Fourier, Vol. 48. 769–783.

- Li and Pong (2015) Guoyin Li and Ting Kei Pong. 2015. Global convergence of splitting methods for nonconvex composite optimization. SIAM Journal on Optimization 25, 4 (2015), 2434–2460.

- Li and Pong (2018) Guoyin Li and Ting Kei Pong. 2018. Calculus of the exponent of Kurdyka–Łojasiewicz inequality and its applications to linear convergence of first-order methods. Foundations of computational mathematics 18, 5 (2018), 1199–1232.

- Łojasiewicz (1963) Stanislaw Łojasiewicz. 1963. Une propriété topologique des sous-ensembles analytiques réels. Les équations aux dérivées partielles 117 (1963), 87–89.

- Luna et al. (2014) Juan Pablo Luna, Claudia Sagastizábal, and Mikhail Solodov. 2014. A class of Dantzig–Wolfe type decomposition methods for variational inequality problems. Mathematical Programming 143, 1-2 (2014), 177–209.

- Nabetani et al. (2011) Koichi Nabetani, Paul Tseng, and Masao Fukushima. 2011. Parametrized variational inequality approaches to generalized Nash equilibrium problems with shared constraints. Computational Optimization and Applications 48, 3 (2011), 423–452.

- Nash et al. (1950) John F Nash et al. 1950. Equilibrium points in n-person games. Proceedings of the national academy of sciences 36, 1 (1950), 48–49.

- Nedic et al. (2010) Angelia Nedic, Asuman Ozdaglar, and Pablo A Parrilo. 2010. Constrained consensus and optimization in multi-agent networks. IEEE Trans. Automat. Control 55, 4 (2010), 922–938.

- Nesterov (2012) Yurii Nesterov. 2012. Efficiency of coordinate descent methods on huge-scale optimization problems. SIAM Journal on Optimization 22, 2 (2012), 341–362.

- Pang and Fukushima (2005) Jong-Shi Pang and Masao Fukushima. 2005. Quasi-variational inequalities, generalized Nash equilibria, and multi-leader-follower games. Computational Management Science 2, 1 (2005), 21–56.

- Pang et al. (2008) Jong-Shi Pang, Gesualdo Scutari, Francisco Facchinei, and Chaoxiong Wang. 2008. Distributed power allocation with rate constraints in Gaussian parallel interference channels. IEEE Transactions on Information Theory 54, 8 (2008), 3471–3489.

- Powell (1969) Michael JD Powell. 1969. A method for nonlinear constraints in minimization problems. Optimization (1969), 283–298.

- Razaviyayn et al. (2013) Meisam Razaviyayn, Mingyi Hong, and Zhi-Quan Luo. 2013. A unified convergence analysis of block successive minimization methods for nonsmooth optimization. SIAM Journal on Optimization 23, 2 (2013), 1126–1153.

- Rockafellar (1974) R Tyrrell Rockafellar. 1974. Augmented Lagrange multiplier functions and duality in nonconvex programming. SIAM Journal on Control 12, 2 (1974), 268–285.

- Rosen (1965) J Ben Rosen. 1965. Existence and uniqueness of equilibrium points for concave n-person games. Econometrica 33 (1965), 520–534.

- Scutari et al. (2016) Gesualdo Scutari, Francisco Facchinei, and Lorenzo Lampariello. 2016. Parallel and distributed methods for constrained nonconvex optimization—Part I: Theory. IEEE Transactions on Signal Processing 65, 8 (2016), 1929–1944.

- Stein and Sudermann-Merx (2018) Oliver Stein and Nathan Sudermann-Merx. 2018. The noncooperative transportation problem and linear generalized Nash games. European Journal of Operational Research 266, 2 (2018), 543–553.

- Uryas’ev and Rubinstein (1994) Stanislav Uryas’ev and Reuven Y Rubinstein. 1994. On relaxation algorithms in computation of noncooperative equilibria. IEEE Trans. Automat. Control 39, 6 (1994), 1263–1267.

- Von Heusinger and Kanzow (2009a) Anna Von Heusinger and Christian Kanzow. 2009a. Optimization reformulations of the generalized Nash equilibrium problem using Nikaido-Isoda-type functions. Computational Optimization and Applications 43, 3 (2009), 353–377.

- Von Heusinger and Kanzow (2009b) Anna Von Heusinger and Christian Kanzow. 2009b. Relaxation methods for generalized Nash equilibrium problems with inexact line search. Journal of Optimization Theory and Applications 143, 1 (2009), 159–183.

- Xu and Yin (2013) Yangyang Xu and Wotao Yin. 2013. A block coordinate descent method for regularized multiconvex optimization with applications to nonnegative tensor factorization and completion. SIAM Journal on Imaging Sciences 6, 3 (2013), 1758–1789.

- Yin et al. (2011) Huibing Yin, Uday V Shanbhag, and Prashant G Mehta. 2011. Nash equilibrium problems with scaled congestion costs and shared constraints. IEEE Trans. Automat. Control 56, 7 (2011), 1702–1708.

Appendix

Appendix A Proofs of Theorems in Section 2

Before studying the relation between a saddle point of the P-Lagrangian (6) and an equilibrium of the GNEP (5), let us observe the following properties of .

Observation 1.

Notice that the inner minimization in (7) can be split into two parts as follows:

| (22) |

Denote by as a unique solution of the problem, for given . If we minimize with respect to , we have

Recall that based on the above optimality condition for , we can add a quadratic (regularization) term to make the Lagrangian strongly concave in the multipliers (for fixed ) and in (for fixed ) since it vanishes at the unique solution . Substituting into , reduces to

| (23) |

Then the P-Lagrangian dual problem can be expressed as

| (24) |

where , which is identical to the standard dual function associated with the original problem (1). Thus the P-Lagrangian dual function is maximized jointly in and if and only if maximizes and . This implies that the multiplier for the constraint in extended problem is precisely to the multiplier for the constraint in problem (1).

Observation 2.

If we maximizing with respect to , we get

which, together with the fact that , implies that at the maximizers and .

Using the Observations 1 and 2, we now establish the equivalence between a saddle point of and an equilibrium of the GNEP (1).

A.1. Proof of Theorem 2.1

Proof (b).

Using the reduced form of P-Lagrangian (23), we have

| (25) | ||||

First, we prove that is feasible for problem (1). Suppose by contradiction that is infeasible, i.e., for some . Then there exist some such that as . This implies by taking the limit as with to maximize the left-hand side of the first inequality in (25), which is a contradiction with the first inequality in (8). Therefore for all . By the definition with the fact that and , we have and . It follows that

A.2. Proof of Theorem 2

Proof (b).

First, we show that the first inequality in (9) holds. From the feasibility of an equilibrium , we have for any , and

| (28) |

implying that

On the other hand, since there exists a pair of multipliers maximizing , we also have for

which together with the fact that gives

| (29) |

Combining (28) and (29), we obtain

It thus follows that

Hence, the first inequality in (9) holds. Furthermore, by using the fact that and with (29), we have that which implies the multiplier satisfies the complementarity slackness and . Thus the maximizer is equivalent to the Lagrange multiplier satisfying the KKT conditions (3) for the original GNEP (1).

Appendix B Proof of Lemma 2

Proof (b).

(a) Fix , and omit the iterates for simplicity in the proof. Let be th component of the unique solution . From the fixed-point characterization of

and the contraction property of projection operator , we have that for all

| (30) | ||||

By expanding the last term on the right, the above inequality can be rewritten as

| (31) | ||||

Since is strongly convex in with constant and is Lipschitz continuous with constant (see properties (P3) and (P4) in Remark 1), we can estimate the second term and third term on right-hand side of (31)

| (32) |

| (33) |

Note that since is a proximal linearized function with the quadratic term , we can take . Substituting (32) with and (33) into (31) yields

Notice that is satisfied since . Now, setting and observing that , where and , it immediately follows that

Thus, for implying that , we obtain

| (34) |

where . Therefore, by summing over the above inequality (34) for all players from to , we deduce the desired result (16).

(b) From the property (P1) in Remark 1 with , we know that

| (35) |

Since and by the result (a), the inner gradient projection (15) can find a point close to such that

| (36) |

in a finite number of iterations. In addition, by the property (P2) in Remark 1 with , we have that for any ,

| (37) |

Combining (35), (36), and (37) yields

Hence, we can derive the desired decrease property of every during inner iterations.

Appendix C Proofs of Key Results in Section 4.1

C.1. Proof of Lemma 3

Proof (b).

Note that since is strongly concave in for fixed , there exists a unique maximizer, denoted by , such that

From the update of defined (as maximizer) in Step 3, we have

By the definition in Step 2 with in Step 3, we have for the same starting point . Adding the above inequalities and a direct computation of give

| (38) | ||||

where, to bound the third term, we used Lemma 1(a) in Nedic et al. (2010); with , , , and the fact . Specifically, since maximizes , we have

and . It thus follows that

which, by definition of projection (Bertsekas and Tsitsiklis, 1989, Section 3.4), means that can be viewed as the projection of onto the solution set . We thus see that

Note that using the Cauchy-Schwarz inequality, we also get that implying the stable sequence of the multipliers. Rearranging terms in (38), we obtain

which leads to

where follows from the Cauchy-Schwarz inequality; is from the continuous differentiability of (Assumption 1), implying that is Lipschitz continuous with constant . Squaring both sides of the inequality gives the desired result (20).

C.2. Proof of Lemma 4

Proof (b).

Consider the difference of two consecutive sequences of :

| (39) | ||||

We estimate the two terms on the right-hand side of (39) one by one. For the first term, using the descent lemma (Lemma 1), we have

| (40) |

Here, we omitted for simplicity. By Step 1 of Algorithm 1, we have

Thus we obtain

By substituting the above expression into (40) and using the definition of in Step 2, we get

| (41) |

Next, consider the second term:

| (42) | ||||

where it follows from Step 3 that the second and third terms on the right-hand side are zero.

We now focus on deriving an upper bound for the term . To this end, we need to consider two cases: and .

Case 1. . By the definition of and from Step 3, we obtain

| (43) |

Case 2. . Note that in this case, and is feasible because . For convenience, we define

Then, by subtracting and adding the term to the right-hand side and using the fact that , it follows that

| (44) |

From the feasibility of , we have that for any , and

Thus, we can get with and that

On the other hand, since maximizes for given and the third term,

is a given constant, we have that

Hence,

| (45) |

Combining (44) and (45) and invoking Lemma 3, we obtain

| (46) | ||||

Notice that the above upper bound on includes the upper bound in Case 1. Therefore, by combining (41), (42) and (46), we obtain the desired result:

which implies that the sequence is monotonically decreasing if is chosen such that with a suitable choice of .

Next, we show that is a convergent sequence. we know from Lemma 2 that a saddle point of exists. Let be a saddle point of . By the updating rules for defined as maximizers for updated and the saddle point condition (8), we see that

| (47) |

which implies that the sequence is lower bounded by a finite value of . Therefore, with the choice of such that , the sequence converges to a finite limit, denoted by , as .

C.3. Proof of Theorem 3

Proof (b).

(a) Recall from Lemma 2 that a saddle point of exists. We know from (47) that is lower bounded by . In addition, since is nonincreasing, it is also upper bounded by a finite value, i.e, . We thus have

Hence, the sequence is bounded due to the coercivity of (Assumption 3) with the facts that and .

(b) Note that since the function is strongly concave, there exists parameter such that for and for given

where we omitted for notational simplicity. Adding the above two inequalities yields

Using the Cauchy-Schwarz inequality and the triangle inequality, we obtain

where the inequality comes from the definition of in Step 3, implying that . Since is bounded and is continuous differentiable (Assumption 1), there exists such that . From the update of in Step 3, we have for any . By taking we have

Therefore, the sequence is bounded on any subset of .

Appendix D Proofs of Main Convergence Results in Section 4.2

D.1. Proof of Theorem 4

Proof (b).

By Theorem 3, the sequence is bounded, so there exists at least one limit point. Let be a limit point of , and let be a subsequence converging to as . From Theorem 3(c), it also follows that as .

First, we show that a limit point satisfies the second inequality of the saddle point condition (8). Because and as , we have from Step 1 that

The limit point is equivalent to a solution of the VI (Facchinei and Pang, 2007, Prop. 1.5.8):

Using the fact that and the convexity of with respect to , we obtain the first-order optimality condition for :

Equivalently,

which implies that satisfies the second inequality of the saddle point condition (8).

Before proceeding with global convergence, let us provide some preliminaries, which are central to our global convergence analysis.

Lemma 5 (Uniformized KŁ Property (Bolte et al., 2014, Lemma 6)).

Let be a compact set and let be proper, lower semicontinuous function. Assume that is constant on and satisfies the KŁ property at each point of . Then there exist , and such that for all in and all in the following intersection:

| (48) |

one has,

| (49) |

Note that if the function is continuously differentiable and , the inequality (49) can be rewritten as

With the uniformized KŁ property, we can prove that the generated sequence has finite length, and hence the whole sequence converges to a saddle point. The techniques developed in Bolte et al. (2014) are extended to our smooth constrained game setting with some modifications.

In order to exploit Lemma 5 for proving global convergence, we need to use the size of the gradient of the P-Lagrangian, denoted by , and derive an upper bound on the gradient. Noting that and are continuously differentiable, , and , we consider the following projected gradients of in and for -component and -component of :

Let us now define the projected gradient of at as

| (50) |

It is clear that if , then a saddle point of is obtained. In what follows, we derive an upper bound on in terms of the generated iterates by Algorithm 1.

Recall that the conditions (2a), (2b), (2e), and (2f) in Assumption 2 imply there exist constants and such that

| (51a) | ||||

| (51b) | ||||

where and .

Lemma 6.

Let be the sequence generated by Algorithm 1. Then, for every , there exist constant such that for all

| (52) |

Proof 6.

We first estimate an upper bound for the norm of component in . Recall that there exists a unique solution of the approximation subproblem in (12) at each iteration (Lemma 2), and denote by the th component of . From the fixed-point characterization of , we know that for every

Hence,

where follows from the nonexpansive property of the projection operator, and is due to the facts that and . Then, by adding and subtracting and using the triangle inequality, we obtain

| (53) |

where the second inequality follows from the Lipschitz continuity of and (see (51a) and (51b)), and the boundedness of and implying that there exist constants and ; in the last inequality we used that (Lemma 3).

Next, notice that from the definition of as a maximizer for given , is also characterized by

which, together with the nonexpansive property of the projection onto and Lemma 3, yields

| (54) |

D.2. Proof of Theorem 5

Proof 6.

Let be a limit point of the sequence that is bounded for every . Then, by the continuity of , we have

| (57) |

In the following, we consider two cases:

Case 1. Suppose that there exists an integer such that for . Since the sequence is nonincreasing, we have that for all . Then, we have from Lemma 4 that for any

which leads to

| (58) |

From Lemma 3, we also obtain that and for all . Therefore, must be eventually constant (stationary), and it thus has finite length.

Case 2. Consider now the case where such an integer does not exist (and every is nonstationary) for . In this case, we first show that the P-Lagrangian is finite and constant on the set of all limit points of the sequence , and then apply Lemma 5 to show that is a Cauchy sequence and convergent.

First, note that since the sequence is nonincreasing, we have that for all . This, along with (57), implies that there exists an integer large enough such that for any and in Lemma 5

| (59) |

where the second comes from the fact that (see Theorem 4). Thus belongs to the intersection in (48) with for all , and is nonempty and compact. Recall that is bounded below by the value of at a saddle point, and hence converges to a finite limit, denoted by . It then follows from (57) that , which shows that is finite and constant on .

Thus, since is a KL function, by applying Lemma 5 with and , we get that for any

which combined with Lemma 6 gives

| (60) |

On the other hand, since is concave function, we know that

| (61) |

For convenience, we define for any

Then we get

| (62) |

Recalling from Lemma 4 that , we combine (60) and (62) to obtain

Multiplying the above inequality by gives

and hence Using the inequality for any with and , we have

| (63) |

Now we show that for any the following inequality holds:

By summing (63) over , we have

| (64) |

and using fact that for all , we get

| (65) |

where the last inequality follows from the fact that . Plugging (65) into (64) and rearranging terms, we obtain

| (66) |

Since the right-hand side of (66) does not depends , the sequence has finite length, i.e.,

This implies is a Cauchy sequence and thus a convergent sequence. By Lemma 3, the multiplier sequences and are also Cauchy. Therefore, we conclude that the whole sequence converges to a saddle point of , .

We end by noting that convergence rate of the generated sequence described in Theorem 5 can be easily derived by applying the generic rate of convergence result in Attouch and Bolte (2009).

Theorem 6 (Convergence Rate).

Suppose that every and satisfy the KL property, where the desingularizing function of is of the form: Let be the limit point of . Then the following convergence rates hold:

-

(a)

If , then converges to in a finite number of steps.

-

(b)

If , then for all , for certain .

-

(c)

If . then .