Proof.

.:

Local Whittle estimation of high-dimensional

long-run variance and precision matrices

111AMS subject classification. Primary: 62M15, 62H12. Secondary: 62H20.

222Keywords and phrases: High-dimensional time series, frequency domain, short- and long-range dependence, spectral density estimation, shrinkage estimation, local Whittle estimation.

333This work was carried out during stays of the first and second authors in the Department of Statistics and Operation Research at the University of North Carolina, Chapel Hill. The first and second authors thank the department, in particular, Vladas Pipiras for their hospitality. The first author was supported by the National Research Foundation of Korea (NRF-2019R1F1A1057104, NRF-2022R1F1A1066209). The second author was supported by the DFG (RTG 2131) and the NSF grant 1934985. The third author was supported in part by the NSF grant DMS-1712966.

Abstract

This work develops non-asymptotic theory for estimation of the long-run variance matrix and its inverse, the so-called precision matrix, for high-dimensional time series under general assumptions on the dependence structure including long-range dependence. The estimation involves shrinkage techniques which are thresholding and penalizing versions of the classical multivariate local Whittle estimator. The results ensure consistent estimation in a double asymptotic regime where the number of component time series is allowed to grow with the sample size as long as the true model parameters are sparse. The key technical result is a concentration inequality of the local Whittle estimator for the long-run variance matrix around the true model parameters. In particular, it handles simultaneously the estimation of the memory parameters which enter the underlying model. Novel algorithms for the considered procedures are proposed, and a simulation study and a data application are also provided.

1 Introduction

Spectral density matrices characterize the component and temporal dependence of multivariate time series, and its estimation is of interest in many areas, including economics and neuroscience. The long-run variance and precision matrices give, respectively, information about correlations and partial correlations between different component series around zero frequency; see Dahlhaus (2000). Their estimation are the frequency domain analogues of covariance and inverse covariance estimation; see Fan et al. (2016) for a survey on large (inverse) covariance matrix estimation. Obtaining an estimate for the spectral density matrix can become particularly challenging in a high-dimensional regime when the number of component series becomes relatively large compared to the length of the time series. In this regime, estimation often employs different shrinkage methods. The development, theoretical verification and application of different shrinkage methods has been an active research area, along with a growing interest in non-asymptotic theory in high-dimensional statistics; see Wainwright (2019) for a survey on non-asymptotic theory.

This paper develops non-asymptotic theory for estimation of the long-run variance and precision matrices of a stationary multivariate time series around zero frequency while allowing for short- and long-range dependence. The local Whittle estimation is used with thresholding and LASSO-type penalizations. Our non-asymptotic theory allows to infer consistency results on the estimators around the true parameters in a high-dimensional regime where the number of component series can be large compared to the number of observations. We also note that our non-asymptotic results are new even for the one-dimensional case.

Our setting is as follows. Consider a -dimensional second-order stationary time series , , with zero mean and autocovariance matrix function , . Suppose that its spectral density matrix , , related to the autocovariance matrix through , satisfies

| (1.1) |

where denotes componentwise asymptotic equivalence, with , , and is Hermitian symmetric and positive definite. Each individual component series , , satisfies (1.1) with memory parameter . The case is associated with short-range dependence, the case with long-range dependence and with antipersistence. We refer to Beran et al. (2013); Pipiras and Taqqu (2017) for more details on univariate short- and long-range dependence and Kechagias and Pipiras (2015a) for a discussion on multivariate long-range dependence. The matrix is the long-run variance matrix and is the precision matrix. They are the focus of this work.

In the presence of long-range dependence, local Whittle estimation is commonly used to estimate the parameters of the model (1.1). We introduce here the classical multivariate local Whittle estimators for and refer to Section 2 for a detailed explanation of the used shrinkage techniques. In particular, we aim to utilize a thresholding technique to estimate the long-run variance matrix sparsely (see (2.2) below) and a LASSO-type estimator to estimate the precision matrix sparsely (see (2.3) below).

The local Whittle estimators introduced in Robinson (2008) are given by

| (1.2) |

for the negative log-likelihood

| (1.3) |

where and denote the determinant and the trace of a matrix,

| (1.4) |

is the periodogram for sample size and is the number of Fourier frequencies used in estimation. The optimization problem (1.3) can be reduced to

| (1.5) |

where

| (1.6) |

Local Whittle estimation was studied by multiple authors. Robinson (1995b) showed consistency and asymptotic normality of the univariate local Whittle estimators. In the bivariate case , the asymptotic normality of the local Whittle estimators of memory parameters was established in Robinson (2008), and that of all model parameters in Baek et al. (2020). Asymptotic normality results in special cases of (1.1) but general fixed dimension appear in Shimotsu (2007); Nielsen (2011). In Düker and Pipiras (2019), an asymptotic normality result for the local Whittle estimators (1.2) of all model parameters and general fixed was obtained.

The graphical local Whittle estimator is an -penalized version of the negative log-likelihood in (1.3), as proposed in Baek et al. (2017) with the focus on its good numerical performance. It can also be written as a function of the precision matrix . We refer to Section 2 and equation (2.4) below for a detailed description of the penalized objective function. The objective function coincides with that used in estimating covariance matrices sparsely; see Bien and Tibshirani (2011). On the other hand, for a penalization of the respective inverse, it coincides with the graphical LASSO estimator; see Friedman et al. (2008). Düker and Pipiras (2019) derived asymptotic results for the estimators of the long-run variance matrix and the precision matrix in a “fixed , large ” regime under the discussed -penalization.

Sparse covariance and its precision matrix estimation were studied by numerous authors. LASSO-type estimators were investigated by Rothman et al. (2008), Cai et al. (2011) and Shu and Nan (2019). See also Cai et al. (2016) for a review of recent developments. Thresholding based strategies were pursued by Bickel and Levina (2008a, b), Rothman et al. (2009) and Cai and Liu (2011). In contrast, there is less research work for high-dimensional spectral density matrix estimation.

The works of Shu and Nan (2019), Sun et al. (2018) and Fiecas et al. (2019) are probably the closest to our work. Shu and Nan (2019) considered the estimation of large covariance and its precision matrices from high-dimensional sub-Gaussian or heavier-tailed observations with slowly decaying temporal dependence. Sun et al. (2018) developed a non-asymptotic theory for estimation of the spectral density matrix of multivariate time series under short-range dependence, that is, when in (1.1). The work in Fiecas et al. (2019) developed some non-asymptotic theory for estimation of the spectral density matrix and its inverse for a class of time series exhibiting short-range dependence under a mixing condition. In contrast, we allow for a quite general dependence structure including short- and long-range dependence and antipersistence.

From a practical perspective estimating the spectral density matrix and its inverse have applications in many fields including signal processing (Schneider-Luftman and Walden, 2016), neuroscience (Fiecas and Ombao, 2011; Bowyer, 2016; Bordier et al., 2017) and economics (Granger, 1969; Hansen and Sargent, 1983; Politis, 2011; Plagborg-Møller and Wolf, 2021; Cavicchioli, 2022). The spectral density matrix captures contemporaneous correlation and correlation across different lags. It therefore provides a richer description of the dependence structure in a multivariate time series than the covariance matrix.

The literature review shows that there is a gap in theoretical results concerning high-dimensional spectral density estimation for time series possibly exhibiting long-range dependence. We are the first to provide non-asymptotic theoretical results for thresholding and graphical local Whittle estimation which allow to infer consistency in a possibly double asymptotic regime of large and . The presence of long-range dependence and the simultaneous estimation of the memory parameters , make it particularly challenging to derive non-asymptotic results. We overcome those challenges by using a uniform concentration inequality and controlling the difference between the sample and the population version of the matrix simultaneously. Our theoretical results turn out to be useful not only for thresholding and graphical local Whittle estimators but can be applied to derive consistency for other kinds of penalized estimators. We demonstrate that by deriving consistency results for estimators based on the coherence matrix and a constrained -minimization (CLIME). We also address the question of consistent model selection by adopting different thresholding procedures to the spectral setting. Additionally, we introduce novel algorithms to compute the thresholded and penalized local Whittle estimators. The results are accompanied by a simulation study which assesses the numerical performance of the suggested algorithms and estimators.

The rest of the paper is organized as follows. In Section 2, we discuss our estimation procedure and present some assumptions required for our theoretical analysis. In Section 3, we present an outline of the proof, our main results and some discussions of those results. Appendix A provides more technical details for the statements of our results, allowing to keep the notation in the paper’s main body shorter. In Section 4, we introduce two algorithms to compute the penalized graphical local Whittle estimators. The performance of those algorithms is analyzed in a simulation study conducted in Section 5 with complementary results in Appendix F. An application can be found in Section 6. We conclude with Section 7. The proofs can be found in Appendix B. In Appendices C and D, we provide some technical results and their proofs. Finally, Appendix E provides the proofs for an extension to linear processes.

Notation: For the reader’s convenience, we give a collection of notation used throughout the paper. We denote the maximum and minimum eigenvalues of a symmetric or Hermitian matrix by and , respectively. To indicate that a matrix is positive (semi-)definite, we write . We use a range of different matrix norms, namely, the maximum norm, the spectral norm and the Frobenius norm, defined respectively as , and for a matrix . We use to denote the th unit vector in for . For the vectorized version of a matrix , we write . The vec operator transforms a matrix into a vector by stacking its columns one underneath the other. For a matrix, composed of -dimensional vectors , we write . We let be the space of square-integrable functions on with respect to the Lebesgue measure. If is an integral operator on of the form , then is called Hilbert-Schmidt if and only if

| (1.7) |

where the double integral in (1.7) is denoted as and called the Hilbert-Schmidt norm. Let further be a linear operator with normed spaces . We write for the operator norm of , where denotes the norm on . As a further convention we write if there exists a universal constant such that . We further use the notation to denote the partial derivative with respect to and to denote the gradient of a function .

2 Estimation methods and assumptions

In this section, we formulate the long-run variance and precision matrix estimation through the thresholding and graphical local Whittle estimators, respectively. Furthermore, we give the required assumptions to prove non-asymptotic bounds which ensure consistency results for the estimators in a double asymptotic regime of large and .

The thresholding and graphical local Whittle estimators require estimation of the memory parameters . We propose here to estimate each , by the univariate local Whittle estimator; see Remark 2.2 below for a discussion of this. We introduce a notation different from that used for the multivariate local Whittle estimators in (1.2) to emphasize the use of the univariate version of the local Whittle estimator. For a multivariate time series satisfying (1.1), each individual, univariate time series , , satisfies

where , , and and denote the th entry of and , respectively. Then, the univariate local Whittle estimator for is given by

| (2.1) |

where the set of admissible estimates is defined as with and

where denotes the th entry of the periodogram in (1.4). After estimating each individual memory parameter by (2.1), we want to estimate the long-run variance matrix and the precision matrix sparsely by thresholding and graphical local Whittle estimation, respectively.

Thresholding local Whittle: We propose to use hard thresholding to estimate the long-run variance matrix sparsely. (Soft or adaptive thresholding could also be used.) That is,

| (2.2) |

where is a threshold and is a thresholding operator applied to , the th entry of the estimator for the long-run variance matrix (1.6) and the components of are estimated univariately by (2.1).

Graphical local Whittle: The precision matrix can be estimated sparsely by the graphical local Whittle estimator, a penalized version of the negative log-likelihood function (1.3). The penalized estimator is given by

| (2.3) |

where is estimated univariately by (2.1) and

| (2.4) |

with a penalty parameter and the -norm excluding the diagonal elements.

Next, we give some assumptions, required to establish our theoretical results. Other assumptions appear in the statements of our results. Subsequently, we discuss those assumptions in several remarks.

Assumption 1.

Suppose that

| (2.5) |

where denotes componentwise asymptotic equivalence, is Hermitian symmetric and positive definite and , where denotes the set of all real-valued diagonal matrices. We further suppose that the positive eigenvalues of can be bounded from below as

| (2.6) |

Assumption 2.

For some , the spectral density matrix satisfies

| (2.7) |

for and some .

Assumption 3.

The function is differentiable on and there is a constant such that

Besides assumptions on the spectral density matrix of the underlying process, we will also impose some mild assumptions on the process itself. In particular, our results are valid not only for Gaussian time series but also for a large class of non-Gaussian processes. Our assumption will be formulated in terms of sub-Gaussian random variables, that is, their distribution is dominated by a centered Gaussian distribution. More precisely, we call a random variable sub-Gaussian if there is a constant such that

We further denote , the sub-Gaussian norm of a real-valued random variable . Gaussian random variables belong to the class of sub-Gaussian random variables. We refer to Vershynin (2010) for more details on sub-Gaussian random variables.

Assumption 4.

The time series is assumed to be either Gaussian or to have a linear representation with and independent mean innovations , where each component , of the random vector is assumed to be sub-Gaussian, satisfying

| (2.8) |

for some constant .

Assumption 5.

The number of frequencies used in estimation and the lower bound of the interval of admissible estimates satisfy

Our work intends to provide non-asymptotic results. However, we impose some mild assumptions on our choices of the number of frequencies and the sample size to simplify some of our bounds. Throughout the paper we suppose that the number of frequencies and the sample size satisfy . Those assumptions allow us to use and , and the same for . Another assumption we impose is which ensures that the bound on the bias term of the periodogram is finite.

We use different measures of sparsity for the long-run variance and the precision matrices. Both are commonly used in the respective literatures.

In the context of thresholding, a commonly used measure of sparsity for the long-run variance matrix is given by

| (2.9) |

for . This measure was proposed in Bickel and Levina (2008b) and shown to capture a variety of sparsity patterns. It was further applied in the context of spectral density estimation in a non-asymptotic regime in Sun et al. (2018).

For the precision matrix, we define the set

| (2.10) |

and bound its cardinality with .

We will also use

as a measure of stability of the time series . This follows Basu and Michailidis (2015) and Sun et al. (2018) who considered the case and , which is associated with short-range dependence of the underlying time series. See also the second paragraph of Section 2 in Sun et al. (2018) for a discussion on how acts as a measure of stability.

The following remarks comment on the model, estimation procedure and on the assumptions above. Remark 2.1 comments on the model and Remark 2.2 concerns estimating the memory parameters univariately, Remark 2.3 is on Assumptions 1 and 2, and Remarks 2.4, 2.5 and 2.6 are on Assumptions 3, 4 and 5, respectively.

Remark 2.1.

In this work, we assume that the matrix in (1.1) is possibly complex valued Hermitian symmetric. In order to achieve sparsity, both real and imaginary part need to be zero. Related literature has also studied an alternative way to parametrize the matrix . Proposed by Robinson (2008) and further studied in Düker and Pipiras (2019) and Baek et al. (2020), one can write in terms of polar coordinates, that is,

with the so-called phase parameter and . In this parametrization, one cannot test for uncorrelatedness between component series (), since the respective phase parameter is not identifiable for , ; see Düker and Pipiras (2019) and Baek et al. (2020) for a related discussion.

Remark 2.2.

Our proposed estimation procedure involves estimating the memory parameters by the univariate local Whittle estimators (2.1) rather than using the multivariate estimator of the matrix in (1.5). The reasons are twofold, one is theoretical, the other computational.

The theoretical reason is that getting a concentration inequality on for the multivariate estimates of involves a concentration inequality on . In the asymptotic regime and for fixed dimension , a consistency result for can be achieved easily by combining the continuous mapping theorem and a consistency result on . However, our non-asymptotic setting involves an inequality of the form , with a generic constant . The additional weakens the results in the sense that has to grow much slower than in order to achieve consistency. Bounding further as results in an additional . A potential way to avoid the second one gets through bounding the operator norm might be to impose a sparsity assumption on and threshold in the objective function (1.5). That is, estimating as in (1.5) involves an estimator for . However, the estimator for is not based on a thresholded version of . One possibility to address this issue is to introduce a shrinkage on in (1.5) by using a thresholded version of .

On the other hand, computationally, it is faster to minimize univariate functions as opposed to optimizing a matrix function over a certain set of diagonal matrices. In a simulation study in Appendix F.3, we show that the difference between the multivariate and univariate estimates is negligible.

Remark 2.3.

Assumption 1 with (2.5) coincides with the basic model (1.1) and supposes additionally that the true memory parameters are contained in the interval of admissible estimates. Besides assuming that the matrix is positive definite, we suppose in (2.6) that the eigenvalues of are bounded from below. This is a typical assumption in sparse covariance estimation; see Rothman et al. (2008). Assumption 2 is a smoothness condition and controls the second order terms of the spectral density matrix. Usually, the componentwise relation , as , is imposed to derive asymptotic results in the context of spectral density estimation. However, we require a slightly stronger assumption (2.7) in order to control the bias terms to derive non-asymptotic results.

Remark 2.4.

Assumption 3 is required to ensure that the bias term is asymptotically negligible. This kind of assumption appears in the asymptotic literature regarding local Whittle estimation as well; see Assumption A.2 in Robinson (1995b) and Assumption A.1 in Robinson (2008). However, those assumptions typically only require differentiability in an epsilon region around the origin. We need to impose differentiability in a region which includes all frequencies used in estimation and allows for all choices of .

Remark 2.5.

Our main assumptions on the underlying process are the parametrization of the spectral density in terms of the matrices as formalized in Assumption 1, and Assumption 4 which ensures that the series is either Gaussian or follows a linear representation. Though, we require the innovations of the linear representation to be sub-Gaussian, our results can be used to derive statements for sub-exponential innovations or assuming finite fourth moments; see Remark E.1 for a more detailed discussion. Our assumptions allow for quite general long- and short-range dependent linear time series. For long-range dependence, examples are multivariate FARIMA series as defined in Kechagias and Pipiras (2015a). For short-range dependence, examples are multivariate ARMA models.

Remark 2.6.

Assumption 5 is satisfied, in particular, when , that is, when the underlying time series exhibits only short- or long-range dependence. In other words, the assumption is only needed when the true memory parameters , , are known to take also values in . The case contributes to the non-asymptotic bounds in our main results in form of two terms and . Assumption 5 is necessary to ensure that our non-asymptotic bounds prove consistency, which is the case as long as both quantities go to infinity while the sample size increases. Assumption 5 not only controls but is also sufficient to control the second quantity, since

3 Main results

In this section, we present our main results. Section 3.1 provides a roadmap for our proofs which reveals what kind of results are necessary to prove consistency for both the thresholding and graphical local Whittle estimation. This includes in particular a consistency result on the maximum norm of . Subsequently, we formally state our main results in Section 3.2, that is, consistency results for the thresholding and graphical local Whittle estimators. Section 3.3 discusses alternative estimators for precision matrix estimation and their convergence rates. We provide results on consistent model selection in Section 3.4. In Section 3.5, we discuss how our results compare to existing results in the literature.

3.1 Proof idea

In contrast to the spectral density estimation under short-range dependence, allowing for long-range dependence and antipersistence requires estimation of two different kinds of model parameters, the matrix and the memory parameters , . For this reason, deriving a concentration inequality becomes particularly challenging. Results for the graphical and thresholding local Whittle estimators require a concentration inequality on the event

| (3.1) |

For this, our theoretical analysis reveals that the memory parameters , , have to be controlled simultaneously, and we propose to derive a concentration inequality on the event (3.1) by incorporating the event , and then use multiple bounds of the probability of the event of interest (3.1) in terms of events which are representable as quadratic forms of i.i.d. sub-Gaussian random vectors. A key tool in our analysis is a uniform concentration inequality introduced by Dicker and Erdogdu (2017). For completeness, we present a slightly modified version of their result in Appendix D.1.

Before we present the main results, we introduce some further notation. We write the population analogue of in (1.6) as

| (3.2) |

and the respective univariate counterpart as . Furthermore, we write

| (3.3) |

We now present the aforementioned inequalities on the probability of the event (3.1), which give insights into what kind of concentration inequalities are required to prove the desired consistency result on . A detailed analysis can be found in the proof of Proposition 3.5 below. For some ,

| (3.4) | |||

| (3.5) |

with

and . The relation (3.4) will follow from Lemma C.6. This way, the problem reduces to finding a uniform concentration inequality on and a concentration inequality on . Instead of considering the maximum, we bound the probability of componentwise for each as

| (3.6) | ||||

with as in (3.22); see Remark 3.4. Furthermore, with and as in Remark 3.4,

| (3.7) |

For the sake of simplicity, in (3.6) and the arguments for (3.6) are not further specified; we refer to the proof of Proposition 3.5 for more details. The inequalities (3.5) and (3.6) reveal that it is enough to prove a uniform concentration inequality for an object of the form

| (3.8) |

with denoting the th elements of

| (3.9) |

where consist of suitable functions of ’s. The set is of the form

| (3.10) |

with

| (3.11) |

The functions are assumed to be differentiable on with bounded derivatives.

From here on, (3.8) can be separated into a probabilistic and a deterministic part as

| (3.12) |

We treat both terms separately. For the first summand, we need a high probability upper bound stated in Lemma B.1. On the other hand, the second term in (3.12) is deterministic and an upper bound is given in Lemma B.2. Lemmas B.1 and B.2 are stated in Appendix B. Both are crucial to infer upper bounds on the probabilities in (3.5) and (3.6). Those results are stated in Propositions 3.1–3.4 below and its proofs can be found in Appendix B.

Technical contributions: The following points highlight our main technical contributions and give some orientation of how the different appendices contribute.

The statement for a probabilistic bound on the first summand of (3.12) is stated in Lemma B.1 in Appendix B. The key tool to handle the first summand of (3.12) is a uniform concentration bound of Dicker and Erdogdu (2017), slightly reformulated to serve better our needs in Appendix D.1. Our arguments above show how the incorporation of the event allows one to get to the setting where that bound could potentially be applicable. Making the bound workable for the probabilities in (3.5) and (3.6) was another major challenge and can be found in Appendix C.1. The difficulties involved allowing for general dependence structure (short- and long-range dependence, and antipersistence) and, more importantly, developing non-asymptotic theory in terms of any dimension and sample size . Though there are certainly many works on local Whittle estimation (and we adapt some of their techniques), non-asymptotic results are not available even for the one-dimensional case . Key to our non-asymptotic developments are bounds of independent interest on various autocovariance matrices under general dependence assumptions in Appendix C.3. Those results are derived by replacing the matrices by integral operators. We believe that those inequalities are crucial in order to derive non-asymptotic theory in any context involving high-dimensional long-range dependence.

3.2 Statements

In this section we formally state our main results. In order to keep the statements as simple as possible, we moved the expressions of some quantities to Appendix A.

We further introduce the following quantity which will allow us to express our bounds in a simplified way and emphasize the necessary distinction between different ranges of the memory parameters as will become clearer in the proofs

| (3.13) |

Proposition 3.1.

Let be a -dimensional, stationary, centered time series with spectral density and suppose Assumptions 1–5 are satisfied. Then, for any with as in Assumption 2, there are positive constants such that for any ,

for

| (3.14) |

where with as in (3.13) and are characterized in Table A.1. A representation of can be found in Table A.2.

The parameter controls the deviation of the estimated memory parameters around , and will be chosen appropriately in Proposition 3.5 below. To ensure that the deviation of around can be controlled, the quantities which characterize in (3.14) have to satisfy and with defined in (A.3) in Appendix A. The quantities in can be expected to satisfy those assumptions since our bounds are sharp enough to get and as . Those asymptotics are crucial in order to achieve consistency which entails a negligible bias. This observation can be made not only for Proposition 3.1 but as well in the similarly structured Propositions 3.2–3.4 below.

Remark 3.1.

Proposition 3.1 and subsequent results provide non-asymptotic bounds when estimating quantities of interest. In the considered setting, is a stationary series with a spectral density and observed for , and of fixed dimension . But note that our non-asymptotic bounds are expressed in terms of and other quantities. When changes, the dependence structure of also changes and our bounds adjust through changing and those other quantities (e.g. in Assumptions 2 and 3). The same with changing . We note that because of the term , in (3.14), the obtained bounds suggest consistent estimation in a typical high-dimensional regime where is much larger than , but is much smaller than (or the power of ). We also note that because of the constants in Proposition 3.1 and similar subsequent results are absolute in the sense that they do not depend on and the underlying stationary series; the dependence on the latter is captured through the other quantities in the bounds.

The following three propositions give upper bounds on the probabilities in (3.6). Those are the probabilities required to control the estimates for the memory parameters .

Proposition 3.2.

In order to ensure meaningful estimation, the quantities which characterize in (3.15) have to satisfy and with defined in (A.3) in Appendix A.

For the following proposition, we use the set in (3.22), which is characterized by some .

Proposition 3.3.

In order to ensure meaningful estimation, the quantities which characterize in (3.16) have to satisfy and with defined in (A.3) in Appendix A.

The next proposition gives a bound on the third probability in (3.6). Recall the definitions of and given in (3.7).

Proposition 3.4.

In order to ensure meaningful estimation, the quantities which characterize in (3.17) have to satisfy , and with defined in (A.3) in Appendix A.

Propositions 3.1–3.4 combined together enable us to obtain a consistency result for (3.1), which is stated in the following proposition. Recall the definition of given in (2.6) and of the function in (3.3).

Proposition 3.5.

In order to ensure meaningful estimation, the term needs to be positive. This is proven in Lemma C.7.

Remark 3.2.

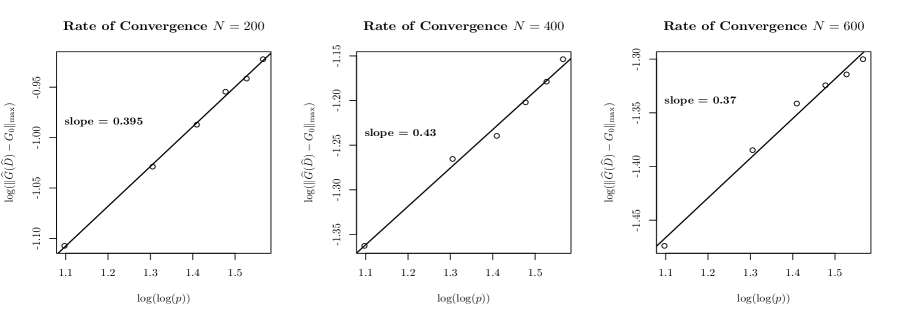

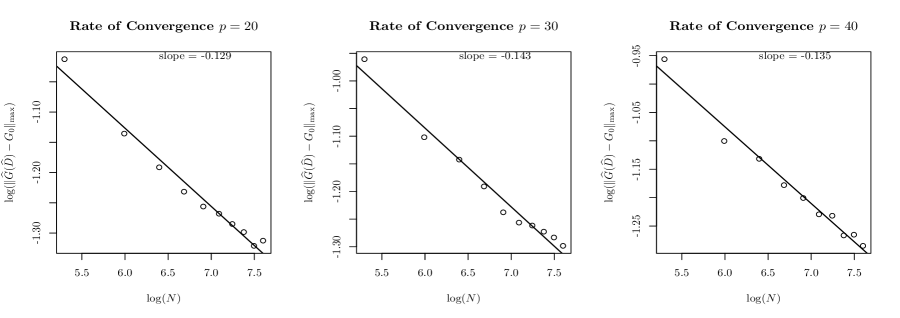

In Corollary A.1, we formally state an analogous result to Proposition 3.5 under the assumption that the underlying process is either short- or long-range dependent. Note that in contrast to Proposition 3.5, Corollary A.1 does not require Assumption 5. In particular, one can infer an asymptotic result without requiring any further assumptions on the relation between and besides for which coincides with Assumption 4 in Robinson (1995b). A numeric illustration of our non-asymptotic results is given in Appendix F.2 in terms of Corollary A.1.

The following propositions give non-asymptotic consistency results for the graphical and thresholding local Whittle estimators, respectively.

Proposition 3.6.

Proposition 3.7.

Propositions 3.6 and 3.7 can be expressed in terms of the quantities in Corollary A.1 when allowing only for long- and short-range dependence. That is, in Propositions 3.6 and 3.7 can be chosen as in Corollary A.1 defined in terms of (A.4).

In contrast to Proposition 3.6, Proposition 3.7 states only a result for the Frobenius norm. A result on the operator norm can be inferred based on the inequality . However, the operator norm provides the same convergence rate as the Frobenius norm. In contrast, for thresholding estimators, the convergence rates differ by one ; see Proposition 3.6. The literature on covariance estimation has addressed this problem by considering alternative estimators. Section 3.3 below presents a modified graphical local Whittle estimator based on estimating the coherence matrix and a constrained -minimization for inverse matrix estimation (CLIME) version.

Remark 3.3.

The probability bounds in Propositions 3.1–3.7 are given in terms of which might suggest consistency only in the limit of , as long as is large enough. Note, however, that may depend on and , and enters in our choices of in (3.14) and , , in (3.15), (3.16) and (3.17). Under suitable assumptions, one can in fact have

in Propositions 3.1–3.4, so that the resulting probability bounds are small even for fixed low-dimensional . In the latter case, even when , these results also provide new non-asymptotic exponential bounds, for example, on the probability of .

Remark 3.4.

The work by Robinson (1995b) concerns consistency results for the univariate local Whittle estimators for and . The consistency of is stated in Theorem 1 in Robinson (1995b). The proof in the asymptotic regime mentions that the function behaves nonuniformly around . For this reason, one has to consider the cases and to separate the set as with

| (3.22) |

| (3.23) |

where . As displayed in (3.22), separating is only necessary if . The case includes since . Note that coincides with the prior knowledge that the observed time series is not long-range dependent. The sets and are used to determine the range of admissible estimates for an individual component series . Then, and depend on instead of . Throughout the paper we do not reflect the dependence on in the notation of and .

3.3 Alternative estimators for precision matrix

We study here a modified graphical local Whittle estimator based on estimating the coherence matrix and a CLIME version; see Sections 3.3.1 and 3.3.2. The section and in particular the corresponding proofs in Appendix B also emphasize the value of our Proposition 3.5 since it can be used to infer consistency results even for modified versions of penalized local Whittle estimators.

3.3.1 Modified graphical local Whittle

As known for covariance matrices, the rate of convergence can be improved for the operator norm by considering the correlation matrix instead; see Rothman et al. (2008) and Shu and Nan (2019) for temporally correlated data. Analogously, we can consider the coherence matrix. Let , where and is the true coherence matrix. Then, the precision matrix satisfies and therefore . We write and for their sample counterparts, and indicate their dependence on the matrix . The matrix can then be estimated as

| (3.24) |

where is estimated univariately by (2.1) and

| (3.25) |

Then, we can define a modified coherence-based graphical local Whittle estimator

| (3.26) |

where . The following statement gives a non-asymptotic consistency result on the spectral norm.

Proposition 3.8.

In contrast to Proposition 3.7, Proposition 3.8 provides a convergence rate for the spectral norm which shows that the modified graphical local Whittle estimator (3.26) can achieve the same convergence rate as the thresholding local Whittle estimator.

A handy result to prove Proposition 3.8 and of independent interest is the following lemma which gives a consistency result for the coherence matrix estimator in (3.24).

Lemma 3.1.

Note that we assume such that only to achieve a simplified representation of the result. In general, it is possible to state the result for any fixed .

3.3.2 CLIME estimation

CLIME estimation for i.i.d. samples was introduced in Cai et al. (2011) and further studied in Shu and Nan (2019) allowing for temporal correlation. We adopt their approach to the spectral domain and set to be the solution of the minimization problem

where is a tuning parameter. Then, the CLIME estimator is defined as

| (3.27) |

We impose the sparsity assumption (2.9) on .

3.4 Graphical model selection consistency

We give here results on consistent recovery of the sparsity pattern and sign consistency for our estimators. For the long-run variance matrix estimation, we focus on the thresholding local Whittle estimator. For the precision matrix, we consider a thresholded CLIME estimator and conclude with a discussion on consistent graph recovery for other estimators. The proofs of the statements in this section can be found in Appendix B.

The following proposition gives a non-asymptotic result for consistent graph recovery of the thresholding local Whittle. Rothman et al. (2009) consider covariance matrix estimation for i.i.d. -dimensional random vectors in a high-dimensional regime. In particular, their Theorem 2 states that the thresholding operator consistently recovers the sparsity pattern. The proof of Theorem 2 in Rothman et al. (2009) is generic and proves, combined with our Proposition 3.5, consistent recovery of the sign and sparsity pattern.

Proposition 3.10.

Let be a -dimensional, stationary, centered time series with spectral density and suppose Assumptions 1–5 are satisfied. Then, there are positive constants , such that choosing a threshold as in (3.19) yields, for any ,

| (3.28) |

If we additionally assume that all non-zero elements of satisfy , where is of the same order as , we have

| (3.29) |

The CLIME estimator in (3.27) can be modified to recover the support of the precision matrix. More precisely, we conduct an additional thresholding step by applying (2.2) to in (3.27). This procedure follows Section 4 in Cai et al. (2011) who considered inverse covariance estimation for i.i.d. data. Subsequently, Shu and Nan (2019) used a thresholded CLIME for inverse covariance estimation under temporal dependence; see Theorem 5 in Shu and Nan (2019) for their result on consistent sparsity and sign recovery. Following their arguments, we can state the following proposition.

Proposition 3.11.

Let be a -dimensional, stationary, centered time series with spectral density and suppose Assumptions 1–5 are satisfied. Then, there are positive constants , such that choosing a penalty parameter as in (3.19) yields, for any ,

| (3.30) |

If we additionally assume that all non-zero elements of satisfy , where is of the same order as , we have

| (3.31) |

For the graphical local Whittle estimation, consistent recovery of the sparsity pattern is not expected. This is discussed in Zou (2006) for the classical LASSO in a regression context. There have been several approaches to modify the classical LASSO to achieve consistent graph recovery. For instance the consideration of an adaptive version (Zou, 2006) and a thresholded LASSO (Zhou, 2010; Ravikumar et al., 2011; Wang and Allen, 2021).

An adaptive version is based on a weighted penalty, where the weights are data driven using a preliminary estimator. Though our results are expected to be helpful to prove consistency for an adaptive version, a detailed investigation goes beyond the scope of this work. A related discussion on the difficulties of proving consistent recovery of the sparsity pattern with help of an extended Bayesian information criterion can be found in Remark 4.1.

A thresholding graphical local Whittle estimator is expected to consistently recover the sparsity pattern. It is similar in flavor to the thresholded CLIME and a consistency result can be inferred with help of Proposition 3.5.

3.5 Comparison to existing results

In this section, we compare our results to related work. Existing results are either for short-range dependent time series or, if they allow for stronger temporal and spatial dependence, the dependence measure is characterized by an unknown and unestimated quantity. In particular, results for data with stronger dependence structure have only been derived in the time domain.

Sun et al. (2018): We recover recently proven results on spectral density estimation at frequency zero for short-range dependent time series. Sun et al. (2018) supposed that and could prove results in a regime. We get the same result by setting in (3.19). Strictly speaking, we do not allow for since in Table A.2 involves . However, a look into the proof of Proposition 3.1 reveals that for , one can bound the respective term by instead. We refrained from incorporating the case explicitly for simplicity. We note also that our result includes an additional . However, this is an artifact of using a slightly simplified notation to make reading easier. More precisely, to prove Proposition 3.5, we apply a uniform concentration inequality in Lemma B.1 which involves the supremum of a partial derivative; see (B.2). The supremum is taken over a closed set. In particular, the set is not empty. For this reason, even when the set contains only one point as in the short-range dependent case (), the derivative is included in the respective bounds. The logarithm appears because of the derivative in our uniform concentration inequality. This can be easily avoided by considering the supremum over a half-open interval. However, it would require careful distinction through all our proofs between whether the set is empty or not. In order to avoid over complicated notation, we refrained from incorporating this case.

Shu and Nan (2019): This related work focusses on the estimation of the covariance matrix and its inverse, with the results in the time domain. However, Shu and Nan (2019) also allow for long-range dependence. They assume that the correlation with in the component series satisfies

| (3.32) |

For the individual time series can thus be long-range dependent in the sense that the correlation sequences are not absolutely summable. To make a fair comparison, we will assume a known memory parameters and, for simplicity, further ignore the bounds on the deterministic part and only consider the case when the time series is short- or long-range dependent. Then, based on Proposition 3.1 for and , our convergence rate simply reduces to

| (3.33) |

with as in (3.13) and

In Shu and Nan (2019), the result analogous to our Proposition 3.1 is Lemma A.2., (i) with rates given in Remark 2. Based on Remark 2 in Shu and Nan (2019), the quantity analogous to in (3.33) is given by

| (3.34) |

Since the results are in the time domain, the convergence rates are in terms of the sample size rather than the number of frequencies used in estimation as in our results and Sun et al. (2018). See also Remark C.1, for a discussion on why our bounds include . Otherwise, our bounds coincide with those in Shu and Nan (2019) for . In contrast to our statements, the results in Shu and Nan (2019) are not non-asymptotic. Furthermore, they do not estimate .

4 The choice of the shrinkage parameters and algorithms

Both thresholding (2.2) and graphical local Whittle estimation (2.3) depend respectively on the threshold and penalization parameter . In this section, we discuss how to select . This choice plays a critical role in finite sample performance. We propose to use cross-validation for the thresholding parameter and an extended Bayesian information criterion (eBIC) for graphical local Whittle estimation.

4.1 Thresholding local Whittle estimation

Cross-validation is generally suggested to select the penalization parameter for thresholding covariance matrix estimation; see Bickel and Levina (2008b). Sun et al. (2018) modified it to sampling over Fourier frequencies in order to account for temporal dependence in spectral density matrix estimation. Similarly, we propose to select the optimal thresholding parameter by cross-validating over the periodogram (1.4). More precisely, we split the sequence of the periodogram evaluated at different frequencies into two groups. Then, we apply the thresholding estimator of the long-run variance matrix (2.2) to the first group. The long-run variance matrix estimator from the latter group is used as a reference. The optimal thresholding parameter is selected by minimizing the average Frobenius norm (squared) between the thresholding estimators and the reference estimators of the long-run variance matrix. The detailed procedure can be found in Algorithm 1. As in Sun et al. (2018), this procedure remains to be justified in theory even for short-range dependent series.

4.2 Graphical local Whittle estimation

For the penalization parameter in graphical local Whittle estimation, we suggest to use an extended Bayesian information criterion (eBIC). Tuning parameter selection for penalized likelihood estimation by an eBIC has been studied by multiple authors allowing the dimension to grow with the sample size. The eBIC was proposed by Foygel and Drton (2010) for Gaussian graphical models and further used in Foygel and Drton (2011) for model selection in sparse generalized linear models. Later, Gao et al. (2012) proved that using the eBIC to select the tuning parameter in penalized likelihood estimation with the so-called SCAD penalty (Fan and Li (2001)) can lead to consistent graphical model selection. See also Chen and Chen (2012). To be more specific, we use the following criterion

| (4.1) |

where is the set of all estimated by (2.3) over a range of and denotes the norm counting the number of non-zero elements in . Furthermore, the criterion is indexed by a parameter ; see Foygel and Drton (2010) and Chen and Chen (2008) for the Bayesian interpretation of . Then, gives us a data-driven estimate of and the associated penalty .

In order to determine over a range of and the set , we consider an algorithm to compute the graphical local Whittle estimator for a given penalty parameter . This algorithm is a natural extension of graphical LASSO algorithms for real symmetric covariance matrices to complex-valued Hermitian matrices. The generalization to complex-valued Hermitian matrices is necessary since the true precision matrix is possibly complex-valued. We propose a complex-valued alternating linearization method (ALM) which is a variation of alternating direction method of multipliers (ADMM) proposed in Scheinberg et al. (2010). Our limited simulation study shows that the proposed method converges faster than the naïve ADMM algorithm. We also note that the complex-valued ADMM for SRD series was considered by Jung et al. (2015).

The ALM (Algorithm 2) solves the problem

subject to being positive definite. It invokes the ADMM algorithm to find sparse positive definite estimates of by introducing augmented Lagrangian. It furthermore carefully selects augmented Lagrangian penalty parameter so that the positive definiteness is achieved throughout the iterations. For the initial estimator in lower dimensions, we take . The shrinkage operator in Step 4 of Algorithm 2 is defined as for a matrix and some . Step 5 of Algorithm 2 requires to update . It is reduced by a constant factor on every iteration till a lower bound is achieved by following the idea of Scheinberg et al. (2010). That is, set as to reduce by a constant factor on every iteration. In this paper, we choose , , and . Finally, we terminate the ALM algorithm following the stopping rules in (20) in Scheinberg et al. (2010) except that the first condition is replaced by stopping after 1000 iterations.

We conclude with a discussion on the criterion (4.1).

Remark 4.1.

The criterion (4.1) is adapted from Foygel and Drton (2010). The log-likelihood function in equation (2) in Foygel and Drton (2010) which gives an estimate for the inverse covariance matrix of a Gaussian model is replaced by the negative log-likelihood function in (1.3) in terms of the matrix . The criterion seems to perform well in our simulation study. However, from a theoretical perspective, a consistency result can only be established when the penalization term in (4.1) is chosen in dependence of the rate of convergence of the th component of around the true . In their theoretical results, Foygel and Drton (2010) considered independent and identically distributed Gaussian random vectors. In this case, the penalization depends on the convergence rate of the deviation of the sample covariance matrix around the true covariance matrix, that is . Foygel and Drton (2010) proved that the eBIC selects the correct model consistently in a high-dimensional regime ; see Theorem 5 in Foygel and Drton (2010). To establish an analogous consistency result in our setting, we suggest to replace the penalization in the eBIC objective function by in (3.19), since gives the convergence rate of the maximum norm of around the true . The detailed proof of such a consistency result goes beyond the scope of this work and, from a practical perspective, the usage of (4.1) seems to be more natural, since including in the penalization would involve a number of unknown parameters.

5 Simulation study

In this section, we examine the proposed methods through simulations. Our two-stage approach first estimates the memory parameters and non-sparse long-run variance matrix based on the local Whittle estimator (1.6). Then, we apply either thresholding or graphical local Whittle estimation to get sparse estimators. Several tuning parameters need to be selected for our methods. We comment first on the number of frequencies used in local Whittle estimation. Details about the selection of tuning parameters for sparse estimation are provided in the subsequent sections.

The selection of the number of frequencies is important in practice and should be balanced: be small enough to capture long-range dependence and large enough to get reliable estimates. In univariate local Whittle estimation, asymptotic theory suggests ; see Robinson (1995b). There are several papers studying data dependent bandwidth. In this regard, the most influential paper is Henry (2001). Henry (2001) suggests a bandwidth minimizing the mean squared error of the univariate local Whittle estimator. A visual approach to ensure the balance between capturing long-range dependence and getting reliable estimates is proposed in Baek et al. (2020). Baek et al. (2020) used the so-called local Whittle plots which present estimates of the memory parameters as function of the tuning parameter supplemented with confidence intervals.

In our simulation study we base our choice on the asymptotic theory in Robinson (1995b) suggesting , where is the largest integer less than or equal to .

5.1 Thresholding local Whittle estimation

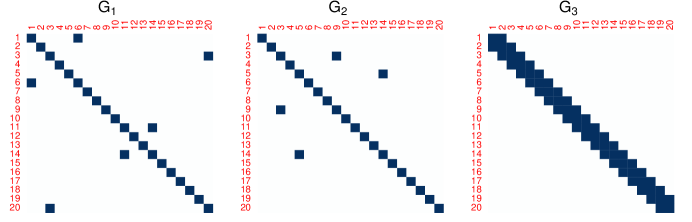

We consider the following three data generating processes (DGPs) to evaluate the finite sample performance of the thresholding local Whittle method. The one-sided and two-sided VARFIMA(0, , 0) (Vector Autoregressive Fractionally Integrated Moving Average) models are used to generate multivariate long-range dependent time series. See Kechagias and Pipiras (2015a); Kechagias and Pipiras (2015b) for definitions of these models. We consider dimensions with sample sizes . Long-range dependent parameters are selected at random from .1 to .45, if not specified otherwise. We use the notation to denote the th entry of . To be more precise, the DGP’s are given as follows:

-

-

(thDGP1)

One-sided VARFIMA() with , where the diagonal entries of are .159 except , , , and , , and .

-

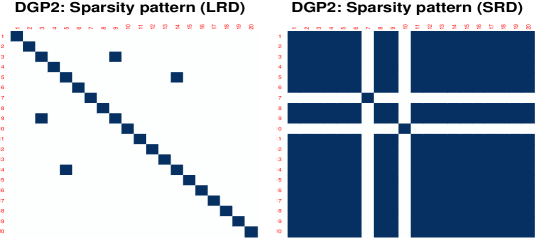

(thDGP2)

Two-sided VARFIMA() with , where the diagonal entries of are 1 and , .

-

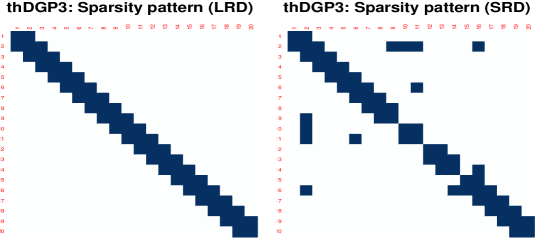

(thDGP3)

Two-sided VARFIMA() with banded matrix given by , where the diagonal entries of are 1 and , .

-

(thDGP1)

For the reader’s convenience, the sparsity patterns imposed on , are depicted in Figure 1.

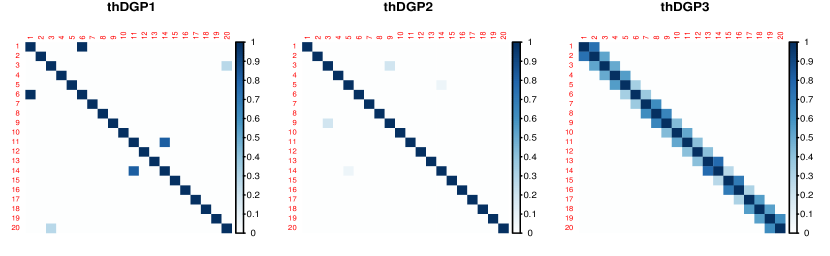

The thresholding parameter is selected based on cross-validation introduced in Section 4.1. We set to be the smallest and the largest value of in (1.6). We evaluated the performance of the thresholding local Whittle estimator using the mean squared error of the parameters , total number of misspecified coefficients , the Frobenius norm and the spectral norm . The performance measures are calculated based on 1000 iterations.

Figure 2 shows the proportion of times each component is estimated to be non-zero using our thresholding local Whittle approach with and . The estimation is close to the true sparsity pattern though some locations are more difficult to be estimated correctly. For example, in thDGP1, is detected as non-zero less frequently, but this is natural since is smaller than the other coefficients. However, such misspecification vanishes as sample size increases. Table F.3 in Appendix F shows the performance measures calculated for . It can be observed that all performance measures are decreasing as the sample size increases.

5.2 Graphical local Whittle estimation

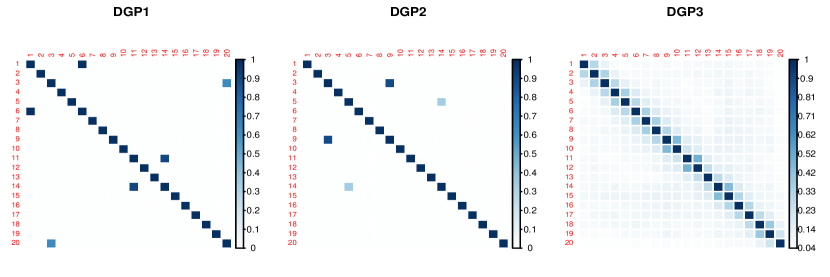

We consider the following three DGPs to see the performance of the graphical local Whittle estimation. We introduce the matrices , , to define the sparsity pattern of . The notation , , denotes the th entry of .

-

-

(DGP1)

One-sided VARFIMA() with , where , , and .

-

(DGP2)

Two-sided VARFIMA() with , where the diagonal entries of are 1 and , .

-

(DGP3)

Two-sided VARFIMA() with banded matrix given by , where the diagonal entries of are 1 and , .

-

(DGP1)

The penalty parameter is chosen by the eBIC in (4.1) with . Also, the ALM algorithm requires the Lagrangian penalty parameter, which as noted above is set to decrease by on every th iteration with but it is taken no smaller than . The same performance measures are used as those for thresholding local Whittle estimation in Section 5.1, but the inverse of long-run variance is used instead of .

Figure 3 shows the proportions of estimated non-zero coefficients in , , when the dimension is and the sample size is . Note that the sparsity patterns of , , are the same as in Figure 1. It can be observed that the graphical local Whittle estimator recovers the sparsity pattern of the underlying model. For example, the non-zero coefficient is found to be non-zero about 90% of times by our proposed method. More detailed performance measures can be found in Table F.4. Table F.4 suggests that for all considered models our performance measures tend to improve as the sample size increases for fixed dimension. The other way around, for fixed sample size , the performance measures are getting worse as the dimension increases. We can conclude that the graphical local Whittle estimator correctly identifies zero coefficients and yields estimates close to the true values as the sample size increases.

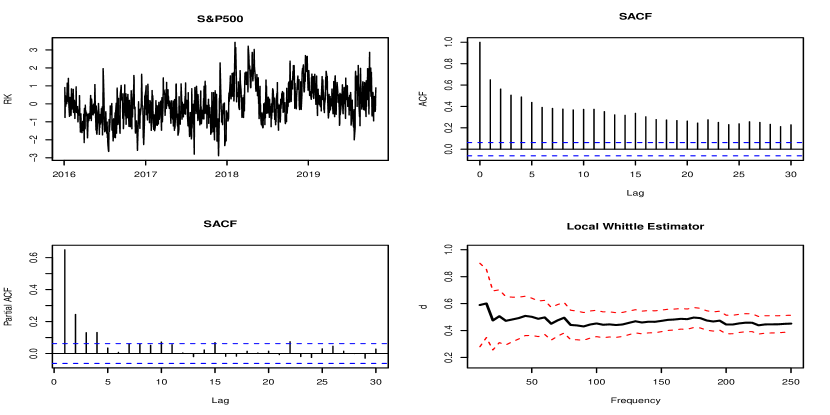

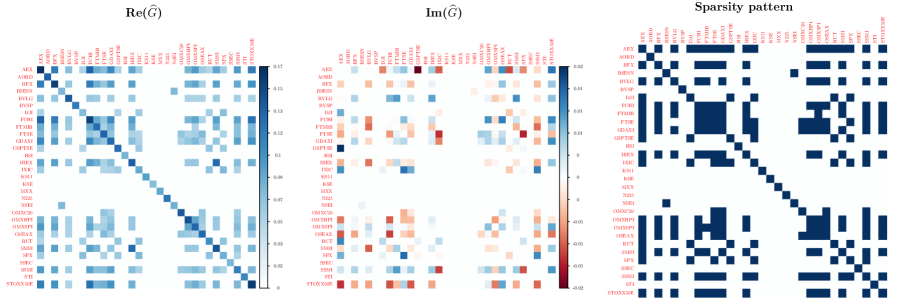

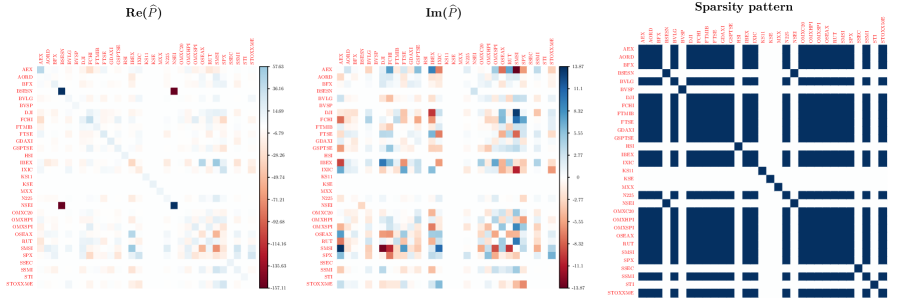

6 Real data application

In this section, we apply our proposed methods to 31 realized volatilities obtained by aggregating the 5-min within-day returns taken from the Oxford Man Institute of Quantitative Finance (http://www.oxford-man.ox.ac.uk). We adjusted the different opening days over the stock markets by applying linear interpolation and log-transforming the data. Furthermore, we removed the possible mean changes in the data by following the proposed procedure in Baek and Pipiras (2014). We also studentized each series to have zero-mean and unit variance in order to focus on volatility linkage. The total number of observations is 1001 dating from Jan 4, 2016 to Oct 31, 2019. The 31 global stock indices are AEX index (AEX), All Ordinaries (AORD), Bell 20 index (BFX), S&P BSE Sensex (BSESN), PSI All Shares Gross Return Index (BVLG), BVSP BOVESPA Index (BVSP), Dow Jones Industrial Average (DJI), CAC 40 (FCHI), FTSE MIB (FTMIB), FTSE 100 (FTSE), DAX (GDAXI), S&P/TSX Composite index (GSPTSE), HANG SENG Index (HSI), IBEX 35 Index (IBEX), Nasdaq 100 (IXIC), Korea Composite Stock Price Index (KS11), Karachi SE 100 Index (KSE), IPC Mexico (MXX), Nikkei 225 (N225), NIFTY 50 (NSEI), OMX Copenhagen 20 Index (OMXC20), OMX Helsinki All Share Index (OMXHPI), OMX Stockholm All Share Index (OMXSPI), Oslo Exchange All-share Index (OSEAX), Russel 2000 (RUT), Madrid General Index (SMSI), S&P 500 Index (SPX), Shanghai Composite Index (SSEC), Swiss Stock Market Index (SSMI), Straits Times Index (STI), EURO STOXX 50 (STOXX50E).

Figure 4 shows some exploratory plots for S&P 500 such as time plot (top left), sample autocorrelation plot (top right), sample partial autocorrelation plot (bottom left) and long-range dependent parameter estimates over the number of frequencies used (bottom right). It shows typical features of long-range dependent time series: non-cyclical trends, slow decay of autocorrelations and memory parameters close to .5. This suggests that multivariate long-range dependence modeling is meaningful and we applied our methods to estimate long-run variance and precision matrices.

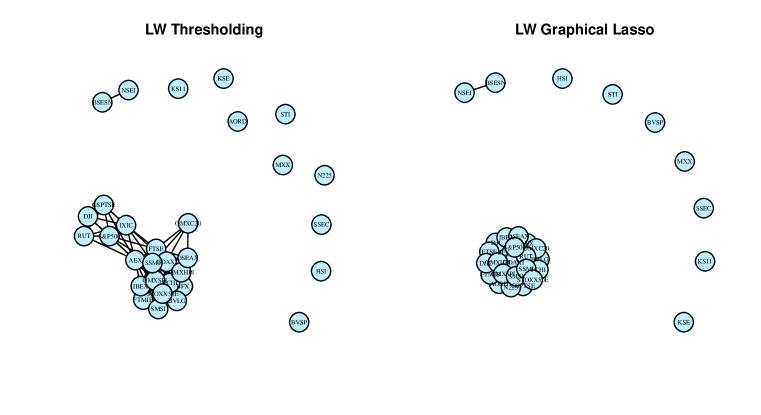

Sparse long-run variance matrix estimation by thresholding is presented in Figure 5. The left panel shows the real parts of and the imaginary parts can be found in the middle panel. The right panel presents the sparsity pattern, that is, the locations of the non-zero coefficients are colored dark blue. Figure 6 follows the same structure as Figure 5 but shows the estimated sparse precision matrix using graphical local Whittle estimation. The penalty parameter is selected by using eBIC in (4.1) with . BSESN and NSEI, both Indian market indices, showed the largest real coefficients in absolute term.

Observe that the thresholding method gives sparser estimation. We also observe the clustering of stock market indices for both long-run variance and precision matrices. It is seen more clearly from a network representation of linkages as in Figure 7. More interestingly, both methods give similar clusterings. The isolated nodes based on correspond to India (BSESN/NSEI), China (SSEC), South Korea (KS11), Hong Kong (HSI), Singapore (STI), Mexico (MXX), Portugal (BSVP), Pakistan (KSE). The sparse long-run variance using thresholding adds Japan (N225) and Australia (AORL). That is, it seems that our empirical analysis tells that stock market indices can be roughly divided into the US-European market and somewhat independent markets from the rest of the world including Asia, India, Australia and Mexico in late 2010s. The thresholding method seems to further distinguish US and European markets. In fact, all US stock indices showed larger values of memory parameter estimates by having more than .4 which is not the case for European market indices. It is particularly interesting to see the grouping of multinational realized volatilities according to regional or spatial dependence.

Finally, we note but do not include the results here, that the analysis of the data assuming short-range dependence led to highly non-sparse patterns for the considered connectivity matrices. These findings were consistent with the scenario where we simulated data from LRD models as in Section 5 but worked as if they were SRD.

7 Conclusions

In this work, we derived consistency results for the long-run variance and precision matrices in a non-asymptotic regime allowing the underlying time series to admit a general dependence structure including long-range dependence. The results are derived under mild assumptions on the underlying time series which is allowed to be either Gaussian or have a linear representation. The shrinkage techniques are thresholding and graphical local Whittle estimation. Our non-asymptotic results can be used to infer consistency in a high-dimensional regime where the number of component series can be large compared to the sample size.

The key technical contribution is the incorporation of the memory parameter matrix which carries information about the dependence structure of the underlying time series. Our results allow estimating those memory parameters simultaneously while estimating the long-run variance and the precision matrices sparsely.

We see the proposed proof techniques as a basis to study other questions concerning high-dimensional long-range dependence. Possible future directions include the use of other shrinkage methods, for example, adaptive penalizations; sparse estimation of fractionally (co)integrated vector autoregressive (VAR) models and sparse estimation of linear regression with long-range dependent errors.

Appendix A Quantities in main results and special cases

In this section we provide the expressions for several quantities appearing in Propositions 3.1–3.4. In addition, we will discuss the case when the underlying time series admits only short- or long-range dependence.

Recall that the non-asymptotic bounds in Propositions 3.1–3.4 are all of the form

| (A.1) |

Here, ’s arise in bounds on the probabilistic parts and ’s on deterministic parts. The sequences can be found in Propositions 3.1–3.4. The quantities and are respectively given in Tables A.1 and A.2 for Propositions 3.1–3.4.

Recall that determine the interval of admissible estimates of the memory parameters and the quantity is defined in (3.13). We further introduce a few quantities which will allow us to express our bounds in a simplified way and emphasize the necessary distinction between different ranges of the memory parameters as will become clearer in the proofs. Let

| (A.2) |

where the subscripts and allude to the dependence on and , respectively.

For the bounds on the deterministic parts we will use

| (A.3) |

and . Recall further that appears in Assumption 2.

As a corollary of Proposition 3.5, we give the result where the underlying process is known to admit only short- or long-range dependence, that is, the true memory parameters satisfy .

Corollary A.1.

The corollary is a simple consequence of setting in Proposition 3.5.

Appendix B Proofs of the main results

In this section we will give bounds on the probabilistic and deterministic terms in (3.12), stated respectively in Lemmas B.1 and B.2. Lemma B.1 focusses on results under the assumption that the underlying process is Gaussian. Its analogue for linear processes can be found in Appendix E. Up to a constant the bounds are the same as for the Gaussian case. For this reason all proceeding results remain true. Note that Lemma B.2 only relies on assumptions on the spectral density and remains valid as well.

The following Lemma B.1 gives multiple upper bounds on the probabilistic term in (3.12). Those different bounds are used later depending on whether the true parameters and are positive or negative. Recall in particular the notation below (3.9) and in (3.10)–(3.11). Let

| (B.1) | ||||

with

| (B.2) | ||||

and

Note that is different from only for . This notation though will allow writing our arguments in a more unified way.

Lemma B.1.

Let be a -dimensional stationary, centered, Gaussian time series with spectral density as in (1.1). Then, there are positive constants such that

| (B.3) |

for , where

| (B.4) |

with if and is given in (3.10). The constant bounds the sub-Gaussian norm of a standard normal random variable as in (D.1) and is defined in (3.13).

Proof.

To prove the desired concentration inequality, we first introduce some general notation. For a fixed frequency, the periodogram in (1.4) can be written as

| (B.5) |

with and

| (B.6) | ||||

see equation (A.6) in Sun et al. (2018). The event of interest can be separated into real and imaginary parts as

| (B.7) | ||||

Note that the imaginary part of the diagonal elements is zero, that is, . We consider the diagonal elements first and then distinguish the real and imaginary parts in (B.7) for the off-diagonal elements .

Diagonal elements: To rewrite the real-valued diagonal elements as a quadratic form, we define the matrix

| (B.8) |

and the matrix-valued function

| (B.9) |

Then, in view of (B.5), (B.8), (B.9) and since , can be written as

| (B.10) | ||||

with , where is Gaussian with and . In (B.11) below, we apply Theorem D.1 with and to obtain

| (B.11) | |||

| (B.12) |

for with and and

| (B.13) | ||||

where . Though , we bound them differently in (B.12). Furthermore,

| (B.14) |

with and as in (B.1). We get (B.12) by bounding the quantities in (B.13). Note that

| (B.15) | ||||

| (B.16) | ||||

| (B.17) |

where we used the submultiplicativity of the spectral norm, Lemma D.1 and the fact that for a matrix for the first inequalities in (B.15)–(B.17), respectively. The last inequalities in (B.15) and (B.16) for the spectral and Frobenius norms of follow by Lemmas C.12 and C.13. Furthermore, we used the fact that the spectral norm of can be calculated as

see Lemma C.4 in Sun et al. (2018).

Real part (off-diagonal): The real part of the off-diagonal elements can be written in terms of (B.5) as

| (B.18) |

As in (B.10), we will write (B.18) as a quadratic form but now using , where is a Gaussian vector with and

| (B.19) |

For this, define the matrix

with as in (B.8). Furthermore, define the matrix with as in (B.9) and

| (B.20) |

Write

with

In order to apply Theorem D.1, we further write

| (B.21) |

Note that the matrix can be rewritten as

| (B.22) |

for with

| (B.23) | ||||

The matrices in (B.22) are defined by replacing ’s in (B.23) by . These matrices are to normalize in (B.22).

We continue to bound (B.21) by applying Theorem D.1. In order to verify the applicability of Theorem D.1, note that the matrix in (B.22) is not diagonal but can be represented as a unitary transformation of a diagonal matrix

| (B.24) | ||||

For this reason, Theorem D.1 remains applicable due to Remark D.1. In (B.25) below, we apply Theorem D.1 with and to obtain

| (B.25) | |||

| (B.26) |

for and with

| (B.27) |

for , where the ’s are given in (B.1) and

| (B.28) |

for . The ’s in (B.27) can indeed be represented as in (B.1) due to (B.24) and Remark D.1, and since and and similarly with , where is in (B.2). We will now discuss bounds on the Frobenius and spectral norms of to get (B.26).

The relation (B.26) is a consequence of bounding the quantities in (B.27) as follows. Let denote a generic constant which might differ from line to line. Then, with the explanations given below,

| (B.29) | ||||

| (B.30) | ||||

| (B.31) | ||||

| (B.32) | ||||

The first bounds in (B.29) and (B.30) follow from the submultiplicativity of the spectral norm and Lemma D.1, respectively. Then, we use Lemma D.2 to eliminate the off-diagonal matrix blocks, and Lemmas C.12 and C.13 are used to bound the spectral and Frobenius norms of . In (B.31), we first apply Lemma D.2 and then the fact that for a matrix . Note also that for two matrices . Similarly, we applied in (B.32) to use (B.29). Note also that , where the first equality is due to the block diagonal structure of and the second equality follows by Lemma C.4 in Sun et al. (2018).

Imaginary part (off-diagonal): The imaginary part of the off-diagonal elements can be written in terms of (B.5) as

Then,

| (B.33) | ||||

We focus on the first probability term in the bound, since the second can be dealt with analogously. Define the matrix

with

Furthermore, define the matrix in terms of the function and recall in (E.6) to write

with

and characterized as in (B.19). In order to apply Theorem D.1, we further write

| (B.34) |

Note that the matrix can be rewritten as

for with and , defined as in (B.23). We continue to bound (B.34). As for the real parts of the off-diagonal elements, note that is not a diagonal matrix. However, it can be rewritten as a unitary transformation of a diagonal matrix

| (B.35) | ||||

where we used the same calculations as in (B.24). Following Remark D.1, Theorem D.1 is applicable. In (B.36) below, we apply Theorem D.1 with and to obtain

| (B.36) | |||

| (B.37) |

for and with

| (B.38) |

for , where the ’s are given in (B.1) and

| (B.39) |

for . Given (B.35), the ’s in (B.38) can indeed be represented as in (B.1).

Since the quantities (B.39) are equal to those in (B.28) by replacing with , the norms and can be bounded as the norms of , , in (B.29)–(B.32). In order to deal with , note that , where the equality is due to the block diagonal structure of and the inequality follows by Lemma C.4 in Sun et al. (2018).

In order to get the statements (E.1)–(E.2) of the lemma, we shall get an upper bound on the probability in (B.7). For the diagonal terms (), the imaginary part is zero. As proved in (B.12), for , (B.7) can be bounded by for ; see (B.14). For the off-diagonal elements, one needs to get a bound on the two probabilities in (B.7). For the real part of the off-diagonal elements, (B.26) gives the upper bound , for . For the imaginary parts of the off-diagonal elements, which was further bounded in (B.33), (B.37) provides the upper bound , for . Combining the different bounds leads to the desired result. ∎

The next lemma gives a bound on the deterministic term in (3.12).

Lemma B.2.

Proof.

We next prove Propositions 3.1–3.4. The proofs are all consequences of Lemmas B.1 and B.2, and structured in the same way. We first choose a function in (3.8)–(3.9) and then apply Lemma B.1 to the respective probabilistic part and Lemma B.2 to the respective deterministic part in the bound (3.12).

For the probabilistic parts in the proofs of Propositions 3.1–3.4, we note that Lemma B.1 requires , with as in (B.1). We do not verify this condition in the proofs since it is automatically satisfied by the bounds we get on the ’s and under the assumptions in Propositions 3.1–3.4. This is due to our choices of , , and in (3.14), (3.15), (3.16) and (3.17), which are always of the form , where accounts for the respective bias terms and is always chosen as .

Proof of Proposition 3.1.

To apply Lemmas B.1 and B.2, we take

| (B.45) |

in (3.8)–(3.9). We consider the probabilistic and deterministic parts separately as in (3.12).

Probabilistic part: We distinguish three cases depending on whether the true memory parameters are positive or negative. Therefore, we write

| (B.46) |

where

and

For each case, we apply Lemma B.1 and bound the respective quantities , in (B.1) that then yield the desired result. We will show that, for ,

| (B.47) |

Case : We get

| (B.48) | ||||

| (B.49) |

Since and do not depend on , applying Lemma B.1 with in (E.2) gives (B.47) with .

Case : We get

| (B.50) | ||||

| (B.51) |

We pause here to draw the attention to inequality (B.50), since the argument will be used not only here but also in the proofs of Proposition 3.2–3.4. It can be assumed that the frequencies satisfy . Then, the function is monotonically decreasing in for all . For a non-negative exponent , reaches its maximum for , for a negative exponent , for . Due to the monotonicity of , the function reaches its supremum for the smallest possible values can take.

We proceed with the case ,

| (B.52) |

with as in (A.2). Since and do not depend on , applying Lemma B.1 with , gives (B.47) with .

Deterministic part: Using Lemma B.2 with (B.45), we get

| (B.55) |

where is in Table A.2 and the inequality can be obtained by bounding the two terms in (B.40) given (B.45) as follows. The first summand in (B.40) can be bounded as

for , and the second summand as

Finally, we combine our results on the probabilistic and deterministic terms to obtain the statement of the proposition. With our choice of in (3.14) and for any , observe that, with explanations given below,

| (B.56) | |||

| (B.57) | |||

| (B.58) | |||

| (B.59) | |||

| (B.60) |

with , defined in (B.48), (B.49), (B.51), (B.52) and (B.53), (B.54). The constants are generic and might differ from line to line. Indeed, the inequality (B.56) is due to (B.55) with as in Table A.2. In (B.57), the probabilistic part is bounded as in (B.46). Applying (B.47) yields (B.58). For the inequality (B.59), note that and are chosen in Table A.1 such that

The inequality (B.60) follows since we work under the assumption ; see the discussion following Proposition 3.1. ∎

Proof of Proposition 3.2.

To apply Lemmas B.1 and B.2, we choose

| (B.61) |

in (3.8)–(3.9). Here, we do not need a uniform bound. For this reason, it is not necessary to take the supremum over all admissible estimates of in Lemmas B.1 and B.2. In particular, Lemma B.1 simplifies, since the derivatives in the respective bounds in (B.1) become zero with the choice (B.61).

Probabilistic part: It is enough to distinguish two cases

| (B.62) |

with and . For both cases, we apply Lemma B.1 and bound the respective quantities , in (B.1) that then yield the desired result. We will show that, for ,

| (B.63) |

Deterministic part: Using Lemma B.2 with (B.61), we get

| (B.67) |

where is in Table A.2 and the inequality can be obtained by bounding the two terms in (B.40) given (B.61) as follows. The first summand in (B.40) can be bounded as

the second summand as

Finally, we combine our results on the probabilistic and deterministic terms. With our choice of in (3.15) and for any , observe that, with explanations given below,

| (B.68) | |||

| (B.69) | |||

| (B.70) | |||

| (B.71) | |||

| (B.72) |

with , defined in (B.64), (B.65) and (B.66). The constants are generic and might differ from line to line. Indeed, the inequality (B.68) is due to (B.67). In (B.69), the probabilistic part is bounded as in (B.62). Applying (B.63) yields (B.70). For the inequality (B.71), note that and are chosen in Table A.1 such that

The inequality (B.72) follows since we work under the assumption ; see the discussion following Proposition 3.2. ∎

Proof of Proposition 3.3.

Probabilistic part: It is enough to distinguish three cases

| (B.74) | ||||

with

For each case, we apply Lemma B.1 and bound the respective quantities , in (B.1) that then yield the desired result. We will show that, for ,

| (B.75) | ||||

Case : In this case, .Then,

| (B.80) |

with as in (A.2) and we distinguish further two cases: for ,

| (B.81) |

with as in (A.2) and for ,

| (B.82) |

Finally, given (B.81) and (B.82), we define

| (B.83) |

Deterministic part: Using Lemma B.2 with (B.73), we get

| (B.84) | ||||

with and is in Table A.2. The inequality can be obtained by bounding the two terms in (B.40) given (B.73) as follows. The first summand in (B.40) can be bounded as

and the second as

Finally, we combine our results on the probabilistic and deterministic terms to obtain the statement of the proposition. With our choice of in (3.16), observe that, with explanations given below,

| (B.85) | |||

| (B.86) | |||

| (B.87) | |||

| (B.88) | |||

| (B.89) |

with , defined in (B.76), (B.77), (B.78), (B.79) and (B.80), (B.83). The constants are generic and might differ from line to line. The inequality (B.85) is due to (B.84). In (B.86), the probabilistic part is bounded as in (B.74). Applying (B.75) yields (B.87). For the inequality (B.88), note that and are chosen in Table A.1 such that

The inequality (B.89) follows since we work under the assumption ; see the discussion following Proposition 3.3. ∎

Proof of Proposition 3.4.

To apply Lemmas B.1 and B.2, we choose

| (B.90) |

in (3.8)–(3.9) with and as in (3.7). Here, we do not need a uniform bound. For this reason, it is not necessary to take the supremum over all admissible estimates of in Lemmas B.1 and B.2. In particular, Lemma B.1 simplifies, since the derivatives in the respective bounds in (B.1) become zero with the choice (B.90). Throughout the proof, we assume .

Probabilistic part: Note that

Then,

| (B.91) | ||||

Furthermore,

| (B.92) |

Deterministic part: Using Lemma B.2 with (B.90), we get

| (B.93) | ||||

where is in Table A.2 and the inequality can be obtained by bounding the two terms in (B.40) given (B.90). as follows. For , the first summand in (B.40) can be bounded as

and the second as

Finally, we combine our results on the probabilistic and deterministic terms to obtain the statement of the proposition. With our choice of in (3.17) and for any , observe that

| (B.94) | |||

| (B.95) | |||

| (B.96) | |||

| (B.97) |

with defined in (B.91) and (B.92). The constants are generic and might differ from line to line. The inequality (B.94) is due to (B.93). Applying Lemma B.1 yields (B.95). For the inequality (B.96), note that and are chosen in Table A.1 such that and . The inequality (B.97) follows since we work under the assumption ; see the discussion following Proposition 3.4. ∎

Proof of Proposition 3.5.

To prove the consistency result in (3.18), we use the inequalities on the probability of discussed in Section 3 and combine the concentration inequalities in Propositions 3.1–3.4. We have

| (B.98) | |||

| (B.99) |

with . The inequality (B.98) follows by Lemma C.6. We proceed with bounding the second probability in (B.98) before we conclude with utilizing Propositions 3.1–3.4 to get the statement of this proposition.