OpReg-Boost: Learning to Accelerate Online Algorithms with Operator Regression

Abstract

This paper presents a new regularization approach – termed OpReg-Boost – to boost the convergence of online optimization and learning algorithms. In particular, the paper considers online algorithms for optimization problems with a time-varying (weakly) convex composite cost. For a given online algorithm, OpReg-Boost learns the closest algorithmic map that yields linear convergence; to this end, the learning procedure hinges on the concept of operator regression. We show how to formalize the operator regression problem and propose a computationally-efficient Peaceman-Rachford solver that exploits a closed-form solution of simple quadratically-constrained quadratic programs (QCQPs). Simulation results showcase the superior properties of OpReg-Boost w.r.t. the more classical forward-backward algorithm, FISTA, and Anderson acceleration.

1 Introduction

In recent years, the increasing volume of streaming data in many engineering and science domains has stimulated a growing number of research efforts on online optimization and learning ([1, 2, 3, 4, 5, 6, 7, 8] and many others). In data processing and machine learning applications, the cost function and the constraints (if present) are parametrized over data points that arrive sequentially; consequently, cost and constraint are time-dependent to reflect new data points and possibly time-varying learning objectives. Beyond data processing and machine learning applications, emerging problems in the context of learning-based control have stimulated lines of research in online identification of dynamical systems [9], and online optimization for robotics [10, 11], model predictive control [12, 13, 14], and games [15, 16], to name a few.

Let now and be a time-varying function, then formally we are interested in time-varying problems of the form

| (1) |

In particular, we assume that is closed, proper, and -weakly convex111Notation. We say that a function is -weakly convex if , with , is convex. The set of convex functions on that are -smooth (i.e., have -Lipschitz continuous gradient) and -strongly convex is denoted as , for ; is the set of -smooth convex functions. An operator is non-expansive iff , for all ; on the other hand, is -contractive, with , iff , for all . We denote the composition of two operators as . We denote by the identity map . We define as the proximal operator of a function with parameter , and we denote by , the projection operator onto the set . We denote by the identity matrix of size , and by the Kronecker product. for each , and is closed, convex and proper uniformly in time (optionally, one can also consider a setting where ). The goal is to design an online algorithm , with updates , so that the sequence exhibits an asymptotic behavior , for a properly defined sequence of optimal value functions and with as small as possible. For this result to be feasible, a blanket assumption common in the online optimization literature is that the variations of problem in time (in terms of path length or functional variability) can be upper bounded by a sub-linear or a linear function of ; see e.g., [2, 5, 7, 6, 8, 17] . If this latter function is linear in , then it is known that online algorithms exhibit an asymptotic error.

A key intuition is to use the existence of this error as an advantage: given the presence of an error due to the dynamics of the cost, one can leverage regularizations in the optimization problem or modifications of the algorithmic steps to boost the convergence without necessarily sacrificing performance. Surprisingly, there may be no trade-off between accuracy and convergence; for example, algorithms constructed based on the regularized problems may offer superior convergence and lower asymptotical errors w.r.t. algorithms built based on the original problem, even though the set of optimal solutions is explicitly perturbed. This line of thought stemmed in the static domain from the seminal works [18, 19, 20], and more recently in the online setting [21, 22].

By building on this, a natural question is “how to best design a surrogate algorithm that allows a gain in convergence rate without compromising optimality?”.

To answer this question, one possibility is to modify the cost function by substituting it with a surrogate function that is, for example, strongly convex and smooth. To fix the idea, consider a non-convex function as in Figure 1. One can evaluate the function at specific points (grey dots) and fit the functional evaluations with a strongly convex function . As long as and are not “dramatically different”, the reasoning is that solving the problem of minimizing instead of will then give the algorithm a boost in terms of convergence rate (without leading to a larger asymptotical error). For this option, which we term Convex Regression, see [23].

In this paper, we focus on a different approach that consists in modifying the algorithmic map . The idea is to substitute with a surrogate mapping that is the “closest” to (in a well defined sense) and has given desirable properties; for example, it is a contractive map. In Figure 1, as an example we consider the case of a gradient descent algorithm in terms of a fixed point operator , with being the step size. The idea here is to use evaluations of to fit a mapping with useful properties (e.g., contractivity). By using in lieu of , then one may be able to boost convergence and possibly reduce the asymptotical error. We show in our numerical experiments that this methodology – referred to as OpReg-Boost – outperforms the first option where one utilizes a surrogate cost. Overall, this paper offers the following contributions.

-

1.

We present a novel OpReg-Boost method to learn-project-and-solve with linear convergence optimization problems. The method is based on operator regression, and it is designed to boost convergence without necessarily increasing the asymptotical error. Operator regression is formulated as a convex quadratically-constrained quadratic programs (QCQPs).

-

2.

We present efficient ways to solve the operator regression problems in dimension with observations via a pertinent reformulation of the Peaceman-Rachford splitting (PRS) method, see e.g. [24]. Our PRS method is trivially parallel and allows for a reduction of the per-iteration complexity from a convex QCQP in variables and constraints (i.e., a complexity of at least , to 1-constraint convex QCQPs in variables. Importantly, we show that these simpler QCQPs admit a closed form solution, which leads to a per iteration complexity of .

-

3.

We test the performance of the proposed method for two optimization problems: i) a linear regression problem with an ill-conditioned cost [c.f. [25]]; and, ii) an online phase retrieval problem, which requires the minimization of a weakly convex function [c.f. [26]]. The proposed operator regression method shows promising performance in both scenarios as compared to forward-backward (with and without backtracking line search) and its accelerated variants FISTA [27] and an online version of the Anderson acceleration in [25].

-

4.

In the Appendix of [23], we discuss an alternative version of OpReg-Boost that leverages an interpolation technique that goes back to 1945 to trade-off accuracy and speed in operation regression, by interpolating the learned mapping outside the data points via alternating projections. And, also in the Appendix, we present the Convex Regression method, which is also novel (but less performing) and represents an additional contribution in the context of the design of surrogate cost functions.

The extended version of this manuscript with appendix and proofs can be found in [23].

1.1 Related work

Learning to optimize and regularize is a growing research topic; see [28, 29, 30, 31, 32, 33, 34, 35] as representative works, even though they focus on slightly different problems. Additional works in the context of learning include the design of convex loss functions in, e.g., [36, 37]. Interpreting algorithms as mappings and operators (averaged, monotone, etc.) has been extremely fruitful for characterizing their convergence properties [38, 39, 24, 40, 41].

Convex regression is treated extensively in [42, 43, 44, 45], while recently being generalized to smooth strongly convex functions [46] based on A. Taylor’s works [47, 48]; an interesting approach using similar techniques for optimal transport is offered in [49]. Operator regression is a recent and at the same time old topic. We are going to build on the recent work [50] and the F.A. Valentine’s 1945 paper [51].

And finally, the class of weakly convex functions is broad and important in optimization [54, 55, 26, 56, 57]. Applications featuring this class include robust phase retrieval and many others. In control theory, this functions extend, e.g., online identification and control to a class on non-linear dynamical systems, and potential games to hypo-monotone settings.

2 Learning to accelerate with operator regression

Consider the time-varying problem (1) and an associated online algorithm , designed to track the optimizers of the problem. The mapping can be written as sum and/or composition of maps. To fix the ideas and notation, we provide the following example, which will be used throughout the paper to concretely convey ideas (although we note that the proposed methodology is more widely applicable).

Example. Consider an online forward-backward type algorithm with updates , where

| (2) |

where is the proximal operator () and the identity map. The properties of this algorithm depend on the map . In case of a generic smooth non-convex or for convex functions, one can show convergence of the regret to a bounded error [58, 17]; on the other hand, if uniformly in , , then (2) can obtain a linear convergence for the sequence to the unique optimizer’s trajectory of up to a bounded error [7].

Our goal can be formulated as follows: if the algorithmic map is not contractive or is only locally contractive, is it possible to find an approximate mapping that is globally contractive to boost the convergence to the optimal solutions (within an error)?

Consider again the proximal-gradient method in the Example, where we recall that , with . When is -strongly convex and -smooth uniformly in time, and , the mapping is contractive; i.e., for all and . Thus, the recursion achieves linear convergence. However, the question we pose here is the following: when is not -strongly convex, can we still learn map , and use the surrogate algorithm to achieve linear convergence?222Notice that the proximal of – which may encode important properties such as sparsity or constraints – is not subjected to the learning procedure and remains unchanged.

To this end, using Fact 2.2 in [50], it follows that a mapping is -contractive interpolable (and therefore extensible to the whole space) if and only if it satisfies:

| (3) |

where is a finite set of indexes for the points . Therefore, using a number of evaluations of the mapping at the points , we pose the following convex QCQP as our operator regression problem:

| (4) |

where the cost function represents a least-square criterion on the “observations” (i.e., the evaluations of the mapping) , , and the constraints enforce contractivity. In particular, the optimal values on the data points represent the evaluations of a -contracting operator when applied to those points, i.e., .

2.1 PRS-based solver

The convex problem (4) can be solved using off-the-shelf solvers for convex programs; however, the computational complexity may be a limiting factor, since the problem has a number of constraints that scales quadratically with the number of data points . In particular, the computational complexity of interior-point methods would scale at least as . This is generally the case in non-parametric regression [44, 59]. To resolve this issue, we propose a parallel algorithm that solves (4) more efficiently based on the so-called Peaceman-Rachford splitting (PRS), see e.g. [24], and that leverages the closed form solution of particular 1-constraint QCQPs.

To this end, define the following set of pairs which are ordered (that is, for example we take and not , to avoid counting the pair twice). We associate with each pair the constraint , for a total of constraints.

Let and be copies of and associated to the -th pair; then we can equivalently reformulate problem (4) as

| (7) |

where we write that if the -th constraint involves , and recall that , , . Problem (7) is a strongly convex problem with convex constraints defined in the variables . Problem (7) is in fact a consensus problem which can be decomposed over the pairs by using PRS, as defined in the following lemma.

Lemma 2.1.

Problem (7) can be solved by using Peaceman-Rachford splitting (PRS), yielding the following iterative procedure. Given the penalty , apply for :

| (8a) | ||||

| (8b) | ||||

At each iteration, the algorithm solves in parallel convex QCQPs – each in variables and constraint – and then aggregates the results. Importantly, the following lemma shows that 1-constraint QCQPs can be solved in closed form with a complexity of , and hence the total per iteration complexity of (8) is .

Proof. See Appendix C.

Lemma 2.2 (Solving 1-constraint QCQPs).

Proof. See Appendix C.

Finally, we discuss how the closed form solution of 1-constraint QCQPs leads to a very low per iteration complexity.

Lemma 2.3 (Computational complexity).

Consider the Peaceman-Rachford splitting (8) that solves the operator regression problem (7), and further notice that the 1-constraint QCQPs (8a) have a closed form solution described in Lemma 2.2.

Then, the computational complexity of the PRS solver is per iteration. In particular, when the budget of operator calls is much smaller than the dimension of the problem (), then the complexity reduces to per iteration.

Proof. See Appendix C.

3 OpReg-Boost

We are now ready to present our main algorithm. To convey ideas concretely, we focus here on online algorithms of the forward-backward type as in Example 1, i.e.,333Access to an operator is the only requirement for the application of OpReg-Boost. However, it is instructive to fix the ideas on a concrete mapping by focusing on the forward-backward algorithm.

| (12) |

where we recall that . In particular, we will utilize the operator regression method on the mapping . We recall that the operator is non-expansive; therefore, the Lipschitz constant of the overall mapping depends on the mathematical properties of [60] and, more specifically, of the function . In particular, since is not assumed to be strongly convex in general, may not be contractive and, consequently, is not contractive either. With this in mind, the goal is to learn a contracting mapping from evaluations of at some points. The OpReg-Boost algorithm can thus be described as follows.

OpReg-Boost algorithm Required: number of points , stepsize , contraction factor , initial condition .

At each time do:

-

[S1]

Learn the closest contracting operator to , say by:

-

[S1.1]

Choose points around to create the set of points , , where the map is to be evaluated.

-

[S1.2]

Evaluate the mapping at the data points: , , i.e., .

-

[S1.3]

Solve (4) on , with the PRS-based algorithm.

-

[S1.4]

Output from the solution of [S1.3].

-

[S1.1]

-

[S2]

Compute .

A couple of remarks are in order. First, the computational complexity of the overall algorithm is dominated by the operation regression problem (4) in step [S1.3]; on the other hand, the number of gradient calls (used to evaluate ) is -times the one of a standard forward-backward algorithm. At each time , we perform gradient evaluations at the points (the points could be obtained, e.g., by adding a zero-mean Gaussian noise term to ). can be as small as in practice.

Second, as one can see from steps [S1.2]–[S1.4], the operation regression problem (4) directly provides the evaluation of the regularized operator at the data point , since we choose to define one of the training points.

4 Numerical results

We present a number of experiments to evaluate the performance of the proposed method444The experiments were implemented in Python and performed on a computer with Intel i7-4790 CPU, GHz, and GB of RAM, running Linux. Code and data are available. The implementation is serial (possible due to the manageable size of the regression problems); future work will look at parallel implementations.. We consider: (i) an ill-conditioned online linear regression with a convex cost (but not strongly convex); (ii) an online phase retrieval problem that is weakly convex, and which is characterized by a high computational cost per operator evaluation. The first example is rather well-studied, at least in the well-conditioned region, and it can be used for example to derive control laws under sparsity requirements [61, 62]. The second example has important repercussions in adaptive optics, where phase retrieval techniques are used as building blocks to generate control signals [63, 64]

The metric used in the experiments is the tracking error, characterized as the distance from the ground truth signal of the solution output by the solvers. By we denote the signal being tracked via linear regression in section 4.1 or the phase being retrieved in section 4.2. We choose the tracking error as a proxy for the distance to the optimizer in line with the work of [26], since (i) determining is in general hard to do computationally in the problems we are considering and it may not be unique, and (ii) the tracking error very naturally provides insights on how the methods perform in estimating the real signals.

4.1 Online linear regression

We consider the following time-varying problem:

| (13) |

with , , such that and having maximum and minimum (non-zero) eigenvalues , . The goal is to reconstruct a signal with sinusoidal components, of them being zero, from the noisy observations , and . Due to being rank deficient, the cost is convex but not strongly so, and we have , where and are the maximum and minimum non-zero eigenvalues of a matrix. The function changes every .

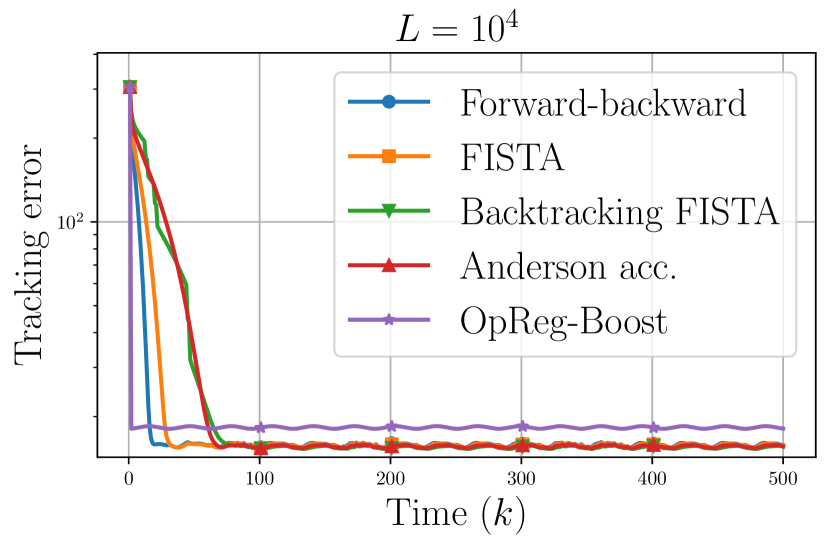

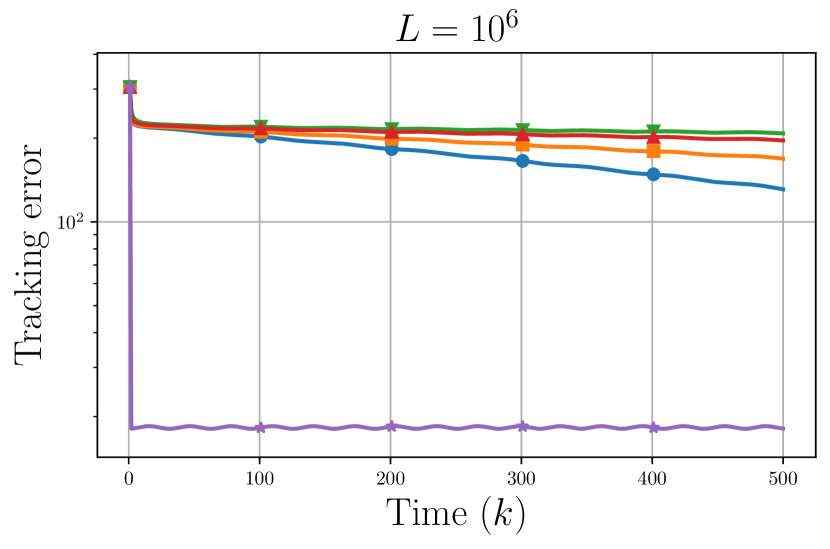

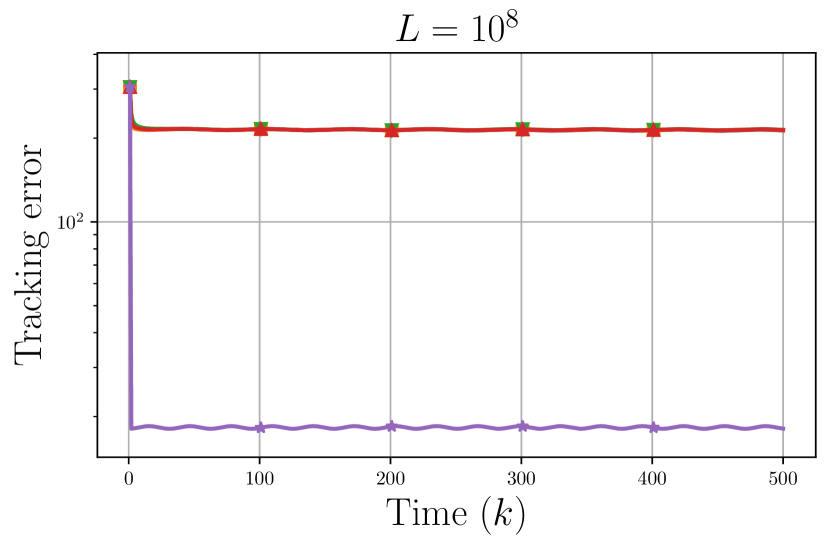

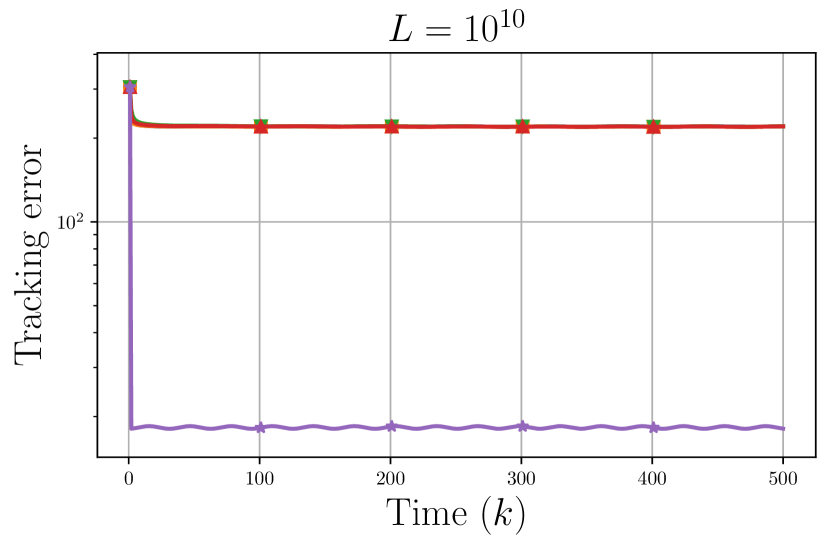

In Figure 2, we show a comparison of the tracking error attained by the proposed OpReg-Boost against the forward-backward method, and its accelerated versions FISTA (with and without backtracking line search) [27], and (guarded) Anderson [25]. The methods are given the same computational time budget555Specifically, we evaluate the computational time required by one iteration of OpReg-Boost, and run the other methods for the same time. We remark that OpReg-Boost requires at least the time needed by iterations of forward-backward to generate the operator regression data. For example, our experiments show that with the choice during one iteration of OpReg-Boost we can apply of forward-backward or FISTA, and one or two of Anderson and FISTA with backtracking., the step-size of forward-backward is , and the parameters of OpReg-Boost are and . For large values of OpReg-Boost outperforms all other methods; in the case it performs slightly worse in terms of asymptotic error, but successfully improves the convergence rate. The reason behind the performance we observe is that as grows larger, the allowed step-size for forward-backward becomes smaller – indeed, we have the bound . We further remark that the performance of OpReg-Boost can be improved in the case by choosing a different value of , see [23].

| Algorithm | as. err. | t. / s. [s] | as. err. | t. / s. [s] | as. err. | t. / s. [s] |

| Forward-backward | ||||||

| FISTA | ||||||

| FISTA (backtr.) | ||||||

| Anderson | ||||||

| OpReg-Boost | ||||||

Finally, in Table 1 we report the asymptotic error and computational time of OpReg-Boost as compared to the forward-backward based solvers for three different sizes of the problem with and . In terms of asymptotic error – evaluated when all methods are given the same total computational time – the performance of OpReg-Boost is consistently better than the other methods. Regarding the computational time per step of the algorithm we see that OpReg-Boost is comparable with the accelerated methods FISTA with backtracking and Anderson. On the other hand, the computationally lighter forward-backward and FISTA require less time per step, but, again, when given the same computational time the performance of OpReg-Boost is still better.

4.2 Online phase retrieval

We consider now the following phase retrieval problem presented in [26]:

| (14) |

where the goal is to reconstruct the time-varying signal , , from the noisy measurements , and . The signal is piece-wise constant, with the value of each constant piece being independently drawn. The additive noises are i.i.d. Laplace with zero mean and scale parameter . The are the rows of , constructed as , with an orthogonal matrix, and a diagonal one with elements , (hence the condition number of is ), and the remaining drawn from . The problem changes every .

We consider the prox-linear solver proposed in the work of [65] (see also [26]), characterized by , where denotes the following linearized version of the cost in (14): We choose the step-size of the prox-linear solver as , which empirically led to convergence (at least in the initial transient) without the need for line search. Notice that the proximal operator does not have a closed form, and each operator call requires the solution of a quadratic program, which takes .

We also consider our OpReg-Boost algorithm applied to the operator666This shows better performance in practice rather than regularizing alone. Strictly speaking, with this choice, function in (1) would be the indicator function of a non-convex set. The good performance of the proposed approach however suggests that it can be applied to more general problems than (1). , and which regularizes the operator to a -contractive operator, yielding then . The solution of an operator regression problem requires . In the results, then, during the time before the arrival of a new problem (), we perform either steps of the prox-linear solver, or one step of OpReg-Boost with training points (and choosing the PRS parameter ).

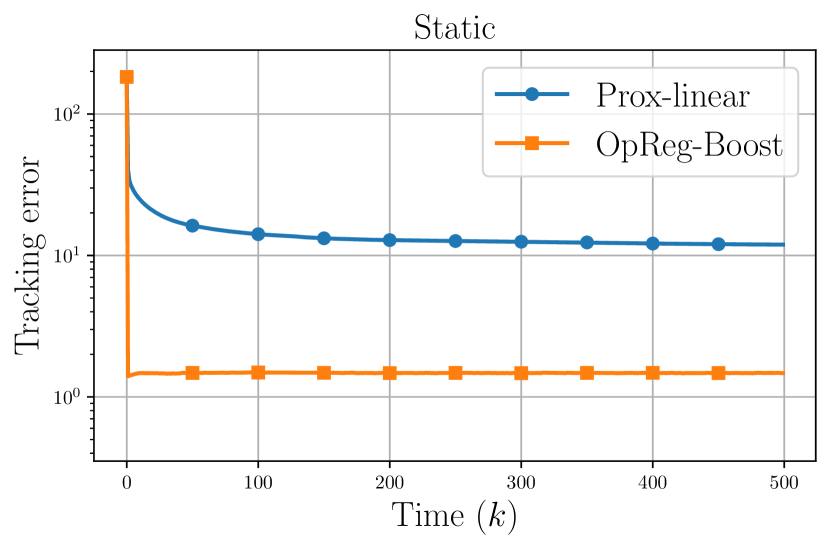

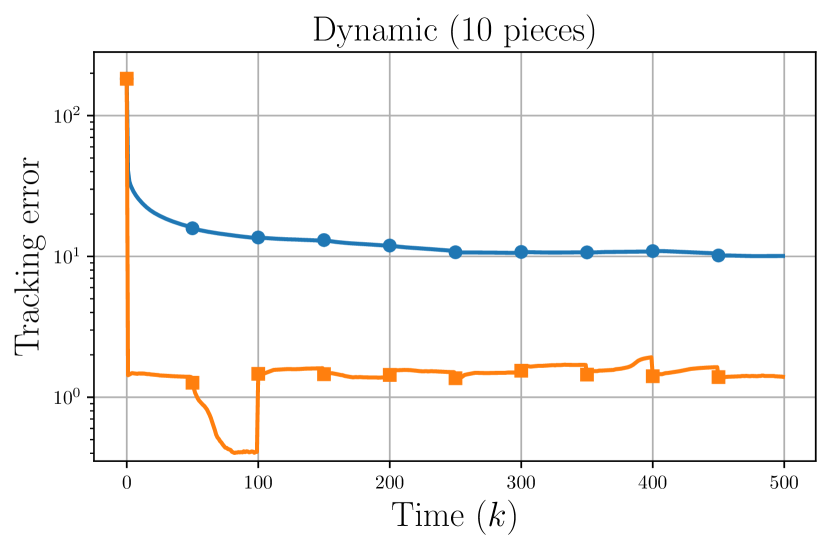

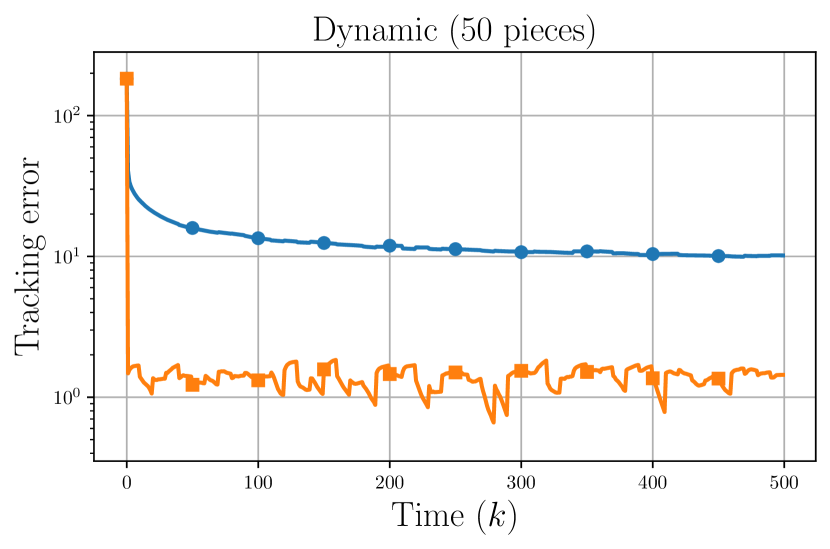

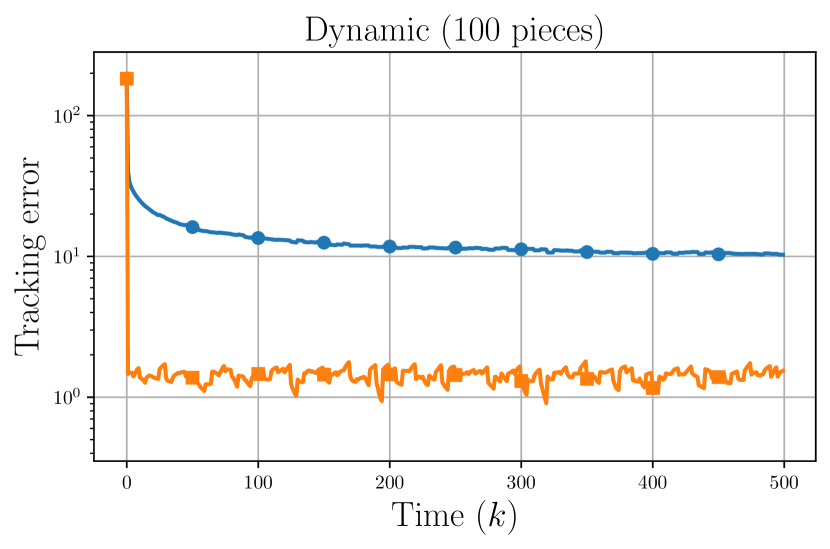

In Figure 3, we show the tracking error of prox-linear compared with OpReg-Boost when the signal has different numbers of constant pieces (from being static – one constant value – to being highly dynamic – changing every ). As we can see, OpReg-Boost consistently outperforms prox-linear, including in the static case, in which OpReg-Boost quickly converges to the (approximate) fixed point, while prox-linear converges more slowly.

References

- [1] A. Y. Popkov, “Gradient methods for nonstationary unconstrained optimization problems,” Automation and Remote Control, vol. 66, no. 6, pp. 883–891, 2005.

- [2] O. Besbes, Y. Gur, and A. Zeevi, “Non-stationary Stochastic Optimization,” Operations research, vol. 63, no. 5, pp. 1227 – 1244, 2015.

- [3] M. S. Asif and J. Romberg, “Sparse recovery of streaming signals using -homotopy ,” IEEE Transactions on Signal Processing, vol. 62, no. 16, pp. 4209 – 4223, 2014.

- [4] E. C. Hall and R. M. Willett, “Online convex optimization in dynamic environments,” IEEE Journal of Selected Topics in Signal Processing, vol. 9, no. 4, pp. 647–662, 2015.

- [5] A. Jadbabaie, A. Rakhlin, S. Shahrampour, and K. Sridharan, “Online Optimization: Competing with Dynamic Comparators,” in Proceedings of the Eighteenth International Conference on Artificial Intelligence and Statistics, PMLR, no. 38, 2015, pp. 398 – 406.

- [6] A. Mokhtari, S. Shahrampour, A. Jadbabaie, and A. Ribeiro, “Online optimization in dynamic environments: Improved regret rates for strongly convex problems,” in IEEE Conference on Decision and Control, 2016, pp. 7195–7201.

- [7] E. Dall’Anese, A. Simonetto, S. Becker, and L. Madden, “Optimization and Learning with Information Streams: Time-varying Algorithms and Applications,” IEEE Signal Processing Magazine, May 2020.

- [8] Y. Li, G. Qu, and N. Li, “Online Optimization with Predictions and Switching Costs: Fast Algorithms and the Fundamental Limit,” arXiv: 1801.07780, 2020.

- [9] Y. Zheng and N. Li, “Non-Asymptotic Identification of Linear Dynamical Systems Using Multiple Trajectories,” IEEE Control Systems Letters, vol. 5, no. 5, pp. 1693–1698, 2021.

- [10] F. Berkenkamp, R. Moriconi, A. P. Schoellig, and A. Krause, “Safe learning of regions of attraction for uncertain, nonlinear systems with Gaussian processes,” in Proceedings of the 55th Conference on Decision and Control, December 2016, pp. 4661 – 4666.

- [11] X. Luo, Y. Zhang, and M. M. Zavlanos, “Socially-Aware Robot Planning via Bandit Human Feedback,” in 2020 ACM/IEEE 11th International Conference on Cyber-Physical Systems (ICCPS), 2020, pp. 216–225.

- [12] S. Paternain, M. Morari, and A. Ribeiro, “A Prediction-Correction Method for Model Predictive Control,” in 2018 Annual American Control Conference (ACC), Jun. 2018, pp. 4189–4194.

- [13] D. Liao-McPherson, M. Nicotra, and I. Kolmanovsky, “A Semismooth Predictor Corrector Method for Real-Time Constrained Parametric Optimization with Applications in Model Predictive Control,” in 2018 IEEE Conference on Decision and Control (CDC), Dec. 2018, pp. 3600–3607.

- [14] R. Zhang, Y. Li, and N. Li, “On the Regret Analysis of Online LQR Control with Predictions,” in 2021 American Control Conference (ACC), 2021, pp. 697–703.

- [15] G. Belgioioso, A. Nedić, and S. Grammatico, “Distributed generalized nash equilibrium seeking in aggregative games on time-varying networks,” IEEE Transactions on Automatic Control, vol. 66, no. 5, pp. 2061–2075, 2021.

- [16] F. Fabiani, A. Simonetto, and P. J. Goulart, “Learning equilibria with personalized incentives in a class of nonmonotone games,” arXiv:2111.03854 [cs, eess, math], Nov. 2021.

- [17] N. Hallak, P. Mertikopoulos, and V. Cevher, “Regret minimization in stochastic non-convex learning via a proximal-gradient approach,” arXiv preprint arXiv:2010.06250, 2020.

- [18] Y. Nesterov, “Smooth minimization of non-smooth functions,” Mathematical Programming, vol. 103, no. 1, pp. 127–152, 2005.

- [19] J. Koshal, A. Nedić, and U. Y. Shanbhag, “Multiuser Optimization: Distributed Algorithms and Error Analysis,” SIAM Journal on Optimization, vol. 21, no. 3, pp. 1046 – 1081, 2011.

- [20] O. Devolder, F. Glineur, and Y. Nesterov, “Double Smoothing Technique for Large-Scale Linearly Constrained Convex Optimization,” SIAM Journal on Optimization, vol. 22, no. 2, pp. 702 – 727, 2012.

- [21] A. Simonetto and G. Leus, “Double Smoothing for Time-Varying Distributed Multi-user Optimization,” in Proceedings of the IEEE Global Conference on Signal and Information Processing, Atlanta, US, December 2014.

- [22] N. Bastianello, A. Simonetto, and R. Carli, “Distributed Prediction-Correction ADMM for Time-Varying Convex Optimization,” in Proceedings of the Asilomar Conference on Signals, Systems, and Computers, 2020.

- [23] N. Bastianello, A. Simonetto, and E. Dall’Anese, “OpReg-Boost: Learning to Accelerate Online Algorithms with Operator Regression,” arXiv:2105.13271 [cs, math], Jul. 2021. [Online]. Available: http://arxiv.org/abs/2105.13271

- [24] H. H. Bauschke and P. L. Combettes, Convex analysis and monotone operator theory in Hilbert spaces, 2nd ed., ser. CMS books in mathematics. Cham: Springer, 2017.

- [25] V. Mai and M. Johansson, “Anderson Acceleration of Proximal Gradient Methods,” in Proceedings of the 37th International Conference on Machine Learning, 2020, pp. 6620–6629.

- [26] J. C. Duchi and F. Ruan, “Stochastic Methods for Composite and Weakly Convex Optimization Problems,” SIAM Journal on Optimization, vol. 28, no. 4, pp. 3229–3259, Jan. 2018.

- [27] A. Beck and M. Teboulle, “A Fast Iterative Shrinkage-Thresholding Algorithm for Linear Inverse Problems,” SIAM Journal on Imaging Sciences, vol. 2, no. 1, pp. 183–202, Jan. 2009.

- [28] T. Meinhardt, M. Moller, C. Hazirbas, and D. Cremers, “Learning proximal operators: Using denoising networks for regularizing inverse imaging problems,” in Proceedings of the IEEE International Conference on Computer Vision, 2017, pp. 1781–1790.

- [29] T. Nghiem, G. Stathopoulos, and C. Jones, “Learning Proximal Operators with Gaussian Processes,” in Proceedings of the Allerton Conference on Communication, Control, and Computing, 2018.

- [30] G. Ongie, A. Jalal, R. B. C.A. Metzler, A. Dimakis, and R. Willett, “Deep Learning Techniques for Inverse Problems in Imaging,” IEEE Journal on Selected Areas in Information Theory, vol. 5, 2020.

- [31] S. Banert, A. Ringh, J. Adler, J. Karlsson, and O. Öktem, “Data-Driven Nonsmooth Optimization,” SIAM Journal on Optimization, vol. 30, no. 1, pp. 102–131, 2020.

- [32] R. Cohen, M. Elad, and P. Milanfar, “Regularization by Denoising via Fixed-Point Projection (RED-PRO),” arXiv:2008.00226, 2020.

- [33] J.-C. Pesquet, A. Repetti, M. Terris, and Y. Wiaux, “Learning Maximally Monotone Operators for Image Recovery,” arXiv:2012.13247, 2020.

- [34] A. Simonetto, E. Dall’Anese, J. Monteil, and A. Bernstein, “Personalized optimization with user’s feedback,” arXiv preprint arXiv:1905.00775, 2019.

- [35] T. Chen, X. Chen, W. Chen, H. Heaton, J. Liu, Z. Wang, and W. Yin, “Learning to optimize: A primer and a benchmark,” arXiv preprint arXiv:2103.12828, 2021.

- [36] H. G. Ramaswamy and S. Agarwal, “Convex calibration dimension for multiclass loss matrices,” The Journal of Machine Learning Research, vol. 17, no. 1, pp. 397–441, 2016.

- [37] J. Finocchiaro, R. Frongillo, and B. Waggoner, “Unifying lower bounds on prediction dimension of consistent convex surrogates,” arXiv preprint arXiv:2102.08218, 2021.

- [38] R. T. Rockafellar, “Monotone Operators and the Proximal Point Algorithm,” SIAM Journal of Control and Optimization, vol. 14, no. 5, pp. 877 – 898, 1976.

- [39] J. Eckstein, “Splitting Methods for Monotone Operators with Applications to Parallel Optimization,” Ph.D. dissertation, MIT, June 1989.

- [40] E. K. Ryu and S. Boyd, “Primer on Monotone Operator Methods,” Applied Computational Mathematics, vol. 15, no. 1, pp. 3 – 43, 2016.

- [41] T. Sherson, R. Heusdens, and W. Kleijn, “Derivation and Analysis of the Primal-Dual Method of Multipliers Based on Monotone Operator Theory,” IEEE Transactions on Signal and Information Processing over Networks, vol. 5, no. 2, pp. 334–347, 2018.

- [42] E. Seijo and B. Sen, “Nonparametric Least Squares Estimation of a Multivariate Convex Regression Function,” The Annals of Statistics, vol. 39, no. 3, pp. 1633 – 1657, 2011.

- [43] E. Lim and P. W. Glynn, “Consistency of Multidimensional Convex Regression,” Operation Research, vol. 60, no. 1, pp. 196 – 208, 2012.

- [44] R. Mazumder, A. Choudhury, G. Iyengar, and B. Sen, “A Computational Framework for Multivariate Convex Regression and Its Variants,” Journal of the American Statistical Association, vol. 114, no. 525, pp. 318–331, 2019.

- [45] J. Blanchet, P. W. Glynn, J. Yan, and Z. Zhou, “Multivariate Distributionally Robust Convex Regression under Absolute Error Loss,” in Proceedings of NeurIPS, 2019.

- [46] A. Simonetto, “Smooth Strongly Convex Regression,” in 2020 28th European Signal Processing Conference (EUSIPCO). Amsterdam: IEEE, Jan. 2021, pp. 2130–2134.

- [47] A. Taylor, J. Hendrickx, and F. Glineur, “Smooth Strongly Convex Interpolation and Exact Worst-case Performance of First-order Methods,” Mathematical Programming, vol. 161, no. 1, pp. 307 – 345, 2017.

- [48] A. Taylor, “Convex Interpolation and Performance Estimation of First-order Methods for Convex Optimization,” Ph.D. dissertation, Université catholique Louvain, Belgium, January 2017.

- [49] F.-P. Paty, A. d’Aspremont, and M. Cuturi, “Regularity as Regularization: Smooth and Strongly Convex Brenier Potentials in Optimal Transport,” in Proceedings of AISTATS, 2020.

- [50] E. K. Ryu, A. B. Taylor, C. Bergeling, and P. Giselsson, “Operator Splitting Performance Estimation: Tight Contraction Factors and Optimal Parameter Selection,” SIAM Journal on Optimization, vol. 30, no. 3, pp. 2251–2271, 2020.

- [51] F. A. Valentine, “A Lipschitz condition preserving extension for a vector function,” American Journal of Mathematics, vol. 67, no. 1, pp. 83–93, 1945.

- [52] D. Scieur, “Acceleration in Optimization,” Ph.D. dissertation, PSL Research University, France, September 2018.

- [53] J. Zhang, B. O’Donoghue, and S. Boyd, “Globally Convergent Type-I Anderson Acceleration for Nonsmooth Fixed-Point Iterations,” SIAM Journal on Optimization, vol. 30, no. 4, pp. 3170–3197, 2020.

- [54] T. R. Rockafellar, “Favorable classes of Lipschitz continuous functions in subgradient optimization,” In Nurminski, E. A. (ed.), Progress in Nondifferentiable Optimization, pp. 125 – 143, 1982.

- [55] J.-P. Vial, “Strong and weak convexity of sets and functions,” Mathematics of Operations Research, vol. 8, no. 2, pp. 231–259, 1983.

- [56] D. Davis and D. Drusvyatskiy, “Stochastic Model-Based Minimization of Weakly Convex Functions,” SIAM Journal on Optimization, vol. 29, no. 1, pp. 207–239, 2019.

- [57] V. Mai and M. Johansson, “Convergence of a Stochastic Gradient Method with Momentum for Non-Smooth Non-Convex Optimization,” in Proceedings of the 37th International Conference on Machine Learning, 2020, pp. 6630–6639.

- [58] A. Simonetto, “Time-Varying Convex Optimization via Time-Varying Averaged Operators ,” arXiv: 1704.07338v1, 2017.

- [59] N. S. Aybat and Z. Wang, “A Parallel Method for Large Scale Convex Regression Problems,” in Proceedings of the IEEE Conference in Decision and Control, 2014.

- [60] H. H. Bauschke, S. M. Moffat, and X. Wang, “Firmly Nonexpansive Mappings and Maximally Monotone Operators: Correspondence and Duality,” Set-Valued and Variational Analysis, vol. 20, no. 1, pp. 131–153, Mar. 2012.

- [61] H. Ohlsson, F. Gustafsson, L. Ljung, and S. Boyd, “Trajectory generation using sum-of-norms regularization,” in 49th IEEE Conference on Decision and Control (CDC), 2010, pp. 540–545.

- [62] F. Lin, M. Fardad, and M. R. Jovanovic, “Design of optimal sparse feedback gains via the alternating direction method of multipliers,” IEEE Transactions on Automatic Control, vol. 58, no. 9, pp. 2426–2431, 2013.

- [63] P. Massioni, C. Kulcsár, H.-F. Raynaud, and J.-M. Conan, “Fast computation of an optimal controller for large-scale adaptive optics,” Journal of the Optical Society of America. A Optics, Image Science, and Vision, vol. 28, no. 11, pp. 2298–2309, 2011.

- [64] J. Antonello and M. Verhaegen, “Modal-based phase retrieval for adaptive optics,” J. Opt. Soc. Am. A, vol. 32, no. 6, pp. 1160–1170, Jun 2015.

- [65] D. Drusvyatskiy and A. S. Lewis, “Error Bounds, Quadratic Growth, and Linear Convergence of Proximal Methods,” Mathematics of Operations Research, vol. 43, no. 3, pp. 919–948, Aug. 2018.

- [66] H. Bauschke and V. Koch, “Projection Methods: Swiss Army Knives for Solving Feasibility and Best Approximation Problems with Halfspaces,” in Contemporary Mathematics, S. Reich and A. Zaslavski, Eds. Providence, Rhode Island: American Mathematical Society, 2015, vol. 636, pp. 1–40.

Appendix A Convex regression

The concept of convex regression is briefly introduced here; we refer the reader to, e.g., [44, 46] for the technical details. Suppose one has noisy measurements of a convex function (say ) at points , , and (optionally) its gradients . Then convex regression is a least-squares approach to estimate the generating function based on the measurements. Formally, letting , then one would like to solve the functional estimation problem

| (15) |

where and are the measurements of the function and its gradient at the data points.

In lieu of the infinite-dimensional problem (15), one can consider an equivalent estimation problem to find the true values of the function and its gradients at the data point (i.e., , ); this amounts to the following convex quadratically-constrained quadratic program:

| (16a) | |||||

Using the point estimate , an interpolation scheme then extends the estimation of the function to the whole space (maintaining the functional properties) as:

| (17) |

where indicates the convex hull and

| (18) |

For the goal of boosting the convergence of online algorithms we can leverage convex regression as follows. For each time we perform evaluations of the function (and optionally its gradients) and utilize the procedure above to project the function onto the space of strongly convex and smooth functions . Then, we can use the estimated function to build an algorithm . For example, for the proximal-gradient method in Example 1, the algorithmic map amounts to .

However, the application of convex regression within the tight time constraints of online optimization hinges on the efficient solution of (16). In the following section we describe a solver based on Peaceman-Rachford splitting that solves (16).

A.1 PRS-based solver

Similarly to operator regression in section 2, the idea is to make multiple copies of the unknowns so that problem (16) can be rewritten as a set of simpler QCQPs in unknowns and with two constraints each.

Recalling the definition of the pairs , we can associate with each the two constraints

| (19) |

where by e.g. we denote the copy of in the pair . Problem (16) then becomes

| (20) |

We can now leverage the separable structure of problem (20) in order to solve it with PRS.

Lemma A.1.

Problem (20) can be solved by using Peaceman-Rachford splitting (PRS), yielding the following iterative procedure. Given the penalty , apply for :

| (21a) | ||||

| (21b) | ||||

where . At each iteration, the algorithm solves in parallel convex QCQPs – each in variables and constraints – and then aggregates the results. Importantly, the following lemma shows that the particular 2-constraint QCQPs can be solved in closed form with a complexity of , and hence the total per iteration complexity of (21) is .

Proof. Follows the same derivation of Lemma 2.1.

Lemma A.2 (Solving (21a)).

The update (21a) can be rewritten as the following QCQP with two constraints:

| (22) |

where , , and

The problem (22) admits the following closed form solution

| (23) | ||||

| (24) |

where

| (25) | ||||

| (26) |

with denoting the -th block in the vector 777Notice that the first two blocks are scalars, while the third and fourth are vectors in ..

Sketch of proof. From the KKT conditions of (22) we can easily derive the expression for , which means that we need to find the optimal solution for the two Lagrange multipliers and .

Assume now that , then the constraints of (22) should be verified as equalities. Substituting the expression for into these two equalities and subtracting them we get the expression for . Summing the two equalities instead yields a quadratic equation in , whose positive solution yields the expression above.

Finally, by definition and , but since and may be negative quantities, we impose that the resulting Lagrange multipliers be non-negative.

Lemma A.3 (Computational complexity).

Consider the Peaceman-Rachford splitting (21) that solves the operator regression problem (20), and further notice that the 2-constraint QCQPs (21a) have a closed form solution described in Lemma A.2.

Then, the computational complexity of the PRS solver is per iteration. In particular, when the budget of operator calls is much smaller than the dimension of the problem (), then the complexity reduces to per iteration.

Proof. The closed form solution described in Lemma A.2 only requires operation on vectors, with complexity . Since we have such closed forms to compute, then the thesis follows.

A.2 CvxReg-Boost

We present here the CvxReg-Boost algorithm.

CvxReg-Boost algorithm Required: number of points , stepsize , functional parameters , initial condition .

At each time do:

- [S1]

-

[S2]

Apply .

A.3 Numerical results

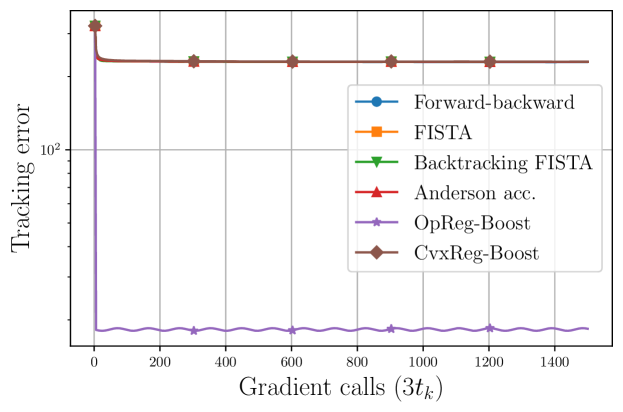

In Figure 4 we report the tracking error for the different methods alongside OpReg-Boost and CvxReg-Boost when applied to the online linear regression problem of section 4.1. In particular, all methods are given a budget of gradient calls per time , and we choose and . We notice that the performance of CvxReg-Boost in terms of tracking error is very similar to the forward-backward based methods, and it is less performing than OpReg-Boost.

In terms of computational time, OpReg-Boost requires per step, whereas for CvxReg-Boost we have , although both methods have a tailored PRS-based solver. Therefore, the much longer computational time of CvxReg-Boost therefore makes it impractical in the online scenario considered in section 4.1.

Appendix B OpReg-Boost with interpolation

The OpReg-Boost method described in section 3 requires that we solve an operator regression problem at each time . In this section we discuss an alternative approach in which we solve an operator regression problem every times, and otherwise perform interpolation of the solution to the last operator regression problem.

B.1 Interpolating a Lipschitz continuous operator

We start by discussing the approach proposed in [51] to interpolate Lipschitz continuous operators while preserving Lipschitz continuity.

Given the pairs – obtained in our case from the solution of (4) – we can interpolate the mapping outside the data points as follows. By the Corollary to Theorem 5 of [51], one has that a -Lipschitz continuous map can be extended (that is, interpolated) in a new point , while preserving Lipschitz continuity (along with its modulus ) as follows:

| (27) |

where denotes a ball centered at with radius . That is, one can interpolate in a new point by finding a point in the intersection of the balls centered in with radii , . Notice that the intersection is guaranteed to be non-empty by Theorem 1 of [51].

By construction, the new evaluation satisfies with , this implies that that contractivity is preserved in this sequential interpolation process.

Interpolating a Lipschitz-continuous operator requires finding a point in the intersection of balls. This can be performed using for example the method of alternating projections (MAP) [66]. In particular, MAP for operator interpolation based on (27) is characterized by the following update:

| (28) |

for any initial condition . In practice we stop MAP when for example for some threshold .

B.2 Interpolation for OpReg-Boost

In the following we present the interpolated version of OpReg-Boost, in which we keep the estimated operator for a few time instances (termed hereafter as interpolation steps ), and we interpolate it to generate new approximate optimizers , . This approach lowers the number of gradient calls, while introducing a lag-type error (since refers to and will be outdated at ).

OpReg-Boost with interpolation algorithm Required: number of points , stepsize , initial condition , interpolation steps .

At each time do:

-

[S1]

IF then,

-

[S2]

Learn the closest contracting operator to , say by employing steps [S1.1]-[S1.4] of OpReg-Boost. Output .

ELSE

-

[S2’]

Interpolate last available for by using (27) with the method of alternating projections and output

-

[S2]

-

[S3]

Apply .

Finally, in Table 2 we compare the performance of the interpolated version with the standard OpReg-Boost as a function of the PRS penalty parameter . We apply the two methods to the online linear regression problem of section 4.1 when and , choosing for the interpolated version – that is, we solve a new operator regression every other time .

First of all, it is interesting to notice that for the performance of the two versions is almost equal in term of asymptotic error, although as mentioned above the interpolation suffers from an additional lag-type error. However, the time required to carry out the interpolation is larger than the time it takes to solve the operator regression. On the other hand, when we require better precision in the solution of the operator regression by choosing we can see that the computational time of OpReg-Boost becomes larger than the interpolation time. This suggests that the choice of applying interpolation has to be made depending on the value of .

| OpReg-Boost | OpReg-Boost (interp.) | |||

| As. err. | Time [s] | As. err. | Time interp. [s] | |

| 18.49 | 0.00243 | 18.49 | 0.06361 | |

| 18.49 | 0.00243 | 18.49 | 0.06340 | |

| 18.49 | 0.00243 | 18.49 | 0.06351 | |

| 15.38 | 0.00243 | 15.60 | 0.01839 | |

| 13.81 | 0.09569 | 90.60 | 0.00411 | |

| 203.60 | 0.02080 | 216.49 | 0.00368 | |

Appendix C Proofs of section 2

Proof of Lemma 2.1 We rewrite here Problem (7) for the reader ease,

| (29a) | |||

| (29b) | |||

| (29c) | |||

Let be the vector stacking all the , then problem (29) is equivalent to

| (30) |

where

| (31) |

with and the indicator function imposing (29b), and the indicator function imposing the “consensus” constraints (29c). The problem can then be solved using the Peaceman-Rachford splitting (PRS) (see e.g. [24]) characterized by the following updates :

| (32a) | |||

| (32b) | |||

| (32c) | |||

The proximal of corresponds to the projection onto the consensus space, and thus can be characterized simply by

| (33) |

Regarding the proximal of , is separable, in the sense that it can be written as

| (34) |

Therefore, the update (32a) can be performed by solving in parallel the problems

| (35) |

We remark that problems (35) are convex QCQPs in variables and with one constraint.

Proof of Lemma 2.2 The KKT conditions for (9) are

| (36a) | |||

| (36b) | |||

| (36c) | |||

| (36d) | |||

Solving (36a) for , we get

| (37) |

and we are left with the need for finding an expression for the Lagrange multiplier.

Assume now that , from (36c) this implies that we need to have and, using (37), this is equivalent to

This is quadratic equation in , with the larger solution being

finally, we impose (36b) to guarantee non-negativity of which yields

and the thesis is proven.

Proof of Lemma 2.3 By Lemma 2.1, at each iteration the PRS needs to solve the problems (8a), which are QCQPs in variables and with a single constraint. We can see that these problems are independent of each other, and so that they can be solved in parallel.

As proved in Lemma 2.2, QCQPs with one constraint admit a closed form solution, which has a computational complexity of . The remaining two steps of PRS then require only vectors sums, and are again .

To conclude, at each iteration the complexity is dominated by the need to solve 1-constraint QCQPs, and so overall we have a complexity of . In the particular case of , which is the typical scenario in practice, then this complexity reduces to .