Block Dense Weighted Networks

with Augmented Degree Correction

Abstract

Dense networks with weighted connections often exhibit a community like structure, where although most nodes are connected to each other, different patterns of edge weights may emerge depending on each node’s community membership. We propose a new framework for generating and estimating dense weighted networks with potentially different connectivity patterns across different communities. The proposed model relies on a particular class of functions which map individual node characteristics to the edges connecting those nodes, allowing for flexibility while requiring a small number of parameters relative to the number of edges. By leveraging the estimation techniques, we also develop a bootstrap methodology for generating new networks on the same set of vertices, which may be useful in circumstances where multiple data sets cannot be collected. Performance of these methods are analyzed in theory, simulations, and real data.

Keywords: Dense Networks; Weighted Networks; Degree Corrected Block Model; Bootstrap; Community Detection

1 Introduction

We are interested in modeling dense weighted networks with real, continuous-valued weights for pairs of nodes , , where denotes the set of all nodes (vertices) in the network. Denseness means that the edge is present for all pairs , where , though we will also discuss the case where a proportion of the weights are “missing.” Examples include structural brain networks (as in Figure 1) and correlation networks. Focusing on dense weighted networks, what are natural modeling approaches? At the simplest level, if a network has no meaningful structure, one could postulate that

| (1.1) |

where are i.i.d. random variables and is a function mapping to the (standard) “normal” space. One can take

| (1.2) |

where is the CDF of and is the inverse CDF of . In practice, we can substitute the empirical CDF for the unknown true .

Most networks of interest, including most real networks, however, have some kind of structure. Two common structures involve communities, broadly understood as sets of particular nodes whose edges exhibit similar connectivity patterns, and degree correction, broadly understood as certain nodes having consistently more edges (or, in dense weighted networks, greater edge weights) than other nodes. A simple way to capture degree correction, which we refer to as “sociability” (or SC, for short) in the “normal” space is to set

| (1.3) |

where and are i.i.d. variables, associated with nodes and respectively, and and are other model parameters. In the equivalent expression, are i.i.d. U random variables (uniform on the interval ), and the function will be allowed to take more general forms below. In the “normal” space, the function is linear. In the case where , a larger value of will tend to make values larger across all ’s, inducing a sociability structure that reflects degree correction. The term in (1) is thus the SC term in the model. The term is thought to consist of independent variables.

Models of the type (1) appear in Fosdick and Hoff (2015), who also include a multiplicative interaction term. In a departure from that work, we allow for community structures and more general functions than (1). After exponentiation, and at the conditional mean level, note also that (1) yields

| (1.4) |

Specifications of the form (1.4) are common for connection probabilities in unweighted degree corrected or SC models. See degree corrected stochastic block models (DCBMs) in Karrer and Newman (2011), Gao et al. (2018), or their extensions, popularity adjusted stochastic block models (PABMs) in Sengupta and Chen (2017), Noroozi et al. (2021). While in the DCBM, “sociability” parameters are global, in the PABM, each node has a possibly different sociability parameter for each community in the network. The models considered here are close in spirit to PABMs and we draw from the techniques in Noroozi et al. (2021) to analyze them. However, our focus is on weighted networks where information may be encoded in the patterns of the edge weights rather than the existence of particular edges in a given network. We shall thus also consider community versions of the model (1), where the function and the parameter can depend on the pair of communities to which and belong. Importantly, according to this definition, communities are not necessarily defined by higher or lower propensities to connect with entire other communities, but rather by particular patterns of edge weights which represent “preferences” for specific nodes over others within the same community.

As noted above, we will go beyond the “linear” sociability patterns encoded by the particular function shown in (1) while, perhaps surprisingly, remaining in the “normal” space. To motivate this extension, instead write the SC term in (1) as

| (1.5) |

where and with . and modulate the influence of relative to . The constant serves a normalizing role so that is ensured to be U, and hence the value of resides in the “normal” space with variance . Plugging (1.5) into the last term of (1) and constraining ensures the resulting values of are in the (standard) “normal” space.

The critical observation, though, is that plugging (1.5) into (1) while constraining will output values in the (standard) “normal” space for any function where U, including functions that bear no similarity to the normal distribution as shown beneath (1.5). We shall consider several broad classes of such -functions. Examples of the sociability patterns resulting from various considered -functions are depicted in Figure 2 below. The key point is that while could be associated with quite different SC patterns, the SC term (1.5) would nonetheless reside in the “normal” space. Used in conjunction with (1.2), which transforms an arbitrary (and possibly nonparametric) distribution of edge weights, this constructs a map between values and edge weights via the (standard) “normal” space. In summary, our key contributions at the model level concern:

-

•

Focus on dense weighted networks;

-

•

Possibility of community structure;

-

•

Multiple nearly arbitrary distributions of edge weights;

-

•

Flexible sociability patterns through -functions.

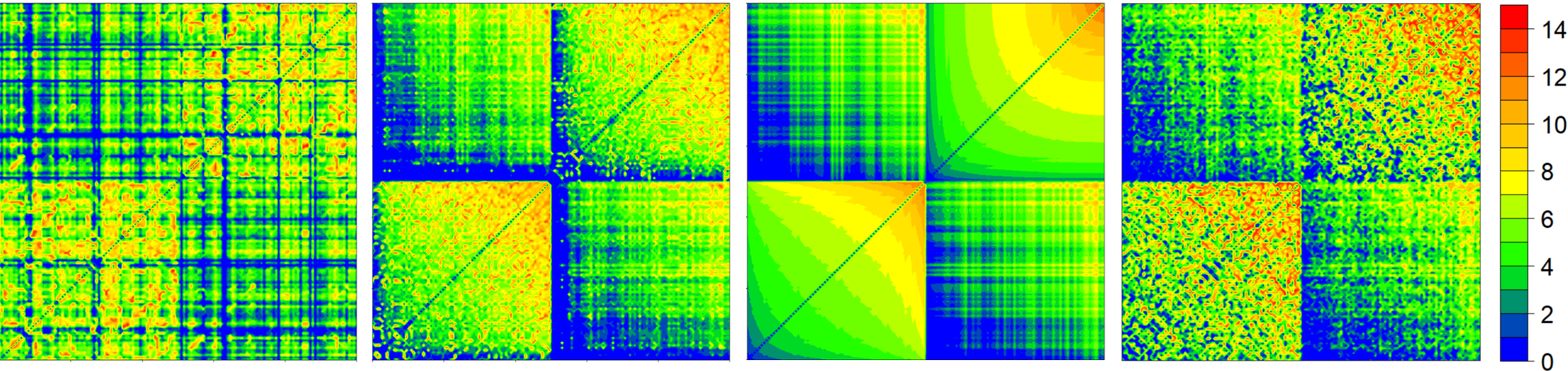

Modeling questions will also be addressed in the paper below. Figure 1 illustrates our modeling approach. It shows a network where the edge weights are the logs of the white matter fiber counts connecting two regions in a patient’s brain. In this case, the two assumed communities are the left and right hemispheres of the brain. We often reorder the nodes first by community, and then within each community, sort the nodes by within community degree. This is what’s seen in the second plot from the left of Figure 1. There are instances where one might want to sort the nodes differently, for example, if there is a core-periphery structure, it might be preferable to sort nodes first by community then by weight of edges connected to nodes in the core. In the third plot from the left, we show an “estimate” of the SC term from our method, with the same ordering as in the second plot. Finally, a bootstrap replicate network of the original network is displayed in the right plot, again reordered for easier viewing. Notably, based on the different contour shapes in the bottom left and the top right sections of the third plot, it can be seen (using the plots in Figure 2 as a point of reference) that the intra-left hemisphere edges have a different best fitting -function than the intra-right hemisphere edges.

There are other models designed to generate weighted networks. The Weighted Stochastic Block Model introduced by Aicher et al. (2013) includes degree correction only with regard to an edge’s existence, not for modeling the weights of particular edges. The generalized exponential random graph model from Desmarais and Cranmer (2012) is indeed a very general model, but requires a lot of advanced knowledge to specify the appropriate model for estimation if given a specific network. As noted above, Fosdick and Hoff (2015) includes a form that looks superficially like the linear models discussed in this paper, but the higher order dynamics described when incorporating multiplicative interaction effects bears little resemblance to the “non-linear” models presented here, and doesn’t accomodate communities. Peixoto (2018) looks for general forms of community structure, but not of the kind proposed here, as their edge weights depend only on community membership without regard for other nodal features. For other work on weighted networks, see the melding of of mutual information and common neighbors in Zhu and Xia (2016), estimates of nodes’ perceptions of one another to predict signed edge weights in Kumar et al. (2016), and leveraging graph metrics to “denoise” weighted networks in Spyrou and Escudero (2018). Related work in the unweighted setting can be found in Bartlett (2017), which deploys pairwise measures of node association to model binary edges, and the use of copulas in Fan et al. (2016).

As seen in Figure 1, for a given network, we can use our model to estimate a data generating process and subsequently generate synthetic data via a bootstrap-type method. This procedure can create “new” networks which replicate the structure of the observed network even without a priori knowing the functional form of the edge weight generating process between particular communities. As in the case of using brain networks as a diagnostic aid, when networks are used as inputs to other analyses, if data collection is difficult, these synthetic network replicates may be used as supplemental data. Additionally, taking a cue from the rightmost plot of Figure 1, the random variation between bootstrap replicate networks can serve as a sensitivity test for results using the original network, allowing for greater robustness even with limited data, as in the classical bootstrap.

The rest of this paper is structured as follows. In Section 2, we develop theory for generating the proposed class of networks, along with details on -functions in Section 3. In Section 4, we discuss methods for estimating the generating processes of observed networks when the community memberships of each node are known or have been estimated. In Section 5, we build on the estimation procedures from Section 4 to generate new synthetic networks that are plausible stand-ins for real networks, in the vein of the bootstrap. In Section 6, we discuss how to adapt community detection techniques to networks of this kind. In Section 7, we discuss applying our methods under slight departures from the main models of interest. In Section 8, we apply our method to real data and compare the performance to other existing models. The appendix discusses technical details and extensions.

2 Model formulation

Let be the vertices (nodes) in a dense network with undirected and weighted edges, and no self-loops. Each node belongs to exactly one community, . Henceforth, and will refer to nodes, and and will refer to communities, e.g. .

In our random graph model, a node has a “sociability” (i.e. “popularity”, degree correction) parameter . These parameters are assumed to be i.i.d. U. Let denote the weight of the edge connecting nodes and . We primarily focus on the case with continuous-valued . At the most general level, we examine random graphs of the following form: for such that , , suppose

| (2.1) |

where is a monotonically increasing function over the range of , is a monotonic function in its 2 arguments, are error terms with , and . Those terms with subscripts are particular to edges where one of the nodes is in community and the other is in community , while terms with subscripts are idiosyncratic for that particular edge. In the most flexible version of the model, as in the PABM, each node may have different values, each one for parametrizing edge weights connecting to nodes in a particular community. A special case of interest is the linear model

| (2.2) |

where , , and for and U. We refer to (2.2) as a linear sociability model (LSM) and to (2.1) where is not linear as a nonlinear sociability model (NSM). Examples and discussion below will provide motivation and intuition about these models.

Under monotonicity assumptions, note that the observed edge weight is monotone in the sociability parameters of nodes and . As a special case, letting in the LSM, node sociability plays no role in the weight of the edge between nodes and , rather the weights are generated independently from some distribution, as in a Weighted Stochastic Block Model. Similarly, letting would generate a network completely determined by random node sociabilities.

In what follows, will denote the CDF of a distribution and . Furthermore, though each pair of communities and are assumed to possibly be connected via a function (along with , etc.), to simplify notation, we will drop the subscript in our notation, assuming that the discussion always concerns the relevant pair of communities based on context, where may or may not be the same as .

Example 2.1

(Normal LSM.) This is (2.2) with

| (2.3) |

where . The function can be the identity (in which case is Gaussian itself, assuming normality of ) or some other transformation, such as .

One natural choice of in (2.1) or (2.2), after a common practice of transforming data to standard normal, is to consider

| (2.4) |

where represents the CDF of . We pursue this case in the following canonical example that we use for NSMs. The example relies upon H-functions, a concept that will be discussed in greater detail in Section 3.

Example 2.2

(-Normal NSM.) This is (2.1) with

| (2.5) |

where is again the CDF of , are i.i.d. , and . Furthermore, is an -function having the following key properties (see Section 3 for more details): U for independent U random variables , and is monotone in both arguments. The first property ensures that

| (2.6) |

are variables, and hence by inverting (2.5), the variables

| (2.7) |

indeed have as their CDF.

Note that the -Normal NSM also has the Normal LSM as a special case. Using the -function

| (2.8) |

one observes that U since , and hence . With the choice (2.8) plugged into (2.5), the latter model becomes

| (2.9) |

by using the identities and . Note that (2.9) is a normalized version of the Normal LSM (1) where is set to 0. Examples of -functions which do not correspond to Normal LSM will be given in Section 3. NSMs are a large class, but some other potentially interesting examples can be constructed in a similar manner to the -Normal NSM above, as is detailed in the technical appendix.

While -Normal NSMs indeed take advantage of many features of the normal distribution, they are actually not very restrictive. Instead of representing the CDF of a linear combination of normal random variables as in (2.8), the -function in (2.5) can represent the CDF of some other weighted combination of random variables, in which case the underlying “shape” of the connections between communities and will look very different, as can be seen in Figure 2. This paper will focus on -Normal NSMs because all -Normal NSMs incorporate normally distributed errors.

Finally, we introduce a bit more terminology. In the LSM (2.2), we distinguish the following cases with specific terms:

-

•

, : positive association,

-

•

, : negative association,

-

•

: Simpson association,

-

•

, : projection onto 1st coordinate,

-

•

, : projection onto 2nd coordinate.

3 -functions

We begin by introducing some terminology.

Definition 3.1

(Positive association.) A function is an -function with positive association if:

-

1.

is non-decreasing in both arguments;

-

2.

, for all .

The term “positive association” refers to the fact that, when considered across communities, such models would tend to produce larger weights for nodes in the two communities with simultaneously larger sociabilities. The monotonicity condition 1 captures the idea of node sociability as discussed above. Condition 2 is equivalent to requiring that is a U random variable. In contrast with copulas, the output of a positively associated -function is not bounded above by the minimum of the inputs.

Definition 3.2

(Negative association; Simpson association.) A function is an -function with negative association if is an -function with positive association. A function is an -function with Simpson association if or is an -function with positive association.

If is a uniform random variable, then is also a uniform random variable, so negative association also ensures that is a uniform random variable. A similar observation can be made for Simpson association. The term “negative association” arises because the monotonicity of results in the fact that, when looking across the communities, nodes with greater node sociabilities actually tend to have smaller edge weights. Simpson associations are so named because they indicate a localized area where certain broader trends of the network may be inverted. This error at the local level when extrapolating from global phenomena is reminiscent of Simpson’s paradox.

A property shared by all -functions is that is a U random variable for such independent random variables . There are many ways to achieve this, but one quite general construction which we found to be flexible and interesting is as follows. Note that a random variable has the CDF for a U random variable . Take now two CDFs and let be their convolution CDF. Then has the same distribution as . This suggests setting

| (3.1) |

By construction, this function satisfies the condition 2 of Definition 3.1, but one can easily check that condition 1 holds as well. The function (2.8) is an example of -function in the form of (3.1) with an explicit convolution . Besides the normal distributions, choosing and to be exponential, Cauchy, or uniform would also give an explicit form for , although (3.1) is far more general than these simple cases imply.

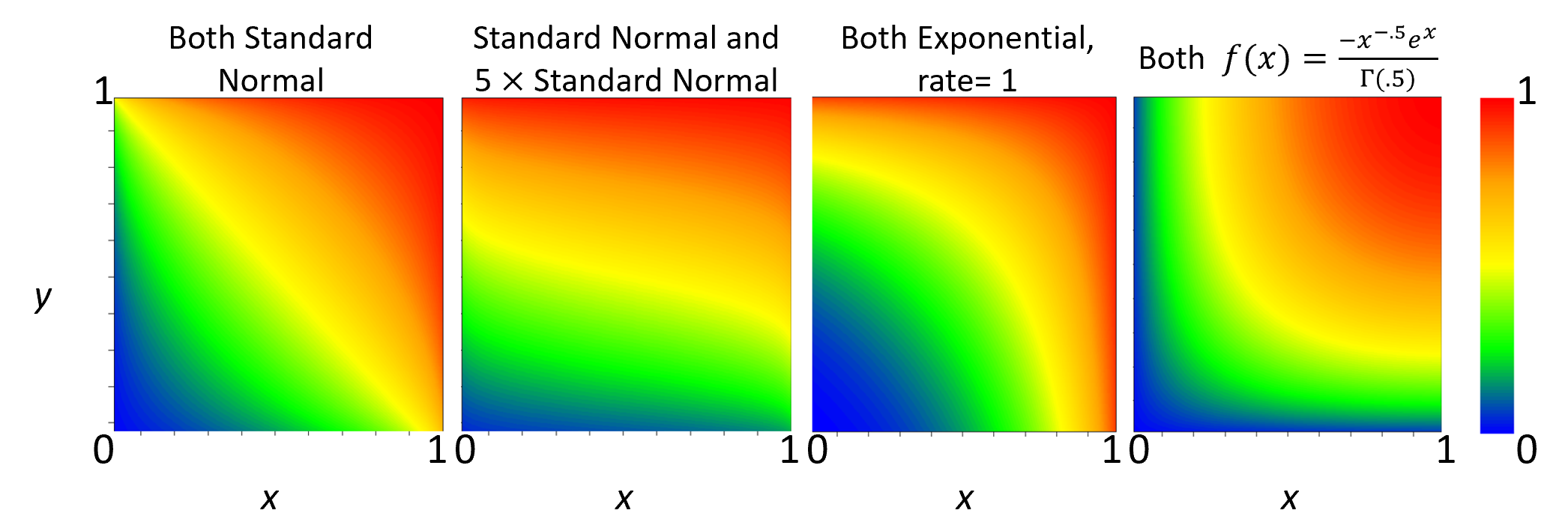

Figure 2 illustrates some of the different kinds of contours that can be created using -functions of the form in (3.1). The resulting weighted bipartite subnetworks between 2 different communities generated using these -functions in -Normal NSM (2.5) would inherit similar connectivity patterns, albeit with normally distributed “errors” included. In this case, the x and y axes represent the values of and , respectively, each running from .01 to .99 by increments of .01, and the colors represent the output of the -function. From left to right, the first plot shows the values of where . The second plot corresponds to this function with . The third plot depicts (3.1) where and are both exponential distributions with a rate parameter 1, and is a gamma distribution with shape parameter of 2 and rate parameter of 1. Finally, the rightmost plot is from the -function (3.1) where and have density

In this case, can be checked to be given by

These different images show that -functions (3.1) make a rather flexible class. Other -functions include maps to the first or second coordinates, which would give perfectly vertical or horizontal contours.

4 Estimation with known communities

In this section, we discuss estimation of the different models discussed in Section 2, while assuming that the true community labels of the nodes in the network are known. As far as estimation goes, we do not impose that each node’s estimated value is constant globally, but rather only constant over each community. It may be desirable in future work to align these estimates over the whole network, but the presented estimation processes are more flexible. Even using this assumption, the model parameters to be estimated depend on the specific model in question. Given a particular set of community labels, we can treat each subnetwork of the larger network – where we analyze the connectivity patterns between 2 different communities and – as a bipartite graph, and any subnetwork where we look at the connectivity within a single community as a smaller network.

4.1 Estimation for Normal LSM

We assume henceforth that and are fixed and work on one smaller subnetwork. It is assumed that the transformation in (2.1) has already been performed, so without loss of generality, . We also assume for simplicity that . Then, the model (2.1) can be expressed after exponentiation as

| (4.1) |

where the last term within the parentheses has an expected value of 1. The structure of (4.1) enables the use of rank-one Nonnegative Matrix Factorization (NMF) to estimate the parameters of interest. NMF approximates the matrix represented by as the decomposition where and are column vectors with positive entries. Taking the log of this approximation yields the approximate identity

| (4.2) |

which suggests the following estimators for the model parameters of interest:

-

= SD, = SD,

-

, , , ,

where SD stands for the standard deviation, and indicates the sample mean of . In light of (2.1), we also set = SD. An adjustment for subnetworks where all nodes are in the same community is given in Appendix LABEL:sa:repeats.

A concentration inequality for a Normal LSM bounding the difference between the best possible estimates of the network’s SC to the true generating SC process without any “error” included is given in Appendix A.

4.2 Extension to LSM

The difference between (2.1) and (2.2), ignoring extra subscripts, is that rather than having standard normal random variables ascribed to each node, (2.2) includes random variables and with possibly different forms, albeit with identical first 2 moments. The procedure described in Section 4.1 will still apply with one exception. The relation (4.2) cannot directly estimate or , but rather and . After getting these estimates, a distribution can be fit to the data points while assuming that and are truly distributed uniformly over the unit interval. The best fitting distribution can then be inverted to estimate and . Finally, the parameter is estimated to be the standard deviation of .

4.3 Estimation for -Normal NSM

Though using NMF is appropriate when the function in (2.1) is linear, it is unsuitable for nonlinear functions, which require an alternative methodology. For an estimator of , by the construction of the graph in the -Normal NSM (2.5), one could naturally set the empirical CDF of the weights . We make a small modification to this and instead set

| (4.3) |

where is the number of edges . That is, we divide by in (4.3) instead of . There are two reasons for this. First, note that the model in (2.5) implies a distorted but generally linear relationship between and . We shall use this relation to estimate the function , and at the empirical level, shall consider in place of . Dividing by ensures that , so is finite. Second, modulo any dependence issues, if one thinks of (an appropriate scaling of) as representing the order statistics of uniform random variables on (0,1), recall that the th order statistic follows a Beta distribution, which has a mean of . At the mean level, it is then natural to place at multiples of , not . In fact, we use one other modification to the definition (4.3) when the values repeat, which can be found in Appendix LABEL:sa:repeats.

For node sociabilities , we define them locally based on two communities and (and possibly so there is only one community). For node , consider

| (4.4) |

We think of as a “local sociability statistic” of , since it looks at how connects to one community , rather than the whole network. By the construction of the NSM model (2.5) and the properties of positively associated -functions, if is positively associated, one expects the ordering of the local sociability statistics ’s of those nodes in community to match the ordering of the sociabilities . This suggests setting

| (4.5) |

where is the number of . That is, defining as the rescaled ordering of the “local sociability statistic” of in its community with respect to community . As in (4.3), note the division by in (4.5), placing the values at the expected values of the order statistics of draws from a U distribution. When the association of is negative, we expect the ordering of these local sociability statistics to have a strong negative correlation with the true values. In other words, if the true has negative association, we expect the ordering of the local sociability statistics ’s of those nodes in community to match the ordering of . The estimation of described next will therefore adapt automatically to any form of the association of .

We view the estimation of as choosing the best candidate from a set of -functions. This set can be parametric (e.g. parametrized by in (2.8)) or consist of several -functions. More precisely, we set:

| (4.6) |

The optimization in (4.6) is carried out numerically over different functional forms of , and the associated minimizing choice of is taken as the estimated .

4.4 Estimated network sociability

There may be a desire to examine the SC of the network implied by the parameter estimates. In this case, the “estimated edge values” are given by

| (4.7) |

These estimates seek to smooth out the effects of any “errors” observed over particular edges in the original network. As grows, shrinks to 0, so the estimate tends toward the median edge weight in the subnetwork. If a subnetwork has a large estimated value, the range of the estimated subnetwork will be much smaller than the range of the observed subnetwork. By contrast, bootstrap replicates of the kind described in Section 5 below are expected to have the same variance structure as the original network.

4.5 Spurious patterns

Note that the -Normal NSM (2.5) allows for the independent edges only in the limit . In practice, even when only independent edges are present, a finite value of will be estimated, and a spurious sociability pattern will be “found.” (This is discussed in connection with Figure 4 below). This scenario could be flagged by examining suitable MSEs.

Using results of (4.6), the MSE in “normal” space is defined as

| (4.8) |

where represents the number of edges connecting nodes in to nodes in . If , then by construction, MSE 1. With no upper bound on , in practice we expect the MSE for independent edges to be slightly smaller than 1. We can compare the observed MSE of a subnetwork to the MSE values we get when edge weights really are generated as independent .

Where overfitting is suspected in a particular subnetwork, we can draw completely random edge weights and create a fictional subnetwork of the same size as the observed subnetwork. From there, we repeat the estimation process to calculate the MSE from this synthetic subnetwork, with the additional restriction that, using the terminology of (3.1), and of the estimated -function for the fictitious subnetwork must be of the same distributional family as the and in the estimated for the real data. We can generate many fictitious subnetworks, and if the MSE obtained from the true subnetwork is smaller than some large proportion of the fictional MSE values, the estimates from (4.7) should be retained. Otherwise, we replace all estimated edge weights in the subnetwork with the median edge weight in the subnetwork.

5 Bootstrap

In certain cases, such as brain scans, it can be difficult to obtain multiple measurements of the same network where the underlying structure broadly remains the same, but there may be some variation at the level of particular edges. For this reason, we want a procedure which can generate new networks that can mimic the structure of real networks, much the same way the classical bootstrap can be used to generate new samples from a single sample. In Section 4, we estimated a network using -functions. In this section, we extend our construction to generate new network samples that still allow for both flexible connectivity patterns between communities as well as node specific degree correction effects.

Assuming the community assignments are correct, pairwise functions and parameters are estimated based on the estimated sociabilities . To get a bootstrapped edge weight, we can draw a new in (2.5) and set

| (5.1) |

When the true is small, can be estimated to be 0. However, for the purposes of the bootstrap, it is useful to include randomness; otherwise each bootstrap replicate network will be identical. In the case where (a small positive value), we can replace in (5.1) with the MSE given by (4.8).

If, after performing the procedure described in Section 4.5, we believe there is no relationship between edge weights and their incident nodes, for each bootstrap replicate, we instead draw every edge at random with replacement from the relevant edge set. In that case

6 Community detection

Estimates above depend on assigning each node into its community. In this work, community is defined as a subset of nodes which all share a common , and for each particular corresponding community , as given in (2.1). As nodes in the same community share functions to generate edge weights, patterns in edge weights can be used to cluster nodes into communities. As estimating requires defining the estimated node set in each community, perhaps surprisingly, the clustering techniques discussed in this section do not depend on , but instead rely upon a measure of cluster goodness.

6.1 Measure accounting for sociability

Letting and fixing any two communities and , for any model discussed in Section 2, with , , if , then so too is . Nodes in the same community share an “order of preferences” over nodes in another particular community , as reflected by persistently greater edge weights. Even allowing for positive , a good clustering for these models should reflect a relatively consistent order of preferences. Since this order of preferences over nodes in is expected for all nodes in community, the local degree of each node in community with respect to community ,

should also display this ordering. For example, in any plot in Figure 2, comparing any set of columns, the rightmost column (representing the node with the larger value) never has a smaller edge weight value than the corresponding location in the left column. That is, if , then . For each node and each community , we can then define a node-community correlation as

For a good clustering with estimated communities , fixing any node and looking at all nodes , the edge weights should be correlated with . A good estimated clustering should result in large, positive values everywhere. Even so, when , even nodes in the same community may exhibit minor variation in preferences over nodes in community . Additionally, we could ensure perfect correlation between a node’s edge weights and its community’s preferences if we made that node its own community, but that would be overly prescriptive. While individual values may be useful for diagnosing localized issues, in a larger network, it is preferable to aggregate these values to get a system-wide overview of clustering success. For a particular assignment of communities, we define our measure as:

| (6.1) |

where is the total number of estimated communities in the network, and is the number of nodes in community . The average and standard deviation of in (6.1) are over .

Nodes placed in the same community should exhibit a shared ordering of preferences over nodes in any other community, represented by the average of the values. In addition to rewarding clusterings that show consistent ordering of preferences, the measure also prefers clusterings with less variation in values for a fixed and , which can reflect a shared value. By multiplying by , there are increasing returns to scale in the size of communities. Without increasing returns to scale, nodes could be clustered into many dyads or triads, all producing consistently large absolute values, but this clustering would lead to overfitting. Under , communities of size one or two are worthless. Finally, within community subnetwork performance is counted twice to balance the influence of all subnetworks. Consider a network with 2 communities of 52 nodes each. Without this doubling, the two within community subnetworks would each have a maximum possible contribution of 2500 to the measure, while the between community subnetwork would have a maximum possible contribution of 5000.

The measure tries to find the appropriate balance between size and homogeneity of the estimated communities. Increasing returns to scale are crucial because they induce larger communities, even if they contain some nodes with minor deviations from the community’s collective ordering of preferences. However, if multiple nodes have preferences at odds with the rest of their assigned community, it would become beneficial to separate this set of crosscutting nodes into their own splinter community to improve the totality of the measure. Of course, just as modularity may not be ideal for community detection in every network model, in cases where node sociabilities do not matter (akin to a standard SBM), this measure will not be effective at recovering the true communities.

It’s worth noting here that absence of an ordering of preferences can also be a valid shared ordering of preferences. In the simplest case, all weights between communities and can be identical, or they can all be generated as i.i.d. random variables. This still may be useful for clustering. For example, if communities and have identical functions to generate both within community and between community edges, it may be inappropriate to call them two different communities. However if the edges between and a third community are generated completely at random, but the generating process of edges between and has some kind of association, that should distinguish nodes in community from nodes in community .

In Appendices LABEL:s:greedy-alg and LABEL:s:spectral-alg, we present 2 community detection algorithms which try to maximize the measure . One is stochastic, while the other is bottom-up and deterministic. Experimentally, there have been occasions where each algorithm outperforms the other. Unless otherwise noted, community estimates presented in figures in this paper are the maximizing clustering given by one of these algorithms.

7 Robustness of estimation procedure

The estimation pipeline described above is tailor made for the dense weighted networks described in Section 2. However, the procedure still appears to succeed for related networks which are not explicitly NSMs or LSMs.

7.1 Sparser networks

While the discussion so far has centered on dense networks, in this section, we propose an extension where many edges may be missing, and there are two layers to the generative model. In this instance, it is necessary to distinguish between the adjacency network, which is the set of present edges, and the set of weights of those edges. In principle, the set of communities in the adjacency network could be different than the set of communities in the weights, but we only consider the case where they are the same. However, we do allow potentially different sets of sociability parameters. To generate a network with missing edges, we can use existing models such as the SBM, DCBM, or PABM to generate the adjacency network. To generate the edge weights, first we generate a dense weighted network as in this paper, then take the Hadamard product of the adjacency network matrix and the dense weighted network.

Moving from generation to estimation, we can extract the adjacency network of an observed network by replacing any non-zero weights with 1, then use established community detection and estimation methods to cluster the nodes and estimate the probability of an edge’s presence. With these estimated community memberships, we can iteratively use a modified version of the estimation method described in Section 4 to estimate the generative process for the edge weights, as shown in Algorithm 1. First, we estimate the model on the observed network while ignoring missing (zero valued) edges. Then, we replace any missing edges in the original network with the estimates from our model. We then re-estimate the model based on this updated network, and continue to update those edges which were missing in the original network. This iteration is useful because a node with larger edge weights could, by chance, have many missing edges, which would deflate its estimated value. With multiple iterations, those missing values should be replaced by better and better estimates, which should hopefully mitigate the impact of these missing values on our estimate of the edge weight generating process. This progression has been observed in simulations, and the performance of Algorithm 1 is discussed in Section 8.3.

After this estimation process completes, we can move back from estimation to generation. The upshot of this entire process is that given one weighted network with missing edges, we can estimate both the adjacency network generating process and the edge weight generating process. This information can serve to generate new weighted networks with missing edges, using (5.1) to get a synthetic edge weight network, and using the estimated SBM-type parameters based on the observed adjacency network to generate a synthetic adjacency network. Finally, take the Hadamard product of these two matrices to generate a synthetic network where the distributions for each edge weight match the estimated distribution in the original network, including treating 0 as a missing edge.

7.2 Noisy edge weights

Our estimation method appears to work even when a dense network is not generated as an -Normal NSM. Rearranging (2.5),

If is a distribution with a maximum, that means no edge weight can exceed that maximum. However, if we include another term into

then, if , each edge weight is distributed over . As can be seen in Appendix LABEL:s:noisyedgesim, the estimation procedure still captures the underlying network dynamics in this case, although the estimates degrade as increases.

8 Simulations

For each simulation, we include a description and a figure showing the original network and the estimated underlying network, where the clustering choice is the estimated measure maximizing clustering using the algorithms presented in Appendix LABEL:a:comm-det2.

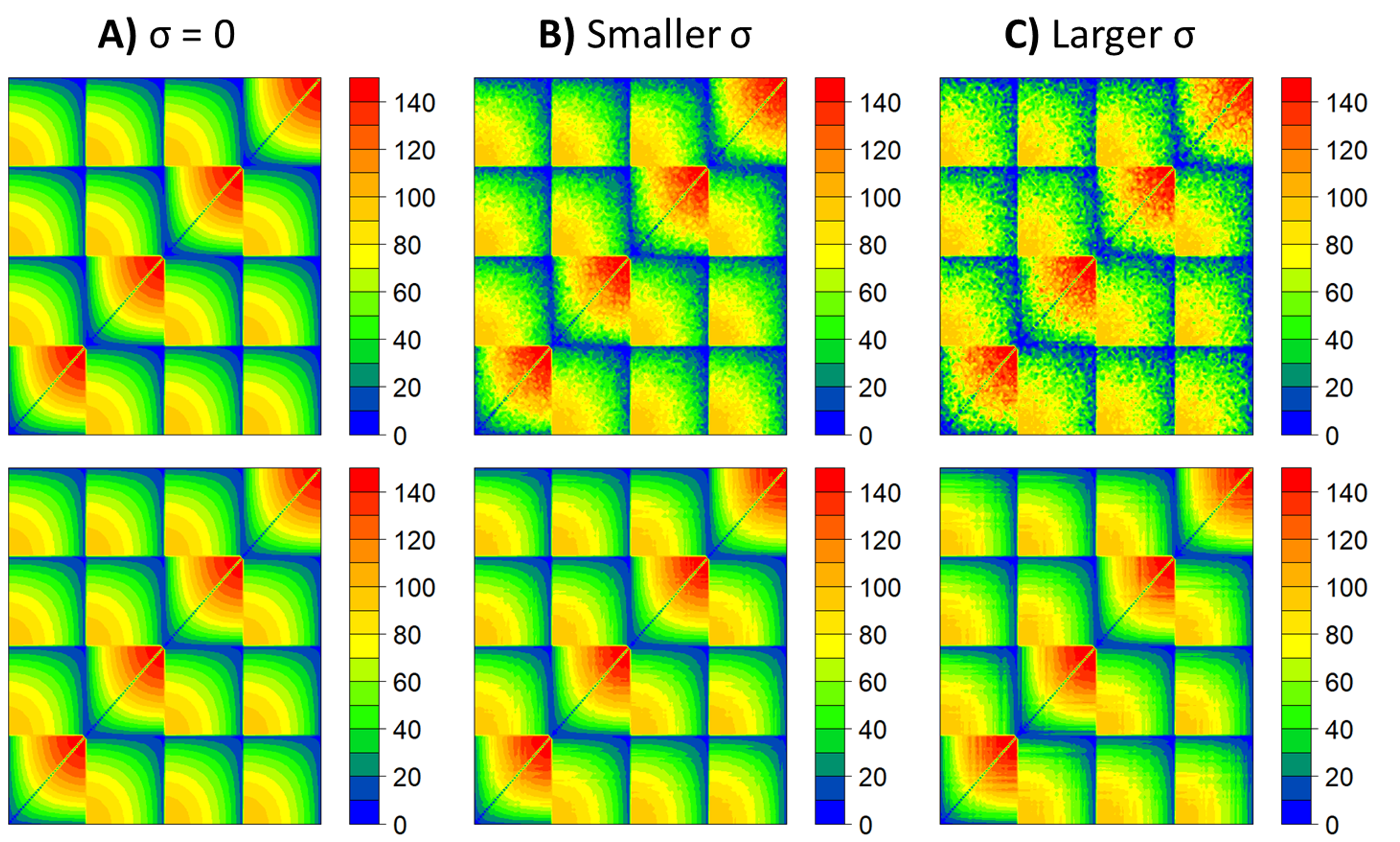

8.1 Varying

Figure 3 depicts variations on and estimates of an underlying network with 4 communities of 37 nodes each. In plot A, the network is displayed with . Within community edges are drawn from a uniform distribution with a maximum of 150, while between community edges are drawn from a uniform distribution with a maximum of 100. Node sociability parameters for both communities range from .05 to .95 in increments of .025. The -function is the same as that used for the rightmost plot in Figure 2, though since the between community edges have negative association, the inputs to that -function are and . This network is ordered so one can visually discern communities and connectivity patterns. Even so, the first step is to estimate community structure, as node ordering does not impact the community detection algorithm. The resulting estimated network is shown below the original and looks very similar to the original network.

Where plot A uses (2.5) with , plot B uses everywhere, leaving the network looking smudged. The estimate looks like a smoothed version of the actual observed network, albeit somewhat “blurrier” than the underlying network seen in plot A. This performance degradation with increasing is to be expected. In plot C, for within community edges, and for between community edges, and the estimate looks slightly worse than in plot B.

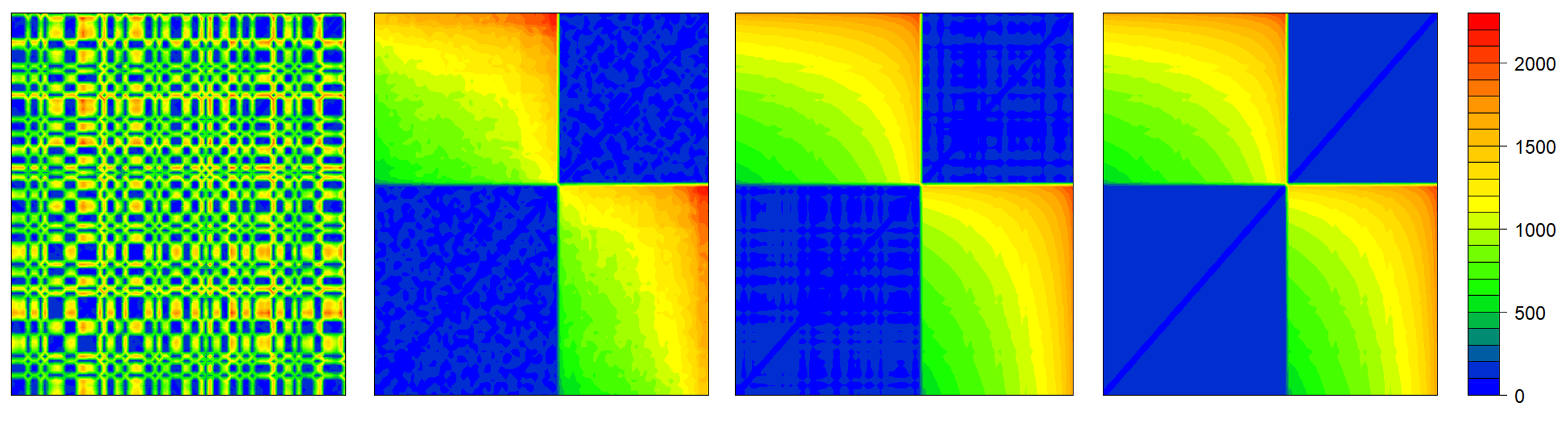

8.2 Disassortative network with spurious patterns

Figure 4 introduces several changes. First, the communities are disassortative, as between community edges are larger than within community edges. Second, the within community edge weights are i.i.d. Third, the between community edge weights are generated using randomly generated Gamma parameters for each node, and using those as inputs into a negative binomial distribution. This is not generated as an -Normal NSM, yet we still use our estimation procedure. Fourth, the nodes are not ordered. If the true community orderings are not known a priori, a network may look like the left plot of Figure 4. Following estimation, the communities are clustered correctly, and the between community estimate broadly looks smoother than the original network. The initial estimated network appears to amplify spurious structure in the within community edges, giving some order to the pure randomness seen in the original network. Utilizing the procedure discussed in Section 4.5, within community edges for subnetworks with spurious patterns are replaced by the median value of that subnetwork’s edge weights.

8.3 Missing edges

Figure 5 shows the network in Figure 3 after deleting many edges at random, along with the final estimated networks using the procedure discussed in Section 7.1. The communities are estimated for the network with 20% of the edges missing, but are assumed to be known for the network with 75% of edges missing. Even accounting for this, as one might expect, the reconstruction is more successful with fewer missing edges.

9 Applications

In this section, we show how the methods described in this paper work on real data where the ground truth clusterings are unknown. In this case, we will show the original network, the network reordered by community then within community degree, and then show the estimated network.

9.1 Brain networks

Figure 1, which has already been discussed in Section 1, shows a preprocessed DTI scan from the ADNI database (http://adni.loni.usc.edu). As in Leinwand et al. (2020), for this scan, the cortical surface has been parcellated into the 148 regions of the Destrieux Atlas using FreeSurfer on the T1-weighted MRI scan. Then probabilistic fiber tractography was applied on DWI and T1-weighted images using FSL software library to obtain a 148 148 matrix. Each entry in the matrix is the log of the count of white matter fibers connecting two brain regions.

In contrast to the structural brain network discussed above, Figures 6 and 7 show the functional brain networks of subject IDs 293 and 108 from Brown et al. (2012), two pre-processed fMRI scans from the ADHD-200 sample. Both networks come from females, where one is age 10.73 and typically developing, and the other is age 10.81 with ADHD. Both are processed using the Athena pipeline resulting in 190 regions. More details about preprocessing can be found at http://umcd.humanconnectomeproject.org.

The most obvious difference between the results is the ADHD network is split into 4 communities, while the typical network breaks into 5 communities. Looking at the typical network, we see clearer negative associations between communities than in the ADHD network, particularly accounting for the slightly different axes. The estimate of both networks shows some “plaid” looking patterns, as opposed to colors monotonically changing in one direction, which indicates the ordering of values within communities may not be the same as the ordering of values between communities. More defined communities and greater negative association patterns in the typical scan would appear to support the hypothesis that ADHD subjects exhibit less modular brain organizations than typical subjects.

Figure 8 shows the control network rearranged and estimated based on WSBM community detection, using the Matlab package accompanying Aicher et al. (2013) and Aicher et al. (2015). Our model does require prespecification of the number of communities nor the distribution of edge weights within or between communities, but for the sake of comparison, we instruct their package to mimic the structure of our results as best as possible, segmenting the network into 5 communities, ignoring the edge distribution, and assuming the weight distribution is Normal. WSBM appears to cluster nodes such that the induced subnetworks have edge weights confined to a relatively narrow band of values, which gives the impression of more solid colors and fewer gradients in the rearranged matrix. It also produces relatively evenly sized clusters. Using an maximizing algorithm, on the other hand, produces a larger community containing almost half of the nodes. The maximizing communities produce a measure value of 6580 compared to 3276 for the WSBM communities. Implementing the estimation methods from Section 4, the mean squared error of the final estimated matrix in Figure 7 is .024 compared to .033 if using the WSBM estimates. The WSBM communities also yield larger values. This provides evidence that the community detection using the measure is capturing something different than WSBM community detection, and likely a signal more suitable for the estimation methods described in this paper. Further experimentation has shown that WSBM community detection of plot A in Figure 3 does not match the intuitive visual clustering. Functional brain networks may not be organized according to an NSM or LSM, but the presence of detectable negative associations merits further investigation.

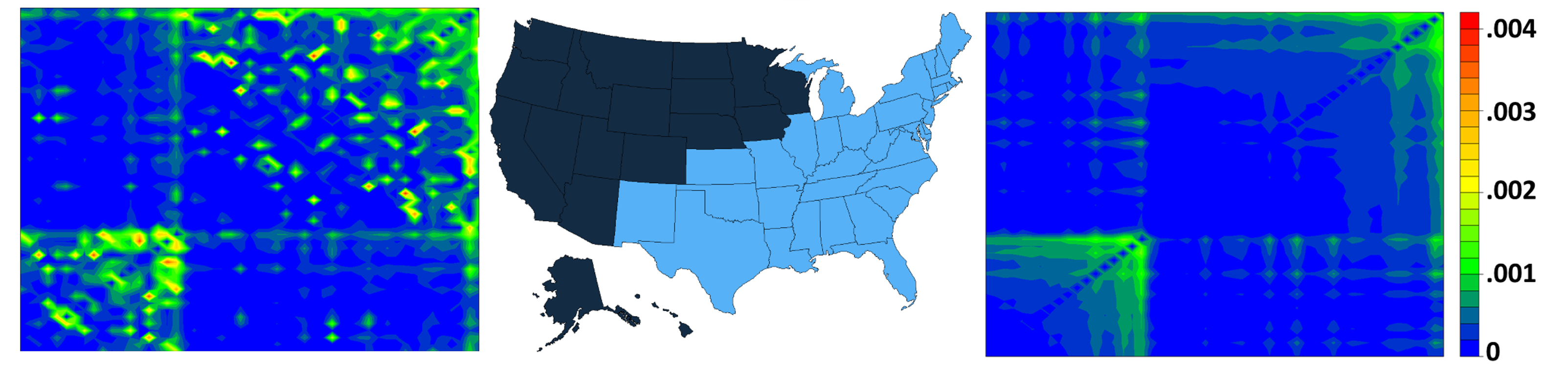

9.2 State to state migration “affinity”

Taking the state-to-state migration flows data from the 2017 American Community Survey 1-Year Estimates and dividing each cell in that table by the outgoing state’s total outflows gives a transition probability matrix for those people who left their state in 2017. For the network shown in Figure 9, this transition probability matrix is added to its transpose to get a symmetric matrix. This final network ignores the direction of greater inflows or outflows, but instead represents the “affinity” between the two states in question. The results show geographic communities which appear to give a reasonable segmentation based on geography. The estimated network displays positively associated within community dynamics, indicating both homophily and degree correction. However, the within community estimates are relatively large for this network, so these estimates have a relatively narrow range. This may be due to small subnetwork size, but also because some of the largest values lie in the interior of the subnetworks, rather than on the frontier.

10 Conclusions

We have introduced new models for dense weighted networks, wherein edge weights depend on node sociabilities and community memberships. The development of these models spurred estimation techniques for networks of this kind. With minor modifications, these estimation techniques appear to be applicable to an even broader class of networks than those introduced in this paper. Furthermore, one can use the results from (4.8) as a gauge of whether the described estimation process is appropriate for a particular network.

One potential consideration for future work is determining whether values should be estimated at the global or local level. In a case where each node’s value is globally consistent, estimating it across the whole network would be preferred to estimating several local estimates. However, given potentially different -functions across different subnetworks, pooling this information is not necessarily straightforward. Similarly, a different kind of information pooling may also play an important role for modeling the dynamics of a given network observed repeatedly over time. The introduced models may also lend themselves to extensions for more generalized forms of graphs such as multilayer networks or – following up on Appendix LABEL:s:Hext – hypergraphs.

References

- (1)

- Aicher et al. (2013) Aicher, C., Jacobs, A. Z. and Clauset, A. (2013), ‘Adapting the stochastic block model to edge-weighted networks’, ICML Workshop on Structured Learning .

- Aicher et al. (2015) Aicher, C., Jacobs, A. Z. and Clauset, A. (2015), ‘Learning latent block structure in weighted networks’, Journal of Complex Networks 3(2), 221–248.

- Bandeira and van Handel (2016) Bandeira, A. S. and van Handel, R. (2016), ‘Sharp nonasymptotic bounds on the norm of random matrices with independent entries’, The Annals of Probability 44(4), 2479–2506.

- Bartlett (2017) Bartlett, T. E. (2017), ‘Network inference and community detection, based on covariance matrices, correlations, and test statistics from arbitrary distributions’, Communications in Statistics - Theory and Methods 46(18), 9150–9165.

- Boucheron et al. (2013) Boucheron, S., Lugosi, G. and Massart, P. (2013), Concentration Inequalities: A Nonasymptotic Theory of Independence, Oxford University Press.

- Brown et al. (2012) Brown, J., Rudie, J., Bandrowski, A., Van Horn, J. and Bookheimer, S. (2012), ‘The ucla multimodal connectivity database: a web-based platform for brain connectivity matrix sharing and analysis’, Frontiers in Neuroinformatics 6, 28.

- Desmarais and Cranmer (2012) Desmarais, B. A. and Cranmer, S. J. (2012), ‘Statistical inference for valued-edge networks: The generalized exponential random graph model’, PLoS ONE 7(1), e30136.

- Fan et al. (2016) Fan, X., Xu, R. Y. D. and Cao, L. (2016), Copula mixed-membership stochastic blockmodel, in ‘Proceedings of the Twenty-Fifth International Joint Conference on Artificial Intelligence’, IJCAI’16, AAAI Press, p. 1462–1468.

- Fosdick and Hoff (2015) Fosdick, B. K. and Hoff, P. D. (2015), ‘Testing and modeling dependencies between a network and nodal attributes’, Journal of the American Statistical Association 110(511), 1047–1056.

- Gao et al. (2018) Gao, C., Ma, Z., Zhang, A. Y. and Zhou, H. H. (2018), ‘Community detection in degree-corrected block models’, The Annals of Statistics 46(5), 2153–2185.

- Hsu et al. (2012) Hsu, D., Kakade, S. and Zhang, T. (2012), ‘A tail inequality for quadratic forms of subgaussian random vectors’, Electronic Communications in Probability 17(52), 1–6.

- Johnstone (2001) Johnstone, I. M. (2001), Chi-square oracle inequalities, in M. de Gunst, C. Klaasen and A. van der Vaart, eds, ‘State of the Art in Probability and Statistics, Festschrift for Willem Van Zwet, Lecture Notes-Monograph Series’, Vol. 36, Institute of Mathematical Statistics, Lecture Notes, Monograph Series, pp. 399–418.

- Karrer and Newman (2011) Karrer, B. and Newman, M. E. J. (2011), ‘Stochastic blockmodels and community structure in networks’, Physical Review E 83(1).

-

Kumar et al. (2016)

Kumar, S., Spezzano, F., Subrahmanian, V. S. and Faloutsos, C.

(2016), Edge weight prediction in weighted

signed networks, in ‘2016 IEEE 16th International Conference on Data

Mining (ICDM)’, IEEE, p. 221–230.

http://ieeexplore.ieee.org/document/7837846/ - Leinwand et al. (2020) Leinwand, B., Wu, G. and Pipiras, V. (2020), Characterizing frequency-selective network vulnerability for alzheimer’s disease by identifying critical harmonic patterns, in ‘2020 IEEE 17th International Symposium on Biomedical Imaging (ISBI)’, IEEE, pp. 1–4.

- Ng et al. (2001) Ng, A. Y., Jordan, M. I. and Weiss, Y. (2001), On spectral clustering: Analysis and an algorithm, in ‘Proceedings of the 14th International Conference on Neural Information Processing Systems: Natural and Synthetic’, pp. 849–856.

- Noroozi et al. (2021) Noroozi, M., Rimal, R. and Pensky, M. (2021), ‘Estimation and clustering in popularity adjusted block model’, Journal of the Royal Statistical Society: Series B (Statistical Methodology) .

- Peixoto (2018) Peixoto, T. P. (2018), ‘Nonparametric weighted stochastic block models’, Physical Review E 97(1), 012306.

- Pons and Latapy (2006) Pons, P. and Latapy, M. (2006), Computing communities in large networks using random walks, in ‘J. Graph Algorithms Appl’, Citeseer.

- Sengupta and Chen (2017) Sengupta, S. and Chen, Y. (2017), ‘A block model for node popularity in networks with community structure’, Journal of the Royal Statistical Society: Series B (Statistical Methodology) 80(2), 365–386.

- Spyrou and Escudero (2018) Spyrou, L. and Escudero, J. (2018), ‘Weighted network estimation by the use of topological graph metrics’, IEEE Transactions on Network Science and Engineering 6(3), 576–586.

- Vershynin (2018) Vershynin, R. (2018), High-Dimensional Probability: An Introduction with Applications in Data Science, Vol. 47, Cambridge University Press.

- Zhu and Xia (2016) Zhu, B. and Xia, Y. (2016), ‘Link prediction in weighted networks: A weighted mutual information model’, PLOS ONE 11(2), e0148265.

This extended appendix discusses several topics related to the main paper. Appendix A contains two concentration inequalities for LSM networks, followed by auxiliary lemmas. Appendix LABEL:sa:repeats discusses estimation while accounting for certain diagonal 0’s for within community subnetworks, along with how to adapt the estimation procedures when there are repeated values. Appendix LABEL:mod-problems explains how modularity may fail to characterize the kinds of communities discussed in the main paper. Appendix LABEL:s:greedy-alg introduces a greedy, agglomerative approach to community detection by trying to maximize the measure . Appendix LABEL:s:spatial considers community detection as a spatial clustering problem, and Appendix LABEL:s:spectral-alg includes an algorithm built upon spectral clustering to try to maximize . Appendix LABEL:s:rotated shows that the real parts of the first several eigenvectors of a normalized version of the network also appear to capture community information. Appendix LABEL:more-sims displays additional simulated networks and results. Finally, Appendix LABEL:s:Hext extends both -functions and the kinds of “errors” which may be observed in LSMs or NSMs.

Appendix A Concentration inequality for Normal LSM

In Section 4, we introduced methods for estimating sociability parameters for certain kinds of network generating models. It would be helpful to ensure these estimates are actually capturing the underlying “error-free” network generating mechanisms, what we refer to as the network’s SC. As there are several introduced models, the accuracy of the estimation results may depend on the specific functional forms of a given network. We present below a result on estimation accuracy of the SC for a Normal LSM network (2.1). The estimation procedure is formulated through theoretical means; it remains to be seen how the procedure compares to the practical estimation approach taken in Sections 4 and 6. The proof of the result adapts ideas from Noroozi et al. (2021).

A.1 Concentration for Normal LSM with known

Theorem A.1

Let be a Normal LSM network such that every edge weight is generated as in (2.1), and be the network such that each edge weight has the same generating process as the corresponding edge weight in , but with every value set to 0. Also let be the estimated network (of the form (2.1) with ) induced by the clustering of nodes that minimizes

| (A.1) |

where is the number of different communities in this “best” clustering, and

| (A.2) |

where is the number of nodes in the network, is the number of communities in the clustering, is some constant such that , is the largest variance parameter of any generating function for edges in network , and and are as given in Lemma LABEL:L:NLSM1. Then, for some constant and any ,

| (A.3) |