On the Rank, Kernel, and Core of Sparse Random Graphs

Abstract.

We study the rank of the adjacency matrix of a random Erdős-Rényi graph . It is well known that when , with high probability, is singular. We prove that when , with high probability, the corank of is equal to the number of isolated vertices remaining in after the Karp-Sipser leaf-removal process, which removes vertices of degree one and their unique neighbor. We prove a similar result for the random matrix , where all entries are independent Bernoulli random variables with parameter . Namely, we show that if is the bipartite graph with bi-adjacency matrix , then the corank of is with high probability equal to the max of the number of left isolated vertices and the number of right isolated vertices remaining after the Karp-Sipser leaf-removal process on . Additionally, we show that with high probability, the -core of is full rank for any and . This partially resolves a conjecture of Van Vu [30] for . Finally, we give an application of the techniques in this paper to gradient coding, a problem in distributed computing.

1. Introduction

Let be a random symmetric matrix in where each entry above the diagonal is an i.i.d. Bernoulli random variable that equals with probability and otherwise, and where the diagonal entries are . Equivalently, is the adjacency matrix of an Erdős-Rényi graph on nodes where an edge appears between each pair of nodes with probability .

Determining the rank of has been a question of considerable interest. Initial results by Tao, Costello, and Vu [12] proved that is non-singular with high probability if is a fixed constant. This result was later improved by Costello and Vu in [14] to show that is non-singular with high probability if . This work also showed that is a threshold for singularity as is singular with high probability if . Recent work by Basak and Rudelson [3] shows this threshold is sharp in the sense that if , then is non-singular with high probability, and if , then is singular with high probability. Furthermore, they prove the same result holds for the asymmetric matrix in where each entry is an independent Bernoulli random variable with parameter . More generally, an fundamental question in discrete random matrix theory, dating back to Komlos [23], studies the exact probability that a random matrix is singular. See the survey of Van Vu [30] and the references therein for discussion of the singularity problem.

Following these threshold results, a natural question is determining the rank of and when is small enough that these random matrices are singular with high probability. One approach to understand the rank, previously emphasized by Costello and Vu, is through the following phenomenon:

Phenomenon 1.1.

Linear dependencies among the columns of random matrices arise from small structures.

Costello and Vu [13] showed that when , with high probability, all dependencies in the column space of result from collections of columns with at most non-zero rows. These so-called non-expanding sets allowed Costello and Vu to prove that when , with high probability,

where denotes the neighborhood of the vertex set , denotes the graph with adjacency matrix , and denotes the vertex set of a graph .

Other work has shown additional instances of Phenomenon 1.1. Addario-Berry and Eslava [1] showed that with probability , if you expose the non-zero entries of or randomly one at time, the matrix becomes singular at the exact moment when any row or column of all zeros disappears. For , with , Tikhomirov [29] and Jain et al. [19] show that the probability of singularity of is nearly exactly the probability that has an all-zero row or column (or two equivalent rows and columns when ). Further work [20, 18] shows that for various ranges of , the probability that has corank is nearly the probability that rows are all zero.

A second approach towards understanding the rank of or is via the Karp-Sipser core of a graph, defined below. Originally introduced in [22] to study maximal matchings, the Karp-Sipser core of graph is obtained by iteratively performing a leaf-removal process, which at each step removes a vertex of degree one and its unique neighbor. At the end of the process, there remain only isolated vertices and a subgraph of minimum degree at least two, which we denote . Notably, this leaf-removal process, which we also call peeling, does not change the corank of the graph111We say the corank of a graph to mean the corank of its adjacency matrix., and so the corank of equals the corank of the plus the number of isolated vertices remaining after the leaf-removal process. The following lower bound on the corank of immediately follows:

| (1.1) |

where is the set of isolated vertices remaining after the Karp-Sipser leaf-removal on . For the asymmetric matrix , a similar lower bound holds. We define to be the bipartite graph with bi-adjacency matrix and left and right vertex sets and respectively. Then using the invariance of the corank during peeling, we obtain:

| (1.2) |

where is the set of isolated vertices remaining after the Karp-Sipser leaf-removal on .

A central question asks if these lower bounds on the corank are tight. Two important works yield results on this front for . Bordenave, Lelarge, and Salez show in [6] that as grows, the corank of the Karp-Sipser core of divided by tends to zero. That is, almost surely,

A related asymptotic formula was shown by Coja-Oghlan et al. [11] for the asymmetric random matrix . They showed222This follows from evaluating their rank formula and comparing to the asymptotic size they give for . that in probability,

Both of these results are proved without explicitly connecting the corank to the size of (or ), but rather by showing that asymptotically these two values coincide. Due to their connections with the size of maximal matchings, the asymptotic size of and are well known, and can be studied via differential equations. Karp and Sipser [22] and the tighter analysis of Aronson, Frieze and Pittel in [2] showed in that for , in probability,

where is the smallest root to the equation , and . Analogously, for the bipartite graph with , Coja-Oghlan et al. showed that in probability,

Our main result is to show that the lower bounds in eqs. 1.1 and 1.2 are sharp for . In the vein of Phenomenon 1.1, we prove a new structural characterization of linear dependencies in and , which holds with high probability, and tightens Costello and Vu’s notion of non-expanding sets. On the event that this characterization holds, it follows almost directly that the Karp-Sipser leaf-removal and isolated vertex removal process is precisely equivalent to removing all vertices whose respective rows and columns are part of linear dependencies. Equivalently, on this event, the Karp-Sipser core of is full rank. We state this result in the following theorem.

Theorem 1.2 (Rank of ).

Let and and . Let . With probability ,

Equivalently, with probability ,

where is the set of isolated vertices remaining after the Karp-Sipser leaf-removal on .

For the asymmetric matrix , the story is slightly complicated by the fact that typically, there are “complex” linear dependencies that involve large sets of rows or columns of . These linear dependencies can not be characterized using the same simple structural characterization we prove for the symmetric matrix. Fortunately, we are able to a prove a modified characterization result which shows that with high probability, such “complex” linear dependencies only appear in the rows of or the columns of , but not both. It follows on this event that the bi-adjacency matrix of the Karp-Sipser core of has full row or column rank. We state this result and the resulting characterization of the rank of in the following theorem.

Theorem 1.3 (Rank of ).

Let and and . Let be a bipartite graph with left vertices and right vertices . With probability , either

-

(1)

or

-

(2)

It follows that with probability ,

where is the set of isolated vertices remaining after the Karp-Sipser leaf-removal on .

Our main tool in proving these theorems is a new characterization of all minimally linearly dependent sets of columns that occur with constant probability in and .

Definition 1.4.

A matrix in is a minimal linear dependency if it satisfies the following two properties:

-

(1)

There exists such that and .

-

(2)

.

We sometimes will abbreviate and call such a matrix a minimal dependency.

It is a simple exercise to show that every linearly dependent set of columns has a subset of columns which form a minimal linear dependency. One can additionally show that in any matrix , if the th column is in the span of the remaining columns , then there exists some subset of columns of including which is a minimal dependency (see Lemma 6.3). Let

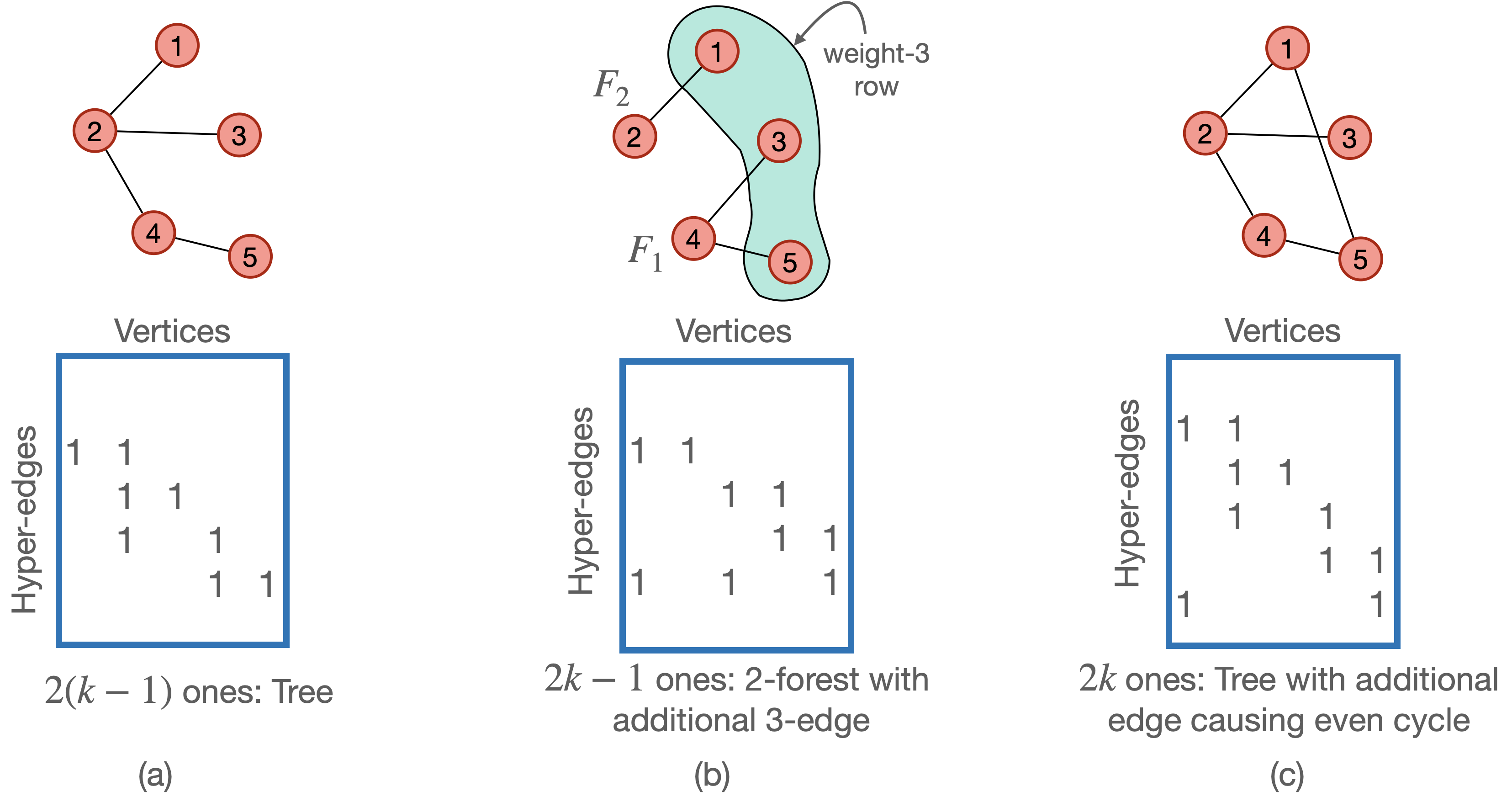

denote the set of {0, 1}-matrices of columns which are minimal linear dependencies. For our main results, we distinguish among one particular class of minimal linear dependencies, illustrated in Figure 1(a).

Definition 1.5 (Tree dependency).

Define as the set of matrices with exactly ’s such that the non-zero columns of form the edge-vertex incidence matrix of a tree on vertices. We call a matrix in a tree dependency.

The following theorem shows that with high probability, all minimal dependencies in are tree dependencies.

Theorem 1.6 (Characterization of minimal dependencies in ).

Let , where and . With probability , for all , all minimal dependencies of columns of are in .

Similarly, either all subsets of columns of or of that are minimal linear dependencies, are tree dependencies.

Theorem 1.7 (Characterization of minimal dependencies in ).

Let , where and . With probability , one of the following holds:

-

(1)

For all , all minimal dependencies of columns of are in .

-

(2)

For all , all minimal dependencies of columns of are in .

Remark 1.

We do not expect the theorem above can be improved, in the sense that often or do have minimal linear dependencies with columns. Intuitively, this is because short and fat rectangular matrices contain minimal dependencies with many columns. When we peel off the rows and columns involved in small minimal linear dependencies, the remaining matrix, , may be rectangular if there are more small minimal linear dependencies in the rows than in the columns (or vice versa). This forces a minimal dependency with many columns in (or ).

Remark 2.

1.1. Additional Results

A second substructure of random graphs which has received considerable attention is the -core of : the largest induced subgraph of with minimal degree . The -core, which we denote , can be obtained by iteratively peeling off vertices of degree less than . When the average degree of is greater than some constant , the -core suddenly emerges and has linear size in the number of vertices of [24]. The exact size of the -core is given by Pittel, Spencer, and Wormald in [25].

Van Vu conjectured in [30] that for , for a constant , almost surely, the adjacency matrix of is non-singular. We prove the following result, which confirms the conjecture of Vu for . Let denote the adjacency matrix of the -core of the graph with adjacency matrix .

Theorem 1.8.

Let , where and . For any constant , with probability ,

We remark that Ferber et al. [15] recently resolved the conjecture of Vu, after a preliminary version of the present paper was made publicly available. This was independent work, and the proof methods are quite different.

We additionally show an application of our techniques to a problem in distributed computing. For this application, we show that our characterization of minimal dependencies also holds for some ensembles of sparse rectangular random matrices. Using this characterization, we can bound the distance from a fixed vector to the span of a random matrix. This is useful for analyzing gradient codes, an object used to provide redundancy in distributed computing. We discuss the particular results in Section 8.

1.2. Notation

For a graph , we use to denote the adjacency matrix of . We use to denote the graph with adjacency matrix . For a bipartite graph , we use to denote the bi-adjacency matrix of , where indexes rows of , and indexes columns. We use to denote the bipartite graph with bi-adjacency matrix . We use or to denote the vertex set of a graph or .

For , let denote the set . For a matrix and , we let denote the submatrix of with columns indexed by . For , we let denote the submatrix of with rows indexed by . Furthermore, for an index , we let denote the th column of and we let denote with the th column removed. We define for rows analogously. We let denote with both the th row and th column removed. Finally, we let denote the transpose of . We say the corank of equals .

For vectors and , let denote the concatenation of and . We use to denote the th standard basis vector.

1.3. Outline

In Section 2, we give a technical overview of the proofs of the main theorems. We break down the proofs of Theorems 1.6 and 1.7 thematically into Sections 3 and 4, where we prove the main technical lemmas. We conclude the proof in Section 5. In Section 6, we prove Theorems 1.2 and 1.3 using Theorems 1.6 and 1.7.

2. Technical Overview

In this section, we give a high level overview of the proof of the main theorems in this paper.

2.1. Overview of Proposition 1.6 and Proposition 1.7

For simplicity, in this overview we primarily focus on the asymmetric matrix , where . We provide comments on when and how the techniques differ for the symmetric matrix .

Our proof of each characterization result is divided into two domains: a “small” domain and a “large” domain. The small domain considers possible kernel vectors with support at most . The large domain considers possible kernel vectors with support at least . Thematically, this is similar to the more-involved casework based on levels of “structuredness” of vectors used classically to show that the kernel of is empty for . (See eg. [27, 29, 19])

2.1.1. Small Domain

The main idea for the small domain comes from the following two simple observations.

Observation 1.

Let be a matrix. Then if some row of contains exactly one , then there is no such that and .

Proof.

If there is only one column of with a at a certain row-index, that column is linearly independent of all other columns in . Thus, no dependency including all columns of exists. ∎

Observation 2.

Let be a matrix. If has support size less than , then is not a minimal linear dependency.

Proof.

The requirement that is rank means that at least rows must have at least one in them. Hence it follows from Observation 1 that each of these rows must contain at least two 1s. Thus, if is a minimal dependency, it contains at least ’s. ∎

Within the small domain, we subdivide into two cases, again depending on the size of the support of the kernel vector. The results for the small domain are proved in Section 3.

Small Case 1

The goal of this case is to prove that with high probability, for any , and with , if is a minimal dependency, then . We will take a union bound over all such sets to prove this. Fix with , and define to be the number of s in . Due to Observation 2, we only must consider the case when . Further, if , then if is a minimal dependency, it must also be in (see Lemma 3.5).

By Observation 1, is not a minimal dependency if there exists a row with exactly one in . To lower bound this probability, we condition on , consider the random process which exposes the positions of s in randomly one at a time. Consider the random walk which increases by every time we expose a in an already occupied row, and stays constant otherwise. As long as the value of this random walk is less than at the time all s are exposed, we know that is not a minimal dependency. When , this occurs with small enough probability that after a union bound on all sets , we succeed with probability .

For the case of symmetric matrices, we modify this argument slightly by considering the random walk which also increases every time a is exposed in the “symmetric” portion of , that is, a row of indexed by an element of .

Small Case 2

This case rules out with high probability any minimal dependencies of columns of for . Again we use Observation 1 and take a union bound over all submatrices for sets of size . We use a Chernoff bound to show that with very high probability, has a row with a single .

2.1.2. Large Domain

As approaches , we can no longer expect to have rows with a single with high enough probability, so we need to look beyond Observation 1 to rule out linear dependencies. Our main tool in ruling out larger minimal dependencies are the following Littlewood-Offord anti-concentration results for sparse vectors, from Costello and Vu [14].

Lemma 2.1 (c.f. [14] Lemma 8.2).

Let be a deterministic vector with support at least . Let be a random vector with i.i.d. Bernoulli entries with parameter . For any ,

In particular, for , we have:

In the symmetric matrix case, we will additionally use a quadratic Littlewood-Offord result, originally due to Costello, Tao, and Vu [12], and adapted to sparse random vectors in [14].

Lemma 2.2 (c.f. [14] Lemma 8.4).

Let be a deterministic matrix with a least non-zero entries in each of distinct columns of . Let be the random vector with i.i.d. Bernoulli entries with parameter . Then for any fixed ,

Again we subdivide into two cases.

Large Case 1

This case rules out with high probability minimal dependencies of columns of for , for some constant . In this case, we again perform a union bound over all submatrices for sets of size . For each , we consider the random process , where we expose rows of one at a time. (Recall that is the submatrix of given by restricting to the columns in and the first rows.) At each step , we keep track of the kernel of . Before any rows are exposed, the dimension of the kernel is equal to . Since our goal is to show that the kernel of contains no vectors with support size , we leverage Lemma 2.1 as follows: if the kernel of contains a vector with support , then it is likely that the next row exposed, , will not be orthogonal to . After exposing enough rows, we show that with high probability, we “knock out” all candidate kernel vectors with large support. Notice that we only need to “knock out” such vectors at most times.

This approach of Large Case 1 breaks down when approaches . For instance, in the extreme case when , we would need to “knock-out” a kernel vector every single time we expose a row of . This certainly won’t occur with high probability. Hence we use a different approach when for some constant .

Large Case 2

Our strategy for ruling out dependencies on the order of columns is inspired by the approach of Ferber, Kwan, Sauermann [16] to show the almost sure non-singularity of when . For the symmetric matrix , we combine these ideas with some techniques used by Costello, Tau, and Vu in [12] to show almost sure non-singularity of when . The following simple observation is key to our argument for both and .

Observation 3.

Let be a matrix. If , and has support size , then there are at least columns such that .

For the asymmetric case, recall that our goal is to show that either or has no kernel vector with support size at least . Let be the event that has a left kernel vector with support size at least , and that column is in the span of the remaining columns . Then by Markov’s Law and Observation 3, the probability that both and have kernel vectors with support size at least is at most . To bound this probability, consider the matrix formed by removing the th column of . We define to be the event that has a left kernel vector with support size at least , and that column is in the span of the remaining columns . Observe that any left kernel vector of is a left kernel vector of , and so . To bound the probability of , we condition on and leverage the independence of from . Assume has some left kernel vector with . Lemma 2.1 tells us that with probability , the column is not orthogonal to , and hence is not in the span of the remaining columns . It follows that .

In the symmetric case, we let be the event that the column is in the span of the remaining columns . Again we use Markov’s Law and Observation 3 to show that the probability that has a kernel vector of support size of at least is at most . To bound , we condition on , the matrix formed by removing the th row and column of , and leverage the randomness of .

We consider two main cases: one in which has a kernel vector with large support, and one in which it doesn’t. If has a kernel vector with large support (on the order of ), we use Lemma 2.1 to show that with probability , is orthogonal to , and hence is not in the span of the remaining columns (recall that denotes the vector with all but the th entry ). If has no kernel vectors with large support, we construct a “pseudoinverse” for , for which implies that is not in the span of . We leverage some additional results from the small domain and Large Case 1 to show that is dense. Lemma 2.2 then guarantees that with probability .

The results for the large domain are proved in Section 4.

Remark 3.

The roadmap of this proof shows the two places where our techniques break down when is a constantFirst, in Small Case 1, our union bound only succeeds in ruling out minimal dependencies outside of with probability . When and are constant, this probability no longer goes to . One can check that with constant probability, there are some minimal dependencies outside , but they are contained in two other classes of special structures, which we formally define in Section 3 as and (pictured in Figure 1). Second, our results for Large Case 2, based on the Littlewood-Offord lemmas, require to go to infinity to get a result which holds with probability that tends to .

2.2. Overview of Theorem 1.2 and Theorem 1.3

Theorems 1.2 and 1.3 follow directly by combining two linear-algebraic claims about the Karp-Sipser leaf-removal process with the results of Theorems 1.6 and 1.7. Specifically, to prove Theorem 1.2 on the rank of , we use the following three claims:

-

(1)

The corank of a matrix is invariant under the Karp-Sipser leaf removal process.

-

(2)

If the Karp-Sipser core has a vector in its kernel, then there must be a kernel vector of whose support contains the support of .

-

(3)

If , then by the characterization of minimal dependencies in Theorem 1.6, for all , the vertex will be removed during the Karp-Sipser leaf-removal process or become isolated after this process. Thus, vertex will not be in the Karp-Sipser core of .

The proof of Theorem 1.3 on the rank of is similar. These claims are proved in Section 6.

2.3. Overview of Theorem 1.8

To prove Theorem 1.8, we need to show that the kernel of is empty. We use the same four cases as in the proof of Theorems 1.6 and 1.7 above.

The techniques used to rule out minimal dependencies in each of these cases is largely the same as before. In the small domain, we leverage the fact that any subset of columns of for must have at least ’s.

In Large Case 2, we adapt our argument in a more involved way. We define to be the event that is in the span of the remaining columns of and that the -core is “normal” with respect to vertex . Formally, we say the -core is normal with respect to if vertex is in the -core, and if we remove vertex from the -core, the remaining graph still has minimum degree at least . Equivalently and symbolically, this means

We proceed to show that the -core is normal with respect to all but vertices. It follows from Observation 3 and Markov’s Law, that the probability that has a kernel vector with support size at least is at most .

We can bound by conditioning on and leveraging the independent randomness of . In a similar vein as before, we consider two main cases: one in which has a kernel vector with large support, and one in which it doesn’t. The logic is similar as before.

We prove these results in Section 7.

3. The Small Domain

3.1. Definitions and Lemmas for Characterizing Minimal Dependencies

We gather here a few definitions and lemmas that we use in the small domain. We summarize notation in Table 1.

Remark 4.

While it is sufficient for our main results to consider only tree dependencies (Definition 1.5), we state our results in the small domain to hold for , for a universal constant. For constant values of , with constant probability, and include small minimal dependencies that are not tree dependencies, defined below. We believe understanding these dependencies may be of independent interest.

| Set of minimal dependencies with columns (Definition 1.4) | |

|---|---|

| Set of tree dependencies of columns (Definition 1.5, Figure 1(a)) | |

| Set of two-forest dependencies of columns (Definition 3.1, Figure 1(b)) | |

| Set of tree-with-added-edge dependencies of columns (Definition 3.2, Figure 1(c)) | |

| Subset of matrices in with exactly ones. (Definition 3.3) | |

| Subset of matrices in with exactly ones and exactly non-zero columns. (Definition 3.4) |

Definition 3.1 (Two-forest dependency).

Let be the set of matrices with exactly ’s satisfying the following:

-

(1)

has non-zero rows: rows supported on two entries and one row supported on three entries.

-

(2)

The submatrix of restricted to the rows of support is the edge-vertex incidence matrix of a forest with two connected components .

-

(3)

The row of support size three contains ’s at column indices where are connected by an even-length path, and for .

Definition 3.2 (Tree-with-added-edge dependency).

Define as the set of matrices with ’s such that the non-zero columns of form the edge-vertex incidence matrix of a tree on vertices, with an added edge between two vertices in the tree of odd distance from each other. The additional edge may create a multi-edge in the this graph.

The first lemma allows us to show that the minimal dependencies we encounter with constant probability have the graph-structures depicted in Figure 1.

Definition 3.3.

Define to be the set of matrices which contain exactly ones.

Definition 3.4.

Define to be the subset of matrices in which have exactly non-zero rows.

The following lemma relates these sets to the sets and introduced earlier in Definitions 1.5, 3.1, and 3.2.

Lemma 3.5 (Classification of Dependencies).

We have the following three equivalences:

-

(1)

.

-

(2)

.

-

(3)

.

Lemma 3.5 is proved in Appendix B. The main step in its proof is the following “connectivity” lemma, also proved in Appendix B.

Lemma 3.6 (Connectivity of Minimal Dependencies).

Let , and let be the hypergraph on vertices with hyperedge-vertex incidence matrix , where the rows of index hyperedges, and the columns index vertices. Then all vertices in are connected.

3.2. Small Case 1

Our main goal in the Small Case 1 is to prove the following general proposition, which holds for as small as . The corollary that follows contains the necessary ingredients from Small Case 1 for proving Theorems 1.6 and 1.7.

Proposition 3.7 (Small Case 1).

Let be any of the following random matrices for :

-

(1)

, where

-

(2)

, where

-

(3)

, where

There exists a universal constant such that for any set of size , we have

-

(1)

.

-

(2)

.

-

(3)

.

-

(4)

.

Union bounding over the sets yields the following corollary when .

Corollary 3.8.

Let and for . Then each of the following hold with probability :

-

(1)

with , .

-

(2)

with , .

-

(3)

with and , .

Proof of Proposition 3.7.

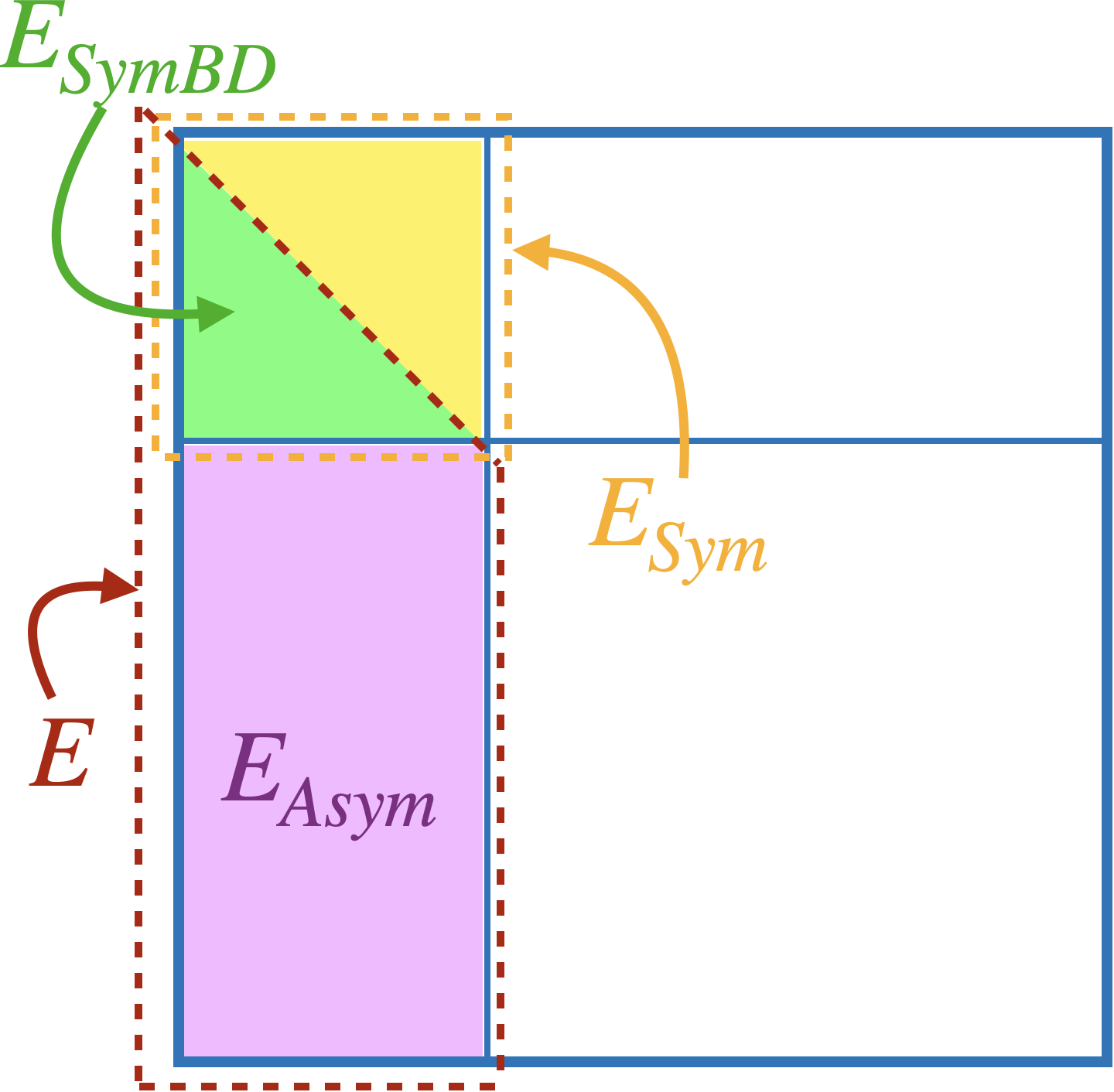

We introduce some notation, pictured in Figure 2. Fix a set of columns and consider the submatrix induced by these columns. If , we define the following partition of the entries of . Let be the set of entries of whose rows are indexed by values in . Let be subset of entries in that are below the diagonal of , and hence mutually independent. Let be the set of entries whose rows are not in , and finally, let be the full set of mutually independent entries that determine . If , we define to be all of the entries in . Formally:

|

|

|

|

| a) | b) where | c) where | d) |

We will couple the process of randomly exposing the ’s in with a random walk that counts the number of times a is exposed in in a row that already contains a or in . Observe that each consecutive is exposed in a random entry in , sampled without replacement. We condition on , the number of ’s in . Note that . Let be the random walk that increases by one if the th exposed is in or if the th exposed is in and is not the first exposed in its row. Otherwise, let .

The following claims say when is small compared to the number of ’s in , is not a minimal dependency.

Claim 3.9.

If and there are at least total ’s in , then there is a row of (not in ) with a single , so .

Proof.

Let be the number of ’s in , and let be the number of ’s in such that and . Let be the number of ’s in which are not the first in their row. Now the number of rows not in which have exactly one is at least

∎

Claim 3.10.

If , then .

Proof.

We prove this by contradiction. Assume . Let be the number of ’s in , and let be the number of ’s in such that and . Observe that if , then it must have exactly non-zero rows. Indeed, if it had less than non-zero rows, then would have rank at most , which contradicts being a minimal dependency. Further, if has more than non-zero rows, then by the fact that is a minimal dependency it must have non-zero rows (as each non-zero row must have at least two ’s and only has ’s). However, if it has non-zero rows and is in , then it must be in . Hence, by lemma 3.5, . We proceed in two cases:

Case 1: . In this case, if each row in has at least two ’s, then we must have

since .

Case 2: . Note that in this case . Let be the number of occupied rows in , such that rows are occupied in . Observe that by the symmetry of , number of occupied columns in is at most .

Since we cannot have all-zero column (this would contradict being a minimal dependency), the number of columns occupied in that are not occupied in must be at least . However, by the connectivity of minimal dependencies (Lemma 3.6), the number of columns occupied in that are not occupied in is at most . Note that here we also used the fact that is non-empty. Thus we have .

Summarizing, we have

-

(1)

-

(2)

-

(3)

Combining (2) and (3), we achieve

which contradicts . ∎

The proof of the next two claims are nearly identical to the proof of Claim 3.9, so we omit them.

Claim 3.11.

If and there are at least ’s total in , then there is a row of (not in ) with a single , so .

Claim 3.12.

If and there are at least ’s total in , then there is a row of (not in ) with a single , so .

Recall from Observation 2 that any minimal dependency must have at least ’s total. By Lemma 3.5, any minimal dependency with ’s must be in . Further, any minimal dependency with ’s must either be in or in .

Thus, any minimal dependency not in must have at least ’s or be in . As a result, we have by Claim 3.9 and Claim 3.10,

Note here the fact that if , then .

Further, because minimal dependencies in have at least ’s, by Claim 3.11,

Finally by Claim 3.12,

To bound the probability that is large, we couple with a random walk which increases by one with probability and otherwise stays constant. Observe that stochastically dominates , because there are at most rows — and hence locations in — in which exposing a will increase . Then conditioned on , for any , we have

Lemma 3.13 (Small Case Binomial Calculation).

For constants , for , there exists a constant such that for any and , we have

We employ this lemma with and , to achieve

Further, letting gives:

| (3.1) |

Finally, setting , gives:

Putting proves the lemma. Note that eq. 3.1 establishes the second and third statements of the lemma simultaneously. ∎

3.3. Small Case 2

Our main goal of this section is to prove the following lemma.

Lemma 3.14 (Small Case 2).

Let be any of the following random matrices for for some universal constant :

-

(1)

, where

-

(2)

, where

-

(3)

, where

Then

Proof.

We will take a union bound over all possible sets of size of the probability that has a kernel vector with support . By Observation 1, it suffices to show that with probability , for all such sets , there is a row in the submatrix with exactly one .

For each of the three choices of ensemble, the rows for are mutually independent, so we have

Note that does not depend on the choice of , just its size . Taking a union bound over all and all sets of size , we achieve:

for sufficiently large . ∎

4. The Large Domain

4.1. Statement of Lemmas

In the large domain, we bound the probability of having minimal dependencies of columns for . Large Case 1 (Section 4.2) considers the case when for some constant . Large Case 2 (Section 4.3) considers the case where . As discussed in the technical overview, our main tool in these two cases are the Littlewood-Offord anti-concentration results.

4.2. Large Case 1

We prove the following lemma.

Lemma 4.1 (Large Case 1).

There exist universal constants and , such that the following holds. Let be any of the following random matrices for :

-

(1)

, where

-

(2)

, where

-

(3)

, where

Then

Proof.

We union bound over all and all sets of size of the probability that there exists with and .

Fix a set of size . We will consider the random process where we expose the rows for one at a time. Note that these rows are all mutually independent since they do not include rows indexed by . Further, they do not include th row (which does not exist in the case that ). For , let be the kernel of the first rows exposed, and let be the span of the set of vectors in which have no zeros. Let be the dimension of .

If , then we can choose an arbitrary vector in with support , and by Lemma 2.1, with probability at least , the th row exposed is not orthogonal to . In this case .

If at any point becomes , then this means there can be no dependency involving all the columns of . It follows that since , we have

| (4.1) |

We employ the following computational lemma, proved in Appendix C:

Lemma 4.2 (Large Case 1 Binomial Calculation).

There exists constants , , and , such that for all , we have

4.3. Large Case 2

As outlined in the technical overview, the proof strategy for Large Case 2 for the symmetric matrix varies significantly from that of the asymmetric matrix . Since the proof for is simpler, we begin with that matrix.

4.3.1. Large Case 2 for

For the asymmetric matrix , it is not possible to rule out both left and right kernel vectors of with large support. Indeed, often such dense kernel vectors do exist. We can, however, rule out having dense right and left kernel vectors simultaneously. We do so in the following lemma.

Lemma 4.3 (Large Case 2 for ).

Let . Let be the set of vectors in with support size at least . For , where is the constant from Lemma 4.1, for for some constant ,

Proof.

For , let be the space spanned by the column vectors . Following Observation 3 from the technical overview, and imply that for all ,

-

(1)

;

-

(2)

.

Let denote the event that these two events occur for index . Let be the indicator of this event, and let . It follows that

By Markov’s inequality,

| (4.2) |

Now by conditioning on and using the sparse Littlewood-Offord Lemma (Lemma 2.1), we have

Here the first inequality follows from the fact that implies that is orthogonal to any normal of . We are able to remove the conditioning in this step because is independent from (and hence also the normal ). The final inequality follows from Lemma 2.1, where we used the fact that for large enough.

Plugging in to eq. 4.2, we have which proves the lemma. ∎

4.3.2. Large Case 2 for

For the symmetric matrix , Large Case 2 reduces the probability of having a kernel vector with large support to the probability of having several smaller structures in . The following is our main technical lemma for :

Lemma 4.4 (Technical Lemma for Large Case 2 for ).

Let . Let denote the submatrix of obtained by removing the th row and column. Let be a random vector with i.i.d. entries. For any with ,

| (4.3) |

where denotes the set of matrices in with some set of columns that each have support size at least .

Lemma 4.4 breaks down the probability that there is a large linear dependency consisting of more than rows into the sum of the probabilities of several other events. Two of these probabilities (lines 1 and 5 of the right hand side of eq. 4.3 in the lemma) we can show to be small via anti-concentration lemmas. Two of the probabilities (lines 2 and 4 of the right hand side of eq. 4.3 in the lemma), we will eventually show to be small using the lemmas from Small Case 1, 2, and Large Case 1.

Instantiating Lemma 4.4 with , , , , where is the constant from Lemma 4.1, we obtain the following lemma.

Lemma 4.5 (Large Case 2 for ).

Let for . With equal to the constant from Lemma 4.1,

Proof.

This follows immediately from plugging in these values of and into Lemma 4.4 and applying the anti-concentration results in Lemmas 2.1 and 2.2 to the first and last terms in eq. 4.3. Indeed, Lemma 2.1 shows that

where we have used the fact that since . Lemma 2.2 shows that

The third term in eq. 4.3 equals which is also . ∎

Lemma 4.6.

Let be a matrix with columns for . Let be the space spanned by the column vectors . Let be the set of all such that . Then there exists some with such that .

Lemma 4.7.

With the terminology of the previous lemma, , if and only if .

Proof of Lemma 4.4.

For each , we define to be the space spanned by the column vectors .

Then, as per Observation 3, for some implies that for all , . Let denote the event that . Let be the indicator of this event, and let . By Markov’s inequality and the exchangeability of the columns,

| (4.4) |

We will break down the probability into several cases, depending on the size of the support of vectors in the kernel of . Let be the set of all such that , such that by Lemma 4.6 and Lemma 4.7,

Case 1: has a kernel vector with large support, that is, .

Case 2: has a kernel vector with medium support, that is .

Case 3: does not have any kernel vectors with large or medium support vectors in its kernel, that is, .

We can expand

| (4.5) |

For simplicity, define to be the first entries of the column .

To evaluate the probability of the first case, we condition on and let be any vector of support at least in the kernel of . Observe that cannot hold if is non-zero. Indeed, if , then let such that . Then by Lemma 4.7, and hence does not occur. Since a is independent from , we have

| (4.6) |

Combined with eq. 4.4, the contribution from this case yields the first term in the right hand side of eq. 4.3.

For the second case, we bound:

| (4.7) |

Combined with eq. 4.4, the contribution from this case yields the second term in the right hand side of eq. 4.3.

The third case will lead to the final three terms in the right hand side of eq. 4.3. In this case, we will show conditions under which we can algebraically construct a vector such that . This will imply by Lemma 4.7 that .

Recall that is the set of all such that . For , let be any vector such that . We next construct a sort of “pseudoinverse" matrix as follows: For , define to be the th entry of . That is, for , the th column of is . Define all other entries of to be zero.

The following claim shows a condition for not holding.

Claim 4.8.

If and , then .

Proof.

Let such that . Hence if , . Define to be the vector with in the first entries and in the final entry. Then the first entries of are , and the last entry is . Evidently, if , then

so . ∎

By definition, in the third case, we have . Hence by Claim 4.8,

| (4.8) |

Notice that is a function of and so a is independent from . It is easy to check that for any set of size at least ,

| (4.9) |

We will break up the second term in eq. 4.8 by conditioning on whether the support of has many entries or not, and using the independence of a from :

| (4.10) |

5. Proof of Characterization of Linear Dependencies: Theorem 1.6 and Theorem 1.7

We are now ready to put the results of the small and large domains together to prove Theorem 1.6 and Theorem 1.7.

5.1. Proof of Theorem 1.6

For the convenience of the reader, we restate this theorem:

See 1.6

We will need the following two lemmas to show that the first two terms in the right hand size of Lemma 4.5 are .

Lemma 5.1.

Proof.

Lemma 5.2.

Let with and let be as in Lemma 4.1. Then

We reduce Lemma 5.2 to Lemma 5.3, which we are better suited to prove with our lemmas from Small Case 1, 2, and Large Case 1.

Lemma 5.3.

Let with and let be as in Lemma 4.1. Let . Then

Similarly, suppose is with the last row removed. Let . Then

Proof of Lemma 5.2.

First we consider vectors with . Applying the first part of Lemma 5.3 to , with probability , there exists some set with such that for all satisfying that and . With probability , , so for all vectors with support in and of size less than , we do not have .

Next we consider vectors with . If such an exists, that is, and , then it must be the case that . By the second part of Lemma 5.3, the probability that such an exists is . ∎

Proof of Lemma 5.3.

Let be the event that

Recall that by Lemma 5.1, this event occurs with probability . To prove the first part, we will show that conditioned on not occurring, we have .

Index the set as follows: . For to , let , where is chosen uniformly from the interval . It follows that with probability , for all ,

If does not occur, then for all , so we have that . It follows that if , then there exists some such that . However, this would imply that holds, which is a contradiction.

We are now ready to prove Theorem 1.6.

Proof of Theorem 1.6.

First observe that if , then the theorem is trivially true since is non-singular with probability . Combining Lemma 4.5 with the Lemmas 5.1 and 5.2 presented above, with probability , for any , there are no minimal dependencies of columns of . Further applying Corollary 3.8, for we see that with probability , all minimal dependencies of columns of must be in . ∎

5.2. Proof of Theorem 1.7

For the convenience of the reader, we restate this theorem:

See 1.7

Proof.

First observe that if , then the theorem is trivially true since is non-singular with probability . Assuming , this theorem follows directly from combining Corollary 3.8, Lemma 3.14, Lemma 4.1, and Lemma 4.3. We apply Corollary 3.8, Lemma 3.14, and Lemma 4.1 to both and to show that with probability , neither nor has minimal dependencies of columns outside of for , where is the constant from Lemma 4.1. Finally, Lemma 4.3 shows that either or has no minimal linear dependencies of more than columns. ∎

6. Proof of Theorem 1.2 and Theorem 1.3 on the Rank of A and B

We will need the following three simple linear algebraic lemmas.

Lemma 6.1 (One-Sided Leaf Removal).

Let , and let be the matrix obtained be removing from a column with a single in it, and the row which indexed the location of the . Then Furthermore, the union of the supports of vectors in the kernel of is a subset of the union of the supports of vectors in the kernel of .

Proof.

Without loss of generality, assume the last column and first row were removed. Let be the kernel of and be the kernel of . Define , by , where . It suffices to show that is a one-to-one and onto mapping from to . The one-to-one is by definition. maps from to since for , and . The mapping is onto since for any , writing , we must have and , because the first row of is orthogonal to . ∎

Lemma 6.2 (Leaf Removal).

Let be a the adjacency matrix of a graph . Let be the adjacency matrix of the graph obtained from by removing any vertex of degree one and its unique neighbor. Then Furthermore the set of vertices in the support of the kernel of is contained in set of vertices in the support of the kernel of .

Proof.

We apply Lemma 6.1 twice. First we remove the column corresponding to the vertex and the row corresponding to its neighbor. This does not change the corank. Then we remove the row corresponding to the vertex and the column corresponding to its neighbor. This does not change the corank, since the matrix is square, so the corank of the row space is the same as the corank of the column space.

To see the last statement, assume without loss of generality the leaf vertex was and its unique neighbor was . Then if , we have , where , where . Clearly the support of is contained in the support of . ∎

Lemma 6.3.

For , if , then for any , there exists some set with such that .

Proof.

It suffices to show that if is not a minimal dependency, then it is possible to find some subset such that , and there exists some with such that . By repeating this process, we will eventually find some set such that is a minimal dependency.

If is not a minimal dependency, then by definition, there exists some with such that and . There must exist some index such that , otherwise, we would not have . Let . Notice that and , so and . ∎

We are now ready to prove Theorem 1.2 using Theorem 1.6. We restate Theorem 1.2 for the readers convenience. Recall that for a graph , we use to denote the Karp-Sipser core of .

See 1.2

Proof.

Let be the graph with adjacency matrix , and let be the adjacency matrix of the graph that remains after iteratively peeling off vertices of degree one from and their unique neighbors. Let be the set of rows peeled during this process. By repeatedly applying Lemma 6.2, we have

Let be the set isolated vertices that remain. Let be the graph that remains after removing those vertices, and be the associated adjacency matrix. Then

It remains to show that on the event that the conclusion of Theorem 1.6 holds, which occurs with probability , we have . Let be the set of columns involved in linear dependencies of :

The equivalence holds because by Lemma 6.3, any column involved in a linear dependency must also be involved in a minimal linear dependency.

Claim 6.4.

Conditional on the event in Theorem 1.6 holding,

Proof.

Conditional on the event, we have

Consider any set for which . By the definition of , is the edge-vertex incidence matrix of a tree. Hence the leaf-removal process and isolated vertex removal step will necessarily remove all the columns in . This shows that . ∎

Suppose for the sake of contradiction was singular, and had some non-zero kernel vector . Then by iteratively applying the second implication of Lemma 6.2, we see that the vertices in the support of the kernel of , namely , must contain the vertices supporting . This implies that contains a vertex in the Karp-Sipser core of , which contradicts the previous claim. It follows that with probability , is non-singular. ∎

The proof of Theorem 1.3 is nearly identical.

See 1.3

Proof.

Let be the bipartite graph that remains after iteratively peeling off vertices of degree one from and their unique neighbors, and let be the associated bi-adjacency matrix (where we have retained the same left-right partition as ). Let be the set of vertices peeled during this process. By repeatedly applying Lemma 6.1, we have

Let be the set isolated vertices in . Let be the graph that remains after removing those vertices, and be the associated bi-adjacency matrix. Then

| (6.1) |

and

| (6.2) |

It remains to show that on the event that the first conclusion of Theorem 1.7 holds, we have or . We condition on the event that the conclusion of Theorem 1.7 holds, which occurs with probability . Without loss of generality, assume the first event holds, which implies that for all such that we have

Let be the set of columns involved in linear dependencies of :

The following claim is proved in the same way as Claim 6.4, so we omit its proof.

Claim 6.5.

Conditional on the first event in Theorem 1.7 holding,

Suppose for the sake of contradiction did not have full column-rank, and had some non-zero kernel vector such that . Then by iteratively applying the second implication of Lemma 6.1, we see that the right vertices in the support of the kernel of , namely , must contain the vertices supporting . This implies that contains a vertex in the right side of the Karp-Sipser core of , which contradicts the previous claim. It follows that .

7. Proof of Theorem 1.8

In the following section, we prove our result showing that if , then with high probability, the -core of of is full rank. Throughout this section, we let .

As outlined in Section 2, the proof of the Theorem 1.8 is divided in two main domains corresponding to the size the minimal dependencies we consider.

7.1. Small Domain

7.1.1. Small Case 1

We prove the following lemma, which rules out minimal linear dependencies of columns of for . Our approach is similar to the prior Small Case 1.

Lemma 7.1 (Small Case 1 for -Core).

Let , where for some universal constant . For a set of columns and subset of rows, let be the event that:

-

(1)

;

-

(2)

;

-

(3)

;

-

(4)

contains no more than one row with a single .

Then

Remark 5.

A slightly weaker version of this lemma would require that contains no rows with a single . By taking to be the set of vertices in the -core, this weaker version would suffice to rule out with high probability any minimal dependencies in with columns for . We state this lemma to be stronger because we will also want to rule out small minimal dependencies in , akin to how we studied for the prior results in this paper on the rank of .

Proof.

We introduce some notation, pictured in Figure 3. Fix a set of columns and consider the submatrix induced by these columns. Let be the set of entries of whose rows are indexed by values in . Let be subset of entries in that are below the diagonal of , and hence mutually independent. Let be the set of entries who rows are not in , and let be the full set of mutually independent entries that determine . Formally:

For , let and denote the respective set additionally restricted to entries with . Observe that it suffices to consider , because otherwise having at least three s in would imply having at least three rows of with a single .

We will couple the process of randomly exposing the ’s in with a random walk that counts the number of times a is exposed in in a row that already contains a or in . Observe that each consecutive is exposed in a random entry in , sampled without replacement. We condition on , the number of ’s in . Note that . Let be the random walk that increases by one if the th exposed is in or if the th exposed is in and is not the first exposed in its row. Otherwise, let .

The following claim says that must be large for to occur for any .

Claim 7.2.

Suppose there exists some such that event occurs. Then .

Proof.

Let be the number of ’s in , and let be the number of s in . Since , we have . It follows by the third condition for the event that . Let be the number of s in , which are not the first in their row. Then . Now the number of rows in which have exactly one is at least , since there are exactly non-empty rows in , and at most of those rows have more than one . Now

Hence if then since is an integer, we have

so meaning that at least two rows in have exactly one . It follows that we must have if contains at most one row with a single one. ∎

It remains to show that is small enough with high enough probability to take a union bound over all sets . We will break up this probability as follows.

Let and define , where . Then (for a fixed ),

We consider first the second term in the equation above. To bound this term, we couple with a random walk that which increases by with probability and otherwise stays constant. Observe that stochastically dominates , because there are at most rows in in which placing a will increase . Then conditioned on ,

The following lemma, which we prove in Appendix D, bounds this probability.

Lemma 7.3 (Binomial Bound 1 for -core Small Case 1).

For any larger than some constant, for any , and for any ,

where and .

Next we bound the probability that . Recall that is the number of ’s in and . Now , and each entry in is with probability . Hence

The following lemma, which we prove in Appendix D, bounds this binomial tail probability.

Lemma 7.4 (Binomial Bound 2 for -core Small Case 1).

For sufficiently large and , if ,

where .

We finish the proof of this lemma by union bounding over all , and all sets of rows. Plugging in the result of Lemma 7.4, we have

Hence with probability at least , for all sets of rows, there are at most ’s among the rows. Assuming , we plug in the result of Lemma 7.3 to obtain:

It follows that

∎

7.1.2. Small Case 2

Lemma 7.5 (Small Case 2 for -core).

Let . For a set of rows and a set of columns , let be the event that

-

(1)

;

-

(2)

;

-

(3)

contains no more than one row with a single .

There exists a constant such that for all ,

Proof.

We union bound over all , and all sets of columns. We will lower bound the number of length rows in which have exactly one . We consider only the mutually independent rows. Let be the event that the th row, , has one for . Then

Let such that . Now because for , we have

so

If has at most one row with a single one, then necessarily , assuming sufficiently large . By a Chernoff bound (see Lemma A.1 for reference), for larger than a large enough constant, for a fixed ,

where we have used in the final inequality the fact that .

Union bounding over all choices of , and all choices of , we have

Since grows at most polynomially in , for a large enough constant, the exponent becomes negative, this probability is . ∎

7.2. Large Domain

7.2.1. Large Case 1

Lemma 7.6 (Large Case 1 for -core).

Let . For a set of rows and a set of columns , let be the event that

-

(1)

;

-

(2)

;

-

(3)

for some with .

There exists a constant and such that for all ,

Proof.

We union bound over all satisfying , and all sets of columns, and over all sets of size . Fix a set of columns and a subset of rows. We will consider only the at least mutually independent rows of , that is, the matrix .

Consider the following process, where we expose the independent rows of one at a time for to . Let be the nullspace of the first rows vectors exposed, and let be the dimension of the smallest subspace of which contains all vectors in which have no zeros.

By Lemma 2.1, if , then we can choose an arbitrary vector in with support , and with probability at least , the th row exposed is not orthogonal to . In this case . If ever becomes , then has no kernel vectors with no zeros, so there is no kernel vector of with support . Since , a Chernoff bound (see Lemma A.1) yields

where . To achieve this value of , we impose that such we can plug in in the last inequality. Finally union bounding over all and , the probability that occurse for some and is at most

which for constants and large enough, is . This concludes the lemma. ∎

7.2.2. Large Case 2

We will use the following lemmas from Section 4.3, which we restate here.

We will use the following notation: For an adjacency matrix , let be the set of vertices in the -core of the graph with adjacency matrix . Further, let denote adjacency matrix of the -core of . For a matrix and set , we let denote the restriction of to the columns and rows in . Thus . Recall that we define to be with both the th row and th column removed.

The following lemma, which follows from [25], states that the -core of is large.

Lemma 7.7 (c.f. Theorem 2 in [25]).

Let . For any constant , and for , with probability at least ,

If and , then with probability at least ,

Our main tool to prove Theorem 1.8 is the following lemma, which rules out large dependencies in .

Lemma 7.8.

Let for and . For any ,

| (7.1) |

where denotes the set of matrices in with some set of columns that each have at least non-zero entries.

Proof.

For , let , and let be the space spanned by the column vectors

Let Then for some implies that for all we have since

We first claim that the set is large, such that if is large, we must have many for which . Let .

Claim 7.9.

With probability , .

Proof.

Fix , and consider the probability that .

Notice that is independent of , and hence

where we used a Chernoff bound (see Lemma A.1) to bound the binomial, and the last two inequalities hold for large enough relative to . By Lemma 7.7, with probability , we have , so we have

Now by Markov’s inequality,

∎

Let denote the event that . Let be the indicator of this event, and let . If , at most vertices can be in the -core but not in . Thus by Markov’s inequality, we have

| (7.2) |

We will break down the probability into several cases, depending on the size of the support of vectors in the kernel of . Let be the set of all such that . By Claim 4.6 and Claim 4.7,

Case 1: has a vector with large support, that is, .

Case 2: has a vector with medium support, that is .

Case 3: does not have any vectors with large or medium support vectors in its kernel, that is, .

We can expand

| (7.3) |

Define to be the restriction of to the indices in the -core of .

To evaluate the probability of the first case, we condition on , and let be any vector of support at least in the kernel of . Observe that cannot hold if is non-zero. Since a is independent from , we have

| (7.4) |

Here the second inequality comes from considering over a larger domain. Combined with eq. 7.2, the contribution from this case yields the first term in the right hand side of eq. 7.1.

For the second case, we bound

| (7.5) |

Combined with eq. 7.2, the contribution from this case yields the second term in the right hand side of eq. 7.1.

In this third case, we will show conditions under which we can algebraically construct a vector such that . This will imply by Claim 4.7 that under those conditions, .

To define these conditions, recall that is the set of all such that . For , let be any vector such that . We next construct a sort of “pseudoinverse" matrix as follows: For , define the column to to be . Define all other entries columns of to be zero. The following claim shows a condition for not holding.

Claim 7.10.

If and , then .

Proof.

Let such that . Hence if , Define to be the vector equal to on the coordinates in and on coordinate . Then

and

Evidently, if , then

so . ∎

By definition, in the third case, we have . Hence

| (7.6) |

Notice that is a function of , so a is independent from . Thus for any set ,

By Lemma 7.7, with probability , we have , thus

| (7.7) |

Combined with eq. 7.2, the contribution from this equation yields the third term in the right hand side of eq. 7.1.

We will break up the second term in eq. 7.6 by conditioning on whether the support of has many entries or not, and then by using the independence of a from :

| (7.8) |

For the second probability on the right hand side, notice that for any positive integers , if x and y are random vectors from some product distributions and respectively, then

Hence since with probability , we have

| (7.9) |

To bound the first probability on the right hand side of eq. 7.8, observe that if and , there must exist at least different such that . So

where the last inequality follows by Markov’s inequality. Plugging this and eq. 7.9 into eq. 7.8 yields

7.3. Proof of Theorem 1.8

We are now ready to prove our main theorem, which we restate here. See 1.8

Proof of Theorem 1.8.

The proof follows by instantiating Lemma 7.8 with the following values: , , , . Here is the constant from Lemma 7.6.

With the following values, it is immediate from the sparse Littlewood-Offord (Lemma 2.1) and quadratic Littlewood-Offord theorems (Lemma 2.2) that the first and last terms in Lemma 7.8 respectively are . The third term is . The two lemmas stated immediately after this proof (Lemmas 7.11 and 7.12) will show that the second and fourth terms are .

Assuming these two lemmas, it follows that with probability , there are no kernel vectors with support size at least in . To rule out any minimal dependencies of less than columns of , we use Lemmas 7.1, 7.5, and 7.6: If there were a minimal dependency among columns of , then it would mean that the matrix , with would:

-

(1)

Contain ’s, because is a -core for and

-

(2)

Be a minimal dependency.

Thus the event of Lemma 7.1 occurs for some , which occurs with probability .

If , then applying Lemmas 7.5, and 7.6 with means that, if , with probability at least , there is no dependency of these sizes in . By Lemma 7.7, with probability .

This rules out all dependencies in with probably , proving the theorem. ∎

Lemma 7.11.

Let for , and let be the constant in Lemma 7.6. For any constant ,

Proof.

This is immediate from the medium and large case Lemmas 7.5 and 7.6, since the -core has size at least with probability . Hence if there was a dependency of columns in the -core for , it would mean there would have to be a set of size at least with such that matrix is a minimal dependency. This implied that the even of Lemma 7.5 or 7.6 occurs. ∎

Lemma 7.12.

Let for , and let be the constant in Lemma 7.6. Then for any constant ,

Lemma 7.13.

Let for , and let be the constant in Lemma 7.6. Let be with the first row removed. Then for any constant ,

Proof of Lemma 7.12 assuming Lemma 7.13.

If such a vector satisfied , then necessarily , where is with the first (zero) coordinate removed, and is with the first row removed. This occurs with probability by Lemma 7.13. ∎

Proof of Lemma 7.13.

By Lemma 7.6, plugging in , with probability , there are no vectors such that where . Since , this implies that there there are no vectors such that where .

Now suppose there was some set of size such that is a minimal dependency. Let , such that is a minimal dependency. It follows that:

-

(1)

;

-

(2)

by definition of the -core, since .

-

(3)

contains no rows with a single , and hence contains at most one row with a single .

This implies that the event of either Lemma 7.1 or Lemmas 7.5 occurs. Such an event occurs with probability . This concludes the lemma. ∎

8. Application to Gradient Codes

In the following section, we will shift our focus to the problem of Gradient Coding. The purpose of this section is to present further applications of our structural characterization beyond analyzing the rank of sparse random matrices.

8.1. Introduction to Gradient Coding

| Assignment Matrix Design | Expected Decoding Error | Adversarial Decoding Error |

|---|---|---|

| Expander Code (Cor. 23 [26]) | - | |

| Pairwise Balanced ([4]) | - | |

| BIBD ( Const. 1 [21]) | - | |

| BRC ([32]) | - | |

| rBGC ([9]) | - | |

| FRC of [28] (and [31]) | ||

| Graph-based Assignment [17] | ||

| This work (Stacked ABC) |

Gradient codes are data replication schemes used in distributed computing to provide robustness against stragglers, machines that are slow or unresponsive [28, 26]. Specifically, such replication schemes can be used to approximately compute the sum of the evaluations of a function over a set of data points . Typically in machine learning, the function represents the gradient of a loss function.

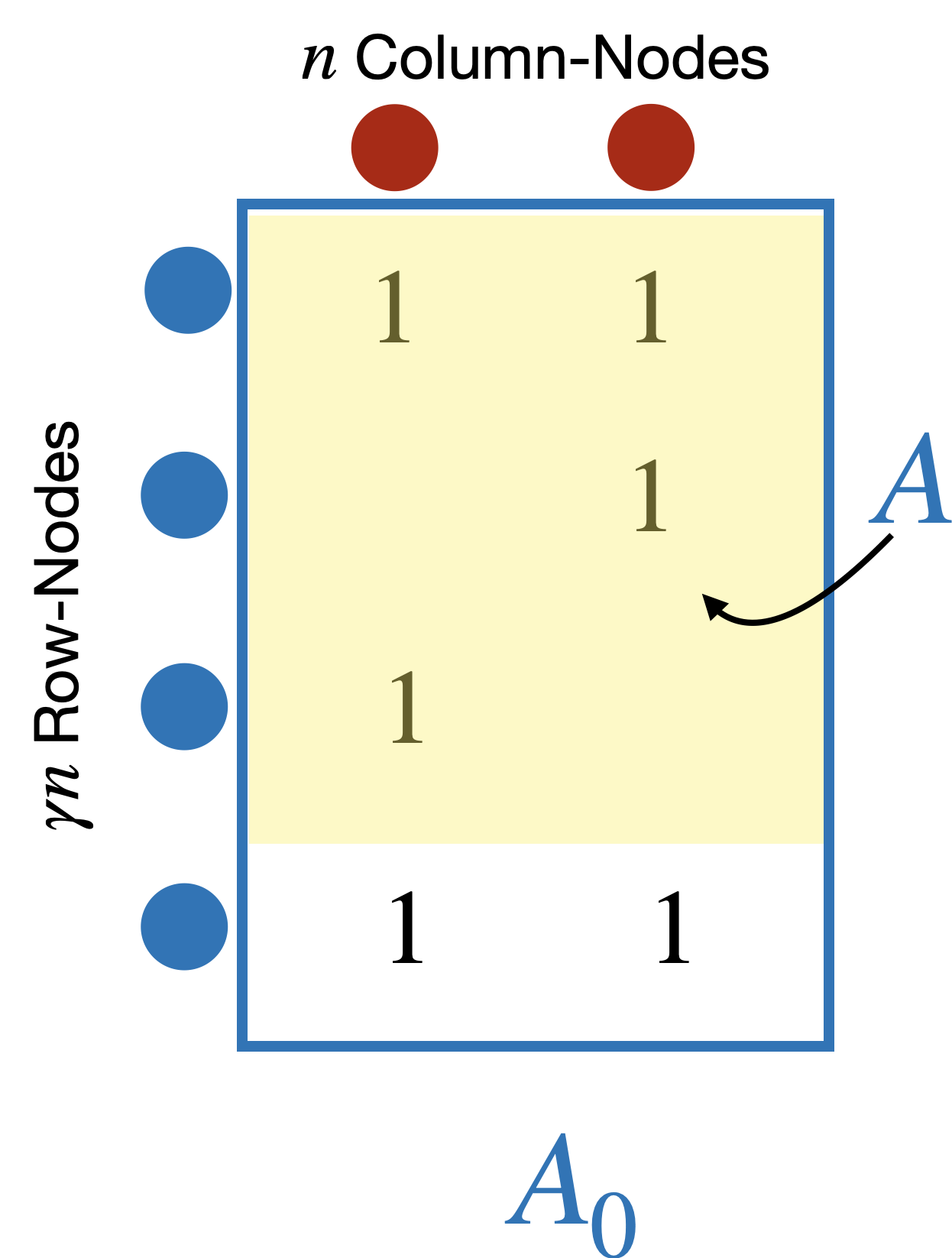

To distribute the computation of while maintaining robustness against stragglers, the data points are distributed redundantly among machines according to an assignment matrix . Each machine is tasked with computing , a weighted sum of over the data it stores. A central server then collects these values for all machines which are not stragglers, and linearly combines the using weights to best approximate .

Formally, we define the decoding error of an assignment along with a set of stragglers to be the squared distance between the all-’s vector, , and the span of the columns :

The decoding error immediately gives us a bound on the approximation error of . Let be the vector in , where . Then for any ,

Hence for any , there exists a vector such that

The gradient coding literature considers two models of decoding error. One in which the set of stragglers is chosen adversarially and one where the set of stragglers is chosen uniformly at random. In the case where is an adversarially chosen fraction of the machines, we consider the adversarial decoding error of :

If is a random fraction of the machines, we consider the expected decoding error of :

A good assignment matrix minimizes the decoding error while keeping the maximum amount of computation per machine — measured by the maximum column sparsity of — small. For an assignment matrix with at most non-zero entries in each column, optimal lower bounds on both the adversarial and random decoding error are known. In particular, Raviv et al. ([26]) showed that the adversarial decoding error must be at least . On the other hand, it is known that the random decoding error is at least , and further, this optimal error is achieved by a design known as the Fractional Repetition Code (FRC) [28]. However, despite its optimality under random stragglers, the FRC of [28] only achieves an adversarial decoding error of . Several works [17, 8] have aimed to design assignment matrices that have small adversarial and expected decoding error, but to our knowledge, no existing assignments have achieved adversarial error that decays in (at any rate) while simultaneously achieving random error that decays faster than like . This leads to the following natural question asked in [17]:

Question 8.1.

Does there exist an assignment matrix which simultaneously has near-optimal random decoding error and near-optimal adversarial decoding error ?

We answer this question in the affirmative. In the rest of this section, we construct a novel gradient code called the Augmented Biregular Code (ABC), and using our structural characterization of linear dependencies, prove that it achieves an expected decoding error of and adversarial decoding error of . In Table 2, we compare the adversarial and expected decoding errors of our work and existing work on gradient coding.

8.2. The ABC and Stacked-ABC Distributions

We use the following process to generate a random matrix from the distribution :

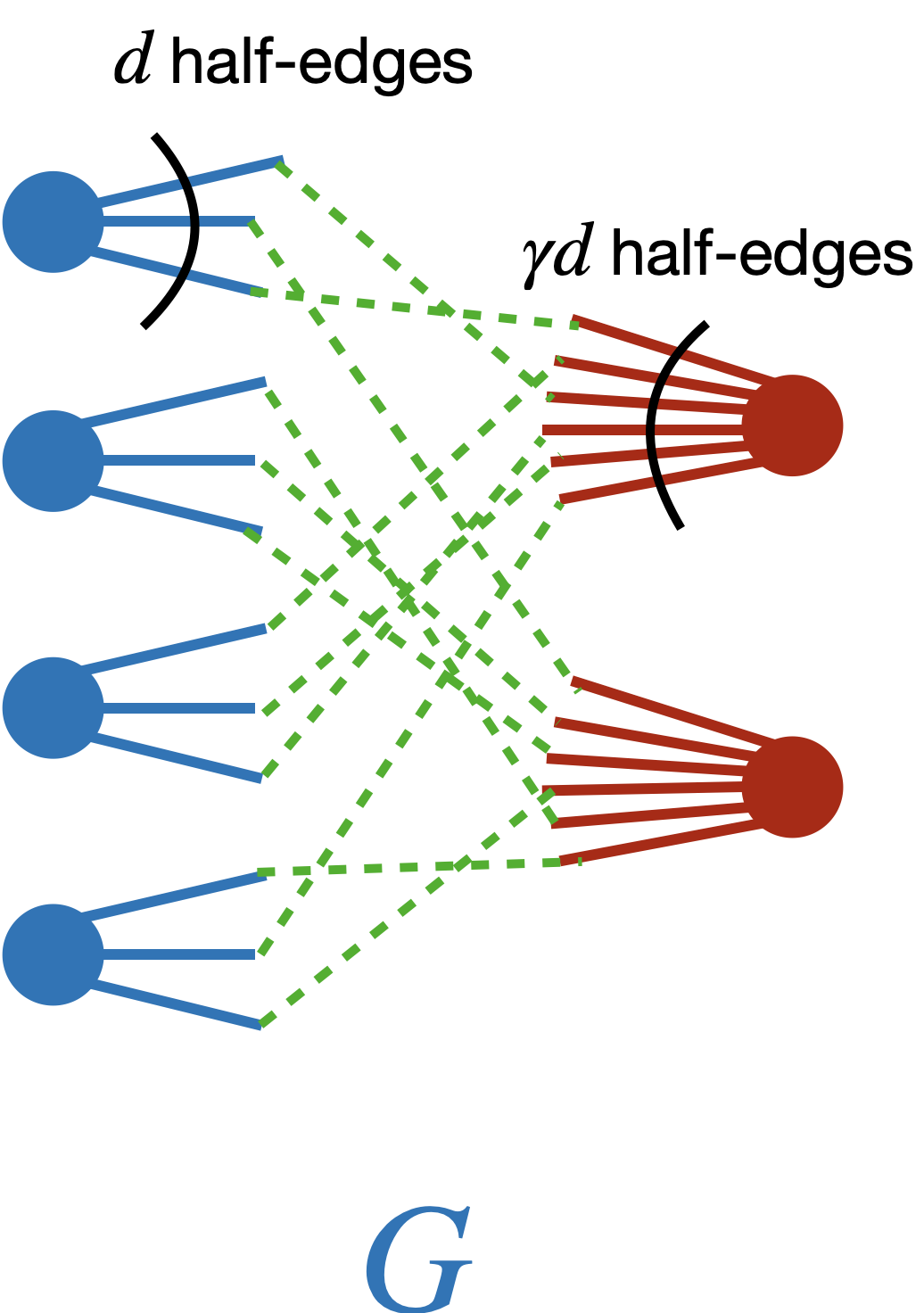

Definition 8.2 (ABC Distribution).

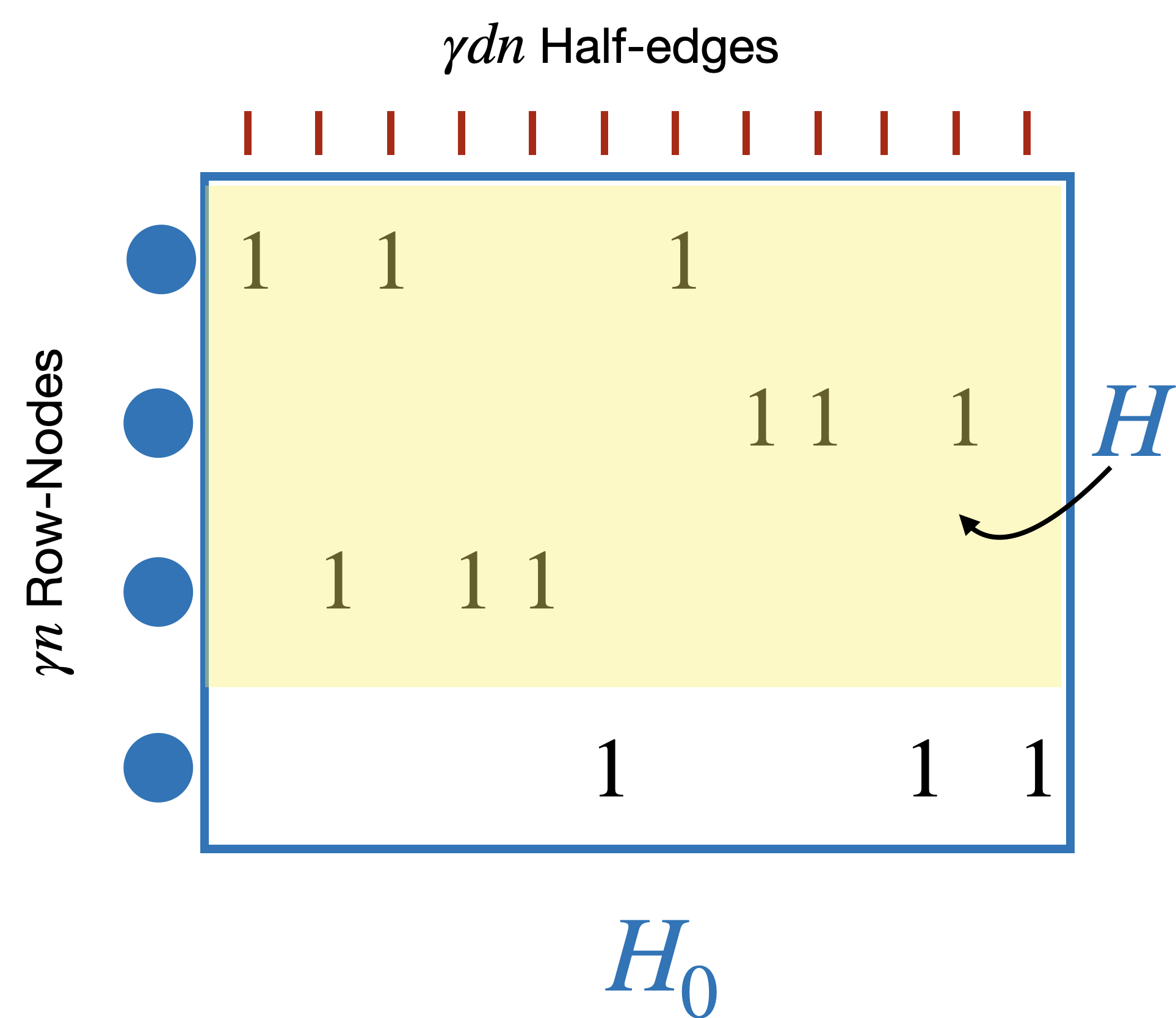

Define to be sampled in the following way. Sample a random permutation . Create row-nodes and column-nodes and associate to each row-node half-edges and to each column node half-edges. Create a multi-graph by pairing the right half-edge to the th left half-edge. Given this bipartite graph, take to be the matrix where if and only if there is at least one edge from row-node to column-node .

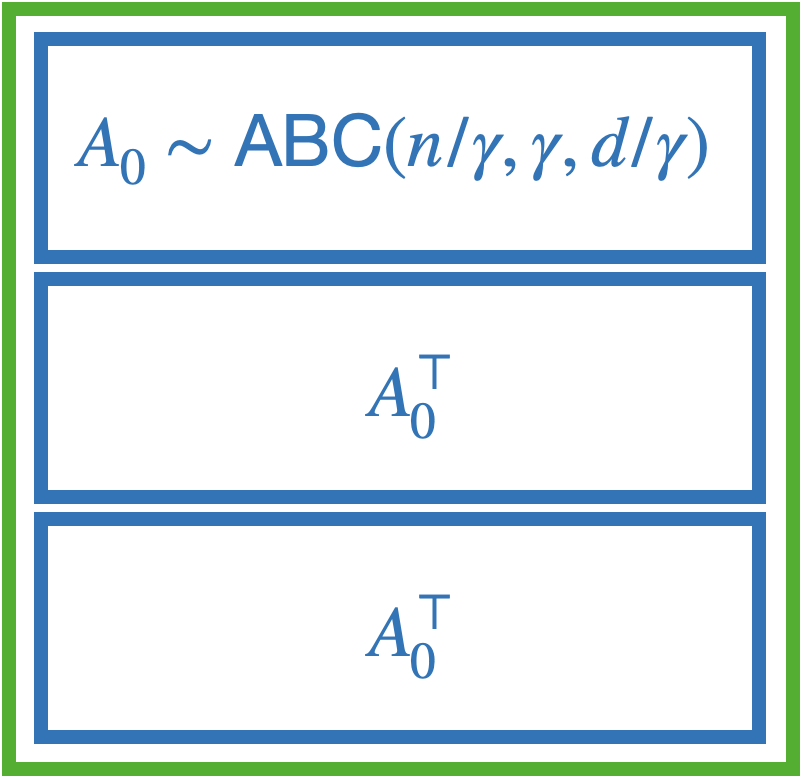

We define a second distribution that results from stacking together several copies of the same transposed ABC matrix to form a square matrix, pictured in Figure 4.

Definition 8.3 (Stacked ABC Distribution).

For such that and , we define the -stacked Augmented Biregular Code to be an matrix formed by sampling and stacking identical copies of . We will denote the distribution of such matrices as .

Using this new distribution of assignment matrices, we prove the following theorem on the decoding error.

Theorem 8.4.

Let be the universal constants from Corollary 8.6. Choose any such that , and . For any divisible by , let . Then with constant probability over the choice of :

and

The main technical parts of Theorem 8.4 follow from the following theorem, which characterizes the minimal dependencies among the columns of the matrix with a random fraction of rows removed. Formally, we define the ensemble of matrices to be given by setting , where .

Theorem 8.5 (Characterization ABC).

There exist universal constants and such that for any , , and , for , with probability :

-

(1)

All minimal dependencies of columns of are in .

-

(2)

The number of columns involved in linear dependencies of is at most , ie.,

The following corollary allows us to deduce the expected decoding error of , leading directly to Theorem 8.4.

Corollary 8.6 (ABC Distance).

Let . For any , there exists constants , and such that for and , with probability ,

Proof.

Let be the set of columns involved in linear dependencies of . Then by Lemma 4.7, for any , we have . It follows that , the vector with in entries indexed by , and elsewhere is in the span of . Thus . Plugging in Theorem 8.5 which give a high probability bound on the size of , yields the corollary. ∎

Remark 6.

Corollary 8.6 it tight in the sense that with probably , . It is easy to check this by counting the number of all-zero rows in .

8.3. Proof Overview

As with the main results of this paper, we split the proof of Theorem 8.5 into two domains: small and large. The goal of the small case is to prove that all small minimal dependencies of columns of must be contained in with high probability. In particular, we prove the following lemma:

Lemma 8.7.

Let for and . Let be any set of size . There exists universal constants and such that if , then:

-

(1)

.

-

(2)

.

-

(3)

.

-

(4)

.

As for the previous results, the goal of the large domain will be to show that with high probability, contains no large set of columns that are linearly dependent.

Lemma 8.8 (ABC Large Case).

Let for some constant . Then there exists a constant such that for ,

Our main tool in proving this Lemma is an anti-concentration Lemma that is based on the sparse Littlewood-Offord Theorem from [13]. While typically such anti-concentration lemmas concern the dot product of a deterministic vector and a random vector with independent entries, we derive a weaker result which concerns the dot product of a deterministic vector with a vector in which there are a fixed number of non-zero entries whose positions are random.

Lemma 8.9 (Anti-concentration for Sparse Regular Vectors).

Let be an arbitrary vector whose most common entry is . Then for any , if is sampled uniformly from the set of vectors with exactly 1s, for any , we have:

Remark 7.

As , the anti-concentration probability approaches the smaller value of , though is tight for .

8.4. Notation and Further Details on Construction of

|

|

|

In our proofs, we will study via the half-edge pairing process used to construction in Definition 8.2. To do this, we will sometimes explicitly consider the permutation which defines the random pairing of half-edges. From , we can can construct an additional matrix , which we call the column half-edge occupancy matrix . Let be the permutation matrix of . From , construct by summing adjacent rows of corresponding to half-edges of the same row nodes. Symbolically,

Note that has rows; row represents row-node in the configuration model. has columns: columns through represent the half edges of column-node , for . Each row contains exactly ’s, corresponding to that row-node’s half edges.

We may write in terms of the random matrix . Because if and only if there is at least one edge from vertex to , we have

Recall that when generating a matrix , we sample and take to be the matrix containing the first rows of . We define to be the first rows of the row half-edge occupancy matrix associated with . For a set with , let be the matrix restricted to the columns corresponding to half-edges of the column-nodes in .

8.4.1. Further Notation

We use to denote the hypergeometric distribution, the random variable which equals the number of successes in draws, without replacement, from a finite population of size that contains exactly objects which are considered successes.

8.5. Small Domain

As noted above, the goal of this section will be to prove the following lemma:

See 8.7

Proof of Lemma 8.7.

We condition on , the number of ’s in . We observe that . Note that is greater than or equal to the number of entries which are in the submatrix , with equality if and only if there does not exist a column-node in which pairs multiple half-edges to the same row-node in .

Let denote the event that there are no rows in with exactly one. It follows from Observation 1 that

Our general strategy to bound relies on the following claim.

Claim 8.10.

Let be the number 1s in which are not the first (leftmost) 1 in their row. If occurs, then .

Proof.

If , then by the pigeonhole principle, there must be at least one row in with a leftmost 1 but no 1s to the right of it, ie. this row has exactly one 1. ∎

We will bound the probability that is large by considering a random walk which this quantity as half-edges are paired one at time. We formalize this random walk as follows.

Conditioned on , the matrix is distributed like a uniformly random matrix on the set of all matrices in with exactly ’s and at most one per column. We construct via the following random process on matrices in , in which the half-edges represented in are paired one at a time. Formally, at each step , we construct from by placing a in a uniformly random location in without a . For , let equal the number of 1s in which are not the first (leftmost) 1 in their row, such that .

When placing the -th , there are at most non-zero rows so far. In particular, since , there are at most non-zero rows throughout this process. Because has rows, we thus have the bound . It follows that the random variable is first-order stochastically dominated by the random variable . So in particular, we have:

which implies

We will use the following claim proved in Appendix E:

Claim 8.11.

Let . There exists constants , and such that for all , and , the following two bounds hold.

For , and , we have:

Further,

Since , it must be the case that Hence if , then necessarily for , which is guaranteed if . Thus we can apply the first bound in Claim 8.11 with , and to study , yielding:

We use the equivalences of , , and from Lemma 3.5 to yield statements 2, 3, and 4 in this lemma.

Next we obtain a bound on the event that . Observe that

If , there must be a column with at least three ’s. So by a similar argument to Claim 8.10, it must be the case that . Hence

Another application of the Claim 8.11 gives us:

This gives us the desired result for sufficiently large and :

This yields the first statement in the lemma. ∎

8.6. Large Case

The main goal of the large case is to prove the following lemma.

See 8.8

We begin by proving the following anti-concentration Lemma.

See 8.9

Proof.

For , let , and let . Then

| (8.1) |

Claim 8.12.

Proof.

By a union bound,

∎

Next we show by induction on that for all . For , we note that the chosen element cannot be the most common element . Thus, is at worst equally as common as the most common element . This implies that the number of times appears in is at most , hence .

Now assume that holds for all . For , we write:

Let such that by the induction hypothesis as if and only if . Thus, we conclude:

Here the second inequality follows from the fact that the optimum over the is achieved by putting the maximum possible mass on , that is, .

Returning to eq. 8.1, we have for all and ,

where the final inequality follows from the fact that for . ∎

To prove Lemma 8.8, we take a similar approach to the large case for the BGC. For a fixed set of size , we consider the stochastic process in which we add the rows of one by one. We define the space:

and let If , then is not a minimal dependency.

Each time we add a new column, either stays constant or decreases by at least (note that can decrease by more than : if a new row has exactly one , then no matter what was). We will use the following lemma to show for , each column we add is close to random. Then, using Lemma 8.9, we show that with decent probability, decreases. We can then apply a Chernoff Bound to show that with high probability.

More formally, we consider the process of constructing (the column half-edge occupancy matrix) one row at a time by pairing the half-edges from each row-node at each step to a random set of unpaired column-half-edges.

Define , that is the number of unpaired half-edges among the column-nodes in after the first row-nodes have randomly paired their half-edges. Observe that . The following lemma uses standard concentration bounds to show that for the first columns, there are many unpaired half-edges out of row-nodes in .

Lemma 8.13.