EiGLasso for Scalable Sparse Kronecker-Sum Inverse Covariance Estimation

Abstract

In many real-world problems, complex dependencies are present both among samples and among features. The Kronecker sum or the Cartesian product of two graphs, each modeling dependencies across features and across samples, has been used as an inverse covariance matrix for a matrix-variate Gaussian distribution, as an alternative to Kronecker-product inverse covariance matrix, due to its more intuitive sparse structure. However, the existing methods for sparse Kronecker-sum inverse covariance estimation are limited in that they do not scale to more than a few hundred features and samples and that the unidentifiable parameters pose challenges in estimation. In this paper, we introduce EiGLasso, a highly scalable method for sparse Kronecker-sum inverse covariance estimation, based on Newton’s method combined with eigendecomposition of the two graphs for exploiting the structure of Kronecker sum. EiGLasso further reduces computation time by approximating the Hessian based on the eigendecomposition of the sample and feature graphs. EiGLasso achieves quadratic convergence with the exact Hessian and linear convergence with the approximate Hessian. We describe a simple new approach to estimating the unidentifiable parameters that generalizes the existing methods. On simulated and real-world data, we demonstrate that EiGLasso achieves two to three orders-of-magnitude speed-up compared to the existing methods.

Keywords: Kronecker sum, sparse inverse covariance estimation, Newton’s method, convex optimization, regularization.

1 Introduction

In many real-world problems for statistical analysis, complex dependencies are found among samples as well as among features. For example, in tumor gene-expression data collected from cancer patients, gene-expression levels are correlated both among genes in the same pathways and among patients with the same or similar cancer subtypes (Dai et al., 2015). Other examples include multivariate time-series data such as temporally correlated stock prices for related companies (King, 1966) or a sequence of images in video data (Kalchbrenner et al., 2017). Gaussian graphical models with -regularization have been widely used to learn a sparse inverse covariance matrix that corresponds to a graph over features (Friedman et al., 2007; Hsieh et al., 2014, 2013). However, they were limited in that samples were assumed to be independent. As an alternative, a multivariate Gaussian distribution has been generalized to a matrix-variate Gaussian distribution, where the sample and feature dependencies were modeled with two separate graphs.

Kronecker-product or Kronecker-sum operators have been used to combine two matrices, each representing a graph over samples and a graph over features, to form an inverse covariance matrix for matrix-variate Gaussian distribution. The Kronecker product of two graphs leads to a hard-to-interpret dense graph and non-convex log-likelihood (Leng and Tang, 2012; Yin and Li, 2012; Tsiligkaridis and Hero, 2013; Zhou, 2014). However, its bi-convexity provided a fast flip-flop optimization method. In contrast, the Kronecker sum has the advantage of producing a sparse graph as the Cartesian product of the two graphs and having a convex log-likelihood, but the existing optimization methods do not scale to large datasets (Kalaitzis et al., 2013; Greenewald et al., 2019). BiGLasso used GLasso as a subroutine to estimate one graph while fixing the other graph in each iteration (Kalaitzis et al., 2013). TeraLasso significantly improved the scalability of BiGLasso with the gradient descent method (Greenewald et al., 2019), but still did not scale to problems with more than a few hundred samples and features.

Another main challenge with the Kronecker sum comes from the unidentifiable parameters in the diagonals of the matrices for feature and sample graphs. BiGLasso did not estimate these unidentifiable parameters. TeraLasso employed a reparameterization to make the parameters identifiable and projected the estimates to the reparameterized space in each iteration. In regression, the Kronecker-sum inverse covariance has been used to model errors in covariates, but the trace of one of the two graphs was assumed to be known (Rudelson and Zhou, 2017; Park et al., 2017; Zhang, 2020). With the Kronecker product, the parameters are unidentifiable as well, but they can be made identifiable with a simple method after the optimization is complete (Yin and Li, 2012).

In this paper, we introduce eigen graphical Lasso (EiGLasso) that addresses these limiations of the existing methods for estimating the Kronecker-sum inverse covariance matrix. Our contribution is two fold. First, we develop an efficient optimization method based on Newton’s method that empirically leads two to three orders-of-magnitude speed-up compared to the existing methods. Second, we describe a simple new approach to identifying and estimating the unidentifiable parameters that generalizes the strategy used in TeraLasso (Greenewald et al., 2019).

For an efficient optimization, we adopt the framework used in QUIC (Hsieh et al., 2014, 2013), the state-of-the-art method for estimating sparse Gaussian graphical models, and extend it to address additional challenges that arise when combining two graphs with the Kronecker-sum operator. Since the gradient and Hessian matrices are far larger with an inflated structure than in QUIC, to reduce the computation time, we leverage the eigendecomposition of the parameters. This eigendecomposition leads to a strategy for approximating the Hessian to further improve the scalability. Extending the theoretical results on the convergence of QUIC, we show EiGLasso achieves quadratic convergence with the exact Hessian and linear convergence with the approximate Hessian. In our experiments, we show that EiGLasso with the approximate Hessian does not require significantly more iterations than EiGLasso with the exact Hessian and achieves two to three orders-of-magnitude speed-up compared to the state-of-the-art method, TeraLasso (Greenewald et al., 2019).

In addition, we introduce a new approach to determining the unidentifiable parameters in Kronecker-sum inverse covariance estimation. Our work is the first to point out that the unidentifiable parameters are uniquely determined given the ratio of the traces of the two parameter matrices for graphs. Building upon this observation, we show that all the quantities involved in Newton’s method, including the gradient, Hessian, the descent directions, and the step size, are uniquely determined regardless of the trace ratio. This allows us to perform the optimization in the original space of the parameters without being concerned about the unidentifiability, rather than in the reparameterized space as in TeraLasso. Furthermore, we show that the parameters can be identified once with the given trace ratio after EiGLasso converges, analogous to the simple approach used in the Kronecker-product inverse covariance estimation (Yin and Li, 2012), rather than in every iteration as in TeraLasso.

Our preliminary work on EiGLasso appeared in Yoon and Kim (2020). While in our earlier work, we presented a flip-flop optimization method as in the Kronecker-product inverse covariance estimation, in this work, we present EiGLasso with the exact Hessian, along with EiGLasso with the approximate Hessian directly derived from the exact Hessian. We investigate the properties of these Hessian matrices and analyze the convergence behavior of EiGLasso. We perform a more extensive experimental evaluation of our method.

The rest of the paper is organized as follows. In Section 2, we review the previous work on statistical methods with the Kronecker-sum operator. We introduce our EiGLasso optimization method in Section 3, study the convergence behavior in Section 4, present experimental results in Section 5, and conlude with future work in Section 6.

2 Related Work

A Gaussian distribution of a matrix random variable for samples and features with a Kronecker-sum inverse covariance matrix (Kalaitzis et al., 2013) is given as

| (1) |

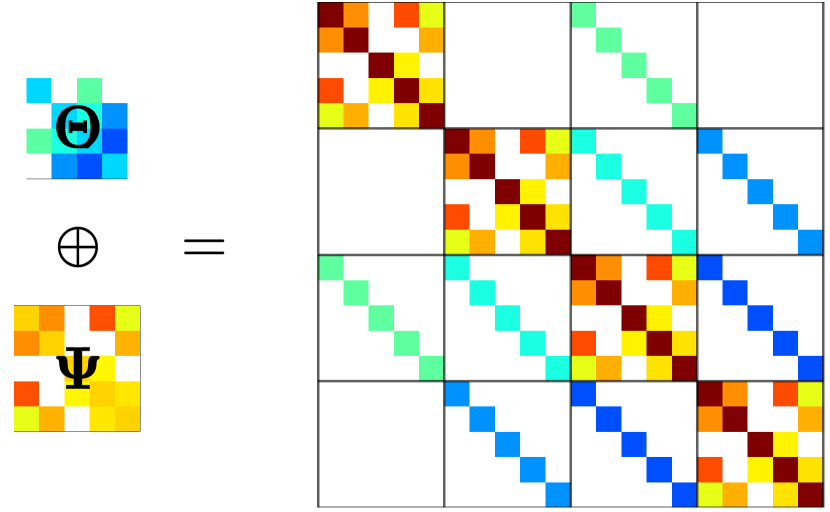

where is the mean and is an operator that stacks the columns of a matrix into a vector. The inverse covariance matrix in Eq. (1) is defined as the Kronecker-sum of two graphs, each given as a matrix and a matrix , modeling dependencies across features and across samples, respectively:

where is the Kronecker-product operator and is an identity matrix. A non-zero value in the th element , , and implies an edge between the th and th nodes in the corresponding graph. The two graphs and are constrained to form a positive-definite Kronecker-sum space as follows:

| (2) |

Then, models a graph over nodes, where each node is associated with an observation for the given sample and feature pair. For the rest of this paper, we assume zero mean, i.e., and focus on the inverse covariance structure.

Compared to the Kronecker product , one main advantage of the Kronecker sum is that as the Cartesian product of the two graphs and , it leads to a more intuitively appealing sparse structure in the graph (Figure 1(a)). In with the Kronecker sum, the sample graph is used only within the same feature (diagonal blocks in in Figure 1(a)) and the feature graph is used only within the same sample (diagonals of off-diagonal blocks in in Figure 1(a)), whereas the Kronecker-product leads to a dense graph, where the sample graph and the feature graph are used even across features and across sample samples. Because of the sparse structure, the Kronecker-sum operator has been adopted in various other statistical methods to represent a sparse association between two sets of variables, such as dependencies between genes and mutations in colorectal cancer (Haupt et al., 2020) and between microRNAs and diseases (Li et al., 2018). It has been embedded in neural networks to model both row and column dependencies in a matrix (Zhang et al., 2018; Gao et al., 2020) and in inputs for more general functions (Benzi and Simoncini, 2017).

Given data , where for for observations, BiGLasso (Kalaitzis et al., 2013) and TeraLasso (Greenewald et al., 2019) obtained a sparse estimate of and by minimizing the -regularized negative log-likelihood of data:

| (3) |

The objective is

with the smooth log-likelihood function and non-smooth penalty , given the sample covariances and , the regularization parameters and , and for the -regularization of the off-diagonal elements of the matrix.

One of the main challenges of solving Eq. (3) arises from the unidentifiable diagonals of and given . Although Greenewald et al. (2019) showed that the objective in Eq. (3) has a unique global optimum with respect to , this does not imply the uniqueness of the pair given , since the set in Eq. (2) forms equivalence classes

| (4) |

Thus, and whose diagonals are modified by a constant and lead to the same . While BiGLasso did not estimate the diagonals of and , TeraLasso formed an identifiable re-parameterization with , where and are forced to have zero traces as follows:

| (5) |

Then, in each iteration of a gradient descent method, TeraLasso projected the gradient to this re-parameterized space and distributed to and as and . For efficient computation and projection of the gradient, TeraLasso employed an eigendecomposition of and : with the eigenvector matrix and the diagonal eigenvalue matrix , and similarly, . TeraLasso exploited the property that the eigendecomposition of the Kronecker sum of and is

| (6) |

Then, the inverse of can be obtained efficiently by inverting the diagonal eigenvalue matrix :

| (7) |

While TeraLasso is significantly faster than BiGLasso, its scalability is limited to graphs with a few hundred nodes.

3 EiGLasso

We introduce EiGLasso, an efficient method for estimating a sparse Kronecker-sum inverse covariance matrix. We begin by describing a simple new scheme for identifying the unidentifiable parameters in Section 3.1. We introduce EiGLasso, Newton’s method with the exact Hessian in Section 3.2 and its modification with approximate Hessian in Section 3.3. In Section 3.4, we describe a simple strategy for identifying the diagonal parameters during EiGLasso estimation. In Section 3.5, we discuss additional strategies for improving the computational efficiency.

3.1 Identifying Parameters with Trace Ratio

Theorem 1 below provides a simple approach to identifying the diagonal elements of and , given and the ratio of the traces of and .

Theorem 1

Assume that the trace ratio of to is given as . Then, a Kronecker-sum matrix can be mapped to a unique pair of symmetric matrices with the diagonals of and identified as

| (8) | ||||

where is a one-hot vector with a single at the th entry and ’s elsewhere.

Proof Given , and are unique, since for any , . From the definition of Kronecker sum, we notice

| (9) |

and

| (10) |

From the trace ratio and Eq. (10), we have . Plugging this into Eq. (9), we identify as

The case for can be shown in a similar way.

Theorem 1 suggests that it is possible to identify the diagonals of and by solving Eq. (3) with the linear constraint :

| (11) |

where the second constraint with is equivalent to . To handle this additional constraint explicitly, the substitution method or Newton’s method for equality-constrained optimization problem could be used (Boyd and Vandenberghe, 2004). Instead, in Sections 3.2 and 3.4, we show that in EiGLasso, because of the special problem structure, it is sufficient to solve Eq. (3) with Newton’s method, ignoring the equality constraint, and to adjust the diagonals of and once after convergence to satisfy the constraint.

3.2 EiGLasso with Exact Hessian

We introduce EiGLasso for an efficient estimation of sparse and that form a Kronecker-sum inverse covariance matrix. We adopt the framework of QUIC (Hsieh et al., 2014), Newton’s method for estimating sparse Gaussian graphical models. In each iteration, QUIC found a Newton direction by minimizing the -regularized second-order approximation of the objective, and updated the parameters given this Newton direction and the step size found by backtracking line search (Bertsekas, 1995; Tseng and Yun, 2009). Using the same strategy, EiGLasso finds Newton directions, for and for , by minimizing the following second-order approximation of the smooth part of the objective in Eq. (11) with the -regularization:

| (12) | |||

where

with the gradient and Hessian

| (13) | |||

| (14) |

As we will show in Section 3.4, the objective above can be optimized without being concerned about the equality constraint. Thus, the coordinate descent optimization can be used to solve Eq. (12) as in QUIC. Given the descent directions and , we update the parameters as and , with the step size found by the line-search method in Algorithm 1.

Two key challenges arise in a direct application of QUIC to Kronecker-sum inverse covariance estimation. First, as we detail in the next section, the gradient and Hessian involves the computation of the matrix significantly larger than a matrix required for a single graph in QUIC. Second, the constraint on the trace ratio in Eq. (12) needs to be considered to handle the unidentifiability of the diagonals of and during the optimization process. In the rest of Section 3, we describe how we address these challenges by leveraging the eigen structure of the model, and provide the details of the EiGLasso optimization outlined in Algorithm 2.

-

1.

,

, where .

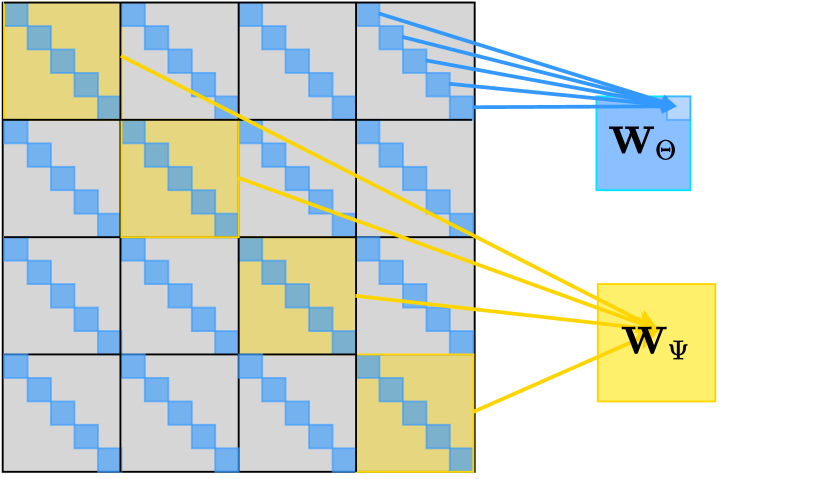

3.2.1 Efficient Computation of Gradient and Hessian via Eigendecomposition

In Lemma 2 below, we provide the form of the gradient in Eq. (13) and Hessian in Eq. (14). We show that can be represented in a significantly more compact form than what has been previously presented in Kalaitzis et al. (2013) and Greenewald et al. (2019). We exploit this compact representation to further reduce the computation time via eigendecomposition of and in Theorem 3.

Lemma 2

Proof Let be a one-hot matrix with at the th element and zero elsewhere. Then, for the gradient , we have

By using , we collect the elements to obtain Eqs. (15) and (16). The case for can be shown similarly. Now, for the Hessian, we have

| by for symmetric matrices , , and , and , | ||||

We collect the elements into a matrix

The cases for and can be shown in a similar way.

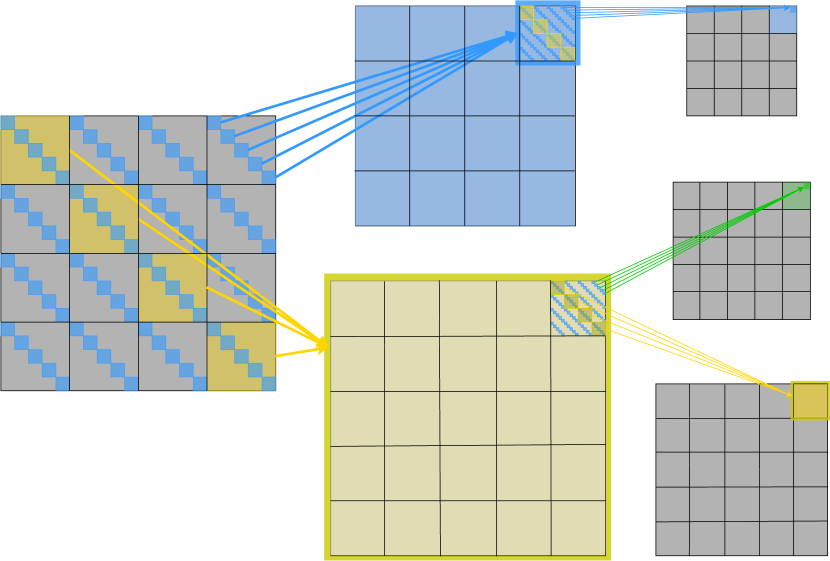

According to Lemma 2, the gradient is obtained by collapsing as in Eq. (16) and the Hessian is obtained by collapsing as in Eq. (17). This collapse is illustrated in Figure 1(b) for the gradient. While the Kronecker sum inflates and into (Figure 1(a)), this inflated structure gets deflated, when computing and in the gradients from (Figure 1(b)). This deflation can be viewed as applying the mask , where is a matrix of one’s, to to obtain such that if , otherwise , and replacing in Eq. (16) with . In other words, only the non-zero elements of contribute towards (blue in Figure 1(b)) and (yellow in Figure 1(b)). The collapse of in Eq. (17) to obtain the Hessian can be viewed as the same type of deflation applied twice to (details in Appendix A).

Lemma 2 reveals the challenge in computing and in a direct application of QUIC to the Kronecker-sum model: involves computing the large matrix and involves computing the even larger matrix . In Theorem 3 below, we show that and can be obtained via eigendecomposition of and without explicitly constructing and .

Theorem 3

Given the eigendecomposition and with the th smallest eigenvalue and in the th element of and , the gradient in Eq. (15) is given as

| (18) |

where

For the Hessian, we have

| (19) |

where

| (20) | ||||

and above are stretched identity matrices, and , where is a one-hot matrix with at the th element and zero elsewhere, and .

Proof We prove for , , and , because the case for and can be proved similarly. Let and be the th eigenvectors of and , given as the th columns of and . Then, we can re-write Eq. (7) as

| (21) |

For , we substitute in in Eq. (16) with Eq. (21):

This is equivalent to in Eq. (18), since the summation can be performed over , instead of over .

To show , we again substitute in of Eq. (17) with Eq. (21).

For , we substitute in of Eq. (17) with Eq. (21).

Theorem 3 provides a significantly more efficient method for computing and , compared to Lemma 2. Since and can be written entirely in terms of the eigenvectors and eigenvalues of and , the operations that involve is replaced with the cheaper operation of eigendecomposition with time and space . TeraLasso also used the eigendecomposition of and in each iteration of the optimization. However, TeraLasso has done this for an efficient projection of the gradient to the re-parameterized space, whereas EiGLasso performs the eigendecomposition for an efficient computation of and in the original parameter space.

It follows from Theorem 3 that ’s in the same equivalence class in Eq. (4) differ only in their eigenvalues, but not in eigenvectors. The equivalence class in Eq. (4) can be written equivalently as

| (22) |

since and similarly for . We exploit this feature to handle the unidentifiable parameters during estimation in Section 3.4 and to analyze the convergence in Section 4.

In the theorem below, we prove several properties of that we will use to prove the line-search properties, convergence guarantees, and convergence rates in Section 4.

Theorem 4

The Hessian in EiGLasso has the following properties:

-

•

It is positive semi-definite with the null space .

-

•

On the Kronecker-sum space in Eq. (2), is positive definite. The minimum eigenvalue outside of the nullspace and the maximum eigenvalue are given in terms of the eigenvalues of and :

Proof To prove the first property, from Lemma 2, we notice that since is positive definite, the null space of is given by and that satisfy

Since the left-hand side of the above can be written as

the null space of is given by and that satisfy .

To prove the second property, we notice that the null space of is outside of the constraint region ; thus, is positive definite on the Kronecker-sum space in Eq. (2). To find the eigenvalues of , we first find the eigenvalues of

by finding the solutions of the characteristic equation :

Thus, the eigenvalues of are , , , and , each with the algebraic multiplicity , , , and 1. From Eq. (17), for any unit vector ,

where and are the minimum and maximum eigenvalues of . Combining this with the minimum eigenvalue and the maximum eigenvalue of outside of the null space of results in

which completes the proof.

3.3 EiGLasso with Approximate Hessian

While EiGLasso pre-computes and stores after eigendecomposing and at the beginning of the coordinate descent to solve Eq. (12), explicitly computing and storing the matrix is still expensive for large and even with the eigendecomposition. To further reduce the computation time and memory, we approximate based on its form in Theorem 3 as follows. We first drop while keeping only and . Since pre-computing and storing the matrix and the matrix is still expensive, we approximate and by approximating their eigenvalues and in Eq. (19), while keeping the same eigenvectors and . The resulting approximate Hessian is

| (23) |

where

| (24) | ||||

In , we keep only the components ’s of in Eq. (20) that contain the smallest eigenvalues . These smallest eigenvalues have the largest contribution toward , since the eigenvalues of contribute to the eigenvalues of through their inverses. We replace the remaining components with , because dropping the eigenvalue components in would amount to assuming that has eigenvalues of infinite magnitude. This approximation leads to the following form

where and . Then, during the coordinate descent optimization, we pre-compute and store ’s and ’s for , and compute the Hessian entries from ’s as needed in each coordinate descent update (details in Appendix B). We assume the same for both and , though this can be relaxed. In our experiments in Section 5 we demonstrate that often suffices.

We provide a geometric interpretation of our approximation of with . Assuming Eq. (12) without the -regularization, we have the descent direction with the exact Hessian and with the approximate Hessian. Since and share the same eigenvectors, in the coordinate system defined by these eigenvectors as bases, the descent directions become with the exact Hessian and with the approximate Hessian (Boyd and Vandenberghe, 2004). The latter is an element-wise scaled matrix of the former. Furthermore, since , in this new coordinate system, each element of the descent direction with is a convex combination of and the corresponding element of the descent direction with .

The following theorem provides the properties of , which will be used to analyze the convergence of EiGLasso in Section 4.

Theorem 5

The approximate Hessian is positive definite. Furthermore, its minimum and maximum eigenvalues are

where

Proof

Since a block-diagonal matrix has the same set of eigenvalues as those of its diagonal blocks,

the eigenvalues of are the same as a union of those of

and in Eq. (24).

The eigenvalues of and are positive, because they

are also the eigenvalues of

in Eq. (7), the inverses of which are the eigenvalues of the positive definite

matrix in Eq. (6). Thus, is positive definite.

3.4 Estimation with the Unidentifiable Parameters

We describe a simple approach to estimating the diagonals of and with EiGLasso. We show that to solve the optimization problem with the constraint on a fixed trace ratio in Eq. (11), it is sufficient to solve the unconstrained problem in Eq. (3) and to adjust the diagonals once to enforce the given trace ratio after EiGLasso converges.

In Lemma 6 below, we show that given the current estimate of and , the quadratic approximation in Eq. (12) for determining descent directions is uniquely defined.

Lemma 6

Within the same equivalence class that contains the current estimate of , , , and are uniquely defined. Thus, the second-order approximation in Eq. (12) is uniquely defined.

Proof According to Eq. (22), the unidentifiability in the diagonal elements of and reduces to the unidentifiability in the eigenvalues of and . In the gradient in Eq. (18) and Hessians in Eqs. (19) and (23), the eigenvalues of and always appear as a pair, where the shift cancels out as follows:

Thus, , , and are unaffected by the shift in the diagonals of and .

Lemma 6 allows us to solve the problem in Eq. (12) to obtain the descent directions , ignoring the constraint on the trace ratio. However, if is a solution to the problem in Eq. (12), then for is also a solution, forming an equivalence class

| (25) |

Lemma 7

Proof

We only need to show that , a term that appears in the computation of

in Algorithm 1, is invariant within the equivalence class in Eq. (25),

since and always appear as Kronecker sum of the two in all the other parts

of the line search such that and in Eq. (25) cancel out.

We have , which

can be directly verified from Eqs. (15) and (16) in Lemma 2

as .

From this, we have , which proves is unaffected by the

unidentifiable diagonals of and .

With Lemmas 6 and 7, we can minimize the EiGLasso objective in Eq. (11) by updating and with and step size and adjusting the diagonals of and using Theorem 1 after each update. The theorem below shows this procedure can be simplified even further.

Theorem 8

In EiGLasso, given the trace ratio , it is sufficient to identify the diagonals of and only once after convergence. This leads to the identical estimate obtained by identifying the diagonals of and in every iteration to maintain the trace ratio . At convergence, the diagonal elements of are adjusted by the scalar factor

| (26) |

Proof

Regardless of which member of the equivalence class is used to update

the current estimate of , we arrive at the same equivalence class

for the estimate of after the update. From Lemma 6,

given this equivalence class , the problem in Eq. (25)

in the next iteration is uniquely defined. Thus, regardless of whether we adjust the diagonals

to meet the constraint on the trace ratio, the sequence of equivalence class

over iterations is the same, and it is not necessary to identify the diagonals

in each iteration of Newton’s method. The adjustment in Eq. (26) is found

by applying Theorem 1 to with the current estimate of

and .

When we set , the one-time identification of diagonal parameters with Eq. (26) in EiGLasso becomes identical to the identification of the parameters that TeraLasso (Greenewald et al., 2019) performs at the end of every iteration. At the end of each iteration, TeraLasso evenly distributes between the re-parameterized and in Eq. (5) and performs the update and similarly for . It is straightforward to show that with and from Eq. (10), Eq. (26) reduces to this update in TeraLasso. Theorem 8 is analogous to the simple approach to handling the unidentifiability of the parameters in Kronecker-product inverse covariance estimation (Yin and Li, 2012), where for any positive constant . The parameters are identified by rescaling and as and with some constant such that is equal to 1 after convergence, similar to the one-time identification in EiGLasso.

3.5 Active Set and Automatic Detection of Block-diagonal Structure

In the graphical lasso, a simple strategy for reducing computation time has been introduced that detects the block-diagonal structure in the inverse covariance parameter from the sample covariance matrix prior to estimation (Witten et al., 2011; Mazumder and Hastie, 2012). Then, only the parameters within the blocks corresponding to the connected components in the graph need to be estimated. In Theorem 9 below, we show that a similar strategy can be applied to EiGLasso with both the exact and approximate Hessian, to detect the block diagonal structures in and from the sufficient statistics and .

Theorem 9

The block-diagonal structure of can be detected by thresholding such that iff . Similarly, the block-diagonal structure of can be detected by thresholding such that iff .

Proof Let denote the subgradient of the norm of a matrix, i.e., is if , if , and if . Then, the Karush-Kuhn-Tucker conditions (Boyd and Vandenberghe, 2004; Witten et al., 2011) for in Eq. (3) is

| (27) |

where is given in Eq. (16).

If is block-diagonal, is also block-diagonal, since and

have the same eigenvectors according to Lemma 2 and Theorem 3.

This implies that if

in the off-diagonal blocks,

in Eq. (27).

The case for can be proven similarly.

QUIC further showed that their active-set strategy amounts to detecting a block-diagonal structure in the first iteration, if the parameters are initialized to a diagonal matrix. This strategy can be extended to EiGLasso, when an approximate Hessian is used. To reduce the computation time, as in QUIC, in each Newton iteration, EiGLasso detects the active set of and

and update only the parameters in the active sets during the coordinate descent optimization, while setting those in the fixed set to zero. When and are initialized to diagonal matrices, the approximate Hessian in iteration 1 is diagonal, since the eigenvector matrices and are diagonal. Then, the optimization problem in Eq. (12) decouples into a set of optimization problems, each of which involves a single element of and has a closed-form solution for as

The soft-thresholding operator above is defined as , where if and if . This closed-form solution is if , which is equivalent to the condition for detecting the block-diagonal structure in from in Theorem 9. The case for can be shown similarly.

4 Convergence Analysis

We examine the properties of the line-search method in Algorithm 1 and analyze the global and local convergence of EiGLasso.

4.1 Line Search Properties

EiGLasso inherits some of the line-search properties shown for QUIC (Hsieh et al., 2014). This is because our objective in Eq. (3) can be written in terms of in the form that resembles the objective of QUIC

where , with an matrix of one’s , and is an element-wise multiplication operator. Then, the EiGLasso’s update and can be written as , where , since . We extend these results for , to prove the results for individual and , where , when unlike in QUIC the exact Hessian is not positive definite everywhere (Theorem 4), and when the approximate Hessian is used.

We begin by showing that both and have bounded eigenvalues in the level set and are Lipschitz-continuous. This result will be used to prove the line-search properties and global and local convergence.

Lemma 10

In the level set , and are Lipschitz continuous and have bounded eigenvalues:

for some constants that depend on , , , and .

Proof We bound the eigenvalues of , , and , and use these bounds to bound the eigenvalues of and . When the diagonals are not identified, it directly follows from Lemma 2 in Hsieh et al. (2014) that all EiGLasso iterates of are contained in the set with bounded eigenvalues of

| (28) |

Next, given a fixed trace ratio , we bound the eigenvalues of and . Since Eq. (28) implies , we apply Theorem 1 to to identify and in the equivalence class in Eq. (22) given , thus, identifying the diagonals of and . We bound each of the two terms in Eq. (8) for as

and combine these to obtain the eigenvalue bounds for and similarly for

| (29) |

From Eq. (28) and Theorem 4,

we obtain the bound on the eigenvalues

of . From Eq. (28) and Theorem 5,

we obtain the bound on the eigenvalues

of ,

since ,

,

,

.

On the set in Eq. (29),

since the log-determinant is a continuous function of class , and a continuous function on a compact set is bounded, both and are locally Lipschitz-continuous.

Now, for EiGLasso with exact and approximate Hessian, we show that the following three line-search properties hold: the line search method is guaranteed to terminate for any symmetric matrices and , as the two line search conditions in Algorithm 1 are satisfied for some step size (Lemma 11); the update with the Newton direction is guaranteed to decrease the objective (Lemma 12); and EiGLasso with the exact Hessian is guaranteed to enter pure-Newton phase where the step size is always chosen. We state and prove the first two properties. The proof of the last property follows directly from the proof in Tseng and Yun (2009) and Hsieh et al. (2014).

Lemma 11

For any and , where , and symmetric matrices and for descent directions found with either the exact or inexact Hessian, there exists a step size such that for all the two conditions in the line search in Algorithm 1 are satisfied.

Proof

If ,

the updated estimates and

satisfy ,

since

and we have and .

Thus, the first line-search condition in Algorithm 1 is satisfied.

From Lemma 1 in Tseng and Yun (2009) and Proposition 3 in Hsieh et al. (2014), it is straightforward

to show the second condition in Algorithm 1 is satisfied.

Lemma 12

Proof

For , the first inequality in Eq. (30) can be shown by a

straightforward application of Lemma 1 and Theorem 1 in Tseng and Yun (2009) and Proposition 4

in Hsieh et al. (2014). To prove the second and third inequalities, since our is not

positive definite everywhere, we need to show that is outside of the nullspace of described in Theorem 4, unless EiGLasso is at the optimum, where .

The null space of , ,

is equivalent to ,

which is the equivalence class of the optimality condition .

This proves the third inequality in Eq. (30) that holds except when .

For , the first inequality in Eq. (31) can be again shown

from Lemma 1 and Theorem 1 in Tseng and Yun (2009) and Proposition 4 in Hsieh et al. (2014).

The second and third inequalities hold since is positive definite.

4.2 Convergence Analysis

To show the global convergence of EiGLasso, as in QUIC, we use a more general non-smooth optimization framework, the block coordinate descent studied in Tseng and Yun (2009). EiGLasso satisfies the following two conditions required to guarantee that the block coordinate descent algorithm converges to the global optimum. First, the objective function of EiGLasso has a bounded positive definite exact or approximate Hessian in the level set : for some positive constants , according to Theorems 4 and 5, and Lemma 10. Second, EiGLasso with the exact or approximate Hessian chooses a subset of variables to be updated in each iteration according to the Gauss-Seidel rule: with , at iteration , EiGLasso updates one of the two subsets of variables, and , where is the entire set of variables and and are active sets in Algorithm 2. Therefore, EiGLasso is guaranteed to converge to the global optimum according to Tseng and Yun (2009).

Now we analyze the local convergence of EiGLasso. We adopt a similar strategy used in QUIC (Hsieh et al., 2014): convergence analysis on a smooth function is applied near the global optimum, where the -regularized non-smooth objective becomes locally smooth.

Theorem 13

Near the optimum, where step size is chosen, EiGlasso with the exact Hessian converges to the optimum quadratically. EiGLasso with the approximate Hessian converges to the optimum linearly.

Proof

Since the exact Hessian is Lipschitz continuous from Lemma 10,

the proof for EiGLasso with the exact Hessian follows from Lemma 2.5 and Theorem 3.1 of

Dunn (1980).

While the convergence analysis in Dunn (1980) assumes that the Hessian is positive definite,

the exact Hessian in EiGLasso is not positive definite everywhere.

However, according to Theorem 4, our Hessian

is positive definite for all iterates ,

since is outside of the null space of , so

the analysis in Dunn (1980) can be applied to EiGLasso.

The proof for EiGLasso with the approximate Hessian follows from the analysis of steepest descent with the quadratic norm (Boyd and Vandenberghe, 2004),

given the bounded eigenvalues of according to Lemma 10.

5 Experiments

We compare the performance of EiGLasso with that of TeraLasso (Greenewald et al., 2019) on simulated data and on real-world data from genomics and finance. TeraLasso is the state-of-the art method for Kronecker-sum inverse covariance estimation, and has been shown to be substantially more efficient than BiGLasso (Kalaitzis et al., 2013), so we did not include BiGLasso in our experiments. We implemented EiGLasso in C++ with the sequential version of Intel Math Kernel Library. We downloaded the authors’ implementation of TeraLasso and modified it to perform more iterations during line search, when the safe-step approach suggested by the authors failed to find a step-size that satisfies the positive definite condition on . All experiments were run on a single core of Intel(R) Xeon(R) CPU E5-2630 v3 @ 2.40GHz. In all of our experiments, we selected the regularization parameters for EiGLasso and used the selected for TeraLasso, because EiGLasso is significantly faster than TeraLasso and minimizes the same objective as TeraLasso. To assess convergence, we used the criterion that the decrease in the objective function value at iteration satisfies the condition for three consecutive iterations.

5.1 Simulated Data

We compared EiGLasso and TeraLasso on data simulated from the known and . We used the true and of different sizes ( 100, 200, 500, 1000, 2000, and 5000), assuming two types of graph structures.

-

•

Random graph: To set the ground-truth , we first generated a sparse matrix by assigning , 0, or 1 to each element with probabilities , , and , respectively. We chose such that the number of non-zero elements of is . To ensure is positive definite, we set to after adding with to each diagonal element of .

-

•

Graph with clusters: We set to a block-diagonal matrix such that each block corresponds to a cluster. For graphs with and , we assumed five blocks, each with size . For larger graphs with , 1000, 2000, and , we assumed 10 blocks, each with size . Each block was generated as a random graph described above, setting so that we have nonzero elements in the block.

The ground-truth was set similarly. Given these parameters, we simulated matrix-variate data from Gaussian distribution with mean zeros and inverse covariance .

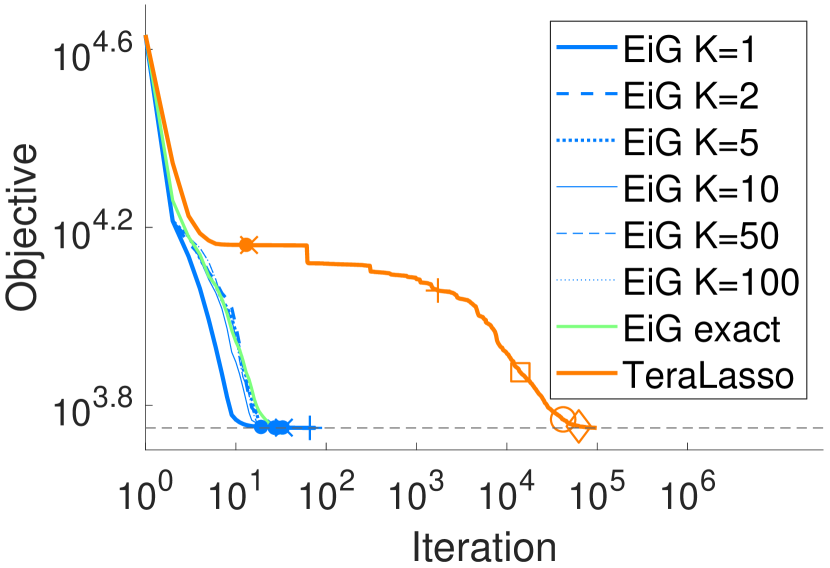

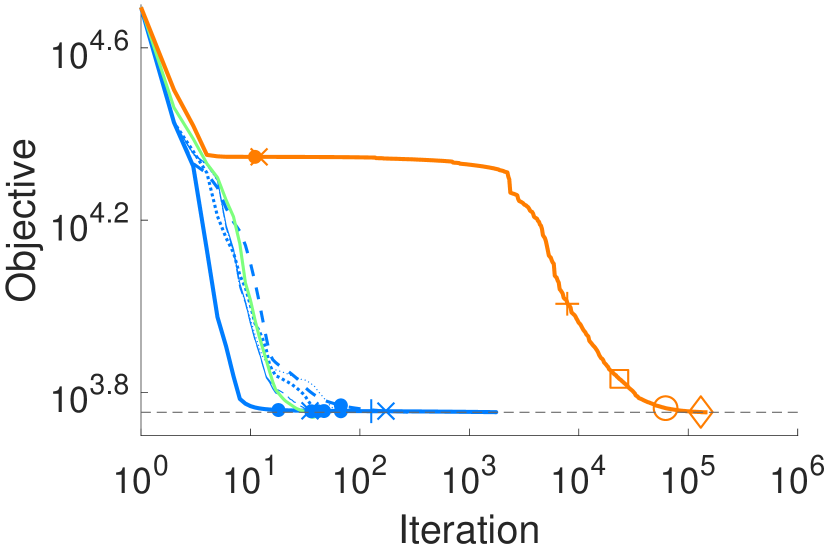

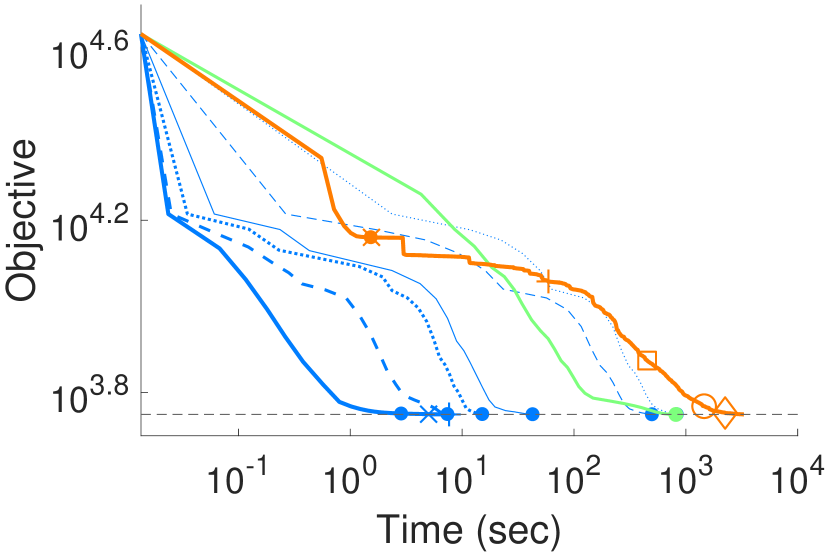

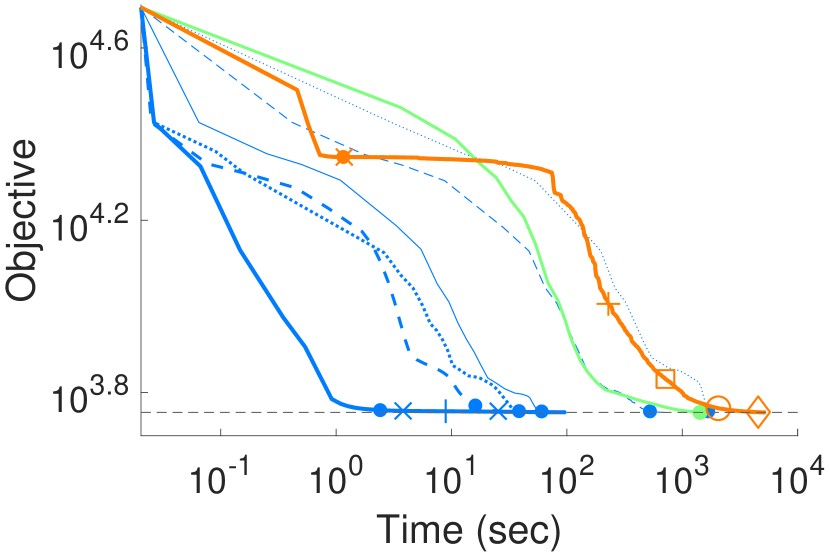

First, we evaluated TeraLasso and EiGLasso on simulated data with graph size . The two methods were compared in terms of computation time and the number of iterations required to reach the same level of optimality, which we define as the objective value that EiGLasso with the exact Hessian converged to with the convergence criterion . The regularization parameters were selected such that the number of non-zero elements in the estimated parameters roughly matches that of the true parameters. EiGLasso with approximate Hessian was run with different ’s ranging from to . Results are shown for four datasets, two from random graphs (Figures 2(a)-(d)) and two from graphs with clusters (Figures 3(a)-(d)). Regardless of the degree of Hessian approximation, EiGLasso required significantly fewer iterations than TeraLasso (Figures 2(a)-(b) and 3(a)-(b)), as expected since methods that use the second-order information in general converge in fewer iterations than the first-order methods. With the exact Hessian and approximate Hessian with large , EiGLasso took longer in each iteration than TeraLasso, but overall required two to three times less computation time than TeraLasso (Figures 2(c)-(d) and 3(c)-(d)). As we reduced , the time taken by EiGLasso decreased substantially, and EiGLasso with achieved two to three orders-of-magnitude speed-up compared to TeraLasso.

| Graph | EiGLasso | TeraLasso | ||||||

|---|---|---|---|---|---|---|---|---|

| Random Graphs | 100 | 1 | 4 | 6 | 40 | 729 | 1019 | 4194 |

| 200 | 7 | 164 | 551 | 3059 | 27049 | 70311 | 16765 | |

| 500 | 29 | 155 | 2252 | 5994 | 31826 | |||

| 1000 | 515 | 11601 | 39568 | |||||

| 2000 | 6361 | |||||||

| 5000 | 10458 | |||||||

| Graphs with Clusters | 100 | 2 | 21 | 28 | 629 | 6516 | 12443 | 21115 |

| 200 | 11 | 410 | 930 | 1042 | 11281 | 59813 | ||

| 500 | 28 | 5231 | 9252 | 10549 | ||||

| 1000 | 2169 | 12614 | 58168 | |||||

| 2000 | 9310 | |||||||

| 5000 | 10461 | |||||||

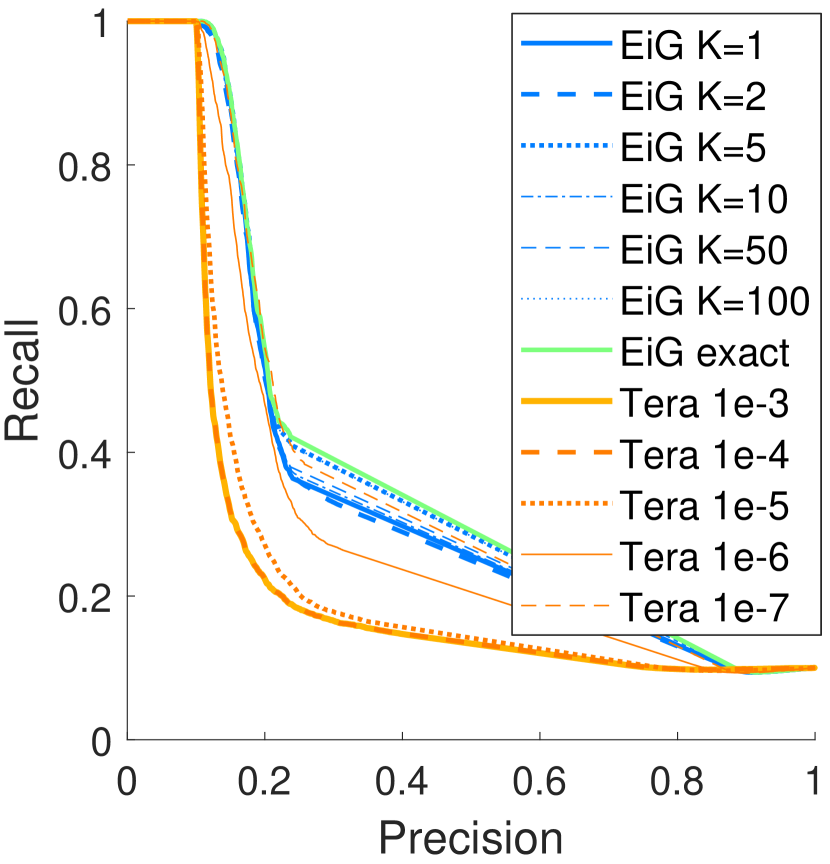

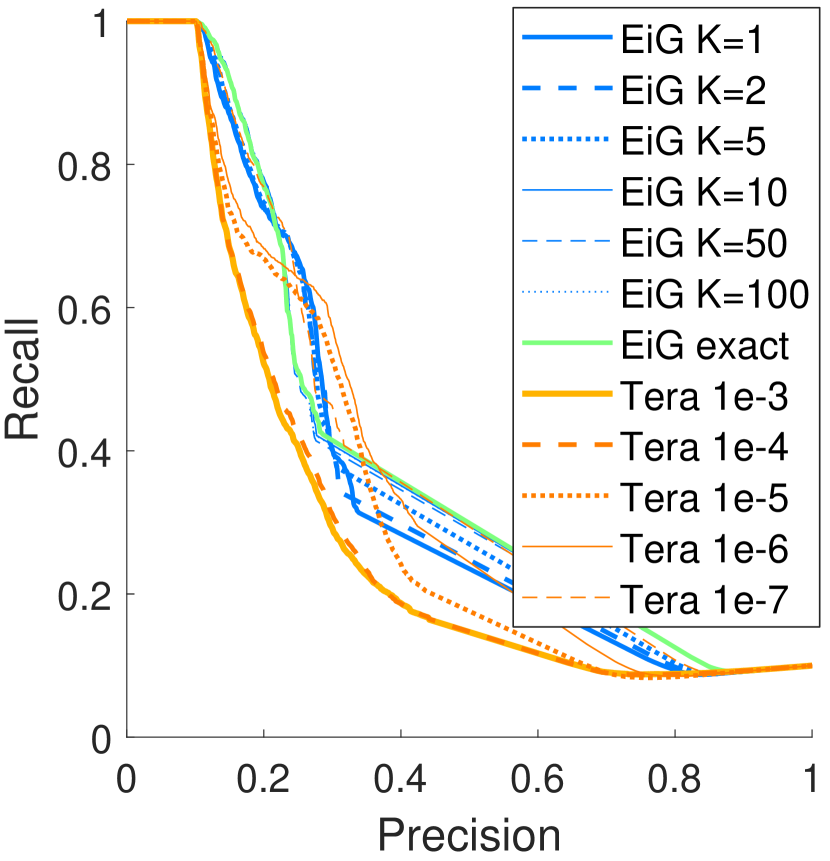

We compared TeraLasso and EiGLasso on the accuracy of the recovered non-zero elements in and , using 10 datasets simulated as above. The precision-recall curves averaged over the 10 simulated datasets (Figure 2(e) and 3(e)) show that the TeraLasso estimates at the convergence criterion and are significantly inferior to the EiGLasso estimates at the same . TeraLasso needed to achieve the accuracy similar to EiGLasso at , whereas more stringent criteria such as and led to nearly identical results in EiGLasso. Thus, in all experiments in the rest of Section 5, we used as convergence criterion for EiGLasso with all ’s, but ran TeraLasso until it reached the similar objective value that EiGLasso reached with , which typically required , or .

Next, we compared the computation time of TeraLasso and EiGLasso on data simulated from larger graphs. For datasets with size , and , we ran TeraLasso and EiGLasso with varying and recorded the time taken by each method if it converged within 24 hours (Table 1). Across the different graph types and sizes, EiGLasso with different ’s almost always converged faster than TeraLasso. In particular, EiGLasso with and was consistently two to three orders-of-magnitude faster than TeraLasso. For example, EiGLasso with took 3 hours for graphs with , while TeraLasso did not converge on the smaller graphs with in 24 hours.

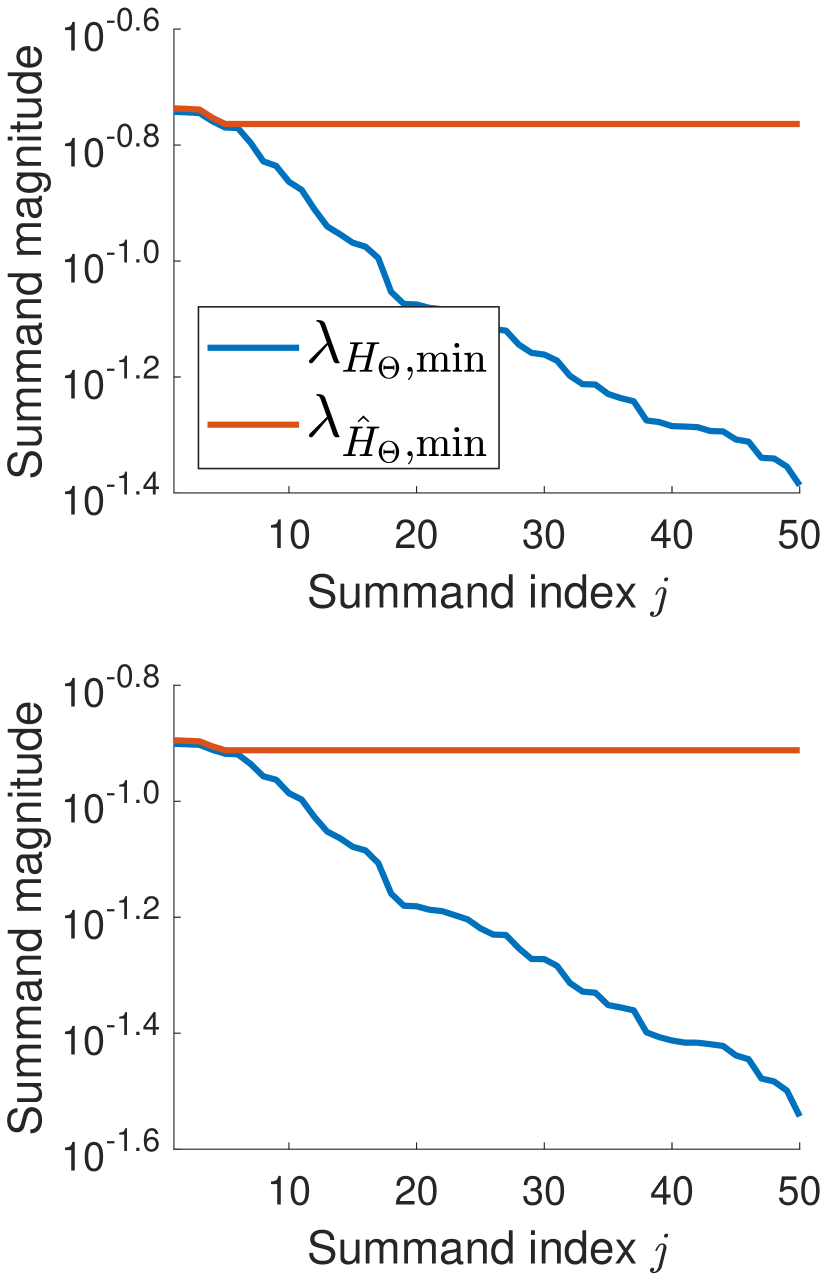

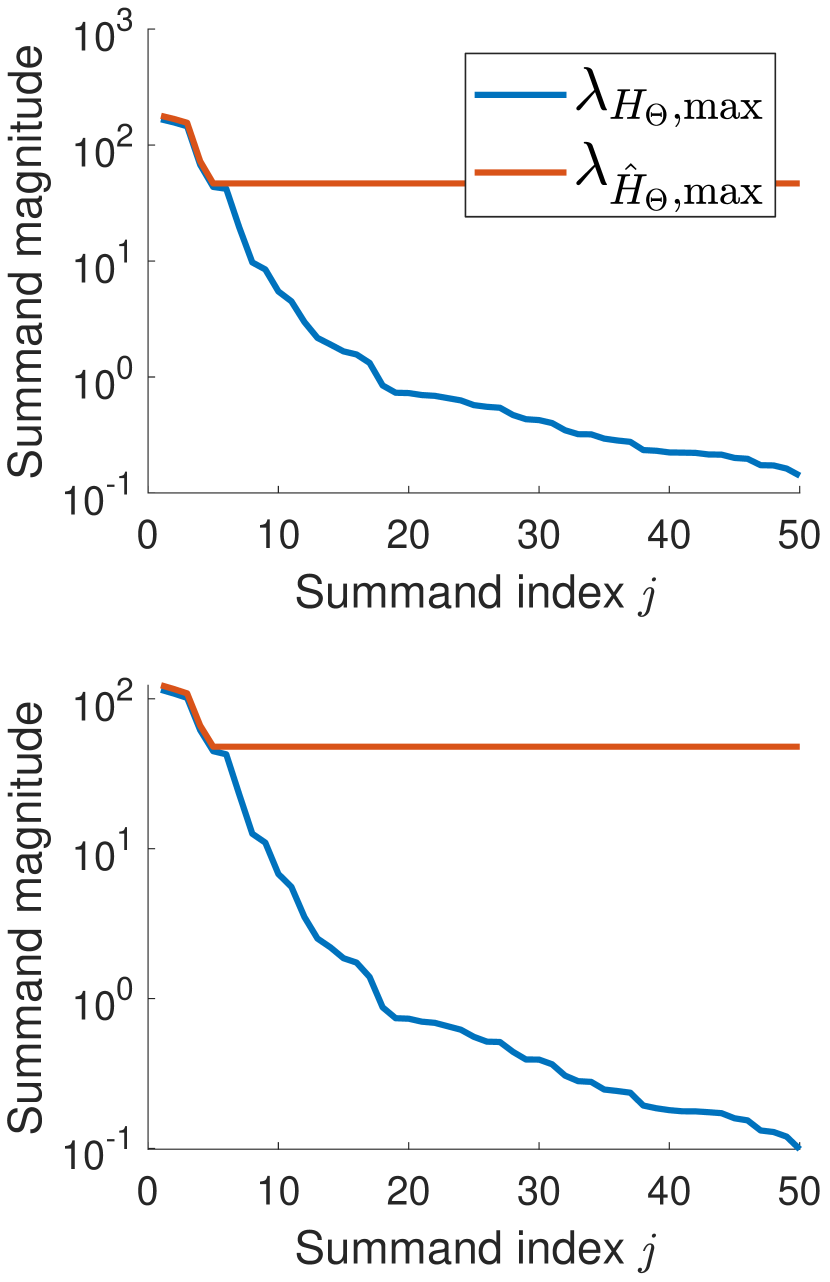

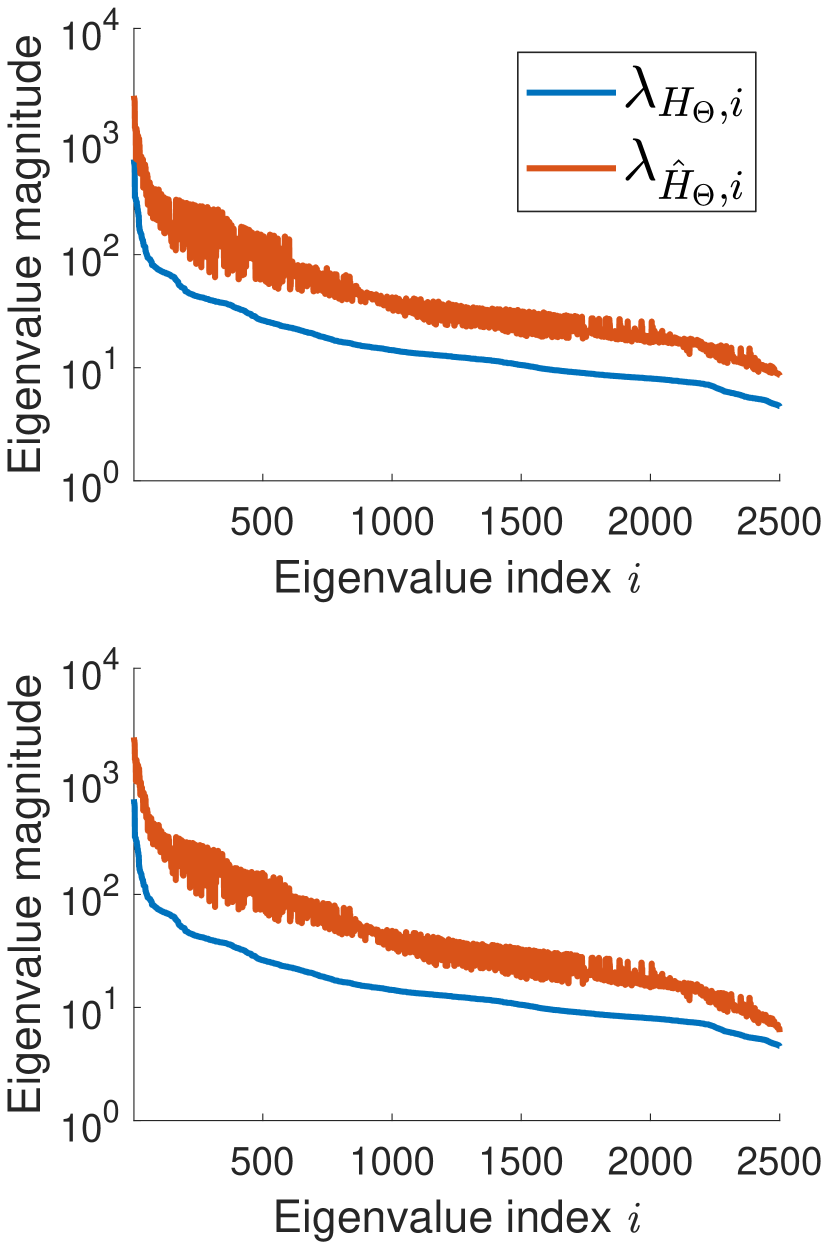

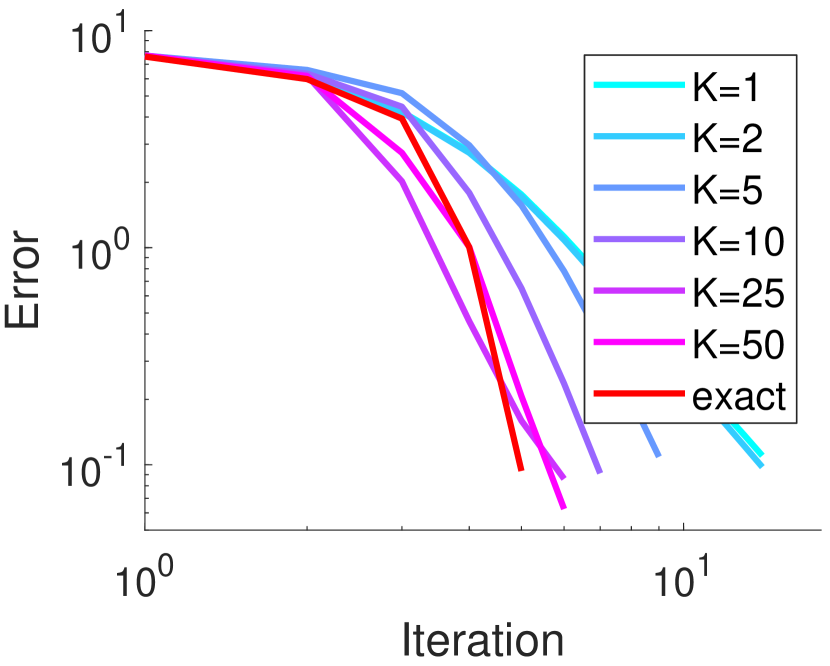

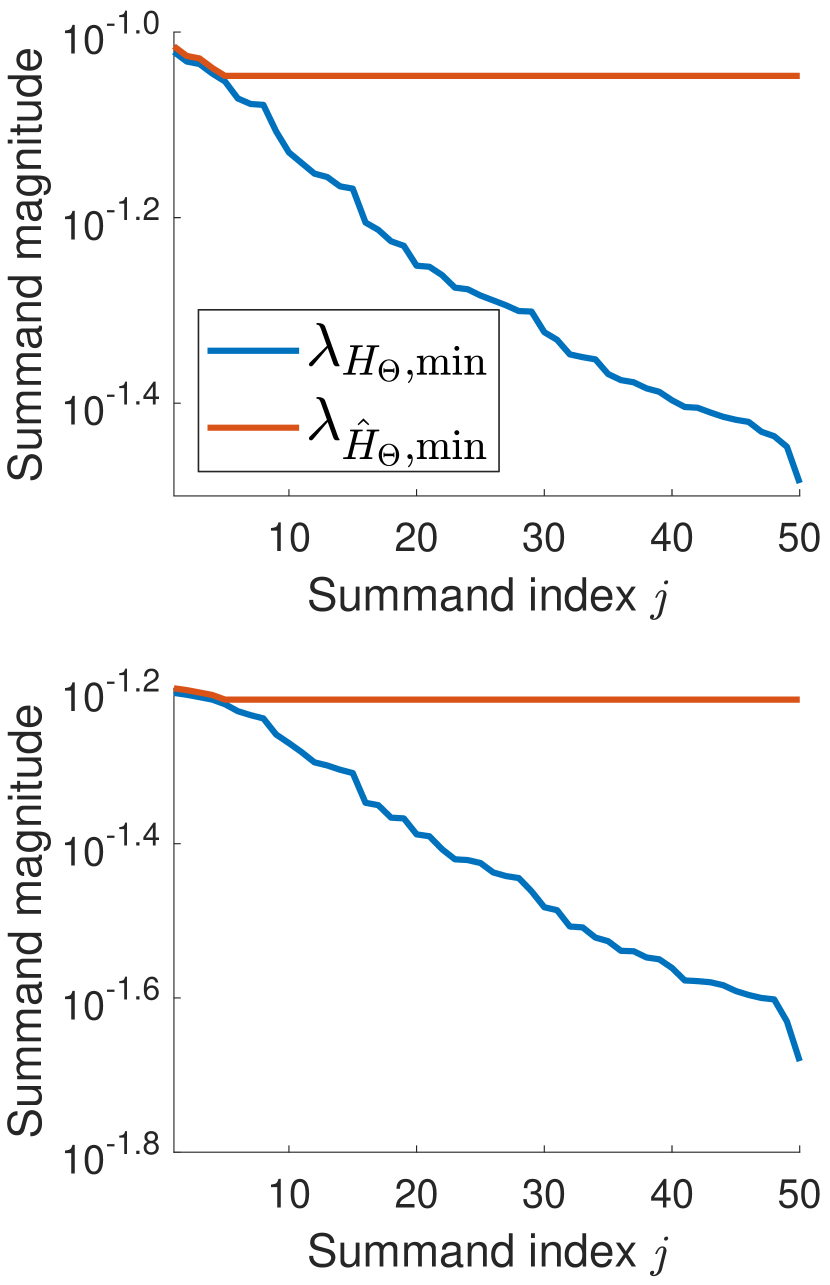

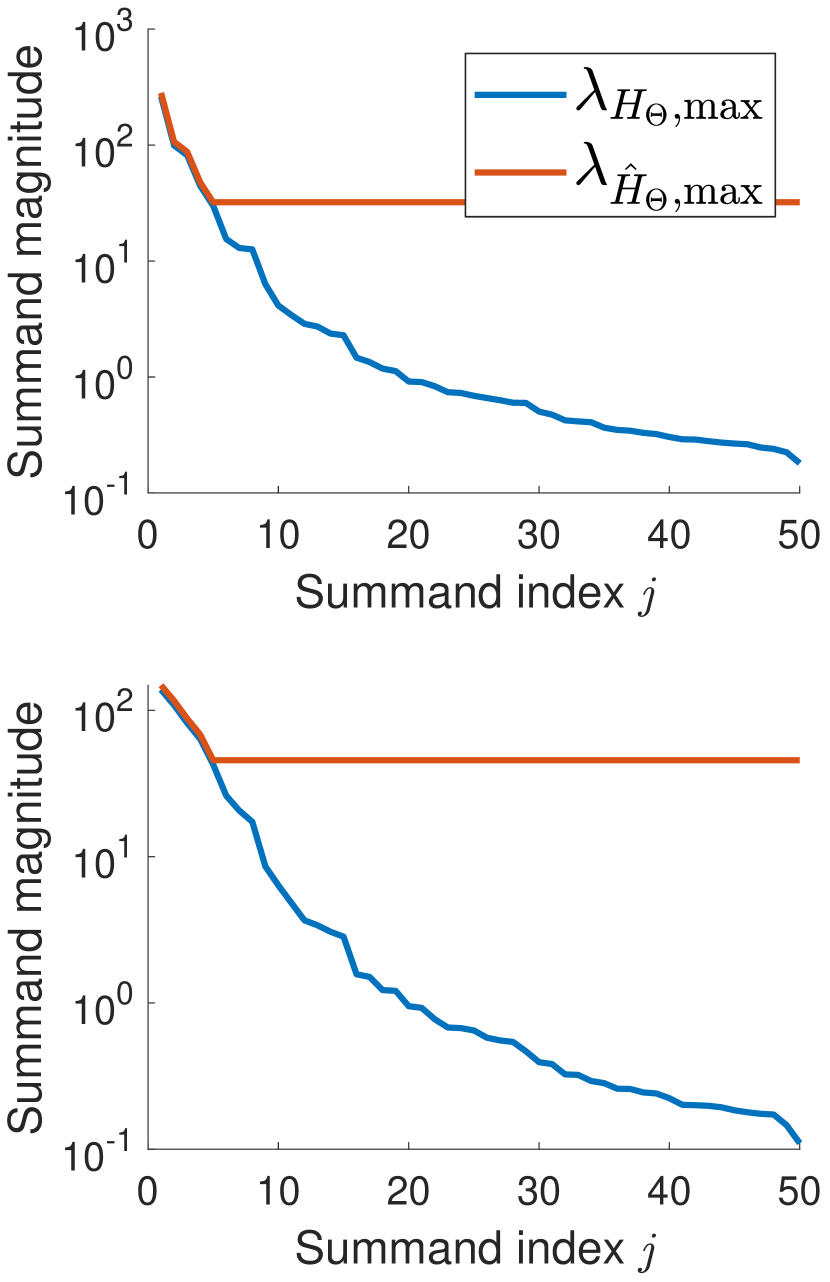

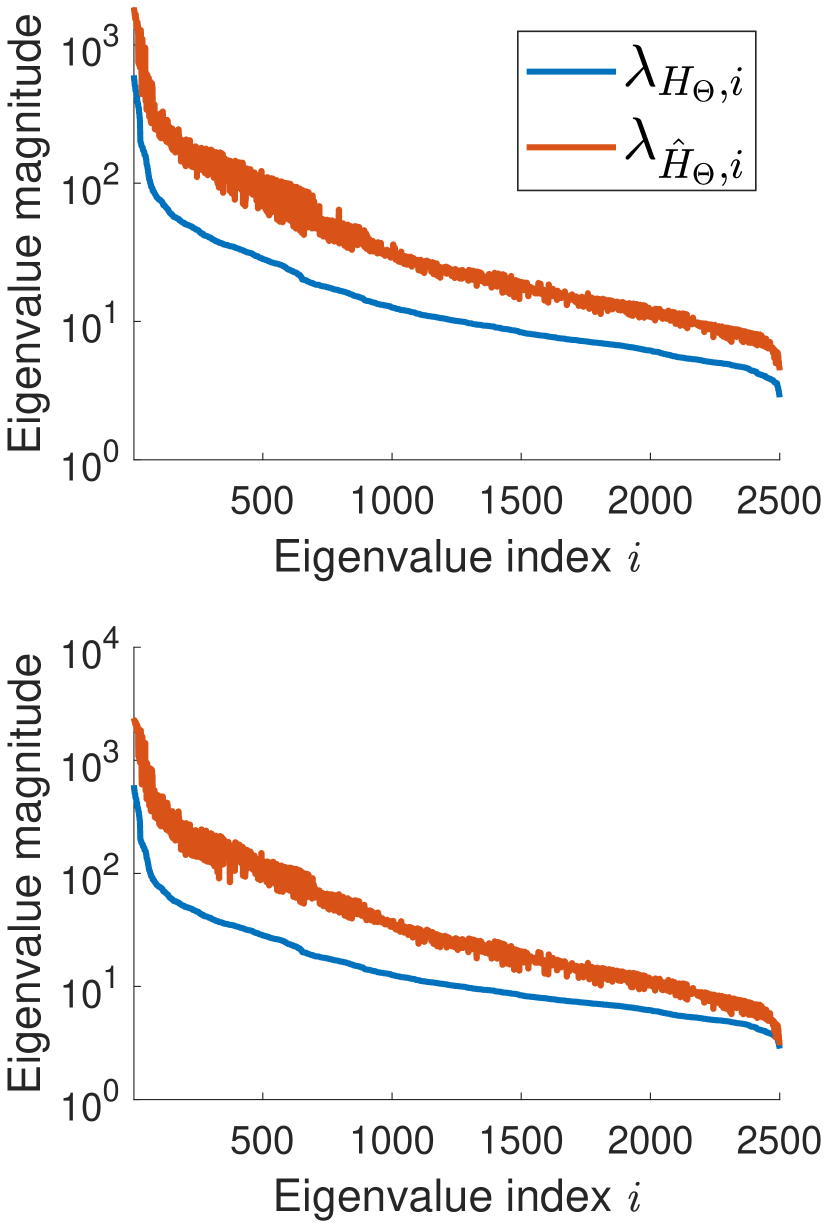

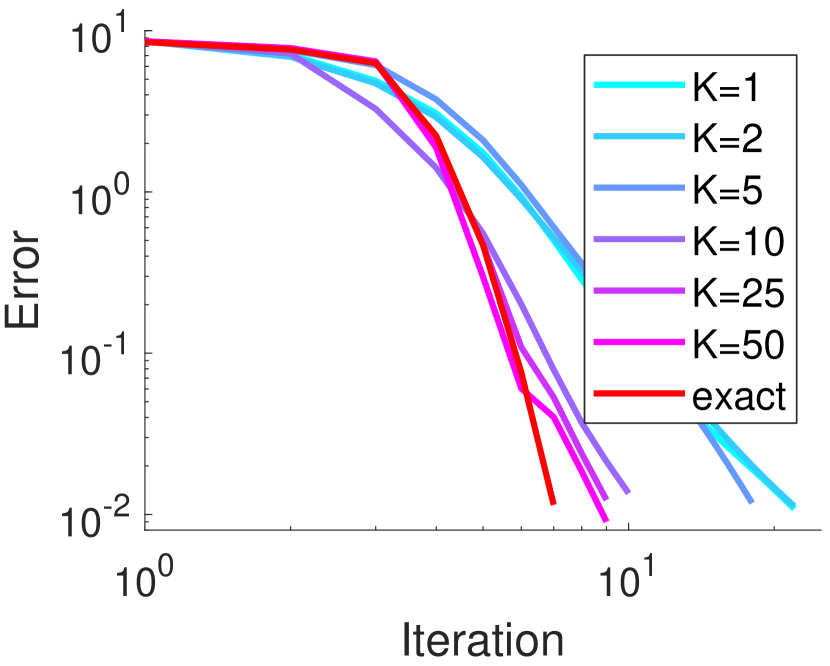

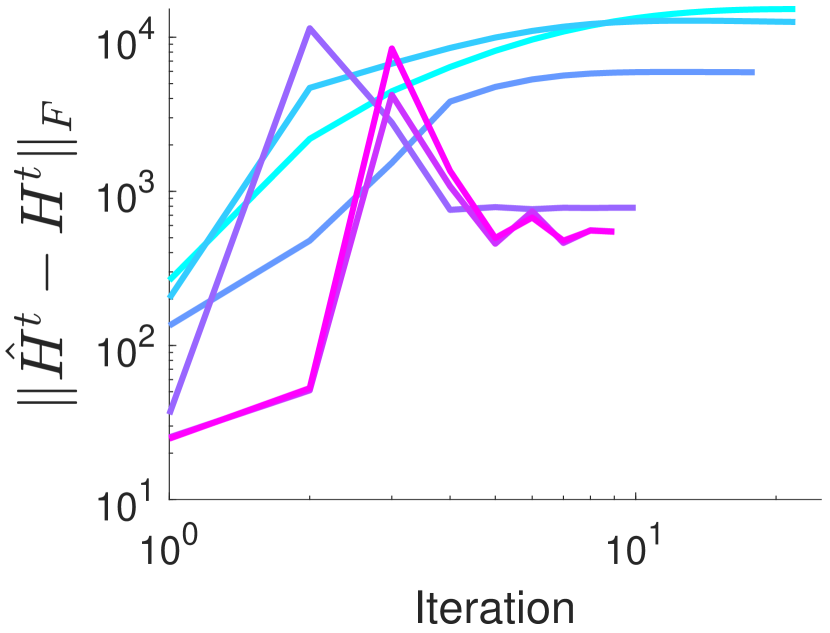

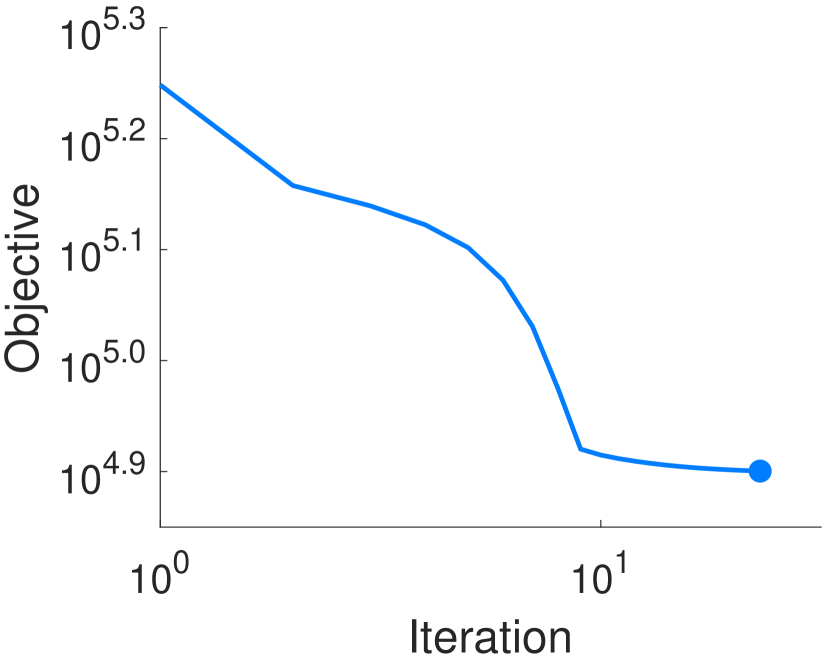

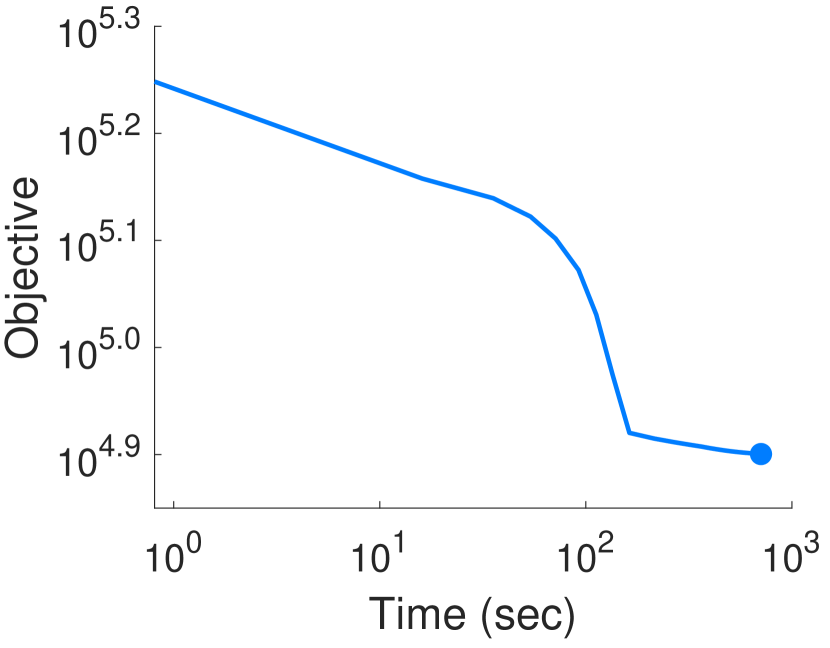

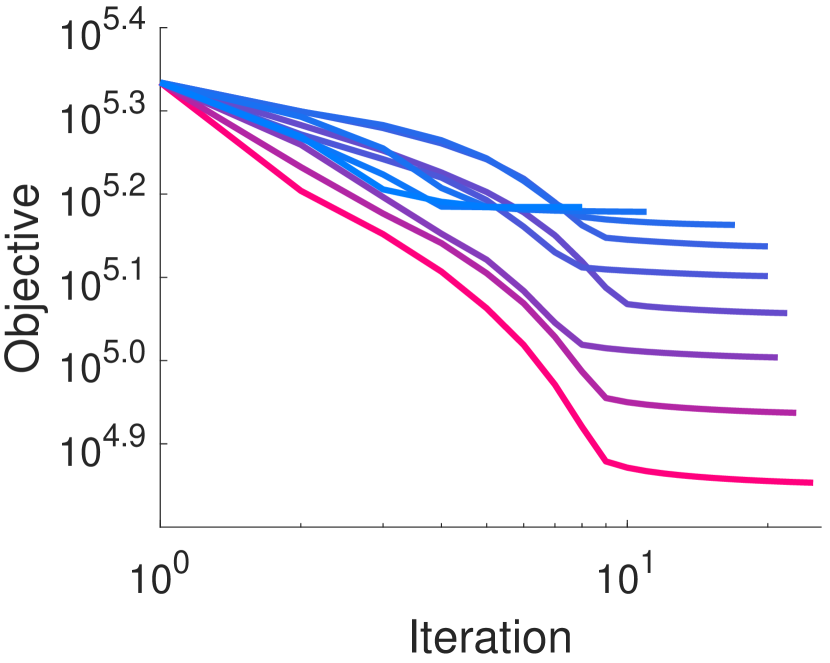

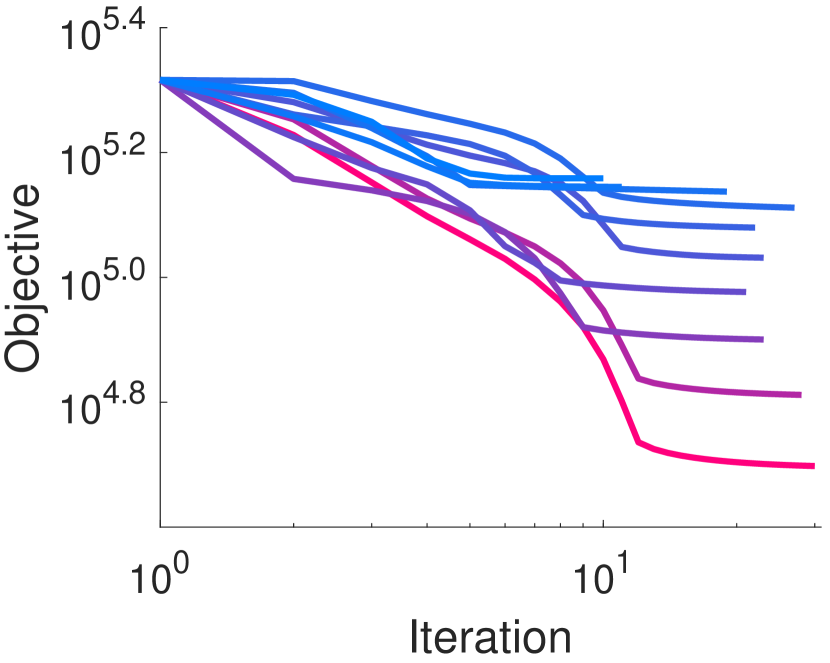

We empirically evaluated the effects of Hessian approximation on the convergence behavior of EiGLasso, using data simulated from a random graph of size . In and of the approximate Hessian , the components of the eigenvalues of and are modified from the summands in Eq. (20) to the summands in Eq. (24). For EiGLasso with , these summands in the eigenvalues before and after the modification are shown for the minimum and maximum eigenvalues of at the th and last iterations in Figures 4(a) and 4(b). The full spectrums of the same and are shown in Figure 4(c). Next, we examined the effects of such Hessian approximation on the convergence of EiGLasso (Figures 4(d) and 4(e)). While EiGLasso with the exact Hessian converges quadratically, with the approximate Hessian, as the degree of Hessian approximation increases with smaller , the convergence of EiGLasso slows down. However, even with , the convergence is not significantly slower than EiGLasso with the exact Hessian. Even if does not approach zero over iterations (Figure 4(e)), EiGLasso with the approximate Hessian quickly reaches the same level of optimality as EiGLasso with the exact Hessian. We obtained similar results from a graph with clusters (Figure 5).

5.2 Mouse Gene Expression Data from RNA-seq

We compared EiGLasso and TeraLasso using the gene expression levels obtained from RNA sequencing of brain tissues for multiple related mice from the same pedigree (Gonzales et al., 2018). The brain tissue samples were collected from generations 50-56 of the LG/J SM/J advanced intercross line of mice. RNA was extracted from three mouse brain tissue types: prefrontal cortex (PFC; 185 mice), striatum (STR; 169 mice), and hippocampus (HIP; 208 mice). Several genes from these tissues have been found relevant to psychiatric and metabolic disorders (Gonzales et al., 2018).

We analyzed this data with EiGLasso and TeraLasso to estimate for the relationship among the mice and for the network over genes. We selected genes from each tissue type by excluding the genes with low variance in expression across the mice. As TeraLasso did not converge within 24 hours on this dataset with , to compare the computation time of EiGLasso and TeraLasso, we formed three smaller datasets for each tissue type by performing hierarchical clustering and selecting clusters of genes. We selected the regularization parameters from the range using Bayesian Information Criterion (BIC). EiGLasso was run with with the convergence criterion . TeraLasso was run up to 24 hours, until it reached similar objective values to those from EiGLasso, which corresponded to or .

| Tissue Type | Genes () | EiGLasso (sec) | TeraLasso (sec) |

|---|---|---|---|

| PFC () | 436 | 2 | 887 |

| 877 | 13 | 18194 | |

| 5108 | 6141 | ||

| 10000 | 25360 | ||

| STR () | 447 | 9 | 6917 |

| 977 | 77 | 39645 | |

| 5007 | 32977 | ||

| 10000 | 65797 | ||

| HIP () | 508 | 90 | 54454 |

| 879 | 708 | ||

| 5529 | 3106 | ||

| 10000 | 20104 |

Across all datasets with different tissue types and with different sizes, EiGLasso was significantly faster than TeraLasso (Table 2). On smaller datasets with less than 1,000 genes, EiGLasso was two to three orders-of-magnitude faster than TeraLasso. On HIP tissue with 879 genes, within 24 hours, TeraLasso was not able to converge to the similar objective value that EiGLasso reached, while EiGLasso converged in about 12 minutes. On the larger datasets with more than 5,000 genes, TeraLasso was not able to reach the same objective as EiGLasso with within 24 hours. On the full dataset with 10,000 genes, EiGLasso took 6 and 7 hours for the HIP and PFC tissue types and 18 hours for the STR tissue type.

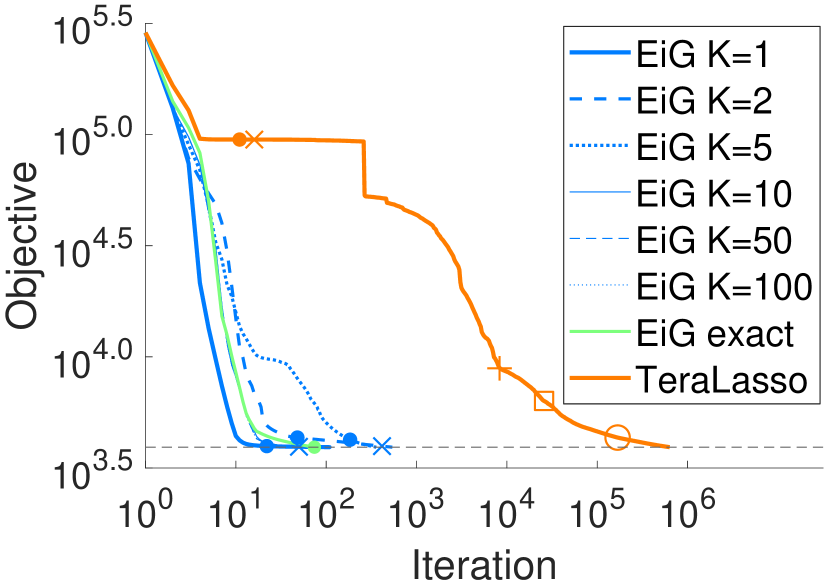

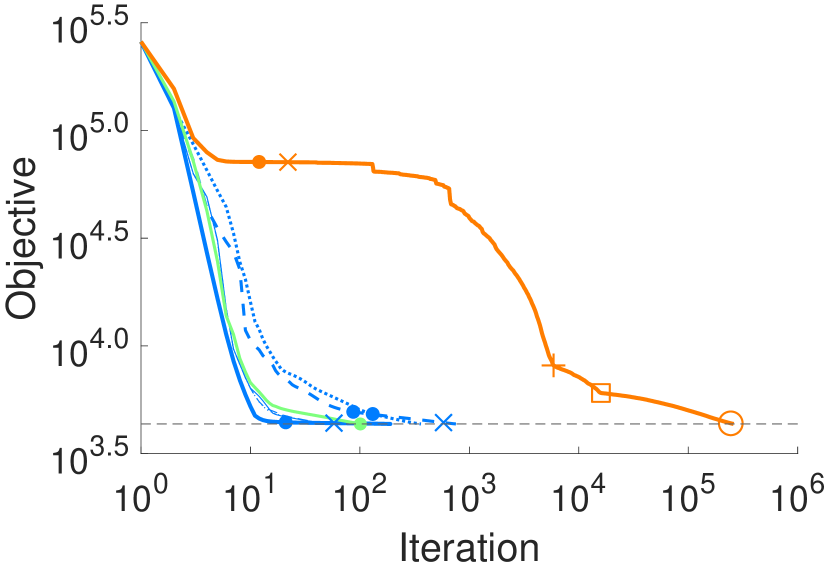

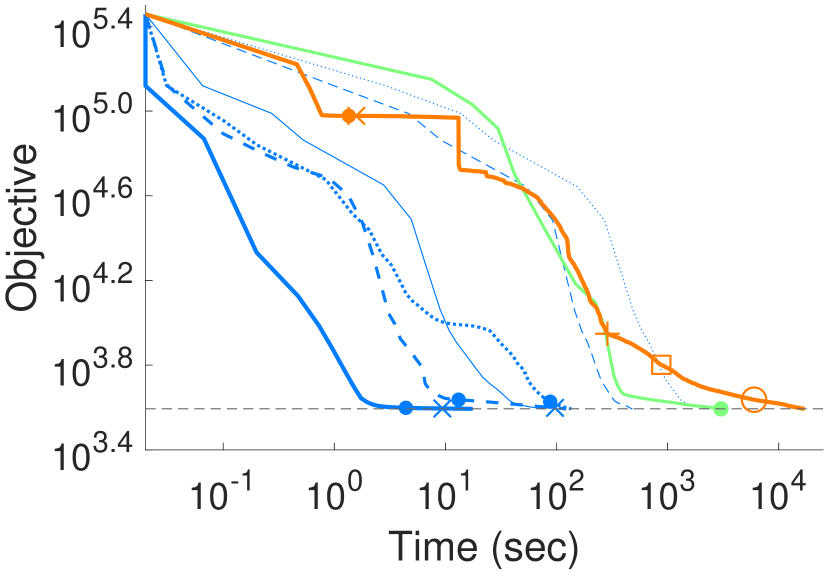

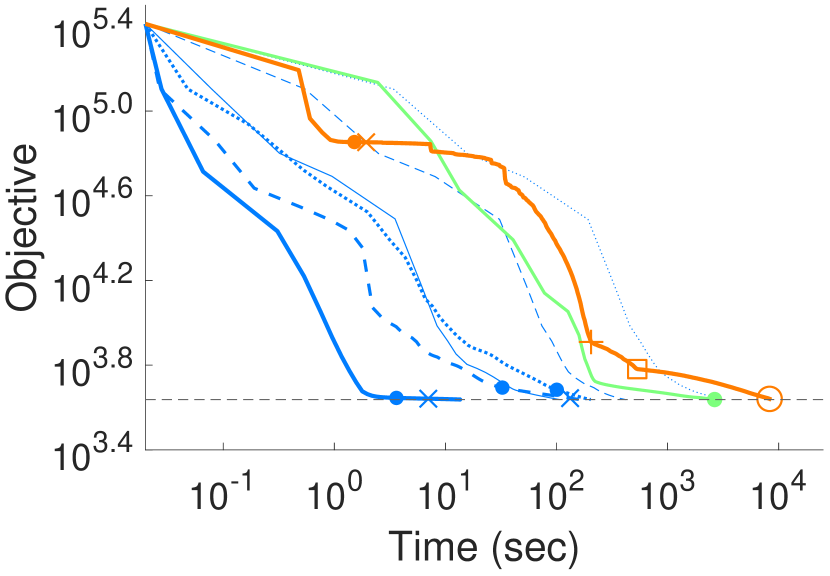

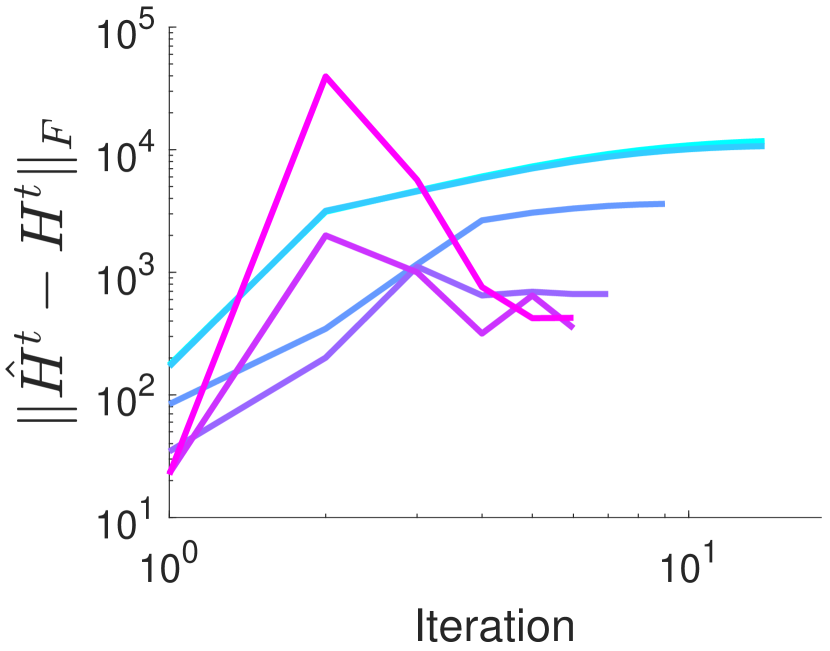

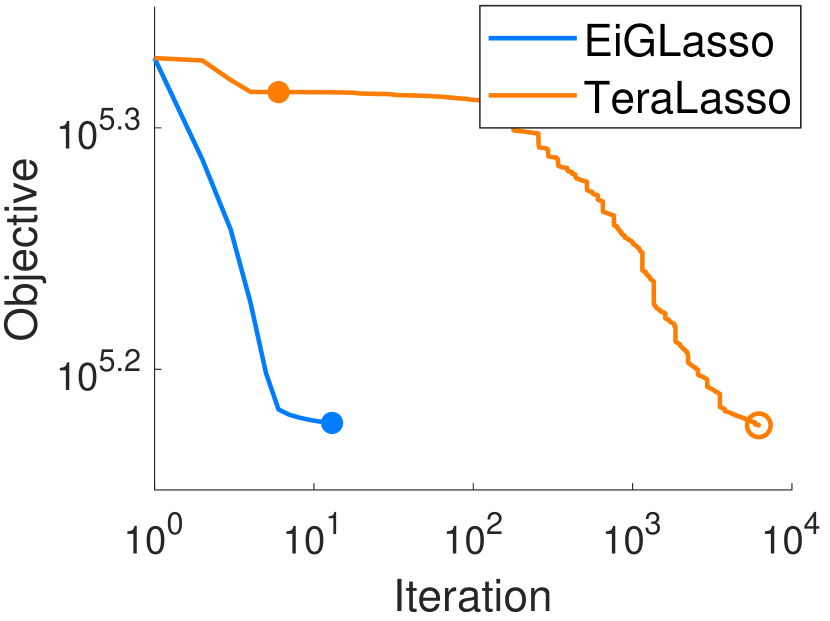

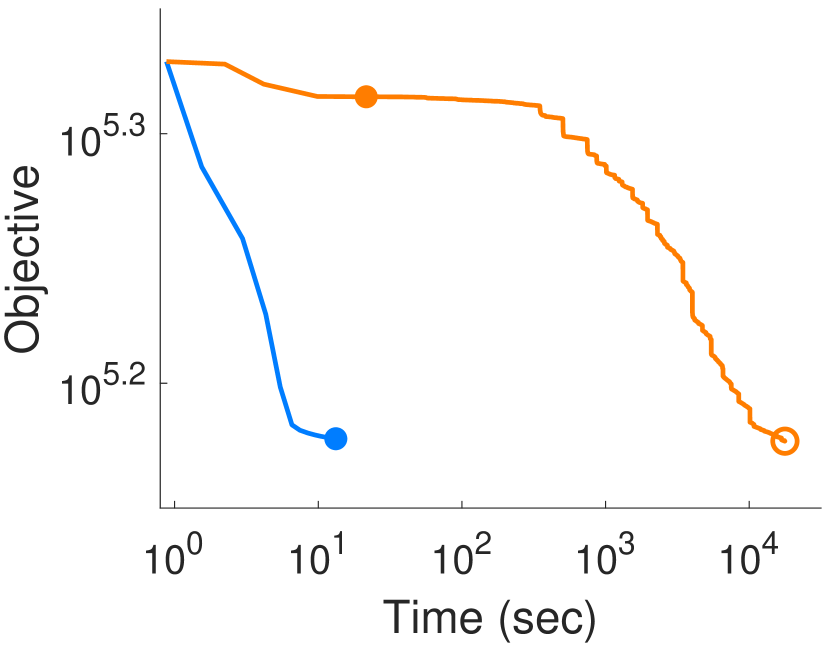

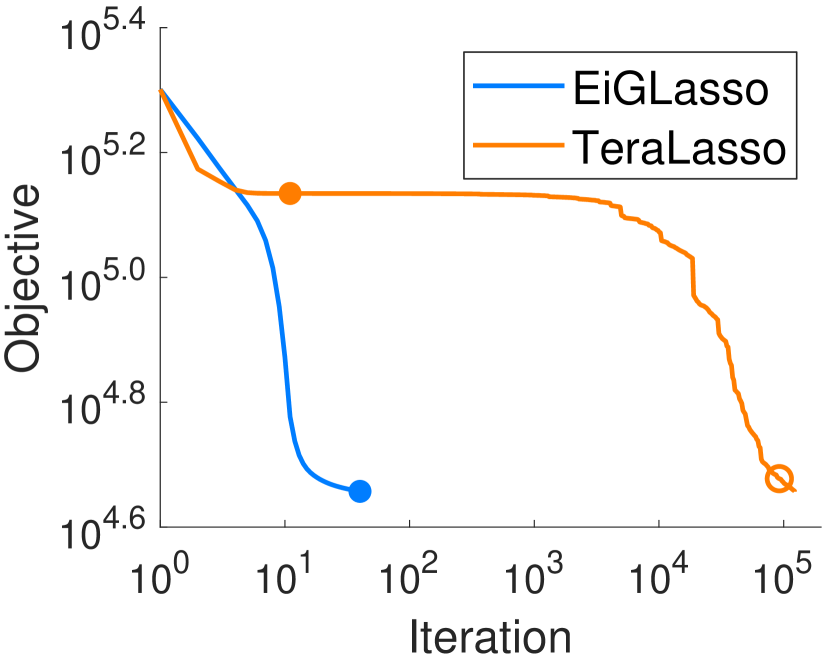

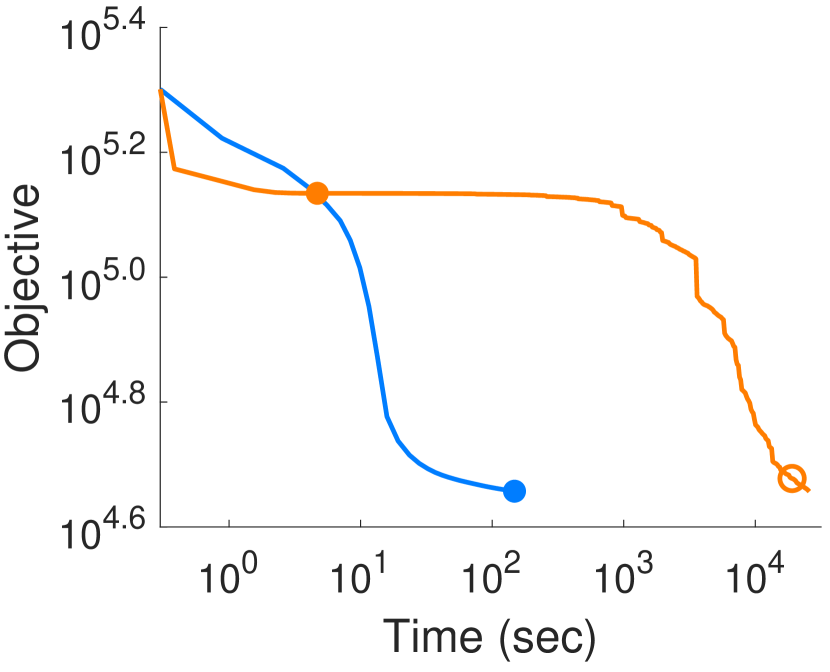

On the second largest dataset from each tissue type in Table 2, we examined the objective values over iterations and over time for EiGLasso and TeraLasso (Figure 6). In all three datasets, EiGLasso converged two orders-of-magnitude faster than TeraLasso with much fewer iterations. To reach the similar objective value as EiGLasso, TeraLasso needed stricter convergence criterion or . The number of iterations required by EiGLasso was not affected significantly by different regularization parameters (Figure 7).

5.3 Financial data

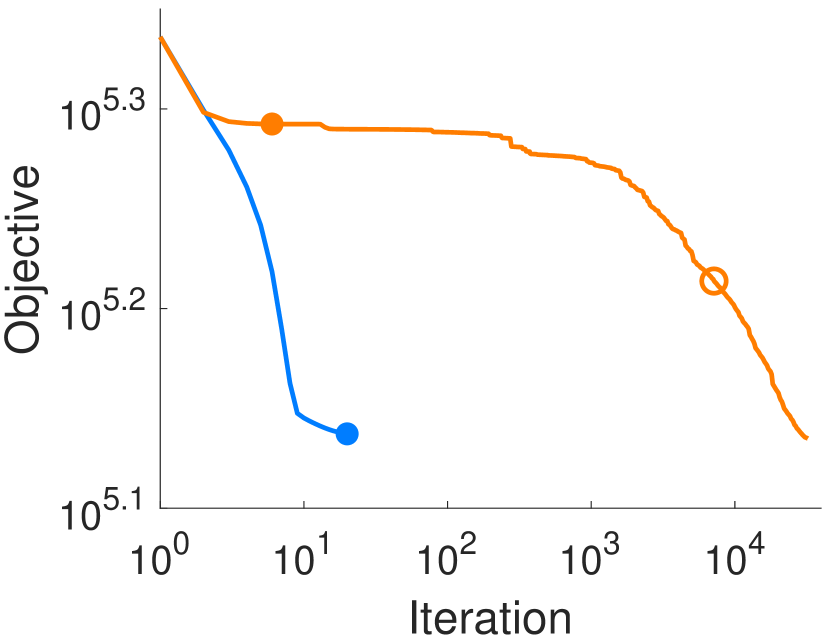

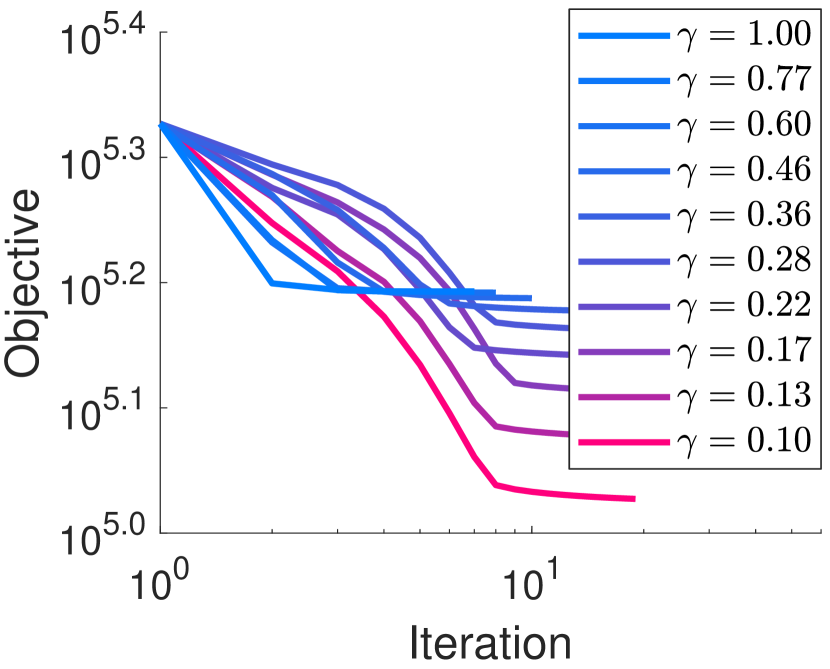

We applied EiGLasso and TeraLasso to the historical daily stock price data of the S&P 500 constituents to model the relationship among companies and dependencies across time points. We obtained the daily stock closing prices for 306 companies that remained in the index from 2/16/2010 to 2/13/2020 for 2,523 days. We excluded the data for six days when the stocks for only a small subset of the constituents were traded. We normalized the data by computing the proportion of price change on day from the previous day as . We ran EiGLasso with and and ran TeraLasso until it reached the similar objective as EiGLasso. We selected the optimal regularization parameter from 10 different values within the range of using BIC.

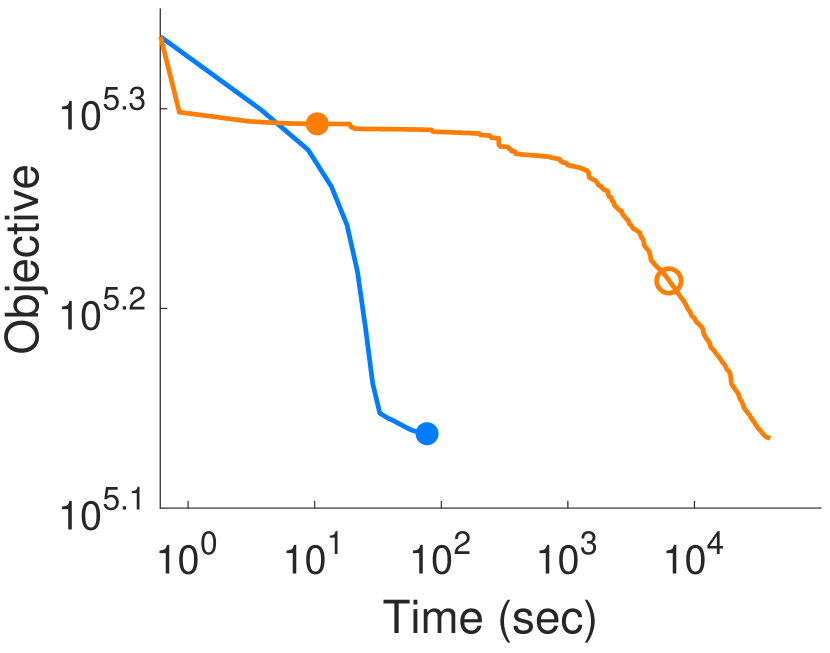

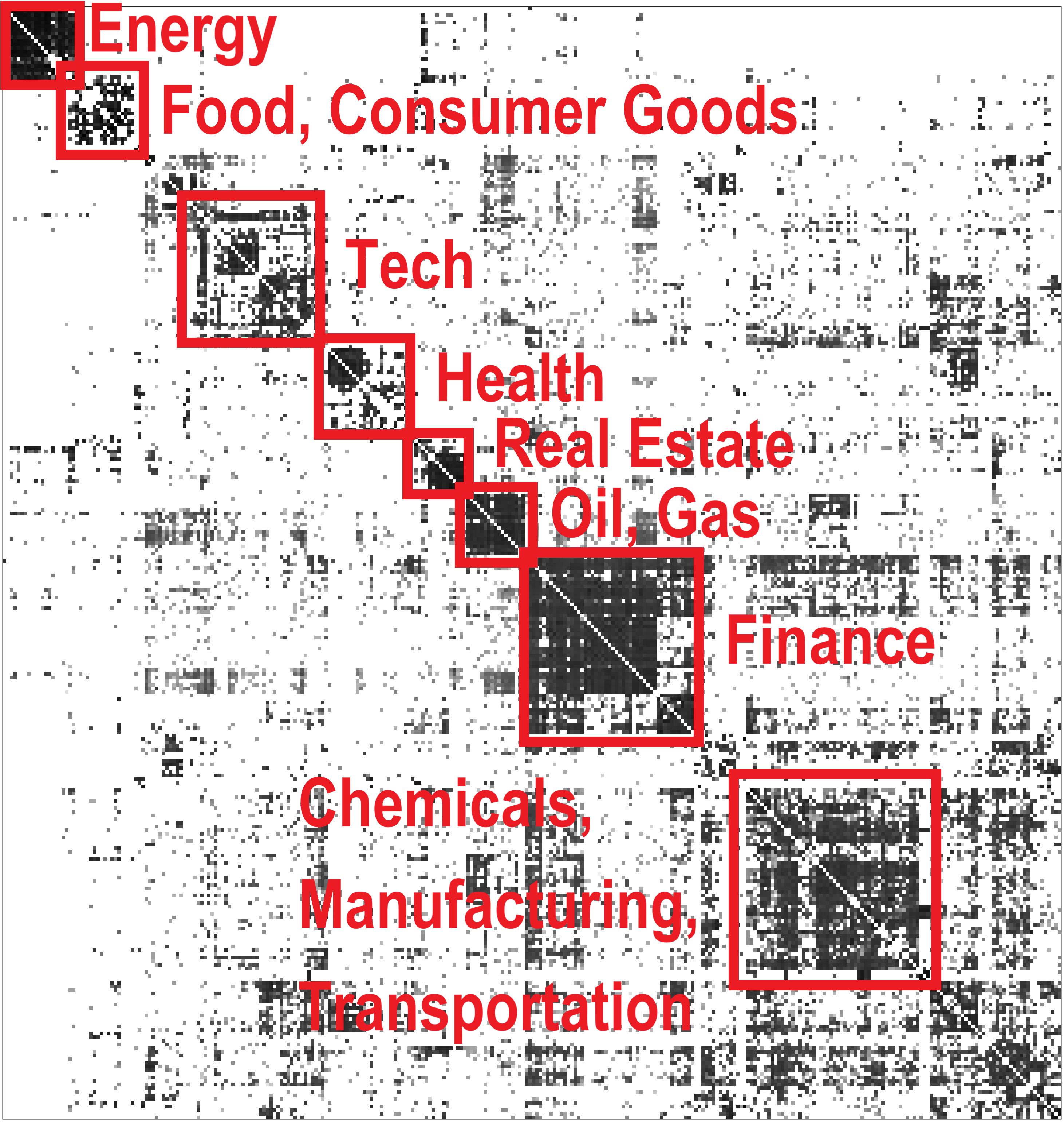

EiGLasso with took 46 hours, whereas TeraLasso did not converge within 48 hours. The graph over 306 companies estimated by EiGLasso match the known sectors (Figure 8(a)). We compared the computation time of EiGLasso with and TeraLasso on a small subset over 500 days for the same 306 companies. On this smaller dataset, EiGLasso took 148 seconds to converge and TeraLasso took 25,739 seconds, showing that EiGLasso was again two orders-of-magnitude faster than TeraLasso (Figure 8(b)).

6 Conclusion

We introduced EiGLasso, an efficient algorithm for estimating an inverse covariance matrix as the Kronecker sum of two matrices, each representing a graph over samples and a graph over features. Extending the second-order optimization method in QUIC for Gaussian graphical models (Hsieh et al., 2014), EiGLasso employed the eigendecomposition of the two matrices for individual graphs during optimization, to avoid an expensive computation of large gradient and Hessian matrices with an inflated structure that arises from the Kronecker sum. EiGLasso approximated the Hessian based on this eigenstructure of the parameters to further reduce the computation time. We showed the quadratic convergence of EiGLasso with the exact Hessian and linear convergence of EiGLasso with the approximate Hessian. In our experiments, EiGLasso achieved two to three orders-of-magnitude speed-up over the state-of-the-art method, TeraLasso (Greenewald et al., 2019).

In addition, we introduced a new approach for identifying and estimating the unidentifiable diagonal elements of the matrices for the feature and sample graphs. We showed that given the ratio of the traces of the two matrices, the diagonal parameters can be identified uniquely within the equivalence class of the unidentifiable parameters. EiGLasso performed the optimization without identifying these parameters, since all quantities involved in the optimization are invariant within the equivalence class regardless of the trace ratio. We further showed that it is sufficient to identify the parameters with the fixed trace ratio once, after the optimization was complete. Thus, EiGLasso used a significantly simpler strategy for estimating the unidentifiable parameters than the previous methods.

There are several possible future directions. One natural extension of EiGLasso is to adopt Big&QUIC (Hsieh et al., 2013), an extension of QUIC to remove the memory requirement, within EiGLasso. Because unlike QUIC, EiGLasso uses the eigendecomposition of the parameter matrices, which in itself has the space complexity cubic in the graph sizes, further research is needed to incorporate the eigendecomposition within the block-wise update used in Big&QUIC. Another future direction is to develop a Hessian approximation technique with faster theoretical convergence. While we showed that EiGLasso with our approximate Hessian converges linearly to the optimum, it may be possible to achieve superlinear convergence with an approximation Hessian that approaches the exact Hessian over iterations.

Acknowledgements

This work was supported by NIH 1R21HG011116 and 1R21HG010948. This work used the Extreme Science and Engineering Discovery Environment (XSEDE), which is supported by NSF ACI-1548562 and ACI-1445606.

References

- Benzi and Simoncini (2017) M. Benzi and V. Simoncini. Approximation of functions of large matrices with Kronecker structure. Numerische Mathematik, 135(1):1–26, 2017.

- Bertsekas (1995) D. P. Bertsekas. Nonlinear programming. Athena Scientific, 1995.

- Boyd and Vandenberghe (2004) S. Boyd and L. Vandenberghe. Convex Optimization. Cambridge University Press, 2004.

- Dai et al. (2015) X. Dai, T. Li, Z. Bai, Y. Yang, X. Liu, J. Zhan, and B. Shi. Breast cancer intrinsic subtype classification, clinical use and future trends. American Journal of Cancer Research, 5:2929–43, 2015.

- Dunn (1980) J. Dunn. Newton’s method and the Goldstein step length rule for constrained minimization. In Proceedings of the 19th IEEE Conference on Decision and Control including the Symposium on Adaptive Processes, pages 17–22. IEEE, 1980.

- Friedman et al. (2007) J. Friedman, T. Hastie, and R. Tibshirani. Sparse inverse covariance estimation with the graphical lasso. Biostatistics, 9(3):432–441, 2007.

- Gao et al. (2020) H. Gao, Z. Wang, and S. Ji. Kronecker attention networks. In Proceedings of the 26th ACM SIGKDD International Conference on Knowledge Discovery & Data Mining, pages 229–237, 2020.

- Gonzales et al. (2018) N. M. Gonzales, J. Seo, A. I. Hernandez Cordero, C. L. St. Pierre, J. S. Gregory, M. G. Distler, M. Abney, S. Canzar, A. Lionikas, and A. A. Palmer. Genome-wide association analysis in a mouse advanced intercross line. Nature Communications, 9(1):5162, 2018.

- Greenewald et al. (2019) K. Greenewald, S. Zhou, and A. Hero III. Tensor graphical lasso (TeraLasso). Journal of the Royal Statistical Society: Series B (Statistical Methodology), 81(5):901–931, 2019.

- Haupt et al. (2020) S. Haupt, A. Zeilmann, A. Ahadova, M. von Knebel Doeberitz, M. Kloor, and V. Heuveline. Mathematical modeling of multiple pathways in colorectal carcinogenesis using dynamical systems with Kronecker structure. bioRxiv doi: 10.1101/2020.08.14.250175, 2020.

- Hsieh et al. (2013) C.-J. Hsieh, M. A. Sustik, I. S. Dhillon, P. Ravikumar, and R. A. Poldrack. BIG & QUIC: Sparse inverse covariance estimation for a million variables. In Advances in Neural Information Processing Systems, volume 26, pages 3165–3173, 2013.

- Hsieh et al. (2014) C.-J. Hsieh, M. A. Sustik, I. S. Dhillon, and P. Ravikumar. QUIC: Quadratic approximation for sparse inverse covariance estimation. Journal of Machine Learning Research, 15(83):2911–2947, 2014.

- Kalaitzis et al. (2013) A. Kalaitzis, J. Lafferty, N. D. Lawrence, and S. Zhou. The bigraphical lasso. In Proceedings of the 30th International Conference on Machine Learning, pages 1229–1237. PMLR, 2013.

- Kalchbrenner et al. (2017) N. Kalchbrenner, A. Oord, K. Simonyan, I. Danihelka, O. Vinyals, A. Graves, and K. Kavukcuoglu. Video pixel networks. In Proceedings of the 34th International Conference on Machine Learning, pages 1771–1779. PMLR, 2017.

- King (1966) B. F. King. Market and industry factors in stock price behavior. The Journal of Business, 39(1):139–190, 1966.

- Leng and Tang (2012) C. Leng and C. Y. Tang. Sparse matrix graphical models. Journal of the American Statistical Association, 107(499):1187–1200, 2012.

- Li et al. (2018) G. Li, J. Luo, Q. Xiao, C. Liang, and P. Ding. Prediction of microRNA–disease associations with a Kronecker kernel matrix dimension reduction model. Royal Society of Chemistry, 8:4377–4385, 2018.

- Mazumder and Hastie (2012) R. Mazumder and T. Hastie. Exact covariance thresholding into connected components for large-scale graphical lasso. Journal of Machine Learning Research, 13(27):781–794, 2012.

- Park et al. (2017) S. Park, K. Shedden, and S. Zhou. Non-separable covariance models for spatio-temporal data, with applications to neural encoding analysis. arXiv preprint arXiv:1705.05265, 2017.

- Rudelson and Zhou (2017) M. Rudelson and S. Zhou. Errors-in-variables models with dependent measurements. Electronic Journal of Statistics, 11(1):1699–1797, 2017.

- Tseng and Yun (2009) P. Tseng and S. Yun. A coordinate gradient descent method for nonsmooth separable minimization. Mathematical Programming, 117(1):387–423, 2009.

- Tsiligkaridis and Hero (2013) T. Tsiligkaridis and A. O. Hero. Covariance estimation in high dimensions via Kronecker product expansions. IEEE Transactions on Signal Processing, 61(21):5347–5360, 2013.

- Witten et al. (2011) D. M. Witten, J. H. Friedman, and N. Simon. New insights and faster computations for the graphical lasso. Journal of Computational and Graphical Statistics, 20(4):892–900, 2011.

- Yin and Li (2012) J. Yin and H. Li. Model selection and estimation in the matrix normal graphical model. Journal of Multivariate Analysis, 107:119–140, 2012.

- Yoon and Kim (2020) J. H. Yoon and S. Kim. EiGLasso: Scalable estimation of Cartesian product of sparse inverse covariance matrices. In Proceedings of the 35th Conference on Uncertainty in Artificial Intelligence, pages 1248–1257. PMLR, 2020.

- Zhang et al. (2018) T. Zhang, W. Zheng, Z. Cui, and Y. Li. Tensor graph convolutional neural network. arXiv preprint arXiv:1803.10071, 2018.

- Zhang (2020) X. Zhang. Statistical Analysis for Network Data using Matrix Variate Models and Latent Space Models. Ph.D. disseration, University of Michigan, 2020.

- Zhou (2014) S. Zhou. Gemini: Graph estimation with matrix variate normal instances. Annals of Statistics, 42(2):532–562, 2014.

Appendix A. Hessian Computation

We show that the collapse of in Eq. (17) to obtain the Hessian can be viewed as the same type of deflation for the gradient in Figure 1(b) applied twice to .

Let denote a matrix of size . Then, the elements of the Kronecker product are given as for and . As a representation of with different row/column indices, we consider whose elements are given as . We define an operator

which maps the elements of to those of . The same operator can be applied to , where ,

| (32) |

Collapsing into amounts to applying the same type of collapse as in the gradient (Figure 1(b)) twice on to obtain , , and . To see this, we re-write as

Then, we apply the operator in Eq. (32) to :

| (33) |

where . Similarly,

| (34) | ||||

| (35) |

where . Eqs. (33)-(35) show the two-stage collapse for Hessian computation: (Figure 9(a)) is collapsed to and (Figure 9(b)), which are then collapsed to , , and (Figure 9(c)). The first collapse of to and is equivalent to applying the same collapse for the gradient in Figure 1(b) at the level of cells in Figure 9(a) each with size , instead of at the level of matrix elements. The second collapse from and to , , and is equivalent to applying the same collapse again on each cell of and in Figure 9(b) at the level of matrix elements. Notice that not all elements of contribute to , , and : Only the elements of corresponding to the non-zero elements of the inflated Kronecker-sum mask and the elements of and , each masked with and , are used to compute , , and .

Appendix B. Computing the Newton Direction

We provide the details on the coordinate descent updates for . Updating can be done in a similar manner.

B1. Exact Hessian

Solving Eq. (12) for assuming that all the other elements of are fixed amounts to solving the following optimization problem:

where is the th column of . This problem has a closed-form solution

where

and is the soft-thresholding function.

B2. Approximate Hessian

Similarly, solving Eq. (12) with instead of for while fixing all the other elements of amounts to solving the following optimization problem:

with a closed-form solution

where