Proof.

A Tale of Two Tails: A Model-free Approach to Estimating Disaster Risk Premia and Testing Asset Pricing Models

I introduce a model-free methodology to assess the impact of disaster risk on the market return. Using S&P500 returns and the risk-neutral quantile function derived from option prices, I employ quantile regression to estimate local differences between the conditional physical and risk-neutral distributions. The results indicate substantial disparities primarily in the left-tail, reflecting the influence of disaster risk on the equity premium. These differences vary over time and persist beyond crisis periods. On average, the bottom 5% of returns contribute to 17% of the equity premium, shedding light on the Peso problem. I also find that disaster risk increases the stochastic discount factor’s volatility. Using a lower bound observed from option prices on the left-tail difference between the physical and risk-neutral quantile functions, I obtain similar results, reinforcing the robustness of my findings.

Keywords: Asset pricing, Disaster Risk, Quantile methods

JEL Codes: G13, G17, C14, C22

1 Introduction

Disaster risk has emerged as a pervasive and influential concept in asset pricing, offering a prominent explanation of the equity premium puzzle, as well as other asset pricing puzzles.111See, for example, Rietz (1988), Barro (2006, 2009), Drechsler and Yaron (2011), Gabaix (2012), Wachter (2013), Constantinides and Ghosh (2017), Isoré and Szczerbowicz (2017), Farhi and Gourio (2018), Seo and Wachter (2019) and Schreindorfer (2020). Little is known, however, about the quantitative properties of disaster risk and evidence for it is often inferred indirectly, such as from the historically high equity premium. Nevertheless, a high equity premium does not necessarily arise due to disaster risk, and the literature has yet to reach an unambiguous conclusion regarding its ability to explain asset pricing puzzles (see, e.g., Julliard and Ghosh (2012)). Ross (2015) refers to disaster risk as dark matter and eloquently summarizes the concept as follows: “It is unseen and not directly observable but it exerts a force that can change over time and that can profoundly influence markets”.

In this paper, I propose a model-free methodology to measure and track through time disaster risk in S&P500 returns. My results unequivocally show that disaster risk is pervasive and is the primary determinant of the equity premium. In establishing these results, I confront two critical challenges that have hindered inference about disaster risk. Firstly, to estimate disaster risk in a model-free manner, the literature often estimates the stochastic discount factor (SDF), defined as the ratio of risk-neutral to physical density. Disaster risk is then defined by the SDF taking large values in the left-tail of the return distribution. However, this approach faces scrutiny due to the potential for erratic results when estimating the density ratio in the tails, thereby complicating robust inference. Secondly, it is crucial to account for changing conditioning information. Typically, estimation of the physical density involves pooling historical returns, while the risk-neutral density relies on forward-looking option prices. This disparity in information sets can lead to inconsistent estimates of conditional disaster risk.

To address these challenges, I consider an approach that avoids the need for density estimation. Starting from the absence of arbitrage opportunities, a risk-neutral distribution exists that can be identified from option prices (Breeden and Litzenberger, 1978). However, the conditional physical distribution, which describes the actual evolution of the market return, remains unobserved. To proceed, I use quantile regression (QR) to estimate

| (1.1) |

where and represent the physical and risk-neutral -quantiles, respectively, of the market return , from period to . The parameters in (1.1) can be estimated using quantile regression, with the observed time series of returns, , as the dependent variable and as the regressor. Importantly, both and are conditioned on the same information set. In general, quantile regression estimates the best linear approximation to the physical quantile function, from which is drawn. Hence, any deviation from the risk-neutral benchmark, , signifies a local difference between the physical and risk-neutral measures at the -quantile. Since the equity premium is determined by these differences, it is natural to define the disaster risk premium as the difference between and in the left-tail, i.e. for values of close to zero.

Based on the QR estimates, two key findings emerge:

(i) the risk-neutral benchmark cannot be rejected in the right-tail () but it is rejected in the left-tail (); and

(ii) the in-sample and out-of-sample explanatory power of the risk-neutral quantile is significantly higher in the right-tail compared to the left-tail.

Both findings suggest that disaster risk is the main driver of the equity premium.

Building on these results, I estimate the conditional Lorenz curve and Gini coefficient associated with the equity premium. These statistics summarize how much the conditional equity premium is driven by the lowest returns, akin to its interpretation of wealth inequality in labor economics. I find that the Lorenz curve is always concave, and the Gini coefficients are far above zero in every time period, thus showing that disaster risk is a pervasive feature of the data. On average, I find that the bottom 5% of returns contribute to 17% of the total equity premium.

While this result demonstrates that disaster risk is an important driver of expected returns, it also adds nuance to the degree of disaster risk necessary to explain the equity premium. In particular, previous papers attribute about 90% of the equity premium to the lowest 5% of returns (Barro, 2009; Backus et al., 2011; Beason and Schreindorfer, 2022). The results differ since I account for conditioning information, whereas unconditional estimates of disaster risk tend to overestimate this risk, since the physical distribution acquires fatter tails when averaging out state variables.

Comparing the physical and risk-neutral quantile functions over time also sheds light on the role of risk aversion and forward-looking beliefs in jointly determining disaster risk premia. Particularly during crises, the value of an insurance contract that hedges against disaster risk increases, resulting in a downward movement in the left-tail of the risk-neutral quantile function. Simultaneously, investors often revise their beliefs about the likelihood of another disaster, frequently assigning a higher probability to such an event. This effect drives down the left-tail of the physical quantile function, creating an ambiguous overall impact on disaster risk premia. However, the quantile regression estimates indicate that the risk-neutral quantile function decreases proportionally more, highlighting the greater influence of risk aversion in determining disaster risk premia.

Given that the equity premium is primarily driven by disaster risk premia, the discussion above implies that the left-tail of the risk-neutral quantile function can predict the equity premium. An OLS regression of the equity premium against the 5% risk-neutral quantile shows preliminary evidence of forecasting ability, especially out-of-sample. In line with theoretical expectations, a decline in the 5% risk-neutral quantile is associated with a substantial increase in the equity premium. Notably, during the 2008 financial crisis and the 2020 Covid-19 crisis, monthly estimates of the equity premium reached peaks of around 5%.

Besides the equity premium puzzle, the QR estimates shed light on the role of first-order stochastic dominance and the pricing kernel puzzle. Specifically, I find that holds across most of the distribution, except in the far right-tail, where frequently occurs. This violation of stochastic dominance raises questions in asset pricing models using the expected utility framework, as it suggests that a representative investor exhibits negative risk aversion. Furthermore, I show that a violation of stochastic dominance implies that the pricing kernel is not monotonic, thereby confirming the pricing kernel puzzle while accounting for conditioning information, and without the need to estimate a density ratio.

To further understand the influence of disaster risk on the pricing kernel, I introduce a distribution bound on the SDF volatility that is closely related to the Hansen and Jagannathan (1991) bound. The distribution bound summarizes the risk-return trade-off of an asset paying out one dollar when the market return falls below a certain threshold. I show that disaster risk makes the risk-return trade off highly favorably by going short in an asset paying one dollar in case of a disaster. The price of such an asset is high because investors are willing to pay a significant premium to insure against disaster risk, but the risk is limited since the actual probability of a disaster is comparatively low. The Sharpe ratio associated to this investment therefore dominates the Sharpe ratio of a direct investment in the market portfolio. Specifically, in the data, the Sharpe ratio on selling an asset that pays out one dollar if the return falls below the 5th percentile is 30% in monthly units, while the Sharpe ratio of investing in the market portfolio is only 13%. I also show that models which do not embed a source of disaster risk, such as conditional lognormal models, cannot rationalize this finding.

I conclude by proposing a model-free lower bound on disaster risk premia to assess the robustness of my earlier findings. This lower bound is observed from option prices and is inspired by recent bounds on the equity premium (Martin, 2017; Chabi-Yo and Loudis, 2020). Using quantile regression, I show that the lower bound explains a substantial proportion of the fluctuation in disaster risk premia over time. Moreover, the lower bound relaxes the assumption of a time-homogeneous relation between the physical and risk-neutral quantile functions. Empirically, the lower bound closely aligns with the disaster risk estimates derived from quantile regression, further strengthening the robustness of my earlier findings.

1.1 Related Literature

My approach, which uses quantile regression to measure local dispersion between the physical and risk-neutral distribution, is related to a larger body of literature that estimates the pricing kernel from returns and option data (Aït-Sahalia and Lo, 2000; Jackwerth, 2000; Rosenberg and Engle, 2002; Beare and Schmidt, 2016; Linn et al., 2018; Cuesdeanu and Jackwerth, 2018). However, estimating the pricing kernel from returns and options can be challenging, especially in the tails of the distribution, where the ratio of densities that defines the pricing kernel can become unstable. In addition, using historical returns to estimate the physical density can lead to inconsistent results (Linn et al., 2018). Beason and Schreindorfer (2022) apply a similar methodology to decompose the unconditional equity premium.

In contrast, QR can be used to draw inference on the pricing kernel indirectly, by leveraging the observed realized return and risk-neutral distribution, which avoids the estimation of a density ratio. Furthermore, QR can account for changes in the shape and scale of the underlying SDF over time due to changing conditional information, while the approach of Cuesdeanu and Jackwerth (2018) renders an estimate of the SDF that only allows the normalizing constant to be time-varying, since the shape and scale are time invariant (see Section 4.1).

The QR approach also lays out a new framework to analyze disaster risk in a model-free fashion, defining this risk as the conditional quantile difference between the physical and risk-neutral measure in the left-tail. Since my results indicate that these differences are substantial, I offer new empirical evidence supporting disaster risk as a key explanation of the equity premium, as in the models of Rietz (1988) and Barro (2006, 2009), or more recently Schreindorfer (2020) and Ai and Bhandari (2021). Furthermore, my analysis adds nuance to the understanding of the equity premium’s drivers. While Beason and Schreindorfer (2022) assert that the worst 5% of returns account for 91.5% of the equity premium, my methodology reveals that these returns contribute only 17% to the equity premium. The results differ since I account for conditioning information, and my time series of returns includes the Covid-19 crisis.

Complementary to the QR estimates, I derive a nonparametric bound on the SDF volatility closely related to the bound of Hansen and Jagannathan (1991). They argue that the SDF is necessarily volatile and use this observation to screen asset pricing models. Several papers have built on this insight using higher-order moment bounds (Snow, 1991; Almeida and Garcia, 2012; Liu, 2021) and entropy bounds (Stutzer, 1995; Bansal and Lehmann, 1997; Alvarez and Jermann, 2005; Backus et al., 2014). These bounds all provide a measure of how much the risk-neutral distribution differs from the physical distribution. Unlike the distribution bound, all of these measures are global in that they rely on averages over the entire state space. The distribution bound in this paper is a function rather than a single statistic and can be considered an intermediate approach between a single bound and a complete estimate of the SDF.

This paper is also related to the growing literature on using options to estimate forward-looking equity premiums (Martin, 2017; Martin and Wagner, 2019; Chabi-Yo and Loudis, 2020). However, unlike those papers that focus on the conditional expectation of excess returns, this paper uses option data to predict conditional return quantiles. The relationship between option prices and expected market return shocks has been extensively studied in the literature (Bates, 1991, 2000, 2008; Coval and Shumway, 2001; Bollerslev and Todorov, 2011; Backus et al., 2011; Ross, 2015). Similar to Bollerslev and Todorov (2011), this paper obtains a nonparametric measure of disaster risk. However, my approach differs in that it only uses risk-neutral information and is motivated by the interplay between the physical and risk-neutral quantile functions.

This approach also complements the recovery literature as it derives forward-looking approximations to the left- and right-tail of the physical distribution using option data (Ross, 2015; Borovička et al., 2016; Qin and Linetsky, 2017; Bakshi et al., 2018; Qin et al., 2018; Schneider and Trojani, 2019; Jackwerth and Menner, 2020). The time variation in the approximation for the left-tail quantile documented in this paper is consistent with the time-varying disaster risk models of Gabaix (2012), Wachter (2013), Constantinides and Ghosh (2017), Isoré and Szczerbowicz (2017), Farhi and Gourio (2018) and Seo and Wachter (2019).

Finally, the QR approach is related to conditional mean regressions that are common in the equity premium literature. The performance evaluation of conditional expected return predictors is well established in the literature, with important contributions from Campbell and Thompson (2008) and Welch and Goyal (2008). To evaluate the performance of the QR approach, I draw on earlier work of Koenker and Machado (1999) and extend the evaluation toolkit to the quantile setting, specifically focusing on out-of-sample performance. This paper thus complements the literature on conditional return prediction by extending it to the entire distribution.

The rest of this paper is organized as follows. Section 2 presents the main empirical results from the quantile regressions and its consequences for the equity premium and SDF are discussed in Section 3. Section 4 provides further evidence on the robustness of QR to estimate disaster risk relative to extant approaches. Section 5 introduces the distribution bound, discusses its use in asset pricing models, and presents estimates of the distribution bound from empirical data. Building on the results of Sections 2 and 3, Section 6 establishes a model-free lower bound on disaster risk premia. Finally, Section 7 concludes.

2 Empirical Estimates of Quantile Difference

This section documents empirical estimates of the conditional difference between the physical and risk-neutral quantile functions. I first discuss the notation and then consider an example to clarify the idea and motivate the methodology.

2.1 Notation

Let denote the market return from period to , where can be measured in days or years, depending on the context. The risk-free rate over the same period is denoted by , which is assumed to be known at time . In the absence of arbitrage, there exists a positive random variable such that, conditional on all time information

| (2.1) |

The random variable is referred to as the stochastic discount factor (SDF) and the expectation in (2.1) is calculated under the physical probability measure , which is the actual distribution of the market return, i.e. . The SDF can potentially depend on many state variables, but these are suppressed from the notation for brevity. It is convenient to restate (2.1) in terms of risk-neutral probabilities:

where the expectation is calculated under the risk-neutral measure induced by . Finally, denotes the physical CDF of the market return conditional on all information available at time , denotes the conditional probability density function (PDF) and denotes the conditional -quantile. As before, a tilde superscript refers to the risk-neutral measure, so that

The physical and risk-neutral quantiles depend on the underlying random variable (i.e., ), but I typically omit this dependence as the underlying random variable always refers to the market return.

To clarify my approach of using quantiles to analyze disaster risk, I consider the following asset pricing model that will be used several times in the paper.

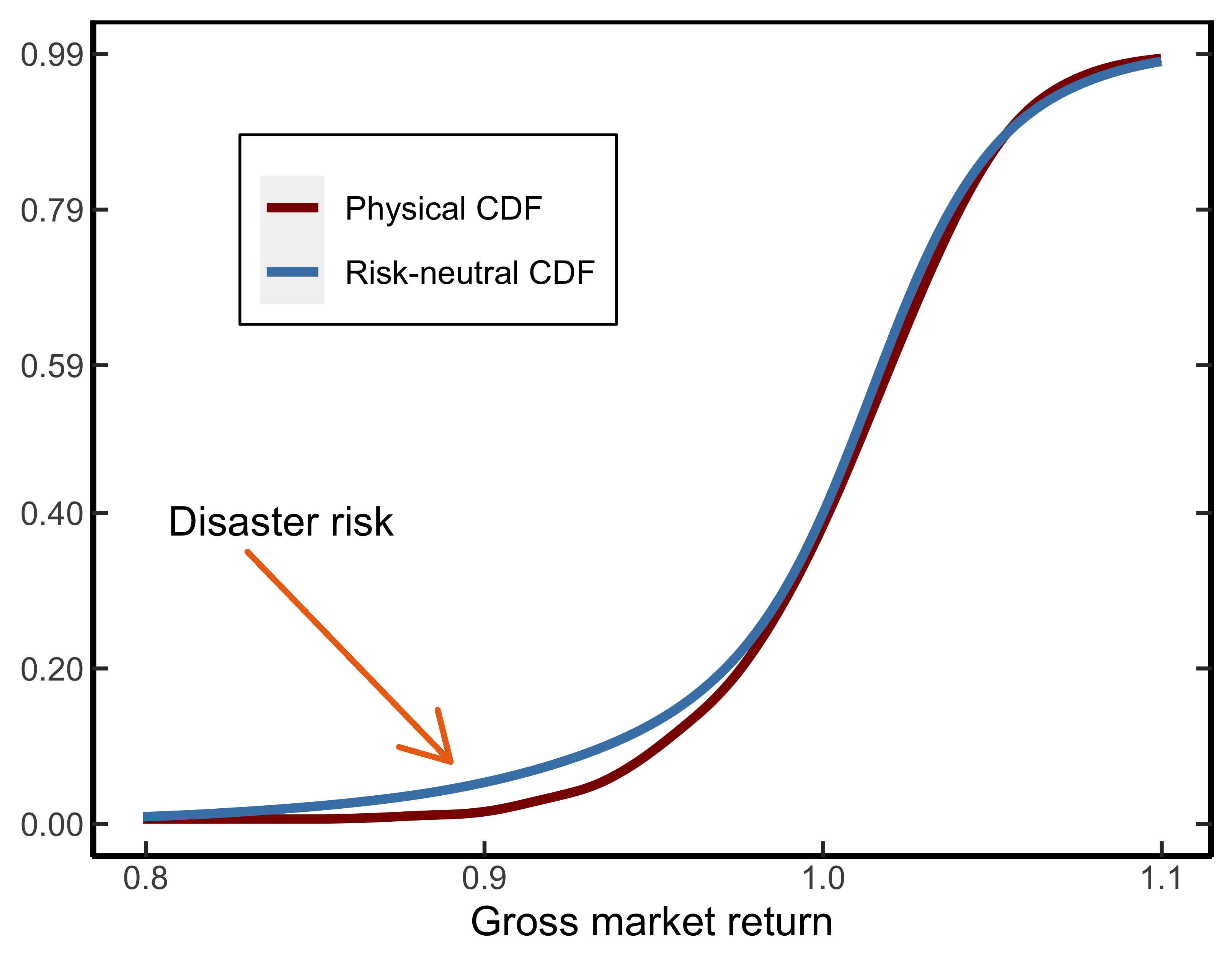

Example 2.1 (Disaster risk).

Consider the disaster risk model analyzed in Backus et al. (2011). The SDF process is given by

where is a time discount factor, is the coefficient of relative risk aversion, and is consumption growth in period . Consumption growth follows a two-component structure:

and is a Poisson mixture of normals to capture jumps representing rare shocks to consumption growth that are large in magnitude. The number of jumps, , take on nonnegative integer values with probability , and conditional on , the jump term is normal: . Backus et al. (2011) show that the risk-neutral distribution of consumption growth in a representative agent model is again a normal mixture with parameters:

| (2.2) |

In this setup, risk aversion amplifies the jump frequency ( if ) as well as the jump size (). If the model is calibrated such that , then can be interpreted as a disaster shock if a jump takes place .

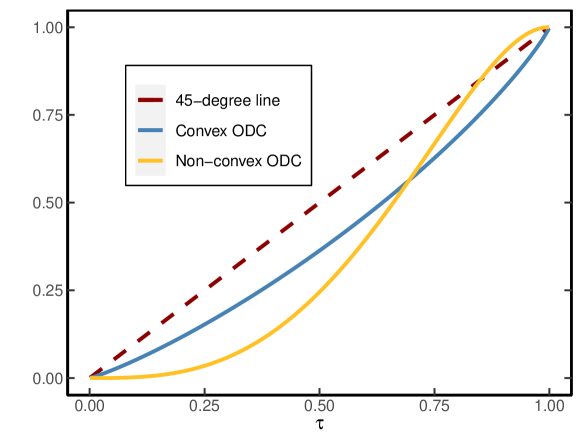

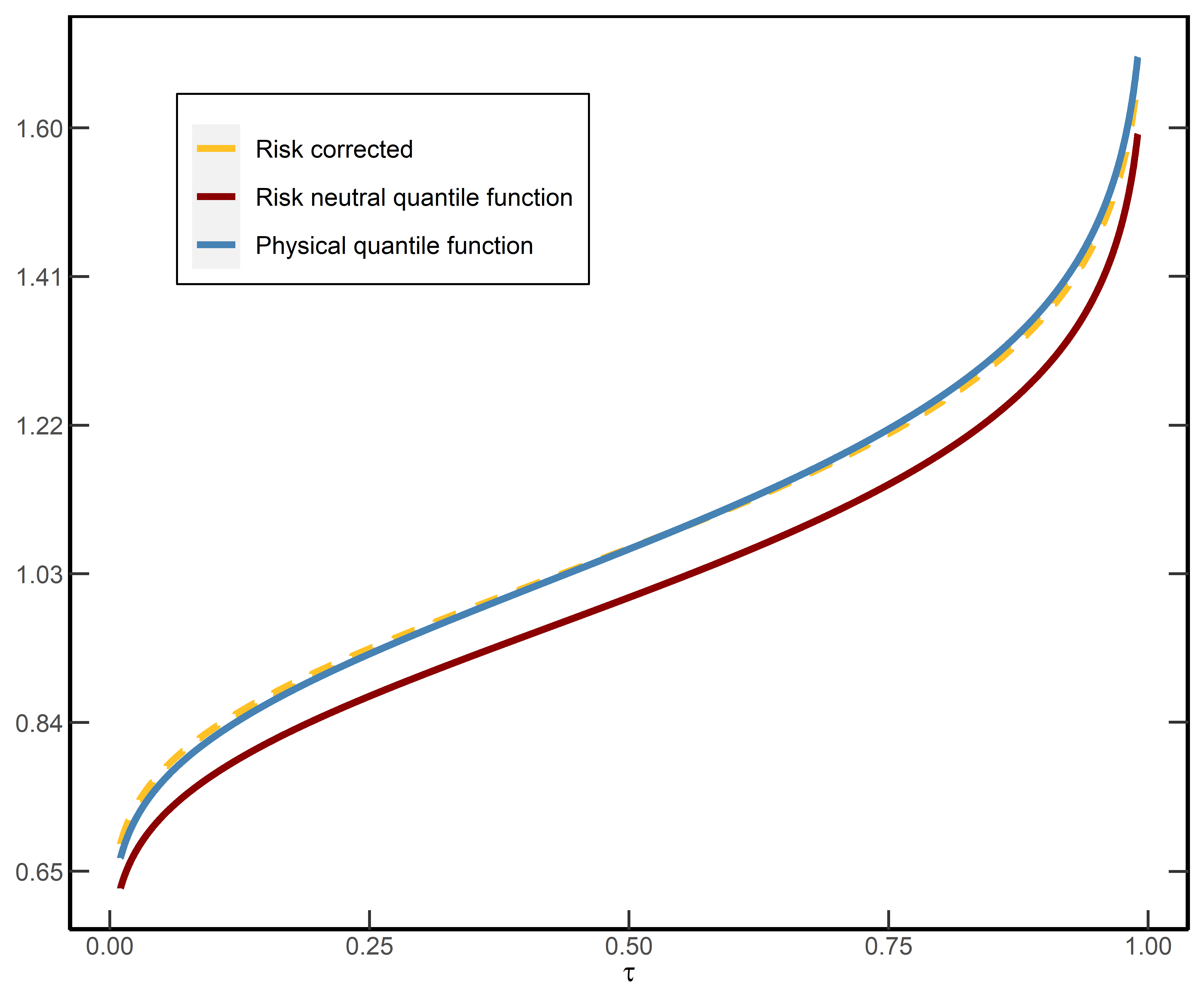

Figures 1(a) and 1(b) illustrate the impact of jumps on the physical and risk-neutral quantile functions.

Specifically, in the absence of jumps, the market return follows a lognormal distribution and Figure 1(a) shows that the difference between the physical and risk-neutral quantile functions is approximately equal in both tails. However, when jumps are introduced, this difference is almost entirely concentrated in the left-tail. This result is driven by the impact of jumps on the risk-neutral distribution, and the requirement that is crucial to drive a wedge between the physical and risk-neutral measures in the left-tail (see (2.2)). The question is whether these distinct shape restrictions on the physical and risk-neutral distribution are supported by the data.

2.2 Methodology and Econometric Model

Building on the discussion in Example 2.1, it is of interest to estimate the quantile difference between the physical and risk-neutral measures. The disaster risk model predicts that these differences are

significant in the left tail while negligible in the right tail. Therefore, I refer to in the left-tail as disaster risk premia.

While the conditional risk-neutral distribution and its quantile function can be inferred from option prices without specific modeling assumptions (Breeden and Litzenberger, 1978), the same cannot be said for the physical distribution, unless strong assumptions are made about the martingale component of the SDF (Ross, 2015; Borovička et al., 2016). The information available about the conditional physical distribution is limited to a single realization of the market return, as follows conditional on time . Consequently, the primary challenge in measuring disaster risk premia lies in the unobservable nature of , which has made model-free inference challenging thus far.

2.2.1 Risk-Neutral Quantile Regression

In order to overcome this difficulty, I assume the following model for the physical quantile function

| (2.3) |

If the world is risk-neutral, for all . Departures from risk-neutrality at a specific percentile are reflected by point estimates of that are far from the benchmark. Given a sample of observations , the unknown parameters in (2.3) can be estimated by quantile regression (Koenker and Bassett, 1978):

| (2.4) |

where is the check function from quantile regression

Even if the world is not risk-neutral, the model in (2.3) can still be correctly specified, as is the case for conditional lognormal models (see Section 4.1). When the model is misspecified, the estimation in (2.4) remains meaningful as QR finds the best linear approximation to the conditional quantile function (Angrist et al., 2006).222This result is analogous to OLS, which finds the best linear approximation to the conditional expectation function, even if the model is misspecified. Since the risk-neutral quantile itself is a highly non-linear transformation of state variables, the model can accommodate non-linear dependence between the physical quantile function and state variables driving the economy. The benefit of using the risk-neutral quantile function as a regressor is that it does not require the econometrician to take a stand on the state variables driving the physical distribution. Furthermore, both and are conditioned on the same information set, thus avoiding the mismatched information critique of Linn et al. (2018).

In addition, theory often suggests tantalizing links between the tails of the physical and risk-neutral distribution. Table 1 presents correlations between and for both left and right tails in different asset pricing models. In most models, these correlations are nearly one, indicating a strong positive relation that can be modeled by (2.3). Only for , the correlation is notably lower at 41% in the Campbell and Cochrane (1999) model and -67% in the Drechsler and Yaron (2011) model.

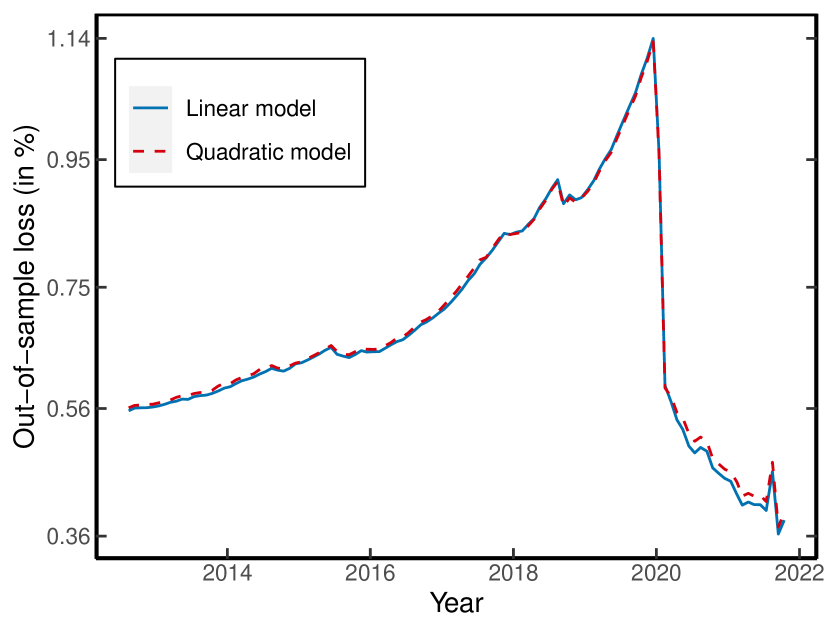

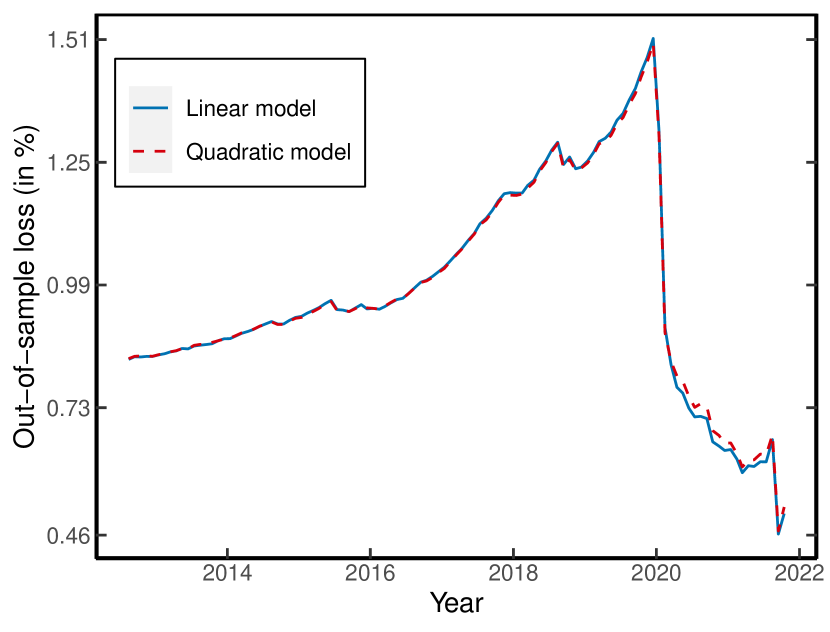

In Appendix F.1, I consider non-linear specifications as alternatives to the linear model in (2.3). Broadly speaking, I find that the linear model outperforms all non-linear models when predicting the physical quantile function out-of-sample. Based on this evidence, and the close linear approximation suggested by asset pricing models, I use the linear specification throughout most of the paper.

Percentile 0.05 0.1 0.2 0.3 0.7 0.8 0.9 0.95 Lognormal Campbell and Cochrane (1999) 96.94 94.49 83.61 40.88 86.51 94.25 97.27 98.26 Bansal and Yaron (2004) 99.97 99.97 99.98 99.98 99.99 99.99 99.99 100.00 Disaster Drechsler and Yaron (2011) 99.90 99.44 94.67 -67.16 96.88 98.75 99.45 99.67 Wachter (2013) 95.40 99.63 99.57 98.98 99.71 99.88 99.94 99.97 Constantinides and Ghosh (2017) 99.86 99.72 99.21 97.58 85.96 94.68 97.32 97.90 • Note: This table reports the correlation between and in conditional lognormal models and models that embed a source of conditional disaster risk. The correlations at various percentiles are obtained by simulating draws of the ergodic distribution of states in each model.

Remark 1.

An alternative to QR is nonparametric estimation of the SDF as proposed by Aït-Sahalia and Lo (2000), Jackwerth (2000) and Rosenberg and Engle (2002). This method can infer the quantile difference from the estimated SDF but relies on pooled historical returns, which can be problematic for forward-looking distribution estimation (Linn et al., 2018). More recently, Linn et al. (2018) and Cuesdeanu and Jackwerth (2018) proposed an estimator of the SDF that accounts for forward-looking information. However, this method presents challenges such as non-convex optimization, the objective function might be undefined due to the small number of existing risk-neutral moments (see Figure G9), ambiguity in basis function selection, and the inability to account for shape changes in the SDF leading to incorrect conditional inference. QR, on the other hand, avoids these issues, as shown in more detail in Section 4.1.

2.2.2 Measures of Fit

Based on the quantile regression (2.4), I consider two measures of fit to evaluate how well the risk-neutral quantile locally approximates the physical distribution. The first in-sample measure, , is defined as333It is well known that in the denominator of (2.5) equals the in-sample -quantile.

| (2.5) |

This measure of fit was proposed by Koenker and Machado (1999) and is a clean substitute for the OLS . I also consider an out-of-sample measure of fit

| (2.6) |

where is the historical rolling quantile of the market return from time to , and is the rolling window length. Notice that (2.6) is a genuine out-of-sample metric since no parameter estimation is used. In the equity premium literature, Campbell and Thompson (2008) stress the importance of out-of-sample predictability; (2.6) is analogous to their out-of-sample .

2.3 Data and Estimation

To estimate the quantile regression in (2.4), I require data on the market return and the risk-neutral distribution over time. I use overlapping returns on the S&P500 index from WRDS over the period 2003–2021 to represent the market return. I calculate the market return over a horizon of 30-, 60-, and 90-days. Second, over the same horizon, I use put and call option prices on the S&P500 on each day from OptionMetrics to estimate the risk-neutral quantile function based on the Breeden and Litzenberger (1978) formula:

| (2.7) |

where denotes the time price of a European put option on the S&P500 index with stock price , strike price and expiration date . This formula is model-free and only requires a no-arbitrage assumption. Due to the lack of a continuum of option prices, interpolation of different maturity options and missing data for option prices far in– and out-of-the money, it is a nontrivial exercise to obtain accurate estimates of (and hence ) from (2.7). A detailed description of my approach that overcomes these issues is described in Appendix B.2, which is based on Filipović et al. (2013).444This approach uses a kernel density and adds several correction terms to approximate the risk-neutral density. I follow Barletta and Santucci de Magistris (2018) and use a principal components step to avoid overfitting in the tails. Finally, I obtain the risk-free rate from Kenneth French’s website.555See http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html#Research

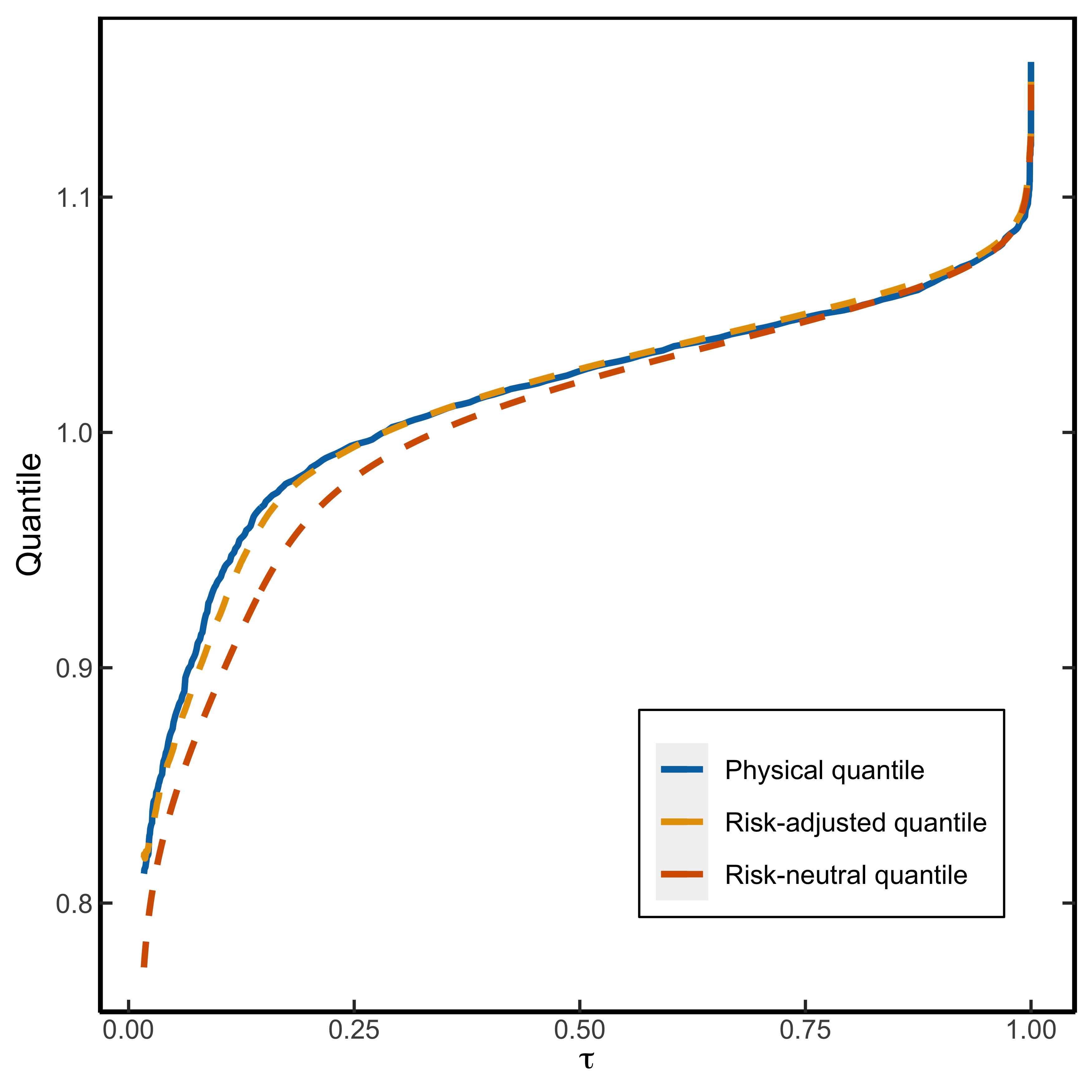

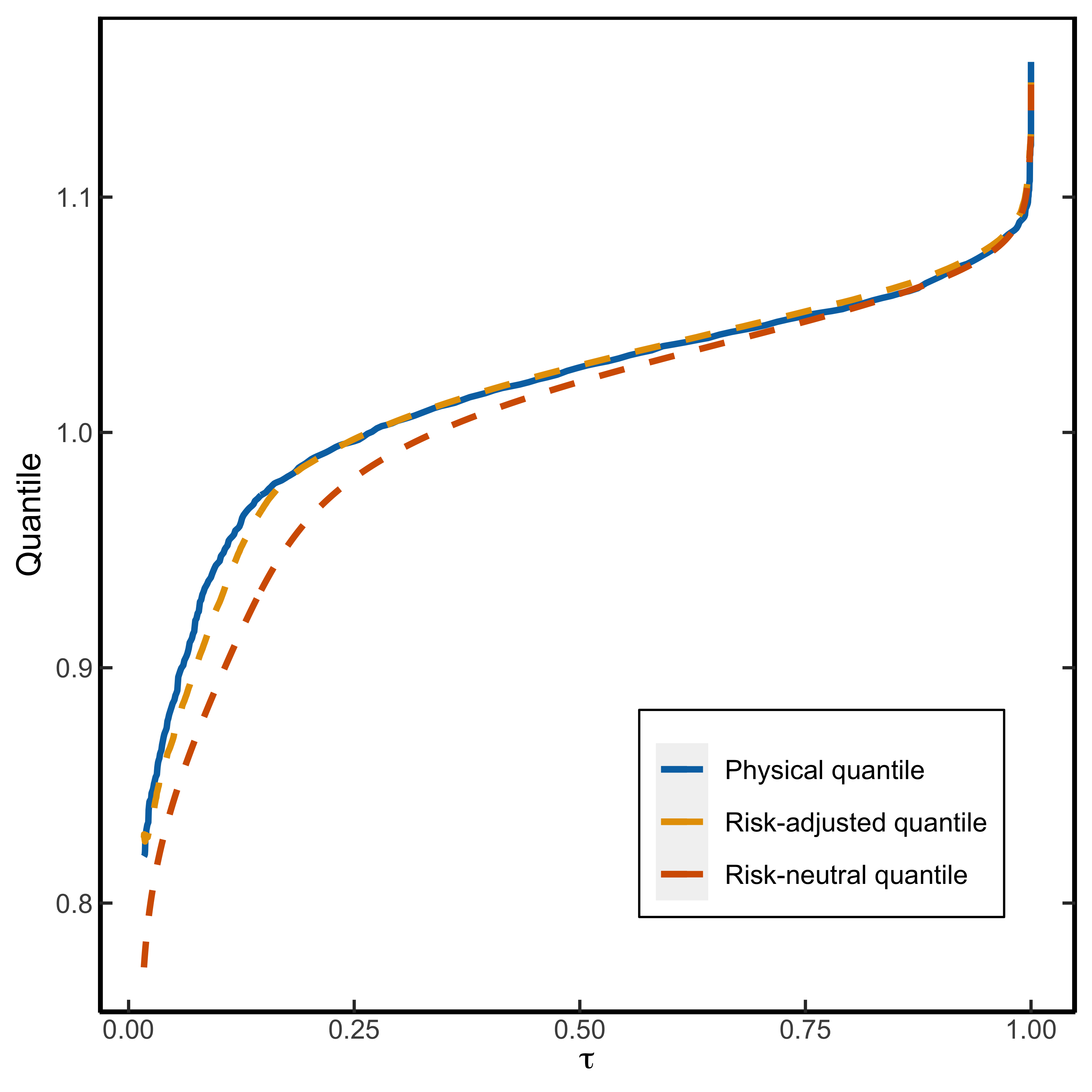

Table 2 shows the QR estimates of (2.4). The point estimates are close to the benchmark in the right-tail (), but not in the left-tail (). Additionally, the joint restriction that is rejected for all , at all horizons. In contrast, the null hypothesis is never rejected for . The fact that the risk-neutral distribution provides a good approximation of the physical distribution in the right-tail is confirmed by the measures of fit, and , which are also shown in Table 2. Specifically, both in- and out-of-sample, the risk-neutral quantile fits the physical distribution much better in the right-tail.

Remark 2.

The standard errors for the quantile regression in Table 2 are obtained by the smooth extended tapered block bootstrap (SETBB) of Gregory et al. (2018), which is robust to heteroscedasticity and weak dependence.666It may seem counterintuitive that the standard errors decrease in the tails, which are generally harder to estimate. However, since the regressor changes with , there is an opposing effect that can cause the standard errors to decrease in the tails. This happens if is more variable in the tails, akin to the intuition in OLS that more variability in the regressor decreases the standard error. In the data, is much more variable in the tails. This robustness is important in the estimation, since I use overlapping returns which creates time dependence in the error term, akin to the overlapping observation problem in OLS (Hansen and Hodrick, 1980). SETBB also renders an estimate of the covariance matrix between and , which can be used to test joint restrictions on the coefficients.777I use the QregBB function from the -package QregBB, available on the author’s Github page: https://rdrr.io/github/gregorkb/QregBB/man/QregBB.html. The only user required input for this method is the block length in the bootstrap procedure.

Horizon [%] [%] [%] [%] 30 days* 0.00 6.28 6.11 99.88 0.01 3.45 1.01 98.52 0.02 0.55 0.89 90.98 0.00 0.00 2.49 99.58 0.00 0.03 1.75 97.25 0.00 4.62 4.19 99.93 0.03 7.79 7.47 99.95 0.19 12.44 12.50 99.95 0.96 20.41 21.88 55.85 *(Obs. 4333) 0.95 0.57 27.07 31.31 22.41 60 days** 0.05 0.00 3.12 13.14 100.00 0.00 1.79 3.50 100.00 0.01 0.38 -0.03 99.95 0.00 0.01 -0.12 99.47 0.02 0.25 2.34 99.79 0.02 5.57 4.60 99.77 0.05 8.41 7.65 99.91 0.07 12.70 12.23 100.00 0.58 21.66 22.79 92.86 **(Obs. 4312) 0.95 0.90 31.07 34.19 13.73 90 days*** 0.05 0.01 2.90 15.63 100.00 0.00 3.46 3.84 100.00 0.03 0.83 1.93 100.00 0.04 0.17 -0.52 99.84 0.02 0.22 -1.76 99.77 0.01 6.37 3.81 99.98 0.02 10.45 8.87 100.00 0.10 15.47 16.54 100.00 0.79 23.18 27.92 100.00 ***(Obs. 4291) 0.95 0.86 32.14 39.88 52.37 • Note: This table reports the QR estimates of (2.4) over the sample period 2003–2021 at different horizons, using overlapping returns. Standard errors are shown in parentheses and based on SETBB with a block length equal to the prediction horizon. Wald test denotes the -value of the joint restriction . denotes the goodness of fit measure (2.5). is the out-of-sample goodness of fit (2.6), using a rolling window of size 10 times the prediction horizon. refers to the sample expectation defined in (3.4) and standard errors are reported in parentheses, which are obtained by stationary bootstrap based on 10,000 bootstrap samples. The last column indicates the time series average of the event that , where .

3 Equity Premium Puzzle and SDF Implications

Building on the estimates in Table 2, this section shows that the conditional equity premium is driven by disaster risk, and that disaster risk is a pervasive feature of the data, which poses a new challenge to asset pricing models. I further comment on two implications of Table 2 that relate to properties of the SDF that have previously received attention in the literature.

3.1 Equity Premium Puzzle

The results in Table 2 show that the physical distribution is close to risk-neutral in the right-tail, but not in the left-tail. Investors in the market portfolio thus get compensated for bearing downside risk, but not upside risk. This result has important repercussions for explanations of the equity premium puzzle. To see this, consider the following decomposition of the equity premium888See Appendix A.1 for a derivation.

| (3.1) |

where is a percentile close to zero. The first term on the right-hand side aggregates the local difference between the risk-neutral and physical quantiles in the left-tail, which I define as the contribution of disaster risk. The results in Table 2 show that these differences are the primary determinant for the equity premium, as in the right-tail we have . The latter finding is consistent with the modeling assumption in (time-varying) disaster risk models that shocks to the market return are negative conditional on a disaster occurring (see, e.g., the condition in Example 2.1). Hence, an asset pricing model seeking to explain the (conditional) equity premium of the market return must embed a source of disaster risk.

To illustrate the pervasiveness of disaster risk in the data, I consider the Lorenz curve associated with the conditional equity premium

The Lorenz curve summarizes the proportion of the equity premium contributed by the bottom % of returns, akin to its interpretation in labor economics to summarize wealth inequality. Since is unobserved, I use instead the inferred value, , with the estimated parameters coming from the QR estimates in (2.4).

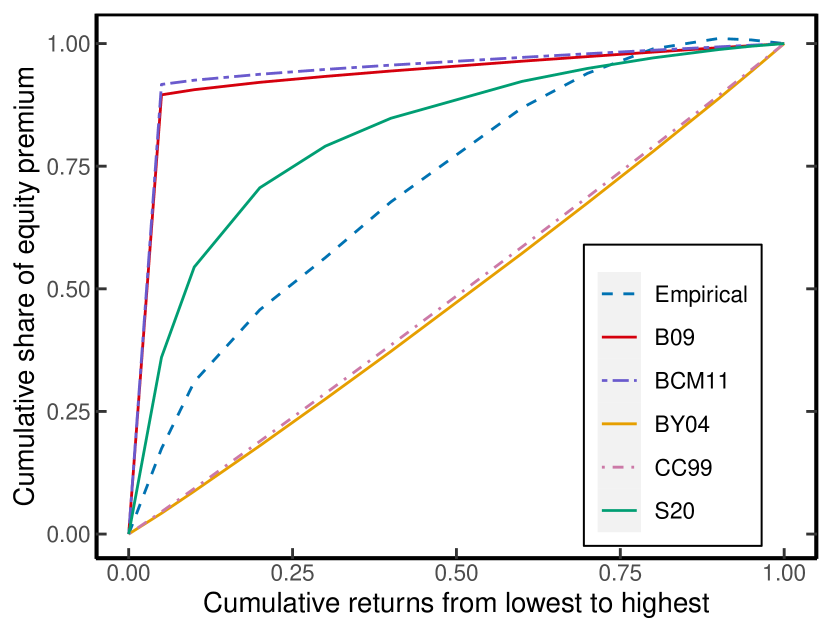

Figure 2(a) shows the average Lorenz curve in the data, together with the Lorenz curve implied by various asset pricing models.999I thank Beason and Schreindorfer (2022) for making the code to simulate from these models publicly available. In the data, the Lorenz curve is quite concave, thus showing that the majority of the equity premium is contributed by the left-tail. At the same time, my estimation adds nuance to the degree of disaster risk influencing the equity premium. Specifically, while the disaster risk models of Barro (2009) and Backus et al. (2011) attribute approximately 90% of the equity premium to the lowest 5% of returns, empirical estimates suggest this proportion is only around 17%. These findings also deviate substantially from the nonparametric estimates of Beason and Schreindorfer (2022), who report that 91.5% of the equity premium is driven by the bottom 5% of returns. Our results differ because I account for conditioning information, while Beason and Schreindorfer (2022) employ an unconditional approach. Using unconditional averages can inflate the tails of the physical distribution (Chabi-Yo et al., 2008), leading to an overestimation of disaster risk.

On the other hand, the models of Campbell and Cochrane (1999) and Bansal and Yaron (2004) are even more misspecified since the Lorenz curve in these models is slightly convex, thus attributing more than 50% of the equity premium to upside returns. The model of Schreindorfer (2020) matches the Lorenz curve best, even though it also overestimates the contribution of disaster risk to the equity premium.

I also consider the Gini coefficient derived from the Lorenz curve

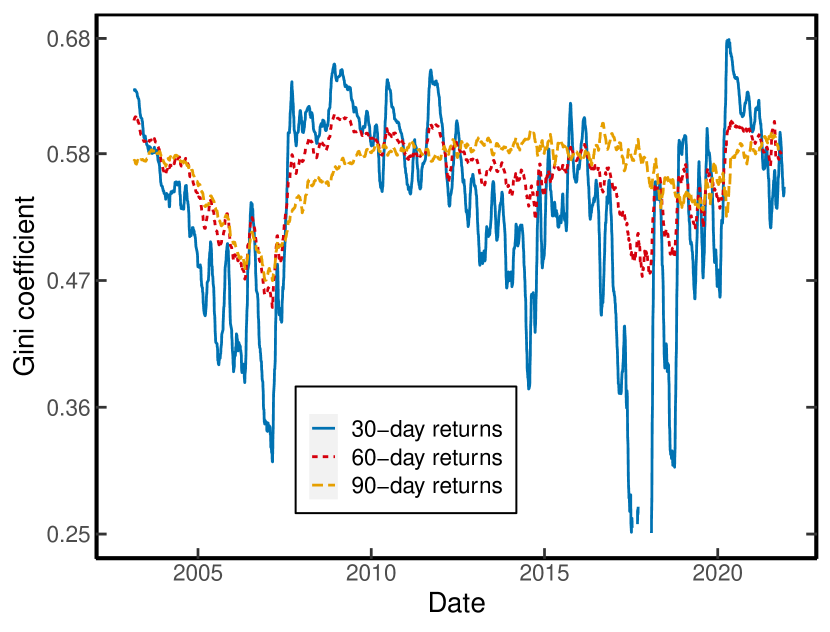

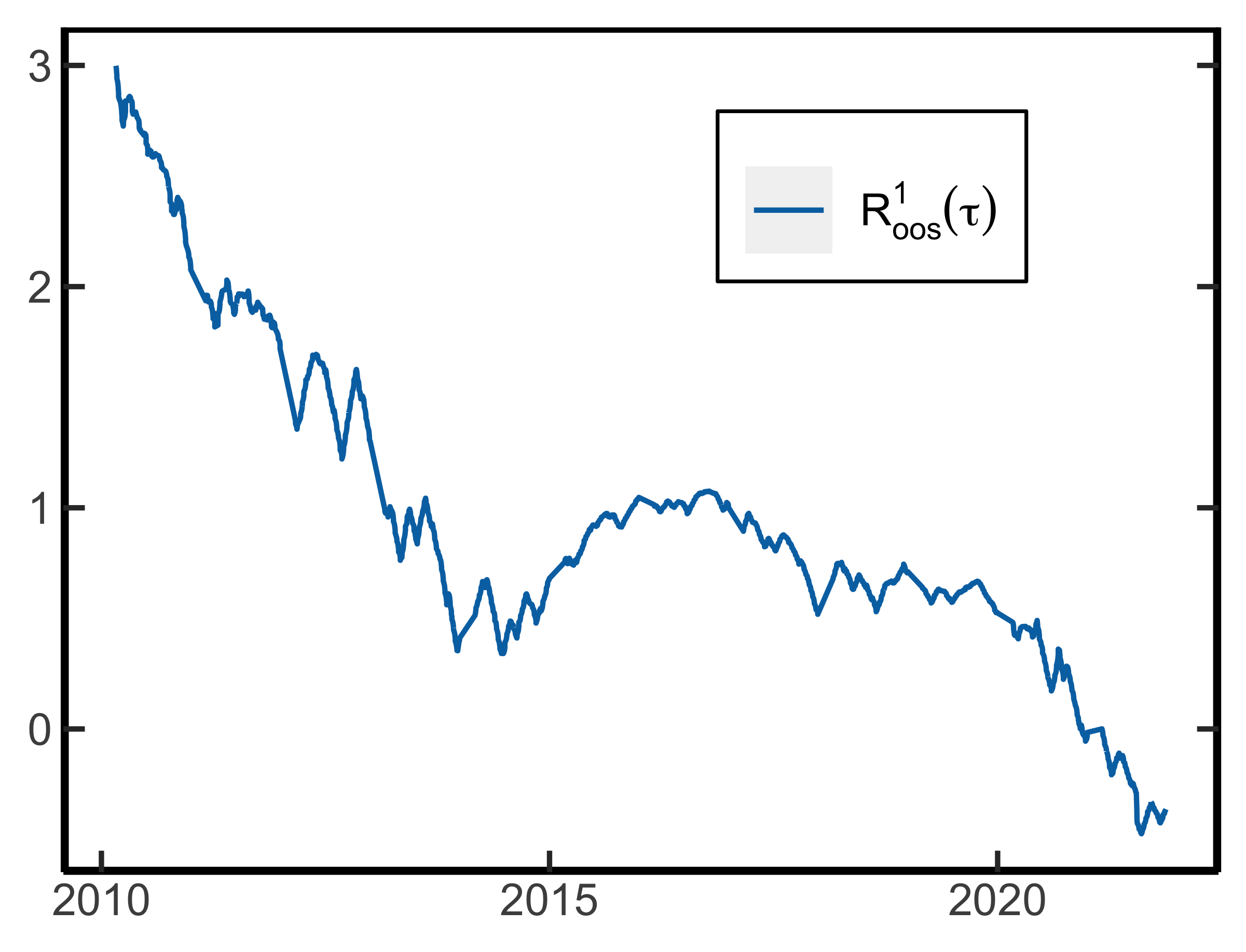

By construction, the Gini coefficient is between -1 and 1, and a value closer to 1 indicates that a bigger proportion of the equity premium is coming from the left-tail. In contrast, a value of 0 suggests that the equity premium is evenly distributed across the return distribution, while negative values imply that the right-tails contribute more to the equity premium than the left-tails. Figure 2(b) shows the time series of conditional Gini coefficients for various return horizons. For 30-day returns, the Gini coefficient mostly hovers between 0.33 and 0.68. At longer horizons, the Gini coefficients exhibit less variability and typically range between 0.47 to 0.6. These coefficients are also countercyclical, peaking during periods associated with economic downturns, such as the 2008 financial crisis and the Covid-19 crisis. Overall, the Gini coefficients consistently exhibit strong positive values, highlighting the pervasiveness of conditional disaster risk in the data, which extends beyond crisis periods.

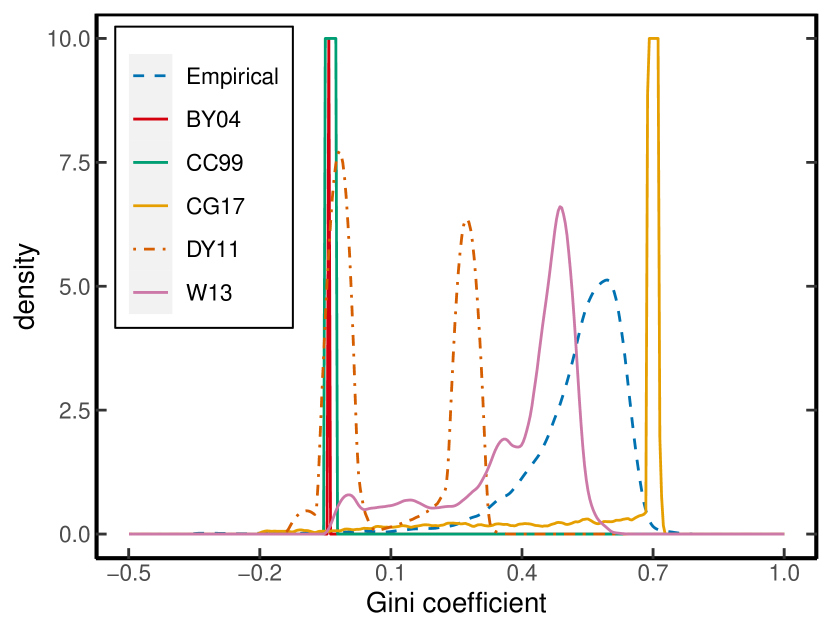

Finally, I analyze the ergodic distribution of Gini coefficients in time-varying asset pricing models and compare it to the distribution implied by the data.101010In the model, I obtain the distribution of Gini coefficients from the state distribution. In the data, I rely on the time series average. If the data are generated by the model and the system is ergodic, Birkhoff’s theorem implies that the state and time averages are equal almost everywhere. Figure 2(c) displays these distributions and shows that many asset pricing models have difficulty in matching the empirical distribution. The conditional lognormal models of Campbell and Cochrane (1999) and Bansal and Yaron (2004) imply negative Gini coefficients, with minimal variation among different states, contrary to what the data indicate. The models of Drechsler and Yaron (2011), Wachter (2013), Constantinides and Ghosh (2017) all incorporate a source of disaster risk, but they also have difficulty to match the empirics. In particular, the models of Drechsler and Yaron (2011) and Wachter (2013) embed too little disaster risk, while the model of Constantinides and Ghosh (2017) overestimates the impact of disaster risk.

3.2 Driver of Disaster Risk Premia: Insurance or Beliefs?

Disaster risk premia have two components: an insurance effect and a forward-looking beliefs effect (under rational expectations). To see this, consider a short position in a derivative security that pays one dollar if the market return is below a threshold, denoted by , in the left tail. The return on such an investment can be expressed as

During a crisis, the price of this security tends to rise. This effect can occur in the disaster risk model (Example 2.1), if risk aversion increases when a disaster hits, leading to an increase in and a subsequent decrease in . Simultaneously, investors may believe that the actual probability of a disaster increases during a crisis. This belief drives up and, consequently, pushes down .

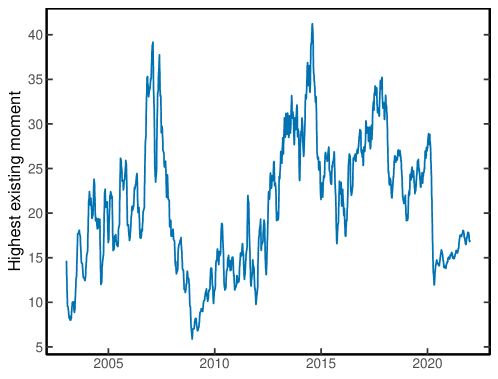

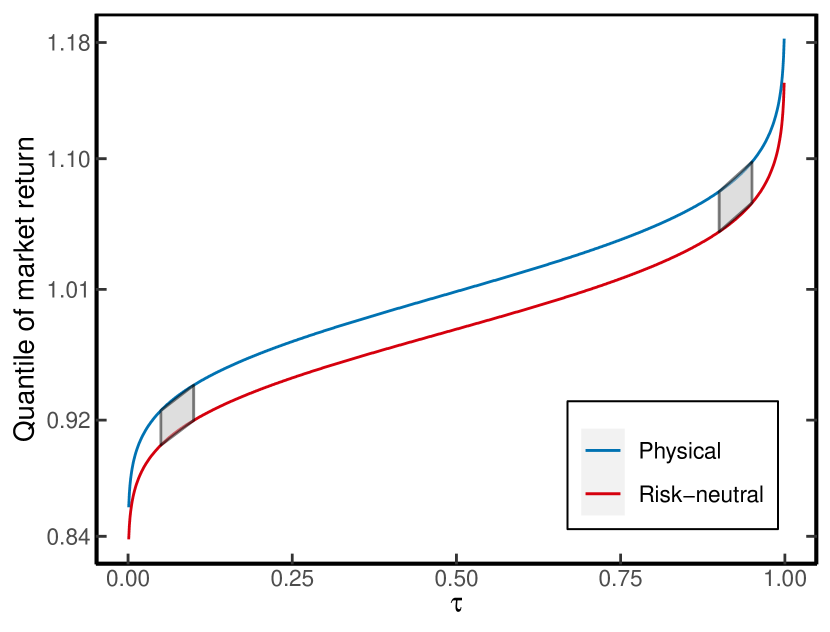

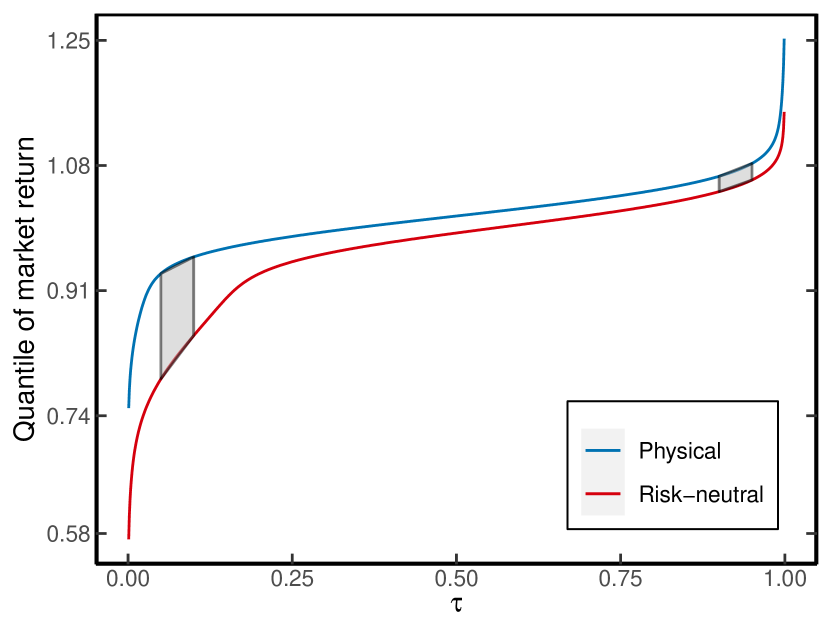

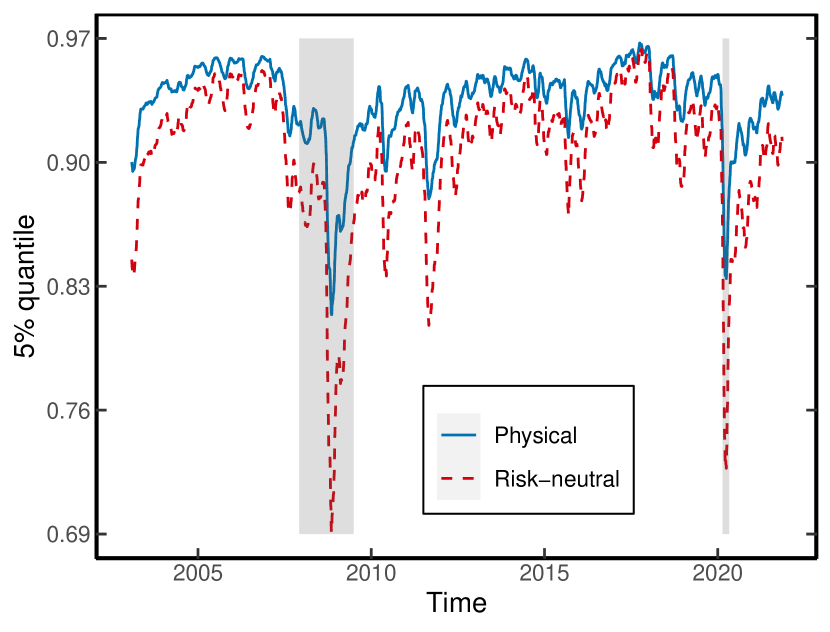

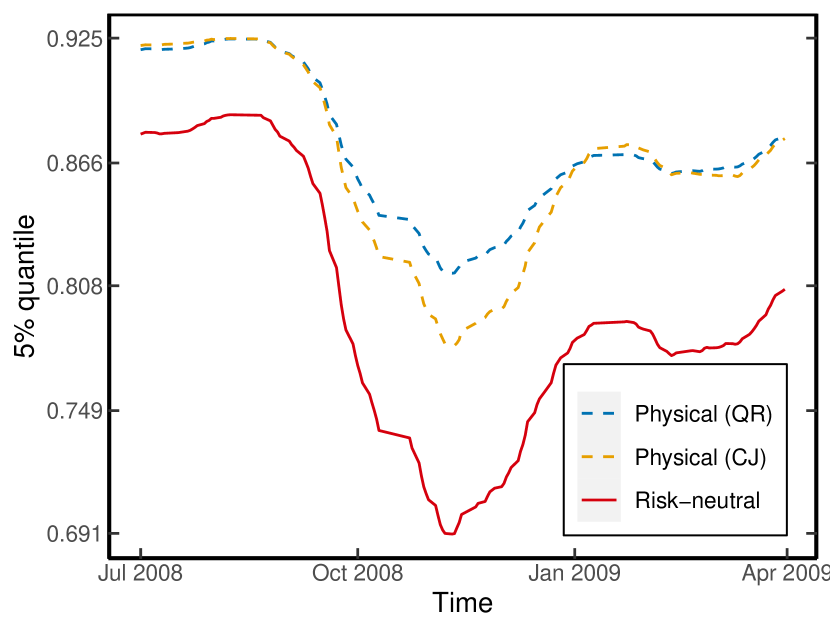

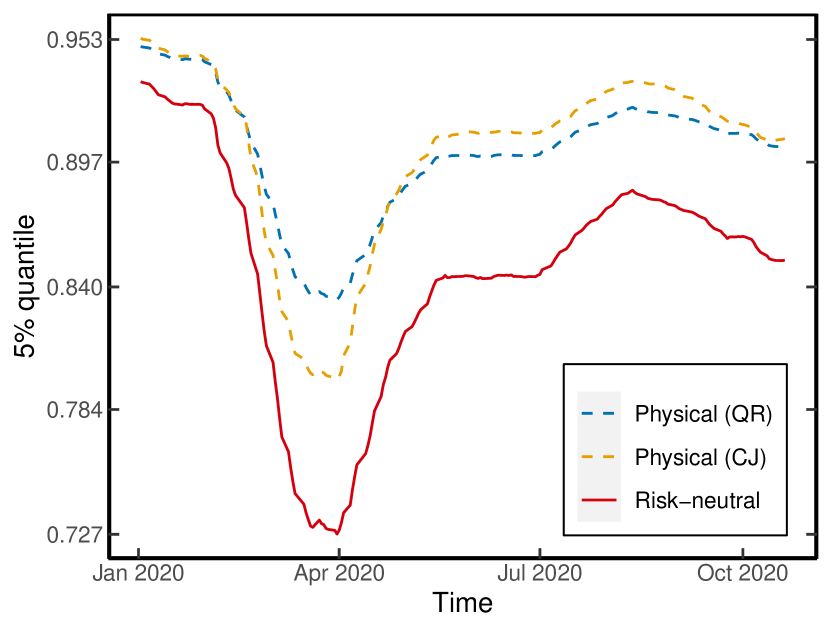

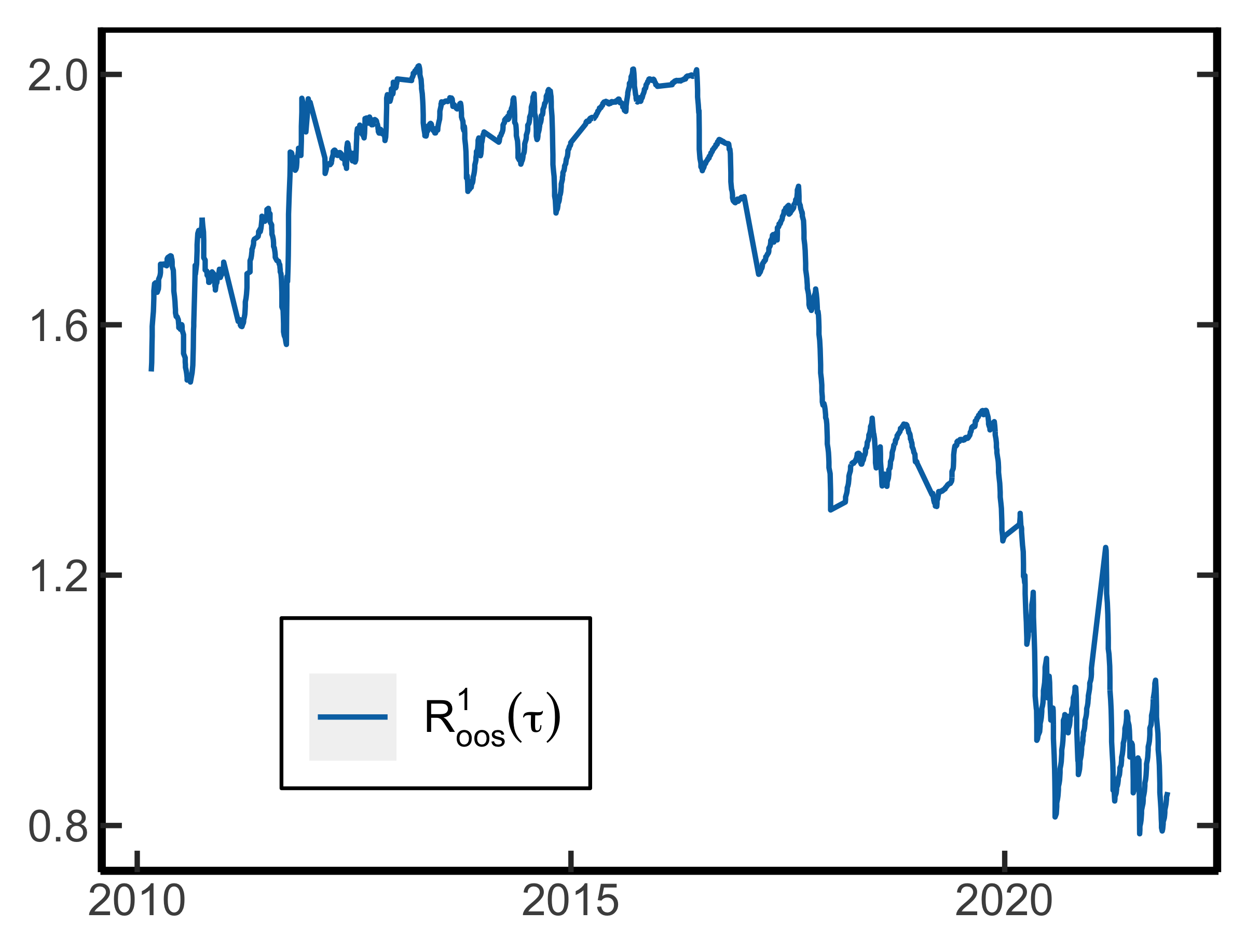

Building on this discussion, it is not immediately clear what the net effect is on disaster risk premia (), as both and tend to decrease during periods of heightened market uncertainty. Figure 3(a) illustrates this effect for 30-day returns and . Notably, during the global financial crisis and Covid-19 crisis, both the physical and risk-neutral quantile functions exhibit significant drops.

However, the downward spikes in the risk-neutral quantile function are more pronounced, as it decreases to 63% in these periods. In contrast, the physical quantile function only drops to 78%, suggesting that a monthly loss of 22% or more had a 5% probability. To put this in perspective, this probability is 14 times higher than the estimate obtained from historical monthly S&P500 returns (from 1926 to 2021). This calculation shows that historical estimates can diverge significantly from forward-looking beliefs. Furthermore, the time fluctuations in the physical quantile function lend empirical support to the notion of time-varying disaster risk, as proposed in various models such as Gabaix (2012), Wachter (2013), Constantinides and Ghosh (2017), Isoré and Szczerbowicz (2017), Farhi and Gourio (2018) and Seo and Wachter (2019).

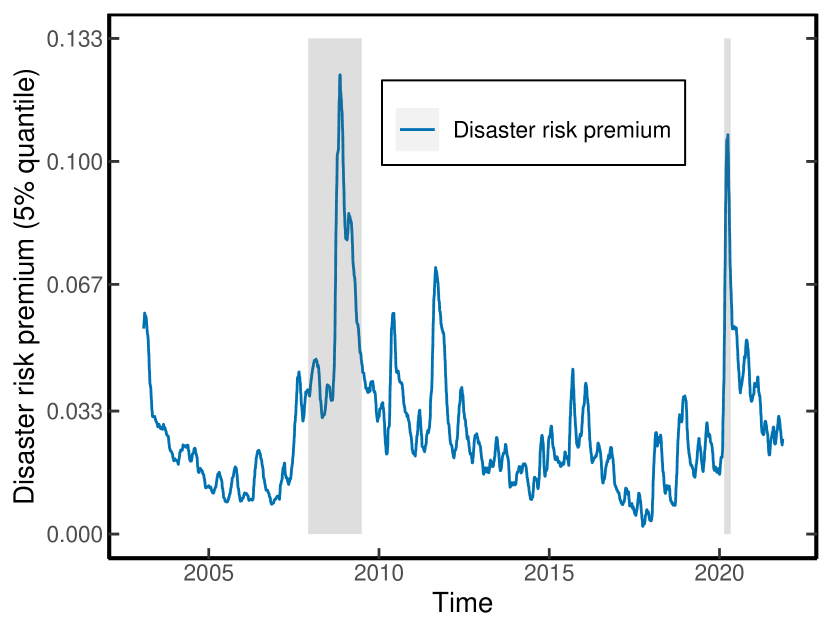

To shed light on the net effect on disaster risk premia during crises, Figure 3(b) displays the evolution of disaster risk premia over time. The most significant change occurs during the peak of the global financial crisis and the Covid-19 crisis. In these turbulent periods, disaster risk premia consistently rise, suggesting that the insurance effect is more substantial than the forward-looking beliefs effect.111111I find similar results for 60- and 90-day returns. Because of these large increases, disaster risk is a more important driver of the equity premium, which clarifies the countercyclical Gini coefficients in Figure 2(b).

3.3 Predicting the Equity Premium

The previous results establish that, in times of heightened market uncertainty, the equity premium is driven more by disaster risk. This observation suggests a strong link between and the tail of the risk-neutral distribution, which motivates the predictive regression

| (3.2) |

where is evaluated at .

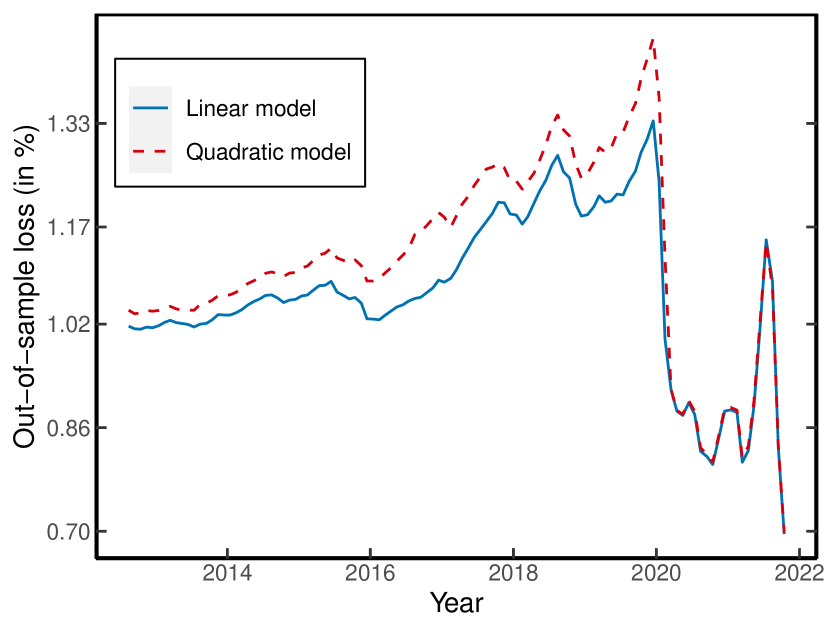

Table 3 shows the results at several return horizons. In all cases, the coefficient is negative, consistent with previous findings that the equity premium increases under market uncertainty. Following Welch and Goyal (2008), the table also reports the out-of-sample , denoted by , which compares the predictions of (3.2) to a rolling average of excess returns. Precisely, I estimate (3.2) using the sub-sample covering 2003–2012, and fix the estimated parameters to predict excess returns over the out-of-sample period 2013–2021. Encouragingly, is always positive and statistically significant according to the Diebold and Mariano (1995) test, thus suggesting that the left-tail of the risk-neutral quantile function outperforms the historical mean benchmark. These values are also substantially higher compared to the reported by Welch and Goyal (2008) using various valuation ratios, or Martin (2017) using SVIX.121212The latter is not directly comparable however, since SVIX does not require parameter estimation.

| Horizon | [%] | [%] | -value DM | ||

|---|---|---|---|---|---|

| 30 days | 10.44 | 1.82 | 0.00 | ||

| 60 days | 18.16 | 3.30 | 0.00 | ||

| 90 days | 26.67 | 4.20 | 0.00 | ||

| Sample | 2003–2021 | 2013–2021 | |||

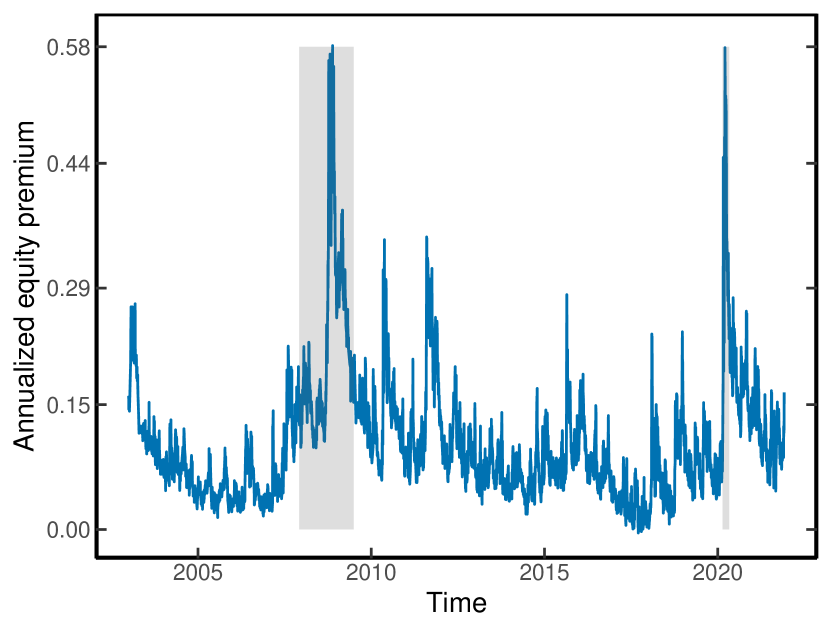

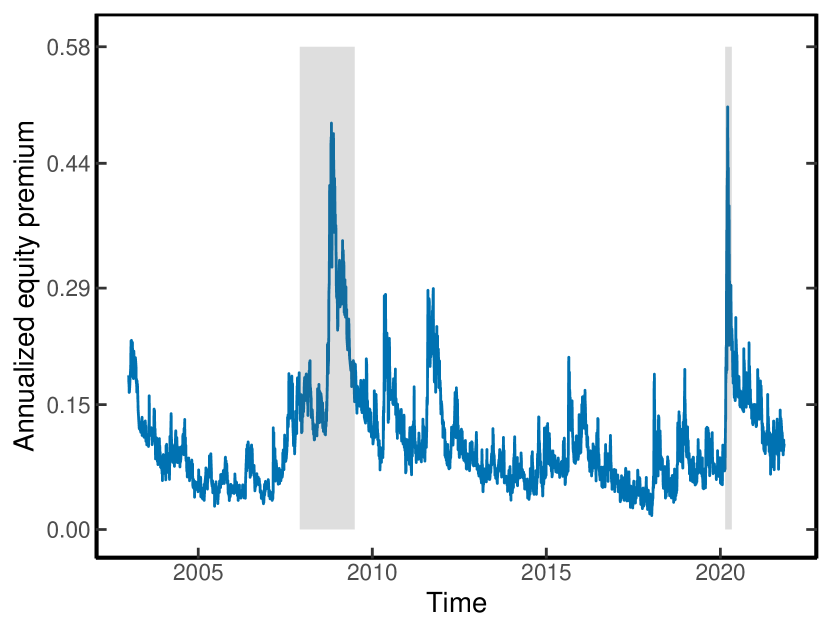

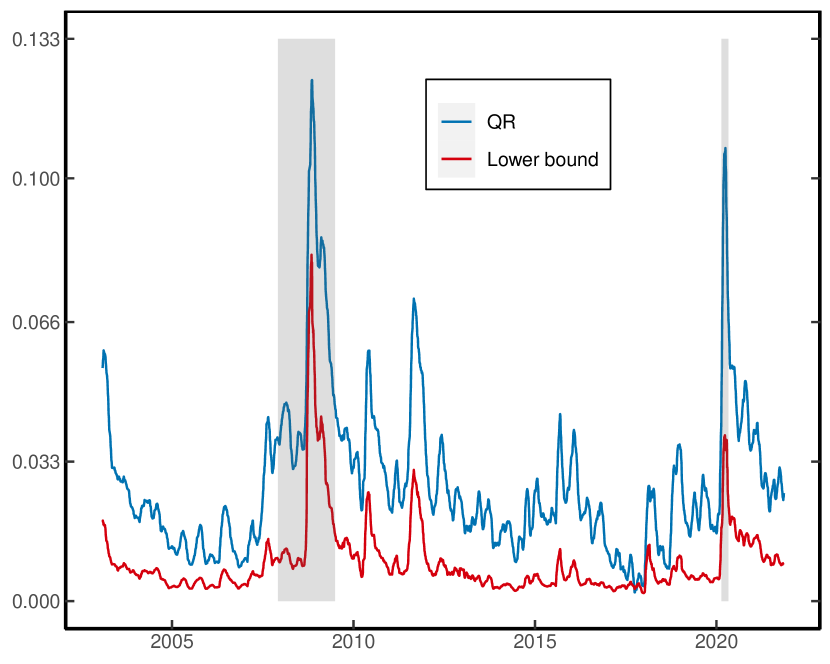

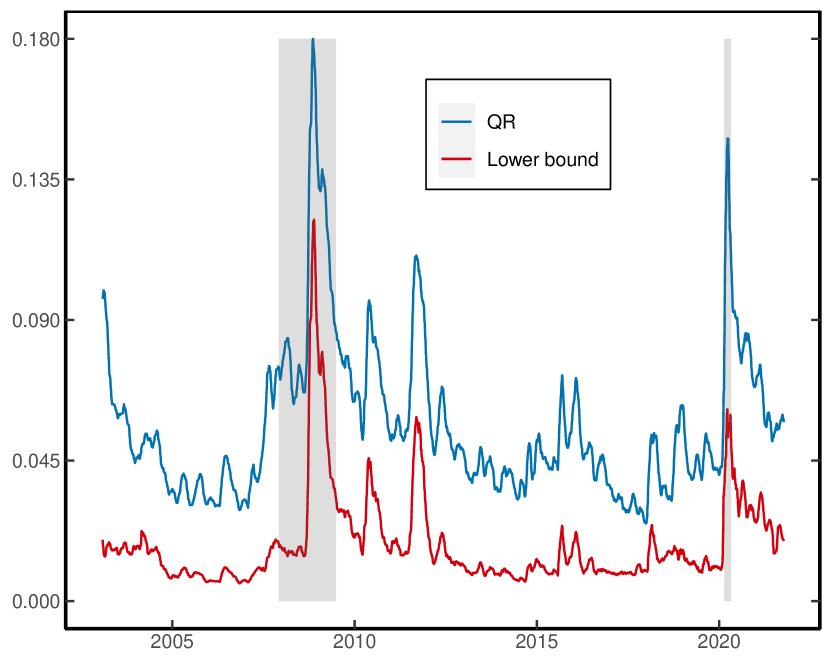

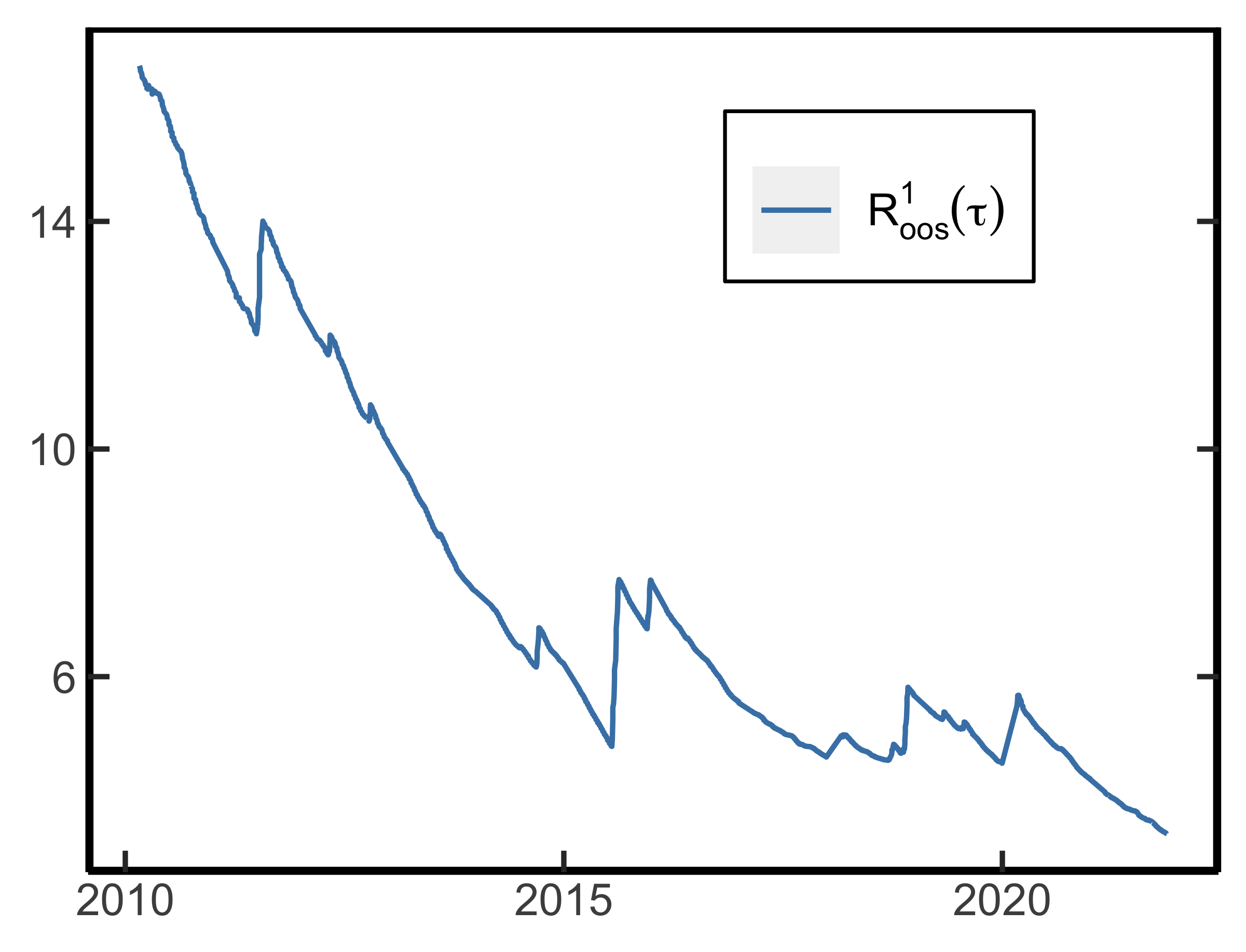

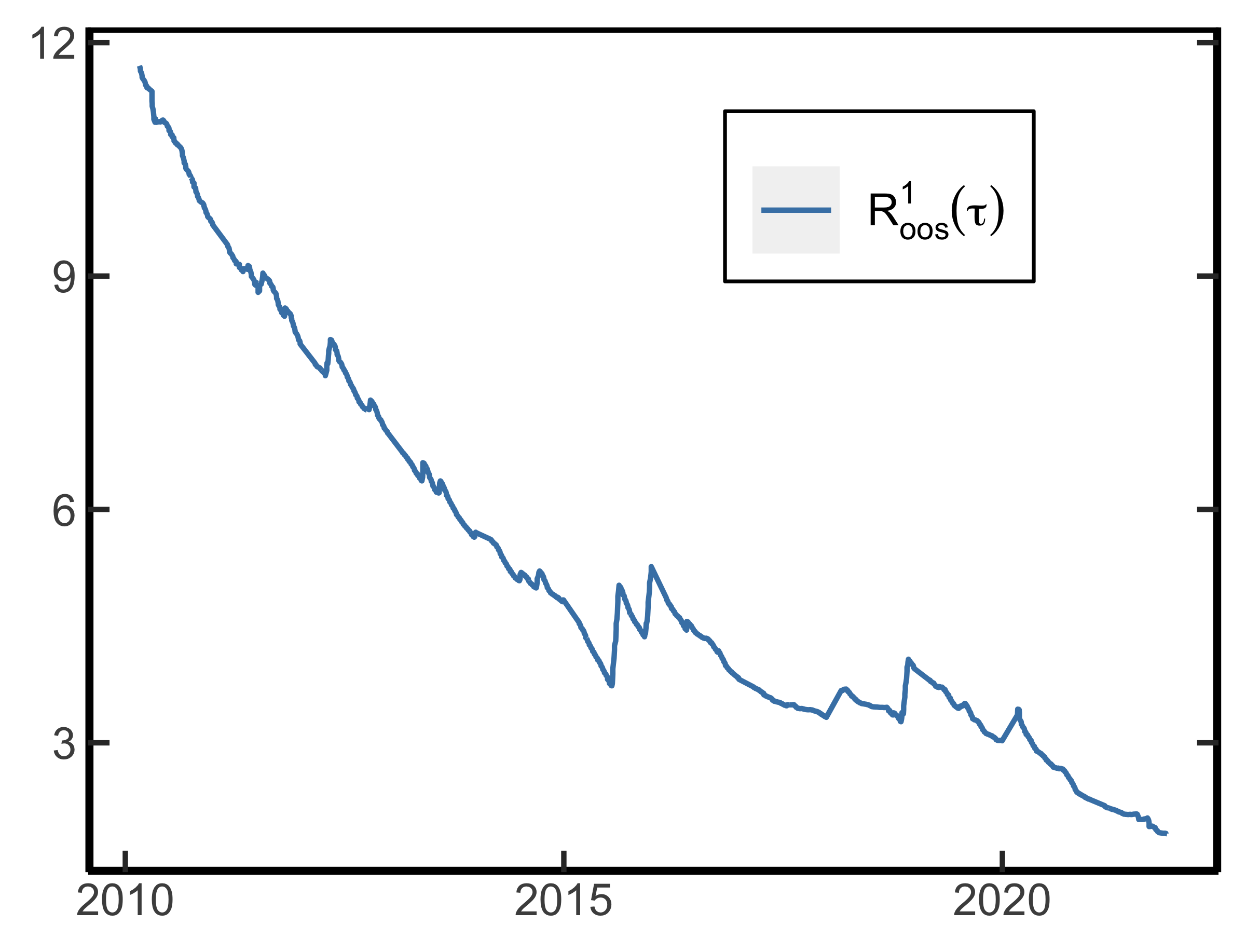

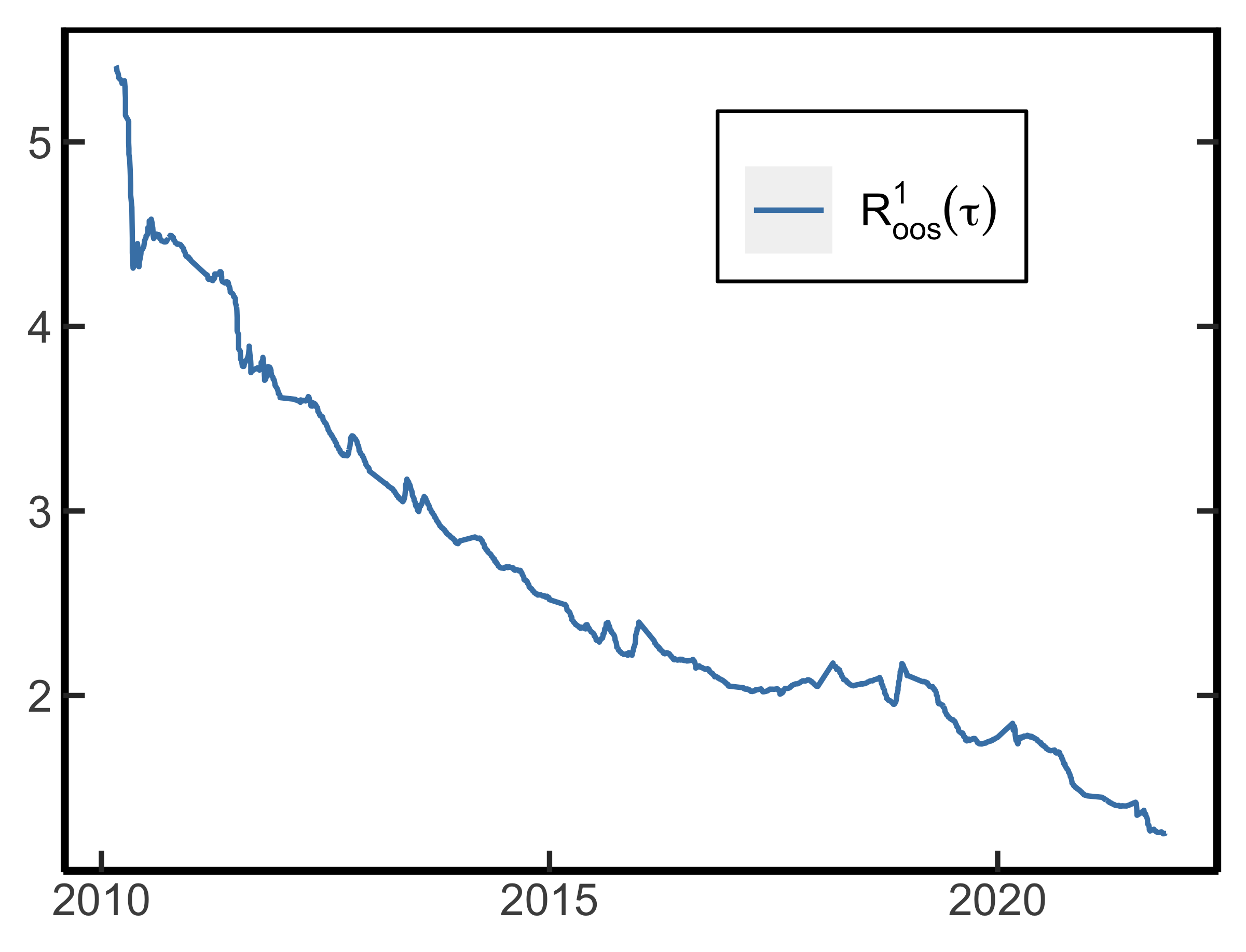

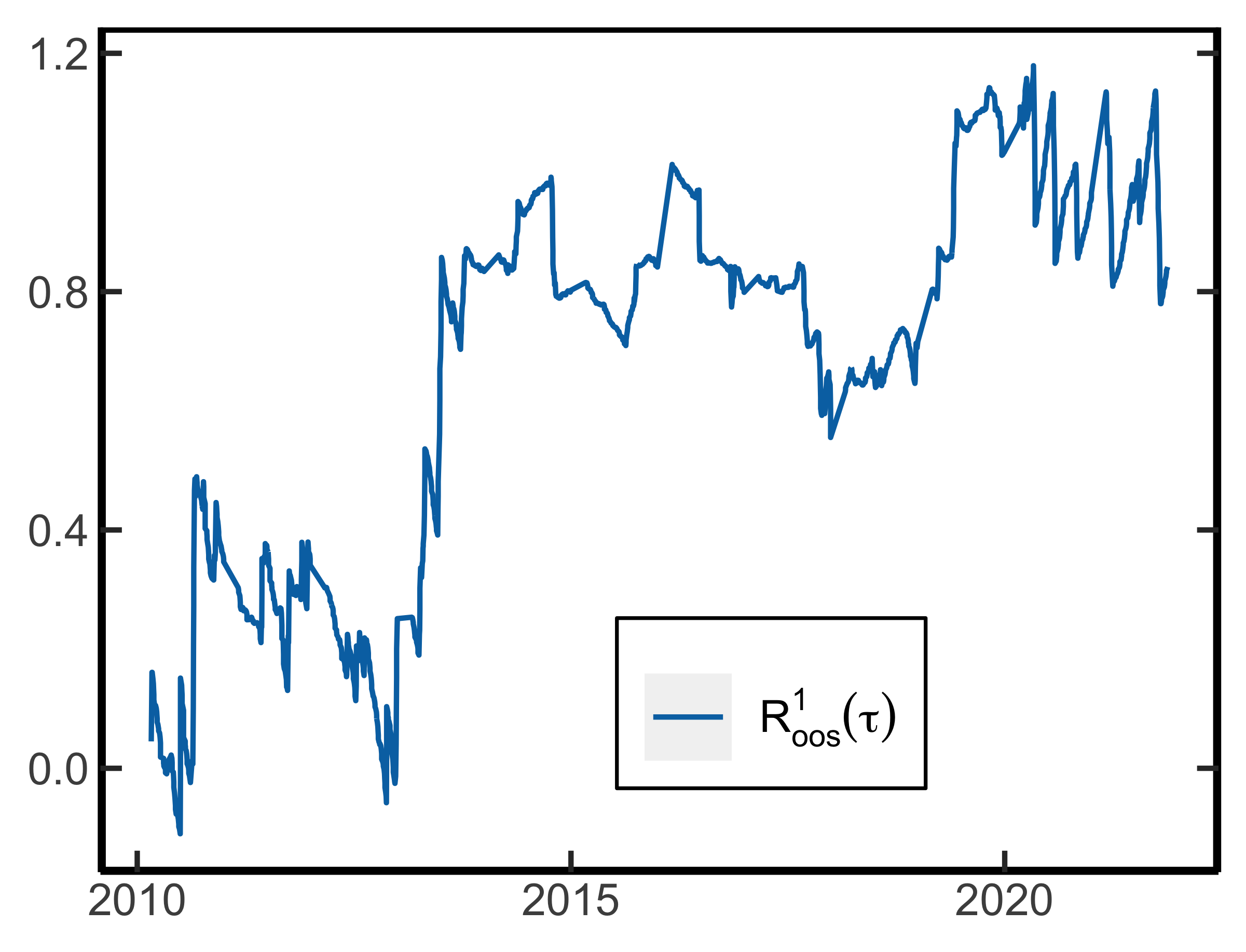

Figure 4 shows the estimated equity premium over time for 30- and 60-day returns. The panels are annualized to make them comparable. Both panels display considerable variation in the equity premium over time and large values during the global financial crisis and Covid-19 crisis. In these periods, Figure 4(a) suggests that the annualized equity premium peaks at 58%, which is substantial relative to more conventional estimates based on dividend-price ratios. On the other hand, the estimates around the 2008 financial crisis are in line with Martin (2017, Figure \@slowromancapiv@).

3.4 Pricing Kernel Monotonicity and Stochastic Dominance

Besides the equity premium puzzle, the QR estimates in Table 2 also provide insights into other asset pricing anomalies, such as pricing kernel monotonicity. Pricing kernel monotonicity refers to the property that is a decreasing function of the market return. Asset pricing models that link the SDF to the marginal rate of substitution imply that the pricing kernel is indeed a decreasing function. Empirically, there is suggestive evidence that the pricing kernel is not monotonic, which is puzzling as it contradicts that a representative investor is risk-averse (see Aït-Sahalia and Lo (1998), Jackwerth (2000), Rosenberg and Engle (2002), Bakshi et al. (2010), Beare and Schmidt (2016) and Cuesdeanu and Jackwerth (2018)). However, a formal statistical test that can detect violations of monotonicity is challenging as one needs uniform confidence bands for the estimated SDF, which requires tools from empirical process theory (see, e.g., Beare and Schmidt (2016)).

I consider a different approach based on stochastic dominance. Proposition A.1 in the Appendix shows that pricing kernel monotonicity implies that the physical distribution is first-order stochastic dominant (FOSD) over the risk-neutral distribution, i.e., for all . The latter condition can be rephrased as for all . A violation of stochastic dominance, and hence pricing kernel monotonicity, is thus implied if there is statistical evidence that for a single . To investigate this possibility, let131313The function was first introduced by Engle and Manganelli (2004) in a different context.

| (3.3) |

Hence, provides an estimate of which ought to be negative for all under FOSD.141414 also yields another measure of the difference between and . Consistent with the quantile regression estimates, the Hit statistic shows that and are similar in the right-tail, but different in the left-tail. The “” column in Table 2 reports the value of (3.4), which is positive for at the 30- and 60-day horizon. However, these estimates are not significant at the conventional levels and a violation of FOSD cannot be concluded.

Since if and only if , it follows that violations of stochastic dominance can also be identified directly from the quantile function. Based on the QR estimates (2.4), consider the predicted quantile function . The last column in Table 2 displays the time series average of instances where . Broadly speaking, for all horizons, violations of stochastic dominance are infrequent, except far in the right-tail. At , stochastic dominance is frequently violated, consistent with a non-monotonic pricing kernel.151515The most significant violations occur during two major financial crises: the 2008 financial crisis and the 2020 Covid-19 crisis. In representative agent models, this result is puzzling as it contradicts the assumption of decreasing marginal utility of wealth (see Proposition A.2 in the Appendix).

3.5 Belief Recovery

A recent literature asks to what extent Arrow prices can be used to learn about the underlying probability distribution of the data, or the subjective probabilities used by investors. Since Arrow prices are confounded by risk aversion, it is impossible to identify the underlying probabilities from Arrow prices alone, unless one imposes additional restrictions (Ross, 2015; Borovička et al., 2016; Bakshi et al., 2018; Qin et al., 2018; Jackwerth and Menner, 2020). For example, Ross (2015) uses the Perron-Frobenius theorem to recover investors’ beliefs, which agrees with the underlying

physical measure under rational expectations.

Complementary to this insight, the QR estimates in Table 2 show that the right-tail of the physical distribution can approximately be recovered from the right-tail of the risk-neutral distribution, which aligns with the investor’s belief under rational expectations. In contrast, the left-tail of the physical distribution cannot be recovered even though the risk-neutral quantile serves as a conservative lower bound. In Section 6, I propose a more stringent lower bound to recover the left-tail of the physical distribution as well from option data.

4 QR and Robust Estimation of Disaster Risk

Section 3.1 demonstrated that the conditional lognormal assumption is inconsistent with the observed disaster risk premia in the market. At the same time, Figure 2(a) showed that disaster risk models tend to overestimate the magnitude of disaster risk in the data. These conclusions heavily rely on the accuracy of QR in providing estimates of the physical quantile function.

In this section, I compare QR to nonparametric SDF methods for estimating disaster risk. Foreshadowing the results, I show that QR is more robust and argue that the SDF approach tends to overestimate disaster risk. These results help explain the current disagreement about the extent of disaster risk in the data, and provide further support for QR to estimate this risk.

4.1 QR in the Conditional Lognormal Model

To convey the intuition, it is convenient to work with a discretized version of the Black and Scholes (1973) model. There is a riskless asset that offers a certain return, , and a risky asset with return

| (4.1) |

where represents the conditional mean return, is the conditional volatility, and is a random shock that follows a standard normal distribution. In this setup, is a valid SDF with conditional Sharpe ratio

| (4.2) |

Hence, under risk-neutral measure, the conditional distribution of is given by

| (4.3) |

Notice that is implicitly observed from the risk-neutral distribution, but is unobserved with mean and variance . The following result characterizes the limiting behavior of the QR estimates (2.4) in the lognormal model when the variance of the equity premium is small. A convenient way to model this is by means of a drifting sequence as , which captures the intuition that the volatility of the equity premium is much smaller than the return volatility.

Proposition 4.1 (QR in Lognormal Model).

In the lognormal model described above with return observations and risk-neutral quantile functions , the following hold.

-

(i)

Suppose that conditional on time , follows a normal distribution , independent of . Let denote the physical quantile function of conditional on only. Then, for all a closed subset of for , the physical quantile function satisfies

where denotes the quantile function of the standard normal distribution.

-

(ii)

Consider a drifting sequence for , denoted by as . Then, under Assumption A.4 in the Appendix, the estimated parameters in the quantile regression

satisfy

(4.4) Furthermore, the quantile forecast based on the QR estimates satisfies

(4.5)

Proof.

See Appendix A.3. ∎

Proposition 4.1(i) shows that the risk-neutral quantile function is a good predictor of when is small, and the difference between the two functions is governed by the unconditional equity premium . In this case, Proposition 4.1(ii) suggests that the QR estimates are almost constant across and close to . This result obtains without assuming that follows a normal distribution. The wedge between and not explained by the equity premium can be attributed to uncertainty about , which increases the variance of the physical distribution. The assumption that is small relative to accords with empirical findings of Martin (2017, Table \@slowromancapi@), who finds that , whereas hovers around 20%. Unreported simulations show that the approximation in (4.4) obtains closely when the model is calibrated to match these stylized facts. As a result, the physical quantile forecast based on the QR estimates in (4.5) is also highly accurate.

4.2 QR versus Nonparametric SDF Estimation

Because of the availability of closed-form expressions in the lognormal model, it is instructive to compare the QR approach to alternative methods for estimating the physical distribution. Since the SDF represents the Radon–Nikodym derivative of the risk-neutral and physical measures, it is possible to obtain the physical quantile function from the estimated SDF. There is a substantial literature on how to estimate the SDF in a forward-looking manner (see Remark 1). For this comparison, I consider the state-of-the-art SDF estimator proposed by Cuesdeanu and Jackwerth (2018) (CJ).

After some algebra, the SDF in the Black-Scholes model can be expressed as a function of the market return:

| (4.6) |

where is the conditional Sharpe ratio (4.2). CJ project the unobserved SDF in (4.6) on the market return and estimate an SDF of the form

where is a time-varying constant, and is an unknown function that can be estimated by choosing a sieve basis. Since is time-homogeneous, it is evident that changes in the shape of the true SDF in (4.6) are not captured by the estimated SDF. Specifically, in times when the Sharpe ratio is high, the physical and risk-neutral measures exhibit more distinct differences, as the true SDF becomes steeper. Because the estimated SDF does not account for these shape changes, it leads to a severe underestimation of the physical quantile function in the left-tail. Proposition 4.1 demonstrates that the QR approach does not suffer from this limitation.

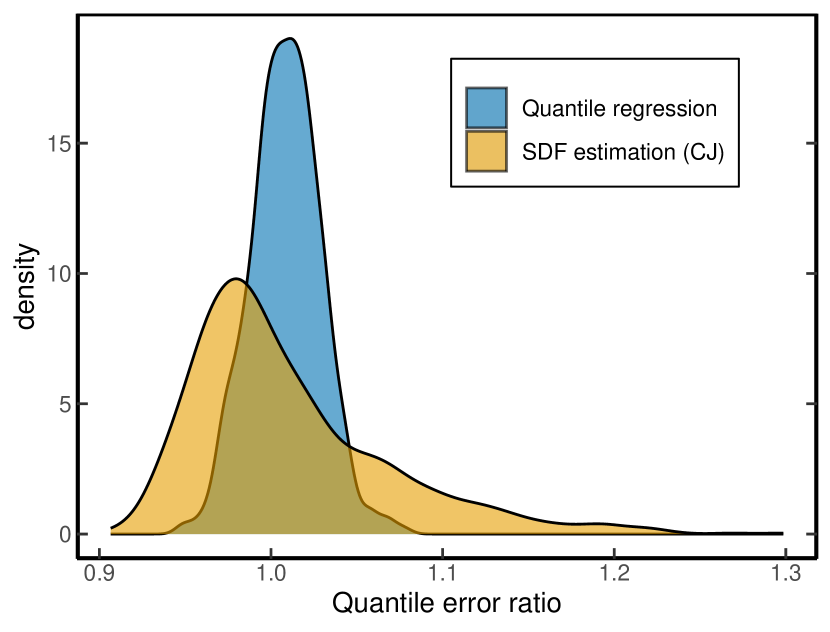

To illustrate this discussion, I simulate returns from the lognormal model and estimate the physical quantile function at the 5th percentile using QR and the SDF estimate of CJ. Since the conditional (physical) quantile function is known analytically in the lognormal model, I evaluate the forecast accuracy using the quantile error ratio, , where is the predicted physical quantile based on QR or the SDF estimate. Panel 5(a) displays the empirical density of error ratios obtained by simulating 1,000 returns. In line with Proposition 4.1(ii), the error ratio corresponding to QR is symmetric and closely centered around one. In contrast, when the physical quantile is inferred from the estimated SDF, the error density is biased and exhibits fat tails since the estimated SDF cannot change shape. Consequently, in periods of high disaster risk premia, the CJ method severely underestimates .

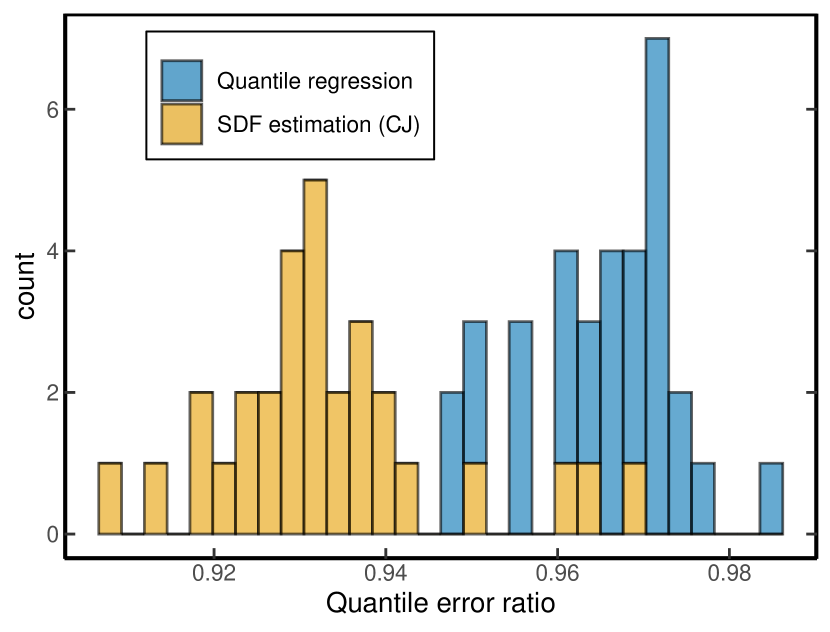

Panel 5(b) presents the histogram of error ratios conditioned on the 30 largest values of , clearly illustrating the downward bias in the SDF method. On average, the predicted physical quantile is 7% lower than its actual value when disaster risk premia are high. The QR approach is less affected by this bias because it can capture changes in the shape of the SDF. The computational benefits of QR are also notable, as the computation of the physical quantile forecast takes less than a second. On the other hand, the SDF method requires more than 20 minutes to complete the same task.161616Moreover, the optimization problem required to implement the sieve estimation did not converge, as the maximum number of iterations were exceeded. This problem occurs due to the large number of parameters to estimate, and because the optimization problem is not convex (see Remark 1).

The bottom panels of Figure 5 further illustrate the difference between QR and CJ using the 30-day return data from Section 2.3, particularly during the 2008 financial crisis and the Covid-19 crisis. At the height of both crises, both methods predict increases in disaster risk premia as rises significantly. As mentioned earlier, the SDF approach implies that disaster risk premia increase less relative to the QR approach, as the shape of the SDF remains constant over time. However, it is worth noting that while the QR approach performs well when returns are conditional lognormal, Appendix F.2 demonstrates that the quantile forecasts based on QR contradict (4.5), casting further doubt on the validity of the lognormal assumption in the data.

5 Disaster Risk and SDF Volatility

Section 3.1 demonstrated that the physical and risk-neutral distributions locally differ most in the left-tail. In this section, I show that these local differences imply that the SDF must be highly volatile; an observation that is closely related to the Hansen and Jagannathan (1991) bound. Furthermore, I use this insight to argue that the left-tail of the physical distribution cannot be too predictable, which clarifies the low explanatory power in Table 2.

5.1 A Bound on the SDF Volatility

For ease of notation, I define , which can be interpreted as the ordinal dominance curve of the measures and (Hsieh and Turnbull, 1996). Furthermore, let

which is the space of all nonnegative conditional SDFs. The volatility bound on the SDF can now be stated as follows.

Proposition 5.1 (Distribution bound).

Assume no-arbitrage, then for any , we have

| (5.1) |

If a risk-free asset exists, then and (5.1) simplifies to

The bound can be further rewritten in terms of the conditional CDFs only

| (5.2) |

Proof.

See Appendix A.4. ∎

If , agents are risk-neutral and the dominance curve evaluates to . In that case the distribution bound degenerates to zero. Proposition 5.1 makes precise the sense in which any local difference between the physical and risk-neutral distribution leads to a volatile SDF. Compare this to the classical Hansen and Jagannathan (1991) (HJ) bound:

| (5.3) |

The lower bound in (5.3) shows that any excess return leads to a volatile SDF. Essentially, (5.3) uses three sources of information:

(i) the mean of the physical distribution

(ii) the mean of the risk-neutral distribution

(iii) the variance of the physical distribution.

The lower bound in (5.3) is also a global measure of distance between and , since the mean and volatility are averages across the whole distribution.

In contrast, the bound in (5.2) compares the physical and risk-neutral distribution at every point , which is a local measure of distance between and . To clarify this local interpretation, consider the following decomposition of the equity premium

| (5.4) |

where the first equation follows since the SDF prices the market return (2.1), and the second equation is a consequence of Hoeffding’s identity (see Lemma A.5.). Equation (5.1) shows that locally measures the dependence between the SDF and market return. In other words, it quantifies how the SDF’s variability relates to the market return’s variability at different quantiles.

To explain the equity premium and disaster risk premia, the SDF must exhibit sufficient variability. Since the distribution bound can be derived from applying the Cauchy-Schwarz inequality to , it is expected to yield sharper bounds on the SDF volatility than the HJ bound if, for example, there is high tail dependence between the SDF and market return such as in the disaster risk model.171717See McNeil et al. (2015, Chapter 7.2.4) for a formal definition of tail dependence.

5.2 Quantile Predictability in the Left-Tail

The bound presented in Proposition 5.1 sheds light on the seemingly “low” explanatory power observed in the left-tail quantile regressions in Table 2. For tractability, it is more convenient to show this for CDFs instead of quantile functions, but the intuition remains the same. Specifically, suppose one could predict at some in the left-tail, then this prediction can be exploited by going short in an asset that pays . The profit and risk associated to this investment are, respectively

| (5.5) | |||

Although such binary state payoffs do not exist in reality, they can be replicated closely by a portfolio of put options. In consequence, high predictability of in the left-tail would render too good a Sharpe ratio; a near-arbitrage opportunity. Following the reasoning in Ross (2005, Chapter 5), a crude upper bound on the SDF volatility imposes limitations on the degree of predictability in the left-tail by the distribution bound in Proposition 5.1. This argument breaks down in the right-tail since (5.5) is roughly zero, and high predictability would not imply counterfactually high SDF volatility.

5.3 Distribution Bound in Asset Pricing Models

The estimated Gini coefficients in Section 3.1 demonstrate that conditional disaster risk is a pervasive feature of the data. This section complements those findings using the unconditional version of the distribution bound in Proposition 5.1:

| (5.6) |

where represents the unconditional SDF volatility, and . In this context, denotes the unconditional physical CDF, and is the unconditional risk-neutral quantile function of the market return. The main benefit of using unconditional distributions is that they can be estimated without estimating the risk-neutral quantile regressions. Moreover, the bound in (5.6) only requires the estimation of distribution functions, whereas existing approaches typically use unconditional density functions to emphasize disaster risk (see, e.g. Beason and Schreindorfer (2022)).

The subsequent examples demonstrate that the HJ bound is always stronger than the distribution bound in models that do not embed a source of disaster risk. In contrast, models that incorporate disaster risk can generate distribution bounds that exceed the HJ bound in the left-tail. Since I use unconditional distributions, the time subscripts will be omitted from the notation.

Example 5.1 (CAPM).

The Capital Asset Pricing Model (CAPM) specifies the SDF as

where denotes the return on the market portfolio. In this case , since the SDF can become negative. However, this probability is very small over short time horizons or we can think of as an approximation to . Since the HJ bound is derived by applying the Cauchy-Schwarz inequality to , the inequality binds if is a linear combination of . Hence, under CAPM, the HJ bound is strictly stronger than the distribution bound regardless of the distribution of .

Example 5.2 (Joint normality).

Suppose that and are jointly normally distributed and denote the mean and variance of by and respectively. The normality assumption violates no-arbitrage since can be negative, but could be defended as an approximation over short time horizons when the variance is small (see Example 5.3). In Appendix A.5, I prove that

| (5.7) |

where is the marginal density of .181818Notice that this is the marginal density under physical measure . This identity gives an explicit expression for the weighting factor in Hoeffding’s identity (5.1). In Appendix A.5, I also derive an explicit expression for the relative efficiency between the distribution and HJ bound

| (5.8) |

To see that the HJ bound is always stronger than the distribution bound, minimize (5.8) with respect to . Appendix A.6 shows that the minimizer satisfies . For this choice, and . Therefore, (5.8) can be bounded by

Hence, the HJ bound is always stronger in a model where the SDF and return are jointly normal.

Example 5.3 (Joint lognormality).

Let and be standard normal random variables with correlation and consider the specification

where governs the time scale. Simple algebra shows that the no-arbitrage condition, , is satisfied when . It is difficult to find an analytical solution for the relative efficiency between the HJ and distribution bound in this case, but linearization leads to a closed form expression which is quite accurate in simulations. The details are described in Appendix A.7, where I show that

| (5.9) |

This expression is independent of . An application of l’Hôspital’s rule reveals that the relative efficiency converges to if .191919This is the same relative efficiency in Example 5.2, which is unsurprising as the linearization becomes exact in the limit as . The ratio in (5.9) is less than 1 if and . Since the annualized market return volatility is about 16%, the HJ bound is stronger than the distribution bound under any reasonable parameterization if the SDF and market return are lognormal.

Example 5.4 (continues=ex:disaster_risk_jumps).

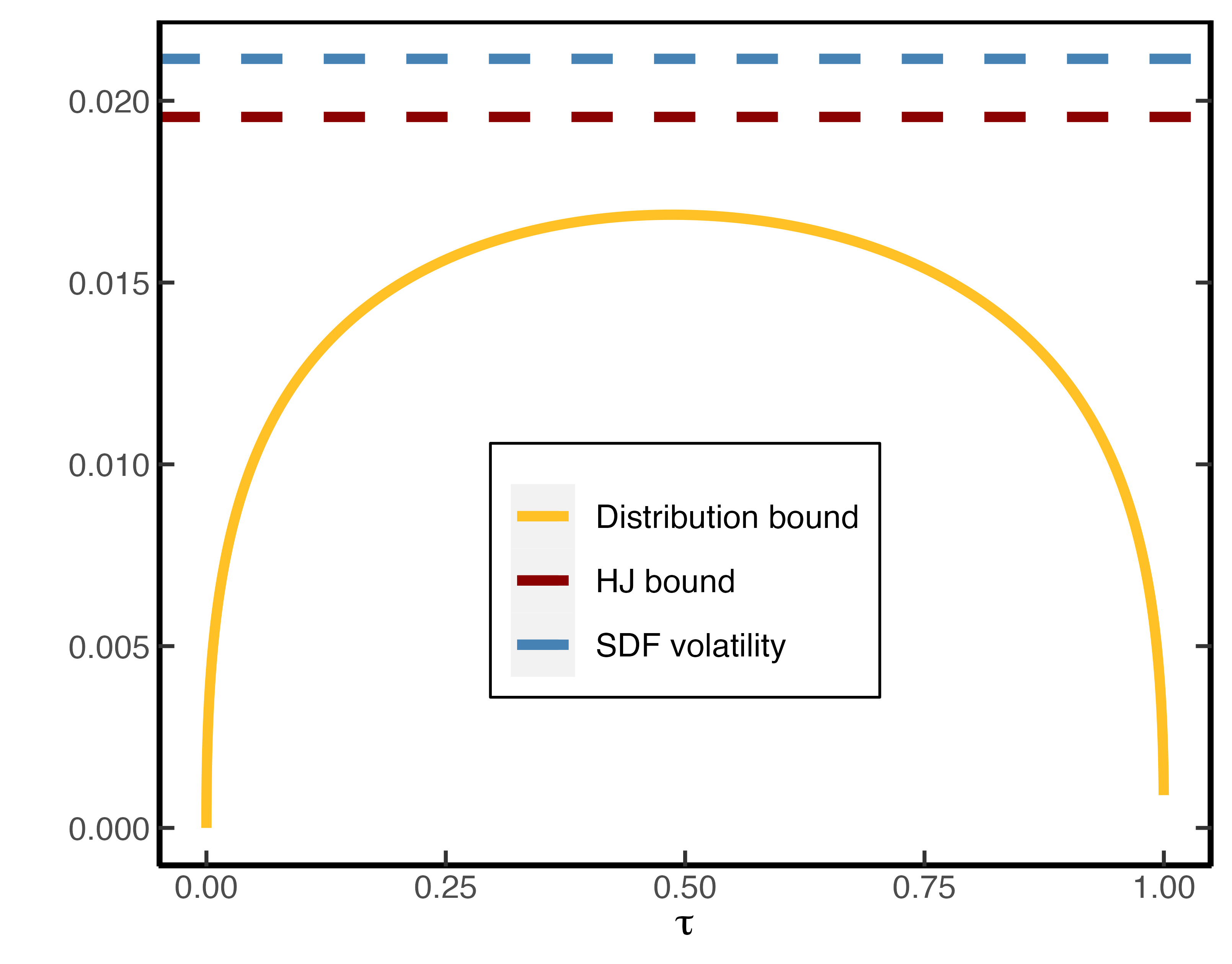

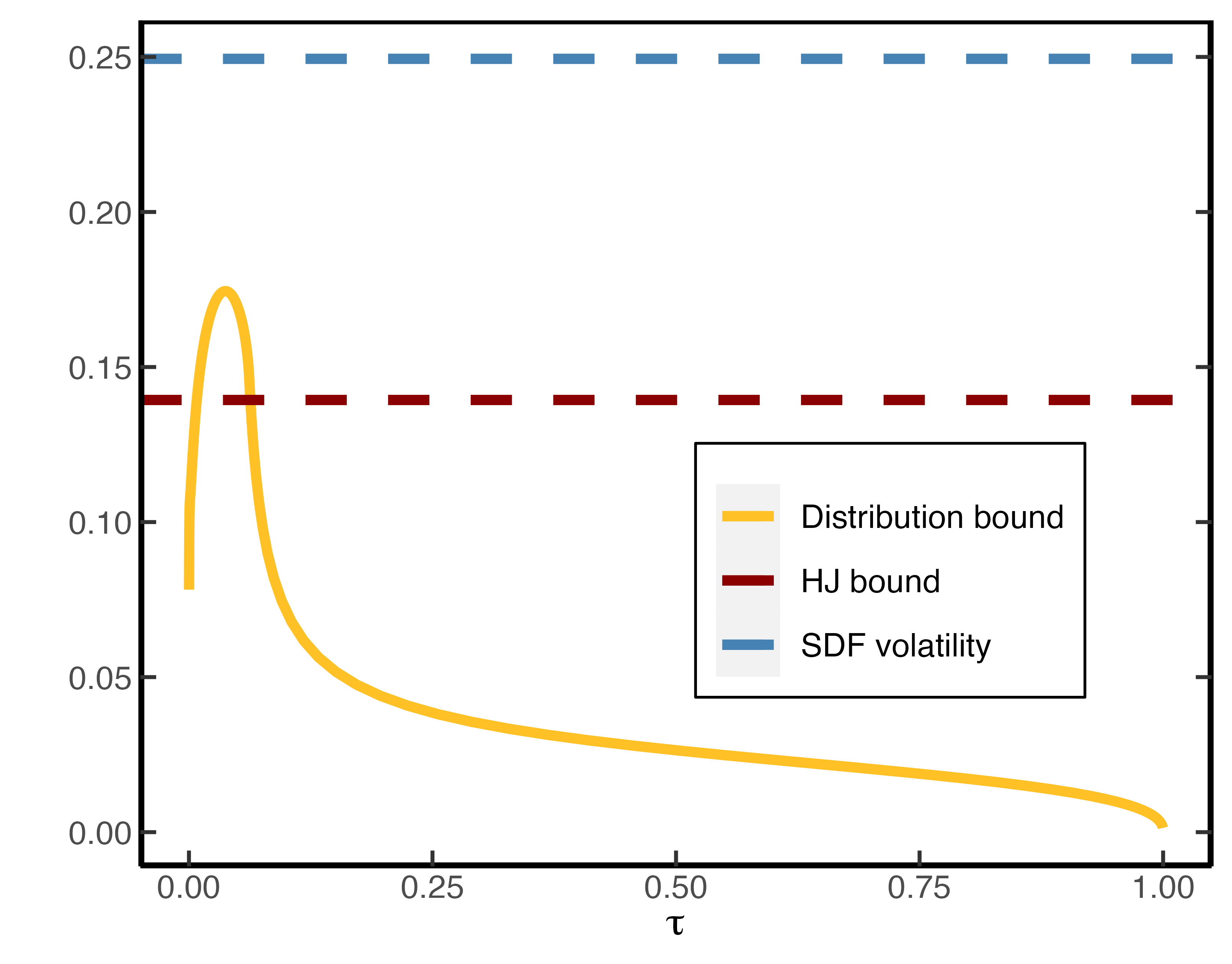

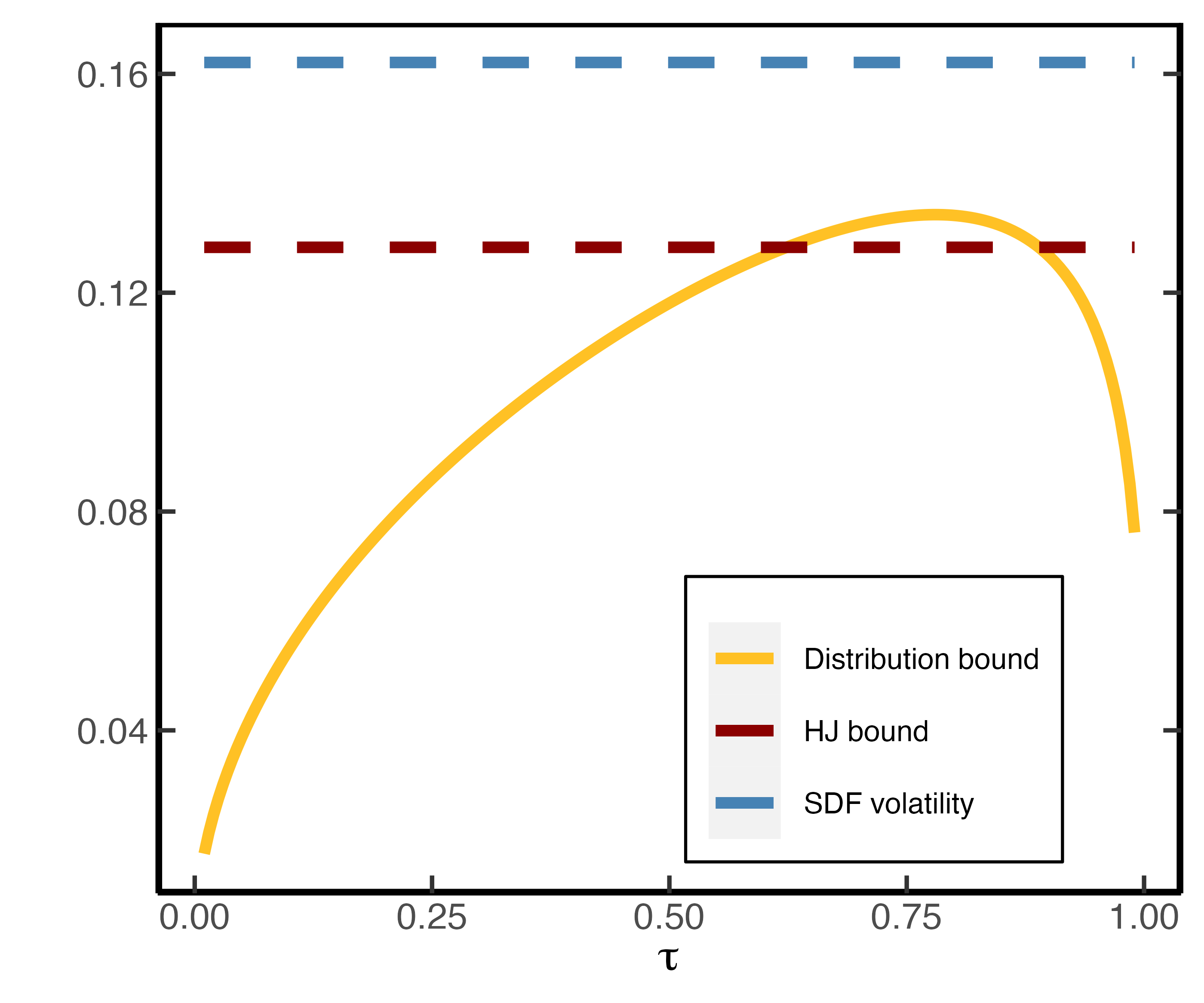

The disaster risk model discussed in Section 2.1 is calibrated according to the results in Backus et al. (2011, Table \@slowromancapii@). The market return in this model is considered as a levered claim on consumption growth, i.e. an asset that pays dividends proportional to . Here governs the variability of the claim to equity. I convert the model implied volatility bounds to monthly units, to facilitate the comparison with the empirical bounds obtained in Section 5.5.

The distribution bound, HJ bound and SDF volatility are depicted in Panels 6(a) (without jumps) and 6(b) (with jumps). Consistent with Example 5.3, the distribution bound in the model without jumps never exceeds the HJ bound because both the market return and SDF follow lognormal distributions. The distribution bound with jumps has a sharp peak at , after which it steadily decreases. Interestingly, there is a range of values for which the distribution bound is stronger than the HJ bound.202020In Appendix A.8, I show that the distribution bound can also exceed the HJ bound when returns follow the Pareto distribution. This result can be understood from the physical and risk-neutral quantile functions in Figure 1(b). The risk-neutral quantile function displays a heavy left-tail, owing to the implied disaster risk embedded in the SDF. Consequently, it is extremely profitable to sell digital put options which pay out in case of a disaster. These put options must have high Sharpe ratios as their prices are high (insurance against disaster risk), but the actual probability of a disaster event occurring is low enough that the risk associated with selling such insurance is limited.

5.4 Data and Empirical Estimation of the Distribution Bound

To further illustrate the presence of disaster risk in the data, I estimate the distribution bound (5.1) empirically, using the same 30-day S&P500 returns as discussed in Section 2.3. However, in this case, I use non-overlapping returns that cover the period 1996–2021.212121I use non-overlapping returns in this section to facilitate testing and to make the results comparable to other nonparametric bounds, which are typically estimated based on non-overlapping returns (see e.g. Liu (2021)). These returns are sampled at the middle of each month, resulting in a total of 312 observations. Over this period, the Sharpe ratio is 13%, and the HJ bound therefore implies that the monthly SDF is quite volatile.

The distribution bound consists of three unknowns that need to be estimated: (i) the physical distribution ; (ii) the risk-neutral quantile function , and; (iii) the risk-free rate (). To estimate the unconditional risk-free rate, denoted by , I rely on the historical average of monthly interest rates. Next, to obtain an estimate of the physical distribution, I employ a kernel (CDF) estimator, given by:

| (5.10) |

where is the Epanechnikov kernel and is the bandwidth determined by cross-validation. This choice of estimator ensures that the distribution bound is a smooth function of , which reduces the impact of outliers relative to the discontinuous empirical CDF.

Finally, I apply the procedure outlined in Section 2.3 to estimate (the conditional risk-neutral CDF). Subsequently, I average the conditional distributions to estimate the unconditional CDF:

Under appropriate assumptions about the distribution of returns, converges to as . An estimate of the unconditional risk-neutral quantile function can then obtained from

| (5.11) |

Finally, based on the physical CDF (5.10) and risk-neutral quantile function (5.11), I estimate the distribution bound by

| (5.12) |

where is the estimated ordinal dominance curve and is a small positive number.

5.5 Unconditional Evidence of Disaster Risk

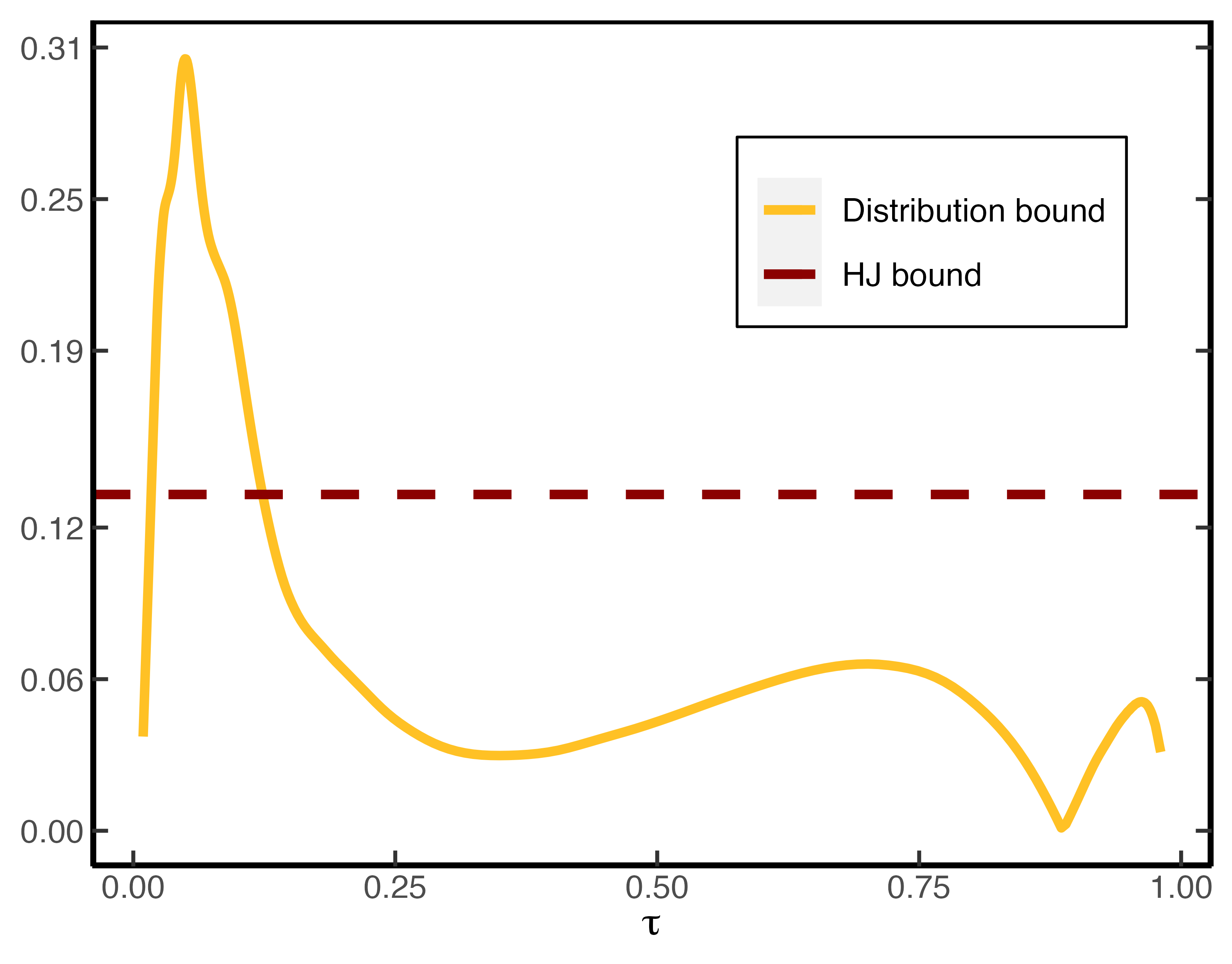

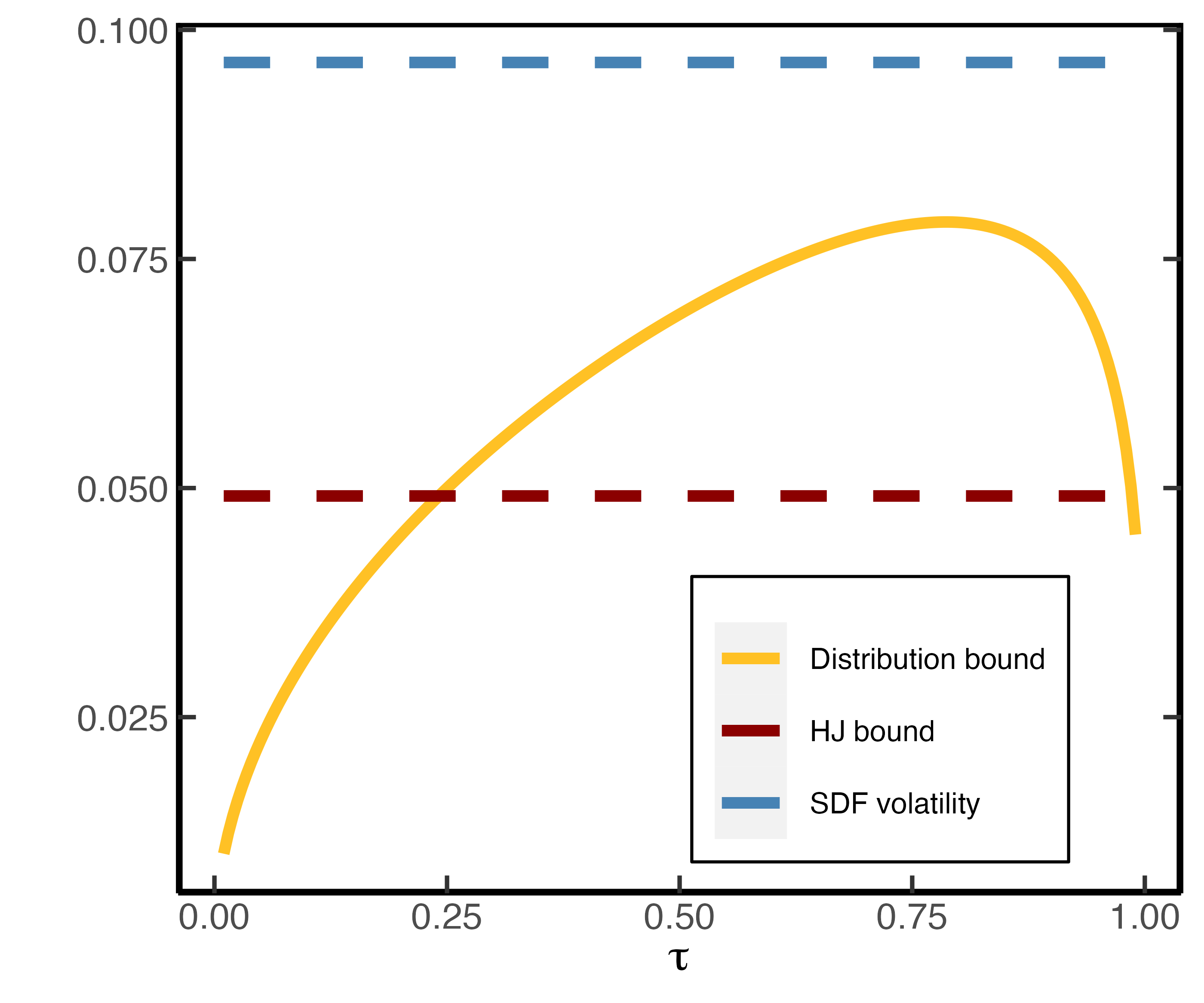

Figure 7(a) illustrates the estimated physical and risk-neutral measures, which differ most in the left-tail. The distribution bound shows that this difference leads to a volatile SDF, which is shown in Figure 7(b). The lower bound on the SDF volatility implied by the distribution bound is much stronger than the HJ bound in the left-tail. This finding aligns with empirical evidence documenting that high Sharpe ratios can be attained by selling out-of-the money put options (see Broadie et al. (2009) and the references therein). The supremum of the distribution bound occurs around the 5th percentile, implying that the monthly SDF volatility must exceed 31%. This value is more than twice the level indicated by the sample HJ bound. Moreover, the shape of the distribution bound is quite similar to the distribution bound implied by the disaster risk model in Figure 6(b).222222The non-monotonicity in the right-tail of the distribution bound occurs because , for large enough. That is, the physical distribution does not first-order stochastically dominates the risk-neutral distribution. This result is consistent with the negative estimates in Table 2.

The graphical evidence suggests that the distribution bound renders a stronger bound on the SDF volatility than the HJ bound. To test this hypothesis more formally, I fix a priori the probability level at 0.037 (), which renders the sharpest bound on the SDF volatility in the disaster risk model (Example 5.4). At this probability level, the distribution bound is 26% in the data, which is roughly double the level implied by the HJ bound.

To see whether this difference is statistically significant, I consider the following test statistic

| (5.13) |

The first term on the right denotes the estimated distribution bound (5.12) evaluated at the 3.7th percentile, using the entire time series of returns . The second term denotes the estimated HJ bound, using and as the respective sample mean and standard deviation of {}. A value of indicates that the distribution bound is stronger than the HJ bound. To test this restriction, consider the null and alternative hypothesis:

| (5.14) | ||||

Since the distribution of (5.13) is difficult to characterize, I use stationary bootstrap to approximate the -value under the null hypothesis. The stationary bootstrap is used to generate time indices from which we recreate (with replacement) bootstrapped returns (Politis and Romano, 1994). The same bootstrapped time indices are used to re-estimate the physical CDF and risk-neutral quantile function. I repeat the bootstrap exercise 100,000 times and for each bootstrap sample, I calculate the test statistic . Finally, the empirical -value is obtained as the fraction of times . The last column in Table 4 shows that the -value is 7.5%, which provides preliminary evidence that the distribution bound significantly exceeds the HJ bound.

Sample size HJ bound distribution bound -value 312 0.133 0.260 0.075 • Note: This table reports the HJ and distribution bound for monthly S&P500 returns over the period 1996–2021. The distribution bound is evaluated at . The final column denotes the -value of the null hypothesis in (5.14). The -value is obtained from 100,000 bootstrap samples and counts the fraction of times that .

Remark 3.

When the HJ bound is stronger than the distribution bound, many of the bootstrap samples may not include disaster shocks. Over the entire sample period, there are only two instances where returns were less than -20%: in September 2008 and February 2020. When considering bootstrap samples that include both of these months, the -value is only 3.6%. In contrast, the -value increases to 22% for bootstrap samples that exclude these months. These findings underscore the sensitivity of the test to the presence of disaster shocks. Overall, the results suggest that, unconditionally, the SDF needs to be highly volatile to be consistent with local differences between the physical and risk-neutral measure in the left-tail.

6 A Model-Free Lower Bound on Disaster Risk Premia

The previous findings indicate that the risk-neutral quantile function is not a good approximation of the physical quantile function in the left-tail. In this section, I derive a lower bound on disaster risk premia observed from option prices. This lower bound does not require parameter estimation and relaxes the assumption of a time-homogeneous linear relation between the physical and risk-neutral quantiles in (2.3).

6.1 Approximating the Quantile Difference

To analyze the difference between and , I use some elementary tools from functional analysis. The quantile function can be regarded as a map between normed spaces, taking as input a distribution function and returning the quantile function: . Expanding around the observed risk-neutral CDF yields

| (6.1) |

where is a norm on a suitable linear space232323Formally, the space can be defined as and is the space of distribution functions (Serfling, 2009). See van der Vaart (2000, Section 20.1) and Serfling (2009, p. 217) for further details about the approximation. and is the Gâteaux derivative of at in the direction of :

| (6.2) |

Heuristically, the Gâteaux derivative can be thought of as measuring the change in the quantile function when the risk-neutral distribution is moved in the direction of the physical distribution. Appendix A.9 shows that the Gâteaux derivative is given by

| (6.3) |

where denotes the conditional ordinal dominance curve (ODC). I proceed under the working hypothesis that the remainder term in (6.1) is “small” in the sup-norm, .

Assumption 6.1.

The remainder term in (6.1) can be neglected.

Remark 4.

The assumption implies that the first order approximation in (6.1) is accurate. The condition that is small can be understood as excluding near-arbitrage opportunities, since the distribution bound in Proposition 5.1 shows that substantial pointwise differences between and lead to a very volatile SDF. Appendix E.3 illustrates the approximation in the Black and Scholes (1973) model.

I combine (6.1) and (6.3) in conjunction with Assumption 6.1 to obtain the approximation

| (6.4) |

The second term on the right can be thought of as a risk-adjustment term to capture the unobserved wedge between and . The approximation in (6.4) contains the terms and , which are directly observed at time using the Breeden and Litzenberger (1978) formula in (2.7). However, is unknown and hence (6.4) cannot be used directly to approximate .

6.2 A Lower Bound on Disaster Risk Premia

To make further progress, I show that the numerator term, , can be lower bounded with option data under economically motivated constraints. This bound, combined with the approximation in (6.4), will then imply a lower bound on disaster risk premia.

I start from the observation that the SDF in representative agent models can be expressed as a function of the market return (Chabi-Yo and Loudis, 2020):

| (6.5) |

where is the agent’s wealth at time and represents the agent’s utility function. Define

| (6.6) |

Notice that is simply the inverse of the intertemporal marginal rate of substitution (IMRS) and are the coefficients of the its Taylor expansion around . I make the following assumptions about the market return and the IMRS of the representative agent.

Assumption 6.2.

In the representative agent model, it holds that (i) ; and (ii) .

Assumption 6.2(i) allows for fat tails in the risk-neutral distribution as long as the third moment exists. This assumption relaxes the implicit assumption made by Chabi-Yo and Loudis (2020) that infinitely many moments exist. Figure G9 in the Appendix illustrates that the risk-neutral distribution frequently exhibits a finite number of moments, some of which may not exceed 4, particularly in turbulent market conditions. Chabi-Yo and Loudis (2020) present sufficient conditions for 6.2(ii) to hold, which relate to the sign of the fifth derivative of the utility function of the representative agent. Specifically, for common utility functions such as CRRA or HARA utility, parameter restrictions are needed to ensure that 6.2(ii) holds.242424For example, for CRRA utility, the risk-aversion coefficient cannot be too large. See Appendix C for a detailed discussion.

I need one additional assumption to bound disaster risk premia. To state this assumption and the resulting lower bound, I use the following notation for high-order risk-neutral moments and truncated high-order risk-neutral moments, respectively.

| (6.7) |

Assumption 6.3.

In the representative agent model, the following holds:

-

(i)

for

-

(ii)

.

Chabi-Yo and Loudis (2020, Table 6) provide empirical evidence that 6.3(i) holds with equality when estimating the conditional equity premium. Assumption 6.3(ii) is a very mild restriction on risk-neutral skewness, which is almost always negative at every date and time horizon. This empirical fact is well known.252525Chabi-Yo and Loudis (2020) argue that all odd risk-neutral moments should be negative, since they expose the investor to unfavorable market conditions.

The following two propositions show how option data can be employed to establish bounds on the difference between the physical and risk-neutral measures in the left-tail.

Proposition 6.4 (Lower Bound on CDF).

Proof.

See Appendix A.10. ∎

Proposition 6.5 (Lower Bound on Disaster Risk Premia).

Proof.

Proposition 6.4 provides a bound on the physical CDF that requires no parameter estimation and relies solely on time information. This result complements recent work on belief recovery. Ross (2015) demonstrated CDF recovery under the assumption of transition independence, but subsequent research has questioned this assumption (Borovička et al., 2016; Qin et al., 2018; Jackwerth and Menner, 2020). In contrast, Proposition 6.4 establishes a lower bound on the left-tail of the physical distribution using a different set of mild economic constraints. Additionally, Section 2.3 showed that the right-tail of can be approximately recovered from the risk-neutral distribution due to the minimal need for risk-adjustment. These findings suggest the potential for approximate recovery of using option prices.

I will test this hypothesis using the lower bound on disaster risk premia in Proposition 6.5. Specifically, a tight lower bound in (6.9) would enable direct inference on both the physical distribution () and disaster risk premia (). While Section 2.2.1 proposed the quantile model (2.3) to estimate , it can be criticized for having time-homogeneous coefficients. Proposition 6.5 relaxes that assumption. Furthermore, the lower bound in (6.9) is not prone to the historical sample bias critique of Welch and Goyal (2008). Alternatively, one can estimate a disaster risk model to infer , but this approach is also susceptible to misspecification concerns and faces challenges in estimation due to the scarcity of disaster events in the data (Julliard and Ghosh, 2012; Martin, 2013).

6.3 Calculating the Lower Bound

Before assessing how tight the lower bound is in Proposition 6.5, I outline the procedure to calculate it, which depends on and . Both functions can be derived from , which is estimated using the same data and procedure of Section 2.3. To see that can be derived from , notice that . The latter term can thus be approximated by262626I slightly abuse notation to emphasize that the derivative is taken w.r.t. , so that denotes .

where is the bandwidth of the -grid. Second, to calculate in (6.8), I use , as well as the formula for high-order risk-neutral moments in Appendix A.11.

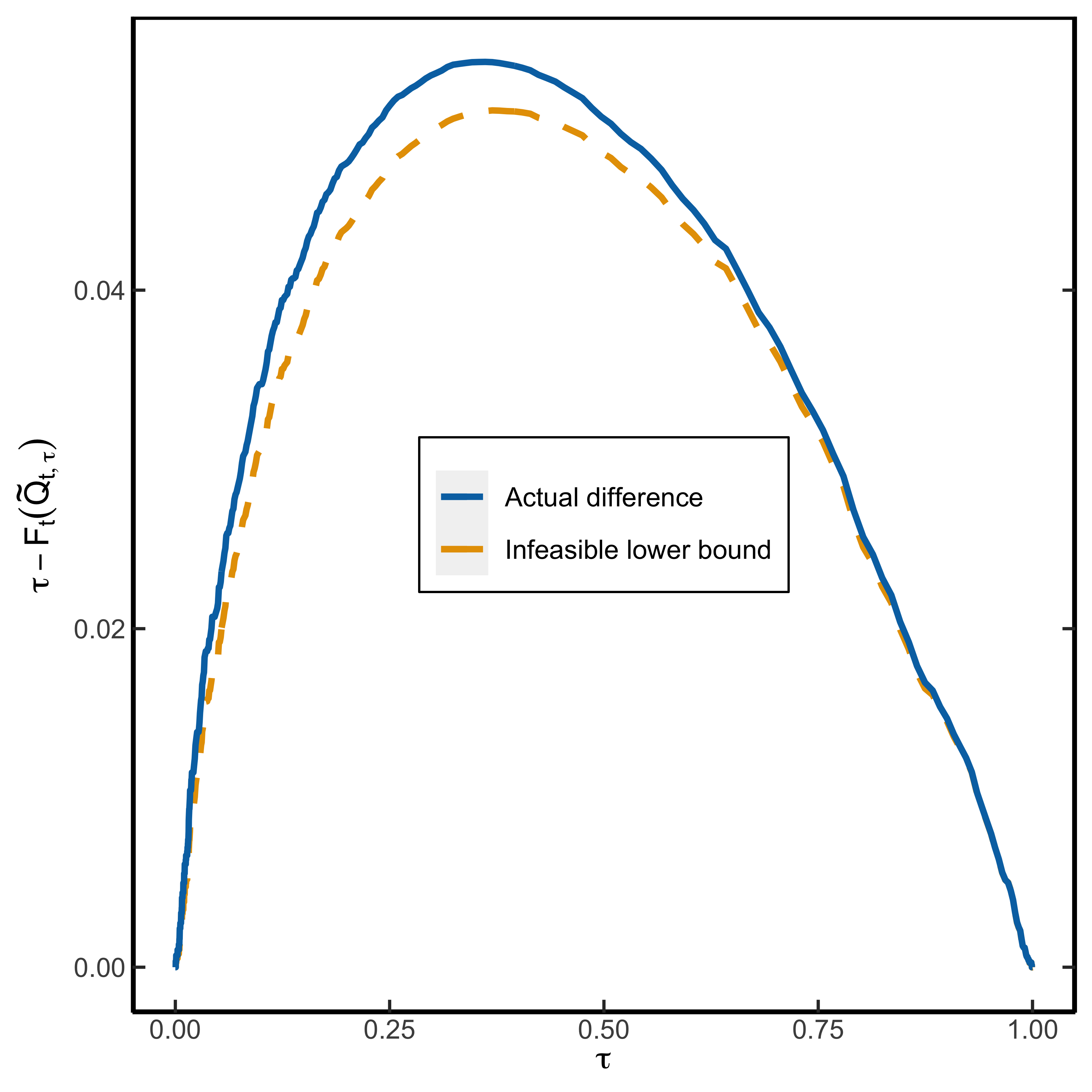

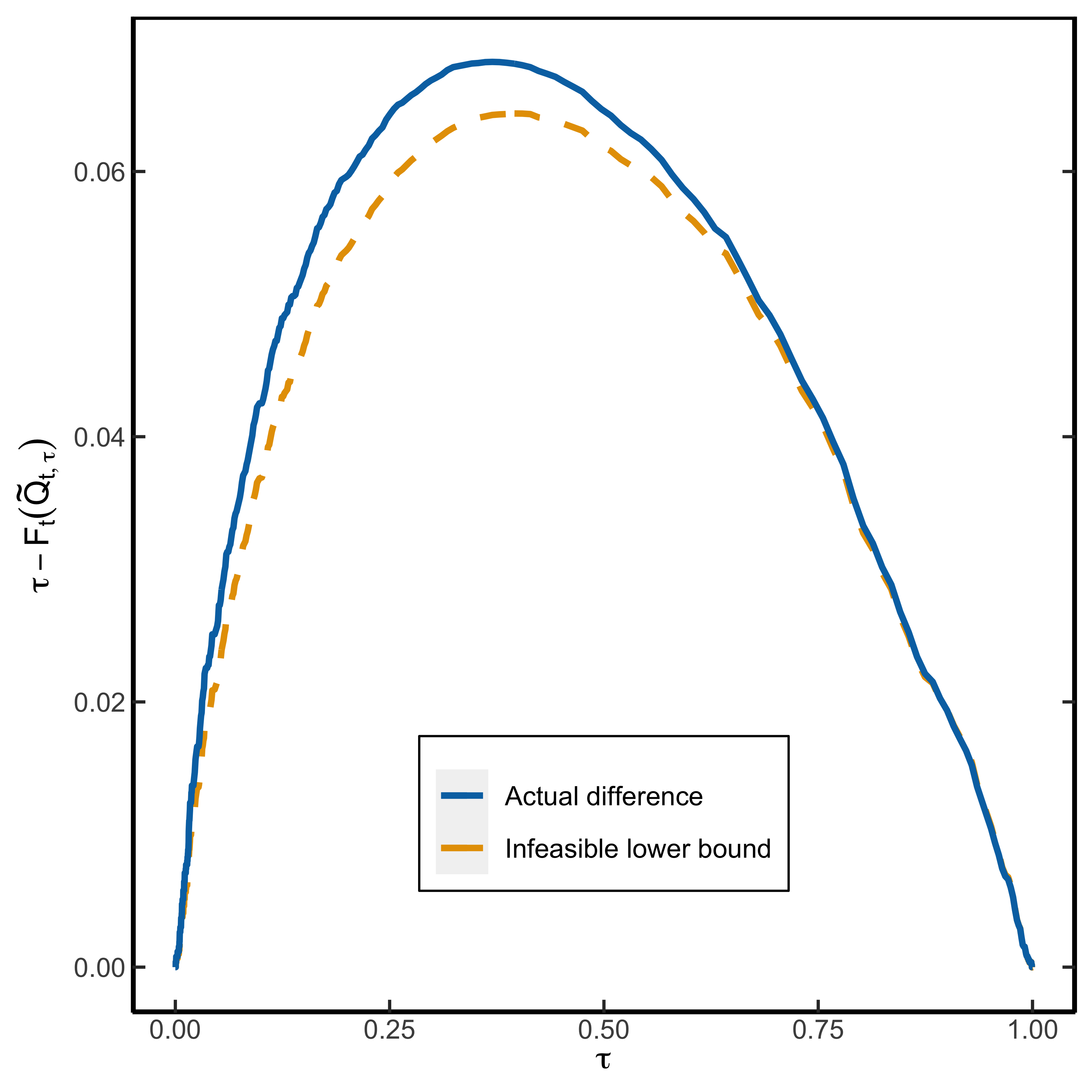

Given the evidence in Table 2 that in the left-tail, Proposition 6.5 has nontrivial content in the data if . Appendix Table E1 contains summary statistics of , which show that the lower bound is always positive, right-skewed, more pronounced in the right-tail and economically meaningful in magnitude, with outliers that can spike up to 29%.

6.4 Tightness of the Lower Bound: In-sample Evidence

To test whether the lower bound in Proposition 6.5 is tight, I form excess quantile returns: . Since is observed at time , it follows that . Subsequently, I use QR to estimate the model

| (6.10) |

Regression (6.4) is a quantile analogue of the mean excess return regressions of Welch and Goyal (2008). Under the null hypothesis that the lower bound is tight, it holds that

| (6.11) |

Less restrictive, one can test whether and , which implies that the statistical “factor” explains the conditional quantile wedge.272727For example, if we start with a quantile factor model , the model has one testable implication for the data: the intercept in a quantile regression of on should be zero. Quantile factor models have recently been proposed by Chen et al. (2021).

Table 5 presents the results of regression (6.4). The null hypothesis of a tight lower bound in (6.11) is not rejected for , but it is rejected for across all horizons. When the null hypothesis is rejected, the -coefficient exceeds 1, consistent with the theory that represents a lower bound on disaster risk premia. In all cases, the lower bound is economically meaningful, since is significantly different from 0, while can never be rejected. However, the explanatory power of the regression in Table 5 is modest, as shown by the measure-of-fit:

| (6.12) |

But, following the reasoning of Section 5.2, the predictive power in the left-tail cannot be too big, for otherwise near-arbitrage opportunities exist.