Abstract

We study wealth rank correlations in a simple model of macroeconomy. To quantify rank correlations between wealth rankings at different times, we use Kendall’s and Spearman’s , Goodman–Kruskal’s , and the lists’ overlap ratio. We show that the dynamics of wealth flow and the speed of reshuffling in the ranking list depend on parameters of the model controlling the wealth exchange rate and the wealth growth volatility. As an example of the rheology of wealth in real data, we analyze the lists of the richest people in Poland, Germany, the USA and the world.

keywords:

Bouchaud–Mézard model; rank correlations; Gini coefficient; wealth distribution; wealth inequality1 \issuenum1 \articlenumber0 \externaleditorAcademic Editor: Firstname Lastname \datereceived \dateaccepted \datepublished \hreflinkhttps://doi.org/ \TitleWealth rheology \AuthorZdzislaw Burda 1,†\orcidA, Malgorzata J. Krawczyk 1,†\orcidB, Krzysztof Malarz 1,∗,†\orcidC, and Malgorzata Snarska 2,†\orcidD \AuthorNamesZdzislaw Burda, Malgorzata J. Krawczyk, Krzysztof Malarz and Malgorzata Snarska \corresCorrespondence: malarz@agh.edu.pl \firstnoteThese authors contributed equally to this work.

1 Introduction

The problem of wealth inequality is the subject of intense research in economics Davis and Shorrocks (2000); Benhabib and Bisin (2016); Nardi (2015); Berman et al. (2016a, b), sociology and econophysics Chakrabarti et al. (2013), but it also arouses great interest outside of science Hardoon (2017); WIR ; Piketty (2014, 2015); Wpr ; Spi ; For . Parallel to empirical studies, theoretical research is carried out to explain the main features of wealth statistics and wealth dynamics observed in macroeconomic data, like the presence of Pareto tails in wealth distribution or increasing wealth inequality in the world.

In theoretical models, wealth dynamics is often described by stochastic equations representing the evolution of wealth of a typical individual in a given economic environment. In physical terminology, this can be called the one-body approach. Even today this approach is used in mainstream economics, for example, in studies of wealth inequality Piketty and Saez (2012). An alternative is to use population dynamics, which in this context is often referred to as agent-based modelling. It was introduced in Angle (1986) and popularised in Samanidou et al. (2007). In agent-based modelling, the economy is perceived as a complex system consisting of many entities interacting with each other under given macroeconomic conditions. Unlike the one-body approach, this can be called the multi-body approach. The main idea of agent-based modelling is to statistically look at the problem of wealth distribution from the perspective of the entire system. This allows studying collective effects, like correlations between agents, or emergent phenomena, such as the formation of wealth classes, or self-organisation of the economy, or instability of the system. This perspective is in many aspects similar to that used in statistical physics, aiming at deriving macroscopic physical laws from microscopic rules by applying laws of large numbers. This is probably why the problem of wealth distribution has been intensively studied in econophysical literature Chakrabarti et al. (2013). Many ideas behind agent-based modelling have been derived from concepts like kinetic theory Dragulescu and Yakovenko (2000); Yakovenko and Rosser (2009), scattering Slanina (2004), rate equations Ispolatov et al. (1998), random matrix theory Burda et al. (2003); Bouchaud and Potters (2015), Brownian motion Van Kampen (2007) which were developed in statistical physics. Using this type of ideas, one was able to model wealth or income distributions Bouchaud and Mézard (2000), dynamics of wealth inequality Adamou and Peters (2016); Burda et al. (2019), wealth concentration Cieśla and Snarska (2020), structure emergence Waśko and Kułakowski (2006); Karpińska et al. (2004), economic instability and corruption mechanisms Burda et al. (2002); Ball (2002); Malarz and Kułakowski (2016), systemic risk in economic networks Diem et al. (2020), emergence of heavy tails in wealth and income distributions Levy and Solomon (1996); Bouchaud and Mézard (2000), and herding behaviour Cont and Bouchaud (2000), or to analyse statistical behaviour or rational agents Venkatasubramanian et al. (2015).

Since the time of Keynes, it has been widely believed that a closed economy eventually reaches a stationary state, also known as a steady state or saturation. What is usually meant as a stationary state economy is a system where macroeconomic quantities have stationary distributions. A typical example is the wealth distribution that does not change over time after reaching a steady state. This does not mean that each person’s wealth is constant in time, but that the system as a whole has a stationary distribution in a statistical sense. In fact, the wealth of individuals may change all the time even in the stationary state. Wealth flows from one individual to another: some people get richer, some poorer, panta rhei. In this article, we will take a closer look at the flow of wealth. We call this class of phenomena wealth rheology. To be specific, in the paper we study the dynamics of wealth rank correlations using the Bouchaud–Mézard model of macroeconomy Bouchaud and Mézard (2000). The model is implemented as a stochastic process based on Gibrat’s law of proportionate growth Gibrat (1931) which is combined with dynamics representing agents’ interactions. The model generates Pareto’s tail in the wealth distribution Pareto (1897). The stochastic process belongs to the class of Kesten processes Kesten (1973), which is a class of multiplicative contracting stochastic processes. It is a generic feature of Kesten processes that they lead to a stationary state with a power-law tail.

2 The model

In this section we briefly recall the Bouchaud–Mézard model Bouchaud and Mézard (2000). The model describes evolution of wealth of interacting agents in a closed macroeconomic system. The evolution is given by stochastic differential equations for wealth of agents at time . In the continuous time formalism the equations read

| (1) |

where , are independent Wiener processes (continuous Brownian motions). The above equations are written in the Itô formalism111In the Stratonovich approach the term would be replaced with .. In this paper we shall use the discrete time formalism. Equation (1) can be discretised by introducing an elementary time interval relating physical time to discrete time as follows . In the leading order, up to -terms, the discretisation of Equation (1) gives

| (2) |

where , and are independent identically distributed random variables with the normal distribution with and . In the limit , Equation (1) is restored. The first term on the right hand side of Equation (2) corresponds to random multiplicative fluctuations of wealth. In economic literature it is referred to as the law of proportionate effect Gibrat (1931) stating that growth rates are independent of wealth. In the simplest version of the model it is assumed that the growth rates have the same mean and the same variance for all agents throughout evolution of the system. The first term on the right hand side of Equation (2) reflects spontaneous changes in wealth due to changing market conditions and expectations. The second one describes the flow of wealth between individuals, resulting from interactions and trading. Coefficient is the fraction of wealth of agent which is transferred to agent within a single time interval . Equations (2) are invariant under rescaling of wealth by a common factor for all . In particular, this means that the equations do not change when the monetary units change. Therefore, it is convenient to express wealth in units of the mean wealth . We denote the corresponding quantities by small letters

| (3) |

The normalised wealth values (3) are insensitive to the parameter controlling the mean growth rate, because it cancels in the numerator and the denominator of Equation (3). The change can be interpreted as a change of the inflation rate by .

The model can be solved in the mean-field approximation assuming that all agents interact with each other with the same intensity for all pairs . For , in the limit and , the normalised wealth (3) can be shown to approach a stationary state with the distribution given by the inverse gamma distribution with the following probability density function Bouchaud and Mézard (2000):

| (4) |

where the parameter is

| (5) |

One can easily check that the mean of this distribution is equal to one, that is in accordance with the normalisation (3). The distribution has a Pareto tail for with the exponent , given by Equation (5). The index depends on the ratio of the flow intensity parameter and the volatility of growth rates , so the stationary distribution does not change when and are simultaneously re-scaled by the same factor and . The parameters and can be interpreted as economic activity parameters. The flow parameter reflects the intensity of trade and wealth exchange. The parameter is the growth rate volatility and it reflects the degree of economic freedom: the larger the more liberal economy. Large values of mean that the state does not intervene and does not help if economic entities need support. On the contrary it supports and encourages a free market, new ideas, bold businesses and the foundation of start-ups, etc. In effect, some companies may quickly grow, while some large established companies can shrink or go bankrupt quickly. For a large , large changes in the wealth of individuals are expected. In such circumstances, the economic landscape is changing rapidly. On the other hand, small values of mean that the economy is very conservative, that is, the system discourages risky investments and the state intervenes when established companies need help, the system supports economic status quo and the economy is more predictable in the short term.

The aim of this paper is to compare the wealth dynamics in steady state for systems having the same stationary distribution (4), but different economic activity parameters and . To get an insight into wealth flow dynamics in the steady state, we study temporal evolution of wealth rank correlations and quantify them by measuring Kendall’s Kendall (1938) and Spearman’s Spearman (1904) for wealth distributions separated by steps of evolution (2). Standard definitions of rank correlations are recalled in Appendix A.

3 Monte Carlo simulations

We perform Monte Carlo simulations to generate evolution of the system. In practice we find it more convenient to use a slightly modified version of the evolution equations (2), where a single step of evolution is split into two

| (6) |

with some intermediate values . The first equation in (6) corresponds to Gibrat’s rule of proportionate growth, while the second one to wealth’s flow which preserves the total wealth in the system . One can easily show that the two representations of the evolution (2), (6) are identical up to -order so they have the same continuous time limit (1) for . Here, for the sake of simplicity, we focus on the mean field system where each agent interacts with all the others with the same intensity . In this case, Equations (6) simplify to

| (7) |

The flow rate can be interpreted as the average fraction of wealth that can flow from an agent to others over a period of time .

We simulated systems up to agents, but the results presented in this paper are for . We used two types of initial configurations:

-

•

a complete equality configuration where for all ;

-

•

an equilibrium configuration, where are drawn independently of each other from the inverse gamma distribution (4).

We call them ‘cold’ and ‘hot’ starts, respectively.

4 Results

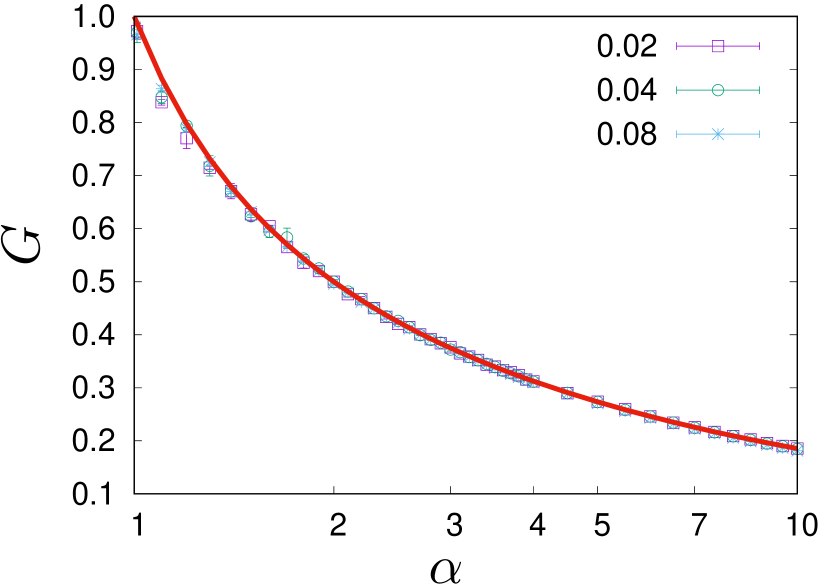

In Figure 1(a) we compare a theoretical prediction for the Gini coefficient with the values obtained in Monte Carlo simulations of the system with and . The theoretical prediction for the distribution (4) reads Burda et al. (2019)

| (8) |

where is the hypergeometric function Arfken et al. (2013). One can see in Figure 1(a) that the experimental and theoretical values are consistent. This means that the evolution equations (7) bring the system to the predicted steady state. In fact, there are some slight deviations from the theoretical prediction which can be attributed to the fact that the theoretical results are derived in the continuous time formalism, while the Monte Carlo simulations are done for discrete time. The deviations grow with the volatility .

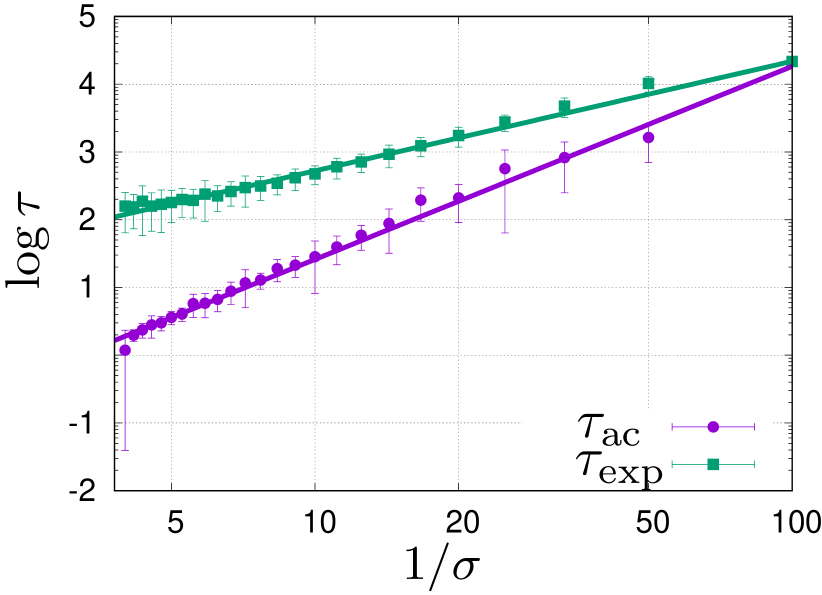

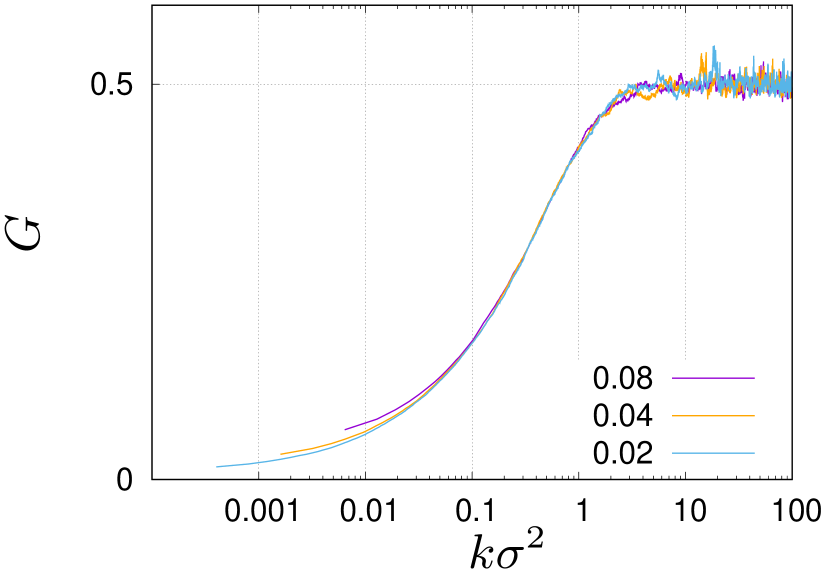

The main conclusion from the comparison shown in Figure 1(a) is that the stationary state in the first-order approximation depends on the combination and not on itself, exactly as predicted by the theoretical formula (8). Let us now address the question how the dynamic properties of evolution depend on . First, we will study the rate of relaxation towards the steady state by measuring the exponential auto-correlation time Madras and Sokal (1988) for the Gini coefficient. Roughly speaking the exponential time corresponds to the time needed for the system to reach the stationary state. To measure we initiate the system from a uniform wealth distribution (cold start), for which the Gini coefficient is , and wait till the Gini coefficient of the current configuration exceeds the steady state value for the first time. In Figure 1(b) we show the mean exponential auto-correlation time as a function of for and averaged over a sample of values obtained from independent simulations. We see that grows as decreases. This effect is clearly seen in Figure 1(c) which shows examples of the evolution of the Gini coefficient for , from cold starts for , and . In all three cases the Gini coefficient evolves from the initial value towards the stationary state value (5) which is equal to for . The values of during the evolution are plotted against in Figure 1(c). The variable on the horizontal axis is proportional to physical time , for given in Equation (1), because . The curves in Figure 1(c) correspond to different time intervals used in the discretization of Equation (1). The small variations between the curves, seen in Figure 1(c) for small , can be attributed to the higher-order corrections in that occur in the discretization of Equation (1), skipped in Equation (2). Generally, we can expect that in the presented range of the evolution is universally described by the parameter , that we shall use from here on.

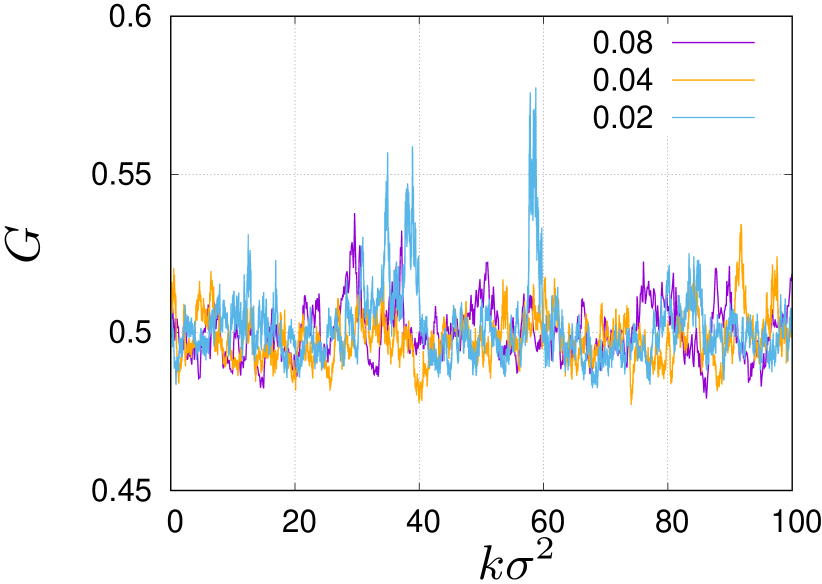

Once the stationary state is reached, the value of the Gini coefficient fluctuates about the steady state value. This is illustrated in Figure 1(d) where we show evolution of the Gini coefficient in systems initiated from hot starts, that correspond to the stationary wealth distribution given by Equation (4). The Gini coefficient fluctuates about the stationary value but the way it fluctuates about this value slightly depends on the volatility . The reason for this is related to the presence of a heavy tail in the limiting distribution (4), which for , leads to an infinite variance. In effect, the curves representing the evolution in Figure 1(d) exhibit strong fluctuations which depart from mean value. For the simulations shown in the figure, the length of evolution measured in the discrete time steps, , is sixteen and four times longer for and , respectively, than for . Therefore, we observe more fluctuations and larger deviations for and than for . To quantify the degree of correlation between the values of the Gini coefficient at different times, we measure the integrated auto-correlation time Madras and Sokal (1988) which gives a typical timescale for the length of temporal fluctuations. Coming back to Figure 1(b) we show there the dependence of the integrated auto-correlation time on for the system with and . It can be compared in the figure to the relaxation time that we previously discussed. As you can see, both and grow when decreases. The straight lines in Figure 1(b) are to guide the eye. They are determined as the best power-law fits: , where and , where .

As mentioned in the introduction, we are mainly interested in the dynamic aspects of the evolution of wealth distribution, such as wealth flow and wealth ranking reshuffling. We are now going to analyse the wealth rank correlations for different systems having the same stationary state, by studying systems with different ’s and ’s but identical ’s (5).

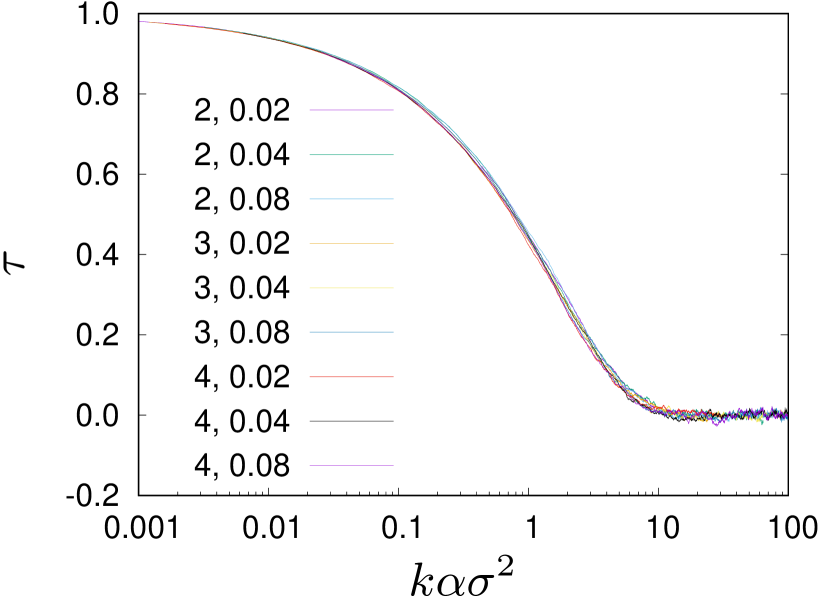

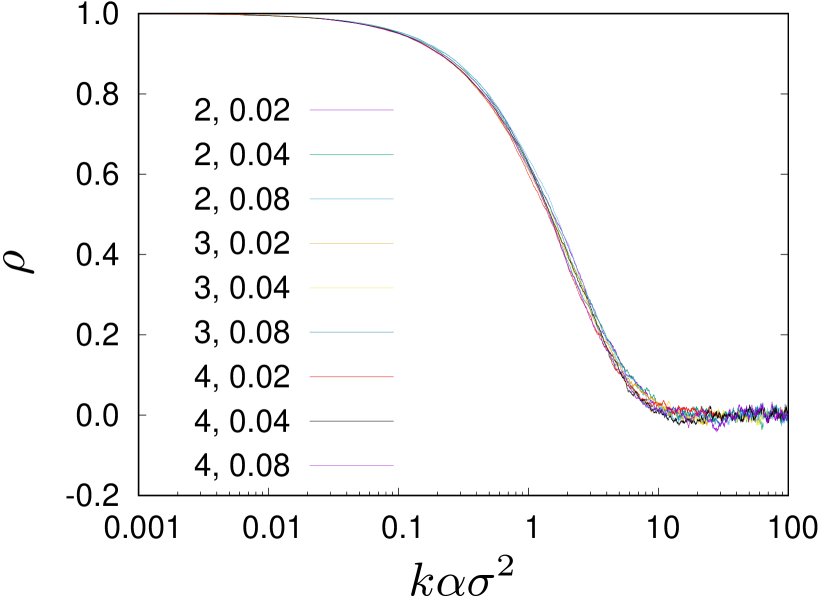

Wealth rank is a position on the ranking list ordered from the richest to the poorest individuals. The wealth ranking is continuously reshuffling, even in the stationary state. The rate of reshuffling depends on and : the larger and the faster is the reshuffling. Changes in wealth ranking are faster when is larger. In Figure 2 we show rank correlations between wealth ranking lists obtained in the Monte Carlo simulations of the Bouchaud–Mézard model Bouchaud and Mézard (2000), for configurations separated by steps of evolution (7), in the stationary state of the system with , and , and , and , and . The degree of rank correlations is quantified by Kendall’s Kendall (1938) and Spearman’s Spearman (1904) (see Appendix A). In Figure 2 we plot and against a rescaled variable . We can see that the curves lie on top of each other, reflecting some universality of the wealth rheology in the model (1).

Another quantity which captures rank correlations is the overlap ratio which is defined as the percentage of people which are among richest people at times and . For example, you may be interested in how many people from the top-100 richest list in some year, are in the top-100 richest list one or two years later. If denotes the set of people being in the top- richest list in the ranking at time and at time , the overlap ratio is:

| (9) |

where the symbol denotes sets’ intersection, and — set’s cardinality. If the dynamics describing the wealth evolution is Markovian, then the overlap ratio depends on the time difference . In such a case, the overlap ratio can be estimated numerically as follows

| (10) |

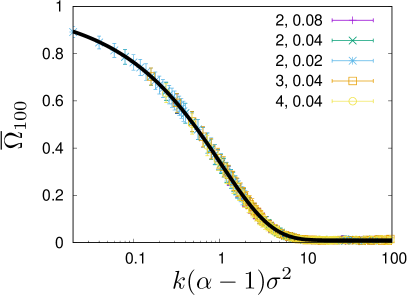

where is the discrete time, which refers to consecutive configurations (rankings), and is the number of configurations in the sample. In Figure 3 we show the expected overlap for the top-100 richest list, estimated from the steady state configurations in Monte Carlo simulations for three values of (4) and for three values of , for . We see that all curves collapse to a single universal curve. By listing explicitly all arguments of the overlap ratio , we see that the overlap ratio becomes a universal function of the argument :

| (11) |

The function interpolates monotonically between for and for . A simple phenomenological formula

| (12) |

gives a very good fit to the data (see Figure 3). Notice that the scaling variable is not the same as the scaling variable for and .

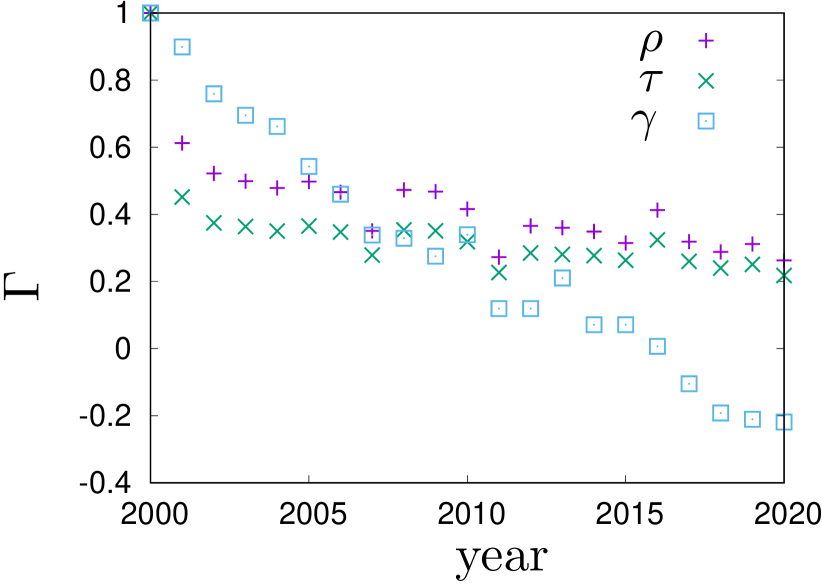

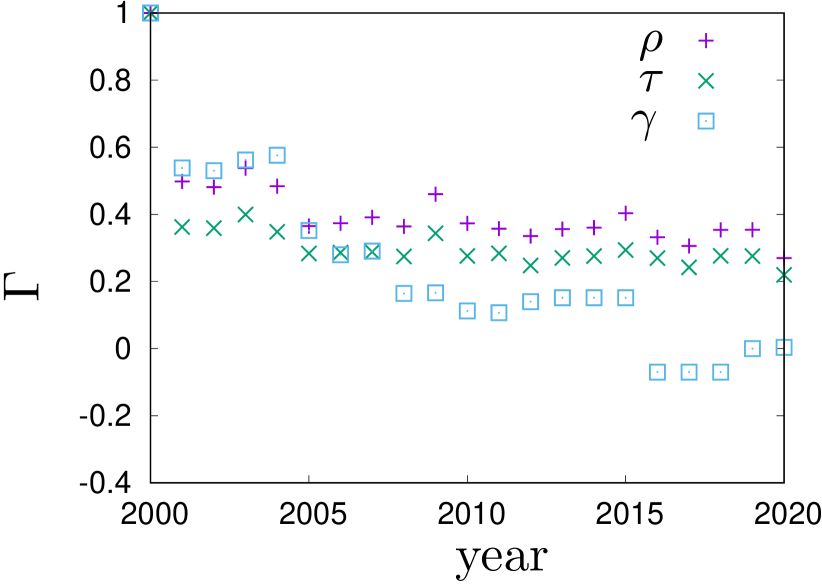

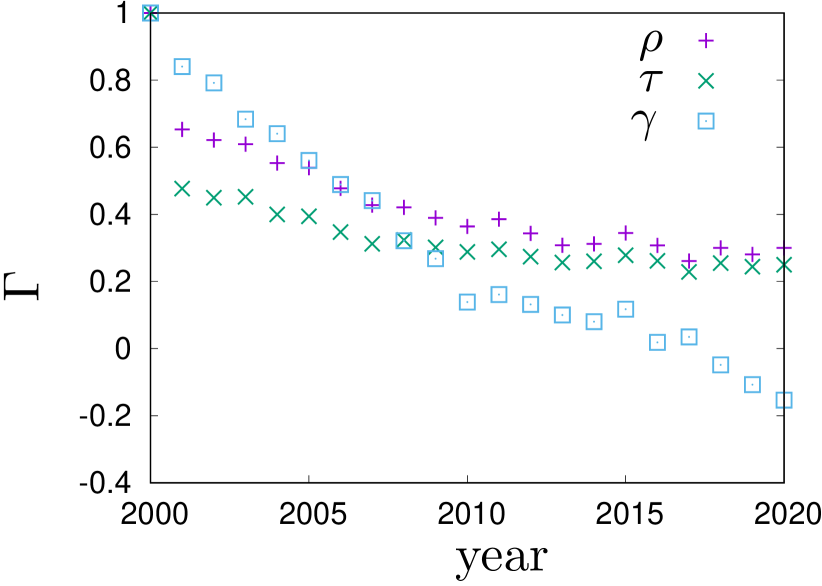

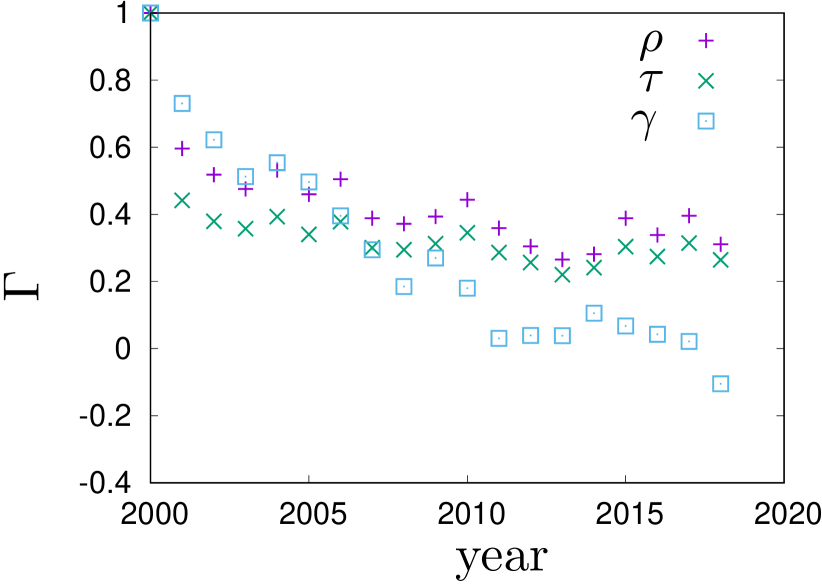

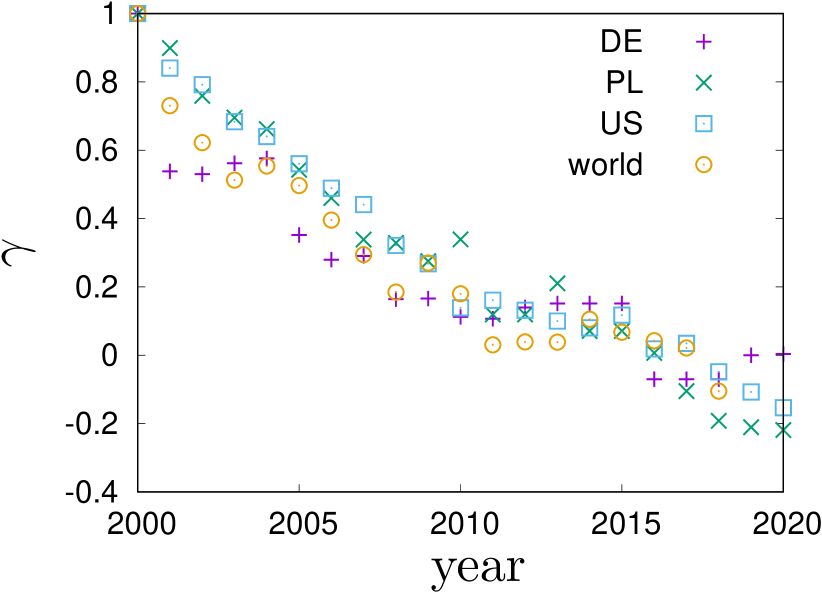

In the remainder of this section we will investigate the rheology of wealth in real world systems. People’s wealth data is very sensitive, so it is almost impossible to collect it. Therefore we restrict ourselves to data on the richest people that is publicly available. To be specific, we focus on the top-100 lists of richest people in Poland, Germany, the USA and the world Wpr ; Spi ; For . The top-100 richest lists are a small part of the whole picture but it is the part that usually gets the most attention. Data that we analyse covers the period 2000–2020 for Poland Wpr , Germany Spi and the USA For , and the period 2000–2018 for the world For . We are going to determine the rank correlation coefficients (14), (16), and (17) between the top-100 richest lists in years and . The sets of people present in the top-100 richest lists vary from year to year: there are people who are in the top-100 richest list in some years but not in others. To compare the lists we must first standardize them so that they include the same set of people every year. To do so, we determine a full set of people who have been present on the top-100 list at least once in the studied period. The full set is then used to complete the annual top-100 lists in the following way: if a person from the full set is not in the top-100 richest list for a given year, s/he is added to this list with a unique random rank in the range between and the number of people in the full set. In the analysed period, the full sets contain people in Poland, in Germany, in the USA and in the world. For each system, all standardized lists are of the same size and contain the same people every year. The standardized lists are used as input to calculations of and . The results are shown in Figure 4. In the figure you can also see the results for Goodman–Kruskal’s (17) computations. To compute we used a slightly different algorithm to complement the annual lists. The algorithm assigns the same ex aequo rank to all people added as a complement, to the list. By design, the coefficient omits ex aequo ranks, thus minimizing the statistical bias coming from the artificial completion of lists. Analysing the plots in Figure 4 we see for example, that the values of drop between and much less than the corresponding values of and . The big drop of and is related to the large number of additional rank pairs, created by the complement algorithm. The number of pairs is less in the complement algorithm for . When the sets of elements vary from year to year, the Goodman–Kruskal’s coefficient better captures rank correlations of the original ranking lists. Therefore, we find it more reliable to use to compare rank correlations for lists of different lengths.

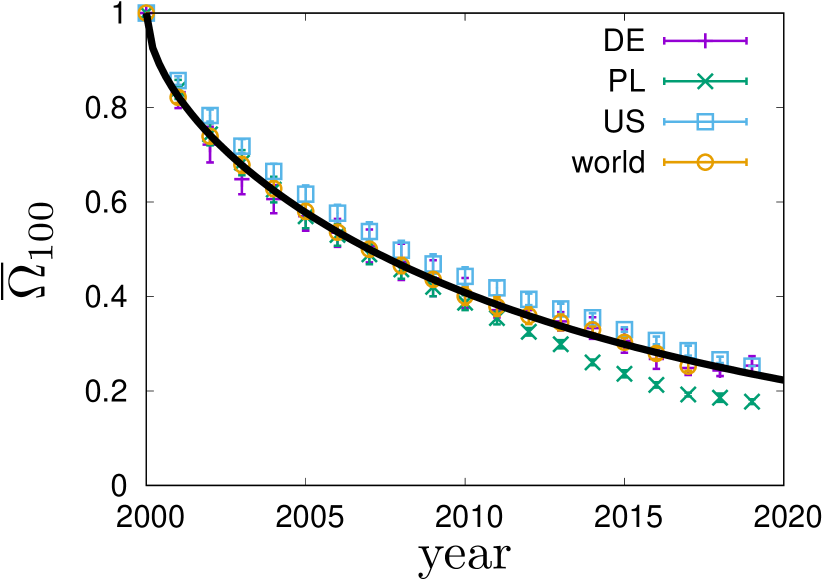

In Figure 5(a), values of the overlap ratio of the annual top-100 richest lists in Poland, Germany, the US and the world are compared. The overlap ratios exhibit a fairly universal behaviour that is well described by the phenomenological formula (12). The best fit to the top-100 richest people in the world is shown with a solid line in Figure 5(a). It fits the data very well. We can see that in the four systems the overlap ratio drops to after years. In Figure 5(b), values of the Goodman–Kruskal’s rank correlation coefficient for the four systems are compared. We can see that the rank correlations fall off from one to zero roughly within years. The rate of decay for is quite similar in all the studied systems. For Germany the dependence of on time exhibits an interesting pattern. The values of stay roughly constant for a couple of years, then significantly drop and again stay roughly constant for a couple of years. This motif repeats a couple of times, forming a stairway shape.

5 Conclusions

Steady-state macroeconomic systems are characterized by no statistical changes in the distribution of wealth and macroeconomic parameters. This does not mean that there are no changes in the system. On the contrary, in the microscale the system undergoes continuous dynamical changes. As far as the wealth distribution is concerned, the internal dynamics can be observed as a continuous process which manifests as reshuffling of wealth ranks of people on the wealth ranking lists: some people get richer, some get poorer. In this paper we have studied the dynamical properties of macroeconomic systems related to the flow of wealth, and wealth rheology. We used the Bouchaud–Mézard model and the agent-based modelling approach to simulate the evolution of wealth in a closed macroeconomy. An interesting property of the Bouchaud–Mézard model is that it generates steady states with a Pareto tail in the wealth distribution, and that different combinations of economic activity parameters may lead to the same limiting wealth distribution. This allowed us to investigate the dependence of wealth rank correlations on the wealth activity parameters for various scenarios but the same wealth distribution. We have seen that the wealth rank correlations depend mainly on the growth rate volatility. The smaller the volatility, the larger the correlations. The rank correlations are closely related to auto-correlations in the system. We have also studied rank correlations on the top-100 richest lists in Poland, Germany, the US and the world using the Goodman–Kruskal’s and the lists overlap ratio . We have observed that the rank correlations in the studied systems exhibit a certain degree of universality, for example, the overlap ratio gets reduced by half within and the Goodman–Kruskal’s decreases to zero within two decades. We have focused on the top-100 richest lists because they are easily available. It would be interesting to perform a similar analysis for top- lists for larger and for longer periods, years, in the future to get a full picture on wealth rank dynamics.

There are also some theoretical questions—regarding the scaling and universality of results—that are extremely interesting. We have seen that the correlation coefficients and depend on a universal variable while the overlap ratio on . The question is if this scaling is the general feature of the Kesten processes? To solve this problem we have considered an alternative implementation of Kesten dynamics, where the wealth of agents is generated as exponents of independent random walks , on the positive semi-axis with the drift towards the reflective wall located at . Such a stochastic process is probably the simplest implementation of the Kesten process. It leads to a stationary state with a power law in the probability density function of wealth distribution for , with the exponent , where are the drift and the volatility of the underlying random walk. The rank statistics of ’s and ’s are the same because the map is monotonic. The Kesten dynamics is thus mapped onto the dynamics of a gas of particles performing independent random walks on the positive semiaxis. The gas of particles is much easier to analyse. For instance, one can give a simple argument that the overlap ratio for this system depends on the combination , so the scaling is different than for the model discussed in this paper. Thus, the scaling is not universal. It would be interesting to find an analytical way to calculate the rank correlation measures in the models discussed in this paper. For the gas of random walkers on the semi-positive axis one can maybe use the spectral methods Karlin and McGregor (1959).

All authors have contributed equally to this work. They have read and agreed to the published version of the manuscript.

MS has been partially supported by the Ministry of Education and Science within the “Regional Initiative of Excellence” Program for 2019–2022.

Acknowledgements.

We thank the anonymous reviewer who drew our attention to the scaling of dynamics in the model. \conflictsofinterestThe authors declare no conflict of interest. \appendixtitlesyes \appendixstartAppendix A Rank correlations

Consider a set of elements, each being characterised by two real quantities , , . For example one can think of the weight and height of pupils in a class. The elements (pupils) can be ranked with respect to the property (weight) and (height). For sake of simplicity assume that all values , are distinct, so that the elements can be unambiguously ranked with respect to , and assume that the same holds for . Denote the corresponding ranks by ’s and ’s. To quantify correlations between the ranks one can introduce a rank score function to define a rank correlation coefficient associated with this score function

| (13) |

The score function is a monotonic odd function . The standard choices of the rank score function are the sign function or the identity function . In the former case the corresponding rank correlation coefficient is usually called Kendall’s . It is calculated as follows:

| (14) |

where and are the numbers of concordant and discordant pairs. A pair is concordant if the elements and are ranked in the same order for and . Otherwise, the pair is discordant. For the identity function the rank correlation coefficient is usually called Spearman’s

| (15) |

Using elementary algebraic operations one can find that

| (16) |

This formula is particularly useful in practice since instead of a double sum it involves only a single sum. The computational complexity to determine increases linearly with in contrast to the complexity to compute (14) which increases quadratically with .

We conclude this Appendix by mentioning that there are rank correlation measures that apply also for the case when there are ex aequo ranks in the sample. In the example given above, you can think of two or more pupils having the same weight or height within a given accuracy. In this case, one can replace Kendall’s by Goodman–Kruskal’s Goodman and Kruskal (1954)

| (17) |

Clearly, if there are no ex aequo ranks in the sample then is equivalent to (14).

References

References

- (1)

- Davis and Shorrocks (2000) Davis, J.B.; Shorrocks, A.E., The distribution of wealth. In Handbook of Income Distribution; Atkinson, A.B.; Bourguignon, F., Eds.; Elsevier, 2000.

- Benhabib and Bisin (2016) Benhabib, J.; Bisin, A. Skewed wealth distributions: Theory and empirics. Working Paper 21924, National Bureau of Economic Research, 2016. doi:10.3386/w21924.

- Nardi (2015) Nardi, M.D. Models of wealth inequality: A survey. http://www.nber.org/papers/w21106, accessed on Feb. 26, 2021.

- Berman et al. (2016a) Berman, Y.; Peters, O.; Adamou, A. Far from equilibrium: Wealth reallocation in the United States, 2016, arXiv:1605.05631 [q-fin.EC].

- Berman et al. (2016b) Berman, Y.; Ben-Jacob, E.; Shapira, Y. The dynamics of wealth inequality and the effect of income distribution. PLoS One 2016, 11, 1–19. doi:10.1371/journal.pone.0154196.

- Chakrabarti et al. (2013) Chakrabarti, B.K.; Chakraborti, A.; Chakravarty, S.R.; Chatterjee, A., Income and wealth distribution data for different countries. In Econophysics of Income and Wealth Distributions; Cambridge University Press, 2013; p. 7–34. doi:10.1017/CBO9781139004169.003.

- Hardoon (2017) Hardoon, D. An economy for the 99%. https://www.oxfam.org/en/research/economy-99, accessed on Feb 26, 2021.

- (9) https://wir2018.wid.world/, accessed on Feb 26, 2021.

- Piketty (2014) Piketty, T. Capital in the Twenty-First Century; Harvard University Press, 2014.

- Piketty (2015) Piketty, T. About ‘Capital in the Twenty-First Century’. American Economic Review 2015, 105, 48–53. doi:10.1257/aer.p20151060.

- (12) Top 100 richest people in Poland. https://rankingi.wprost.pl/100-najbogatszych-polakow/2020, accessed on Feb 23, 2021. Wprost.

- (13) Die 500 reichsten Deutschen. https://www.manager-magazin.de, accessed on Apr 20, 2021. Manager Magazin (Spiegel Group).

- (14) The richest people in the world. https://www.forbes.com/billionaires/, accessed on Apr 20, 2021. Forbes.

- Piketty and Saez (2012) Piketty, T.; Saez, E. A theory of optimal capital taxation. Working Paper 17989, National Bureau of Economic Research, 2012. doi:10.3386/w17989.

- Angle (1986) Angle, J. The surplus theory of social stratification and the size distribution of personal wealth. Social Forces 1986, 65, 293–326. doi:10.2307/2578675.

- Samanidou et al. (2007) Samanidou, E.; Zschischang, E.; Stauffer, D.; Lux, T. Agent-based models of financial markets. Reports on Progress in Physics 2007, 70, 409–450. doi:10.1088/0034-4885/70/3/r03.

- Dragulescu and Yakovenko (2000) Dragulescu, A.; Yakovenko, V.M. Statistical mechanics of money. The European Physical Journal B - Condensed Matter and Complex Systems 2000, 17, 723–729. doi:10.1007/s100510070114.

- Yakovenko and Rosser (2009) Yakovenko, V.M.; Rosser, J.B. Colloquium: Statistical mechanics of money, wealth, and income. Reviews of Modern Physics 2009, 81, 1703–1725. doi:10.1103/RevModPhys.81.1703.

- Slanina (2004) Slanina, F. Inelastically scattering particles and wealth distribution in an open economy. Physical Review E 2004, 69, 046102. doi:10.1103/PhysRevE.69.046102.

- Ispolatov et al. (1998) Ispolatov, S.; Krapivsky, P.; Redner, S. Wealth distributions in asset exchange models. The European Physical Journal B - Condensed Matter and Complex Systems 1998, 2, 267–276. doi:10.1007/s100510050249.

- Burda et al. (2003) Burda, Z.; Jurkiewicz, J.; Nowak, M.A. Is econophysics a solid science? Acta Physica Polonica B 2003, 34, 87–131.

- Bouchaud and Potters (2015) Bouchaud, J.P.; Potters, M., Financial applications of random matrix theory: A short review. In The Oxford Handbook of Random Matrix Theory; Akemann, G.; Baik, J.; Di Francesco, P., Eds.; Oxford University Press, 2015. doi:10.1093/oxfordhb/9780198744191.013.40.

- Van Kampen (2007) Van Kampen, N.G. Stochastic Processes in Physics and Chemistry, 3 ed.; Elsevier, 2007.

- Bouchaud and Mézard (2000) Bouchaud, J.P.; Mézard, M. Wealth condensation in a simple model of economy. Physica A: Statistical Mechanics and its Applications 2000, 282, 536–545. doi:10.1016/S0378-4371(00)00205-3.

- Adamou and Peters (2016) Adamou, A.; Peters, O. Dynamics of inequality. Significance 2016, 13, 32–35. doi:10.1111/j.1740-9713.2016.00918.x.

- Burda et al. (2019) Burda, Z.; Wojcieszak, P.; Zuchniak, K. Dynamics of wealth inequality. Comptes Rendus Physique 2019, 20, 349–363. doi:10.1016/j.crhy.2019.05.011.

- Cieśla and Snarska (2020) Cieśla, M.; Snarska, M. A simple mechanism causing wealth concentration. Entropy 2020, 22, 1148. doi:10.3390/e22101148.

- Waśko and Kułakowski (2006) Waśko, M.; Kułakowski, K. Efficiency of pair formation in a model society. Acta Physica Polonica B 2006, 37, 3171–3176.

- Karpińska et al. (2004) Karpińska, J.; Malarz, K.; Kułakowski, K. How pairs of partners emerge in an initially fully connected society. International Journal of Modern Physics C 2004, 15, 1227–1233. doi:10.1142/S0129183104006686.

- Burda et al. (2002) Burda, Z.; Johnston, D.; Jurkiewicz, J.; Kamiński, M.; Nowak, M.A.; Papp, G.; Zahed, I. Wealth condensation in Pareto macroeconomies. Physical Review E 2002, 65, 026102. doi:10.1103/PhysRevE.65.026102.

- Ball (2002) Ball, P. Wealth spawns corruption. Physicists are explaining how politics can create the super-rich. Nature 2002. doi:10.1038/news020121-14.

- Malarz and Kułakowski (2016) Malarz, K.; Kułakowski, K. Game of collusions. Physica A: Statistical Mechanics and its Applications 2016, 457, 377–390. doi:10.1016/j.physa.2016.03.068.

- Diem et al. (2020) Diem, C.; Pichler, A.; Thurner, S. What is the minimal systemic risk in financial exposure networks? Journal of Economic Dynamics and Control 2020, 116, 103900. doi:10.1016/j.jedc.2020.103900.

- Levy and Solomon (1996) Levy, M.; Solomon, S. Power laws are logarithmic Boltzmann laws. International Journal of Modern Physics C 1996, 07, 595–601. doi:10.1142/S0129183196000491.

- Cont and Bouchaud (2000) Cont, R.; Bouchaud, J.P. Herd behavior and aggregate fluctuations in financial markets. Macroeconomic Dynamics 2000, 4, 170–196. doi:10.1017/S1365100500015029.

- Venkatasubramanian et al. (2015) Venkatasubramanian, V.; Luo, Y.; Sethuraman, J. How much inequality in income is fair? A microeconomic game theoretic perspective. Physica A: Statistical Mechanics and its Applications 2015, 435, 120–138. doi:10.1016/j.physa.2015.04.014.

- Gibrat (1931) Gibrat, R. Les Inégalités économiques; 1931.

- Pareto (1897) Pareto, V. Cours d’Économie Politique; Vol. II, F. Rouge: Lausanne, 1897.

- Kesten (1973) Kesten, H. Random difference equations and Renewal theory for products of random matrices. Acta Mathematica 1973, 131, 207–248. doi:10.1007/BF02392040.

- Kendall (1938) Kendall, M.G. A new measure of rank correlation. Biometrika 1938, 30, 81–93. doi:10.1093/biomet/30.1-2.81.

- Spearman (1904) Spearman, C. The proof and measurement of association between two things. The American Journal of Psychology 1904, 15, 72–101. doi:10.2307/1412159.

- Arfken et al. (2013) Arfken, G.B.; Weber, H.J.; Harris, F.E. Mathematical Methods for Physicists, 7 ed.; Academic Press: Boston, 2013; pp. 871–933. doi:10.1016/B978-0-12-384654-9.00018-9.

- Madras and Sokal (1988) Madras, N.; Sokal, A.D. The pivot algorithm: A highly efficient Monte Carlo method for the self-avoiding walk. Journal of Statistical Physics 1988, 50, 109–186. doi:10.1007/BF01022990.

- Goodman and Kruskal (1954) Goodman, L.A.; Kruskal, W.H. Measures of association for cross classifications. Journal of the American Statistical Association 1954, 49, 732–764. doi:10.2307/2281536.

- Karlin and McGregor (1959) Karlin, S.; McGregor, J. Random walks. Illinois Journal of Mathematics 1959, 3, 66–81. doi:10.1215/ijm/1255454999.