How Costly is Noise?

Data and Disparities in Consumer Credit††thanks: We thank Mario Curiki, David Du, Pranav Garg, Jacob Hartwig, Xuechen Hong, and Michael Yip for their excellent research assistance on the project. We thank Susan Athey, Stefania Albanesi, Bob Adams, Juliane Begenau, Neil Bhutta, Ken Brevoort, Greg Buchak, Lisa Cook, Will Dobbie, Anders Humlum, Paul Goldsmith-Pinkham, Erik Hurst, Dan Ringo, Claudia Robles-Garcia, Ashesh Rambachan, Amit Seru, Ken Singleton, Amir Sufi, Jann Spiess, Johannes Stroebel, Paul Willen, Francis Wong, and seminar participants at the University Of Chicago, UC Davis, Dartmouth, the Federal Reserve Board, the Federal Reserve Bank of St. Louis, NBER Household Finance, NBER Economics of AI, Stanford SITE, and Stanford University for helpful discussions and comments, as well as the Becker Friedman Institute and the Fama-Miller center at Chicago Booth for generous support. An earlier version of this paper circulated under the title “How Costly is Noise? Data and Disparities in the US Mortgage Market.” Any errors or omissions are the responsibility of the authors.

Abstract

We show that lenders face more uncertainty when assessing default risk of historically under-served groups in US credit markets and that this information disparity is a quantitatively important driver of inefficient and unequal credit market outcomes. We first document that widely used credit scores are statistically noisier indicators of default risk for historically under-served groups. This noise emerges primarily through the explanatory power of the underlying credit report data (e.g., thin credit files), not through issues with model fit (e.g., the inability to include protected class in the scoring model). Estimating a structural model of lending with heterogeneity in information, we quantify the gains from addressing these information disparities for the US mortgage market. We find that equalizing the precision of credit scores can reduce disparities in approval rates and in credit misallocation for disadvantaged groups by approximately half.

1 Introduction

Credit scores are used as a signal of applicant quality in many high-stakes screening decisions, including lending, rental housing, insurance underwriting, and hiring. Reliance on credit scores is becoming even more widespread with the advent of algorithmic decision-making, which automates the screening decision based on data inputs such as a credit score. As credit scores guide allocation in a growing share of the economy, it is crucial to understand how properties of credit scores affect allocative efficiency and who is able to borrow, rent a home, be insured, or obtain a job offer. There is particular concern as to whether credit scores can contribute to disparities in these outcomes across social groups such as minority or low-income applicants. Credit markets, specifically the US mortgage market, present a natural setting to study this question because reliance on commercial credit scores is high, the shift towards algorithmic underwriting is already underway, and resulting disparities can translate into inequality in home ownership and wealth accumulation.

This paper argues that lenders face higher uncertainty when assessing default risk of traditionally under-served groups and that this information disparity is a quantitatively important driver of inequality in credit market outcomes. We first show that widely used credit scores, which are designed to be predictors of default risk, are statistically noisier indicators of default risk for traditionally under-served groups.111Throughout the paper, we will be studying the VantageScore 3.0 credit score. We then show that this noise emerges primarily through the explanatory power of the underlying credit report data (e.g., thin credit files), not through issues with model fit (e.g., regulations that limit the flexibility of credit scoring models for disadvantaged groups), and thus cannot be fixed by more advanced prediction technology.

We present evidence that the gains from addressing these information disparities can be substantial. Estimating a structural model of the US mortgage market, we use a series of counterfactual exercises to show that equalizing the precision of credit scores can shrink disparities in efficiency and in loan approval rates for disadvantaged groups by approximately 50%. These estimates provide a stark illustrative example of how promoting disadvantaged groups’ ability to show their quality as borrowers can advance the goals of efficient and equitable credit access that are central in much of US policy.

New data help make these findings possible. We merge a large panel of consumer credit report data from TransUnion for 50 million anonymized consumers with three complementary datasets: first, public data from property deeds and related mortgage transactions for these consumers; second, a marketing dataset containing socio-economic characteristics of the same consumers; and third, public data on the mortgage lenders who originate loans for these consumers. The marketing dataset is sourced from the firm Infutor, as in Diamond et al. (2019). This unique merge across datasets makes possible both an instrumental variables strategy, which we use to identify unobserved default risk of marginally rejected applicants, and our analysis of various consumer groups, such as minority and low-income applicants.222To our knowledge, neither lender-specific information nor similarly detailed demographic data have previously been merged with credit report data in academic work, with the notable exception of the demographic variables in Avery et al. (2009) and Avery et al. (2012). The results in those two papers are consistent with the motivational evidence we build on in this paper.

We use these rich data to overcome the key challenge of measuring the default risk of unsuccessful loan applicants; this challenge is similar to assessing unobserved potential outcomes in other settings, such as judges’ bail decisions (Arnold et al., 2018) or employers’ hiring choices (Autor and Scarborough, 2008). We take two broad approaches in overcoming this challenge. In our structural work, we use an instrumental variables strategy based on lender-by-time-by-geography credit supply shocks that allows us to recover the default risk of marginally approved borrowers from various groups of applicants, which, together with other empirical moments, helps us estimate the distribution of unobserved default risk in different applicant populations. We complement this with a second approach in our reduced-form work, where we use consumer credit report data for rejected mortgage applicants and measure default risk using non-mortgage loans’ default outcomes (e.g., a rejected mortgage applicant’s auto loan). We show that this non-mortgage loan default measure is highly correlated with mortgage default in the sample of approved mortgages.

Starting with these reduced-form results, we find 7% to 9% lower fit of widely used credit scores (VantageScore 3.0 credit score) for minority or low-income mortgage applicants, in the sense of how well scores at the time of mortgage application predict later default. Our preferred performance metric is the Area Under the Curve (AUC) – a simple summary measure of the difference in predictive power exhibited in receiver operating characteristic curves, a widely used tool in machine learning to evaluate model performance. We confirm these results using the R2 metric, which suggests 16 to 18% lower model fit for the same disadvantaged groups.

To understand the sources of these precision differences, we next characterize two reasons why statistical risk prediction models can be less informative for different consumers, which we term modeling bias and data bias.333We note that these frictions do not necessarily introduce mean-nonzero bias in the statistical sense; we nevertheless follow the terminology of the computer science literature in terming such algorithmic frictions as biases. The first relates to whether prediction models successfully capture heterogeneity across groups in the data generating process for default, while the second relates to differences across groups in the data with which prediction models are estimated. The most obvious example of modeling bias is lower model fit for minority groups due to legal restrictions on the inclusion of protected class information in credit scoring models. The most obvious example of data bias are so-called thin-file consumers who have sparser credit report data. While modeling bias can be resolved by changing how we train scoring models, e.g., fitting separate models by group, data bias cannot be solved simply by improving the predictive models, but rather requires undoing the underlying data property that drives the poorer fit.

We provide two sets of evidence that the differential informativeness of credit scores for disadvantaged consumer groups stems more from data bias – that is, the underlying credit report data – as opposed to modeling bias. First, “fixing” modeling bias has little effect on precision differences across groups. In particular, neither training separate risk-prediction models for each group nor re-weighting groups’ influence in the model’s loss function reduces meaningfully the difference in predictive accuracy across groups. This finding holds both for logit models as well as advanced machine learning models that we estimate using hundreds of credit report features. Second, we find evidence in favor of data bias. Differences in the composition of credit report data – such as sparsity (in the sense of having data from few loans or few years of history), past default history, and account diversity (in the sense of only holding multiple types of loans) – explain roughly half of the between-group gap in credit scores’ predictive power. The residual gap is concentrated in “clean” credit files (those without a history of default), which we argue can be explained both by differences in default reporting as well as by between-group differences in the inherent predictability of default.

To complement our reduced-form work, and to quantify the importance of these precision differences in a high-stakes context, we build a structural model of a mortgage lender making loan approval decisions based on various information sources. The goal of the model is threefold. First, the model allows us to quantify differences in credit score precision while accounting flexibly for other differences across groups, both in terms of the precision of other, non-credit-score information sources and in terms of the underlying distribution of unobserved default risk. Second, the model provides a complementary and independent empirical strategy for estimating the precision differences emphasized in our reduced-form work. Third, and most importantly, the model allows us to quantify the importance of these precision differences in economic terms: that is, given the model’s estimates of between-group differences in other factors such as the distribution of actual default risk or the precision of other available information sources, how much would improvements in credit score precision for disadvantaged groups reduce disparities in credit allocation?

In the model, a mortgage applicant’s true default risk is unobserved by the lender but the lender receives both a credit score signal and other signals that she uses to screen applicants. We assume normality in both signal noise and in underlying default risk types, which allows us to express the lender’s posterior belief (after observing the signals) in tractable terms. The lender can observe either signal precision or, equivalently, group membership, knowing how precision differs across groups, and forms her belief about default risk accordingly. We deliberately abstract from modeling pricing decisions or markups from imperfect competition in order to focus on the changes in the information structure which are the emphasis of this paper.

Model identification relies on an instrumental variables strategy that recovers the characteristics of marginally approved loan applicants, building on a classic Becker (1957) test of marginal borrowers’ characteristics. Our instrument exploits Community Reinvestment Act (CRA) exams, following Agarwal et al. (2012). The Community Reinvestment Act, passed in 1977, mandates US financial regulators “to encourage insured depository institutions to help meet credit needs of all segments of their local communities” (Federal Reserve Board, 2018b). Consistent with Agarwal et al. (2012), we find that banks increase lending, in particular in CRA-eligible locations, just prior to CRA exams.444We discuss the validity of the instrument and the broader literature on CRA-induced lending extensively in Sections 6.1 and 6.2. This plausibly exogenous variation in approval leniency of mortgage lenders allows us to identify marginal loan applicants and their default outcomes. Intuitively, holding approval rates constant, the difference between the marginal and average default rate tells us how much information lenders obtain through their screening tools – with a perfectly uninformative screening tool implying no difference between marginal and average default rates, and informative screening tools implying a large difference. Additional data moments include the mean of credit scores of rejected and approved applicants, approval rates, and the slopes of forward and “reverse” regressions relating credit score with default outcomes – a standard way of assessing measurement error in a regressor (Black et al., 2000), which helps identify how much of lenders’ total information across all signals is coming from credit scores as opposed to other information sources.

The structural model yields estimates of credit score noise disparities that are similar to our reduced-form approach. Concretely, we estimate that the standard deviation of credit score noise of minority applicants is 2.2 times higher than that of non-minority applicants. Simulating out default rates and credit scores, these differences translate to a 5% difference in terms of AUC (cf. 7% in our reduced-form evidence). Low-income applicants similarly have greater credit score noise than higher-income applicants, which translates into a 10% difference in terms of AUC (cf. 9% in our reduced-form evidence).

Finally, we use the structural model to quantify the importance of these precision differences in economic terms, by way of solving for counterfactual mortgage approval decisions under alternative information structures that reduce or change the precision differences faced by various groups. These exercises hold constant other features of the mortgage market, such as differences in the distribution of underlying default risk across groups, in order to speak precisely to the costs of credit score noise. We find that equalizing credit score signal noise can shrink efficiency differences and disparities in approval rates by up to 50%. For minority mortgage applicants, nearly half of the counterfactual increase in approval rates is due to a reduction in inefficient rejections – rejections for borrowers to whom it would be ex ante efficient to lend.

Related literature

Our paper contributes to a large literature on the causes and consequences of credit market disparities. Much existing research focuses on human frictions such as discrimination, bias, or agency conflict after controlling for observables such as credit score (Dobbie et al., 2019; Bartlett et al., 2019; Bhutta and Hizmo, 2020; Heimer and Yu, 2021; Bayer et al., 2018; Zhang and Willen, 2020; Hanson et al., 2016; Ross et al., 2008; Butler et al., 2020). We instead study how these observables themselves can drive credit misallocation and disparities. We focus on the mortgage market which plays a prominent role in the persistence of wealth gaps across generations (Charles and Hurst, 2003; Kuhn et al., 2020), with historically disadvantaged groups being less likely to transition into home ownership and build home equity (Charles and Hurst, 2002). Our results highlight a mechanism by which a credit scoring system can perpetuate credit misallocation over time: disparities in credit access at one point in time translate into disparities in credit report information in the future, a persistence that might be termed “credit score hysteresis” in the tradition of Blanchard and Summers (1986).555In the Blanchard and Summers (1986) context, long-run unemployment becomes endemic to a labor market through a hysteresis effect. Other recent work on hysteresis at the intersection of wealth inequality and credit markets includes Mian et al. (2020).

We also contribute to a literature that studies the role of credit scores for market efficiency and distributional outcomes. Relative to this literature, we identify differences in credit score precision as a key channel through which credit market disparities arise, and we study how these disparities appear not just in credit access but also in credit misallocation. In addition, we show that realizing improvements in these dimensions requires more than changes in statistical technology alone but rather a change in the underlying credit report data. Prior work on credit scoring or statistical technology in credit markets in contrast has emphasized credit scores’ role in overcoming asymmetric information among new borrowers (Einav et al., 2013; Adams et al., 2009), incentivizing loan repayment (Chatterjee et al., 2020), and facilitating loan securitization while discouraging lenders’ use of soft information (Keys et al., 2012, 2010). Recent work has also warned that more flexible statistical technology such as machine learning can reduce overall loan approval rates for disadvantaged groups (Fuster et al., 2020), and that modern, FinTech underwriting continues to generate cross-group disparities in loan terms (Bartlett et al., 2019); credit scores likewise are seen to play a role in geographic misallocation in the US mortgage market (Hurst et al., 2016). Much of this work echoes persistent policy concerns about equity across consumers in credit scoring (Avery et al., 2009, 2012; Traub, 2013).

By studying the effects of changes in the information structure in lending markets, we also contribute to a literature that studies how regulation or innovation in information sources can affect different groups’ outcomes in markets with screening. An active labor literature studies the consequences of using screening tools such as criminal records or credit reports,666Examples include Autor and Scarborough (2008); Agan and Starr (2018); Bartik and Nelson (2020); Doleac and Hansen (2020); Wozniak (2015); Corbae and Glover (2018). and recent work has emphasized the importance of heterogeneity in signal precision in these or related settings especially (Arnold et al., 2020b; Chan and Gentzkow, 2020; Bartik and Nelson, 2020). This draws on a longer tradition of work concerned with signal precision heterogeneity (e.g., Aigner and Cain (1977)). Likewise, there is extensive work in finance that studies changes in lenders’ ability to use public credit report data, their own private information, or other lenders’ assessment of default risk.777While far from an exhaustive list, examples of such research include Liberman et al. (2018); Nelson (2020); Hertzberg et al. (2011).

More broadly, we contribute to a rapidly growing literature on Fairness, Accountability, and Transparency (FAT) in computer science.888For summaries see e.g. Barocas et al. (2019); Kleinberg et al. (2018); Barocas and Selbst (2016); Zafar et al. (2017); Kleinberg et al. (2018); Lakkaraju et al. (2017); Kearns and Roth (2019); Rambachan and Roth (2019); Cowgill and Tucker (2020). While this literature has taken a largely axiomatic approach to evaluating disparities in algorithmic decision-making based on various fairness metrics, for example equal error rates across demographic subgroups (Zafar et al., 2017), we offer an alternative approach grounded in economic theory.999We share this goal with Rambachan et al. (2020) who use a principal-agent approach to characterize optimal fair lending policy. The type of quantification exercises our structural model provides are key for welfare considerations which have largely been absent from the computer science or machine learning literature. A key focus of this literature has been what type of restrictions to impose on algorithms with regard to the use of protected class. While protected class is typically considered a prohibited input in credit scoring models (Bartlett et al., 2020; Yang and Dobbie, 2019), recent research has suggested that such restrictions are no longer feasible in a world of complex algorithms (Gillis and Spiess, 2019; Gillis, 2020) and less disparate outcomes might result from allowing the inclusion of protected class. We show that the precision gains from including protected class are limited in practice and that challenges with the underlying data, not restrictions on algorithmic inputs, present the binding constraint for improving allocative efficiency in US mortgage markets.

This paper is organized as follows: Section 2 presents our data. Section 3 presents our reduced-form evidence and Section 4 develops our analysis of the sources of credit score noise. Section 5 describes our structural model of lender underwriting in the presence of noisy signals, and Section 6 presents our results from the instrumental variables strategy and then from model estimation. Section 7 concludes.

2 Data

Our dataset is based on a sample drawn from a marketing dataset with broad coverage across the US, merged to publicly available data drawn from property records from CoreLogic. These data are then linked with publicly available, bank-specific information for use in our instrumental variables strategy, and, finally, linked with a panel of credit bureau data.

The marketing dataset is acquired from Infutor, as in Diamond et al. (2019), Bernstein et al. (2019), Diamond et al. (2020), and Qian and Tan (2020). The data include a near-universe of address histories and socioeconomic information that allow us to identify the various groups studied in our analysis. We probabilistically sampled from this near-universe, allowing us both to recover a representative sample for the population and to ensure sufficient sample size in several sub-populations of interest.101010We probabilistically oversampled several disadvantaged groups and geographies in order to ensure sufficient power. Based on name and address, we merge these data with publicly available property-specific data for US homeowners, sourced from CoreLogic. The latter data include property-specific characteristics including the history of home prices at each sale date, and also mortgage-relevant characteristics, including the amount, date, and lender for each mortgage loan, and information on whether the loan was a refinance or purchase loan.

Based on lender names and property location, these marketing data and property-specific data are then linked with publicly available, bank-specific data for 6,954 US mortgage lenders. This merge allows us to include several potential shifters of bank loan supply in our analysis, including details on the timing of bank regulators’ examinations under the Community Reinvestment Act (CRA), which we detail more below. We find that the idiosyncratic timing of these exams shifts bank loan supply, as also evidenced in Agarwal et al. (2012), which we exploit in an instrumental variables strategy to identify the characteristics of marginally rejected loan applicants. Our sample includes 2,324 banks that undergo a CRA exam in our sample period. Lenders have an average of 1.2 CRA exams in our sample period with a maximum of four exams.

Finally, our credit report data from TransUnion are available for the period between 2009-2017. TransUnion performed a merge between the Infutor data and the credit report data based on social security numbers, first and last names, and the most recent address. TransUnion returned only the de-identified data. The credit report data allow us to construct mortgage applications, mortgage approvals, as well as loan performance in the 24 months following the mortgage application. We infer applications from a hard credit inquiry by a mortgage lender (Avery et al., 2003). We infer a rejection in any instance where we see one or more applications for a new mortgage and no new mortgage origination in the subsequent 3 quarters.111111Our preferred horizon of 3 quarters is based on advice from credit risk model building teams at large financial institutions. We show robustness to our choice of 3 quarters in Table A.1 in Appendix A.121212Beyond those included in this section, additional details about data construction are reported in Appendix B.

The credit report data usefully allow us to observe rejected loan applications, and to observe the performance of rejected applicants on their other, non-mortgage loans in order to learn about their underlying default risk. The availability of credit scores (VantageScore 3.0 credit score) in the credit report data also allows us to measure how the mean, variance, and default covariance of credit scores differ across accepted and rejected applicants, which we use to help discipline our model estimates about the amount of statistical noise in credit scores relative to other information sources used in approval decisions.

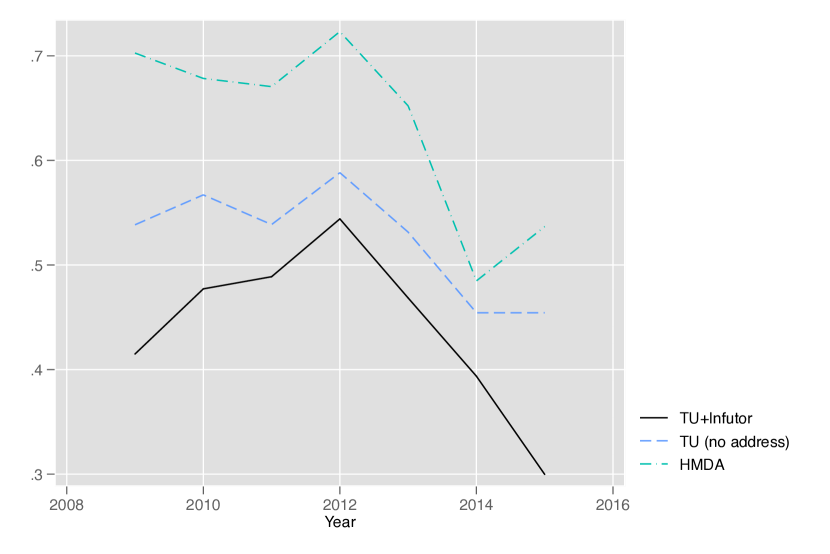

Table 1 shows summary statistics for our sample of originated mortgages across the data merges. The first column reflects our primary sample, individuals for whom we successfully link credit bureau data with Infutor. Subsequent columns reflect increasingly restrictive subsamples conditioned on various merges, including our initial merge with CoreLogic (column 2), screens for high-quality matches between CoreLogic and the credit bureau data (columns 3 and 4), and a merge with mortgage lender information based on bank names (column 5). While merge rates are considerably below 100%, given data limitations and the need for merges on inexact name strings, we are reassured that the sample summary statistics are quite comparable across columns. For example, the share of minority mortgage holders ranges from 10% to 12% across columns, the share of conventional mortgages ranges from 68% to 74%, and mortgage amounts stay within a $7,000 range, relative to a mean of slightly over $200,000.131313Table A.2 in Appendix A shows summary statistics for our sample of mortgage applicants. This sample only relies on the successful merge with Infutor which we require to estimate minority status. The first column shows all initial matches with Infutor, and the second column shows a subsample conditioned on various screens for high-quality matches, such as having a current address (in Infutor). As in the origination sample, the distribution of observables remains stable across the two samples. The latter sample is a superset of the sample in column (1) of Table 1, which further conditions on observing an originated mortgage.

We classify a mortgage origination as a refinance loan if the borrower has at least one open mortgage prior to the application date; the Infutor address indicates that the borrower does not move in a 1-year window around the origination;141414Our Infutor data end in 2017. Hence for transactions in late 2016, we classify them as a refinance if there is no move before and on the date of the origination. and the number of open mortgage does not increase (to rule out second homes). A closely similar approach is followed in Mian and Sufi (2018). We validate the refinance flag using data both from CoreLogic and HMDA. See Appendix C for details.

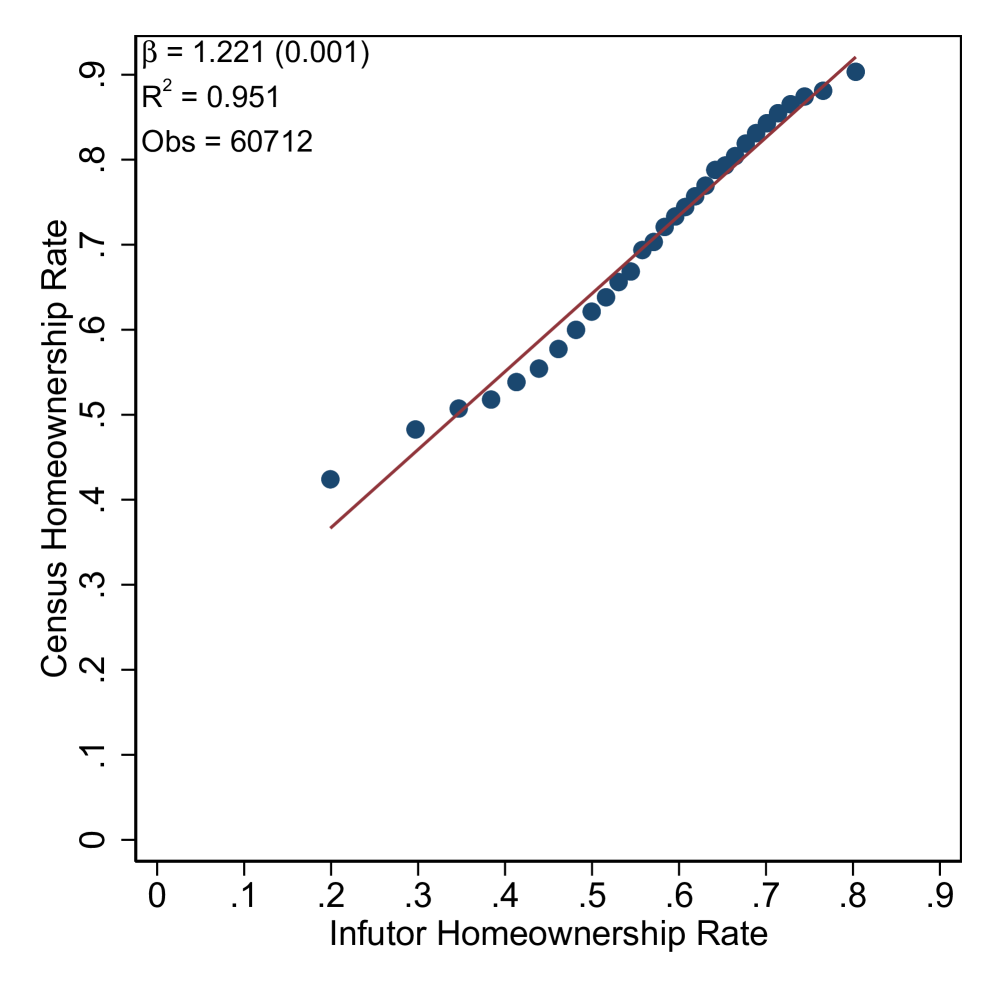

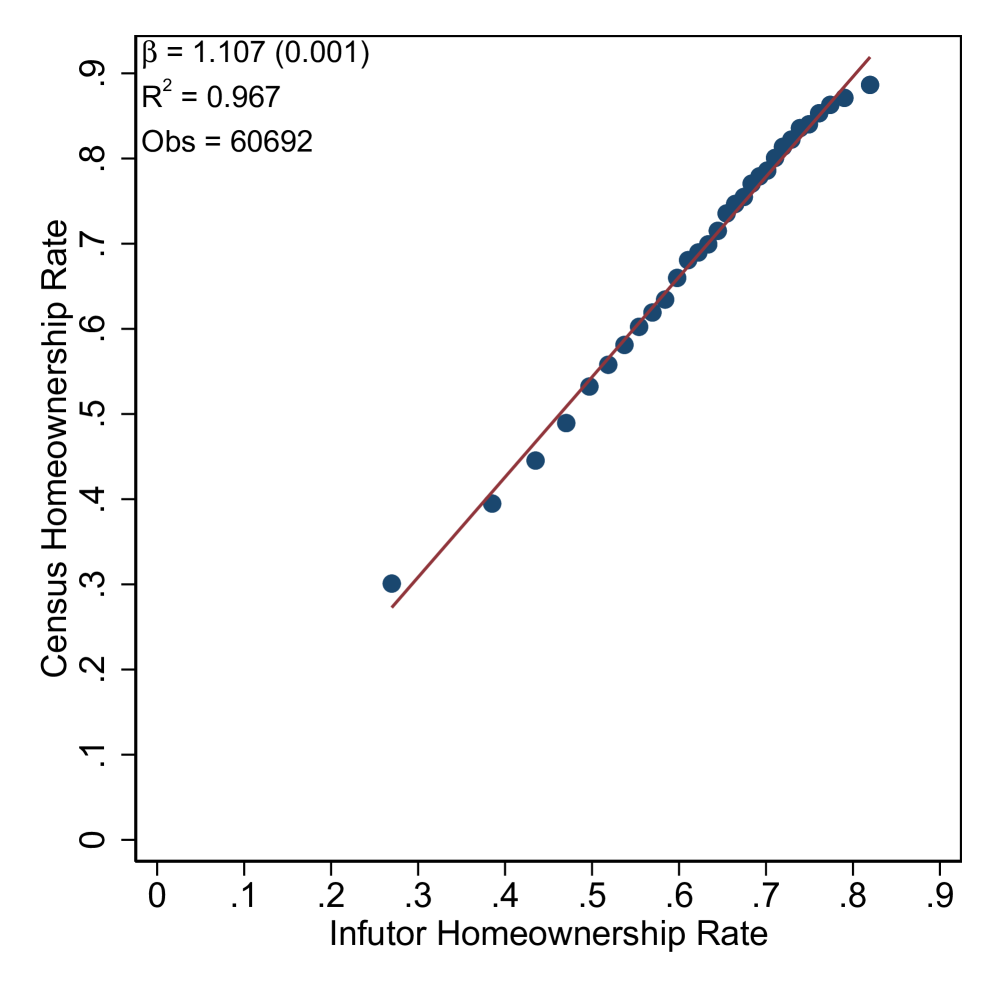

We define two indicators of economic disadvantage: low income, and racial or ethnic minority. To classify income status, we use a measure of estimated income based on a proprietary algorithm provided by the credit bureau. The algorithm was developed based on income reported on tax filings between 2008 to 2012 and estimates income to the nearest thousands. We define low-income applicants as those that fall in the bottom quartile of the income distribution in our sample (cut-off is defined year-by-year). Second, we infer minority/non-minority status using a standard Bayesian Improved Surname Geocoding (BISG) approach, which uses name and geographic information to predict race and ethnicity (see Appendix D for details).151515We use a two-step procedure to assign race and ethnicity in the marketing dataset that provides names and addresses, which we merge to both the CoreLogic and credit bureau data. First, we follow an approach developed by Sood and Laohaprapanon (2018), which uses Voter Registration data to predict the relationship between the sequence of characters in a name and race and ethnicity. After applying their approach, we update each individual’s baseline racial/ethnic probabilities with the racial and ethnic characteristics of the census block associated with her or his place of residence in 2000 using Bayes’ Rule, and we then update the Bayesian posterior again using an individual’s 2010 address and the 2010 census data. An individual is assigned to a racial/ethnic category if this category has the highest posterior probability for that individual. This two-step method is similar to methods used by the CFPB to construct race and ethnicity in fair lending analysis. Work by the CFPB (2014) and Elliott et al. (2009) shows that combining geographic and name-based information outperforms methods using either of these sources of information alone. We aggregate all ethnic and racial minorities into a single minority category and define its complement as the non-minority group.161616Table E.4 shows the cross-tab between minority and income status. Since both our measures of economic disadvantage rely on an imputation strategy, we conduct extensive validation in Appendix E. Our validation relies on matching originated mortgages in our sample to HMDA, which contains the borrower’s self-reported income and race/ethnicity. The match is performed on mortgage amount, geography, year, and lender name. We successfully match 16m purchase loans and 24m refinance loans. Given data limitations of the publicly available HMDA data, we cannot perform the merge for loan applications. We find that both our low-income and minority indicators are highly correlated with the corresponding indicators in HMDA.

3 Quantifying Noise in Credit Scores

This section presents our reduced-form work quantifying noise in credit scores. The key challenge we address in this section is unobserved potential default outcomes for rejected applicants – also known as reject inference in credit scoring.171717See Siddiqi (2017) for an extended discussion. Reject inference is also analogous to what Lakkaraju et al. (2017) call the “selective labels problem” and more broadly to the classic econometric issue of unobserved potential outcomes. See also Arnold et al. (2020a) drawing the analogy between selective labels and unobserved potential outcomes, and Rambachan and Roth (2019) for a discussion of how selection into training data can have subtle effects on the predictive power of algorithms trained on those data. A frequent solution is to simply drop rejected applicants and compute credit score performance in the sample of approved applicants. However, differences in credit score performance for approved applicants may not reflect the differences in the overall applicant sample, as loans are not randomly approved. We propose two different solutions to the reject inference challenge: first, a reduced-form approach described below, where we measure unobserved default risk using outcomes on other credit products, and second, a structural model described in Section 5, where we identify unobserved risk based on moments from approved, rejected, and marginal applicants.

3.1 Measuring Risk Using Non-Mortgage Loan Products

We infer outcomes for rejected applicants using delinquency on any non-mortgage product 24 months after the application date, which is available for nearly all the mortgage rejects. This approach exploits the fact that we can follow the credit report of both rejected and approved applicants over time.181818This is a type of reject inference by extrapolation. (See also Coston et al. (2021) for an application of this type of reject inference to credit data.) Unlike most applications of this type of reject inference, we leverage that we observe other applicant credit behavior after the application regardless of the outcome of the application.

Table 2 shows default rates across different loan products for the sample of applicants by loan approval status and loan type. More than 90% of applicants in our sample have at least one loan product on their credit report. A similarly large fraction have a credit card, around 50% of applicants have an auto loan, and around 10% have a home-equity loan. We exclude information on student and personal loans due to data limitations.191919We conduct robustness tests using an all-encompassing any-default variable provided by TransUnion that includes all loan products reported to the credit bureau. Our results are very similar when using this measure. As expected, rejected applicants have higher default rates across products.

We construct a summary default measure on non-mortgage products from information on credit cards, auto loans, and HELOCs (hereafter “non-mortgage default” measure). Table 3 shows how well the non-mortgage default measure predicts mortgage default in the sample of approved mortgage applicants. The table shows confusion matrices as well as precision and recall as we vary the severity of the non-mortgage measure.202020Precision in this context refers to the ratio of correct positive predictions to the total predicted positives. (This is distinct from precision in the sense of the inverse variance of signal noise, as we use in Sections 5 and 6.) Recall refers to the ratio of correct positive predictions to the total positive cases. A positive is a default and a true positive is a correctly predicted default. Our strategy has to balance precision and recall. With the most encompassing default definition, which includes a one-off missed credit card payment, we maximize recall but will sacrifice precision, as missing a card payment once is unlikely to be a good predictor of mortgage default. As we move to more stringent default definitions (e.g., requiring delinquency of at least 60 days), we improve precision but sacrifice some recall. Our preferred measure is the non-mortgage default measure of 90 days or more past-due. This measure also corresponds to the default measure typically used in the construction of consumer credit scores (Federal Reserve Board, 2007). In Appendix F, we provide further information on these default measures.

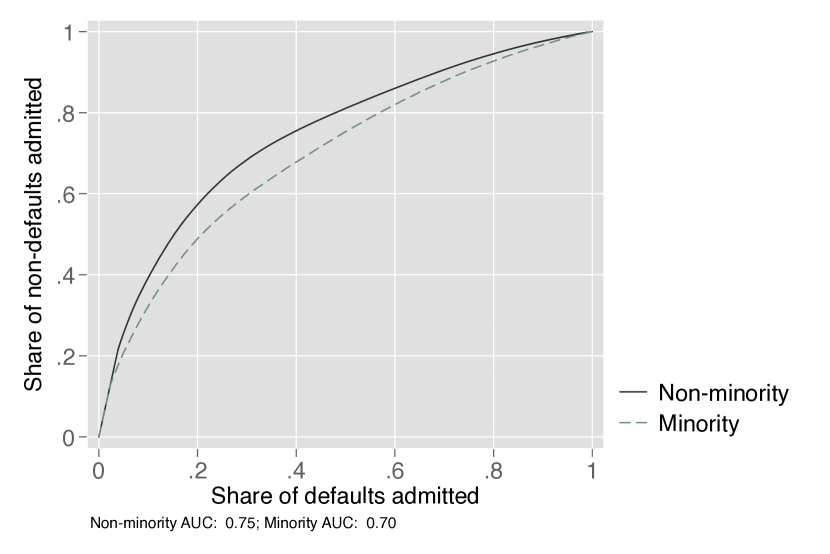

We use the non-mortgage default outcomes to construct receiver operating characteristic (ROC) curves, which are a popular tool in machine learning to assess model fit. ROC curves show the ability of a prediction algorithm, such as a credit score, to predict non-defaults separately from defaults as the (credit score) approval threshold is varied. An efficient predictor maximizes the fraction of non-defaults approved (referred to as a true positive rate) and minimizes the number of defaults mistakenly approved (referred to as a false positive rate). The predictive performance visualized in a ROC curve is summarized in the Area Under the Curve (AUC) measure. An alternative approach relies on the (observable) relationship between mortgage and non-mortgage default to directly compute the mortgage ROC and leads to a similar conclusion (see Appendix F for details).

3.2 Noise in Credit Scores: Results

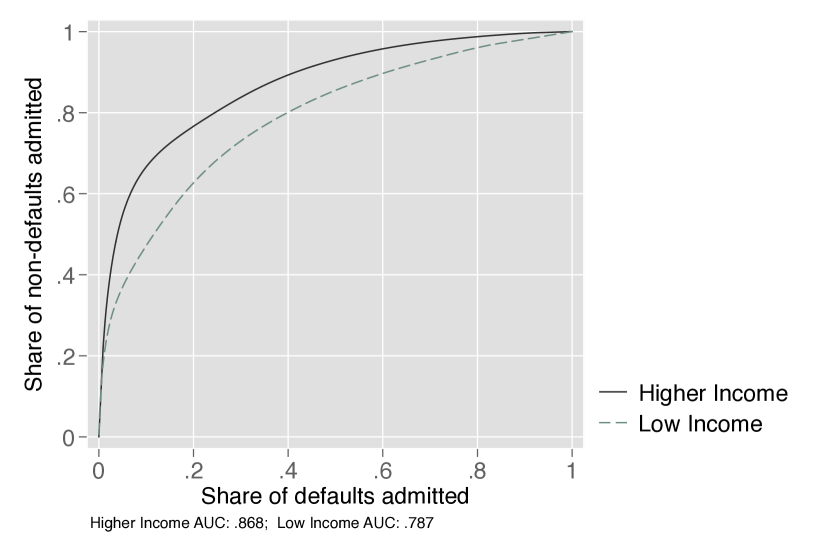

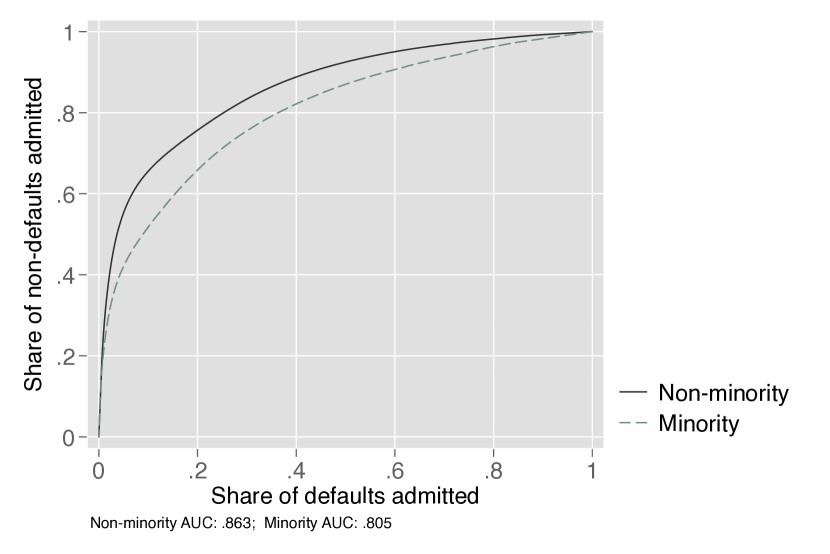

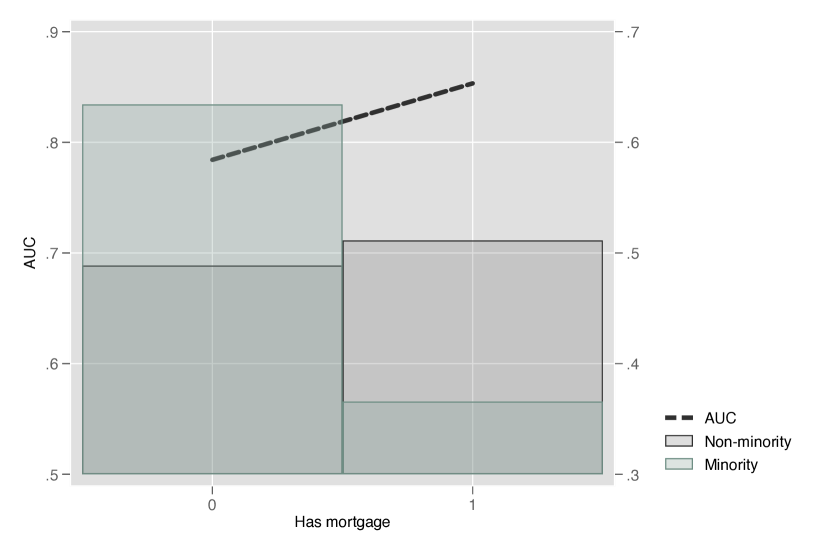

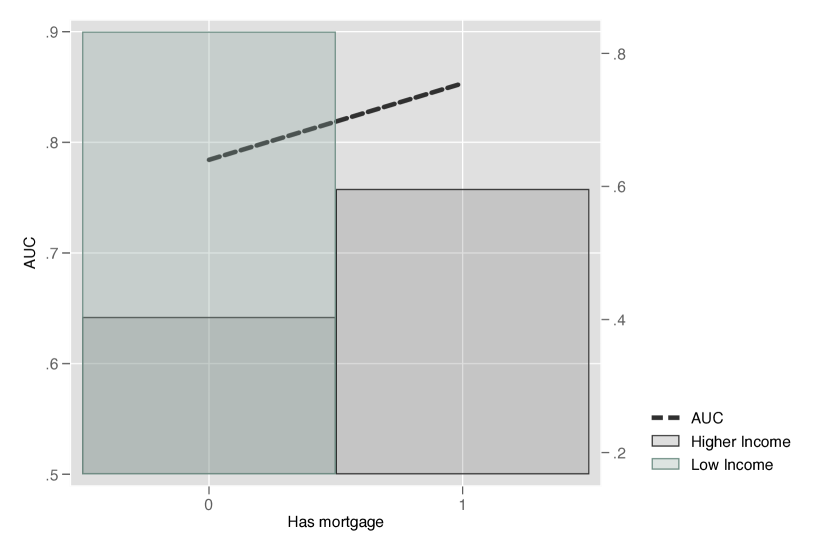

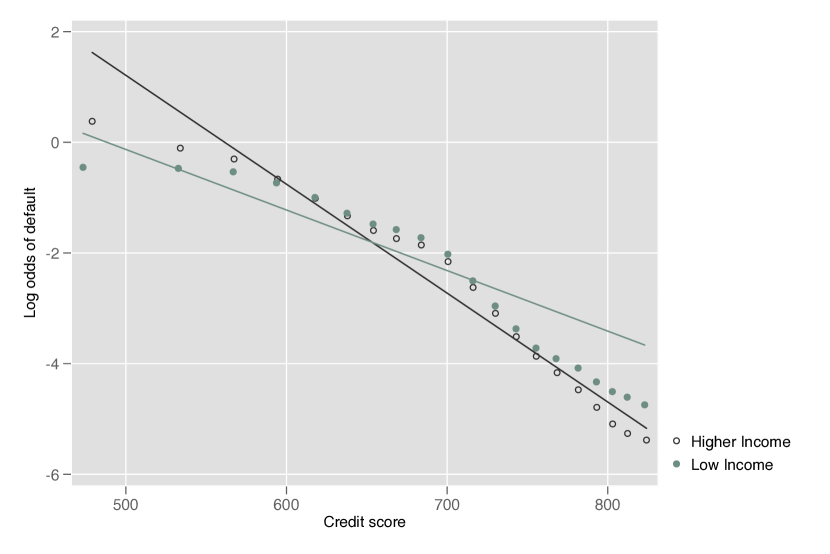

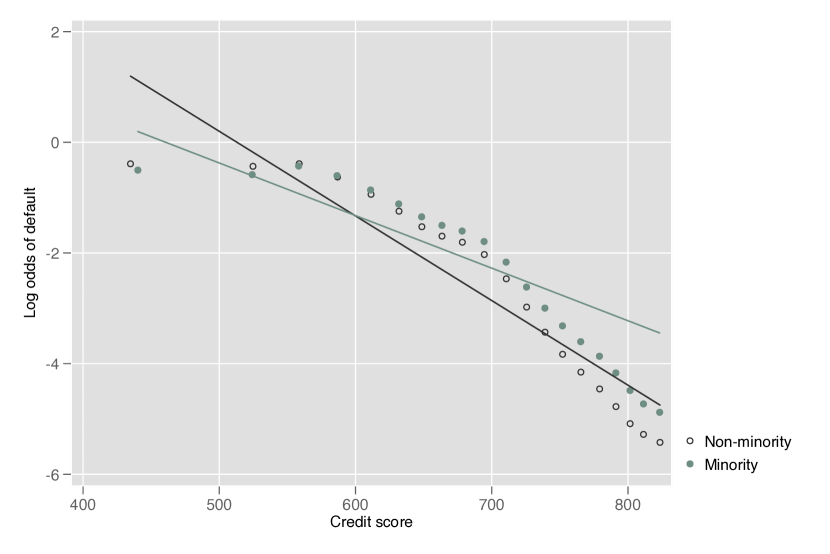

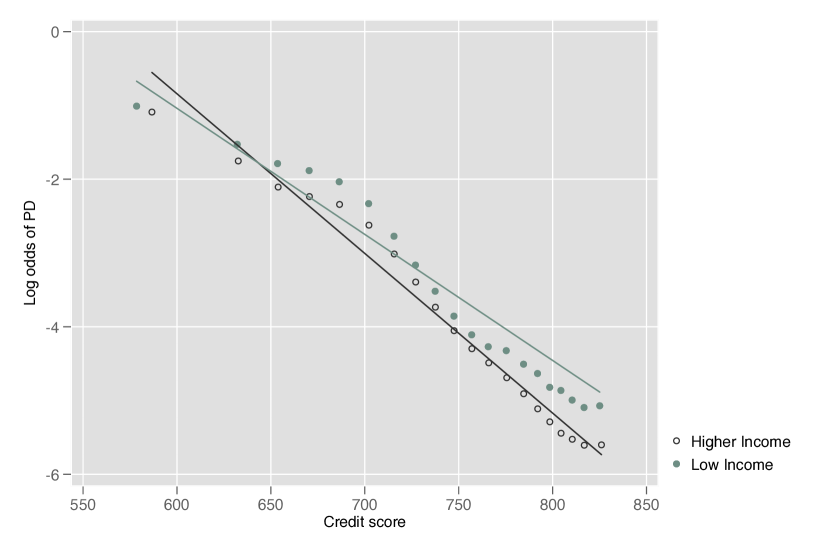

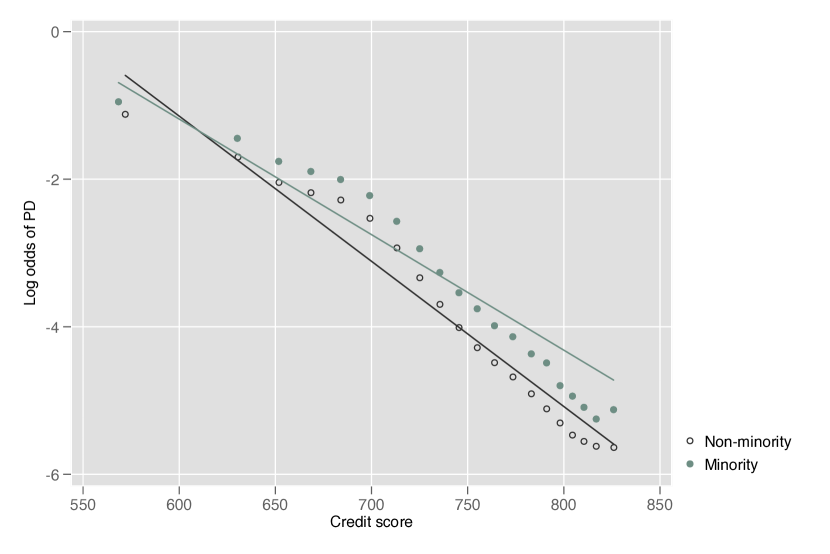

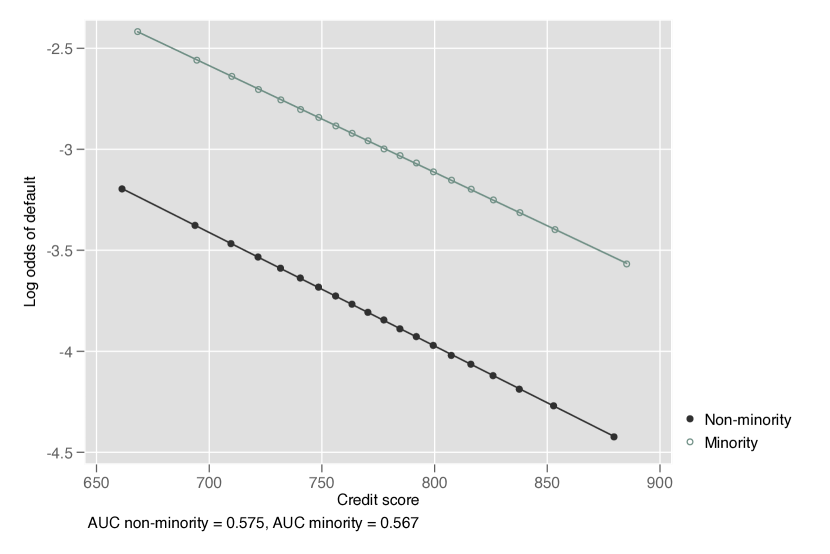

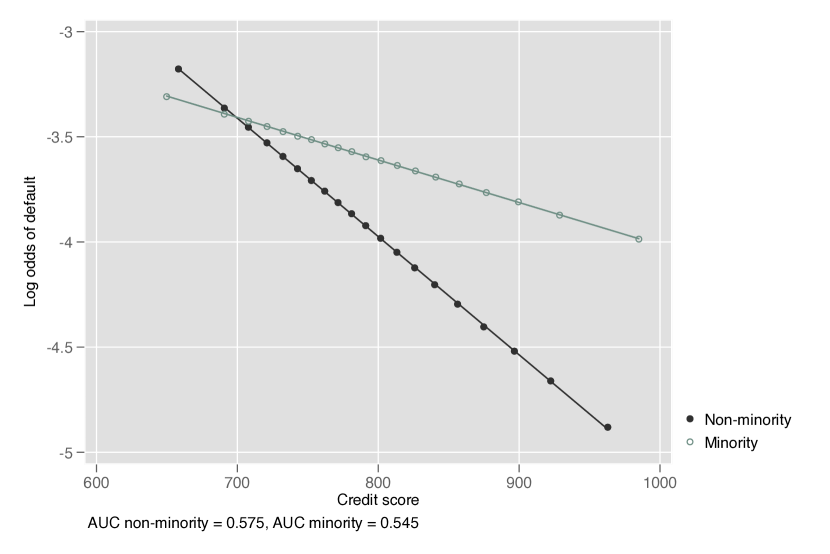

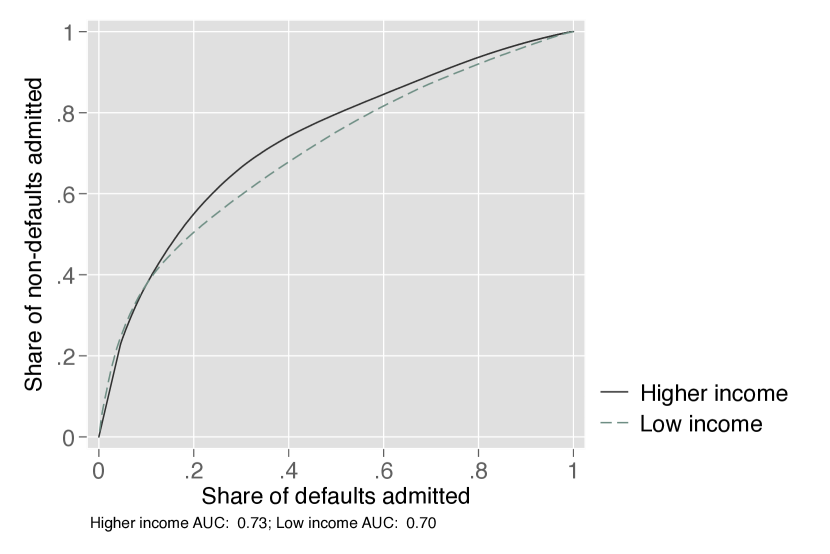

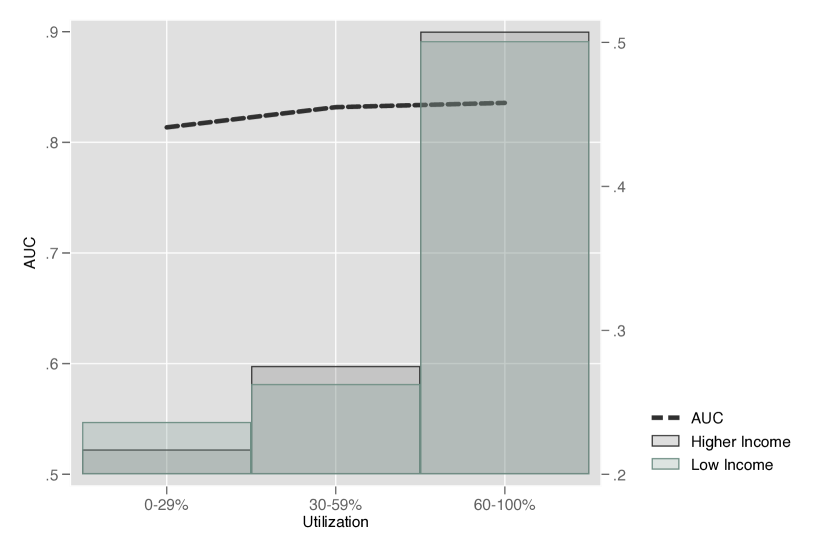

We show that the VantageScore 3.0 credit score has lower predictive accuracy – based on AUC and R2 – for low-income and minority groups among our sample of mortgage applicants. The ROC curves in Figure 1 show this result visually, with minority and low-income consumers’ ROC curves falling markedly below ROC curves for non-minority and higher income consumers. Table 4 tabulates the AUC and R2 metrics corresponding to the ROC curves in Figure 1 as well as several alternatives.212121We show results for the full sample of applicants. We obtain essentially identical results when computing predictive accuracy in a sample where both groups are equally represented to ensure that sample sizes are not affecting our performance measures. According to the Area Under the Curve (AUC) measure, which summarizes the differential model fit across all possible credit scores, model fit is 9% lower for the lowest income quartile relative to higher-income consumers. The credit score at time of mortgage application has a 16% lower R2 for default for borrowers in the lowest income quartile relative to applicants in the other three income quartiles. For minorities, the R2 difference is 18% while the AUC difference is 7%. The R2 is obtained by first computing the average log odds of default in each one-point score bin and then regressing the log odds on the credit score, weighting by the number of observations in each bin.222222An alternative specification would be to run a logistic regression of default on the credit score at the individual level. Given the size of our data, this aggregation approach is computationally easier. When we compare our results to R2 obtained at the individual level in a random sample of our data, we obtain very similar results on between-group gaps.

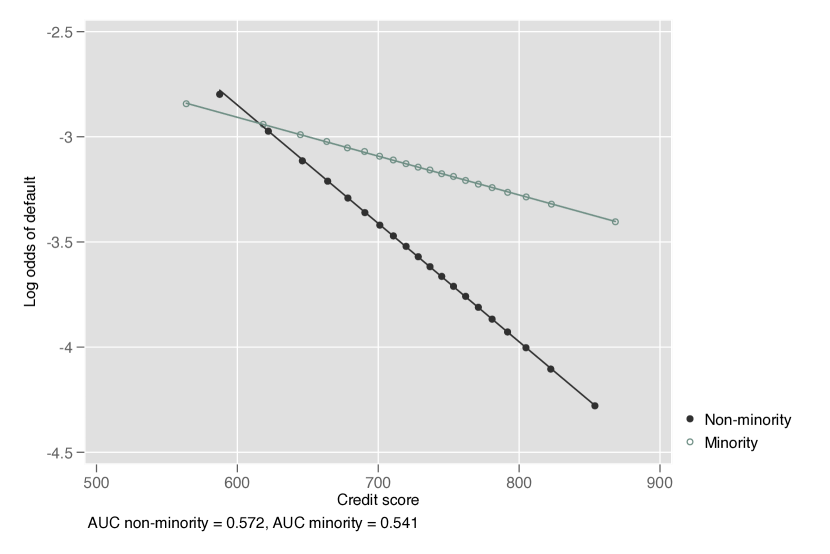

We provide a second type of visual evidence for our finding of differential informativeness. In Figure A.2 in Appendix A, we plot the relationship between default and credit score separately for various consumer types. We show that this relationship is flatter for the consumer types we found to have lower R2 and AUCs, consistent with higher noise – that is, higher measurement error – in scores attenuating the relationship towards zero.232323To understand this result, consider regressing the log odds ratio of default on a signal of default risk (credit score) for each group , as , where is probability of default for individuals in group , conditional on a realization of the signal or score . Assume the signal is measured with noise . If the signal has more measurement error for a consumer group, classical errors-in-variable theory indicates that the coefficient for that group is more heavily attenuated towards zero. Table A.3 in Appendix A provides the point estimates for this specification.

Our findings have important implications for how to interpret prior evidence that commercial credit scores are not calibrated across groups (e.g., Avery et al. (1996)); that is, the probability of default conditional on a given credit score is not identical across groups. Figure A.2 in Appendix A reveals a similar result in our sample. This miscalibration is often interpreted as driven by some sort of “bias,” whereby the credit score signal is not centered around a consumer’s true default risk but around the true default risk plus some bias term. However, simulations in Appendix A Figure A.3 show that the patterns observed in the data arise even if credit scores feature only noise (but no bias), as long as the underlying true default processes are different. The simulations also show that any potential bias would have little impact on AUC differences across groups, since AUC focuses on the ability of an algorithm to correctly rank consumers according to risk. In other words, an algorithm can correctly rank applicants even if the point estimate of the probability of default is on average too high or too low.

4 Sources of Noise

In this section, we investigate the possible sources of noise. We propose two potential sources of noise, explain how to test for sources of noise in the data, and present results.

4.1 Framework

We propose two potential sources of noise: modeling bias and data bias.242424As emphasized in the introduction, these frictions do not necessarily introduce mean-nonzero bias in the statistical sense; we nevertheless follow the terminology of the computer science literature in terming such frictions as biases. We further sub-divide modeling bias into aggregation bias and majority bias. Recall that a credit score is a mapping from observables (e.g., credit report data) into a predicted default outcome such that , where can be viewed as a conditional expectation function.

Aggregation bias arises when the true conditional expectation function for two groups differs but the algorithm is prevented from fitting separate models for each group.252525The terminology is based on Suresh and Guttag (2020). For example, the Equal Credit Opportunity Act’s prohibitions against “disparate treatment” forbid using data on protected class membership (for example, minority status) in credit risk model building. Similarly, income data are not used in credit scoring due to regulatory restrictions.262626Income is typically evaluated in a separate ability-to-pay exercise that considers debt-to-income constraints. However, it is not used directly in the credit score, given concerns about disparate impact arising through income’s correlation with membership in various protected classes (LaCour-Little and Fortowsky, 2004). Aggregation bias can be resolved by either fitting separate models for each group, or allowing the algorithm access to the group membership variable and sufficient flexibility to effectively fit the differences in .

Second, majority bias compounds the aggregation bias problem since a predictive model will be able to achieve higher precision when given more data. The fact that there are likely to be fewer minority and low-income individuals in the training data would imply that the models are inherently less able to achieve the same precision for these groups. Majority bias should disappear if the training data is re-weighted to represent both groups equally.272727Some recent papers in machine learning refer to majority/aggregation biases as a type of data bias, e.g. Blum and Stangl (2020).

Finally, we use data bias to refer to sources of noise that come from the underlying data as opposed to the mapping from the data into predicted default outcomes. There are three forces that can drive data bias in our setting: compositional differences; differences in how default is or is not reported to credit bureaus for different groups; and differences in outcome predictability. Compositional differences matter if some types of credit report data are less informative about future default and disadvantaged groups are more likely to have these types of credit report data. Examples are sparse data (e.g., thin or young credit files), “dirty” files (e.g., showing past default), or non-diverse files (e.g., only holding one type of loan). Differences in default reporting can lead to a mismatch between the true outcome we would like to observe – did a borrower miss a payment – and the outcome we observe in the data – is a missed payment reported to the credit bureau. This can be driven by, for example, differential use of lenders who do not report to traditional credit bureaus. Finally, available observables might just be less informative for predicting default of disadvantaged groups, for example because the shock process that drives default could be more volatile for minority or low-income applicants.

4.2 Empirical Approach and Results

In order to test these hypotheses on the sources of noise, we proceed in two steps. First, we build our own set of default prediction models to test whether we can reduce precision differences across groups through two approaches: training group-specific models to avoid aggregation bias, or re-weighting training data to avoid majority bias. A significant reduction in the precision gap across groups when using these approaches would point to modeling bias being a primary source of noise. Second, we investigate differences in the underlying credit report data between groups. In particular, we investigate whether there are significant differences in the composition of credit report data, and whether any differences remain once we condition on similar credit report observables.

4.2.1 Modeling Bias

We build a suite of default prediction models based on a logit, a random forest, and a XGBoost algorithm. We train the models on a sample of 364,979 mortgage applicants. Our baseline models are trained on a pooled sample that has 22.9% minority applicants and 28.3% low-income applicants. We use the same non-mortgage default outcome as in our reduced-form reject inference exercise in Section 3. We select 219 credit report variables that include information on delinquencies across all credit products, evolution of the consumer’s debt balance over time, public records related to debt collection (for example, a court judgment), credit availability, credit file “thickness” (for example, the number of accounts or items on the report), applications for new credit, as well as a range of mortgage-specific variables. We deliberately do not include existing credit scores in our set of predictors, in order to focus on the explanatory power of the underlying credit report data itself. We use this full set of features for our machine learning models, whereas for the logit model, we hand-select 35 features. All models are estimated using the Python skicit-learn library.282828We tune the models using a random grid search using 5-fold cross-validation. Table A.4 in Appendix A reports search grids and chosen hyperparameters for each model.

Table 5 shows results from the estimated models. Our baseline models attain predictive performance that is comparable to the VantageScore 3.0 credit score, giving us confidence that we have built reliable and representative risk prediction models.292929All performance statistics are calculated on the test (or holdout) data set. Moreover, Figure 2 shows the correlation between commercially available credit scores (Vantage Score 3.0) and predicted default probabilities from our XGBoost model. The correlation coefficient is 0.760, suggesting that our models generate output similar to commercially available models.

Our models also have lower precision for the disadvantaged groups we study, suggesting that our models are subject to the same challenges that drive noise we illustrate for commercially available credit scores. In particular, column-wise comparisons in Table 5 indicate overall lower model performance for low-income and minority applicants.

We then use our prediction models to test the effect of fitting group-specific models (addressing potential aggregation bias) and re-weighting the training data (addressing potential majority bias). Table 5 shows the results. Across performance metrics (in table panels), sampling or re-weighting strategies (in table sub-panels), and models (in table rows), we find that allowing credit scoring models to fit more flexibly has virtually no effect on precision differentials. In particular, the Different Models sub-panels, where we fit group-specific models, show similar precision differentials as the Baseline sub-panels, both for a random forest (RF) model, an XGBoost model, and a 35-feature logit model. These provide evidence against aggregation bias playing a meaningful role in generating credit score precision disparities.303030The changes in model performance metrics that we calculate from fitting group-specific models are similar to analogous estimates in Fuster et al. (2020); we find these changes are small relative to the the effects of data bias, as shown in the following section. Turning to majority bias, we similarly see in the Re-weight Training Data sub-panels that by re-weighting, which equalizes sample size across groups to undo majority bias, we again produce similar precision differentials as in the Baseline sub-panels. These findings suggest that majority bias is unlikely to account for the credit score precision differentials observed in the data.313131One potential concern is that flexible machine-learning models were already able to re-construct group status from the data and effectively fit the differences in the prediction function. However, we also find no precision gains for a 35-feature logit model, as shown in the Logit rows of the table.

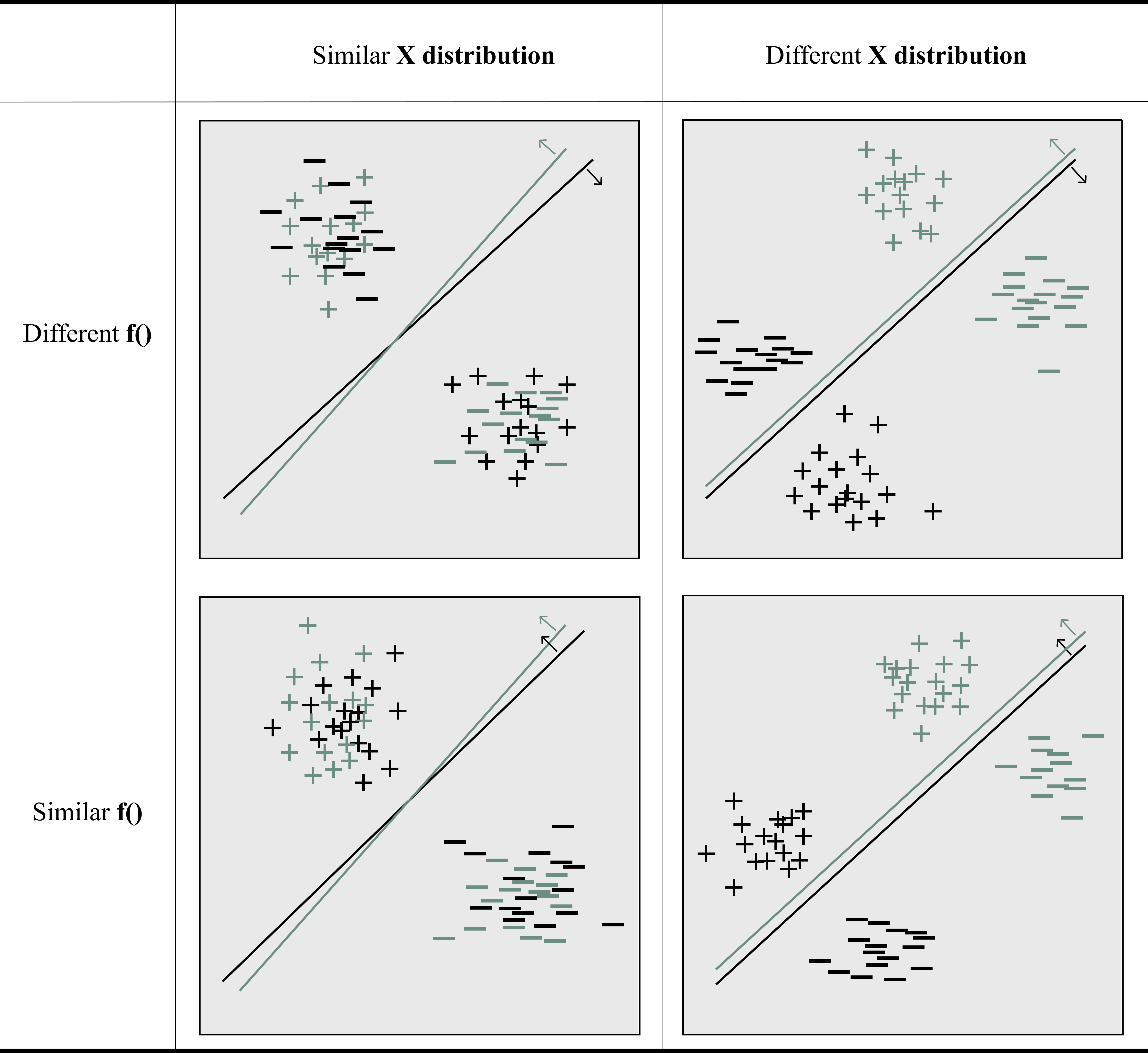

To understand this null result, it is helpful to consider when we would expect training group-specific models to have the largest benefit. Wang et al. (2020) show theoretically that group-specific models (“model-splitting”) yield the largest benefit if both groups have similar joint distribution of predictors but different conditional expectation function (see the top left panel of Figure A.1 in Appendix A). Intuitively, if the two groups have very distinct clustering of predictors, then a sufficiently complex algorithm would likely already have reconstructed group membership (see the bottom right panel of Figure A.1 in Appendix A). Conversely, there is only a benefit to model-splitting if the conditional expectation function differs across groups (see the top right panel of Figure A.1 in Appendix A).

Our finding that model-splitting does not result in precision gains can then be explained either by (i) significant differences in the joint distribution of predictors across groups which are already captured by existing algorithms, or (ii) similar conditional expectation functions across group which make model-splitting unnecessary. There are several reasons why the first explanation is unlikely to apply. If already-reconstructed differences were the main driver of our results, we would expect more complex algorithms, which are presumably better at re-constructing group membership, to feature smaller precision differentials and to have smaller precision gains for the disadvantaged groups when training separate models. In Table A.5 in Appendix A, we show that the machine learning algorithms are in fact better than a logit model at predicting minority and low-income status. However, Table 5 shows that a simple 20-variable logit model has similar precision differences across groups and does not have larger precision gains for disadvantaged groups as we fit separate models. This explanation is also inconsistent with existing work that has found that the variables used in typical credit scoring models do not serve as proxies for race and ethnicity (Avery et al., 2012).

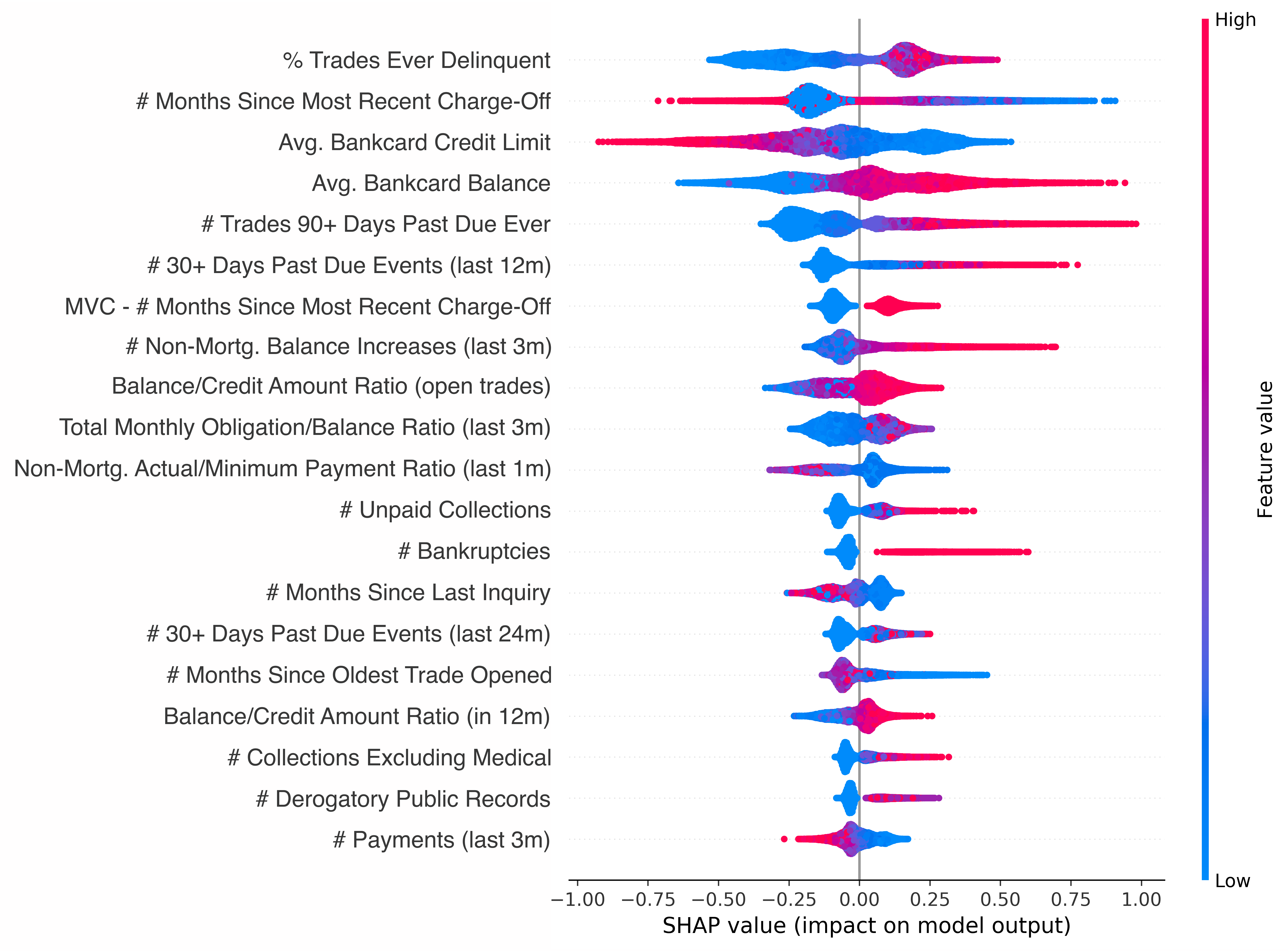

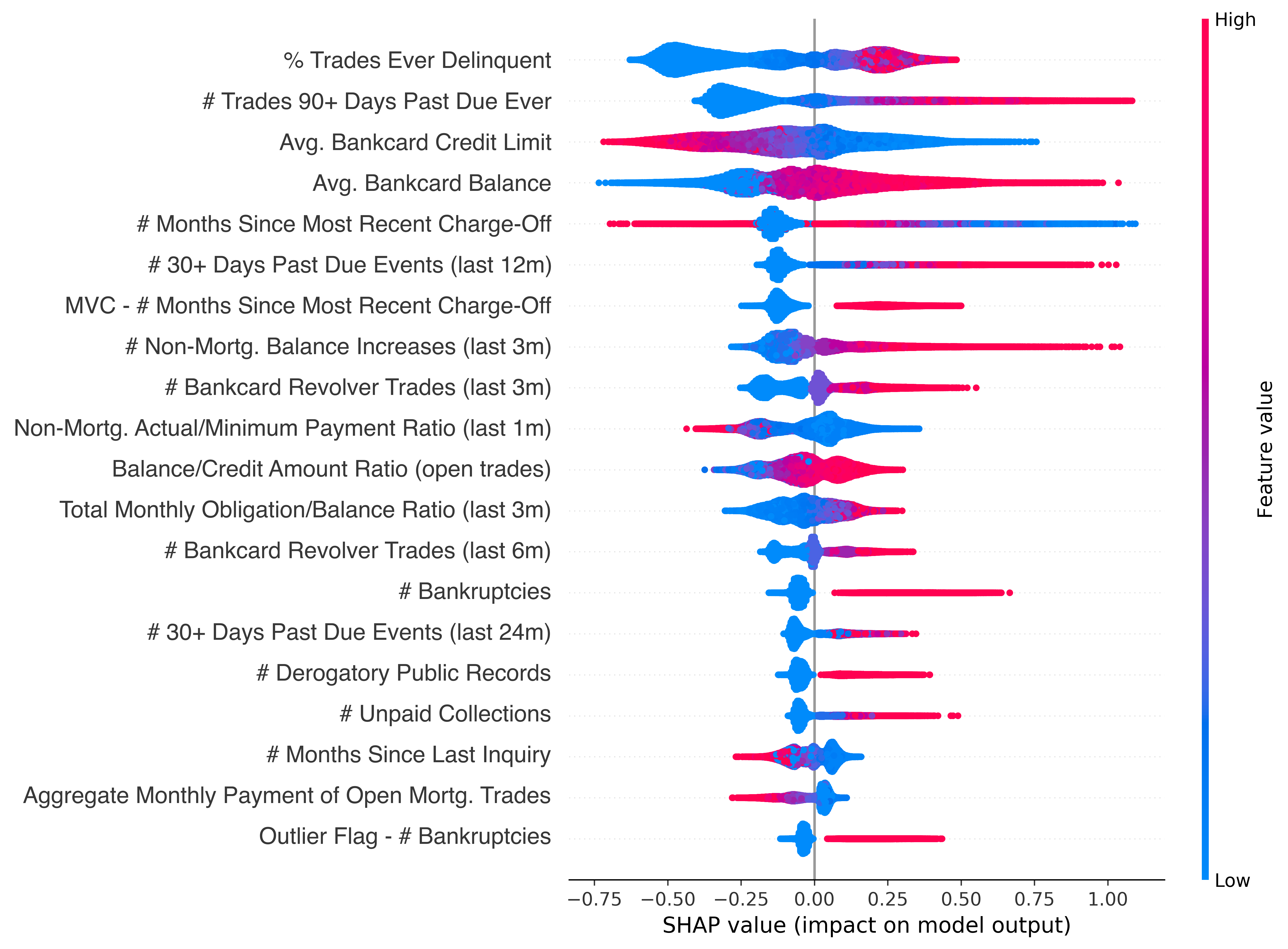

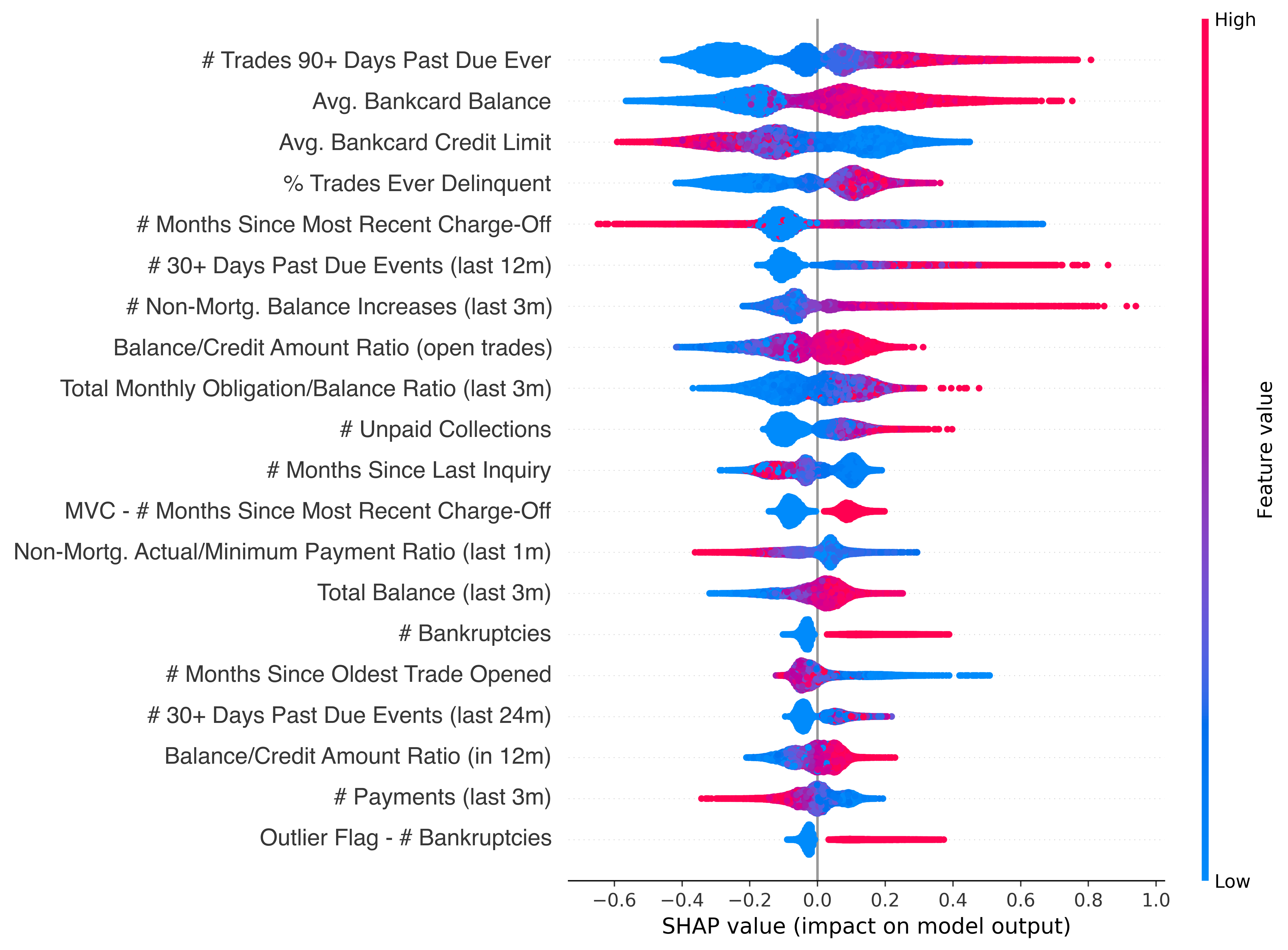

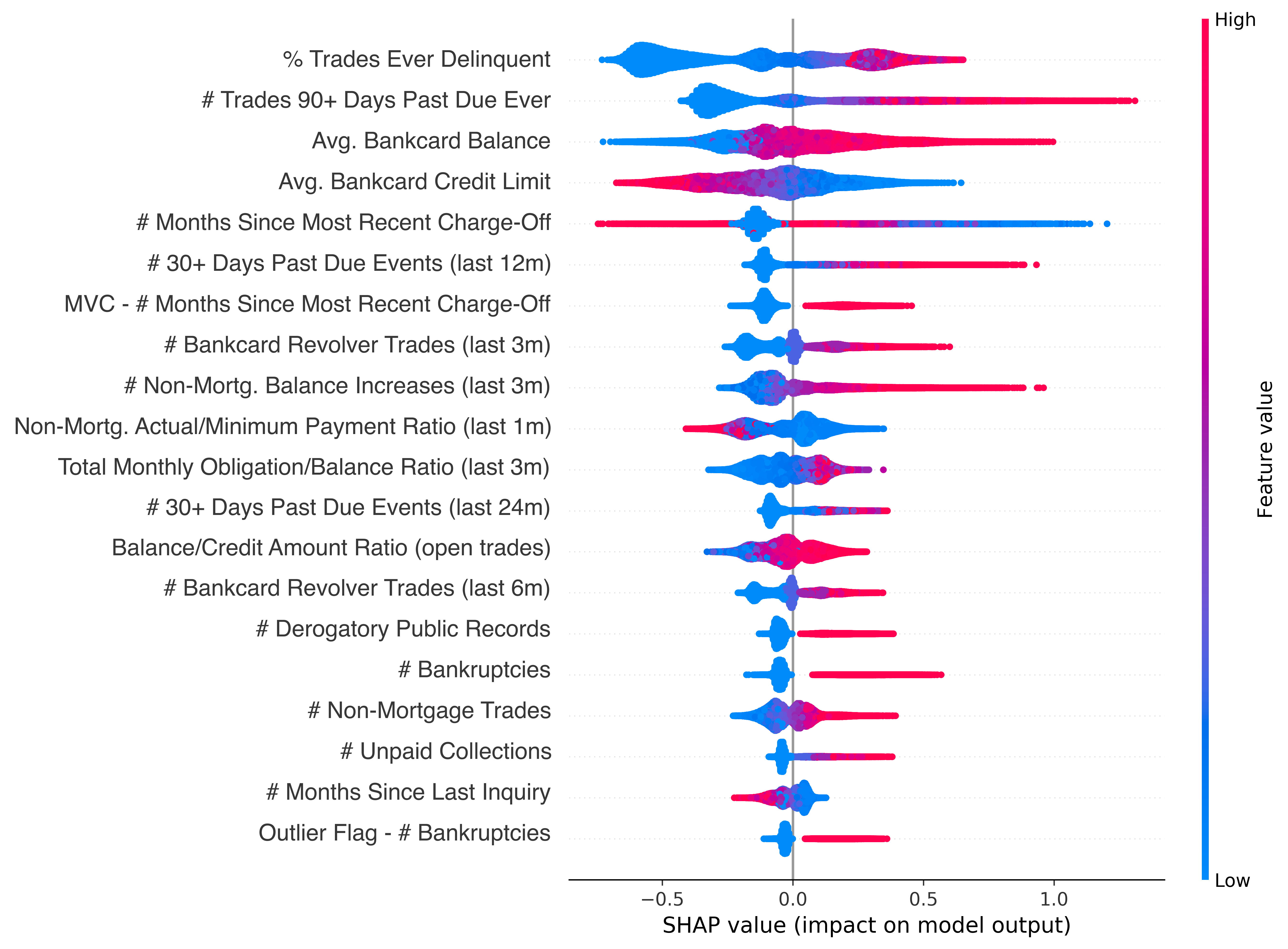

Our findings are instead consistent with the second explanation: conditional expectation functions simply are similar across groups.323232One potential caveat is that the improvement from solving aggregation bias is masked by an overfitting problem that is more acute for the group with the smaller sample size when training separate models (see Wang et al. (2020)). The gain in fitting a group-specific model could be erased by a reduction in performance due to the smaller sample size. However, this overfitting problem should also apply to the non-minority group when we fit separate models with identical samples sizes. As there should be little gain from eliminating aggregation bias, we would expect the overfitting problem to induce a large deterioration in performance for the non-minority group when limiting the sample size to the size of the minority group. The row labeled Different models: Same N of Table 5 shows that we do not observe large drops in performance for the non-minority group suggesting that the overfitting problem is unlikely to be a problem given our sample sizes. This interpretation is supported by Figure 3 which shows variable importance measures (SHAP values) for the models trained separately by group (Lundberg and Lee, 2017). In the figure, variables are sorted from top to bottom in order of average absolute variable importance across consumers, while the distribution of (signed) importance measures across consumers, in the sense of having a positive or negative effect on the predicted probability of default, is shown in each row. The figure shows that the group-specific models rely on similar variables and that these variables play similar roles (in terms of sign and magnitude) in driving the predictive output of the respective models.333333We obtain similar results when comparing coefficients of the logit models trained separately by group.

4.2.2 Data Bias

This section characterizes three forces that drive differences in the informativeness of credit report data: compositional differences; differences in how default is or is not reported to credit bureaus for different groups; and differences in outcome predictability. Of these, we show that compositional differences explain 46%-53% of the informativeness gap across groups. We then find suggestive evidence that reporting differences and differential outcome predictability, for example due to different exposure to future shocks, both help explain the remaining differences.

Compositional Differences

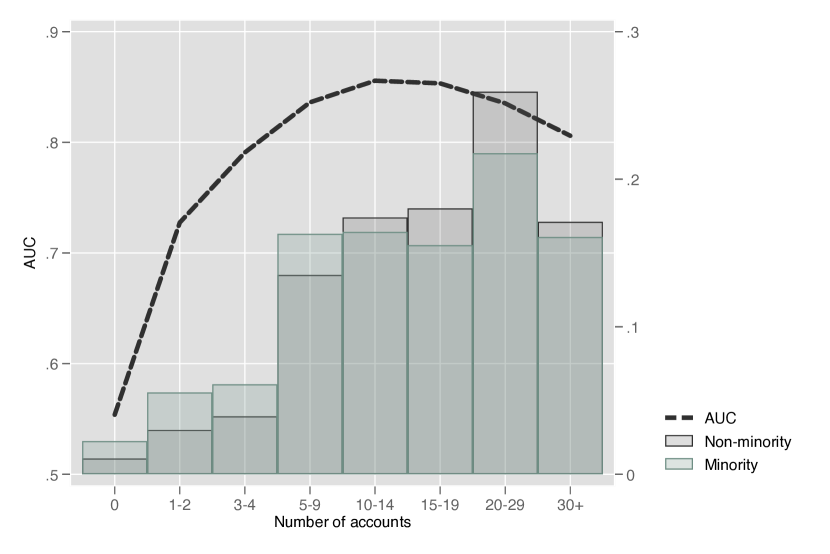

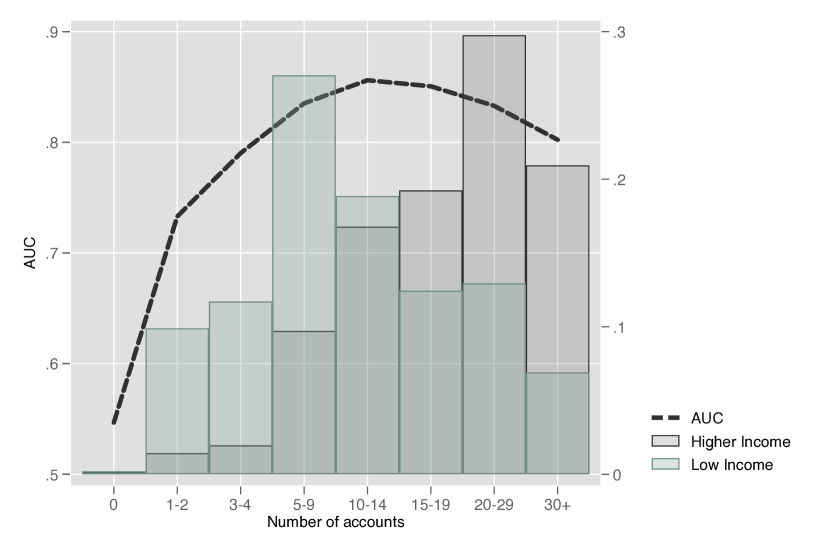

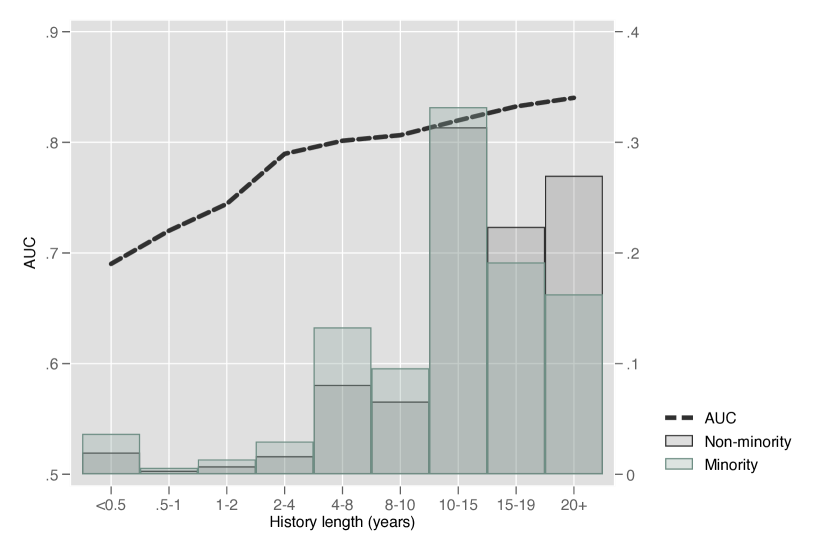

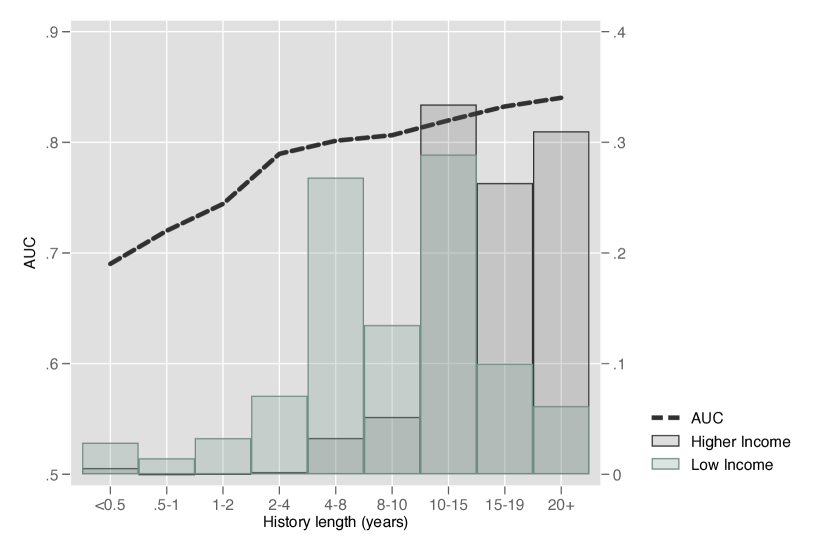

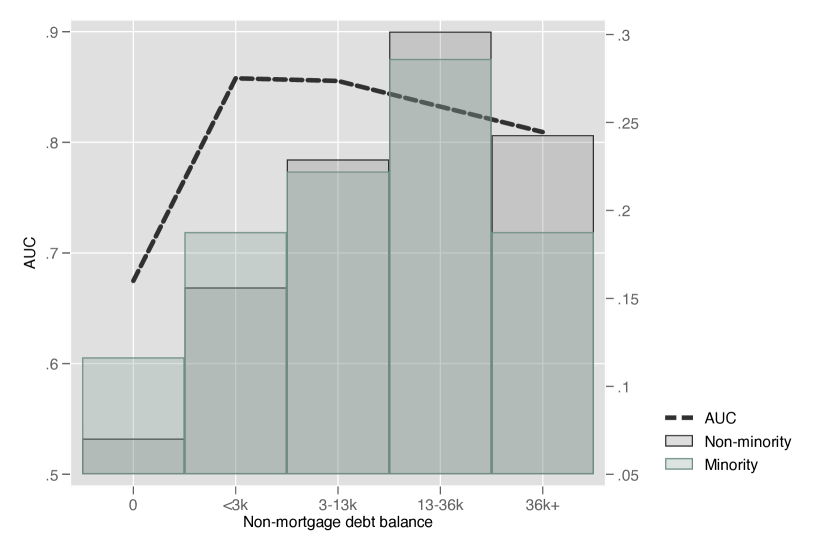

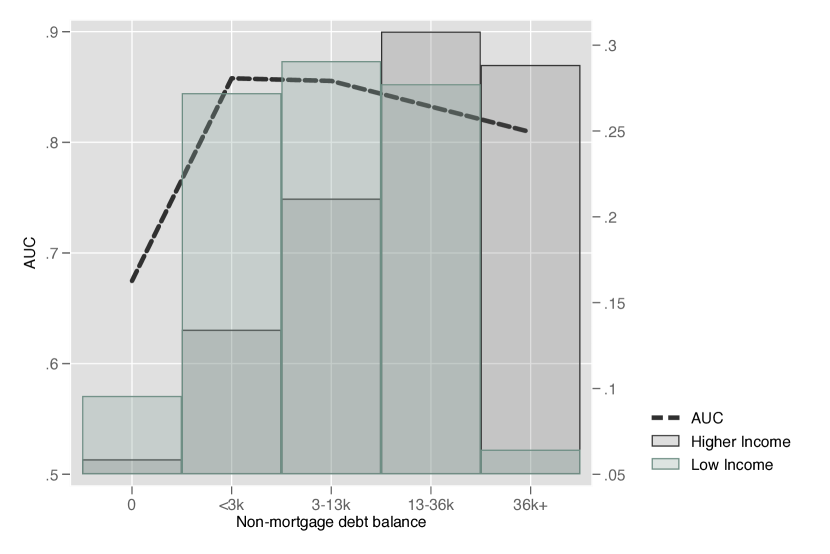

We first investigate whether compositional differences in credit report data can explain the informativeness gap across consumer types. We center our analysis on the five key components of credit report data that are commonly understood to determine credit scores.343434These components are: number of accounts, length of file history, past default history, usage (utilization and balances), and account mix (how many types of accounts a borrower has). Across these components, we show that credit report data are less informative about future default when the data are sparse (e.g., thin or young credit files), “dirty” (e.g., showing past default), or non-diverse (e.g., only holding one type of loan). We then show disadvantaged groups’ credit report data are more likely to be sparse, dirty, and non-diverse. Figure 4 shows the AUC of the VantageScore 3.0 credit score as we condition on various characteristics of credit report data, together with with estimated distributions across these characteristics for different groups. The top two panels of the figure show that “thicker” credit files – those with data from more past or current loans – are associated with higher AUCs, while the distribution of minority (in panel (a)) and low-income (in panel (b)) consumers’ credit report data is skewed toward “thinner” credit files. For example, moving from 1-2 accounts to 10-14 accounts increases the AUC from 0.72 to 0.85, while the share of minority consumers with 1-2 accounts is roughly twice the share for non-minority consumers. Next, panels (c) and (d) show a similar result for history length, or how many years an individual has had a credit report: sparser data are associated with lower AUCs, and disadvantaged groups are more likely to have sparse data.

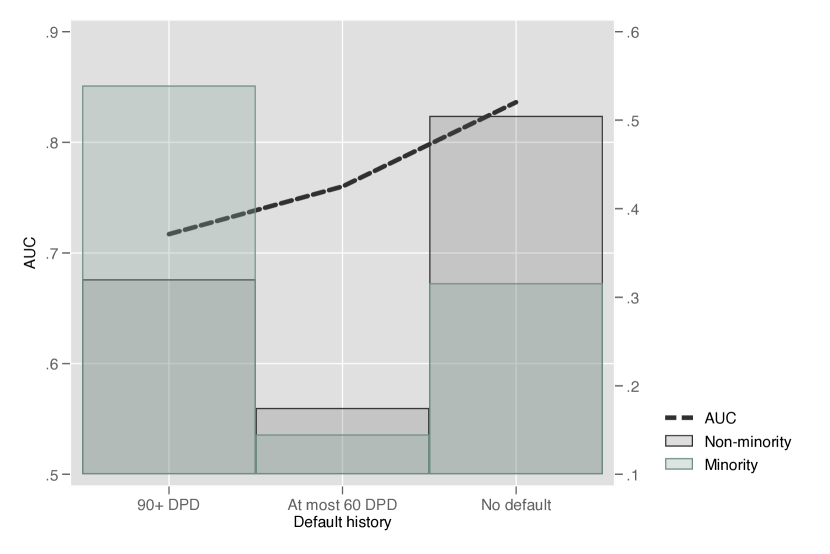

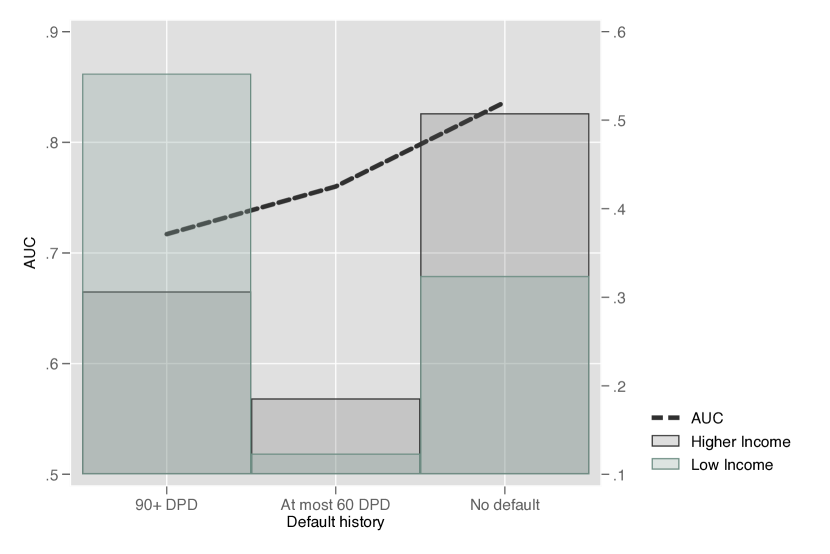

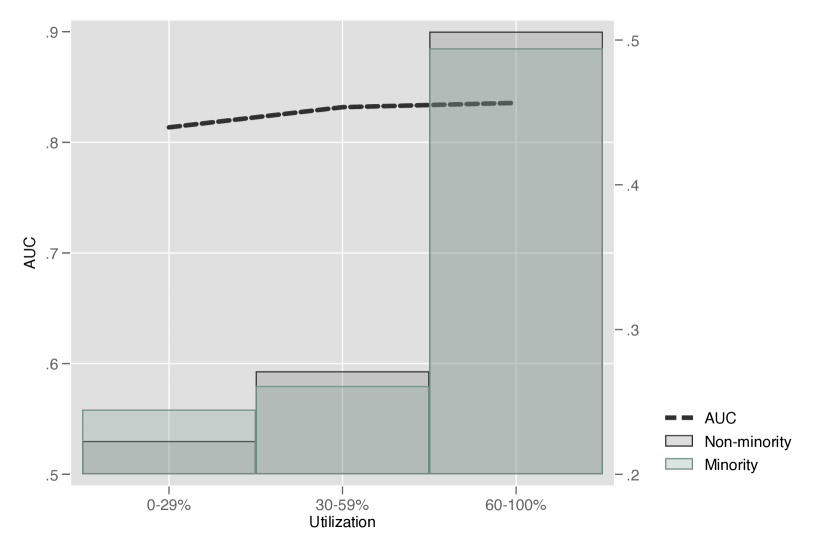

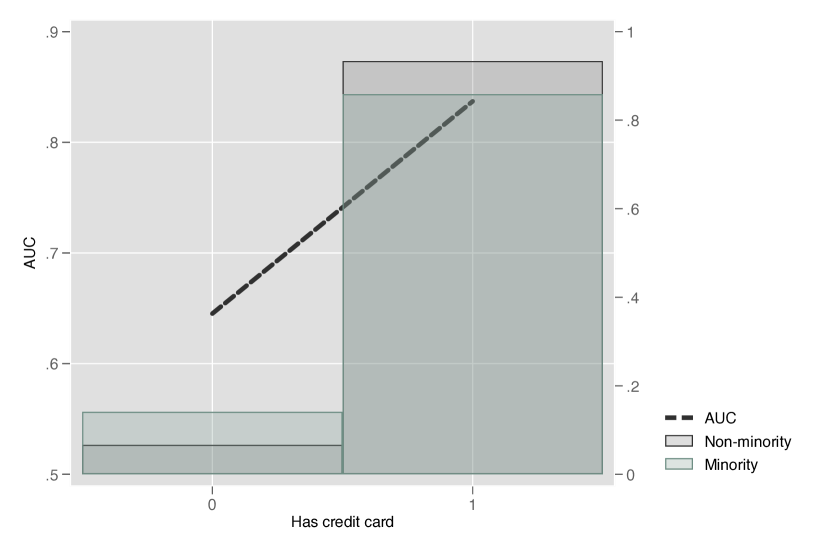

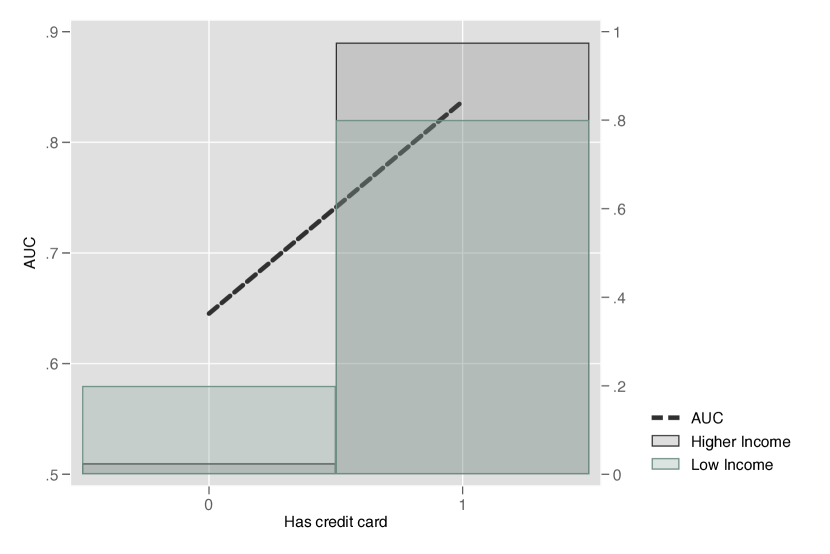

Moving to the bottom half of Figure 4, panels (e) and (f) show that credit files with no past default history (“clean files”) have higher AUCs than those with past default (“dirty files”) and that minority and low-income groups are more likely to have “dirty” files. For example, the average AUC of clean file applicants is 0.82 compared to 0.72 of applicants with a past severe default (90+ days overdue), and minority applicants are roughly twice as likely as non-minority applicants to have a past severe default. Finally, panels (g) and (h) show credit files that include data from at least one mortgage account have higher AUCs than those that do not and that, again, minority and low-income groups are less likely to have a mortgage. Similar evidence for other credit report characteristics is shown in Appendix Figure H.1 for total balances, credit utilization, and the presence of a credit card. Overall, we consistently find that sparse, dirty, and non-diverse credit report data are associated with lower informativeness of credit scores and such data also are substantially more likely to belong to disadvantaged groups.

To quantify the effect of these compositional differences, we present a simple back-of-the-envelope decomposition. We first divide applicants into nine (mutually exclusive) sub-samples that condition on similar default history, account mix, and file thickness – the credit report characteristics associated in the previous figure with the largest AUC differences.353535The nine sub-samples are defined by all pairwise interactions of two triples. The first triple is whether a file is thin (less than nine life-time accounts or less than 10 years of history), or thick (the complement of thin) with no mortgage, or thick with a mortgage. The second triple is whether the file has no default history, mild default history (at most 60 days past due (DPD)), or severe default history (90+ DPD). We can then decompose the overall difference in AUC between groups into differences in each group’s distribution across subsamples, and a residual term that captures differences in AUC within each sub-sample. While this back-of-the-envelope estimate should be interpreted carefully,363636One important caveat to note is that this exercise is a linear approximation to the nonlinear relationship between population-level AUC and sub-population AUCs. A separate caveat is, of course, that some unobservables may be correlated with both credit report data composition and future default outcomes that determine AUCs. Nevertheless, this exercise provides a useful estimate in the spirit of a Kitagawa (Oaxaca-Blinder) decomposition of the importance of group-specific distributions of observables, similar to work that decomposes black-white earnings gaps into the composition of observables and other residual effects (Kitagawa, 1955; Oaxaca, 1973; Blinder, 1973). As we emphasize when we discuss the potential for credit score hysteresis (see e.g. Section 7), noting that these observables explain much of the observed gap should be seen as underscoring, rather than minimizing, the importance of understanding the history that gives rise to these different observables (Spriggs, 2020). it provides a useful quantification of how much compositional differences in credit report data drive the gap in credit score informativeness.

Table 6 shows that 46%-53% of the overall AUC difference is accounted for by the fact that disadvantaged groups are over-represented in sub-samples where credit report data have less predictive power. Concretely, this is calculated by taking the average (not group-specific) AUC in each subsample, and averaging these across sub-samples using the group-specific distributions; for example, in the case of AUC gaps between minority and non-minority applicants considered in panel (a) of the table, this average is .025, which is 46% of the .054 overall gap between groups. The residual term can then be calculated as the unexplained part of the overall gap between groups, or equivalently by taking group-specific AUCs within each subsample and averaging across them using a population-level (not group-specific) distribution across sub-samples. These residual terms capture the other near-half of AUC differences.

Residual Differences

Table 6 also provides important clues as to what drives these residual gaps in predictive power. The residual gap is not uniform across sub-samples but rather is concentrated in sub-samples that have clean files, indicating residual credit score noise is driven by disparities in the data’s ability to predict a consumer’s first observed default.373737This finding – that credit score informativeness is similar across minority and non-minority individuals after conditioning on those that have a history of default – is interestingly consistent with results in Bartik and Nelson (2020), where noise in credit report data is estimated to be similar across groups in a labor market context where employers largely focus on negative information such as past loan default. Credit report data’s predictive power for future loan default and for worker match quality may also just differ due to other differences in these target outcomes or in these markets. Two possible explanations appear most consistent with this pattern: differential measurement error arising from how first defaults are reported to credit bureaus; and second, differences in the inherent predictability of a first-ever default, for example due to differences in groups’ exposure to future shocks.

While prior work has suggested various types of measurement error may be important in this setting,383838For example, Cherry et al. (2021) find that forbearance rates are higher for low income borrowers and in areas with more minority representation. This finding suggests that default outcomes might be differentially under-reported across groups. See also Federal Trade Commission (2013) for other evidence on the prevalence of measurement error. we focus on a particular type of measurement error that our data are uniquely well-suited to study: disadvantaged groups may be more likely to borrow from lenders that do not report defaults to traditional credit bureaus, for example payday lenders.393939For background and related research see e.g. Morse (2011), Bhutta (2014), and Carrell and Zinman (2014). Using linked individual-level data from FactorTrust, a leading alternative credit bureau that covers payday borrowing, we investigate this possibility by including information on payday loan use and default in our predictive models of default, previously described in Section 4.2.1. However, we find that the inclusion of these additional variables does not reduce the across-group differences in credit score informativeness (see Table H.2 in Appendix H).404040This finding is consistent with prior research by Bhutta et al. (2015b) who find that consumers who use alternative credit such as payday loans also tend to be delinquent on traditional credit products; their Table 2 shows the average payday loan applicant is delinquent on more than half of their balances reported to a traditional credit bureau.

Another explanation for the residual differences in informativeness is that available observables are less informative for predicting default for minority or low-income applicants due to differences in the inherent predictability of future default. A long-standing literature finds that minority individuals (Bils, 1985; Shin, 1994; Solon et al., 1994) and low-income individuals (Guvenen et al., 2017; Patterson et al., 2019) have earnings that are more exposed to business-cycle risk. In addition, uninsured idiosyncratic risk may also plausibly vary across groups. At the same time, there is evidence that liquidity constraints play an important role in driving default (Indarte (2020), Ganong and Noel (2020)). Together, these findings imply that more volatile incomes might drive differences in the volatility of default. We find some suggestive evidence consistent with such differences: transition probabilities from no default to default states are higher for low income and minority applicants for clean, but not dirty, credit files (see Table H.1 in Appendix H).

5 A Model of Information in Mortgage Lending

Thus far we have shown two main results: quantifying the differential precision of credit report information across groups, and illustrating the role of data bias rather than modeling bias in generating these differences. We now develop and estimate a model of credit market information to assess the effects of these precision differences on economic efficiency, focusing on the context of the US mortgage market. We then use the model to study counterfactual information structures relevant to potential or ongoing changes in consumer credit markets.

5.1 Setup

We model a lender who receives signals about a borrower’s unobservable type . These signals may include, for example, a credit score, home equity, or soft information gathered through interactions or relationship lending.414141For evidence on the role of soft information in US mortgage lending, see Keys et al. (2012), or Rajan et al. (2015) for the role of hard information not captured by credit scores. We define noise in a standard way relative to the type : for each signal , the signal error is the gap between the signal value and the true type, , such that the noise in a signal is .

We specify that approved loans default with probabilities dependent on borrower types. Risk-neutral lenders make approval decisions based on their posterior belief about a borrower’s type given observed signals and approve loans for which their posterior falls above an approval threshold . This yields profits equal to,

| (1) |

Here the parameters , , and respectively capture non-interest revenue, the present value of interest revenue retained by the lender given net interest rate , and the lender’s exposure to losses from loan default. Meanwhile the marginal cost captures other per-loan variable costs not driven by default. This profit function is relatively general in the mortgage-lending context because it describes both portfolio lending, where the lender fully internalizes interest revenue and default losses, as well as originate-to-distribute and GSE-funded business models, where lenders share revenue and risk externally. See also Bhutta and Hizmo (2020) and Woodward and Hall (2012) for discussions of similar mortgage lender profit functions.424242This profit function also includes flexibility across groups in view of Canay et al. (2020)’s emphasis on how different groups studied in marginal outcome tests may also differ in unobservable dimensions of the signal receiver’s payoff function.

We suppose that posterior beliefs are Bayesian posterior expectations of the applicant’s type, and lenders observe the true distribution of signal noise for each applicant. Using this type of posterior is profit-maximizing for a risk-neutral lender in many settings, including the normal-normal parameterization we develop more below.

5.2 Estimating the Model

We use an empirical analog of this model in order to study a mortgage lender’s problem of which applications to approve given noisy information about default.

To make empirical headway, we suppose that unobserved types for individuals from each applicant group are normally distributed with potentially group-specific mean and inverse variance,

| (2) |

Likewise signal noise is normally distributed with potentially group-specific variance,

| (3) |

Recalling , this structure implies the lender’s Bayesian posterior of each applicant’s type is,

| (4) |

We also map from unobserved types to observable default with default probabilities parameterized as,

| (5) |

We follow the standard parameterization in the credit scoring industry (Thomas, 2009) and suppose that observed credit scores are an affine transformation of a predicted log odds of default,

| (6) |

With these parameterizations in hand, we use a simulated method of moments strategy to estimate the key primitives of the environment: two parameters for each group describing the distribution of unobserved types for that group’s loan applicants, and ; signal noise for each group and for each signal, ; the scalar parameters of the affine mapping from credit report signals to credit scores, and ; and finally the approval threshold for each group.434343Note that the approval threshold can differ across groups even if the profit function is the same across groups, because of non-linearity in will make groups with noisier signals exhibit higher average default for the same posterior . Given the existence of an (unobserved) approval threshold , we do not need to estimate the profit function parameters directly in order to recover these primitives on signal noise, so we postpone profit-function estimation until the counterfactual exercises described in Section 6.6.

We estimate a model with two signals (). We take one of of these two signals to be a credit score, and the other signal to be a composite of all other information available to the lender, which includes factors such as loan-to-value ratios, debt-to-income ratios, soft information, and other information sources potentially unobservable in our data. Combining all non-credit-score signals into a single composite is without loss of generality for i.i.d. signal noise.

To estimate the model primitives, we simulate the following moments and match them to corresponding empirical moments for each group: loan approval rates; the mean of credit scores among accepted applicants; the mean of credit scores among rejected applicants; the slope of default outcomes with respect to credit scores among approved loans; the slope of the “reverse regression” of scores on default outcomes; default rates among approved applicants; and the default rate of marginally approved loans. This final moment corresponds to the expectation .

The model is transparently identified off of the target moments. First, the forward and “reverse” regression slopes between credit scores and default realizations help identify the amount of signal noise in credit scores, similar to how reverse regressions can be used to test for measurement error (Black et al., 2000). Intuitively, the same attenuation in regression coefficients that we showed as evidence of credit score noise in Section 3.2 is used in model estimation to identify how much noise there is, quantified in terms of the variance of terms in a credit score signal.

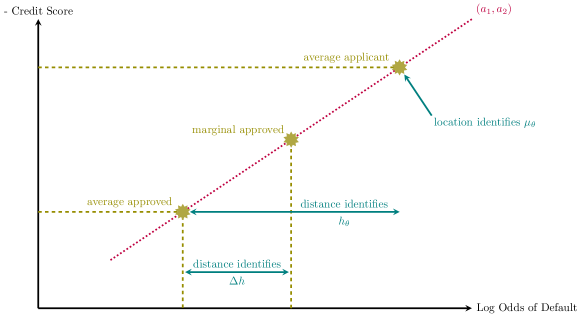

To further illustrate how our empirical moments identify model parameters, Figure 5 shows visually how we identify other key parameters of interest: the mean and variance of the unobserved risk distribution, and the total precision of all signals available about a given applicant, summed across the credit score signal and other, non-score signals. This “total precision” measure, denoted , is the sum of the model parameters that describe the precision of the credit score and non-score signals ().

In the figure, the gold stars and dashed gold lines denote moments that we can observe, corresponding to average applicants, marginally approved applicants, and average approved applicants. Moments for these subgroups of applicants can be observed either in terms of their credit score, or in terms of their default outcomes, or both, with the two axes of the figure corresponding to these two types of observables. The dashed gold lines in the figure then illustrate which types of observables are available for which subgroups. For example, default for non-approved applicants is not observed, but credit score is. Connecting these two types of observables, the dotted red line illustrates the affine mapping to be estimated between the x- and y-axis outcomes.

Based on those empirical moments illustrated in the figure, the blue-colored labels then illustrate how these moments identify model parameters. It is straightforward that the location of the average applicant in this figure identifies the average applicant type, . Conditional on other parameters, the distance between approved and rejected applicants then reveals how much dispersion there is in unobserved risk types. Finally, the difference between average and marginally approved applicants in terms of default odds reveals, conditional on an observed approval rate and the dispersion of risk types, how much information is conveyed by all available signals about default risk. Intuitively, if very little information were available to lenders about mortgage applicants, then lender posteriors would be minimally diffuse, and, holding fixed a given approval rate, marginally approved borrowers would be minimally different from average approved borrowers. Conversely (but again holding fixed the approval rate), when marginally approved and average borrowers are more different from each other in terms of default outcomes, this reveals that the available signals are more informative about borrower types.

6 Model Estimation and Results

6.1 Construction of the Instrument

Important in our model estimation is the ability to identify the characteristics of marginally approved mortgage applicants; this is the moment described in Section 5.2. We use the idiosyncratic timing of Community Reinvestment Act (CRA) exams as an instrumental variable to obtain exogenous variation in the approval leniency of banks, such that the local average treatment effect in a two-stage least squares regression reveals the characteristics of the marginally approved.444444Focus on marginal applicants in credit and labor markets has a long tradition dating back at least to Becker (1957). For a recent application of an IV strategy to identify characteristics of marginal loan applicants, see Dobbie et al. (2019).

The Community Reinvestment Act, passed in 1977, directs federal banking regulators “to encourage insured depository institutions to help meet credit needs of all segments of their local communities” (Federal Reserve Board, 2018a). The Federal Reserve, FDIC, and the OCC conduct exams at regular intervals to evaluate whether lenders comply with the CRA lending requirements. Unsatisfactory CRA exams can be grounds for the regulator to deny applications for mergers and acquisitions or the opening of new branches.

Compliance is measured in loan quantity (not in terms of the interest rates changed on the loans). Two types of loans satisfy the CRA requirements: first, any loans made in low- and moderate-income areas where the bank has a physical branch and takes deposits, or made in moderate-income areas deemed depressed or under-served by banking regulators (“CRA-eligible census tracts”); second, lending to low- and moderate-income individuals in any area regardless of area-average income.

We construct the CRA instrument following Agarwal et al. (2012) and consider a twelve-month window prior to and during a lender’s CRA exam. These exams occur at fixed intervals – every five (resp. two) years for banks with assets under (resp. over) $250 million – and therefore, as argued by Agarwal et al. (2012), the timing of these exams is likely unrelated to local economic conditions and, in particular for our setting, credit demand and credit risk.454545Foote et al. (2013) argue that the regulator would also take into consideration loans originated long before the three-quarters prior to an exam. This makes it potentially challenging to evaluate the CRA program (Agarwal et al., 2012). Unlike Agarwal et al. (2012), we just require that the CRA increased leniency in the time window relative to non-examined banks. Other work examining channels through which the CRA can incentivize mortgage lending includes, for example, Avery and Brevoort (2015); Bhutta et al. (2015a); Bhutta (2011); Ringo (2017); Avery et al. (2005).

To establish that our instrument affects origination, we estimate the following first stage in a half-year () - treatment geography () - bank () panel, separately by observable borrower groups :

| (7) | ||||

where is the quantity of loans originated, is a bank-geography fixed effect for group and is a geography-quarter fixed effect for group . We weight by the bank’s origination share in a given geography, and standard errors are clustered at the geography level.

Geographies are defined by measuring CRA eligibility at the Census-tract level, and then pooling tracts within county that have the same CRA eligibility status across years. Hence our treatment geography is essentially a partition of a county that is defined using tract-level CRA eligibility. This results in a relatively fine level of geography fixed effects, including thousands of sub-county-specific partitions across the US. Given these fixed effects, our first stage regressions are identified off of within-geography-time variation and within-lender variation by comparing lenders that are and are not subject to a CRA exam at a particular place and time.

We define a CRA-eligible tract using low- and moderate-income status relative to area median income as defined by the FFIEC.464646We focus on CRA-eligible tracts that are eligible by virtue of their income level, rather than higher-income tracts deemed distressed or under-served in a given year; by doing so we focus on the vast majority of loans made in CRA-eligible tracts. We find that the CRA instrument is strongest within CRA-eligible tracts, so we limit our estimation to treatment geographies that are CRA-eligible throughout our sample period.

Because refinance loans constitute the bulk of all mortgage loans, we focus on refinance loans in our main results.474747Results for purchase loans are available upon request. The institutional details of the refinancing market also make our instrument and estimates more straightforward to interpret for refinance loans than for purchase loans: the much smaller market share of FHA and VA loans among refinances means that there are fewer margins of adjustment for lenders in response to the instrument, and smaller effective choice sets of borrowers; we discuss this choice in the context of the standard IV monotonicity assumption more in the following section.

6.2 Instrument validity

Our identification assumption is that a CRA exam affects origination only through the increased leniency of the lender. The exclusion restriction would be violated if there are other time trends coinciding with the CRA examinations driving loan demand specific to the examined lenders. Including geography-time and bank-geography fixed effects helps to address these concerns. Additional loan-level controls are only required if we believe that the instrument is only valid conditional on these additional controls; we view this as unlikely, given how the bank-specific timing of CRA exams is set independently of local market conditions.

We see three reasons why a bank may choose to defer CRA-eligible lending until just before an exam. First, CRA-induced lending involves, almost by definition, loans that have lower-NPV than other loans for the bank: these are the marginal loans the bank is only induced to make because of the CRA restrictions. Making these lower NPV loans as late as possible – just before an exam – therefore maximizes overall value for the bank. Second, there may be option value in delaying CRA lending, as the bank potentially will issue sufficient CRA-eligible loans without needing to change its approval leniency. Third, there may be behavioral or agency frictions that make it difficult to incentivize loan officers to make CRA-eligible loans, which may result in under-production of CRA loans that the bank has to correct for just before its exam.