Fast Randomized Numerical Rank Estimation for Numerically Low-Rank Matrices

Abstract

Matrices with low-rank structure are ubiquitous in scientific computing. Choosing an appropriate rank is a key step in many computational algorithms that exploit low-rank structure. However, estimating the rank has been done largely in an ad-hoc fashion in large-scale settings. In this work we develop a randomized algorithm for estimating the numerical rank of a (numerically low-rank) matrix. The algorithm is based on sketching the matrix with random matrices from both left and right; the key fact is that with high probability, the sketches preserve the orders of magnitude of the leading singular values. We prove a result on the accuracy of the sketched singular values and show that gaps in the spectrum are detected. For an matrix of numerical rank , the algorithm runs with complexity , or less for structured matrices. The steps in the algorithm are required as a part of many low-rank algorithms, so the additional work required to estimate the rank can be even smaller in practice. Numerical experiments illustrate the speed and robustness of our rank estimator.

keywords:

Rank estimation , numerical rank , randomized algorithm , Marčenko-Pastur ruleMSC:

[2020] 65F55, 65F99 , 68W20 , 60B201 Introduction

Low-rank matrices are ubiquitous in scientific computing and data science. Sometimes a matrix of interest can be shown to be of numerically low rank [6, 45], for example by showing that the singular values decay rapidly. More often, matrices that arise in applications may have a hidden low-rank structure, such as low-rank off-diagonal blocks [30, 32]. As is well known, low-rank approximation is also the basis for principal component analysis.

Numerous studies and computational algorithms exploit the (approximately) low-rank structure of these types of matrices to devise efficient algorithms. Such algorithms usually require finding a low-rank approximation of a given matrix. For large-scale matrices, traditional deterministic algorithms for low-rank approximation based on computing a truncated singular value decomposition (SVD) might be infeasible. This can be caused by the sheer scale of the matrix and the complexity of classical algorithms, as well as the fact that access to the matrix may be restricted because it is stored in RAM or cannot be stored at all (streaming model) [32]. Randomized algorithms have become a powerful and reliable tool for efficiently computing a near-best low-rank approximation for such matrices. Landmark references on randomized low-rank factorizations are [48] and [19], which extensively analyze the randomized SVD.

A key step in low-rank algorithms, including randomized SVD, is the determination of the numerical rank (based on the spectral norm). For instance, a variety of low-rank factorization techniques require the target rank of the factorization as input information. Once a low-rank approximation of the specified target rank has been computed, a posteriori estimation of the error via a small number of matrix-vector multiplications [32] is a reliable means of checking if the input rank was sufficient. If was too low, one would need to sample the matrix with more vectors. This clearly requires more computational work, and can be a major difficulty in the streaming model, wherein revisiting the matrix is impossible [41]. Conversely, if the input rank was too high, the computational cost of computing would be higher than it could be. Having a fast and reliable rank estimator is therefore highly desirable.

In this work we propose and analyze a fast randomized algorithm for estimating the numerical rank of an approximately low-rank matrix or . The algorithm is based on sketching both the column as well as the row space of , forming , where and are random (subspace embedding) matrices. The key idea is that with high probability, the singular values of are good estimates of the (leading) singular values of . Therefore the decay of can be reliably estimated by the decay of . To estimate we once again sketch to obtain the much smaller matrix ; it is only (or their estimates) that we actually need to compute. It is noteworthy that in the algorithm it is only necessary to view to matrix once. Furthermore, since we obtain estimates for the leading singular values , we will be able to detect a gap in the spectrum of and hence have the possibility of setting a tolerance for the numerical rank in a data-driven manner.

To our knowledge, the fact that a sketch of the form preserves ‘some coarse spectral structure’ was first noted in [1]. We use techniques similar to their proofs for our theoretical results. Related results for the bulk of the eigenvalues of were first obtained in [17]. The main theoretical contributions of this work, deterministic and probabilistic bounds on the accuracy of as estimates for , build on these results. In particular, we provide a tighter lower bound on relevant for small singular values of .

The complexity of our algorithm is for dense matrices, and can be lower if has structure that can be exploited for computing the sketches and . This is clearly a subcubic complexity (assuming ), and it runs significantly faster than computing the full SVD. Moreover, in many cases, computing (which is usually the dominant part of our rank estimation algorithm) is a required part of the main algorithm (e.g. randomized SVD); and in some algorithms [11, 36] this is true even of . In such cases, the additional work needed for estimating the rank is therefore significantly smaller, such as or sometimes even . Our algorithm is competitive when the target rank is much smaller than the dimensions of the matrix.

In particular, for the widely used randomized SVD we argue that it is computationally efficient to compute and its singular values, after having computed a sketch . The reason is that will provide information on how appropriate the size of the sketch is. Subsequently, more columns can be added or columns can be removed before computing a QR decomposition and computing the product . This will save computational cost in either case: an unnecessary large sketch, or a sketch of insufficiently large dimension. We also introduce an algorithm that combines the rank estimation algorithm with randomized SVD, using the information provided by .

Notation. Unless specified otherwise, is an matrix where . The th largest singular value of is denoted by , and we furthermore use and for the largest and smallest singular values respectively. We use to denote the spectral norm , and is the Frobenius norm. denotes the field, in our case or . The numerical rank estimate will be denoted by .

Throughout the paper we use and for random oblivious subspace embedding matrices, such that with high probability, for any fixed with orthonormal columns we have and for some . We use , and to refer to the size of embedding matrices, which must be at least the number of columns in . The matrix is required to have more columns than , and the same goes for the rows of . For brevity we simply call such and embedding matrices.

The analysis will be specified to Gaussian or subsampled randomized trigonometric transform (SRTT) [32] embedding matrices at times. We will use , where , to denote a matrix where each entry is iid distributed and call this matrix a real (standard) Gaussian matrix. In case of , denotes a complex Gaussian matrix with iid entries. That is, and independent. A Gaussian matrix can be scaled to an embedding matrix by defining (in both the real and complex case); we call the scaled Gaussian matrices Gaussian embedding matrices. SRTT matrices are defined in Section 3.3 and as the scaling is included in the definition, they are naturally embedding matrices. We will use to denote an SRTT matrix.

1.1 Numerical rank and goal of a rank estimator

So far we have been using the term “the numerical rank” informally. Let us now define the notion. This is a standard definition, see for example [6].

Definition 1.

Let . The -rank of , denoted by , is the integer111If no such exists, we take ; however, in this paper we are never interested in this full-rank case. We also note that MATLAB’s rank function takes the absolute -rank, i.e., for a user-specified tolerance . such that .

We adopt the relative -rank definition as it is a natural choice in the context of low-rank matrix approximation. One could easily adapt the algorithm presented to estimate the absolute -rank. Let us discuss what the goal of a rank estimator should be. One natural answer of course is that the estimator should output given and the (user-defined) relative threshold . However, we argue that the situation is more benign: consider, for example, a matrix with and singular values , five singular values in , five more in , and the remaining are . What should the estimator output? Is it crucial that the “correct” value is identified?

In this paper we take the view that the goal of the rank estimator is to find a good -rank, not necessary the -rank. In the example above, any number between and would be an acceptable output. In most applications that we are aware of (including low-rank approximation, regularized linear systems, etc), there is little to no harm in choosing a rank : a slight overestimate usually results in slightly more computational work, whereas a slight underestimate is fine if , that is, a rank- matrix can approximate to relative -accuracy.

On the other hand, it is clearly not acceptable if the rank is unduly underestimated in that . It is also unacceptable if . The goal in this paper is to devise an algorithm that efficiently and reliably finds an such that

-

•

(say, ): is not a severe underestimate, and

-

•

(say, ): is not a severe overestimate.

Any such is sensible in that there exists a rank- approximation of with relative accuracy, and is not much larger than the best possible for the accuracy required. In addition, the nature of randomized algorithms means that the user must be willing to accept results that do not hold precisely and that small inaccuracies in the results are acceptable. As a result, we assume one is not looking for the exact numerical rank, but an order-of-magnitude estimate. Our rank estimate will satisfy these conditions with high probability. In particular, in situations where the numerical rank is clearly defined, i.e., if a clear gap is present in the spectrum , the algorithm will reliably find the exact rank .

Additionally, in situations where it is unknown whether the matrix is low-rank approximable, our rank estimator can tell us (roughly) how well can be approximated with a low-rank matrix. Similarly, if it is unknown what a suitable tolerance would be and/or the user would like to detect a gap in the spectrum, the algorithm can be used to plot an estimated spectrum and detect gaps.

This paper is organized as follows. Section 2 discusses related studies in the literature. In Section 3 we show that gives useful information about for leading values of . Then in Section 4 we show that can be estimated via . Section 5 summarizes the overall rank estimation algorithm. Numerical experiments are presented in Section 6.

2 Related work

2.1 Existing methods for numerical rank estimation

At the core of numerical rank estimation lies singular value estimation; specifically, the rank can be found by counting the number of singular values greater than the tolerance . The most direct way to do this is to explicitly compute the singular values of a matrix. However, as is well known, this requires operations for an matrix [18], and for large matrices this is computationally inadmissible. Another point of view, specifically for Hermitian matrices, is that a numerical rank estimate can follow from estimating the density of states (DOS). The DOS can be interpreted as a probability density function describing the position of the eigenvalues, and can be estimated with algorithms analyzed in [27].

Regarding fast algorithms that can run with subcubic complexity, the literature on rank estimation appears rather scant. Exceptions include the work of Ubaru and Saad [42], Ubaru, Saad and Seghouane [43], Zhang, Wainwright and Jordan [50] and Di Napoli, Polizzi and Saad [14]. These works are all concerned with counting the number of eigenvalues in a certain interval for a Hermitian matrix. Alternatively, [10] discusses an algorithm for computing the exact rank of a matrix.

The first two references [42, 43] employ the idea of density of states (DOS). In [42], the authors use the DOS to locate a gap in the spectrum, derive an appropriate tolerance and subsequently use polynomial approximation and stochastic trace estimation to count the number of eigenvalues greater than the tolerance. Computationally, the algorithm only requires matrix-vector products with but consequently also requires many views of . In the second paper [43], the authors also first estimate the DOS to locate a gap and then estimate the integral of the DOS. We compare against these algorithms in the numerical experiments, although they need to be adjusted slightly to account for matrices that are not symmetric positive semi-definite. An advantage of both methods is that the entire spectrum is estimated, however they require many more views of the matrix than most randomized methods. The results are discussed in Section 6.3. The works [50] and [14] are similar in spirit. The first focuses on minimizing communication cost involved with rank estimation in a distributed setting, the second approximates an eigenvalue count using polynomial and rational approximation filtering.

As for more theoretical contributions, much of this work builds upon Andoni and Nguyễn [1], which is to the best of the authors’ knowledge the first work that shows rank can be estimated via sketches. The work is focused on estimating eigenvalues of Hermitian matrices via the sketch , but also considers the singular values of non-symmetric matrices using . While Andoni and Nugyen work with the Gram matrix of the sketch, obtaining results in terms of the difference of the squared singular values (or via the Jordan-Wieldant matrix, which is larger), we work with directly. Moreover, their work is of a theoretical nature, and do not present a concrete algorithm for estimating the rank. They also state results that only come with relatively low probability guarantees, although it is possible to take a larger sample to improve the probability.

Here we introduce precise algorithms (also for low-rank approximation), show numerical experiments, and phrase our results in terms of popular embedding matrices allowing for results that hold with exponentially small failure probability.

2.2 Related work in statistics

Rank estimation, or singular value estimation, is a well-known problem in the context of covariance matrix estimation or PCA in statistics, or the detection of signals in signal processing. Most rank estimation algorithms in this context require computing an SVD or eigendecomposition; exceptions include [44]. Since we consider a context where computing these decompositions exactly is not computationally feasible, we do not take this into account.

The statistics literature is connected to this work in yet another way: relating the singular values of the sketch to the singular values of is equivalent to the problem of covariance matrix estimation. This can be seen as follows: let be the SVD of and note the singular values of are the same as the singular values of , where is a Gaussian embedding matrix. The columns of can be viewed as scaled observations from an -dimensional distribution. As the number of observations tends to infinity, the singular values of the ’data matrix’ tend to the singular values of . Estimation of (approximately) low-rank covariance matrix is studied in, among others, [46, 47, 23] and has a clear relation to PCA.

One specific related example in the statistics literature that is well studied is the spiked covariance matrix model, introduced by Johnstone [21] and analyzed by, among others, Bai and Silverstein [4], Nadler [35] and Rao et al. [37]. We find that the theory in these works cannot be applied in our context, since the tail of the singular values in this model is very heavy. In the general context of covariance matrix estimation, various authors have suggested different manipulations to the sample covariance matrix or its eigenvalues to improve the estimator, known as shrinkage. See, for instance, the work by Ledoit and Wolf on linear shrinkage [24], nonlinear computational shrinkage [25] and nonlinear analytical shrinkage [26], or by El Karoui based on random matrix theory [16]. Our numerical experiments suggest these methods are either inefficient for large-scale matrices or unsuitable for numerically low-rank matrices, and we do not discuss them further.

2.3 Related algorithms in (randomized) numerical linear algebra

A number of recent papers focus on randomized algorithms to perform numerical linear algebra tasks on large matrices. Specifically, randomized algorithms for either full or low-rank matrix factorization are of interest in the discussion of numerical rank estimation. This relevance is two-fold, as a numerical rank estimate can be a natural consequence of a factorization. In other cases, an a priori rank estimate can aid in performing a (low-rank) factorization.

The former is the case for rank-revealing full factorizations, such as rank-revealing QR decompositions [15] or UTV factorizations [31]. Full factorizations are (relatively speaking) most useful when the -rank is not much smaller than the matrix dimensions, and still require cubic complexity. As we mainly consider the case where , we focus on methods that have subcubic complexity.

A number of randomized algorithms for a low-rank factorization have been proposed and they can often be modified to yield a (rank ) QB factorization: , where is a matrix with orthonormal columns and is a short and fat matrix. Singular value estimates can then be obtained by computing the exact singular values of , which in turn leads to a numerical rank estimate. Within randomized algorithms for QB factorizations, we can distinguish between (adaptive) algorithms that focus on solving the fixed-precision problem and non-adaptive algorithms that focus on the fixed-rank problem.

The fixed-precision problem can be summarised as: find such that . Adaptive algorithms for this problem include the adaptive randomized range finder [19], the incremental rangefinder [32], RandQB_b [29] and RandQB_EI [49]. The fixed-precision problem is discussed in more detail in Section 6.4.

Conversely, the fixed-rank problem is: find of exact rank such that is as small as possible. One of the most well-known algorithms in randomized fixed-rank factorization is randomized rangefinder [19], which is a core part of the randomized SVD algorithm proposed in [19].

We discuss these algorithms further, comparing with our algorithm, in Sections 5–6, to demonstrate that our algorithm is much more efficient for rank estimation, and can often be used as a convenient preprocessing step for a low-rank approximation algorithm to determine the input rank.

Conversely, a numerical rank estimate can aid the factorization process. This is discussed in detail in Section 6.4 and forms the basis for a non-adaptive low-rank factorization algorithm we propose for the fixed-precision problem.

3 Sketching roughly preserves singular values: for leading

In this section we show that if a matrix has low numerical rank, then sketching preserves its leading singular values sufficiently well to provide an estimate for its numerical rank. Again drawing the connection to sample covariance matrix estimation, it is intuitive that it should be difficult, if not impossible, to obtain information about an -dimensional distribution using only samples, when . Clearly, there are singular values (or signals) we cannot detect, but it is also not clear why the singular values we estimate would be any good. One way to think about this is to see that lies close to a low-dimensional subspace, since is approximately low-rank. This makes it more intuitive why a small sample size could suffice to retrieve a reasonably accurate approximation of (see also [46, Sec. 9.2.3]).

We make the connection between the low-rank structure of and our ability to estimate its singular values using explicit with the deterministic and probabilistic error bounds on the ratio . The analysis will focus on Gaussian matrices. As explained before, denotes a Gaussian matrix with iid () or () entries, and a Gaussian embedding matrix will be of the form . We start from the unscaled sketch . Let be the SVD of and decompose this further to , where contains the leading singular vectors of . Now decompose as

| (1) |

where is and and are independent Gaussian matrices. Define and . We start with the following result, which examines the relation between and .

Lemma 2.

Let and . Decompose as in (1). Then, for ,

| (2) |

where is an matrix consisting of the first rows of , and is the matrix of the last rows of . Furthermore, if is a Gaussian matrix, then for each , the random matrices , , and are independent Gaussian in .

Proof.

The proof consists of establishing the identities

| (3) | ||||

| (4) |

for .

It is immediate from the definitions of and that . As a result, we have by Weyl’s theorem, for ,

| (5) |

The upper bound follows from observing . The lower bound is immediate.

We use the interlacing property of singular values to show (4). For a square matrix , let denote a submatrix of obtained by deleting any columns. Then [33]

| (6) |

First, notice the upper bound (4) is trivial for . For , partition as

where and are diagonal matrices which contain the singular values of . We then have

where we applied (6) with and for the first inequality. Similarly, for the lower bound and , consider the partition

where now is and is . We have

The lower bound is immediate for .

If is Gaussian, its orthogonal invariance implies is also Gaussian. Since , , and are submatrices of this matrix with no overlap for a fixed , it immediately follows that they are Gaussian and independent. ∎

It is worth noting that (2) holds without the assumption that is Gaussian.

Lemma 2 motivates us to look at the singular values of independent Gaussian matrices , and . To this end we use two classic results from random matrix theory to derive probabilistic bounds on the expected error and on the failure probability.

Theorem 3 (Marčenko and Pastur [28], Davidson and Szarek [13], Aubrun and Szarek [2]).

Let be a standard Gaussian matrix with . Then

| (7) |

Furthermore, for every one has

| (8) |

Let be a complex Gaussian matrix with . Then, for every one has

| (9) |

Furthermore, for every ,

| (10) |

A useful way to interpret these results in simple terms is that rectangular random (Gaussian) matrices with aspect ratio are well-conditioned, with singular values supported in . We note that (7), which follows from the Marčenko and Pastur rule [28], holds more generally for random matrices with iid entries with mean 0 and variance 1. The second pair of bounds (8) do not generally hold for other random matrices, see [39] for details. As far as the authors are aware, there does not exist a lower bound on the expectation of the smallest singular value of a complex normal matrix. An upper bound for the largest singular value can be found in [2, Prop. 6.33]. We use these results to bound the singular values of , , and , which leads to the following theorem. We present the result only in the real case, but it can easily be extend to the complex case by combining Lemma 2 with (9) and (10).

Theorem 4.

Let be a Gaussian embedding matrix, i.e., , and let , where . Then, for

| (11) |

Additionally, for each we have, with failure probability at most ,

| (12) |

Proof.

Note first from Marčenko-Pastur (7) that we have

We can combine this with the result of Lemma 2 to find

and

The first result of Theorem 4 then follows by applying the scaling . Similarly, by (8) we have with failure probability at most that the following statements hold simultaneously:

Since the deterministic results in Lemma 2 imply

the result follows. ∎

3.1 Bounds for general subspace embeddings

The results above focus on Gaussian embedding matrices, and show that the ratios of the singular values are reasonably close to , as specified by (11). We now show that much of this carries over to a general subspace embedding . Note that an -dimensional subspace embedding will not generally embed an -dimensional space, but rather a smaller, say -dimensional, space.

Theorem 5.

Let be the leading right singular vectors of , and suppose is a subspace embedding for the subspace satisfying for some . Then, for ,

| (13) |

Proof.

3.2 The effect of tail singular values and oversampling

The proof of Lemma 2 allows us to see how the tail of the singular values, , affects the lower bound on the ratio . This allows us to make a case for oversampling based on singular value estimation, whereas usually oversampling is inspired through a discussion on singular vectors. Again using the Courant-Fischer theorem, we have

Now let and be such that

Then . We can use this to show

| (14) |

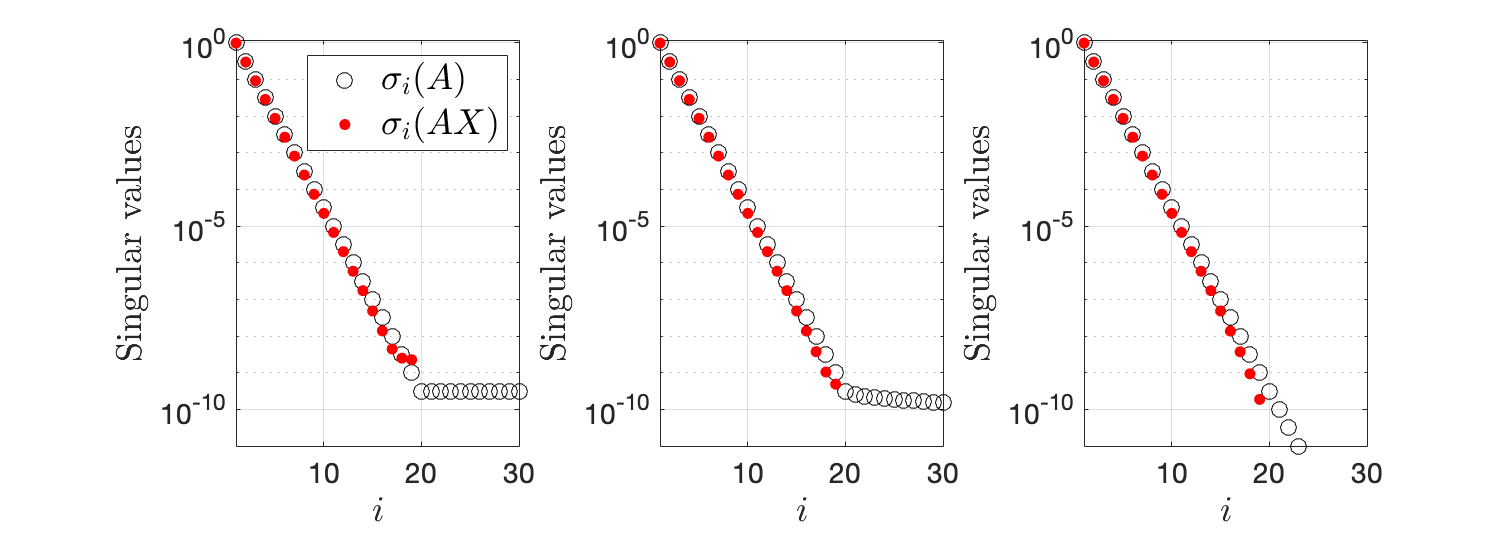

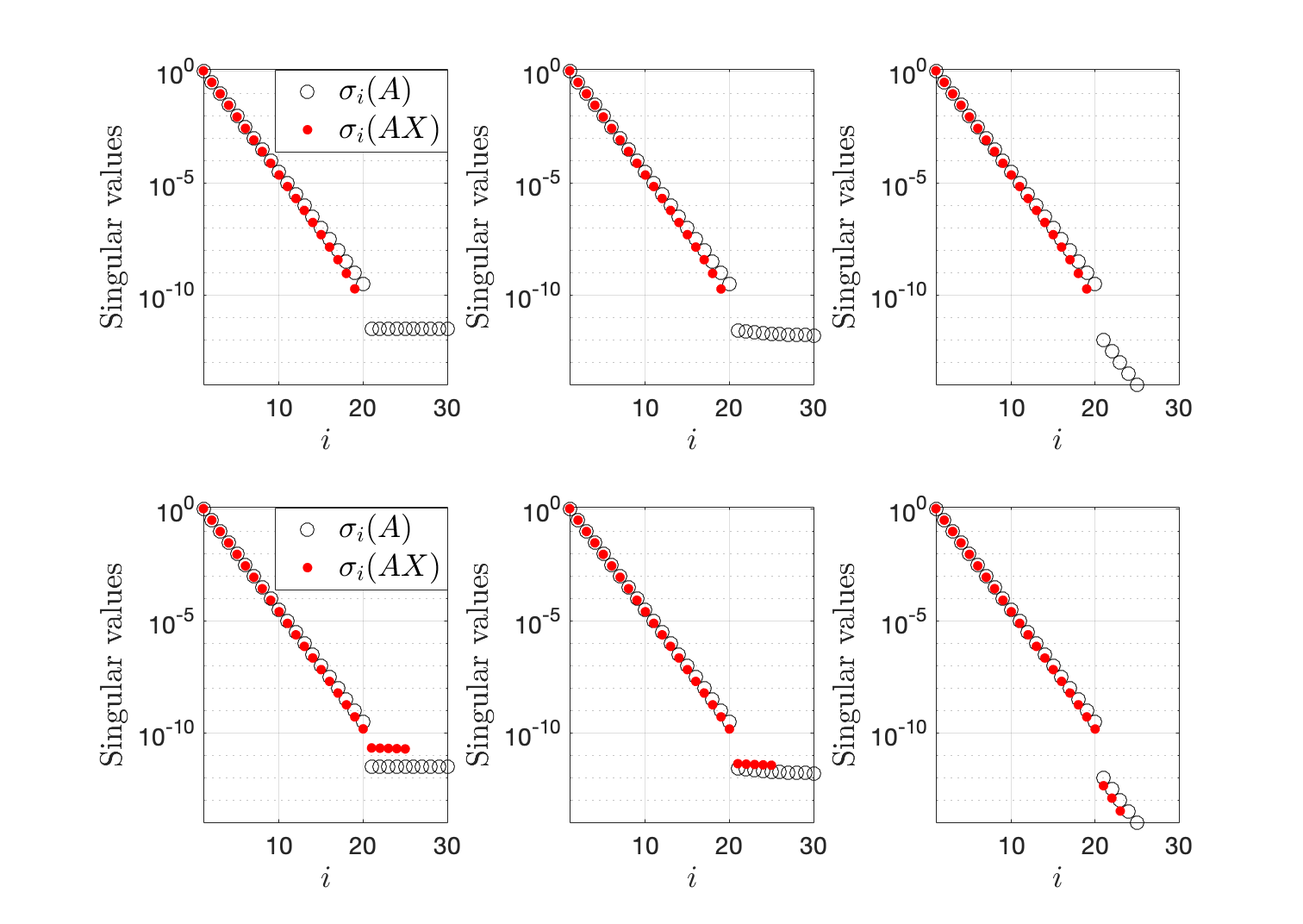

As is a Gaussian vector, we know . Additionally, it is worthwhile to note in expectation. The lower bound (14) thus suggests that a heavier tail , in terms of , would result in larger values for than a light tail. Consider in particular the last few singular values of , where the term is small. If the tail is light too, i.e. is small, the lower bound will not be strong. We see in practice that this effect is indeed noticeable for the smallest singular values of , making them less reliable estimators. The bulk of the singular values of are, however, not affected by the size of the tail given the low-rank structure of the matrix. We display this effect in Figures 1 and 2 with small-scale experiments.

The small-scale experiments agree with bigger numerical results, as well as with theoretical results, in the sense that the extreme (smallest) singular value estimates are not trustworthy. For this reason we recommend oversampling by 10% and disregarding the singular values corresponding to the oversampling.

3.3 Choice of sketch matrix

In our analysis we have mainly focused on Gaussian embedding matrices, as they are the most well-studied class of random matrices and allow us to derive sharp constants. A Gaussian embedding matrix is a random matrix with iid entries . They are often the simplest sketch to implement. While it requires operations to compute , when the complexity is optimal as is a lower bound for dense , as clearly all entries of need to be read. In fact, Gaussian sketches can be among the fastest to execute when . Furthermore, Gaussian is the most efficient type of embedding in the sense that an embedding for an -dimensional subspace can be achieved with high probability using samples.

Otherwise, if , other, more structured, classes of sketch matrices have been suggested and employed to speed up the computation of . These include subsampled randomized trigonometric transforms (SRTTs) [32], hashed randomized trigonometric transforms (HRTTs) [9], and sparse matrix embeddings [12, 11, 22].

In particular, SRTTs such as the subsampled randomized Hadamard, Fourier, discrete cosine or discrete Hartley transforms are random embeddings that allow fast application to a matrix. The use of these sketches can be justified by Theorem 5. While they come with weaker theoretical guarantees than Gaussian embeddings [40] (in that the size of the sketch needs to be at least to ensure an embedding with high probability), empirical evidence strongly suggests that they usually perform just as well. The performance of SRTT matrices is discussed more in the next section.

Related to SRTTs are the recently introduced class of random embeddings, HRTTs [9]. In these works it is shown an embedding for an -dimensional subspace can be achieved with high probability using samples (as with Gaussians) rather than , by replacing the subsampling matrix in (15) with a hashing matrix (e.g. Countsketch [48]), which can be done without increasing the complexity. Computational results suggest HRTTs perform adequately in pathological cases where SRTTs fail, such as diagonal matrices (see discussions on coherence in [20, 8]).

Finally, highly sparse embedding matrices have attracted much attention in the theoretical computer science literature [11, 22]. The state-of-the-art result [12] suggests an oversampling by a factor is needed to obtain an embedding with high probability.

When has no structure to take advantage of (e.g. dense), such SRTT embeddings allow us to compute with operations, which is optimal up to an factor. When has structure such as sparsity, could be computed much more efficiently, for example in operations for a Gaussian and less for sparse sketches.

The choice of therefore depends on the structure of ; but the complexity of the sketching can be bounded from above by for dense matrices. We mainly use HRTT embedding matrices — specifically hashed randomized DCTs — in this paper as they are able to perform optimally, even for very coherent matrices. In our numerical experiments, we use diagonal matrices which is the most coherent type of matrix, and therefore most difficult to sketch.

3.4 A numerical experiment

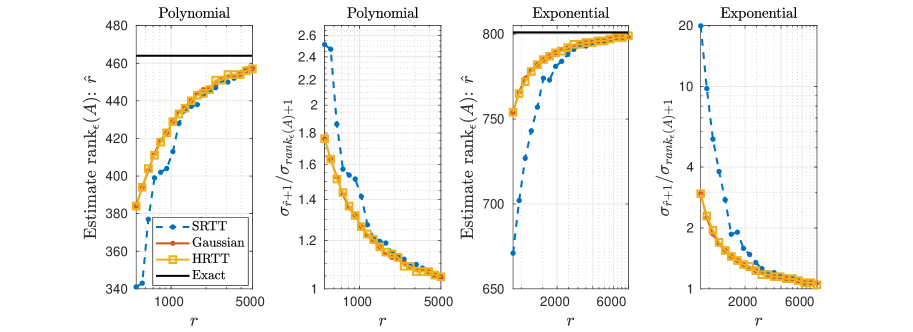

We show how the theoretical result of this section, namely for leading , practically translates to a rank estimation technique. After sketching with an embedding matrix , we compute the singular values and estimate for a given tolerance to be the first such that . If (an estimate of) is unavailable, we may use . We applied this method to two synthetic example matrices, one diagonal matrix with polynomially decaying singular values (), and one diagonal matrix with exponentially decaying singular values (). The matrices are square of dimension .

Figure 3 shows the results of the experiment. We plot the estimates for the numerical rank that result from varying embedding dimensions , and the ratio . As both matrices do not have large gaps in the spectrum, the latter is an important quantity to judge the effectiveness of the rank estimator (see Section 1.1). We see that even for small values of and when using an HRTT or Gaussian embedding, is very close to and and well within the acceptable range described in Section 1. Additionally, we see that SRTT matrices perform less than optimal for this pathological example of a diagonal matrix.

4 Randomized approximate orthogonalization:

We have seen that the numerical rank of is a good estimator for the numerical rank of , provided that is approximately low-rank. Although is of much smaller dimension than , it may still be prohibitively expensive to compute its exact singular values. Furthermore, one could question whether it is worth calculating the singular values accurately spending work, considering the accuracy that was lost in the sketching step. Here we describe a method, which we call randomized approximate orthogonalization, to cheaply compute estimates of the singular values of in operations. The idea is similar to Section 3, in that sketches roughly preserve (the leading) singular values, but as we are working with a tall-skinny matrix , here all the singular values will be preserved up to a small multiplicative factor.

Randomized approximate orthogonalization is inspired by the randomized least-squares solver framework named sketch-to-precondition. The ideas were introduced in [38] and a fast implementation was introduced in Blendenpik [3]. In the framework, a preconditioner for an overdetermined least-squares problem where ( is generated. The solvers work as follows: the first step is to sample the rowspace of by sketching with a random embedding matrix , where , to obtain the small matrix . Secondly, one computes the QR factorization of . The upper triangular factor is then used as a preconditioner for an iterative solver such as LSQR. Even though the QR factorization is based on a sketch of , it is now a well-known fact in RNLA that is ‘close to orthonormal’ in the sense that . Consequently, the singular values of , or equivalently , are close to the singular values of (in the relative sense for all ). One could also view this process as a ‘randomized approximate orthogonalization’ of .

It follows that, in our context, we may estimate the singular values of using the singular values of , where is another random embeddding (independent of ) of size . It is then only necessary to compute the numerical rank (by computing the exact singular values) of the very small matrix to estimate the numerical rank of the large matrix . This is the final step of our rank estimation algorithm, which is discussed fully in the next section.

As for the choice of : unlike the first sketch of computing , in most cases the structure of (such as sparsity, if present) is lost in . It is therefore usually recommended that we take to be an SRTT embedding, so that can be computed in operations. We assume this choice below and throughout the remainder of the paper, switching between the notations and when appropriate. That is,

| (15) |

where is a sampling matrix, a square orthogonal (or unitary) trigonometric transform (such as Fourier or DCT) of dimension and a diagonal matrix of independent random signs.

Specifically the subsampled randomized Hadamard transform is analyzed extensively in [40, 7]. These results can be readily extended to a general SRTT matrix and used in our context, as we show in the appendix in Lemma 7. This is essentially a restatement of [40, Thm. 3.1] and [7, Lem. 4.1]. It leads to the following result on the accuracy of as estimates for .

Corollary 6.

Let , with , and let be an SRTT matrix as in (15), where the trigonometric transform in satisfies . Let and If

| (16) |

then, with failure probability at most

| (17) |

for each .

The use of the number is a natural choice as it only depends on the choice of trigonometric transform, not on the size of the matrices involved. Choices for the trigonometric transform include Fourier, cosine, Hadamard, and Hartley transforms. The optimal is attained for a Hadamard transform, for which . The same holds for a Fourier matrix, but this involves operations in and when is real, we may prefer real transforms. Since the Hadamard transform is only available when the dimension is a power of 2 (for which one solution is to append zeros to the matrix), we make use of the discrete cosine transform with in our experiments when is real. Alternatively, we could have chosen the discrete Hartley transform with the same coherence . See [3] for more discussion.

We also note that a result analogous to Corollary 6 is given in [34, Thm. 4.4] when is a Gaussian matrix (and hence in a closer spirit to Section 3). Results for a general subspace embedding matrix can be found in [48].

4.1 A numerical experiment

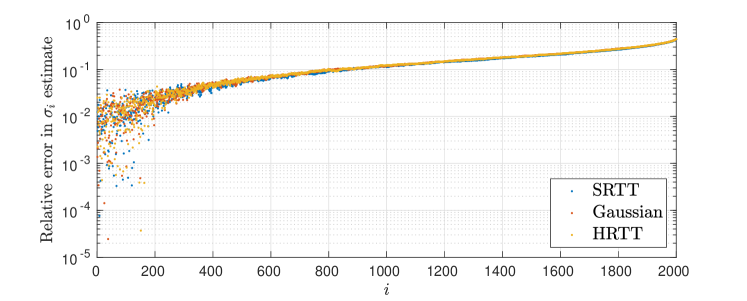

We explained how all singular values of a tall and skinny matrix can be estimated by the singular values of , where is an embedding matrix and . In the next section we conclude how this, combined with the results of the previous section, leads to a rank estimation algorithm. In the following numerical experiment, we first illustrate the error one can expect in practice in the step from to .

We let be a dense matrix with fast polynomially decaying singular values, , of size . We estimate with , where is either a subsampled randomized DCT embedding or a Gaussian embedding of dimension . The relative error is plotted in Figure 4. We see the relative errors are for each . We use a dense matrix with incoherent left singular vectors to resemble the matrix , which will never be very coherent due to the prior application of embedding . As a result, the SRTT embedding is sufficient.

5 A numerical rank estimation scheme

The numerical rank estimation scheme that follows from the observations

-

1.

for an approximately low-rank matrix and leading singular values, and

-

2.

for all singular values of ,

is displayed in pseudocode in Algorithm 1.

The algorithm requires an upper bound for the numerical rank as an input (). This input informs the size of first embedding , and is the total number of singular values estimates that will be obtained. If the input rank was not large enough, i.e. , Algorithm 1 is naturally only able to detect that is a lower bound for . To get a proper estimate, we then need to rerun the algorithm with a larger input rank, taking advantage of the preceding computation by appending extra columns to and rows to .

The choice of can be based on a number of possible considerations. For example, one might choose based on memory requirement, e.g. when one is unwilling to store more than numbers. If some information is available on (e.g. it is updated from a matrix with known singular values), that can provide a good choice of . If no information is available one might choose , say ; however, this can result in some inefficiency.222If the sketches employed are Gaussian, the complexity is (dominated by sketching) and the overhead of underestimating is minimal, bounded by a factor 2 (assuming the update rule ; other increments are of course possible). However, with other sketches such as SRTT, increasing without resketching the whole matrix requires some care: For the SRTT , where is a subsampling matrix, is a FFT/DCT matrix, and is a diagonal matrix of random signs, we store , , etc., and then subsample the big matrix .

Provided the algorithm runs sucessfully, the computational complexity is for a dense matrix , where the two terms come from steps 3 and 7, assuming both and are SRTT matrices. The cost of step 3 can be lower if has structure, in which case the cost in step 6 may become significant.

Regarding step 7, computing the singular values of , one can of course compute them via the SVD. We do this in most cases as the cost is usually negligible. Alternatively, since it suffices to retrieve estimates for , one can compute the QR factorization and take the diagonal elements of as approximations of the singular values; this works as a QR factorization of a matrix whose (right) singular vectors are randomized are rank-revealing with high probability [5].

5.1 Rank estimation as part of randomized low-rank approximation

It is worth discussing the case where Algorithm 1 is used as an initial step for randomized low-rank approximation, such as RSVD [19] or generalized Nyström [36]. In such cases, computing the sketch is needed anyway, so step 3 incurs no additional cost.

Moreover, with generalized Nyström, even is required, as the low-rank approximant is of the form . Furthermore, to evaluate a QR factorization is computed. It follows that the additional work needed to execute Algorithm 1 is just to estimate the singular values of . As described above, to do so one can simply take the diagonal elements of , requiring just work. Thus in the context of generalized Nyström, a rank estimate can be obtained essentially for free.

In the next section we explain how this rank estimate can be employed to speed up fixed-precision low-rank approximation. In particular, we note that using the singular value estimates we can reduce the size of a sketch as appropriate before performing the dominant computational work.

5.1.1 Fixed-precision low-rank approximation problem

Rank estimation as part of low-rank approximation is inherently linked to the fixed-precision problem, where one aims to compute a low-rank factorization of unspecified rank such that for some user-specified tolerance . We propose a scheme to combine rank estimation and low-rank approximation through existing error estimates. The algorithm will be used here for approximation in the Frobenius norm but can easily be extended to approximation in any other norm for which randomized low-rank approximation error estimates are available. The aim will be to find an approximation of the form , where has orthonormal columns and .

In their landmark paper of 2011, Halko, Martinsson and Tropp [19] describe and extensively analyze the randomized rangefinder (or randomized SVD) algorithm to compute such an approximation. This algorithm is displayed as Algorithm 2. Note that it can be extended to the randomized SVD algorithm by computing the SVD of and then taking . A limitation of this factorization routine, as well as of other randomized low-rank approximation algorithms, is that we often wish to solve a fixed precision problem instead of a fixed rank algorithm, where the appropriate choice of the input rank is usually unknown.

As mentioned, we propose to use rank estimation to tackle this problem using a priori error estimates. Under the conditions of Algorithm 2 with a Gaussian embedding matrix, it is known that [19, Thm. 10.5]

| (18) |

We can use the Rank Estimation Algorithm 1 to compute estimates of the trailing singular values which appear in the estimate (18). Suppose we have estimates for the first singular values of , as a result of step 6 of Algorithm 1. Conservatively, and taking into account that there could be underestimation in the last few estimates if the tail is light, we set for . We can then choose the target rank in the rangefinder algorithm to be the first such that

where is fixed to be 5 or 10 as suggested in [19] or where is fixed relative to , say , as suggested in [36].

As mentioned before, the rank estimation part of this scheme requires only additional cost. More importantly, the singular value estimates it provides allow us to reduce the size of the sketch ahead of the rangefinder process. This could result in considerable speed-up, as the QR factorization of and the matrix-matrix multiplication are usually the dominant costs in the algorithm. Finally, we also know the rank of is nearly minimal while (approximately) satisfying the accuracy criteria; by contrast, reducing the rank of a factorization without rank estimation requires computing the SVD of and truncating it.

| (19) |

6 Numerical experiments

We introduce synthetic example matrices to experimentally support the theoretical results. Each of the matrices is diagonal and square of dimension . They are, however, treated as dense matrices by the algorithms here. The singular values are on the diagonal in decreasing order. We distinguish the following singular value spectra and resulting matrices, inspired by [41]:

-

1.

Gaps in spectrum: we define a matrix with for , for , for , for and for .

-

2.

Polynomial decay: each singular value takes the value for a parameter . We define a matrix with a slow polynomial decaying spectrum (SP) with , and a matrix with fast polynomial decay (FP) with .

-

3.

Exponential decay: the singular values are logarithmically equally spaced between 1 and , that is for a parameter . We study a matrix with slow exponential decay (SE) for which and a matrix with fast exponential decay (FE) for which .

Each of the matrices has spectral norm so the relative accuracy notation will be suppressed in this section. In each of the experiments in subsections 6.2-6.4, we will choose the embedding matrix to be a hashed randomized DCT matrix and to be a subsampled randomized DCT matrix. We display the perfomance of Algorithms 1 and 3 in various numerical experiments.

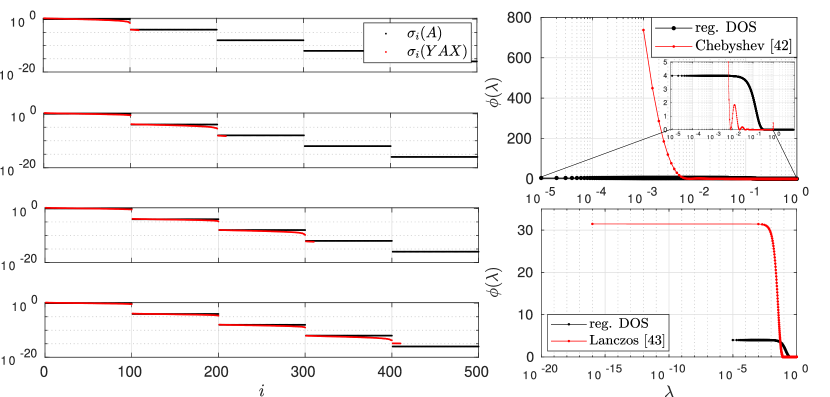

6.1 Detecting gaps in the spectrum

Here we demonstrate that Algorithm 1 works extremely well for approximately low-rank matrices that have gaps in their singular value spectrum. The algorithm can in fact be used in two ways: 1) if the specified tolerance is within the gap between two singular values, the algorithm will perform very well in identifying the correct rank even for a small number of samples, and 2) by considering the gaps in the singular value spectrum of , one can identify gaps in the singular value spectrum of and use this to inform the value and target rank.

To illustrate this we compare the singular values to for various values of (see Algorithm 1). Note that we oversample by 10% and disregard the singular values associated with oversampling. The results are shown in Figure 5. The figure displays the remarkable effectiveness of the algorithm, where gaps in the spectrum are clearly identified even for small values of .

We use Gaussian embeddings for the column space and SRCTs for the row space, to allow for an adaptive procedure. That is, we start with a Gaussian of dimension 110, compute and its singular values, and then increase the sketch dimension of by a 100 until we can identify the gap. This is how Algorithm 1 could be used if there is no upper bound on available. We compare against the performance of the DOS algorithms [42] (Chebyshev-based) and [43] (Lanczos-based). Our rank estimation algorithm took 18.33 seconds to reveal the gap at the 400th singular value. The runtime of the DOS algorithms was 2223 sec. for [42] and 199.1 sec. for [43]. The DOS plots are also shown in Figure 5.

It is inherently difficult to detect gaps visible on a log-scale using a DOS algorithm. The algorithms are based on estimating a sum of Dirac delta functions using a sum of smooth functions such as Gaussians. To be able to distinguish between very small eigenvalues, the width of the Gaussian has to be as small as the smallest eigenvalue. That is, it would be necessary to have a very high-resolution spectral density. The resolution refers to the size of the interval in which we estimate the number of eigenvalues [27]. However, a fine resolution implies the number of sample points needed to detect larger eigenvalues is large. As a result, the computational effort necessary is not tractable. Figure 5 shows that even if the DOS is estimated perfectly for the chosen Gaussian standard deviation, the gaps are not visible.

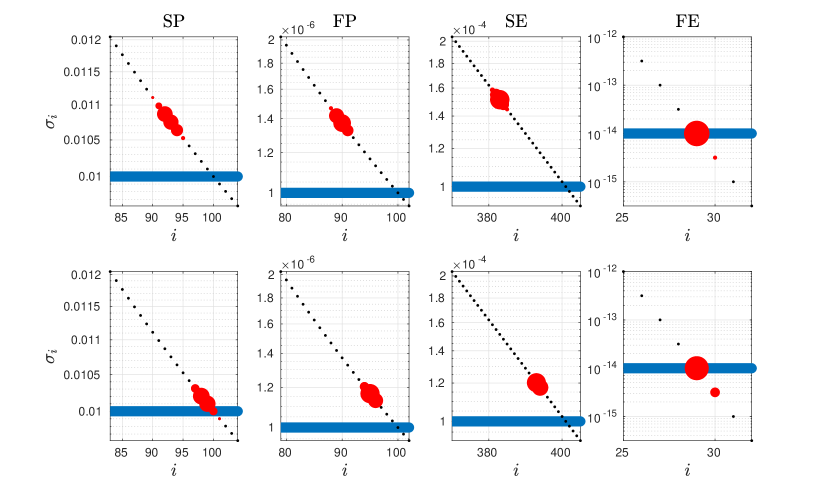

6.2 Robustness of the rank estimator

The other four example matrices discussed (SP, FP, SE, and FE) do not have significant gaps in their singular value spectra, which makes the numerical rank less well-defined. Rather than focusing on the numerical rank estimate, , it thus makes sense to look at and its proximity to . Figure 6 shows the results of Algorithm 1 applied 100 times to each of the example matrices. We see that, although the rank estimate we recover is often an underestimate when there are no significant gaps between singular values near the desired accuracy , is always very close to . One could argue this is not necessarily a shortcoming of the algorithm, but rather a display of the difficulties associated to the concept of the exact numerical rank when . Importantly, the algorithm always found a rank that satisfies the two desiderata set out in Section 1.1. In particular, when there are significant gaps in the singular value spectrum we recover the exact numerical rank in all except one instance; see the rightmost column of the figure (and the forthcoming Figure 5).

6.3 Comparison with other numerical rank estimation algorithms

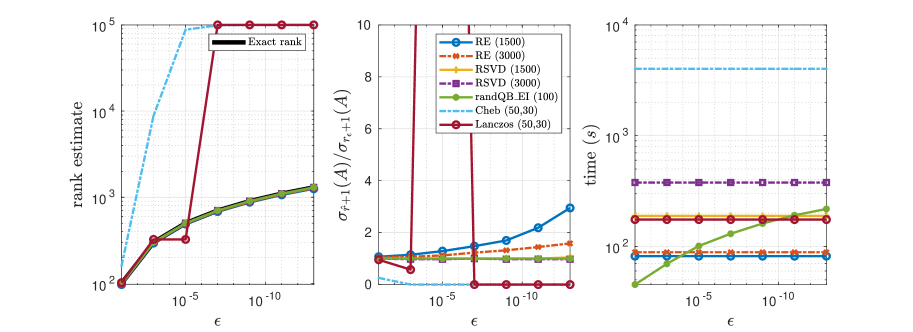

Suppose that the goal is to obtain the numerical rank of a given matrix for some tolerance . We compare five different methods to achieve this for a matrix with slow exponential decaying spectrum (SE) and various values of ranging from to . The results are shown in Figure 7.

The algorithms we compare are rank estimation (RE) with different parameters , the rank estimate obtained from RSVD with different parameters for , the rank estimate obtained from randQB_EI [49] with parameter , the DOS algorithm with Chebyshev filters introduced in [42] (Cheb) and the Lanczos DOS algorithm introduced in [43] (Lanczos), both with degree and samples, which are the default parameters in the authors’ implementation333The implementation used is available at https://shashankaubaru.github.io/codes.html.. We see that the latter two DOS algorithms do not accurately compute the rank for smaller values of . A higher degree polynomial approximation would be necessary for this, which will slow down the computation. The DOS algorithms work very well for smaller matrices, but in the case of small tolerances and extremely large data, where each matrix-vector operation is costly in communication, the algorithms are outperformed by RE, RSVD, and randQB_EI.444We used the implementation of randQB_EI by the authors of [49], available at https://github.com/WenjianYu/randQB_auto.

As for these three, we see that RE is considerably faster in the context of rank estimation. Note also that the difference in running time will be more pronounced when the matrix is too large to fit into fast memory, as the other algorithms need to pass over the data more than once. Although the numerical rank is slightly underestimated for each value of with the Rank Estimation algorithm, and is exact for the other algorithms, we see that is always extremely close to . This requirement for a good rank estimation set out in the introduction is thus satisfied.

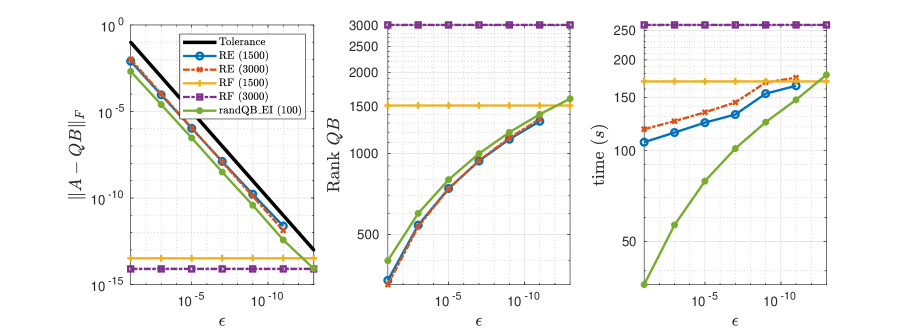

6.4 The fixed-precision problem

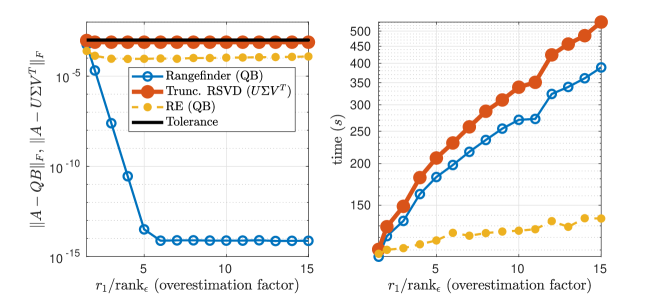

Often when dealing with large-dimensional approximately low-rank matrices, our aim is to obtain a low-rank approximation that is accurate within a given tolerance, as discussed in Section 5.1. We compare three different algorithms to obtain such an approximation, Rank Estimation combined with Randomized Rangefinder (Algorithm 3), Randomized Rangefinder (Algorithm 2), and the adaptive algorithm RandQB_EI [49]). The results are shown in Figure 8. The figure shows that the adaptive algorithm RandQB_EI is the fastest in most cases.

It is difficult to compare these algorithms as the performance is very dependent on the context of the problem, and the parameters chosen. We argue that our algorithm is the best choice when it is very expensive to communicate with the matrix, and a reliable prior rank estimate is unavailable. In this case, overestimating the target rank in randomized rangefinder and randomized SVD is much more expensive than it is in Algorithm 3, rank estimation with rangefinder. This is portrayed in Figure 9.

7 Discussion

Let us conclude with a few extensions and open problems related to Algorithm 1.

As presented, Algorithm 1 does not take into account the structure of such as symmetry or sparsity. It would be of interest to devise a variant that respects such structure.

When the input rank is insufficient, i.e. , Algorithm 1 needs to be rerun with a larger . It would be helpful (if possible) to be able to find an appropriate new from the information obtained from the first run.

While we primarily focused on rank estimation, the analysis indicates that many of the (leading) singular values of can be estimated by . Tuning each to obtain a reliable (ideally unbiased) estimator is left for future work.

Acknowledgement

We would like to thank the referees for their valuable comments, which improved the contents and exposition of the paper considerably. We also thank Nick Trefethen for valuable comments.

Appendix A Additional Proofs

A.1 Proof of Corollary 6

We wish to prove the following lemma from which Corollary 6 follows in a straightforward fashion:

Lemma 7.

Let have orthonormal columns and let be a SRTT matrix as in (15), where the trigonometric transform in satisfies . Let and If

| (20) |

then, with failure probability at most

| (21) |

The proof of Lemma 7 consists of two main steps: first to show that premultiplying an orthonormal matrix with a randomized trigonometric transform smooths out information in the rows (or equivalently, equalizes the row norms), and second to show that sampling rows from a matrix with ‘smoothed out’ information works well. The proof is analogous to those by Boutsidis and Gittens [7], but as their discussion only covers subsampled randomized Hadamard transforms instead of general SRTT matrices, we include the proof for completeness.

A key concept in the proof is coherence, which is strongly related to the notion of ‘smoothing out’ information in the rows. Let be a tall and skinny matrix and let be a matrix with orthonormal columns spanning the column space of . Then the coherence of is defined

| (22) |

where denotes the th row of . The minimal, and optimal, coherence of a matrix of size is . This can be interpreted as all rows being equally important, which makes sampling rows more effective. The following lemma essentially states that applying a randomized trigonometric transform reduces the coherence of a matrix.

Lemma 8 (Tropp [40]).

Let have orthonormal columns. Let be a square orthogonal matrix of dimension with , be a diagonal matrix of independent random signs, and define . Let . Then, with probability at least

We use the following lemma in the proof.

Proposition 9 ([40], Prop. 2.1).

Suppose is a convex function that satisfies the Lipschitz condition

Let be a vector of random signs. Then for all ,

The proof of the lemma then follows from defining such a convex, Lipschitz function.

Proof of Lemma 8 [40].

Fix a row index and define the function

where is a diagonal matrix constructed from the th row of . Let be a vector of random signs. Since the diagonal of is also a vector of random signs, we can bound the norm of the th row of by bounding using Proposition 9. We will first show that satisfies the conditions of Proposition 9. Note that it is convex by the triangle inequality. Since we have that for all , the entries of all have magnitude less than or equal to as well, which means . We use this to show the Lipschitz constant of is .

We bound the expected value of as

Now apply Proposition 9 with to find

We need this to hold for each of the rows. By the union bound, we obtain

Finally, note that . ∎

We need to combine this result with Lemma 4.3 of [7] which is a corollary to Lemma 3.4 of [40]. The proof can be found in the references.

Lemma 10 (Boutsidis and Gittens [7]).

Let have orthonormal columns and let denote its coherence. Let and . Let be an integer such that

Let sample rows uniformly at random and without replacement, and define . Then, with probability at least

References

- [1] A. Andoni and H. L. Nguyễn. Eigenvalues of a matrix in the streaming model. Proc. Annu. ACM-SIAM Symp. Discrete Algorithms, pages 1729–1737, 2013.

- [2] G. Aubrun and S. J. Szarek. Alice and Bob meet Banach, volume 223. American Mathematical Society, 2017.

- [3] H. Avron, P. Maymounkov, and S. Toledo. Blendenpik: Supercharging LAPACK’s least-squares solver. SIAM J. Sci. Comp., 32(3):1217–1236, 2010.

- [4] Z. Bai and J. W. Silverstein. Spectral Analysis of Large Dimensional Random Matrices. Springer, 2010.

- [5] G. Ballard, J. Demmel, and I. Dumitriu. Minimizing communication for eigenproblems and the singular value decomposition. Technical Report 237, LAPACK Working Note, 2010.

- [6] B. Beckermann and A. Townsend. On the singular values of matrices with displacement structure. SIAM J. Matrix Anal. Appl., 38(4):1227–1248, 2017.

- [7] C. Boutsidis and A. Gittens. Improved matrix algorithms via the subsampled randomized Hadamard transform. SIAM J. Matrix Anal. Appl., 34(3):1301–1340, 2013.

- [8] E. J. Candès and B. Recht. Exact matrix completion via convex optimization. Found. Comput. Math., 9(6):717–772, 2009.

- [9] C. Cartis, J. Fiala, and Z. Shao. Hashing embeddings of optimal dimension, with applications to linear least squares. arXiv:2105.11815, 2021.

- [10] H. Y. Cheung, T. C. Kwok, and L. C. Lau. Fast matrix rank algorithms and applications. J. ACM, 60(5):1–25, 2013.

- [11] K. L. Clarkson and D. P. Woodruff. Low-rank approximation and regression in input sparsity time. J. ACM, 63(6):54, 2017.

- [12] M. B. Cohen. Nearly tight oblivious subspace embeddings by trace inequalities. In Proc. Annu. ACM-SIAM Symp. Discrete Algorithms, pages 278–287. SIAM, 2016.

- [13] K. R. Davidson and S. J. Szarek. Local operator theory, random matrices and Banach spaces. In Handbook of the geometry of Banach spaces, pages 317–366. Elsevier, 2001.

- [14] E. Di Napoli, E. Polizzi, and Y. Saad. Efficient estimation of eigenvalue counts in an interval. Numer. Lin. Alg. Appl., 23(4):674–692, 2016.

- [15] J. A. Duersch and M. Gu. Randomized projection for rank-revealing matrix factorizations and low-rank approximations. SIAM Rev., 62(3):661–682, 2020.

- [16] N. El Karoui. Spectrum estimation for large dimensional covariance matrices using random matrix theory. Ann. Stat., 36(6):2757–2790, 2008.

- [17] A. Gittens and J. A. Tropp. Tail bounds for all eigenvalues of a sum of random matrices. 1:1–23, 2011.

- [18] G. H. Golub and C. F. Van Loan. Matrix Computations. The Johns Hopkins University Press, 4th edition, 2012.

- [19] N. Halko, P.-G. Martinsson, and J. A. Tropp. Finding structure with randomness: Probabilistic algorithms for constructing approximate matrix decompositions. SIAM Rev., 53(2):217–288, 2011.

- [20] I. C. Ipsen and T. Wentworth. The effect of coherence on sampling from matrices with orthonormal columns, and preconditioned least squares problems. SIAM J. Matrix Anal. Appl., 35(4):1490–1520, 2014.

- [21] I. M. Johnstone. On the distribution of the largest eigenvalue in principal components analysis. Ann. Stat., pages 295–327, 2001.

- [22] D. M. Kane and J. Nelson. Sparser Johnson-Lindenstrauss transforms. J. ACM, 61(1):1–23, 2014.

- [23] V. Koltchinskii and K. Lounici. Concentration inequalities and moment bounds for sample covariance operators. Bernoulli, 23(1):110–133, 2017.

- [24] O. Ledoit and M. Wolf. A well-conditioned estimator for large-dimensional covariance matrices. J. Multivar. Anal., 88(2):365–411, 2004.

- [25] O. Ledoit and M. Wolf. Nonlinear shrinkage estimation of large-dimensional covariance matrices. Ann. Stat., 40(2):1024–1060, 2012.

- [26] O. Ledoit and M. Wolf. Analytical nonlinear shrinkage of large-dimensional covariance matrices. Ann. Stat., 48(5):3043–3065, 2020.

- [27] L. Lin, Y. Saad, and C. Yang. Approximating spectral densities of large matrices. SIAM Rev., 58(1):34–65, 2016.

- [28] V. A. Marčenko and L. A. Pastur. Distribution of eigenvalues for some sets of random matrices. Mathematics of the USSR-Sbornik, 1(4):457–483, 1967.

- [29] P.-G. Martinsson. Randomized methods for matrix computations. arXiv preprint 1607.01649, 2016.

- [30] P.-G. Martinsson. Fast Direct Solvers for Elliptic PDEs. SIAM, 2019.

- [31] P.-G. Martinsson, G. Quintana-Orti, and N. Heavner. randUTV: A blocked randomized algorithm for computing a rank-revealing UTV factorization. ACM Trans. Math. Soft., 45(1):1–26, 2019.

- [32] P.-G. Martinsson and J. A. Tropp. Randomized numerical linear algebra: Foundations and algorithms. Acta Numer., pages 403–572, 2020.

- [33] R. Mathias. Two theorems on singular values and eigenvalues. Am. Math. Mon., 97(1):47–50, 1990.

- [34] X. Meng, M. A. Saunders, and M. W. Mahoney. LSRN: A parallel iterative solver for strongly over-or underdetermined systems. SIAM J. Sci. Comp., 36(2):C95–C118, 2014.

- [35] B. Nadler. Finite sample approximation results for principal component analysis: A matrix perturbation approach. Ann. Stat., 36(6):2791–2817, 2008.

- [36] Y. Nakatsukasa. Fast and stable randomized low-rank matrix approximation. arXiv:2009.11392, 2020.

- [37] N. R. Rao, J. A. Mingo, R. Speicher, and A. Edelman. Statistical Eigen-Inference from large Wishart matrices. Ann. Stat., 36(6):2850–2885, 2008.

- [38] V. Rokhlin and M. Tygert. A fast randomized algorithm for overdetermined linear least-squares regression. Proc. Natl. Acad. Sci., 105(36):13212–13217, 2008.

- [39] M. Rudelson and R. Vershynin. Non-asymptotic theory of random matrices: Extreme singular values. In Proc. ICM, pages 1576–1602, 2010.

- [40] J. A. Tropp. Improved analysis of the subsampled randomized Hadamard transform. Advances in Adaptive Data Analysis, 3(1-2):115–126, 2011.

- [41] J. A. Tropp, A. Yurtsever, M. Udell, and V. Cevher. Streaming low-rank matrix approximation with an application to scientific simulation. SIAM J. Sci. Comp., 41(4):A2430–A2463, 2019.

- [42] S. Ubaru and Y. Saad. Fast methods for estimating the numerical rank of large matrices. In ICML, pages 468–477. PMLR, 2016.

- [43] S. Ubaru, Y. Saad, and A.-K. Seghouane. Fast estimation of approximate matrix ranks using spectral densities. Neural Comput., 29(5):1317–1351, may 2017.

- [44] S. Ubaru, A.-K. Seghouane, and Y. Saad. Find the dimension that counts: Fast dimension estimation and krylov pca. In Proc. SIAM Int. Conf. on Data Min., pages 720–728. SIAM, 2019.

- [45] M. Udell and A. Townsend. Why are big data matrices approximately low rank? SIAM J. Math. Data Sci., 1(1):144–160, 2019.

- [46] R. Vershynin. High-dimensional probability: An introduction with applications in data science, volume 47. Cambridge University Press, 2018.

- [47] M. J. Wainwright. High-dimensional statistics: A non-asymptotic viewpoint. Cambridge University Press, 2019.

- [48] D. P. Woodruff. Sketching as a tool for numerical linear algebra. Found. Trends Theor. Comput. Sci., 10(1–2):1–157, 2014.

- [49] W. Yu, Y. Gu, and Y. Li. Efficient randomized algorithms for the fixed-precision low-rank matrix approximation. SIAM J. Matrix Anal. Appl., 39(3):1339–1359, 2018.

- [50] Y. Zhang, M. Wainwright, and M. Jordan. Distributed estimation of generalized matrix rank: Efficient algorithms and lower bounds. In ICML, pages 457–465. PMLR, 2015.