Derivation of wealth distributions from biased exchange of money

Abstract

In the manuscript, we are interested in using kinetic theory to better understand the time evolution of wealth distribution and their large scale behavior such as the evolution of inequality (e.g. Gini index). We investigate three type of dynamics denoted unbiased, poor-biased and rich-biased exchange models. At the individual level, one agent is picked randomly based on its wealth and one of its dollar is redistributed among the population. Proving the so-called propagation of chaos, we identify the limit of each dynamics as the number of individual approaches infinity using both coupling techniques [48] and martingale-based approach [36]. Equipped with the limit equation, we identify and prove the convergence to specific equilibrium for both the unbiased and poor-biased dynamics. In the rich-biased dynamics however, we observe a more complex behavior where a dispersive wave emerges. Although the dispersive wave is vanishing in time, its also accumulates all the wealth leading to a Gini approaching (its maximum value). We characterize numerically the behavior of dispersive wave but further analytic investigation is needed to derive such dispersive wave directly from the dynamics.

Key words: Econophysics, Agent-based model, Propagation of chaos, Entropy, Dispersive wave

1 Introduction

Econophysics is an emerging branch of statistical physics that apply concepts and techniques of traditional physics to economics and finance [45, 18, 25]. It has attracted considerable attention in recent years raising challenges on how various economical phenomena could be explained by universal laws in statistical physics, and we refer to [15, 16, 41, 30] for a general review.

The primary motivation for study models arising from econophysics is at least two-fold: from the perspective of a policy maker, it is important to deal with the raise of income inequality [21, 22] in order to establish a more egalitarian society. From a mathematical point of view, we have to understand the fundamental mechanisms, such as money exchange resulting from individuals, which are usually agent-based models. Given an agent-based model, one is expected to identify the limit dynamics as the number of individuals tends to infinity and then its corresponding equilibrium when run the model for a sufficiently long time (if there is one), and this guiding approach is carried out in numerous works across different fields among literatures of applied mathematics, see for instance [38, 5, 12].

Although we will only consider three distinct binary exchange models in the present work, other exchange rules can also be imposed and studied, leading to different models. To name a few, the so-called immediate exchange model introduced in [27] assumes that pairs of agents are randomly and uniformly picked at each random time, and each of the agents transfer a random fraction of its money to the other agents, where these fractions are independent and uniformly distributed in . The so-called uniform reshuffling model investigated in [25] and [32] suggests that the total amount of money of two randomly and uniformly picked agents possess before interaction is uniformly redistributed among the two agents after interaction. For models with saving propensity and with debts, we refer the readers to [14], [17] and [33].

1.1 Unbiased/poor-biased/rich-biased dynamics

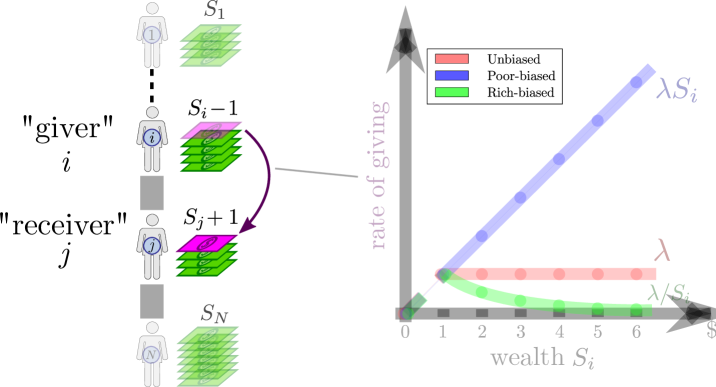

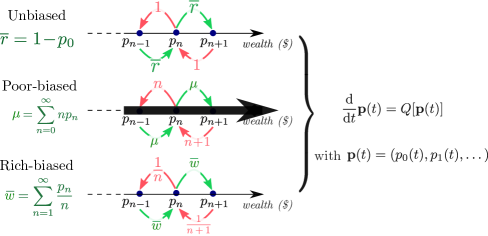

In this work, we consider several dynamics for money exchange in a closed economical system, meaning that there are a fixed number of agents, denoted by , with an (fixed) average number of dollar . We denote by the amount of dollars the agent has at time . Since it is a closed economical system, we have:

| (1.1) |

As a first example of money exchange, we review the model proposed in [25]: at random time (exponential law), an agent is picked at random (uniformly) and if it has one dollar (i.e. ) it will give it to another agent picked at random (uniformly). If does not have one dollar (i.e. ), then nothing happens. From now on we will call this model as unbiased exchange model as all the agents are being picked with equal probability. We refer to this dynamics as follow:

| (1.2) |

In other words, any agents with at least one dollar gives to all of the others agents at a fixed rate. Later on, we will adjust the rate (more exactly ) by normalizing by in order to have the correct asymptotic as (the rate of one agent giving a dollar per unit time is of order otherwise).

Another possible dynamics is to pick the giver agent, i.e. agent , with higher probability if the agent is rich, i.e. large. Thus, poor agent will have a lower frequency of being picked. From now on we will call this model as poor-biased model and it illustrates as follow:

| (1.3) |

Notice that since the rate of giving is , an agent with no money, i.e. , will never have to give. As for the unbiased dynamics (1.2), we will also adjust the rate, normalizing by .

Our third dynamics that we would like to explore is the rich-biased model: we reverse the bias compared to the previous dynamics, rich agents are less likely to give:

| (1.4) |

As a consequence of this dynamics, rich agents will tend to become even richer compared to poor agents creating a feedback that could lead to singular behavior. The adjustment of the rate for this dynamics is more delicate since the sum of the rates is no longer constant. In particular, we will see that a normalization of the rates to have a constant rate of giving a dollar per agent will lead to finite time blow-up of the dynamics in the limit .

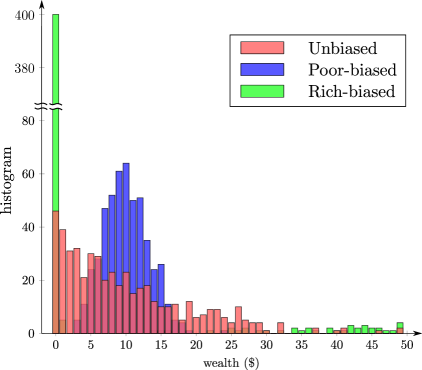

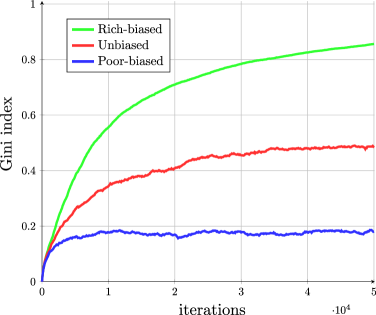

We illustrate the dynamics in figure 1-left. The key question of interest is the exploration of the limiting money distribution among the agents as the total number of agents and the number of time steps become large. We illustrate numerically (see figure 2) the three previous dynamics using agents. In the unbiased dynamics (pink), the wealth distribution is (approximately) exponential with the proportion of agent decaying as wealth increases. On the contrary, the poor-biased dynamics (blue) has the bulk of its distribution around (the average capital per agent). For the rich-biased dynamics (green), most of the agents are left with no money and few with large amounts (more than ). To visualize the temporal evolution of the three dynamics, we estimate the Gini index after each iteration in figure 1-right:

| (1.5) |

where is the average wealth (). The widely used inequality indicator Gini index measures the inequality in the wealth distribution and ranges from (no inequality) to (extreme inequality). Since all agents have the same amount of dollar initially (), the Gini index starts at zero (i.e. ). In the unbiased dynamics, the Gini index stabilizes around (which corresponds to the Gini index of an exponential distribution). The Gini index is strongly reduced in the poor-biased dynamics (). On the contrary, the Gini index keeps increasing in the rich-biased dynamics and seems to approach (its maximum). We study in more details this phenoma in section 5.3. We emphasize that the “rich-get-richer” phenomenon, numerically observed in the rich-biased dynamics in the present work, has also been reported in other models from econophysics, and we refer interested readers to [7, 8] and references therein.

1.2 Asymptotic dynamics: and

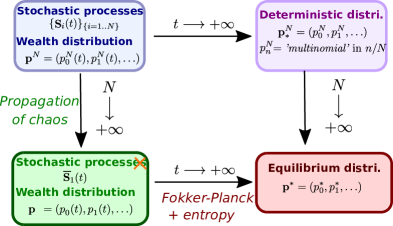

One of the main difficulty in any rigorous mathematical treatment lies in the general fact that models in econophysics typically consist of a large number of interacting (coupled) economic agents. Fortunately the framework of kinetic theories allows simplification of the mathematical analysis of certain such models under some appropriate limit processes. For the unbiased model (1.2) and the poor-biased model (1.3), instead of taking the large time limit and then the large population limit as in [31], we first take the large population limit to achieve a transition from the large stochastic system of interacting agents to a deterministic system of ordinary differential equations by proving the so-called propagation of chaos [48, 36, 37, 39] through a well-designed coupling technique, see figure 3 for a illustration of these strategies. After that, analysis of the deterministic description is then built on its (discrete) Fokker-Planck formulation and we investigate the convergence toward an equilibrium distribution by employing entropy methods. [3, 34, 28]. For the rich-biased model, we prove the propagation of chaos by virtue of a novel martingale-based technique introduced in [36], and we report some interesting numerical behavior of the associated ODE system. We illustrate the various (limiting) ODE systems obtained in the present work in figure 4.

For the poor-biased model, we present an explicit rate of convergence of its associated system of ordinary differential equations toward its equilibrium via the Bakry-Emery approach [4]. Then, we resort to numerical simulation in the determination of the sharp rate of convergence and a heuristic argument is used in support of our numerical observation.

This paper is organized as follows: in section 2, we briefly review different approaches to tackle the propagation of chaos. Section 3 is devoted to the investigation of the unbiased exchange model, where the rigorous large population limit is carried out via a coupling argument and the limiting system of ODEs is studied in detail. We perform the analysis, for the poor-biased model in section 4 and for the rich-biased model in section 5, in a parallel fashion that resembles section 3. A subsection is dedicated in 5.3 to the emergence of a dispersive traveling wave in the rich-biased dynamics. Finally, a conclusion is drawn in section 6.

2 Review propagation of chaos

2.1 Definition

We propose to review the method used to prove the so-called propagation of chaos. But first we need to carefully define what propagation of chaos means. With this aim, we consider a (stochastic) particle system denoted where particles are indistinguishable. In other words, the particle system is invariant by permutation, i.e. for any test function and permutation :

In particular, all the single processes for have the same law (but they are in general not independent). Denote by the density distribution of the process and let be the marginal density, i.e. the law of the process (for ):

Consider now a limit stochastic process where are independent and identically distributed. Denote by the law of a single process, thus by independence assumption the law of all the processes is given by:

Definition 1

We say that the stochastic process satisfies the propagation of chaos if for any fixed :

| (2.1) |

which is equivalent to have for any test function :

| (2.2) |

2.2 Coupling method

The coupling method [48] consists in generating the two processes and simultaneously in such a way that:

-

i)

and satisfy their respective law,

-

ii)

and are closed for all .

The main difficulty is that are independent but are not, thus the two processes cannot be too closed. In practice, we expect to find a bound of the form:

| (2.3) |

Such result is sufficient111using as a test function to prove (2.2) and therefore one deduces propagation of chaos.

2.3 Empirical distribution - tightness of measure

Another approach to prove propagation of chaos is to study the so-called empirical measure:

| (2.4) |

where is the Delta distribution, i.e. for a smooth test function the duality bracket is defined as:

| (2.5) |

Notice that is a distribution of a single variable, thus the domain of remains the same as increases which simplifies its study. However, is also a stochastic measure, i.e. is a random variable on the space of measures [6]. The link between propagation of chaos and empirical distribution relies on the following lemma.

Lemma 2.1

The stochastic process satisfies the propagation of chaos (2.1) if and only if:

| (2.6) |

i.e. for any test function the random variable converges in law to the constant value .

3 Unbiased exchange model

3.1 Definition and limit equation

We consider first the unbiased model that is briefly mentioned in the introduction above. For the three models investigated in this work, we consider a (closed) economic market consisting of agents with dollars per agents for some (fixed) , i.e. there are a total of dollars. We denote by the amount of dollars that agent has (i.e. and for any ).

Definition 2 (Unbiased Exchange Model)

The dynamics consist in choosing with uniform probability a “giver” and a “receiver” . If the receiver has at least one dollar (i.e. ), then it gives one dollar to the receiver . This exchange occurs according to a Poisson process with frequency .

The unbiased exchange model can be written as a stochastic differential equation [43, 46]. Introducing independent Poisson processes with constant intensity , the evolution of each is given by:

| (3.1) |

To gain some insight of the dynamics, we focus on and introduce some notations:

The two Poisson processes and are of intensity . The evolution of can be written as:

| (3.2) |

with Bernoulli distribution with parameter (i.e. ) representing the proportion of “rich” people:

| (3.3) |

Thus, the dynamics of can be seen as a compound Poisson process.

Motivated by (3.2), we give the following definition of the limiting dynamics of as from the process point of view.

Definition 3 (Asymptotic Unbiased Exchange Model)

We define to be the (nonlinear) compound Poisson process satisfying the following SDE:

| (3.4) |

in which and are independent Poisson processes with intensity , and independent Bernoulli variable with parameter

| (3.5) |

We denote by the law of the process , i.e. . Its time evolution is given by:

| (3.6) |

with:

| (3.7) |

and .

3.2 Coupling for the unbiased exchange model

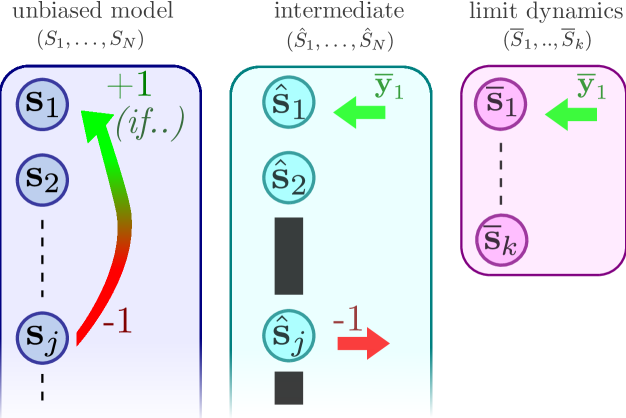

We now provide the coupling strategy to link the particle system with the limit dynamics . In [48], the core of the method is to use the same “noise” in both the particle system and the limit system. Unfortunately, it is not possible in our settings: the clocks cannot be used “as it” since they would correlate the jump of with the jump of which is not acceptable. Indeed, if and are independent, they cannot jump at (exactly) the same time.

For this reason, we have to introduce an intermediate dynamics, denoted by , which employs exactly the same “clocks” as our original dynamics (3.1), but the property of being rich or poor is decoupled.

Definition 4 (Intermediate model)

We define for to be a collection of identically distributed (nonlinear) compound Poisson processes satisfying the following SDEs for each :

| (3.9) | |||||

in which , the Poisson clocks () are the same as those used in (3.1), the two extra clocks and are independent with rate .

We do not use the “self-giving” clocks since we want to decouple the receiving and giving dynamics.

An schematic illustration of the above coupling technique is shown in Fig 5 below. We first have to control the difference between the process and the intermediate dynamics . The key idea is based on the following simple yet effective lemma that allows to create optimal coupling between two flipping coins [23].

Lemma 3.1

For any , there exist and such that .

Proof.

Let a uniform random variable. Define the Bernoulli random variables as and . It is straightforward to show that , and .

More generally, if and are two inhomogeneous Poisson processes with rate and , respectively, then there exists a coupling such that

This leads to the following proposition.

Proposition 3.2

Proof.

The processes and “share” the same clocks and for . Denote the ’rich or not’ random Bernoulli random variables:

| (3.11) |

Once a clock rings, the processes become:

| (3.12) |

Notice that the difference can only decay after the jump from the clock (the ’give’ dynamics reduce the difference). However, the ’receive’ dynamics from the clock could increase the difference if . More precisely, we find:

| (3.13) |

where the extra is due to the extra clocks and in (3.9).

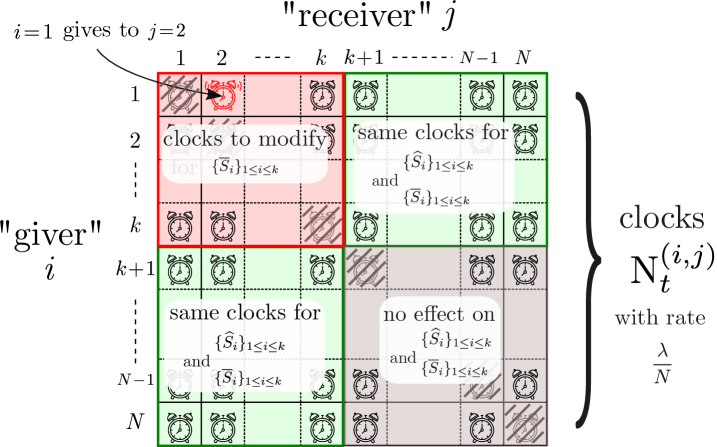

Now we have to couple the Bernoulli process with in a convenient way to make the difference as small as possible. Here is the strategy:

-

•

Step 1: generate a master Poisson clock with intensity which gives a collection of jumping times.

-

•

Step 2: to select which clock rings, calculate the proportions of “rich people” for the particle system and for the limit dynamics:

(3.14) -

•

Step 3: let a uniform random variable.

-

–

if , pick an index uniformly among the rich people (i.e. such that ), otherwise we pick uniformly among the poor people (i.e. such that ). Pick index uniformly among .

-

–

if , let , otherwise (i.e. ).

-

–

-

•

Step 4: if , update using (3.12)

Thanks to our coupling, the ’receiving’ dynamics of and will differ with probability :

| (3.15) |

Plug in the expression in (3.13) concludes the proof.

Remark. The update formula (3.12) for highlights that the ’give’ and ’receive’ dynamics are now independent in the auxiliary dynamics (i.e. and are independent). In contrast, we use the same process to update and .

Now we turn our attention to the coupling between the auxiliary dynamics and the limit dynamics for a fixed (while ). The idea is to remove the clocks for to decouple the time of the jump in and as described in the figure 6.

Proposition 3.3

Proof.

We assume to simplify the writing. To couple the two processes and , we use the same Bernoulli variable to generate both ’receive’ dynamics:

Meanwhile, the Poisson clocks are already determined in (3.9):

| (3.17) |

Unfortunately, we cannot use the same definition for the clocks and as the clocks and are not independent (they both contain the clock ). Thus, we need to remove those coupling clocks when defining and . Fortunately, we only have to generate the dynamics for process, thus we only have to replace the clocks and for (see figure 6):

| (3.18) |

where and are independent Poisson clocks with rate .

Using this coupling strategy, the difference could only increase (by ) if the clocks , , or ring for leading to (3.16).

Theorem 1

Let to be a solution to (3.1). Then for any fixed and , there exists a coupling between and (with the same initial conditions) such that:

| (3.19) |

with holding for each .

Proof.

We assume without loss of generality that . First, we show that the processes and remain closed. We denote:

We have:

where we use . To control the variance, we expand:

since is a Bernoulli variable its variance is bounded by . Controlling the covariance of and is more delicate since the two processes are not independent due to the clocks and . Fortunately, these clocks have a rate of only and thus the covariance has to remain small for a given time interval. To prove it, let’s use the independent processes and :

using Cauchy-Schwarz. Since the two processes and remain close, we deduce:

using proposition 3.3 (with ). We conclude that:

Going back to proposition 3.2, we find:

with . Using Gronwall’s lemma, since , we obtain:

| (3.20) |

We finally conclude by using proposition 3.3 and triangular inequality.

Remark. In the community of Markov chains, the process with can serve as an example a zero-range process [47], and it is also observed in [36] that the unbiased exchange model exhibits a cutoff phenomenon (see for instance [24, 1, 2]), which is now ubiquitous among literatures on interacting Markov chains.

3.3 Convergence to equilibrium

After we achieved the transition from the interacting system of SDEs (2) to the deterministic system of nonlinear ODEs (3.6), in this section we will analyze (3.6) with the intention of proving convergence of solution of (3.6) to its (unique) equilibrium solution. The main ingredient underlying our proof lies in the reformulation of (3.6) into a (discrete) Fokker-Planck type equation, combined with the standard entropy method [3, 34, 28]. We emphasize here that the convergence of the solution of (3.6) has already been established in [26, 36], but we include a sketch of our analysis here for the sake of completeness of the present manuscript.

To study the ODE system (3.6), we introduce some properties of the nonlinear binary collision operator , whose proof is merely a straightforward calculations and will be omitted.

Lemma 3.4

If is a solution of (3.6), then

| (3.21) |

In particular, the total mass and the mean value is conserved.

Thanks to these conservations, we have for all , where

is the space of probability mass functions with the prescribed mean value . Next, the equilibrium distribution of the limiting dynamics (3.6) is explicitly calculated.

Proposition 3.5

The (unique) equilibrium distribution in associated with the limiting dynamics (3.6) is given by:

| (3.22) |

where if we put initially that for some .

This elementary observation can be verified through straightforward computations, which we will omit here.

Next, we recall the definition of entropy [19], which will play a major role in the analysis of the large time behavior of the system (3.6).

Definition 5

(Entropy) For a given probability mass function , the entropy of is defined via

Remark. It can be readily seen through the method of Lagrange multipliers that the geometric distribution (3.22) has the least amount of entropy among probability mass functions from .

To prove (strong) convergence of the solution of (3.6) to its equilibrium solution (3.22), a major step is first to realize that the original ODE dynamics (3.6) can be reformulated as a variant of a Fokker-Planck equation [44]. Indeed, let us introduce with . Notice that . Thus, for we can deduce that

Setting , we obtain

| (3.23) |

with the convention that . This formulation leads to the following:

Proposition 3.6

Let be the solution to (3.6) and to be a continuous function, then

| (3.24) |

Corollary 3.7

Taking and for in (3.24), we recover the facts that and are preserved over time.

Inserting , we can deduce the following important result.

Proposition 3.8 (Entropy dissipation)

Let be the solution to (3.6) and be the associated entropy, then for all ,

where is defined by and for .

Proof.

It is worth noting that

so that indeed defines a probability distribution (for all ). Then we deduce from (3.24) that

in which () is the Kullback-Leiber divergence from the probability distribution to .

Remark. By a property of the Kullback-Leiber divergence [20], if and only if , but it can be readily shown that if and only if coincides with the equilibrium distribution .

Our next focus is on the demonstration of the strong convergence of solutions of (3.6) to its unique equilibrium solution given by (3.22). First of all, we notice that is clearly closed and bounded in for each , whence there exists some and a diverging sequence such that weakly in () as . In particular, we have the point-wise convergence

Our ultimate goal is to show that , for which we first establish the following proposition.

Proposition 3.9

Suppose that is a sequence of probability distributions in such that

weakly in for some . If the family satisfies the following uniform integrability condition [40]

| (3.25) |

for some , then

| (3.26) |

Proof.

It suffices to show that for any given , there exists some universal constant such that

| (3.27) |

Assume that holds uniformly in for some constant , where is fixed. Then for all and . Since is an increasing function for small , we have for some fixed sufficiently large that

and the proof is completed.

The next lemma ensures that the solution of our limiting ODE system (3.6) is uniformly integrable (in time), whose proof is elementary and is thus skipped.

Lemma 3.10

Let to be the solution of (3.6). Assume that for some , then for each fixed ,

holds uniformly in time.

We are now in a position to prove the desired convergence result.

Proposition 3.11

Proof.

Our proof follows closely to the general strategy presented in [42] and is in essence a continuity argument. We will denote the flow of the ODE system (3.6) with initial data by . It is recalled that we only need to show that . We argue by contradiction and suppose that . Since is strictly decreasing along trajectories of (3.6) and since weakly in () as , we deduce that by combining proposition 3.9 and proposition 3.10, whence

for all . But if , then for all we must have , and by continuity, it follows that for all sufficiently close to in the norm () we have for all . But then for and sufficiently large , we have

which contradicts the above inequality. Therefore we must have that and hence weakly in () as . In particular, we have the pointwise convergence

Now since

by taking to be sufficiently large and independent of , the desired strong convergence in for follows immediately.

4 Poor-biased exchange model

We now investigate our second model where the ’given’ dynamics is biased toward richer agent: the wealthier an agent becomes, the more likely it will give a dollar. As for the previous model, we first investigate the limit dynamics as the number of agents goes to infinity, then we study the large time behavior and show rigorously the convergence of the wealth distribution to a Poisson distribution.

4.1 Definition and limit equation

We use the same setting as the unbiased model: there are agents with initially the same amount of money with .

Definition 6 (Poor-biased exchanged model)

The dynamics consists in choosing a “giver” with a probability proportional to its wealth (the wealthier an agent, the more likely it will be a “giver”). Then it gives one dollar to a “receiver” chosen uniformly.

From another point of view, the dynamics consist in taking one dollar from the common pot (tax system) and re-distribute the dollar uniformly among the individuals. Thus instead of ‘taxing the agents’ in the unbiased exchange model, the poor-biased model is ‘taxing the dollar’.

The poor-biased model can be written in term of stochastic differential equation, the wealth of agent evolves according to:

| (4.1) |

with Poisson process with intensity .

Since the clocks are now time dependent (in contrast to the unbiased model), the dynamics might appear more difficult to analyze. But it turns out to be simpler, since the rate of receiving a dollar is constant:

where is the (conserved) initial mean. In contrast, in the unbias dynamics, the rate of receiving a dollar is equal to the proportion of rich people which fluctuates in time. Let’s focus on and sum up the clocks introducing:

| (4.2) |

where the two Poisson processes and have intensity and (respectively). Thus, the poor-biased model leads to the equation:

| (4.3) |

Notice that is not independent of as both processes can jump at the same time due to the two clocks and .

Motivated by the equation above, we give the following definition of the limiting dynamics as .

Definition 7

(Asymptotic Poor-biased model) We define to be the compound Poisson process satisfying the following SDE:

| (4.4) |

in which and are independent Poisson processes with intensity and (respectively) where is the mean of (i.e. ).

If we denote by the law of the process , its time evolution is given by:

| (4.5) |

with:

| (4.6) |

and .

4.2 Proof of propagation of chaos

The aim of this subsection is to prove the propagation of chaos, i.e. that the process converges to as goes to infinity. As for the unbiased exchange model, the key is to define the Poisson clocks for the limit dynamics and close to the clocks of the particle system and for , but at the same time making the clocks independent. With this aim, we have to ’remove’ the clocks and for .

Theorem 2

Proof.

To simplify the writing, we suppose . We define for the clocks for the limit dynamics as follow:

| (4.8) |

Here, is a Bernoulli random variable that prevents the clocks to ring for if the rates of the clocks from are too large compare to . The parameter of this Bernoulli random variable is given by:

| (4.9) |

with for any . On the contrary, the two processes and are used to compensate if the rates of the clocks and from are not large enough. Both processes and are independent (inhomogeneous) Poisson processes with rates respectively:

| (4.10) |

where for any . One can check that under the aforementioned setup (coupling of Poisson clocks), and are indeed independent counting processes with intensity and , respectively.

The difference could increase due to types of events:

-

i)

and ring for ,

-

ii)

and ring

-

iii)

ring for and .

Notice that the third type of event leads to:

| (4.11) |

i.e. only gives. However, the event only occurs if . Therefore, the event iii) could only make to decay.

Therefore, we deduce:

| (4.12) | |||||

using for any . Let’s bound the rates and :

We deduce from (4.12):

| (4.13) |

Applying the Gronwall’s lemma to (4.13) yields the result.

4.3 Large time behavior

After we achieved the transition from the interacting system of SDEs (4.1) to the deterministic system of linear ODEs (4.5), we now analyze the long time behavior of the distribution and its convergence to an equilibrium. The main tool behind proof relies again on the reformulation of (4.5) into a (discrete) Fokker-Planck type equation, in conjunction with the standard entropy method [3, 34, 28].

Let’s introduce a function space to study :

| (4.14) | |||||

| (4.15) |

where denote the vector space of square-summable sequences. In contrast to the unbias model with the dynamics (4.5), the operator is an unbounded operator (i.e. ). For any , it is straightforward to show that:

| (4.16) |

which express that the total mass and the mean value is conserved. Moreover, there exists a unique equilibrium for in given by a Poisson distribution:

| (4.17) |

To investigate the convergence of solution to (4.5) to the equilibrium (4.17), we introduce two function spaces.

Definition 8

We define the sub-vector spaces of :

| (4.18) | |||||

| (4.19) |

and define corresponding scalar products:

| (4.20) |

The advantage of using the scalar product is that the operator becomes symmetric. To prove it, we rewrite the operator a la Fokker-Planck.

Lemma 4.1

For any , we have:

| (4.21) |

with , and the convention .

Proof.

Since , we find

with . Using the notation and , we write:

Remark. Equation (4.21) has a flavor of a Fokker-Planck equation of the form

| (4.22) |

where is an equilibrium distribution to which converges (and may also depend on , making the equation nonlinear).

As a consequence, we deduce that the operator is symmetric on .

Proposition 4.2

Proof.

We simply use integration by parts:

Furthermore, the operator would have a so-called spectral gap if one can show that the norm controls the norm . To prove it, we establish a Poincaré inequality.

Lemma 4.3

Proof.

Similar to the standard proof of a classical Poincaré inequality we proceed by contradiction. Assume that no such exists, then there exists a sequence (of sequence) such that and

| (4.26) |

for all . Denote . Then we have and (4.26) reads

| (4.27) |

Without loss of generality, we can assume the normalization condition for all and thus . By weak compactness, there exists such that in and in particular for all .

Since , we also have for all , or equivalently, . Thus, and therefore for all . As , we must have and therefore . Contradiction, since for all .

As a result of the lemma, the operator has a spectral gap of at least since:

| (4.28) |

We shall establish the existence of a unique global solution to the linear ODE system (4.5). The key ingredient in our proof relies heavily on standard theory of maximal monotone operators (see for instance Chapter 7 of [9]).

Proposition 4.4

Proof.

We use the Hille-Yosida theorem and show that the (unbounded) linear operator on is a maximal monotone operator. The monotonicity of follows from its symmetric property on :

To show the maximality of , it suffices to show , i.e., for each , the equation admits at least one solution . To this end, the weak formulation of reads

| (4.29) |

whence the Lax-Milgram theorem yields a unique .

Theorem 3

Let be the solution of (4.5) and the corresponding equilibrium. Then:

| (4.30) |

where is the initial condition, i.e. .

Proof.

Taking the derivative of the square norm gives:

| (4.31) | |||||

using the symmetry of and the relation (4.24). Using the Poincaré constant from lemma (4.3), we deduce:

Applying the Gronwall’s lemma leads to the result.

To finish our investigation of the poor-biased dynamics, we would like to find an explicit rate for the decay of the solution toward the equilibrium , i.e. find an explicit value for the Poincaré constant in lemma (4.3). The key idea, due to Bakry and Emery [4], is to compute the second time derivative of .

Lemma 4.5

For any , we have:

| (4.32) |

Proof.

Using the symmetry of , we have:

with . Since , integration by parts gives:

Using , we deduce:

To conclude we have to show that . Notice that , thus:

Remark. In general, the computation of the second time derivative of the energy (in our case, ) requires a number of smartly-chosen integration by parts. However, these computations can actually be made more tractable and organized to some extent. We refer interested readers to [35, 29, 10] for ample illustration of the technique known as systematic integration by parts.

Proposition 4.6

The exponential decay rate in theorem (3) is at least , i.e. .

Proof.

Taking the second derivative and using the symmetry of give:

thanks to (4.32) and (4.31). Denoting , we have: . Integrating over the interval yields:

and the Gronwall’s lemma allows to obtain our result.

It remains to justify that . Theorem (3) already shows that . Moreover, denoting , we have . Thus, by Gronwall’s lemma, .

4.4 Numerical illustration poor-biased model

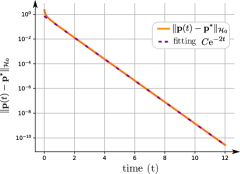

We investigate numerically the convergence of solution to the poor-biased model (4.5) to the equilibrium distribution (4.17). We use (average money) and (rate of jumps) for the model. To discretize the model, we use components to describe the distribution (i.e. ). As initial condition, we use and for . The standard Runge-Kutta fourth-order method (e.g. RK4) is used to discretize the ODE system (4.5) with the time step .

We plot in figure (7)-left the numerical solution at unit time and compare it to the equilibrium distribution . The two distributions are indistinguishable. Indeed, plotting the evolution of the difference (figure (7)-right) shows that the difference is already below . Moreover, the decay is clearly exponential as we use semi-logarithmic scale.

Notice that the numerical simulation suggests that the optimal decay rate of is , which is twice the analytical decay rate proved in proposition 4.6. The reason for this discrepancy is that the solution of remains in the subspace , i.e. the mean of is preserved. The analysis of the spectral gap of in the proposition 4.6 does not take account this constraint.

We numerically investigate the spectrum of denoted . The first eigenvalue satisfies due to the equilibrium (i.e. ). The other eigenvalues are and in particular the spectral gap is . One can find explicitly a corresponding eigenfunction given by:

| (4.33) |

Thus, for any , we find:

This explains why the effective spectral gap for the dynamics is given by and not : the solution (4.5) lives in and therefore it is orthogonal to .

Remark. We can find explicitly the exact formulation of the eigenfunction of for all . We find by induction:

| (4.34) |

leading to:

| (4.35) |

with binomial coefficient (i.e. ). Moreover, through an induction argument and some combinatorial identities, we can verify that for . We speculate that spans the entire space , but we do not have a proof for this conjecture.

5 Rich-biased exchange model

In our third model, the selection of the ’giver’ is biased toward the poor instead of the rich, i.e. the more money an individual has the less likely it will be chosen.

5.1 Definition and limit equation

As before, the definition of the model is given first.

Definition 9

(Rich-biased exchange model) A “giver” is chosen with inverse proportionality of its wealth. The “receiver” is chosen uniformly.

The rich-biased model leads to the following stochastic differential equation:

| (5.1) |

with Poisson process with intensity given by:

| (5.2) |

An agent receives a dollar at rate where is the inverse of the harmonic mean:

| (5.3) |

Definition 10

(Asymptotic Rich-biased model)

| (5.4) |

in which and are independent Poisson processes with intensity (if ) and respectively. The inverse mean is given by:

| (5.5) |

where the law of the process . The time evolution of is given by:

| (5.6) |

with:

| (5.7) |

We will also need the weak form of the operator: for any test function :

| (5.8) |

5.2 Propagation of chaos using empirical measure

We investigate the propagation of chaos for the rich-biased dynamics using the empirical measure (see subsection 2.3). We consider the solution to (5.1) and introduce the empirical measure:

| (5.9) |

The goal is to show that the stochastic measure converges to the deterministic density solution of (5.6). The main difficulty is that the empirical measure is a stochastic process on a Banach space and thus of infinite dimension. Fortunately, the space is a discreet (i.e. ) and therefore we do not have to consider stochastic partial differential equations which are famously difficult. Moreover, we only have to consider a finite number of possible jumps.

When agent gives a dollar to (i.e. ), the empirical measure is transformed as

| (5.10) |

To write down the evolution equation satisfied by , we regroup the agents with the same number of dollars (i.e. we project the dynamics on a subspace).

Proposition 5.1

The empirical measure (5.9) satisfies:

| (5.11) |

where independent Poisson clock with intensity:

| (5.12) |

where is the th coordinate of .

Proof.

Following the jump process given in (5.10), the empirical measure satisfies:

| (5.13) |

Introducing the Poisson process regrouping all the clocks corresponding to a giver with dollars giving to a receiver with dollars:

| (5.14) |

In this sum, each clock has the same intensity . Moreover, counting the number of clocks involved in the sum (5.14) leads to (5.12). The indicator is here to remove the self-giving clocks : when an agent gives to itself, nothing happens.

Corollary 5.2

Proof.

The operator (5.16) corresponds to the bias in the evolution of the empirical measure compared to the evolution of solution to the limit equation (5.6). This bias vanishes as goes to zero when the number of agents becomes large. The other source of discrepancy between and is the variance of (as it is a stochastic measure). Let’s review an elementary result on compensated Poisson process.

Remark. Denote a compound jump process and its compensated version:

| (5.17) |

where denotes the (independent) jumps and Poisson process with intensity and . The Ito’s formula is given by:

In particular, for , we obtain:

| (5.18) | |||||

Here, we assume that the jump is independent of the value . To generalize the formula, one has to replace by .

Motivated by this remark, we obtain the following result.

Proposition 5.3

Denote the compensated process of the empirical measure :

| (5.19) |

then is a -value martingale and satisfies:

| (5.20) |

Proof.

We are now ready to prove the propagation of chaos for the rich-biased dynamics by showing that the empirical measure converges to as . The key

Lemma 5.4

The operator (5.7) is globally Lipschitz on and is an bounded on .

| (5.23) | |||||

| (5.24) |

Proof.

Since , the rate of receiving (5.3) satisfies . Thus,

Summing in gives the result. We proceed similarly for the operator .

Theorem 4

Proof.

Remark. The martingale-based technique, developed in [36] and employed here for justifying the propagation of chaos, is remarkable since it does not require us to study the -particle process but solely its generator. One drawback is that this method might not work if the generator of the limit process is unbounded, which is the case for the generator of the (limit) poor-biased dynamics (4.5).

5.3 Dispersive wave leading to vanishing wealth

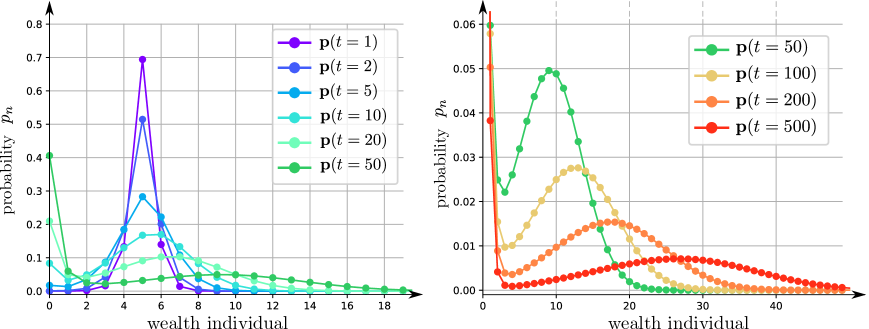

As illustrated in the introduction (figure 2), the rich-biased dynamics tend to accentuate inequality, i.e. the Gini index was approaching (its maximum value) for the agent-based model (1.4) (5.1). We would like to investigate numerically the behavior of the solution to the rich-biased dynamics using the limit equation (5.6) and the distribution .

In figure 8, we plot the evolution of the distribution starting from a Dirac distribution with mean (i.e. and for ). We observe that the distribution spreads in two parts: the bulk of the distribution moves toward zero whereas a smaller proportion is moving to the right. One can identify the two pieces as the “poor” and the “rich”. Thus, the dynamics could be interpreted as the poor getting poorer and the rich getting richer. Notice that the proportion of poor is increasing (e.g. is increasing) whereas the “rich” distribution resembles a dispersive traveling wave. Since both the total mass and the total amount of dollar are preserved (i.e. for any ), the dispersive traveling wave contains the bulk of the money but it is also vanishing in time.

To investigate more carefully the dispersive wave, we try to fit numerically its profile. After numerically examination, we choose to approximate by a Gaussian distribution. Meanwhile we approximate the “poor” distribution by a Dirac centered at zero . Thus, we approximate the distribution by the following Ansatz:

| (5.26) |

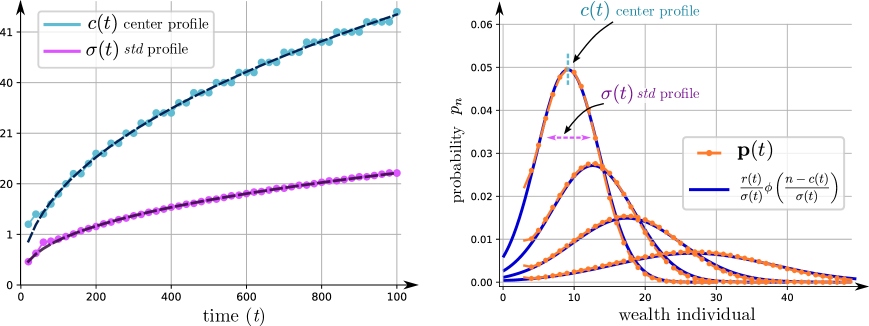

where is the standard normal distribution (i.e. ), is the center of the profile, its standard deviation and the proportion of rich. The speed of the wave and its standard deviation are estimated numerically and plotted in figure 9. Their growth is well-approximated by a power-law of the form:

| (5.27) |

Since the total amount of money is preserved, the proportion of rich can be easily deduced from since we must have . Such approximation leads to the fitting in figure 8-right (dotted-black curves). We notice that the proportion of rich in our Ansatz is vanishing:

| (5.28) |

Thus, we make the conjecture that converges weakly toward , i.e. all the money will asymptotically disappear.

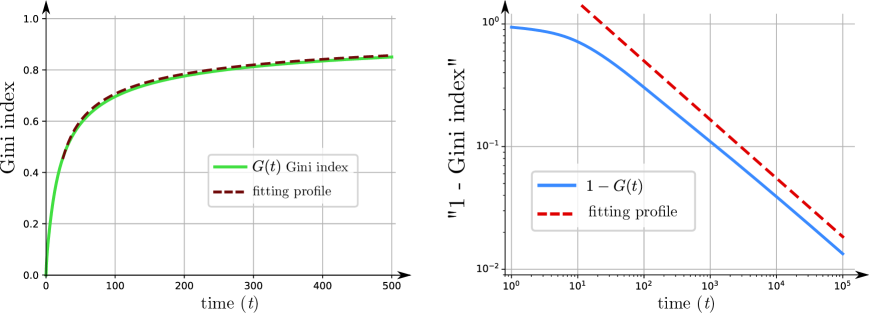

To further assess our conjecture, we measure the evolution of the Gini index for the distribution :

| (5.29) |

with the standard mean. Using the Ansatz (5.26), we can approximate the value of the Gini index given (see appendix 7.2):

| (5.30) |

We plot in figure 10-left the evolution of the Gini index along with its approximation (5.30). We observe a good agreement between the two curves. To examine closely the long time behavior of the curves, we plot the evolution of in log-scales (figure 10-right) over a longer time interval (up to ). Both curves seem to converges similarly toward (indicating that ) with a slight overshoot for the Ansatz. This overshoot might be due to our approximation that the “poor distribution” of is concentrated exactly at zero (i.e. ). This approximation amplifies the inequality between the “poor” and “rich” parts of the distribution and hence increases slightly the Gini index. But overall the asymptotic behavior of the Gini index for matches with the formula (5.30) and thus strengthens our assumption that will converge (weakly) to a Dirac . However, further analytically studies are needed to derive the asymptotic behavior of directly from the rich-biased evolution equation (5.6).

6 Conclusion

In this manuscript, we have investigated three related models for money exchange originated from econophysics. For the unbiased and poor biased dynamics, we rigorously proved the so-called propagation of chaos by virtue of a coupling technique, and we found an explicit rate of convergence of the limit dynamics for the poor biased model thanks to the Bakry-Emery approach. We have also introduced a more challenging dynamics referred to as the rich biased model, and a propagation of chaos result was established via a powerful martingale-based argument presented in [36]. In contrast to the two other dynamics, the rich-biased dynamics do not converge (strongly) to an equilibrium. Instead, we have found numerically evidence of the emergence of a (vanishing) dispersive wave. Such wave of extreme wealthy individual increases the inequality in the wealth distribution making the corresponding Gini index converging to its maximum .

Although we have shown numerically strong evidence of a dispersive wave, it is desirable to derive such emerging behavior directly from the evolution equation. One direction of future work would be to derive space continuous dynamics of evolution equations in order to investigate analytically the profile of traveling waves. However, space continuous description such as the uniform reshuffling model could lead to additional challenges. For instance, proving propagation of chaos using the martingale technique for the uniform reshuffling model was more involved [11].

From a modeling perspective, one should explore how selecting the "receiver" as well as the "giver" could impact the dynamics. Indeed, in the three dynamics studied in the manuscript, the re-distribution process (how the one-dollar is redistributed) is uniform among all the agent. It would be reasonable to have the redistribution of the dollar based on the individual wealth (e.g. poor individual being more likely to receive a dollar). The interplay between receiver and giver selection could lead to novel emerging behaviors.

7 Appendix

7.1 Proof of lemma 2.1

Proof.

Suppose first that the stochastic process satisfies the propagation of chaos. Let be a test function, a random variable and a constant. For notation convenience, we write . To prove that converges in law to , it is sufficient to prove the convergence in :

using (2.2) with and .

Proving the converse is more challenging. Let’s take as test function and denote the random variable for all . By assumption, converges in law to the constant . We deduce:

Since each converges to the constant , all the product in convergence to zero using Slutsky’s theorem. For , we use the invariance by permutations:

where is the set of all the permutations of elements in and in particular . To conclude, we split the set in two parts:

Thus, denoting an upper-bound for any :

7.2 Gini index dispersive wave

We estimate the Gini coefficient for a (continuous) distribution of the form:

| (7.4) |

where is the standard normal distribution, some positive constant with . The law can be represented by a random variable:

| (7.5) |

with random Bernoulli variable with probability (i.e. ), a random variable with normal law (i.e. ), and being independent. To estimate the Gini index of , we take two independent random variables and with such law and estimate the expectation of their difference:

| (7.6) | |||||

We then take the conditional expectation with respect to and :

| (7.7) | |||||

For large , we made the approximation . Moreover, the expectation of the difference between two standard Gaussian random variables is known explicitly: . We deduce:

| (7.8) |

Furthermore, if , we obtain:

| (7.9) |

References

- [1] David Aldous. Random walks on finite groups and rapidly mixing Markov chains. In Séminaire de Probabilités XVII 1981/82, pages 243–297. Springer, 1983.

- [2] David Aldous and Persi Diaconis. Shuffling cards and stopping times. The American Mathematical Monthly, 93(5):333–348, 1986.

- [3] Anton Arnold, Peter Markowich, Giuseppe Toscani, and Andreas Unterreiter. On convex Sobolev inequalities and the rate of convergence to equilibrium for Fokker-Planck type equations. 2001. Publisher: Taylor & Francis.

- [4] Dominique Bakry and Michel Émery. Diffusions hypercontractives. In Séminaire de Probabilités XIX 1983/84, pages 177–206. Springer, 1985.

- [5] Alethea BT Barbaro and Pierre Degond. Phase transition and diffusion among socially interacting self-propelled agents. Discrete & Continuous Dynamical Systems-B, 19(5):1249, 2014. Publisher: American Institute of Mathematical Sciences.

- [6] Patrick Billingsley. Convergence of probability measures. John Wiley & Sons, 2013.

- [7] Bruce M. Boghosian, Adrian Devitt-Lee, Merek Johnson, Jie Li, Jeremy A. Marcq, and Hongyan Wang. Oligarchy as a phase transition: The effect of wealth-attained advantage in a Fokker–Planck description of asset exchange. Physica A: Statistical Mechanics and its Applications, 476:15–37, 2017. Publisher: Elsevier.

- [8] Bruce M. Boghosian, Merek Johnson, and Jeremy A. Marcq. An H theorem for Boltzmann’s equation for the Yard-Sale Model of asset exchange. Journal of Statistical Physics, 161(6):1339–1350, 2015. Publisher: Springer.

- [9] Haim Brezis. Functional analysis, Sobolev spaces and partial differential equations. Springer Science & Business Media, 2010.

- [10] Mario Bukal, Ansgar Jüngel, and Daniel Matthes. Entropies for radially symmetric higher-order nonlinear diffusion equations. Communications in Mathematical Sciences, 9(2):353–382, 2011. Publisher: International Press of Boston.

- [11] Fei Cao, Pierre-Emmanuel Jabin, and Sebastien Motsch. Entropy dissipation and propagation of chaos for the uniform reshuffling model. arXiv preprint arXiv:2104.01302, 2021.

- [12] Eric Carlen, Robin Chatelin, Pierre Degond, and Bernt Wennberg. Kinetic hierarchy and propagation of chaos in biological swarm models. Physica D: Nonlinear Phenomena, 260:90–111, 2013. Publisher: Elsevier.

- [13] Eric Carlen, Pierre Degond, and Bernt Wennberg. Kinetic limits for pair-interaction driven master equations and biological swarm models. Mathematical Models and Methods in Applied Sciences, 23(07):1339–1376, 2013. Publisher: World Scientific.

- [14] Anirban Chakraborti and Bikas K. Chakrabarti. Statistical mechanics of money: how saving propensity affects its distribution. The European Physical Journal B-Condensed Matter and Complex Systems, 17(1):167–170, 2000.

- [15] Anirban Chakraborti, Ioane Muni Toke, Marco Patriarca, and Frédéric Abergel. Econophysics review: I. Empirical facts. Quantitative Finance, 11(7):991–1012, 2011.

- [16] Anirban Chakraborti, Ioane Muni Toke, Marco Patriarca, and Frédéric Abergel. Econophysics review: II. Agent-based models. Quantitative Finance, 11(7):1013–1041, 2011.

- [17] Arnab Chatterjee, Bikas K. Chakrabarti, and S. S. Manna. Pareto law in a kinetic model of market with random saving propensity. Physica A: Statistical Mechanics and its Applications, 335(1-2):155–163, 2004.

- [18] Arnab Chatterjee, Sudhakar Yarlagadda, and Bikas K. Chakrabarti. Econophysics of wealth distributions: Econophys-Kolkata I. Springer Science & Business Media, 2007.

- [19] Thomas M. Cover. Elements of information theory. John Wiley & Sons, 1999.

- [20] Imre Csiszár and Paul C. Shields. Information theory and statistics: A tutorial. Foundations and Trends® in Communications and Information Theory, 1(4):417–528, 2004.

- [21] Ms Era Dabla-Norris, Ms Kalpana Kochhar, Mrs Nujin Suphaphiphat, Mr Frantisek Ricka, and Ms Evridiki Tsounta. Causes and consequences of income inequality: A global perspective. International Monetary Fund, 2015.

- [22] Jakob De Haan and Jan-Egbert Sturm. Finance and income inequality: A review and new evidence. European Journal of Political Economy, 50:171–195, 2017. Publisher: Elsevier.

- [23] Frank den Hollander. Probability theory: The coupling method. Lecture notes available online (http://websites. math. leidenuniv. nl/probability/lecturenotes/CouplingLectures. pdf), 2012.

- [24] Persi Diaconis. The cutoff phenomenon in finite Markov chains. Proceedings of the National Academy of Sciences, 93(4):1659–1664, 1996.

- [25] Adrian Dragulescu and Victor M. Yakovenko. Statistical mechanics of money. The European Physical Journal B-Condensed Matter and Complex Systems, 17(4):723–729, 2000.

- [26] Benjamin T. Graham. Rate of relaxation for a mean-field zero-range process. The Annals of Applied Probability, 19(2):497–520, 2009.

- [27] Els Heinsalu and Marco Patriarca. Kinetic models of immediate exchange. The European Physical Journal B, 87(8):170, 2014.

- [28] Ansgar Jüngel. Entropy methods for diffusive partial differential equations. Springer, 2016.

- [29] Ansgar Jüngel and Daniel Matthes. An algorithmic construction of entropies in higher-order nonlinear PDEs. Nonlinearity, 19(3):633, 2006. Publisher: IOP Publishing.

- [30] Ryszard Kutner, Marcel Ausloos, Dariusz Grech, Tiziana Di Matteo, Christophe Schinckus, and H. Eugene Stanley. Econophysics and sociophysics: Their milestones & challenges. Physica A: Statistical Mechanics and its Applications, 516:240–253, 2019. Publisher: Elsevier.

- [31] Nicolas Lanchier. Rigorous Proof of the Boltzmann–Gibbs Distribution of Money on Connected Graphs. Journal of Statistical Physics, 167(1):160–172, 2017.

- [32] Nicolas Lanchier and Stephanie Reed. Rigorous results for the distribution of money on connected graphs. Journal of Statistical Physics, 171(4):727–743, 2018.

- [33] Nicolas Lanchier and Stephanie Reed. Rigorous results for the distribution of money on connected graphs (models with debts). Journal of Statistical Physics, pages 1–23, 2018.

- [34] Daniel Matthes. Entropy methods and related functional inequalities. Lecture Notes, Pavia, Italy. http://www-m8. ma. tum. de/personen/matthes/papers/lecpavia. pdf, 2007.

- [35] Daniel Matthes, Ansgar Jüngel, and Giuseppe Toscani. Convex Sobolev inequalities derived from entropy dissipation. Archive for rational mechanics and analysis, 199(2):563–596, 2011. Publisher: Springer.

- [36] Mathieu Merle and Justin Salez. Cutoff for the mean-field zero-range process. Annals of Probability, 47(5):3170–3201, 2019. Publisher: Institute of Mathematical Statistics.

- [37] Sylvie Méléard and Sylvie Roelly-Coppoletta. A propagation of chaos result for a system of particles with moderate interaction. Stochastic processes and their applications, 26:317–332, 1987.

- [38] Giovanni Naldi, Lorenzo Pareschi, and Giuseppe Toscani. Mathematical modeling of collective behavior in socio-economic and life sciences. Springer Science & Business Media, 2010.

- [39] Karl Oelschlager. A martingale approach to the law of large numbers for weakly interacting stochastic processes. The Annals of Probability, 12(2):458–479, 1984.

- [40] Bernt Oksendal. Stochastic differential equations: an introduction with applications. Springer Science & Business Media, 2013.

- [41] Eder Johnson de Area Leão Pereira, Marcus Fernandes da Silva, and HB de B. Pereira. Econophysics: Past and present. Physica A: Statistical Mechanics and its Applications, 473:251–261, 2017. Publisher: Elsevier.

- [42] Lawrence Perko. Differential equations and dynamical systems, volume 7. Springer Science & Business Media, 2013.

- [43] Nicolas Privault. Stochastic finance: an introduction with market examples. Chapman and Hall/CRC, 2013.

- [44] Hannes Risken. Fokker-planck equation. In The Fokker-Planck Equation, pages 63–95. Springer, 1996.

- [45] Gheorghe Savoiu. Econophysics: Background and Applications in Economics, Finance, and Sociophysics. Academic Press, 2013.

- [46] Steven E. Shreve. Stochastic calculus for finance II: Continuous-time models, volume 11. Springer Science & Business Media, 2004.

- [47] Frank Spitzer. Interaction of Markov processes. In Random Walks, Brownian Motion, and Interacting Particle Systems, pages 66–110. Springer, 1991.

- [48] Alain-Sol Sznitman. Topics in propagation of chaos. In Ecole d’été de probabilités de Saint-Flour XIX—1989, pages 165–251. Springer, 1991.