Actuarial strategy for pricing Asian options under a mixed fractional Brownian motion with jumps

Abstract.

The mixed fractional Brownian motion () has become quite popular in finance, since it allows one to model long-range dependence and self-similarity while remaining, for certain values of the Hurst parameter, arbitrage-free. In the present paper, we propose approximate closed-form solutions for pricing arithmetic Asian options on an underlying described by the . Specifically, we consider both arithmetic Asian options and arithmetic Asian power options, and we obtain analytical formulas for pricing them based on a convenient approximation of the strike price. Both the standard and the with Poisson log-normally distributed jumps are taken into account.

Key words and phrases:

Mixed fractional Brownian motion; Asian options; Power options; Jump-diffusion; Option pricing2010 Mathematics Subject Classification:

91G20; 91G80; 60G221. Introduction

As documented by several empirical studies, returns of financial assets are often affected by long-range dependence and self-similarity, and thus several scholars have proposed to model them by using the so-called fractional Brownian motion () with Hurst exponent , see, e.g., [9], [12], [17]. Nevertheless, as shown in [3], and [7], the is not arbutrage-free, and thus, some authors [6], [13], [14], [28] have proposed to use the so-called mixed fractional Brownian motion (), i.e., a linear combination of the Wiener process and the itself. When the Hurst exponent of the is greater than , the results in a Gaussian long-memory process suitable for modeling the returns of financial assets. Furthermore, as shown in [6], if is greater than the is arbitrage-free. Therefore, the has been largely employed for pricing various kinds of derivatives, including stock options [2], [5], [25], equity warrants [26], currency options [22, 20, 19], and credit derivatives [10].

The has also been used for pricing Asian options, i.e. options whose payoff depends on the average, either geometric or arithmetic, of the underlying asset over the whole option’s lifespan [18]. In particular, [16] obtained an exact closed-form solution for geometric Asian options, [27] derived an exact analytical formula for geometric Asian power options, [25] proposed an exact closed-form solution for geometric Asian rainbow options on two underlying assets, which was generalized to the case on an arbitrarily large number of underlying assets in [1]. Furthermore, [15] considered a with jumps and obtained an exact analytical formula for valuing geometric Asian power options.

All the exact closed-form solutions proposed in the aforementioned papers are valid for Asian options of geometric type. By contrast, for arithemtic Asian options, exact closed-form solutions cannot be found, and thus some numerical approximation is required. To this aim, some researchers have proposed to apply the Monte Carlo simulation method, which could also be enhanced by using the price of a geometric Asian option as a control variate (see [15]). Nevertheless, this approach, albeit flexible and relatively simple to implement, has the disadvantage of being very slow to converge.

Therefore, in this paper we propose the use of approximate closed-form solutions. Specifically, we consider both arithmetic Asian options and arithmetic Asian power options, and we value them by applying an analytical formula that we obtain by a convenient approximation of the strike price. Both the standard and the with Poisson log-normally distributed jumps are taken into account.

The remainder of the paper is organized as follows: in Section 2 we describe the with jumps and present exact analytical formulas for pricing Asian options of geometric type. In Section 3 we derive an approximate closed-form solution for pricing arithmetic Asian options, which in Section 4 we extend to arithmetic Asian power options. Finally, Section 5 concludes.

2. Preliminaries

We assume that the following assumptions hold:

-

(i)

the dynamics of the stock price is governed by the following equation

(2.1) where is a non-random function of , and, , are constants; and are a standard Brownian motion and a respectively; is a poisson process with rate ; is jump size which is a sequence of independent identically distributed and . Moreover, all three sources of randomness, the and and are supposed to be independent;

-

(ii)

the risk free interest rate and dividend rate are known and constant through time;

-

(iii)

the option can be exercised only at the maturity time;

-

(iv)

there are no transaction costs in buying or selling the stocks or option.

Based on option valuation strategy and risk neutral measure (cf.Refs.[8, 21]), the dynamics of the stock price process can be written as:

| (2.2) |

Lemma 2.1.

| (2.3) |

where .

Proof.

| (2.4) | |||||

and

| (2.5) | |||||

Then,

| (2.6) |

∎

This section deals with the new pricing model for the currency options using the actuarial approach, when the spot exchange rate follows the with jumps process. This model can be applied to different financial markets such as: in the arbitrage-free, equilibrium and complete markets and also in the arbitrage,non-equilibrium and incomplete markets.

Definition 2.1.

([4]) The expectation return rate of on is defined to as follows:

| (2.7) |

where is the continuously compounding ram of return of at time .

Definition 2.2.

Let be the average price of the underlying asset over the predetermined interval. Then, the value of geometric Asian options with exercise price and maturity time by actuarial approach are as follows:

| (2.8) |

for Asian call option, where .

| (2.9) |

for Asian put option, .

Theorem 2.1.

Let the stock price satisfy Equation (2.2). Then, the value of geometric Asian options with exercise price is given by

| (2.10) | |||||

for the call options, and

| (2.11) | |||||

for the put options, where

| (2.12) |

and is cumulative normal density function.

Proof.

We know that and . If and , then and . Given that and is a sequence of independent identically distributed, we have ; and for we have . Then for , it follows

| (2.13) |

| (2.14) | |||||

here

| (2.15) |

Let,

| (2.16) |

and

| (2.17) |

We know that the random variable has Gaussian distribution under the risk-neutral probability measure. Let and denote the mean and the variance of the random variable , respectively. If , then

| (2.18) | |||||

and

| (2.19) | |||||

The random variable is log-normally distributed and the random variable has the Gaussian distribution with the mean and the variance as obtained above. Then, from Eq. (2.8), the price of geometric Asian call option is:

| (2.20) | |||||

where and . Let

| (2.21) | |||||

Observe that

| (2.22) | |||||

and

| (2.23) | |||||

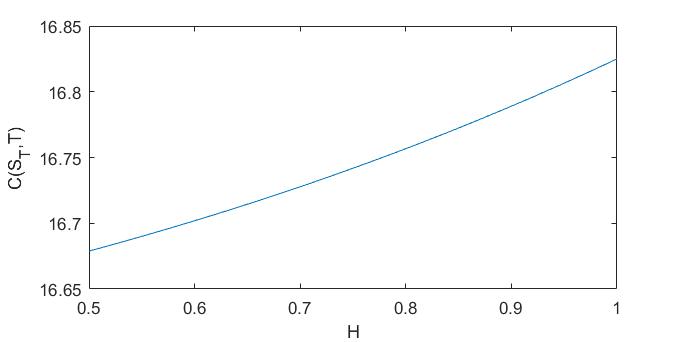

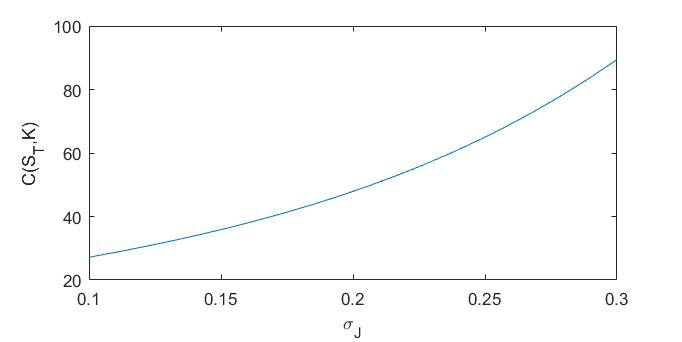

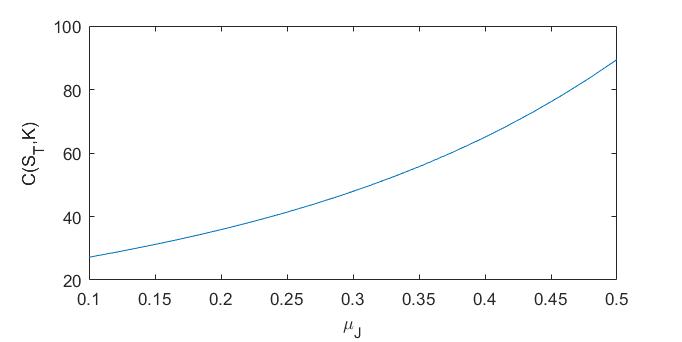

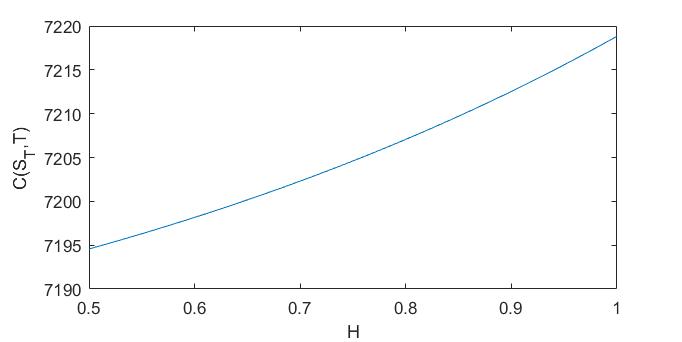

In Figs 1-3 we show the price of the geometric Asian option computed using formula (2.10) as a function of the Hurst and the jump parameters.

3. Arithmetic Asian option

Lemma 3.1.

([24])

An approximate value of the arithmetic Asian option is given by

| (3.1) |

where ia the geometric Asian option and is the adjusted strike price as follows

| (3.2) |

Now, based on the actuarial approach an approximate of the arithmetic Asian options are proposed [23, 11].

Theorem 3.1.

An approximate value of the arithmetic Asian option is given by

| (3.3) | |||||

for the call options, and

| (3.4) | |||||

for the put options, where

| (3.5) |

and is cumulative normal density function.

Proof.

| (3.7) | |||||

From Theorem 3.1, to provide an approximation of the arithmetic Asian options, we need to calculate the new exercise price ,

Suppose, and be the geometric and arithmetic average, respectively. Since the geometric average is less than the arithmetic average, , the geometric option price is a lower bound for the arithmetic option price

| (3.9) |

The inequality

| (3.10) | |||||

leads to the upper bound

| (3.11) |

Therefore, we have the following bounds on the arithmetic option price

| (3.12) |

To compute the upper bound we need to compute the mean of arithmetic average, which is obtained in Theorem 3.1.

Theorem 3.2.

The pricing error of arithmetic approximate vale is given by

| (3.13) |

Proof.

Sine

| (3.14) | |||||

it follows that

| (3.15) | |||||

The analogous bounds exert for the exact value , then the absolute difference between and is less than the difference between the upper and lower bounds

| (3.16) | |||||

∎

4. Asian power options

This section is deals with evaluate Asian power options by using actuarial approach in a mixed fractional Brownian motion with jumps environment. From [some references], we know that the payoff function of Asian options is given by and for the geometric and arithmetic call options with some integer , respectively.

Theorem 4.1.

Proof.

For the geometric Asian power options, the payoff function is . Using the strategy given in proof of Theorem 2.1, then we have

| (4.3) | |||||

where and . Let

| (4.4) | |||||

Observe that

| (4.5) | |||||

and

| (4.6) | |||||

∎

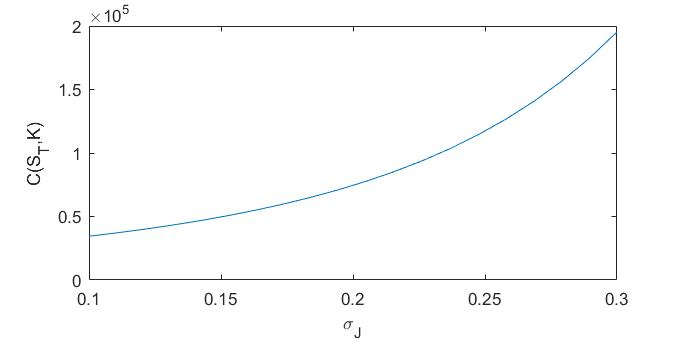

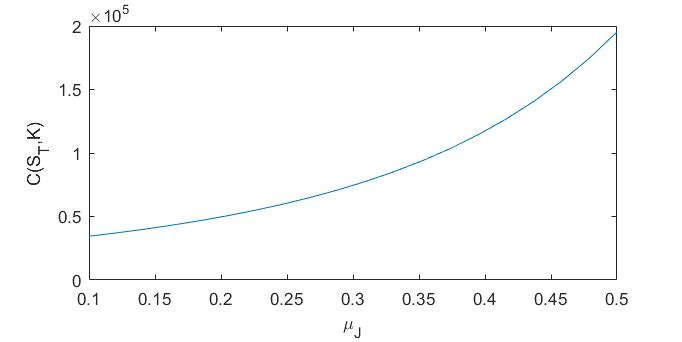

In Figs 5-7 we show the price of the power Asian option computed using formula 4.1 as a function of the Hurst and the jump. parameters.

.

.

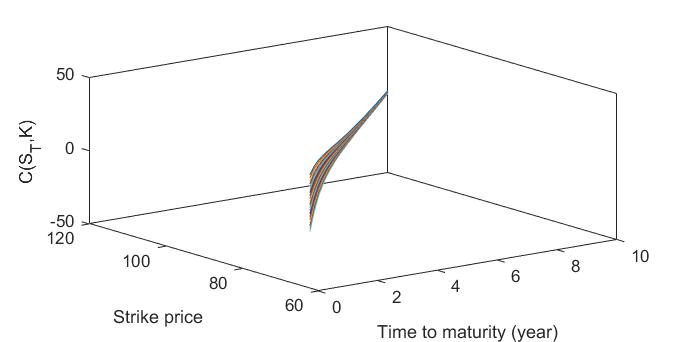

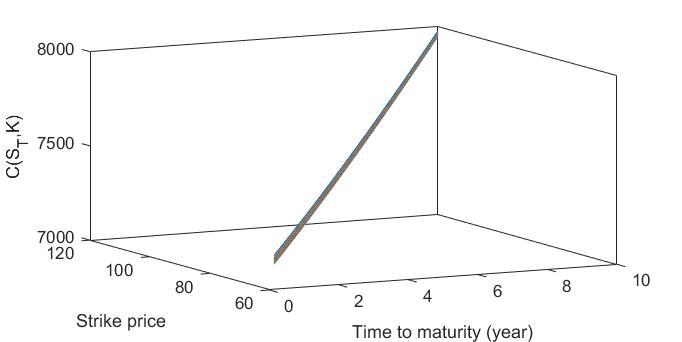

In Fig 8 we show the price of the power Asian option computed using formula 4.1 as a function of the strike price and of the maturity.

The payoff function of the power Asian power call option is , then its approximate value is given by the following theorem.

Theorem 4.2.

An approximate value of the arithmetic Asian power option is given by

| (4.7) | |||||

for the call options, and

| (4.8) | |||||

for the put options, where and other parameters are defined in Theorem 3.1.

5. Conclusions

We derived approximate closed-form solutions for pricing arithmetic Asian options on an underlying described by the mixed fractional Brownian motion (). In the last decade, the has gained increasing popularity in finance, since it allows one to incorporate long-range dependence and self-similarity and, for certain values of the Hurst parameter, it is arbitrage-free. In the present paper, suitable approximate closed-form solutions are obtained for both arithmetic Asian options and arithmetic Asian power options, by applying a convenient approximation of their strike prices. Both the standard and the with Poisson log-normally distributed jumps are considered.

References

- [1] D. Ahmadian and L. V. Ballestra. Pricing geometric Asian rainbow options under the mixed fractional Brownian motion. Physica A: Statistical Mechanics and its Applications, 555:124458, 2020.

- [2] L. V. Ballestra, G. Pacelli, and D. Radi. A very efficient approach for pricing barrier options on an underlying described by the mixed fractional Brownian motion. Chaos, Solitons & Fractals, 87:240–248, 2016.

- [3] C. Bender and R. J. Elliott. Arbitrage in a discrete version of the Wick-fractional Black-Scholes market. Mathematics of Operations Research, 29:935–945, 2004.

- [4] Mogens Bladt and Tina Hviid Rydberg. An actuarial approach to option pricing under the physical measure and without market assumptions. Insurance: Mathematics and Economics, 22(1):65–73, 1998.

- [5] J. H Chen, F. Y. Ren, and W. Y. Qiu. Option pricing of a mixed fractional-fractional version of the Black-Scholes model. Chaos, Solitons & Fractals, 21:1163–1174, 2004.

- [6] P. Cheridito. Mixed fractional Brownian motion. Bernoulli, 7:913–934, 2001.

- [7] P. Cheridito. Arbitrage in fractional Brownian motion models. Finance and Stochastics, 7:533–553, 2003.

- [8] Patrick Cheridito. Arbitrage in fractional Brownian motion models. Finance and Stochastics, 7(4):533–553, 2003.

- [9] Z. Ding, C. W. J. Granger, and R. F. Engle. A long memory property of stock market returns and a new model. Journal of Empirical Finance, 1:83–106, 1993.

- [10] X. He and W. Chen. The pricing of credit default swaps under a generalized mixed fractional Brownian motion. Physica A: Statistical Mechanics and its Applications, 404:26–33, 2014.

- [11] Angelien GZ Kemna and Antonius CF Vorst. A pricing method for options based on average asset values. Journal of Banking & Finance, 14(1):113–129, 1990.

- [12] A. W. Lo. Long-term memory in stock market prices. Econometrica, 59:1279–1313, 1991.

- [13] Y. S. Mishura. Stochastic Calcular for Fractional Brownian Motion and Related Process. Springer–Verlag, Berlin, 2008.

- [14] Y. S. Mishura and E. Valkeila. The absence of arbitrage in a mixed Brownian fractional Brownian model. In Proceedings of the Steklov Institute of Mathematics, number 237, pages 224–233. Trudy Matematicheskogo Instituta Imeni V.A. Steklova, 2002.

- [15] B. Peng and F. Peng. Pricing Asian power options under jump-fraction process. Journal of Economics Finance and Administrative Science, 17:2–9, 2012.

- [16] B. L. S. Prakasa Rao. Pricing geometric Asian power options under mixed fractional Brownian motion environment. Physica A: Statistical Mechanics and its Applications, 446:92–99, 2012.

- [17] S. Rostek and R. Schöbel. A note on the use of fractional Brownian motion for financial modeling. Economic Modelling, 30:30–35, 2013.

- [18] Foad Shokrollahi. The evaluation of geometric Asian power options under time changed mixed fractional Brownian motion. Journal of Computational and Applied Mathematics, 344:716–724, 2018.

- [19] Foad Shokrollahi and Adem Kılıçman. Pricing currency option in a mixed fractional Brownian motion with jumps environment. Mathematical Problems in Engineering, 2014, 2014.

- [20] Foad Shokrollahi and Adem Kılıçman. Actuarial approach in a mixed fractional Brownian motion with jumps environment for pricing currency option. Advances in Difference Equations, 2015(1):1–8, 2015.

- [21] Steven E Shreve. Stochastic calculus for finance II: Continuous-time models, volume 11. Springer Science & Business Media, 2004.

- [22] L. Sun. Pricing currency options in the mixed fractional Brownian motion. Physica A: Statistical Mechanics and its Applications, 392:3441–3458, 2013.

- [23] Stuart M Turnbull and Lee Macdonald Wakeman. A quick algorithm for pricing European average options. Journal of Financial and Quantitative Analysis, pages 377–389, 1991.

- [24] Ton Vorst. Prices and hedge ratios of average exchange rate options. International Review of Financial Analysis, 1(3):179–193, 1992.

- [25] X.-T. Wang, E.-H. Zhu, M.-M. Tang, and H.-G. Yan. Scaling and long-range dependence in option pricing II: Pricing European option with transaction costs under the mixed Brownian–fractional Brownian model. Physica A: Statistical Mechanics and its Applications, 3:445–451, 2010.

- [26] W. L. Xiao, W. G. Zhang, X. Zhang, and X. Zhang. Pricing model for equity warrants in a mixed fractional Brownian environment and its algorithm. Physica A: Statistical Mechanics and its Applications, 391:6418–6431, 2012.

- [27] W. G. Zhang, Z. Li, and Y. J. Liu. Analytical pricing of geometric Asian power options on an underlying driven by a mixed fractional Brownian motion. Physica A: Statistical Mechanics and its Applications, 490:402–418, 2018.

- [28] M. Zili. On the mixed fractional Brownian motion. Journal of Applied Mathematics and Stochastic Analysis, ID 32435:1–9, 2006.