Weak equilibria for time-inconsistent control: with applications to investment-withdrawal decisions

Abstract

This paper considers time-inconsistent problems when control and stopping strategies are required to be made simultaneously (called stopping control problems by us). We first formulate the time-inconsistent stopping control problems under general multi-dimensional controlled diffusion model and propose a formal definition of their equilibria. We show that an admissible pair of control-stopping policy is equilibrium if and only if the auxiliary function associated with it solves the extended HJB system, providing a methodology to verify or exclude equilibrium solutions. We provide several examples to illustrate applications to mathematical finance and control theory. For a problem whose reward function endogenously depends on the current wealth, the equilibrium is explicitly obtained. For another model with a non-exponential discount, we prove that any constant proportion strategy can not be equilibrium. We further show that general non-constant equilibrium exists and is described by singular boundary value problems. This example shows that considering our combined problems is essentially different from investigating them separately. In the end, we also provide a two-dimensional example with a hyperbolic discount.

Keywords:

Time-inconsistency, Weak equilibria, Stopping-control problems, Extended HJB system, Sophisticated decision makers.

AMS Subject Classification (2010): 93E20, 60G40, 91A40, 91G80.

1 Introduction

In economics and finance, it is common that people make control and stopping decisions simultaneously. When making investment decisions, they are usually free to terminate the investment discretionarily; when participating the gambling, besides how much to bet, when to exit the casino is also an important decision to make; when provided with a voluntary early retirement option, they shall simultaneously decide how much to consume before (and after) retirement and when to retire.

In this paper, under the general multi-dimensional controlled diffusion model, we provide a solution theory for the stopping control problems with pay-offs of the form

Unlike stopping control problems in existing literature, our problems are generally time-inconsistent because the reward function depends on the starting states . Time-inconsistency appears when the optimal control or stopping policies at each starting state do not match with each other, in which case the dynamic programming principle is invalid and the problem to find an “dynamic optimal control” is generally ill-posed. In this paper, we formulate the time-inconsistent problem as an intra-person game and propose the notion of equilibrium solution when stopping and control strategies are coupled together. Although time-inconsistent stopping or control problems have been widely studied in recent years, this paper is the first step towards the coupled problems along with time-inconsistency to the best of our knowledge. Several difficulties arise immediately.

There are several notions of equilibrium in existing literature, such as strong, weak, and mild equilibrium. We will discuss them in detail in Subsection 1.1. For the present paper, the first question is to choose the notion of equilibrium on which we work. The strong equilibrium formulation is at its early stage and is found to be rather difficult to characterize. Strong equilibrium may not exist in some simple examples (see Section 4.4 in He and Jiang (2019)). Mild equilibrium, on the other hand, only makes sense when we consider stopping (or discrete-valued) policies. It is not clear for now what the mild equilibrium for the control problem is. Therefore we choose to work on weak equilibrium formulation. However, it is not trivial to extend the notion of weak equilibrium to the context of stopping control. If stopping control strategies are considered together, one disadvantage is that these two parts of strategies influence each other and hence are fully coupled. To address this, we choose to work on weaker game-theoretical reasoning that “unilateral deviation of stopping or control strategy separately does not improve utility”. We emphasize that the proposed definition not only brings tractability for deriving associated extended HJB systems but is also consistent with the weak equilibrium formulations for pure control/stopping problems in existing literature. For completeness, we also briefly discuss the definition where the stopping and control strategies are allowed to deviate simultaneously. We prove that the latter is strictly stronger than the former and also explain why we do not concentrate on this stronger notion (see Definition 2.2 and Remark 13).

The second difficulty is the derivation of the associated extended HJB system. One of the main contributions of Björk, Khapko, and Murgoci (2017) is to characterize the equilibrium value and find equilibrium strategies via extended HJB equations. The tractability of finding the equilibrium strategies is considered to be one of the main superiorities of considering solely the control problem. Therefore, establishing the associated extended HJB system when stopping and control are coupled together will be the central task of the research on this topic. Using cut-off and localization techniques and the properties of characterization operators of transition semigroups, we rigorously establish the associated extended HJB system, which does not only contain equations but also inequalities as well as a complicated boundary term. Combining the above arguments with parabolic PDE theory, we can weaken the conditions in He and Jiang (2019). We emphasize that the derived extended HJB system is an equivalent characterization of equilibria, which is thus beyond the verification scope. Moreover, the extended HJB system established in this paper is a nontrivial generalization of both the extended HJB equations in Björk, Khapko, and Murgoci (2017) and the time-inconsistent variational inequalities in Christensen and Lindensjö (2018).

The last difficulty is the further characterization of the boundary term (3.4) in the extended HJB system. This term is missed in pure control problems and appears as the celebrated smooth fitting principle in pure stopping problems. However, in pure stopping problems, smooth fitting is usually just a sufficient condition of equilibrium (see e.g. Christensen and Lindensjö (2018)). In Christensen and Lindensjö (2020), it is proved that smooth fitting is also necessary for equilibrium, under a one-dimensional diffusion model. Using cut-off techniques mentioned above, we apply Peskir’s generalized local time formula on (hyper-) surfaces (see e.g. Peskir (2007)) to prove that smooth fitting is in some sense both sufficient and necessary for the boundary term (3.4) in extended HJB system. The sufficiency part is useful for verification procedures (see our examples in Section 4). The necessity part, on the other hand, states that the equilibrium value function is global along spatial directions. Global regularity of value functions is a very important topic in optimal stopping theory (see De Angelis and Peskir (2020) and literature review therein), and we have obtained similar results in the time-inconsistent counterpart, yet based on stronger regularity assumptions on stopping boundary.

We extend all of our results to the infinite time horizon case, and thoroughly investigate three examples, illustrating the applications of our theoretical framework to some practical financial models or interesting mathematical problems. Our examples include:

-

(1)

An investment-withdrawal decision model with endogenous habit formation. Constant investment proportion with a one-side withdrawal threshold can still be equilibrium in this case, but this is only assured when the dependence on habit is not very “strong” (see Proposition 4.2 for details). This strategy structure is similar to those obtained in existing literature, such as time-consistent stopping control problems Karatzas and Wang (2000), pure stopping problems Christensen and Lindensjö (2018) or pure control problems He and Jiang (2019). However, our numerical experiments show that combining the control and stopping strategies brings novel financial insights. For example, the withdrawal threshold will decline when the market risk is higher. See Subsection 4.2

-

(2)

An investment-withdrawal decision model with logarithm utility and ambiguity on discount factor. In this example, constant investment proportion can not constitute equilibrium, no matter what the withdrawal strategy is. This phenomenon is rare in the existing literature, because if the desired solution can be obtained explicitly, the investment strategy is usually constant proportion (or time-dependent but wealth-independent proportion, if the time horizon is finite)111See Karatzas and Wang (2000), Ekeland and Pirvu (2008), Yong (2012), Björk, Khapko, and Murgoci (2017), Alia, Vives, and Khelfallah (2017) and He and Jiang (2019), among others.. Moreover, with a two-point quasi-exponential discount, we further show that the equilibrium does exist, thus it must be a non-constant one. We find that in this case the control and stopping parts of the equilibrium pair are completely coupled and are described by two highly nonlinear singular boundary value problems (see (4.26)-(4.27)). They are themselves very interesting mathematical objectives and we show the existence of their solutions based on the cut-off technique, Leray-Schauder degree theory, and Green function (see Appendix D). This example shows that combining stopping control problems with time-inconsistency leads to highly nontrivial and challenging problems. It also provides a theoretical counter-view against constant proportion investment suggested by Merton’s theory or classical stopping-control problems even in the simplest market. See Subsection 4.3. This example also constitutes the main contributions of this paper, both mathematical and financial.

-

(3)

A stopping control decision problem about planar Brownian Motion, where the agent determines diffusion coefficient and stopping radius. The reward is a hyperbolic discount factor multiplied by the stopping radius, thus there is a trade-off between a larger radius and less discount. Using our theoretical framework, the rational strategy is to diffuse the system as much as possible, and choose a stopping radius that is proportional to , where is the discount rate. The value of this radius is related to a universal constant ( 8.3419) determined by Bessel functions. This example is interesting in the aspect of mathematics and is the first step to further studies on time-inconsistent multi-dimensional stopping control problems. See Subsection 4.4.

To conclude, the main contributions of the present paper are as follows:

-

(1)

We establish the framework for studying time-inconsistent stopping control problems under weak equilibrium formulation, and the proposed formulation is a nontrivial extension for weak formulations in pure stopping/control problems.

-

(2)

Using cut-off and localization techniques, we rigorously obtain an equivalent characterization of the equilibrium, which is an extended HJB system, and the assumptions needed are weakened. We believe that the extended HJB system established in this paper will become the foundation of future research on time-inconsistent stopping control problems in more specific models such as investment with discretionary stopping under non-exponential discount.

-

(3)

We build connections between the aforementioned HJB system and the smooth fitting principles in optimal stopping theory, and show that smooth fitting is in some sense sufficient and necessary for equilibrium conditions.

-

(4)

We demonstrate two concrete investment-withdrawal problems shedding light on people’s behaviors facing time-inconsistent preference, which is common in behavioral finance. One of these examples indicates that combining stopping control problems with time-inconsistency brings us essential differences and produces highly nontrivial problems. Finally, we also provide a multi-dimensional example controlling planar Brownian motion, which is interesting mathematically.

The rest of the paper is organized as follows: We formulate the time-inconsistent stopping control problem and define the equilibrium strategies in Section 2. Section 3 and Section 4 include the main results of this paper. In Section 3, we obtain characterizations of the equilibrium. In Section 4, we provide three concrete examples to illustrate the theoretical results in Section 3. Section 5 concludes this paper. Technical proofs are mainly presented in Appendix A. In Appendix B, we discuss how to use PDE theory to obtain our assumptions in Section 3. Appendices C and D include some technical results related to our examples.

1.1 Literature Review

Classical stopping control problems are extensively studied, and they are typically time consistent, which means that at any given initial time and state, the agent conducts the static optimization and the resulting strategies are consistent between different starting states. Karatzas and Wang (2000) and Karatzas and Zamfirescu (2006) study stopping control problems in a specific setting of portfolio choice. Interpreting this as a cooperative game between “controller” and “stopper”, Karatzas and Sudderth (2001), Karatzas and Zamfirescu (2008), Bayraktar and Huang (2013) and Bayraktar and Li (2019), among others, study the noncooperative version of stopping control problems. Stopping control modelings are also widely applied to retirement decisions research, see Choi, Shim, and Shin (2008), Farhi and Panageas (2007), Dybvig and Liu (2010), Jeon and Park (2020), Xu and Zheng (2020) and Guan, Liang, and Yuan (2020).

Although originated in the early but seminal paper Strotz (1955), game-theoretical formulations for time-inconsistent problems in continuous time have been taken into researchers’ sight only in decades. Earlier developments focus on control problems, where the state dynamics are controlled and the terminal times are fixed. In some specific settings such as portfolio management or economic growth, Ekeland and Pirvu (2008) and Ekeland and Lazrak (2010) propose the notion of equilibrium in continuous time problems and provide existence. Among many other works on the same topic, one breakthrough is that Björk, Khapko, and Murgoci (2017) derives the necessary conditions of equilibrium under the general Markovian diffusion model, which is an extended HJB equation system. This formulation of equilibrium is usually called weak equilibrium in the literature, and, roughly speaking, reveals the game theoretical reasoning “unilateral deviation does not improve the pay-off” in a weak sense. Formally, is said to be a weak equilibrium if

where is properly-defined perturbation of .

He and Jiang (2019) rigorously proves the extended HJB equation system for weak equilibrium formulation. Hu, Jin, and Zhou (2012) and Hu, Jin, and Zhou (2017) study the stochastic linear-quadratic control in similar formulation, and importantly, they obtain a uniqueness result for this particular control model. More recently Hu, Jin, and Zhou (2020) obtains an analytical solution to a portfolio selection problem with the presence of probability distortion. In He and Jiang (2019) and Huang and Zhou (2018), the authors extend the scope of research on this topic and propose different notions of equilibria. An important one of those newly proposed notions is strong equilibrium, which requires ,

This notion is closer to the concept of subgame perfect equilibrium (SPE) in game theory, but is rather difficult to study, as revealed in He and Jiang (2019) and Huang and Zhou (2018). Most recently, Hernández and Possamaï (2020) studies time-inconsistent control problems in the most general non-Markovian framework, where the notion of equilibrium is also refined.

Stopping decision problems with time-inconsistency, on the other hand, are at the early stages of research. In recent years there are substantial works and theoretical breakthroughs on this topic. Series of papers including Huang and Nguyen-Huu (2018), Huang, Nguyen-Huu, and Zhou (2020), Bayraktar, Zhang, and Zhou (2021), Huang and Zhou (2020), Huang and Wang (2020) and Huang and Yu (2019) study time-inconsistent stopping problems under the so-called “mild equilibria” ( Bayraktar, Zhang, and Zhou (2021)), which only considers the deviation from the strategy “stopping” to “continuation”: is an equilibria stopping policy (continuation region) if

We also note that there are indeed papers adopting weak equilibrium formulations when studying stopping problems, such as Christensen and Lindensjö (2018) and Christensen and Lindensjö (2020), where not only deviation from “stopping” to “continuation”, but also any infinitesimal perturbation of stopping policies are considered (see Definition 2.1 and remarks therein for detailed discussion). In the context of time-inconsistent stopping problems, Bayraktar, Wang, and Zhou (2022) studies the relationships among different notions of equilibrium solutions. Similar to our paper, they provide full characterizations of weak equilibrium (under a one-dimensional diffusion model). Moreover, they prove that under some conditions, optimal mild equilibrium is strong, so that the existence of strong (weak) equilibrium can be obtained. Ebert, Wei, and Zhou (2020) investigates weak equilibrium of time-inconsistent stopping problems from an economic point of view, and Tan, Wei, and Zhou (2021) thoroughly studies the smooth fitting principle with the presence of time-inconsistency, which is also one of our concerns. In addition to the pure stopping rules which consist of the mainstream of current research, Bodnariu, Christensen, and Lindensjö (2022) focuses on the local time pushed mixed stopping rules and also provide smooth fitting principle under their formulation. Interestingly, they find that there is sometimes a dichotomy between the existences of pure and local time pushed mixed stopping rules.

2 Notations and model formulations

We first introduce key ingredients for our problem formulation:

-

•

State space: Let be a region, equipped with the Euclidean norm and , the Borel -algebra induced by it. will be the (space-time) state space.

-

•

Control space: Let be a Polish space, equipped with , the Borel -algebra induced by its metric. We assume that the control takes value in .

-

•

Set of admissible controls: Let be a subset of all measurable closed-loop control. In other words, any is a measurable map . Some assumptions will be imposed on to guarantee the well-posedness of the problem (see Assumption 1).

-

•

Set of admissible stopping policies: Let be a subset of the collection of relative open subsets of , including and . will be considered as the set of admissible continuation region, hence can be equivalently thought as the set of stopping policies.

-

•

The implemented stopping time: . After the agent has chosen the control , the stopping policy , and the minimal stopping time , he will implement as his stopping strategy. In other words, he will not consider stopping before , and after time , he will stop immediately when the state process under exits the continuation region for the first time.

-

•

Set of admissible strategies at time : .

In addition, the mathematical notations that will be used are listed below for convenience:

-

•

is the set of the functions that are once continuously differentiable in and twice continuously differentiable inside some subset .

-

•

is the set of continuous functions.

-

•

is the set of smooth functions with compact support.

-

•

is the parabolic distance. .

-

•

is the parabolic cylinder.

-

•

means that for any there exist which is sufficiently small, and a function such that .

The probability basis for our problem is as usual. Let be a complete probability space supporting a standard -dimensional Brownian motion , where is a filtration satisfying the usual conditions, and 222Here we are not concerned with what the filtration is. We choose to restrict the information by allowing only the Markovian closed-loop strategies, instead of specifying the filtration. See Remark 2 for detailed discussion. For any , we consider the strong formulation of the controlled state dynamics:

| (2.1) |

For any , , we define the characterization operator of by333We denote by the transpose of the matrix .

where

We make the standing assumption on the admissible set , which is crucial for the analysis later, as follows:

Assumption 1.

For any , we have:

-

(1)

.444Here we identify any with the constant map . Therefore any element in can also be seen as a closed-loop control.

-

(2)

and are Lipschitz in , uniformly in .

-

(3)

and are right continuous in , and are bounded in , uniformly for in any compact subsets of .

-

(4)

For any , the solution of (2.1) with initial condition , denoted by , satisfies .

Based on the theory of stochastic differential equations (see e.g., Friedman (1975) or Yong and Zhou (1999)), under Assumption 1, (2.1) is well-posed in the strong sense, and the solution is strong Markovian, for any . We introduce the Markovian family with .

We now state our problem. The agent aims to maximize the pay-offs among all admissible strategies , which is given by

However, due to the dependence of the reward on state, the problem is generally time-inconsistent, and it does not make sense to find the dynamic “optimal” strategies555For the discussion on time-inconsistency for pure control problems, see Ekeland and Pirvu (2008) or Yong (2012). For discussions on stopping problems, refer to Huang, Nguyen-Huu, and Zhou (2020).. As in Björk, Khapko, and Murgoci (2017) and He and Jiang (2019), we consider the perturbed control of by , which is defined as

| (2.2) |

We are now ready to give the definition of equilibrium policies of time-inconsistent stopping control problems.

Definition 2.1.

is said to be an equilibrium if and only if all of the followings hold with :

| (2.3) | |||

| (2.4) | |||

| (2.5) |

Remark 1.

This paper provides a unified theory to investigate the stopping and control problems. Noting that and are only required to be some subset of universal feasible action space, our work generalizes previous literatures. Indeed, take to be the singleton, the problem degenerates to pure stopping problem, as in Christensen and Lindensjö (2018). Take , the problem degenerates to pure control problems, as in Björk, Khapko, and Murgoci (2017) and He and Jiang (2019).

Remark 2.

It is crucial to specify how much information the agent can make use of. Indeed, limited information is one important reason for the occurrence of time-inconsistency. Most literatures impose the limitation on filtration: the control process is required to be measurable with respect to the filtration generated by state process. In the present setting of (Markovian) controlled-diffusion model, we choose to impose similar limitation implicitly by allowing only closed-loop control. This is the analogy of considering only pure Markovian stopping times when studying time-inconsistent stopping problems, as in Christensen and Lindensjö (2018), Huang and Nguyen-Huu (2018), among others.

Remark 3.

If , (2.3) becomes equality and hence trivial. If , (2.3) states that it is better to continue than to stoping. However, implies that the equilibrium policy commands the agent to continue. As such, (2.3) states that the agent has no reason to deviate the equilibrium stopping policy from continuation to stopping. (2.4) requires that the agent is not willing to deviate even an infinitesimals from equilibrium stopping policy. In conclusion, our definition requires the agent not to deviate from equilibrium stopping policy, if all the -agents follow the equilibrium.

Remark 4.

(2.5) states that if all the -agents follow the equilibrium (control and stopping policy), then he is not willing to deviate from equilibrium control policy. Here the -agents with is irrelevant because they have stopped and exited the system, as the equilibrium stopping policy commands.

Remark 5.

It should be noted that in Remarks 3 and 4, the game-theoretical concept of equilibrium is in a weak sense. Indeed, when the limit in (2.4) or (2.5) is 0, then deviation from equilibrium may indeed improve the preference level. However, as understood in Hernández and Possamaï (2020), if we ignore those improvements that are as small as a proportion of length of time interval perturbed, the definition of (weak) equilibrium fits into the game-theoretical consideration. For other types of equilibrium, see Huang and Zhou (2018), Bayraktar, Zhang, and Zhou (2021) for examples. In the context of time-inconsistent stopping, different types of equilibrium have also been studied. Christensen and Lindensjö (2018) and Christensen and Lindensjö (2020) consider the weak equilibrium, which we adopt. Generally it is difficult to characterize strong equilibrium, even for pure stopping or control problems, see Huang and Zhou (2018) for this under the setting of discrete Markov chain. It shall be an interesting topic for future work to characterize strong equilibrium for continuous-valued state process, in pure stopping and control problems, as well as stopping-control problems.

Remark 6.

Note that , where is the family of shift operators. Therefore, comparing to Christensen and Lindensjö (2018), the infinitesimal perturbation of is in the time horizon , not in the space horizon . In our case, to make two perturbations of control and of stopping consistent with each other, we consider perturbation in time. Note that the perturbation of control can not be in space, because that would destroy the Lipschitz property of and so the SDE could be ill-posed.

In Definition 2.1, the possible deviations of control and stopping policies are separable, i.e., deviating from stopping policies when fixing control policies, and deviating from control policies when fixing stopping policies. This definition makes perfect sense from game theoretical perspective if the problem is understood as a cooperative stopper-controller problem, where one agent controls the system and another chooses when to terminate. For the one-agent setting in this paper, it is very natural to consider concept of equilibrium where deviations of policies are allowed to be mixed. Here we introduce the following definition of strict weak equilibrium.

Definition 2.2.

is said to be a strict weak equilibrium if and only if the followings hold with :

| (2.6) | |||

| (2.7) |

In (2.6) we capture the deviation of policies when the stopping part is “from continuing to stopping”, and in this case the control policy is absent because it is irrelevant. Thus (2.6) is exactly the same as (2.3). In (2.7), on the other hand, we hope to describe the change of policies when stopping part is from stopping to continuing. Here comes a dilemma: in this case deviation for control policy only matters in continuation region, while for stopping policy it is more important to consider stopping region. That is why we require all rather than to satisfy (2.7). This paradox is the most important reason that makes us think that weak equilibrium is a better concept for studying time-inconsistent stopping control problems. This point is also the crucial point that makes strict weak equilibrium stronger than weak equilibrium. In Section 3 after stating the characterization theorem in infinite time horizon case (Theorem 3.7), we will briefly explain why strict weak equilibrium implies a weak one (see Remark 11). At the end of Section 3 we provide an example showing a weak equilibrium need not to be strict (see Remark 13). In the rest of this paper, we focus on weak equilibrium.

3 Characterizations of the equilibrium

We now present the main results of this paper, including assumptions and technical lemmas that are needed for proofs. This section is further divided into two subsections. In Subsection 3.1 we present results for finite time horizon, and all proofs are provided in Appendix A. In Subsection 3.2 we briefly discuss the infinite time horizon case, which will be used for in Section 4, but we omit all the proofs there because they are similar to the finite time horizon case.

3.1 Finite time horizon

In this subsection we fix and investigate whether it is equilibrium. For convenience, we drop all the superscripts , e.g., , , if needed. Moreover, we denote by the space of function that has at most polynomial growth at infinity, i.e.,

We have the following main result of this paper:

Theorem 3.1.

If the auxiliary function satisfies:

| (H1) |

Then is an equilibrium if and only if and solve the following system:

| (3.1) | |||

| (3.2) | |||

| (3.3) | |||

| (3.4) | |||

| (3.5) | |||

| (3.6) | |||

| (3.7) |

where .

Furthermore, when is equilibrium, we have

| (3.8) |

for those such that the map is well-defined.

Theorem 3.1 builds upon the following several lemmas, which calculate the limits (2.4) and (2.5). Their proofs are given in Appendix A.

Lemma 3.2.

For any ,

Lemma 3.3.

For any , ,

Proof of Theorem 3.1.

(3.1), (3.5) and (3.6) hold no matter whether is equilibrium or not, thanks to Lemma 3.4. Clearly, by Lemmas 3.2 and 3.3, (2.3) is equivalent to (3.7), (2.5) is equivalent to (3.2) with , (2.4) in is equivalent to (3.3), (2.4) on is equivalent to (3.4). Moreover, taking in (3.1), (3.2) with can be replaced by the one with . (3.8) is obvious from (3.1) and (3.2). ∎

Note that Theorem 3.1 provides full characterization of equilibrium if we know a priori the form of auxiliary function. However, using Theorem 3.5 below, we know that if solves some part of the system mentioned above, it is exactly the auxiliary function needed.

Proof.

In order to provide refined characterization of the equilibrium, and prepare for the verification procedure in Section 4 at the same time, we discuss the boundary condition (3.4). Similar to Christensen and Lindensjö (2020) and many other literature where free boundary problems play important roles, one usually expects smooth fitting principle to make an ansatz. We propose smooth fitting in multi-dimensional setting as follows:

| (3.9) |

Indeed, we prove that, under mild conditions, this is necessary for equilibrium condition (3.4). On the other hand, it is also helpful to the verification procedure if we can obtain some sufficient condition for (3.4). In fact, we propose:

| (3.4’) |

When making ansatz, we usually aim to find a solution that has continuous spatial derivatives, especially when spatial dimension . Therefore, combined with (3.4’), (3.9) is also an appropriate sufficient condition. To provide connections between (3.9) and (3.4), we need the following mild technical assumption on :

| (H2) |

Although is already defined on , it is not across the boundary . The key point of (H2) is that we consider the restriction of on (which is ) and extend it smoothly to . This is needed for the application of local time formula (see Appendix A). Moreover, (3.9) is in fact not perfectly rigorous because is not smooth across , but now based on (H2) we see that it actually means on the boundary. We have the following theorem, which is another main result of this paper:

Theorem 3.6.

Remark 7.

Remark 8.

Recall that is the diffusion coefficient under the candidate equilibrium strategy . The conclusion (2) in Theorem 3.6 thus asserts that (3.9) is necessary if we only consider the equilibria that give nondegenerate diffusion term. This is true in many situations, including those where the diffusion term cannot be controlled.

Remark 9.

Smooth fitting principles are always important topics in optimal stopping theory. For review of classical results on this topic, see Peskir and Shiryaev (2006). Recently efforts have been made to establish global regularity of value function of optimal stopping problems, see De Angelis and Peskir (2020) and Cai and De Angelis (2021) for examples. We have obtained similar results for time-inconsistent stopping control under additional regularity imposed on stopping boundary. It is very interesting to try to drop this assumption and prove the regularity directly from equilibrium conditions. We hope to establish this type of results in future works.

Remark 10.

We now make some comments on assumptions (H1) and (H2). It is known that in control theory, to make regularity assumptions on value function is sometimes restrictive (see e.g., Example 2.3 on page 163 of Yong and Zhou (1999)). However in our context, when fixing and , has clear connection to linear parabolic equations with initial and boundary value. Thus, PDE theory helps to establish regularity inside . Moreover, the growth of itself follows directly from that of , and we do not require the growth of derivatives of , weakening the condition in He and Jiang (2019). At last, the assumption (H2) can be established by uniform continuity and Whitney’s extension theorem, thanks to the Hlder estimates for parabolic equations. See Appendix B for details.

3.2 Infinite time horizon

To prepare for the studying of the concrete examples in Section 4, for which we hope to get analytical solutions, we extend the main results in the previous subsection to infinite time horizon case. One of the advantages for adapting the (weak) equilibrium formulation is that all the arguments are local (see all the proofs in Appendix A). Therefore, it is almost trivial to exntend Theorem 3.1 once we neglect the condition (3.5). Furthermore, Theorem 3.6 still holds true for the same reason. The only thing we need to refine for the infinite time horizon theory is that the estimate (A.2) in Appendix A seems not to be directly applicable anymore. However, the estimate there is still valid, except that we do not substitute , but choose for any fixed . This is sufficient because when applying it, we only consider the behaviour for trajectory of on . The similar arguments in the proofs of results in Subsection 3.1 (see Appendix A) are still applicable and anything follows. We thus have the following:

Theorem 3.7.

If the auxiliary function satisfies (H1), then is an equilibrium if and only if and solve the following system:

| (3.10) | |||

| (3.11) | |||

| (3.12) | |||

| (3.13) | |||

| (3.14) | |||

| (3.15) |

Furthermore, when is equilibrium, we have

| (3.16) |

for those such that the map is well-defined.

Remark 11.

We now make comments on the concept of strict weak equilibrium (see Definition 2.2). From the proof of Theorem 3.1 (Appendix A), the equilibrium condition (2.7) is equivalent to

The subtle point is that this requirement is imposed on any point in the whole state space and any admissible control , not just the equilibrium one. Translating to the infinite time horizon case, the characterization system of strict weak equilibrium is similar to that in Theorem 3.7, with (3.12) revised to

| (3.12’) |

We immediately conclude that a strict weak equilibrium must be weak.

Remark 12.

In Theorem 3.7, we define the auxiliary function to be the expected reward restricted on the event . On the one hand, this event does not necessarily have probability 1. On the other hand, it is reasonable to assume that outside this event, i.e., in the “never stop” scenario, the reward is zero, because it is never realized.

In applications, especially in the infinite time case, the controlled is usually time-homogenous and takes the form , with discount function satisfying and nonincreasing. Under these additional assumptions, the system used to characterize the equilibrium solution becomes more elegant. Indeed, the first simplification is from the time symmetry: we can now take the open subsets of (under its relative topology) with boundary as admissible stopping polices, and taking brings us to notations of the previous sections. Furthermore, it is straightforward to show that under this choice of stopping policy, has the form , where under the notation of Section 2. Therefore, restricting on the diagonal, functions and do not depend on , and we denote and . To ease our notation, we still denote by the spatial deferential with respect to the second variable only, i.e., . Combining the above discussions, we have the following corollary, which will be used repeatedly in concrete examples in Section 4:

Corollary 3.8.

Suppose that the dynamic of diffusion under admissible control is time-homogeneous, that is invertible for any , and that the reward function has the form . Moreover, assume that under the strategy pair , the auxiliary function satisfies (H1) and (H2). Then is an equilibrium if and only if and solve the following system:

| (3.17) | |||

| (3.18) | |||

| (3.19) | |||

| (3.20) | |||

| (3.21) | |||

| (3.22) |

Remark 13.

After providing smooth fitting result in infinite time horizon case, we are able to provide an one-dimensional example where a weak equilibrium need not to be strict. Consider a discount function with and . Take admissible control policy as (only two constant controls allowed), where and . We assume that the state process under control is , where is a Brownian motion. Take the continuation region and control . Note that for , . Therefore, in . Moreover, , if , and for . Thus, based on Corollary 3.8, it is trivial that is a weak equilibrium666Note that the sufficiency part of Corollary 3.8 does not need the non-degeneracy condition of . See Theorems 3.6 and 3.7. Therefore, it is valid to show that consists a weak equilibrium even it does not satisfy the non-degeneracy condition.. However, for , violating (3.12’), proving that is not strict. Choosing for some , the problem is time-consistent. In this case, we provide an example where a weak equilibrium strategy need not to be optimal. It is interesting to investigate the relations between weak equilibrium and strict weak equilibrium (say, to find conditions under which a weak equilibrium is strict, or to investigate whether a strict equilibrium is optimal for time-consistent problems). This direction is left for future studies.

4 Examples

In this section we investigate three concrete examples to illustrate the usage of the theoretical results established in the last section. In Subsection 4.1 we introduce the general formulation of an investment-withdrawal decision problem, and in Subsections 4.2 and 4.3 we study the examples in detail. In Subsection 4.4 we provide an example in 2-dimension, where the equilibrium stopping boundary is a circle.

4.1 Investment-withdrawal decision model

For simplicity we assume that the decision maker has the opportunity to invest in one stock:

where and are both positive constants. In this situation, it is usually assumed . We only consider the case . Suppose that the decision maker can invest on . The decision maker will also establish (for himself) a withdrawal mechanics. For example, he will choose a continuation region . Once his wealth leaves , he will withdraw all his investment and stop any exchange for the moment. Therefore, choosing (time-homogenous) investment proportion and continuation region , the wealth dynamics and the expected pay off are expressed respectively by

| (4.1) | |||

| (4.2) |

When making decisions, the decision maker takes . The reward function will be specified in the following several subsections.

4.2 Reduction of utility by wealth level

Christensen and Lindensjö (2018) studies an example of time-inconsistent stopping problem, where the reward is affected by the current wealth level . Using the investment-withdrawal model developed in the last subsection, that example can be interpreted as an investment chance where the proportion of money invested is locked (or set) to be 1 and the agent can choose a time to withdraw. Here we extend this example to the occasion where the agent is allowed to choose and adjust the investment in response to the market performance and can also decide when to withdraw the investment. Now we briefly introduce the setting. To obtain semi-analytical solution we shall work on the case . If the agent, with his wealth , chooses the investment strategy (which depends on only) and decides to stop at , then he will get

| (4.3) |

where , and are positive constants, and is an increasing function with . It is seen that the larger , the less he will actually get at , given the same outcome of . This is well-interpreted economically: to get ten thousand dollars means a lot to the homeless, but could mean nothing to a billionaire. We also require to be nondecreasing, which means once withdrawn, more wealth gives more utility. Under the setting mentioned above, using the notations in Corollary 3.8 we have , , , , and, to find equilibrium, we try to find and solving (3.17)-(3.22). In this subsection we aim to find equilibrium among those with a threshold type stopping strategy, i.e., for some 777 Using (3.19), if is an equilibrium, it can be shown that there exists such that (see similar arguments in the proof of Proposition 4.3). We assume for simplicity..

As a first step, we first use the necessity part of Corollary 3.8 to narrow down our search to a candidate solution. To do this, suppose is an equilibrium, where is Lipschitz, , and . As a well known result from one-dimensional diffusion theory, is an inaccessible boundary point for (see Itô and McKean (1996) and Helland (1996)), thus , -a.s. for any . Therefore we have

where solves

| (4.4) |

Using Corollary 3.8, we know

| (4.5) |

Plugging this back into (4.4), we conclude that must satisfy

| (4.6) |

with . Moreover, is strictly increasing in . There are multiple ways tho show that (4.6) has only one increasing solution , 888 For example, one can transform the equation of (4.6) into and integrating backwards from . Details can be provided upon requirements. One can also use inverse function method similar to the proof of Proposition D.2 in Appendix D.. Using (4.5), we know . Therefore we have proved the following result:

Proposition 4.1.

Suppose is equilibrium, then .

The next step is to determine a threshold and provide sufficient conditions to ensure that our candidate strategy is indeed equilibrium. To this end, we note that has the following form inside :

where . Here we introduce the function for convenience of numerical experiments, where for comparison, the control may be locked to other constants rather than . Clearly and satisfy (3.17) and (3.21). To show that (3.20) holds, we need

which, after direct computation, becomes

| (4.7) |

Under the choice described by (4.7), (3.19) becomes, for any ,

| (4.8) | ||||

We consider the following two cases of :

-

Case1.

. In this case it is obvious that (4.8) is true.

- Case2.

To conclude, we have shown that (3.19) holds if

| (4.10) |

Now the only condition left to be verified is (3.22), being equivalent to

| (4.11) |

This needs some further assumptions, which we will provide in Proposition 4.2 below999There are in fact gaps in the argument proving similar relations as (3.22) in Christensen and Lindensjö (2018). In pages 31-32 of that paper, the authors reduce their arguments to the case . However this reduction is not allowed directly. Indeed, from (4.7) we know that the value of depends crucially on the choice of . Consequently, in the inequality (4.11) are different when . This leads to essential difficulties for proving (4.11). We also provide counter example where (4.11) is not true, even with simple choice of (see Remark 15 and Figure 1)..

Proposition 4.2.

Proof.

See Appendix C. ∎

Remark 14.

The assumptions in Proposition 4.2, as well as (4.10), seem to be complicated. In fact, there are financial insights: on the one hand, if a constant holding ratio is rational, the withdrawal threshold (desired asset level) cannot be too low (see (4.10)), which will be revealed again in the next subsection under a different preference model; on the other hand, if the effect of habit on preference is too strong ( is large), we cannot explicitly determine the rational strategies. Indeed, a preference that is easily influenced by habit can be regarded as a modelling of irrationality. In the numerical experiments below, we will show that under a broad and reasonable set of market parameters, all these assumptions are satisfied.

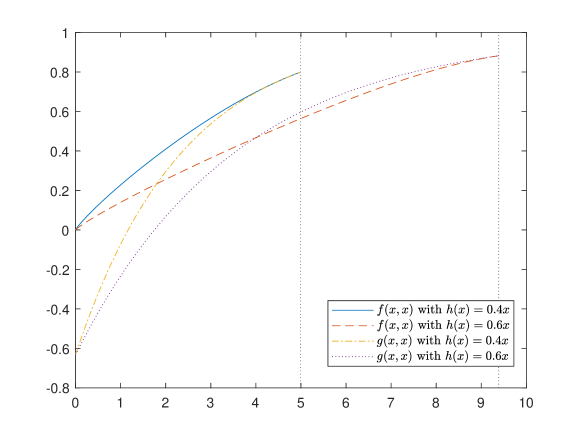

Remark 15.

Here we emphasize that the assumptions on in Proposition 4.2 are just convenient sufficient conditions. There are indeed some other possible choice of that satisfies , and there are also possible choice of that violates it. In Figure 1 we simply try linear function . It is seen that for , although the condition proposed in Proposition 4.2 is invalid, described above is still an equilibruim. However, for , clearly, for some . Therefore, (3.22) is invalid, and is not an equilibrium. This reveals an interesting fact: smooth fitting principle (by which is determined) does not necessarily give an equilibrium solution. This phenomenon is studied in detail by Tan, Wei, and Zhou (2021), and in Bodnariu, Christensen, and Lindensjö (2022), it is shown that introducing a kind of local time pushed mixed stopping rules can fill this gap.

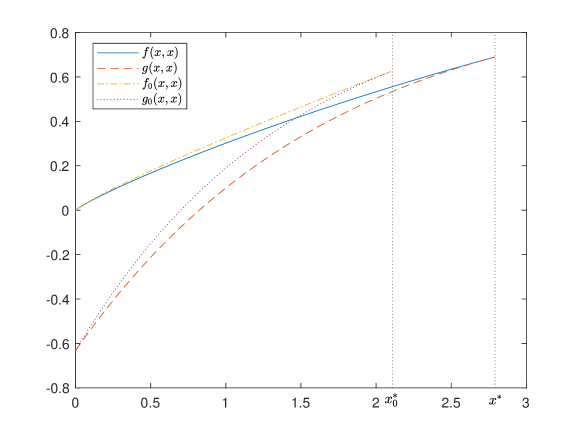

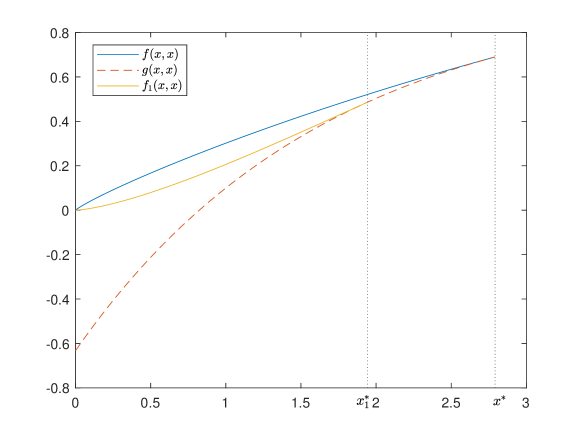

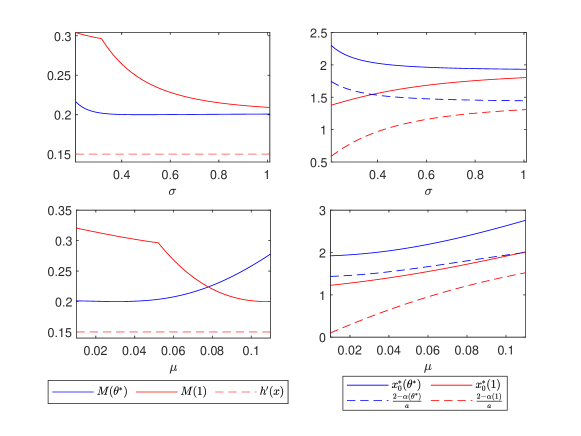

We now take a look at some numerical examples. Here we take , , , , . In this case, we choose , then all assumptions in Proposition 4.2 are satisfied. Under this setting we have the equilibrium , . For comparison, if there is no habit dependence, i.e., , then remains the same and the equilibrium withdrawal level is . In this case, the problem is denegerated to time consistent one, and this is also the optimal investment and withdraw strategy (see Karatzas and Wang (2000)). If the investment level is locked to be and the investor is only allowed to choose the withdrawal time, then the corresponding equilibrium withdrawal level is . It is seen that under the current market parameter, for sophisticated agent, the chance of discretionarily choose the investment level will make him improve the investment level while set a higher expectation wealth level. For the graphical illustrations of these results, see Figures 2 and 3.

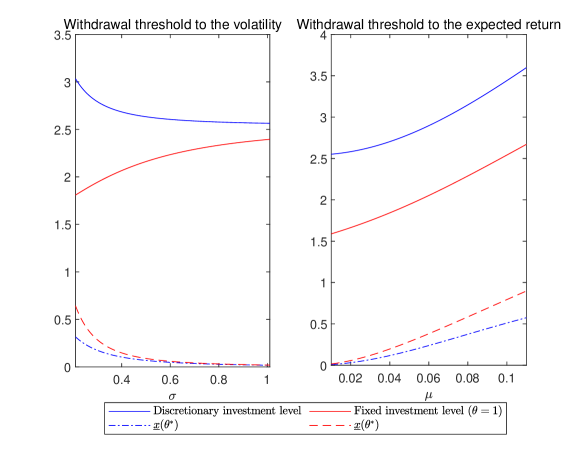

Through numerical experiment, there are some novel financial insights from our investment-withdrawal decision model, comparing to stopping model without the discretionary investment opportunity. Specifically, there are different behaviors of the equilibrium withdrawal threshold when the volatility change. Under non-exponential discount model, it is found in Ebert, Wei, and Zhou (2020) that the equilibrium withdrawal threshold increases with both and . We confirm this result under the endogenous habit formation model, as originally developed in Christensen and Lindensjö (2018). Using equilibrium theory developed in the present paper, we find that if the agent is provided with discretionary investment opportunity, the withdrawal threshold decreases with the volatility and still increases with return rate (see Figure 4). Because higher volatility implies more risk, and withdrawal threshold can be seen as the expectation of agent, this result is much more intuitive: giving other things the same, people should reduce their expectation when market risk becomes higher.

To assure that when and are varying in the given range, the derived pair remains to be the equilibrium, we need to check the assumptions (4.12) and (4.14). For simplicity we denote by the right hand side of (4.14), where the dependence of comes from , and . Figure 5 justifies our analysis, and also shows that the assumptions we propose are reasonable.

4.3 Ambiguity on discount factor

In this subsection, we develop a decision model where the agent is uncertain (ambiguous) about his discount factor , but has a belief on it. Under this setting, the problem he faces is time-inconsistent. By showing the nonexistence of constant equilibrium (the equilibrium solution with constant investment proportion), we argue that the theory proposed in this paper generates nontrivial results and is demanding for better understanding of the time-inconsistency in mathematical finance.

We consider the same model of underlying asset as in Subsection 4.1, while consider the following reward:

| (4.15) |

where is the mean discount function with belief :

| (4.16) |

Here is a probability density on the interval . Recall that choosing continuation region and investment proportion , the agent will implement (see the last paragraph in Subsection 4.1). For simplicity, we will use instead of , if there is no confusion.

Remark 16.

The model is a time-inconsistent generalization of the example in Appendix A of Karatzas and Wang (2000). We prove that there is no constant serving as equilibrium investment proportion (in other words, we exclude many irrational strategies). Because the uniqueness of equilibrium is hard to achieve, the fact that we can rule out many irrational strategies is quite insightful. To the best of our knowledge, this is the only negative result on the existence of constant equilibrium, except a recent paper He, Jiang, and Kou (2020) for a completely different problem (see (3) of Theorem 1 therein). In most of the existing literatures, where analytical solutions are attainable, the resulting equilibrium investment proportions are constant (or at least independent from the wealth). See Karatzas and Wang (2000) for time-consistent stopping control problems, Ekeland and Pirvu (2008), Yong (2012), Björk, Khapko, and Murgoci (2017), Alia, Vives, and Khelfallah (2017), He and Jiang (2019), among others, for time-inconsistent control problems. Combining these observations we argue that the proposed model in the present paper, where the agent are supposed to make stopping and control decision simultaneously with the presence of time-inconsistency, brings essential differences from various existing models, and generates non-trivial results.

Remark 17.

In this model the mean discount functions are special forms of general discount functions displayed in Subsection 3.2. Indeed, as shown in Ebert, Wei, and Zhou (2020), many popular discount functions can be expressed via a weighted distribution, similar to (4.16). Typical examples for our mean discount functions include:

-

(1)

(Quasi-exponential discount)

-

(2)

(Generalized hyperbolic discount)

(4.17) -

(3)

(Compactly supported belief)

.

Surprisingly, considering real ambiguity (i.e., is not singleton supported) will exclude constant investment proportion. Because the developed model is used to be describe rationality when optimal principle is not applicable, we have shown that under the developed model, any constant investment proportion is irrational. This conclusion (see Proposition 4.3) provides a possible explanation to many empirical documents (see e.g., Wachter and Yogo (2010)) in contrary to classical Merton’s suggestion or solution obtained in Karatzas and Wang (2000) under time-consistent setting, which is constant proportion. Formally, we have the following:

Proposition 4.3.

If the reward function takes the form as in (4.15), and is not singleton, then for any open subset of such that , , and any , can not be equilibrium.

Proof.

We show the proof by contradiction. Suppose that is indeed an equilibrium, we claim that must be singleton. First, for any , we have . Or otherwise suppose that there is such that . Observing the following expression:

we find that, choosing large enough (can be dependent on ), we are able to assure that , contradicting (3.11). Therefore, we assume that . Because is open subset of , it can be uniquely expressed by , where the family are countably many disjoint open intervals. We first claim that there must be one interval, say , with the form . Otherwise, we deduce that we can choose a sequence and . However, using (3.12), we have

where

This leads to

which clearly contradicts the fact that with . In what follows, we focus on . For any , can be calculated by:

where . Using (3.13) and Theorem 3.6 (i.e., the weak smooth fitting principle), we have , which yields

Direct calculation also shows

In light of (3.16), for , we consider

We have for any . Taking derivative gives

Based on the condition of Cauchy-Schwartz inequality being equality, there exists such that

for any , . Because the map is injective, and remains the same for all , we conclude that contains at most two elements. If , we assume , , then we have

Here we denote , and without loss of generality assume . It is clear that and . now gives , a contradiction. Therefore, is singleton. ∎

By Proposition 4.3 we conclude that there is no investment proportional to the wealth (constant equilibrium) that can serve as equilibrium strategy. The natural question is that is there any equilibrium strategy at all? In the rest of the present subsection, we give a positive answer in a special case where the discount function is two-point quasi exponential (see Remark 17). Using the methodology proposed in this paper, we find that the equilibrium strategy is described by two coupled singular boundary value problems (sBVP). They are interesting and mathematically challenging in their own rights and the existence of positive solutions of such problems are dealt with in Appendix D.

To see this, we pick

with 101010To avoid complicated notations, we choose two-point distribution and uniform weight (i.e., both discount rates appear with probability 1/2). It is straightforward to generalize the content of this part to the general finite discrete distributions: where . But this generalization leads to complicated notations and tedious combinatorial discussions. Moreover, the equilibrium is described by an ()-coupled system of singular boundary value problem, which is a generalization of (4.26).. Recall that when we choose the control strategy , the dynamic of the wealth will be (see (4.1)):

Now for a candidate strategy (not necessarily constant) and a continuation region , the corresponded value function is

| (4.18) |

where

From one-dimensional diffusion theory we know that when the drift and diffusion function is Lipschitz (which we require), is an inaccessible boundary point (see Itô and McKean (1996) and Helland (1996) for detailed illustrations). Therefore, under the stopping policy and control strategy , the implemented stopping time is , hence justifying the expression (4.18). Using Corollary 3.8, we conclude that the pair is equilibrium if and only if is Lipschitz, and

| (4.19) | |||

| (4.20) | |||

| (4.21) | |||

| (4.22) |

where , and . Meanwhile, from diffusion theory, we know that the function is the unique positive increasing solution of the following boundary value problem:

| (4.23) |

Plugging (4.19) into (4.23) and rearranging the resulted problem equivalently, we have

| (4.24) |

The following simple lemma will be the first of some auxiliary results in this subsection.

Lemma 4.4.

Proof.

In the following we focus on (4.24), which is a fully coupled nonlinear singular boundary problem. To simplify it we first use the following linear transformation:

Under this transformation, (4.24) is transformed to

| (4.25) |

We then consider the decoupling function , i.e., we suppose . By direct calculation, we can decouple (4.25) into two sBVP ():

| (4.26) |

| (4.27) |

Remark 18.

The trivialization of the case is through the sBVP (4.26) because if , it admits analytical solution .

It turns out that our existence result about equilibrium stopping and control strategies depends crucially on the existence of positive solutions together with some upper and lower bound estimation. We state this result in Lemma 4.5 below, whose proof relies on Leray-Schauder topological degree theory, and is postponed to Appendix D.

Lemma 4.5.

Proof.

See Appendix D. ∎

(4.19) can now be verified using the results in Lemmas 4.4 and 4.5. The next lemma, on the other hand, deals with conditions (4.20)-(4.22).

Proposition 4.6.

Proof.

Using the equation and initial condition at in (4.27), we have the following expression:

Because , we have

Therefore, is equivalent to

By the fact that and we have

Here we use , which directly comes from (4.28). That is to say, is at most linear growth on . Therefore for large enough, . But for , . From continuity with respect to (see the proof of Proposition D.2 in Appendix D), we conclude that there exist a such that , i.e., (4.20) holds. Using the same way, but estimating the lower bound, we get

Therefore

due to (4.28), thus (4.22) is satisfied. (4.21) is equivalent to

We investigate . Note that

Therefore we conclude for any , i.e., (4.21) holds. To show the rest of the proposition, we only need to prove are both ( strictly) increasing, because the diffusion theory then implies is indeed identified with . To do this, we notice that by the transformation , , we have

Therefore , , which are both non-negative. Suppose for some , . Because is strictly increasing, . By (4.24),

This implies that for some , , which is a contradiction. This implies that both for , , completing the proof. ∎

Remark 19.

(4.28) is very mild and is satisfied by typical model parameters. Moreover, it is only a technical assumption used to guarantee (4.20)-(4.22) and is irrelevant to (4.19), which is usually the most important relation determining equilibrium control . As illustrated at the beginning of this subsection, taking control into consideration brings essential differences and difficulties when studying time-inconsistent problems.

Remark 20.

To the best of our knowledge, this is the first existence result of time-inconsistency problems where no explicit form is available and the diffusion coefficient is controlled. Existence of equilibrium has been widely acknowledged as challenging and open problems. Even when stopping and control are considered separately, the existence results (of general form equilibrium) are based on either specific model (LQ or diffusion coefficient uncontrolled) or restrictive technical assumptions (say, Lipschitz condition uniform in control). In this subsection, we give an existence result under a rather practical model and mild assumptions. Indeed, it is a little bit unfortunate that all of our arguments in this subsection only apply to finitely supported distributions. It is conjectured that we have a correspondence between discount function and “mysterious function” (which is the solution to (4.26) in the current situation). We choose to leave this as a direction for future work.

4.4 A two-dimensional example

In this subsection we give an example in two dimensions to illustrate possible applications of our theoretical results to a multi-dimensional setting. For simplicity, we assume that a controller controls the diffusion coefficients of two independent Brownian motions:

The reward function is the expected squared euclidean distance to origin, discounted by a hyperbolic function of rate . To be specific, we choose

for . Using notations in Section 2, we assume . In other words, the controller can only choose the diffusion coefficient from a bounded interval. Besides, he can choose a region and terminate the system once the state pair exits . He will then receives

We denote by the Bessel process of order 0, and . As we have , we may choose , i.e., exclude the origin from state space. For this example, we have the following equilibrium result:

Proposition 4.7.

Denote by the ball without its center. Then is an equilibrium pair, where is later determined in (4.30).

To prove this proposition, considering and , we derive by direct computation for ,

In the calculation above, the indicator function is neglected because . Invoking formula (2.0.1) on page 297 of Borodin and Salminen (2002) and (4.17) with , we further have

Here and afterwards, we denote by the modified Bessel function of the first kind, with order . We will find a pair such that (3.17)-(3.22) are true. By definition of , we have when operating on functions . Therefore for any

On the other hand, it is straightforward to show that, for and ,

Thus, we have

Here we have use the fact that for . Obviously, choosing will make satisfy (3.11), and (3.19) will be true if

| (4.29) |

which will be handled at last. Next, we claim that if , i.e., the smooth fitting condition is verified, then inside so that (3.22) is also true. Define

It now suffices to show for because is equivalent to . By properties of modified Bessel functions of the first kind, we know any order derivatives of are positive. In particular, satisfies . Thus is increasing. As , , smooth fitting condition implies , i.e., . Now combining the facts that is increasing, and we know for . Clearly , , we thus conclude that for , which in turn implies inside . We now only need to determine such that smooth fitting condition and (4.29) are true. By direct computation, smooth fitting condition translates to

or equivalently (by a change of variable formula) , where satisfies

| (4.30) |

Numerical results show that . Noticing that , we have , which yields

which leads to (4.29). To conclude, we have proved that in the present example, the equilibrium pair is .

5 Conclusion

This paper provides a unified framework for the studying of time-inconsistent stopping-control problems, which has not been considered before. We define the equilibrium strategies and obtain an equivalent characterization based on an extended HJB system, providing a methodology to verify or exclude equilibrium. As applications, we propose an investment-withdrawal decision model, where the time-inconsistent decision makers are provided with both the opportunity to choose portfolios and the right to stop discretionarily. Two concrete examples are studied using the equilibrium theory established in this paper, and we can show the existence of equilibrium strategies respectively in these two examples. Finally, a two-dimensional example is also provided to illustrate applications of our theoretical framework in multi-dimensional case.

There are also many other interesting yet unexplored topics for future research. An ongoing work by the authors will consider the existence of equilibrium solutions for stopping control problems under fairly general assumptions. Generalizations of existence results in Subsection 4.3 to other non-exponential discount functions are also listed here as important open problems.

The established framework can also be coupled with other topics in financial mathematics, such as a more complicated market model.

Acknowledgements. The authors acknowledge the support from the National Natural Science Foundation of China (Grant No.11871036, No.12271290). The authors also thank the members of the group of Actuarial Sciences and Mathematical Finance at the Department of Mathematical Sciences, Tsinghua University for their feedbacks and useful conversations. The authors gratefully appreciate Ravi P. Agarwal from Texas A&M University-Kingsville, Guohui Guan from Renmin University of China and Kristoffer Lindensjö from Stockholm University for their useful discussions and suggestions. We are also particularly grateful to the two anonymous reviewers and the associated editor whose suggestions helped us to greatly improve the quality of the article.

Data availability statement. Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.

References

- Alia et al. (2017) I. Alia, J. Vives, and N. Khelfallah. Time-consistent investment and consumption strategies under a general discount function. arXiv, 2017.

- Bayraktar and Huang (2013) Erhan Bayraktar and Yu Jui Huang. On the multidimensional controller-and-stopper games. SIAM Journal on Control and Optimization, 51(2):1263–1297, 2013.

- Bayraktar and Li (2019) Erhan Bayraktar and Jiaqi Li. On the controller-stopper problems with controlled jumps. Applied Mathematics and Optimization, 80(1):195–222, 2019.

- Bayraktar et al. (2021) Erhan Bayraktar, Jingjie Zhang, and Zhou Zhou. Equilibrium concepts for time-inconsistent stopping problems in continuous time. Mathematical Finance, 31(1):508–530, 2021.

- Bayraktar et al. (2022) Erhan Bayraktar, Zhenhua Wang, and Zhou Zhou. Equilibria of Time-inconsistent Stopping for One-dimensional Diffusion Processes. pages 1–39, 2022. URL http://arxiv.org/abs/2201.07659.

- Björk et al. (2017) Tomas Björk, Mariana Khapko, and Agatha Murgoci. On time-inconsistent stochastic control in continuous time. Finance and Stochastics, 21(2):331–360, 2017.

- Bodnariu et al. (2022) Andi Bodnariu, Sören Christensen, and Kristoffer Lindensjö. Local time pushed mixed stopping and smooth fit for time-inconsistent stopping problems. pages 1–20, 2022. URL http://arxiv.org/abs/2206.15124.

- Borodin and Salminen (2002) A. N. Borodin and P. Salminen. Handbook of Brownian Motion—Facts and Formulae. Handbook of Brownian Motion—Facts and Formulae, 2002.

- Brown (1993) Robert F. Brown. A Topological Introduction to Nonlinear Analysis. 1993.

- Cai and De Angelis (2021) Cheng Cai and Tiziano De Angelis. A change of variable formula with applications to multi-dimensional optimal stopping problems. pages 1–18, 2021. arXiv:2104.05835.

- Choi et al. (2008) Kyoung Jin Choi, Gyoocheol Shim, and Yong Hyun Shin. Optimal portfolio, consumption-leisure and retirement choice problem with CES utility. Mathematical Finance, 18(3):445–472, 2008.

- Christensen and Lindensjö (2018) Sören Christensen and Kristoffer Lindensjö. On finding equilibrium stopping times for time-inconsistent markovian problems. SIAM Journal on Control and Optimization, 56(6):4228–4255, 2018.

- Christensen and Lindensjö (2020) Sören Christensen and Kristoffer Lindensjö. On time-inconsistent stopping problems and mixed strategy stopping times. Stochastic Processes and their Applications, 130(5):2886–2917, 2020.

- De Angelis and Peskir (2020) Tiziano De Angelis and Goran Peskir. Global regularity of the value function in optimal stopping problems. Annals of Applied Probability, 30(3):1007–1031, 2020.

- Dybvig and Liu (2010) Philip H Dybvig and Hong Liu. Lifetime consumption and investment: Retirement and constrained borrowing. Journal of Economic Theory, 145(3):885–907, 2010.

- Ebert et al. (2020) Sebastian Ebert, Wei Wei, and Xun Yu Zhou. Weighted discounting—On group diversity, time-inconsistency, and consequences for investment. Journal of Economic Theory, 189:1–40, 2020.

- Ekeland and Lazrak (2010) Ivar Ekeland and Ali Lazrak. The golden rule when preferences are time inconsistent. Mathematics and Financial Economics, 4(1):29–55, 2010.

- Ekeland and Pirvu (2008) Ivar Ekeland and Traian A. Pirvu. Investment and consumption without commitment. Mathematics and Financial Economics, 2(1):57–86, 2008.

- Farhi and Panageas (2007) Emmanuel Farhi and Stavros Panageas. Saving and investing for early retirement: A theoretical analysis. Journal of Financial Economics, 83(1):87–121, 2007.

- Friedman (1975) Avner Friedman. Stochastic Differential Equations and Applications. Academic Press, 1975.

- Guan et al. (2020) Guohui Guan, Zongxia Liang, and Fengyi Yuan. Retirement decision and optimal consumption-investment under addictive habit persistence. 2020. arXiv:2011.10166.

- He et al. (2020) Xue Dong He, Zhao Li Jiang, and Steven Kou. Portfolio Selection under Median and Quantile Maximization. SSRN Electronic Journal, pages 1–63, 2020. doi: 10.2139/ssrn.3657661.

- He and Jiang (2019) Xuedong He and Zhaoli Jiang. On the equilibrium strategies for time-inconsistent problems in continuous time. 2019. SSRN:3308274.

- Helland (1996) Inge Helland. One-dimensional diffusion processes and their boundaries. 1996. URL https://www.duo.uio.no/bitstream/handle/10852/47728/1996-20.pdf?sequence=1.

- Hernández and Possamaï (2020) Camilo Hernández and Dylan Possamaï. Me, myself and I: A general theory of non-Markovian time-inconsistent stochastic control for sophisticated agents. 2020. arXiv:2002.12572.

- Hu et al. (2012) Ying Hu, Hanqing Jin, and Xun Yu Zhou. Time-inconsistent stochastic linear-quadratic control. SIAM Journal on Control and Optimization, 50(3):1548–1572, 2012.

- Hu et al. (2017) Ying Hu, Hanqing Jin, and Xun Yu Zhou. Time-inconsistent stochastic linear-quadratic control: Characterization and uniqueness of equilibrium. SIAM Journal on Control and Optimization, 55(2):1261–1279, 2017.

- Hu et al. (2020) Ying Hu, Hanqing Jin, and Xun Yu Zhou. Consistent investment of sophisticated rank-dependent utility agents in continuous time. 2020. arXiv: 2006.01979.

- Huang and Nguyen-Huu (2018) Yu Jui Huang and Adrien Nguyen-Huu. Time-consistent stopping under decreasing impatience. Finance and Stochastics, 22(1):69–95, 2018.

- Huang and Wang (2020) Yu Jui Huang and Zhenhua Wang. Optimal equilibria for multi-dimensional time-inconsistent stopping problems. 2020. arXiv:2006.00754.

- Huang and Yu (2019) Yu Jui Huang and Xiang Yu. Optimal stopping under model ambiguity: a time-consistent equilibrium approach. 2019. arXiv:1906.01232.

- Huang and Zhou (2018) Yu Jui Huang and Zhou Zhou. Strong and weak equilibria for time-inconsistent stochastic control in continuous time. 2018. arXiv:1809.09243.

- Huang and Zhou (2020) Yu Jui Huang and Zhou Zhou. Optimal equilibria for time-inconsistent stopping problems in continuous time. Mathematical Finance, Forthcoming:1–32, 2020.

- Huang et al. (2020) Yu Jui Huang, Adrien Nguyen-Huu, and Xun Yu Zhou. General stopping behaviors of naïve and noncommitted sophisticated agents, with application to probability distortion. Mathematical Finance, 30(1):310–340, 2020.

- Itô and McKean (1996) Kiyosi Itô and H. P. McKean. Diffusion processes and their sample paths: Reprint of the 1974 edition. Springer Science & Business Media, 1996.

- Jeon and Park (2020) Junkee Jeon and Kyunghyun Park. Optimal retirement and portfolio selection with consumption ratcheting. Mathematics and Financial Economics, 14(3):353–397, 2020.

- Karatzas and Sudderth (2001) Ioannis Karatzas and William D. Sudderth. The controller-and-stopper game for a linear diffusion. Annals of Probability, 29(3):1111–1127, 2001.

- Karatzas and Wang (2000) Ioannis Karatzas and Hui Wang. Utility maximization with discretionary stopping. SIAM Journal on Control and Optimization, 39(1):306–329, 2000.

- Karatzas and Zamfirescu (2006) Ioannis Karatzas and Ingrid Mona Zamfirescu. Martingale approach to stochastic control with discretionary stopping. Applied Mathematics and Optimization, 53(2):163–184, 2006.

- Karatzas and Zamfirescu (2008) Ioannis Karatzas and Ingrid Mona Zamfirescu. Martingale approach to stochastic differential games of control and stopping. Annals of Probability, 36(4):1495–1527, 2008.

- Lieberman (1986) Gary M. Lieberman. Intermediate Schauder theory for second order parabolic equations. I. Estimates. Journal of Differential Equations, 63(1):1–31, 1986.

- Lieberman (1996) Gary M. Lieberman. Second Order Parabolic Differential Equations. World Scientific, 1996.

- Peskir (2007) Goran Peskir. A change-of-variable formula with local time on surfaces. Lecture Notes in Mathematics, pages 70–96, 2007.

- Peskir and Shiryaev (2006) Goran Peskir and Albert Shiryaev. Optimal Stopping and Free-Boundary Problems. 2006.

- Seeley (1973) Robert T. Seeley. Extension of Functions Defined in a Half Space. Proceedings of the American Mathematical Society, 37(2):622, 1973.

- Strotz (1955) Robert Henry Strotz. Myopia and inconsistency in dynamic utility maximization. The Review of Economic Studies, 23(3):165–180, 1955.

- Tan et al. (2021) Ken Seng Tan, Wei Wei, and Xun Yu Zhou. Failure of smooth pasting principle and nonexistence of equilibrium stopping rules under time-inconsistency. SIAM Journal on Control and Optimization, 59(6):4136–4154, 2021.

- Wachter and Yogo (2010) Jessica A. Wachter and Motohiro Yogo. Why do household portfolio shares rise in wealth? Review of Financial Studies, 23(11):3929–3965, 2010. ISSN 08939454. doi: 10.1093/rfs/hhq092.

- Whitney (1934) Hassler Whitney. Analytic Extensions of Differentiable Functions Defined in Closed Sets. Transactions of the American Mathematical Society, 36(1):63, 1934.

- Xu and Zheng (2020) Zuo Quan Xu and Harry Zheng. Optimal investment, heterogeneous consumption and best time for retirement. 2020. arXiv:2008.00392.

- Yong (2012) Jiongmin Yong. Time-inconsistent optimal control problems and the equilibrium HJB equation. Mathematical Control and Related Fields, 2(3):271–329, 2012.

- Yong and Zhou (1999) Jiongmin Yong and Xun Yu Zhou. Stochastic Controls: Hamiltonian Systems and HJB Equations. Springer, 1999.

Appendix A Proofs of results in Section 3

Proof of Lemma 3.2.

We first introduce some notations that will be used. For Markov times and taking value in , we define . Strong Markovian property of the Markov processes implies

for Borel-measurable . The fact and strong Markovian property yield

From now on, write , for fixed . Consider . For sufficiently small, let . Choose a cut-off function such that , on and denote . Clearly . Based on the definition of , we have

| (A.1) | |||||

where

for some . Here we have used the fact that , , Hlder’s inequality, and standard estimation in stochastic differential equations: under Assumption 1, for any , ,

| (A.2) |

See Yong and Zhou (1999). For , we still use the cut-off technique near to make and all other things remain the same. ∎

Proof of Lemma 3.3.

Based on the definition of , we have

| (A.3) |

Noting that (see (2.2)), we conclude , and for some with ,

To estimate , we conclude from Theorem 6.3, Chapter 1 in Yong and Zhou (1999) that under the case of constant initial condition, we can take . As such, using arguments in the proof of Lemma 3.1 of Huang and Yu (2019), we have

for . Thus, picking , we have

| (A.4) |

On the other hand, it is clear from definition that . Moreover, for any ,

| (A.5) |

Now, using (A.5) and Markovian property (of ), and conditioning on if necessary, we have

The indicator function can be ignored by the same reason of estimation (A.4). Using the similar cut-off technique as in the proof of Lemma 3.2, we have

| (A.6) |

Proof of Lemma 3.4.

To proceed with the proof of Theorem 3.6, we need the following technical lemmas. For simplicity, we write and define

Lemma A.1.

For any compact subset , , uniformly in .

Proof.

We choose another compact such that , and denote the cut-off of on by . For any , , we have the following estimates:

where

We emphasize that the in the last inequality is uniform for . Combining the last two estimates, we have

Letting , and using uniform continuity on , we complete the proof. ∎

Proof.

First assume that (3.9) holds. We consider the Taylor expansion of when is sufficiently small. When or , we can assume that both and are in or , and is , as such, Taylor expansion is directly applicable. Let us focus on . For , using Taylor expansion for , we have

| (A.8) |

For , we use Taylor expansion for to get

| (A.9) |

Using locally boundedness of , , and , we have in (A.8) and (A.9) are uniform in . Now, using the usual cut-off techniques, we only consider . Combining (A.8), (A.9) and (3.9), we have

As

using the above estimates and (A.2), we have the desired conclusion. ∎

Lemma A.3.

Suppose that with is a continuous semimartingale such that

| (A.10) |

and

| (A.11) |

Then

Proof.

We are now ready to give the proof of sufficiency part of Theorem 3.6.

Proof of Theorem 3.6, (1).

Based on Lemma A.2, it is sufficient to prove that if (A.7) and (3.4’) are ture, then (3.4) holds. Pick a sequence of , such that . For simplicity, we still denote this limit by . Fix for now. For each , using continuity of , we find a such that

Picking a subsequence, we assume . If , fixing another such that , letting on both sides of

and using the boundedness of from (A.7), we have

yielding a contradiction. Thus, we can choose a sufficiently small, such that

where

Using Lemma A.1, we conclude

As such, using (3.4’), we have

On the other hand, for any ,

Letting on the right hand side of the last inequality gives

completing the proof. ∎

To provide a proof of necessity part of Theorem 3.6, we need to invoke a local time formula on surfaces (c.f., Peskir (2007)) because no regularity of across is guaranteed and thus standard It’s formula is not applicable. However, local time formula needs the boundary to be the graph of a function with certain properties. In our work, it is sufficient to express locally as graph of a smooth function, based on the prescribed regularity and implicit function theorem. However this can only be done along directions not in tangent space. To resolve this we first propose a weaker version of smooth fitting, prove that it is a necessary condition of (3.4) and finally show that it is equivalent to (3.9). To this end, we need to introduce some notations. For , we write , where is canonical orthogonal basis. For , denote the unit normal vector by . Moreover, for , we define:

We propose another version of smooth fitting:

| (A.13) |

Proof.