The role of information in high dimensional stochastic optimal control

Abstract.

The stochastic optimal control of many agents is an important problem in various fields. We investigate the problem of partial observations, where the state of each agent is not fully observed and the control must be decided based on noisy observations. This results in a high-dimensional Markov decision process that is impractical to handle directly. However, in the limit as the number of agents approaches infinity, a finite-dimensional mean-field optimal control problem emerges, which coincides with the problem of full information.

Our main contribution is to investigate a central limit theorem for the Gaussian fluctuations of the mean-field optimal control. Our findings show that partial observations play an essential role in the fluctuations, in contrast to the mean-field limit. We establish a method that uses an approximate Kalman filter, which is straightforward to compute even when the number of states is large. This provides some theoretical evidence of the efficacy of Kalman filter methods that are commonly used across a range of practical applications. We demonstrate our results with two examples: an epidemic model with observations of positive tests and a simple two-state model that exhibits a phase transition at which point the fluctuations diverge.

1. Introduction

The role of information in stochastic control has been central to many applications. The Kalman filter was developed to predict a dynamically evolving state with noisy observations [22],[21] and has been employed in aeronautics, navigation, and economics, among other fields. The Kalman filter provides part of the well-known solution to the linear-quadratic-Gaussian (LQG) control problem, which is the basis of this study.

While individual behavior can be impossible to predict, systems comprised of many individuals tend to develop recognizable behaviors. To give an economic perspective to the problem, we highlight two influential works in economics, amid a vast research field. The role of information was recognized in [31] as part of the critique that a socialist economy cannot adapt to individual needs as the information on the individual is lost, albeit the argument is made without mathematical formalism. Later in [18], [19] imperfect information is shown to give rise to inefficient free markets using mathematical models.

In this work, we study the optimal policies given available observations, such as by a government maximizing the well-being of the population or by a private enterprise maximizing its profit. We present a solution that both closely approximates the optimal policy and may be computed using well-established and computationally efficient techniques.

The concept of a mean-field limit originates in physics and provides a simplified framework to study systems of many interacting particles. The central assumption of this framework is that the particles only interact through a macroscopic field, corresponding to their mean values. Connections between mean-field theories and partial observation stochastic control have been developed in the recent works of [4], [7]. The fluctuations of the mean-field limit capture how the system of particles deviates from its mean. For the stochastic optimal control of many agents with partial information, we find that the role of information is in the fluctuations of the mean-field limit.

We consider a mathematical framework of a finite-state Markov decision process with a parallel finite-state observation process. We assume the problem involves a large number, , of identical agents each with a fixed number of states. Adding additional states allows for further specification of the individual agents. In this framework, each individual produces observations at rates depending on their state. We consider a fixed number of control parameters to be chosen at each time based on the available observations. The cost is given by functions of the macroscopic state variables, which aggregate the individuals in each state. Some socio-economic applications of related finite-state mean field games have been given in [17].

Our first inquiry is of the limit as the number of agents, , approaches infinity. In this asymptotic limit, the (discrete) finite-state stochastic control problem approaches a (continuous) finite-dimensional nonlinear problem of (deterministic) optimal control. We call this problem the mean-field limit. The deterministic nature of the limiting control problem allows the state to be predicted, and the optimal control can be computed without using any observations. A similar remark has been made for related problems in [8], Remark 2.27, and in a context closely related to our own in [9]. Alternatively, mean-field control problems where the information of individual agents have been considered, for example in [20] where they develop the stochastic maximum principle approach and calculate the solution of a linear-quadratic-Gaussian example. The problem of rigorous computational approaches to such problems beyond linear-quadratic-Guassian assumptions appears to be unsolved.

We next study the fluctuations of the mean-field limit. Such fluctuations in Markovian population models were obtained in [23], [5], [27], [30], [11]. For the fully observed controlled version, analysis of the fluctuations has been carried out in [32], [9] for finite-state spaces. Furthermore, the approach has been extended to continuous-state spaces in [12] where the master equation is used to find a feedback control form. Rather than focusing on the master equation, which involves additional complications with partial observations, we focus on a localized analysis around a mean-field trajectory.

The localized asymptotic analysis we carry out involves solving a linear-quadratic-Gaussian control (LQG) problem using the problem data approximated quadratically about a mean-field solution. This approximation follows an approach similar to [6], here it was used for fully observed optimal control. The solution to the LQG problem satisfies the separation principle, where the Kalman filter is used to estimate the state, and the dynamic programming principle readily provides a linear feedback control. Computation of these solutions involves solving decoupled forward and backward Ricatti-type systems of ordinary differential equations. Given these solutions, we can then express an approximate feedback control policy, which we show is accurate to the first order () correction of the cost.

We analyze two illustrative examples. The first example is motivated by the Ising model of statistical physics and provides a glimpse of the behavior near a phase transition. In this example, we see clearly that the fluctuations diverge at the critical point for the phase transition.

Our second example is to consider a simple epidemic model with observations corresponding to tests of individuals. This example showcases the computational and practical possibilities of our approach. While most of this paper is written for continuous time, the approach applies to discrete time, which is used in this example.

We briefly mention a few extensions and related problems that may be of interest to keep in mind.

-

•

While we consider ‘global’ controls with a centralized planner, it includes the case of individual controls, where each agent selects a control with the same access to ’global’ information and full information of their state. Since agents are identical and have the same information, the optimal policy will have the same control for any agents in the same state, and thus we can reduce to global controls by considering the control in a feedback form, where denotes the number of states. The case when individual agents have partial observations of their state is similar to what appears in [20] and other works, and would also be interesting in our context.

-

•

A game-theoretic problem where each player has the same information and is in a Nash equilibrium can be considered. In the special case of a potential game, Nash equilibria can be found as optimal policies within our framework. Otherwise, the Nash equilibrium constraint introduces additional complications. While mathematically elegant, the assumption that each player behaves optimally is unlikely to hold in applications. See for instance [13], where the behavior of financial investors with imperfect information is modeled based on experiments.

-

•

Market price is commonly considered in economic models by including a market-clearing constraint. The convergence of a finite-state model to its mean-field limit has been considered in the recent work [15].

-

•

Continuous-space problems present many interesting challenges. The problems we consider may come from a discretization of continuous space problems by ‘coarse-graining’ nearby particles into the same state and approximating the state transitions. Understanding the continuum limits can be a highly difficult problem. It has been discussed for mean-field games in [12], although including partial observation has its own challenges.

2. Many agent problem

We consider identical agents with states for and a global control . We let denote the empirical measure of states, so that . We make the important simplifying ‘mean-field’ assumption that all interactions are through this empirical measure.

An agent in state transitions to state at rate . If is constant, then this makes the time until the next transition an exponential random variable with a rate of The transitions from , accounting for all individuals in state , occur at rate , where is the number of individuals in stat .

These dynamics can be expressed by the equations

| (1) |

where each is an independent Poisson process with non-homogeneous rate

There is always a unique (in law) solution , see [16] for details on constructing such processes. We will abbreviate the paths as

We consider also cumulative measurements , where at rate and thus the dynamics of can be expressed as

| (2) |

where again each is an independent non-homogeneous Poisson process of rate . We let be the natural filtration of , and be the natural filtration of so that . The filtration represents the information available through the observations of .

The finite time-horizon problem is to find to minimize

| (3) |

over control policies dependent on the history of measurements, for a measurable sequence of functions (). Equivalently, is progressively measurable with respect to the filtration .

Remark 2.1.

There are many possible generalizations of these controlled processes. The simplest is to add the possibility of births and deaths, which would cause no problem for our analysis and we omit simply to reduce the burden of notation. Inhomogeneity in time for and could also be easily handled.

A very interesting case would be when has additional dependence on . This includes, for example, when each particle has a given position on a lattice, , and interactions take place with nearest neighbors on the lattice. This may result in much more complicated phenomena and will be partly explored by the author in related work.

We will consider the mean behavior and the fluctuations of the mean. To anticipate these results it is useful to consider the Doob-Meyer decomposition of , which takes the form

| (4) |

where the expected drift is given by

| (5) |

and the covariation of the martingale term, , sums the squared jumps so that for ,

| (6) |

where is an by matrix with entries, supposing the column corresponds to the transition from to ,

or for the matrix product

Basic results on uncontrolled models can be found in [23] and many subsequent works. Four different representations of the martingale term for similar Markovian queue models are given in [29], along with the proof of a central limit governing the fluctuations about a high-intensity limit.

Illustrative examples of the problem we study are given and worked out in Section 5.

3. Mean-field approximation

The mean-field approximation ignores the stochastic martingale term of the Doob-Meyer decomposition (4) and recovers the limiting behavior as . In the mean-field problem, the empirical state measure becomes a deterministic trajectory , the control becomes , and the transition rates are replaced by a drift from (5). The resulting dynamics are necessarily nonlinear in .

The mean-field problem considers (weak) solutions to the dynamics

| (7) |

with cost

| (8) |

The following theorem is a basic result for the mean-field theory of stochastic optimization problems. We note that the state naturally takes values in the probability simplex, which we denote by . We make the following assumptions on the problem data:

-

A1

We assume that , , are jointly continuous in and . We assume that is uniformly bounded below and is uniformly bounded.

-

A2

We assume that is coercive in the sense that is compact for each and .

-

A3

We assume the standard convexity condition that for each , the set

is convex. In the case that is linear (as in our examples) this assumption reduces to that is convex.

We use the notation to denote convergence in distribution for the random variable, i.e., weak convergence. In Theorem 3.1, weak convergence is equivalent to convergence in probability because the limits are deterministic.

There are several approaches to analyzing the mean-field limit of the -player problem, from which we will borrow some results.

-

•

The -convergence approach. Our main arguments are inspired by this approach, but we do not attempt to show the full -convergence. This approach is well-suited as it does not require convergence of the control policy, which we do not expect in all cases.

-

•

The approach of Young-measures. We borrow the concept from Young-measures of a compactification of the control policies. Assumption A3 enables us to pass from a Young-measure randomized control back to a control policy using a sort of barycenter.

-

•

The approach by Hamilton-Jacobi equation. Since we are interested in applications for high-dimensional problems the Hamilton-Jacobi equation does not provide a very practical approach and also cannot easily incorporate partial information. However, when we address the fluctuations in Section 4 we will require estimates that closely parallel results from the Hamilton-Jacobi equations.

The assumption that the mean-field problem has a unique minimizer is a simplifying assumption to avoid obfuscation from having randomized limits.

Theorem 3.1.

If the mean-field problem has unique minimizer, , and are optimizers of the -player problem (3), then as and .

Furthermore, is an approximate optimal control for the -player problem in the sense that .

Proof.

We let denote the Skorokhod space of càdlàg paths from into . We first obtain tightness for the distributions of , which follows from A1 by considering that and decompose as the difference of increasing processes in (1) and (2). We next compactify the control in the space of measures, , such that for ,

| (9) |

Assumption A2 and boundedness of the cost implies tightness for these measures . We let denote the disintegration of the measure with respect to the distribution of . For every subsequence we find a subsubsequence such that and .

Using A1 , we have that

holds almost surely, and

By A3 and the Kuratowski-Ryll-Nardzewski measurable selection theorem, we find a random measurable control policy such that, for almost every ,

and

hold almost surely. (In the case when is linear and is convex, this is given simply by the barycenter, .)

We obtain the lower bound inequality for the sequence of minimizers

and , is a (randomized) weak solution to the mean-field dynamics (7).

We now consider the optimizer of the mean-field problem, and . Since, is deterministic, we can directly use as a policy for the player problem with cost . Note that makes no use of information. We now observe, using tightness and continuity as above, that as and

which proves the final statement of the theorem.

We now also infer the optimality of the limit of optimizers, , because

The inequality implies that equality holds almost everywhere and thus almost surely.

Since every subsequence of has a subsubsequence converging, as , we conclude that as and . ∎

3.1. Optimality Criterion

Having obtained a minimizer of the mean-field problem (8) we consider the first-order optimality criteria. We call the co-state and define the generalized Hamiltonian to be

Given an optimal trajectory , , we let solve the co-state equation, with , , so that and solve

| (10) | ||||

The operators and are the partial derivatives with respect to the co-state and state, respectively. The Pontryagin maximum principle states that at points of continuity of and ,

| (11) |

Assuming some smoothness of the trajectories, provides the first variation of the cost. A variation of the position at time , yields a change in the optimal cost of .

While (10) and (11) provide necessary conditions, if a unique solution exists with the minimal cost then Theorem 3.1 implies this is the mean-field limit of the -agent problem.

The mean observations are easily recovered by

| (12) |

where

3.2. Propagation of Chaos

It is often interesting to see what Theorem 3.1 says about individual particles. A propagation of chaos result states that for each agent, its limiting distribution corresponds to an independent Markov process with the mean-field empirical measure fixed.

More generally, choose agents with states , then the joint distribution of these particles converges to the distribution of independent agents, where each agent satisfies the Markovian transitions determined by

4. Fluctuations of the Mean Field Limit

We aim to refine the mean-field approximation to capture the Gaussian fluctuations of the limit. We assume and are the unique minimizers of the mean-field problem and is the co-state that solves (10). We also let be the mean observations that solve (12). We will show that the state, observations, and control can be expanded as

where , and have mean zero, and minimize a linear-quadratic-Gaussian problem.

4.1. Linear-Quadratic-Gaussian Approximation

The linear approximation of the dynamics for the state and observations are

| (13) | ||||

We have used to represent the gradient operator, such that is a linear transformation mapping and . The diffusion coefficients and are an by matrix and a by matrix that captures the quadratic variation of the process see (6) and and are independent Brownian motions. Specifically, when

and

Similarly,

We assume that where is Gaussian with mean zero and . The cost will have the asymptotic expansion

where the correction to the cost from the fluctuations is given by (dependence on , , and is implicit)

| (14) | ||||

The control will now be restricted to depend only on the linearized observations, . The problem to minimize with such a partial information constraint is well known [21].

To express the solution, we define the following

| (15) | ||||

Now we can express the linear quadratic cost in a standard form:

subject to

| (16) |

where is a continuous martingale process with infinitesimal covariance (i.e., quadratic covariation) given by .

Furthermore, we impose the information constraint that , where the linearized observations are given by

| (17) |

with and is a continuous martingale process with infinitesimal covariance .

The first step to solve the LQG problem is to compute the estimator . The separation theorem states that computing the estimator decouples from determining the control problem, and the optimal control is given as the linear feedback optimizer of the full information LQ problem substituting in .

We compute the covariance matrix by solving the forward matrix Ricatti differential equation

| (18) |

with . Importantly, while the covariance of may depend on the control, the covariance of the estimation error difference does not. Equation (18) always has a solution on because so the semidefinite inequality, is maintained.

We get the estimator given control by solving

with . Supposing that , we have computed .

For the optimal control, we solve the backward Ricatti equation

| (19) |

with . The optimal control is then given by

4.2. Central Limit Theorem

We will now address the convergence to the solution of the LQG approximation. We make the additional assumption of regularity for the mean-field solution and problem data:

-

A4

We suppose that is smooth and and are smooth near in a neighborhood of .

We begin with a lemma that relates the first-order asymptotic expansion of the cost to the linear quadratic cost, using the optimality criteria and Taylor expansions of the data.

Lemma 4.1.

Proof.

The proof is a direct calculation using the Taylor expansion of the cost, the optimality criteria (10) and (11), and an expansion of the drift in the dynamics of (1).

The terms of are part of our conclusion, and to handle the term we have

We now use (11) to equate

and we use the Doob-Meyer decomposition (4) to rewrite under the expectation

We obtain

and conclude the proof. ∎

We next show that solutions to the LQG problem can be approximated with -agents. This result also shows how the information is incorporated into an asymptotically optimal approximate control.

Proposition 4.2.

We assume A1 - A4 , is the global minimum of the mean-field problem, and , and a solution to (19) exists on . We suppose that as , and .

We define the approximate Kalman filter and control by

| (20) |

and

| (21) |

Let be the optimal solution of the LQG problem defined above. Then, with that solves (1), the asymptotic cost for this approximate optimal control is given by

and , , and as .

Proof.

There exist unique solutions locally for (18), and if we show this solution is bounded then it exists for all . We bound from above by the solution of

and is bounded from below by , thus the unique solution to (18) exists.

Itô’s lemma implies that

The terms and are similarly bounded. An application of Gronwall’s inequality yields

We would like to continue with a final result that gives a lower bound to the first-order asymptotics of the finite -agent problem by the LGQ problem, which would complete our characterization of the fluctuations. We will sketch an argument for such a result, but cannot provide a complete proof due to a lack of full understanding of a key technical component.

Theorem* 4.1.

We assume A1 - A4 , is the global minimum of the mean-field problem, and , and (19) has a solution on . We suppose that , which is normally distributed with zero mean and finite covariance and . We then let and denote optimal solutions of the linear-quadratic-Gaussian approximation.

Then the first-order asymptotic formula for the cost holds that

and .

Given minimizers of the finite -agent problem, we consider , , and . Based on the principles of tightness from [2] and estimates using asymptotic coercivity of LQG with respect to

one can obtain a weak limit of .

We define the measure-valued process as the conditional distribution

The approach for Markov control policies has been developed in [14] and implemented for the ‘closed-loop’ mean-field convergence problem in [24], and we show how this can be adapted to Markov control policies of the conditional distributions . Proceeding as in Theorem 3.1, we compactify the control variable as a function of the conditional distribution as , such that for , with now the conditional-Markovian interpretation that

| (22) |

This allows us to obtain a weak limit from which we can disintegrate into maps and finally consider the control policy

The cost has the form, using the law of total expectation and that is -adapted,

where

Since is convex (recall we have assumed that ) it follows that

We also have that (16) holds.

Our key technical obstacle is that the information constraint, , requires convergence of to that is the conditional probability distribution of given , the filtration generated by . It is well-known that the weak convergence of and is not sufficient to guarantee that is -adapted.

We can mention a couple of works that address this issue but have been able to fully understand a resolution for our problem. The ambitious work of [1] develops a theory of extended weak convergence, under which the conditional distributions converge. It is found that the continuity of paths of the limit process plays a fundamental role. Further development related to the convergence of conditional expectations was undertaken in [10] and [25]. Extended weak convergence has had success in the analysis of optimal stopping as well as backward stochastic differential equations. The recent work [3] has shown that extended weak convergence coincides with other definitions of an ‘adapted’ weak topology when the time is discrete. In particular, the adapted Wasserstein distance minimizes the expected distance between the ‘causal couplings’ of probability measures on the probability space and provides a natural metric for the extended weak convergence topology.

5. Examples

5.1. Ising Game

In the Ising example, there are two states for each agent and two global controls that determine the rate of transitions between the states. It is inspired by the physical Ising model and provides an example of a critical phase transition. We consider the following parameters of the model:

-

•

governs the cost of deviating the control from the rest state of . (Small corresponds to high cost).

-

•

adds an external bias to a preferred state.

-

•

adds a preference to congregate in one state (when ).

-

•

governs the rate of observations of the states.

The controls are exactly the transition rates, i.e., and . We assume the cost is

We reduce the problem to a single dimension by ( and ). We now have that jumps by at rate and jumps by at rate .

We will observe measurements of each particle, with rate so that

for some constant .

We work in the reduced form with the mean-field limit of . The dynamics of the mean-field system simplify to

with cost

If we consider the difference of the number of measurements, it evolves by

The optimal control given co-state is

Similarly,

The Hamiltonian reduces to,

The Hamiltonian flow for the mean-field limit is

When , the critical points are solved simply by and , and, when ,

so

thus

so

We have

We will consider the equilibrium at . First we compute

and

We then calculate

The error covariance matrix, , in equilibrium solves

We want the positive root which simplifies to

Of course, the covariance becomes smaller when is larger and more measurements are available. When , , there is no benefit in deviating from the mean-field control and (although this no longer satisfies the assumptions of Theorem 4.1) is simply the covariance of given the dynamics

To solve for we have

We solve to get

so the solution exists if and is given by

In the critical case, , . The evolution is given by

and so, since remains near , the drift cancels over long times while the fluctuations grow.

5.2. SIR Epidemic Model

As a second example we consider a compartmental epidemic model. There are three states:

-

•

, susceptible,

-

•

, infectious,

-

•

, recovered,

and one control (a social distancing parameter). The additional parameters of the problem are

-

•

is the recovery rate.

-

•

is the base line infection rate.

-

•

is a coefficient of the cost to reduce below .

-

•

is a cost of infections.

-

•

rate of testing of infected individuals.

We then suppose that a transition from susceptible to infectious occurs as , and a transition from infectious to recovered occurs at rate .

We assume the infected individuals are tested at a rate ,

The cost is

A similar cost was used in [28] with applications to the COVID-19 pandemic. We can consider the problem with a terminal condition, but for simplicity we set .

For the mean field SIR example, the mean-field dynamics are

The number of confirmed tests evolves simply by

The recovered state, , is irrelevant so we will ignore it. The Hamiltonian is then

The control satisfies

Plugging this back in we get

The Hamiltonian equations are

and

Equilibria occur when and

Due to the possible instability at the equilibrium, linearizing can lead to very bad results.

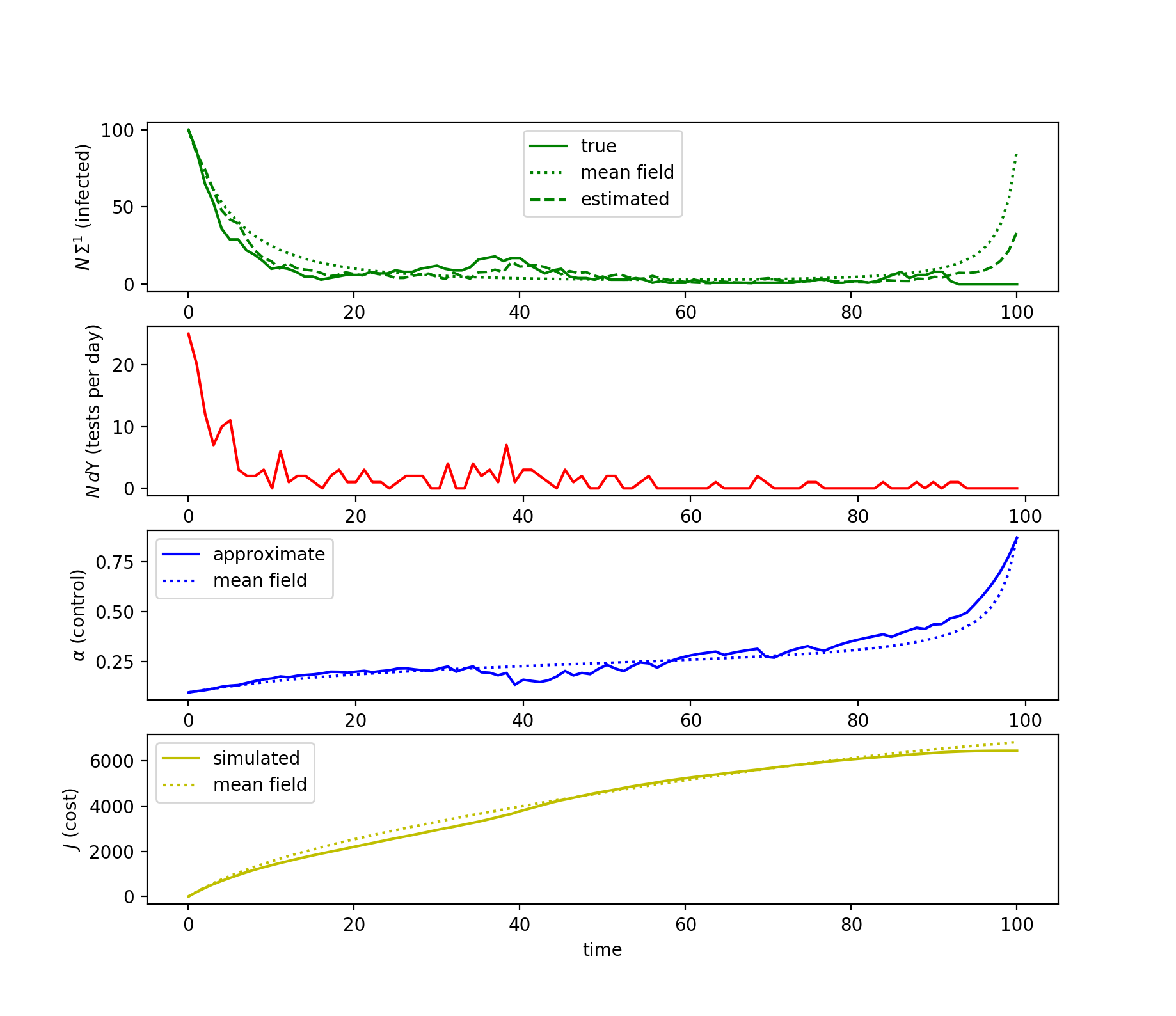

We show numerical results based on solving the Hamiltonian equations and Kalman filter numerically in discrete time (; see Section 6). We select as parameters , , , , , , and . Results are shown in Figure 1.

6. Discrete Time

All of our analysis also applies to a problem in discrete time. We present it in a way that is a discretization of our continuous time problem, although it is not necessary that the time steps are small. We suppose that at time the transitions at time from state to occur with probability . We require that . We assume the cost has the form

When is large and is small, the number of agents transitioning from to is well approximated by a Poisson distribution of rate . We then can use the same definitions for , , , and .

The mean-field problem corresponds to the discretized dynamics

The co-state, ,

allows us to compute the gradient of the cost as

The statement and proof of Theorem 3.1 is now essentially the same.

To express the linear quadratic problem to describe the fluctuations, we again define the following

| (23) | ||||

The discrete form of the covariance equation, (18), takes the form

| (24) |

and the estimator is given by

| (25) | ||||

The backward Ricatti equation is

| (26) |

and the optimal control is

References

- [1] David Aldous. Weak convergence and the general theory of processes. Unpublished manuscript, 1981.

- [2] David Aldous. Stopping times and tightness. ii. The Annals of Probability, pages 586–595, 1989.

- [3] Julio Backhoff-Veraguas, Daniel Bartl, Mathias Beiglböck, and Manu Eder. All adapted topologies are equal. Probability Theory and Related Fields, 178(3):1125–1172, 2020.

- [4] Elena Bandini, Andrea Cosso, Marco Fuhrman, and Huyên Pham. Randomized filtering and Bellman equation in Wasserstein space for partial observation control problem. Stochastic Processes and their Applications, 129(2):674–711, 2019.

- [5] Andrew D Barbour. On a functional central limit theorem for Markov population processes. Advances in Applied Probability, 6(1):21–39, 1974.

- [6] Pierpaolo Benigno and Michael Woodford. Linear-quadratic approximation of optimal policy problems. Journal of Economic Theory, 147(1):1–42, 2012.

- [7] Alain Bensoussan and Sheung Chi Phillip Yam. Mean field approach to stochastic control with partial information. ESAIM: Control, Optimisation and Calculus of Variations, 27:89, 2021.

- [8] R. Carmona and F. Delarue. Probabilistic Theory of Mean Field Games with Applications I: Mean Field FBSDEs, Control, and Games. Probability Theory and Stochastic Modelling. Springer International Publishing, 2018.

- [9] Alekos Cecchin and Guglielmo Pelino. Convergence, fluctuations and large deviations for finite state mean field games via the master equation. Stochastic Processes and their Applications, 129(11):4510–4555, 2019.

- [10] François Coquet, Jean Mémin, and Leszek Słominski. On weak convergence of filtrations. In Séminaire de probabilités XXXV, pages 306–328. Springer, 2001.

- [11] Donald Andrew Dawson and Xiaogu Zheng. Law of large numbers and central limit theorem for unbounded jump mean-field models. Advances in Applied Mathematics, 12(3):293–326, 1991.

- [12] François Delarue, Daniel Lacker, Kavita Ramanan, et al. From the master equation to mean field game limit theory: A central limit theorem. Electronic Journal of Probability, 24, 2019.

- [13] Larry G Epstein and Martin Schneider. Ambiguity, information quality, and asset pricing. The Journal of Finance, 63(1):197–228, 2008.

- [14] Wendell H Fleming and Makiko Nisio. On stochastic relaxed control for partially observed diffusions. Nagoya Mathematical Journal, 93:71–108, 1984.

- [15] Masaaki Fujii and Akihiko Takahashi. A finite agent equilibrium in an incomplete market and its strong convergence to the mean-field limit. arXiv preprint arXiv:2010.09186, 2020.

- [16] Iosif Il’ich Gihman and Anatolij Vladimirovič Skorohod. Controlled stochastic processes. Springer Science & Business Media, 2012.

- [17] Diogo Gomes, Roberto M Velho, and Marie-Therese Wolfram. Socio-economic applications of finite state mean field games. Philosophical Transactions of the Royal Society A: Mathematical, Physical and Engineering Sciences, 372(2028):20130405, 2014.

- [18] Bruce C Greenwald and Joseph E Stiglitz. Imperfect information, credit markets and unemployment. Technical report, National Bureau of Economic Research, 1986.

- [19] Bruce C Greenwald, Joseph E Stiglitz, and Andrew Weiss. Informational imperfections in the capital market and macro-economic fluctuations. Technical report, National Bureau of Economic Research, 1984.

- [20] Mokhtar Hafayed, Syed Abbas, and Abdelmadjid Abba. On mean-field partial information maximum principle of optimal control for stochastic systems with Lévy processes. Journal of Optimization Theory and Applications, 167(3):1051–1069, 2015.

- [21] R. E. Kalman and R. S. Bucy. New results in linear filtering and prediction theory. Journal of Basic Engineering, 83(1):95–108, 03 1961.

- [22] Rudolph Emil Kalman. A new approach to linear filtering and prediction problems. 1960.

- [23] Thomas G Kurtz. Limit theorems for sequences of jump Markov processes approximating ordinary differential processes. Journal of Applied Probability, 8(2):344–356, 1971.

- [24] Daniel Lacker. On the convergence of closed-loop Nash equilibria to the mean field game limit. arXiv preprint arXiv:1808.02745, 2018.

- [25] Jean Mémin. Stability of Doob-Meyer decomposition under extended convergence. Acta Mathematicae Applicatae Sinica, 19(2):177–190, 2003.

- [26] Paul André Meyer and WA Zheng. Tightness criteria for laws of semimartingales. In Annales de l’IHP Probabilités et statistiques, volume 20, pages 353–372, 1984.

- [27] M Frank Norman. A central limit theorem for Markov processes that move by small steps. The Annals of Probability, 2(6):1065–1074, 1974.

- [28] Aaron Z Palmer, Zelda B Zabinsky, and Shan Liu. Optimal control of covid-19 infection rate with social costs. arXiv preprint arXiv:2007.13811, 2020.

- [29] Guodong Pang, Rishi Talreja, Ward Whitt, et al. Martingale proofs of many-server heavy-traffic limits for Markovian queues. Probability Surveys, 4:193–267, 2007.

- [30] Tokuzo Shiga and Hiroshi Tanaka. Central limit theorem for a system of Markovian particles with mean field interactions. Zeitschrift für Wahrscheinlichkeitstheorie und verwandte Gebiete, 69(3):439–459, 1985.

- [31] Ludwig Von Mises. Economic calculation in the socialist commonwealth. Lulu Press, Inc, 2016.

- [32] Wei Zhang, Carsten Hartmann, and Max von Kleist. Optimal control of Markov jump processes: Asymptotic analysis, algorithms and applications to the modelling of chemical reaction systems. arXiv preprint arXiv:1512.00216, 2015.