Generalized Autoregressive Moving Average Models with GARCH Errors

Abstract

One of the important and widely used classes of models for non-Gaussian time series is the generalized autoregressive model average models (GARMA), which specifies an ARMA structure for the conditional mean process of the underlying time series. However, in many applications one often encounters conditional heteroskedasticity. In this paper we propose a new class of models, referred to as GARMA-GARCH models, that jointly specify both the conditional mean and conditional variance processes of a general non-Gaussian time series. Under the general modeling framework, we propose three specific models, as examples, for proportional time series, nonnegative time series, and skewed and heavy-tailed financial time series. Maximum likelihood estimator (MLE) and quasi Gaussian MLE (GMLE) are used to estimate the parameters. Simulation studies and three applications are used to demonstrate the properties of the models and the estimation procedures.

Keywords Generalized ARMA model; GARMA-GARCH model; Non-negative time series; Proportional time series; Realized volatility; Stock returns

1 Introduction

The traditional autoregressive and moving average (ARMA) models for time series analysis assume the conditional mean of given the past information depends linearly on the past observations and past innovations. To capture empirical characteristics such as serial dependence between squared innovations, volatility clustering and other heteroskedasticity in many time series encountered in the real data, especially in economic and financial applications, additional assumptions on the conditional variance are often introduced and included in the model, resulting in models such as the generalized autoregressive conditional heteroskedasticity (GARCH) models proposed by Engle (1982) and Bollerslev (1986) and stochastic volatility (SV) models proposed by Taylor (1982, 1986). The resulting combined ARMA and GARCH processes are often referred to as the ARMA-GARCH models. In dealing with non-Gaussian time series exhibiting heavy tailed and asymmetric behaviors, the innovation (error) process in the ARMA-GARCH models is often assumed to follow certain non-Gaussian distributions, including Student- (Bollerslev, 1987), generalized error distribution (Nelson, 1991), skewed Student- (Lambert and Laurent, 2001), and others. These approaches are often referred to as the innovations-based approaches for dealing with non-Gaussian time series.

A different approach for modeling non-Gaussian time series is the data-based approach, in which one first assumes a non-Gaussian conditional distribution of given the past, then models the temporal evolution of the parameters of the distribution. Such an approach is often used to model time series of count, time series of positive random variables and proportional time series, including the autoregressive conditional duration models (Engle and Russell, 1998), multiplicative error models (Engle, 2002a; Engle and Gallo, 2006), Poisson and negative binomial models for discrete-valued or count data (Davis, Dunsmuir and Streett, 2003; Ferland, Latour and Oraichi, 2006; Davis and Wu, 2009; Fokianos, Rahbek and Tjøstheim, 2009; Fokianos and Fried, 2010; Qian, Li and Zhu, 2020), Beta autoregressive moving average (ARMA) models (Rocha and Cribari-Neto, 2009; Scher, Cribari-Neto, Pumi and Bayer, 2020), and many others. A general class of such models is the Generalized ARMA (GARMA) model of Benjamin, Rigby and Stasinopoulos (2003) and its martingalized version (M-GARMA) model of Zheng, Xiao and Chen (2015). Through a link function, GARMA and M-GARMA assumes an ARMA form for the conditional mean process.

Similar to the need of extending the approach of modeling only the conditional mean to jointly modeling the conditional mean and variance in the innovation-based approach mentioned above, there is also a need to extend the GARMA models to include the modeling of the conditional variance process, in order to address conditional heteroskedasticity often observed in applications. This is actually more important in the data-based approaches since here we directly model the conditional distribution. If the conditional distribution involves more than one parameter, then the conditional mean itself is often not sufficient to capture the time varying behavior of the conditional distribution. For example, if the distribution is parametrized by its mean and some other parameters, the GARMA model would need to require all the parameters except the mean to be fixed, and only the mean parameter to be time varying and carry the past information. Such an assumption limits the modeling flexibility for real applications.

In this paper we propose a data-based approach for modeling non-Gaussian time series by jointly modeling the conditional mean and variance processes, through a link function. It is an extension of the GARMA model, with an additional GARCH structure for the conditional variance process.

It is not straightforward to include a GARCH structure under the GARMA model framework of Benjamin, Rigby and Stasinopoulos (2003). The reason is that if the specified link function in the GARMA formation is not identity, the induced error sequence under the link function is not a martingale difference sequence (MDS) and thus its squared counterparts as a measure of the conditional variance are complicate and difficult to interpret. On the other hand, the Martingalized-GARMA (M-GARMA) model proposed by Zheng, Xiao and Chen (2015) provides a promising framework, allowing the error sequence being an MDS.

Based on the preceding discussions, this paper formally proposes the GARMA-GARCH model under the M-GARMA framework of Zheng, Xiao and Chen (2015) to capture the conditional heteroskedasticity of non-Gaussian time series. We also introduce three specific models under the general framework: a log-Gamma-GARMA-GARCH model for non-negative time series, a logit-Beta-GARMA-GARCH model for proportional time series, and a generalized hyperbolic skew Student- (GHSST) distribution based GARMA-GARCH model for financial time series. We then present the maximum likelihood estimator (MLE) and quasi Gaussian MLE (GMLE) for estimating the parameters in the GARMA-GARCH models.

The rest of this paper is organized as follows. Section 2 introduces the GARMA-GARCH model, together with the three specific models and their properties. In Section 3, we introduce the MLE and GMLE for GARMA-GARCH models. Second 4 presents some simulation studies to demonstrate the finite sample performance of the estimators. In Section 5, empirical applications are carried out for realized volatility, U.S. personal saving rate and stock returns by using the three specific models, respectively. The last section concludes.

2 The Model

2.1 GARMA-GARCH model

The GARMA-GARCH model relies on a given parametric family of distributions with parameters and , and a y-link function . Here both and can be vectors. Define the functions and , where follows the distribution . The GARMA-GARCH model assumes that the conditional distribution is

| (1) |

where is determined by through the conditional expectation and variance of , i.e.

| (2) | ||||

| (3) |

where , and . We assume that is a vector of time invariant parameters, and can be uniquely solved from (2) and (3), once is given. Note that in most cases, this would require that is a 2-dimensional vector.

We use to denote the set of all model parameters

Since (3) is regarding the conditional variance, we impose the natural requirement that is strictly positive, and () and () are nonnegative.

Adding on both sides of (2) leads to the following ARMA representation of .

| (4) |

The joint model (4) and (3) is in the standard ARMA-GARCH model form, for the transformed time series , except that the innovation process here is a martingale difference process, instead of an i.i.d sequence.

Similar to the GARCH model, the equation (3) can also be represented in an ARMA form. For this purpose we define , and add on both sides of (3), resulting in the following equivalent representation:

| (5) |

where denotes the maximum of and .

Some remarks on different issues of the model are in order:

Remark 1 (Relationship to the M-GARMA Model).

The GARMA-GARCH model is a direct extension of the M-GARMA model of Zheng, Xiao and Chen (2015), with the additional equation (3) for the conditional variance of . The M-GARMA model only allows a one dimensional time varying parameter in (1). The GARMA-GARCH model allows two parameters to be time varying and to depend on past information. It also closely mimics the standard ARMA-GARCH model widely used in applications.

Remark 2 (Relationship to the innovation-based ARMA-GARCH).

The innovation-based ARMA-GARCH model assumes the form (4) and (3) for the transformed series with the error term , where are independent, following a common distribution such as normal, Student’s , and skewed . In this case, the GARCH process is said to be strong, following definition of Francq and Zakoïan (2010) and Drost and Nijman (1993). For such models, the conditional distribution of given can be found through the inverse transformation of the transformed random variable . In certain non-Gaussian time series such as time series of counts, the data-based approach taken here is more natural and the model is easier to interpret. Under the GARMA-GARCH model, the “innovation” process is not an i.i.d. sequence, but a MDS, and the GARCH component is said to be semi-strong. The parallel between the two models allow us to obtain a quasi likelihood estimator for the GARMA-GARCH model by assuming that follows a ARMA-GARCH model with i.i.d. Gaussian innovations.

Remark 3 (Mean and variance link functions).

Define

| (6) | ||||

| (7) |

These functions link the conditional mean and variance of given to the underlying time varying parameter . Different to the M-GARMA model, the link function here is not necessarily a function of conditional mean of . If the y-link function is identity, the mean and variance link functions are indeed directly linked to the conditional mean and variance of . Otherwise, they differ greatly. The link functions of course depend on the form of parametrization of the conditional distribution in (1).

Remark 4 (Solving time-varying parameters).

It is important to be able to solve the time-varying parameters using (2) and (3), given past information. This is because they are needed to evaluate the likelihood function of the model and so to carry out the maximum likelihood estimation. That is, we need to solve based on given and using the link functions (6) and (7) as a system of equations, via exact or numerical methods. In practice, when there are more than one solution for the system, we can select the solution that maximizes the corresponding likelihood function value of the GARMA-GARCH model.

Remark 5 (The choice of the y-link function).

One of the key components of a good GARMA-GARCH model is a properly chosen y-link function , which specifies the explicit links between and . The y-link function is similar to the link function of the generalized linear models of McCullagh and Nelder (1989). It is a model assumption that is based on the problem at hand, and can be checked and sometimes justified with sensible model validation statistics and procedures.

Remark 6 (Dimension of the time-varying parameters).

In general, the dimension of the time-varying parameter is assumed to be two under the GARMA-GARCH model, as discussed earlier. If the dimension of is one, one may choose to use either the conditional mean relationship (2) or the conditional variance relationship (3), but not both. An alternative is to adopt a generalized moment method approach by solving the one dimensional with two moment equations. This is an interesting problem to be further investigated. When the dimension of is larger than 2, two equations with the mean and variance link functions are not enough to determine the time-varying parameters. In this case, we may extend the GARMA-GARCH model to include modeling assumptions of the higher moments of given .

Remark 7 (Extensions to multivariate non-Gaussian time series).

In this paper we study univariate time series through GARMA-GARCH model. The model can be easily extended to multivariate time series, with a multivariate y-link function , and a vector ARMA form in place of (2) and a multivariate GARCH form in place of (3). To avoid various ambiguities in multivariate ARMA, vector AR models can be used (Lütkepohl, 2005; Tsay, 2014). There are also many different multivariate GARCH models, including those in Archakov, Hansen and Lunde (2020); Engle (2002b); Engle and Kroner (1995). The dependencies among the components of (as a vector) and (as a covariance matrix) induce dependencies among the components of .

2.2 Some specific models

In this section we introduce three specific models under the general GARMA-GARCH model framework, with specific choices of the conditional distribution , and the y-link function . They are designed for certain types of non-Gaussian time series.

To simplify the model formula, define the following characteristic polynomials: , , , and . Let be the backward shift operator such that .

(1) Log-Gamma-GARMA-GARCH model: Suppose is a non-negative continuous random variable. Using Gamma distribution as the conditional distribution and log function as the y-link function, the log-Gamma-GARMA()-GARCH() model for a time series is given by

| (8) |

with , where and are the shape and rate parameters of Gamma distribution respectively, and are the conditional expectations of and respectively, and is the conditional variance of or . Moreover, the resulting conditional mean and variance link functions are expressed as

| (9) | ||||

| (10) |

where is the digamma function, and is the trigamma function.

In this model (8), we have no fixed parameter , and are the time-varying parameters of the distribution. Given the values of and , we can first obtain the unique root from (10) via the numerical methods or the bisection method, and then substituting it into the link function (9) to calculate .

Without the conditional variance process, Zheng, Xiao and Chen (2015) proposed the log-Gamma-M-GARMA model in which the conditional distribution is assumed to be with a time invariant parameter , the y-link function used is the log function, and the conditional mean process assumes an ARMA form. Comparing to the log-Gamma-GARMA-GARCH model, its shape parameter is time-invariant, and it does not have all the GARCH parameters in the conditional variance process.

Remark 8.

Here we point out a special feature of the log-Gamma-M-GARMA process. Because the y-link function is , the conditional distribution of is actually completely determined by the shape parameter , no matter what value takes. To see this, note that , and

On the other hand, according to (10), is uniquely determined by (note that is a strictly decreasing function on the positive real line). Consequently, we can give an equivalent definition of the log-Gamma-GARMA-GARCH model. We first define the process according to

| (11) |

Once is given, the process can be constructed by (4) using the pre-generated process. This equivalent definition reveals that can be defined without referring to the conditional mean equation (2), and is simply a linear ARMA process with innovations . This feature simplifies the investigation of various probabilistic properties of the process.

(2) Logit-Beta-GARMA-GARCH model: This model is based on the logit-Beta-M-GARMA model proposed by Zheng, Xiao and Chen (2015). Suppose a proportional time series lies in interval (0,1). Using the Beta distribution as the conditional distribution and the logit transformation as the y-link function, i.e., , the logit-Beta-GARMA()-GARCH() model is given by

| (12) |

with , where and are two positive parameters of the Beta distribution, is the conditional expectation of , and is the conditional variance of or . The resulting mean and variance functions are expressed as

| (13) | ||||

| (14) |

where and are the digamma and trigamma functions.

In this case, we also have no fixed parameter , but two time-varying parameters of the distribution, and . Although this system of equations (13) and (14) is nonlinear, the solution given the values of and is unique. Since both digamma and trigamma are strictly monotonic on , there must exist a unique solution such that (for a given ), and also a unique solution of to the nonlinear equation since is monotonically increasing and is monotonically decreasing. In practice, since the system of (13) and (14) is highly nonlinear, numerical methods are used to solve both and simultaneously.

Again, without the conditional variance process, Zheng, Xiao and Chen (2015) proposed the logit-Beta-M-GARMA model in which the conditional distribution is assumed to be with a time invariant parameter , the y-link function used is the logit function, and the conditional mean process assumes an ARMA form. Comparing to the logit-Beta-GARMA-GARCH model, it has one extra time-invariant parameter (with ), but does not have all the GARCH parameters in the conditional variance process.

(3) GHSST-GARMA-GARCH model: To model leptokurtic and skewed financial time series , we consider a generalized hyperbolic skew Student-t (GHSST) distribution proposed by Aas and Haff (2006). It is shown that the GHSST distribution can exhibit unequal thickness in both tails, contrary to other skewed extensions of the Student-, and that this offers more modeling flexibility. Using the identity y-link function, we propose the following GHSST-GARMA()-GARCH() model

| (15) |

where . The conditional density of follows the GHSST distribution

| (16) |

where and are the time varying location and scale parameters of the GHSST distribution, and and are the degrees of freedom and shape parameters. The function for denotes the modified Bessel function of the third kind and of order (Abramowitz and Stegun, 1972). The conditional density can be recognized as the density of a non-central (scaled) Student’s -distribution with degrees of freedom. In particular when , it becomes the standard Student’s -distribution.

In model (15), the corresponding conditional mean and variance functions are given by

| (17) | ||||

| (18) |

The variance is only finite when , as opposed to the symmetric Student’s -distribution which only requires . In this case, we can first solve the roots of the polynomial on the right hand side of (18) and select the unique positive real root as the value of , that is,

where . Then, the other time-varying parameter can be calculated as .

Under the model framework presented in this study, we can estimate all parameters in (15) using the maximum likelihood estimation procedure directly. We note that Deschamps (2012) proposed another ARMA-GARCH form by assuming as a mixture of normal and inverted Gamma random variables, the likelihood function cannot be expressed analytically and thus the MLE estimator is infeasible. In practice under the mixture representation, one has to use the Markov Chain Monte Carlo methods for the parameter estimation.

2.3 Stationarity and Ergodicity

To study the stationarity and ergodicity of the GARMA-GARCH model, we consider the state space representation of the model and apply the theory of Markov Chains on a general state space. The theoretical tools involved in our analysis are covered by the classical treatise in Meyn and Tweedie (2009), especially Chapter 15. We will not repeat the concepts and terminologies about the Markov Chains here, but refer the readers to the aforementioned book.

To represent the GARMA-GARCH model in the state space form, we start from (4) and (5). Without loss of generality, assume for (4), , and at least one of and is nonzero, and similarly for (5), , and at least one of and is nonzero. Define the square matrices

| (19) |

and set and . Let and . We first define a Markov Chain on , where and are - and -dimensional, respectively. Given and , we generate as

| (20) |

where the parameter is determined by

We then set , , and define

| (21) |

Clearly is a time-homogeneous Markov chain. It can be shown that , and the process defined in (20) satisfies the recursive relationship (1), (2) and (3).

In general, the stationarity and ergodicity of the Markov Chain can be implied by the geometric drift condition (see Chapter 15 of Meyn and Tweedie, 2009). Such conditions depend on the conditional distribution assumption and the y-link function used. As an illustration, we next show when this condition is fulfilled for the log-Gamma-GARMA-GARCH and logit-Beta-GARMA-GARCH models. Recall that , and is the matrix defined in (21). Let be the matrix whose first row is , and other elements are zero. Define the sequence of matrices recursively as , and for .

Theorem 1.

Theorem 2.

Note that in Theorem 2, the condition that the operator norm of is strictly less than one for some entails that for . The proofs of the theorems are in Appendix.

3 Parameter Estimation

Let be the fixed and unknown parameter vector containing all model parameters. We partition the parameter vector into three sub-vectors: includes all the parameters in the ARMA process (2), includes all the parameters in the GARCH process (3), and includes all time invariant parameters in the conditional distribution (1). Specifically, , where

We further set the initial values , , and , where .

Suppose the available data set is . We next introduce two approaches for parameter estimation. The first is based on the likelihood, and the second is based on quasi Gaussian likelihood with additional conditional likelihood estimation.

3.1 Maximum likelihood estimation

The log-likelihood function conditional on the initial values (, , , and ) is

| (22) |

where for can be solved by the system consisting of the link and variance functions given by (6) and (7).

Given a set of parameters , and can be recursively obtained for . Recursively solving the system consisting of mean and variance link functions yields for . By plugging into (22), we can evaluate the log-likelihood function . The maximum likelihood estimate is then obtained by maximizing (22), using nonlinear optimization procedures.

In practice, one can set the initial values to zero and to the unconditional variance to reduce the complexity, a common practice in time series estimation. The resulting estimate is the conditional maximum likelihood estimate. One can also use the quasi Gaussian MLE for the ARMA and GARCH parameters and its corresponding ML estimate for (see the next subsection) as the initial values for this procedure.

The theory of Hall and Heyde (1980) can be applied to study the asymptotic distribution of the MLE. However, for concrete GARMA-GARCH models, sufficient conditions that ensure the asymptotic normality are still under investigation. Regardless of the technical issues, we provide a reasonable formula for the asymptotic covariance matrix. Let

Let be the true parameter. Under regularity conditions, is an MDS with respect to . Define

Under regularity conditions, it holds that

For some GARMA-GARCH models presented in this study, for a given , the conditional information can be calculated explicitly. By substituting the estimate , we get an estimate of the Fisher information. In practice, the standard errors of the estimates can also be obtained by evaluating the Hessian matrix of the log-likelihood function (22) at the MLE. Our empirical experiences have shown that this estimator works very well.

3.2 Gaussian ML estimation

Just based on (2) and (3), one can use quasi Gaussian likelihood to estimate the ARMA and GARCH parameters quickly. This estimate will be referred to as quasi Gaussian maximum likelihood estimator (GMLE). Let . The GMLE for the GARMA-GARCH model is equivalent to a minimizer of

| (23) |

where and are defined by (2) and (3). This objective function can be evaluated relatively cheaply, and many algorithms are available for finding its minima.

The asymptotic properties such as consistency and asymptotic normality (CAN) of the GMLE can be obtained based on the existing studies. For example many studies such as Lumsdaine (1996), Berkes, Horváth, and Kokoszka (2003), Ling (2007) and Francq and Zakoïan (2004, 2010, 2012) have investigated the CAN of the GMLE when the GARCH process of in our model is strong with i.i.d. innovations. Lee and Hansen (1994) studied the CAN of the GMLE for strictly stationary semi-strong GARCH(1,1) model and Escanciano (2009) further proved the CAN of the GMLE for general GARCH() model under martingale assumptions.

The general CAN theory of the GARMA-GARCH model is very challenging to establish, which we leave to the future work. Here we only discuss how the result in Escanciano (2009) can be adapted to give the asymptotic normality of the GMLE for the two examples given in Section 2.2.

For the log-Gamma-GARMA-GARCH or the logit-Beta-GARMA-GARCH model, we assume the conditions of Theorem 1 or Theorem 2 hold, respectively. Assume in addition that (i) the parameter space of is compact and belongs to the interior of ; (ii) and have no common roots, and when ; (iii) and have no common roots, when , and , ; and (iv) for some . Under these regularity conditions, it holds that

| (24) |

where denotes the information matrix, which is defined as minus the expected Hessian, i.e.,

The GML estimation procedure does not provide an estimator for the invariant parameter . However, given the GML estimate , we can obtain the estimated ARMA residual and the estimated conditional variance . Set . Given , and with and , we can obtain by solving the system of equations and . We emphasize that depends on . Now define the log-likelihood function of given fixed as

The maximizer of can be treated as the pseudo-ML estimator of .

Remark 9 (Model identification and model checking).

Both AIC and BIC can be used for model/order selection. Standard time series analysis tools such as ACF, PACF and EACF (Tsay and Tiao, 1984; Chen et al., 2013) can be used to obtain the preliminary lag orders for the ARMA process. Empirical studies have shown that are often sufficient for the GARCH process in practice and can be used as the starting point of the model building process. For model checking, the portmanteau Q-statistic of the residuals and the squared standardized residuals can be used, as a standard exercise for time series model checking, especially for time series with potential conditional heteroskedasticity, along with other residual analysis tools.

4 Simulation Examples

In this section, we investigate finite sample performances of the preceding two estimators (named as GMLE and MLE) under the log-Gamma-GARMA-GARCH and logit-Beta-GARMA-GARCH models introduced in Section 2.2. We also present empirical evidence regarding the impact of model mis-specification when ignoring the GARCH process in the model. Without the GARCH part, the models become the log-Gamma-M-GARMA and logit-Beta-M-GARMA models in Zheng, Xiao and Chen (2015).

All estimates are obtained through a constraint optimization procedure that uses the MaxSQP algorithm, implementing a sequential quadratic programming technique, see Nocedal and Wright (1999). We also use the solver for systems of nonlinear equations (SolveNLE) in OxMetrics software (see Doornik, 2007) to recursively obtain the solution of .

4.1 Log-Gamma-GARMA(1,1)-GARCH(1,1) model

| Log-Gamma-M-GARMA | Log-Gamma-GARMA-GARCH | |||||

| Parameter | True | GMLE | MLE | GMLE | MLE | |

| 0.00 | 0.0006 (0.1189) | 0.0025 (0.0791) | 0.0052 (0.0052) | 0.0033 (0.0758) | ||

| 0.95 | 0.8551 (0.1741) | 0.8635 (0.1293) | 0.8642 (0.1272) | 0.8710 (0.1230) | ||

| 0.65 | 0.5768 (0.1941) | 0.5873 (0.1618) | 0.5850 (0.1640) | 0.5886 (0.1555) | ||

| 2.8333 (0.8293) | 2.8497 (0.8247) | – | – | |||

| 0.02 | – | – | 0.0882 (0.1044) | 0.0830 (0.1045) | ||

| 0.06 | – | – | 0.0712 (0.1002) | 0.0638 (0.0848) | ||

| 0.90 | – | – | 0.7227 (0.2927) | 0.7401 (0.2913) | ||

| 0.00 | 0.0007 (0.0150) | 0.0003 (0.0181) | 0.0011 (0.0144) | 0.0003 (0.0139) | ||

| 0.95 | 0.9369 (0.0238) | 0.9259 (0.0274) | 0.9374 (0.0245) | 0.9379 (0.0214) | ||

| 0.65 | 0.6396 (0.0538) | 0.6371 (0.0506) | 0.6395 (0.0503) | 0.6393 (0.0436) | ||

| 2.5598 (0.3815) | 2.5706 (0.3733) | – | – | |||

| 0.02 | – | – | 0.0417 (0.0606) | 0.0376 (0.0561) | ||

| 0.06 | – | – | 0.0655 (0.0357) | 0.0623 (0.0310) | ||

| 0.90 | – | – | 0.8458 (0.1538) | 0.8574 (0.1424) | ||

| 0.00 | 0.0003 (0.0060) | 0.0000 (0.0076) | 0.0003 (0.0056) | 0.0002 (0.0057) | ||

| 0.95 | 0.9467 (0.0111) | 0.9331 (0.0135) | 0.9468 (0.0105) | 0.9467 (0.0095) | ||

| 0.65 | 0.6473 (0.0255) | 0.6436 (0.0246) | 0.6471 (0.0105) | 0.6464 (0.0110) | ||

| 2.4904 (0.2099) | 2.4987 (0.2029) | – | – | |||

| 0.02 | – | – | 0.0228 (0.0103) | 0.0220 (0.0082) | ||

| 0.06 | – | – | 0.0613 (0.0169) | 0.0602 (0.0135) | ||

| 0.90 | – | – | 0.8923 (0.0328) | 0.8952 (0.0259) | ||

Note: For each cell, the statistics given are based on 500 simulated samples. The mean and root mean squared error (in parentheses) for each estimator are shown.

We consider a log-Gamma-GARMA-GARCH model with lag orders . Specifically,

with and . The specific true parameter values are assigned as , , , , , and . We consider different sample sizes , or . Each simulation is repeated for 500 times. The mean and standard errors of the estimates are presented in Table 1.

Several observations can be drawn from Table 1. First, under the true GARMA-GARCH model, both GMLE and MLE perform well, especially when the sample size is large. This result is consistent with the theoretical result of Lee and Hansen (1994) and Escanciano (2009) that the GMLE is consistent under relatively weak conditions. GMLE performs slightly worse than the MLE when sample size is large, with slightly larger biases and root mean squared errors (in parentheses) than that of the MLE. This is possibly due to the loss of efficiency when using GMLE. Nevertheless, the GMLE can serve as good starting values for ML estimation. Second, under the mis-specified log-Gamma-M-GARMA model, both GMLE and MLE produce relative accurate estimates for the ARMA parameters, with slightly larger variances than those under the true model. The parameter under log-Gamma-M-GARMA model is the extra time invariant shape parameter in the conditional Gamma distribution, as mentioned in Section 2.2.

4.2 Logit-Beta-GARMA(1,1)-GARCH(1,1) model

| Logit-Beta-M-GARMA | Logit-Beta-GARMA-GARCH | |||||

|---|---|---|---|---|---|---|

| Parameter | True | GMLE | MLE | GMLE | MLE | |

| 0.10 | 0.1790 (0.1466) | 0.1758 (0.1397) | 0.1531 (0.1080) | 0.1531 (0.1071) | ||

| 0.90 | 0.8203 (0.1473) | 0.8237 (0.1403) | 0.8459 (0.1090) | 0.8460 (0.1079) | ||

| 0.50 | 0.4363 (0.2216) | 0.4380 (0.2178) | 0.4601 (0.1572) | 0.4586 (0.1578) | ||

| 90.418 (42.408) | 90.476 (42.386) | – | – | |||

| 0.01 | – | – | 0.0135 (0.0092) | 0.0136 (0.0092) | ||

| 0.45 | – | – | 0.3940 (0.1796) | 0.3940 (0.1791) | ||

| 0.45 | – | – | 0.3999 (0.2311) | 0.3964 (0.2306) | ||

| 0.10 | 0.1154 (0.0497) | 0.1142 (0.0524) | 0.1085 (0.0261) | 0.1084 (0.0261) | ||

| 0.90 | 0.8844 (0.0498) | 0.8856 (0.0524) | 0.8914 (0.0262) | 0.8915 (0.0262) | ||

| 0.50 | 0.4922 (0.1042) | 0.4906 (0.4906) | 0.4908 (0.0545) | 0.4906 (0.0542) | ||

| 69.287 (19.761) | 69.375 (19.658) | – | – | |||

| 0.01 | – | – | 0.0106 (0.0032) | 0.0106 (0.0033) | ||

| 0.45 | – | – | 0.4330 (0.0798) | 0.4341 (0.0801) | ||

| 0.45 | – | – | 0.4450 (0.0836) | 0.4440 (0.0839) | ||

| 0.10 | 0.1068 (0.0280) | 0.1047 (0.0240) | 0.1017 (0.0111) | 0.1017 (0.0110) | ||

| 0.90 | 0.8932 (0.0281) | 0.8953 (0.0238) | 0.8983 (0.0109) | 0.8984 (0.0108) | ||

| 0.50 | 0.4938 (0.0648) | 0.4948 (0.0563) | 0.4983 (0.0254) | 0.4981 (0.0251) | ||

| 64.576 (11.430) | 64.612 (11.441) | – | – | |||

| 0.01 | – | – | 0.0101 (0.0014) | 0.0101 (0.0014) | ||

| 0.45 | – | – | 0.4478 (0.0434) | 0.4480 (0.4480) | ||

| 0.45 | – | – | 0.4477 (0.0388) | 0.4476 (0.0387) | ||

Note: For each cell, the statistics given are based on 500 simulated samples. The mean and root mean squared error (in parentheses) for each estimator are shown.

In this example, we simulate the time series of proportions from the following logit-Beta-GARMA(1,1)-GARCH(1,1) model

where and . Again we consider three sample sizes , and . The true parameter values are set as , , , , , and . We carry out 500 repeated experiments for each simulation.

Table 2 reports the empirical performance of the two estimators. It is seen that, under the true model, the GMLE and MLE perform very similarly in both small and large samples. This implies that the GMLE can be used as a surrogate of the MLE for this model. On the other hand, when the model is mis-specified as the logit-Beta-M-GARMA model, the corresponding GMLE and MLE of the ARMA parameters have larger biases and root mean squared errors (in parentheses) than the GMLE and MLE under the true logit-Beta-GARMA-GARCH model. The parameter under the logit-Beta-M-GARMA model is the extra time invariant parameter in the conditional Beta distribution.

5 Applications

5.1 High-frequency realized volatility

| Log-Gamma-M-GARMA | Log-Gamma-GARMA-GARCH | ||||

| Parameter | GMLE | MLE | GMLE | MLE | |

| 0.0582 (0.0198) | 0.0609 (0.0221) | 0.0623 (0.0179) | 0.0816 (0.0228) | ||

| 0.9552 (0.0115) | 0.9532 (0.0120) | 0.9533 (0.0108) | 0.9422 (0.0126) | ||

| 0.4067 (0.0386) | 0.3517 (0.0371) | 0.4315 (0.0394) | 0.3829 (0.0424) | ||

| 2.4924 (0.1013) | 2.4992 (0.1126) | – | – | ||

| – | – | 0.0433 (0.0228) | 0.0534 (0.0237) | ||

| – | – | 0.0583 (0.0224) | 0.1093 (0.0362) | ||

| – | – | 0.8311 (0.0718) | 0.8053 (0.0651) | ||

| Loglik | 258.79 | 260.11 | 191.63 | 272.59 | |

| AIC | 0.5303 | 0.5330 | 0.3863 | 0.5548 | |

| BIC | 0.5100 | 0.5127 | 0.3559 | 0.5244 | |

| RSS | 3034.3 | 3026.4 | 3029.5 | 2919.7 | |

| JB-test | 30.58∗∗ | 26.31∗∗ | 34.78∗∗ | 30.00∗∗ | |

| (1) | 0.7653 | 0.3027 | 1.1873 | 0.0007 | |

| (5) | 4.6380 | 6.2492 | 6.7898 | 4.9045 | |

| (22) | 28.301 | 29.504 | 26.229 | 28.331 | |

| (1) | 4.148∗∗ | 2.8142 | 0.2282 | 0.2198 | |

| (5) | 17.84∗∗ | 14.359∗ | 2.9546 | 2.9060 | |

| (22) | 52.18∗∗ | 50.35∗∗ | 9.5137 | 13.797 | |

Note: “” and “” indicate that the test statistic is significant at 1% and 5% levels, respectively. The standard deviation errors of parameter estimates are reported in parentheses.

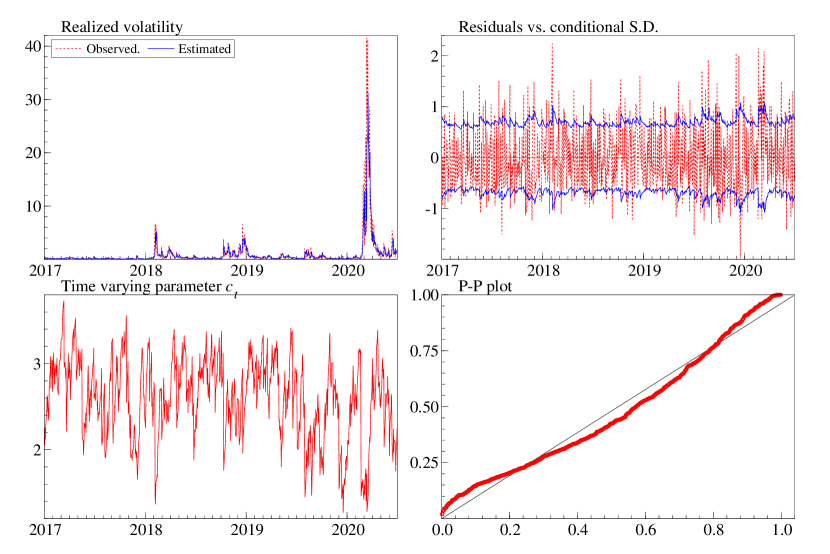

In this application, we employ the proposed log-Gamma-GARMA-GARCH model (8) to capture the time-varying volatility phenomenon of the realized volatility. Realized volatility has been extensively modeled and studied in financial econometrics, see for example Barndorff-Nielsen and Shephard (2002), Hansen and Lunde (2005), Takahashi, Omori and Watanabe (2009), and Zheng and Song (2014). In particular, a recent study related to this paper by Corsi, Mittnik, Pigorsch and Pigrosch (2008) showed that allowing for time-varying volatility of the realized volatility and logarithmic realized variance substantially improves model fitting as well as predictive performance. We use the 5-min daily realized volatility (RV5m, computed by the sum of squared 5-minute log returns) of Standard & Poor 500 Index (SP500), taken from the “Oxford-Man Institute’s realized library” (version 0.3, available at the website: http://realized.oxford-man.ox.ac.uk). The data is sampled from January 3, 2017 to June 30, 2020 with observations. Based on the extended autocorrelation function (Tsay and Tiao, 1984; Chen et al., 2013), the order is selected as and for the log-Gamma-M-GARMA process. We then set for the log-Gamma-GARMA-GARCH model.

Table 3 shows the estimation performance of different estimators, including the GMLE and MLE of the log-Gamma-M-GARMA and log-Gamma-GARMA-GARCH models, respectively. Again, the shape parameter is the fixed extra parameter for the log-Gamma-M-GARMA model. In the top panel of Table 1 we report the parameter estimates and their standard errors. In the bottom panel we report a few statistics for model validation. The first three rows provide the maximum log likelihood, AIC and BIC, respectively. In the fourth row, RSS stands for root residual sum of squares defined by . The fifth row reports the test statistic of Jarque and Bera (1987) for normality. The quantity denotes the Box-Ljung test statistic with lags (Ljung and Box, 1978). The statistic is the portmanteau test statistic based on squared standardized residuals , which are defined as , where . This statistic is used to test whether the conditional heteroskedasticity has been accommodated by the model (McLeod and Li, 1983).

The parameter estimates from the GMLE and MLE seem to be close under both models, indicating that the GMLE is a good estimator. However, comparing the left and right panels of Table 3, we see that including the GARCH process is indeed appropriate since the coefficients and are significant, and the resulting AIC and BIC values are smaller.

Based on the statistics and for various , it can be seen that the log-Gamma-GARMA-GARCH model is more suitable for the data than the log-Gamma-M-GARMA model since it captures the conditional heteroskedasticity in the process adequately, while the latter one fails to do so. Moreover, the values of log-likelihood function and RSS show that including the GARCH process improves the in-sample fitting performance greatly. In addition, the normality test shows that the residuals from the GMLE do not follow a normal distribution, indicating that the Gaussian assumption for the innovations is not suitable here.

Figure 1 shows some features of the estimated log-Gamma-GARMA(1,1)-GARCH(1,1) model. The upper-left panel is a plot of the original time series and the fitted values , showing a good fit to the data. The upper-right panel compares the estimated residuals with conditional standard deviation , further showing a good description of the conditional heteroskedasticity in the process. The lower left panel presents the estimated time-varying parameter , indicating that this shape parameter varies between 1 and 4, mostly around 2 and 3. We also construct a P-P plot to check the conditional distribution assumption of the model. Specifically, if the distribution assumption is valid, then should follow the uniform distribution, where is the cumulative distribution function. The lower right panel plots the quantiles of versus the quantiles of the uniform distribution. It suggests that the conditional Gamma assumption is reasonable.

5.2 U.S. personal saving rate

| Logit-Beta-M-GARMA | Logit-Beta-GARMA-GARCH | ||||

| Parameter | GMLE | MLE | GMLE | MLE | |

| 0.0140 (0.0119) | 0.0123 (0.0116) | 0.0049 (0.0078) | 0.0047 (0.0079) | ||

| 0.6148 (0.0521) | 0.6275 (0.0527) | 0.6027 (0.0590) | 0.5979 (0.0586) | ||

| 0.0775 (0.0610) | 0.0721 (0.0597) | 0.1956 (0.0705) | 0.2019 (0.0718) | ||

| 0.0191 (0.0611) | 0.0260 (0.0607) | 0.0031 (0.0601) | 0.0054 (0.0612) | ||

| 0.1362 (0.0610) | 0.1432 (0.0607) | 0.1163 (0.0484) | 0.1135 (0.0488) | ||

| 0.1460 (0.0521) | 0.1425 (0.0458) | 0.0567 (0.0381) | 0.0547 (0.0379) | ||

| 121.56 (10.486) | 121.59 (5.0038) | – | – | ||

| – | – | 0.0063 (0.0012) | 0.0065 (0.0013) | ||

| – | – | 0.6964 (0.0777) | 0.7058 (0.0767) | ||

| – | – | 0.2495 (0.0639) | 0.2397 (0.0623) | ||

| Loglik | 616.34 | 616.39 | 689.64 | 689.76 | |

| AIC | 3.3852 | 3.3855 | 3.7813 | 3.7820 | |

| BIC | 3.3097 | 3.3099 | 3.6842 | 3.6848 | |

| RSS | 0.6798 | 0.6796 | 0.6962 | 0.6977 | |

| JB-test | 534.27∗∗ | 550.41∗∗ | 563.58∗∗ | 556.53∗∗ | |

| (1) | 3.3e-6 | 0.0542 | 3.2231 | 3.4302 | |

| (3) | 1.6662 | 1.6532 | 7.6838 | 7.9635 | |

| (12) | 9.7379 | 9.8820 | 19.555 | 19.805 | |

| (1) | 41.224∗∗ | 40.405∗∗ | 0.0344 | 0.0454 | |

| (3) | 44.417∗∗ | 43.264∗∗ | 2.8419 | 3.1277 | |

| (12) | 46.474∗∗ | 45.255∗∗ | 15.216 | 17.064 | |

Note: “” and “” indicate that the test statistic is significant at 1% and 5% levels, respectively. The standard deviation errors of parameter estimates are reported in parentheses.

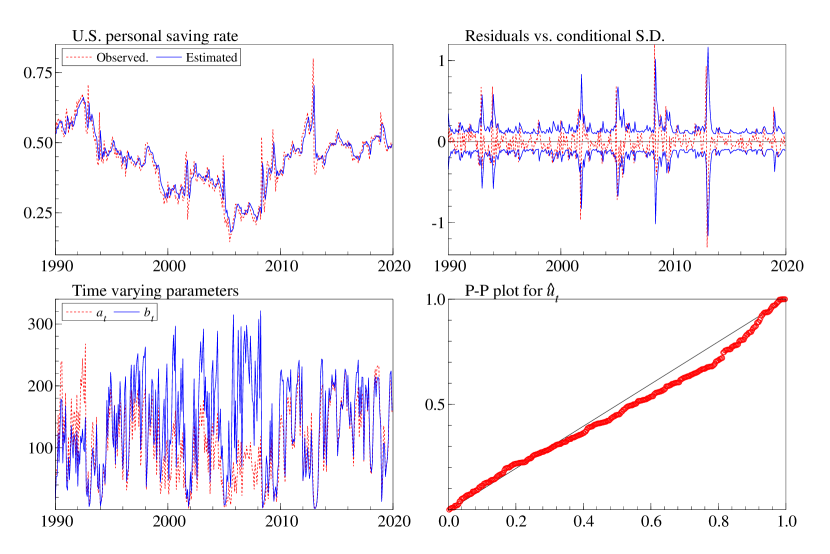

In this example we study the monthly U.S. personal saving rate from January 1990 to December 2019 with observations, shown in the upper left panel of Figure 2. This seasonal adjusted monthly series is retrieved from FRED, the Federal Reserve Bank of St. Louis (https://fred.stlouisfed.org/series/PSAVERT). We assume that the saving rate is in the range , and hence multiply the series by . The unit-root test with Phillips-Perron test statistic indicates that the series is stationary. Using BIC and standard ARMA modeling, the order of the ARMA process is determined as and . We then use , and for the logit-Beta-GARMA-GARCH model, which can be represented as

where . We then estimate the logit-Beta-M-GARMA(5,0) model and logit-Beta-GARMA(5,0)-GARCH(1,1) model using different estimators.

Table 4 reports the estimation results and some summary statistics. Again, the log-Gamma-M-GARMA model has an extra time invariant parameter . From the parameter estimates shown in the upper panel, we can see that the estimated AR coefficients are significantly different under the two models. In particular, the coefficient is statistically significant under the logit-Beta-M-GARMA model, but insignificant under the logit-Beta-GARMA-GARCH model. Moreover, the GARCH coefficients and are strongly significant, indicating that adding the GARCH process to the logit-Beta-M-GARMA model is reasonable.

In the lower-left panel of Table 4, the significant statistics show that the squared standardized residuals of the logit-Beta-M-GARMA model, , have strong autocorrelations. However, under the logit-Beta-GARMA-GARCH model, the portmanteau test results in the lower-right panel show no significant autocorrelations in the squared standardized residuals , indicating the advantage of including the GARCH type conditional variance process in the model.

Figure 2 depicts some features of the estimated logit-Beta-GARMA(5,0)-GARCH(1,1) model using the MLE. The estimated conditional mean is shown together with the observed series in the upper left panel of the figure. The conditional standard deviation (upper right panel) are shown in the upper right panel along with the estimated residuals , showing reasonable coverage. The lower left panel shows the estimated time-varying parameters and , indicating strong time varying behavior of the two parameters. The lower right panel shows the P-P plot similar to that in Figure 1, indicating that the logit-Beta-GARMA-GARCH model is reasonable for this time series data.

5.3 Stock returns

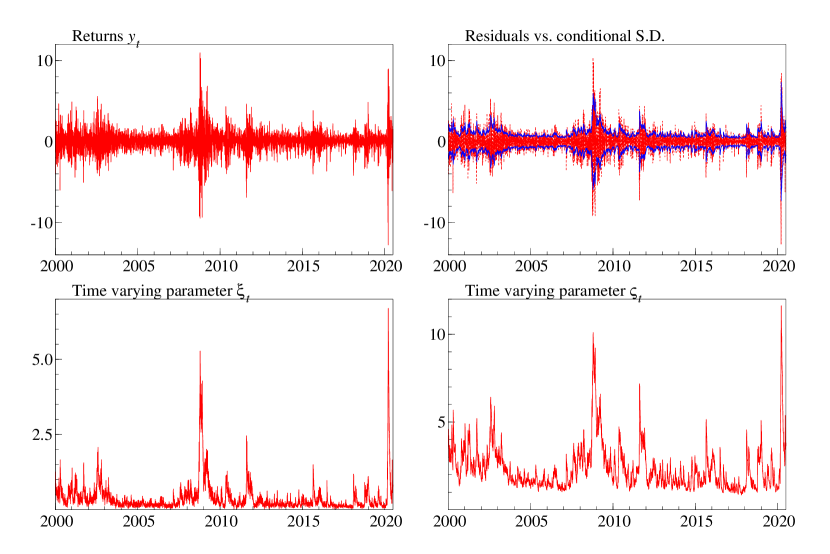

In this example, the proposed GHSST-GARMA-GARCH model in Section 2.3 is employed to investigate the skewness, fat-tail and volatility in stock returns. We use the daily log returns of Standard & Poor 500 Index (SP500) from January 3, 2000 to June 30, 2020 with observations, obtained from Yahoo Finance (https://finance.yahoo.com/). The upper-left panel of Figure 3 shows the time series.

| Parameter | Normal | Student- | GHSST |

|---|---|---|---|

| 0.0628 (0.0110) | 0.0764 (0.0102) | 0.0636 (0.0104) | |

| 0.0602 (0.0151) | 0.0632 (0.0140) | 0.0729 (0.0141) | |

| 0.0203 (0.0029) | 0.0088 (0.0019) | 0.0121 (0.0025) | |

| 0.1275 (0.0100) | 0.0807 (0.0078) | 0.1196 (0.0102) | |

| 0.8627 (0.0099) | 0.8771 (0.0105) | 0.8773 (0.0103) | |

| – | 5.9138 (0.5056) | 6.9631 (0.6246) | |

| – | – | 0.2006 (0.0502) | |

| Loglik | 7089.7 | 6969.3 | 6951.1 |

| AIC | 2.7515 | 2.7052 | 2.6985 |

| BIC | 2.7611 | 2.7145 | 2.7107 |

| (1) | 0.5559 | 0.8591 | 2.3289 |

| (5) | 8.0251 | 8.4076 | 10.189 |

| (22) | 32.868 | 33.618 | 30.475 |

| (1) | 1.1042 | 0.6035 | 0.3015 |

| (5) | 5.1283 | 3.8969 | 4.4023 |

| (22) | 21.172 | 17.881 | 23.367 |

Note: “” and “” indicate that the test statistic is significant at 1% and 5% levels, respectively. The standard deviation errors of parameter estimates are reported in parentheses.

We consider a GHSST-GAR(1)-GARCH(1,1) model specified as follows:

We also estimate the AR(1)-GARCH(1,1) models with normal and Student- distributions for comparison, which can be seen as special cases of the GHSST distribution.

Table 5 reports the estimation results based on different models. First, according to the the portmanteau tests in the lower panel, the residuals and squared standardized residuals have no significant autocorrelations for all three models, indicating that all the models can explain the conditional heteroskedasticity in the process. Second, the parameter estimates and for GHSST-GAR(1)-GARCH(1,1) model in the upper panel are significant, showing that the log returns are indeed leptokurtic and left skewed. We also see the advantage of the GHSST model over the normal and Student- settings, with its larger log-likelihood value.

Figure 3 plots the residuals along with conditional standard deviation , (the upper right panel) and the two time varying parameters and in the lower left and right panels, respectively. The figures show that the GHSST-GAR(1)-GARCH(1,1) captures the salient features of the observed time series.

6 Concluding remarks

The GARMA model is a useful class of data-based models for analyzing non-Gaussian time series. Since it only models the conditional mean process though an ARMA formation, it lacks the ability to address conditional heteroskedasticity often encountered in applications. In this paper we extend the GARMA model to GARMA-GARCH model with an additional model assumption on the conditional variance process, under a GARCH formation. In addition, three special GARMA-GARCH models are proposed for non-negative time series, proportional time series, and skewed and heavy tailed financial time series. Furthermore, maximum likelihood and quasi Gaussian likelihood estimation procedures are introduced, and their finite sample performances are illustrated. We find that the GMLE performs very well and the corresponding parameter estimates can be used as starting values of the MLE procedure. Three real data examples are used to demonstrate the properties of the proposed models.

There are several directions to extend the model. It is possible to introduce additional model assumptions on the higher moments of the conditional distribution so to capture additional time varying features of the conditional distribution. Modeling additional higher moments can be fruitful even when the conditional distribution is specified with a small number of parameters, since a generalized moment method type of procedure can be used to enhance the parameter estimation. Another direction is to extend the model to analyzing multivariate non-Gaussian time series, a topic less studied. The GARMA-GARCH framework conveniently introduces dependencies among the component time series though dependencies among the conditional mean and variance processes under a multivariate version of the ARMA and GARCH formations.

Acknowledgement

Zheng acknowledges financial supports from the National Science Foundation of China (No. 71973110, 71371160) and the Fundamental Research Fund for the Central Universities (No. 20720191038).

References

- Aas and Haff (2006) Aas, K., Haff, I. H., (2006), “The generalized hyperbolic skew Student’s t-distribution,” Journal of Financial Econometrics, 4, 275-309.

- Abramowitz and Stegun (1972) Abramowitz, M., Stegun, I. A., (1972), Handbook of Mathematical Function, New York: Dover.

- Archakov, Hansen and Lunde (2020) Archakov, I., Hansen, P. R., Lunde, A., (2020), ”A multivariate realized GARCH model,” Papers 2012.02708, arXiv.org.

- Barndorff-Nielsen and Shephard (2002) Barndorff-Nielsen, O. E., Shephard, N., (2002), “Econometric analysis of realized volatility and its use in estimating stochastic volatility models,” Journal of the Royal Statistical Society, Series B, 64, 253-280.

- Benjamin, Rigby and Stasinopoulos (2003) Benjamin, M. A., Rigby, R. A., Stasinopoulos, D. M., (2003), “Generalized autoregressive moving average models,” Journal of the American Statistical Association, 98, 214-223.

- Berkes, Horváth, and Kokoszka (2003) Berkes, I., Horváth, L., Kokoszka, P., (2003) GARCH processes: Structure and estimation. Bernoulli, 9, 201-227.

- Bollerslev (1986) Bollerslev, T., (1986), “Generalized autoregressive conditional heteroskedasticity,” Journal of Econometrics, 31, 307-327.

- Bollerslev (1987) Bollerslev, T., (1987), “A conditionally heteroskedastic time series model for speculative prices and rates of return,” Review of Economics and Statistics, 69, 542-547.

- Chan (1993) Chan, S. P. (1993) “A statistical study of log-gamma distribution”. PhD Thesis, McMaster University.

- Chen et al. (2013) Chen, S., Min, W., Chen, R., 2013. “Model identification for time series with dependent innovations”. Statistica Sinica 23, 873-899.

- Corsi, Mittnik, Pigorsch and Pigrosch (2008) Corsi, F., Mittnik, S., Pigorsch, C., and Pigrosch, U. (2008), “The Volatility of Realized Volatility,” Econometric Reviews, 27, 46-78.

- Davis, Dunsmuir and Streett (2003) Davis, R. A., Dunsmuir, W. T. M., Streett, S. B. (2003), “Observation-driven models for Poisson counts,” Biometrika, 90(4), 777-790.

- Davis and Wu (2009) Davis, R., Wu, R., (2009), “A negative binomial model for time series of counts,” Biometrika, 96, 735-749.

- Deschamps (2012) Deschamps, P. J., (2012), “Bayesian estimation of generalized hyperbolic skewed student GARCH models,” Computational Statistics & Data Analysis, 56(11), 3035-3054.

- Doornik (2007) Doornik, J., (2007), Ox: An Object-Oriented Matrix Programming Language, International Thomson Business Press.

- Drost and Nijman (1993) Drost, F. C., Nijman, T. E., (1993), “Temporal aggregation of GARCH processes,” Econometrica, 61(4), 909-27.

- Engle (1982) Engle, R. F., (1982), “Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation,” Econometrica, 50, 987-1007.

- Engle (2002a) Engle, R. F., (2002a), “New frontiers for ARCH models,” Journal of Applied Econometrics, 17, 425-446.

- Engle (2002b) Engle, R. F., (2002b), ”Dynamic conditional correlation: A simple class of multivariate generalized autoregressive conditional heteroskedasticity models,” Journal of Business and Economic Statistics 20, 339–350.

- Engle and Gallo (2006) Engle, R. F., Gallo, G. M., (2006), “A multiple indicators model for volatility using intra-daily data,” Journal of Econometrics, 131, 3-27.

- Engle and Kroner (1995) Engle, R. F., Kroner, K. F., (1995), ”Multivariate simultaneous generalized ARCH,” Econometric Theory 11, 122-150.

- Engle and Russell (1998) Engle, R. F., Russell, J. R., (1998), “Autoregressive conditional duration: a new model for irregularly spaced transaction data,” Econometrica, 66, 1127-1162.

- Escanciano (2009) Escanciano, J. C., (2009), “Quasi-maximum likelihood estimation of semi-strong GARCH models,” Econometric Theory, 25, 561-570.

- Ferland, Latour and Oraichi (2006) Ferland, R., Latour, A., Oraichi, D., (2006), “Integer-valued GARCH process,” Journal of Time Series Analysis, 27(6), 923-942.

- Fokianos and Fried (2010) Fokianos, K., Fried, R., (2010), “Intereventions in INGARCH processess,” Journal of Time Series Analysis, 31, 210-225.

- Fokianos, Rahbek and Tjøstheim (2009) Fokianos, K., Rahbek, A., Tjøstheim, D., (2009), “Poisson autoregression,” Journal of the American Statistical Association, 104, 1430-1439.

- Francq and Zakoïan (2004) Francq, C., Zakoïan, J.-M., (2004), “Maximum likelihood estimation of pure GARCH and ARMA-GARCH processes,” Bernoulli, 10(4), 605-637.

- Francq and Zakoïan (2010) Francq, C., Zakoïan, J.-M., (2010), GARCH Models: Structure, Statistical Inference and Financial Applications. John Wiley & Sons Ltd.

- Francq and Zakoïan (2012) Francq, C., Zakoïan, J.-M., (2012), “Strict stationarity testing and estimation of explosive and stationary generalized autoregressive conditional heteroscedasticity models,” Econometrica, 80(2), 821-861.

- Hall and Heyde (1980) Hall, P, Heyde, C. C., (1980), Martingale limit theory and its application, Academic Press Inc., New York.

- Hansen and Lunde (2005) Hansen, P. R., Lunde, A., (2005), “A realized variance for the whole day based on intermittent high-frequency data,” Journal of Financial Econometrics, 3, 525-554.

- Jarque and Bera (1987) Jarque, C. M., Bera, A. K., (1987), “A test for normality of observations and regression residuals,” International Statistical Review, 55, 163-172.

- Lambert and Laurent (2001) Lambert, P., Laurent, S., (2001), “Modeling financial time series using GARCH-type models and a skewed student density,” Mimeo, Université de Liège.

- Lee and Hansen (1994) Lee, S.-W., Hansen, B. E., (1994), “Asymptotic theory for the GARCH(1,1) quasi-maximum likelihood estimator,” Econometric Theory, 10, 29-52.

- Ling (2007) Ling, S., (2007), “Self-weighted and local quasi-maximum likelihood estimators for ARMA-GARCH/IGARCH models,” Journal of Econometrics, 140, 849-873.

- Ljung and Box (1978) Ljung, G. M., Box, G. E. P., (1978), “On a measure of lack of fit in time series models,” Biometrika, 65, 297-303.

- Lumsdaine (1996) Lumsdaine, R.L., (1996), “Consistency and asymptotic normality of the quasi-maximum likelihood estimator in IGARCH(1,1) and covariance stationary GARCH(1,1) models,” Econometrica, 64, 575-596.

- Lütkepohl (2005) Lütkepohl, H., 2005, New Introduction to Multiple Time Series Analysis. Springer, Berlin.

- Nocedal and Wright (1999) Nocedal, J., Wright, S., (1999), Numerical Optimization. Springer-Verlag, New York.

- McCullagh and Nelder (1989) McCullagh, P., Nelder, J. A., (1989), Generalized Linear Models, 2ed, Chapman & Hall/CRC, London.

- McLeod and Li (1983) McLeod, A. I., Li, W. K., (1983), “Diagnostic checking ARMA time series models using squared residual autocorrelations,” Journal of Time Series Analysis, 4, 269-273.

- Meyn and Tweedie (2009) Meyn, S., Tweedie, R.L., 2009. Markov chains and stochastic stability, 2ed. Cambridge University Press, Cambridge.

- Nelson (1991) Nelson, D. B., (1991), “Conditional heteroskedasticity in asset returns: a new approach,” Econometrica, 59, 347-370.

- Qian, Li and Zhu (2020) Qian, L., Li, Q. and Zhu, F., (2020), “Modelling heavy-tailedness in count time series,” Applied Mathematical Modelling, 82, 766-784.

- Rocha and Cribari-Neto (2009) Rocha, A. V., Cribari-Neto, F., (2009), “Beta autoregressive moving average models,” Test, 18, 529-545.

- Scher, Cribari-Neto, Pumi and Bayer (2020) Scher, V. T., Cribari-Neto, F., Pumi, G., Bayer, F. M., (2020), “Goodness-of-fit tests for ARMA hydrological time series modeling,” Environmetrics, 31, 1-19.

- Takahashi, Omori and Watanabe (2009) Takahashi, M., Omori, Y., Watanabe, T., (2009), “Estimating stochastic volatility models using daily returns and realized volatility simultaneously,” Computational Statistics & Data Analysis, 53, 2404-2426.

- Taylor (1982) Taylor, S. J., (1982), “Financial returns modeled by the product of two stochastic processes, a study of daily sugar prices 1961-79,” In Time Series Analysis: Theory and Practice 1, Anderson OD (Ed.). North-Holland: Amsterdam; 203-226.

- Taylor (1986) Taylor, S. J., (1986), Modeling Financial Time Series, John Wiley: New York.

- Tsay (2014) Tsay R.S., 2014, Multivariate Time Series Analysis with R and Financial Applications. John Wiley, Hoboken, NJ.

- Tsay and Tiao (1984) Tsay, R.S., Tiao, G.C., 1984. Consistent estimates of autoregressive parameters and extended sample autocorrelation function for stationary and nonstationary ARMA models. Journal of the American Statistical Association 79, 84-96.

- Zheng and Song (2014) Zheng, T., Song, T., (2014), “A realized stochastic volatility model with Box-Cox transformation,” Journal of Business & Economic Statistics, 32, 593-605.

- Zheng, Xiao and Chen (2015) Zheng, T., Xiao, H., Chen, R., (2015), “Generalized ARMA models with martingalized difference errors,” Journal of Econometrics, 189, 492-506.

A Appendix

We give the proofs of Theorem 1 and 2 in the appendix. The proof relies on the geometric drift condition discussed in Chapter 15 of Meyn and Tweedie (2009). Lemma 1 of Zheng, Xiao and Chen (2015) is a convenient wrap-up of the tool that we need, so we repeat it here.

Let be a Markov chain on the state space , equipped with some -field . Let be the transition probability kernel. The geometric drift condition requires that there exists an extended-valued function , a measurable set , and constants , such that

| (25) |

Lemma 1.

Suppose is a -irreducible and aperiodic Markov chain. If for some , the skeleton satisfies the drift condition (25) for a petite set and a function which is everywhere finite. Then is geometrically ergodic, and , where is the unique invariant probability measure.

Proof of Theorem 1.

According to Remark 8, we can embed the process into the following Markov chain . Given , we generate as , where the parameter is determined by . We then set , , and define . It holds that

According to §2.2 of Chan (1993),

where is the order- polygamma function defined as the -th derivative of the function . The polygamma function has the following two properties

| (26) |

It follows that for each , there exists a such that

| (27) |

and

Next, by taking a double expectation

Applying (27) again,

It follows that

where is the -th entry of .

Following the same argument recursively, we have for any positive integer ,

where is the -th entry of for , and . Choose , such that the operator norm of is less than for some . Choosing such that , we have

Since the log-Gamma distribution is absolutely continuous on , from here it is easy to verify that for the skeleton , the drift condition (25) is met with for , and other conditions of Lemma 1 are also fulfilled. Therefore, the chain is geometrically ergodic, and , where is the unique invariant probability measure. Because , it follows that .

Finally, once the strictly stationary process has been generated, the condition for guarantee that the process generated according to (4) admits a strictly stationary solution such that . ∎

Proof of Theorem 2.

For the logit-Beta-GARMA-GARCH model, the process cannot be generated by itself, and has to be generated together with . Therefore, we need to consider the Markov chain defined in (21). For notational simplicity, denote . Using the relationship between the Beta and Gamma distribution, it can be shown that

Suppose for some, the operator norms of both and are less than with some . Let be the -th entry of , and be the -th entry of for , and set . Note that for each . By (26), for each , there exists a such that

| (28) |

It follows that (using the preceding inequality with )

Since

and

applying (28) again with we have

Similar to the proof of Theorem 1, applying (28) recursively, we have

Choosing such that , it holds that

The rest of the proof follows the same argument of Theorem 1, so we skip the details. The proof is complete. ∎