Inflation - who cares?

Monetary Policy in Times of Low Attention

Link to most recent version )

Abstract

I propose an approach to quantify attention to inflation in the data and show that the decrease in the volatility and persistence of U.S. inflation after the Great Inflation period was accompanied by a decline in the public’s attention to inflation. This decline in attention has important implications (positive and normative) for monetary policy as it renders managing inflation expectations more difficult and

can lead to inflation-attention traps: prolonged periods of a binding lower bound and low inflation due to slowly-adjusting inflation expectations. As attention declines the optimal policy response is to increase the inflation target.

Accounting for the lower bound fundamentally changes the normative implications of declining attention. While lower attention raises welfare absent the lower-bound constraint, it decreases welfare when accounting for the lower bound.

JEL Codes: E31, E52, E58, E71

Keywords: Monetary Policy, Limited Attention, Inflation Expectations, Inflation Target, Effective Lower Bound

1 Introduction

Managing inflation expectations is an important instrument for monetary policy. It offers a powerful substitute to conventional tools if the nominal interest rate is constrained by the lower bound. By making promises about the future conduct of its policy, the monetary authority can shape inflation expectations, and thus, steer the real interest rate even when the nominal rate is constrained. At least this is how it works in theory.111For optimal monetary policy under full-information rational expectations, see e.g., Clarida et al. (1999), Woodford (2003) or Galí (2015). See Eggertsson and Woodford (2003), Adam and Billi (2006) or Coibion et al. (2012) for early analyses including the lower bound on nominal interest rates. But while traditional analyses assume that agents are perfectly informed and have rational expectations, recent empirical evidence suggests that the general public is usually poorly informed about and inattentive to monetary policy and inflation.222Candia et al. (2021) and Coibion et al. (2023) show that U.S. firms as well as households are usually poorly informed about and quite inattentive to monetary policy. Coibion and Gorodnichenko (2012, 2015a), for example, show that models of limited attention more closely align with empirical patterns of inflation expectations, compared to models with full-information rational expectations. In line with limited attention, D’Acunto et al. (2022) show that forward guidance is quite ineffective in stimulating inflation expectations. What do these low levels of attention imply for the conduct of monetary policy? And how has the public’s attention to inflation changed over the last fifty years?

To tackle these questions, I propose an approach to quantify attention to inflation in the data. This approach is based on a model of optimal attention choice subject to information acquisition costs. The result is a law of motion for inflation expectations in which attention governs how strongly agents update their expectations following an inflation surprise. The optimal degree of attention depends positively on how volatile and persistent inflation is.

Using micro survey data of professional forecasters and consumers in the U.S., I then use this approach to estimate attention to inflation in the data and show that attention was very low in the years just before the Covid-19 crisis. In the 1970s and 1980s, on the other hand, attention to inflation was substantially higher. Consistent with the underlying model, times of higher inflation volatility and persistence are characterized by higher attention to inflation.

How does this decline in attention matter for the conduct of optimal monetary policy? To answer this question, I solve for the Ramsey optimal monetary policy in a standard New Keynesian model augmented with an effective lower bound (ELB) on the nominal interest rate and with inflation expectations that are characterized by limited attention. Both of these ingredients matter greatly for optimal monetary policy and the normative implications of declining attention. Lower attention has a stabilizing effect on inflation expectations and actual inflation, resembling more anchored (short-run) expectations. These stabilization benefits imply that lower attention is welfare improving—if we do not account for the ELB (similar to the findings in Paciello and Wiederholt (2014)). Accounting for the occasionally-binding ELB, however, completely overturns the normative implications of lower attention. Lower levels of attention lead to a decline in welfare when we account for the lower-bound constraint. The reason is that lower attention renders managing expectations more difficult, which is particularly relevant if the nominal interest rate is constrained by the lower bound.333Coibion et al. (2022) and Coibion et al. (2023) show that managing expectations by the central bank is indeed a difficult task and the effects of monetary policy are much smaller than in most theoretical models. D’Acunto et al. (2022) find small effects of forward guidance on inflation expectations and durable consumption.

To better understand these results, I first show that under sub-optimal policy, i.e., if monetary policy follows an ad-hoc Taylor rule, limited attention can lead to substantially longer periods at the ELB. Even though lower levels of attention attenuate the initial response of inflation expectations to a given shock, the decline in expectations becomes more persistent which hinders actual inflation from recovering quickly. Due to the persistently-low inflation, the monetary authority keeps the interest rate at the ELB for longer. I refer to these periods of long spells at the ELB and persistent declines in inflation and inflation expectations as inflation-attention traps. The response of the output gap, on the other hand, is very similar to the one under rational expectations. Thus, low attention offers a potential explanation for why inflation was relatively stable during the Great Recession but was persistently low during the subsequent recovery, seemingly disconnected from output (as documented in Del Negro et al. (2020)).

When replacing the ad hoc Taylor rule with the Ramsey optimal policy, I find that it is optimal to induce a higher average inflation rate to deal with these attention traps and the overall inability to manage inflation expectations at low levels of attention. With a higher average inflation rate, the nominal interest is also higher on average. This provides additional space when cutting the interest rate following adverse shocks, thus, mitigates the drawbacks of lower attention, and therefore helps to prevent long spells at the ELB.444Thus, the reason for the higher inflation rate is different from earlier papers that also consider an occasionally-binding ELB (e.g., Adam and Billi (2006), Adam et al. (2022)). In these papers, the higher average inflation rate arises due to promises the policymaker makes at the lower bound. In the present paper, on the other hand, the higher inflation rate arises due to considerations before the lower bound binds, foreseeing what will happen at the lower bound. Such an increase in the average inflation rate is not optimal if we abstract from the ELB, as then the nominal rate can go negative. Given the estimates of attention just before the Covid-19 crisis, the average inflation rate under Ramsey optimal policy is about 2-3 percentage points higher than under rational expectations. This increase in the level of inflation, however, is costly from a welfare perspective and it turns out that this level effect dominates the stabilization benefits. Thus, lower attention is welfare deteriorating when accounting for the ELB.

Another instrument to mitigate the drawbacks of limited attention are negative interest rate policies. Allowing for negative interest rates up to (annualized) lowers the necessary increase in the optimal inflation target. As attention declines, however, the effectiveness of negative interest rate policies decreases and the optimal increase in the inflation target is close to the one without negative rates.

Related literature.

Bracha and Tang (2023) show that attention to inflation increases, when inflation increases. Using Google search data, Korenok et al. (2022) find that people’s attention to inflation increases with inflation only after inflation exceeds a threshold of around 2-4%. Cavallo et al. (2017) and Weber et al. (2023) use randomized information treatments and show that attention of households and firms is higher in times of high inflation. Link et al. (2023) also find that attention to inflation is higher in times of high and volatile inflation. My key contribution relative to these papers is that I provide estimates of attention in a way that directly maps into otherwise standard macroeconomic models.

The empirical part of this paper is related to recent findings in Jørgensen and Lansing (2023) who show that inflation expectations have become more anchored over the last decades.555Similarly, Gáti (2022) documents that anchoring of long-run inflation expectations is time varying and has substantially increased recently. My measure of attention is inversely related to their definition of anchoring, but attention is concerned with short-run expectations whereas anchoring usually refers to the stabilization of long-run expectations. I complement their empirical analysis along several dimensions which I detail more closely in the empirical Section 2. Additionally, I offer new insights in how stabilized expectations matter when nominal interest rates are constrained by a lower-bound constraint and what this implies for optimal monetary policy.

My limited-attention model of inflation expectations is closely related to the general information choice problem in Maćkowiak et al. (2023). In contrast to their model, and the rational inattention literature more generally, agents in my model have a perceived law of motion of inflation that can potentially differ from the actual law of motion.666Maćkowiak et al. (2023) provide a recent overview of this literature, which was inspired by the seminal paper Sims (2003). For further developments in this literature, see, among others, Mackowiak and Wiederholt (2009), Paciello and Wiederholt (2014), Maćkowiak et al. (2018), Afrouzi and Yang (2021), and see Gabaix (2019) for an overview of behavioral inattention. The reduced-form of the model that I bring to the data is close to the one in Vellekoop and Wiederholt (2019). In contrast to their paper, I focus on how attention changed over the last fifty years and show that attention tends to be higher in times of volatile and persistent inflation.

Ball et al. (2005), Adam (2007), Paciello and Wiederholt (2014) and Gáti (2022) characterize optimal monetary policy in models with different forms of limited attention. I contribute to this literature by allowing for an occasionally-binding lower-bound constraint. I show that accounting for the lower bound can lead to qualitatively different welfare implications due to changes in the optimal level of inflation. Wiederholt (2015) and Gabaix (2020) examine how information rigidities and inattention matter at the zero lower bound. Angeletos and Lian (2018) study the implications of relaxing the common knowledge assumption for forward guidance and show that the effects of forward guidance are attenuated in such a setting. My paper complements these three papers by studying the Ramsey optimal policy in a fully stochastic setup and focuses on the implications for the optimal inflation target. To the best of my knowledge, the present paper is the first to study the trade off of lower attention in a fully stochastic model with an occasionally binding lower-bound constraint and to characterize the Ramsey optimal monetary policy in such a setting.

Outline.

The rest of the paper is structured as follows. The empirical strategy to quantify attention, the description of the data and the empirical results are presented in Section 2. In Section 3, I show how limited attention can lead to inflation-attention traps, before I then study optimal policy in Section 4. Section 5 concludes. An online appendix provides all the derivations, several extensions and robustness checks.

2 Quantifying Attention

In this section, I derive an expectations-formation process under limited attention that provides a straightforward approach to measure attention to inflation empirically. The model is an application of Maćkowiak et al. (2023), who study a general problem of optimal information acquisition. I relegate all the details and derivations to appendix A.

The main difference to Maćkowiak et al. (2023) is that agents in my model do not exactly know the underlying process of inflation but have a simplified view of how inflation evolves.777In the monetary model, later on, I will disentangle the effects from this potentially misperceived law of motion from the assumption of costly attention and show that most of the results are driven by limited attention and not the misperceived law of motion (see section 4.3.5). In particular, the agent believes that (demeaned) inflation tomorrow, , depends on (demeaned) inflation today, , as follows

where denotes the perceived persistence of inflation and . This assumption is supported by empirical evidence (see e.g., Faust and Wright (2013) or Canova (2007)).888Fulton and Hubrich (2021) show that simple models such as AR(1) models are hard to beat when forecasting inflation in real time. Note, that the perceived volatility and persistence do not need to be the same as their actual counterparts, consistent with the empirical evidence on inflation expectations (see Table 7 in the Appendix). The agent wants to minimize her expected forecast error but inflation in the current period is unobservable and acquiring and processing information is costly. The agent thus faces a trade off how attentive she wants to be. I follow the literature on rational inattention and assume that the loss arising from making mistakes in her forecasts is quadratic with a scaling factor , and the cost of information acquisition and processing is linear in mutual information with a scaling parameter .

In this setup and with a normal prior, the optimal signal takes the form

with (see Matějka and McKay (2015)).

The optimal forecast is given by , and Bayesian updating implies

| (1) |

where measures how much attention the agent pays to inflation, and denotes the prior mean of .

Solving for the optimal and writing the cost of information relative to the stakes, , yields the optimal level of attention, summarized in the following Lemma.

Lemma 1.

The optimal level of attention is given by

| (2) |

which shows that the optimal level of attention is

-

(i)

decreasing in the relative cost of information acquisition, ,

-

(ii)

increasing in inflation volatility, , and

-

(iii)

increasing in inflation persistence, .

From Lemma 1, we see that aside from the relative information cost, , the persistence, , and the volatility of inflation, , are crucial drivers of attention. The model predicts a positive relationship between attention and , as well as between attention and . In the following, I will first estimate attention , asses how it has changed over time and then test whether there is indeed evidence for these positive relations.

2.1 Bringing the Model to the Data

To estimate attention in the data, I extend the law of motion of inflation expectations, equation (1), to a dynamic setup. The agent believes that inflation follows

where is the agent’s long-run belief about inflation and is the perceived persistence of inflation. I assume that the error term is normally distributed with mean zero and variance .999In Appendix B.1, I discuss the case in which the agent believes that inflation follows an AR(2) process.

The agent receives a signal about inflation of the form

where the noise is assumed to be normally distributed with variance .

Given these assumptions, it follows from the (steady state) Kalman filter that optimal updating is given by

| (3) |

where the updating gain captures the agent’s level of attention, and is a scaled version of the i.i.d. noise term . From equation (3), we observe that lower attention, i.e., a lower , implies that the agent updates her expectations to a given forecast error, , less strongly. Lower attention is reflected in more noisy signals, and more noise means the agent trusts her received signals less and thus, puts less weight on these signals. Hence, her expectations remain more strongly anchored at her prior beliefs.

2.2 Data

I focus on the Survey of Professional Forecasters (SPF) from the Federal Reserve Bank of Philadelphia, as well as the Survey of Consumers from the University of Michigan (SoC). In the Appendix, I show that the findings extend to other data sets as well. For the SPF, I consider individual and aggregate forecasts. The main focus is on expectations about the quarter-on-quarter percentage change in the GDP deflator, which is available since 1969. I drop forecasters for which I have less than eight observations. As a robustness check, I will show that the results are robust to using expectations about the consumer price index, CPI. This data series, however, is only available since 1979.

While the SPF provides data on expectations about the next quarter, the SoC only provides one-year-ahead expectations. Therefore, I will compare them to the actual year-on-year changes in the CPI.101010The question in the SoC is not explicitly about the CPI but about “prices”. Using GDP deflator inflation instead of CPI inflation barely affects the results. As the SoC does not have a panel dimension, I consider average (and median) expectations. Additionally, I estimate attention using the Survey of Consumer Expectations from the Federal Reserve Bank of New York (SCE). The SCE, launched in 2013, has a panel structure and thus allows me to estimate attention using individual-consumer data, at least for the period after 2013. Data on actual inflation comes from the FRED database from the Federal Reserve Bank of St. Louis. Throughout, I focus on the pre-Covid period and end the sample in 2019Q4.111111In a follow-up paper, I study the implications of changes in people’s attention to inflation in driving high and persistent inflation and show that this offers a potential explanation for the inflation surge that occurred after the Covid-19 pandemic (Pfäuti, 2023). Appendix B provides summary statistics and plots the discussed time series.

Jørgensen and Lansing (2023) estimate how strongly anchored inflation expectations in the U.S. are and how this changed over the last fifty years. I extend their empirical strategy in several dimensions. First, I allow the persistence of perceived inflation to change over time and do not restrict it to follow a random walk. Second, I show that not only aggregate professional forecasters’ expectations have become more anchored, but also consider individual-specific expectations, as well as consumers’ inflation expectations. Third, I do not impose the structure of the New Keynesian Phillips Curve on the data but directly estimate attention simply based on the proposed law of motion for inflation expectations. That said, we will see that my results are consistent with the results in Jørgensen and Lansing (2023).

2.3 Estimation Results

Before estimating attention, I rewrite the updating equation (3) as

| (4) |

where , and . For the SPF, where I can use individual forecasts, I estimate (4) using a forecaster-fixed-effects regression. Since the dependent variable shows up with a lag on the right-hand side, however, a standard fixed-effects regression introduces a bias (Nickell, 1981). Therefore, I apply the estimator proposed by Blundell and Bond (1998) (BB for short) and I use all available lags of the dependent variable as instruments.121212Appendix B.1 shows that the results are robust to using fewer lags. All reported standard errors are robust with respect to heteroskedasticity and serial correlation. As an alternative to the BB estimator, I also estimate (4) using pooled OLS. For the Survey of Consumers I cannot include individual fixed effects as I use average and median expectations and thus, I apply the Newey-West estimator using four lags (Newey and West (1987)).

To examine how attention changed over time, I run regression (4) for the period before and after 1990, separately. The results are robust to different split points (see Appendix B.1). Later on, I will estimate (4) using rolling-windows of ten years each and show that the general patterns I document are robust.

| Professional Forecasters | Consumers | |||

| Blundell Bond | Pooled OLS | Averages | Median | |

| 0.70 | 0.44 | 0.75 | 0.43 | |

| s.e. | (0.1005) | (0.0397) | (0.1574) | (0.0970) |

| 0.41 | 0.22 | 0.31 | 0.24 | |

| s.e. | (0.0522) | (0.0290) | (0.0881) | (0.0601) |

| 3566 | 3566 | 120 | 120 | |

Note: This table shows the results from regression (4) for professional forecasters (SPF) as well as for consumers. For the SPF, I use the Blundell and Bond (1998) (BB) estimator (first two columns), as well as pooled OLS (columns 3-4). For the Survey of Consumer, I consider average expectations (columns 5-6) and median expectations (columns 7-8). and denote the estimated attention parameters for the period pre 1990 and post 1990, respectively. The standard errors, reported in parentheses, are robust with respect to heteroskedasticity and serial correlation.

Table 1 shows the results. Here, and denote the estimated attention parameters for the period pre 1990 and post 1990, respectively. We see that attention is substantially lower after 1990 compared to the period before 1990.131313I test the validity of the instruments in the Blundell-Bond estimation by testing for autocorrelation of order one and two in the first-differenced error terms. The respective -values are 0.000 (order 1) and 0.973 (order 2) for the period before 1990 and 0.000 (order 1) and 0.737 (order 2) for the period after 1990. This indicates that the instruments used in the estimation are valid. This is true for professional forecasters and for consumers, and as I show in Appendix B.1, also for other datasets. The point estimates after 1990 are basically half of what they were before the 1990s and these differences are statistically significant at the 1% level.

The decline in attention is even more pronounced when focusing on the most recent decade. To show this, I run regression (4) for the period between 2010 and 2020. Additionally, I also use data from the New York Fed Survey of Consumer Expectations, starting in 2013. The advantage of this survey compared to the Michigan Survey is that it surveys the same consumers up to twelve times in a row, providing a much larger sample size and a panel dimension. Table 2 shows the results. We see that overall, attention declined substantially compared to earlier periods and is between 0.04 and 0.17 during this period of low and stable inflation. Furthermore, the results from the SCE lie in the same ballpark as the ones from the Michigan Survey, which indicates that using average (or median) consumer expectations does not fundamentally affect the results. In fact, the estimated attention parameter for the average expectations from the Michigan Survey is 0.04 when restricting the sample to 2013-2020, which is exactly the same as the estimate obtained from the New York Fed Survey.

| Professional Forecasters | Consumers | NY Fed Survey | |||

| Blundell Bond | Pooled OLS | Averages | Median | Pooled OLS | |

| 0.17 | 0.07 | 0.12 | 0.09 | 0.04 | |

| s.e. | (0.0729) | (0.0333) | (0.0658) | (0.0616) | (0.0316) |

| 1322 | 1322 | 40 | 40 | 74229 | |

Note: This table shows the results from regression (4) for the period between 2010 and 2020 for professional forecasters (SPF) as well as for consumers. For the SPF, I use the Blundell and Bond (1998) (BB) estimator (first column), as well as pooled OLS (column 2). For the Survey of Consumer, I consider average expectations (column 3) and median expectations (columns 4). The standard errors, reported in parentheses, are robust with respect to heteroskedasticity and serial correlation. Additonally, column 5 shows the results for consumer inflation expectations from the New York Fed Survey of Consumer Expectations.

2.3.1 When is Attention High?

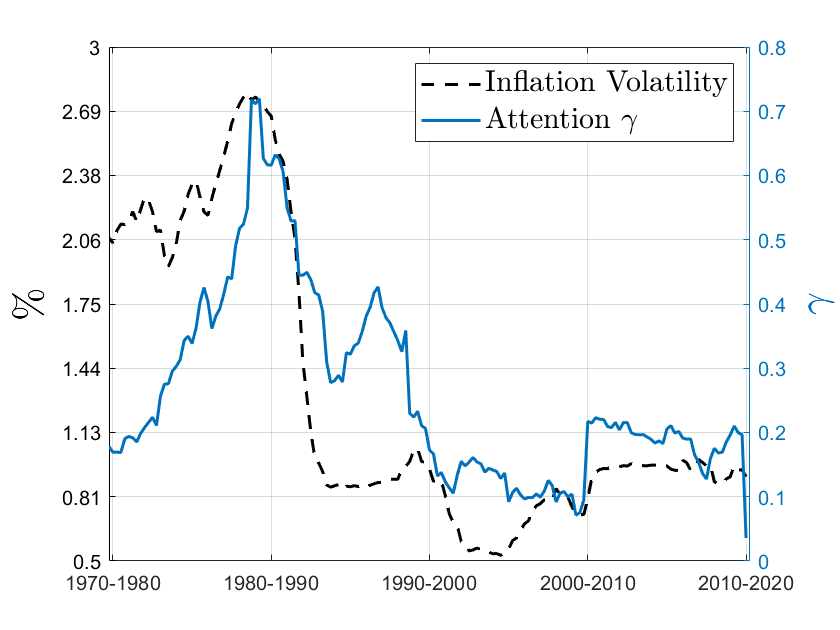

Lemma 1 states that two key drivers of attention are inflation volatility and inflation persistence. To examine these relationships empirically, I estimate regression (4), using a rolling-window approach in which every window is 10 years long, and estimate one attention parameter for every window, , as well as the period-specific inflation volatility, and the persistence parameter, . In particular, I use the window-specific standard deviation of inflation as my measure of and the first-order autocorrelation of inflation for . Appendix B.1 shows that the following results also hold for different window lengths or when using the standard deviation and persistence of expected inflation for and .

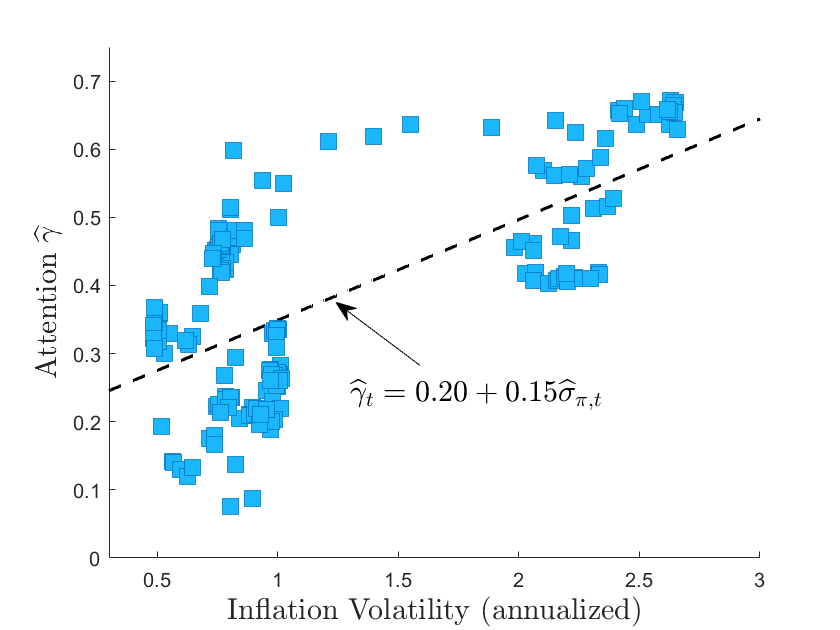

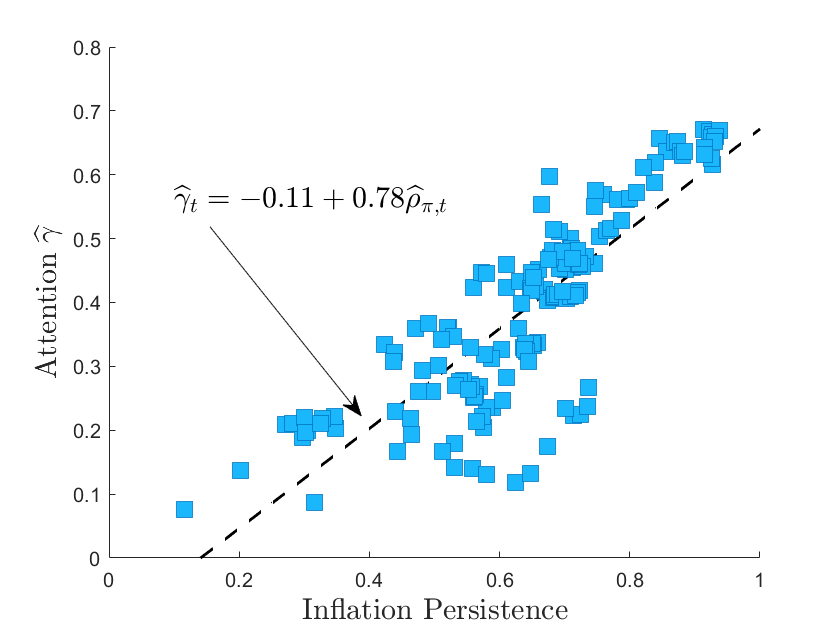

Figure 1 summarizes the results graphically. The left scatterplot shows the inflation volatility on the horizontal axis and the estimated attention parameter, , on the vertical axis. The attention parameters shown in the figure are the ones for individual professional forecasters, obtained via pooled OLS. The right panel shows the relationship between attention and inflation persistence (on the horizontal axis). In both cases, we see that there is a clear positive relationship, just as the limited-attention model predicts.

| (a) Inflation Volatility | (b) Inflation Persistence |

|---|---|

|

|

Notes: The right panel shows the relationship between inflation volatility and the estimated attention parameter, . The left panel shows the relationship between the persistence of inflation and the estimated attention parameter. Both panels report the results for individual professional forecasters where the attention parameter was estimated via pooled OLS.

To check if these findings are statistically significant, I regress attention on inflation volatility or on inflation persistence as follows

| (5) | ||||

| (6) |

| Professional Forecasters | Consumers | |||

| Estimator | Blundell-Bond | Pooled OLS | OLS | |

| s.e. | (0.0155) | (0.0105) | (0.0272) | |

| s.e. | (0.0568) | (0.0349) | (0.0714) | |

| 165 | 165 | 163 | ||

Table 3 reports the results. Standard errors are robust with respect to heteroskedasticity. We see that the observed patterns in Figure 1 are indeed statistically significant. Attention to inflation is positively correlated with inflation volatility and inflation persistence, as Lemma 1 predicts. This is true for professional forecasters as well as for consumers. Overall, the magnitudes of the estimates indicate that the results are somewhat stronger for professional forecasters. Appendix B.1 shows that these results hold when regressing attention on inflation volatility and persistence jointly. I also show that the results are robust when controlling for the average level of inflation and the average level of inflation has no significantly-positive effect on attention when controlling for volatility and persistence. Given the decline in inflation volatility and inflation persistence over the last fifty years (see Table 7 in Appendix B), the positive correlation with attention supports the findings in Table 1: attention declined as the volatility and persistence of inflation declined.141414Benati (2008) documents a decline in inflation persistence in advanced economies, especially for countries that introduced inflation targeting regimes.

Additional evidence and robustness.

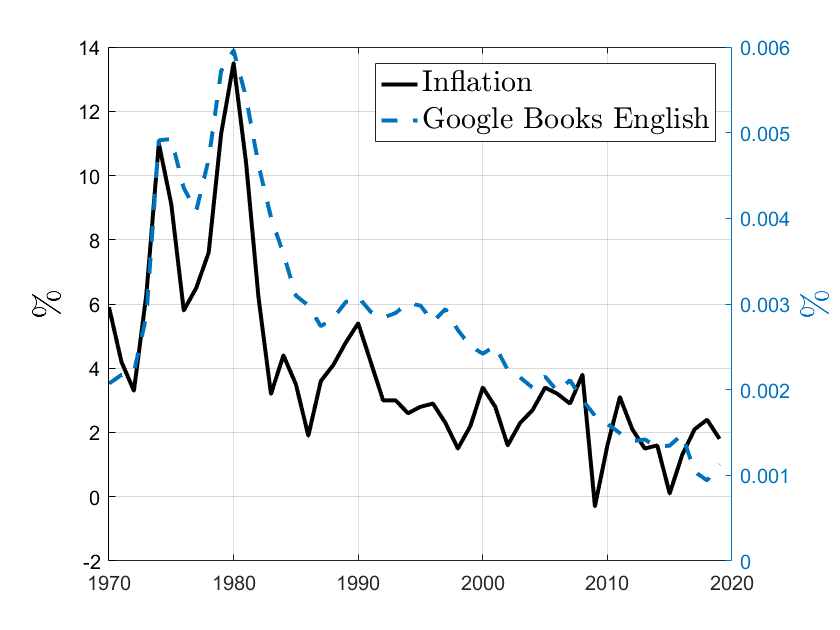

In Appendix B.1, I show that the presented results are robust to using different data sources, different sample splits, different specifications of the BB estimator, allowing for time-fixed effects to account, for example, for varying trend inflation, as well as constructing a quasi panel of consumers, based on their income. I further discuss the case in which the agent believes that inflation follows an AR(2) process. I again find that attention has declined substantially after the 1990s and that the additional coefficients showing up due to the AR(2) rather than the AR(1) tend to be insignificant. In Appendix B.2, I document a decline in news coverage of inflation in popular news papers as well as in books, thus, providing additional, complementary evidence on the decline in attention after the 1980s.151515Carroll (2003) proposes a micro-foundation of sticky information models (as in Mankiw and Reis (2002)) that relies on news coverage of inflation. Lamla and Lein (2014) and Pfajfar and Santoro (2013) test these predictions empirically. Additionally, I show that another measure of attention (based on survey respondents answering "I don’t know" when asked about their inflation expectations) is strongly correlated with my proposed measure of attention. Finally, I provide additional evidence favoring the proposed attention model compared to a setup in which the agent cannot distinguish between a trend and a cyclical component with time-varying volatilities of these two components. In that case, if the trend component’s contribution to overall inflation increases, the agent’s forecast would become more responsive to current inflation, too. I show that professional forecasters’ nowcasts of inflation are more accurate in times of high inflation volatility and persistence, which supports the proposed attention model rather than this alternative model.

3 Monetary Policy Implications of Limited Attention

How does the decline in attention to inflation affect the conduct of monetary policy? To answer this question, I augment the standard New Keynesian model with inflation expectations that are characterized by limited attention, and a lower-bound constraint on the nominal interest rate (model details and all derivations are in Appendix C). I build on the standard New Keynesian model without capital, with rigid prices in the spirit of Rotemberg (1982) and with a lower bound on the nominal interest rate. The government pays a subsidy to intermediate-goods producers to eliminate steady state distortions arising from market power. I focus on the case with zero-steady state inflation as my baseline case, but discuss the case of positive trend inflation in Section 4.3.3.

The linearized model consists of an aggregate supply equation, the New Keynesian Phillips Curve, and an aggregate Euler (or IS) equation:

| (7) | ||||

| (8) |

where measures the sensitivity of aggregate inflation to changes in the output gap, , denotes the time discount factor of the representative household, and are cost-push shocks, following an AR(1) process with persistence and innovations . The output gap is the log deviation of output from its efficient counterpart that would prevail under flexible prices. Altogether, equation (7) summarizes the aggregate supply side of the economy. Equation (8), together with monetary policy, determines aggregate demand in this model. Here, measures the real rate elasticity of output, is the nominal interest rate which is set by the monetary authority, and is the natural interest rate. The natural interest rate is the real rate that prevails in the economy with fully flexible prices and is exogenous. It follows an AR(1) process with persistence and innovations independent of . The nominal interest rate and the natural rate are both expressed in absolute deviations of their respective steady state values, and . denotes the full-information rational expectations operator. I relax the assumption that agents have rational expectations about the output gap in section 4.3 and in appendix E.1.

Inflation expectations are characterized by limited attention and are given by

| (9) |

where the notation is the same as in Section 2. Given the representative agent assumption, I abstract from noise shocks in (9). The law of motion of inflation expectations, equation (9), is driven by two main assumptions. First, the perceived law of motion follows an AR(1) process and second, paying attention is costly. In Section 4.3.5, I will disentangle the two and show that it is mainly the second assumption that drives the implications for optimal monetary policy. For the most part, I will focus on in which case average inflation expectations align with actual average inflation and long-run beliefs are irrelevant. I discuss the case with in Appendix E.4. For empirically-realistic values of the results are very similar to the case with . This belief formation process is empirically plausible, in the sense that it is consistent with recent empirical findings, documented in Angeletos et al. (2021): after a shock, expectations initially underreact, followed by a delayed overreaction (see Appendix E.3).

As is standard in the rational inattention literature, I assume that the attention parameter is constant.161616See, e.g., Mackowiak and Wiederholt (2009), Maćkowiak et al. (2018, 2023). The usual assumption to obtain this is that in period the agent chooses her level of attention and then obtains all future signals at this point. This leaves conditional second moments time-invariant and thus, the optimal level of attention constant. I will, however, compare economies with different levels of attention. In Section 4.3.4, I discuss the case in which attention to inflation is time varying.

| Parameter | Value | Source/Target |

| Preferences and technology | ||

| 0.9975 | Average natural rate of | |

| Adam and Billi (2006) | ||

| Adam and Billi (2006) | ||

| Exogenous shock processes | ||

| 0.8 | Adam and Billi (2006) | |

| 0.2940% | Adam and Billi (2006) | |

| 0 | Adam and Billi (2006) | |

| 0.154% | Adam and Billi (2006) | |

Calibration.

Attention and the Phillips Curve.

Inflation expectations are a crucial driver of actual inflation through the supply side of the economy, and thus, changing levels of attention affect the Phillips Curve. The following Proposition summarizes these effects.

Proposition 1.

The New Keynesian Phillips Curve under limited attention is given by

Proof.

See Appendix D.2. ∎

From Proposition 1, we see that for a given prior inflation expectation, , and a given realization of the exogenous shock , inflation becomes less sensitive to changes in the output gap at lower levels of attention. Put differently, a decrease in attention resembles a flatter Phillips Curve. We also see that for a given output gap, inflation becomes less sensitive to cost-push shocks at lower levels of attention.

Thus, Proposition 1 captures the stabilizing effects of lower attention. As attention declines, firms’ inflation expectations react less to changes in actual inflation. Through the Phillips Curve, this muted reaction of expectations in turn stabilizes inflation itself. What cannot be seen from Proposition 1, but what will be crucial in the subsequent analysis, is that lower attention not only affects the initial response of inflation and inflation expectations but the dynamics as well. Changes in inflation and inflation expectations become more persistent at low levels of attention, even though the initial response is muted. I now show in a numerical example that at low levels of attention the economy can get stuck in an inflation-attention trap.171717In Appendix D, I show analytically how lower levels of attention mute the effects of forward guidance.

3.1 Inflation-Attention Traps

To close the model from Section 3, I assume for now that, away from the lower bound, the monetary authority sets the nominal interest rate according to a Taylor rule

| (10) |

where captures interest rate smoothing, and denote the reaction coefficients to inflation and the output gap, respectively. The actual interest rate, , however is constrained by the lower bound

| (11) |

where I set the lower bound (in levels) to zero.

I set the persistence parameter of the nominal interest rate to 0.7, and the reaction coefficients and , as in Andrade et al. (2019). In Appendix E.2, I show that the exact specification of the Taylor rule is inconsequential for the following results.

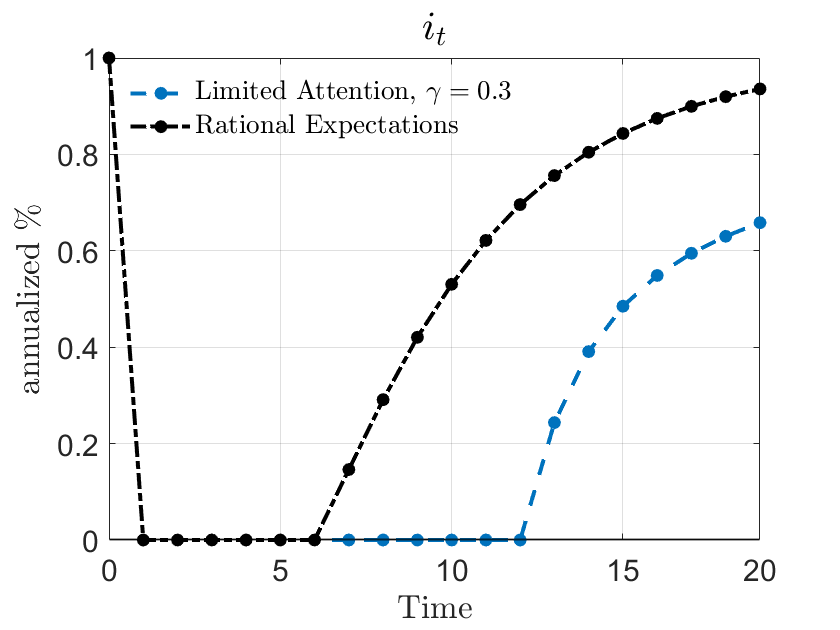

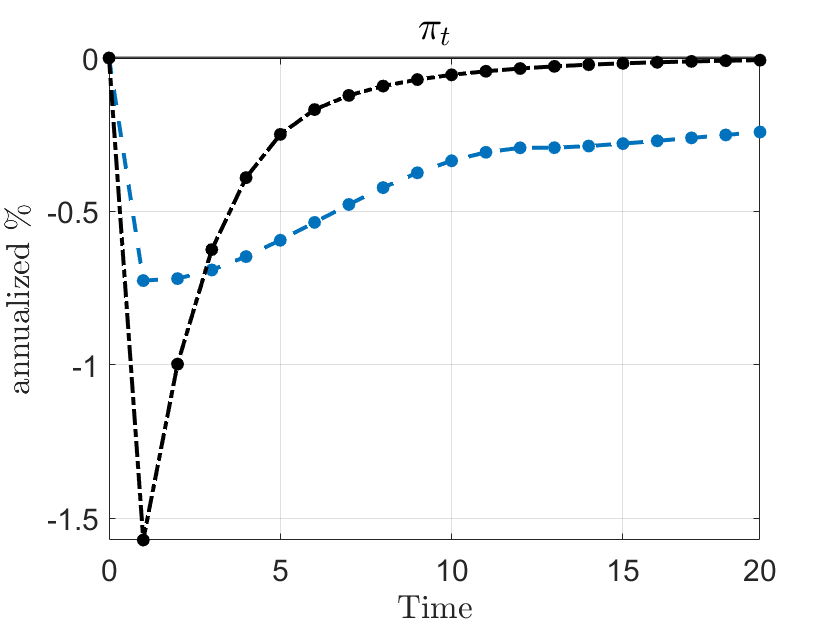

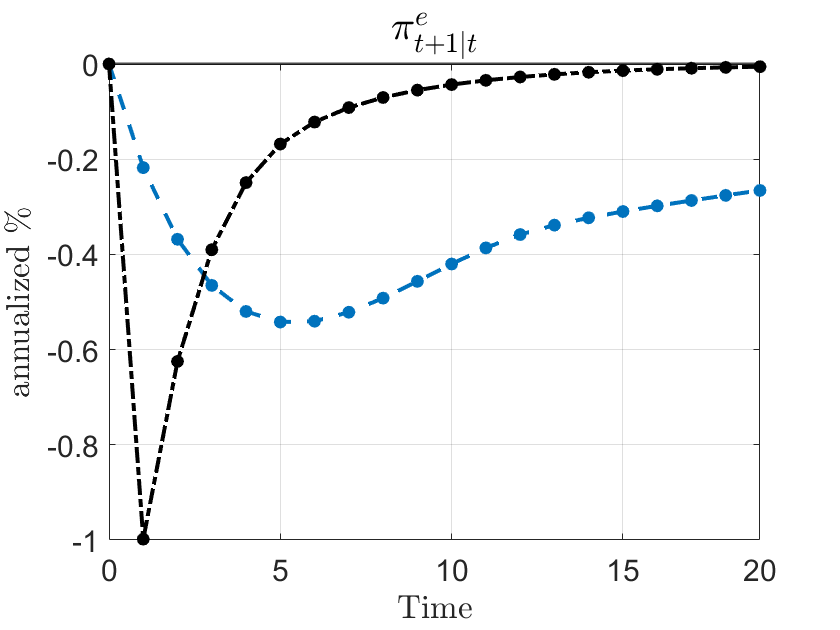

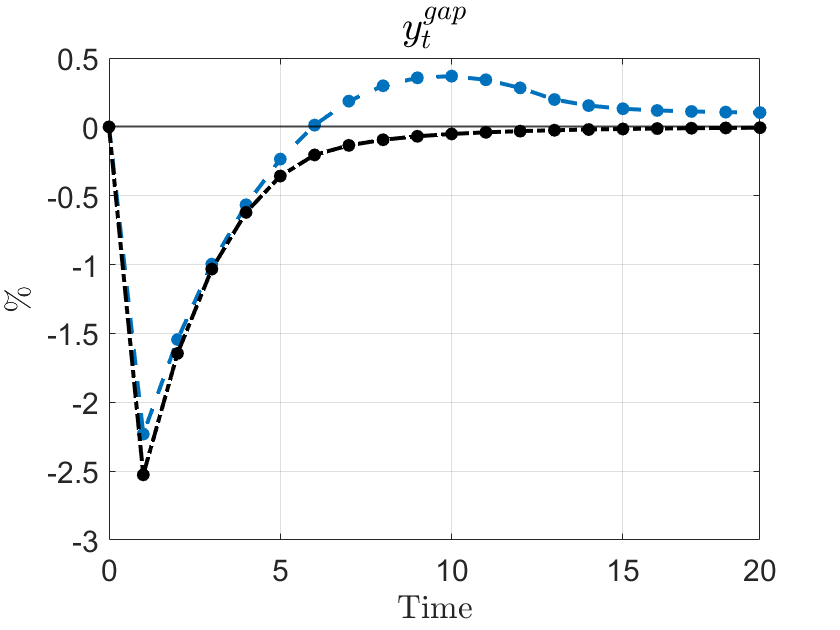

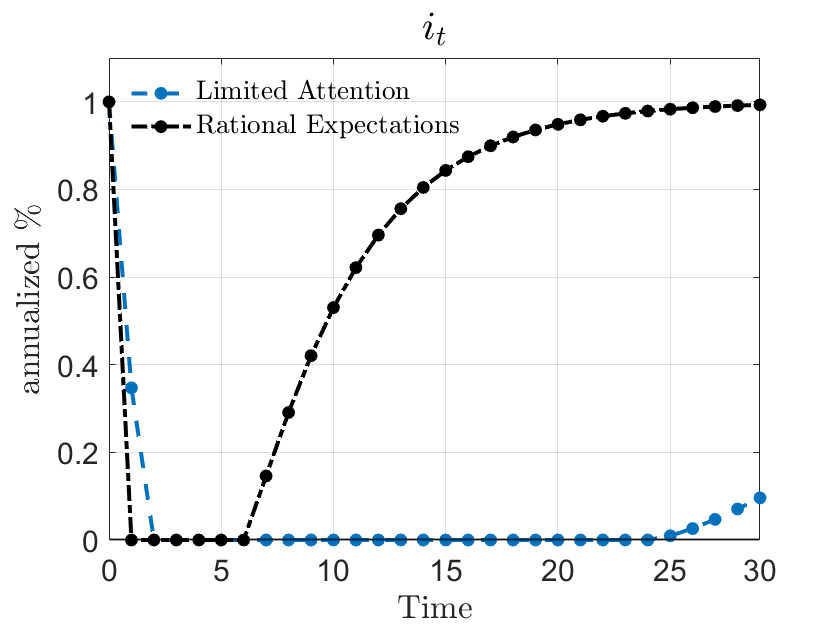

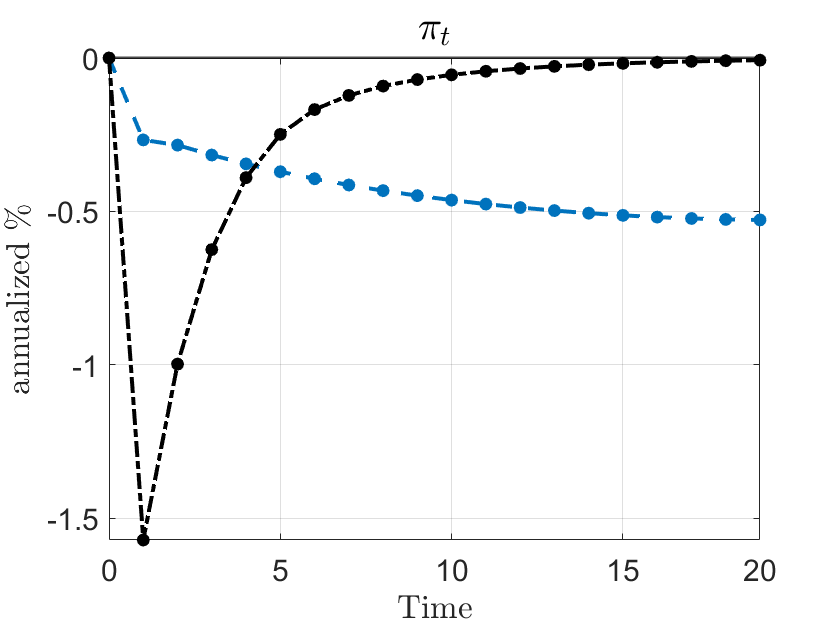

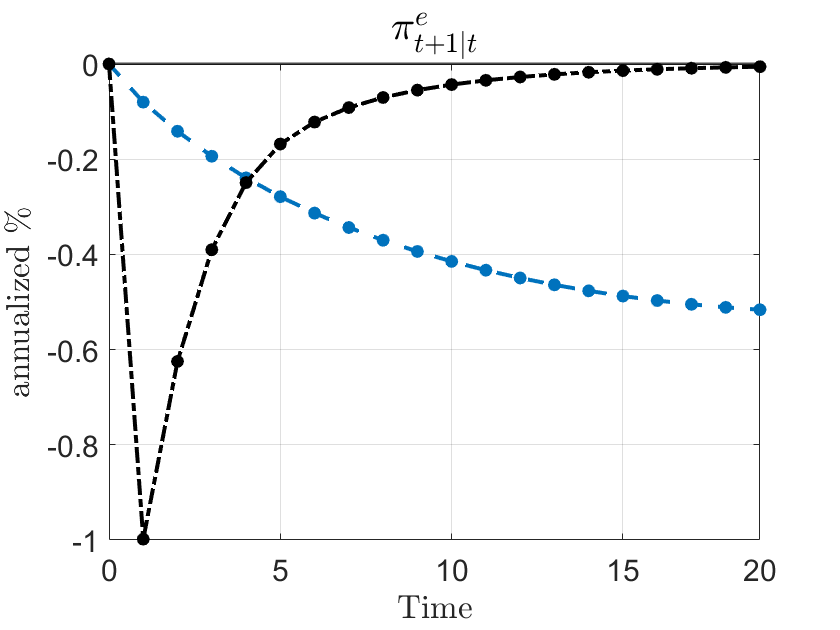

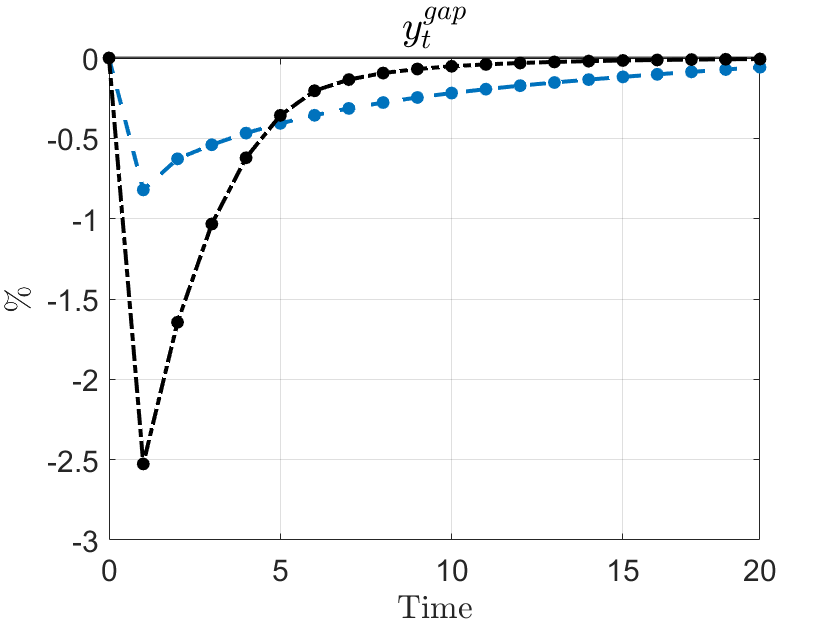

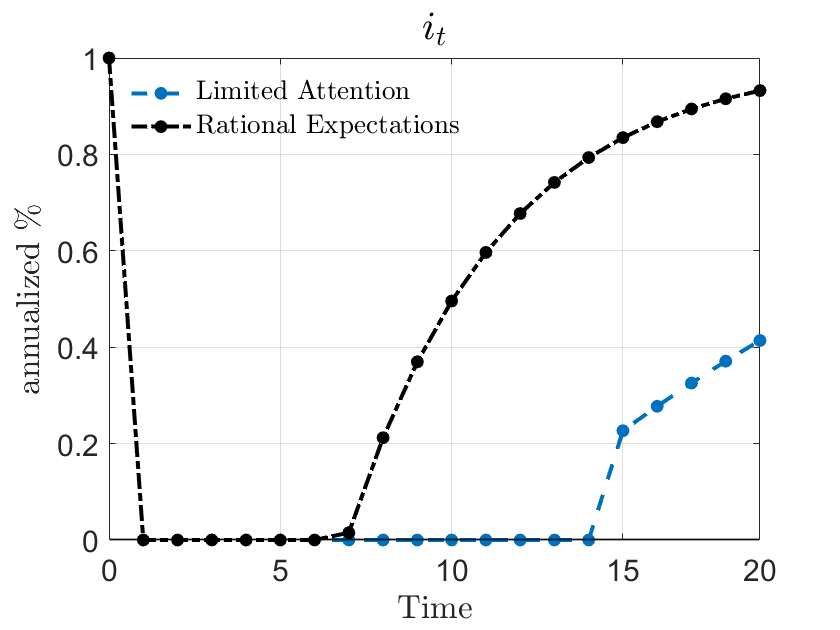

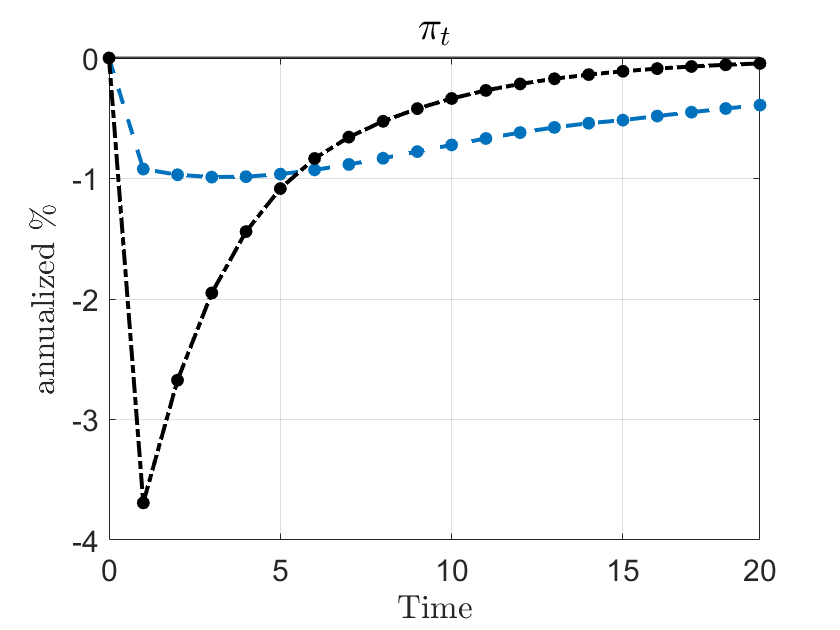

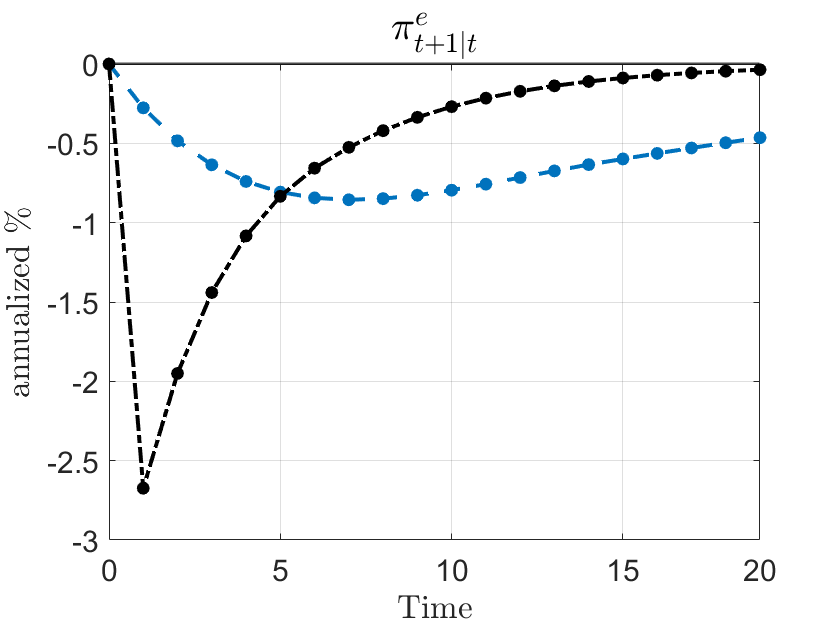

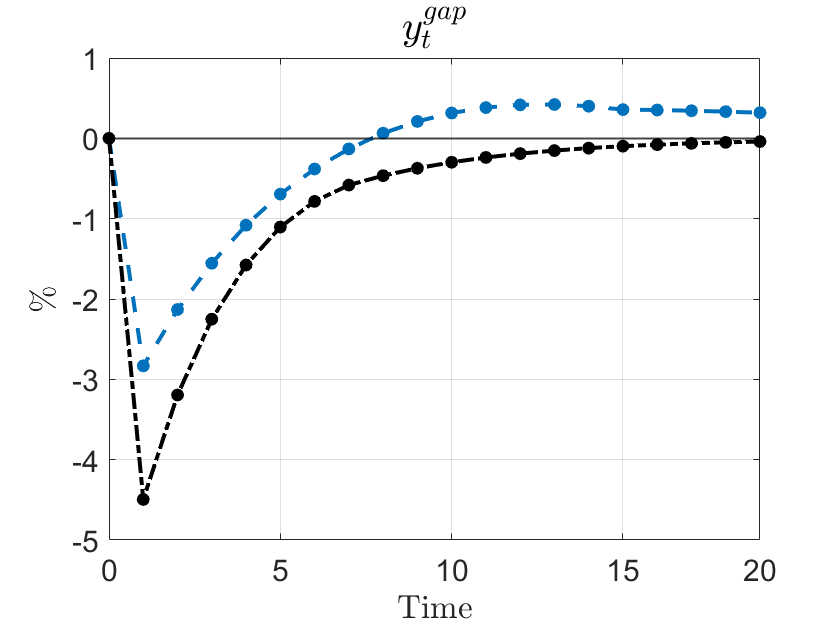

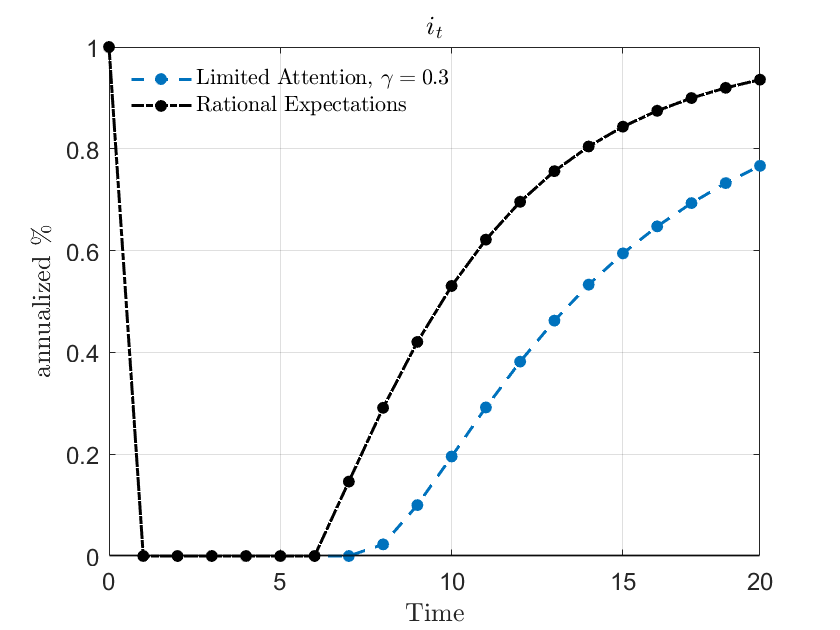

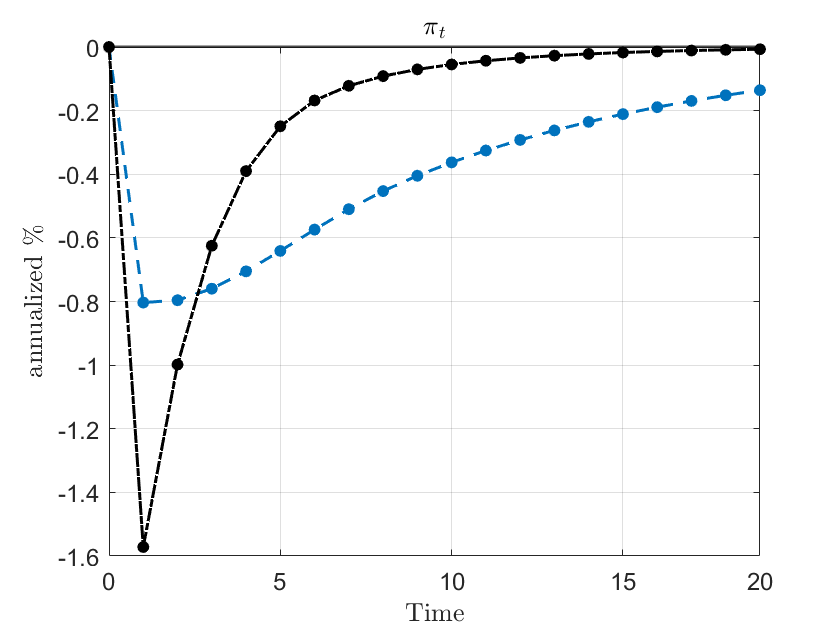

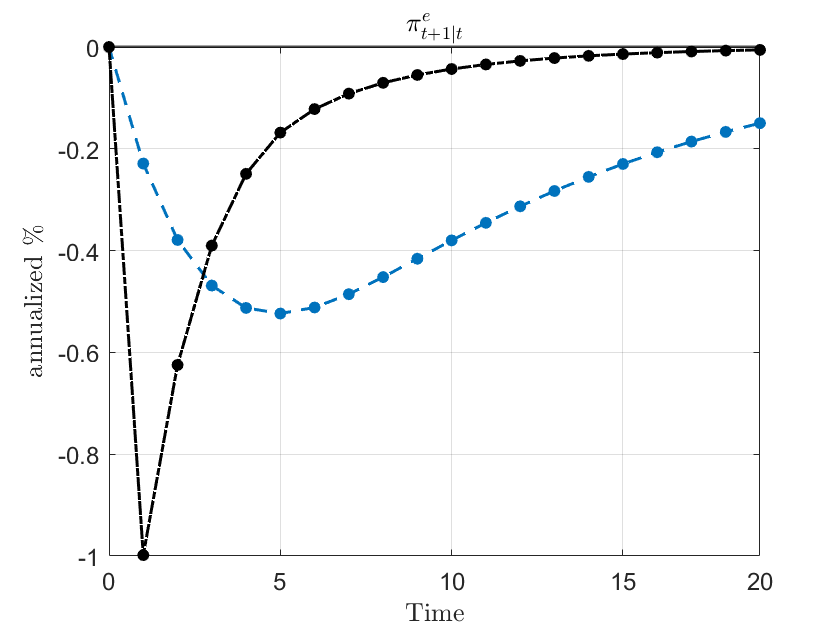

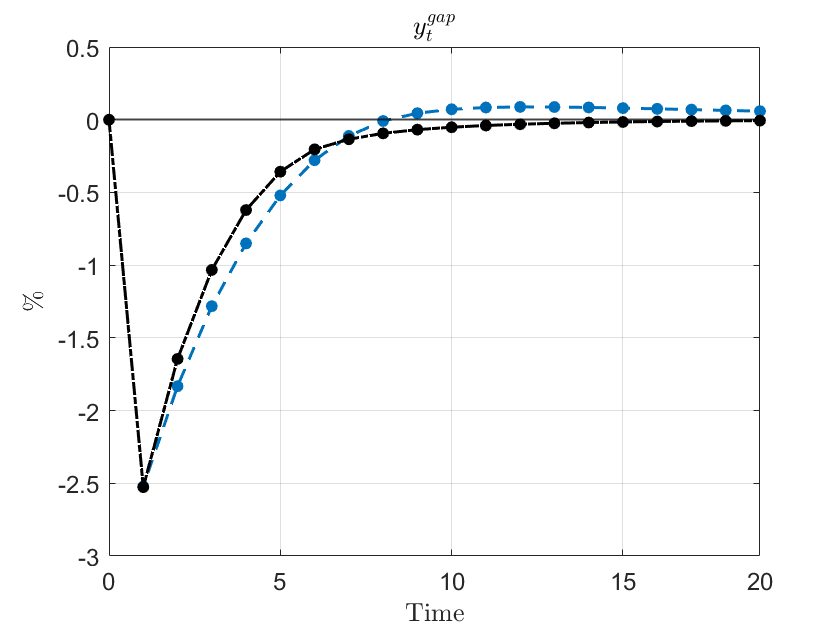

Figure 2 plots the impulse response functions of the model’s main variables to a negative natural rate shock of three standard deviations that pushes the nominal interest rate to the lower bound. The black-dashed-dotted lines are the IRFs in the model under FIRE and the blue-dashed lines are the ones under limited attention for the case .

|

|

|

|

Note: This figure shows the impulse-response functions of the nominal interest rate (upper-left panel), inflation (upper-right panel), inflation expectations (lower-left) and the output gap (lower-right) to a negative natural rate shock of three standard deviations. The blue-dashed lines show the case for the limited-attention model and the black-dashed-dotted lines for the rational expectations model. Everything is in terms of percentage deviations from the respective steady state levels, except the nominal rate is in levels.

In both cases, the shock is large enough to push the economy to the lower bound. While the reaction of the output gap is very similar in both economies, the responses of inflation and inflation expectations are strikingly different. Initially, the muted response of inflation expectations to the adverse shock is reflected in a smaller downturn of inflation itself under limited attention. This captures the stabilizing effects that come with lower attention. The sluggish adjustment of inflation expectations in the following, however, leads to a very persistent undershooting of inflation. Even five years after the shock, inflation and inflation expectations are still substantially below their steady state levels of zero. The result is a prolonged period of a binding lower bound. While the economy under rational expectations escapes the ELB six periods after the shock, the economy under limited attention is stuck for twice as long. This is what I label inflation-attention trap. A side-effect of these traps is that the long ELB period leads to an output boom. As discussed earlier, this (expected) output boom in the future, however, has rather small effects on the economy today if people are inattentive.

Overall, limited attention to inflation offers a possible explanation for why several advanced economies were stuck at the ELB after the financial crisis, as well as inflation that undershot the central banks’ inflation targets, even though the initial decrease was muted and output recovered quite strongly after declining severely initially (Del Negro et al. (2020)). In other words, the limited-attention model can explain the missing deflation puzzle as well as the missing inflation puzzle (Coibion and Gorodnichenko (2015b), Constancio (2015)).

4 Optimal Monetary Policy

To understand how monetary policy should optimally deal with declining attention, I now derive the Ramsey optimal monetary policy in this economy. I focus on the case of , in which average inflation expectations coincide with the actual inflation average. Appendix E.4 reports the results when relaxing this assumption.

The policymaker’s objective is to maximize the representative household’s utility, taking the household’s and firms’ optimal behavior, including their attention choice, as given. Thus, the policymaker cannot exploit the private agent’s lack of information. Nevertheless, the policymaker can affect inflation expectations by influencing inflation itself and can set the average inflation expectations by setting the average inflation rate.

The policymaker is paternalistic in the sense of Benigno and Paciello (2014) and evaluates the household’s utility under rational expectations. A second-order approximation to the household’s utility function yields the policymaker’s objective

| (12) |

where is the relative weight of the output gap, which I set to as in Adam and Billi (2006). In the following, I refer to (12) as welfare.

In sum, the optimal policy problem is given by

| (13) |

subject to

| (14) | |||

| (15) | |||

| (16) | |||

| (17) | |||

| (18) | |||

| (19) |

with and and (19) is the lower-bound constraint.181818I solve this numerically by recursifying the constrained optimization problem, as in Marcet and Marimon (2019). All variables are in percent deviations from their respective steady state, except the nominal interest rate and the natural rate which are in absolute deviations.

4.1 The Optimal Inflation Target

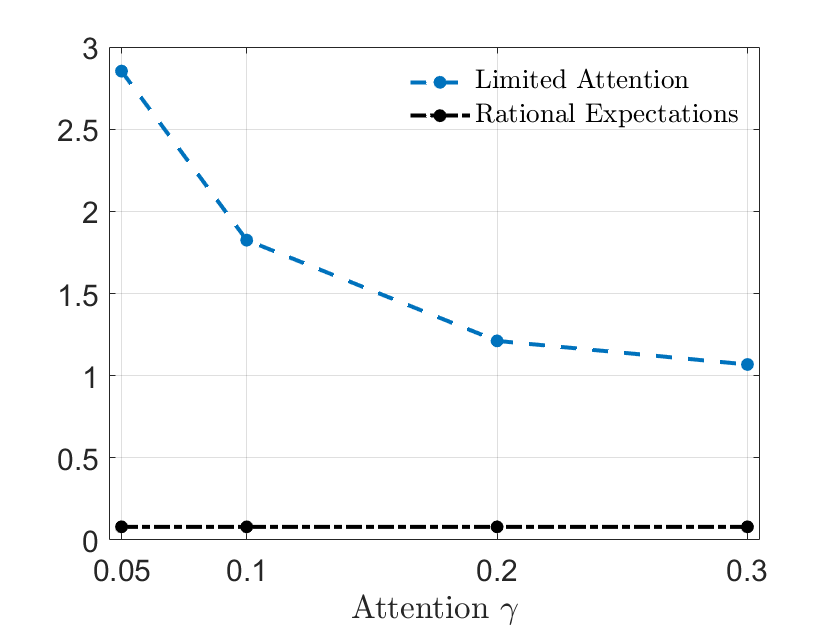

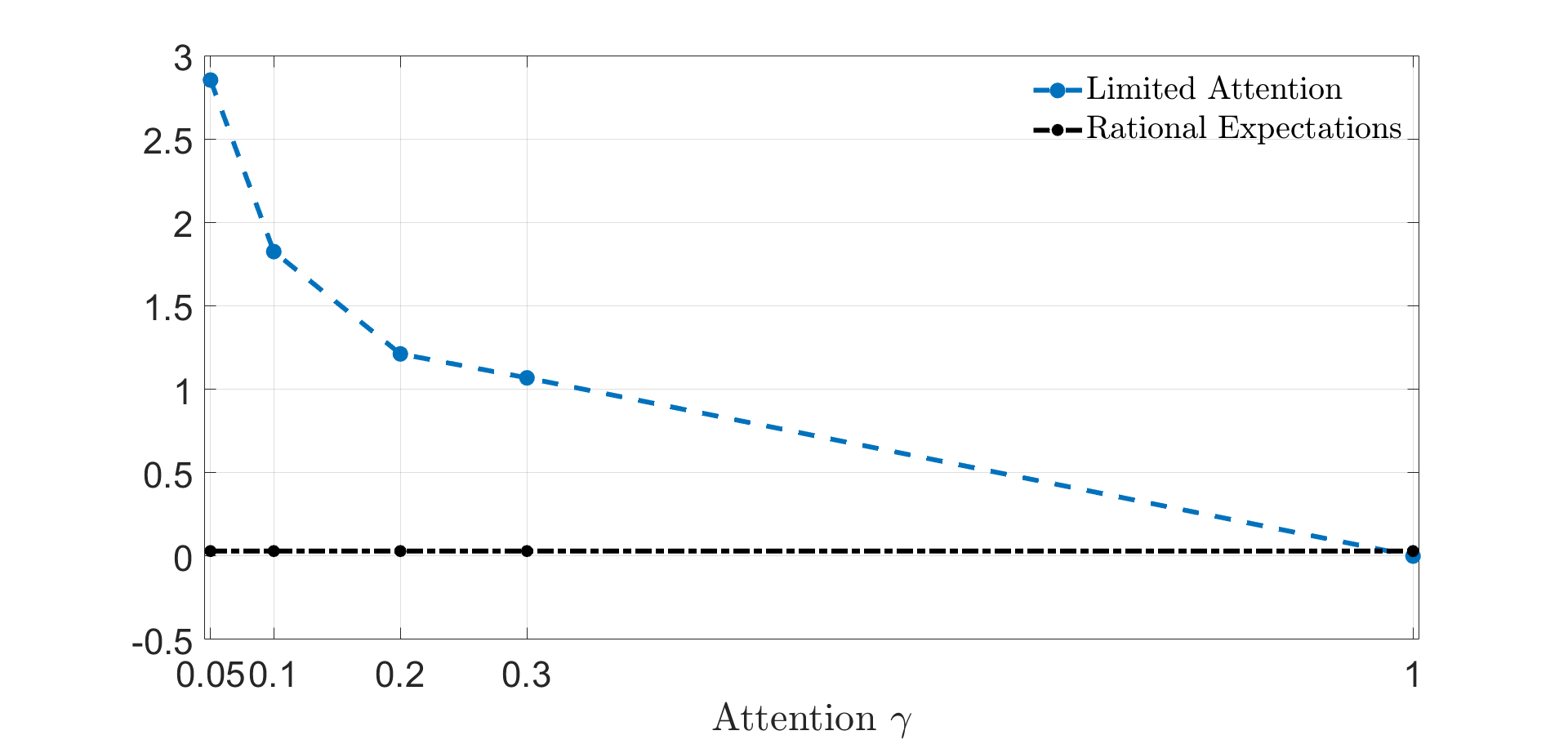

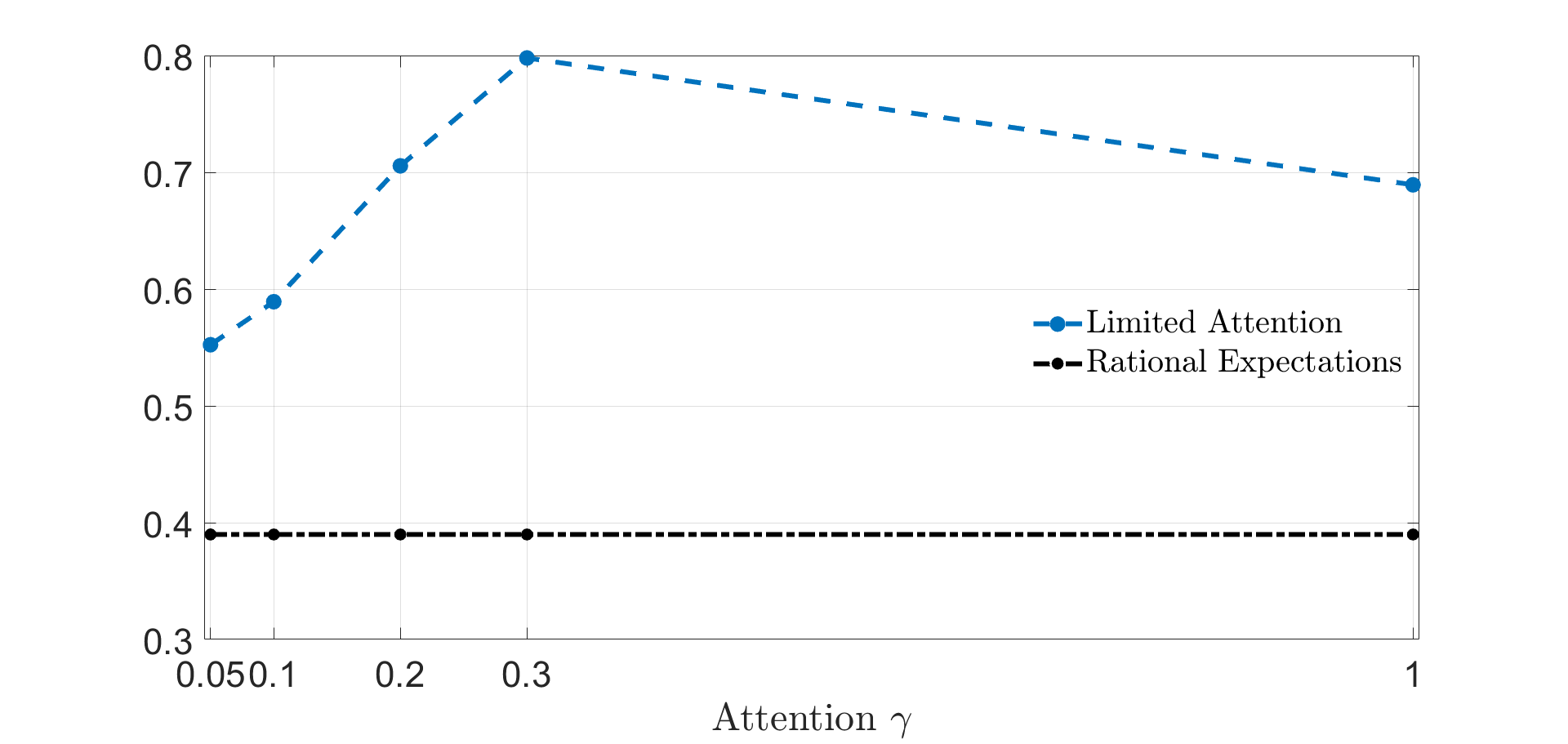

What do low levels of attention imply for inflation volatility and the optimal inflation target? For this, I solve the Ramsey problem for different levels of attention, namely . An attention parameter of 0.3 is close to the estimates for consumers’ attention after 1990, and the lower levels of 0.05 and 0.1 are close to the ones observed since 2010.

| (a) Optimal Inflation Target | (b) Inflation Volatility |

|---|---|

|

|

Notes: This figure shows the average inflation rate under Ramsey optimal policy (left panel) and inflation volatility for different attention levels. The blue-dashed lines show the results for the model under limited attention, and the black-dashed-dotted lines for the rational-expectations model.

Figure 3 shows the results. The average inflation rate under Ramsey optimal policy—what I refer to as the optimal inflation target—is plotted in the left panel and the inflation volatility in the right panel. The blue-dashed lines show the results for the model under limited attention, and the black-dashed-dotted lines for the rational-expectations model. We see that the optimal inflation target increases substantially as attention declines. At the levels of attention estimated just before the Covid crisis, , the inflation target is about 2-3 percentage points higher than under rational expectations due to the discussed ineffectiveness of forward-guidance policies. By increasing the average level of inflation the average nominal interest rate increases and thus makes it less likely that the ELB becomes binding. Indeed, the frequency of a binding ELB decreases substantially. For , the ELB is binding 22% of the time under optimal policy, whereas this value shrinks to 1.4% for an attention level of 0.05.

While lower attention renders forward guidance, make-up policies and other policies that work (partly) through inflation expectations less effective, lower attention also stabilizes inflation, as can be seen from the right panel in Figure 3. First, because lower attention mutes the inflation response to shocks and output (see Proposition 1). Second, the lower ELB frequency further stabilizes the economy. Thus, lower attention to inflation can help stabilizing actual inflation and reduces the number of binding-ELB periods. The lower inflation volatility at lower levels of attention in fact justifies these low attention levels, as optimal attention depends positively on inflation volatility (see Section 2). This low volatility, however, requires an increase in the inflation target, which is costly. Thus, it is not clear a priori whether lower attention leads to welfare gains or not.

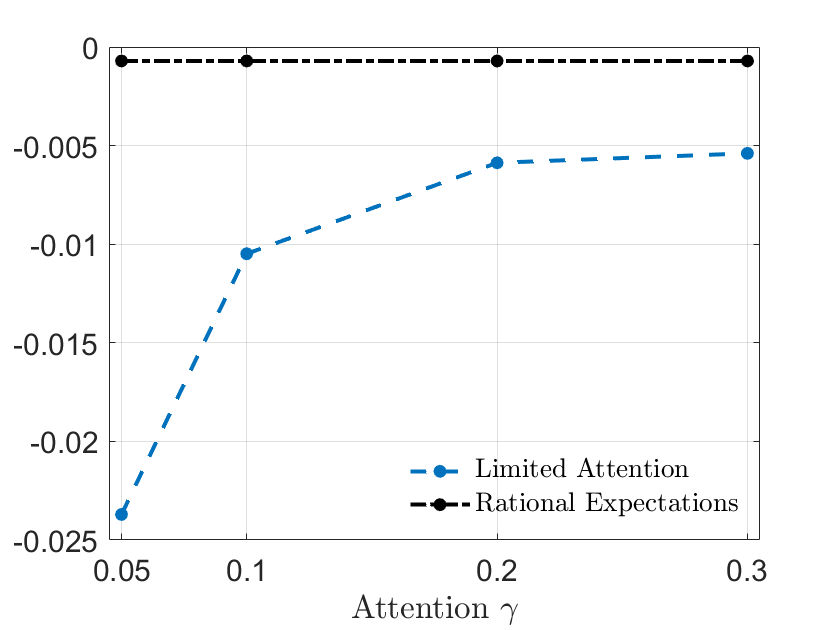

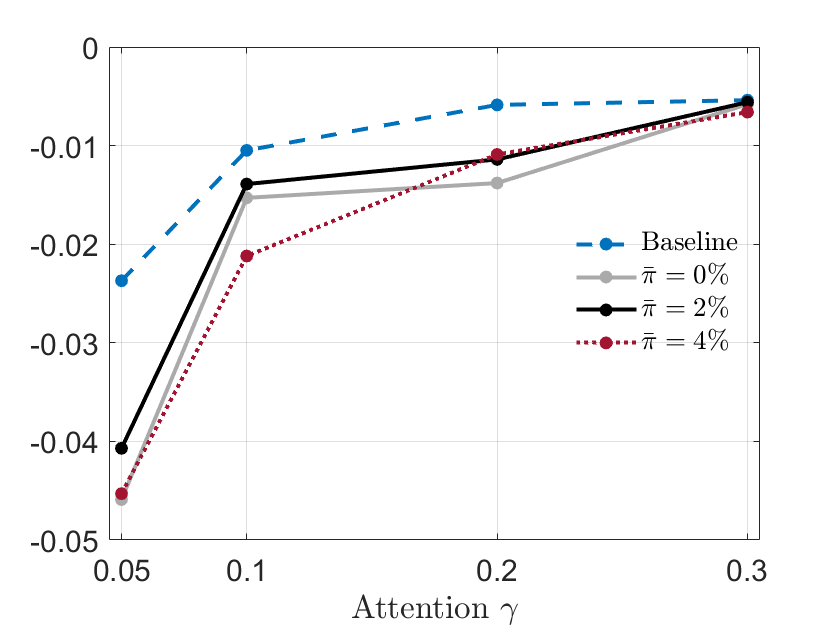

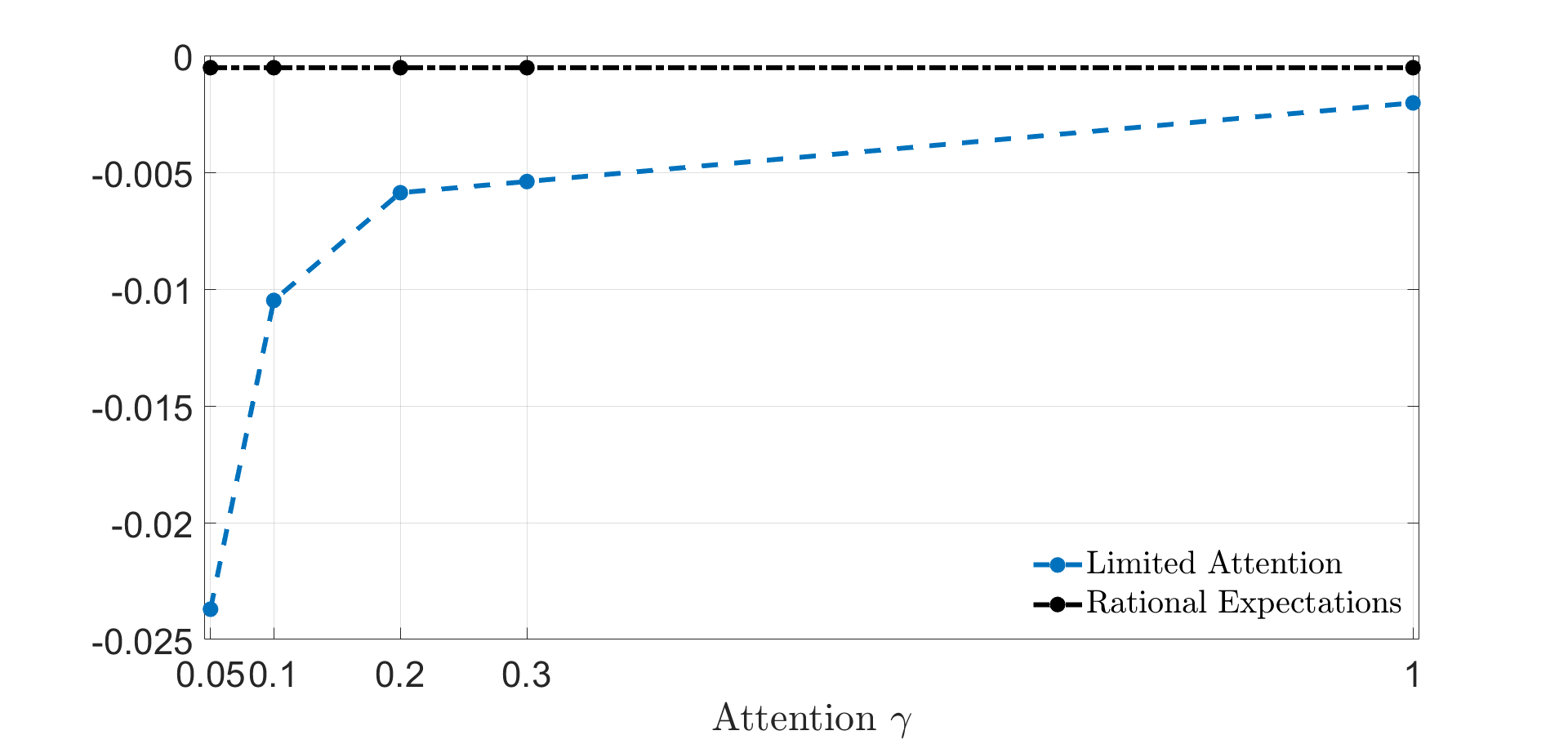

4.2 Welfare

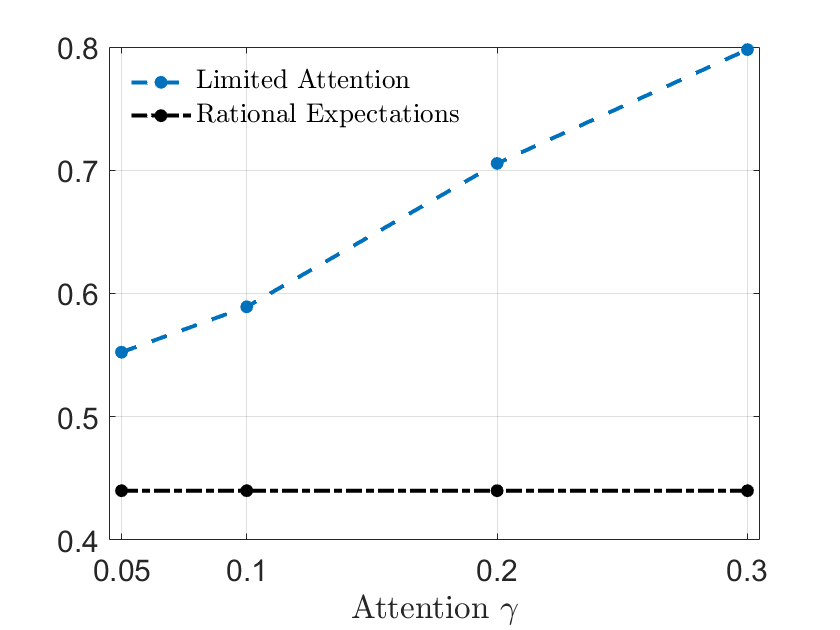

What are the effects of declining attention on overall welfare? Welfare is given by equation (12) and from the previous discussion, we know that lower attention poses a trade off. On the one hand, inflation volatility decreases and the ELB binds less frequently, when attention is low. This raises welfare. On the other hand, lower attention complicates managing inflation expectations and thus, the optimal average level of inflation increases, which is costly. Which effect dominates?

Panel (a) in Figure 4 shows that the cost of the level effect outweighs the stabilization benefits. As attention falls, welfare decreases. This is especially pronounced at low levels of attention, where the optimal inflation target increases substantially (see Figure 3).

| (a) ELB | (b) No ELB |

|---|---|

|

|

Notes: This figure shows welfare (12) under Ramsey optimal policy for different levels of attention. The left panel shows the results for the case with an occasionally-binding ELB, and the right panel without an ELB. The blue-dashed lines show the results for the model under limited attention, and the black-dashed-dotted lines for the rational-expectations model.

Absent the lower-bound constraint, the complications in managing inflation expectations due to limited attention are much less pronounced since managing expectations is particularly important at the lower bound. In fact, lower attention is welfare improving in the case without an ELB. Panel (b) in Figure 4 shows this graphically. The stabilization benefits that arise from lower attention—which is reflected in more anchored expectations—lead to an increase in welfare.

These findings show that accounting for the ELB is crucial for making a normative statement about costs and benefits of stabilizing inflation expectations. The ELB highlights the drawbacks that arise from the stabilization of expectations due to the fall in attention, as the management of expectations becomes particularly relevant when the ELB binds.

4.3 Extensions

In this section, I present several extensions of the baseline model and show that the overall implications derived so far remain robust, even when allowing (i) for a negative ELB, (ii) for non-rational output gap expectations, (iii) for a time-varying slope of the Phillips Curve or with non-zero trend inflation, and (iv) with time-varying attention to inflation. In 4.3.5, I further show that the results are largely driven by the agents’ limited attention rather than by their perceived law of motion.

4.3.1 Negative Interest Rate Policies

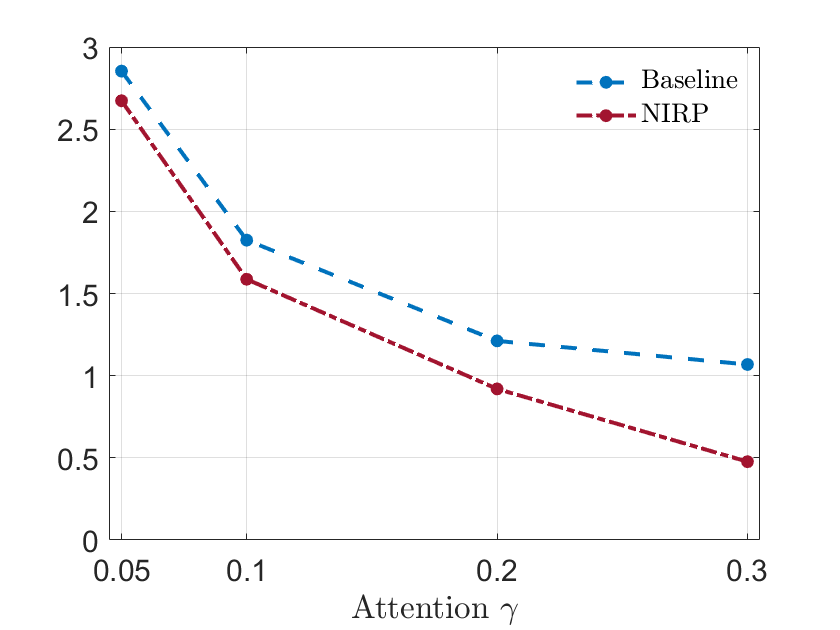

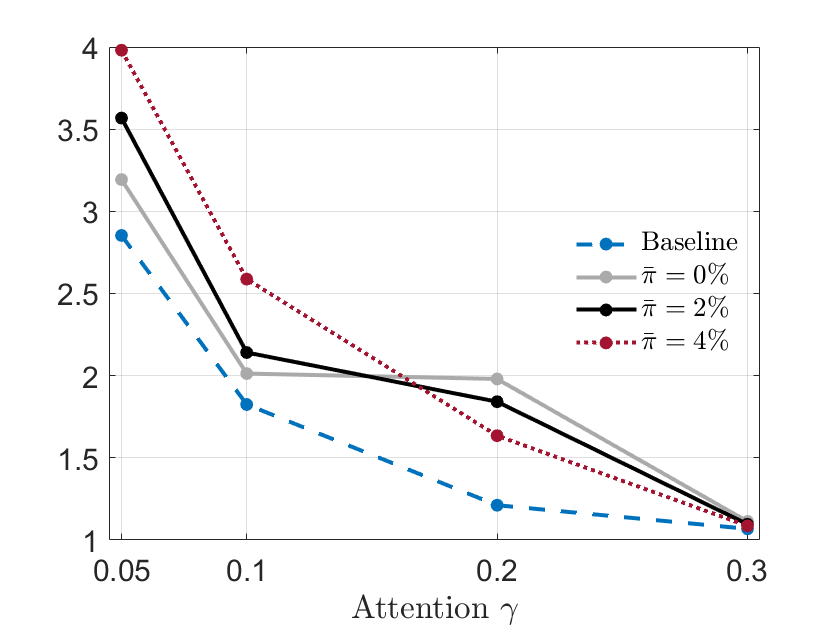

In recent years, several central banks in advanced economies have implemented negative interest rate policies (NIRP).191919See Brandao-Marques et al. (2021) for a recent survey on negative interest rate policies and its effectiveness. Could negative rates limit the negative consequences of declining attention? In order to answer this question, I solve the same Ramsey optimal policy problem as above, but set the effective lower bound to (annualized).

| (a) Optimal Inflation Target | (b) Change in Inflation Target |

|---|---|

|

|

Notes: The left panel shows the average inflation rate under optimal policy for different degrees of attention . The blue-dashed lines show the results for the benchmark model where the lower bound is at 0, and the red-dashed-dotted lines show the results when allowing for negative interest rates up to (annualized). The right panel shows the difference in the optimal inflation targets, defined as , where denotes the optimal inflation target and the superscripts and denote the two cases where the ELB is at or , respectively.

Figure 5 reports the outcomes. Panel (a) shows the optimal inflation target (red-dashed-dotted line) and compares it to the case with an ELB at 0 (blue-dashed line). We see that the additional policy space due to the negative lower bound indeed calls for a lower inflation target. However, the decline in attention also weakens the effectiveness of NIRP. We see this by observing that the optimal inflation target under NIRP gets closer to the one without negative rates as attention declines. To see these gaps clearly, panel (b) shows the difference in the optimal inflation targets, defined as , where denotes the optimal inflation target and the superscripts and denote the two cases where the ELB is at or , respectively. Overall, allowing for negative policy rates can help limiting the drawbacks of low attention but these policies itself become less effective as attention declines.

4.3.2 Non-Rational Output Gap Expectations

So far, I assumed that output gap expectations are fully rational. I now relax this assumption and show that in this case, (i) the optimal inflation target further increases and (ii) non-rational output gap expectations are welfare deteriorating. But before going into these results, I need to quantify people’s attention to the output gap. As expectations about the output gap are not available, I use expectations about unemployment changes over the next year from the Michigan Survey and then estimate attention to unemployment as in Section 2. As I detail in Appendix E.1, I estimate attention to unemployment to have slightly increased from 0.09 to 0.1 from the period before 1990 to the period after 1990. This difference, however, is not statistically significant. Thus, I do not find any evidence for changes in people’s attention to unemployment over the same period in which their attention to inflation decreased.

To understand the monetary policy implications of non-rational output gap expectations in the presence of an ELB, I extend the baseline model by allowing for limited attention to inflation and the output gap. Output gap expectations are given by

| (20) |

As I show in Appendix E.1, limited attention with respect to the output gap exacerbates attention traps. The economy remains stuck at the ELB for longer than in the case of rational expectations and, additionally, inflation, inflation expectations, and now also the output gap stay below their initial values very persistently. The reason for this is that make-up policies, such as forward guidance, not only work through inflation expectations but also through output gap expectations (via the IS equation). When households, however, form their expectations according to (20), output gap expectations become backward looking, which implies that these make-up policies do not stimulate output gap expectations any longer. Thus, the ELB becomes longer lasting.

To prevent these long periods at the ELB, I show in Appendix E.1 that the optimal inflation target becomes even higher than under rational output gap expectations and welfare deteriorates. Higher attention to the output gap serves a similar role as higher attention to inflation: the optimal inflation target is lower and welfare is higher at higher attention levels. These results hold independently of whether attention to inflation is higher than attention to the output gap (which was likely to be the case before the 1990s) or lower (which was the case before the Covid-19 pandemic).

4.3.3 The Role of the Phillips Curve

Ascari and Haber (2022) show that in high-inflation environments, the price level becomes more responsive to monetary policy shocks. Similarly, Alvarez et al. (2019) find that prices are adjusted more frequently in such high-inflation environments (see also Alexandrov (2022)). Thus, by inducing a higher average inflation rate, i.e., by raising the inflation target, the price-setting behavior of firms may change and thus, affect the optimal average inflation rate. To understand the implications of such changes in price-setting behavior, I now extend the analysis along three dimensions. First, I consider the case of a permanently steeper slope of the Phillips Curve, i.e., a higher in equation (7), which may arise due to a lower price adjustment cost. Second, I let the slope of the Phillips Curve to be time-varying, i.e., I model as a function of . Third, I solve for the optimal policy for the case in which trend inflation is positive.202020I use trend inflation and steady-state inflation interchangeably. Table 5 presents the results, which I now discuss in more detail.

| Inflation Target | Welfare | |||

|---|---|---|---|---|

| Baseline | 1.06% | 1.82% | -0.0049 | -0.0096 |

| Higher | ||||

| Fixed | 0.95% | 2.52% | -0.0041 | -0.0173 |

| Higher | 1.02% | 2.98% | -0.0045 | -0.0239 |

| Time-varying | 1.09% | 1.83% | -0.0050 | -0.0097 |

| Positive trend inflation | 1.04% | 2.02% | -0.0029 | -0.0069 |

Notes: This table shows the implications of different Phillips Curve specifications for the optimal inflation target and welfare, for and .

For the first case, I set the slope of the Phillips Curve to a permanently higher level. This may reflect that in an economy with a higher inflation target, and a higher average inflation rate, the cost of adjusting prices is lower. I set to 1.5 times the value I use in my baseline calibration (the baseline calibration sets as in Adam and Billi (2006)). The row in Table 5 labeled Fixed shows the implications of that change for the optimal inflation target and for welfare for the case in which attention to inflation is relatively high () and in which it is relatively low (). The row labeled Higher shows the results for the case in which the welfare weight on the output gap is adjusted accordingly.212121The weight on the output gap is given by , where denotes the price elasticity of demand for the intermediate goods (Adam and Billi, 2006). When comparing it to the baseline calibration (row labeled Baseline), we see that the optimal inflation target and welfare are not much affected in the case of by these changes. In the case of low attention, , however, the optimal inflation target substantially increases by 0.7-1.16 percentage points and welfare decreases. The reason for this increase in the optimal inflation rate is that when the Phillips Curve is steep, fluctuations in the output gap translate into larger changes in inflation. When the economy is pushed to the ELB by adverse demand shocks, output gap decreases and hence, pushes inflation substantially down. Thus, the real rate is relatively high and hence, demand remains low. When attention is low, it takes longer for inflation expectations to recover after such a downturn and the economy remains at or close to the ELB for longer. To prevent this, it is optimal for the central bank to induce a higher inflation rate ex-ante which reduces the likelihood of reaching the ELB in the first place.

In the second case, I allow to be time-varying and to be a function of inflation . In particular, I assume the following functional form:

where I set to my baseline value of 0.057 and set to 0.1. This captures the idea that the Phillips Curve steepens when inflation is high in a reduced form way. The row Time-varying shows that this has barely an effect on the optimal inflation rate and welfare. The optimal inflation rate slightly increases, but the quantitative effects are very small.

In the third case, I allow for non-zero trend inflation (see Appendix C for details on the derivations, which follow Ascari and Rossi (2012)). With Rotemberg price-adjustment costs (Rotemberg, 1982), this gives rise to the aggregate IS equation and Phillips Curve:

where

Following Ascari and Rossi (2012), I set the demand elasticity . Given , this implies a price-adjustment cost parameter .222222In general, there would be an additional term with the expected change of the output gap in the Phillips Curve, but this term drops out in my case, because I set (see Appendix C for details). When trend inflation is zero, , it follows that and , so that we are back to the baseline case analyzed above. Note, that now denotes inflation in deviations from trend inflation (similarly, in the welfare objective (12)). The last row in Table 5 labeled Positive trend inflation shows the policy implications of trend inflation of 0.5%. We see that the optimal inflation rate is barely affected for the case of high attention () but increases slightly at low levels of attention (). However, the increase in the average inflation rate is less than trend inflation.

Overall these results highlight that the main policy implications of my analysis turn out to be robust to accounting for changing price-setting behavior in high-inflation environments: the optimal inflation target is substantially higher under limited attention to inflation and increases as attention falls.

4.3.4 Time-Varying Attention

Up to now, I assumed that attention does not respond to short-term changes in the economy and therefore, compared economies with different degrees of attention but in which attention was time invariant within economy. To analyze how the results change, when attention responds to short-run changes, I impose that attention takes the form

I set to an intermediate value of 0.2 and solve for the optimal policy for the cases and . Table 6 shows that when attention increases with inflation (), the optimal inflation target increases and welfare decreases. In contrast, when attention decreases with inflation (), the optimal inflation rate decreases and welfare increases. When the economy is pushed to the ELB due to an adverse demand shock, inflation decreases. In the case of , attention therefore then decreases as well which implies that inflation expectations tend to be lower for longer, keeping actual inflation low, too. Thus, the economy is likely to stay at the ELB for longer. In order to prevent this, it is therefore optimal to induce a higher average inflation rate which makes the ELB less likely to be binding. However, higher average inflation is costly from a welfare perspective, and hence, welfare is lower in that case. When , the opposite is the case, and therefore, the optimal inflation rate is lower and welfare is higher.

| Inflation Target | Welfare | |

|---|---|---|

| Baseline | 1.20% | -0.0060 |

| 1.32% | -0.0069 | |

| 0.98% | -0.0046 |

Notes: This table shows the implications of time-varying attention to inflation for the optimal inflation target and welfare.

4.3.5 Full Attention

There are two main assumptions underlying the law of motion of inflation expectations (9). First, the assumption that agents perceive inflation to follow an AR(1) process. Second, that paying attention to inflation is costly and thus, their attention is limited. To disentangle these two effects, Figure 15 in Appendix E.5 shows the implications of shutting down the second channel, i.e., if we set . Put differently, how much of the results in previous sections is solely due to the misperception of the law of motion of inflation? Panel (a) shows that the optimal average inflation rate is practically identical to the one under rational expectations. Thus, as argued above, it is really the lack of attention that pushes up the optimal inflation rate, whereas the assumption of a misperceived law of motion is rather innocuous from this perspective.

Panel (b) in Figure 15 reports the inflation volatility under Ramsey optimal policy for different levels of attention, including the full attention case, . Inflation is substantially more volatile than under rational expectations. Thus, while the misperception of the law of motion of inflation is rather inconsequential for the optimal inflation target, it predicts a higher inflation volatility. Indeed, there is a trade-off. On the one hand, higher attention increases the response of inflation to shocks. On the other hand, if agents are fully attentive, inflation also reacts more strongly to changes in expected future output. Thus, to achieve a certain effect on today’s inflation rate, the policymaker is required to make smaller promises about its policies in the future which in turn stabilizes inflation and output already today. While the first channel dominates at lower levels of , the second effect pushes inflation volatility down at higher levels of .

Finally, panel (c) in Figure 15 shows the welfare implications of the misperceived law of motion. Welfare is slightly more negative when agents have a misperceived law of motion of inflation compared to fully rational agents. Given the results in panels (a) and (b), we see that these additional welfare losses are mainly due to increased inflation volatility rather than its level.

5 Conclusion

With the stabilization of inflation in advanced economies since the Great Inflation period, inflation has become less important in people’s lives. In this paper, I quantify this using a limited-attention model of inflation expectations. In line with this model, I show that attention to inflation decreased together with inflation volatility and inflation persistence since the 1970s. Especially in the period between 2010 and 2020, the general public’s attention to inflation was close to zero.

For monetary policy the decline in attention was desirable at first, since lower attention stabilizes inflation expectations and hence, stabilizes actual inflation. With the outbreak of the Great Recession and nominal rates at their lower bound, however, managing inflation expectations became a central tool for monetary policy. But managing inflation expectations is difficult when people are inattentive.

The optimal policy response is a substantial increase in the inflation target. This increases the average nominal rate and thus, binding ELB periods become less likely. The cost of this increase in inflation, however, outweighs the stabilization benefits of lower attention. Lower attention, therefore, decreases welfare if we account for the lower bound. This stands in stark contrast to the case without an ELB in which case lower attention leads to welfare gains through the stabilization of inflation expectations and inflation. My paper thus shows that accounting for the ELB is crucial when assessing the role of the public’s attention to inflation.

References

- Adam (2007) Adam, K. (2007): “Optimal monetary policy with imperfect common knowledge,” Journal of Monetary Economics, 54, 267–301.

- Adam and Billi (2006) Adam, K. and R. M. Billi (2006): “Optimal monetary policy under commitment with a zero bound on nominal interest rates,” Journal of Money, Credit and Banking, 1877–1905.

- Adam and Padula (2011) Adam, K. and M. Padula (2011): “Inflation dynamics and subjective expectations in the United States,” Economic Inquiry, 49, 13–25.

- Adam et al. (2022) Adam, K., O. Pfäuti, and T. Reinelt (2022): “Subjective Housing Price Expectations, Falling Natural Rates and the Optimal Inflation Target,” Working paper.

- Afrouzi et al. (2023) Afrouzi, H., S. Y. Kwon, A. Landier, Y. Ma, and D. Thesmar (2023): “Overreaction in expectations: Evidence and theory,” The Quarterly Journal of Economics.

- Afrouzi and Yang (2021) Afrouzi, H. and C. Yang (2021): “Dynamic Rational Inattention and the Phillips Curve,” Working paper.

- Alexandrov (2022) Alexandrov, A. (2022): “The Effects of Trend Inflation on Aggregate Dynamics and Monetary Stabilization,” Working paper.

- Alvarez et al. (2019) Alvarez, F., M. Beraja, M. Gonzalez-Rozada, and P. A. Neumeyer (2019): “From hyperinflation to stable prices: Argentina’s evidence on menu cost models,” The Quarterly Journal of Economics, 134, 451–505.

- Andrade et al. (2019) Andrade, P., J. Galí, H. Le Bihan, and J. Matheron (2019): “The Optimal Inflation Target and the Natural Rate of Interest,” Brookings Papers on Economic Activity, 2019(2), 173–255.

- Angeletos et al. (2021) Angeletos, G.-M., Z. Huo, and K. A. Sastry (2021): “Imperfect macroeconomic expectations: Evidence and theory,” NBER Macroeconomics Annual, 35, 1–86.

- Angeletos and Lian (2018) Angeletos, G.-M. and C. Lian (2018): “Forward guidance without common knowledge,” American Economic Review, 108, 2477–2512.

- Ascari and Haber (2022) Ascari, G. and T. Haber (2022): “Non-linearities, state-dependent prices and the transmission mechanism of monetary policy,” The Economic Journal, 132, 37–57.

- Ascari and Rossi (2012) Ascari, G. and L. Rossi (2012): “Trend inflation and firms price-setting: Rotemberg versus Calvo,” The Economic Journal, 122, 1115–1141.

- Ball et al. (2005) Ball, L., N. G. Mankiw, and R. Reis (2005): “Monetary policy for inattentive economies,” Journal of Monetary Economics, 52, 703–725.

- Benati (2008) Benati, L. (2008): “Investigating inflation persistence across monetary regimes,” The Quarterly Journal of Economics, 123, 1005–1060.

- Benigno and Paciello (2014) Benigno, P. and L. Paciello (2014): “Monetary policy, doubts and asset prices,” Journal of Monetary Economics, 64, 85–98.

- Bhandari et al. (2022) Bhandari, A., J. Borovička, and P. Ho (2022): “Survey data and subjective beliefs in business cycle models,” Working paper.

- Blundell and Bond (1998) Blundell, R. and S. Bond (1998): “Initial conditions and moment restrictions in dynamic panel data models,” Journal of Econometrics, 87, 115–143.

- Bracha and Tang (2023) Bracha, A. and J. Tang (2023): “Inflation levels and (in) attention,” Working Paper.

- Brandao-Marques et al. (2021) Brandao-Marques, L., M. Casiraghi, G. Gelos, G. Kamber, R. Meeks, et al. (2021): “Negative interest rates: Taking stock of the experience so far,” IMF Departmental Papers, 3.

- Candia et al. (2021) Candia, B., O. Coibion, and Y. Gorodnichenko (2021): “The Inflation Expectations of US Firms: Evidence from a New Survey,” Working paper.

- Canova (2007) Canova, F. (2007): “G-7 inflation forecasts: Random walk, Phillips curve or what else?” Macroeconomic Dynamics, 11, 1.

- Carroll (2003) Carroll, C. D. (2003): “Macroeconomic expectations of households and professional forecasters,” the Quarterly Journal of economics, 118, 269–298.

- Cavallo et al. (2017) Cavallo, A., G. Cruces, and R. Perez-Truglia (2017): “Inflation expectations, learning, and supermarket prices: Evidence from survey experiments,” American Economic Journal: Macroeconomics, 9, 1–35.

- Clarida et al. (1999) Clarida, R., J. Galí, and M. Gertler (1999): “The Science of Monetary Policy: Evidence and Some Theory,” Journal of Economic Literature, 37, 1661–1707.

- Coibion and Gorodnichenko (2012) Coibion, O. and Y. Gorodnichenko (2012): “What can survey forecasts tell us about information rigidities?” Journal of Political Economy, 120, 116–159.

- Coibion and Gorodnichenko (2015a) ——— (2015a): “Information rigidity and the expectations formation process: A simple framework and new facts,” American Economic Review, 105, 2644–78.

- Coibion and Gorodnichenko (2015b) ——— (2015b): “Is the Phillips curve alive and well after all? Inflation expectations and the missing disinflation,” American Economic Journal: Macroeconomics, 7, 197–232.

- Coibion et al. (2023) Coibion, O., Y. Gorodnichenko, E. S. Knotek, and R. Schoenle (2023): “Average inflation targeting and household expectations,” Journal of Political Economy Macroeconomics, 1, 403–446.

- Coibion et al. (2022) Coibion, O., Y. Gorodnichenko, and M. Weber (2022): “Monetary policy communications and their effects on household inflation expectations,” Journal of Political Economy, 130, 1537–1584.

- Coibion et al. (2012) Coibion, O., Y. Gorodnichenko, and J. Wieland (2012): “The optimal inflation rate in New Keynesian models: should central banks raise their inflation targets in light of the zero lower bound?” Review of Economic Studies, 79, 1371–1406.

- Constancio (2015) Constancio, V. (2015): “Understanding inflation dynamics and monetary policy,” in Speech at the Jackson Hole Economic Policy Symposium, vol. 29.

- Del Negro et al. (2020) Del Negro, M., M. Lenza, G. E. Primiceri, and A. Tambalotti (2020): “What’s up with the Phillips Curve?” Working paper.

- D’Acunto et al. (2022) D’Acunto, F., D. Hoang, and M. Weber (2022): “Managing households’ expectations with unconventional policies,” The Review of Financial Studies, 35, 1597–1642.

- Eggertsson and Woodford (2003) Eggertsson, G. and M. Woodford (2003): “The Zero Interest-Rate Bound and Optimal Monetary Policy,” Brookings Papers on Economic Activity, (1), 139–211.

- Faust and Wright (2013) Faust, J. and J. H. Wright (2013): “Forecasting inflation,” in Handbook of economic forecasting, Elsevier, vol. 2, 2–56.

- Fulton and Hubrich (2021) Fulton, C. and K. Hubrich (2021): “Forecasting US inflation in real time,” Econometrics, 9, 36.

- Gabaix (2019) Gabaix, X. (2019): “Behavioral inattention,” in Handbook of Behavioral Economics: Applications and Foundations 1, Elsevier, vol. 2, 261–343.

- Gabaix (2020) ——— (2020): “A behavioral New Keynesian model,” American Economic Review, 110, 2271–2327.

- Galí (2015) Galí, J. (2015): Monetary policy, inflation, and the business cycle: an introduction to the new Keynesian framework and its applications, Princeton University Press.

- Gáti (2022) Gáti, L. (2022): “Monetary Policy & Anchored Expectations An Endogenous Gain Learning Model,” Working paper.

- Hamilton (1994) Hamilton, J. D. (1994): Time series analysis, Princeton university press.

- Jørgensen and Lansing (2023) Jørgensen, P. L. and K. J. Lansing (2023): “Anchored Inflation Expectations and the Slope of the Phillips Curve,” .

- Jurado (2023) Jurado, K. (2023): “Rational inattention in the frequency domain,” Journal of Economic Theory, 208, 105604.

- Korenok et al. (2022) Korenok, O., D. Munro, and J. Chen (2022): “Inflation and attention thresholds,” Working paper.

- Lamla and Lein (2014) Lamla, M. J. and S. M. Lein (2014): “The role of media for consumers’ inflation expectation formation,” Journal of Economic Behavior & Organization, 106, 62–77.

- Link et al. (2023) Link, S., A. Peichl, C. Roth, and J. Wohlfart (2023): “Attention to the Macroeconomy,” Working Paper.

- Maćkowiak et al. (2018) Maćkowiak, B., F. Matějka, and M. Wiederholt (2018): “Dynamic rational inattention: Analytical results,” Journal of Economic Theory, 176, 650–692.

- Maćkowiak et al. (2023) ——— (2023): “Rational inattention: A review,” Journal of Economic Literature, 61, 226–273.

- Mackowiak and Wiederholt (2009) Mackowiak, B. and M. Wiederholt (2009): “Optimal sticky prices under rational inattention,” American Economic Review, 99, 769–803.

- Mankiw and Reis (2002) Mankiw, N. G. and R. Reis (2002): “Sticky information versus sticky prices: a proposal to replace the New Keynesian Phillips curve,” The Quarterly Journal of Economics, 117, 1295–1328.

- Marcet and Marimon (2019) Marcet, A. and R. Marimon (2019): “Recursive contracts,” Econometrica, 87, 1589–1631.

- Matějka and McKay (2015) Matějka, F. and A. McKay (2015): “Rational inattention to discrete choices: A new foundation for the multinomial logit model,” American Economic Review, 105, 272–98.

- Newey and West (1987) Newey, W. K. and K. D. West (1987): “A Simple, Positive Semi-Definite, Heteroskedasticity and Autocorrelation,” Econometrica, 55, 703–708.

- Nickell (1981) Nickell, S. (1981): “Biases in dynamic models with fixed effects,” Econometrica: Journal of the econometric society, 1417–1426.

- Paciello and Wiederholt (2014) Paciello, L. and M. Wiederholt (2014): “Exogenous information, endogenous information, and optimal monetary policy,” Review of Economic Studies, 81, 356–388.

- Pfajfar and Santoro (2013) Pfajfar, D. and E. Santoro (2013): “News on inflation and the epidemiology of inflation expectations,” Journal of Money, Credit and Banking, 45, 1045–1067.

- Pfäuti (2023) Pfäuti, O. (2023): “The Inflation Attention Threshold and Inflation Surges,” arXiv preprint arXiv:2308.09480.

- Pfäuti and Seyrich (2022) Pfäuti, O. and F. Seyrich (2022): “A behavioral heterogeneous agent New Keynesian model,” Working Paper.

- Rotemberg (1982) Rotemberg, J. J. (1982): “Sticky Prices in the United States,” Journal of Political Economy, 90, 1187–1211.

- Sims (2003) Sims, C. A. (2003): “Implications of rational inattention,” Journal of Monetary Economics, 50, 665–690.

- Vellekoop and Wiederholt (2019) Vellekoop, N. and M. Wiederholt (2019): “Inflation expectations and choices of households,” Working paper.

- Weber et al. (2023) Weber, M., S. Sheflin, T. Ropele, R. Lluberas, S. Frache, B. Meyer, S. Kumar, Y. Gorodnichenko, D. Georgarakos, O. Coibion, et al. (2023): “Tell Me Something I Don’t Already Know: Learning in Low and High-Inflation Settings,” Working Paper.

- Wiederholt (2015) Wiederholt, M. (2015): “Empirical properties of inflation expectations and the zero lower bound,” Working paper.

- Woodford (2003) Woodford, M. (2003): “Interest and prices,” Princeton University Press, Princeton, NJ.

Online Appendix

Appendix A A Limited-Attention Model of Inflation Expectations

In this section, I derive the expectations-formation process under limited attention sketched in Section 2. The agent believes that (demeaned) inflation tomorrow, , depends on (demeaned) inflation today, , as follows

where denotes the perceived persistence of inflation and . Inflation in the current period is unobservable, so before forming an expectation about future inflation, the agent needs to form an expectation about today’s inflation. I denote this nowcast , and the resulting forecast about next period’s inflation . Given her beliefs, the full-information forecast is

But since is not perfectly observable, the actual forecast will deviate from the full-information forecast. Deviating, however, is costly, as this causes the agent to make mistakes in her decisions.

The agent’s choice is not only about how to form her expectations given certain information, but about how to choose this information optimally, while taking into account how this will later affect her forecast. That is, she chooses the form of the signal she receives about current inflation. Since acquiring information is costly, it cannot be optimal to acquire different signals that lead to an identical forecast. Due to this one-to-one relation of signal and forecast, we can directly work with the joint distribution of and , , instead of working with the signal.

Let denote the negative of the loss that is incurred when the agent’s forecast deviates from the forecast under full information, and the cost of information. Then, the agent’s problem is given by

| (21) | ||||

| subject to |

where is the agent’s prior, which is assumed to be Gaussian; . is the cost function that captures how costly information acquisition is. It is linear in mutual information , i.e., the expected reduction in entropy of due to knowledge of :

where is the entropy of and is a parameter that measures the cost of information.

The objective function is assumed to be quadratic:

where measures the stakes of making a mistake.232323A quadratic loss function is usually derived from a second-order approximation of the household’s utility function or the firm’s profit function (see, e.g., Mackowiak and Wiederholt (2009)).,242424These stakes (or also the information cost parameter ) can be interpreted as a way to incorporate other variables to which the agent might pay attention. For example, a household might not only want to forecast inflation but also her own income stream going forward. In this case, a smaller could capture an increase in her idiosyncratic income volatility. Thus, paying attention to inflation is relatively less beneficial, as the relative importance of her idiosyncratic income increases. Such an interpretation also explains why professional forecasters might not be fully informed about inflation, given that they usually forecast a whole array of variables.

In this setup, Gaussian signals are optimal (and in fact the unique solution, see Matějka and McKay (2015)). The optimal signal thus has the form

with .252525In this case, the entropy becomes , where is the variance of . Note, that here denotes the number “pi” and not inflation. The problem (21) now reads

| (22) |

The optimal forecast is given by , and Bayesian updating implies

| (23) |

where measures how much attention the agent pays to inflation, and denotes the prior mean of .

Appendix B Appendix to Empirical Results

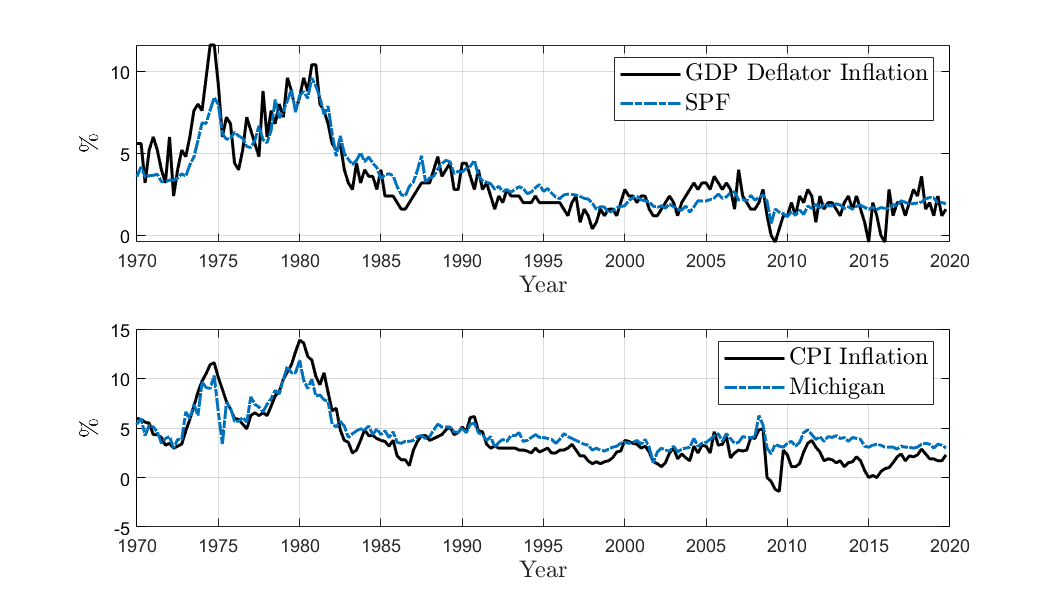

Figure 6 shows the main time series that are used in the empirical analyses of Section 2. Apart from the apparent decrease in the level and volatility of inflation as well as inflation expectations, we see that expectations became more and more detached from actual inflation. First, consumer expectations seem to be biased on average in the most recent decades, as can be seen in the lower panel. While these expectations closely tracked inflation in the 70s and 80s, this is not the case anymore.262626In the empirical analysis I account for this mean bias by including an intercept in the regressions. Second, professional forecasters’ expectations seem to perform quite well on average. In the last twenty years, however, they barely react to actual changes in inflation anymore. Overall, these observations suggest that attention decreased in the last decades.

Note: This figure shows the raw time series of inflation, as well as survey expectations about future inflation. Everything is in annualized percentages.

Table 7 shows the summary statistics, for the period before and after the 1990s, separately. For professional forecasters, the perceived persistence is higher than the actual one. This is especially the case when the actual persistence is relatively low, as was the case after 1990. Afrouzi et al. (2023) document a similar finding in an experimental setting. This might point towards lower attention since the 1990s. Note, that in the empirical analysis I account for changes in the perceived persistence.

| GDP Deflator Inflation | SPF Expectations | |||

| 1968-1990 | 1990-2020 | 1968-1990 | 1990-2020 | |

| Mean | ||||

| Std. Dev. | ||||

| Persistence | 0.84 | 0.55 | 0.93 | 0.92 |

| CPI Inflation | Consumer Expectations | |||

| 1968-1990 | 1990-2020 | 1968-1990 | 1990-2020 | |

| Mean | 6.09 | 2.42 | 6.00 | 3.62 |

| Std. Dev. | 3.00 | 1.26 | 2.17 | 0.68 |

| Persistence | 0.96 | 0.77 | 0.85 | 0.70 |

Note: This table shows the summary statistics of the data. The upper panel shows the statistics for the quarter-on-quarter GDP deflator inflation (left) and the corresponding inflation expectations from the Survey of Professional Forecasters (right). The lower panel shows the year-on-year CPI inflation (left) and the corresponding inflation expectations from the Survey of Consumers from the University of Michigan. All data are annualized.

B.1 Robustness and Additional Evidence

In this section, I show that the empirical results are robust along several dimensions.

Additional Data Sources