Consistent estimation of distribution functions

under increasing concave and convex stochastic ordering

Abstract

A random variable is said to be smaller than in the increasing concave stochastic order if for all increasing concave functions for which the expected values exist, and smaller than in the increasing convex order if for all increasing convex . This article develops nonparametric estimators for the conditional cumulative distribution functions of a response variable given a covariate , solely under the assumption that the conditional distributions are increasing in in the increasing concave or increasing convex order. Uniform consistency and rates of convergence are established both for the -sample case and for continuously distributed .

1 Introduction

The nonparametric estimation of distribution functions under stochastic order restrictions is a classical problem in statistics. It can be formulated very generally as the task to estimate the conditional distributions of a random variable given a covariate , solely under the assumption that these distributions are increasing in a certain stochastic order. The classical and best understood order is first order stochastic dominance, requiring that the conditional cumulative distribution functions (CDFs) are decreasing in for every fixed . Brunk et al., (1966) were the first to consider this constrained estimation problem in the two sample case . Almost 40 years later, El Barmi and Mukerjee, (2005) have described an estimator for taking discrete ordered values, say, , and again after more than a decade, Mösching and Dümbgen, 2020b extended it to continuously distributed . In a further leap of complexity, Henzi et al., 2021c have shown that consistent estimation under first order stochastic dominance is even possible with partially ordered covariates . Stronger orders considered in the literature are the uniform stochastic ordering and the likelihood ratio order, see El Barmi and Mukerjee, (2016) and Mösching and Dümbgen, 2020a and the references therein. A weaker constraint is stochastic precedence (Arcones et al.,, 2002), and a structurally different stochastic order is the peakedness order, where the variability of the conditional distributions of around a center is increasing in the covariate (Rojo and Batún-Cutz,, 2007; El Barmi and Mukerjee,, 2012; El Barmi and Wu,, 2017). A common attractive feature of all these order restricted estimators is that they do not require the specification of tuning parameters, and automatically adapt to the smoothness of the underlying functions that are estimated, such as in Mösching and Dümbgen, 2020b (, Theorems 3.3 and 3.4).

So far, the main efforts in developing estimators under stochastic order restrictions have been focused on first order stochastic dominance and stronger orders, and consistency results in the case of continuously distributed have only been derived for first order stochastic dominance. This is a limitation insofar as these orders require the conditional CDFs to be decreasing in for all fixed . In particular, the CDFs for different values of are not allowed to cross, which in practice often happens in the tails when the variability of increases (or decreases) with . The purpose of this article is to develop consistent estimators under the increasing concave and increasing convex stochastic order, which are weaker orders applicable in situations where first order stochastic dominance is not appropriate. Estimation under the increasing concave order has been studied before by Rojo and El Barmi, (2003) and El Barmi and Marchev, (2009) in the two-sample case . In this article, an estimator generalizing the one by El Barmi and Marchev, (2009) to the -sample case and continuously distributed is proposed, and uniform consistency and rates of convergence are established.

For two random variables and with finite expected values, is said to be smaller in the increasing concave order than if for all increasing concave functions for which the expectations exist. Similarly, is smaller than in the increasing convex order if for all increasing convex functions , which is equivalent to being smaller than in the increasing concave order. In the following, these orders are abbreviated as and , respectively, and and are both used as orders on random variables and on their CDFs. Another characterization (see Shaked and Shanthikumar,, 2007, Chapter 4) for the increasing concave order is

where , and and are the CDFs of and , respectively. For the increasing convex order, the analogous condition reads as

A useful sufficient condition for the increasing concave order is that the CDFs and cross at a single point with for and for , or with the reverse inequalities for the CDFs in case of the increasing convex order. The increasing concave order is well-known in economics as second order stochastic dominance, with “second order” referring to the fact that monotonicity is required for the integrated CDFs and not for the CDFs themselves. If and are portfolio returns, then means that all individuals with increasing concave utility functions , i.e. all risk-averse utility maximizers, prefer over . In the literature on finance and insurance, the increasing convex order appears under the name stop-loss order, a term introduced by Goovaerts et al., (1982) referring to the characterization , which states that the expected stop-loss of over any retention limit exceeds the stop-loss of . This suggests using as an order for comparing risks.

In the economics and finance literature, research has so far mainly been focused on developing tests for verifying if conditional distributions satisfy - or -order constraints, rather than using these orders as restrictions for estimating distributions. Baringhaus and Gruebel, (2009), Berrendero and Cárcamo, (2011), and Donald and Hsu, (2016) develop methods for the two-sample case; see the references in these articles for earlier works on the two-sample testing problem. The -sample case has been addressed by Linton et al., (2005) and Zhang and Zhang, (2015). The test by Linton et al., (2005), which covers first, second and higher order stochastic dominance, allows for dependency among the observations and also adjustment by covariates. Zhang and Zhang, (2015) assume independent data and apply an isotonic regression estimator corresponding to the intermediate estimator in Section 2 of this article. For a continuous covariate, Hsu et al., (2019) and Chetverikov et al., (2021) propose more general tests of monotonicity, which are also applicable to testing higher order stochastic dominance.

If one detaches the increasing concave (convex) order from its economic interpretation, then it can be viewed as an order relation where increases with , but its variability decreases (increases). More precisely, if and only if there exists a variable such that and , where and denote first order stochastic dominance and the convex order, respectively. The latter is a variability order requiring that for all convex functions such that the expectations exist (see Shaked and Shanthikumar,, 2007, Chapter 3 and Theorem 4.A.6). For the increasing convex order, one has instead of . With this broader perspective, one can find practical situations where the - and -order arise as natural constraints. For example, Vittorietti et al., (2021) perform a study in materials science, where intuition about physical properties suggests a model with and for measurements of a certain outcome in different types of materials. This model, also studied by Shi, (1994), satisfies the increasing concave order, and the methodology in this article provides an alternative nonparametric method for estimating the conditional distributions in their applications. Another application where the - and -order may be useful is the post-processing of point forecasts. Following Henzi et al., 2021c , if is a point forecast for an outcome variable , say, an expert’s inflation forecast, then one would expect that attains higher values as increases. Henzi et al., 2021c suggest to quantify the uncertainty of by estimating the conditional CDFs on training data under the assumption that they are increasing in first order stochastic dominance in . This is plausible for many variables with right-skewed distribution, such as accumulated precipitation (Henzi et al., 2021c, ) or patient length of stay (Henzi et al., 2021b, ; Henzi et al., 2021a, ). But the assumption may fail to hold in situations where the variability of strongly changes with . The case study in Section 6 presents an example with income expectations, where such an effect can be observed and the -order provides a more plausible constraint than first order stochastic dominance.

2 Estimation

To avoid redundancy, only the estimation for the increasing concave order is presented here; the necessary adaptations for the increasing convex order are straightforward. Let be covariate-observation pairs based on which the conditional distributions are to be estimated. In the literature on estimation under stochastic order restrictions, the CDFs are often only estimated at the distinct values of and and of , and frequently used estimation methods are nonparametric maximum likelihood estimation (NPLME) (e.g. in Dykstra et al.,, 1991; Mösching and Dümbgen, 2020a, ) and monotone least squares regression (e.g. in El Barmi and Mukerjee,, 2005; Mösching and Dümbgen, 2020b, ). However, these two approaches turn out to be unrewarding in the case of the increasing concave order. Firstly, they lead to a constrained optimization problem with variables in general, namely the estimators for , which is not efficiently solvable for large . And secondly, for the -constrained estimator, proving consistency using the definition of the estimator as maximizer of the likelihood or least squares estimator seems intractable. The construction here is therefore an indirect approach. For , define

Under the assumption that if , the quantities should be decreasing in for all fixed , and they satisfy

This suggests that an estimator for may yield, under some conditions, an estimator for . We restrict the estimation of to ; in Section 3, it is shown that under a continuity assumption, any interpolation method to obtain estimates for is sufficient for uniform consistency.

Since equals the expected value , a reasonable estimator for it is the antitonic least squares regression of with covariates , that is,

The order constraints enforce if , so the above problem is equivalent to the reduced, weighted antitonic regression

where , , and

This antitonic regression has the min-max-representation

| (1) |

see Equations (1.9)-(1.13) of Barlow et al., (1972). In principle, one could now try to estimate by taking the right-sided derivative of at . However, is not necessarily convex and therefore its derivative may be decreasing and not a CDF. To correct this, let be the greatest convex minorant to the function , which is the pointwise greatest convex function bounded by from above, and define as the right-hand slope of at . The following proposition, which is a consequence of the above min-max-formula and basic properties of greatest convex minorants, shows that this is a valid strategy. Its proof, and the proofs of all subsequent theoretical results, are deferred to the appendix.

Proposition 2.1.

-

(i)

The functions and are increasing and piecewise linear in for fixed , and decreasing in for fixed .

-

(ii)

The functions for fixed are piecewise constant CDFs with for and for .

In practice, it is not possible to compute and at all . Although these functions are piecewise linear, there is no efficient procedure to identify the knots where their slope changes. A pragmatic solution is to evaluate and on a fine grid with and , and interpolate linearly in between. This has the consequence that the CDFs can only put mass on . By a standard result about isotonic regression (see Appendix A), the right-sided slope of the greatest convex minorant to the interpolation of equals the isotonic regression of the slopes

with weights , . This isotonic regression directly yields the estimators for the conditional CDFs,

and by Proposition 2.1 (ii) if . To summarize, the estimation procedure consists of two series of monotone regressions, informally speaking one in the -direction for fixed threshold to obtain -ordered distributions, and another in the -direction for fixed covariate to ensure that the CDFs are increasing. It is not necessary to compute the functions explicitly, since the computation of the greatest convex minorant is indirect via its right-hand slope. The exact solution of monotone regression problems can be obtained efficiently with the Pool-Adjacent Violators Algorithm (PAVA), which has complexity with sorted covariate and sample size . Hence the overall complexity of the estimation procedure is if the number of distinct values in or grows at the rate .

If the distinct values of are taken as the grid for computation, then the estimated distributions can only put mass on the actual observations in the data, and they are equal to the conditional empirical cumulative distribution functions (ECDF) if these already satisfy the increasing concave order condition. That is, if is the ECDF of all with and if , then for . If in addition are pairwise distinct, is the Dirac measure at for . The estimators under first order stochastic dominance (El Barmi and Mukerjee,, 2005; Mösching and Dümbgen, 2020b, ) also have this property. However, with the increasing concave order, even if the grid contains , the estimator can put probability mass on points outside of . In particular, if the response variable is known to take values in a discrete set, say , then the grid should be chosen within this set to avoid positive estimated probabilities outside of the actual support.

The increasing concave order is preserved under pointwise convex combinations of CDFs, i.e. if and , then also for . This fact opens the possibility to combine the estimation procedure with sample splitting as suggested in Henzi et al., 2021c for first order stochastic dominance. Instead of estimating the conditional distributions with the complete dataset, one may draw random subsamples from the data and aggregate the estimated conditional CDFs from each run by their pointwise average. This subsample aggregation (subagging) yields smoother estimated CDFs and prevents overfitting. Alternatively, the data can also be partitioned into several disjoint subsets instead of drawing subsamples, and Banerjee et al., (2019) have proved that this divide and conquer strategy may lead to better convergence rates of isotonic mean regression. Partitioning of the data is a valid strategy for very large datasets, but in smaller datasets it is more desirable to apply subagging to avoid that the estimator depends too strongly on the chosen partition. In principle, the averaging step in subagging or sample splitting could also be done on the level of the estimators instead of the CDFs , but if the goal is to obtain smoother CDFs, it is more natural to average the .

Finally, we show that the estimator proposed here generalizes the one by El Barmi and Marchev, (2009) for the case . Their estimator depends on a parameter , and equality holds for . This follows from the fact that with , one can write as

for , where is the indicator function. Taking the right-hand slope of the greatest convex minorant of the above functions then yields Equation (8) from El Barmi and Marchev, (2009). The choice was already suggested in their article, and it corresponds to the natural weight for which , , are the antitonic regression estimators.

3 Uniform consistency

The following notation and assumptions are required for stating the theorems about uniform consistency. Let , , , be a triangular array defined on a measurable space with a probability measure . For a sequence of events , the statement “ holds with asymptotic probability one” means . The covariates are assumed to be independent and have distinct values , and the response variables are independent conditional on such that , with the CDFs increasing in in the increasing concave order. The distinct values of are again denoted by . A subscript in , , and will be used to indicate that these quantities depend on the sample size , but the dependency of and on is not written explicitly to lighten the notation. If , it is only assumed that for all if , and if or if . The same property then also holds for .

The key condition for proving consistency of is the following.

(A) There exists and a sequence of sets , , such that

Sufficient conditions for (A) will be given below, and the convergence rate depends on whether is discrete or continuously distributed and on the tail properties of . If , one can simply set . For continuously distributed covariates on an interval , will be of the form with , that is, it is in general not possible to show consistency at the boundary of the covariate domain. This is also the case in isotonic mean regression and estimation under first order stochastic dominance (Mösching and Dümbgen, 2020b, ).

The following proposition establishes the connection between the uniform consistency of and .

Proposition 3.1.

Assume that (A) holds and is a set such that , .

-

(i)

If there exist and constants , such that for all , , then with ,

-

(ii)

If the distribution functions , , have support in and if is computed with grid , then

Proposition 3.1 shows that if is uniformly consistent in and at a rate , then the estimator is also uniformly consistent. When the response variable is integer-valued, is consistent at the same rate. Otherwise, if the distribution functions are Hölder continuous with index , the corresponding rate for is , for example if the are Lipschitz continuous. Note that in the case , the sets in Proposition 3.1 (i) are also equal to , and in (ii), the support of , , could be any discrete lattice instead of .

We proceed to state conditions under which (A) holds. For the -sample case, the assumption on the covariate is the following.

(K) The covariates take values in , and for some .

Instead of in (K), the set could be any discrete ordered set with cardinality . In the continuous case, the assumptions are analogous to (A.1) and (A.2) in Mösching and Dümbgen, 2020b .

(C1) The covariates admit a Lebesgue density bounded away from zero by on an interval .

(C2) There exists a constant such that for all and ,

Note that the set and the constants in (K) and (C1) and in (C2) do not depend on . Condition (C1) could be replaced by the weaker assumption that the number of points in every subinterval of of a certain size grows sufficiently fast, like in (A.2) of Mösching and Dümbgen, 2020b (, see also their Remark 3.2). In particular, it is not necessary to assume that the covariates are pairwise distinct or independent. However, this more general condition would require to introduce additional notation and constants. Similarly, in (K), it is sufficient that each value is attained at least times with asymptotic probability one for some . The Lipschitz assumption (C2) in the continuous case is standard in isotonic regression (see e.g. Yang et al.,, 2019; Dai et al.,, 2020), and it could be replaced by Hölder continuity with index at the cost of a slower convergence rate.

Since the goal is to prove consistency for an estimator of the expected values , it is natural that some additional assumptions on the tail behaviour of the distributions are required. In the two cases below, the set is assumed to be the one from (K) or from (C1), (C2).

(P) There exist and such that for all and ,

(E) There exist and such that for all and ,

Theorem 3.2.

Condition (A) holds with

and

In the -sample case, Theorem 3.2 implies uniform consistency at a rate of at least if the distribution functions are Lipschitz continuous in and have exponential tails. This is slower than the -rate of the empirical distribution functions stratified by the covariate values, and suggests that this lower bound is not always tight. Indeed, if the conditional CDFs , , have support on disjoint, pointwise increasing intervals, then are equal to the ECDFs of the corresponding subsamples and hence known to converge at the faster rate. Nevertheless, the result extends the ones from the current literature. In the two-sample case , Rojo and El Barmi, (2003) establish strong uniform convergence and pointwise but not uniform root- convergence for their estimator, while El Barmi and Marchev, (2009) only prove strong uniform consistency, but do not derive rates of convergence.

For a continuously distributed covariate and exponential tails, converges uniformly in and at a rate of up to a logarithmic factor, which is known to be the global rate of convergence of the isotonic regression estimator. When the conditional distributions have power tails with exponent , the rate becomes slower by a factor of . In general, the global -rate of convergence for isotonic regression does not require the assumption of exponential tails, but the results across the literature are not directly comparable. For example, Zhang, (2002) shows that with bounded second moments, the risk of the isotonic mean regression estimator, i.e. the root mean squared error at the design points, scales at a rate of , whereas Yang et al., (2019) prove uniform consistency with the same rate (up to logarithmic factors) in the supremum norm under sub-gaussianity of the error terms. Theorem 3.2 yields a stronger statement since convergence is also uniform in the parameter , and with exponential tails it still matches the optimal global rate up to the logarithmic factor. For , Theorem 3.2 implies a rate of at least under the favorable assumption (E) and Lipschitz continuity of in .

Isotonic regression for the mean has the property that it automatically adapts to the local smoothness of the underlying function; see for example Guntuboyina and Sen, (2018); Yang et al., (2019). A slight adaptation in the proof of Theorem 3.2 shows that this is also true for the estimator . For example, if is constant in , for all fixed , then the bound on the error under (E) becomes and is thus of order up to the logarithmic factor. Similarly, rates in between and can be obtained when for and all , with suitable . The same phenomenon occurs in part (i) of Proposition 3.1, where faster convergence rates are obtained for larger exponents in the Hölder continuity assumption.

4 Inference

Constructing confidence intervals for conditional distributions under stochastic order constraints is difficult. This section does not provide a solution to this problem for the - and -order, but it gives an overview of potential approaches and their pitfalls.

The limiting distributions of shape-constrained estimators are often rather complicated and depend on unknown characteristics of the underlying functions (Park et al.,, 2012; Guntuboyina and Sen,, 2018), which makes it difficult to derive confidence intervals from them. For -order in the -sample case, Zhang and Zhang, (2015) have shown converges to a process which is described by a min-max formula similar to (1) applied to integrated Brownian bridges with rescaled time. To construct confidence intervals for or from these distributions, one would need knowledge about the true CDFs and about the groups where the constraints are binding, i.e. hold with equality, which is usually not available in practice.

A more promising approach seem to be bootstrap methods, which have been explored by Park et al., (2012) in the case of first order stochastic dominance. However, the bootstrap is delicate in shape restricted regression, where it was shown that some popular bootstrap methods can be inconsistent (Guntuboyina and Sen,, 2018, Section 4.2.1, and the references therein), and so far there has been no thorough analysis of this phenomenon in the case of estimating conditional distributions. For the maximum likelihood estimator of a decreasing density, the Grenander estimator, it has been shown that suitable smoothing can yield a consistent bootstrap estimator (Groeneboom et al.,, 2010). This suggests to study the smoothed estimator

where is a smooth CDF, a bandwidth, and an estimator under stochastic order restrictions. This modification, which has not been studied for smoothing restricted estimators of conditional distributions so far, may also be interesting from a pure estimation perspective as an alternative to the bagging procedure suggested in Section 2.

Finally, Yang et al., (2019) developed a method for constructing simultaneous confidence intervals in isotonic mean regression which requires no tuning parameters. These confidence bands only assume subgaussian error distributions, and are similar to the restricted confidence intervals by El Barmi and Mukerjee, (2005, Section 5) under first order stochastic dominance. In the case of the increasing concave order, they might help to construct confidence bands for for varying and fixed , but it is not obvious whether this allows to derive practically useful bands for the derivative .

5 Simulations

In the following simulation examples, the - and -order constrained estimators are compared to competitors in terms of the distance between the estimated and the true CDFs, and in terms of the mean absolute error (MAE) of quantile estimates,

where denotes an estimator for and the expected value is taken over the sampling distribution of for the given sample size. The expected value in the definition of and is approximated by the empirical mean over simulations for the examples with discrete and simulations for those with continuously distributed covariates.

With covariate values , the following three settings are considered:

| (2) | ||||

| (3) | ||||

| (4) |

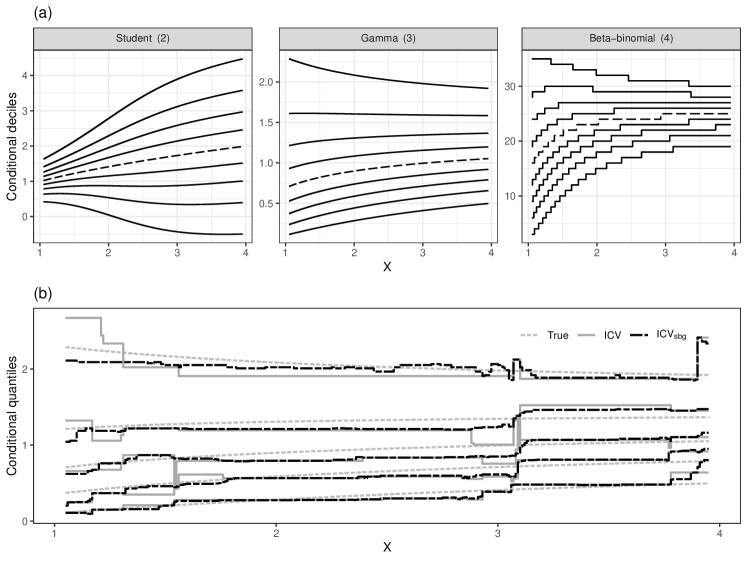

The conditional distributions of given are ordered in the increasing convex order, and the those of and with respect to the increasing concave order; see Figure 1 (a) for an illustration. In the -sample case, takes values in , , and , i.e. , which allows comparing the change in estimation error at previously available values of when the number of samples increases. For simulation examples with continuous covariate, the sample of is generated independent and uniformly distributed on . In all simulations the distinct observed values of the response variable are taken as grid for the computation of the - and -order constrained estimators.

| Student (2) | Gamma (3) | Beta-binomial (4) | |||||||||||

| 2 | 1.0 | 0.00 | 0.00 | 0.00 | 0.00 | 0.02 | 0.00 | 0.00 | 0.07 | 0.00 | 0.00 | 0.00 | 0.00 |

| 4.0 | 0.00 | 0.00 | 0.00 | 0.00 | -0.03 | 0.00 | 0.00 | -0.04 | 0.00 | 0.00 | 0.00 | 0.00 | |

| 4 | 1.0 | 0.00 | 0.00 | 0.00 | 0.00 | 0.06 | 0.00 | 0.05 | 0.12 | 0.00 | 0.00 | 0.00 | 0.00 |

| 2.0 | -0.01 | -0.10 | 0.01 | -0.01 | 0.08 | 0.05 | 0.12 | 0.19 | 0.05 | 0.00 | 0.05 | 0.09 | |

| 3.0 | 0.06 | 0.19 | 0.08 | 0.05 | 0.09 | 0.13 | 0.18 | 0.21 | 0.13 | 0.09 | 0.09 | 0.12 | |

| 4.0 | 0.05 | 0.16 | 0.10 | 0.10 | 0.03 | 0.11 | 0.11 | 0.14 | 0.08 | 0.09 | 0.15 | 0.10 | |

| 7 | 1.0 | 0.00 | -0.01 | 0.00 | 0.00 | 0.08 | 0.04 | 0.10 | 0.13 | 0.01 | 0.00 | 0.00 | 0.01 |

| 1.5 | -0.02 | -0.10 | 0.00 | -0.01 | 0.14 | 0.13 | 0.21 | 0.29 | 0.05 | 0.00 | 0.04 | 0.05 | |

| 2.0 | 0.01 | 0.01 | 0.05 | 0.00 | 0.16 | 0.20 | 0.26 | 0.35 | 0.12 | 0.05 | 0.12 | 0.14 | |

| 2.5 | 0.08 | 0.23 | 0.15 | 0.08 | 0.18 | 0.25 | 0.31 | 0.37 | 0.21 | 0.14 | 0.22 | 0.24 | |

| 3.0 | 0.13 | 0.33 | 0.23 | 0.19 | 0.17 | 0.28 | 0.32 | 0.36 | 0.28 | 0.24 | 0.22 | 0.29 | |

| 3.5 | 0.14 | 0.33 | 0.26 | 0.25 | 0.15 | 0.28 | 0.30 | 0.32 | 0.27 | 0.29 | 0.29 | 0.20 | |

| 4.0 | 0.09 | 0.23 | 0.19 | 0.21 | 0.07 | 0.19 | 0.19 | 0.22 | 0.15 | 0.15 | 0.26 | 0.19 | |

| Student (2) | Gamma (3) | Beta-binomial (4) | |||||||||||

| 2 | 1.0 | 0.00 | 0.00 | 0.00 | 0.00 | 0.01 | 0.00 | 0.00 | 0.05 | 0.00 | 0.00 | 0.00 | 0.00 |

| 4.0 | 0.00 | 0.00 | 0.00 | 0.00 | -0.02 | 0.00 | 0.00 | -0.02 | 0.00 | 0.00 | 0.00 | 0.00 | |

| 4 | 1.0 | 0.00 | 0.00 | 0.00 | 0.00 | 0.04 | 0.00 | 0.02 | 0.10 | 0.00 | 0.00 | 0.00 | 0.00 |

| 2.0 | -0.01 | -0.07 | 0.00 | 0.00 | 0.05 | 0.02 | 0.08 | 0.14 | 0.03 | 0.00 | 0.02 | 0.08 | |

| 3.0 | 0.04 | 0.13 | 0.05 | 0.04 | 0.07 | 0.08 | 0.14 | 0.20 | 0.09 | 0.05 | 0.04 | 0.07 | |

| 4.0 | 0.04 | 0.13 | 0.07 | 0.07 | 0.03 | 0.07 | 0.09 | 0.11 | 0.06 | 0.06 | 0.12 | 0.05 | |

| 7 | 1.0 | 0.00 | 0.00 | 0.00 | 0.00 | 0.07 | 0.02 | 0.07 | 0.13 | 0.00 | 0.00 | 0.00 | 0.00 |

| 1.5 | -0.01 | -0.07 | 0.00 | 0.00 | 0.11 | 0.09 | 0.16 | 0.25 | 0.03 | 0.00 | 0.02 | 0.03 | |

| 2.0 | 0.00 | -0.04 | 0.02 | -0.01 | 0.13 | 0.14 | 0.21 | 0.29 | 0.08 | 0.02 | 0.08 | 0.12 | |

| 2.5 | 0.05 | 0.15 | 0.09 | 0.03 | 0.15 | 0.19 | 0.26 | 0.32 | 0.16 | 0.09 | 0.19 | 0.20 | |

| 3.0 | 0.11 | 0.28 | 0.19 | 0.15 | 0.16 | 0.23 | 0.28 | 0.34 | 0.23 | 0.17 | 0.16 | 0.25 | |

| 3.5 | 0.13 | 0.27 | 0.23 | 0.22 | 0.14 | 0.24 | 0.27 | 0.31 | 0.25 | 0.26 | 0.26 | 0.16 | |

| 4.0 | 0.08 | 0.20 | 0.16 | 0.18 | 0.07 | 0.16 | 0.16 | 0.18 | 0.14 | 0.11 | 0.26 | 0.12 | |

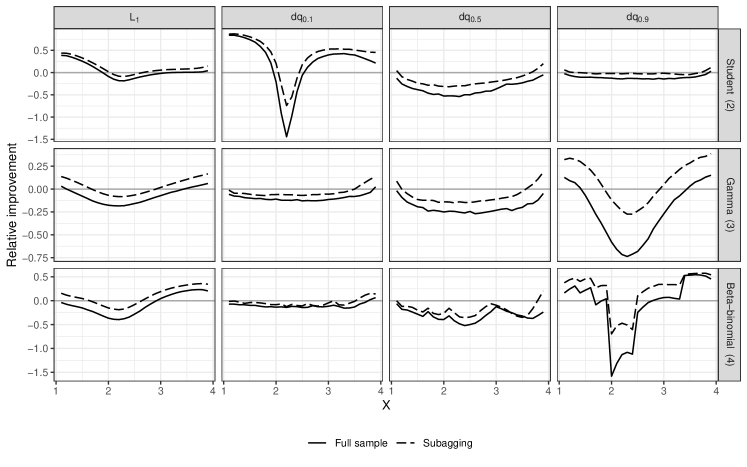

Table 1 shows the performance order restricted estimators compared to the ECDF in the -sample case, with fixed group sizes as in El Barmi and Marchev, (2009). One would expect that the improvement of the restricted estimator over the ECDF is larger when more constraints are binding. That is, when the conditional CDFs (or the functions ) are close to each other for the different values of , and when the sample size is small, then the restricted estimator may gain precision by pooling information across the groups. The case study confirms this intuition. For (groups and ) the ECDF already satisfies the order constraints in most cases and has similar estimation error as the constrained estimator. However, as new groups are included with covariate value in between those of the previously present groups, the order restricted estimators benefit from the larger total sample size and achieve a lower estimation error both globally, i.e. in -distance, and for most quantiles considered. This improvement is larger for than for , since with the larger sample size the ECDFs are already closer to the true distributions and require fewer corrections to satisfy the order constraints.

In the continuous case, the estimator under first order stochastic dominance by Mösching and Dümbgen, 2020b is chosen as competitor. This comparison is of interest since in situations where a variable depends monotonically on one might want to impose first order stochastic dominance as a restriction, but it is sometimes not fully clear if the monotone relationship is strong enough such that all conditional exceedance probabilities are increasing in for all , or if there might be crossings of the CDFs.

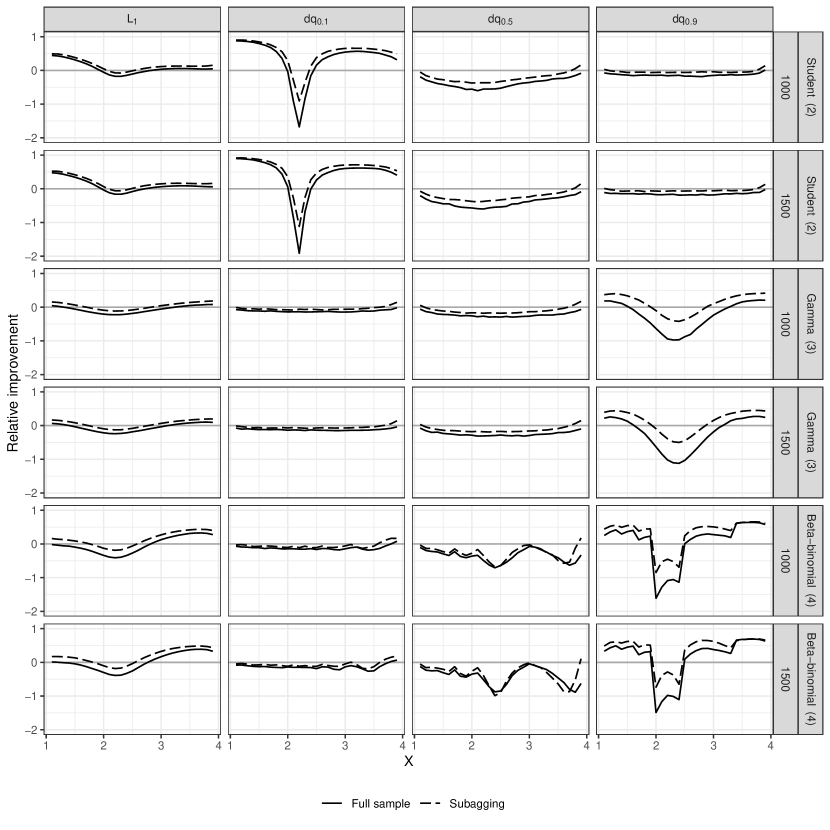

As Figure 1 (a) shows, for the simulations (3) and (4) the conditional quantile curves up to the seventh decile are all increasing in the covariate , and so are the conditional quantile curves above the third decile in (2). Therefore, although first order stochastic dominance is violated, it serves as a reasonable approximation in these problems. Figure 2 shows the relative performance of the estimators for . The estimator by Mösching and Dümbgen, 2020b achieves a lower absolute error for the median, for the -quantile in (3) and (4), and for the -quantile in (2), uniformly over all values of . This is due to the fact that the corresponding quantile curves are monotone and estimation under this correct constraint is more efficient than with the weaker - and -constraints. The picture is different for the low quantiles in (2) and the high quantiles in (3) and (4), where the conditional quantile curves are antitonic and the best isotonic approximation is constant, which generally provides a poor fit. Figure 2 also compares the errors of subagging variants of the estimators; see Figure 1 (b) for an illustration of the estimated quantile curves in the Gamma example. For both estimators, random subsamples of size are drawn from the data, and the conditional CDFs from each fit to the subsamples are averaged pointwise. It can be seen that the - and -order constrained estimators benefit more from subagging than the estimator with first order stochastic dominance. A comparison of different subagging variants and results for other sample sizes are given in the Appendix D.

There are many other methods for estimating conditional distributions than the shape-constrained regression methods discussed so far in this article, such as models based on parametric families (Rigby and Stasinopoulos,, 2005), nonparametric kernel methods (Li and Racine,, 2008), or quantile regression (Koenker,, 2005), only to name a few. In general, the advantage of shape-constrained estimators is that they are free from tuning parameters and automatically adapt to the (unknown) smoothness of the underlying functions which are to be estimated, but other estimation methods can achieve a smaller estimation error when their assumptions are satisfied. Indeed, in a simulation and case study, Henzi et al., 2021c (, Sections 4 and 5, Supplement S4) have found that estimators with first order stochastic dominance constraints are often not superior to competitors in terms of estimation error. This can be expected also for the estimators proposed in this article, which do not generally outperform the estimator under first order stochastic dominance.

6 Case study

It is well known that in the the evaluation of point forecasts, a wrongly specified loss function, such as the absolute error for comparing mean forecasts, may lead to counterintuitive results and distorted forecast rankings (Gneiting,, 2011). This causes problems in the interpretation of economic surveys, where respondents are often asked to issue point predictions for future quantities, but it is unspecified what functional of their (hypothetical) predictive distribution is meant. As a remedy, various tests of forecast rationality, or forecast calibration, have been proposed in the literature. A recent contribution is by Dimitriadis et al., (2019), who develop tests for the hypothesis that a given point forecast is the mean, median, or mode functional, or a convex combination of the three. The case study in this section demonstrates that the estimation of conditional distributions can complement such tests to gain additional information for the interpretation of point forecasts.

If denotes a point forecast and the observation, the hypothesis of forecast rationality with respect to a functional can be defined as , where denotes the conditional law of given the forecast . This formulation is a special but important case of equation (2.1) in Dimitriadis et al., (2019), which allows including additional information available to the forecaster for conditioning. If is the mean functional, then forecast rationality is equivalent to the moment condition . For the median, the corresponding condition is , provided that is a continuous distribution. Based on such conditions, Dimitriadis et al., (2019) developed asymptotic tests for forecast rationality.

Distributional regression provides a different, more qualitative approach to this problem. If the conditional distributions were known, one could easily derive the functional of interest and detect violations of forecast rationality by directly comparing and . Estimators with stochastic order restrictions allow to mimic this ideal situation, without having to impose restrictive or implausible assumptions on the conditional distributions. For sufficiently precise point forecasts , one would expect that the actual observation tends to attain higher values as increases. Moreover, estimating under stochastic order constraints only requires the ranks of the forecasts in a sample, but not their values. This makes a comparison of and sensible, because themselves have not been provided to the model. Other estimation methods, such as kernel regression (Li and Racine,, 2008), generally do not have this property.

To illustrate the approach, consider the data example from Section 5.1 of Dimitriadis et al., (2019). In the Labor Market Survey by the Federal Reserve Bank of New York, respondents are asked three times per year to report their annualized income in four months. The sample analysed here ranges from March 2015 to November 2019. Some respondents participate in several rounds of the survey, and only the first round is included for those individuals which occur several times to obtain independent observations. Additionally, like in Dimitriadis et al., (2019), observations with very high or low expectations or income (above 300’000 or below 1000, 4.0% of the sample; an upper bound of 1 million was used in Dimitriadis et al., (2019)) are removed since the data is very sparse and uninformative for such values, as are cases when the ratio of expectation and income or the inverse ratio is between and (27 instances), which might be due to misplaced decimal points or erroneously reporting monthly instead of annualized income. The remaining sample consists of 3161 observations. The survey of consumer expectations (SCE; © 2013-2020 Federal Reserve Bank of New York) data for this case study are available without charge at https://www.newyorkfed.org/microeconomics/sce, and may be used subject to license terms posted there. The New York Fed disclaims any responsibility for the analysis and interpretation of Survey of Consumer Expectations data in this article.

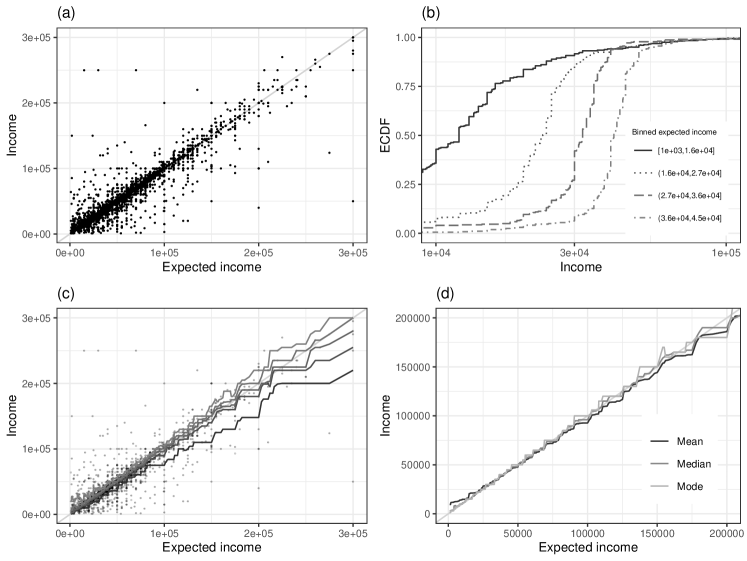

Panels (a) and (b) of Figure 3 illustrate the joint distribution of the income expectations and realizations. There is a strong monotone relationship, with a Pearson correlation of , but interestingly, for the lowest deciles of the income expectations, the corresponding conditional CDFs of the observed income cross in the upper tail, indicating a violation of first order stochastic dominance. The intuition behind these results is that individuals are generally able to predict their income well, which explains the strong monotone relationship, but low income expectations are sometimes overly pessimistic. Rozsypal and Schlafmann, (2021) have found with different data that people with lower income tend to have pessimistic expectations, both conditionally on potential confounder covariates and unconditionally. The increasing concave order can accomodate this situation, as it allows that the conditional CDFs cross in the upper tail. To estimate the conditional distributions, a subagging version of the -order restricted estimator with subsamples of half of the total sample size is applied. From the estimated distributions, the mean, median, and mode functional are then computed, with the mode taken as the location of the largest jump of the conditional CDFs, which are piecewise constant stepfunctions. Panels (c) and (d) of Figure 3 display estimated quantile curves and the three functionals depending on the income expectation.

For the mean functional, the forecast rationality test of Dimitriadis et al., (2019) yields a p-value of , computed with the R package fcrat available on https://github.com/Schmidtpk/fcrat. As can be seen in Figure 3, the conditional mean curve lies above the bisector for expectations below 25’000, and below the bisector when the expectation exceeds 75’000, so there is indeed a systematic deviation of the income expectation from the estimated mean. For the median and the mode functional, the p-values of the rationality test are and , respectively. This huge difference in the p-values is in contrast to the curves in Figure 3 (d), where the expected income does not seem to deviate systematically from either functional. A simulation reveals that for data where the outcome may be exactly equal to , the p-value for the median should indeed be interpreted with care. By taking the estimated medians as new income expectation and simulating new observations from the estimated conditional distributions, one obtains new data sets where the income expectation equals the median of the underlying distribution by construction. Over 10’000 simulations, the rejection rate for the median rationality test is , and at the levels , , and – the test is anticonservative. The reason for the non-validity of the median rationality test is likely to be the discreteness in the data: The realized incomes only take distinct values with a sample size of , and in of the cases the income expectation is exactly equal to the realized income. Hence the condition may be violated even if is equal to the conditional median due a point mass of the conditional distributions at the expected income .

In conclusion, the -constrained estimator suggests that both median and mode could rationalize the income expectations, and it confirms that the income expectations should not be interpreted as a mean forecast.

7 Discussion

The estimators proposed in this article may extended to more complex settings than univariate covariates . One avenue for future work is to consider partially ordered instead of real-valued covariates. A partial order relation on a space satisfies the same properties as the usual order of real numbers (transitivity, reflexivity, antisymmetry), but not all elements of need to be comparable; an example is the componentwise order of vectors on . To construct estimators in this setting, it suffices to slightly modify the definition

from Section 2, with the only difference that in the are now compared with respect to the partial order . A similar min-max formula as in (1) also applies in this case (see Barlow et al., (1972)), so that Proposition 2.1 continues to hold. The computation of is still feasible since it is a quadratic minimization problem with linear constraints, for which most statistical software programs provide efficient algorithms. While consistency with partially ordered covariates has been proved for estimation under first order stochastic dominance constraints (Henzi et al., 2021c, ), it remains an open problem for the orders considered in this article.

The generalization to partially ordered covariates is of interest as it allows to construct nonparametric distributional regression models with shape and scale parameters. In the spirit of Henzi et al., 2021c , assume that we are interested in estimating the conditional distribution of a variable given a collection of point forecasts , say, predictions from a survey of experts or from different numerical models. This conditional distribution provides a corrected, re-calibrated version of the forecasts. An effective approach is to model with Gaussian distributions , where and are the mean and variance of the point forecasts , respectively, and the parameters are estimated on training data of past forecasts and observations. Gneiting et al., (2005) apply this approach in weather forecasting, and Gneiting and Thorarinsdottir, (2010) a slightly more sophisticated model in inflation prediction. When , which usually the case or even imposed (Gneiting et al.,, 2005), the distributions are increasing in the -order when the vector increases componentwise. Hence, the estimator with -order constraints and covariate vector could provide a flexible nonparametric alternative to such a parametric location-scale model.

A further potential extension are distributional single index models in the spirit of Henzi et al., 2021b , where the covariate itself is derived from a higher dimensional covariate with some dimension reducing function , such as for . Henzi et al., 2021b have shown that when the conditional CDFs of only depend on via , and when these distributions are increasing in first order stochastic dominance as increases, then the combination of a consistent estimator for and a shape constrained estimator applied to , , may again yield a consistent estimator of the conditional CDFs. It is an open question whether similar results hold for the increasing concave and convex order.

Acknowledgements

This work was supported by the Swiss National Science Foundation. The author is grateful to Johanna Ziegel and Timo Dimitriadis for helpful comments and discussions.

References

- Arcones et al., (2002) Arcones, M. A., Kvam, P. H., and Samaniego, F. J. (2002). Nonparametric estimation of a distribution subject to a stochastic precedence constraint. Journal of the American Statistical Association, 97:170–182.

- Banerjee et al., (2019) Banerjee, M., Durot, C., Sen, B., et al. (2019). Divide and conquer in nonstandard problems and the super-efficiency phenomenon. Annals of Statistics, 47:720–757.

- Baringhaus and Gruebel, (2009) Baringhaus, L. and Gruebel, R. (2009). Nonparametric two-sample tests for increasing convex order. Bernoulli, 15:99–123.

- Barlow et al., (1972) Barlow, R. E., Bartholomew, D. J., Bremner, J. M., and Brunk, H. D. (1972). Statistical inference under order restrictions. The theory and application of isotonic regression. John Wiley & Sons, London-New York-Sydney. Wiley Series in Probability and Mathematical Statistics.

- Berrendero and Cárcamo, (2011) Berrendero, J. R. and Cárcamo, J. (2011). Tests for the second order stochastic dominance based on l-statistics. Journal of Business & Economic Statistics, 29:260–270.

- Brunk et al., (1966) Brunk, H., Franck, W., Hanson, D., and Hogg, R. (1966). Maximum likelihood estimation of the distributions of two stochastically ordered random variables. Journal of the American Statistical Association, 61:1067–1080.

- Chetverikov et al., (2021) Chetverikov, D., Wilhelm, D., and Kim, D. (2021). An adaptive test of stochastic monotonicity. Econometric Theory, 37:495–536.

- Dai et al., (2020) Dai, R., Song, H., Barber, R. F., and Raskutti, G. (2020). The bias of isotonic regression. Electronic Journal of Statistics, 14:801.

- Dimitriadis et al., (2019) Dimitriadis, T., Patton, A. J., and Schmidt, P. (2019). Testing forecast rationality for measures of central tendency. arXiv preprint arXiv:1910.12545.

- Donald and Hsu, (2016) Donald, S. G. and Hsu, Y.-C. (2016). Improving the power of tests of stochastic dominance. Econometric Reviews, 35:553–585.

- Dümbgen et al., (2004) Dümbgen, L., Freitag, S., and Jongbloed, G. (2004). Consistency of concave regression with an application to current-status data. Mathematical Methods of Statistics, 13:69–81.

- Dykstra et al., (1991) Dykstra, R., Kochar, S., Robertson, T., et al. (1991). Statistical inference for uniform stochastic ordering in several populations. Annals of Statistics, 19:870–888.

- El Barmi and Marchev, (2009) El Barmi, H. and Marchev, D. (2009). New and improved estimators of distribution functions under second-order stochastic dominance. Journal of Nonparametric Statistics, 21:143–153.

- El Barmi and Mukerjee, (2005) El Barmi, H. and Mukerjee, H. (2005). Inferences under a stochastic ordering constraint: the k-sample case. Journal of the American Statistical Association, 100:252–261.

- El Barmi and Mukerjee, (2012) El Barmi, H. and Mukerjee, H. (2012). Peakedness and peakedness ordering. Journal of Multivariate Analysis, 111:222–233.

- El Barmi and Mukerjee, (2016) El Barmi, H. and Mukerjee, H. (2016). Consistent estimation of survival functions under uniform stochastic ordering; the k-sample case. Journal of Multivariate Analysis, 144:99–109.

- El Barmi and Wu, (2017) El Barmi, H. and Wu, R. (2017). On estimation of peakedness-ordered distributions. Communications in Statistics-Theory and Methods, 46:4855–4869.

- Gneiting, (2011) Gneiting, T. (2011). Making and evaluating point forecasts. Journal of the American Statistical Association, 106:746–762.

- Gneiting et al., (2005) Gneiting, T., Raftery, A. E., Westveld III, A. H., and Goldman, T. (2005). Calibrated probabilistic forecasting using ensemble model output statistics and minimum CRPS estimation. Monthly Weather Review, 133:1098–1118.

- Gneiting and Thorarinsdottir, (2010) Gneiting, T. and Thorarinsdottir, T. L. (2010). Predicting inflation: Professional experts versus no-change forecasts. arXiv preprint arXiv:1010.2318.

- Goovaerts et al., (1982) Goovaerts, M., De Vylder, F., and Haezendonck, J. (1982). Ordering of risks: a review. Insurance: Mathematics and Economics, 1:131–161.

- Groeneboom et al., (2010) Groeneboom, P., Jongbloed, G., and Witte, B. I. (2010). Maximum smoothed likelihood estimation and smoothed maximum likelihood estimation in the current status model. The Annals of Statistics, 38(1):352–387.

- Guntuboyina and Sen, (2018) Guntuboyina, A. and Sen, B. (2018). Nonparametric shape-restricted regression. Statistical Science, 33(4):568–594.

- (24) Henzi, A., Kleger, G.-R., Hilty, M. P., Wendel Garcia, P. D., and Ziegel, J. F. (2021a). Probabilistic analysis of COVID-19 patients’ individual length of stay in Swiss intensive care units. PLOS ONE, 16:1–14.

- (25) Henzi, A., Kleger, G.-R., and Ziegel, J. F. (2021b). Distributional (single) index models. Journal of the American Statistical Association. Forthcoming.

- (26) Henzi, A., Ziegel, J. F., and Gneiting, T. (2021c). Isotonic distributional regression. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 83:963–993.

- Hsu et al., (2019) Hsu, Y.-C., Liu, C.-A., and Shi, X. (2019). Testing generalized regression monotonicity. Econometric Theory, 35:1146–1200.

- Koenker, (2005) Koenker, R. (2005). Quantile regression, volume 38 of Econometric Society Monographs. Cambridge University Press, Cambridge.

- Li and Racine, (2008) Li, Q. and Racine, J. (2008). Nonparametric estimation of conditional CDF and quantile functions with mixed categorical and continuous data. Journal of Business & Economic Statistics, 26:423–434.

- Linton et al., (2005) Linton, O., Maasoumi, E., and Whang, Y.-J. (2005). Consistent Testing for Stochastic Dominance under General Sampling Schemes. The Review of Economic Studies, 72:735–765.

- (31) Mösching, A. and Dümbgen, L. (2020a). Estimation of a likelihood ratio ordered family of distributions–with a connection to total positivity. arXiv preprint arXiv:2007.11521.

- (32) Mösching, A. and Dümbgen, L. (2020b). Monotone least squares and isotonic quantiles. Electronic Journal of Statistics, 14:24–49.

- Park et al., (2012) Park, Y., Taylor, J. M., and Kalbfleisch, J. D. (2012). Pointwise nonparametric maximum likelihood estimator of stochastically ordered survivor functions. Biometrika, 99:327–343.

- Rigby and Stasinopoulos, (2005) Rigby, R. A. and Stasinopoulos, D. M. (2005). Generalized additive models for location, scale and shape. Journal of the Royal Statistical Society: Series C (Applied Statistics), 54:507–554.

- Robertson et al., (1988) Robertson, T., Wright, F. T., and Dykstra, R. L. (1988). Order restricted statistical inference. Wiley Series in Probability and Mathematical Statistics: Probability and Mathematical Statistics. John Wiley & Sons, Ltd., Chichester.

- Rojo and Batún-Cutz, (2007) Rojo, J. and Batún-Cutz, J. (2007). Estimation of symmetric distributions subject to a peakedness order. In Advances In Statistical Modeling And Inference: Essays in Honor of Kjell A Doksum, pages 649–669. World Scientific.

- Rojo and El Barmi, (2003) Rojo, J. and El Barmi, H. (2003). Estimation of distribution functions under second order stochastic dominance. Statistica Sinica, 13:903–926.

- Rozsypal and Schlafmann, (2021) Rozsypal, F. and Schlafmann, K. (2021). Overpersistence bias in individual income expectations and its aggregate implications. Danmarks Nationalbank Working Papers 173, Copenhagen.

- Shaked and Shanthikumar, (2007) Shaked, M. and Shanthikumar, J. G. (2007). Stochastic orders. Springer Series in Statistics. Springer, New York.

- Shi, (1994) Shi, N.-Z. (1994). Maximum likelihood estimation of means and variances from normal populations under simultaneous order restrictions. Journal of Multivariate Analysis, 50(2):282–293.

- Vittorietti et al., (2021) Vittorietti, M., Hidalgo, J., Sietsma, J., Li, W., and Jongbloed, G. (2021). Isotonic regression for metallic microstructure data: estimation and testing under order restrictions. Journal of Applied Statistics, pages 1–20.

- Yang et al., (2019) Yang, F., Barber, R. F., et al. (2019). Contraction and uniform convergence of isotonic regression. Electronic Journal of Statistics, 13:646–677.

- Zhang, (2002) Zhang, C.-H. (2002). Risk bounds in isotonic regression. Annals of Statistics, 30:528–555.

- Zhang and Zhang, (2015) Zhang, J. and Zhang, Z. (2015). Multi-sample test based on bootstrap methods for second order stochastic dominance. Hacettepe Journal of Mathematics and Statistics, 44:503–512.

Appendix A Greatest convex minorants

Let be an interval and a function. The greatest convex minorant of is the pointwise greatest convex function such that for all . It exists if and only if can be bounded from below by an affine linear function, and if the greatest convex minorant exists, it is unique since the pointwise supremum of convex functions is again convex. By the same reason, if and are functions with greatest convex minorants and , then for all implies that also .

A standard result about isotonic regression (see e.g. Robertson et al.,, 1988, Theorem 1.2.1) states that the isotonic regression of with weights , that is, the minimizer of over all , equals the left-hand slope of the greatest convex minorant to the function that results from linearly interpolating

This result allows to describe right-hand slope of the greatest convex minorant of any piecewise linear function with finitely many knots.

Lemma A.1.

Let be piecewise linear with knots at and let be its greatest convex minorant. Then the right-hand slope of at is given by the isotonic regression of with weights , .

The following lemma is known as Marshall’s Inequality.

Lemma A.2.

Let be an interval and a function, and let be the greatest convex minorant of and any convex function. Assume that , where is the usual supremum norm of functions. Then, .

Proof.

Let . The function is convex and satisfies for all by definition of . This and the definition of imply that for all . Since also by the definition of , this yields

and so . ∎

Appendix B Proofs of theoretical results

Some proofs rely on properties of greatest convex minorants, which are stated in Section A.

Proof of Proposition 2.1.

Formula (1) in the article shows that is decreasing in and increasing in when the respective other argument is fixed, and

| (5) |

In particular, it follows that the greatest convex minorant of exists. For with , the functions are piecewise linear with finitely many knots, a property which is preserved when taking pointwise maxima and minima of finitely many functions. Therefore, the are also piecewise linear. For any , and ,

so , and hence is increasing in . Lemma A.1 and (5) together with the inequality imply that with for and for , and is continuous from the right and increasing because is is the right-hand derivative of a convex function. Finally, is decreasing in because is pointwise decreasing in for all ; see Section A. ∎

Proof of Proposition 3.1.

The proof is similar to the proof of Corollary 1 in Dümbgen et al., (2004). With from (A), define . Then , and in the following derivations, assume that the inequality in holds. In case (i), let . For , by convexity of ,

and the same property holds for and instead of and . The function is convex, so due to Lemma A.2,

Combining these facts yields, for any ,

and similarly

Thus with on for and , for each . Under (ii), for and ,

and analogously , which gives For , the same bound is valid since and , where the latter holds if and are only computed at and interpolated linearly. ∎

The proof of Theorem 3.2 requires several auxiliary results.

Proposition B.1.

Let be random variables in a non-degenerate interval . Then there exists a universal constant such that for all ,

Proof.

Let be the cumulative distribution function of . The assumption for implies that , so

Theorem 4.6 of Mösching and Dümbgen, 2020b now yields the result. ∎

For and , let . The following inequality, which follows by simple case distinctions, will be applied several times: For all ,

| (6) |

where and for .

Lemma B.2.

Let be a random variable such that for some and all ,

Then for ,

Proof.

Replacing by the random variable in (6) implies that for all ,

To compute the expected value in the upper bound, let denote the cumulative distribution function of . Then,

This implies

In the first case, for , it holds . In the second case, the upper bound is . ∎

Proposition B.1 and Lemma B.2 allow to derive an analogous result to Corollary 4.7 of Mösching and Dümbgen, 2020b , for which some additional notation is required. For and , , define and

Recall that the estimator has the representation

for the distinct values of , , and

For fixed , let be indices such that

Assuming , with , , the estimator equals

This implies that

and an asymptotic upper bound for is derived below.

Proposition B.3.

Let . Then for any ,

where

Proof.

For , define

By Lemma B.2, for any and ,

Also by (P) or (E) and by (6),

This implies that the events

satisfy . Let and be defined as and but with the truncated variables instead of . By the above considerations, conditional on , for any ,

Proposition B.1 implies that

Replace now by

This yields

and therefore . Also,

which gives , using in the first case. For , define . Then, for large enough such that , and by conditioning on ,

Proof of Theorem 3.2, discrete setting (K).

For , let , and define . Recall that is the antitonic regression of , . Corollary B of Robertson et al., (1988, p. 42) implies that for all ,

This gives

Assume that , and define for , and . Then , and by assumption (K),

with asymptotic probability one. Since and , Proposition B.3 implies that, with asymptotic probability one for any and ,

With , the upper bound equals

Proof of Theorem 3.2, continuous setting (C1), (C2).

With Proposition B.3, one can apply the same strategy of proof as for Theorem 3.3 in Mösching and Dümbgen, 2020b . Let be a sequence such that and . By assumption (C1) and by the result in Section 4.3 of Mösching and Dümbgen, 2020b , for all subintervals of length at least and any , the inequality holds with asymptotic probability one. Let such that , and define

By the above considerations, with asymptotic probability one, and are well-defined, satisfy , , and . Therefore, for any ,

| (7) | ||||

| (8) |

using antitonicity of in the first line, equation (1) from the article in the second line, and antitonicity of in the second-last step. An analogous argument for and the asymptotic bound for in Proposition B.3 yield

for . The convergence rates of these two summands are balanced if , and for and , the upper bound equals

If is constant in for all , then the difference in (7) equals zero, and the term in (8) disappears. In that case, one can set , which again with and yields the upper bound

under (E), which is valid for all such that .

∎

Appendix C Convergence rates with interpolation

In Section 2 in the manuscript, it is suggested to estimate and only on a finite grid . Below is a proof that this indeed does not influence the convergence rates, provided that , , and that the grid is fine enough.

Proof that convergence rates are valid under interpolation.

Assume that (A) holds, i.e.

for some sequences of sets . Let be the linear interpolation of computed on this grid. That is, for , set with , and for and for . Then, since is Lipschitz continuous with Lipschitz constant 1,

for all . Provided that , this implies , so the same convergence rate applies if and are evaluated on a sufficiently fine grid. If are independent and admit a density bounded away from zero on , then the results of Section 4.3 in Mösching and Dümbgen, 2020b imply that holds with asymptotic probability one for the from Theorem 3.2 in the manuscript, so it is admissible in this case to take the observed values as the grid. ∎

Appendix D Additional figures for Section 4

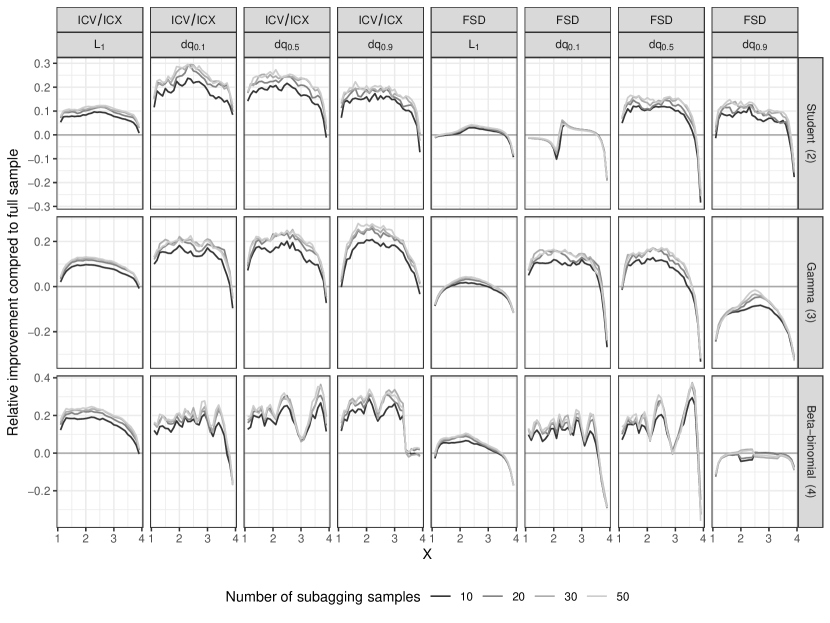

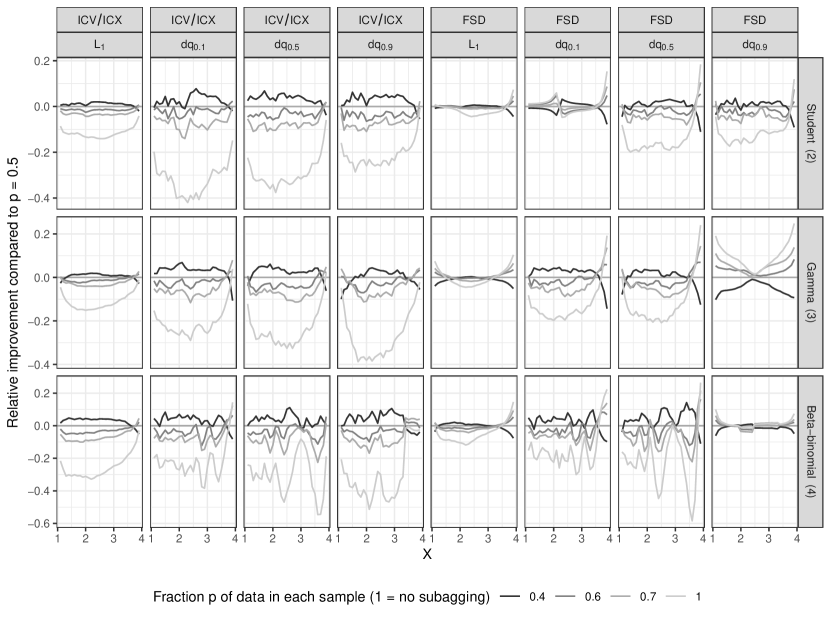

Figure 4 shows the same comparison as Figure 1 in the manuscript for and . In Figures 5 and 6, different variants of subagging are compared. Using more than of the total data in subsamples is generally not better than or less. A higher number of subsamples improves the subagging variants of the estimators, but the effect diminishes as the number of subsamples increases.