Randomized Stochastic Variance-Reduced Methods for Multi-Task Stochastic Bilevel Optimization

Abstract

In this paper, we consider non-convex stochastic bilevel optimization (SBO) problems that have many applications in machine learning. Although numerous studies have proposed stochastic algorithms for solving these problems, they are limited in two perspectives: (i) their sample complexities are high, which do not match the state-of-the-art result for non-convex stochastic optimization; (ii) their algorithms are tailored to problems with only one lower-level problem. When there are many lower-level problems, it could be prohibitive to process all these lower-level problems at each iteration. To address these limitations, this paper proposes fast randomized stochastic algorithms for non-convex SBO problems. First, we present a stochastic method for non-convex SBO with only one lower problem and establish its sample complexity of for finding an -stationary point under Lipschitz continuous conditions of stochastic oracles, matching the lower bound for stochastic smooth non-convex optimization. Second, we present a randomized stochastic method for non-convex SBO with lower level problems (multi-task SBO) by processing a constant number of lower problems at each iteration, and establish its sample complexity no worse than , which could be a better complexity than that of simply processing all lower problems at each iteration. Lastly, we establish even faster convergence results for gradient-dominant functions. To the best of our knowledge, this is the first work considering multi-task SBO and developing state-of-the-art sample complexity results.

1 Introduction

A stochastic bilevel optimization (SBO) problem is formulated as:

| (1) | ||||

where and are continuously differentiable functions, and are random variables. This problem has many applications in machine learning, e.g., meta-learning [30], neural architecture search [21], reinforcement learning [18], hyperparameter optimization [9], etc.

Besides the above problem, we consider a more general SBO problem with many lower problems in the following form:

| (2) | ||||

where . We refer to the above problem as multi-task stochastic bilevel optimization. One challenge of dealing with the problem (2) compared with the problem (1) is that processing lower problems at each iteration could be prohibitive when is large.

Related Work.

Although bilevel optimization has a long history in the literature [4, 19, 20, 24, 31, 32], non-asymptotic convergence was not established until recently [10, 17, 13, 3]. [10] proposes a double-loop stochastic algorithm, where the inner loop solves the lower level problem up to a certain accuracy level. For non-convex and strongly convex , their algorithm’s sample complexity is for finding an -stationary point of the objective function , i.e., a solution satisfying . [17] improves the sample complexity of a double-loop algorithm to by using a large mini-batch size at each iteration. [13] proposes a single-loop two timescale algorithm TTSA, which suffers from a worse complexity of for finding an -stationary point. Recently, [3] proposes a single-loop single timescale algorithm (STABLE) based on a recursive variance-reduced estimator of the second-order Jacobian and Hessian matrix , which enjoys a sample complexity of without using a large mini-batch size at each iteration. However, these studies focus on the formulation (1) and do not explicitly consider the challenge for dealing with (2) with many lower level problems. Hence, the existing results are limited in two perspectives: (i) their sample complexities are high, which do not match the state-of-the-art result for non-convex stochastic optimization, i.e., [8, 5]; (ii) their algorithms are tailored to problems with only one lower-level problem and are not appropriate for solving (2) with .

Our Contributions. In this paper, we further improve the sample complexity of optimization algorithms for solving SBO problems. First, we present a stochastic method for non-convex SBO with only one lower problem and establish a sample complexity of for finding an -stationary point under Lipschitz continuous conditions of stochastic oracles, matching a lower bound for stochastic smooth non-convex optimization [1]. Second, we present a randomized stochastic method (RSVRB) for non-convex multi-task SBO with lower level problems by processing only a constant number of lower problems at each iteration, and establish its sample complexity no worse than , which could have a better complexity than simply processing all lower problems at each iteration. Lastly, we establish even faster convergence rates in the order of for gradient-dominant functions. To the best of our knowledge, this is the first work considering SBO with many lower level problems and establishing state-of-the-art sample complexity. We present the comparison between our results and existing results in Table 1.

Applications & Significance.

Although this paper focuses on theoretical developments, the proposed algorithms have broad applications in machine learning. We name some of these applications below and discuss the significance of our results.

Meta Learning. An important application of SBO with many lower level problems is model-agnostic meta learning (MAML) with many tasks [30], which can be formulated as following:

where corresponds to the (expectation or average) loss function for the -th task, and denotes the personalized model increment for the -th task by minimizing the lower problem. Existing algorithms [10, 17, 13, 3, 30] for bilevel optimization do not consider the scenario that is very large. Hence, these algorithms require processing tasks at each iteration. In contrast, the proposed RSVRB only needs to process one task per-iteration and only requires a constant mini-batch size and enjoys a smaller sample complexity under appropriate conditions. This also improves existing stochastic algorithms and their theory for MAML [7, 14], which require processing a large number of tasks or a large mini-batch size per-iteration and suffer from worse complexities with the best complexity of under similar conditions as ours [14].

Optimizing a Sum of Stochastic Compositional Functions. Existing literature has considered the following compositional optimization problem:

| (3) |

which is a special case of SBO, i.e.,

Although the two-level stochastic compositional optimization problem (3) has been studied extensively in the literature [34, 12, 36, 16, 37, 22], the following extension with many components has been less studied:

| (4) |

which is a special case of SBO with many lower-level problems:

The problem (4) has important applications in machine learning. We give one example, which is the optimization of area under precision-recall curve (AUPRC). Recently, [28] proposes to optimize a surrogate loss of averaged precision for AUPRC optimization, which can be formulated as

| (5) |

where denotes a model parameter, denote an input data and its corresponding label , and denotes a pairwise loss function. Define , and , the above problem reduces to an instance of (4) and hence an instance of (2). [28] has proposed a stochastic algorithm for solving (5), whose sample complexity is . Under a Lipschitz continuity condition of and other appropriate conditions, the proposed RSVRB method has a better sample complexity of .

Structured Non-Convex Strongly-Concave Min-Max Optimization. The proposed RSVRB can be applicable to the following structured min-max problem:

| (6) |

For the problem (6) with , our algorithm SVRB reduces to a stochastic variance-reduced algorithm for solving non-convex strongly-concave min-max problem proposed in [15]. However, when is large, our algorithm RSVRB could be more efficient. One application of (6) with large is multi-task deep AUC maximization where each corresponds to a binary classification task since AUC maximization for one task can be written as a non-convex strongly-concave min-max optimization problem with one dual variable [23, 35].

2 Preliminaries

Notations.

We use to denote the norm of a vector or a matrix. The norm of a matrix is known as the spectral norm. Let denote the Frobenius norm of a matrix. In the following, an Euclidean norm refers to norm of a vector or Frobenius norm of a matrix. Let denotes Euclidean projection onto a convex set for a vector and denotes a projection onto the set . We use the notation denote a projection onto the set . Both and can be implemented by using SVD and thresholding the singular values. For an Euclidean ball , we abuse the notation .

Let us first present some preliminaries for solving SBO with only one lower-level problem. Recall the problem:

| (7) | ||||

We make the following assumptions about the above problem.

Assumption 1

For any , is -smooth and -strongly convex function, i.e., .

Assumption 2

For we assume the following conditions hold

-

•

(i) is -Lipschitz continuous, is -Lipschitz continuous, is -Lipschitz continuous, is -Lipschitz continuous, is -Lipschitz continuous, all respect to .

-

•

(ii) , , , and have a variance bounded by .

-

•

(iii) , .

-

•

(iv) , where .

Remark: Assumption 1 is made in many existing works for SBO [10, 17, 13, 3]. Assumptions 2 (ii)(iv) are also standard in the literature [10, 17, 13]. In terms of Assumption 2 (i) compared with [3], we assume stronger conditions that for any fixed and are Lipschitz continuous; in contrast, they assume for any fixed and are Lipschitz continuous. However, we have weaker assumptions , . In contrast, they assume , and for both , and and . It is also notable that [10, 13] make an additional (implicit) assumption that (cf. the proof of Lemma 3.2 in [10]). Notice that this is a much stonger assumption, which usually does not hold in practice.

In order to understand the proposed algorithms, we present following proposition about the gradient of , which is a standard result in the literature of bilevel optimization [10].

Proposition 1

Under Assumption 1, we have

3 SBO with One Lower-level Problem

Motivation of the Proposed Algorithm. A naive approach to approximate the gradient at any iterate is to compute and then approximate each term in the R.H.S of the equation in Proposition 1 by their (mini-batch) stochastic gradients, i.e., , where are independent stochastic random variables. There are two deficiencies of this naive approach: (i) Due to the inverse function, the expectation of above stochastic variable is not equal to . In order to control the error of the stochastic gradient estimator, a straightforward approach is to use a mini-batch stochastic gradient estimator for with a large mini-batch size. A better way is to use a variance-reduced estimator for , which has been studied extensively in the literature of stochastic optimization and stochastic compositional optimization [27, 5, 2, 33, 11]. The inverse function in makes it similar to a gradient of a compositional function. Hence, an estimator of with variance-reduced property is important to the convergence of an algorithm without using a large mini-batch size. (ii) Computing exactly at each iteration is computationally expensive and is also not necessary. This is because at the beginning is far from good, hence computing an approximate solution of is enough for the algorithm to make the progress.

Based on the above motivation, at each iteration , we use to approximate , and use variance-reduced stochastic gradient estimators to estimate each term in the following:

To this end, we will maintain four quantities for estimating , , , , respectively, and estimate by

Then we can update by .

Next, we consider the update for . This update is for approximating . A simple approach is to simply use the stochastic gradient of at previous solutions . However, in order to match the variance-reduced property of , we will also use a variance-reduced gradient estimator for to update , i.e., , where is a variance-reduced estimator of .

Based on the motivation described above, we present the detailed steps in Algorithm 1. The algorithm is referred to as stochastic variance-reduced bilevel (SVRB) method. The key to the algorithm lies at using the STROM technique to compute the variance reduced estimators, which is developed by [5] with the idea originated from several earlier variance reduced estimators (SPIDER [8], SARAH [25]) for stochastic non-convex minimization. Another important feature of SVRB is the projection of onto an appropriate domain to ensure appropriate boundness.

Differences between SVRB and STABLE. The key differences between SVRB and STABLE lie at (i) SVRB uses a variance-reduced estimator with the STORM technique to approximate ; in contrast STABLE uses unbiased estimators for these gradients; (ii) SVRB does a simple update for using the variance-reduced estimator ; in contrast STABLE uses a step that includes in the update of . These differences make the analysis of SVRB different from that of STABLE, especially on bounding . Finally, we note that the in Step 4 of Algorithm 1 can be efficiently computed by the conjugate gradient (CG) algorithm that only involves Hessian-vector product [29].

The main convergence result of SVRB is presented in the following theorem.

Theorem 1

Remark: The above theorem implies that SVRB enjoys a sample complexity of for finding an epsilon-stationary point. The logarithmic factor can be removed by setting as a fixed value at the level of . It is also notable that the step sizes for and are at the same level, which is referred to as single time-scale. The proof is included in the Appendix A.

4 SBO with Many Lower-level Problems

In this section, we present an randomized algorithm by extending the algorithm in last section for tackling SBO with many lower-level problems, i.e.,

Regarding the above problem, we make the following assumptions.

Assumption 3

For any , is -smooth and -strongly convex function, i.e., .

Assumption 4

For we assume the following conditions hold

-

•

is -Lipschitz continuous, is -Lipschitz continuous, is -Lipschitz continuous, is -Lipschitz continuous, is -Lipschitz continuous, all respect to .

-

•

, , , .

-

•

Assume is bounded such that , and for .

-

•

, where .

Remark: Note that the boundness assumption is similar to [3] except for . In order to ensure it bounded, we have an additional assumption that the optimal solutions to the lower problems are bounded and use this to ensure the boundness condition on holds.

The following proposition states the gradient of .

Proposition 2

Under Assumption 3, we have

An extra challenge for computing the gradient of is processing lower problems (sampling data and computing stochastic gradients). When is large, the cost of processing all lower problems would be prohibitive. Below, we will present an efficient algorithm for tackling bilevel optimization with many lower level problems.

4.1 Algorithm and Convergence

Motivation. From the above proposition, one might consider randomly sampling a lower problem and then using the gradient estimator of from the last section for the -th lower problem. However, the variance of compared with cannot be well controlled to ensure fast convergence. To address this issue, we use another layer of variance-reduced update (STORM) to approximate .

Based on the above motivation, we maintain a stochastic gradient estimator and update it by

where is a sampled lower problem at iteration for updating . At each iteration, we only need to make one non-trivial update of for a sampled . The detailed steps are presented in Algorithm 2.

Explanation of Algorithm 2. We let , , , , . Steps 4 - 9 of Algorithm 2 conduct updates for . Taking as an example. Its update is

where and satisfying

This step is applying the STORM technique for updating based on randomized stochastic unbiased estimators, where only one coordinate of the unbiased estimators is non-zero. We refer to this step as randomized-coordinate STORM (RC-STORM) update.

The RC-STORM update is the key to achieving efficiency, i.e., it only processes (non-trivially) one coordinate of for a sampled lower problem explicitly, where is sampled following a distribution . For other coordinates , are updated trivially, which are scaled by . This scaling can be delayed until it is sampled in the future since it is not used in updating presumably unless . In this case, there will be one more coordinate of that will be evaluated at most twice for the current and the last iteration. Overall, at each iteration, we only sample data from one lower problem to update the corresponding and evaluate trivially another coordinate at most twice without sampling data from the corresponding lower problem. Similar updates are applied to .

Next, we present the convergence of Algorithm 2 below. Define and , and similarly for other quantities. Let and .

Theorem 2

Suppose Assumptions 3 and 4 hold. With , , , , , , , , and , where are appropriate constants specified in the proof, and by using a large mini-batch size of at the initial iteration for computing and computing an accurate solution such that . Then, in order to have , we need a total sample complexity .

Remark: The above theorem implies that in order to find an epsilon stationary point, we need sample complexity, which is no worse than , and could be in a lower order if we could optimize over the sampling probability . The proof is included in the Appendix B.

5 Faster Convergence for Gradient-Dominant Functions

In this section, we present faster algorithms and their convergence for problems satisfying a stronger condition, namely the gradient dominant condition or Polyak-Łojasiewicz (PL) condition, i.e.,

To leverage the above condition for achieving a faster rate, we employ the restarting trick with a stagewise decreasing step size strategy. The procedure is described in Algorithm 3.

Theorem 3

Remark: It follows that the total sample complexity is . Similar to remark for Theorem 2, the sample complexity is no worse than . If , the dependence on and matches the optimal rate of to minimize a strongly convex problem, which is a stronger condition than PL condition. In contrast, to get , the STABLE algorithm [3] takes a complexity of , TTSA [13] takes , BSA [10] takes , all under the strong convexity, while ours only takes to achieve this under the PL condition.

6 Proof Sketch

Here we provide a proof sketch of the proposed algorithms and highlight the key differences from [3]. We start with Lemma 1 which follows standard analysis for non-convex optimization.

Lemma 1

Let . For , we have

The problem then reduces to bounding the error for the stochastic estimator . Then, we decompose this error into several terms and bound them separately.

Lemma 2

For all , we have

where are constants.

Next, we will bound each term in the RHS in the above inequality separately. For the last four terms, we use the analysis of STORM to bound the error. For the first term, we use Lemma 11 and Lemma 12. For bounding these terms, we will have a term in the upper bound that is proportional to and , where . In [3], the authors bound these two terms by their step sizes in the order of , which is in the order of the required accuracy bound for . However, the differences of our algorithms are that (i) the gradient estimators are not necessarily bounded (Algorithm 1) due to weaker boundness assumption in Assumption 2; (ii) even with similar boundness assumption in Assumption 4, our step size is in the order of (using fixed step size), which is one order larger than the required accuracy bound. Hence, using the step size to bound and as in [3] will not yield an improved sample complexity. To this end, we will use the following lemma to bound due to [15].

Lemma 3

Let with and satisfy Assumption 1, we have

7 Conclusions

In this paper, we have proposed a randomized stochastic algorithm for solving SBO with many lower level problems. We used a recursive variance reduction method for estimating all first-order and second-order moments. We achieved the state-of-the-art sample complexity for solving a class of SBO problems. One drawback of the proposed algorithms is that they need to compute the projection of a matrix onto a positive-definite matrix space with a minimum eigen-value, which could have a cubic time complexity in the worst case. For future work, we will consider reducing the worst-case per-iteration costs further.

References

- Arjevani et al. [2019] Yossi Arjevani, Yair Carmon, John C Duchi, Dylan J Foster, Nathan Srebro, and Blake Woodworth. Lower bounds for non-convex stochastic optimization. arXiv preprint arXiv:1912.02365, 2019.

- Chen et al. [2020] Tianyi Chen, Yuejiao Sun, and Wotao Yin. Solving stochastic compositional optimization is nearly as easy as solving stochastic optimization. arXiv preprint arXiv:2008.10847, 2020.

- Chen et al. [2021] Tianyi Chen, Yuejiao Sun, and Wotao Yin. A single-timescale stochastic bilevel optimization method. arXiv preprint arXiv:2102.04671, 2021.

- Colson et al. [2007] Benoît Colson, Patrice Marcotte, and Gilles Savard. An overview of bilevel optimization. Annals of Operations Research, 153(1):235–256, 2007.

- Cutkosky and Orabona [2019] Ashok Cutkosky and Francesco Orabona. Momentum-based variance reduction in non-convex SGD. In Advances in Neural Information Processing Systems 32 (NeurIPS), pages 15236–15245, 2019.

- Dua and Graff [2017] Dheeru Dua and Casey Graff. UCI machine learning repository, 2017. URL http://archive.ics.uci.edu/ml.

- Fallah et al. [2020] Alireza Fallah, Aryan Mokhtari, and Asuman Ozdaglar. On the convergence theory of gradient-based model-agnostic meta-learning algorithms. In International Conference on Artificial Intelligence and Statistics (AISTATS), pages 1082–1092, 2020.

- Fang et al. [2018] Cong Fang, Chris Junchi Li, Zhouchen Lin, and Tong Zhang. SPIDER: near-optimal non-convex optimization via stochastic path-integrated differential estimator. In Advances in Neural Information Processing Systems 31 (NeurIPS), pages 687–697, 2018.

- Franceschi et al. [2018] Luca Franceschi, Paolo Frasconi, Saverio Salzo, Riccardo Grazzi, and Massimiliano Pontil. Bilevel programming for hyperparameter optimization and meta-learning. In Proceedings of the 35th International Conference on Machine Learning (ICML), pages 1568–1577, 2018.

- Ghadimi and Wang [2018] Saeed Ghadimi and Mengdi Wang. Approximation methods for bilevel programming. arXiv preprint arXiv:1802.02246, 2018.

- Ghadimi et al. [2020a] Saeed Ghadimi, Andrzej Ruszczynski, and Mengdi Wang. A single timescale stochastic approximation method for nested stochastic optimization. SIAM J. Optim., 30(1):960–979, 2020a. doi: 10.1137/18M1230542. URL https://doi.org/10.1137/18M1230542.

- Ghadimi et al. [2020b] Saeed Ghadimi, Andrzej Ruszczynski, and Mengdi Wang. A single timescale stochastic approximation method for nested stochastic optimization. SIAM Journal on Optimization, 30(1):960–979, 2020b.

- Hong et al. [2020] Mingyi Hong, Hoi-To Wai, Zhaoran Wang, and Zhuoran Yang. A two-timescale framework for bilevel optimization: Complexity analysis and application to actor-critic. arXiv preprint arXiv:2007.05170, 2020.

- Hu et al. [2020] Yifan Hu, Siqi Zhang, Xin Chen, and Niao He. Biased stochastic first-order methods for conditional stochastic optimization and applications in meta learning. In Advances in Neural Information Processing Systems 33 (NeurIPS), 2020.

- Huang et al. [2020] Feihu Huang, Shangqian Gao, Jian Pei, and Heng Huang. Accelerated zeroth-order momentum methods from mini to minimax optimization. arXiv preprint arXiv:2008.08170, 2020.

- Huo et al. [2018] Zhouyuan Huo, Bin Gu, Ji Liu, and Heng Huang. Accelerated method for stochastic composition optimization with nonsmooth regularization. In Proceedings of the Thirty-Second AAAI Conference on Artificial Intelligence, (AAAI), pages 3287–3294, 2018.

- Ji et al. [2020] Kaiyi Ji, Junjie Yang, and Yingbin Liang. Provably faster algorithms for bilevel optimization and applications to meta-learning. arXiv preprint arXiv:2010.07962, 2020.

- Konda and Borkar [1999] Vijaymohan R Konda and Vivek S Borkar. Actor-critic–type learning algorithms for markov decision processes. SIAM Journal on Control and Optimization, 38(1):94–123, 1999.

- Kunapuli et al. [2008] Gautam Kunapuli, Kristin P Bennett, Jing Hu, and Jong-Shi Pang. Classification model selection via bilevel programming. Optimization Methods and Software, 23(4):475–489, 2008.

- Kunisch and Pock [2013] Karl Kunisch and Thomas Pock. A bilevel optimization approach for parameter learning in variational models. SIAM Journal on Imaging Sciences, 6(2):938–983, 2013.

- Liu et al. [2019] Hanxiao Liu, Karen Simonyan, and Yiming Yang. DARTS: Differentiable architecture search. In 7th International Conference on Learning Representations (ICLR), 2019.

- Liu et al. [2018] Liu Liu, Ji Liu, Cho-Jui Hsieh, and Dacheng Tao. Stochastically controlled stochastic gradient for the convex and non-convex composition problem. arXiv preprint arXiv:1809.02505, 2018.

- Liu et al. [2020a] Mingrui Liu, Zhuoning Yuan, Yiming Ying, and Tianbao Yang. Stochastic AUC maximization with deep neural networks. In 8th International Conference on Learning Representations (ICLR), 2020a.

- Liu et al. [2020b] Risheng Liu, Pan Mu, Xiaoming Yuan, Shangzhi Zeng, and Jin Zhang. A generic first-order algorithmic framework for bi-level programming beyond lower-level singleton. In Proceedings of the 37th International Conference on Machine Learning (ICML), pages 6305–6315, 2020b.

- Nguyen et al. [2017] Lam M Nguyen, Jie Liu, Katya Scheinberg, and Martin Takác. SARAH: A novel method for machine learning problems using stochastic recursive gradient. In Proceedings of the 34th International Conference on Machine Learning (ICML), pages 2613–2621, 2017.

- Platt [1999] John C. Platt. Fast training of support vector machines using sequential minimal optimization. 1999.

- Qi et al. [2020] Qi Qi, Zhishuai Guo, Yi Xu, Rong Jin, and Tianbao Yang. A practical online method for distributionally deep robust optimization. arXiv preprint arXiv:2006.10138, 2020.

- Qi et al. [2021] Qi Qi, Youzhi Luo, Zhao Xu, Shuiwang Ji, and Tianbao Yang. Stochastic optimization of area under precision-recall curve for deep learning with provable convergence. arXiv preprint arXiv:2104.08736, 2021.

- Rajeswaran et al. [2019a] Aravind Rajeswaran, Chelsea Finn, Sham Kakade, and Sergey Levine. Meta-learning with implicit gradients. arXiv preprint arXiv:1909.04630, 2019a.

- Rajeswaran et al. [2019b] Aravind Rajeswaran, Chelsea Finn, Sham M. Kakade, and Sergey Levine. Meta-learning with implicit gradients. In Advances in Neural Information Processing Systems 32 (NeurIPS), pages 113–124, 2019b.

- Sabach and Shtern [2017] Shoham Sabach and Shimrit Shtern. A first order method for solving convex bilevel optimization problems. SIAM Journal on Optimization, 27(2):640–660, 2017.

- Shaban et al. [2019] Amirreza Shaban, Ching-An Cheng, Nathan Hatch, and Byron Boots. Truncated back-propagation for bilevel optimization. In The 22nd International Conference on Artificial Intelligence and Statistics (AISTATS), pages 1723–1732, 2019.

- Wang et al. [2017a] Mengdi Wang, Ethan X Fang, and Han Liu. Stochastic compositional gradient descent: algorithms for minimizing compositions of expected-value functions. Mathematical Programming, 161(1-2):419–449, 2017a.

- Wang et al. [2017b] Mengdi Wang, Ethan X Fang, and Han Liu. Stochastic compositional gradient descent: algorithms for minimizing compositions of expected-value functions. Mathematical Programming, 161(1-2):419–449, 2017b.

- Yuan et al. [2020] Zhuoning Yuan, Yan Yan, Milan Sonka, and Tianbao Yang. Robust deep auc maximization: A new surrogate loss and empirical studies on medical image classification. arXiv preprint arXiv:2012.03173, 2020.

- Zhang and Xiao [2019] Junyu Zhang and Lin Xiao. A stochastic composite gradient method with incremental variance reduction. In Advances in Neural Information Processing Systems 32 (NeurIPS), pages 9075–9085, 2019.

- Zhou et al. [2019] Yi Zhou, Zhe Wang, Kaiyi Ji, Yingbin Liang, and Vahid Tarokh. Momentum schemes with stochastic variance reduction for nonconvex composite optimization. arXiv preprint arXiv:1902.02715, 2019.

Appendix

A Convergence Analysis of Theorem 1

In this section, we present the convergence analysis of Theorem 1. To this end, we will first present several technical lemmas.

Lemma 4

Let . For , we have

From the above lemma, we can see that the key to the proof of Theorem 1 is the bounding of . The lemma below will decompose this error into several terms that can be bounded separately.

Lemma 5

For all , we have

where , , , and .

Next, we will bound each term in the RHS in the inequality of the above lemma separately. We first bound the first term.

Lemma 6

Let with , we have

Based on this lemma, we derive the following lemma.

Lemma 7

Let , we have

For the last four terms in the RHS of the inequality in Lemma 5, we can use the following lemma about the variance reduced property of the STROM update.

Lemma 8

Suppose is a -Lipschitz continuous mapping, , and . For any sequence where , let , for an Euclidean norm ,

If for a convex set , let

Remark: The above lemma can be easily proved by following the analysis in [5]. Based on this lemma we have the following lemma.

Lemma 9

Let , we have

Proof [Proof of Theorem 1] First, we apply Lemma 9 to . We have

Set . To ensure , we need . Thus,

| (8) |

where the first inequality holds by the concavity of the function , i.e., , the second inequality is because . With ( for large enough constant . By combining the recursion of with , we have

where is given below.

To continue, we add the above recursion with the recursions for , , , , we have

With large enough constant , by setting , , , , (which means the constant ), we have

With and , we have , . As a result,

Adding the above inequality with that in Lemma 4, we have

With (), we have

As a result,

Thus,

According to the analysis in [5], we have

B Convergence Analysis of Theorem 2

In this section, we present the convergence analysis of Theorem 2. In the following, we let , , , , . By defining , we have is strongly convex in terms of . Hence Lemma 6, Lemma 7 still hold. The Lemma 4 also holds. The lemma below will decompose into several terms that can be bounded separately.

Lemma 10

For all , we have

where , , , and .

Next, we will bound each term in the RHS in the inequality of the above lemma separately. We first bound the first term.

Lemma 11

Assume

where , , , .

The following lemma bounds the last four terms in RHS in the inequalities of the above two lemmas.

Lemma 12

Let . We apply RC-STROM update to with unbiased stochastic estimators and , i.e., . Assume and is -Lipschitz continuous. Define and and . Then we have

and

Proof [Proof of Theorem 2] Define , , , , , , , , , according to that in Lemma 12 using Assumption 4. Let , , , , . We can see that . Define and .

Let . By the setting of , we have , with (where for small enough constant and large enough constant , where is given below). Set , , , , , and . With , all .

Adding all recursions for , , , and , we have

For the last four terms, we can bound them by

| (9) |

With (by ) and , we have

Adding the above inequality with that in Lemma 4 (noting that notation in this subsection is corresponding to in Lemma 4), we have

| (10) |

As a result,

| (11) |

where and . Dividing both sides by , we have

Note that . By choosing , , such that the maximum of , which can be achieved by using a large mini-batch at the beginning , and , which can be achieved by processing all lower problems at the beginning, , which can be achieved by computing the finding a good initial solution with accuracy with a complexity of . In the uniform sampling case, . The worse case iteration complexity is .

C Proof of Theorem 3

Proof Applying (11) in Appendix B, and defining a constant , we obtain that for any of the epochs,

| (12) |

From Theorem 2, we know that it is required that . Without loss of generality, let us assume that , i.e., . The case that can be simply covered by our proof. Then denote and .

In the first epoch (), we have initialization such that . In the following, we let the last subscript denote the epoch index. Setting and , we bound the error of the first stage’s output as follows,

| (13) |

where the first inequality uses (12) and the fact that the output of each epoch is randomly sampled from all iterations, and the last line uses the choice of . It follows that

| (14) |

Starting from the second stage, we will prove by induction. Suppose we are at -th stage. Assuming that the output of -th stage satisfies that and . We have

| (15) |

where the last inequality holds by the setting , .

It follows that

| (16) |

Thus, after stages, .

D Proof of Lemmas

D.1 Useful Lemmas

D.2 Proof of Lemma 4

Proof Due the smoothness of , we can prove that under

D.3 Proof of Lemma 5

Proof First, we have

where (a) uses the Lipschitz continuity of , , , , and upper bound of , , and . Next,

where , , and . As a result,

D.4 Proof of Lemma 6

Proof Define .

As a result,

| (17) |

Due to smoothness of , we have

Hence

Due to strong convexity of , we have

Combining the above inequalities we have

| (18) |

Note that . Since is a convex set and the function is convex in , according to the first order optimality condition of convex function, we have

| (19) |

Then we obtain

| (20) |

Thus,

Hence we have

where we use and . As a result,

where we use .

D.5 Proof of Lemma 10

where the last inequality can be proven as in Lemma 5 with , , , and .

D.6 Proof of Lemma 11

Proof

where , , , .

D.7 Proof of Lemma 12

Proof

E Preliminary Experiments

In this section, we present some preliminary experiments to verify the effectiveness of the proposed algorithms.

E.1 One Lower-level Problem

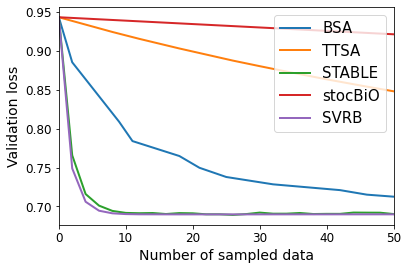

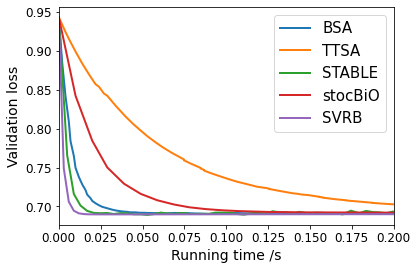

We consider an application of hyper-parameter optimization in machine learning (ML). A potential problem in ML is that the distribution of training examples might not be the same as the testing data. In this case, it could be beneficial to assign non-uniform weights to training examples to account for the difference between training set and testing set. The non-uniform weights will be learned to minimize the error on a separate validation data. In particular, we consider the following formulation:

where and are the training and validation dataset, and is the logistic loss for clasification. To evaluate the algorithms, we consider two UCI Adult benchmark datasets (a1a, a8a) and two web page classification datasets (w1a, w8a) [6, 26]. The prediction task of the Adult datasets is to determine whether a person makes over 50K a year based on binary attributes. Here a1a and a8a stand for different training and testing separation of the same data set. The webpage classification task is a text categorization problem, of which each input contains sparse binary keyword attributes extracted from each web page. Note that w1a and w8a differ in the similar way to a1a and a8a.

For our experiment, we use the testing test of each datas as the validation data for evaluating the convergence speed of different algorithms. For all algorithms, we use two step sizes, one step size updating the main variable and another step size for updating the variable for the lower problem. For all baselines except for STABLE, we set and , for STABLE, we use . The reason is that STABLE is the single time-scale algorithm. For SVRB, we use step sizes and use the same parameter for updating all gradient estimators. The constants , and are tuned in a range. For SVRB and STABLE, the Hessian inverse times a vector is implemented by the conjugated gradient algorithm.

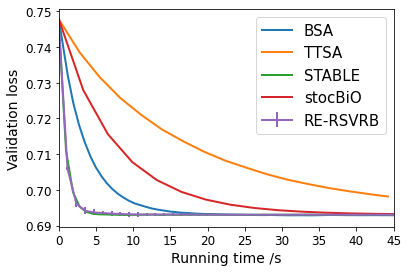

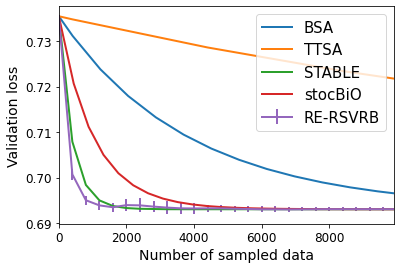

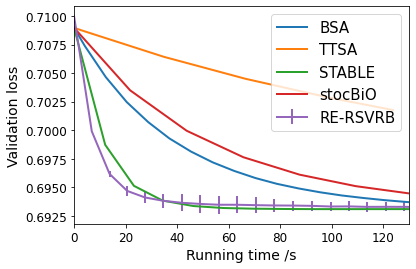

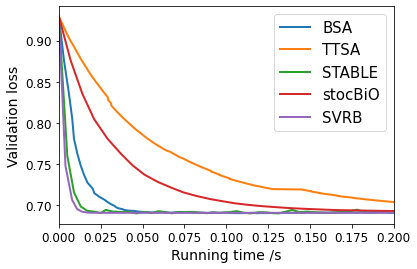

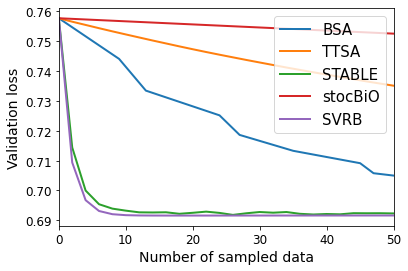

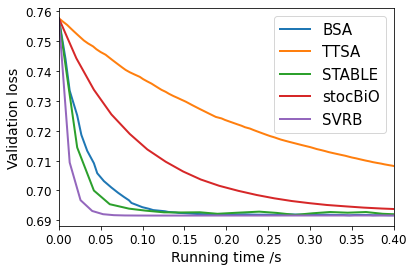

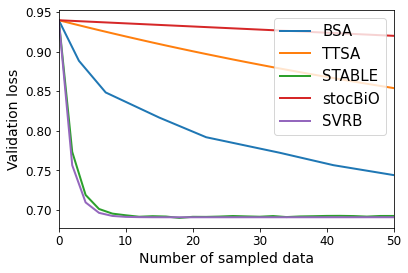

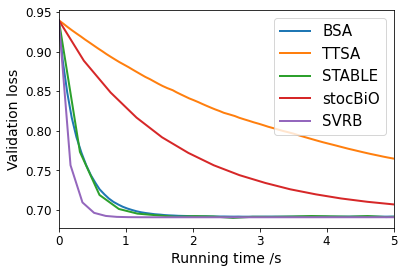

We report the results in Figure 1, where the top panel shows the validation loss (objective) vs the number of samples and the bottom panel shows validation loss (objective) vs running time. We can see tht the proposed SVRB achieves the fastest convergence rate among all algorithms in terms of running time and sample complexity.

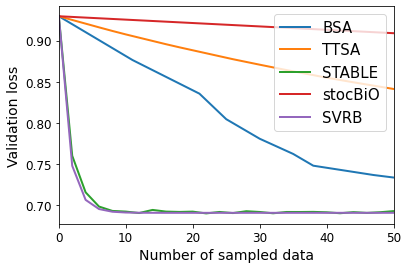

E.2 Many Lower-level Problems

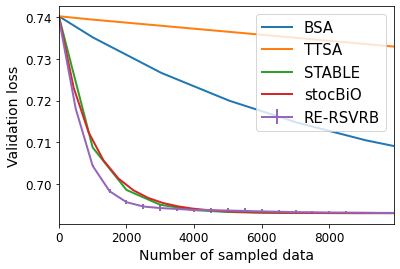

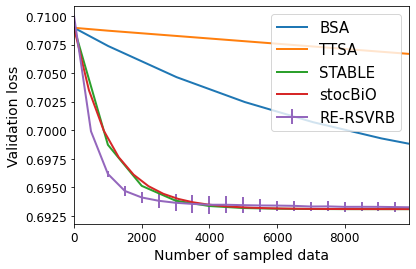

To conduct an experiment on the proposed algorithm RE-RSVRB for SBO with many lower-level problems, we consider an extension of hyper-parameter optimization with many different loss functions:

where the loss function is defined as

where is a temperature parameter. The step sizes are chosen in the similar way to the experiment for SBO with one lower-level problem.

For RE-RSVRB, we sample multiple lower problems (10 tasks) at each iteration for updating the model. We test the baselines and RE-RSVRB on two datasets, namely a1a and w1a. To control the time spent on the objective function value evaluations, we only choose data points from the testing part of each dataset as the validation data. Note that the size of validation data has minimal impact on the performance of the algorithms. The starting step size is tuned between and , and the constant in the update of is chosen from . The constants in the loss function are randomly generated from the interval and fixed. We use D-m as a shorthand of data set D with lower-level problems. It can be seen from Figure 2 that RE-RSVRB outperforms the baselines in most cases.