Stochastic gradient descent with noise of machine learning type

Part I: Discrete time analysis

Abstract.

Stochastic gradient descent (SGD) is one of the most popular algorithms in modern machine learning. The noise encountered in these applications is different from that in many theoretical analyses of stochastic gradient algorithms. In this article, we discuss some of the common properties of energy landscapes and stochastic noise encountered in machine learning problems, and how they affect SGD-based optimization.

In particular, we show that the learning rate in SGD with machine learning noise can be chosen to be small, but uniformly positive for all times if the energy landscape resembles that of overparametrized deep learning problems. If the objective function satisfies a Łojasiewicz inequality, SGD converges to the global minimum exponentially fast, and even for functions which may have local minima, we establish almost sure convergence to the global minimum at an exponential rate from any finite energy initialization. The assumptions that we make in this result concern the behavior where the objective function is either small or large and the nature of the gradient noise, but the energy landscape is fairly unconstrained on the domain where the objective function takes values in an intermediate regime.

Key words and phrases:

Stochastic gradient descent, almost sure convergence, Łojasiewicz inequality, non-convex optimization, machine learning, deep learning, overparametrization, global minimum selection2020 Mathematics Subject Classification:

Primary: 90C26, 90C15, Secondary: 68T07, 90C30, 60H301. Introduction

Stochastic gradient descent algorithms play an important role in convex and non-convex optimization. They are used in machine learning when the computation of the exact gradient of the objective function is computationally costly, but stochastic approximations can be evaluated fairly cheaply. The stochastic noise is furthermore believed to aid the algorithm in non-convex optimization by allowing it to escape ‘bad’ local minima and saddle points.

this work, we analyze toy models for stochastic gradient descent in machine learning applications. These differ from more classical perspectives principally in the fact that the intensity of noise in estimating depends on the value of the objective function. By comparison, more classical works on SGD assume uniform -bounds for , independently of . Our toy models are inspired by overparametrized supervised learning, i.e. minimization problems where the objective function vanishes on a high-dimensional set. In this setting, SGD with ML noise has the following novel properties:

-

(1)

The learning rate has to be small in terms of the smoothness of the objective function and the noise intensity, but can be uniformly positive for all time.

-

(2)

If the learning rate remains uniformly positive, we can prove almost sure convergence to a global minimizer, not just a critical point that is not a strict saddle.

Let us make these claims more precise. The crucial property of ML noise is that its variance scales at most linearly with the objective function . In particular, if is small, so is the noise. If satisfies a Łojasiewicz inequality (e.g. if is strongly convex), the learning rate has to be small enough for the noise to not exceed a certain strength, and compared to the Lipschitz constant of . It does not have to vanish asymptotically to guarantee convergence to the global minimum. In this sense, SGD with ML noise resembles deterministic GD more than it does SGD with classical noise. For details, see Theorem 3.1.

If the learning rate is strictly positive, at any time there are two options:

-

•

is small and so is the noise. If has good properties on the set for some , then with large probability we stay inside the set once we enter for the first time. Conditioned on this event, we expect to converge to a minimizer linearly.

-

•

is large and so is the noise. If has nice properties on the set for some , we expect SGD with ML noise to not let us escape to infinity despite the growing noise intensity. If additionally the set is not too spread out away from the set of minimizers and the noise is ‘uniformly unbounded’ (but with bounded variance), then from any point in there is a positive probability of jumping into the set independently of the local gradient.

This intuition can be extended and made precise. In particular, under strong conditions on the target function and noise, we find that we converge linearly to a minimizer almost surely from any finite energy initialization. However, since the probability of jumping into the set may be exceedingly small, we note that we do not expect to observe this linear convergence on realistic time scales in complicated real world applications for poor initialization. A precise statement of our main result can be found in Theorem 3.6.

Stochastic gradient descent can be studied as a general tool in convex and non-convex optimization or specifically in the context of deep learning applications. In this article, we take a balanced approach by incorporating key features of the energy landscape and stochastic noise in deep learning problems, but without specializing to a specific machine learning model.

The article is structured as follows. In Section 2, we review known results on stochastic gradient descent and objective functions in deep learning. We deduce some properties of the energy landscape and stochastic noise which a suitable toy model should satisfy. Discrete time SGD with ML noise is discussed in Section 3. Numerical examples in Section 4 illustrate the difference of SGD with classical and ML noise in a toy problem. Some proofs are postponed to the appendices. Continuous time results on continuous time SGD with noise of ML type are presented in a companion article [Woj21].

The different parts of the article – analysis of energy landscape and noise, discrete time analysis – can be read independently, and a reader only interested in one chapter can easily skip ahead.

1.1. Context

Stochastic gradient descent algorithms have been an active field of research since their inception in the seminal paper [RM51]. Stochastic gradient descent (SGD) and advanced gradient descent-based optimization schemes with stochastic gradient estimates have been the subject of increased attention recently due to their relevance in neural network-based machine learning, see e.g. [DDB17, NWS14, VBS19, WWB19, XWW20, DBBU20, AZ17, MB11, RSS11, JKNvW21, GLZ16, GL13, FGJ20, BCN18, BAWA18, BM13] and many more. A good literature review can be found in [FGJ20].

Theoretic guarantees for the convergence of SGD can be split into two categories:

-

•

For convex target functions, SGD converges to the global minimum.

-

•

For smooth non-convex target functions, SGD converges to a critical point, which is not a strict saddle.

Both types of guarantee can be obtained under different conditions and either in expectation or almost surely, and both can be complemented with sharp rates. We review results of both types in Section 2.1. Results may hold for the final iteration of SGD, the best parameter along the SGD trajectory up to time , or a weighted average of previous positions of SGD. We focus on guarantees for the final position since a list of previous values, or even a non-trivially weighted average of previous positions, is expensive to maintain in deep learning, where a model may have millions of parameters.

Recently, it has been noted in the SGD literature [KNS16] that convexity can be replaced by the condition that the objective function satisfies a Łojasiewicz-inequality, i.e.

| (1.1) |

This advance is particularly crucial since objective functions in deep learning typically have complicated geometries where the set of global minimizers is a submanifold of high dimension and co-dimension. Such functions are not usually convex, even in a neighbourhood of a minimizer.

The inequality (1.1) holds in particular for all strongly convex functions, but may not hold for smooth convex functions, e.g. . Like for convex functions, the only critical points of a function satisfying a Łojasiewicz inequality lie in the set of global minimizers. The assumption of a global Łojasiewicz inequality thus remains restrictive, and other models, e.g. functions satisfying local Łojasiewicz inequalities at the critical level sets have been considered [DK21].

Classically, the only assumption on SGD noise is a uniform second moment bound. In this work, we consider more realistic noise model inspired by deep learning applications. In this setting, we can prove convergence to the global minimum for a more general class of functions which are neither required to be convex, nor to satisfy a Łojasiewicz inequality. In this sense, we prove a first type guarantee under weaker second type assumptions.

While we obtain fast (linear) convergence to the global minimum

which is typical in the stochastic setting, we note that the random variable is typically too large to yield meaningful bounds in practice, unless the target function and noise have particularly convenient properties. Nevertheless, the fast convergence allows us to circumvent a common ‘staying local’ assumption, which is automatic for exponentially decaying sequences.

The guarantees we obtain hold almost surely (i.e. with probability ) over the choice of initial condition and stochastic gradient optimization. The importance of almost sure statements in this context has for example been emphasized in [Pat20] in the context of deriving stopping criteria which are ‘triggered’ with probability .

1.2. Notation and conventions

All random variables are defined on a probability space which remains abstract and is characterized mostly as expressive enough to support a random initial condition and countably many iid copies of a random variable to select a gradient estimator. The dyadic product of two vectors is denoted by

2. Energy landscapes and stochastic noise in machine learning

2.1. A brief review of stochastic gradient descent

Stochastic gradient descent algorithms are a class of popular algorithms in machine learning to find minimizers of an objective function . Instead of taking a small step in the direction in every iteration, we choose the update direction randomly according to a random variable with expectation and suitable -bounds for some .

More formally, we consider the following model.

-

(1)

is a -function

-

(2)

satisfies the one-sided Lipschitz-condition

-

(3)

is a probability space and is a family of functions such that

-

(a)

for all and

-

(b)

for all .

-

(a)

The SGD algorithm associated to the family of gradient estimators is given by the time-stepping scheme

| (2.1) |

where

-

(1)

the initial condition is a random variable in ,

-

(2)

is the learning rate (or time step size) in the -th time step, and

-

(3)

is a family of random variables in with law , which are iid and independent of .

In theoretical works, we typically consider decaying learning rates. This is rooted in results such as this, originating from [RM51].

Theorem 2.1.

Assume that is Lipschitz-continuous with constant and that

-

•

is convex or

-

•

satisfies the Łojasiewicz inequality for some .

If

| (2.2) |

and the learning rates satisfy the Robbins-Monro conditions

then . If satisfies the Łojasiewicz inequality and , then

A proof for the Łojasiewicz case (which in particular contains the uniformly convex case) can be found in [KNS16, Theorem 4], albeit under the assumption that is uniformly bounded, which contradicts the assumption that satisfies a Łojasiewicz inequality (unless is constant). This can be weakened to the assumption that the noise has bounded variance [BCN18].

The first summation condition is equivalent to stating that we are solving a gradient-flow type equation on the entire real line. Violating it would introduce a finite time horizon, which would prevent convergence to the minimizer as even in the non-stochastic setting and even for smooth and strongly convex objective functions. The second condition guarantees that the impact of gradient noise diminishes sufficiently as such that the iterates are not driven away from the global minimum in the long term by random oscillations. Unlike the first condition, it can be weakened [KY03, Chapter 5]. It has been suggested that the learning rate decay is optimal [LTW17, Section 4.1.2].

If the objective function is non-convex and does not satisfy a Łojasiewicz inequality, convergence to a critical point which is not a strict saddle can be guaranteed under suitable conditions on and . We only give an imprecise statement.

Theorem 2.2.

[MHKC20] Under suitable conditions on the objective function and a condition of the type , the following holds: If for some , then

-

(1)

converges to a random variable almost surely and lies in the set of critical values of almost surely.

-

(2)

almost surely.

-

(3)

for every trajectory of SGD, there exists a connected component of the set of critical points of such that .

-

(4)

If is a connected component of the set of critical points of such that has a negative eigenvalue for all (a ridge manifold), then .

In particular, an isolated strict saddle point is a zero-dimensional ridge manifold. Stronger statements, including a rate of convergence, are available at isolated local minima. The conditions on posed in [MHKC20] are neither implied by our assumptions, nor are they more general. While sublevel sets of have to be compact in [MHKC20] but not for us, we impose stronger conditions on the gradient away from the set of minimizers.

In practice, we typically choose learning rates according to a schedule of the form for , for , …with a discrete set of switching times and learning rates . Generally, the learning rates are chosen as large as possible without inducing numerical instability, and it is realistic to consider the setting where the learning rate is reduced only a finite number of times.

We consider the setting where even in the long term limit, the learning rate remains strictly positive. Under the conditions of Theorem 2.1, we find that the energy quickly decays below a threshold depending on the learning rate.

Theorem 2.3.

2.2. On energy landscapes in machine learning

Consider a parameterized function class

where is the space of parameters, is the space in which the data is given, and is a target space. In supervised learning problems, we seek to minimize functions of the form

where

-

(1)

is our training set of data/output or data/label pairs in ,

-

(2)

denotes the parameters of our function model, and

-

(3)

is a positive function.

We use to establish a concept of similarity on and optimize in order to make “similar” to with respect to , i.e. to make small.

Remark 2.4.

Depending on the context, both and are referred to as the loss function. At times, is referred to as ‘risk’ and denoted by the symbol instead.

Example 2.5.

The prototypical example of a loss function in our context is MSE (mean squared error)/-loss

Another popular loss function in the setting of classification problems is softmax cross entropy loss

The energy landscapes in both types of learning problems are quite different since cross entropy loss is never zero (see 2.11 for more details) and our results do not apply in the second setting.

In this article, we focus on -type losses. Note that

We give a modified version of a theorem of Cooper [Coo18, Theorem 2.1].

Theorem 2.6.

[Coo18] Assume that

-

(1)

the function model is overparametrized, i.e. ,

-

(2)

the function model is so expressive that for any collection of outputs there exists such that

-

(3)

is -smooth in .

Then for Lebesgue-almost any choice of , the set

is a closed -dimensional -submanifold of . If is Lipschitz-continuous in the first argument for every fixed and sufficiently overparameterized that it can fit arbitrary values at points, then is non-compact.

The conditions of this theorem are satisfied by certain overparametrized neural networks with smooth activation function [Coo18, Lemma 3.3], but also many other suitably expressive function classes. The condition is implicit in the assumptions on expressivity and smoothness of .

Proof.

We can write where

By assumption, is non-empty and if is a regular value of , then is a -manifold of dimension . Since is as smooth as , we can conclude by Sard’s theorem [Sar42] that Lebesgue-almost every is a regular value of . As the pre-image of a single point under a continuous map, is closed.

If is sufficiently overparametrized that it can fit values not only at but at points, then for any and there exists such that for . In particular, for any choice we have .

Let and associated indices in . Since

we see cannot be compact since achieving very different outputs requires very different parameters . ∎

We observe the following: If is convex, then the set of minimizers is convex. An -dimensional closed submanifold of is a convex set if and only if it is an -dimensional affine subspace of . If the map is generically non-linear, there is no reason to expect to be an affine space. Thus, we typically expect that is non-convex, even close to its set of minimizers. A rigorous statement on the non-convexity of objective functions in deep learning is given in Appendix A.

Thus, any toy model for the energy landscape of deep learning in overparametrized regression problems should have the following property: There exists a non-compact closed -manifold such that if and only if . We can think of both the dimension and co-dimension of as being large.

Remark 2.7.

While functions with these properties in general cannot be convex even in a neighbourhood of their set of minimizers, they may satisfy a Łojasiewicz inequality of the form

One such function is for any since

The assumption that a Łojasiewicz inequality holds is standard in non-convex optimization, but may not be realistic in machine learning, where complex energy landscapes with many local minima, maxima, ridges and saddle points are observed. For a fascinating demonstration of how diverse these energy landscapes can be, see [SB19].

However, we note that there are no critical points of high risk in square loss regression problems under very general conditions in the finite data or infinite data case.

Lemma 2.8.

Let be a probability distribution on with finite second moments (the data distribution). Assume that is a multi-layer perceptron with weights which maps to . Define the risk functional

Then there exists a constant such that

In particular, there exists such that

The function is an empirical risk functional if is a finite sum of Dirac deltas and a population risk functional otherwise.

Proof.

Let and the distribution of in if is distributed according to . Then

For a neural network, we can decompose and where is a neural network with one layer less than and is linear. If is larger than

then , so in particular . We can therefore compute

since the representation of is linear in , so . Consequently

The claim follows since . ∎

2.3. Łojasiewicz landscapes

We briefly discuss local Łojasiewicz conditions in machine learning and beyond. For sufficiently ‘nice’ objective functions, these can easily be seen to hold.

Example 2.9.

Assume that is -smooth and is a -manifold. Assume that

-

(1)

is globally Lipschitz-continuous on the set and

-

(2)

there exists such that for all and .

Then there exists such that satisfies a Łojasiewicz inequality on the set since

so if and we have

Since and due to the uniform Lipschitz bound, the smallness of the correction term is uniform over the set .

Example 2.10 (Quadratic regression).

For quadratic regression problems

we have

In particular if , the Hessian terms of drop out and

The upper bound is therefore satisfied on if the map is Lipschitz-continuous. The lower bound corresponds to the assumption that the vectors are bounded away from zero and bounded away from becoming linearly dependent. If this is the case, the lower bound

holds since lies in the -dimensional space spanned by . These assumptions correspond to a function model in which we can always change the parameters by a small amount and change the model output by a positive amount, and in which the output at different data points is principally governed by different parameters. The Lipschitz-condition on corresponds to the assumption that are Lipschitz-continuous and bounded.

Example 2.11 (Cross-entropy classification).

For classification problems, the cross-entropy loss function

never vanishes, so the energy landscape is fundamentally different from that of quadratic regression problems. We show that generally, a Łojasiewicz condition of the type cannot hold even for small values of the objective function.

The loss function

satisfies

With the counting density , we find that

so

Assume for the sake of contradiction that on the set . Then the solution of the gradient flow equation satisfies

In particular

if . In particular, is contained in a compact subset of and as , leading to a contradiction.

2.4. Random selection SGD

Consider a more general objective function of the form

where is a probability space and is a non-negative function such that

-

(G1)

for any fixed , the function is -measurable,

-

(G2)

for any fixed , the function is continuously differentiable, and

-

(G3)

for any compact set , there exists such that

-almost everywhere.

The assumptions guarantee that expectation and parameter gradient commute [Kön13, Section 8.4]. A particular gradient estimator is

since

Denote by the covariance matrix of the estimator :

which we assume is well-defined:

-

(G4)

for all we have .

This model encompasses machine learning problems as discussed above with

if the loss function and the data distribution are compatible via growth conditions and moment bounds.

2.5. SGD noise in machine learning

We make an obvious observation.

Lemma 2.12.

Assume there exists an -dimensional manifold such that for -almost all . Then everywhere on for the random selection gradient estimator.

Proof.

Since an , we find that is minimal at , so for all . Since there is no oscillation in the gradient estimator, the variance vanishes. ∎

Remark 2.13.

A popular toy model for SGD is the family of gradient estimators

where and is a standard Gaussian random variable. Unlike machine learning SGD, the estimators correspond to calculating exact gradients and deliberately perturbing them stochastically. Clearly, this toy model fails to capture key features of random selection SGD at the minimizing manifold.

We prove a more quantitative version of Lemma 2.12.

Lemma 2.14.

Let be a data distribution and a parametrized function model such that for -almost every . For a quadratic regression problem

the noise satisfies

For a cross-entropy classification problem

the noise satisfies

Proof.

Quadratic regression.

where . Under the assumption that is uniformly bounded on , we observe that

As a Corollary, also

since .

Remark 2.15.

Neural networks with layers can be decomposed as

where is a neural network with layers and is a nonlinear map between vector spaces. In particular

i.e. also the gradient of with respect to deep layer weights is linear in the final linear weights. The derivative has to be interpreted as a diagonal matrix. By the chain rule, the linearity extends to the gradient of the loss function. The assumption that independently of and is therefore unrealistic in deep learning, but a weaker assumption like

holds for two-layer neural networks with ReLU activation and deep networks (ResNets, multi-layer perceptra, …) if the activation function and its first derivative are bounded.

All statements above apply to both the overparametrized and underparametrized setting. A noise intensity which may scale with the objective function is a key feature of machine learning applications in general. The next result is specific to the overparametrized regime, where we show that the stochastic noise has low rank.

Lemma 2.16.

Under the same conditions as Theorem 2.6, we find that for all , independently of .

Proof.

If we set , then

is a sum of rank matrices. ∎

3. Stochastic gradient descent with ML noise in discrete time

3.1. Functions satisfying a Łojasiewicz inequality

It is easy to prove that if the noise in SGD is proportional to an objective function which satisfies a Łojasiewicz condition, SGD reduces with small, but fixed positive step size . The SGD scheme converges linearly, much like non-stochastic gradient descent. This is not a realistic model for machine learning, as Łojasiewicz inequalities rule out the presence of all critical points which are not the global minimum, but the same tools can be used in more complex topics below.

Theorem 3.1.

Assume the following.

-

(1)

satisfies the Łojasiewicz inequality

-

(2)

is -smooth and satisfies the one-sided Lipschitz-condition

-

(3)

The family of gradient estimators satisfies the following properties:

-

(a)

for all .

-

(b)

.

-

(a)

-

(4)

The initial condition is a random variable which satisfies the bound .

-

(5)

The random gradient selectors are iid with law and independent of .

If is generated by the SGD iteration law and , then

Furthermore almost surely for every .

We note that similar results for SGD with non-standard noise bounds have been proved in the uniformly convex setting in [SK20, Sti19].

Proof.

Expected objective value. Take to be fixed for now and . Then

Now we consider as the random variables they are in practice. We note that only depends on and is independent of . Thus in expectation

by the tower identity for conditional expectations. Hence

If , i.e. , we can estimate further that

or equivalently

The prefactor is smaller than if and only if

Almost sure convergence. The argument is standard for series with summable norms. Set

Then

satisfies

By taking , we observe that , i.e. almost surely. As this holds for all , we find that almost surely. ∎

The optimal learning rate if the constants are known satisfies

In the noiseless case , this boils down to the well-known estimate for deterministic gradient descent.

Corollary 3.2.

Assume that and are like in Theorem 3.1. Then converges to a random variable in and almost surely. The rate of convergence is

almost surely.

Proof.

Note that

and that

Recall that

for non-negative functions with Lipschitz-continuous gradient (see e.g. Lemma B.1 in Appendix C) and that

as above. Thus

i.e. the limit

exists in the -sense and

Since the increments are summable, the convergence is pointwise almost everywhere by the same argument as in Theorem 3.1. ∎

3.2. Convergence close to the minimum

Any function which has a critical point that is not the global minimum does not satisfy a Łojasiewicz inequality. However, if such an inequality holds close to the minimum and the initial condition is very close to the global minimum, then with high probability we converge to the minimum exponentially fast.

Theorem 3.3.

Assume that there exists such that the local Łojasiewicz inequality

holds on the set

and that is -Lipschitz continuous on . Then for every there exists such that the following holds: If almost surely, then with probability at least we have for all .

Conditioned on the event that for all , the estimate

holds almost surely for every

if the learning rate satisfies

The proof idea is as follows: In any iteration, we expect the objective value to decrease. While it may increase at times, it can only increase by small amounts as long as the objective value is small, and it is unlikely for errors to accumulate sufficiently for to exceed if is small enough. In the event that for all , we can follow along the lines of Theorem 3.1. The rigorous proof is a variation of that of [MHKC20, Theorem 4] and given in Appendix C. The main difference to the original is that the error is controlled by a decaying learning rate in [MHKC20] and by the low noise intensity for low objective value in our context. If the set has multiple connected components, of course the Łojasiewicz inequality and Lipschitz-condition are only required to hold locally as the result is local in nature.

Remark 3.4.

A version of Corollary 3.2 holds also in this case with virtually the same proof, conditioned on the event that for all .

3.3. On the global convergence of SGD with ML noise

Whether SGD converges to a global minimum even with poor initialization if the target function does not satisfy a Łojasiewicz inequality is quite delicate and requires strong assumptions. In general, this cannot be guaranteed.

Example 3.5.

Consider the functions

For , the function has two minima of equal depth at . If is small but non-zero, the two local minima do not have equal depth. Assume that the gradient estimators are of the form

where is equal to or with equal probability. If

and is reasonably small, can never escape the potential well it started in.

The situation is different if the noise is unbounded and the objective function has particularly convenient properties not only at the set of global minimizers.

Theorem 3.6.

Let be a function such that

-

(1)

The set is not empty.

-

(2)

is -smooth and satisfies the one-sided Lipschitz condition

-

(3)

A Łojasiewicz inequality holds on the set where is small, i.e. there exist such that

-

(4)

A Łojasiewicz inequality holds on the set where is large, i.e. there exist such that

- (5)

Assume that the gradient noise satisfies the following:

-

(1)

The noise has ML type, i.e.

-

(2)

The noise is uniformly unbounded in the sense that

and there exists a continuous function such that satisfies

(3.7) independently of .

Finally, assume that the learning rate satisfies

Assume that is an initial condition such that . Then the estimate

holds almost surely for every

Proof sketch.

We use the Łojasiewicz inequality on the set to show that SGD iterates visit the set infinitely often almost surely. For , there exists a uniformly positive probability that the due to the condition on the noise to be sufficiently ‘spread out’ and on the set to be sufficiently close to . Thus for infinite time, we visit the set almost surely.

Once we enter , we remain trapped in the set with high probability by Theorem 3.3, and in that case, we almost surely observe that at a linear rate. Even if we leave from , we almost surely visit again. The probability to escape infinitely often vanishes, so we expect that for all for almost every realization of SGD for some random time . ∎

The full proof is given in Appendix D. With a variation of the proof of Corollary 3.2, the following can be obtained. Note that the rate of convergence depends only on the Łojasiewicz constant on the set where is small.

Corollary 3.7.

Assume that and are like in Theorem 3.6. Then converges to a minimizer of almost surely.

Remark 3.8.

Our results suggest that, in a fairly general class of functions, SGD with ML noise converges to a global minimizer exponentially fast (or at least that the objective function decays exponentially along SGD iterates). However, it may take a very long time to reach the set in which exponential convergence is achieved, especially if the dimension of the parameter space and the co-dimension of the minimizer manifold are both high.

We give a few simple examples of situations in which Theorem 3.6 can in fact be applied. Despite its weaknesses, we believe this mechanism to be a major driving factor behind the success of SGD in the machine learning of overparametrized neural networks.

Remark 3.9.

If the function satisfies the conditions of Theorem 3.6, noise of the form

is admissible, where where is standard Gaussian noise.

Example 3.10.

The following functions satisfy the conditions of Theorem 3.6, but do not satisfy a global Łojasiewicz inequality:

-

(1)

. The set of minimizers is a lattice, is bounded, and every minimizer is non-degenerate.

-

(2)

for any fixed . The only minimizer is at . Far away from the origin, the oscillatory perturbation becomes negligible in both and .

More generally, if is a perturbation of a quadratic form in the following sense, then Theorem 3.6 applies:

-

•

.

-

•

The set is a finite union of disjoint compact -manifolds (potentially of different dimensions). If , then has rank at and the smallest non-zero singular value of is bounded away from zero.

-

•

The perturbation becomes negligible at infinity, i.e. there exists a positive definite symmetric matrix such that

Also the first example could be generalized to small perturbations of periodic functions with non-degenerate minimizers.

Example 3.11.

The following functions do not satisfy the conditions of Theorem 3.6 since there are low energy points arbitrarily far away from the set of global minimizers:

In this one-dimensional setting, that problem could presumably be solved by appealing to the recurrence of random walks, but the situation is hopeless in analogous constructions in dimension three or higher.

Let us consider the conditions placed in Theorem 3.6 in the context of deep learning.

Remark 3.12.

- •

- •

- •

-

•

It is currently unknown to us whether the condition (5) that the set of low objective values is within a bounded tube around is generically satisfied or not. We offer the following rationale: Let such that . Choose additional points (assuming that is an integer) and set for . If the map

has a Lipschitz-continuous inverse, then there exists such that

-

(1)

for and for .

-

(2)

and are somewhat close as

Thus a condition of the type (5) may hold for nicely parametrized models, but the constant is expected to be somewhat large if the data set is large.

-

(1)

-

•

The type of noise specified in (3.7) is unrealistic in overparametrized learning models as it is omni-directional, whereas realistic noise is necessarily low rank due to Lemma 2.16. The fact that the noise is ‘spread out’ is needed to guarantee that we may randomly ‘jump’ into the set from anywhere in the set . Identifying more realistic geometric conditions with similar guarantees remains an open problem.

Remark 3.13.

Theorem 3.6, were it to apply, could be viewed as a negative result in the context of implicit regularization in machine learning. We can decompose the mean squared error population risk functional as

where is the risk minimizer in the class of measurable functions and is the minimum Bayes risk. If the distribution admits any uncertainty in the output given observations , then . However, in overparametrized learning the empirical risk

can be zero. Thus if is large and the parameters of a model are trained by SGD with small positive learning rate, then after a long time, we expect and to differ greatly at the parameters . To avoid overfitting the training data, we therefore require an early stopping strategy. If the observations are virtually noiseless (which is the case for benchmark image classification problems), then this rationale may not apply, and SGD may perform well without early stopping.

4. A numerical illustration

We compare toy models for stochastic gradient descent

| (4.1) |

where is a learning rate, control the noise level, and is an is a standard Gaussian. For a fair comparison, and have to be chosen such that the noise has the same magnitude at a certain point of interest. Consider the function

where is a parameter and is chosen such that . For any , the function has two distinct local minima at and where . Clearly, we have .

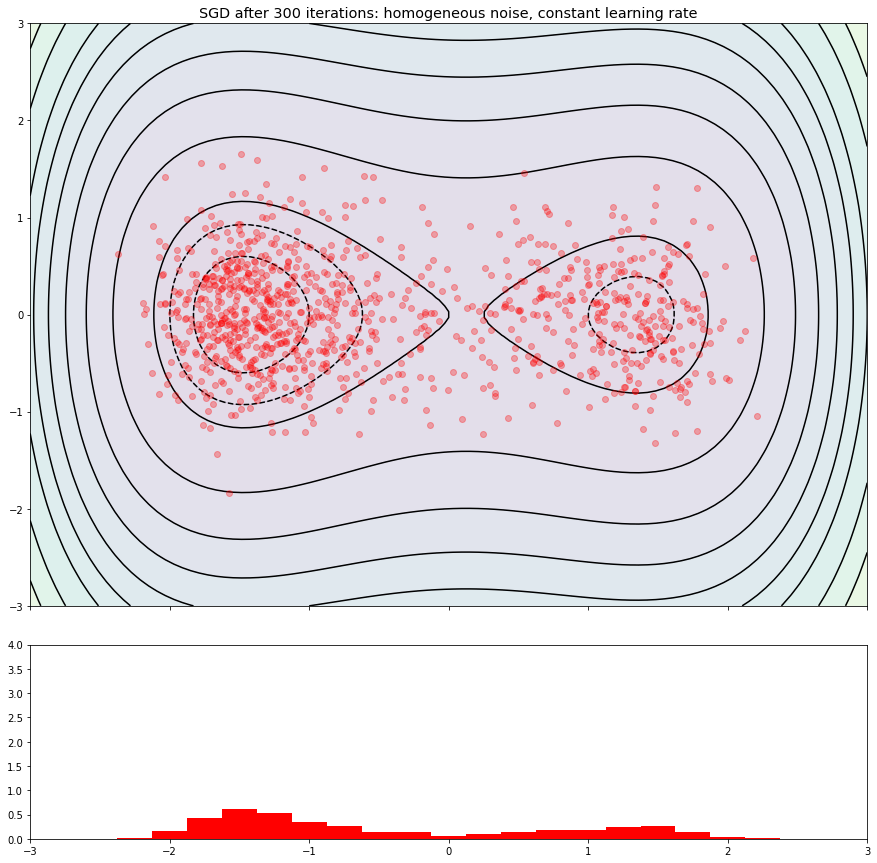

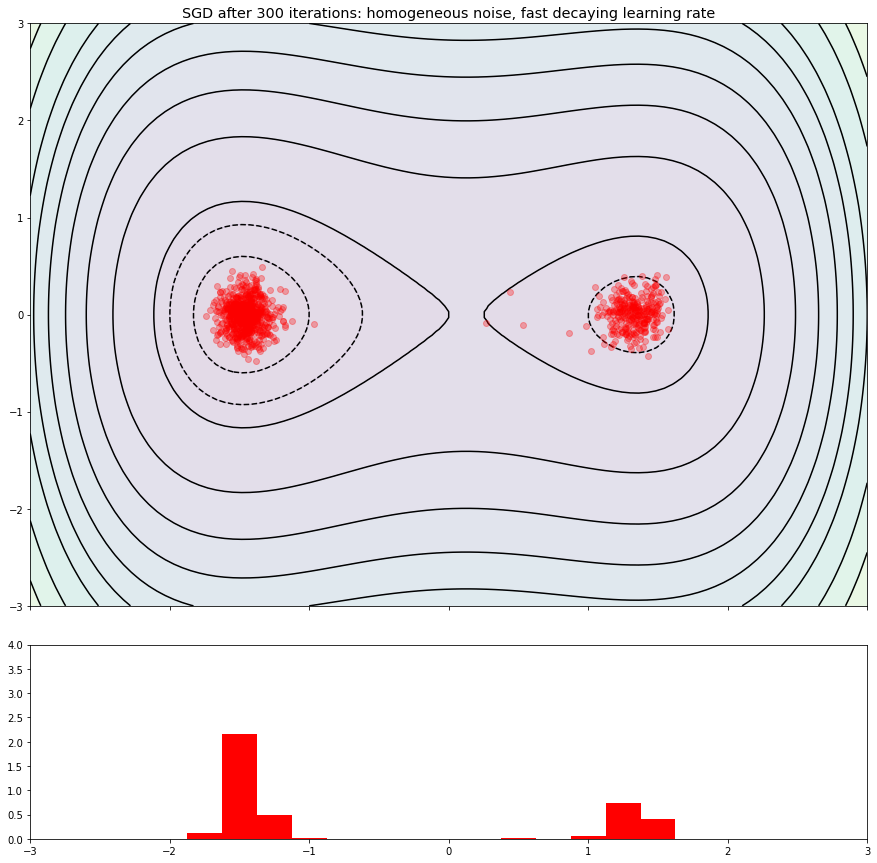

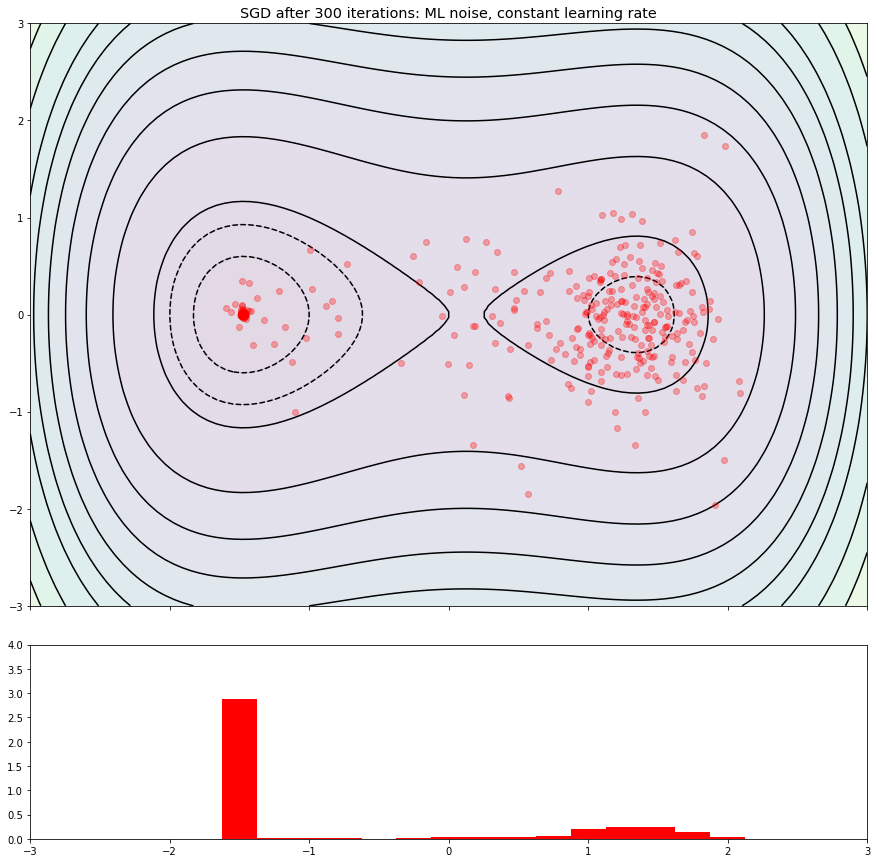

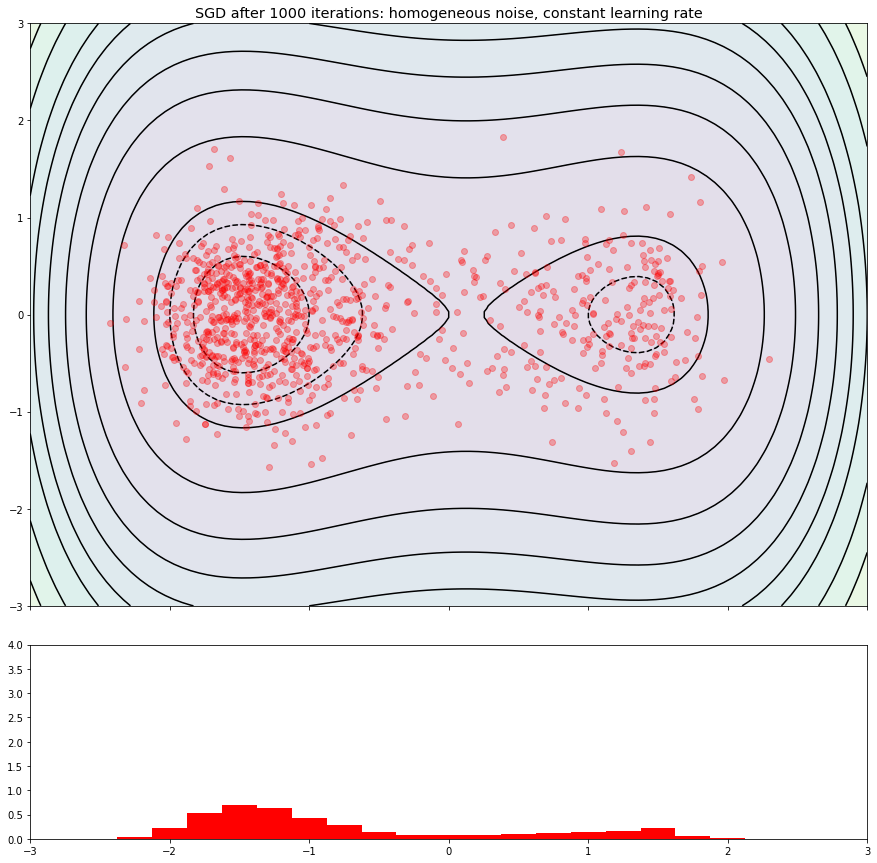

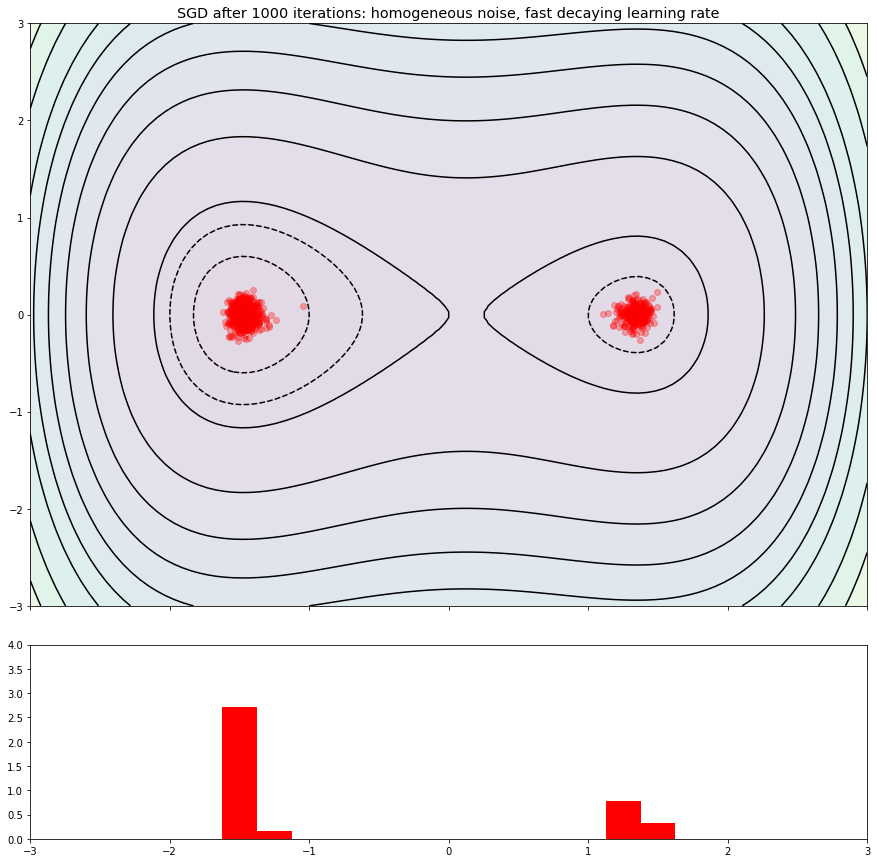

We considered 1000 realizations of SGD according to the schemes (4.1) with , learning rate and noise . The parameter was chosen such that the noise at the ridge between the minima of has the same intensity for both algorithms to give them equal opportunity to escape the local minimum. In all runs, the initial condition was .

In Figure 1, we see that SGD with ML type noise and constant learning rate approaches the global minimum rapidly whereas SGD with homogeneous Gaussian noise and constant learning rate forms a cloud around the minima which has higher density at the global minimum. SGD with homogeneous noise and decaying learning rate forms more focussed clouds around the minima, but about 25% of trajectories do not escape the local minimum. The decaying learning rate is chosen as

| (4.2) |

We make similar observations if the learning rate decays of the same order but less rapidly with and , but with less focussed point clouds.

After 300 iterations, the point cloud of SGD with homogeneous noise and positive learning rate is comparable to that of SGD with ML noise at the local minimum. This seems to be due to the fact that both start closer to the local minimum and are equally likely to escape the local minimum due to our scaling of the noise.

Once a trajectory of SGD with ML noise enters the potential well of the global minimum, it is unlikely to escape, whereas SGD with homogeneous Gaussian noise exchanges particles back and forth between the two wells. Once within the potential well of the global minimum, a trajectory of SGD with ML noise converges to the global minimum rapidly. Therefore, after 1000 iterations, trajectories of SGD with ML noise are almost guaranteed to have found the global minimum, whereas trajectories of SGD with homogeneous noise are somewhat likely to be found in the potential well of the local minimum, independently of whether the learning rate is constant or decaying.

5. Conclusion

More realistic abstract models for the noise of stochastic gradient descent in machine learning may explain help explain some of the success that SGD has enjoyed in this specific non-convex optimization task. We believe our results are indicate why SGD often finds global minima/low loss local minima rather than positive loss local minima.

Our results give an indication that it may be admissible in these applications to leave the learning rate uniformly positive. This may be particularly relevant for online learning tasks, where new data is added to the model. Decaying learning rates significantly diminish the effect that new data can have in finite time. The reason that the learning rate should be small in these optimization tasks is related both to the roughness of the loss landscape and the presence of stochastic noise. The estimates resemble non-stochastic gradient descent more closely than SGD with homogeneous noise estimates.

There are several pressing questions that were not explored in this work, both on the theoretical and practical side.

-

(1)

The biggest deficiency of our global convergence result is the reliance on omni-directional noise while realistic noise in machine learning SGD is low rank, at least for overparametrized models. Understanding the geometry of realistic noise and its impact on the convergence of SGD is an important open problem.

-

(2)

The objective functions we employ serve as toy models for the energy landscape of -regression problems in deep learning. The energy landscape of classification problems and the associated gradient noise are quite different as noted in Example 2.5 and Lemma 2.14. Understanding the behavior of SGD in classification-like loss landscapes and noise models remains an open problem.

-

(3)

While our assumptions are fairly general in the context of optimization theory, they likely are too restrictive in the setting of deep learning. Understanding the geometry of deep learning problem, and whether they allow for similar results, is the next important step in this approach to the analysis of SGD.

-

(4)

The Lipschitz-constant of the gradient of the objective function is not generally uniformly controlled over the parameter space. If a minimum is too steep, gradient descent may escape from it exponentially fast due to finite step size effects. This mechanism cannot be captured by continuum models and renders the positive step-size analysis invalid in the context of deep learning, unless we assume or enforce confinement to a bounded domain by other means.

-

(5)

In practice we do not use random selection SGD (choosing a batch of data samples randomly from the training set), but random pass SGD (passing through the entire training set batch by batch before repeating the same data point). The random directions in consecutive iterations are therefore not truly iid, and the noise may be less oscillatory in practice than random selection estimation would suggest. We believe the impact of this difference to be negligible for large data sets, but a rigorous connection has not been established to the best of our knowledge.

-

(6)

Typically, advanced optimizers like gradient descent with momentum, Nesterov’s accelerated gradient descent or ADAM are used in deep learning with stochastically estimated gradients. It remains to be seen whether noise of ML type allows for stronger estimates and global convergence guarantees also in that setting.

-

(7)

The main goal of this article was to understand SGD in toy models inspired by problems of deep learning. Another interesting direction is whether artificially perturbing (exact or estimated) gradients by omni-directional noise of ML type can improve the convergence of a gradient descent type optimization algorithm.

References

- [AZ17] Z. Allen-Zhu. Natasha 2: Faster non-convex optimization than sgd. arXiv preprint arXiv:1708.08694, 2017.

- [BAWA18] J. Bernstein, K. Azizzadenesheli, Y.-X. Wang, and A. Anandkumar. Convergence rate of sign stochastic gradient descent for non-convex functions. 2018.

- [BCN18] L. Bottou, F. E. Curtis, and J. Nocedal. Optimization methods for large-scale machine learning. Siam Review, 60(2):223–311, 2018.

- [BM13] F. Bach and E. Moulines. Non-strongly-convex smooth stochastic approximation with convergence rate o (1/n). arXiv preprint arXiv:1306.2119, 2013.

- [Coo18] Y. Cooper. The loss landscape of overparameterized neural networks. arXiv:1804.10200 [cs.LG], 2018.

- [DBBU20] A. Défossez, L. Bottou, F. Bach, and N. Usunier. On the convergence of adam and adagrad. arXiv preprint arXiv:2003.02395, 2020.

- [DDB17] A. Dieuleveut, A. Durmus, and F. Bach. Bridging the gap between constant step size stochastic gradient descent and markov chains. arXiv preprint arXiv:1707.06386, 2017.

- [DK21] S. Dereich and S. Kassing. Convergence of stochastic gradient descent schemes for lojasiewicz-landscapes. arXiv preprint arXiv:2102.09385, 2021.

- [FGJ20] B. Fehrman, B. Gess, and A. Jentzen. Convergence rates for the stochastic gradient descent method for non-convex objective functions. Journal of Machine Learning Research, 21, 2020.

- [GL13] S. Ghadimi and G. Lan. Stochastic first-and zeroth-order methods for nonconvex stochastic programming. SIAM Journal on Optimization, 23(4):2341–2368, 2013.

- [GLZ16] S. Ghadimi, G. Lan, and H. Zhang. Mini-batch stochastic approximation methods for nonconvex stochastic composite optimization. Mathematical Programming, 155(1-2):267–305, 2016.

- [HIMM19] Y.-G. Hsieh, F. Iutzeler, J. Malick, and P. Mertikopoulos. On the convergence of single-call stochastic extra-gradient methods. arXiv preprint arXiv:1908.08465, 2019.

- [HIMM20] Y.-G. Hsieh, F. Iutzeler, J. Malick, and P. Mertikopoulos. Explore aggressively, update conservatively: Stochastic extragradient methods with variable stepsize scaling. arXiv preprint arXiv:2003.10162, 2020.

- [JKNvW21] A. Jentzen, B. Kuckuck, A. Neufeld, and P. von Wurstemberger. Strong error analysis for stochastic gradient descent optimization algorithms. IMA Journal of Numerical Analysis, 41(1):455–492, 2021.

- [Kle06] A. Klenke. Wahrscheinlichkeitstheorie, volume 1. Springer, 2006.

- [KNS16] H. Karimi, J. Nutini, and M. Schmidt. Linear convergence of gradient and proximal-gradient methods under the polyak-łojasiewicz condition. In Joint European Conference on Machine Learning and Knowledge Discovery in Databases, pages 795–811. Springer, 2016.

- [Kön13] K. Königsberger. Analysis 2. Springer-Verlag, 2013.

- [KY03] H. Kushner and G. G. Yin. Stochastic approximation and recursive algorithms and applications, volume 35. Springer Science & Business Media, 2003.

- [LTW17] Q. Li, C. Tai, and E. Weinan. Stochastic modified equations and adaptive stochastic gradient algorithms. In International Conference on Machine Learning, pages 2101–2110. PMLR, 2017.

- [MB11] E. Moulines and F. Bach. Non-asymptotic analysis of stochastic approximation algorithms for machine learning. Advances in neural information processing systems, 24:451–459, 2011.

- [MHKC20] P. Mertikopoulos, N. Hallak, A. Kavis, and V. Cevher. On the almost sure convergence of stochastic gradient descent in non-convex problems. arXiv preprint arXiv:2006.11144, 2020.

- [NWS14] D. Needell, R. Ward, and N. Srebro. Stochastic gradient descent, weighted sampling, and the randomized kaczmarz algorithm. Advances in neural information processing systems, 27:1017–1025, 2014.

- [Pat20] V. Patel. Stopping criteria for, and strong convergence of, stochastic gradient descent on bottou-curtis-nocedal functions. arXiv preprint arXiv:2004.00475, 2020.

- [RM51] H. Robbins and S. Monro. A stochastic approximation method. The annals of mathematical statistics, pages 400–407, 1951.

- [RSS11] A. Rakhlin, O. Shamir, and K. Sridharan. Making gradient descent optimal for strongly convex stochastic optimization. arXiv preprint arXiv:1109.5647, 2011.

- [Sar42] A. Sard. The measure of the critical values of differentiable maps. Bulletin of the American Mathematical Society, 48(12):883–890, 1942.

- [SB19] I. Skorokhodov and M. Burtsev. Loss landscape sightseeing with multi-point optimization. arXiv preprint arXiv:1910.03867, 2019.

- [SK20] S. U. Stich and S. P. Karimireddy. The error-feedback framework: Better rates for sgd with delayed gradients and compressed updates. Journal of Machine Learning Research, 21:1–36, 2020.

- [Sti19] S. U. Stich. Unified optimal analysis of the (stochastic) gradient method. arXiv preprint arXiv:1907.04232, 2019.

- [VBS19] S. Vaswani, F. Bach, and M. Schmidt. Fast and faster convergence of sgd for over-parameterized models and an accelerated perceptron. In K. Chaudhuri and M. Sugiyama, editors, Proceedings of the Twenty-Second International Conference on Artificial Intelligence and Statistics, volume 89 of Proceedings of Machine Learning Research, pages 1195–1204. PMLR, 16–18 Apr 2019.

- [Woj21] S. Wojtowytsch. Stochastic gradient descent with noise of machine learning type. part ii: Continuous time analysis. arXiv:2106.02588 [cs.LG], 2021.

- [WWB19] R. Ward, X. Wu, and L. Bottou. Adagrad stepsizes: Sharp convergence over nonconvex landscapes. In International Conference on Machine Learning, pages 6677–6686. PMLR, 2019.

- [XWW20] Y. Xie, X. Wu, and R. Ward. Linear convergence of adaptive stochastic gradient descent. In International Conference on Artificial Intelligence and Statistics, pages 1475–1485. PMLR, 2020.

Appendix A On the non-convexity of objective functions in deep learning

Under general conditions, energy landscapes in machine learning regression problems have to be non-convex. The following result follows from Theorem 2.6.

Corollary A.1.

Assume that is a parameterized function model, which is at least -smooth in for fixed . Let where .

-

(1)

If is convex for every , the map is linear for all .

-

(2)

Assume that and that there exists such that has rank . Then for every , there exists such that and has a negative eigenvalue.

-

(3)

Assume that and that there exists such that has rank . Assume furthermore that the gradients are linearly independent. Then for every , there exists such that and has a negative eigenvalue.

The first statement is fairly weak, as the proof requires us to consider the convexity of far away from the minimum. The second statement shows that even close to the minimum, can be non-convex if the function model is sufficiently far from being ‘low dimensional’ – this statement concerns perturbations in . The third claim is analogous, but concerns perturbations in . It is therefore stronger, as it shows that is not convex in any neighborhood of a given point in the set of minimizers.

Proof.

First claim. Compute

If , there exists such that since the Hessian matrix is symmetric. Thus

meaning that cannot be convex. Thus if is convex for all , by necessity for all , i.e. is linear.

Second claim. Set for and . Then by a simple result in linear algebra (see Lemma A.3 below), the matrix

has a negative eigenvalue.

Third claim. Let . Since the set of gradients is linearly independent, there exists such that but . Thus to leading order

As before, we conclude that has a negative eigenvalue if is small enough. ∎

Remark A.2.

If is linear, then vanishes, i.e. . The large discrepancy between the conditions ensuring local convexity and global convexity is in fact necessary. Consider for all and

If is bounded and is fixed, then for every we can choose so small that is convex on . Note that the rank of is at most in this example.

We prove a result which we believe to be standard in linear algebra, but have been unable to find a reference for.

Lemma A.3.

Let be a symmetric positive definite matrix of rank at most . Let be a symmetric matrix of at least . Then, for every at least one of the matrices or has a negative eigenvalue.

Proof.

Without loss of generality, we assume that .

First case. The Lemma is trivial if there exists such that since then

is a linear function.

Second case. Assume that for all . Since has rank , there exists an eigenvector for a non-zero eigenvalue of such that . Without loss of generality, we may assume that . Consider

Thus, we choose the correct sign for depending on and , then

In this situation, is indefinite and the sign of does not matter. ∎

Appendix B Auxiliary observations on objective functions and Łojasiewicz geometry

Lemma B.1.

Assume that is a non-negative function and is Lipschitz continuous with constant . Then

Proof.

Take . The statement is trivially true at if , so assume that . Consider the auxiliary function

Then and

Thus

The bound on the right is minimal for when

Since also , so . ∎

Remark B.2.

In particular, If satisfies a Łojasiewicz inequality and has a Lipschitz-continuous gradient, then

| (B.1) |

We show that the class of objective functions which can be analyzed by our methods does not include loss functions of cross-entropy type under general conditions.

Corollary B.3.

Proof.

Choose and consider the solution of the gradient flow equation

Then

and thus . Furthermore

whence we find that converges to a limiting point as . By the continuity of , we find that

∎

Appendix C Proof of Theorem 3.3: Local Convergence

We split the proof up over several lemmas. Our strategy follows along the lines of [MHKC20, Appendix D], which in turn uses methods developed in [HIMM19, HIMM20]. We make suitable modifications to account for the fact that the smallness of noise comes from the fact that the values of the objective function are low, not that the learning rate decreases. Furthermore, we have slightly weaker control since we do not impose quadratic behavior with a strictly positive Hessian at the minimum, but only a Łojasiewicz inequality and Lipschitz continuity of the gradients.

While weaker conditions may hold for the individual steps of the analysis, we always assume that the conditions of Theorem 3.3 are met for the remainder section. We decompose the gradient estimators as

and interpolate for . With these notations, we can estimate the change of the objective in a single time-step as

where

All three variables scale like and the difference between them can be ignored for the essence of the arguments. As usual, we denote by the filtration generated by , with respect to which is measurable. We note that is a martingale difference sequence with respect to since

To analyze the over several time steps, we define the cumulative error terms

We furthermore define the events

for and . The sets are useful as they allow us to estimate the measure of , where all sets in the union are disjoint.

Lemma C.1.

The following are true.

-

(1)

and .

-

(2)

If for , then if .

-

(3)

Under the same conditions, the estimate

(C.1) holds, where the constant incorporates the factors between , and .

Proof.

The first claim is trivial.

Second claim. Recall that is initialized in . In particular is the entire probability space since the sum condition for is empty. We proceed by induction.

Assume that . Then in particular , so by the induction hypothesis. Thus it suffices to show that , i.e. to focus on the last time step. A direct calculation yields

Third claim. A simple algebraic manipulation shows that

since on . We recall that

and that

where the analysis of reduces to that of and the bound from Lemma B.1 was used. The result now follows by putting all estimates together. ∎

We now proceed to estimate the probability that the quadratic noise does not remain small by bounding the probability that it exceeds the given threshold in the -th step and summing over .

Lemma C.2.

The estimate

| (C.2) |

holds.

Proof.

First step. The probably that does not occur coincides with the probability that there exists some such that exceeds at , but not . More precisely

since is the whole space. Hence

Using and , we bound

| (C.3) |

since as a sum of squares.

Second step. From (C.1), we obtain

so by the telescoping sum identity

| (C.4) |

Note that the second term on the right hand side vanishes since the sum defining is empty.

Finally, we are in a position to prove the local convergence result.

Proof of Theorem 3.3.

Step 1. Since and , we have

where

as previously for functions which satisfy the Łojasiewicz inequality globally. We conclude from (C.4) that

Thus for every , there exists such that for all if almost surely.

Step 2. Consider the event

since and . Then

as in Step 1. We conclude that for every the estimate

holds almost surely conditioned on as in the proof of Theorem 3.1. ∎

Appendix D Proof of Theorem 3.6: Global Convergence

Again, we split the proof up over several Lemmas. First, we show that

We always assume that satisfies the conditions of Theorem 3.6, although weaker conditions suffice in the individual steps.

Lemma D.1.

If , the estimate

holds.

Proof.

Recall that for any we have

as in the proof of Theorem 3.1. We distinguish two cases:

-

•

If , then

-

•

If , then

due to the Łojasiewicz inequality on the set where is large.

In particular, since is non-negative, we have

where . If we abbreviate , we deduce that

Thus if is large, then decays. In fact

independently of the initial condition. ∎

Note that the finiteness of the bound hinges on the fact that the learning rate remains uniformly positive in this simple proof. In other variants of gradient flow, it can be non-trivial to control the possibility of escape.

The trajectories of SGD satisfy stronger bounds than the expectations.

Lemma D.2.

Proof.

Let

In particular, for all and for all . Thus

for any . Thus for all . Hence also

∎

We have shown that we visit the set infinitely often almost surely. We now show that in every visit , the probability that is uniformly positive. Below, we will use this to show that we visit the set infinitely often with uniformly positive probability (which then implies that SGD iterates approach the set of minimizers almost surely). In this step, we use that the noise is uniformly ‘spread out’.

Lemma D.3.

There exists such that the following holds: If , then

Proof.

We consider two cases separately: or . In the first case, we can argue by considering the gradient descent structure, while we rely on the stochastic noise in the second case.

First case. If , then

since satisfies a Łojasiewicz inequality in this region. In particular

Second case. By assumption, the set of moderate energy is not too far from the set of global minimizers in Hausdorff distance, i.e. there exists such that

-

(1)

and

-

(2)

.

Due to the Lipschitz-continuity of the gradient of , there exists depending only on such that for all . We conclude that

By assumption, the radius

is uniformly positive and the center of the ball

is in some large ball independent of . Thus the probability of jumping into , albeit small, is uniformly positive with a lower bound

∎

By Lemma D.2, the sequence of stopping times ,

is well-defined except on a set of measure zero. Consider the Markov process

Note that we use for odd times, not . To show the stronger statement that

we use the conditional Borel-Cantelli Lemma D.4.

Lemma D.4.

[Kle06, Übung 11.2.6] Let be a filtration of a probability space and a sequence of events such that for all . Define

Then where denotes the symmetric difference of and .

Corollary D.5.

Proof.

Consider the filtration generated by and the events

Then

except on the null set where is undefined for some . Thus , so almost surely there exist infinitely many such that . In particular, almost surely there exist infinitely many such that . ∎

We are now ready to prove the global convergence result.

Proof of Theorem 3.6.

Let and consider the event

Choose and associated . By Corollary D.5, the stopping time

is finite except on a set of measure zero. Consider as the initial condition of a different SGD realization and note that the conditional independence properties which we used to obtain decay estimates still hold for the gradient estimators with respect to the -algebras generated by the random variables for .

By Theorem 3.3, we observe that with probability at least , we have

Thus for any , with probability at least we have

Taking and , we find that almost surely

∎

We conclude by proving that not just the function values , but also the arguments converge.