Model Reduction for Large Scale Systems

Abstract.

Projection based model order reduction has become a mature technique for simulation of large classes of parameterized systems. However, several challenges remain for problems where the solution manifold of the parameterized system cannot be well approximated by linear subspaces. While the online efficiency of these model reduction methods is very convincing for problems with a rapid decay of the Kolmogorov n-width, there are still major drawbacks and limitations. Most importantly, the construction of the reduced system in the offline phase is extremely CPU-time and memory consuming for large scale and multi scale systems. For practical applications, it is thus necessary to derive model reduction techniques that do not rely on a classical offline/online splitting but allow for more flexibility in the usage of computational resources. A promising approach with this respect is model reduction with adaptive enrichment. In this contribution we investigate Petrov-Galerkin based model reduction with adaptive basis enrichment within a Trust Region approach for the solution of multi scale and large scale PDE constrained parameter optimization.

Key words and phrases:

PDE constraint optimization and reduced basis method and trust region method.1. Introduction

Model order reduction (MOR) is a very active research field that has seen tremendous development in recent years, both from a theoretical and application point of view. For an introduction and overview on recent development we refer e.g. to [4]. A particular promising model reduction approach for parameterized partial differential equations (pPDEs) is the Reduced Basis (RB) Method that relies on the approximation of the solution manifold of pPDEs by low dimensional linear spaces that are spanned from suitably selected particular solutions, called snapshots. For time-dependent problems, the POD-Greedy method [9] defines the Gold-Standard. As RB methods rely on so called efficient offline/online splitting, they need to be combined with supplementary interpolation methods in case of non-affine parameter dependence or non-linear differential equations. The empirical interpolation method (EIM) [3] and its various generalizations, e.g. [6], are key technologies with this respect. While RB methods are meanwhile very well established and analyzed for scalar coercive problems, there are still major challenges for problems with a slow convergence of the Kolmogorov N-width [13]. Such problems in particular include pPDEs with high dimensional or even infinite dimensional parameter dependence, multiscale problems as well as hyperbolic or advection dominated transport problems. Particular promising approaches for high dimensional parameter dependence and large or multiscale problems are localized model reduction approaches. We refer to [5] for a recent review of such approaches, including the localized reduced basis multiscale method (LRBMS) [15]. Several of these approaches have already been applied in multiscale applications, in particular for battery simulation with resolved electrode geometry and Buttler-Volmer kinetics [7]. Based on efficient localized a posteriori error control and online enrichment, these methods overcome traditional offline/online splitting and are thus particularly well suited for applications in optimization or inverse problems as recently demonstrated in [16, 14]. In the context of PDE constrained optimization, a promising Trust Region (TR) – RB approach that updates the reduced model during the trust region iteration has recently been studied in [17, 11, 2]. In the latter two contributions a new non-conforming dual (NCD) approach has been introduced that improves the convergence of the adaptive TR-RB algorithm in the case of different reduced spaces for the corresponding primal and dual equations of the first order optimality system.

While these contributions were all based on Galerkin projection of the respective equations, we will introduce a new approach based on Petrov-Galerkin (PG) projection in the following. As we will demonstrate in Section 2 below, the PG-reduced optimality system is a conforming approximation which allows for more straight forward computation of derivative information and respective a posteriori error estimates. In Section 3 we evaluate and compare the Galerkin and Petrov-Galerkin approaches with respect to the error behavior and the resulting TR-RB approaches with adaptive enrichment. Although the convergence of the TR-RB method can be observed for both approaches, the results demonstrate that the PG approach may require further investigation with respect to stabilization.

2. Petrov-Galerkin based model reduction for PDE constrained optimization

In this contribution we consider the following class of PDE constrained minimization problems:

| (P) |

| (P.a) | |||||

| subject to being the solution of the state – or primal – equation | |||||

| (P.b) | |||||

where denotes a parameter functional.

Here, denotes a real-valued Hilbert space with inner product and its induced norm , , with denotes a compact and convex admissible parameter set and a quadratic continuous functional. In particular, we consider box-constraints of the form

for given parameter bounds , where “” has to be understood component-wise.

For each admissible parameter , denotes a continuous and coercive bilinear form, are continuous linear functionals and denotes a continuous symmetric bilinear form. The primal residual of (P.b) is key for the optimization as well as for a posteriori error estimation. We define for given , , the primal residual associated with (P.b) by

| (1) |

Following the approach of first-optimize-then-discretize, we base our discretization and model order reduction approach on the first order necessary optimality system, i.e. (cf. [2] for details and further references)

| (2a) | |||||

| (2b) | |||||

| (2c) | |||||

From (2b) we deduce the so-called adjoint – or dual – equation

| (3) |

with solution for a fixed and given the solution to the state equation (P.b). For given , we introduce the dual residual associated with (3) as

| (4) |

2.1. Petrov-Galerkin based discretization and model reduction

Assuming to be a finite-dimensional subspaces, we define a Petrov-Galerkin projection of (P) onto by considering, for each , the solution of the discrete primal equation

| (5) |

and for given , the solution of the discrete dual equation as

| (6) |

Note that the test space of one equation corresponds with the ansatz space of the other equation. In order to obtain a quadratic system, we require . Note that a Ritz-Galerkin projection is obtained, if the primal and dual discrete spaces coincide, i.e. .

Given problem adapted reduced basis (RB) spaces of the same low dimension we obtain the reduced versions for the optimality system as follows:

We define the PG-RB reduced optimization functional by

| (8) |

with being the solution of (7a). We then consider the RB reduced optimization problem by finding a locally optimal solution of

| () |

Note that in contrast to the NCD-approach that has been introduced in [11, 2], we do not need to correct the reduced functional in our PG-RB approach, as the primal and dual solutions automatically satisfy . Actually, this is the main motivation for the usage of the Petrov-Galerkin approach in this contribution. In particular this results in the possibility to compute the gradient of the reduced functional with respect to the parameters solely based on the primal and dual solution of the PG-RB approximation, i.e.

| (9) |

for all and , where and denote the PG-RB primal and dual reduced solutions of (7a) and (7b), respectively. Note that in [17], the formula in (9) was motivated by replacing the full order functions by their respective reduced counterpart which resulted in an inexact gradient for the non-conforming approach. In the PG setting, (9) instead defines the true gradient of without having to add a correction term as proposed in [11, 2]. This also holds for the true Hessian which can be computed by also replacing all full order counterparts in the full order Hessian. In this contribution we however only focus on quasi-Newton methods that do not require a reduced Hessian.

2.2. A posteriori error estimation for an error aware algorithm

In order to construct an adaptive trust region algorithm we require a posteriori error estimation for (7a), (7b) and (8). For that, we can utilize standard residual based estimation. For an a posteriori result of the gradient , we also refer to [11].

Proposition 2.1 (Upper error bound for the reduced quantities).

Proof.

It is important to mention that the computation of these error estimators include the computation of the (parameter dependent) inf-sup constant of which involves an eigenvalue problem on the FOM level. In practice, cheaper techniques such as the successive constraint method [10] can be used. For the conforming approach , the inf-sup constant is equivalent to the coercivity constant of which can be cheaply bounded from below with the help of the min-theta approach, c.f. [8].

2.3. Trust-Region optimization approach and adaptive enrichment

Error aware Trust-Region - Reduced Basis methods (TR-RB) with several different advances and features have been extensively studied e.g. in [17, 11, 2]. They iteratively compute a first-order critical point of problem (P). For each outer iteration of the TR method, we consider a model function as a cheap local approximation of the quadratic cost functional in the so-called trust-region, which has radius and can be characterized by the a posteriori error estimator. In our approach we choose

for , where the super-index indicates that we use different RB spaces in each iteration. Thus, we can use for characterizing the trust-region. We are therefore interested in solving the following error aware constrained optimization sub-problem

| (10) | ||||

In our TR-RB algorithm we build on the algorithm in [11]. In the sequel, we only summarize the main features of the algorithm and refer to the source for more details. We initialize the RB spaces with the starting parameter , i.e. and . For every iteration point , we locally solve (10) with the quasi-Newton projected BFGS algorithm combined with an Armijo-type condition and terminate with a standard reduced FOC termination criteria, modified with a projection on the parameter space to account for constraints on the parameter space. Additionally, we use a second boundary termination criteria for preventing the subproblem from spending too much computational time on the boundary of the trust region. After the next iterate has been computed, the sufficient decrease conditions helps to decide whether to accept the iterate:

| (11) |

This condition can be cheaply checked with the help of an sufficient and necessary condition. If is accepted, we use the parameter to enrich the RB spaces in a Lagrangian manner, i.e. For more basis constructions, we refer to [2] where also a strategy is proposed to skip an enrichment. After the enrichment, overall convergence of the algorithm can be checked with a FOM-type FOC condition

where the FOM quantities are available from the enrichment. Moreover, these FOM quantities allow for computing a condition for possibly enlargement of the TR radius if the reduced model is better than expected. For this, we use

| (12) |

For the described algorithm the following convergence result holds.

Theorem 2.2 (Convergence of the TR-RB algorithm, c.f. [2]).

For sufficient assumptions on the Armijo search to solve (10), every accumulation point of the sequence generated by the above described TR-RB algorithm is an approximate first-order critical point for , i.e., it holds

| (13) |

Note that the above Theorem is not affected from the choice of the reduced primal and dual equations as long as Proposition 2.1 holds. In fact, the result can also be used for the TR-RB with the proposed PG approximation of these equations.

Let us also mention that it has been shown in [2] that a projected Newton algorithm for the subproblems can enhance the convergence speed and accuracy. Moreover, a reduced Hessian can be used to introduce an a posteriori result for the optimal parameter which can be used as post processing. In the work at hand, we neglect to transfer the ideas from [2] for the PG variant.

3. Numerical experiments

In this section, we analyze the behavior of the proposed PG variant of the TR-RB (BFGS PG TR-RB) algorithm.

We aim to compare the computational time and the accuracy of the PG variant to existing approaches from the literature.

To this end, we mention the different algorithms that we compare in this contribution:

Projected BFGS FOM: As FOM reference optimization method, we consider a standard projected BFGS method,

which uses FOM evaluations for all required quantities.

Non-conforming TR-RB algorithm from [11] (BFGS NCD TR-RB):

For comparison, we choose the above described TR-RB algorithm but with a non conforming choice of the RB spaces, which means that (7a) and (7b) are Galerkin projected equations where the test space coincides with the respective ansatz space.

This requires to use the NCD-corrected reduced objective functional and requires additional quantities for computing the Gradient.

For computational details including the choice of all relevant tolerances for both TR-RB algorithms we again refer to [11], where all details can be found. We only differ in the choice of the stopping tolerance . Also note that, as pointed out in Section 2.2, we use the same error estimators as in [11] which include the coercivity constant instead of the inf-sub constant. The source code for the presented experiments can be found in [12], which is a revised version of the source code for [11] and also contains detailed interactive jupyter-notebooks111Available at https://github.com/TiKeil/Petrov-Galerkin-TR-RB-for-pde-opt..

3.1. Model problem: Quadratic objective functional with elliptic PDE constraints

For our numerical evaluation we reconsider Experiment 1 from [2]. We set the objective functional to be a weighted -misfit on a domain of interest with a weighted Tikhonov term, i.e.

with a desired state and desired parameter . We added the constant term to verify that . With respect to the formulation in (P.a), we have , , and . From this general choice we can construct several applications. One instance is to consider the stationary heat equation as equally constraints, i.e. the weak formulation of the parameterized equation

| (14) |

with parametric diffusion coefficient and source , outside temperature and Robin function . From this the bilinear and linear forms and can easily be deduced and we set the parameter box constraints

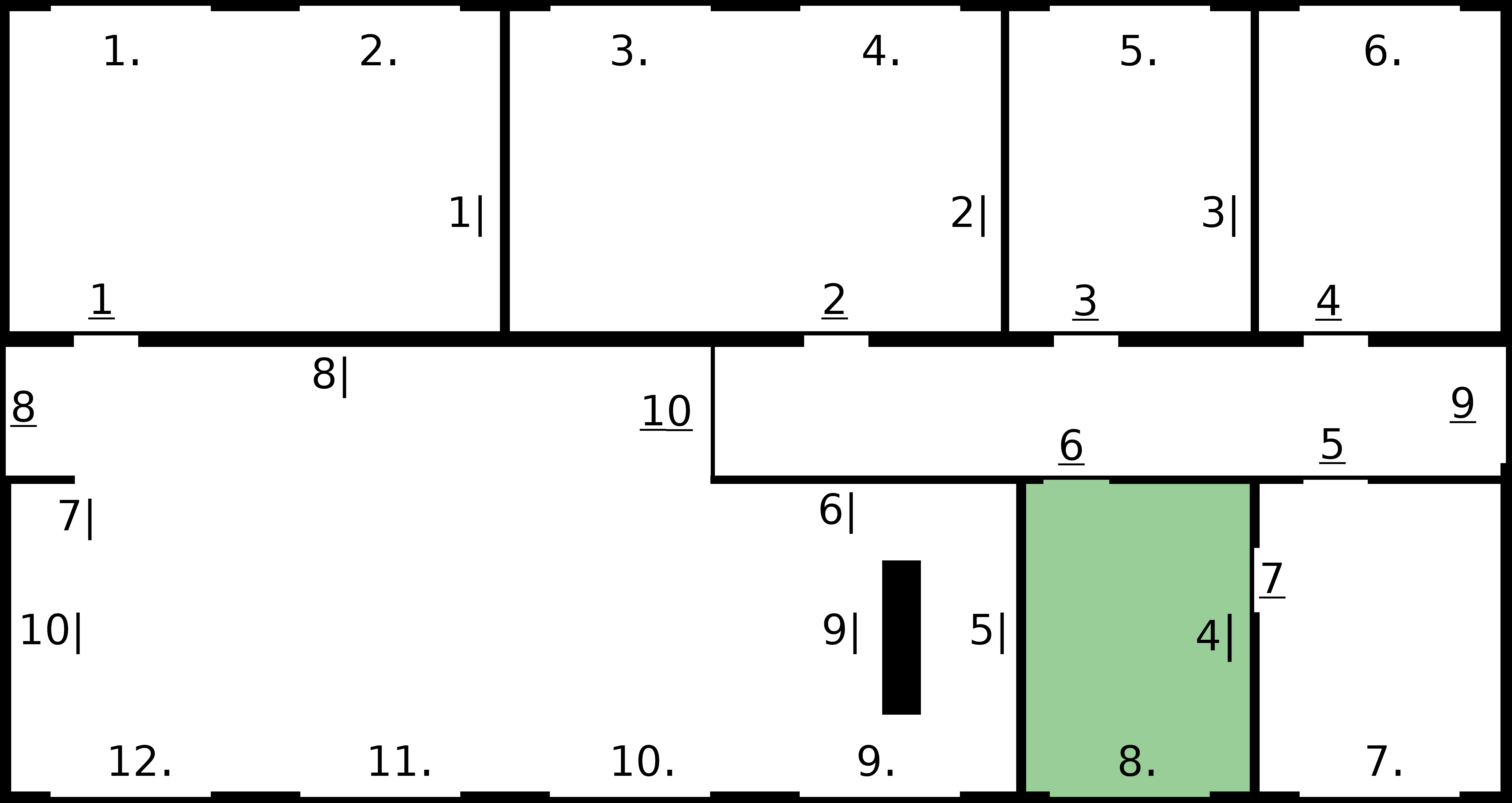

As an application of (14), we use the blueprint of a building with windows, heaters, doors and walls, which can be parameterized according to Figure 1. We picked a certain domain of interest and we enumerated all windows, walls, doors and heaters separately.

We set the computational domain to and we model boundary conditions by incorporating all walls and windows that touch the boundary of the blueprint to the Robin function . All other diffusion components enter the diffusion coefficient , whereas the heaters are incorporated as a source term on the right hand side . Moreover, we assume an outside temperature of . For our discretization we choose the conforming case for the FOM, i.e. , and use a mesh size which resolves all features from the given picture and results in degrees of freedom.

For the parameterization, we choose 2 doors, 7 heaters and 3 walls which results in a parameter space of 12 dimensions. More details can be viewed in the accompanying source code.

3.2. Analysis of the error behavior

This section aims to show and discuss the model reduction error for the proposed Petrov–Galerkin approach. Furthermore, we compare it to the Galerkin strategy from the NCD-corrected approach, where we denote the solutions by , and the corrected functional by , as well as to the non corrected approach from [17] whose functional we denote by . For this, we employ a standard goal oriented Greedy search algorithm as also done in [11, Section 4.3.1] with the relative a posteriori error of the objective functional . As pointed out in Section 2.2, due to , we can replace the inf-sup constant by a lower bound for the coercivity constant of the conforming approach. It is also important to mention that for this experiment, we have simplified our objective functional by setting the domain of interest to the whole domain . As a result the dual problem is simpler which enhances the stability of the PG approach. The reason for that is further discussed below. Figure 2 shows the difference in the decay and accuracy of the different approaches. It can clearly be seen that the NCD-corrected approach remains the most accurate approach while the objective functional and the gradient of the PG approach shows a better approximation compared to the non corrected version. Clearly the PG approximation of the primal and dual solutions are less accurate and at least the primal error decays sufficiently.

While producing the shown error study, we experienced instabilities of the PG reduced primal and dual systems. This is due to the fact that for very complex dual problems, the test space of each problem very poorly fits to the respective ansatz space. In fact, the decay of the primal error that can be seen in Figure 2(B) can not be expected in general and is indeed a consequence of the simplification of the objective functional, where we chose . The stability problems can already be seen in the dual error and partly on the primal error for basis size 20. In general it can happen that the reduced systems are highly unstable for specific parameter values. Instead, a sophisticated Greedy Algorithm for deducing appropriate reduced spaces may require to build a larger dual or primal space by adding stabilizing snapshots, i.e. search for supremizers [1]. Since the aim of the work at hand is not to provide an appropriate Greedy based algorithm, we instead decided to reduce the complexity of the functional where stability issues are less present.

3.3. TR-RB algorithm

We now compare the PG variant of the TR-RB with the above mentioned NCD-corrected TR-RB approach. Importantly, we use the original version of the model problem, i.e. we pick the domain of interest to be defined as suggested in Figure 1. In fact, we accept the possibility of high instabilities in the reduced model. We pick ten random starting parameter, perform both algorithms and compare the averaged result. In Figure 3 one particular starting parameter is depicted and in Table 1 the averaged results for all ten optimization runs are shown.

| runtime[s] | iterations | ||||

|---|---|---|---|---|---|

| avg. (min/max) | speed-up | avg. (min/max) | rel. error | FOC cond. | |

| FOM BFGS | 6955 (4375/15556) | – | 471.44 (349/799) | 3.98e-5 | 3.36e-6 |

| TR NCD-BFGS | 171 (135/215) | 40.72 | 12.56(11/15) | 4.56e-6 | 6.05e-7 |

| TR PG-BFGS | 424 (183/609) | 16.39 | 17.56(11/22) | 4.62e-6 | 7.57e-7 |

It can be seen that the PG variant is a valid approach and converges sufficiently fast with respect to the FOM BFGS method. Surely, it can not be said that this stability issues do not enter the performance of the proposed TR-RB methodology but regardless of the stability of the reduced system, we note that the convergence result in Theorem 1 still holds true. However, the instability of the reduced systems clearly harms the algorithm from iterating as fast as the NCD-corrected approach. One reason for that is that the trust region is much larger for the NCD-corrected approach, allowing the method to step faster. We would like to emphasize that the depicted result in Figure 3 is neither an instance of the worst nor the best performance of the PG approach but rather an intermediate performance. The comparison highly depends on the starting parameter, and the structure of the optimization problem. As discussed above, the suggested PG approach can potentially benefit from more involved enrichment strategies that account for the mentioned stability issues.

Last but not least, it is important to mention that the above experiment showed weaknesses of the chosen projected BFGS approach as FOM method as well as for the TR-RB subproblems which has been extensively studied in [2]. Instead, it is beneficial to choose higher order optimization methods, such as projected Newton type methods, where also the PG variant can be applied to neglect the more involved contributions from the NCD-corrected approach that are entering the Hessian approximation.

4. Concluding remarks

In this contribution we demonstrated, how adaptive enrichment based on rigorous a posteriori error control can be used within a Trust-Region-Reduced-Basis approach to speed up the solution of large scale PDE constrained optimization problems. Within this approach the reduced approximation spaces are tailored towards the solution of the overall optimization problem and thus circumvent the offline construction of a reduced model with good approximation properties with respect to the whole parameter regime. In particular, we compared a new Petrov-Galerkin approach with the NCD-Galerkin approach that has recently been introduced in [2]. Our results demonstrate the benefits of the Petrov-Galerkin approach with respect to the approximation of the objective functional and its derivatives as well as with respect to corresponding a posteriori error estimation. However, the results also show deficiencies with respect to possible stability issues. Thus, further improvements of the enrichment strategy are needed in order to guarantee uniform boundedness of the reduced inf-sup constants.

References

- [1] F. Ballarin, A. Manzoni, A. Quarteroni, and G. Rozza. Supremizer stabilization of pod–galerkin approximation of parametrized steady incompressible navier–stokes equations. International Journal for Numerical Methods in Engineering, 102(5):1136–1161, 2015.

- [2] S. Banholzer, T. Keil, L. Mechelli, M. Ohlberger, F. Schindler, and S. Volkwein. An adaptive projected newton non-conforming dual approach for trust-region reduced basis approximation of pde-constrained parameter optimization, 2020. arXiv 2012.11653.

- [3] M. Barrault, Y. Maday, N. C. Nguyen, and A. T. Patera. An ‘empirical interpolation’ method: application to efficient reduced-basis discretization of partial differential equations. C. R. Math., 339(9):667–672, 2004.

- [4] P. Benner, M. Ohlberger, A. Patera, G. Rozza, and K. Urban, editors. Model reduction of parametrized systems, volume 17 of MS&A. Modeling, Simulation and Applications. Springer, Cham, 2017. Selected papers from the 3rd MoRePaS Conference held at the International School for Advanced Studies (SISSA), Trieste, October 13–16, 2015.

- [5] A. Buhr, L. Iapichino, M. Ohlberger, S. Rave, F. Schindler, and K. Smetana. Localized model reduction for parameterized problems, pages 245–306. De Gruyter, 2021.

- [6] M. Drohmann, B. Haasdonk, and M. Ohlberger. Reduced basis approximation for nonlinear parametrized evolution equations based on empirical operator interpolation. SIAM Journal on Scientific Computing, 34(2):A937–A969, 2012.

- [7] J. Feinauer, S. Hein, S. Rave, S. Schmidt, D. Westhoff, J. Zausch, O. Iliev, A. Latz, M. Ohlberger, and V. Schmidt. MULTIBAT: Unified workflow for fast electrochemical 3d simulations of lithium-ion cells combining virtual stochastic microstructures, electrochemical degradation models and model order reduction. Journal of Computational Science, 31:172–184, 2019.

- [8] B. Haasdonk. Reduced basis methods for parametrized PDEs – A tutorial introduction for stationary and instationary problems. Technical report, 2014. Chapter to appear in P. Benner, A. Cohen, M. Ohlberger and K. Willcox: ”Model Reduction and Approximation: Theory and Algorithms”, SIAM.

- [9] B. Haasdonk and M. Ohlberger. Reduced basis method for finite volume approximations of parametrized linear evolution equations. Mathematical Modelling and Numerical Analysis, 42(2):277–302, 2008.

- [10] D. Huynh, D. Knezevic, A. Patera, and H. Li. Methods and apparatus for constructing and analyzing component-based models of engineering systems, 2015. US Patent 9,213,788.

- [11] T. Keil, L. Mechelli, M. Ohlberger, F. Schindler, and S. Volkwein. A non-conforming dual approach for adaptive trust-region reduced basis approximation of pde-constrained optimization, 2020. arXiv 2006.09297. To appear in: ESAIM: M2AN (2021).

- [12] T. Keil and M. Ohlberger. Software for Model Reduction for Large Scale Systems, url: https://doi.org/10.5281/zenodo.4627971, Mar. 2021.

- [13] M. Ohlberger and S. Rave. Reduced basis methods: Success, limitations and future challenges. Proceedings of the Conference Algoritmy, pages 1–12, 2016.

- [14] M. Ohlberger, M. Schaefer, and F. Schindler. Localized model reduction in PDE constrained optimization. International Series of Numerical Mathematics, 169:143–163, 2018.

- [15] M. Ohlberger and F. Schindler. Error control for the localized reduced basis multiscale method with adaptive on-line enrichment. SIAM Journal on Scientific Computing, 37(6):A2865–A2895, 2015.

- [16] M. Ohlberger and F. Schindler. Non-conforming localized model reduction with online enrichment: towards optimal complexity in PDE constrained optimization. In Finite volumes for complex applications VIII—hyperbolic, elliptic and parabolic problems, volume 200 of Springer Proc. Math. Stat., pages 357–365. Springer, Cham, 2017.

- [17] E. Qian, M. Grepl, K. Veroy, and K. Willcox. A certified trust region reduced basis approach to PDE-constrained optimization. SIAM J. Sci. Comput., 39(5):S434–S460, 2017.