Estimating the conditional distribution in functional regression problems

Abstract

We consider the problem of consistently estimating the conditional distribution of a functional data object given covariates in a general space, assuming that and are related by a functional linear regression model. Two natural estimation methods are proposed, based on either bootstrapping the estimated model residuals, or fitting functional parametric models to the model residuals and estimating via simulation. Whether either of these methods lead to consistent estimation depends on the consistency properties of the regression operator estimator, and the space within which is viewed. We show that under general consistency conditions on the regression operator estimator, which hold for certain functional principal component based estimators, consistent estimation of the conditional distribution can be achieved, both when is an element of a separable Hilbert space, and when is an element of the Banach space of continuous functions. The latter results imply that sets that specify path properties of , which are of interest in applications, can be considered. The proposed methods are studied in several simulation experiments, and data analyses of electricity price and pollution curves.

Keywords: functional regression, functional time series, conditional distribution, quantile estimation, bootstrap

1 Introduction

We suppose that we have observed data from a strictly stationary process that are assumed to follow a general functional linear regression model of the form

| (1) |

Here is a curve in a normed function space , the covariates take values in a normed space and are distributed so that is independent of the model error , and is a linear operator mapping to . For example, might be a single curve living in the same space as the response, in which case (1) describes simple linear function-on-function regression. This setting also includes functional autoregressive models (Bosq, 2000) when . Generally though, might be comprised of several curves, a mixture of curves and scalar covariates, etc., and more detailed assumptions on the nature of the space will follow.

Suppose is a generic pair following (1). The goal of this paper is to introduce and study methods to consistently estimate the conditional distribution of given , , for some specific sets of interest . By choosing appropriate sets , one may make inference on a wide range of interesting properties of :

-

1.

Often we are interested in some transformation of the response, and then might consider sets of the form . For instance, when , with denoting standard Lebesgue measure on , contains curves that occupy a range of interest for a certain amount of time. More generally, when is a scalar, then we are often interested in the conditional distribution function

- 2.

-

3.

We might wish to choose such that it yields a prediction set for , so that for a given . Estimating can be used to appropriately calibrate . See Goldsmith et al. (2013), Choi and Reimherr (2016), Liebl and Reimherr (2019), Hyndman and Shang (2009), and Paparoditis and Shang (2020) for a review of methods for constructing prediction sets for functional responses and parameters.

At this point, when referring to examples (a) and (b), an important remark is necessary. In the case where is scalar, it might appear more natural to directly employ some scalar-on-function regression with response variable . However, one of the main strengths of the approach we pursue and which is a clear distinction to competitive methods, is that we first model the entire response curve and then extract the feature of interest. This has the advantage that we can harness the full information contained in the functional responses when estimating the conditional distribution of .

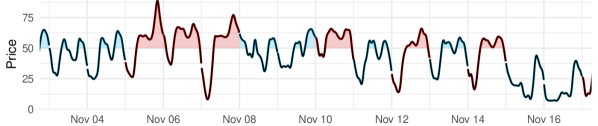

Aside from interest in the general problem, this work was primarily motivated by the statistical challenge of forecasting aspects of response curves describing daily electricity prices. The specific data that we consider consists of hourly electricity prices, demand, and wind energy production in Spain over the period from 2014 to 2019, which includes observations from 2191 days (the data are available at www.esios.ree.es). We project the hourly data onto a basis of 18 twice differentiable B-splines to construct daily price, demand, and wind energy production curves, as illustrated in Figure 1. The price of electricity naturally fluctuates based on supply and demand, and exhibits daily, weekly, and yearly seasonality. The rather predictable variation in demand does not influence the price as much as surges in wind energy production, especially if they occur on days with weak demand. Letting denote the price curves and the vector of the demand and wind curves, both adjusted for yearly seasonality and trends, we then model using an FAR(7) model with exogenous variables

| (2) |

where denote autoregressive operators; see González et al. (2018). The details of this are explained in Section 5, but for now it suffices to acknowledge that this is a regression model of the form (1). For such electricity price curves, their likelihood of falling within sets of the following type are of particular interest:

Example 1 (Level sets).

Let

for some and . contains curves that stay a limited amount of time above a threshold .

Forecasting whether price or demand curves will spend prolonged periods of time above certain levels is useful in anticipating volatility in continuous intraday electricity markets, and planning for peak loads (Vilar et al., 2012). This falls within the scope of the general problem we consider.

The literature in functional data analysis on regression models of the form (1) is vast, although the most frequent problems considered regarding consistent estimation in model (1) are (i) how to find a consistent estimator of , and (ii) how to forecast consistently, i.e. to guarantee that suitably in probability. Moreover, the majority of the literature on the topic of function-on-function linear regression concentrates on the setting when , the separable Hilbert space of square integrable functions on , equipped with its standard inner product and norm. Ramsay and Silverman (2006) for example proposes a double truncation scheme based on functional principal component analysis to estimate in this setting, and Mas (2007), Imaizumi and Kato (2018) derive a convergence rate for in a “single-truncation” estimation scheme based on an increasing (in the sample size) number of principal components, where here denotes the Hilbert–Schmidt norm. Similar consistency results for the resulting forecasts in functional linear regression can be found in Crambes and Mas (2013), and under general stationarity conditions and in the FAR setting in Hörmann and Kidziński (2015) and Aue et al. (2015). Estimating the operator can be viewed as a special case of estimating the conditional mean , and this general problem has also been extensively considered; see Chiou et al. (2004), Ferraty et al. (2012), and Wang et al. (2016).

The problem of estimating the conditional distribution of given has been comparatively far less studied. Numerous methods have been proposed to estimate the conditional distribution of a scalar response with a functional covariate , including Chen and Müller (2012), Kato (2012), Yao et al. (2017), Wang et al. (2016), and Sang and Cao (2020), who propose estimators based on quantile regression, and Ferraty and Vieu (2006), who propose Nadaraya–Watson style kernel-smoothed estimators. Estimating the conditional distribution of when and take values in a general function space is largely unexplored to our knowledge, even in the context of model (1). Fernández de Castro et al. (2005) and Paparoditis and Shang (2020) develop bootstrap procedures based on functional principal component analysis to produce prediction sets in the context of forecasting with Hilbertian FAR models, which can be viewed as a special case of this problem. For functional data taking values in , Chen and Müller (2014) and Fan and Müller (2021) develop methods for estimating the conditional distribution of given assuming and are jointly Gaussian, and that the conditional distribution of the response has sample paths satisfying natural differentiability conditions.

A technical problem that is encountered in consistently estimating the conditional probability is that one could at most expect consistent estimation for continuity sets of the distribution of the response, i.e. sets for which . This property evidently depends strongly on the choice of the space , as well as the norm that it is equipped with. For many interesting examples, the metric on the space is too weak to allow for meaningful continuity sets . An illustrative example is simple prediction band sets of the form , where and are continuous functions on , in which case when is viewed as a subset of . More appropriate spaces to handle many interesting examples in functional data analysis involving path properties of the response, such as level sets, are the spaces , the space of continuous function on equipped with the supremum norm, or the Sobolev spaces equipped with their canonical norms; see Brezis (2010). For these latter spaces, the problem of estimating, and consistently forecasting with, has been only lightly studied to date, and in specialized settings; see Pumo (1999), Ruiz-Medina and Álvarez Liébana (2019), and Bosq (2000) in the context of FAR estimation. Further, the problem of consistently estimating the conditional distribution in these settings has not been studied, to our knowledge. We also refer the reader to Dette et al. (2020) for a review of functional data analysis methods in .

In this paper, we propose natural procedures to estimate , in which we first estimate with a suitably consistent estimator , and then either (i) resample the estimated residuals to estimate with the empirical distribution of , or (ii) assuming Gaussianity of the model errors , we estimate using simulation by modelling conditioned on as a Gaussian process with mean , and covariance estimated from the residual sequence . We establish general conditions on the estimator in both the settings when is a separable Hilbert space, and when is , such that these procedures will lead to consistent estimation of . Subsequent to this, we define an estimator that we show satisfies these conditions under regularity assumptions on the operator , and the process , which allow for serial dependence of both the response and covariates. In the space , we introduce a number of examples of sets of potential interest, compute their boundaries, and establish under what conditions , which can be non-trivial even when is a Gaussian process. In several simulation studies and data analyses, the proposed methods generally outperformed competing methods in which is estimated using functional logistic regression, functional Nadaraya–Watson estimation, or functional quantile regression. Another advantage, which derives from the simple form of our estimators for , is that they satisfy basic properties of a probability measure, e.g. they are monotone in . While this may seem like an obvious requirement, it is not necessarily fulfilled by some competing approaches.

The rest of the paper is organized as follows. In Section 2, we formally introduce the methods described above to estimate , and present results on their consistency, including results on uniform consistency over monotone families of sets that are relevant in constructing prediction sets with a specified coverage and quantile function estimates. These results depend on the properties of the estimator , and we define an estimator based on functional principal component analysis and single truncation scheme, and establish that it leads to consistent estimation of when is a separable Hilbert space and when in Section 3. Section 4 presents numerous examples of sets of interest, and a discussion of their boundaries in . A number of competing methods are introduced in Section 5, and these are compared and studied with the proposed methods in several simulations studies and real data illustrations. The proofs of all technical results follow these main sections.

2 Estimation procedures and consistency results

We let , and for , we use the notation to denote the standard inner product on , with induced norm . In order to consider path properties of functions in , we consider the space equipped with the supremum norm . While is a separable Hilbert space, is a Banach space, with their norms satisfying . The space may hence be naturally embedded in . We use the tensor product notation to denote the operator if is viewed as an element of a Hilbert space, and the kernel integral operator with kernel if is viewed as an element of . We assume that the covariate space is a Hilbert space with norm . In order to lighten the notation, and when it is clear from the context, we write in place of a specific norm on either the space or . In the context of Hilbert spaces, we use and to denote the Hilbert–Schmidt norm and the trace norms of operators, respectively.

We assume throughout that the covariates and the model errors satisfy the following independence condition, which we do not explicitly state in the below results, but take as granted.

Assumption 1.

In model (1), , and is independent from for all .

In order to formally describe the methods we use to estimate , we assume that we may consistently estimate with an estimator based on the sample . Specific conditions on this estimator, and examples satisfying these conditions, will follow. The first method we describe is based on applying an i.i.d. bootstrap to the estimated residuals.

Algorithm 1, Residual Bootstrap (abbreviated boot):

-

1.

Estimate in (1) with .

-

2.

Calculate the model residuals .

-

3.

Define the estimator of as

We show below that this estimator is consistent under quite mild conditions. The algorithm boot can be applied without specific distributional assumptions on the errors. If though the model errors are thought to be Gaussian processes, then we may take this into account in estimating . As the mean of the model errors is zero by assumption, in this case their distribution is determined by their covariance , which is defined by

The above algorithm may then be adapted as follows:

Algorithm 2, Gaussian process simulation (abbreviated Gauss):

-

1.

Estimate in (1) with .

-

2.

Calculate the model residuals .

-

3.

Estimate the empirical covariance operator

(3) where . Let denote the ordered eigenvalues of , with corresponding eigenfunctions satisfying , .

-

4.

Let denote a sequence of i.i.d. standard normal random variables, independent of the sample , and define

Note that conditionally on the sample, in particular on , is a Gaussian process with mean zero and covariance operator . Define the estimator of as

(4) The right hand side above can be approximated by Monte-Carlo simulation. To do so, generate an i.i.d. sample conditionally on , , distributed as , by simulating independent standard Gaussian sequences and setting

The right hand side of (4) can be estimated, for a large , by

Remark 1.

The scaling in the definition of does not take into account the degrees of freedom lost in the estimation of the regression operator . It has thus been advocated, for example in Crambes et al. (2016), to instead divide by , where is related to the dimension of the dimensionality reduction technique used in estimating . If , as is the case for most estimation approaches, the resulting scaling difference is asymptotically negligible. Some authors also propose splitting the sample and estimating the regression operator and the noise covariance operator on separate parts of the sample in order to reduce the bias of the estimator ; see Crambes and Mas (2013).

Remark 2.

Algorithm Gauss can be extended to other parametric distributions of the noise. A notable example for this are infinite dimensional elliptic distributions, where with two independent random variables , which is Gaussian, and from a known univariate parametric distribution. The following investigation can easily be adapted to this setting. For details on elliptical distributions of functional data, we refer to Boente et al. (2014).

We now aim to establish consistency results for these algorithms. In order to keep the results as general as possible and allow for different estimators of , these results are stated in terms of the following consistency properties of .

Assumption 2.

The estimator is such that

-

(a)

its out-of-sample prediction is consistent, i.e. if , and is independent from the sample, then

-

(b)

its in-sample prediction is consistent, i.e. let be independent from the sample and uniformly distributed on , then

In order to establish the consistency of the algorithm Gauss, we additionally need conditions on the estimator of the covariance operator of the model errors defined by (3). We state two conditions depending on whether is a separable Hilbert space, or .

Assumption 3.

is a separable Hilbert space. The estimator is such that

Assumption 4.

-

(a)

. The estimator is such that

-

(b)

The estimated variance of the model errors,

satisfies the Hölder condition

for some , where is a positive random variable with .

Assumption 4 is a analog of Assumption 3, but with the addition of Assumption 4 (b) that implicitly demands a degree of continuity of and the model errors . Under the above assumptions, we can now formulate our main consistency results.

Theorem 1.

Suppose that Assumption 2 holds and that . Then as .

Theorem 2.

Theorems 1 and 2 show that consistent estimation of can be achieved by both boot and Gauss when takes values in either a separable Hilbert space, or , under natural consistency conditions on , and when is a continuity set of the response . We note that these results can be readily extended to sets that, rather than being fixed, are dependent on the predictor , as well as using the estimator , so long as there is a certain degree of continuity in relating to . This is often of interest when constructing prediction sets for the response , as in the following examples in which it is natural to consider .

Example 2 (Pointwise and uniform prediction sets).

Suppose and are positive functions in . Given a covariate , let, for ,

and

These approximate the sets

and

Corollary 1.

2.1 Uniform consistency over monotone families of sets

For a potentially unbounded interval , we call a family of measurable subsets of monotone if the sets are increasing or decreasing in . Suppose that is increasing, the decreasing case can be handled similarly, and that we are interested in finding

As an example where this problem is relevant, consider a scalar transformation of the response , and suppose we wish to estimate the conditional quantile of given the covariate

The sets evidently define a monotone family. Consistent scalar-on-function quantile regression can hence be cast as the problem of consistently estimating from the sample, which can be done using or . To this end we consider the estimator

| (6) |

We note that based on the definition of , is a non-decreasing function in . The same holds for , which is defined using . While this observation is rather trivial, in other approaches to scalar-on-function quantile regression one often has to take special care in order to guarantee monotonicity of estimators of , see e.g. Kato (2012).

The goal is now to show that and . In order to do so, we need the following uniform convergence result for the estimated conditional probabilities.

Proposition 1.

Let be a monotone family of sets such that is a.s. continuous in . Suppose the estimator is non-decreasing, right-continuous, and satisfies for all . Then

3 Estimation of the regression operator

In this section we aim to define an estimator that satisfies the consistency conditions detailed in Assumptions 2, 3, and 4. In order to do so, we make the following assumptions on model (1).

Assumption 5.

-

(a)

is a separable Hilbert space.

-

(b)

The process has mean zero, and is --approximable in (see Hörmann and Kokoszka (2010)).

-

(c)

The operator is a bounded linear operator.

-

(d)

The sequence is a mean zero, i.i.d. sequence in , and satisfies .

Assumption 5 (b) supposes that is a (strongly) stationary and ergodic sequence with , and allows the to be weakly serially dependent in a certain sense. Hörmann and Kokoszka (2010) show that many commonly studied stationary time series in function space, like FAR processes or functional analogs of GARCH processes, are --approximable under suitable moment conditions.

The estimator that we consider is a truncated (functional) principal components based estimator. Let the empirical covariance operator of , and the empirical cross-covariance operator between and , be denoted as

Letting denote the inner product on , we note that defines a non-negative sequence of eigenvalues , and eigenfunctions , satisfying , . We then define

| (7) |

The estimator (7) only truncates the covariance operator of in order to obtain a feasible approximation to , yielding a so-called “single-truncated” estimator. The asymptotic properties of these estimated operators have e.g. been studied in Mas (2007) and Hörmann and Kidziński (2015). In order to select the truncation parameter in such a way that leads to asymptotic consistency of , we use the following criterion:

| (8) |

Here is a tuning parameter, tending to infinity at a rate specified in the results below.

We note that another standard way to select is to use the percentage of variance explained (PVE) approach, which entails taking

where is a user specified percentage treated as a tuning parameter. While the criterion in (8) is more transparent in terms of describing the asymptotic consistency of , since it gives a direct description of the decay rate of the sequence of eigenvalues , in applications the PVE criterion is prevailing, due to its ease of interpretation. By choosing the associated tuning parameters appropriately, the two criteria may be made comparable.

Now we present results which imply Assumptions 2–4, and hence the consistency of the estimators in the Algorithms boot and Gauss.

Proposition 2.

Proposition 3.

In the case when , we add the following assumption in addition to Assumption 5, supposing a degree of smoothness to and :

Assumption 6.

If , and for some ,

-

(a)

The model errors a.s. satisfy the Hölder condition

(9) where is a positive random variable independent from , with .

-

(b)

For all , the regression operator satisfies

where is a finite constant.

Assumption 6 (a) is fulfilled by a wide range of stochastic processes, most notably the Brownian motion and the fractional Brownian motion. Since is linear, Assumption 6 (b) is a natural formulation of the Hölder condition for the conditional mean of the response. In particular, this implies that is a bounded, compact operator.

Remark 3.

Suppose , so that model (1) describes function-on-function regression. A frequently employed class of operators in this setting are kernel integral operators, defined by a continuous kernel as

If there exists an such that almost everywhere

then one can easily verify that

and thus Assumption 6 (b) is fulfilled.

Proposition 4.

Proposition 5.

The proofs of Propositions 2–4 are relegated to Section 7, while the proof of Proposition 5 is given in Appendix A.

We conclude this section with some technical discussion. We begin by noting that the sequence , which controls how many principal components of are used in forming , can be of asymptotically higher order if is a Hilbert space compared to the setting when , and . In the case where the Hölder exponent in Assumption 6 is , the responses are Lipschitz continuous, which implies they are weakly differentiable. As a result one may then take , a separable Hilbert space, leading back to the rate condition . The order is sufficient but not sharp. In fact, for , a different proof yields that also leads to consistency. In the case of the Brownian motion, demands that . This is still of higher order than that suggested to be used by Hörmann and Kidziński (2015) for consistent estimation of the regression operator in Hilbert spaces.

Our second technical remark concerns the choice of . Assumption 5 (a) requires to be a Hilbert space. While typically this is not a restriction, some care needs to be taken in the case of an FAR model. Here, when we study continuous functions, we choose . While it is natural to assume that the covariate and response space coincide for an FAR (i.e. requiring , too), this is not necessarily the case. For example when we consider a kernel integral operator with a continuous kernel, then we may still use and using the natural embedding of in . Alternatively we can resort to the Sobolev space of once (weakly) differentiable functions in equipped with the norm ; see Chapter 8 of Brezis (2010). The space is a separable Hilbert space, and because , the space can be embedded in . This will allow for more general class of continuous operators (for example, including pointwise evaluations). When viewed with the moment conditions on implicit to Assumption 5 (b), this can be done so long as the covariates are sufficiently smooth.

4 Some further examples of events

In addition to level sets and pointwise or uniform prediction sets mentioned in Examples 1 and 2 above, in this section we list some specific examples of sets that are of interest for the data that we discuss, and which might be useful in other applications.

Example 3 (Contrast sets).

For some and let

For example, when , then is the set of curves which are in average above level . If , or and , then the set can be identified as functions with decreasing trend.

Example 4 (Extremal sets.).

Let and let and

Then contains functions which will exceed a certain threshold . Note that this is the compliment of a boundary set with bounds and .

Example 5 (Excursion sets.).

Let , and . Set

Then are the functions which uninterruptedly stay strictly above a certain threshold for a certain amount of time.

A crucial condition in Theorems 1 and 2 is that . Below we discuss some examples for which this requirement is fulfilled. For the purpose of illustration, we give details in the case of level sets (Example 1) and . The other examples can be explored similarly.

Proposition 6.

Let and . We define . The following conditions imply :

| (10) | ||||

| (11) |

The conditions in (10) and (11) are satisfied by many well known processes, including Brownian motion. They are also generally satisfied by continuously differentiable Gaussian processes under standard non-degeneracy conditions. Such processes might be used to model functional data generated by applying standard smoothing operations, for instance using cubic-splines or trigonometric polynomials, to raw discrete data. We note that comparable differentiability conditions are assumed in Fan and Müller (2021). The following proposition, whose proof we defer to Section 7, describes these conditions.

Proposition 7.

Suppose that is a continuously differentiable Gaussian process with covariance kernel . If for all , then (10)(i) holds. For , and , let

If in addition for all and , there exists constants such that , then (10)(ii) holds. If is twice continuously differentiable, and has a non-degenerate distribution, then (11) holds.

If is a contrast set with some , , then from the continuity of the inner product it follows that , both for , and . As for the boundary set , with ,

5 Simulation experiments and data illustrations

In this section we present the results of several simulation experiments and real data analyses that aimed to evaluate and compare the performance of the algorithms boot and Gauss, and illustrate their application. We begin by defining some alternate methods that may be used to estimate , and we describe two recent procedures proposed for functional quantile regression and construction of prediction sets in functional data prediction, respectively.

5.1 Competing methods

A simple method to estimate is to employ functional binomial regression. This entails positing the model

for some and , and a link function that can be chosen from a variety of possibilities, but is most often the logistic link function, or the cumulative distribution function of a standard normal random variable (the “probit link”). For more details of such models, we refer to Müller and Stadtmüller (2005) and Mousavi and Sørensen (2017). One drawback of note in applying logistic regression in this setting is that changing the set necessitates refitting the model, which can be computationally cumbersome, and further, as a consequence, the resulting estimators of need not be monotone with respect to increasing (or decreasing) sets . An approach to adjust such estimators to restore monotonicity is to use rearrangement or isotonization, as discussed in e.g. Chernozhukov et al. (2010).

Since the exact relationship between the function and the event is unknown and difficult to describe in parametric terms, even under model (1), another promising approach is to use nonparametric techniques such a kernel estimators. Generalizing the method found in Section 5.4 of Ferraty and Vieu (2006), the conditional distribution can be estimated by the functional extension of the Nadaraya–Watson estimator

| (12) |

where is a kernel function on the nonnegative real numbers, is a distance measure on , and is a smoothing parameter corresponding to the bandwidth of the kernel. Note that while the choice of is typically unproblematic, the choice of is more intricate and is often taken to depend on the data. The bandwidth represents the trade-off between bias (oversmoothing) and error (undersmoothing), and is normally taken to decrease with the sample size . Ferraty and Vieu (2006) establish consistency conditions for the estimator (12) in the case when the sequence is -mixing and is scalar. When we apply this method below, we take to be the standard Gaussian kernel, to be the norm on , and select using cross-validation. We note that similarly to functional logistic regression based estimators, a draw back of these estimators is that if one changes the set , then the bandwidth in general should be recalibrated, and the resulting estimators need not be monotone in if the bandwidth is not held fixed for all sets .

Similar options may be derived from the local linear functional estimator, which improves upon the Nadaraya–Watson estimator by including a linear terms of the form into the computation of the weights; see Berlinet et al. (2011). The -nearest neighbors (kNN) functional estimator is a variation on the Nadaraya–Watson estimator with adaptive bandwidth, i.e. is the smallest number such that . The kNN estimator has been shown to be consistent for non-parametric regression by Kudraszow and Vieu (2013).

In order to evaluate the proposed algorithms for the construction of prediction sets, we compared to the method of Paparoditis and Shang (2020) in the setting of forecasting FAR(1) processes . Subsequent to forming the estimator using functional principal component analysis, their method entails performing a (sieve) bootstrap on the functional principal component scores of the residuals in order to estimate the distribution of the prediction error. is then forecast by , and uniform prediction sets for are constructed of the form

where for a specified coverage level ,

In the setting of scalar-on-function quantile regression, we compare to the method of Sang and Cao (2020), which entails for a scalar response modelling

where is an assumed to be unknown link function. The link function as well as the parameter function are assumed to be linear combinations of splines, and estimated in order to estimate the level quantile of by minimizing the check function loss

subject also to a roughness penalty on the functions and .

5.2 Construction of prediction sets

Following the simulation experiment considered in Paparoditis and Shang (2020), we construct a time series of continuous functions as follows:

| (13) |

where , and is a standard Brownian motion. We fit an FAR(1) model to each simulated sample where we chose the truncation parameter using the PVE criterion with . This is the same value as used in Paparoditis and Shang (2020). If is chosen as , the FAR(1) model is correctly specified, whereas with , there is a model misspecification that should be detrimental to the quality of the model predictions. Following the method proposed in Paparoditis and Shang (2020) and as described above, we constructed uniform prediction sets to forecast each series 1-step ahead, with nominal coverage probabilities of 80% and 95%. This was repeated independently 1000 times, with sample sizes . While the model for the forecast is the same for both methods, the difference between our approach and Paparoditis and Shang (2020) is in the methods used to estimate the noise distribution . These results are summarised in Table 1 in terms of empirical coverage probabilities from the 1000 replications.

In the case and , the method boot yielded empirical coverage probabilities that were up to 4–6 percentage points below the method of Paparoditis and Shang (2020), which are both below the nominal level. Apart from this notable exception, the empirical coverage probabilities are comparable to those of Paparoditis and Shang (2020), and were closer to nominal coverage in 10 out of 16 cases considered. The results of Gauss were generally better, which is to be expected since the model errors are Gaussian processes, especially for the nominal coverage probability of 95%.

| Nominal | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| coverage | |||||||||

| 80% | boot | 0.683 | 0.694 | 0.745 | 0.754 | 0.777 | 0.778 | 0.789 | 0.791 |

| Gauss | 0.703 | 0.716 | 0.756 | 0.763 | 0.781 | 0.783 | 0.791 | 0.793 | |

| P., S. (2020) | 0.740 | 0.689 | 0.766 | 0.740 | 0.791 | 0.768 | 0.803 | 0.786 | |

| 95% | boot | 0.861 | 0.872 | 0.913 | 0.917 | 0.933 | 0.936 | 0.944 | 0.944 |

| Gauss | 0.898 | 0.904 | 0.927 | 0.931 | 0.940 | 0.943 | 0.946 | 0.946 | |

| P., S. (2020) | 0.902 | 0.856 | 0.918 | 0.899 | 0.927 | 0.913 | 0.936 | 0.924 | |

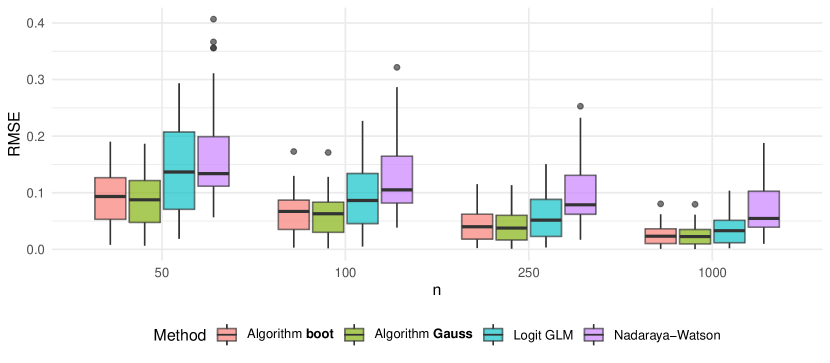

5.3 Comparison to functional GLM and Nadaraya–Watson estimation

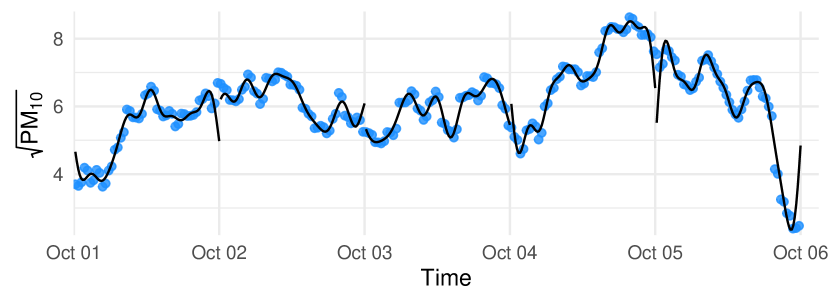

In this simulation experiment, we generated synthetic data under model (1) in such a way that it resembled a real functional time series derived from daily square-root transformed PM10 concentration curves constructed by smoothing half-hourly measurements of PM10. This is done using the function Data2fd in the fda package with default settings; see Ramsay et al. (2020). PM10 concentration denotes the concentration in air of respirable coarse particles having a diameter less than 10, and the data that we consider was collected in Graz, Austria over the period from October 1st, 2010 to March 31st, 2011. An illustration of these data is given in Figure 2, and they are available in the ftsa package in R; see Hyndman and Shang (2020).

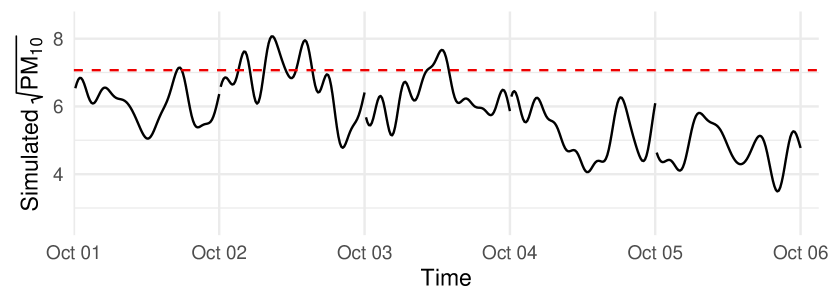

We use these data as a means to devise a realistic data generating process. To this end, we first fit an FAR model to the square-root transformed PM10 curves. The estimator for the FAR operator obtained in this way differs from operators typically used in simulation settings in that the estimator for the kernel is highly asymmetric, as illustrated in the right hand panel of Figure 2.

With the estimated sample mean and the fitted FAR operator, we then generate synthetic FAR time series samples by drawing model errors from a Gaussian distribution, with the covariance operator estimated from the residuals of the FAR(1) model fit to the original data. This can be done as in the algorithm Gauss. The first 30 observations are dropped as part of the burn-in phase. A snapshot of the raw data in comparison to the synthetic data can be seen in Figure 2. In this manner we may generate time series of arbitrary sample sizes that are similar to the original PM10 data. We generated 1000 independent samples for each sample size . Then, for 50 different values of predictors , simulated independently from the stationary distribution of the data generating process, we estimated the conditional probability of lying in the level set for each such sample. For each of the 50 predictors, we also approximated the true probability using Monte-Carlo simulation () from the data generating process.

We compared the estimators from algorithms boot and Gauss, as well as from a logistic functional GLM, and Nadaraya–Watson estimation. The number of principal components used to estimate was chosen using criterion (8), so that

We introduce into the definition of so that the criterion does not depend on the scale of the eigenvalues, yielding a more practicable way of choosing . For , this approximately covers 98% of the variance of the simulated curves in the sense of the PVE criterion. Naturally, less variance is covered in for smaller sample sizes. For the logistic GLM, we used the approach suggested by Müller and Stadtmüller (2005) and took the truncated Karhunen–Loève expansion as the predictor. In order to keep the methods comparable, we used the same number of principal components for our algorithms and for the functional GLM. We calibrated the bandwidth for the Nadaraya–Watson estimator using leave-one-out cross-validation on each generated sample. The results in terms of the root mean squared error (RMSE) over the 1000 simulations are displayed in Figure 3. Because it is difficult to visualize this for the 50 different predictors, we present boxplots summarizing the RMSE of each method over all predictors . More details on the results for a variety of specific values of can also be found in Table 4 in the Appendix.

We observed that algorithms boot and Gauss exhibited similar predictive performance in both examples and over all sample sizes. These methods clearly outperformed functional logistic regression and Nadaraya–Watson estimation in estimating the conditional probability of level sets. The proposed methods achieved a similar mean squared error in this case to functional logistic regression with about a quarter of the sample size. The performance of the Nadaraya–Watson estimator was poor compared to the other methods considered in both cases and varied strongly depending on the predictor . In Appendix B, we also present results in which we considered contrast sets rather than level sets, in which case the same overall pattern was observed, although the results were more comparable across the four methods.

| boot | Gauss | boot | Gauss | boot | Gauss | boot | Gauss | |

|---|---|---|---|---|---|---|---|---|

| 1 | 0.770 | 0.704 | 0.559 | 0.491 | 0.457 | 0.356 | 0.487 | 0.434 |

| 2 | 0.530 | 0.437 | 0.396 | 0.292 | 0.333 | 0.170 | 0.341 | 0.189 |

| 3 | 0.517 | 0.419 | 0.432 | 0.287 | 0.348 | 0.199 | 0.308 | 0.137 |

| 4 | 0.595 | 0.501 | 0.464 | 0.371 | 0.404 | 0.262 | 0.347 | 0.187 |

| 5 | 0.589 | 0.480 | 0.470 | 0.355 | 0.378 | 0.247 | 0.336 | 0.144 |

Although the estimator Gauss performs similarly to boot in the above example, it can be expected that boot runs into problems when is close to or , since boot only uses the estimated model residuals to estimate , whereas in producing the estimator Gauss, one can generate a Monte-Carlo sample of residuals as large as needed to give a non-degenerate estimate of these probabilities, which can be expected to be accurate if the Gaussian assumption is plausible. To highlight this, we present the results of a short simulation study in which for a probability , we aimed to estimate using boot and Gauss such that . This problem is hence related to the Value-at-Risk estimation. We compared the RMSE of from the two algorithms for 50 different realizations of the predictor that were simulated from the same data generating process. We note that the value of varies between 7.26 and 11.77, depending on and . In Table 2, we present the results from a subset of five predictors that were representative of the variability observed in the simulated series. It is apparent from these results that Gauss outperforms boot in all cases, and the relative advantage increases with sample size. If we look at the results for all 50 predictors, RMSE of decreases by about 15% for , 22% for , 35% for and 42% for . This gives some indication of the difference in performance that can be expected between the two methods in forecasting extreme quantiles or events whenever the Gaussian assumption is plausible.

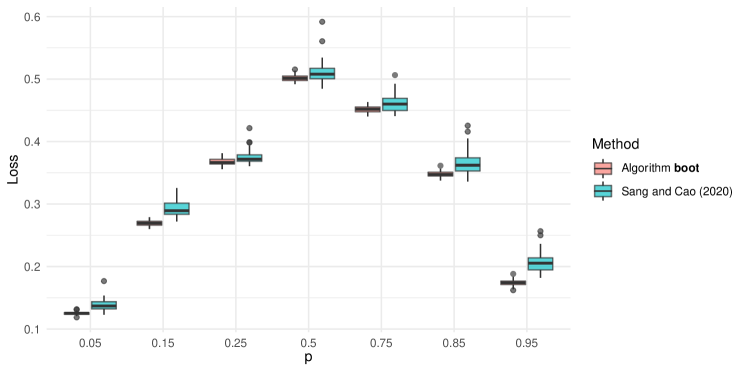

5.4 Functional quantile regression

In this application, we compare to the data analysis of Sang and Cao (2020). As in our previous example, those authors consider the functional time series of daily square-root transformed PM10 concentration curves constructed by smoothing half-hourly measurements of PM10.

The goal of the analysis is to compare forecasts of the quantiles of the maximum values (we remark the relation to Example 4), where is the transformed PM10 curve on day at intraday time . As the covariate the curve is used. Now we model the relationship between by a FAR(1) process and apply the method boot to estimate the conditional quantile of . We select the truncation parameter in order to explain 98% of the variance in the variables since for this fixed sample size, tuning by an asymptotic criterion is not meaningful. At a quantile level , we compared these methods by 5-fold cross-validation the mean check-function loss . We did this for seven different quantile levels . The experiment was repeated on 50 random splits of the data set. The results are displayed in Figure 4. In 87.4% of the cases, boot outperformed the functional single-index quantile regression model of Sang and Cao (2020) in terms of the loss considered. This advantage was much smaller for more central quantiles and became more apparent for the more extreme quantiles.

5.5 Spanish electricity price data

| 30 | 35 | 40 | 45 | 50 | 55 | 60 | 65 | 70 | ||

|---|---|---|---|---|---|---|---|---|---|---|

| boot | 0.03 | 0.06 | 0.10 | 0.13 | 0.16 | 0.24 | 0.23 | 0.19 | 0.16 | |

| GLM | 0.11 | 0.17 | 0.23 | 0.36 | 0.30 | 0.24 | 0.22 | 0.21 | 0.24 | |

| N–W | 0.05 | 0.10 | 0.20 | 0.21 | 0.22 | 0.31 | 0.29 | 0.27 | 0.26 | |

| boot | 0.05 | 0.07 | 0.10 | 0.15 | 0.15 | 0.19 | 0.17 | 0.16 | 0.12 | |

| GLM | 0.22 | 0.18 | 0.22 | 0.25 | 0.18 | 0.19 | 0.17 | 0.19 | 0.24 | |

| N–W | 0.08 | 0.14 | 0.18 | 0.22 | 0.25 | 0.26 | 0.23 | 0.22 | 0.18 | |

| boot | 0.05 | 0.10 | 0.12 | 0.13 | 0.20 | 0.17 | 0.15 | 0.13 | 0.09 | |

| GLM | 0.25 | 0.15 | 0.26 | 0.23 | 0.23 | 0.17 | 0.23 | 0.20 | 0.39 | |

| N–W | 0.10 | 0.16 | 0.23 | 0.23 | 0.26 | 0.22 | 0.24 | 0.22 | 0.14 | |

| boot | 0.08 | 0.10 | 0.11 | 0.17 | 0.20 | 0.17 | 0.15 | 0.11 | 0.07 | |

| GLM | 0.11 | 0.15 | 0.26 | 0.27 | 0.23 | 0.19 | 0.18 | 0.20 | 0.37 | |

| N–W | 0.14 | 0.17 | 0.26 | 0.24 | 0.27 | 0.23 | 0.23 | 0.17 | 0.07 | |

| boot | 0.09 | 0.11 | 0.14 | 0.19 | 0.22 | 0.18 | 0.12 | 0.08 | 0.03 | |

| GLM | 0.12 | 0.18 | 0.27 | 0.26 | 0.25 | 0.24 | 0.20 | 0.40 | 0.12 | |

| N–W | 0.16 | 0.20 | 0.23 | 0.26 | 0.28 | 0.25 | 0.19 | 0.13 | 0.02 | |

| boot | 0.14 | 0.17 | 0.20 | 0.24 | 0.23 | 0.14 | 0.08 | 0.02 | 0.00 | |

| GLM | 0.21 | 0.26 | 0.25 | 0.26 | 0.27 | 0.17 | 0.21 | 0.13 | 0.10 | |

| N–W | 0.24 | 0.29 | 0.29 | 0.31 | 0.29 | 0.19 | 0.09 | 0.03 | 0.00 |

We now return to the Spanish electricity price data that we gave as an introductory example. We take as the goal of this analysis to compare estimates for the conditional probability that the price curves will lie in specified level sets, given the covariates of demand, and wind energy production. In order to compare the various methods for doing this, we split the data into a training and testing set by randomly taking four months from each year, and assigning them to the test set, which created a 2:1 split between the training and testing set. Since we used 6 years of this data, the training set thus consists of 1453 days, and the test set consists of 731 days. Let denote one of functional variables electricity price, demand or wind energy production. Then these variables were deseasonalized as follows:

where is the yearly seasonality obtained by taking the mean for each day of the year and smoothing the result using a rolling mean with a window size of 21 days. is the weekly seasonality that is estimated as the mean for each day of the week. For the wind curves, no weekly seasonality was removed. In order to employ the methods boot and Gauss, we fit the FARX(7) model described in (2) using the estimator introduced in Section 3 with the data in the training set. The truncation parameter was again chosen in order to explain 98% of the variance of the covariates.

In order to compare the estimated conditional probabilities to the realized outcomes on the test set, we used the cross-entropy measure. The cross-entropy of a distribution relative to a distribution is defined as , where is the probability mass function of ; see Section 2.8 of Murphy (2012). Given the realisations , , and corresponding estimated conditional probabilities in the testing set of size , the plug-in estimator of the cross-entropy estimated on the test set is

We considered level sets of the form for various values of and , and calculated the cross-entropy on the test set of estimates of using the method boot, as well as for functional logistic regression, which was estimated using the same covariates (and PVE criterion) as those considered in generating the estimator in boot, as well as functional Nadaraya–Watson estimation with a Gaussian kernel with the predictors demand, wind and lagged price, and the bandwidth parameters were selected using leave-one-out cross-validation on the training set. We do not present the results for the method Gauss, as the results are again very similar to the method boot. The estimated cross entropies on the test set for each set considered are presented in Table 3. The smallest value in each cell is marked in bold font.

The method boot achieved lower values of cross-entropy on the test set compared to the competing methods for most combinations of and . boot had higher estimated cross-entropy in one case compared to functional logistic regression model, and two cases compared to functional Nadaraya–Watson estimation. The values of and considered were chosen such in a way that most price curves belong to at least one set, and so we do not think this superior performance resulted from the sets focusing on outcomes that are well modelled using the FARX(7) model.

6 Summary

We considered two methods, based on either a residual bootstrap or Gaussian process simulation, to estimate the conditional distribution , where and satisfy the functional linear regression model (1). We showed under mild consistency conditions on the estimated regression operator that these methods lead to consistent estimation, in particular in the setting where is assumed to be an element of the Banach space , which allows for the consideration of sets that describe more detailed path properties of the response. We put forward one example of an operator estimator that has the specified consistency properties under natural regularity conditions on the covariates, which allow for weak serial dependence, and on the choice of tuning parameters. In several simulation experiments and data analyses we observed that these methods generally outperformed prominent competitors, which are often more complicated to implement.

References

- Aue et al. (2015) A. Aue, D. D. Norinho, and S. Hörmann. On the prediction of stationary functional time series. Journal of the American Statistical Association, 110(509):378–392, 2015.

- Azais and Wschebor (2009) J.-M. Azais and M. Wschebor. Level sets and extrema of random processes and fields. Wiley, Hoboken, NJ, 2009.

- Berlinet et al. (2011) A. Berlinet, A. Elamine, and A. Mas. Local linear regression for functional data. Annals of the Institute of Statistical Mathematics, 63(5):1047–1075, 2011.

- Billingsley (1999) P. Billingsley. Convergence of probability measures. 1999.

- Boente et al. (2014) G. Boente, M. S. Barrera, and D. E. Tyler. A characterization of elliptical distributions and some optimality properties of principal components for functional data. Journal of Multivariate Analysis, 131:254–264, 2014.

- Bosq (2000) D. Bosq. Linear processes in function spaces: theory and applications. Lecture Notes in Statistics. Springer, New York, 2000.

- Brezis (2010) H. Brezis. Functional analysis, Sobolev spaces and partial differential equations. Springer Science & Business Media, 2010.

- Bulinskaya (1961) E. V. Bulinskaya. On the mean number of crossings of a level by a stationary gaussian process. Theory of Probability & Its Applications, 6(4):435–438, 1961.

- Chaumont and Yor (2003) L. Chaumont and M. Yor. Exercises in probability, volume 13 of cambridge series in statistical and probabilistic mathematics. Cambridge University Press, Cambridge, 2003.

- Chen and Müller (2014) K. Chen and H.-G. Müller. Modeling conditional distributions for functional responses, with application to traffic monitoring via GPS-enabled mobile phones. Technometrics, 56(3):347–358, 2014.

- Chen and Müller (2012) K. Chen and H.-G. Müller. Conditional quantile analysis when covariates are functions, with application to growth data. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 74(1):67–89, 2012.

- Chernozhukov et al. (2010) V. Chernozhukov, I. Fernández-Val, and A. Galichon. Quantile and probability curves without crossing. Econometrica, 78(3):1093–1125, 2010.

- Chiou et al. (2004) J.-M. Chiou, H.-G. Müller, and J.-L. Wang. Functional response models. Statistica Sinica, pages 675–693, 2004.

- Choi and Reimherr (2016) H. Choi and M. Reimherr. A geometric approach to confidence regions and bands for functional parameters. arXiv preprint arXiv:1607.07771, 2016.

- Crambes and Mas (2013) C. Crambes and A. Mas. Asymptotics of prediction in functional linear regression with functional outputs. Bernoulli, 19(5B):2627–2651, 2013.

- Crambes et al. (2016) C. Crambes, N. Hilgert, and T. Manrique. Estimation of the noise covariance operator in functional linear regression with functional outputs. Statistics and Probability Letters, 113:7 – 15, 2016. ISSN 0167-7152.

- Dette et al. (2020) H. Dette, K. Kokot, and A. Aue. Functional data analysis in the Banach space of continuous functions. The Annals of Statistics, 48(2), 2020.

- Fan and Müller (2021) J. Fan and H.-G. Müller. Conditional distribution regression for functional responses. Scandinavian Journal of Statistics, To Appear, 2021.

- Fernández de Castro et al. (2005) B. Fernández de Castro, S. Guillas, and W. González Manteiga. Functional samples and bootstrap for predicting sulfur dioxide levels. Technometrics, 47(2):212–222, 2005.

- Ferraty and Vieu (2006) F. Ferraty and P. Vieu. Nonparametric functional data analysis: theory and practice. Springer Science & Business Media, 2006.

- Ferraty et al. (2012) F. Ferraty, I. Van Keilegom, and P. Vieu. Regression when both response and predictor are functions. Journal of Multivariate Analysis, 109:10–28, 2012.

- Goldsmith et al. (2013) J. Goldsmith, S. Greven, and C. Crainiceanu. Corrected confidence bands for functional data using principal components. Biometrics, 69(1):41–51, 2013.

- González et al. (2018) J. P. González, A. M. S. Muñoz San Roque, and E. A. Pérez. Forecasting functional time series with a new hilbertian armax model: Application to electricity price forecasting. IEEE Transactions on Power Systems, 33(1):545–556, 2018. doi: 10.1109/TPWRS.2017.2700287.

- Hörmann and Kidziński (2015) S. Hörmann and Ł. Kidziński. A note on estimation in hilbertian linear models. Scandinavian journal of statistics, 42(1):43–62, 2015.

- Hörmann and Kokoszka (2010) S. Hörmann and P. Kokoszka. Weakly dependent functional data. The Annals of Statistics, 38(3):1845–1884, 2010.

- Hyndman and Shang (2009) R. Hyndman and H.-L. Shang. Forecasting functional time series. Journal of the Korean Statistical Society, 38:199–211, 2009.

- Hyndman and Shang (2020) R. J. Hyndman and H. L. Shang. ftsa: Functional Time Series Analysis, 2020. URL https://CRAN.R-project.org/package=ftsa. R package version 6.0.

- Imaizumi and Kato (2018) M. Imaizumi and K. Kato. PCA-based estimation for functional linear regression with functional responses. Journal of Multivariate Analysis, 163:15 – 36, 2018. ISSN 0047-259X.

- Kato (2012) K. Kato. Estimation in functional linear quantile regression. The Annals of Statistics, 40(6):3108 – 3136, 2012.

- Kudraszow and Vieu (2013) N. L. Kudraszow and P. Vieu. Uniform consistency of knn regressors for functional variables. Statistics & Probability Letters, 83(8):1863–1870, 2013.

- Liebl and Reimherr (2019) D. Liebl and M. Reimherr. Fast and fair simultaneous confidence bands for functional parameters. arXiv preprint arXiv:1910.00131, 2019.

- Mas (2007) A. Mas. Weak convergence in the functional autoregressive model. Journal of Multivariate Analysis, 98(6):1231–1261, 2007.

- Mousavi and Sørensen (2017) S. N. Mousavi and H. Sørensen. Multinomial functional regression with wavelets and lasso penalization. Econometrics and Statistics, 1:150 – 166, 2017. ISSN 2452-3062.

- Müller and Stadtmüller (2005) H. G. Müller and U. Stadtmüller. Generalized functional linear models. The Annals of Statistics, 33(2):774–805, 2005.

- Murphy (2012) K. Murphy. Machine Learning: A Probabilistic Perspective. Adaptive Computation and Machine Learning series. MIT Press, 2012. ISBN 9780262018029.

- Paparoditis and Shang (2020) E. Paparoditis and H. L. Shang. Incorporating model uncertainty in the construction of bootstrap prediction intervals for functional time series. In Nonparametric Statistics, pages 415–422, Cham, 2020. Springer International Publishing. ISBN 978-3-030-57306-5.

- Pumo (1999) B. Pumo. Prediction of continuous time processes by c[0,1]-valued autoregressive process. Statistical Inference for Stochastic Processes, 1:297–309, 1999.

- Ramsay and Silverman (2006) J. Ramsay and B. W. Silverman. Functional Data Analysis. Springer Series in Statistics. Springer New York, 2006. ISBN 9780387227511.

- Ramsay et al. (2020) J. O. Ramsay, S. Graves, and G. Hooker. fda: Functional Data Analysis, 2020. URL https://CRAN.R-project.org/package=fda. R package version 5.1.9.

- Ruiz-Medina and Álvarez Liébana (2019) M. D. Ruiz-Medina and J. Álvarez Liébana. Strongly consistent autoregressive predictors in abstract banach spaces. Journal of Multivariate Analysis, 170:186–201, 2019.

- Sang and Cao (2020) P. Sang and J. Cao. Functional single-index quantile regression models. Statistics and Computing, pages 1–11, 2020.

- Suquet (1999) C. Suquet. Tightness in schauder decomposable banach spaces. Translations of the American Mathematical Society-Series 2, 193:201–224, 1999.

- Talagrand (2014) M. Talagrand. Upper and lower bounds for stochastic processes: modern methods and classical problems, volume 60. Springer Science & Business Media, 2014.

- van der Vaart and Wellner (1996) A. van der Vaart and J. Wellner. Weak Convergence and Empirical Processes. Springer-Verlag, 1996.

- Vilar et al. (2012) J. M. Vilar, R. Cao, and G. Aneiros. Forecasting next-day electricity demand and price using nonparametric functional methods. International Journal of Electrical Power & Energy Systems, 39(1):48–55, 2012.

- Wang et al. (2016) J.-L. Wang, J.-M. Chiou, and H.-G. Müller. Functional data analysis. Annual Review of Statistics and Its Application, 3(1):257–295, 2016.

- Yao et al. (2017) F. Yao, S. Sue-Chee, and F. Wang. Regularized partially functional quantile regression. Journal of Multivariate Analysis, 156:39–56, 2017.

7 Proofs

Below for a sequence of random variables taking values in a metric space, we use the notation to denote weak convergence (convergence in distribution). We let denote unimportant positive constants that may change between uses. We state a number of Lemmata, and if their proof is not immediately given, then it is given in Appendix A.

Lemma 1.

Let be the i.i.d. noise sequence of model (1) and let be drawn independently from the same regression model. Then

| (14) |

The following slightly modified version of the continuous mapping theorem can be proven along similar lines as Theorem 1.9.5 of van der Vaart and Wellner [1996].

Lemma 2.

Let , , and be random elements of a metric space. Suppose that if and that for all . Let and let be the set of discontinuity points of . Then if , we have .

Proof of Theorem 1. We note that by Lemma 1, it suffices to show

| (15) |

To this end we define random variables which are uniformly distributed on and independent of and . A consequence of Assumption 2 b is that

Consider the indicator function and let be the discontinuity points of , i.e. . Noting that , we deduce by Lemma 2 that , provided Since is bounded, we get . Hence

and consequently (15) holds. ∎

We suppose that is a variable in distributed as a generic model error in (1).

Lemma 3.

Suppose that Assumption 3 holds. Then

Lemma 4.

Suppose that Assumption 4 holds. Then

Lemma 5.

Consider a sequence of random variables satisfying as . Additionally, let be independent from both and . Suppose there exists a mapping and a sequence of random maps , independent from , such that , and

| (16) |

Let be a continuous function. Then for all with , it holds that

Proof of Theorem 2. Lemmata 3 and 4 imply that that in the metric space if Assumption 3 or 4 holds. The theorem then follows from Lemma 5 with and . ∎

Proof of Proposition 1. We will adapt the usual Glivenko–Cantelli argument for this proof. Let . We show first that our assumptions imply that there exists a set of finitely many deterministic points such that

To this end we use the notation . If the interval is unbounded, we can choose and such and . If the interval is bounded, then we do not need this step and set . On the compact interval , the process is now uniformly continuous in probability, i.e. for every , and , there exists a which doesn’t depend on , such that implies that . Now set and .

For any , we have for some and with a probability of at least ,

Similar arguments yield

with a probability of at least . Therefore,

The proposition follows as the maximum on the right hand side converges to 0 in probability. ∎

Proof of Corollary 2. By the uniform convergence of obtained in Proposition 1 we get It is clear by definition that for all . We even have , because of the definition (6) of and the uniform convergence in probability of to a continuous function. This proves the first statement.

As for the second statement, we note that if is a.s. continuous and strictly increasing in , then (i) and (ii) for any we can find a , such that implies . Because , it follows by (i) and (ii) that

∎

Proof of Proposition 2. When is a bounded linear operator, and are centered, --approximable random sequences, where is white noise independent of , then it follows from Hörmann and Kidziński [2015] that

| (17) |

if . In particular (17) holds for both, out-of-sample and in-sample prediction, since if is uniformly distributed on , then . ∎

In order to lighten the notation, the covariance operator of a random variable will be denoted by . The usual operator norm will just be denoted by .

Proof of Proposition 3. We will show that

We will denote the inverse of the truncated estimated covariance as

and the projection onto the subspace spanned by the first eigenfunctions of as . Accordingly, . Note that and thus

| (18) |

Then

| (19) |

It follows that

| (20) |

We treat each term separately and show convergence to zero.

As for the second term in (20), we remark that The mean squared Hilbert–Schmidt norm of asymptotically vanishes since

Note that all summands with vanish due to either or being independent from all other variables. Thus, the second term in (20) vanishes.

Finally, we note that for the third term in (20) we have

Since , this converges to zero, concluding the proof of the proposition. ∎

Proof of Proposition 4. We denote all operator norms that stem from the sup-norm on with , in order to distinguish them from the operator norms with respect to the -norm. If is bounded, it means that

From the definition, it is clear that by embedding into , the inequality implies that for the respective operator norm.

We begin by showing that Assumption 2 holds. Let us first remark that in the following proof, it will not be important whether is an element of the sample or not; it suffices that . We assume and are centered to simplify the presentation. We have according to (18) that

By Lemmata 10, 12 and 13 in Hörmann and Kidziński [2015] the first term is

| (21) |

with our choice of .

As for the second summand, (8) implies that

For any and fixed ,

which clearly implies that

Due to independence of from , we have that

and the right-hand side is independent from . Let and , then

The expectation of the second term is bounded by . As for the first term, we first note that for any ,

| (22) |

due to the independence of from . We can now bound the maximum by the sum of increments and obtain

Setting , it follows that

| (23) |

Therefore, if we choose a sequence then . Lastly, we note that these results also hold if we use , where is drawn independently and uniform on . Therefore, Assumption 2 holds. This concludes the proof of the proposition. ∎

Appendix A Additional Proofs

Proof of Lemma 1. Let , , be probability spaces, such and for . The are suitable -algebras on . The measure characterizes the distribution of and the distribution of , i.e. . Then, without loss of generality, we can assume that are defined on the canonical product space

with and , where . It is clear that the transformation with is -measurable and measure preserving. We can write

where . Hence, by the ergodic theorem we have that

where is the -algebra of the invariant sets of . If is an invariant set of , it means that . Hence if , then for any and by induction we conclude that for any and any . This implies that for any we have

Thus . From Chaumont and Yor [2003, p. 29] we deduce that

where is the tail -algebra . Since by Kolmogorov’s zero-one law contains only events with probability zero or one, . ∎

In the proof of the following lemma, we will use sufficient conditions for tightness that stem from Suquet [1999]. We restate them for clarity.

Lemma 6.

Let be a set of measures on a separable Hilbert space, and an orthonormal system (ONS). Define the projection operator onto the subspace spanned by . is tight if and only if

-

(a)

is tight.

-

(b)

Proof of Lemma 3. We first show that converges to in probability. We use to denote the empirical covariance operator of the model errors, which is naturally not observable. From Theorem 4.1 of Bosq [2000], we have that as Let

It follows from elementary calculations using that that , and so in order to simplify the calculations we assume that the terms are properly centered in the definition of . For conciseness, we write

It holds that

where in the last step we used an inequality of the form . From Assumption 3 it follows via Cauchy–Schwarz that , implying that . According to Theorem 2.3 in Bosq, to show weak convergence it suffices to show that for all , and that the sequence is tight. To prove this, we note that

where is a standard normal random variable which is independent of the sample . By the considerations above it follows that . This yields the distributional convergence via Slutzky’s lemma.

We will now establish tightness of the measures. We first fix some ONS and note that is finite dimensional and

As per our assumption, the numerator is bounded for fixed and large . Thus, for each , is uniformly bounded in probability. Hence the first requirement is met. As for the second requirement, it is equivalent to

| (24) |

where we let be the eigenfunctions of . By Markov’s inequality and using , (24) follows if

For all self-adjoint and non-negative definite operators, the trace norm can be written as where all summands are non-negative. Since we can choose any an such that for all and for all it holds that . Hence

Since is arbitrary, this concludes the proof. ∎

Proof of Lemma 4. First we note that under our assumptions, the estimated noise covariance converges uniformly in probability. Plugging into the definition of and applying the Cauchy–Schwarz inequality along with , we obtain

The second part converges to zero in probability by assumption, and for the first part we can apply the law of large numbers in Banach space; see Theorem 2.4 of Bosq [2000]. Therefore, converges uniformly in probability to . To show weak convergence in , we apply Theorem 7.5 from Billingsley [1999]. First, we show that for any finite collection of ,

The right-hand side of this is multivariate Gaussian with mean zero and covariance matrix . Conditionally on , the covariance matrix of the left-hand side is and it converges uniformly in probability to . To show the convergence in distribution of the vector, the same approach as in the proof of Lemma 3 can be used, and we omit the details.

Next we show the tightness. To this end we prove that

| (25) |

We will make use of Dudley’s theorem [Talagrand, 2014], which states that for a Gaussian process on ,

where the pseudometric is defined by and denotes the number of balls of size in the pseudometric that are needed to cover the whole interval . Thus, if we fix an , then conditionally on we have

where is a universal constant. We also remark that is -measurable. By Assumption 4 (b) we have that and hence implies . Moreover, . Thus, we obtain

Taking the expectations, we see that

with the bound being independent from and vanishing as . In particular we note that has a modification with continuous sample paths, i.e. for all . Returning to (25), we obtain by Markov’s inequality that

This holds for all and therefore implies in . ∎

Proof of Lemma 5. Define the set with

| and |

It can thus be easily deduced that for we have . This in turn implies by the continuous mapping theorem that . For such that , and if , it follows that

Now notice that if is independent of , and , then we have that

What is left to show is that . We have by assumption that . We know that for all ,

where we used dominated convergence and (16). Because the expectation vanishes, it must hold that

Therefore, by -subadditivity

Weak convergence follows via the Portmanteau theorem, concluding the proof.∎

Proof of Proposition 5. We first show that Assumption 4 (a) holds. We use the same decomposition of as before to obtain

For the first summand on the right we have by (23)

which by our choice of converges to zero. For the second summand, we take the expectation and see that with our choice of ,

Thus, the second summand is . Therefore, Assumption 4 (a) holds. As for Assumption 4 (b), we observe

Note that

It follows from Assumption 6 that

Taking the expectation and using (22) for the last term, we have that

Since , the right-hand side is bounded uniformly in and Assumption 4 (b) holds.

Lemma 7.

Suppose and . Then .

Proof.

We can consider and as random variables on the probability space . Convergence implies also weak convergence . This means that

in all continuity points of . The condition implies that is a continuity point. ∎

Proof of Proposition 6. We define the set

We show that and by assumption . To this end we note that means that there exists a sequence such that (i) and one of the pairs

| (ii) | |||

| (ii’) |

holds. We assume that (ii) and (iii) for all . We show that (i), (ii) and (iii) imply that . To achieve a contradiction, we suppose that (i), (ii) and (iii) hold along with

| (iv) and (v) . |

By (ii) and (iv) it follows that (vi) . In Lemma 7 below we will show that (i) and (v) imply that

| (vii) |

Now (vi) and (iii) contradict to (vii). For the case (ii’) and (iii’) we can argue similarly. This shows part (a). For part (b) we can argue along the same line as for part (a). ∎

Proof of Proposition 7. Fix and , and let . Since is also a continuously differentiable Gaussian process sharing the same covariance as , we may assume without loss of generality that in the definition of . Let , where denotes the number of elements in . By Theorem 1 of Bulinskaya [1961], is finite with probability one, which implies (10)(i). Moreover, letting , with , it follows from the proof of Theorem 1 in Bulinskaya [1961], specifically equation (2) therein and the subsequent calculations, that there exists so that . From this we obtain that

| (26) |

Clearly . For each , we define the following collections of points in , with and :

Set . and define the set of all possible points at which the process can cross zero times, with each crossing spaced at least a width apart, such that , respective of whether the process starts above or below zero. Evidently then for ,

| (27) |

We define for all

Elementary calculations making use of the fact that the definitions of and prescribe a single linear constraint on the points give that . For , let be a sequence of real numbers tending to infinity such that . Then, due to the assumption that is continuously differentiable, if , as , where is the derivative of . It follows that

Note that on the set , the derivative of is uniformly bounded by , and hence on this set at any point at which , there must exist a nearby point of the form for some such that , and . It follows that

where in the last inequality, we used the fact that the joint density of is bounded from above for all . This follows from the assumption that the determinant of the correlation matrix of is bounded from below by a constant multiplied by a positive power of the minimal distance between , the latter of which is bounded from below for by . Letting gives then that , which in conjunction with (26) and (27) implies (10)(ii). When is twice continuously differentiable with having a non-degenerate distribution, (11) follows from Theorem 7.3 of Azais and Wschebor [2009].∎

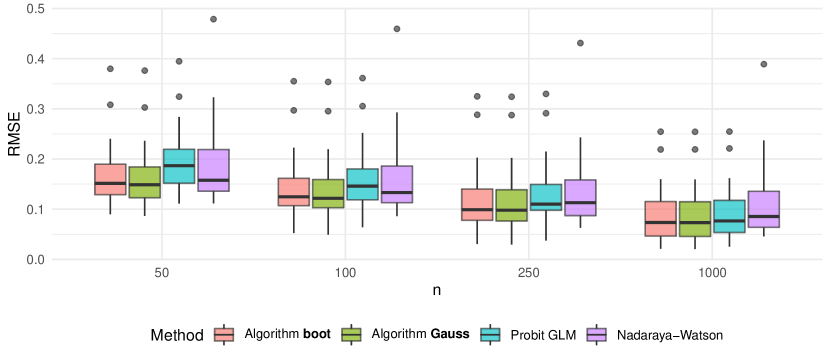

Appendix B Additional simulation results

We present here some additional simulation results from Section 5.3. For each sample we estimated the conditional probability of lying in the level set , and lying in the contrast set . We took the function to be a step-function that compares the mean between 2-4am and 7-9am, thus estimating the rise of the pollutant levels every morning. We compared the estimators from algorithms boot and Gauss, as well as from a probit GLM and Nadaraya–Watson estimation. We calibrated the bandwidth for the Nadaraya–Watson estimator using leave-one-out cross-validation on each generated sample. The results in terms of the root mean squared error (RMSE) over the 1000 simulations are displayed in Figure 5 for the contrast set. Additional results for specific values of are displayed in Table 5. We remark that the choice of a probit or a logit link in the GLM appeared to have little influence on the predictive performance of the level set case. For contrast sets, given how the data was generated, the functional logistic regression model with probit link is in fact correctly specified, and we saw in this case that it tended to perform similarly well as boot and Gauss in large sample sizes. In smaller sample sizes, its performance suffers from the lost information during the estimation.

| boot | Gauss | GLM | N–W | boot | Gauss | GLM | N–W | ||

| 1 | 0.053 | 0.139 | 0.134 | 0.190 | 0.356 | 0.086 | 0.083 | 0.099 | 0.252 |

| 2 | 0.449 | 0.157 | 0.155 | 0.238 | 0.217 | 0.126 | 0.122 | 0.165 | 0.166 |

| 3 | 0.772 | 0.095 | 0.088 | 0.139 | 0.140 | 0.068 | 0.063 | 0.100 | 0.112 |

| 4 | 0.914 | 0.066 | 0.059 | 0.092 | 0.189 | 0.045 | 0.041 | 0.062 | 0.160 |

| 5 | 0.969 | 0.037 | 0.033 | 0.045 | 0.134 | 0.022 | 0.018 | 0.027 | 0.101 |

| boot | Gauss | GLM | N–W | boot | Gauss | GLM | N–W | ||

| 1 | 0.053 | 0.052 | 0.050 | 0.054 | 0.181 | 0.034 | 0.033 | 0.036 | 0.129 |

| 2 | 0.449 | 0.080 | 0.077 | 0.104 | 0.129 | 0.045 | 0.045 | 0.060 | 0.101 |

| 3 | 0.772 | 0.046 | 0.042 | 0.066 | 0.080 | 0.028 | 0.028 | 0.048 | 0.052 |

| 4 | 0.914 | 0.028 | 0.027 | 0.039 | 0.126 | 0.019 | 0.018 | 0.023 | 0.089 |

| 5 | 0.969 | 0.014 | 0.012 | 0.017 | 0.075 | 0.010 | 0.009 | 0.009 | 0.048 |

| boot | Gauss | GLM | N–W | boot | Gauss | GLM | N–W | ||

| 1 | 0.161 | 0.090 | 0.086 | 0.111 | 0.166 | 0.067 | 0.065 | 0.079 | 0.132 |

| 2 | 0.110 | 0.149 | 0.147 | 0.155 | 0.232 | 0.137 | 0.135 | 0.138 | 0.219 |

| 3 | 0.524 | 0.180 | 0.177 | 0.200 | 0.179 | 0.163 | 0.160 | 0.172 | 0.167 |

| 4 | 0.417 | 0.149 | 0.144 | 0.187 | 0.123 | 0.115 | 0.112 | 0.145 | 0.102 |

| 5 | 0.356 | 0.194 | 0.192 | 0.227 | 0.150 | 0.170 | 0.169 | 0.192 | 0.127 |

| boot | Gauss | GLM | N–W | boot | Gauss | GLM | N–W | ||

| 1 | 0.161 | 0.057 | 0.056 | 0.062 | 0.085 | 0.049 | 0.048 | 0.051 | 0.049 |

| 2 | 0.110 | 0.120 | 0.119 | 0.123 | 0.192 | 0.086 | 0.086 | 0.087 | 0.160 |

| 3 | 0.524 | 0.150 | 0.149 | 0.154 | 0.149 | 0.108 | 0.107 | 0.111 | 0.140 |

| 4 | 0.417 | 0.082 | 0.080 | 0.099 | 0.070 | 0.049 | 0.048 | 0.056 | 0.050 |

| 5 | 0.356 | 0.152 | 0.151 | 0.162 | 0.114 | 0.118 | 0.117 | 0.121 | 0.110 |