Ridge Regularized Estimation of VAR

Models for Inference

Abstract: Ridge regression is a popular method for dense least squares regularization. In this work, ridge regression is studied in the context of VAR model estimation and inference. The implications of anisotropic penalization are discussed and a comparison is made with Bayesian ridge-type estimators. The asymptotic distribution and the properties of cross-validation techniques are analyzed. Finally, the estimation of impulse response functions is evaluated with Monte Carlo simulations and ridge regression is compared with a number of similar and competing methods.

Keywords: ridge regularization, vector autoregression, inference, impulse responses

JEL codes: C32, C51, C52

1 Introduction

While the idea of using ridge regression for vector autoregressive model estimation dates back to Hamilton, (1994), there seems to be no complete analysis of its properties and asymptotic theory in the literature. This paper fills this gap by analyzing the geometric and distributional properties of ridge in a VAR estimation framework, discussing its comparison to well-known Bayesian approaches and deriving the validity of cross-validation as a selection procedure for the ridge penalty.

First, I show that the shrinkage induced by the ridge estimator, while intuitive in the setting of an isotropic penalty, produces complex effects when estimating a VAR model with a more flexible penalization scheme. This implies that the benefits of the bias-variance trade-off (Hastie, , 2020) may be be hard to gauge a priori. I provide a tractable example where ridge can yield estimates that have higher autoregressive dependence than the least squares solution. To better understand how different ridge penalization strategies can be designed, I also make a comparison with Bayesian VAR estimators commonly used in macroeconometric practice.

Second, I generalize the analysis of Fu and Knight, (2000) and prove the consistency and asymptotic normality of the ridge estimator, a result that seems to be missing in the literature. For standard inference, the ridge penalty should either be negligible in the limit or its centering converge in probability to the true parameter vector. In both these cases, there is no asymptotic bias and no reduction in variance. Alternatively, in settings where a researcher is willing to assume that a subset of the VAR parameters features small coefficients, one can achieve an asymptotic reduction of variance by correctly tuning the ridge penalty matrix. I further derive the properties of cross-validation, which is a popular approach in practical applications to tune penalized estimators (Hastie et al., , 2009, Bergmeir et al., , 2018). More specifically, I show that cross-validation is able to select penalties that are asymptotically valid for inference. In passing, I also prove that in an autoregressive setup the time dependence of regressors has an exponentially small effect on in-sample prediction error evaluation.

Lastly, I use Monte Carlo simulations to study the performance of the different ridge approaches discussed, focusing on impulse response inference. I consider two exercises: one is based on a three-variable VARMA(1,1) data generating process from Kilian and Kim, (2011); the other is a VAR(5) model estimated in levels from a set of seven macroeconomic series, following Giannone et al., (2015). The finding is that ridge can lead to improvements over unregularized methods in impulse response confidence interval length, while Bayesian estimators show the best overall performance due to the underlying flexibility of their priors.

Related Literature.

This paper does not discuss the high-dimensional setting, where the number of regressors grows together with the sample size. Some important work has been done in this direction already. Dobriban and Wager, (2018) derive an explicit expression for the predictive risk of ridge regression assuming a high-dimensional random effects model. Other works in this vein are Liu and Dobriban, (2020), Patil et al., (2021) and Hastie et al., (2022), which are mostly focused on penalty selection by cross-validation as well as structural features of ridge. Generally speaking, the complexity of analyzing ridge regression in high dimensions is a challenge to precisely understanding its practical implications. As I show below, in the context of finite-dimensional VARs, asymptotic inference demands that the ridge penalty becomes asymptotically negligible at appropriate rates. Thus, a challenge is understanding in what way high-dimensional time series problems would benefit from the use of ridge. This question is beyond the scope of this paper.

In the time series forecasting literature, ridge regression is commonly used for prediction. I provide a partial list of contributions in this direction. Inoue and Kilian, (2008) use ridge regularization for forecasting U.S. consumer price inflation and argue that it compares favorably with bagging techniques; De Mol et al., (2008) use a Bayesian VAR with posterior mean equivalent to a ridge regression in forecasting; Ghosh et al., (2019) again study the Bayesian ridge, this time however in the high-dimensional context; Goulet Coulombe et al., (2022), Fuleky, (2020), Babii et al., (2021), and Medeiros et al., (2021) compare LASSO, ridge and other machine learning techniques for forecasting with large economic datasets. Fuleky, (2020) gives a textbook treatment of penalized time series estimation, including ridge, but does not discuss inference. The ridge penalty is considered within a more general mixed - penalization setting in Smeekes and Wijler, (2018), who study the performance and robustness of penalized estimates for constructing forecasts.

Regarding inference, Li et al., (2022) provided a general exploration of shrinkage procedures in the context of structural impulse response estimation. Very recently, Cavaliere et al., (2022) suggested a methodology for inference on ridge-type estimators that relies on bootstrapping. Finally, shrinkage of autoregressive models to constrained sub-models was discussed by Hansen, 2016b in a more general setting.

Finally, various estimation problems can either be cast as or augmented with ridge-type regressions. Goulet Coulombe, (2023) shows that the estimation of VARs with time-varying parameters can be written as ridge regression. Plagborg-Møller, (2016) and Barnichon and Brownlees, (2019) both use ridge to derive smoothed local projection impulse response functions.

Outline.

Section 2 provides a discussion of the ridge penalty and the ridge VAR estimator. In Section 3 I deal with the properties of ridge-induced shrinkage in the autoregressive coefficients. I discuss the connections between frequentist and Bayesian ridge for VAR models within Section 4. Section 5 develops the asymptotic theory and inference result in the case where there is no asymptotic shrinkage. This includes studying the property of cross-validation under dependence. Section 6 provides inference and CV results in a setting where some shrinkage of a subset of parameters is possible. Section 7 presents Monte Carlo simulations focused on impulse response estimation. Section 8 concludes. Finally, the Appendix contains more detailed derivations, as well as all proofs and supplementary information.

Notation.

Define to be the set of strictly positive real numbers. Vectors and matrices are always denoted with lower and upper-case letters, respectively. Throughtout, I will use to represent the identity matrix of dimension . For any vector , is the Euclidean norm. For any matrix , is the spectral norm unless stated otherwise; is the maximal entry norm; is the Frobenius norm; is the vectorization operator and is the Kronecker product (Lütkepohl, , 2005). If a vector represents a vectorized matrix, then it will be written in bold, that is, for I write . Let , for all . To give the partial ordering of diagonal positive semi-definite penalization matrices, let and . I write if for all ; if for all and such that . Symbols and are used to indicate convergence in probability and convergence in distribution, respectively.

2 Ridge Regularized VAR Estimation

Let be a -dimensional vector autoregressive process with lag length and parametrization

| (1) |

where is additive noise such that are identically, independently distributed with and , and is a deterministic trend. For simplicity, in the remainder I shall assume that so that has no trend component – equivalently, is a de-trended series.

For a given sample size define , , , , , and vectorized counterparts , and . Accordingly, and , where . Importantly, throughout this work, I will assume that the cross-sectional dimension remains fixed.

Ridge regularization is a modification of the least squares objective by the addition of a term dependent on the Euclidean norm of the coefficient vector. The isotropic Ridge-regularized Least Squares (RLS) estimator is therefore defined as

where is the scalar regularization parameter or regularizer. When is replaced with quadratic form for a positive definite matrix the above is often termed Tikhonov regularization. To avoid confusion, I shall also refer to it as “ridge”, since in what follows will always be assumed diagonal. Since does not, in general, penalize coefficients equally, it will yield an anisotropic ridge estimator.

By solving the normal equations (see Appendix A.1), the RLS estimator with positive semi-definite regularization matrix is shown to be

When a centering vector is included in penalty , the RLS estimator becomes

| (2) |

In the context of multivariate estimation, one has to make a further distinction between two related types of ridge estimators. I let be the de-vectorized coefficient estimator obtained from reshaping to a matrix. But one can also consider the matrix RLS estimator given by

where and is a centering matrix. The distinction is important because the vectorized and matrix RLS estimators in general need not coincide. As discussed in Appendix A.2, allows for more general penalty structures compared to . I, therefore, focus on the former rather than the latter.

3 Shrinkage

In this section, I discuss both the isotropic ridge penalty, i.e. the “standard” ridge approach, as well as an anisotropic penalty that is better adapted to the VAR setting. An important result is that, even in simple setups with only two variables, the shrinkage induced by ridge can either increase or reduce bias, as well as the stability of autoregressive estimates.

Throughout this section, I consider fixed design matrices and the focus will be on the geometric properties of ridge.

3.1 Isotropic Penalty

The most common way to perform a ridge regression is through isotropic regularization, that is, for some scalar . Isotropic ridge has been extensively studied, see for example the comprehensive review of Hastie, (2020). In regards to shrinkage, an isotropic ridge penalty can be readily studied.

Proposition 1.

Let , for be regression matrices. For and isotropic RLS estimator it holds

Proof.

Using the full singular-value decomposition (SVD), decompose where is orthogonal, is diagonal and is orthogonal. Write

Since , the term within brackets is . Moreover, because the spectral norm is unitary invariant and , it follows that

Finally, by the sub-multiplicative property it holds

as claimed. ∎

Proposition 1 and its proof expose the main ingredients of ridge regression. From the SVD of used above, it is clear that ridge regularization acts uniformly along the orthogonal directions that are the columns of . The improvement in conditioning of the inverse comes from all diagonal factors being well-defined even when (as is the case in collinear systems).

However, directly applying isotropic ridge to vector autoregressive models is not necessarily the most effective estimation approach. Stable VAR models show decay in the absolute size of coefficients over lags. So it is reasonable to chose a more general ridge penalty that can accommodate lag decay.

3.2 Lag-Adapted Penalty

I now consider a different form for that is of interest when applying ridge specifically to a VAR model. Define family of lag-adapted ridge penalty matrices as

where each intuitively implies a different penalty for the elements of each coefficient matrix , .111Note that with a lag-adapted penalty it is also possible to directly use the matrix ridge estimator since the penalty for is given by , see Appendix A.2. Family allows imposing a ridge penalty that is coherent with the lag dimension of an autoregressive model. It is parametrized by distinct penalty factors, meaning that the penalization is anisotropic.

Proposition 2.

Let , for be multivariate VAR regression matrices. Given subset of cardinality , for define as the vector of coefficient estimates located at indexes for . Let be the complement of .

-

(a)

If , then for any . The inequality is strict when .

-

(b)

Let be the least squares estimator of the autoregressive model with only the lags indexed by included and zeros as coefficients for the lags indexed by . Similarly, let be the subset of diagonal elements in penalizing the lags in . Then

where and are to be intended as the element-wise convergence.

Proposition 2 shows that the limiting geometry of a lag-adapted ridge estimator is thus identical to that of a least squares regression run on the subset specified by . By controlling the size of coefficients it is therefore possible to obtain pseudo-model-selection. However, in the next section I show that anisotropic penalization produces complex effects on the models’ coefficient estimates.

3.3 Effects of Anisotropic Penalization

In this section, I explore the effect of a lag-adapted ridge penalty on the estimate VAR coefficients, and, more generally, the properties of ridge estimators with anisotropic penalization.

Since ridge operates along the principal components, there is no immediate relationship between a specific subset of estimated coefficients and a given diagonal block of . For autoregressive modeling, three effects are of interest: the shrinkage of coefficient matrices relative to the choice of ; the entity of the bias introduced by shrinkage, and the impact of shrinkage on the persistence of the estimated model.

To evaluate these effects, I consider a simple VAR(2) model

where

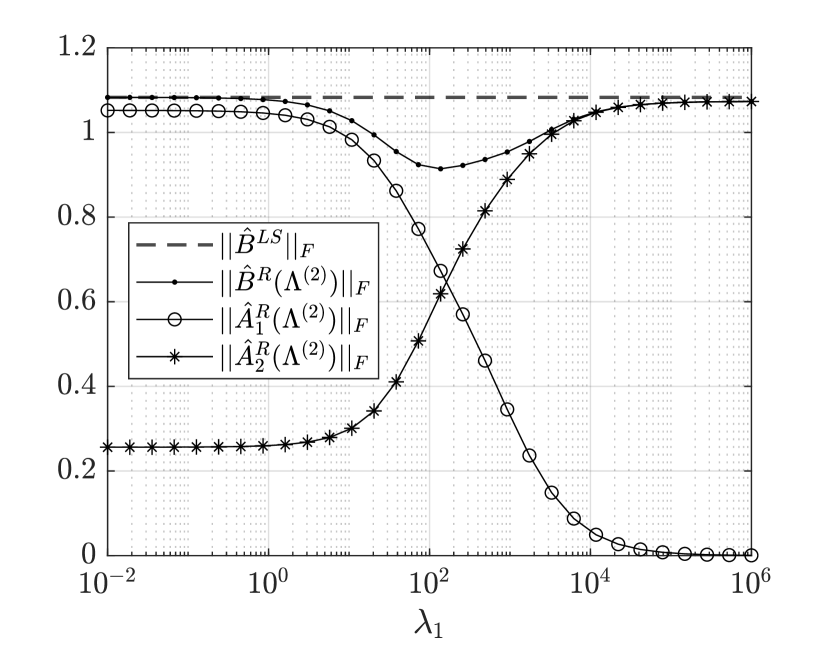

A sample of length is drawn, demeaned and used to estimate coefficients and . The VAR(2) model is fitted using the lag-adapted ridge estimator , where , which can be partitioned into estimates and .

Shrinkage.

To study shrinkage, I consider the restricted case of and . The ridge estimator is computed for varying over a logarithmically spaced grid. Figure 1(a) shows that for , but as the penalty increases decreases while grows. The resulting behavior of is non-monotonic in , although indeed in the limit . This effect is due to the model selection properties of lag-adapted ridge, and the resulting omitted variable bias. Therefore, in practice it is not generally true that anisotropic ridge induces monotonic shrinkage of estimates.

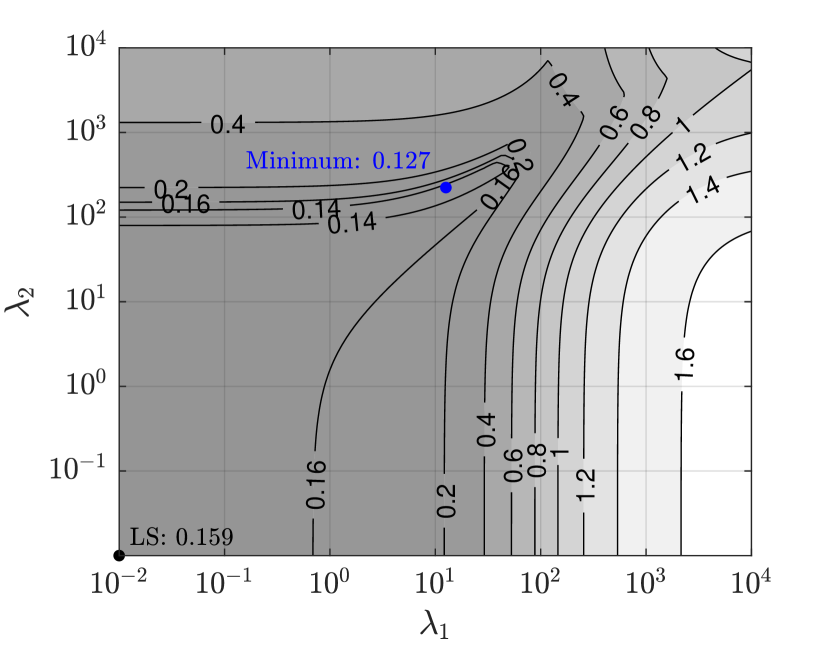

Bias.

Since ridge bias is hard to study theoretically, I use a simulation with the same setup of Figure 1(a), this time with . The grid is logarithmic with points. Figure 1(b) presents a level plot of the sup-norm ridge bias given multiple combinations of and . While there can be gains compared to the least squares estimator , they are modest. Moreover, level curves of the bias surface show that gains concentrate in a very thin region of the parameter space. Consequently, in practice any (data-driven) ridge penalty selection criterion is unlikely to yield bias improvement over least squares. Yet, in large VAR models with many lags the reduction in variance of the ridge estimator often yields improvements over unregularized procedures (Li et al., , 2022). However, the bias-variance trade-off in ridge is not a free-lunch when performing inference. Pratt, (1961) showed that it is not possible to produce a test (equivalently, a CI procedure) which is valid uniformly over the parameter space and yields meaningfully smaller confidence intervals than any other valid method.

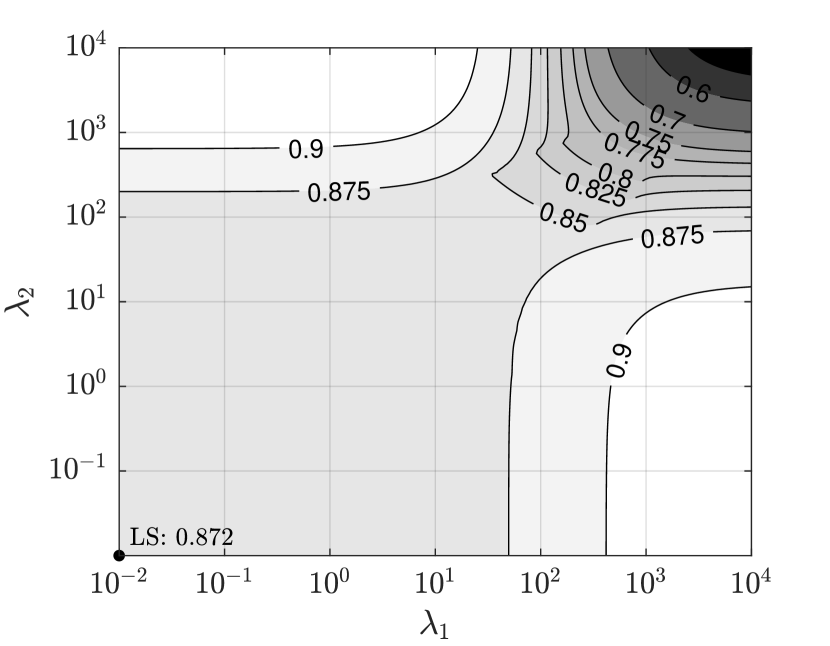

Stability.

To study the stability of ridge VAR estimates, I reuse the results of the bias simulation above. Let be the companion matrix of , and the companion matrix of estimates . For all combinations , I compute the largest eigenvalue of . Note that if , then the estimated VAR(2) is stable (Lütkepohl, , 2005). Figure 1(c) presents the level sets for the surface of maximal eigenvalue moduli, and for comparison is shown at the origin.222If , then by continuity of eigenvalues it follows that , see Appendix A.3. While along the main diagonal there is a clear decrease in as isotropic penalization increases, when is large and (or vice versa) the maximal eigenvalue increases instead. Therefore, an estimate of a VAR model obtained with anisotropic ridge may be closer to unit root than the least squares estimate.

4 Bayesian and Frequentist Ridge

So far, I have discussed standard ridge penalization schemes. In this section, I study the posterior mean of Bayesian VAR (BVAR) priors commonly applied in the macroeconometrics literature. I show that such posteriors are in fact specific GLS formulations of the ridge estimator. This comparison highlights that ridge can be seen as a way to embed prior knowledge into the least squares estimation procedure by means of centering and rescaling coefficient estimates.

4.1 Litterman-Minnesota Priors

In Bayesian time series modeling, the so-called Minnesota or Litterman prior has found great success (Litterman, , 1986). For stationary processes which one believes to have reasonably small dependence, a zero-mean normal prior can be put on the VAR parameters, with non-zero prior variance. Assuming that the covariance matrix of errors is known, the Litterman-Minnesota has posterior mean

| (3) |

where is the prior covariance matrix of (Lütkepohl, , 2005). It is common to let be diagonal, and often the entries follow a simple pattern which depends on lag, individual components variances, and prior hyperparameters. For example, Bańbura et al., (2010) suggest the following structure for the diagonal

| (4) |

where is the prior variance for coefficients for and . Here, is the -th diagonal element of , specifies beliefs on the explanatory importance of own lags relative to other variables’ lags, while controls the overall tightness of the prior. The extreme yields a degenerate prior centered at , while reduces the posterior mean to OLS estimate . Factor , which explicitly shrinks variance at higher lags, was originally introduced by De Mol et al., (2008), who formally developed the idea that coefficients at deeper lags should be coupled with more penalizing priors. Note that, in (4), assuming for all and setting , produces a that has a lag-adapted structure with quadratic lag decay.

Equation (3) more generally demonstrates that the Minnesota posterior mean is equivalent to a ridge procedure. It is important to notice that, while with least squares the OLS and GLS estimators of VAR coefficients coincide, this is not the case with ridge regression. Regularizing a GLS regression will yield

| (5) |

instead of , which is equivalent to (3) under an appropriate choice of . While I develop the asymptotic results for assuming a centering parameter in general, I do not directly study the properties . The generalization to GLS ridge employing the least squares error covariance estimator should follow from straightforward arguments. In Section 7, I focus on providing evidence on the application in terms of its pointwise impulse response estimation mean-squared error.

4.2 Hierarchical Priors

Recent research on Bayesian vector autoregressions exploit more sophisticated priors compared to the Litterman-Minnesota design. Giannone et al., (2015) develop an advanced BVAR model by setting up hierarchical priors which entail not only model parameters, but also hyperparameters. They impose

for hyperparameters , , and , where IW is the Inverse-Wishart distribution. Here, too, scalar controls prior tightness. Let be the matrix form of the VAR coefficient prior mean, so that . The resulting (conditional) posterior mean is given by

| (6) |

Observe that equation (6) is effectively equivalent to a centered ridge estimator, c.f. (2).

The introduction of a hierarchical prior leaves space to add informative hyperpriors on the model hyperparameters, allowing for a more flexible fit. Indeed, removing the zero centering constraint from the prior on can improve estimation. It is often the case that economic time series show a high degree of correlation and temporal dependence, therefore imposing as in the Minnesota prior is inadequate. In fact, Giannone et al., (2015) show that their approach yields substantial improvements in forecasting exercises, even when hyperparameter priors are relatively flat and uninformative.

5 Standard Inference

In this section, I state the main asymptotic results for the RLS estimator with general regularization matrix . I shall allow and non-zero centering coefficient to be, under appropriate assumptions, random variables dependent on sample size . In particular, may be a consistent estimator of .

I will impose the following assumptions.

Assumptions

-

A.

is a sequence of i.i.d. random variables with , covariance non-singular positive definite and , .

-

B.

There exists such that for all complex , .

-

C.

There exist such that , where is the autocovariance matrix of and , are its largest and smallest eigenvalues, respectively.

Assumption A is standard and allows to prove the main asymptotic results with well-known theoretical devices. Assuming is white noise or assuming respects strong mixing conditions (Davidson, , 1994) would require more careful consideration in asymptotic arguments but is otherwise a simple generalization, although more involved in terms of notation, see e.g. Boubacar Mainassara and Francq, (2011).

Assumption B guarantees that has no unit roots and is stable. Of course, many setups of interest do not satisfy this assumption, the most significant ones being unit roots, cointegrated VARs, and local-to-unity settings. Incorrect identification of unit roots does not invalidate the use of LS or ML estimators (Phillips, , 1988, Park and Phillips, , 1988, 1989, Sims et al., , 1990), however inference is significantly impacted as a result (Pesavento and Rossi, , 2006, Mikusheva, , 2007, 2012).

Assumption C is standard in the literature regarding penalized estimation and does not imply significant additional constraints on the process , cf. Assumption A. It is sufficient to ensure that for large enough the plug-in sample autocovariance estimator is invertible even under vanishing .

Before stating the main theorems, let

be the regression covariance matrix, regression residuals and sample innovation covariance estimator, respectively.

Theorem 1.

Let Assumptions A-C hold and define be the centered RLS estimator as in (2). If and , where is positive semi-definite diagonal matrix and is a constant vector, then

-

(a)

,

-

(b)

,

-

(c)

,

-

(d)

.

Theorem 1 considers the most general case, and, as previously mentioned, gives the asymptotic distribution of under rather weak conditions for the regularizer . The resulting normal limit distribution is clearly dependent on the unknown model parameters , complicating inference.

However, it is possible – under strengthened assumptions for or – for to have a zero-mean Gaussian limit distribution.

Theorem 2.

In the setting of Theorem 1, results (a)-(c) hold and (d) simplifies to

-

(d′)

if either

-

(i)

,

-

(ii)

and .

The following corollary is immediate.

Corollary 1.

Let be a consistent and asymptotically normal estimator of . Then, under condition (i) or (ii) of Theorem 2 results (a)-(d′) hold.

5.1 Joint Inference

To handle smooth transformations of VAR coefficients, such as impulse responses (Lütkepohl, , 1990), I also derive a standard joint limit result for both and the variance estimator .

Theorem 3.

5.2 Cross-validation

In practice, the choice of ridge penalty is often data-driven, and cross-validation is an very popular approach to select . I now turn to the properties of CV as applied to .

For simplicity, assume that is an AR() process, that is, . In this setting,

where . Following Patil et al., (2021), the prediction error of ridge estimator given penalty is

where and are random variables from an independent copy of . In particular, is the vector of lags of . Moreover, the error curve for is given by

The prediction error is crucial because it allows to determine the oracle optimal penalization,

Clearly, is unavailable in practice and must be substituted with a feasible alternative. Cross-validation proposes to construct a collection of paired, non-overlapping subsets of the sample data such that the first subset of the pair (estimation set) is used to estimate the model, while the second (validation set) is used to provide an empirical estimate of the prediction error. The CV penalty is then selected to minimize the total error over validation sets. A very popular approach to build cross-validation subsets is -fold CV, wherein the sample is split into blocks, so-called folds, of sequential observations (possibly after shuffling the data). Each fold determines a validation set, and is paired with its complement, which gives the estimation set. For more details, see e.g. Hastie et al., (2009).

Again with the intent of keeping complexity low – as this work is not focused on cross-validation – I will make the additional simplifying assumption that CV is implemented with two folds and one pair. Specifically, the first fold is the estimation set, where and are constructed and is estimated. The second fold is the validation set and yields , , where and . To account for dependence, a buffer of observations between validation and estimation folds is introduced. The last observation of in the estimation set is , while the first observation in validation set is , that is, the total number of available observations is . This is a stylized version of the CV setup of Burman et al., (1994) – also called -block or non-dependent cross-validation in Bergmeir et al., (2018) – and is effectively equivalent to an out-of-sample (OOS) validation scheme. Thus, the 2-fold -buffered CV error curve is

| (7) |

Theorem 4.

Under Assumptions A-C, for every in the cone of diagonal positive definite penalty matrices with diagonal entries in , , it holds that

as . Furthermore, the convergence is uniform in over compact subsets of penalty matrices.

In the current setup, the joint limit should be thought as , where aspect ratio determines the balance of the cross-validation split.

Remark 1.

Theorem 4 thus shows that gives an asymptotically valid way to evaluate the prediction error curve, and thus tune , over any compact set of diagonal positive semi-definite penalization matrices. Moreover, in Theorem 7, Appendix C.2, I show that the impact of dependence due to the VAR data generating process is exponentially small for sufficiently large. This property of is desirable because it lets one choose small also in applications with moderate sample sizes, and theoretical justifies the prescription of Burman et al., (1994).

5.3 Asymptotically Valid CV

So far, I have shown that a simple 2-fold CV – or, equivalently, out-of-sample validation – correctly estimates the predictive error of the ridge estimator, even under dependence. I turn now to the question of selecting an asymptotically valid penalty, that is, a such that condition (1) of Theorem 2 is fulfilled. This enables inference, since one is in a setting where the bias is asymptotically negligible.

The idea is to scale the ridge penalty used at the estimation step of CV by a factor , so that the validated penalty converges to zero at an appropriate rate as both and grow. In other words, an over-smoothed ridge regression turns out to be key when studying cross-validation. To derive this result, first let

be the over-smoothed ridge estimator.

Theorem 5.

Under Assumptions A-C, let be the compact set of diagonal positive semidefinite penalization matrices such that . It holds

Remark 2.

The previous theorem is stated in terms of the oracle predictive error , which equals the 2-fold CV error curve up to a factor of order . Therefore, assuming that the CV aspect ratio is strictly between zero and one, the result of Theorem 5 also directly generalizes to an empirically cross-validated penalty.

6 Inference with Shrinkage

Fu and Knight, (2000) have argued that results such as Theorems 1 and 2 portray penalized estimators in a somewhat unfair light, because they result in asymptotic distributions showing no bias-variance trade-off. Indeed, they show that ridge shrinkage yields estimates with asymptotic variance no different than that of least squares. Of course, in finite samples shrinkage has an effect on since is used in place of to estimate the error term variance matrix. To better understand the value of ridge penalization in practice, one should therefore consider the situation where a number of VAR coefficients are small, but not necessarily zero.

Formally, assume that for some one can partition the VAR coefficients as , where and , and assume that for and is fixed. Such ordered partitioning of is without loss of generality.333The dimensions of and are chosen to be multiples of to better conform to the lag-adapted setting. This choice is also without loss of generality and simplifies exposition. In this context, it is desirable to penalize and differently when constructing the ridge penalty. From a practical perspective, one can consider, for example, the case of a VAR() model derived by inverting a stable VARMA() process: for sufficiently large, coefficient matrices decay exponentially to zero.444This result follows from a straightforward generalization of Lemma 1 in Appendix C. The choice of norm to measure such decay is not fundamental as they are equivalent given that dimension is fixed. In a finite sample, an asymptotic framework with non-negligible penalization of higher-order lag coefficients can be more appropriate than that of Theorem 1. This approach to inference is also in the vein of De Mol et al., (2008), who argue for explicit lag penalization into BVAR priors on similar grounds. Thus, the idea of partitioned penalization exploits prior information on the structure of autoregressive coefficients to asymptotically improve on the bias-variance trade-off. In the context of maximum-likelihood estimation, the use of appropriate and plausible model restrictions to improve efficiency by shrinkage, rather then perform hypothesis testing, has also been discussed by Hansen, 2016a .

Let where and . Assume that

for a fixed vector . In particular, letting and ,

| (8) |

One can now develop an asymptotic result which shows non-negligible shrinkage in the limit distribution of the ridge estimator. For simplicity of exposition, here I will assume that ridge centering is chosen to be zero.

Theorem 6.

It is easy to see that indeed the term in Theorem 6 is weakly smaller than in the positive-definite sense. Note that

The last inequality is true by definition of . Shrinkage gains are concentrated at the components that have non-zero asymptotic shrinkage, i.e. those penalized by .

Remark 3.

A key point in the application of Theorem 6 is identification of and . In practice, one may then proceed in two ways. As discussed in Section 4, one can see the ridge approach as a frequentist “counterpart” to implementing a Bayesian prior. Therefore, the researcher may split into subsets of small and large parameters based on economic intuition, domain knowledge or preliminary information. Alternatively, in the following section I show that cross-validation is automatically able to tune appropriately.

6.1 Cross-validation with Partitioned Coefficients

One can use the same approach applied to derive Theorem 5 in order to show that cross-validating the RLS estimator with is also asymptotically valid.

Corollary 2.

In theory, one would like to be able to quantify the gains obtained in the asymptotic shrinkage setup of Theorem 6 compared to the standard setting of Theorems 1 and 2, particularly when using cross-validation. Unfortunately, it is in general hard to study the cross-validation error loss even in setups without dependence. Stephenson et al., (2021) in fact show that the ridge leave-one-out CV loss is not generally convex. This suggests that studying the behavior of CV when penalizing with a diagonal anisotropic can be a very complex task in a finite sample setup.

7 Simulations

To study the performance of ridge-regularized estimators, I now perform simulation exercises focused on impulse response functions (IRFs). Throughout the experiments I will consider structural impulse responses, and I assume that identification can be obtained in a recursive way (Kilian and Lütkepohl, , 2017), which is a widely used approach for structural shock identification in macroeconometrics.

I consider two setups:

-

1.

The three-variable VARMA(1,1) design of Kilian and Kim, (2011), representing a small-scale macro model. I term this setup “A”.

-

2.

A VAR(5) model in levels, using the model specification of Giannone et al., (2015) with the dataset of Hansen, 2016b consisting of variables in levels.555The dataset is supplied by the author at https://users.ssc.wisc.edu/~bhansen/progs/var.html. While the data provided by Hansen, 2016b includes releases until 2016. I do not include more recent quarterly data since this is a simulation exercise. Moreover, due to the effects of the COVID-19 global pandemic, an extended sample would likely only add data released until Q4 2019 due to overwhelming concerns of a break point. I term this setup “B”. For the ease of exposition, in the discussion I will tabulate results only for three variables – real GDP, investment and federal funds rate – but complete tables can be found in Appendix D.5.

The specification of Kilian and Kim, (2011) has already been extensively used in the literature as a benchmark to gauge the basic properties of inference methods. On the other hand, the estimation task of Giannone et al., (2015) involves more variables and a higher degree of persistence. This setting is useful to evaluate the effects of ridge shrinkage when applied to realistic macroeconomic questions. It is also a suitable test bench to compare Bayesian methods with frequentist ridge.

Estimators.

For frequentist methods, I include both and ridge estimators as well as the local projection estimator of Jordà, (2005). For Bayesian methods, I implement both the Minnesota prior approach of Bańbura et al., (2010) with stationary prior and the hierarchical prior BVAR of Giannone et al., (2015).666To estimate hierarchical prior BVARs I rely on the original MATLAB implementation provided by Giannone et al., (2015) on the authors’ website at http://faculty.wcas.northwestern.edu/gep575/GLPreplicationWeb.zip. The full list of method I consider is given in Table 1. To make methods comparable, I have extended the ridge estimators to include an intercept in the regression. A precise discussion regarding the tuning of penalties and hyperparameters of all methods can be found in Supplementary Appendix D.

| Type | Name | Description |

| Frequentist | LS | Least squares estimator |

| RIDGE | Ridge estimator, CV penalty | |

| RIDGE-GLS | GLS ridge estimator, CV penalty | |

| RIDGE-AS | Ridge estimator with asymptotic shrinkage, CV penalty | |

| LP | Local projections with Newey-West covariance estimate | |

| Bayesian | BVAR-CV | Litterman-Minnesota Bayesian VAR, CV tightness prior |

| H-BVAR | Hierarchical Bayesian VAR of Giannone et al., (2015) |

7.1 Pointwise MSE

The first two simulation designs explore the MSE performance of ridge-type estimators versus alternatives. Let be the horizon structural IRF for variable given a unit shock from variable . To compute the MSE for each , define

which is the total MSE for variable over all possible structural shocks. In simulations, I use replications to estimate the expectation. All MSEs are normalized by the mean squared error of the least squares estimator.

Setup A.

A time series of length is generated a number of times for replication. All VAR estimators are computed using lags, while LPs include regression lags. Table 2 shows relative MSEs for this design. It is important to notice that in this situation GLS ridge has remarkably low performance at horizon compared to other methods. The primary issue is that features strong correlation between components, and thus the diagonal lag-adapted structure does not shrink along the appropriate directions. This is much less prominent as the horizon increases due to the fact that impulse responses eventually decay to zero, since the underlying VARMA DGP is stationary. While there is no clear ranking, the MSE of the baseline ridge VAR estimator is in between those of the BVAR and hierarchical BVAR approaches. The degrading quality of local projection estimates are mainly due to the smaller samples available in regressions at each increasing horizon (Kilian and Kim, , 2011). This behavior is one of the prime reasons behind the development of LP shrinkage estimators, like that proposed in Plagborg-Møller, (2016) or the SLP estimator of Barnichon and Brownlees, (2019).

| Variable | Method | = 1 | = 4 | = 8 | = 12 | = 16 | = 20 | = 24 |

|---|---|---|---|---|---|---|---|---|

| RIDGE | 0.97 | 0.74 | 0.64 | 0.64 | 0.65 | 0.63 | 0.60 | |

| Investment | RIDGE-GLS | 5.16 | 0.89 | 0.55 | 0.47 | 0.44 | 0.41 | 0.38 |

| Growth | LP | 1.00 | 1.05 | 1.13 | 1.52 | 2.15 | 3.20 | 4.87 |

| BVAR-CV | 1.55 | 0.84 | 0.70 | 0.70 | 0.71 | 0.70 | 0.66 | |

| H-BVAR | 1.80 | 0.66 | 0.53 | 0.52 | 0.54 | 0.53 | 0.50 | |

| RIDGE | 0.93 | 0.78 | 0.69 | 0.68 | 0.67 | 0.64 | 0.59 | |

| Deflator | RIDGE-GLS | 2.43 | 0.83 | 0.59 | 0.52 | 0.48 | 0.44 | 0.40 |

| LP | 1.00 | 1.05 | 1.13 | 1.44 | 1.99 | 2.90 | 4.47 | |

| BVAR-CV | 1.03 | 0.89 | 0.74 | 0.73 | 0.73 | 0.70 | 0.66 | |

| H-BVAR | 1.01 | 0.70 | 0.58 | 0.56 | 0.55 | 0.53 | 0.50 | |

| RIDGE | 0.94 | 0.76 | 0.66 | 0.66 | 0.66 | 0.64 | 0.60 | |

| Paper Rate | RIDGE-GLS | 1.80 | 0.87 | 0.59 | 0.52 | 0.47 | 0.43 | 0.39 |

| LP | 1.00 | 1.05 | 1.13 | 1.46 | 1.99 | 2.86 | 4.31 | |

| BVAR-CV | 0.87 | 0.87 | 0.74 | 0.73 | 0.73 | 0.71 | 0.66 | |

| H-BVAR | 0.81 | 0.69 | 0.57 | 0.55 | 0.56 | 0.54 | 0.51 |

| Variable | Method | = 1 | = 4 | = 8 | = 12 | = 16 | = 20 | = 24 |

|---|---|---|---|---|---|---|---|---|

| RIDGE | 1.11 | 1.08 | 1.16 | 1.06 | 0.90 | 0.89 | 0.94 | |

| RIDGE-GLS | 1.16 | 1.00 | 0.99 | 1.00 | 0.93 | 0.93 | 0.95 | |

| Real GDP | LP | 1.00 | 1.14 | 1.37 | 1.52 | 1.72 | 1.98 | 2.24 |

| BVAR-CV | 0.90 | 0.87 | 1.04 | 1.01 | 0.92 | 0.92 | 0.98 | |

| H-BVAR | 0.83 | 0.62 | 0.78 | 0.73 | 0.62 | 0.62 | 0.68 | |

| RIDGE | 1.49 | 1.27 | 1.17 | 0.99 | 0.70 | 0.73 | 1.61 | |

| RIDGE-GLS | 1.34 | 1.14 | 1.02 | 1.02 | 0.86 | 0.82 | 0.86 | |

| Investment | LP | 1.00 | 1.15 | 1.40 | 1.63 | 2.03 | 2.76 | 3.59 |

| BVAR-CV | 1.51 | 1.01 | 0.97 | 0.97 | 0.93 | 1.08 | 1.24 | |

| H-BVAR | 1.06 | 0.68 | 0.69 | 0.66 | 0.63 | 0.87 | 1.14 | |

| RIDGE | 2.17 | 1.21 | 0.96 | 0.93 | 1.03 | 4.00 | 53.18 | |

| RIDGE-GLS | 1.21 | 1.04 | 0.90 | 0.93 | 0.90 | 0.88 | 0.91 | |

| Fed Funds | LP | 1.00 | 1.18 | 1.51 | 1.71 | 1.97 | 2.44 | 2.99 |

| Rate | BVAR-CV | 0.92 | 0.94 | 0.91 | 0.90 | 0.86 | 0.87 | 0.92 |

| H-BVAR | 0.75 | 0.77 | 1.32 | 1.38 | 1.25 | 1.15 | 1.20 |

Setup B.

Using the data of Hansen, 2016b , I estimate and simulate a stationary but highly persistent VAR(5) model using the same sample size and number of replications of Setup A. For all methods, lags are used, so that VAR estimators are correctly specified. In this setup, unlike in the previous experiment, one can clearly notice that impulse responses computed via cross-validated ridge show increasing MSE as horizon grows. There are two main reasons behind this behavior. First, the chosen setup features a very persistent data generating process, as the largest root of the underlying VAR model is . This means that the true IRFs revert to zero only over long horizons, while lag-adapted ridge estimates yields models with lower persistence and thus flatter impulse responses. Secondly, the dataset from Hansen, 2016b is not normalized, and the included series have markedly heterogenous variances. Since GLS ridge shrinks along covariance-rotated data, shrinkage is adjusted according to each series variance, unlike that baseline ridge estimator . The MSE for the Fed Fund Rate impulse responses shows that the pointwise difference between baseline and GLS ridge can be severe for long horizon IRFs when the DGP is highly persistent. On short horizons, Bayesian estimators perform on par or better than baseline least squares estimates, while at longer horizons differences are less stark. It is, however, clear that the hierarchical prior BVAR of Giannone et al., (2015) shows the overall best results. As in the previous setup, local projections show degrading performance at larger horizons.

7.2 Confidence Intervals

I now try and evaluate whether ridge shrinkage has a negative impact on inference. There have also been recent contributions directly aimed at studying shrinkage effects. Li et al., (2022) give an extensive treatment of the issue in terms of bias-variance trade-off, showing that, to a large extent, shrinkage is desirable unless bias is a primary and sensitive concern. Using the same simulation setups as in the previous section, I investigate coverage and size properties of pointwise CIs constructed using the methods in Table 1. All confidence intervals are constructed with nominal 90% level coverage.

In this set of simulations, I swap GLS ridge for the asymptotic shrinkage ridge estimator, , see Section 6, since the latter allows for a partially non-negligible penalization in the limit. To implement , one needs to choose a partition of which identifies asymptotically negligible coefficient. To do this, I split by lag and penalize all coefficients with lag orders greater than a given threshold , such that . In setup A, I choose , while in setup B I set . In Bayesian methods, including the cross-validated Minnesota BVAR, I construct high-probability intervals by drawing from the posterior. Comparison between frequentist CIs and Bayesian posterior densities is not generally valid, because they are not analogous concepts. Therefore, the discussion below is intended to highlight differences in structure between ridge approaches.

| Variable | Method | = 1 | = 4 | = 8 | = 12 | = 16 | = 20 | = 24 |

|---|---|---|---|---|---|---|---|---|

| LS | 0.88 | 0.88 | 0.87 | 0.88 | 0.91 | 0.93 | 0.94 | |

| RIDGE | 0.90 | 0.92 | 0.94 | 0.93 | 0.94 | 0.95 | 0.95 | |

| Investment | RIDGE-AS | 0.90 | 0.92 | 0.88 | 0.88 | 0.88 | 0.89 | 0.89 |

| Growth | LP | 0.88 | 0.97 | 0.99 | 0.99 | 0.99 | 0.99 | 0.99 |

| BVAR-CV | 0.77 | 0.88 | 0.88 | 0.90 | 0.92 | 0.94 | 0.96 | |

| H-BVAR | 0.72 | 0.89 | 0.89 | 0.92 | 0.93 | 0.95 | 0.96 | |

| LS | 0.88 | 0.87 | 0.86 | 0.88 | 0.91 | 0.92 | 0.94 | |

| RIDGE | 0.91 | 0.92 | 0.93 | 0.92 | 0.93 | 0.94 | 0.95 | |

| Deflator | RIDGE-AS | 0.91 | 0.91 | 0.88 | 0.88 | 0.87 | 0.87 | 0.88 |

| LP | 0.88 | 0.97 | 0.99 | 0.99 | 0.99 | 0.99 | 1.00 | |

| BVAR-CV | 0.80 | 0.86 | 0.88 | 0.91 | 0.93 | 0.94 | 0.96 | |

| H-BVAR | 0.84 | 0.88 | 0.90 | 0.92 | 0.94 | 0.95 | 0.97 | |

| LS | 0.87 | 0.86 | 0.86 | 0.88 | 0.90 | 0.92 | 0.94 | |

| RIDGE | 0.90 | 0.91 | 0.93 | 0.93 | 0.93 | 0.94 | 0.95 | |

| Paper Rate | RIDGE-AS | 0.89 | 0.90 | 0.89 | 0.88 | 0.88 | 0.88 | 0.88 |

| LP | 0.87 | 0.97 | 0.99 | 0.99 | 0.99 | 0.99 | 0.99 | |

| BVAR-CV | 0.82 | 0.84 | 0.87 | 0.90 | 0.92 | 0.93 | 0.95 | |

| H-BVAR | 0.88 | 0.88 | 0.90 | 0.92 | 0.93 | 0.95 | 0.96 |

| Variable | Method | = 1 | = 4 | = 8 | = 12 | = 16 | = 20 | = 24 |

|---|---|---|---|---|---|---|---|---|

| LS | 2.99 | 5.11 | 5.78 | 5.35 | 4.79 | 4.17 | 3.56 | |

| RIDGE | 3.13 | 5.20 | 5.82 | 5.17 | 4.48 | 3.78 | 3.09 | |

| Investment | RIDGE-AS | 3.11 | 5.15 | 4.84 | 4.33 | 3.70 | 3.06 | 2.48 |

| Growth | LP | 2.99 | 7.50 | 10.97 | 12.89 | 13.99 | 14.55 | 14.70 |

| BVAR-CV | 2.84 | 4.48 | 4.70 | 4.38 | 3.99 | 3.56 | 3.11 | |

| H-BVAR | 2.71 | 4.20 | 4.50 | 4.29 | 3.96 | 3.56 | 3.13 | |

| LS | 1.19 | 1.92 | 2.23 | 2.14 | 1.94 | 1.71 | 1.46 | |

| RIDGE | 1.24 | 1.97 | 2.25 | 2.09 | 1.84 | 1.54 | 1.26 | |

| Deflator | RIDGE-AS | 1.24 | 1.95 | 1.95 | 1.78 | 1.52 | 1.25 | 1.01 |

| LP | 1.19 | 3.03 | 4.56 | 5.42 | 5.90 | 6.14 | 6.21 | |

| BVAR-CV | 1.03 | 1.69 | 1.87 | 1.80 | 1.67 | 1.50 | 1.31 | |

| H-BVAR | 1.01 | 1.64 | 1.83 | 1.79 | 1.67 | 1.51 | 1.33 | |

| LS | 0.97 | 1.42 | 1.64 | 1.57 | 1.44 | 1.27 | 1.09 | |

| RIDGE | 1.01 | 1.44 | 1.65 | 1.53 | 1.36 | 1.16 | 0.95 | |

| Paper Rate | RIDGE-AS | 1.01 | 1.43 | 1.42 | 1.31 | 1.13 | 0.94 | 0.77 |

| LP | 0.97 | 2.19 | 3.28 | 3.90 | 4.26 | 4.43 | 4.48 | |

| BVAR-CV | 0.84 | 1.22 | 1.35 | 1.30 | 1.21 | 1.09 | 0.96 | |

| H-BVAR | 0.85 | 1.21 | 1.34 | 1.31 | 1.22 | 1.10 | 0.97 |

Setup A.

Simulations with the DGP of Kilian and Kim, (2011), presented in Tables 4 and 5, highlight some of the advantages of applying ridge when performing inference. Focusing on estimator , it is clear that CI coverage is in fact higher than the intervals obtained by least squares estimation in all situations. At impact, ridge CIs are larger than the LS baseline, but they shrink as horizons increase. Thus, is IRFs revert relatively quickly to zero, ridge can effectively reduce length while preserving coverage. As discussed in Section 3, these gains are inherently local to the DGP – shrinkage to zero at deep lags embodies correct prior knowledge of a weakly persistent process. For Bayesian estimators, one can note that quantile intervals at small horizons tend to be shorter compared to least squares and ridge methods.

Setup B.

The effects of ridge shrinkage on a DGP with high persistence are much more severe, as shown in Tables 6 and 7. Focusing on frequentist ridge, one can observe that close to impact () ridge has similar or even higher coverage than other methods for real GDP777This also is the case with consumption and compensation, c.f. Tables 9 and 10 in Appendix D.5. However, as the IRF horizon grows, shrinkage often leads to severe undercoverage, with asymptotic shrinkage estimator giving the worst results. In comparison, Bayesian methods are much more reliable at all horizons, although the only estimator that can consistently improve upon the benchmark least squares VAR CIs is the hierarchical prior BVAR of Giannone et al., (2015). The reason behind this is simple enough: the implementation of the Minnesota-prior BVAR I have used here has a white noise prior on all variables, which in this case is far from the truth. Indeed, Bańbura et al., (2010) implement the same BVAR by tuning the prior to a random walk for very persistent variables in their applications. In this sense the cross-validated BVAR considered – which is assumed centered at zero – is really the flip-side of ridge estimators. Therefore, the addition of a prior on the mean of the autoregressive parameters as done by Giannone et al., (2015) is a key element to perform shrinkage in high persistence setups in a way that does not systematically undermine asymptotic inference on impulse responses.

| Variable | Method | = 1 | = 4 | = 8 | = 12 | = 16 | = 20 | = 24 |

|---|---|---|---|---|---|---|---|---|

| LS | 0.87 | 0.81 | 0.75 | 0.72 | 0.71 | 0.72 | 0.73 | |

| RIDGE | 0.90 | 0.79 | 0.66 | 0.62 | 0.65 | 0.68 | 0.68 | |

| Real GDP | RIDGE-AS | 0.89 | 0.72 | 0.61 | 0.58 | 0.61 | 0.65 | 0.65 |

| LP | 0.87 | 0.93 | 0.94 | 0.94 | 0.93 | 0.93 | 0.91 | |

| BVAR-CV | 0.70 | 0.71 | 0.63 | 0.64 | 0.71 | 0.75 | 0.76 | |

| H-BVAR | 0.84 | 0.86 | 0.76 | 0.76 | 0.83 | 0.88 | 0.88 | |

| LS | 0.87 | 0.82 | 0.76 | 0.73 | 0.75 | 0.82 | 0.87 | |

| RIDGE | 0.85 | 0.79 | 0.65 | 0.62 | 0.73 | 0.80 | 0.81 | |

| Investment | RIDGE-AS | 0.82 | 0.69 | 0.59 | 0.57 | 0.68 | 0.77 | 0.77 |

| LP | 0.87 | 0.94 | 0.94 | 0.95 | 0.94 | 0.94 | 0.94 | |

| BVAR-CV | 0.70 | 0.73 | 0.67 | 0.71 | 0.77 | 0.81 | 0.83 | |

| H-BVAR | 0.80 | 0.86 | 0.81 | 0.82 | 0.87 | 0.88 | 0.88 | |

| LS | 0.85 | 0.83 | 0.80 | 0.78 | 0.77 | 0.79 | 0.80 | |

| RIDGE | 0.79 | 0.77 | 0.74 | 0.68 | 0.68 | 0.72 | 0.72 | |

| Fed Funds | RIDGE-AS | 0.78 | 0.66 | 0.68 | 0.64 | 0.64 | 0.68 | 0.69 |

| Rate | LP | 0.85 | 0.94 | 0.96 | 0.96 | 0.95 | 0.94 | 0.93 |

| BVAR-CV | 0.76 | 0.72 | 0.76 | 0.77 | 0.77 | 0.81 | 0.83 | |

| H-BVAR | 0.87 | 0.86 | 0.74 | 0.73 | 0.78 | 0.84 | 0.87 |

| Variable | Method | = 1 | = 4 | = 8 | = 12 | = 16 | = 20 | = 24 |

|---|---|---|---|---|---|---|---|---|

| LS | 0.71 | 1.56 | 2.07 | 2.31 | 2.32 | 2.24 | 2.15 | |

| RIDGE | 0.79 | 1.56 | 1.85 | 1.95 | 1.92 | 1.85 | 1.77 | |

| Real GDP | RIDGE-AS | 0.74 | 1.31 | 1.65 | 1.76 | 1.75 | 1.70 | 1.64 |

| LP | 0.71 | 2.42 | 4.21 | 5.40 | 5.90 | 5.91 | 5.70 | |

| BVAR-CV | 0.53 | 1.23 | 1.74 | 2.00 | 2.10 | 2.13 | 2.15 | |

| H-BVAR | 0.58 | 1.36 | 1.87 | 2.16 | 2.32 | 2.44 | 2.55 | |

| LS | 3.38 | 6.65 | 7.89 | 7.89 | 7.31 | 6.69 | 6.18 | |

| RIDGE | 3.79 | 6.81 | 6.93 | 6.46 | 5.79 | 5.19 | 4.73 | |

| Investment | RIDGE-AS | 3.59 | 5.57 | 6.11 | 5.77 | 5.21 | 4.72 | 4.34 |

| LP | 3.37 | 10.16 | 16.00 | 18.85 | 19.06 | 18.22 | 17.23 | |

| BVAR-CV | 2.64 | 5.26 | 6.59 | 6.91 | 6.78 | 6.57 | 6.38 | |

| H-BVAR | 2.89 | 5.74 | 7.08 | 7.54 | 7.63 | 7.60 | 7.58 | |

| LS | 0.25 | 0.39 | 0.43 | 0.43 | 0.41 | 0.38 | 0.35 | |

| RIDGE | 0.29 | 0.39 | 0.37 | 0.36 | 0.33 | 0.30 | 0.29 | |

| Fed Funds | RIDGE-AS | 0.27 | 0.31 | 0.33 | 0.32 | 0.30 | 0.28 | 0.27 |

| Rate | LP | 0.25 | 0.59 | 0.88 | 1.01 | 1.05 | 1.03 | 0.98 |

| BVAR-CV | 0.21 | 0.31 | 0.36 | 0.37 | 0.36 | 0.35 | 0.34 | |

| H-BVAR | 0.23 | 0.36 | 0.42 | 0.44 | 0.45 | 0.45 | 0.46 |

8 Conclusion

In this paper, I have studied ridge regression and its application to vector autoregressive model estimation in detail. This appears to be the first work that provides a thorough analysis of ridge penalization in the context of time series data, including geometric as well as asymptotic properties. I have also derived results on the validity of cross-validation as a method to select the penalty intensity in practice, and I have shown that CV produces asymptotically valid penalization rates. Finally, I have compared both frequentist and Bayesian ridge formulation in simulations aimed at quantifying the applicability of ridge for impulse response inference.

The key takeaway of this work is that ridge penalization is a useful approach to VAR estimation as long as the chosen penalty structure is well-adapted to the models’ structure. Bayesian ridge posteriors are especially flexible, with hierarchical priors also allowing shrinkage towards non-zero coefficient vectors. However, it is important to note that the Bayesian approach also permits the researcher to specify uninformative priors, so that the influence of the priors’ hyperparameters is less pronounced. This is not the case in frequentist ridge, c.f. including an explicit non-zero centering vector. However, prior knowledge or a pre-estimation procedure may be available to the researcher, so that ridge can be effectively implemented without the need to implement a BVAR.

To conclude, there are still avenues of research regarding ridge which would be interesting to develop. First and foremost, the high-dimensional setup, for which, however, it seems non-trivial to find a domain of applicability, as discussed in the introduction. Secondly, a more in-depth analysis of cross-validation, especially in the multivariate case, would be extremely valuable. Moreover, both the latter and former topics should be jointly addressed in the context of mild cross-sectional dimension growth, i.e. such that , which is comparable to factor model setups.

Declaration of Interest Statement.

The author reports there are no competing interests to declare.

References

- Babii et al., (2021) Babii, A., Ghysels, E., and Striaukas, J. (2021). Machine Learning Time Series Regressions With an Application to Nowcasting. Journal of Business & Economic Statistics, 40(3):1–23.

- Bańbura et al., (2010) Bańbura, M., Giannone, D., and Reichlin, L. (2010). Large Bayesian vector auto regressions. Journal of Applied Econometrics, 25(1):71–92.

- Barnichon and Brownlees, (2019) Barnichon, R. and Brownlees, C. (2019). Impulse Response Estimation by Smooth Local Projections. The Review of Economics and Statistics, 101(3):522–530.

- Bergmeir et al., (2018) Bergmeir, C., Hyndman, R. J., and Koo, B. (2018). A note on the validity of cross-validation for evaluating autoregressive time series prediction. Computational Statistics & Data Analysis, 120:70–83.

- Bhatia, (1997) Bhatia, R. (1997). Matrix Analysis. Springer, New York, NY, New York, NY, USA.

- Boubacar Mainassara and Francq, (2011) Boubacar Mainassara, Y. and Francq, C. (2011). Estimating structural VARMA models with uncorrelated but non-independent error terms. Journal of Multivariate Analysis, 102(3):496–505.

- Brüggemann et al., (2016) Brüggemann, R., Jentsch, C., and Trenkler, C. (2016). Inference in VARs with conditional heteroskedasticity of unknown form. Journal of Econometrics, 191(1):69–85.

- Burman et al., (1994) Burman, P., Chow, E., and Nolan, D. (1994). A Cross-Validatory Method for Dependent Data. Biometrika, 81(2):351–358.

- Cavaliere et al., (2022) Cavaliere, G., Gonçalves, S., and Nielsen, M. Ø. (2022). Bootstrap inference in the presence of bias. Working Paper.

- Davidson, (1994) Davidson, J. (1994). Stochastic limit theory: An introduction for econometricians. OUP Oxford.

- De Mol et al., (2008) De Mol, C., Giannone, D., and Reichlin, L. (2008). Forecasting using a large number of predictors: Is Bayesian shrinkage a valid alternative to principal components? Journal of Econometrics, 146(2):318–328.

- Dobriban and Wager, (2018) Dobriban, E. and Wager, S. (2018). High-dimensional asymptotics of prediction: Ridge regression and classification. Annals of Statistics, 46(1):247–279.

- Fu and Knight, (2000) Fu, W. and Knight, K. (2000). Asymptotics for lasso-type estimators. The Annals of Statistics, 28(5):1356–1378.

- Fuleky, (2020) Fuleky, P., editor (2020). Macroeconomic Forecasting in the Era of Big Data: Theory and Practice, volume 52 of Advanced Studies in Theoretical and Applied Econometrics. Springer International Publishing, Cham.

- Ghosh et al., (2019) Ghosh, S., Khare, K., and Michailidis, G. (2019). High-Dimensional Posterior Consistency in Bayesian Vector Autoregressive Models. Journal of the American Statistical Association, 114(526):735–748.

- Giannone et al., (2015) Giannone, D., Lenza, M., and Primiceri, G. E. (2015). Prior Selection for Vector Autoregressions. The Review of Economics and Statistics, 97(2):436–451.

- Goulet Coulombe, (2023) Goulet Coulombe, P. (2023). Time-Varying Parameters as Ridge Regressions. Working Paper.

- Goulet Coulombe et al., (2022) Goulet Coulombe, P., Leroux, M., Stevanovic, D., and Surprenant, S. (2022). How is machine learning useful for macroeconomic forecasting? J. Appl. Econ., 37(5):920–964.

- Hamilton, (1994) Hamilton, J. D. (1994). Time Series Analysis. Princeton University Press.

- (20) Hansen, B. E. (2016a). Efficient shrinkage in parametric models. Journal of Econometrics, 190(1):115–132.

- (21) Hansen, B. E. (2016b). Stein Combination Shrinkage for Vector Autoregressions. Working Paper.

- Hastie, (2020) Hastie, T. (2020). Ridge Regularization: An Essential Concept in Data Science. Technometrics, 62(4):426–433.

- Hastie et al., (2022) Hastie, T., Montanari, A., Rosset, S., and Tibshirani, R. J. (2022). Surprises in high-dimensional ridgeless least squares interpolation. The Annals of Statistics, 50(2):949–986.

- Hastie et al., (2009) Hastie, T., Tibshirani, R., Friedman, J. H., and Friedman, J. H. (2009). The Elements of Statistical Learning: Data Mining, Inference, and Prediction. Springer, second edition.

- Hoerl and Kennard, (1970) Hoerl, A. E. and Kennard, R. W. (1970). Ridge Regression: Applications to Nonorthogonal Problems. Technometrics, 12(1):69–82.

- Inoue and Kilian, (2008) Inoue, A. and Kilian, L. (2008). How Useful Is Bagging in Forecasting Economic Time Series? A Case Study of U.S. Consumer Price Inflation. Journal of the American Statistical Association, 103(482):511–522.

- Jordà, (2005) Jordà, Ò. (2005). Estimation and Inference of Impulse Responses by Local Projections. American Economic Review, 95(1):161–182.

- Kilian and Kim, (2011) Kilian, L. and Kim, Y. J. (2011). How Reliable Are Local Projection Estimators of Impulse Responses? Review of Economics and Statistics, 93(4):1460–1466.

- Kilian and Lütkepohl, (2017) Kilian, L. and Lütkepohl, H. (2017). Structural vector autoregressive analysis. Cambridge University Press.

- Li et al., (2022) Li, D., Plagborg-Møller, M., and Wolf, C. K. (2022). Local Projections vs. VARs: Lessons From Thousands of DGPs. Working Paper.

- Litterman, (1986) Litterman, R. B. (1986). Forecasting with Bayesian vector autoregressions five years of experience. Working Papers 274, Federal Reserve Bank of Minneapolis.

- Liu and Dobriban, (2020) Liu, S. and Dobriban, E. (2020). Ridge Regression: Structure, Cross-Validation, and Sketching. In International Conference on Learning Representations.

- Lütkepohl, (1990) Lütkepohl, H. (1990). Asymptotic Distributions of Impulse Response Functions and Forecast Error Variance Decompositions of Vector Autoregressive Models. The Review of Economics and Statistics, 72(1):116–125.

- Lütkepohl, (2005) Lütkepohl, H. (2005). New Introduction to Multiple Time Series Analysis. Springer.

- Medeiros et al., (2021) Medeiros, M. C., Vasconcelos, G. F. R., Veiga, Á., and Zilberman, E. (2021). Forecasting Inflation in a Data-Rich Environment: The Benefits of Machine Learning Methods. Journal of Business & Economic Statistics, 39(1):98–119.

- Mikusheva, (2007) Mikusheva, A. (2007). Uniform Inference in Autoregressive Models. Econometrica, 75(5):1411–1452.

- Mikusheva, (2012) Mikusheva, A. (2012). One-Dimensional Inference in Autoregressive Models With the Potential Presence of a Unit Root. Econometrica, 80(1):173–212.

- Park and Phillips, (1988) Park, J. Y. and Phillips, P. C. (1988). Statistical inference in regressions with integrated processes: Part 1. Econometric Theory, 4(3):468–497.

- Park and Phillips, (1989) Park, J. Y. and Phillips, P. C. (1989). Statistical inference in regressions with integrated processes: Part 2. Econometric Theory, pages 95–131.

- Patil et al., (2021) Patil, P., Wei, Y., Rinaldo, A., and Tibshirani, R. (2021). Uniform Consistency of Cross-Validation Estimators for High-Dimensional Ridge Regression. In Proceedings of The 24th International Conference on Artificial Intelligence and Statistics, pages 3178–3186. PMLR.

- Pesavento and Rossi, (2006) Pesavento, E. and Rossi, B. (2006). Small-sample confidence intervals for multivariate impulse response functions at long horizons. Journal of Applied Econometrics, 21(8):1135–1155.

- Phillips, (1988) Phillips, P. C. B. (1988). Regression Theory for Near-Integrated Time Series. Econometrica, 56(5):1021–1043.

- Plagborg-Møller, (2016) Plagborg-Møller, M. (2016). Essays in Macroeconometrics. PhD thesis, Harvard University.

- Pratt, (1961) Pratt, J. W. (1961). Length of Confidence Intervals. Journal of the American Statistical Association, 56(295):549–567.

- Rio, (2017) Rio, E. (2017). Asymptotic Theory of Weakly Dependent Random Processes, volume 80 of Probability Theory and Stochastic Modelling. Springer Berlin Heidelberg, Berlin, Heidelberg.

- Sims et al., (1990) Sims, C. A., Stock, J. H., and Watson, M. W. (1990). Inference in linear time series models with some unit roots. Econometrica: Journal of the Econometric Society, pages 113–144.

- Smeekes and Wijler, (2018) Smeekes, S. and Wijler, E. (2018). Macroeconomic forecasting using penalized regression methods. International Journal of Forecasting, 34(3):408–430.

- Stephenson et al., (2021) Stephenson, W., Frangella, Z., Udell, M., and Broderick, T. (2021). Can we globally optimize cross-validation loss? Quasiconvexity in ridge regression. In Advances in Neural Information Processing Systems, volume 34, pages 24352–24364. Curran Associates, Inc.

- Whitney, (1972) Whitney, H. (1972). Complex Analytic Varieties, volume 131. Addison-Wesley Reading.

Appendix

Appendix A Preliminaries

A.1 LS and RLS Estimators.

Lütkepohl, (2005), Chapter 3, shows that the multivariate least squares and GLS estimator of parameter vector is given by

as the minimizer of . The multivariate ridge-regularized least squares (RLS) – or, simply, ridge – estimator considered in this paper is defined to be the minimizer of the regularized problem,

The first partial derivative,

gives the normal equations . The Hessian is positive definite when , thus indeed the minimum is achieved by

Identical derivations prove that re-centering the ridge penalty at produces the estimator

A.2 Structure of the Regularization Matrix

The vectorized RLS estimator has maximal flexibility in terms of the regularization structure that matrix imposes. Since contains all the coefficients of it is indeed possible to individually penalize each lag of each series differently. In fact, by relaxing the assumption that be a diagonal matrix, even more general penalization structures are possible, although I do not consider them in this paper.

An interesting special case arises if the RLS estimator is instead written in its matrix form888 For details in the least squares case, see again Lütkepohl, (2005), Chapter 3. The derivations for the ridge estimator are identical. ,

where here it is of note that has size . The regularization structure imposed is different in general than that in : induces column-wise ridge regularization, which penalizes coefficient estimates uniformly over each of the columns of . The associated vectorized estimator then simplifies:

On the other hand, the devectorized RLS estimator is given by

that is, is simply a restructuring of the vectorized estimator into a matrix with identical dimensions to . Importantly then, is equivalent to if . Because and allow for the most generality in penalization structure, I will consider them to be the reference RLS estimators, so the dimension subscript to will be dropped unless explicitly required.

A.3 Autocovariance and Asymptotic Conditioning

The conditioning of the autocovariance is an important measure for the role that the regularization in the RLS estimator should be playing. This in turn depends on the eigenvalues of with respect to those of . Hoerl and Kennard, (1970) showed in the linear regression setting that, when the sample covariance matrix deviates significantly from the identity matrix, its small eigenvalues excessively inflate the variance of least squares estimates, even though the regression problem itself is well-posed. This fragility is inherently a byproduct of finite sampling, and partially due to numerical procedures. Nowadays, numerical precision is virtually not a concern anymore, as robust linear algebra procedures are implicitly implemented in most scientific languages and toolboxes. Yet estimation issues tied to small or unfavorable data samples remain extremely relevant from both theoretical and practical viewpoints.

In the spirit of ridge as a regularization procedure, the following Lemma establishes convergence in probability of the ordered eigenvalues of the sample autocovariance matrix.

Lemma A.1.

If where is positive definite, then

where is the largest eigenvalue of .

Proof.

First, recall that for all matrices , the determinant is clearly a continuous mapping999This follows from for permutation over . Furthermore, for any polynomial , factored as , , where the ordering of roots is arbitrary, it holds that for any there exists such that for every polynomial with decomposed as , , , see Whitney, (1972), Appendix V.4. This in particular implies that the roots of the characteristic polynomial of matrix are continuous functions of its coefficients.

Let and be the (real) characteristic polynomials of and respectively. Because of the continuity arguments above, for every there exist , such that

for . Since by assumption , the RHS of the above converges to zero as , thus . ∎

Appendix B Proofs

B.1 Shrinkage

Proof of Proposition 2

Proof.

Notice that, by introducing , any lag-adapted regularization matrix can be written as , so that

by the properties of Kronecker product. It is now possible to derive the statements of the proposition as follows:

-

(a)

The result regarding isotropic regularizer is trivial given Proposition 1.

-

(b)

Without loss of generality due to the ordering of lags in , one may write the Gram matrix in a block fashion,

where is the sub-matrix containing all the components not indexed by subset , and the subscript has been dropped from for ease of notation.

Define , and . The matrix block-inversion formula yieldsIf and , then , . Therefore , since for sufficiently large and thus the Sherman-Morrison-Woodbury formula implies

The above results finally yield

as required.

∎

B.2 Ridge Asymptotic Theory

Proof of Theorem 1

Proof.

-

(a)

Assumptions A-B imply directly that is a consistent estimator for : in particular, is a stationary, stable and ergodic VAR process.

-

(b)

Rewriting yields

I study the last two terms of the last equality separately. The first term is ,

since . Considering the matrix sequence

which under Assumptions B and D.(ii) converges in probability to , by the continuous mapping theorem (Davidson, , 1994) the second term gives

under Assumption A.

-

(c)

The residuals can be written as

Thus

(9) From (a) one finds that , so , while and : the terms involving these quantities then vanish asymptotically. Lastly, the first term of the sum gives

for under Assumptions A and B.

-

(d)

With the same expansion used in (b),

where . Following the arguments above, the first term in the sum converges in probability,

The second term has normal limiting distribution,

see Lütkepohl, (2005), Proposition 3.1. By Slutky’s theorem claim (d) follows.

∎

Proof of Theorem 2

Proof.

-

(1)

Since condition (i) implies that , results (a)-(c) are unchanged, while (d) now involves the limit

yielding (d′).

-

(2)

Assuming simplifies the terms in the proof of Theorem 1 since now . The weaker rate imposed on does not influence results (a)-(c). Moreover,

so that (d′) follows.

∎

Proof of Theorem 3

Proof.

I make a straightforward adaptation of the proof found in Hamilton, (1994), Proposition 11.2. Define , which is expanded to

Contrary to the least squares estimator, cross-terms do not cancel out since for the residuals are not in the orthogonal space of . From the consistency results of Theorem 1,

and

Further,

since again is asymptotically normal, and . The same holds for the remaining transpose term, too.

It is thus proven that , meaning so that the two terms may be exchanged in computing the joint asymptotic distribution. Theorem 1 accordingly yields

where and . As in Hamilton, (1994), Proof of Proposition 11.2, is a martingale difference sequence, thus the claim

as follows. When the strengthened assumptions (1) or (2) of Theorem 2 are used instead, the non-zero limiting mean vanishes

proving that the joint asymptotic distribution is mean-zero Gaussian.

Finally, to compute the explicit expression of the asymptotic variance , one must take care and note that is not assumed to be normally distributed, contrary to the remainder of the proof in Hamilton, (1994), pp. 342-343. A correct expression for i.i.d. non-Gaussian can be found in Remark 2.1, Brüggemann et al., (2016), yielding

where . ∎

Proof of Theorem 6

Proof.

The stated results reduce to studying the behavior of two components used in the proof of Theorem 1 and Theorem 2, under the additional simplification of .

-

(a)

Identical to result (a) in Theorem 1.

-

(b)

Consistency follows immediately by the fact that .

-

(c)

Follows from (c), Theorem 1 and (b) above.

-

(d)

The bias term in the expression of is driven by

meaning there is no asymptotic bias. On the other hand,

Setting yields the claim since there are no further simplifications in the asymptotic variance formula, cf. proof of (d), Theorem 1.

∎

Appendix C Cross-validation

Later in this section, the following lemma will be useful.

Lemma 1.

Let a stationary and stable mean-zero AR() process with companion form matrix . Then, the associated MA() coefficients, , decay exponentially for sufficiently large, that is,

for some constant .

Proof.

Recall from e.g. Lütkepohl, (2005) that if is the companion matrix of the AR() model, then , where . Note that by construction and that the spectral radius of is less than one under the assumption of stability. Let be the Jordan canonical form of the companion matrix and the dominant eigenvalue. Under the assumption of stability . Now observe that, supposing has diagonal blocks, for

where is the dominant Jordan block, while are the non-dominant blocks. Then, letting , one gets

for some constant , as for one can see that . Since for complex it holds , letting the proof is complete. ∎

C.1 Two-fold CV

Proof of Theorem 4

Proof.

Write as

By a strong LLN for weakly dependent processes (see, for example, Rio, 2017), it holds that , and . Since, by a similar decomposition, it holds that

where is positive definite, almost sure convergence is proven.

To prove uniform convergence over compact subsets, I follow the proof of Patil et al., (2021), Theorem 4.1, which relies on verifying the conditions of the Arzelà-Ascoli theorem. That is, one must prove that function as well as its first derivatives are bounded over compact sets. As the Arzelà-Ascoli theorem readily generalizes to Euclidean spaces of arbitrary (fixed) dimension, I will directly consider the matrix derivative when checking boundedness.

Assume that , where is a compact set of positive semidefinite penalization matrices such that and . Note where . Using this decomposition, one gets first

where the last line follows from applying Weil’s eigenvalue inequalities (Bhatia, , 1997) to and the fact that by a strong LLN, so that there exists a constant bounding for large enough.

Additionally, the matrix derivative of with respect to is

so that, by using similar argument as the one used above, one gets

The almost sure bound in the last display is also clearly finite for any , as required.

One can easily bound and its first derivative as , with only addition of an extra term depending on . This means that forms an equicontinuous family of functions with respect to over any . Therefore, Arzelà-Ascoli yields uniform convergence of a subsequence, and since the difference converges to zero pointwise, too, the entire sequence converges uniformly. ∎

C.2 Cross-validation under Dependence

The result of Theorem 4 may be only partially informative in practice, as it does not give information on how dependence, in terms of the buffer block of size , impacts . Indeed, due to averaging, the effects of time dependence between the estimation and evaluation folds are washed out in the limit even when is fixed. Therefore, Theorem 4 is not useful in finite samples, where one would preferably set to be as small as possible.

To address dependence, in the same setup as above, consider an alternative predictive error measure, the -dependence prediction error,

and the associated error curve, . The empirical counterpart to this quantity is given by for . The next theorem shows that in the case of a purely autoregressive data generating process, the error one commits by choosing a finite buffer size is exponentially small.

Theorem 7.

Under Assumptions A-C, for every in the cone of diagonal positive definite penalty matrices with diagonal entries in , it holds that

where is a constant that does not depend on .

Proof.

In line with the definition of , I set , and . With the same approach as in the proof of Theorem 4, here one finds

where I have removed the subscript from expectation to make notation clearer. Since is independent of , the cross term reduces to zero, while . Thus, it is the first term in the last display that is effected by dependence.

To see this, let for be the th entry of . Then, using the MA() decomposition of , i.e. , one can write

Note that is independent of , and is belongs with the -algebra generated by and . Therefore,

as .

Now, I prove that and at an exponential rate. First, let

and observe that

since , lag order is fixed and the maximal entry of decays exponentially for sufficiently large following Lemma 1. Secondly, much in the same vein

The proof concludes by setting . ∎

Remark 4.

Theorem 7 is reassuring because it suggests that, in practice, if the AR() model is correctly specified, one may keep small and still get a valid prediction error estimate in sense of Theorem 4. In simulations, I set , which is a common simplification to more effectively exploit the entire sample and does not, as discussed above, effect consistency (Bergmeir et al., , 2018). Moreover, note that Theorem 7 intuitively gives a worst-case rate: the dependence of between and data in the estimation set gets milder, on average, as grows. Thus, if CV aspect ratio is balanced, dependence only plays a negligible role.

C.3 Asymptotically Valid CV

Proof of Theorem 5

Proof.

First, recall that

It also holds . Now, notice that

since . It follows

One can now consider a sequence of regularizers in . By taking the limit, one gets that

meaning that can not be optimal asymptotically, since the least squares solution at achieves a lower predictive error. Additionally, any sequence with lower convergence order is also asymptotically invalid. Therefore, by contradiction, it must hold that . ∎

Proof of Corollary 2

Proof.

The first results follows directly from Theorem 5. Further, the fact that is trivial because it is assumed that .

To prove the second part of the theorem, one can simply notice that, given the assumption on the coefficients in Theorem 6,

where was partitioned into two diagonal blocks, and , as done previously. Block must be following the proof of Theorem 5. Finally, the fact that as means that, in the limit, a nonzero does not yield a sub-optimal cross-validation loss value. ∎

Appendix D Monte Carlo Simulations

D.1 Cross-validation Details

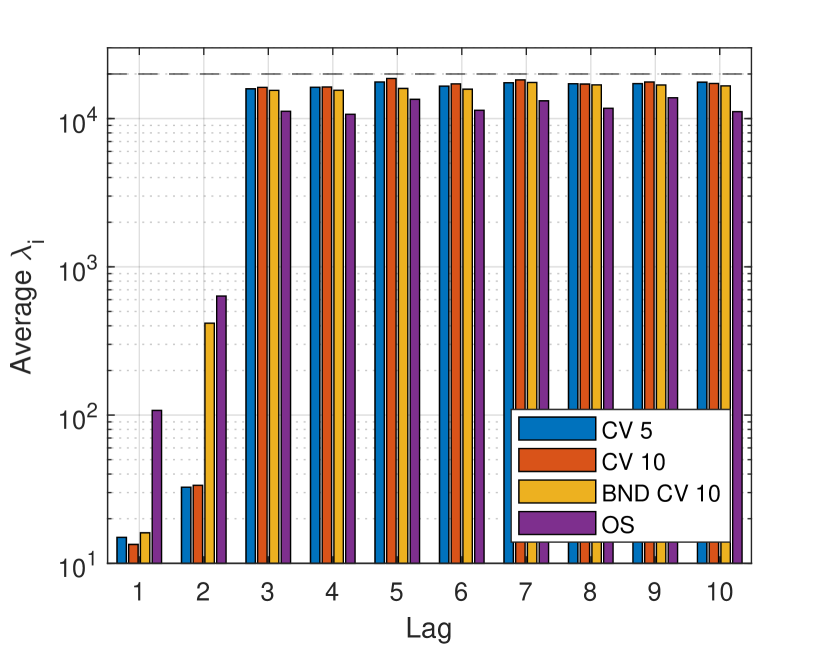

To select the ridge penalty, I implement the lag-adapted structure and choose the relevant ’s using block non-dependent cross-validation, c.f. Burman et al., (1994), Bergmeir et al., (2018). I constraint the optimization domain of to be , without discretization. An issue with cross-validation regards the GLS ridge estimator: the matrices involved can quickly become prohibitively large due to Kronecker products, making CV optimization impractical. To avoid this, I set the penalty for lag-adapted to be the same as that obtained for via CV, which means the regularizer is tuned sub-optimally. Nonetheless, an identical choice of for both methods can help shed light on the difference in structure between the two estimators.

In contrast to Bańbura et al., (2010), I do not tune the shrinkage parameter of the Minnesota BVAR using a mean squared forecasting error (MSFE) criterion: instead, I again use block CV. Since a Minnesota prior can be easily implemented with the use of augmented regression matrices, cross-validation can be much more efficiently implemented than for . The resulting choice of prior tightness is reasonable because CV, too, estimates the (one step ahead) forecasting risk. Since in this context only the mean of the posterior is used to compute pointwise impulse responses, one can even directly interpret the cross-validated Minnesota BVAR estimator as a refinement of GLS ridge.

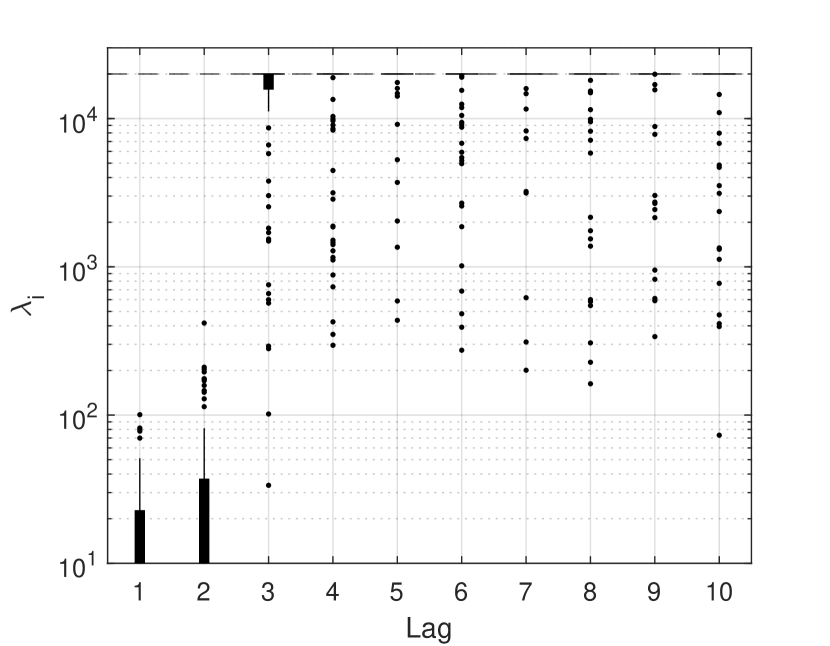

D.2 Penalty Selection in Simulations

In the simulations of Section 7, an interesting aspect to study is how data-driven penalty selection methods behave. Both average and individual behavior are important, because the former generally gives intuition for the kind of regularization structure that is selected for the model, while the latter is relevant for empirical modeling where estimation can be done only on one sample.