Marginal Treatment Effects with a Misclassified Treatment

Abstract.

This paper studies identification of the marginal treatment effect (MTE) when a binary treatment variable is misclassified. We show under standard assumptions that the MTE is identified as the derivative of the conditional expectation of the observed outcome given the true propensity score, which is partially identified. We characterize the identified set for this propensity score, and then for the MTE. We show under some mild regularity conditions that the sign of the MTE is locally identified. We use our MTE bounds to derive bounds on other commonly used parameters in the literature. We show that our bounds are tighter than the existing bounds for the local average treatment effect. We illustrate the practical relevance of our derived bounds through some numerical and empirical results.

Keywords: Heterogeneous treatment effects, misclassification, instrumental variable, set identification.

JEL subject classification: C14, C31, C35, C36.

1. Introduction

The existence of measurement error in a treatment variable makes the identification of many parameters used in the causal inference literature challenging. When the treatment variable is binary, it is well-understood in the literature that the measurement error is nonclassical, that is, it depends on the true treatment. Even in the homogeneous treatment effect framework, measurement errors in a binary regressor can result in severe identification deterioration of regression coefficients (Kreider, 2010). Ura (2018) appears to be the first to investigate the identifying power of an instrumental variable (IV) in the (unobserved) heterogeneous treatment effect model when the treatment is endogenous and mismeasured. He derives bounds on the local average treatment effect (LATE) when a binary instrument is available.111Mahajan (2006) and Lewbel (2007) allow for heterogeneous treatment effect through observed covariates. Calvi, Lewbel, and Tommasi (2022) propose a new estimand for the LATE, called the measurement robust LATE (MR-LATE), and obtain point-identification in an alternative framework. Yanagi (2019) shows that with the help of exogenous covariates, point-identification of the LATE can be obtained under some conditions when there is misclassification in the treatment. Tommasi and Zhang (2020) extend the results in Ura (2018), and Calvi, Lewbel, and Tommasi (2022) to the case with multivalued discrete instruments.

This paper investigates the identification of the MTE in settings where a binary treatment variable is misclassified, and a valid instrument is available. We show under standard assumptions that the MTE is identified as the derivative of the conditional expectation of the observed outcome given the true propensity score, which is partially identified. We provide a tractable characterization (which is an outer set) of the identified set for this propensity score, and then for the MTE. We show under some mild regularity conditions that the sign of the MTE is locally identified. We also derive functional sharp bounds for this propensity score when the misclassification is non-differential. We use our MTE bounds to derive bounds on other commonly used parameters in the literature. In particular, we show that our bounds for the LATE are tighter than the existing Ura’s (2018) and Tommasi and Zhang’s (2020) bounds when the instrument is discrete. We illustrate the practical relevance of our derived bounds through some numerical and empirical results. More precisely, we apply our methodology on data from the third wave of the Indonesia Family Life Survey to measure marginal returns to upper secondary or higher schooling while allowing for the possibility that education be mismeasured. We find that the return is heterogeneous and weakly decreases with the unobserved schooling cost.

Several papers have extensively studied issues related to misclassification in treatment variables. See, for example, Aigner (1973), Bollinger (1996), Hausman, Abrevaya, and Scott-Morton (1998), Molinari (2008), Hu (2008), Hu and Schennach (2008), etc. Recently, Mahajan (2006) uses an additional instrument, which he called “instrument-like variable,” to nonparametrically identify the regression function in models with a misclassified binary regressor. Considering the same model as Mahajan (2006) under different assumptions, Lewbel (2007) also uses a “second” instrument to nonparametrically identify the average treatment effect (ATE) when the treatment is misclassified. However, their results hold when the true treatment is exogenous. DiTraglia and Garcia-Jimeno (2019) show that the identification result in Mahajan (2006) does not extend to the case of an endogenous treatment. In that context, they derive bounds on the average treatment effect under standard assumptions. Nguimkeu, Denteh, and Tchernis (2019) study a homogenous treatment effect linear regression model in which a binary regressor is potentially misclassified and endogenous. They use exclusion restrictions for both the participation equation and measurement error equation to identify the regression coefficient with endogenous participation and one-sided endogenous misreporting. Millimet (2011) studies the performance of several commonly used estimators in the causal inference literature when there is measurement error in a binary treatment, and warns researchers about the consequences of ignoring the presence of measurement errors. Kreider et al. (2012) partially identify the average effects of food stamps on health outcomes of children when participation is endogenous and misreported by using relatively weak nonparametric assumptions and information from auxiliary data. Our paper studies potential heterogeneity in the treatment effect through the marginal treatment effect when the treatment is endogenous and mismeasured. A more related work to ours is Ura (2020), who investigates heterogeneous treatment effects in the presence of a misclassified endogenous binary treatment variable through the instrumental variable quantile regression model.

Our paper also complements the work of Battistin and Sianesi (2011) and Battistin, De Nadai, and Sianesi (2014), who investigate the identification of average returns to education in the United Kingdom when attainment is potentially measured with error. While these authors focus on average returns, we investigate marginal returns, which may reveal (unobserved) heterogeneity in the treatment effects that would otherwise be hidden when looking at only average effects. Our work is also related to Chalak’s (2017) who discusses the interpretation of various estimands (Wald, local IV) when the instrument is mismeasured, but the treatment variable is correctly measured. Differently from his framework, the instrument is observed with no error, while the treatment variable is potentially misreported. Recently, Jiang and Ding (2020) study identification in the binary IV model when allowing for simultaneous measurement errors in the instrument, treatment and/or outcome. They derive sharp bounds on the LATE assuming non-differential measurement errors and a valid IV. Our framework encompasses multivalued discrete/continuous outcomes and instruments, while the treatment variable is maintained binary. But, we only allow for misclassification in the treatment variable. Using a framework similar to ours, Possebom (2021) derives complementary identification results for the MTE, allowing for dependence between the instrument and the misclassification variable. While we focus on the case where the instrument is completely randomly assigned, we show in Appendix G how our approach can be extended to the situation where there is dependence between the instrument and the misclassification variable. This extension is similar to Ura’s (2018) in the LATE framework. Note that Kasahara and Shimotsu (2021) study identification in regression models when an endogenous binary regressor is misclassified, allowing for correlation between the instrument and the misclassification error. They show identification of the regression coefficient when a “special” covariate in the outcome equation is excluded from the misclassification probability. While they allow for heterogeneity in the average effect through observed covariates, we focus on unobserved heterogeneity using marginal treatment effects.

The remainder of the paper is organized as follows. Section 2 introduces the model and discusses the assumptions. Section 3 presents the main identification results, Section 4 discusses how information about the false positive/negative misclassification rates can be helpful for our identification approach. Section 5 illustrates the empirical relevance of the MTE bounds, Section 6 presents some extensions, Section 7 provides a real world empirical example, and Section 8 concludes. Proofs of the main results are relegated to the appendix.

2. Analytical Framework

Consider the following model:222We show in Lemma 3 in Appendix A that the specification is without loss of generality. Existing papers such as Ura (2018), Calvi, Lewbel, and Tommasi (2022), Tommasi and Zhang (2020), among others have considered the following specification . We show that the binary nature of and imposes that (see Lemma 3). This restriction brings some extra information that helps in our identification strategy.

| (2.6) |

where the vector represents the observed data, while the vector is latent. In this model, is the observed outcome, is the unobserved true treatment variable, while is the observed mismeasured treatment, is an indicator for misreporting, and are the potential outcomes that would have been observed if the true treatment had been externally set to 0 and 1, respectively. The variable is an instrument, and is a nontrivial/nonconstant function. In this paper, we are interested in identifying the marginal treatment effect defined as

Example 1 (Marginal returns to schooling (leading example)).

In this example, we assume that the researcher is interested in measuring marginal returns to college education. It is well-documented that education is usually mismeasured. For example, Black, Sanders, and Taylor (2003) find that more than a third of respondents to the U.S. Census claiming to hold a professional degree have no such degree. In this case, the variable is earnings/wage, and is the indicator for college degree. The variable could be distance to college. The latent variable could be interpreted as an index for the cost of going to college (which includes the financial cost, the opportunity cost, the psychological cost, etc.), while is the potential earnings for someone with a college degree, and is the potential earnings for someone without a college degree. The variable is the individual’s true indicator for college degree.

Example 2 (Marginal effects of masks).

The variable could be the indicator that an individual tests positive to Covid-19, the indicator that the individual actually wears masks, the indicator that the individual reports wearing masks, the disutility/discomfort (cost) of wearing masks, and could be a shifter for the benefit of wearing masks (number of children).333Children are less likely to get the virus, and therefore less likely to contaminate others. Hence, the variable number of children in the households is likely to satisfy the exclusion restriction assumption. We may add the number of adults in the households as a control variable to the model. However, the validity of number of children as instrument remains questionable, as is the distance to college instrument in Example 1. People could report wearing masks while they actually do not (for example, because of social pressure). They could also pretend to wear mask while they do not wear it properly. On the other hand, someone could report not wearing regularly a mask (because of political reasons for example), while she actually does (because of her underlying health conditions). These facts could lead to misclassification in the report of mask wearing, and therefore induce some bias in the measurement of the marginal effects of mask wearing on the positivity rate. could be the indicator that the individual tests positive to Covid-19 while she is wearing masks, and could be the indicator that the individual tests positive to Covid-19 while she is not wearing masks. The effect of wearing masks on the positivity rate could be heterogeneous. Healthy individuals tend to think that they are immune or they will survive if they are infected. For them, the disutility of wearing masks may be higher, and they may be less likely to wear masks. We are interested in measuring the effect of wearing masks on the positivity rate for different levels of the disutility, i.e., .

We will use the following assumptions for identification:

Assumption 1 (Random assignment).

The instrument is independent of , i.e., , for each .

Assumption 1 requires that be a valid instrument, in the sense that it is statistically independent of all the unobservables in the model. This is a commonly used assumption in the literature. Note that the model (2.6) implicitly assumes that exclusion restriction holds, i.e., for all and . For this reason, we do not state this assumption explicitly. Assumption 1 requires more than the standard random assignment assumption when there is no misclassification (i.e., a.s.), which states that is statistically independent of for each treatment arm . Assumption 1 extends the standard random assignment assumption to include the misclassification variable . Strictly speaking, we should have called this assumption “extended random assignment.” We are abusing notation by simply calling it random assignment. As discussed in Possebom (2021), the independence between the instrument and the misclassification variable could be too restrictive in practice. We discuss how this assumption can be relaxed in Appendix G. Note however that this assumption has been considered in existing work such as Ura (2018), Calvi, Lewbel, and Tommasi (2022), Tommasi and Zhang (2020), etc.

In our framework, the measurement error is nonclassical by definition of the model. Indeed, we can rewrite . So, the measurement error is dependent on the true unobserved treatment . This fact is well-documented and understood in the literature. See Aigner (1973), Mahajan (2006), Lewbel (2007), Kreider et al. (2012), Ura (2018), Yanagi (2019), etc.

Assumption 2 (Absolute continuity of ).

The latent variable is absolutely continuous. Without loss of generality, the unconditional distribution of is uniform over , and the support of the function is included in .

This assumption is standard in the literature and has been considered in Heckman and Vytlacil (1999, 2001, 2005), Carneiro and Lee (2009), Carneiro, Heckman, and Vytlacil (2010, 2011), etc. It does not require that the conditional density of given exists, as will be apparent in the different specifications we consider in the appendix. This assumption implies the following:

| (2.7) |

where denotes the conditional distribution of given .

Assumption 3 (Continuous instrument).

The instrument is continuous such that the support of the random variable is an interval.

Assumption 3 is also standard in the literature and is crucial for our identification methodology for the MTE. In Section 6, we show how our methodology can be used to identify multiple LATEs when the instrument is discrete. Identification results for the MTE with discrete instruments have been developed in Acerenza (2021), which built on insights from the current paper and Mogstad, Santos, and Torgovitsky (2018).

Assumption 4 (Upper bound on misclassification rate).

The (unconditional) misclassification rate has a known upper bound , that is, .

A similar assumption to Assumption 4 has been considered in Horowitz and Manski (1995), Kreider and Pepper (2007), Molinari (2008), Kreider et al. (2012), etc. In this assumption, we only impose an upper bound on the extent of the misclassification, as we allow for the treatment to be correctly classified. One can alternatively place a lower bound on the misclassification probability too. For example, one can combine information from different sources (e.g., government, universities, etc.) to bound the extent of the misclassification from below as well as from above. For instance, universities can provide information on the number of individuals who actually have a college degree. This information can help identify . One can then use the absolute difference between and as , a lower bound for the misclassification rate.444Indeed, we have , which implies . Therefore, , since . Hence, we can set . We can also use this information to provide a value for .555We have . If , and , then we can set . In the context of example 1, we can set (following Black, Sanders, and Taylor (2003)), and (assuming someone with a degree is unlikely to misreport). The case corresponds to the scenario where the researcher is agnostic about the range of the misclassification rate. All our derived results still hold in this case.

3. Identification Results

3.1. Identification of the MTE

We have

| (3.1) | |||||

where the first equality holds from the definition of the model, the second holds from Assumption 1, and the third equality holds from Assumption 2. Under Assumption 3, we can differentiate each side of the equation with respect to . Hence, we obtain

Below, we summarize this result in Lemma 1.

Lemma 1.

The result in Lemma 1 shows that the marginal treatment still has the local instrumental variable (LIV) interpretation as in Heckman and Vytlacil (1999, 2001, 2005), except that the true propensity score is now set-identified, because of the presence of misclassification. The intuition is that the conditional expectation can be decomposed between the treatment and control groups as usual, even if these groups are unobserved due to the presence of misclassification. The above result holds whether there is misclassification or not, since the model assumes that misreporting does not have a direct effect on the outcome variable. Now, the fact that the treatment and control groups are observed with some noise leaves the propensity score partially identified.

3.2. Identification of

For any Borel set , we have

| (3.2) | |||||

where the first equality holds from the law of total probability, and the second equality follows from the definition of the model and Assumption 1. In the special case where , we have

| (3.3) |

When there is no misclassification in the treatment, i.e., a.s., then is identified as the propensity score , since the distribution of is normalized to be uniform over . When the treatment is completely misclassified, i.e., a.s., is identified under the previous normalization as . We can rewrite the last equality as follows:

| (3.4) |

We have . Thus, is the true (unidentified) propensity score. We show that the propensity score is partially identified using Equations (2.7) and (3.4). Equation (3.4) implies

For now, we assume , since the cases where can be dealt with separately. Combining this with Equation (2.7), and solving for and in the system of equations, we obtain:

Therefore, the above functions need to satisfy all required conditions for a cumulative distribution on : monotonicity, right-continuity, , and . In general, it will be difficult to nonparametrically characterize the sharp identification region for the propensity score function using those conditions. We are going to focus on the monotonicity condition and the fact that the probabilities and lie between 0 and 1. For any and such that , we have:

which implies

This latter inequalities respectively imply

In the special case where , we have

Using the condition that , we identify . Therefore, the above constraints on become

Similar argument holds for the special case where , but this yields the above same constraints on . Hence, the following proposition holds.

Proposition 1.

In Appendix B, we provide two different specifications for the relationship between the decision to misreport and the unobserved heterogeneity that achieve the above bounds on . However, these bounds are not necessarily functionally sharp in the language of Mourifié, Henry, and Méango (2020), as taking the difference of the bounds for and will not necessarily yield the tightest bounds for the difference . We show this in Subsection 3.3 below. Intuitively, note that the pointwise bounds on in Proposition 1 are derived using only information from the first stage equation. We are going to use information from the second stage equation to tighten the bounds on .

Remark 1.

The bounds in Proposition 1 are non-informative if . Indeed, if , then the lower bound on is 0, and if , then the upper bound on is 1. Also, note that the bounds on are monotonic in : bigger values of yield wider bounds, while smaller values of lead to narrower bounds.

For the rest of the paper, we derive our results for each value of . As in Proposition 1, one can take the infimum of the lower bound on the parameter of interest over the range , and similarly the supremum of the upper bound over .

3.3. Analytical bounds for the MTE

In this subsection, we provide analytical bounds on the MTE. Define and . Inequalities (3.2) and (3.2) imply the following bounds on the when .

These above bounds on the difference can be tightened using Equations (3.10) and (3.11) below. Notice that the model implies the following index sufficiency result:

| (3.9) |

Indeed, similar to Equation (3.2), the following holds under Assumption 1:

From Equation (3.2), we can show under Assumptions 1 and 2 that

| (3.10) | |||||

A similar result holds for the observed control group:

| (3.11) | |||||

The above derived equalities allow us to characterize the functional identified set for .

Definition 1.

This characterization of the identified set for is broad, but less tractable. We are going to derive analytical expressions for the MTE bounds based on the previous results.

The density versions of Equations (3.10) and (3.11) hold. We first consider Equation (3.10). For two values and of the instrument , we have

where is the conditional density of given that is absolutely continuous with respect to a known dominating measure . Using the triangle inequality, we have

Therefore, by integrating each side of the last inequality over the support , and using the Fubini-Tonelli theorem, we have

Hence, we have , where

Using a similar argument on Equation (3.11)), we have . Therefore, we obtain the following bounds on the difference :

We can show that .666To show this, use the fact that for any -integrable function , , and . Consequently, we have

| (3.12) |

These above bounds on are tighter than the ones one would get by taking the difference of the pointwise bounds derived previously in Proposition 1.

Define

Suppose and . Then, the following holds.

Hence, we have

Therefore, we can take the limit of each side when goes to . Suppose that , , and exist.777Then, we have . When the first two limits do not exist, we replace them by and in the lower and upper bounds of (3.14). Then, using the fact that the functions and are continuous, and assuming that is continuous in , we obtain

| (3.14) | |||

These bounds may not be sharp, but they provide a tractable outer set of the identified set for . In practice, we may set to be equal to the midpoint of its bounds derived in the previous subsection. We summarize the results in the following proposition.

Proposition 2.

The proof on Proposition 2 is shown in Appendix C. This proposition shows that when there is no misclassification (), our bounds collapse to a point, which is the standard MTE estimand as a limit of a generalized LATE. When , the sign of the is locally identified for each value . Equation (3.16) shows that our derived bounds are not changing with . In particular, the bounds in Equation (3.16) remain valid even when the researcher is agnostic about the misclassification probability (). The numerical example below illustrates how informative the bounds can be in practice, depending on the underlying structure in the data generating process.

Numerical illustration

We consider the following data generating process (DGP)

| (3.24) |

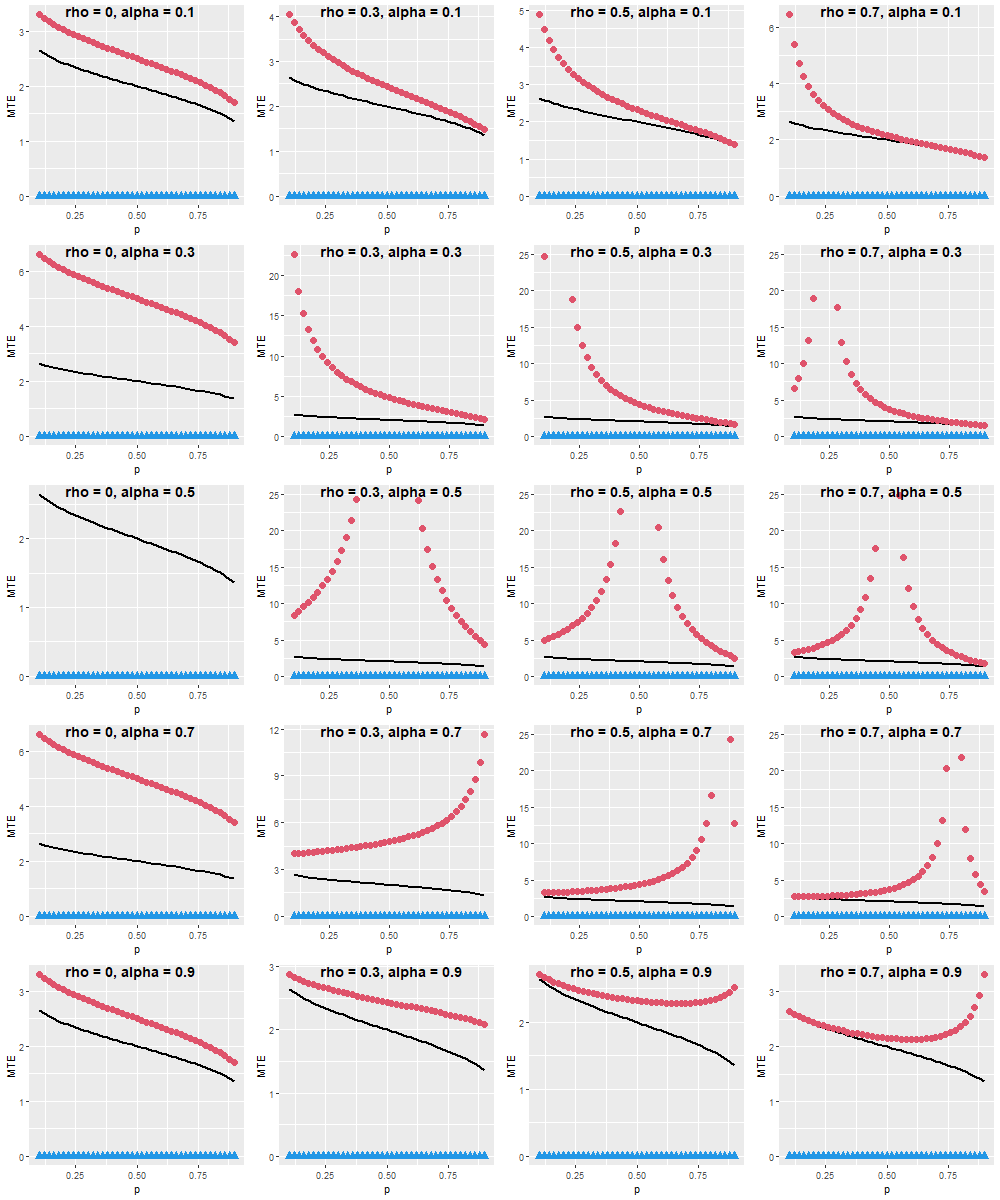

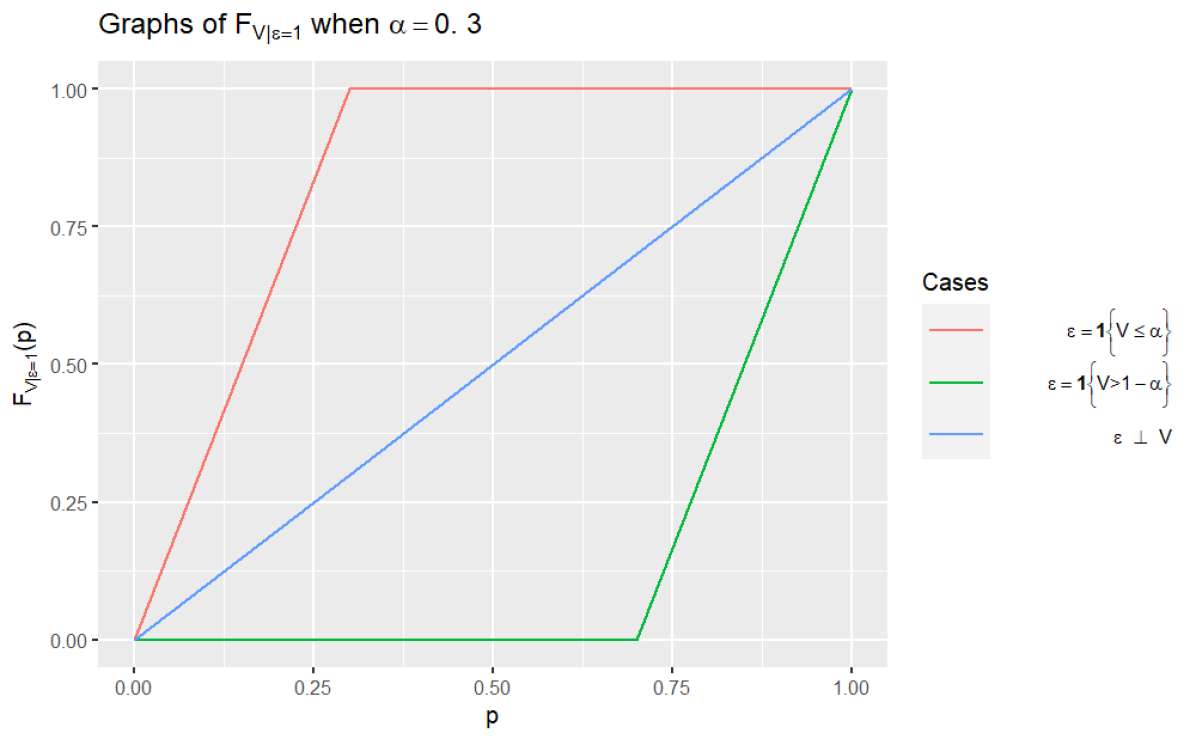

where , , , with , and . Details on the DGP are provided in Subsection I.1 in the appendix. As we can see on Figure 1, the upper bound becomes closer to the true MTE as the misclassification rate approaches 0 or 1. The MTE is positive for all values of in this example, and our bounds identify this sign. In some cases, our derived bounds appear tight and informative. The coefficient captures the degree of dependence between the unobserved heterogeneity and the indicator for misreporting . It is unclear how this dependence parameter affects the bounds.

* The black line represents the true MTE from the model.

* The red circles (blue triangles) are the approximated upper (lower) bound at each grid point of .

Figure 8 in Appendix I.1 displays the MTE bounds, the local IV estimand and the true MTE curve for and different values of . In most cases, we see that the standard LIV estimand does not lie within our derived bounds. Therefore, ignoring the presence of measurement errors in the treatment variable may result in an important bias in the MTE function. Our proposed bounds always cover the true MTE function, when our identifying assumptions holds.

3.4. Sharp characterization under non-differential misclassification assumption

In this subsection, we are going to characterize the (sharp) identified set for the MTE. We add the non-differential measurement error assumption to the set of our identifying assumptions.

Assumption 5 (Non-differential misclassification).

The misclassification variable is independent of conditional on , i.e., , for each .

This assumption states that conditional on the unobserved heterogeneity that drives the selection into treatment, misreporting is independent of the potential outcomes. Combined with Assumption 1, it implies that misreporting is independent of the outcome conditional on the true treatment. This assumption could be too restrictive, as there may exist some returns to misreporting. In our leading example, there could exist some “returns to lying” about college completion, as discussed in Hu and Lewbel (2012), and DiTraglia and Garcia-Jimeno (2019).

For the sake of simplicity, we assume in this subsection that the distribution of given is absolutely continuous. We have

| (3.25) | |||||

where the first equality follows from the results derived in the previous subsection, and the second equality holds from the law of iterated expectations. Therefore, by taking the derivatives of both sides of this equality with respect to , we obtain the following:

| (3.26) | |||||

where the second equality holds under Assumption 5. Similarly, we can show that

| (3.27) | |||||

Applying equality (3.26) to the special case where , and using the fact that (since ), we have

Therefore,

Hence, the function must satisfy the following conditions:

| (3.28) | |||

| (3.29) | |||

| (3.30) | |||

| (3.31) | |||

| (3.32) | |||

| (3.33) | |||

| (3.34) |

| (3.35) | |||

| (3.36) |

for all such that , all , and all Borel set , where , and . The constraints (3.32) and (3.33) come from the fact that and are probabilities. In fact, using equalities (3.26) and (3.27) we can solve for and as follows:

Equations (3.34) and (3.35) are like terminal conditions, and come from Equation (3.25). Note that conditions (3.30) and (3.31) are equivalent, and come from the fact that density functions integrate to 1, while Equations (3.28) and (3.29) are the non-negativity conditions for density functions. The following proposition holds.

Proposition 3.

The proof of Proposition 3 is given in Appendix E. Although this proposition provides sharp identification region for the propensity score and the MTE, this identified set is not tractable. It is important to point out that the identified set for the MTE in the proposition is uniformly sharp in the sense that the joint distribution on that achieves each element in this latter is the same across .

4. How can knowledge about false positive/negative rates help?

4.1. When false positive/negative misclassification probabilities do not depend on the instrument

Equation (3.3) implies

where the second equality holds from Assumption 2, is the false negative misclassification rate, and is the false positive misclassification rate. Suppose that .888This constraint is known as the monotonicity condition is the literature on misclassification, and is different from the monotonicity restriction imposed on the treatment selection in model (2.6). Then,

The misclassification rate functions and can be partially identified using the conditions that they lie within the interval , and that . We are going to follow the literature (Hausman, Abrevaya, and Scott-Morton, 1998) to first assume that the misclassification rates and are constant across .999Note however that in a recent paper, Haider and Stephens Jr. (2020) show that this assumption is invalid in routine empirical settings. In Subsection 4.2, we discuss how one can allow the false positive/negative rates to depend on . The true propensity score is therefore identified up to the misclassification probabilities and as follows:

The following lemma holds.

Lemma 2.

Suppose Assumption 1 holds. Then, false positive rate and false negative rate do not depend on if and only if the misclassification is symmetric, i.e., .

Lemma 2 shows that under Assumption 1 the false positive rate and false negative rate are constant across if and only if the misclassification is symmetric, i.e., . This misclassification is symmetric if is independent of (exogenous misclassification).

From the previous paragraph, we conclude that in the scenario where false positive and false negative rates do depend not on the instrument, they must be equal under our identifying assumptions. Hence, in such a scenario, we have

where is partially identified:

Hence, the MTE is partially identified as a function of :

where is the local instrumental variable (LIV) estimand.

Numerical illustration of this special case

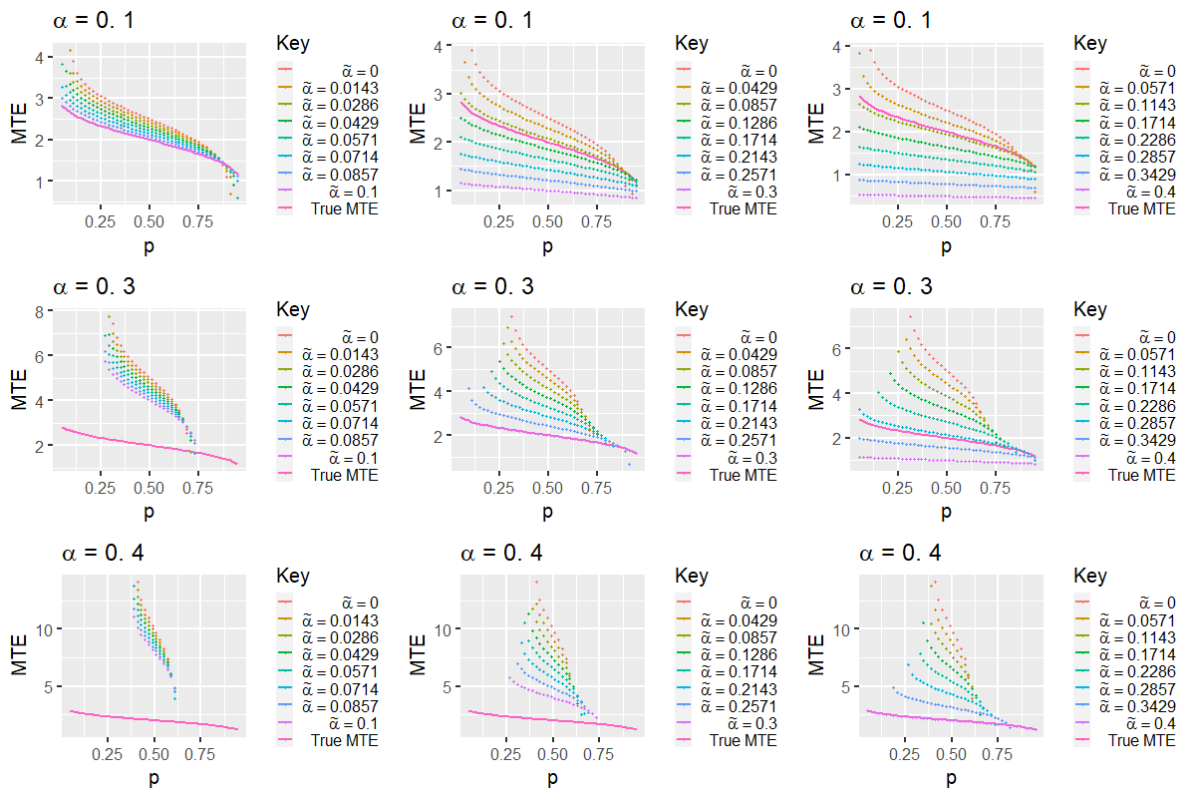

We assume in this illustration that the researcher knows that the rate of misclassification is less than 1/2. Consider the same example from the previous section (3.24) where (i.e., is independent of ). Details on this illustration are given in Subsection I.2 in the appendix.

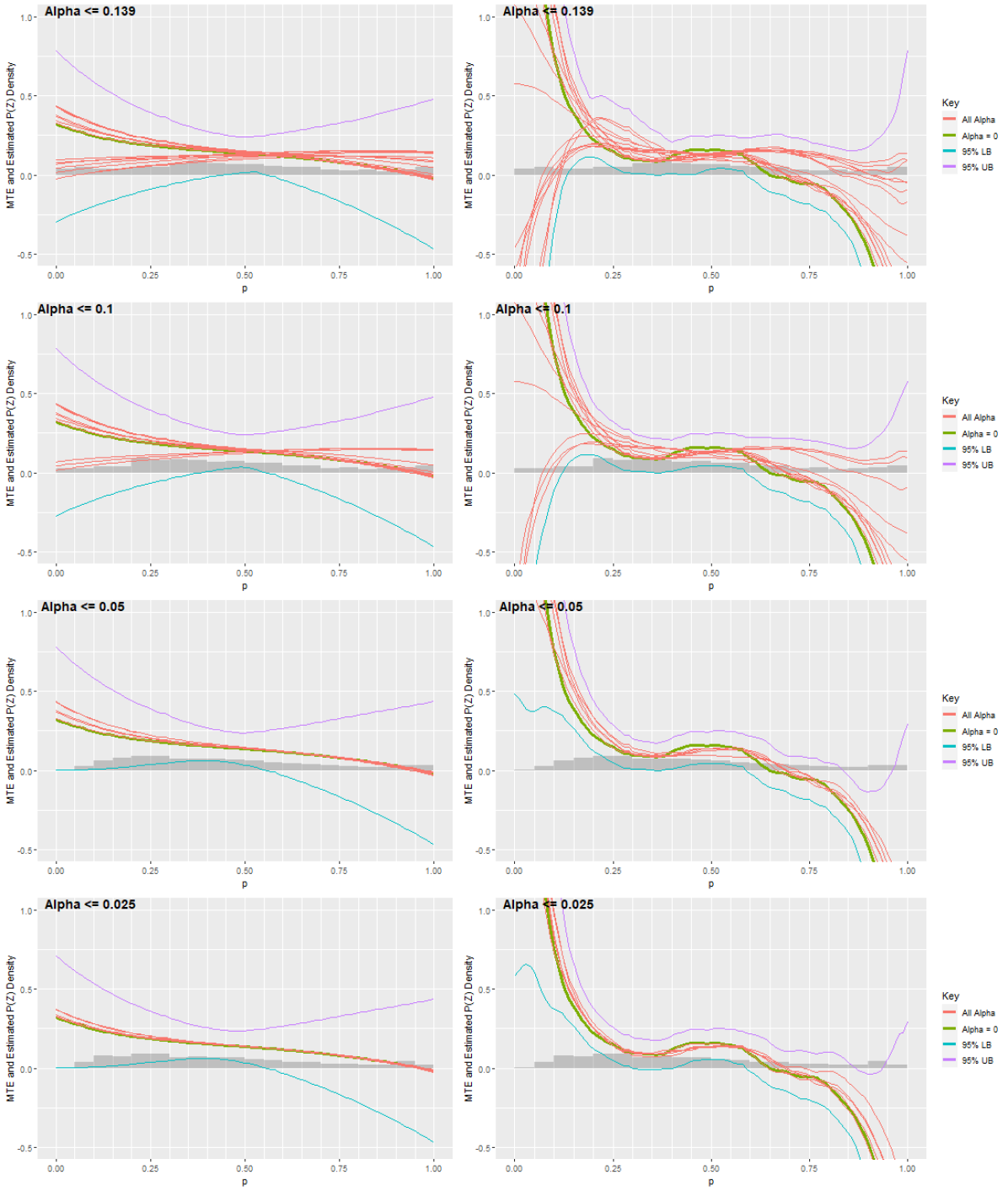

Figure 2 displays the MTE bounds for different misclassification probabilities and different values of . On the one hand, the rows show the identification regions when takes values , , and , respectively. On the other hand, the columns display the MTE bounds when is equal to , , and , respectively. Eight different discretized values within the support are used to show the corresponding plots for the MTE bounds. We note that the identification region for the MTE grows with for each value of the true misclassification rate . When is sufficiently large, the bounds contain the true MTE (see the last column). However, when is set too small, the true MTE lies outside the bounds, and the model is misspecified (see the first column). This suggests that researchers should do some sensitivity analysis by trying different values of .

4.2. When false positive/negative rates depend on the instrument

When the misclassification is asymmetric in the sense that false positive and false negative rates depend on the instrument, without further assumptions the researcher can use the bounds we derive in Section 3. However, there may exist some parametrization of the misclassification probabilities that can yield tighter bounds.

5. Empirical Relevance of the MTE bounds

The identification of the MTE can help reveal the presence of heterogeneity in the treatment effect. It can also be useful in the estimation of policy relevant treatment effect parameters (PRTEs) or conventional parameters such as the ATE, the average treatment effect on the treated (ATT), the average treatment effect on the untreated (ATU), the LATE, etc. Tables 1 and 2, which we borrow from Heckman and Vytlacil (2005), show the link between the MTE and those parameters. Unlike the weights in Heckman and Vytlacil (2005), the weights for the parameters ATT, ATU, and PRTE are not point-identified in our setting. They are only partially identified, as is the true propensity score . Like the MTE, these policy parameters are also partially identified. In the next section, we explicitly derive analytical bounds for different LATEs when the instrument is multivalued discrete.

| for two policies and that affect only |

6. Extension to discrete instruments

Assumption 6 (Discrete instrument).

The instrument is discrete with support and the propensity score satisfies

This assumption states that the ordering of the true propensity score is known, but the support of the instrument does not necessarily have the same ranking. This assumption does require monotonicity in the propensity score. For example, when the false positive and negative rates do not depend on , we have shown is Subsection 4.1 that the propensity score can be written as:

As we can see, in such a case, the ordering of the true propensity score is the same as that of the reported propensity score .

We sum up Equations (3.10) and (3.11), and take the difference for and , respectively. Combining this with the index sufficiency result (3.9), we have

Therefore,

The analog of the result holds with expectations. Hence, we identify the MTE up to the function as follows:

We have

| (6.1) |

Equations (3.3) and (6.1) imply the following additional bounds on :

Therefore, the following bounds hold for :

where

The proposition below holds.

Proposition 4.

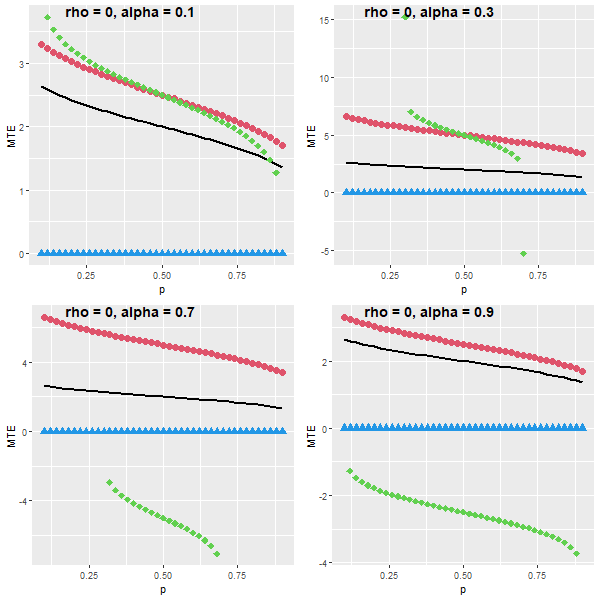

At this point, we do not have a result on the sharpness of the bounds in Proposition 4. This could be investigated in future work. However, when is completely unknown (i.e., ), these bounds are tighter than the existing bounds in Tommasi and Zhang (2020). Moreover, when is completely unknown and the instrument is binary, the bounds in Proposition 4 are tighter than the existing Ura (2018) bounds, which appear to be the tightest in the literature before our work. In such a case, we show in Appendix D that the bounds are sharp. Indeed, when is binary and is completely unknown (i.e., ), our bounds on are

The improvement over the existing bounds mainly stems from the fact that these bounds were not derived using the constraint that the specification imposes. As we prove in Lemma 3 in Appendix A, this constraint is without loss of generality. The results in Proposition 4 hold under the same assumptions that the existing papers have used.

7. Empirical illustration

To illustrate our methodology, we use data from the third wave of the Indonesia Family Life Survey (IFLS) fielded from June through November 2000. We build upon Carneiro, Lokshin, and Umapathi (2017) who estimate average and marginal returns to schooling in Indonesia using a semiparametric selection model. The authors use exogenous geographic variation in access to upper secondary schools to identify their model when ignoring the presence of measurement errors in the treatment variable. In their analysis, these researchers control for several family and village characteristics, namely father’s and mother’s education, an indicator of whether the community of residence was a village, religion, whether the location of residence is rural, province dummies, and distance from the village of residence to the nearest health post.

The IFLS is a household and community level panel survey that was conducted in 1993, 1997 and 2000. The sample was drawn from 321 randomly selected villages, spread among 13 Indonesian provinces containing 83% of the population, and consists of males aged 25–60 employees in public and private sectors. Females are excluded from the sample because of low labor force participation, self-employed workers are also excluded because it is difficult to measure their earnings. The sample size is 2608.

Following Carneiro, Lokshin, and Umapathi (2017), we define the dependent variable in the analysis as the log of the hourly wage , which is constructed from self-reported monthly wages and hours worked per week. The treatment variable is the indicator that the individual has an upper secondary or higher education (i.e., he completed at least 10 years of education). As we argue in Example 1, people often misreport their education level. So, we observe their true education level with some measurement errors. The control variables are indicator variables for age, indicators for the level of schooling completed by each of the parents (no education, elementary education, secondary education, and an indicator for unreported parental education), an indicator for whether the individual was living in a village at age 12, indicators for the province of residence, an indicator of rural residence, and distance (in kilometers) from the office of the head of the community of residence to the nearest community health post.

The instrumental variable for schooling is the distance (in kilometers) from the office of the community head to the nearest secondary school. The main assumption from Carneiro, Lokshin, and Umapathi (2017) is that if we consider two individuals with equally educated parents, with the same religion, living in a village which is located in an area that is equally rural, in the same province, and at the same distance of a health post, then distance to the nearest secondary school is uncorrelated with direct determinants of wages other than schooling. The authors present evidence that this assumption is likely to hold, suggesting that the IV is valid. In particular, they show that, once the previously mentioned variables are controlled for, there is no dependence between the distance to the nearest secondary school and whether the individual ever failed a grade in elementary school, how many times he repeated a grade in elementary school, and whether he had to work while attending elementary school. In addition, they show (using a different sample) that the distance variable is unrelated to test scores (Math, Bahasa, Science, and Social Studies) in elementary school. However, the validity of the distance to the nearest secondary school instrument remains highly questionable. For this reason, this exercise should be seen as illustrative.

Estimation Results

The estimation procedure follows the same steps as in the numerical illustration in Subsection 4.1, with the exception that we do not know the true DGP. We consider the specification , which we obtain under the symmetric misclassification assumption as described in Subsections 4.1. As we discussed, this scenario occurs when there is exogenous misclassification: . The scenario under exogenous misclassification implies that the conditional distribution of given is linear. Next, we consider alternative assumptions about the misclassification mechanism in Appendix H, where depends on and the conditional distributions of given are respectively concave and convex. The results are roughly similar across all specifications.

Choice of

As previously discussed in Section 2, following the comment below Assumption 4, we assume that someone who has at least an upper secondary education in Indonesia will proudly and truthfully report it. Hence, the false negative rate is set to zero. Furthermore, following Black, Sanders, and Taylor (2003), we assume that among those who report having at least an upper secondary schooling, the proportion of misclassification is bounded by 1/3, i.e., . Therefore, . Hence, we set . However, to check the sensitivity of our results with respect to the choice of , we try three other values for

Implementation

As mentioned above, for sensitivity analysis reasons, we consider four candidates for the upper bound on the misclassification rate . For as an example, we consider 15 grid points for within .101010We consider 15, 11, 6, and 6 grid points for = 0.139, 0.1, 0.05, and 0.025, respectively. After we estimate using a logit specification to obtain the observed propensity scores for each individual, we estimate the true propensity scores for each of the 15 different values on the grids within .111111As the logit specification forces the propensity scores estimates to lie over [0, 1], we trim the estimated true propensity scores to lie between with (Carneiro and Lee, 2009). Afterwards, we estimate the MTE nonparametrically using a local quadratic approximation, as recommended by Fan and Gijbels (1996) for estimating a first-order derivative, using each of the 15 possible values of the true propensity score. To do so, we use either (a) a Gaussian kernel and a bandwidth of 0.27 as used in the original work by Carneiro, Lokshin, and Umapathi (2017) or (b) the R package nprobust developed by Calonico, Cattaneo, and Farrell (2019). Note that the plug-in approach is asymptotically valid when the bandwidth used in the nonparametric estimation goes to zero as the sample size goes to infinity, since the first stage estimator converges at the parametric rate , and the second stage nonparametric estimator converges at . The first stage estimation bias does not vanish asymptotically with fixed bandwidth. For this reason, we prefer the nprobust method.121212Note that the nprobust package uses the epanechnikov kernel, and the optimal bandwidth is chosen from a direct plug-in implementation of MSE-optimal choices which considers whether an evaluation point is interior or boundary. However, whenever it is not applicable, the rule-of-thumb implementation of MSE-optimal choices is selected.

In order to control for exogenous covariates in a tractable manner, we assume the partially linear regression model, and implement the Robinson (1988) approach, following Carneiro, Lokshin, and Umapathi (2017). More precisely, we specify

where . Since , we have

where , and .

Therefore, we have

The estimation procedure for a given set of true propensity score estimates is as follows. First, we save residuals from a set of nonparametric regressions of , , and on . Then, we regress the residualized on the residualized and to obtain and . Finally, we run a local quadratic regression of the residual on to obtain as a first derivative.

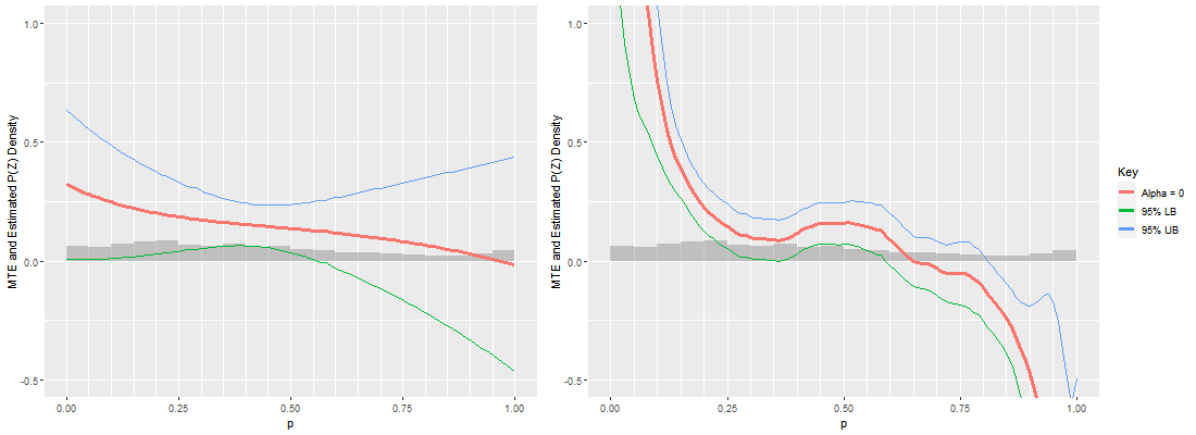

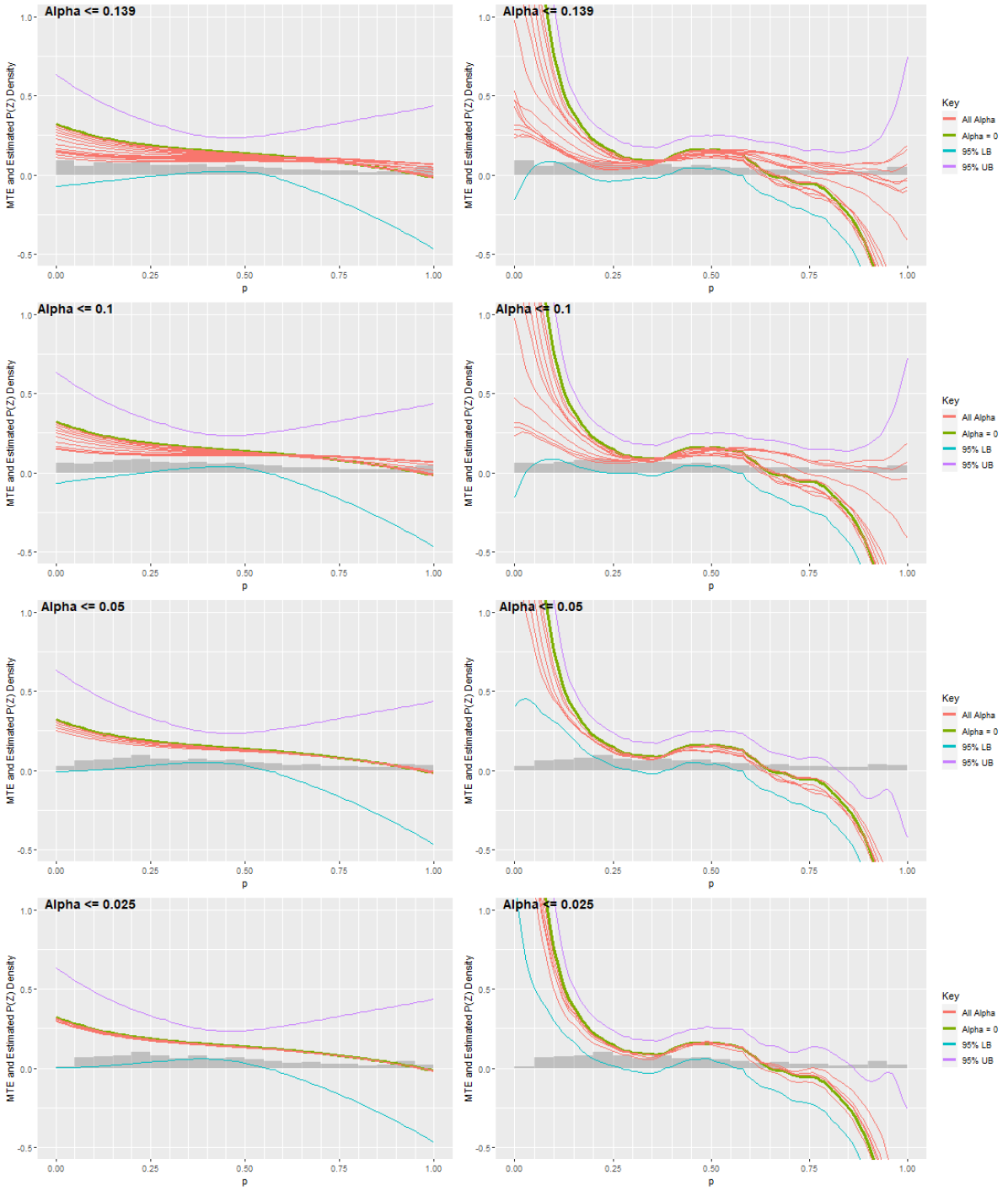

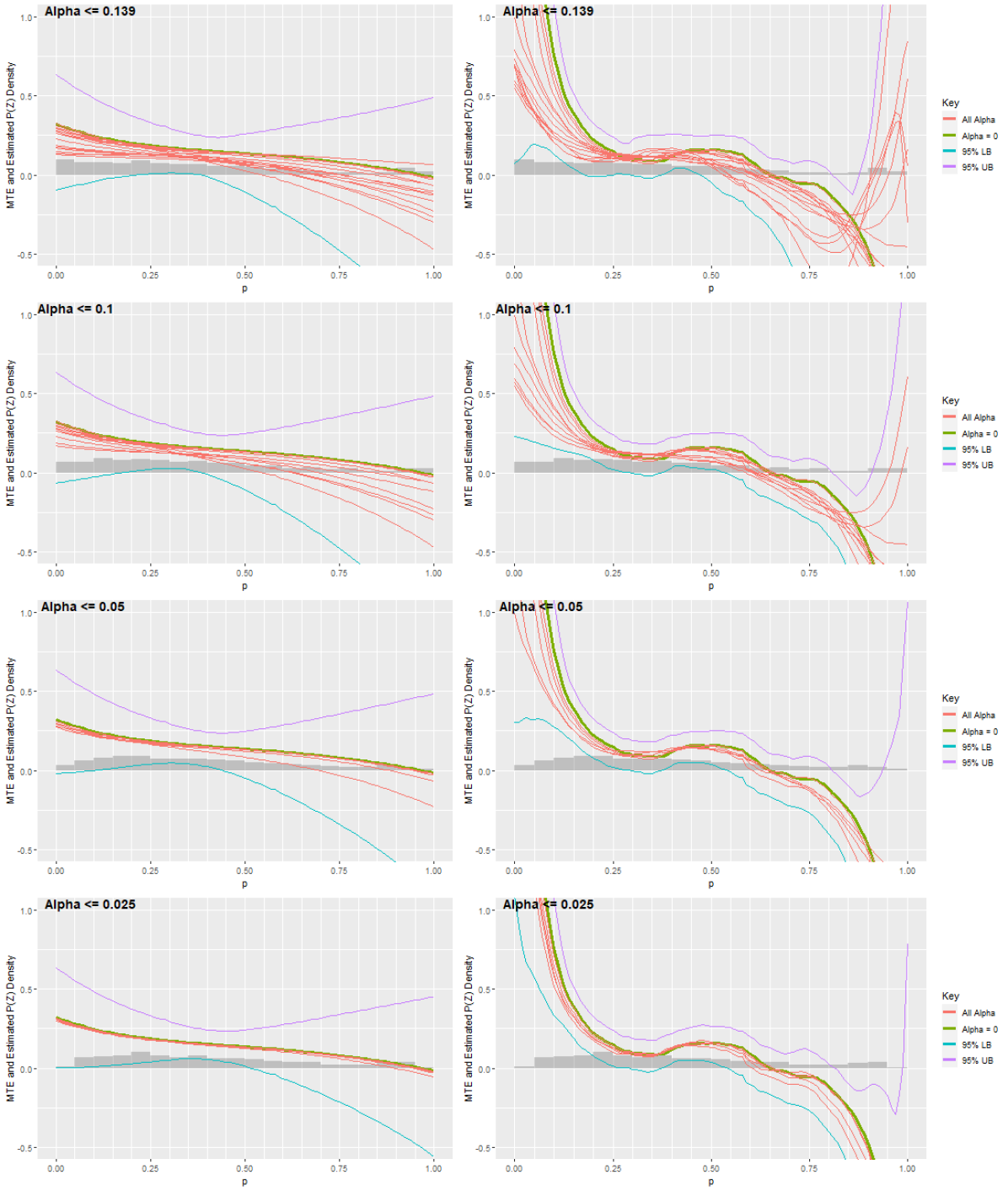

Figure 3 shows the results assuming no misclassification (), while Figure 4 shows the results of the Gaussian kernel and nprobust estimations for each row under the 3 different values of , with the histograms of the estimated true propensity score evaluated at . For each , the 95% confidence bounds of MTE region are obtained by taking the union of each of the confidence bands for the MTE over the grid points in . We use 250 bootstrap replications to obtain the standard errors of the MTE estimates for the Gaussian kernel estimation, while we use the robust standard errors available from the nprobust package for the second estimation method. Finally, we use the same simulation-based method as Carneiro, Lokshin, and Umapathi (2017) to obtain the average parameters such as ATE, ATT, ATU, and AMTE (average marginal treatment effect).131313We obtain AMTE using a metric of for 3 different values of , and note that it is equivalent to MPRTE (marginal policy relevant treatment effect) for policy alternatives of the form when (Carneiro, Heckman, and Vytlacil, 2010). See Tables 3 and 5. Inference on these parameters also relies on 250 bootstrap replications for both the Gaussian kernel and the nprobust methods (see Tables 4 and 6).

| ATE | ATT | ATU | |||||

|---|---|---|---|---|---|---|---|

| LB | UB | LB | UB | LB | UB | ||

| Gaussian | 0.139 | ||||||

| 0.1 | |||||||

| 0.05 | |||||||

| 0.025 | |||||||

| nprobust | 0.139 | - | |||||

| 0.1 | - | ||||||

| 0.05 | - | - | |||||

| 0.025 | - | - | |||||

| ATE | ATT | ATU | |||||

|---|---|---|---|---|---|---|---|

| LB | UB | LB | UB | LB | UB | ||

| Gaussian | 0.139 | - | - | ||||

| 0.1 | - | ||||||

| 0.05 | - | ||||||

| 0.025 | - | ||||||

| nprobust | 0.139 | - | - | - | |||

| 0.1 | - | - | - | ||||

| 0.05 | - | - | |||||

| 0.025 | - | - | |||||

| 0.1 | 0.05 | 0.01 | ||||||

|---|---|---|---|---|---|---|---|---|

| LB | UB | LB | UB | LB | UB | |||

| Gaussian | 0.139 | |||||||

| 0.1 | ||||||||

| 0.05 | ||||||||

| 0.025 | ||||||||

| nprobust | 0.139 | |||||||

| 0.1 | ||||||||

| 0.05 | ||||||||

| 0.025 | ||||||||

| 0.1 | 0.05 | 0.01 | ||||||

|---|---|---|---|---|---|---|---|---|

| LB | UB | LB | UB | LB | UB | |||

| Gaussian | 0.139 | |||||||

| 0.1 | ||||||||

| 0.05 | ||||||||

| 0.025 | ||||||||

| nprobust | 0.139 | - | - | - | ||||

| 0.1 | - | - | - | |||||

| 0.05 | - | - | - | |||||

| 0.025 | - | - | ||||||

| Point Estimates | Confidence Bounds | |||||

|---|---|---|---|---|---|---|

| LB | UB | LB | UB | |||

| 0.139 | ||||||

| 0.1 | ||||||

| 0.05 | ||||||

| 0.025 | ||||||

| 0.139 | ||||||

| 0.1 | ||||||

| 0.05 | ||||||

| 0.025 | ||||||

| 0.139 | ||||||

| 0.1 | ||||||

| 0.05 | ||||||

| 0.025 | ||||||

| 0.139 | ||||||

| 0.1 | ||||||

| 0.05 | ||||||

| 0.025 | ||||||

Discussion

First of all, Figure 3 shows that the nprobust method (second column) seems to better reveal the heterogeneity in the standard LIV estimate than the Gaussian kernel approach (first column). When there is no measurement error in the schooling variable (), we see that the return to upper secondary schooling is strongly positive for individuals who face low costs (), close to zero for those who face medium costs (), and negative for those whose costs are very high (). This heterogeneity was revealed in the original work of Carneiro, Lokshin, and Umapathi (2017) when considering the point estimate of the MTE, but it disappears when considering the confidence intervals of the MTE, because they used the Gaussian kernel approach which shows less heterogeneity.

On the one hand, in Figure 4, when (first row) or (second row), we observe that the MTE is weakly positive for individuals at all cost margins between completing an upper secondary education level or not. The estimate of the identified set for the MTE suggests that the return to upper secondary schooling is heterogeneous in Indonesia. Individuals who face smaller costs tend to have higher marginal returns compared to those who face higher costs. However, the MTE is generally not significant for most values of the schooling cost.

On the other hand, when (third row) or (fourth row), the heterogeneity in the return becomes more apparent with the nprobust approach. Even when allowing for the presence of misreporting in the education variable, the MTE is heterogeneous across individuals. Individuals at lower cost margins have higher and positive returns, while those at medium cost margins show returns close to zero, and those at higher cost margins seem to have lower and negative returns. The average marginal returns vary between -6% and 35% for values of between 0.01 and 0.1 when using the nprobust inference, while they vary between 3% and 25% when using the Gaussian kernel inference method.

Furthermore, the ATU (return for people who did not complete an upper secondary schooling had they done so) is not statistically different from zero, as their confidence bounds contain zero for both methods. However, the ATT (return for people who completed at least an upper secondary schooling) lies between 0.2% and 38.4% with the Gaussian kernel method, and between -0.6% and 121.5% with the nprobust approach. Similarly, the ATE lies roughly between 2% and 25% with the Gaussian kernel method, and between -19% and 46% with the nprobust approach. These results confirm that the MTE helps reveal heterogeneity in the return, which would otherwise be hidden when considering only the ATE, the ATT, and the ATU.

Overall, note that the patterns shown in Figure 4 are consistent across all other specifications considered in the appendix. The MTE curve seems weakly decreasing for all values of the schooling cost.

Another advantage of the MTE is that it helps answer policy-relevant questions. For example, as in Sasaki and Ura (2021), consider a counterfactual policy that exposes fraction of people with less than upper secondary schooling to upper secondary or higher education. More precisely, assume that the counterfactual policy has the form , where is the new propensity score that results from the policy. What would be the effect of such a policy on wages? To answer this question, we compute bounds on the policy-relevant treatment effect parameter for values . We use Sasaki and Ura’s (2021) inferential method to construct confidence bounds on the PRTE parameter.141414While Sasaki and Ura (2021) use a probit specification for the potentially misclassified propensity score, we use a logit specification to be consistent with Carneiro, Lokshin, and Umapathi (2017). For this reason, our point estimates of the PRTE parameter are different from Sasaki and Ura’s. Table 7 summarizes the results. For the four values of , the PRTE varies between 28% and 52%. These results suggest that the policy that induces about 5–20% of the population to upper secondary education is expected to increase wages by 28–52% per treated individual on average.

8. Conclusion

In this paper, we show that the MTE is generally partially identified in the presence of misclassification. We show that the MTE is equal to the derivative of the expectation of the observed outcome conditional on the true propensity score, which is partially identified. We provide nonparametric characterization of the identified set for the propensity score and the MTE. We show under some mild regularity conditions that the sign of the MTE is locally identified. We use our MTE bounds to derive bounds on other commonly used parameters in the literature. We show that our bounds are tighter than the existing bounds for the local average treatment effect. We illustrate the methodology numerically and empirically. We investigate the measurement of the return to upper secondary schooling in Indonesia, and find that the return is heterogeneous for people at the cost margin. Overall, marginal returns seem weakly decreasing with the schooling cost.

We have not developed a formal inference method for the analytical bounds for the MTE in this work. We believe that constructing a confidence set for these bounds could be worth exploring in future research. Also, future research could explore identification of the MTE in the presence of misclassification when imperfect instruments are available.

Appendix A Discussion about the model specification

One might think that the specification is too restrictive. But, it is general. To show this claim, we prove the following lemma.

Lemma 3.

For any two binary variables and , there exist two binary variables and such that

| (A.1) |

where .

Proof.

Let and be two binary variables. We can write , where . Since and are binary, we have

We can see that if and if . Hence, we can write . By setting and , we have . Since , we have . ∎

Appendix B Proofs of Proposition 1

Since the function and are continuous, there exist the in the lower bound on is attained. Similar result holds for the upper. We propose two misclassification scenarios that yield the lower or upper bound for each value of .

B.1.

Here, we assume that the misclassification occurs when the unobserved heterogeneity is less than or equal to . Then, we have , and . Hence, the conditional distribution of given is concave. Using Equation (2.7), we obtain that .

B.2.

Given this specification for the misclassification, we have , and . From there, we have . Hence, the conditional distribution of given is convex.

From Equation (3.4), we have:

If , the above equation becomes:

which implies

| (B.3) |

If , the equation becomes:

which implies

| (B.4) |

Appendix C Proof of Proposition 2

-

(i)

Suppose . Then, there is no misclassification, and the testable implications of the model are given by: for any such that , and . Therefore, , which implies . In this case, we also have . Thus, the result holds.

-

(ii)

Suppose . Then, for any such that , for any , and . Therefore, .

Appendix D Proof of sharpness when the instrument is binary

In this section, we assume that the researcher has no information about the misclassification rate . Suppose , and for each , either or for all . Define

Notice that and are well-defined probabilities. Define a joint distribution on .

for each . Define

for each , and each .

We can verify that the above proposed joint distribution is well-defined, (Assumption 1), and (Assumption 2), the joint distribution is compatible with the data, that is, it satisfies the following conditions:

for all , and all Borel set .

Now, we are going to show that . From the last equations, we have

Therefore,

Using Bayes’ rule, we have

Hence,

Finally, the expectation version of the result also holds, and we obtain

We have just shown that one of the bounds for the is achieved. Next, we will show that the other bound is also achievable. This case implies that , which is possible only when and , that is, there is full compliance: . This is possible if . Indeed, and imply that , and .

Appendix E Proof of sharpness under non-differential measurement error

Proof.

For each , we need to find a joint distribution on the vector , such that it satisfies model (2.6) and Assumptions 1, 2, and 5, and induces the joint distribution on . For any function satisfying the constraints in (3.28)-(3.36), define:

where , and . Define

It is easy to check that the above quantities are well-defined probabilities/distributions under the constraints (3.28)-(3.35), and the vector satisfies Assumptions 1, 2, and 5. Define

| (E.6) |

We will now show that the vector has the same distribution as the vector . We have

where the first equality holds from Equation (3.36). Given the definition of our DGP, we have

Therefore,

At this point, it remains to show that

This equality holds from condition (3.34).

Similarly, . ∎

Appendix F Proof of Lemma 2

Proof.

Suppose that and for all . Then

where the first equality holds from Assumption 1, the second holds from the law of total probability and Bayes’ rule, the third holds from the definition of and , and the fourth holds from our assumption that and are constant across .

If , then which is constant across , which contradicts the relevance condition that is a nontrivial function of , since under Assumption 1. Therefore, Hence,

Suppose now that the misclassification is symmetric in the sense that . Then, a similar derivation as above yields

From the last equality, we deduce that Therefore, ∎

Appendix G Allowing for dependence between misclassification and IV

Similarly to Equation 3.1, we have under , :

Hence, for any we have

Using the triangle inequality, we have

Therefore, by integrating each side over the support and using the Fubini-Tonelli theorem, we have

Hence, we have , where

Then, we have

Therefore, the following bounds hold for the MTE:

| (G.1) | |||

These bounds are wider those derived in Subsection 3.3 under Assumptions 1-4.

Appendix H Additional empirical results

| ATE | ATT | ATU | |||||

|---|---|---|---|---|---|---|---|

| LB | UB | LB | UB | LB | UB | ||

| Gaussian | 0.139 | ||||||

| 0.1 | |||||||

| 0.05 | |||||||

| 0.025 | |||||||

| nprobust | 0.139 | - | - | ||||

| 0.1 | - | ||||||

| 0.05 | - | - | |||||

| 0.025 | - | - | |||||

| ATE | ATT | ATU | |||||

|---|---|---|---|---|---|---|---|

| LB | UB | LB | UB | LB | UB | ||

| Gaussian | 0.139 | - | - | - | |||

| 0.1 | - | - | |||||

| 0.05 | - | ||||||

| 0.025 | - | ||||||

| nprobust | 0.139 | - | - | - | |||

| 0.1 | - | - | - | ||||

| 0.05 | - | - | - | ||||

| 0.025 | - | - | - | ||||

| 0.1 | 0.05 | 0.01 | ||||||

|---|---|---|---|---|---|---|---|---|

| LB | UB | LB | UB | LB | UB | |||

| Gaussian | 0.139 | |||||||

| 0.1 | ||||||||

| 0.05 | ||||||||

| 0.025 | ||||||||

| nprobust | 0.139 | |||||||

| 0.1 | ||||||||

| 0.05 | ||||||||

| 0.025 | ||||||||

| 0.1 | 0.05 | 0.01 | ||||||

|---|---|---|---|---|---|---|---|---|

| LB | UB | LB | UB | LB | UB | |||

| Gaussian | 0.139 | |||||||

| 0.1 | ||||||||

| 0.05 | ||||||||

| 0.025 | ||||||||

| nprobust | 0.139 | - | - | - | ||||

| 0.1 | - | - | ||||||

| 0.05 | - | - | ||||||

| 0.025 | - | - | ||||||

| Point Estimates | Confidence Bounds | |||||

|---|---|---|---|---|---|---|

| LB | UB | LB | UB | |||

| 0.139 | ||||||

| 0.1 | ||||||

| 0.05 | ||||||

| 0.025 | ||||||

| 0.139 | ||||||

| 0.1 | ||||||

| 0.05 | ||||||

| 0.025 | ||||||

| 0.139 | ||||||

| 0.1 | ||||||

| 0.05 | ||||||

| 0.025 | ||||||

| 0.139 | ||||||

| 0.1 | ||||||

| 0.05 | ||||||

| 0.025 | ||||||

| ATE | ATT | ATU | |||||

|---|---|---|---|---|---|---|---|

| LB | UB | LB | UB | LB | UB | ||

| Gaussian | 0.139 | - | - | ||||

| 0.1 | - | - | |||||

| 0.05 | - | ||||||

| 0.025 | |||||||

| nprobust | 0.139 | - | - | - | |||

| 0.1 | - | - | - | ||||

| 0.05 | - | - | |||||

| 0.025 | - | - | |||||

| ATE | ATT | ATU | |||||

|---|---|---|---|---|---|---|---|

| LB | UB | LB | UB | LB | UB | ||

| Gaussian | 0.139 | - | - | - | |||

| 0.1 | - | - | - | ||||

| 0.05 | - | - | |||||

| 0.025 | - | - | |||||

| nprobust | 0.139 | - | - | ||||

| 0.1 | - | - | |||||

| 0.05 | - | - | |||||

| 0.025 | - | - | |||||

| 0.1 | 0.05 | 0.01 | ||||||

|---|---|---|---|---|---|---|---|---|

| LB | UB | LB | UB | LB | UB | |||

| Gaussian | 0.139 | |||||||

| 0.1 | ||||||||

| 0.05 | ||||||||

| 0.025 | ||||||||

| nprobust | 0.139 | |||||||

| 0.1 | ||||||||

| 0.05 | ||||||||

| 0.025 | ||||||||

| 0.1 | 0.05 | 0.01 | ||||||

|---|---|---|---|---|---|---|---|---|

| LB | UB | LB | UB | LB | UB | |||

| Gaussian | 0.139 | - | - | - | ||||

| 0.1 | - | - | - | |||||

| 0.05 | ||||||||

| 0.025 | ||||||||

| nprobust | 0.139 | - | - | - | ||||

| 0.1 | - | - | - | |||||

| 0.05 | - | - | - | |||||

| 0.025 | - | - | - | |||||

| Point Estimates | Confidence Bounds | |||||

|---|---|---|---|---|---|---|

| LB | UB | LB | UB | |||

| 0.139 | ||||||

| 0.1 | ||||||

| 0.05 | ||||||

| 0.025 | ||||||

| 0.139 | ||||||

| 0.1 | ||||||

| 0.05 | ||||||

| 0.025 | ||||||

| 0.139 | ||||||

| 0.1 | ||||||

| 0.05 | ||||||

| 0.025 | ||||||

| 0.139 | ||||||

| 0.1 | ||||||

| 0.05 | ||||||

| 0.025 | ||||||

Appendix I Details on the numerical illustrations

I.1. Numerical illustration in Section 3

In this example, we have:

Hence, .

Moreover, note that

and thus it can be shown that

where is the bivariate normal distribution function with a correlation coefficient of , and is the bivariate normal copula.

Hence, we have the upper bound of MTE151515Note that this upper bound does not exploit the information from . as follows:161616This implicitly assumes that is known to be monotone because it states that as increases also increases (same direction).

or using L’Hôpital rule and properties of the copula (Meyer, 2013),

whenever the limit exists. Note that the limit does not exist if or if .

MTE bounds and LIV estimand

* The black line represents the true MTE from the model.

* The red circles (blue triangles) are the approximated upper (lower) bound at each grid point of .

* The green squares are the local IV estimand at each grid point of .

I.2. Details on the numerical illustration of the special case

We assume in this illustration that the researcher knows that the rate of misclassification is less than 1/2. Consider the same example from the previous section (3.24) where (i.e., is independent of ). Note that

because we have (Meyer, 2013). Hence, the following can be verified for the identification region for :

Moreover, because we have

and

for , we verify the true MTE lies within the identification region as follows:

References

- Acerenza (2021) Acerenza, S. 2021. “Partial Identification of Marginal Treatment Effects with Discrete Instruments and Misreported Treatment.” Working Paper .

- Aigner (1973) Aigner, D. J. 1973. “Regression with a Binary Independent Variable Subject to Errors of Observation.” Journal of Econometrics 1:49–60.

- Battistin, De Nadai, and Sianesi (2014) Battistin, E., M. De Nadai, and B. Sianesi. 2014. “Misreported schooling, multiple measures and returns to educational qualifications.” Journal of Econometrics 181:136–150.

- Battistin and Sianesi (2011) Battistin, E. and B. Sianesi. 2011. “Misclassified Treatment. Status and Treatment Effects: An application to Returns to Education in the United Kingdom.” The Review of Economics and Statistics 93 (2):495–509.

- Black, Sanders, and Taylor (2003) Black, D., S. Sanders, and L. Taylor. 2003. “Measurement of Higher Education in the Census and CPS.” Journal of the American Statistical Association 98:463:545–554.

- Bollinger (1996) Bollinger, C. R. 1996. “Bounding mean regressions when a binary regressor is mismeasured.” Journal of Econometrics 73 (2):387–399.

- Calonico, Cattaneo, and Farrell (2019) Calonico, Sebastian, Matias D. Cattaneo, and Max H. Farrell. 2019. “nprobust: Nonparametric Kernel-Based Estimation and Robust Bias-Corrected Inference.” arXiv e-prints :arXiv:1906.00198.

- Calvi, Lewbel, and Tommasi (2022) Calvi, C., A. Lewbel, and D. Tommasi. 2022. “Women’s Empowerment and Family Health: Estimating LATE with Mismeasured Treatment.” Journal of Business and Economic Statistics 40 (4):1701–1717.

- Carneiro, Lokshin, and Umapathi (2017) Carneiro, P., M. Lokshin, and N. Umapathi. 2017. “Average and Marginal Returns to Upper Secondary Schooling in Indonesia.” Journal of Applied Econometrics 32:16–36.

- Carneiro, Heckman, and Vytlacil (2010) Carneiro, Pedro, James J Heckman, and Edward Vytlacil. 2010. “Evaluating Marginal Policy Changes and the Average Effect of Treatment for Individuals at the Margin.” Econometrica 78 (1):377–394.

- Carneiro, Heckman, and Vytlacil (2011) ———. 2011. “Estimating Marginal Returns to Education.” American Economic Review 101 (6):2754–2781.

- Carneiro and Lee (2009) Carneiro, Pedro and Sokbae Lee. 2009. “Estimating distributions of potential outcomes using local instrumental variables with an application to changes in college enrollment and wage inequality.” Journal of Econometrics 149:191–208.

- Chalak (2017) Chalak, K. 2017. “Instrumental Variables Methods with Heterogeneity and Mismeasured Instruments.” Econometric Theory 33:69––104.

- DiTraglia and Garcia-Jimeno (2019) DiTraglia, Francis J. and Camilo Garcia-Jimeno. 2019. “Identifying the effect of a mis-classified, binary, endogenous regressor.” Journal of Econometrics 209:376–390.

- Fan and Gijbels (1996) Fan, Jianqing and Irene Gijbels. 1996. Local polynomial modelling and its applications: monographs on statistics and applied probability 66, vol. 66. CRC Press.

- Haider and Stephens Jr. (2020) Haider, S. J. and M. Stephens Jr. 2020. “Correcting for Misclassified Binary Regressors Using Instrumental Variables.” NBER Working Paper No. 27797 .

- Hausman, Abrevaya, and Scott-Morton (1998) Hausman, J. A., J. Abrevaya, and F. M. Scott-Morton. 1998. “Misclassification of the dependent variable in a discrete-response setting.” Journal of Econometrics 87:239–269.

- Heckman and Vytlacil (1999) Heckman, James J and Edward Vytlacil. 1999. “Local Instrumental Variable and Latent Variable Models for Identifying and Bounding Treatment Effects.” Proceedings of the National Academy of Sciences 96:4730–4734.

- Heckman and Vytlacil (2001) ———. 2001. “Local Instrumental Variables.” in Nonlinear Statistical Modeling: Proceedings of the Thirteenth International Symposium in Economic Theory and Econometrics: Essays in Honor of Takeshi Amemiya :1–46.

- Heckman and Vytlacil (2005) ———. 2005. “Structural Equations, Treatment Effects, and Econometric Policy Evaluation.” Econometrica 73 (3):669–738.

- Horowitz and Manski (1995) Horowitz, Joel L. and Charles F. Manski. 1995. “Identification and Robustness with Contaminated and Corrupted Data.” Econometrica 63 (2):pp. 281–302.

- Hu (2008) Hu, Y. 2008. “Identification and estimation of nonlinear models with misclassification error using instrumental variables: A general solution.” Journal of Econometrics 144:27–61.

- Hu and Lewbel (2012) Hu, Y. and Arthur Lewbel. 2012. “Returns to lying? identifying the effects of misreporting when the truth is unobserved.” Front. Econ. China 7 (2):163–192.

- Hu and Schennach (2008) Hu, Y. and S. M. Schennach. 2008. “Instrumental variable treatment of nonclassical measurement error models.” Econometrica 76 (1):195–216.

- Jiang and Ding (2020) Jiang, Z. and P. Ding. 2020. “Measurement errors in the binary instrumental variable model.” Biometrika 107 (1):238–245.

- Kasahara and Shimotsu (2021) Kasahara, H. and K. Shimotsu. 2021. “Identification of Regression Models with a Misclassified and Endogenous Binary Regressor.” Econometric Theory (forthcoming) .

- Kreider (2010) Kreider, B. 2010. “Regression coefficient identification decay in the presence of infrequent classification errors.” The Review of Economics and Statistics 92 (4):1017–1023.

- Kreider and Pepper (2007) Kreider, B. and J. V. Pepper. 2007. “Disability and Employment: Reevaluating the Evidence in Light of Reporting Errors.” Journal of American Statistical Association 102 (478):432–441.

- Kreider et al. (2012) Kreider, B., J. V. Pepper, C. Gundersen, and D. Jolliffe. 2012. “Identifying the effects of SNAP (food stamps) on child health outcomes when participation is endogenous and misreported.” Journal of American Statistical Association 107:958–975.

- Lewbel (2007) Lewbel, Arthur. 2007. “Estimation of Average Treatment Effects with Misclassification.” Econometrica 75 (2):537–551.

- Mahajan (2006) Mahajan, Aprajit. 2006. “Identification and Estimation of Regression Models with Misclassification.” Econometrica 74 (3):631–665.

- Meyer (2013) Meyer, Christian. 2013. “The bivariate normal copula.” Communications in Statistics-Theory and Methods 42 (13):2402–2422.

- Millimet (2011) Millimet, D. 2011. “The elephant in the corner: a cautionary tale about measurement error in treatment effects models.” In Missing Data Methods: Cross-Sectional Methods and Applications. In: Advances in Econometrics Advances in Econometrics, Emerald Group Publishing Limited 27:1–39.

- Mogstad, Santos, and Torgovitsky (2018) Mogstad, Magne, Andres Santos, and Alexander Torgovitsky. 2018. “Using Instrumental Variables for Inference about Policy Relevant Treatment Effects.” Econometrica 86 (5):pp. 1589–1619.

- Molinari (2008) Molinari, F. 2008. “Partial identification of probability distributions with misclassified data.” Journal of Econometrics 144:81–117.

- Mourifié, Henry, and Méango (2020) Mourifié, I., M. Henry, and R. Méango. 2020. “Sharp Bounds and Testability of a Roy Model of STEM Major Choices.” Journal of Political Economy 8 (128):3220–3283.

- Nguimkeu, Denteh, and Tchernis (2019) Nguimkeu, P., A. Denteh, and R. Tchernis. 2019. “On the estimation of treatment effects with endogenous misreporting.” Journal of Econometrics 208:487–506.

- Possebom (2021) Possebom, V. 2021. “Crime and Mismeasured Punishment: Marginal Treatment Effect with Misclassification.” Working Paper .

- Robinson (1988) Robinson, P M. 1988. “Root-N-Consistent Semiparametric Regression.” Econometrica 56 (4):931.

- Sasaki and Ura (2021) Sasaki, Y. and T. Ura. 2021. “Estimation and inference for policy relevant treatment effects.” Journal of Econometrics (forthcoming) .

- Tommasi and Zhang (2020) Tommasi, D. and L. Zhang. 2020. “Bounding Program Benefits When Participation Is Misreported.” Discussion Working Paper series, IZA DP No. 13430 .

- Ura (2018) Ura, Takuya. 2018. “Heterogeneous Treatment Effects with Mismeasured Endogenous Treatment.” Quantitative Economics 9 (3):1335–1370.

- Ura (2020) ———. 2020. “Instrumental variable quantile regression with misclassification.” Econometric Theory (forthcoming) .

- Yanagi (2019) Yanagi, T. 2019. “Inference on local average treatment effects for misclassified treatment.” Econometric Reviews 38:938–960.