DeFiRanger: Detecting Price Manipulation Attacks on DeFi Applications

Abstract

The rapid growth of Decentralized Finance (DeFi) boosts the Ethereum ecosystem. At the same time, attacks towards DeFi applications (apps) are increasing. However, to the best of our knowledge, existing smart contract vulnerability detection tools cannot be directly used to detect DeFi attacks. That’s because they lack the capability to recover and understand high-level DeFi semantics, e.g., a user trades a token pair X and Y in a Decentralized EXchange (DEX).

In this work, we focus on the detection of two types of new attacks on DeFi apps, including direct and indirect price manipulation attacks. The former one means that an attacker directly manipulates the token price in DEX by performing an unwanted trade in the same DEX by attacking the vulnerable DeFi app. The latter one means that an attacker indirectly manipulates the token price of the vulnerable DeFi app (e.g., a lending app). To this end, we propose a platform-independent way to recover high-level DeFi semantics by first constructing the cash flow tree from raw Ethereum transactions and then lifting the low-level semantics to high-level ones, including token trade, liquidity mining, and liquidity cancel. Finally, we detect price manipulation attacks using the patterns expressed with the recovered DeFi semantics.

We have implemented a prototype named DeFiRanger and applied it to more than million transactions. It successfully detected real-world attacks in the wild. We confirm that they belong to four known security incidents and five zero-day ones. We reported our findings. Two CVEs have been assigned. We further performed an attack analysis to reveal the root cause of the vulnerability, the attack footprint, and the impact of the attack. Our work urges the need to secure the DeFi ecosystem.

1 Introduction

The recent Decentralized Finance (DeFi) boom brings Ethereum a new climax, attracting billion USD locked in DeFi apps up to st January 2021. With the rapid growth of the DeFi ecosystem, security issues are also emerging. DeFi-related security issues have been reported, including front-running [48, 47, 75], Pump-and-Dump (P&D) scams [55, 72], and flash loan attacks [61]. In addition, code and logic vulnerabilities in DeFi apps bring many security incidents [30, 16, 29, 17, 28, 36, 18, 19, 40, 21, 38, 26].

Existing detection tools [57, 64, 53, 52, 71, 63, 54, 65, 50, 49, 62, 45, 70] mainly focus on the code vulnerability, such as the re-entrancy and the integer overflow. However, to the best of our knowledge, they cannot be directly used to detect DeFi attacks caused by logic vulnerabilities due to the lack of the capability to recover and understand high-level DeFi semantics, e.g., a user trades a token pair X and Y in a Decentralized EXchange (DEX).

Among DeFi apps, decentralized exchanges and lending apps are the two most popular types of ones. According to the statistics [23], there are five DEXes and four lending apps in the top ten DeFi apps. Automated Market Maker (AMM) is the most popular type of DEX that provides the cryptocurrency exchange service. Each pool in the AMM maintains two or more types of cryptocurrencies and leverages a price mechanism to decide the exchange rate. Besides, a user can borrow cryptocurrencies from a lending app by depositing the collateral (e.g., the USDC token) into the app. To determine how many cryptocurrencies that a user can borrow, the lending app needs to retrieve the current price of the collateral, e.g., from a pool in AMM.

We observe that with the popularity of DEXes and lending apps, two types of new attacks are emerging, i.e., direct and indirect price manipulation attacks. As the name suggests, the former one means that an attacker directly manipulates the token111In this paper, we interchangeably use cryptocurrencies, assets, and tokens to denote Ether and ERC20 tokens. price in a pool of an AMM. It is usually achieved through performing an unwanted trade in the same pool by attacking the vulnerable DeFi app. The latter one means that an attacker indirectly manipulates the token price of the vulnerable DeFi app (e.g., a lending app), whose price mechanism depends on the real-time status, e.g., the quotation and reserves of a token, in an AMM. An attacker can manipulate the status by making a trade in the AMM. For instance, the attacker can raise up the price of the collateral in the AMM pool that provides the price information to the lending app before borrowing loans. By doing so, the attacker can borrow much more tokens than a legitimate borrower can borrow with the same amount of collateral.

Our work Our work aims to detect price manipulation attacks. It requires us to analyze transactions between multiple smart contracts and understand the high-level semantics of DeFi apps. There are two challenges in this process.

-

•

Challenge I: Complicated interactions. DeFi apps often consist of multiple smart contracts that interact with each other. For example, one attack transaction of the Harvest Hack incident [26] (explained in Section 5.6) involves internal transactions. Fig. 8 shows part of the internal transaction graph. How to analyze the complicated interactions between smart contracts is the first challenge.

-

•

Challenge II: Semantic Gap. There is a semantic gap between raw transactions that can be observed on Ethereum and high-level DeFi semantics that are defined in DeFi apps. On Ethereum, we can only observe the field values of these (external or internal) transactions, such as from, to, and input. However, we cannot get the high-level DeFi semantic such as there exists an account that trades USDC for Ether in the USDC-Ether pool using the Uniswap V2 protocol. This high-level DeFi semantic is critical to detect price manipulation attacks since the attack usually involves the trade of tokens.

Our work solves the two challenges in the following way. First, our insight to solve the first challenge is that though a DeFi-related transaction often triggers many internal transactions between smart contracts, not all of them are useful for our analysis. We can prune unnecessary ones. Second, we propose a platform-independent way to recover DeFi semantics. We name it semantic lifting since it lifts low-level semantics in raw transactions to high-level DeFi semantics.

Specifically, we first collect raw Ethereum transactions and then construct the cash flow tree (CFT in short). This tree reflects the token transfer initialized by an external (or internal) transaction and the corresponding account. We call the token transfer as the basic DeFi action. After that, our system recovers the high-level DeFi semantics based on the token transfer behavior in CFT. In particular, our system can automatically recognize three types of advanced DeFi semantics, including the liquidity mining (depositing tokens into an DeFi app), liquidity cancel (withdrawing tokens from a DeFi app), and the trade (of different tokens in an AMM pool). Finally, we detect the price manipulation attacks using the detection patterns that are expressed with these recovered DeFi semantics.

Evaluation We have implemented a prototype system called DeFiRanger and evaluated its effectiveness from two perspectives. First, whether the proposed method can accurately recover DeFi semantics? Second, whether our system can detect real-world price manipulation attacks in the wild, including zero-day ones?

To answer the first question, we compare the result of recovered DeFi semantics with Etherscan [4]. Our comparison shows that DeFiRanger can identify more DeFi semantics than Etherscan, with a lower false negative rate. What’s more important, until the writing of this paper in April 2021, Etherscan can identify none of the DeFi semantics of vulnerable DeFi apps that are detected by DeFiRanger. This clearly shows the value of our system to recover DeFi semantics. Otherwise, none of the attacks can be detected.

To answer the second question, we performed a large-scale price manipulation attack detection from transactions. As a result, DeFiRanger detected real-world attacks in the wild. We confirm that they belong to four known security incidents and five zero-day ones, and they caused a total loss of around USD. Note that, one security incident can have hundreds of attacks, thus the number of security incidents is less than the number of real attacks. We reported our findings, and two CVEs have been assigned 222For the anonymity purpose, we do not include the CVE numbers in the paper.. This result clearly shows that DeFiRanger can effectively detect price manipulation attacks.

Attack Analysis We further analyze the detected nine security incidents to understand the root cause of the vulnerability, the attack footprint, and the financial impact to the vulnerable DeFi apps. First, we find that vulnerabilities are either due to insufficient access control of critical interfaces in the smart contract or insecure price dependence. Second, we find that attackers are becoming mature. They take a clean attack strategy to make the trace of attackers challenging. Third, security incidents have a direct impact on the market value of vulnerable DeFi apps, which urges the need to secure DeFi apps.

Contributions We summarize our main contributions as below.

-

•

We first propose two price manipulation attacks and elaborate the challenges to detect them in the wild. Then we propose a method to recover DeFi semantics to facilitate the detection. To the best of our knowledge, our work is the first to systematically detect price manipulation attacks on DeFi apps.

-

•

We implement a prototype named DeFiRanger and apply it to perform a large-scale price manipulation attack detection. It successfully detected real-world attacks. These attacks contribute to four known security incidents and five zero-day ones. After reporting our findings to vulnerable DeFi apps, two CVEs have been assigned.

-

•

We perform detailed analysis on confirmed security incidents to understand the root cause of the vulnerability, attack footprint, and financial impact to victim DeFi apps. Our analysis urges a need to secure the DeFi ecosystem.

To engage the community, we will release DeFiRanger to the research community.

2 Background

This section presents necessary background information to better understand our work.

2.1 Ethereum Accounts and Transactions

Ethereum has two types of accounts, i.e., External Owned Account (EOA) and smart contract account. A transaction can be used to send Ether between accounts or to invoke APIs in smart contracts. There are two types of transactions, i.e., external transaction and internal transaction. The external transaction is triggered by an EOA, while the internal transaction is triggered by a smart contract. Specifically, an external transaction sent by an EOA can invoke functions inside a smart contract, which will further create an internal transaction. The internal transaction can take a similar way to invoke a smart contract and trigger other internal transactions. In the following of this paper, the usage of “transaction” without specifying “external” or “internal” implies that we take an external transaction and the triggered internal transactions as a whole, as shown in Fig. 1.

2.2 Ethereum Cryptocurrencies

There are two types of cryptocurrencies in Ethereum: Ether and ERC20 token. Ether is the native token in Ethereum, and an ERC20 token is the third-party one that complies with the ERC20 standard. Every account, including EOA and the smart contract account, can own Ether and ERC20 tokens. Though there are many types of ERC20 tokens, the following two are related to our work.

Stablecoins Stablecoins are a class of cryptocurrencies that guarantee price stability. Typically, stablecoins are either directly/indirectly backed or intervened through different stabilization mechanisms [58, 46]. The popular stablecoins include USDC [13] or USDT [7].

Liquidity Provider (LP) Tokens A DeFi app may issue LP tokens to motivate users to provide more liquidity (i.e., depositing cryptocurrencies into that DeFi app). Users providing liquidity are called liquidity providers. Liquidity providers can use the LP tokens as certificates to withdraw their deposits or exchange for other cryptocurrencies in those decentralized exchanges (Section 2.3). In this paper, we interchangeably use cryptocurrencies, assets, and tokens to denote Ether and ERC20 tokens.

2.3 Decentralized Finance (DeFi)

DeFi app usually consists of multiple smart contracts to implement its functionality, running on the blockchain. Some financial services, such as lending, exchange and portfolio management, have emigrated in the DeFi ecosystem. As of this writing, more than 200 DeFi apps have been deployed on Ethereum.

Decentralized EXchange (DEX) DEX is an exchange where users can trade different tokens in a decentralized way by interacting with the smart contract(s). Compared with the traditional centralized exchange, DEX possesses several distinct advantages, especially in privacy and capital management.

There are two modes in DEX, including List of Booking (LOB) and Automated Market Maker (AMM). DEX using the LOB mode maintains an off-chain order book to record users’ bids and asks, namely,the matching of orders will be completed off-chain. Alternatively, the AMM mode achieves a full decentralized exchange. The market maker may put two or more tokens into a liquidity pool with an equivalent or a self-defined weight. The trade rate between cryptocurrencies in the pool will be calculated automatically based on the pricing mechanism. AMM becomes the most popular mode in DEX due to its flexible liquidity.

Lending To borrow cryptocurrencies, borrowers are required to over-collateralize other cryptocurrencies for covering the loan due to the pseudo-anonymity of Ethereum.

For example, in MakerDAO [6], borrowing 100 DAI requires tokens that are worth 150 Ether as collateral. Moreover, once the collateral’s value falls below a fixed threshold, it causes liquidation (the lending app will sell the collateral), as well as a designed penalty that will be applied to borrowers.

Flash Loan Some DeFi apps [8] [35] [9] provide a type of non-collateral loan called flash loan. A valid flash loan ”generously” lends users a considerable amount of capital without any collateral. The security of the loan is guaranteed since the user needs to borrow and return the loan in a single transaction (with multiple following internal transactions). Otherwise, the lending transaction will be reverted by the loan provider.

The flash loan gives everyone the ability to temporarily own a large number of tokens. However, it can also be abused to launch attacks, and a number of such attacks have been observed in the wild [67, 61, 44].

Portfolio Management As more and more DeFi apps motivate clients to provide liquidity, another kind of apps, known as portfolio management apps, debut to help users (liquidity providers) to invest their cryptocurrencies. In particular, they automatically find the apps that provide the highest Annual Percentage Yields (APY) and then invest clients’ deposits to these apps.

3 Price Manipulation Attacks

In this work, we aim to detect two types of price manipulation attacks, including the direct and the indirect ones. As the name suggests, the former one means that an attacker directly manipulates the token price in a liquidity pool of an AMM. It is usually achieved through performing an unwanted trade in the same pool by attacking the vulnerable DeFi app. The latter one means that an attacker indirectly manipulates the token price of the vulnerable DeFi app, whose price mechanism depends on the real-time status, e.g., the quotation and reserves of a token, in an AMM. An attacker can manipulate the status by making a trade in the AMM.

In the following, we first use the Uniswap V1 protocol [14] as an example to introduce the price mechanism of an AMM and then elaborate the two types of attacks.

3.1 Price Mechanism of the Uniswap Protocol

A liquidity pool of Uniswap makes up reserves of two cryptocurrencies. Users can trade tokens with the price determined by the pricing mechanism/formula of Uniswap, as follows:

| (1) |

Specifically, shows the amount of token Y that a user can trade with the token X in an amount of . and are the balances of the token X and token Y in the liquidity pool, respectively. Since the exchange rate between the token pair depends on the pool’s reserve balances (or reserves), attackers who are capable of draining the pool can make a trade to inflate or reduce a token’s price, namely, manipulate the price deviating from the market price. Such a behavior is referred to as price manipulation. DeFi apps that interact with a manipulated pool may suffer from financial losses.

3.2 Direct Price Manipulation Attack

Some DeFi apps have interfaces to trade tokens in AMMs. However, if the interfaces are not properly protected, an attacker can abuse these interfaces to trade tokens on behalf of the vulnerable DeFi app, which affects the exchange rate of a token pair. Then the attacker can make another trade of his or her own token to gain profits. Since the token price is directly manipulated by trading a token pair in an AMM, we call such an attack a direct price manipulation attack.

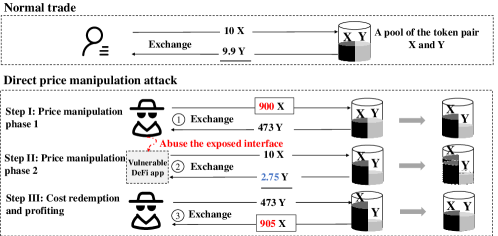

Fig. 2 shows an example. Suppose the pool has the same initial reserves () of a token pair X and Y. In a normal trade, a user can get Y with X, according to the formula (1). An attacker can use the following three steps to perform the direct price manipulation attack.

Step I: Price manipulation phase one The attacker uses X, that occupies a large proportion of the pool to exchange for the token Y, which breaks the balance of the token pair and lifts the token Y’s price in the pool.

Step II: Price manipulation phase two The attacker invokes the public interface of the vulnerable DeFi app to sell X. However, the DeFi app only gets Y after consuming X. That’s because the previous step reduces the price of the token X. Besides, this trade further lifts the price of the token Y in the pool.

Step III: Cost redemption and profiting The attacker sells Y and gets X with a reverse exchange. That’s because the token Y’s price has been raised in the second step. By doing so, the attacker can get a profit of X.

Specifically, the first step inflates token Y’s price and reduces token X’s price in the pool. This is an expected behavior according to the formula (1). However, the second step makes the vulnerable DeFi app sell its token X and further raises the price of the token Y. This is achieved by exploiting the exposed interface of the vulnerable DeFi app. As a result, the attacker can make a reverse exchange by selling the token Y and get more X ( in the example). Compared with a normal trade ( X with Y), the victim DeFi app losses Y (i.e., ).

3.3 Indirect Price Manipulation Attack

Some DeFi apps need the token price for business purposes. For instance, a lending app is required to calculate the collateral’s price to decide how many tokens a borrower is eligible to borrow. If the price mechanism of the lending app is manipulable, a borrower might borrow more tokens than the outstanding principal balance of the collateral (i.e., undercollateralization [15]).

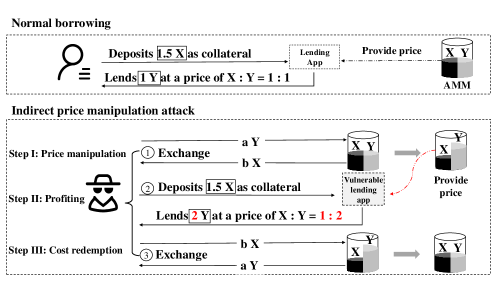

Fig. 3 gives an example. The lending app uses the real-time exchange rate of a token pair fetched from an AMM (through invoking the API exposed by the smart contract of the AMM) to determine the value of the collateral. Suppose the initial exchange rate between the token X and Y is 1:1. In the normal borrowing scenario, a user deposits token X to the lending app as the collateral and borrows token Y, since the collateral ratio [1] of the lending app is . An attacker is able to take the following steps to launch the indirect price manipulation attack.

Step I: Price manipulation The attacker trades a tremendous amount of token Y for token X, draining out a large proportion of the token X in the pool, thus creating an inflated price for the token X. Since the lending app’s price mechanism depends on the AMM’s real-time quotation, the token X’s price is also inflated in the lending app.

Step II: Profiting After manipulating the token X’s price, the attacker simply borrows the token Y using the token X as the collateral. In particular, he or she can borrow Y rather than Y with the same amount of the collateral ( X) as in the normal borrowing scenario.

Step III: Cost redemption The attacker only needs to redeem the cost of price manipulation by making a reverse exchange in the AMM pool.

The root cause of this attack is that the vulnerable lending app leverages an AMM’s real-time quotation to decide the collateral’s price. As a result, the attacker can make a trade in the AMM’s pool to affect the token price (Step I) and then borrow an undercollateralized loan from the lending app (Step II). After that, the attacker makes a reverse trade to redeem the cost (Step III).

Note that the previous steps of these two attacks are simplified for better illustration. In a real attack, the attacker may leverage the flash loan [41, 67, 61, 44] to borrow a large number of tokens that are required in the first step.

4 Challenges and Solutions

In this section, we present two challenges in detecting price manipulation attacks and then illustrate our methods to address these challenges.

4.1 Challenges

The price manipulation attacks originate from logic vulnerabilities of DeFi apps, which makes it non-trivial to perform the detection. Namely, detecting such attacks requires us to analyze transactions between multiple smart contracts and understand the high-level semantics of DeFi apps.

Challenge I: Complicated interactions DeFi apps tend to have complicated business logic and consist of multiple smart contracts that interact with each other. For instance, the average number of smart contract invocations triggered by each transaction before December is . From December to April , the number becomes , due to the DeFi boom. Besides, DeFi-related transactions between multiple smart contracts are too complicated to be analyzed by existing tools [4, 34]. For example, one attack transaction of the Harvest Hack incident [26] (explained in Section 5.6) involves internal transactions. Fig. 8 shows part of the internal transaction graph. Obviously, it is challenging to analyze the complicated interactions between smart contracts.

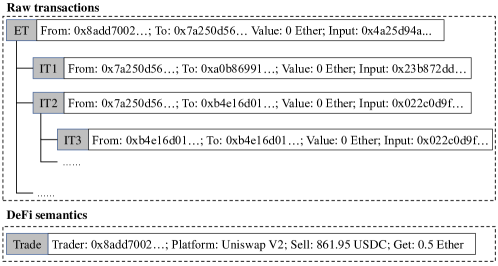

Challenge II: Semantic gap There exists a semantic gap between raw transactions that are observed on Ethereum and DeFi semantics that are defined in DeFi apps. As shown in Fig. 4, the address 0x8add7002 launches an external transaction that uses the Uniswap V2 protocol to exchange tokens. This external transaction further triggers internal transactions. On Ethereum, we can only observe the field values of these (external or internal) transactions, such as from, to, and input. However, we cannot identify the high-level DeFi action that the address 0x8add7002 trades USDC for Ether in the USDC-Ether pool using the Uniswap V2 protocol. This high-level DeFi semantic is critical to detect price manipulation attacks since they usually involve the trade of tokens.

4.2 Our Solutions

Our work takes the following methods to address the two challenges.

Method I: Pruning unnecessary transactions Our observation suggests that not all of the internal transactions triggered by a DeFi-related transaction are helpful for our analysis. As such, we can solve the first challenge by pruning those unnecessary ones.

For example, the transaction in Fig. 4 triggers internal transactions. Only three of them are closely related to the token trade. The remaining ones are used for auxiliary operations, such as finding the suitable pool and checking token balances. Furthermore, we observe that the token transfer (including token minting and burning) is the primitive action in the DeFi ecosystem. Therefore, we simplify the interaction in DeFi-related transactions by removing transactions that are unrelated to the token transfer. We illustrate this process in Section 5.3.

Method II: Recovering high-level semantics We recover high-level DeFi semantics from raw transactions to solve the second challenge. Note that, even though Etherscan [4] provides the recovered DeFi semantics on its website, the information is incomplete. The experimental result in Section 6.1 shows that Etherscan [4] has a higher false negative rate in identifying DeFi actions. Our work takes a platform-independent way to recover DeFi actions. We name it semantic lifting since it lifts low-level semantics in raw transactions to high-level DeFi semantics. We will illustrate the process in Section 5.4.

5 Methodology

Fig. 5 shows the overview of our work. In particular, we first propose a system called DeFiRanger to detect price manipulation attacks. Then for the detected attacks, we perform further analysis from multiple perspectives, e.g., understanding the root cause of the vulnerability and the impact on the vulnerable DeFi apps. We elaborate DeFiRanger in this section and attack analysis in Section 7, respectively.

5.1 Overview

5.2 Data Collection

Though a few online services, including Google’s BigQuery Ethereum service, provide interfaces to query transactions, they are not enough to support the analysis of DeFiRanger. For instance, the internal states of EVM when executing a smart contract are not available. To serve the need, we deploy an Ethereum full node with a modified Geth [5] client to collect the required data. First, we collect internal transactions’ metadata, including from, to, input, etc. Second, we collect the EVM depth when executing each internal transaction. This helps us recover the invocation order of different functions in multiple smart contracts. Third, we collect the execution order between internal transactions and events. This can help us to retrieve the sequence of token transfers.

5.3 CFT Construction

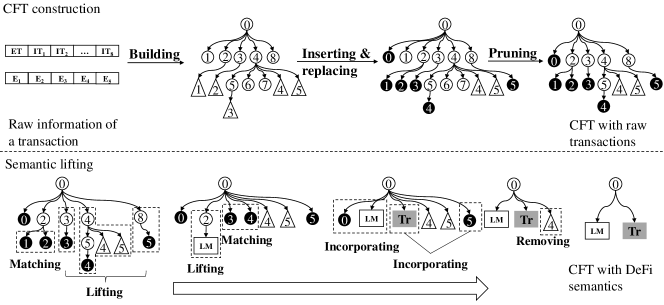

After collecting the Ethereum raw transactions, our system builds the cash flow tree [42] (CFT for short). The CFT is used to convert raw transactions to token transfer, which lays a foundation to lift DeFi semantics (Section 5.4). For a better understanding, we use Fig. 6 as an example to illustrate the whole process. There are three types of nodes inside the tree.

-

•

Transaction node Both external and internal transactions are included in the tree. The directed edge between two (external or internal) transactions means that the child transaction is created by the parent transaction. For instance, the external transaction creates an internal transaction . Thus, there is a directed edge from to in the graph.

-

•

Event node Events are emitted by a smart contract during its execution for the logging purpose. A smart contract can selectively emit events. In the graph, events are child nodes of internal transactions since the event emitting is initialized by an internal transaction to execute a smart contract.

-

•

Transfer node Transfer node denotes the existence of Ether or ERC20 token transfer that is initiated by an external (or internal) transaction.

Building the tree structure The first step is to build a tree from raw transactions, including internal and external ones. This process is straightforward. We only need to append a child node to a parent node if the child transaction is created from the parent. For instance, five internal transactions (from to and ) are created by one external transaction, thus they are the child nodes of the parent node . Note that, we also append the event node in the graph as the child of the transaction node that creates the event. For instance, the event node is the child of node since it is created by this internal transaction.

Inserting and replacing with transfer nodes With the tree structure built in the previous step, we need to append transfer nodes in the tree. That’s because the token transfer is the basis for recovering DeFi semantics. First, we append the Ether transfer node to the tree. We can easily retrieve such nodes since the Ether transfer has a non-zero Value field of a transaction. We insert the Ether transfer node as the first child of the corresponding transaction node, e.g., in the figure. Second, we leverage the standard event Transfer to locate the transfer of ERC20 tokens. We replace Transfer event nodes with ERC20 token transfer nodes, e.g., replacing to . Note that, internal transaction creates two transfers, one is transferring Ether ( ) and the other is transferring the ERC20 token ( ).

Pruning tree branches Our system traverses the tree and prunes all branches without a transfer node. That’s because such branches are not helpful to lift semantics. This can greatly remove unnecessary interactions to address the challenge I discussed in Section 4.1. For instance, it removes () transaction nodes for a real-world attack in Section 5.6. In Fig. 6, transaction nodes , and are removed from the tree.

| DeFi Action | Symbol | Attributes | Condition | Assignment | Description |

|---|---|---|---|---|---|

| Basic actions | Basic actions include the following three types of transfer: , , and . | ||||

| Transfer(normal) |

,

, , |

and zeroaddress and zeroaddress and 0 |

;

; ; |

An account () transfers a certain amount () of certain asset () to another account (). | |

| Transfer(minting) |

,

, , |

zeroaddress;

and 0; |

;

; ; |

An ERC20 token contract mints a certain amount () of certain asset () to an account (). | |

| Transfer(burning) |

,

, , |

zeroaddress

and 0 |

;

; ; |

An account () burns a certain amount () of certain asset (). | |

| Advanced actions | Advanced actions include the below three ones: , , and . | ||||

| Liquidity Mining |

,

, , , , , |

Exists and

and |

|

An account () of a liquidity provider deposits certain amount () of certain asset () to provide liquidity in a liquidity pool () of a DeFi app, which then mints certain amount () of its LP token () to an account () that is specified by the liquidity provider. | |

| Liquidity Cancel |

,

, , , , , |

Exists and

and |

|

An account () of a liquidity provider burns a certain amount () of certain DeFi app’s LP token () to redeem deposits, a pool () of the app then transfers a certain amount () of certain asset () to an account () that is specified by the liquidity provider. | |

| Trade |

,

, , , , , |

(Exists two transfers(normal)

and and and ) or (exists and and and and ) |

or ();

or (); or (); or (); or (); or (); or () |

An account () of a trader sells a certain amount () of certain asset () for a certain amount () of certain asset () in a liquidity pool () of an AMM, and the trader specifies an account () as recipient. |

5.4 Semantic Lifting

Based on the CFT, we can further recover DeFi semantics that are critical to detect price manipulation attacks. In this work, we first define DeFi actions and then introduce the algorithm to lift the DeFi semantics from the CFT.

5.4.1 DeFi actions

In this work, we focus on the following four DeFi actions. More actions could be recovered if they are necessary in the future. Table 1 shows the definition.

Transfer Transfer means a token (asset) is transferred from one address (spender) to another (recipient). Besides, ERC20 token standard [3] defines that when the spender field is set to the zero address 333Zero address: 0x0000000000000000000000000000000000000000, it means a token mining, i.e., directly depositing tokens into the address (recipient). Similarly, if the recipient is set to the zero address, then the tokens are burning. They are denoted as , and , respectively in Table 1.

Liquidity Mining and Liquidity Cancel To get more liquidity, DeFi apps issue LP tokens to create incentives for users to provide liquidity (deposit cryptocurrencies), known as liquidity mining (). Besides, liquidity providers can redeem cryptocurrencies with the LP tokens as certificates, which is named liquidity cancel (). Accordingly, the liquidity mining consists of two components, i.e., depositing users’ liquidity () and minting DeFi app’s LP token (). The liquidity cancel consists of burning LP tokens () and redeeming the deposited liquidity ().

Trade In the normal situation, a trade consists of two transfers. Therefore, we combine a pair of transfers, that transfer different assets and have a pivot address ( or ) as a trade. We further assign the pivot address to the attribute of the trade. That’s because traders exchange their tokens through the liquidity pool (as the intermediary).

| Combination of DeFi actions | Detection rules | Description | |

|---|---|---|---|

|

Direct price

manipulation attack |

(or ) |

Exists a sequence of DeFi actions: , (or ), and

and and and and and and and and and (( and and ) or ( and and )) |

An attacker () inflates an asset’s () price in a liquidity pool () of an AMM via a trade () and then abuses the exposed interface of a vulnerable app ( or ) to further inflate the asset’s () price in the pool on behalf of the vulnerable app. Finally, the attacker launches a reverse trade () in the same pool () to gain profits. Above three steps are consistent to the three steps in Section 3.2, but we extend the middle step to transfer and trade for detecting more attacks. |

|

Indirect price

manipulation attack |

(or ) |

Exists a sequence of DeFi actions: , (or ), and

and and and and and and and and and ( or ( and )) |

An attacker () leverages a trade () to indirectly manipulate the price in a vulnerable app ( or ) and then profits from the vulnerable DeFi app via certain DeFi action ( or ). Finally, the attacker launches a reverse trade () to redeem costs. Similarly, above three steps are consistent to the three steps in Section 3.3, but we extend the middle step to any DeFi action that can profit the attacker for detecting more attacks. |

| Arbitrage |

Exists a sequence of trades: , , …, and

and and and and …… and |

An arbitrager leverage a sequence of trades (, , …, and ) to profit from the price differences crossing multiple exchanges. |

-

•

: represents the execution order; : for better illustration, we do not consider the fee charged by AMM.

5.4.2 Lifting algorithm

With the well-defined DeFi actions, we then propose an algorithm to lift CFT’s semantics. Algorithm 1 post-order traverses the CFT (LiftLeaves). For each non-leaf node, the function repeatedly merges its child nodes in pairs until they cannot be merged (line -).

The algorithm follows two guidelines to merge the nodes MergeLeaves (line ). First, if two adjacent leaves match the conditions of a DeFi advanced action defined in Table 1, they will be merged as the DeFi advanced action. This is called matching in this paper. For instance, transfer nodes and are merged into a node.

Second, if there exists a transfer chain in the two adjacent leaves, one will incorporate another one. For example, two transfers are “A transfers Ether to B”, and “B transfers Ether to C”, the former one will incorporate the latter one. This is called incorporating in this paper. For instance, transfer node and transfer node in the liquidity mining node constitute a transfer chain, then the node incorporates transfer node .

Besides, if a subtree consists of only one leaf, its parent node will be removed, and it will be lifted (line -) to form more adjacent leaves. In the end, it will remove redundant events on the CFT (line ). For a better understanding, we name them as lifting and removing in Fig.6. For instance, the subtree of the transaction node consists of only one leaf (the node), then our algorithm removes the transaction node and lifts its subtree. Besides, it also removes the redundant event node .

5.5 Attack Detection

After recovering DeFi semantics, We detect price manipulation attacks by matching recovered semantics with attack patterns (or rules). We then manually confirm the detected transactions. Table 2 shows the rules.

Detecting direct price manipulation attacks The rule follows the attack flow discussed in Section 3.2. Specifically, the first step and the third step are identified by a pair of reverse trade ( and ). The second step is a trade () or a transfer ( including , , and ). That’s because a transfer can also influence the reserves of a liquidity pool of an AMM.

Detecting indirect price manipulation attacks Similarly, the rule follows the flow discussed in Section 3.3. Particularly, we detect step I and step II by identifying a pair of reverse trades ( and ). We extend the step II (profiting) from borrowing (that is often a transfer) to any action ( or ) that can profit the attacker.

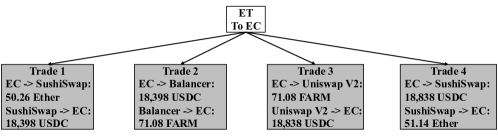

Note that, the reverse trade pairs widely appear in arbitrages [74], which will cause false positives. We need to identify arbitrages and then remove them from the result. Our observation is that arbitrage bots often only hold one type of asset. They first purchase the asset used for arbitrage and then sell it back for the original asset afterwards. As shown in Fig. 7, the arbitrage bot (EC) only holds Ether. It purchases the asset (USDC) used for arbitrage in trade and gets Ether back in trade . The trade and trade constitute a pair of reverse trades. In addition, the trade and trade , that capture the arbitrage opportunity also constitute a pair of reverse trades. The rules to detect arbitrages are presented in Table 2.

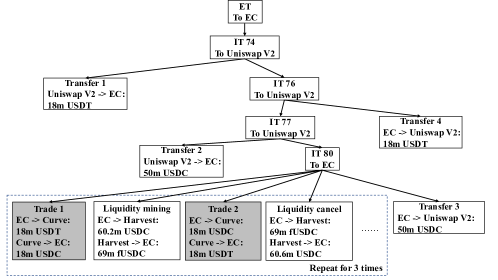

5.6 A Real Example

We use a real attack transaction 4440xb460b70f11a93364fecf1f3c3ec49f053aecd2d6d9912c01- 2170aa7a0de2d526 in Harvest Hack [26] to show the entire process. The security incident made Harvest lose almost USD.

DeFiRanger transforms raw transactions into a CFT with DeFi semantics via two steps, i.e., CFT construction and semantic lifting. During this process, it prunes branches in CFT to address challenge I (Section 4.1) and uses the semantic lifting to address challenge II (Section 4.1). The comparison of the transaction graph in Fig. 8 and the CFT with DeFi semantics in Fig. 9 shows the effectiveness of our system to solve the challenges.

In the attack detection process, DeFiRanger identifies trade 1 and trade 2 in Fig 9 as a pair of reverse trades ( and ), the entry contract (EC) as the attacker (), and Curve as the manipulated pool (). Furthermore, in the liquidity mining, the attacker deposits USDC to provide liquidity to the third-party app. Harvest then mints fUSDC to the attacker as certificates (, ). Since the detection rule is satisfied, DeFiRanger labels it as a suspicious indirect price manipulation attack.

6 Evaluation

In this section, we evaluate DeFiRanger from two perspectives: DeFi action identification and price manipulation attack detection, i.e., whether it can accurately identify DeFi actions, and whether it can detect real price manipulation attacks.

6.1 DeFi Action Identification

To the best of our knowledge, there is no ground truth for labeled DeFi actions in Ethereum. Etherscan [4] is the only public online service that identifies DeFi actions for each transaction. To evaluate the effectiveness of our method, we compare our result with that of Etherscan. In particular, we crawled transactions 555All transactions were downloaded on January 30, 2021. Etherscan has a speed limit and anti-crawling mechanism. We did not crawl more transactions to honor these mechanisms. from Etherscan. Then we apply our system on the downloaded transactions. Finally, we compare the identified actions with the labels reported by Etherscan.

For the same transactions, Etherscan and DeFiRanger identify and DeFi actions, as shown in the left and right oval in Fig. 10, respectively. The number of actions that are identified by both Etherscan and DeFiRanger is (B), while the number of actions that are identified by Etherscan but are missed by DeFiRanger is (A). Besides, DeFiRanger identifies extra (C+D) DeFi actions. Among them, we manually confirm that ones (D) are false positives.

|

# TP | # FP | # TN | # FN | FNR | TPR | Accuracy | |||

|---|---|---|---|---|---|---|---|---|---|---|

| Etherscan | 29,201 | 29,201 | 0 | 1,667 | 10,634 | 26.7% | 100% | 74.38% | ||

| DeFiRanger | 37,732 | 36,065 | 1,667 | 0 | 3,770 | 9.46% | 95.58% | 86.9% |

| (2) |

Table 3 shows the detailed result. Since we do not have the ground truth, all actions identified by Etherscan are treated as true positives (this assumption actually favors Etherscan). Then we use formula (2) to compute the accuracy. Specifically, the accuracy of DeFiRanger () is higher than Etherscan (). What’s more important, the false negative rate of DeFiRanger () is much lower than Etherscan (). This means DeFiRanger can identify more actions that will be missed by Etherscan. Since the attack detection is based on identified DeFi actions, the miss of DeFi actions will lead to the miss of real-world attacks. Until the writing of this paper in April , Etherscan can identify none of the DeFi actions for victim DeFi apps that are involved in the reported attacks by DeFiRanger (Section 6.2 and Section 7).

We summarize the advantages and disadvantages of our method to identify DeFi actions in the following.

Advantages Our method to identify DeFi actions is platform-independent, which saves the manual efforts to understand every new DeFi protocol. Note that, DeFi apps tend to have their own protocols. Moreover, our system can detect more DeFi actions than Etherscan, which leads to the detection of real attacks (Section 6.2).

Disadvantages DeFiRanger misidentifies actions in a few cases, such as the exchange of more than two types of tokens and adding multiple types of tokens to provide liquidity. This causes incorrect DeFi actions (with a false positive rate of ). Our system can tolerate such false positives since the detected attacks will be manually confirmed.

Summary: DeFiRanger can identify more DeFi actions than Etherscan, with a lower false negative rate. The identified DeFi actions are critical to detect price manipulation attacks reported in Section 6.2 and analyzed in Section 7.

| # Total | # Labeled | True positives | False positives | # Unconfirmed | |||

|---|---|---|---|---|---|---|---|

| transactions | transactions | # Successful Attacks | # Failed Attacks | # Arbitrages | # Recognition errorsa | transactions | |

| Indirect price manipulation attack | 350,823,625 | 101 | 41 | 3 | 51 | 0 | 6 |

| Direct price manipulation attack | 423 | 391 | 0 | 0 | 31 | 1 | |

-

•

: The recognition error represents false positives caused by misidentified DeFi actions.

6.2 Price Manipulation Attack Detection

We performed a large-scale detection on the transactions from Nov. 25, 2019, to Dec. 17, 2020. As shown in Table 4, DeFiRanger detected attacks in total. We manually confirmed that of them are true positives. In total, nine security incidents are detected. Four of them are known [26, 21, 38, 40], while five of them are zero-day incidents. We reported our findings and two CVEs were assigned.

The false positives consist of transactions for arbitrage and transactions with misidentified DeFi actions. First, our arbitrage detection strategy in Section 5.5 misses arbitrage transactions. This can be improved with a more accurate pattern to identify arbitrage. Second, DeFiRanger misidentifies a borrow action of bZx [12] as a trade. As a result, it further misidentifies a borrow-redeem pair as a pair of reverse trades, which causes the false positives. That’s because DeFiRanger does not yet support the identification of loan-related actions.

In summary, DeFiRanger not only detects four known security incidents [26, 21, 38, 40] but also reveals five zero-day incidents. In addition, DeFiRanger is the first tool to detect price manipulation attacks in Ethereum. Besides, DeFiRanger finishes the large-scale experiment in hours and consumes negligible memory during the process.

Summary: The detected nine security incidents with attacks shows the effectiveness of DeFiRanger. Among them, five security incidents are zero-day ones (with attacks in the wild.) To the best of our knowledge, DeFiRanger is the first tool that has the capability to detect price manipulation attacks in Ethereum.

7 Attack Analysis

| Direct price manipulation attacks | |||||||||

|

Incident | # Attacks | Profit | Victim app’s type | Root cause | CVE-ID | Zero-day? | ||

| Sep 30, 20 - Oct 15, 20 | LRC Incident | ETH a | DEX | Insufficient access control | CVE-2021-3xxx | ||||

| Oct 08, 20 - Dec 11, 20 | DRC Incident | ETH b | Portfolio management | Insufficient access control | - | ||||

| Nov 15, 20 - Dec 15, 20 | SEAL Incident | SEAL c | Portfolio management | Insufficient access control | CVE-2021-3xxx | ||||

| Nov 26, 19 - Oct 24, 20 | MET Incident | ETH d | Auction | Insufficient access control | - | ||||

| Indirect price manipulation attacks | |||||||||

| Oct 26, 20 | Harvest Hack [26] | stablecoins of USD | Portfolio management | Insecure price dependency | |||||

| Oct 29, 20 | Plouto Hack | stablecoins of USD | Portfolio management | Insecure price dependency | |||||

| Nov 06, 20 | Cheese Bank Incident [21] | stablecoins of USD | Lending | Insecure price dependency | |||||

| Nov 14, 20 | Value DeFi Incident [38] | stablecoins of USD | Portfolio management | Insecure price dependency | |||||

| Dec 17, 20 | WarpFinance Incident [40] | stablecoins of USD | Lending | Insecure price dependency | |||||

-

•

: ETH was worth around USD on Sep 30; : ETH was worth around USD on Oct 8;

-

•

: SEAL was worth around USD on Nov 15; : ETH was worth around USD on Nov 26.

In this section, we present the analysis result on the confirmed security incidents and insights to secure the DeFi ecosystem.

7.1 Vulnerability Root Cause Analysis

After analyzing each security incident, we find that the root causes of the vulnerabilities are falling into two categories, i.e., insufficient access control of the smart contract’s APIs and insecure price dependency between DeFi apps.

7.1.1 Insufficient access control

Four DeFi apps, including Loopring [27], Dracula [24], Seal Finance [32], and Metronome [10], are susceptible to direct price manipulation attacks. The root cause of the vulnerability is the same: they do not properly enforce the access control to the function that may change the AMM’s reserves.

The four vulnerable functions are sellTokenForLRC, drain, breed and closeAuction in these apps. The first three could be exploited by an attacker to sell cryptocurrencies in a liquidity pool of an AMM. An attacker can manipulate the pool in advance to decrease related cryptocurrencies’ prices and then invoke these functions to sell them cheaply, which causes the vulnerable apps to suffer losses. After that, the attacker can make profits by buying these cryptocurrencies at a relatively low price. The last one (closeAuction) directly deposits Ether into the Metronome’s AMM pool. Thus, an attacker first swaps Ether for the MET token and then invokes closeAuction to increase the AMM’s Ether reserves, which lifts MET’s price. Finally, the attacker swaps the same amount of MET for more Ethers than that are used in the first swap. As a result, the attacker can make profits with each invocation of clouseAuction.

Note that, Dracula [24] implemented an access control for the function drain in the latest version [25].

Insight I: Insufficient access control for functions that can change the AMM’s reserves makes the vulnerable DeFi apps susceptible to direct price manipulation attacks.

| Symbol | Description |

|---|---|

| The amount of the minted to a user. | |

| The amount of the burning by a user. | |

| The amount of the depositing by a user. | |

| The amount of the redeemed to a user. | |

| The current reserves of the in the pool. | |

| The total supply of the . | |

| The unit price of the . |

7.1.2 Insecure price dependency

Two types of vulnerable apps are susceptible to the indirect price manipulation attack, including portfolio management apps and lending apps. The portfolio management apps leverage AMM’s real-time quotation to price clients’ deposits, and lending apps rely on AMM’s real-time reserves to price clients’ collaterals. Thus, an attacker can manipulate the real-time quotation and reserves in AMMs to attack vulnerable apps.

Depending on AMM’s real-time quotation Harvest [37], Plouto [31], and Value DeFi [37] are portfolio management apps. They provide the same financial services and share a similar price mechanism. We use Harvest as a representative example.

The attack flow of the Harvest Hack [26] has been described in Section 5.6. We focus on its insecure price dependency. After receiving a user’s stablecoins, such as USDC, Harvest automatically deposits stablecoins to a DeFi app with the highest Annual Percentage Yield (APY). In short, Harvest acts as an account manager that helps users (clients) to invest their stablecoins.

One of Harvest’s investment strategies is to deposit clients’ USDC into Curve Y pool [22] to provide liquidity. During the process, clients get fUSDC (Harvest’s LP token) from Harvest as certificates, and Harvest gets yCrv (Y pool’s LP token) from Y pool as certificates. Formula 3 describes the number of fUSDC tokens that Harvest should mint and send to clients after receiving clients’ deposits (USDC), and the number of USDC that Harvest should refund to clients after receiving and burning clients’ fUSDC.

| (3) | ||||

According to the formula (3), the amount of minted fUSDC equals the product of the deposited USDC’s share and the total supply of fUSDC. The amount of refunded USDC equals the product of burned fUSDC’s share and the Total Value Locked (TVL). Since Harvest invests part of USDC into Curve, the TVL consists of the reserves of USDC and yCrv. To unify the unit, Harvest leverages the real-time price provided by the Curve Y pool (). However, the real-time price of the AMM (Curve) can be manipulated. Therefore, attackers can make profits through increasing the amount of refunded USDC by manipulating the Curve Y pool, as shown in the Harvest Hack Section (Section 5.6).

To the best of our knowledge, using the average price over a period of time can mitigate the indirect price manipulation attack. In fact, Curve has the interface (virtual_price) that provides the average token price. However, Harvest does not use this interface in its smart contract.

Depending on AMM’s real-time reserves Cheese Bank [20] and WarpFinance [39] are lending apps. They support Uniswap V2’s LP token as the collateral. Since Uniswap does not provide its LP tokens’ price, two lending apps implement their own pricing mechanism for Uniswap’s LP tokens.

| (4) |

Each Uniswap V2 pool maintains a pair of cryptocurrencies. Cheese Bank only supports the LP tokens of a limited number of Ether-related pools, e.g, Ether-USDT, Ether-USDC, Ether-CHEESE, and Ether-DAI. As shown in formula (4), it takes twice the value of Ether reserves in the pool as the pool’s TVL, which decides the LP token’s unit price.

| (5) |

Formula (5) shows how WarpFinance prices Uniswap V2’s LP token. Differ from Cheese Bank, WarpFinance takes the value of all reserves in an Uniswap V2’s pool as the pool’s TVL. Then, it takes a pool’s TVL divided by the total supply of the pool’s LP token as the unit price of the LP token.

The two price mechanisms are vulnerable because they both depend on the real-time reserves of Uniswap V2’s pools (, , and ). Therefore, attackers can lift the collateral’s price by manipulating the related Uniswap V2’s pool in advance. After collateralizing the “expensive collaterals”, attackers can borrow out more valuable stablecoins. They will, of course, not redeem their collaterals.

Insight II: The insecure price dependency is the root cause of vulnerable apps that are susceptible to indirect price manipulation attacks.

7.2 Footprint analysis

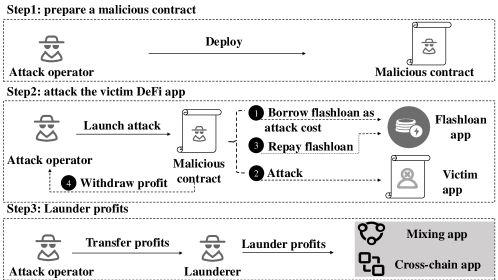

Attackers have used similar steps to launch the attack. We summarize the attack footprint in Fig. 11.

-

•

Prepare a malicious contract: The attacker uses an EOA, i.e., the attack operator, to deploy a malicious contract.

-

•

Attack the vulnerable apps: The attack operator invokes the malicious contract to launch the attack. Note that, the attacker usually leverages the flash loan to get a large number of tokens that are needed during the attack.

- •

Furthermore, we check whether a malicious contract has other callers or whether a malicious contract’s creator has deployed other smart contracts. The result is interesting. There are almost no other transactions except for the ones that are used for attacks. This clean attack strategy makes tracing attackers more challenging.

Insight III: Attackers are becoming mature. They leverage the mixing service and cross-chain apps to launder the profits, and hide their traces by using a clean attack strategy.

7.3 Impact Analysis

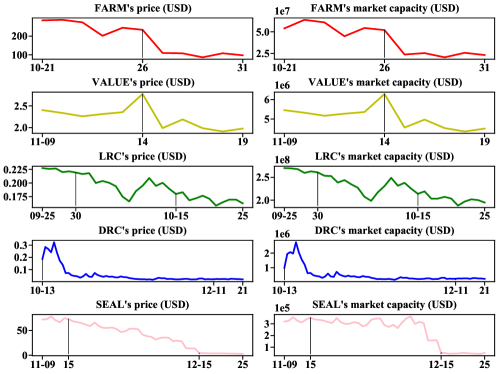

We analyze the impact on vulnerable DeFi apps’ market value after the security incidents. As shown in Fig. 12, we use the unit price and market capacity (in USD) to describe the market value of five vulnerable apps’ protocol tokens (tokens issued by DeFi apps). The price is retrieved from CoinGecko [2].

The market value of Harvest and Value dropped sharply on the day of the related incidents. We suspect that they are caused by the security incidents. In addition, the market value of Loopring, Dracula, and Seal Finance is also falling after the day of the related incidents. However, we cannot simply conclude that they are affected by related security incidents due to two main reasons. First, the market values are declining before related incidents. Second, LRC incident, DRC incident, and SEAL incident are zero-day. The lack of visibility limits their follow-up impacts.

Insight IV: Security incidents have direct impact on the market value of vulnerable DeFi apps, especially for the publicly known attacks.

8 Discussion

In this section, we discuss DeFiRanger’s limitations and future improvements.

Identify more DeFi actions Currently, DeFiRanger cannot identify a few DeFi actions, such as loan-related actions. For example, among missed actions compared with Etherscan (Section 6.1), of them are loan-related actions. We will extend DeFiRanger’s capability to identify more DeFi actions as one of the future work.

Detect more types of DeFi attacks Currently, DeFiRanger only focuses on two types of price manipulation attacks. In fact, with the recovered DeFi semantics, DeFiRanger is able to detect more types of DeFi attacks, if the detection patterns can be developed. To secure the Ethereum DeFi ecosystem, we will design more attack patterns and extend DeFiRanger’s detection ability. This process might be coupled with the extension of DeFi semantics identification.

9 Related Work

9.1 Ethereum DeFi ecosystem

The wave of DeFi brings many traditional financial applications to Ethereum, which attempt to use the openness and transparency of the blockchain technology to evolve finance from opaque to transparency. Werner et al. [69] summarize DeFi’s current development, including DeFi basic knowledge, popular DeFi protocols, and DeFi security issues. Particularly, Clark et al. [46], Pernice et al. [60], and Moin et al. [58] perform the empirical study about current stablecoins’ protocol design and provide the comprehensive taxonomy of stablecoins with their insights. Wang [68] studies mathematical models of AMMs. Bartoletti et al. [43] study various implementations of existing lending apps. Furthermore, Perez et al. [59] provide the first in-depth empirical study for liquidations on protocols for loanable funds (PLFs), such as lending apps. Liu et al. [56] present the first measurement for DeFi price oracles. The knowledge of these studies can help better understand the DeFi ecosystem.

9.2 DeFi security

9.2.1 Off-chain security issues

Front-running and Pump-and-Dump are two typical threats for DeFi security. They mainly focus on are off-chain activities.

Front-running In traditional finance, front-running often refers to a broker prioritizing his trade ahead of his clients’ market-moving order to benefit himself. Front-runners prioritize their transactions ahead of others by lifting transaction fees 666Miners tend to pack transactions with higher transaction fee.. Eskandari et al. [48] analyze the front-running issues across the top DeFi apps in Ethereum and present the evidence of abnormal miners’ behaviors of purchasing cryptocurrencies for front-running. Daian et al. [47] study bots’ arbitrage strategies and reveal the situation of front-running between bots. Zhou et al. [75] formalize the sandwich attack combining front- and back-running actions and present an empirical evaluation on it.

Pump-and-Dump (P&D) P&D often refers to a scheme that boosts the price of a stock by misleading information. The perpetrator of this scheme purchases a lot of these stocks in advance and sells them after the price has been driven up. Recently, this type of scheme also appears on the Ethereum DeFi ecosystem. Kamps et al. [55] construct a group of patterns by analyzing existing P&D schemes and define a set of identifying criteria, which can detect suspected P&D behaviors. Xu et al. [72] aggregate P&D schemes in telegram channels and build a machine learning model that can predict the likelihood of a cryptocurrency being pumped.

9.2.2 On-chain security issues

Various DeFi protocols are arising but with many security issues. Particularly, Flash loan is a nascent service that can lend any unsecured cryptocurrencies to clients. With this temporary funding capacity, some security issues have surfaced. Gudgeon et al. [51] demonstrated a simulated governance attack with the flash loan on the MakerDao [6]. Qin et al. [61] analyze two existing flash loan attacks and propose an optimization strategy that can increase the attacker’s benefit to and times the previous. Wang et al. [66] implement a preliminary work on automatically hunting for DeFi attacks.

Our work is different from them and aims to detect two new types of DeFi attacks.

9.3 Smart Contract Code Vulnerability

Ethereum smart contracts suffer from code vulnerabilities, such as re-entrancy and integer overflow. Many systems have been proposed to detect vulnerable smart contracts [57, 64, 53, 71, 54, 65, 63] or real-world attacks [50, 49, 62, 45, 73, 70]. For instance, Oyente [57] applies the symbolic execution technique to detect code vulnerabilities. eThor [63] leverages formal verification to reveal code vulnerabilities in smart contracts. TXSPECTOR [73] and EthScope [70] focus on uncovering historical attacks caused by code vulnerabilities in Ethereum. These systems cannot be directly applied to detect price manipulation attacks since they lack the capability to recover DeFi semantics.

10 Conclusion

In this work, we aim to detect two types of price manipulation attacks on DeFi apps. To this end, we present a new approach to automatically recover DeFi semantics from raw transactions. Then we detect attacks based on the recovered DeFi semantics. We implemented our approach in a tool named DeFiRanger. The evaluation result shows that our system can accurately recover DeFi semantics, and effectively detect DeFi attacks. In total, it revealed real real-world attacks that involve four known security incidents and five zero-day security incidents. Our work urges the need to secure the DeFi ecosystem.

References

- [1] Dictionary of law insider: collateral rate. https://www.lawinsider.com/dictionary/collateral-rate, 2010. [Online; accessed April-2021].

- [2] Coingecko. https://www.coingecko.com/en, 2014. [Online; accessed December-2020].

- [3] ERC20 Token Standard. https://eips.ethereum.org/EIPS/eip-20, 2015. [Online; accessed March-2020].

- [4] Etherscan. https://etherscan.io/, 2015. [Online; accessed Jan-2021].

- [5] Go ethereum. https://geth.ethereum.org/, 2015. [Online; accessed Feb-2021].

- [6] Makerdao. https://makerdao.com/zh-CN/, 2015. [Online; accessed December-2020].

- [7] Tether: Fiat currencies on the bitcoin blockchain. https://tether.to/wp-content/uploads/2016/06/TetherWhitePaper.pdf, 2016. [Online; accessed December-2020].

- [8] Aave. https://aave.com/, 2017. [Online; accessed December-2020].

- [9] dydx. https://dydx.exchange/, 2017. [Online; accessed December-2020].

- [10] Metronome. https://www.metronome.io/, 2017. [Online; accessed Jan-2021].

- [11] Ren. https://renproject.io/, 2017. [Online; accessed Jan-2021].

- [12] bzx. https://bzx.network/, 2018. [Online; accessed December-2020].

- [13] Centre: Centre whitepaper. https://www.centre.io/pdfs/centre-whitepaper.pdf, 2018. [Online; accessed December-2020].

- [14] Uniswap v1. https://uniswap.org/docs/v1/, 2018. [Online; accessed December-2020].

- [15] Wiktionary: undercollateralized. https://en.wiktionary.org/wiki/undercollateralized, 2019. [Online; accessed April-2021].

- [16] 88mph incident. https://peckshield.medium.com/88mph-incident-root-cause-analysis-ce477e00a74d, 2020. [Online; accessed December-2020].

- [17] Akropolis incident. https://peckshield.medium.com/akropolis-incident-root-cause-analysis-c11ee59e05d4, 2020. [Online; accessed December-2020].

- [18] bzx hack i. https://peckshield.medium.com/bzx-hack-full-disclosure-with-detailed-profit-analysis-e6b1fa9b18fc, 2020. [Online; accessed December-2020].

- [19] bzx hack ii. https://peckshield.medium.com/bzx-hack-ii-full-disclosure-with-detailed-profit-analysis-8126eecc1360, 2020. [Online; accessed December-2020].

- [20] Cheese bank. https://cheesebank.io/, 2020. [Online; accessed December-2020].

- [21] Cheese bank incident. https://peckshield.medium.com/cheese-bank-incident-root-cause-analysis-d076bf87a1e7, 2020. [Online; accessed December-2020].

- [22] Curve.fi y pool. https://curve.fi/iearn, 2020. [Online; accessed April-2020].

- [23] Defi pulse: Defi app rank list. https://defipulse.com/, 2020. [Online; accessed December-2020].

- [24] Dracula. https://dracula.sucks/, 2020. [Online; accessed December-2020].

- [25] Dracula protocol v2, the lastest commit id is 137186a9c06acb05d879df90faa62a63af48e712 at the time of writing. https://github.com/Dracula-Protocol/contracts-v2/blob/main/contracts/MasterVampire.sol, 2020. [Online; accessed March-2021].

- [26] Harvest finance attack. https://www.coindesk.com/harvest-finance-24m-attack-triggers-570m-bank-run-in-latest-defi-exploit, 2020. [Online; accessed December-2020].

- [27] Loopring. https://loopring.org/, 2020. [Online; accessed December-2020].

- [28] Opyn incident. https://peckshield.medium.com/opyn-hacks-root-cause-analysis-c65f3fe249db, 2020. [Online; accessed December-2020].

- [29] Origin incident. https://peckshield.medium.com/origin-dollar-incident-root-cause-analysis-f27e11988c90, 2020. [Online; accessed December-2020].

- [30] Pickle incident. https://peckshield.medium.com/pickle-incident-root-cause-analysis-5d73496ebc9f, 2020. [Online; accessed December-2020].

- [31] Plouto finance. http://plouto.finance/, 2020. [Online; accessed Jan-2021].

- [32] Seal finance. https://seal.finance/, 2020. [Online; accessed December-2020].

- [33] tornado cash. https://tornado.cash/, 2020. [Online; accessed Jan-2021].

- [34] Transaction decoder. https://ethtx.info/, 2020. [Online; accessed Jan-2021].

- [35] Uniswap v2. https://uniswap.org/, 2020. [Online; accessed December-2020].

- [36] Uniswap/lendf.me hacks. https://peckshield.medium.com/uniswap-lendf-me-hacks-root-cause-and-loss-analysis-50f3263dcc09, 2020. [Online; accessed December-2020].

- [37] Value defi. https://valuedefi.io/, 2020. [Online; accessed December-2020].

- [38] Value defi incident. https://peckshield.medium.com/value-defi-incident-root-cause-analysis-fbab71faf373, 2020. [Online; accessed December-2020].

- [39] Warp finance. https://warp.finance/, 2020. [Online; accessed December-2020].

- [40] Warpfinance incident. https://peckshield.medium.com/warpfinance-incident-root-cause-analysis-581a4869ee00, 2020. [Online; accessed December-2020].

- [41] Coindesk: What is a flash loan? https://www.coindesk.com/what-is-a-flash-loan, 2021. [Online; accessed April-2021].

- [42] Wikipedia: cash flow. https://en.wikipedia.org/wiki/Cash_flow, 2021. [Online; accessed April-2021].

- [43] Massimo Bartoletti, James Hsin-yu Chiang, and Alberto Lluch-Lafuente. Sok: Lending pools in decentralized finance. arXiv preprint arXiv:2012.13230, 2020.

- [44] Yixin Cao, Chuanwei Zou, and Xianfeng Cheng. Flashot: A snapshot of flash loan attack on defi ecosystem. arXiv preprint arXiv:2102.00626, 2021.

- [45] Ting Chen, Rong Cao, Ting Li, Xiapu Luo, Guofei Gu, Yufei Zhang, Zhou Liao, Hang Zhu, Gang Chen, Zheyuan He, et al. Soda: A generic online detection framework for smart contracts. In 27th Ann. Network and Distributed Systems Security Symp. The Internet Society, 2020.

- [46] Jeremy Clark, Didem Demirag, and Seyedehmahsa Mahsa Moosavi. Sok: Demystifying stablecoins. Communications of the ACM, Forthcoming, 2019.

- [47] Philip Daian, Steven Goldfeder, Tyler Kell, Yunqi Li, Xueyuan Zhao, Iddo Bentov, Lorenz Breidenbach, and Ari Juels. Flash boys 2.0: Frontrunning in decentralized exchanges, miner extractable value, and consensus instability. In 2020 IEEE Symposium on Security and Privacy (SP), pages 910–927. IEEE, 2020.

- [48] Shayan Eskandari, Seyedehmahsa Moosavi, and Jeremy Clark. Sok: Transparent dishonesty: front-running attacks on blockchain. In International Conference on Financial Cryptography and Data Security, pages 170–189. Springer, 2019.

- [49] Christof Ferreira Torres, Mathis Baden, Robert Norvill, Beltran Borja Fiz Pontiveros, Hugo Jonker, and Sjouke Mauw. Ægis: Shielding vulnerable smart contracts against attacks. In Proceedings of the 15th ACM Asia Conference on Computer and Communications Security, pages 584–597, 2020.

- [50] Shelly Grossman, Ittai Abraham, Guy Golan-Gueta, Yan Michalevsky, Noam Rinetzky, Mooly Sagiv, and Yoni Zohar. Online detection of effectively callback free objects with applications to smart contracts. Proceedings of the ACM on Programming Languages, 2(POPL):1–28, 2017.

- [51] Lewis Gudgeon, Daniel Perez, Dominik Harz, Arthur Gervais, and Benjamin Livshits. The decentralized financial crisis: Attacking defi. arXiv preprint arXiv:2002.08099, 2020.

- [52] Jingxuan He, Mislav Balunović, Nodar Ambroladze, Petar Tsankov, and Martin Vechev. Learning to fuzz from symbolic execution with application to smart contracts. In Proceedings of the 2019 ACM SIGSAC Conference on Computer and Communications Security, pages 531–548, 2019.

- [53] Bo Jiang, Ye Liu, and WK Chan. Contractfuzzer: Fuzzing smart contracts for vulnerability detection. In 2018 33rd IEEE/ACM International Conference on Automated Software Engineering (ASE), pages 259–269. IEEE, 2018.

- [54] Sukrit Kalra, Seep Goel, Mohan Dhawan, and Subodh Sharma. Zeus: Analyzing safety of smart contracts. In Ndss, pages 1–12, 2018.

- [55] Josh Kamps and Bennett Kleinberg. To the moon: defining and detecting cryptocurrency pump-and-dumps. Crime Science, 7(1):1–18, 2018.

- [56] Bowen Liu and Pawel Szalachowski. A first look into defi oracles. arXiv preprint arXiv:2005.04377, 2020.

- [57] Loi Luu, Duc-Hiep Chu, Hrishi Olickel, Prateek Saxena, and Aquinas Hobor. Making smart contracts smarter. In Proceedings of the 2016 ACM SIGSAC conference on computer and communications security, pages 254–269, 2016.

- [58] Amani Moin, Emin Gün Sirer, and Kevin Sekniqi. A classification framework for stablecoin designs. arXiv preprint arXiv:1910.10098, 2019.

- [59] Daniel Perez, Sam M Werner, Jiahua Xu, and Benjamin Livshits. Liquidations: Defi on a knife-edge. arXiv preprint arXiv:2009.13235, 2020.

- [60] Ingolf GA Pernice, Sebastian Henningsen, Roman Proskalovich, Martin Florian, Hermann Elendner, and Björn Scheuermann. Monetary stabilization in cryptocurrencies–design approaches and open questions. In 2019 Crypto Valley Conference on Blockchain Technology (CVCBT), pages 47–59. IEEE, 2019.

- [61] Kaihua Qin, Liyi Zhou, Benjamin Livshits, and Arthur Gervais. Attacking the defi ecosystem with flash loans for fun and profit. arXiv preprint arXiv:2003.03810, 2020.

- [62] Michael Rodler, Wenting Li, Ghassan O Karame, and Lucas Davi. Sereum: Protecting existing smart contracts against re-entrancy attacks. arXiv preprint arXiv:1812.05934, 2018.

- [63] Clara Schneidewind, Ilya Grishchenko, Markus Scherer, and Matteo Maffei. ethor: Practical and provably sound static analysis of ethereum smart contracts. In Proceedings of the 2020 ACM SIGSAC Conference on Computer and Communications Security, pages 621–640, 2020.

- [64] Christof Ferreira Torres, Julian Schütte, and Radu State. Osiris: Hunting for integer bugs in ethereum smart contracts. In Proceedings of the 34th Annual Computer Security Applications Conference, pages 664–676, 2018.

- [65] Petar Tsankov, Andrei Dan, Dana Drachsler-Cohen, Arthur Gervais, Florian Buenzli, and Martin Vechev. Securify: Practical security analysis of smart contracts. In Proceedings of the 2018 ACM SIGSAC Conference on Computer and Communications Security, pages 67–82, 2018.

- [66] Bin Wang, Han Liu, Chao Liu, Zhiqiang Yang, Qian Ren, Huixuan Zheng, and Hong Lei. Blockeye: Hunting for defi attacks on blockchain. arXiv preprint arXiv:2103.02873, 2021.

- [67] Dabao Wang, Siwei Wu, Ziling Lin, Lei Wu, Xingliang Yuan, Yajin Zhou, Haoyu Wang, and Kui Ren. Towards understanding flash loan and its applications in defi ecosystem. arXiv preprint arXiv:2010.12252, 2020.

- [68] Yongge Wang. Automated market makers for decentralized finance (defi). arXiv preprint arXiv:2009.01676, 2020.

- [69] Sam M Werner, Daniel Perez, Lewis Gudgeon, Ariah Klages-Mundt, Dominik Harz, and William J Knottenbelt. Sok: Decentralized finance (defi). arXiv preprint arXiv:2101.08778, 2021.

- [70] Lei Wu, S. Wu, Yajin Zhou, Runhuai Li, Zongguo Wang, X. Luo, C. Wang, and K. Ren. Time-travel investigation: Towards building a scalable attack detection framework on ethereum. arXiv: Cryptography and Security, 2020.

- [71] Valentin Wüstholz and Maria Christakis. Harvey: A greybox fuzzer for smart contracts. In Proceedings of the 28th ACM Joint Meeting on European Software Engineering Conference and Symposium on the Foundations of Software Engineering, pages 1398–1409, 2020.

- [72] Jiahua Xu and Benjamin Livshits. The anatomy of a cryptocurrency pump-and-dump scheme. In 28th USENIX Security Symposium (USENIX Security 19), pages 1609–1625, 2019.

- [73] Mengya Zhang, Xiaokuan Zhang, Yinqian Zhang, and Zhiqiang Lin. TXSPECTOR: Uncovering attacks in ethereum from transactions. In 29th USENIX Security Symposium (USENIX Security 20), pages 2775–2792, 2020.

- [74] Liyi Zhou, Kaihua Qin, Antoine Cully, Benjamin Livshits, and Arthur Gervais. On the just-in-time discovery of profit-generating transactions in defi protocols. arXiv preprint arXiv:2103.02228, 2021.

- [75] Liyi Zhou, Kaihua Qin, Christof Ferreira Torres, Duc V Le, and Arthur Gervais. High-frequency trading on decentralized on-chain exchanges, 2020.