The Raise Regression: Justification, properties and application

Abstract

Multicollinearity produces an inflation in the variance of the Ordinary Least Squares estimators due to the correlation between two or more independent variables (including the constant term). A widely applied solution is to estimate with penalized estimators (such as the ridge estimator, the Liu estimator, etc.) which exchange the mean square error by the bias. Although the variance diminishes with these procedures, all seems to indicate that the inference is lost and also the goodness of fit. Alternatively, the raise regression (Garcia et al. (2011) and Salmerón et al. (2017)) allows the mitigation of the problems generated by multicollinearity but without losing the inference and keeping the coefficient of determination. This paper completely formalizes the raise estimator summarizing all the previous contributions: its mean square error, the variance inflation factor, the condition number, the adequate selection of the variable to be raised, the successive raising and the relation between the raise and the ridge estimator. As a novelty, it is also presented the estimation method, the relation between the raise and the residualization, it is analyzed the norm of the estimator and the behaviour of the individual and joint significance test and the behaviour of the mean square error and the coefficient of variation. The usefulness of the raise regression as alternative to mitigate the multicollinearity is illustrated with two empirical applications.

Keywords: multicolinearity, raise regression, estimation, inference, detection, variance inflation factor, mean square error.

1 Introduction

The presence of collinearity between independent variables in a regression models leads to serious problems with the ordinary least squares (OLS) estimator which becomes unstable. According to Willan and Watts (1978), the multicollinearity produces “inflated variances and covariances, inflated correlations, inflated prediction variances and the concomitant difficulties in interpreting the significance values and confidence regions for parameter”.

The ridge estimation is an early answer to the problem of estimating a model with collinearity. The solution of the normal equations is an algebraic problem within the numerical analysis and, for this reason, the beginnings of ridge estimator could be found in the numerical analysis. Following OM (2001) and Singh (2011), the first antecedent is found in the Tikhonov regularization (TR), which is one of the most widely applied techniques to solve the problem of a ill-conditioning matrix. OM (2001) concluded that the TR applied in numerical analysis has been presented in statistics and econometrics as ridge regression (RR) and, in some way, he claimed for Tikhonov the merit of the ridge regression due to he presented its regularization in 1943 while ridge regression was formally presented by Hoerl and Kennard (1970a) and Hoerl and Kennard (1970b).

However, one question is to solve a system of equations with an ill-conditioning matrix and another question is to find an estimator for a vector of parameters in a lineal model. It is clear than an estimator is an expression that can be obtained from resolving a system of equations but an estimator must verify also some characteristics as being a random variable and allow the obtention of inference from it. Thus, while the numerical analysis focus on the resolution of a system of equation, the statistic and the econometric are focus on the qualities and properties of the estimator since an estimator should be accompanied by the possibility of doing inference and prediction which are the main reasons for its estimation.

Several authors consider that the origin of ridge regression is found on the paper presented by Levenberg (1944) where the increase of matrix are presented for the first time, see Piegorsch and Casella (1989). Marquardt (1963) developed a procedure to Levenberg but without express knowledge of it. Riley (1955) is the first that applied the expression and showed that the matrix is better conditioned than the matrix . Marquardt (1963) and Hoerl (1962) showed that to invert matrix is easier than to invert matrix . Despite of this fact, the most of the references attribute the ridge estimator to Hoerl and Kennard (1970a) and Hoerl and Kennard (1970b), who proposed the ridge estimator for a linear model where with the following expression:

| (1) |

being a biased estimator that coincides to ordinary least squares (OLS) when . These papers formalized the ridge estimator and showed that it verifies the mean squared error (MSE) admissibility condition assuring an improvement in MSE to OLS for some . Thus, this estimator provided a solution to the problems indicated by Willan and Watts (1978).

Regardless of the (always post-hoc) theoretical justification for the introduction of the values of in the main diagonal of matrix , the ridge estimator and, in general, the constrained estimators present problems with the measure of goodness of fit and with the inference. These problems appear due to the introduction of the value (a non deterministic value) which impedes the verification of the traditional sum of squares decomposition (see, for more detail, Salmerón et al. (2020)).

In relation to this problem, Hoerl and W. Kennard (1990) indicated: “It appears to be common practice with ridge regression to obtain a decomposition of the total sum of squares, and assign degrees of freedom according to established least squared theory” emphasising the mistake of this practice. These authors presented a descomposition for the variance analysis concluding that “In any case, Obenchain (1977) has shown that is no unique exact F tests possible with non stochastic ridge estimators”. Formerly, Schmidt (1976) (p. 53) indicated that the ridge regression (RR) may not be useful to econometricians because the underdeveloped theory of hypothesis testing with RR limits its utility. He may be the first author who questioned the inference in ridge regression.

It seems to be appropriate to ponder the wide success of the ridge estimator endorsed by numerous references in the scientific literature in empirical and theoretical fields. Certainly, the ridge regression allows to overpass the problems indicated by Willan and Watts (1978), but in exchange for this, is the inference lost? In this line, it is interesting to comment the paper by Smith and Campbell (1980) entitled “A Critique of Some Ridge Regression Methods” which was included together to the comments and the final answer in the paper 496 of Cowles Fundation Papers. This document collects different criticism to the ridge estimator in relation to its bayesian version, the lack of invariance to scale changes and the problems with inference on which we focus now.

The first paper that addresses in depth the problem of inference is the one of Obenchain (1977) who provided a rigorous analysis of hypothesis testing and confidence interval construction in a (generalized) ridge regression when the shrinkage factor is deterministic. The abstract of this paper indicates “testing general linear hypotheses in multiple regression models, it is shown that non-stochastically shrunken ridge estimators yield the same central F-ratios and t-statistics as does the least squares estimator”. From this statement we raise the following question: What is the relation between these results with the inference in OLS?. On the other hand, we also consider that the assumption that the shrinkage is non-stochastic excessively limits the applicability of the results.

By following Obenchain (1977), other authors such as Coutsourides et al. (1979) insisted in the results of Obenchain (1977) and extend them (with the same restrictions) to the RR, principal components (PC) and Shrunken Estimators (SH) yield the same central t and F statistics as the OLS estimator. They concluded that “It is important to point out that confidence intervals which are centred at biased estimators have greater maximum diameter that the least squares interval of the same confidence”. We raise another question: if the interval for the biased estimator have a greater diameter, then the tendency (in presence of multicollinearity) to not reject the null hypothesis of individual significance test () while the null hypothesis of the joint significance test is rejected, will be even higher and, then, the application of the ridge estimation makes not statistical sense due to we only have stabilized the estimation but we have not obtained a model which overpass the validation step. On the other hand, the restrictions about the parameter will be the same: it will be not stochastic as stated by Thisted (1980) in the comment to the paper of Smith and Campbell (1980), when indicated that the authors “completely disregarded some of the most promising aspect of the ridge regression such as the adaptive estimation of ”. Stahlecker and Schmidt (1996) also extended the work presented by Obenchain (1977) to a more wide range of estimators that content the ridge estimator as a particular case, but keeping the deterministic hypothesis of . Hoerl and W. Kennard (1990) had already indicated the problem of the sum of squares descomposition which is common to all the penalized estimator such as the Lasso and the elastic net apart from the ridge regression. Vinod (1987) dedicated a full chapter to present the confidence intervals for the ridge estimator concluding that, if the economist wishes to use a confidence interval focused on the ridge estimator, three possibilities exist: the approximate Bayes, bootstrapping, those based on Stein (1981) unbiased estimate of the mean squared error (MSE) of a biased estimator of multivariate normal mean and the bootstrap. Van Nostrand (1980), in other comment to the paper of Smith and Campbell (1980), goes even further and points in relation to inference that “It must be emphasized that these condition are commonly not met; in particular, is usually stochastic and not fixed” supporting this statement in the papers of McDonald and Galarneau (1975), Bingham and Larntz (1977) and in its own analysis of the study of Lawless (1978), that according to Van Nostrand (1980) seem to indicate it roughly holds for stochastically chosen . Also see Thisted (1976).

The inference of the ridge regression is still a debatable and controversial question. Thus, Halawa and El Bassiouni (2000) indicated that there are numerous works in relation to the obtention of the ridge estimator, but few works focused on the individual or joint inference of the parameters, citing among others Obenchain (1977), Coutsourides et al. (1979), Ullah et al. (1984), Ohtani (1985) and cited the sum of squares decomposition of Hoerl and W. Kennard (1990) and the degree of freedom for the analysis of the variance. Halawa and El Bassiouni (2000) investigated two non-exact, ridge-based, type tests, for a certain values of checked with simulations. Monarrez et al. (2007) says to establish the conditions required to get that the central t-Student distribution applied in OLS will be also applicable in ridge regression but it may receive the same criticism and limitations than previous. Bae et al. (2014) derive a test statistic for the general linear test in the RR model. The exact distribution for the test statistic is too difficult to derive; therefore, they suggest an approximate reference distribution and used numerical studies to verify that the suggested distribution for the test statistic is appropriate. Gökpınar and Ebegil (2016), by following Halawa and El Bassiouni (2000) investigate others popular values used the RR for testing significance of regression coefficient and compare tests in terms of type I error rates and powers by using Monte Carlo simulation. Sengupta and Sowell (2020) presented another recent attempt within the field of the inference in ridge regression characterizing the asymptotic distribution of the ridge estimation when the adjustment parameter is selected with a test sample. Finally, we want to consider the work of Vanhove (2020) entitled “Collinearity isn’t a disease that needs curing”, where the lack of inference in ridge estimator is considered as an argument against the treatment of the multicollinearity, based on the recent paper presented by Goeman et al. (2018).

Certainly, the multicollinearity produces an inflation in the variance due to the correlation between two or more independent variables (constant term included), but when the problem is treated applying penalized estimator, the mean squared error is exchanged by biased. Additionally, although the variance is diminished, all seems to indicate that the inference is lost and, not only that, but also the goodness of fit is lost since the coefficient of determination makes no sense at least in its traditional form.

It is difficult to understand how being the inference of ridge regression questioned and despite of the numerous paper published in relation to ridge estimator, only a few of them are focused on the inference. Indeed, there are not much more works in relation to inference in ridge regression that the ones cited in this paper that all found its origin in the work of Obenchain (1977). It is possible that the problem of inference in ridge regression has no solution and this fact motivate the formalization of the raise regression as a possible alternative.

The raise estimator allows, as the penalized estimator, mitigate the problems indicated by Willan and Watts (1978) but without losing the inference and keeping the coefficient of determination, not only the same value of the OLS regression but also its statistical interpretation due to the sum of squares is verified after the application of the raise estimator. In addition, the basis in which the raise estimator is founded lead, in a natural way, to the inclusion of the values of in the main diagonal of matrix without being necessary any other justification. Indeed, recently García-Pérez et al. (2020) showed that the ridge estimator is a particular case of the raise estimator or the raising procedures where this estimator founds its origin. Ultimately, the goal of this paper is to present a global vision of the raising procedure, making new contributions to this technique and summarizing those already carried out in previous works (in order to have a better understanding of this technique). In addition, the procedure is performed for any number of regressors and establishing relationships with OLS and residualization, the latter technique also applied when there is a worrying degree of multicollinearity (see García et al. (2020) for more details).

The structure of the paper is as follows: Section 2 presents as a novelty the generalization of its estimation and the relation between the raise regression with the ordinary least squares and with residualization. It is also presented originally its goodness of fit, global characteristics and individual inference. This section also includes a review about previous results in relation to the mean square error of the raise regression. Section 3 presents as a novelty the norm of the raised estimator, the variance of the estimators and it is shown that the raise regression is able to mitigate not only the essential multicollinearity but also the non-essential one (due to its coefficient of variation increases when the raise regression is applied) together to a summary of how to obtain the Variance Inflation Factors and the Condition Number. Section 4 proposes some criteria, some of them also presented in an original way, to select the variable to be raised that can be applied individually or as a combination. Due to the Variance Inflation Factor and the Condition Number presents lower bound in raise regression, it is possible that may not exist a raising factor that get the enough mitigation of the multicollinearity. In this case, it is possible to apply a successive raise regression that is summarized in Section 5. Section 6 compares, also as a novelty, the OLS, the raise and the ridge estimators under the criteria of MSE and also summarizes the contribution of García-Pérez et al. (2020) who conclude that the ridge estimator is a particular case of the raising procedures. The usefulness of the raise estimator is illustrated with two empirical applications in Section 7. Finally, Section 8 summarizes the main contributions of this paper.

2 Raise regression

This section analyze the raise regression presenting as a novelty, for any value of , its estimation, goodness of fit, global characteristics and individual inference. In all cases, it is also analyze its relation with the OLS estimator of the initial model and with the residualization (see, for more details about this technique, García et al. (2020)). Due to the estimators obtained with this methodology are biased, it will be interesting to analyzed its Mean Square Error (MSE). Thus, it will be also summarized the results showed by Salmerón et al. (2020) in relation to MSE.

2.1 Estimation

Considering the multiple linear regression model for independent variables and observations:

| (2) |

being a vector containing the observations of the dependent variable, is a matrix with order that contains (by columns) the observations of the independent variables (where is a vector of ones with dimension and , with , is the results of eliminating the column of matrix ), is a vector that contains the coefficient of the independent variables and is a vector that represents the random disturbance, which is supposed to be spherical (it is to say, and where is a vector of zeros with dimension and the identity matrix of adequate dimensions ).

Considering the residuals, , of the auxiliary regression of the dependent variable , with , as a function of the rest of the independent variables of the model (2):

| (3) |

the variable is raised as with (called raising factor) and verifying111 In addition, due to is verified that: where was used that that .

In this case, the raise regression consists in the estimation by OLS of the following model:

| (4) |

where and is a random disturbance which is also supposed to be spherical. The OLS estimator of the model (4) will be given by:

| (9) | |||||

| (14) | |||||

| (19) |

being the sum of squares of residuals (SSR) of model (3), are the estimator of the coefficients associated to the non altered variables in and is the coefficient of the raise variable .

Taking into account the Appendix C, that summarizes the residualization formally developed in García et al. (2020), it is possible to conclude that:

-

•

For , the estimation of the not altered variables coincide to the estimation obtained with orthogonal variables:

-

•

For , the estimation of the raise variable tends to zero: .

Finally, taking into account that, for , it is obtained that:

and, consequently, the matrix of expression (4) can be written as where:

| (20) |

Thus, we have that:

and then the estimator of obtained from (4) is biased unless , which only occurs when . It is to say, when the raise regression coincides to the ordinary least square regression.

2.2 Mean Square Error

Since is a biased estimator of when , it will be interesting to obtain its mean square error (MSE). From Salmerón et al. (2020) the MSE for raise regression is given by:

| (21) |

where and .

Once it is obtained the estimations of and from model (2) by OLS, minimizes MSE and it is verified that . That is, it is always possible to obtain a value for that verifies that it has an associated MSE less than that of OLS.

Also, if it is obtained that for all . That is, it is always verified that the MSE of the raised is less than that of the OLS. If , then for .

2.3 Goodness of fit and global characteristics

To analyze the goodness of fit of model (4), its residuals are obtained from the following expression:

| (25) |

Taking into account the results included in Appendix A, it is obtained that . It is to say, the residuals of initial (2) and raised (4) models coincide. It that case it is possible to conclude that:

-

•

It is evident that the sum of squares of residual also coincide and, consequently, both models provide the same estimation for the variance of the random disturbance: .

-

•

Since the explained variable is the same in both models, the sum of total squares coincide and, consequently, the coefficient of determination of both models is also the same: .

-

•

Since the statistic of the test of joint signification can be expressed as a function of the coefficient of determination, it is evident that the joint signification of both models coincide: .

-

•

These global characteristics (estimated variance of the random disturbance, the coefficient of determination and the statistic of the joint significance test) coincide also to the residualization (see Appendix C).

-

•

Since the observed values are the same, both models provide the same estimations for the dependent variable. Thus, when this technique is applied, the estimations are not modified while the degree of multicollinearity is mitigated as will be show in section 3.

2.4 Individual inference

In relation to the individual inference of model (4), taking into account (see Appendix B) that:

| (26) |

the null hypothesis , with , is rejected (in favor of the alternative hypothesis ) when:

| (27) |

where is the value of a t-student distribution with degree of freedom that accumulate to its let a probability of and is the OLS estimation of the variance of the random disturbance of initial model (2) that, as previously commented, coincide to the one of the raised model (4).

Taking into account Appendix A, it is obtained that . It is to say, the individual inference of the raised variable is unaltered.

At the same time, the null hypothesis is rejected (in favor of the alternative hypothesis ) when:

| (28) |

where and are the elements (,) of matrices and , respectively. Note that is the element of with .

To summarize, the inference of the non raised variables changes as the raising factor varies. Salmerón et al. (2017) presents a simulation for where supposing a sample size equal to 20, it is concluded that in more than in the 50% of the cases the null hypothesis is rejected. In addition, this percentage increases as the size of the sample increases reaching almost the 84% for . This fact is due to the effect that the sample size has on the variance of the estimated variables (see O’brien (2007) for more details).

Finally, taking into account the Appendix C, it is obtained that:

it is to say, for the inference of the non raised variables is the same in the raise and residualization.

3 Multicollinearity

Originally, the raise regression appears with the goal of estimating multiple linear regression models with worrying multicollinearity. Thus, its application should mitigate the multicollinearity.

To check if this goal is reached, this section analyze as a novelty for any value of , the norm of its estimations, the variance of the estimators and the usefulness of the raise regression to mitigate the essential and non-essential multicollinearity.

This section also summarizes the results presented by Garcia et al. (2011), García-Pérez et al. (2020), Salmerón et al. (2020), Roldán López De Hierro et al. (2018) and De Hierro et al. (2020) that adapted the Variance Inflation Factor and the Condition Number, traditionally applied to measure the degree of multicollinearity, to be used after the application of the raise regression.

3.1 Estimator norm

As known, one of the consequences of strong multicollinearity is the instability of the estimated coefficients. For this reason, it will be interesting to analyze the norm222If , then . That is, . of the raise estimator (expression (19)) in order to analyze if there is a value of the raising factor that stabilize the norm of the estimator analogously to that presented in Hoerl and Kennard (1970b) and Hoerl and Kennard (1970a) for the ridge estimation.

Thus, from expression (19) it is obtained that:

| (29) | |||||

From expression (29) it is obtained that:

It is to say, the norm of the raise estimator presents a horizonal asymptote (that coincides to the one of the estimations of the non-residualizated variables in residualization). Thus, there must be a raising factor for which the norm of the estimator is stabilized.

3.2 Estimated variance

Another symptom of multicollinearity in a multiple linear regression model is the inflation of the variance of the estimated parameters. This subsection analyzes the effect of the raised regression on these variances.

Thus, by comparing the elements of the main diagonal of expressions (26) and (51) it is obtained that both coincide when and the first diminish as the value of increases. Then, the raised regression diminishes the variances of the estimated coefficients which are supposed to be inflated as a consequence of the multicollinearity. This fact shows the usefulness of this technique to mitigate the multicollinearity.

In addition, taking into account the expression of included in expression (59), it is observed that for the elements of the main diagonal of (26) for the non-raised variables coincide to the one of . Once again, it is showed the asymptotic relation between the raise and the residualization technique.

3.3 Variance Inflation Factor

Given the model (2), the Variance Inflation Factor (VIF) is obtained as:

| (30) |

where is the coefficient of determination of auxiliary regression (3). If the variable has not linear relation (it is orthogonal) with the rest of independent variables, it is obtained that and then . Thus, the (and consequently the ) increases as the relation between the variables is stronger. Then, the higher the value of the VIF associated to the variable the higher the linear relation between this variable and the rest of the independent variables of the model (2). For values of the VIF higher than 10, it is considered that the presence of multicollinearity is worrying (see, for example, Marquardt (1970) or Salmerón et al. (2018)).

Analogously, the VIF in the raise regression is given by:

| (31) |

where to calculate it is necessary to distinguish two cases depending of which will be the dependent variable of the auxiliary regression: a) if it is the raised variable, with , or b) if it is not the raised variable, with being .

Garcia et al. (2011) shows that the VIF associated to the raise variable diminishes as the raising factor increases, while García-Pérez et al. (2020) shows that the VIFs of the non-raised variables also diminish as the raising factor increases.

Finally, these results are completed with the contribution of Salmerón et al. (2020), where it is shown that the has the very desirable properties of a) being continuous ( with ), b) monotone in the raise parameter ( decrease if increase) and c) higher than one (, for and ). In addition, the following conditions are verified:

-

•

When , the VIF associated to the raised variable tends to one.

-

•

When , the VIFs associated to the not raised variables present a horizonal asymptote given by the VIF of the regression . Note that in this case, the limit of the VIF of the non raised variables coincide to the unaltered variables of the residualization (see Appendix C).

3.4 Condition Number

Given the model (2), the Condition Number (CN) is defined as:

| (32) |

where and are the maximum and the minimum eigenvalues of the matrix , respectively. Note that before calculating the eigenvalues of the matrix , it is necessary to transform it to present unit length columns. Values of CN between 20 and 30 indicate moderate multicollinearity while values higher than 30 indicate strong multicollinearity (see, for example, Belsley et al. (2005) or Salmerón et al. (2018)).

Analogously, the CN of the raise regression is given by the following expression:

| (33) |

where and are, respectively, the maximum and minimum eigenvalues of matrix .

Roldán López De Hierro et al. (2018) analyzed with detail the condition number for in the model (2) and standardizing the independent variables (subtracting its mean and dividing by the square root of times its variance). De Hierro et al. (2020) generalized these results for any value of and without transforming the variables obtaining that has the very desirable properties of a) being continuous (), b) monotone in the raise parameter ( decrease if increase) and c) higher than one ( for ) since when , presents a horizontal asymptote that coincide to the CN of the matrix . Note that in this case, the limit of the CN coincide to the CN of the residualization (see Appendix C).

3.5 Essential and non-essential multicollinearity

Marquardt and Snee (1975), Marquardt (1980) and Snee and Marquardt (1984) distinguished between essential and non-essential multicollinearity. The first one is the existence of a linear relation between the independent variables of model (2) excluding the intercept, while the second one is the linear relation between the intercept and at least one of the independent variables of the model. In Salmerón et al. (2020) is presented a definition of nonessential multicollinearity “that generalizes the definition given by Marquardt and Snee. Note that this generalization can be understood as a particular kind of essential multicollinearity: a near-linear relation between two independent variables with light variability. However, it is shown that this kind of multicollinearity is not detected by the VIF, and for this reason, we consider it more appropriate to include it within the nonessential multicollinearity”.

Salmerón et al. (2018) and Salmerón et al. (2019) showed that the VIF is only able to detect the essential multicollinearity. Therefore, from results of subsection 3.3 it is concluded that the raise regression mitigates this kind of multicollinearity. It is also possible to conclude that the raise regression mitigates the non-essential multicollinearity due to the CN also diminishes when the raise regression is applied (see subsection 3.4) being this measure able to detect both kind of multicollinearity. However, this question, that raise regression mitigates non-essential multicollinearity, is analyzed with more detail below.

Salmerón et al. (2019) showed that the most adequate measure to detect non-essential multicollinearity is the coefficient of variation (CV) of each one of the independent variables providing the following threshold: values of the coefficient of variation lower than 0.1002506 will indicate that the degree of non-essential multicollinearity is worrying. Thus, if it is shown that the coefficient of variance increases when the raise regression is applied, it will show that the raise regression mitigates the non-essential multicollinearity.

Indeed, taking into account that the for and that:

-

•

due to where is the estimation of obtained from the auxiliary regression (3) and, consequently, it is verified that , and

-

•

,

it is verified that:

In this case, since , then for .

4 Choice of variable to raise and the raise parameter

From the results of previous sections, the possible criteria to select the variable to be raised are enumerated:

-

•

To raise the variable whose parameter will be initially different from zero, taking into account that this characteristic will be maintained (see subsection 2.4).

-

•

If none estimated parameters are not individually significant, it is recommendable to raise the variable considered less important since the not raised coefficient variable (considered more relevant) can become individually significant after the application of the raise estimation (see subsection 2.4).

-

•

To raise the variable with the higher VIF (see subsection 3.3) since it limit tends to 1.

- •

-

•

To raise the variable with the lower CV (see subsection 3.5) since it will increase.

In relation to the criteria to select the raising factor we propose the following possibilities:

-

•

To select the value that minimizes the MSE or the one that provides a value of MSE lower than the one provided by OLS (see subsection 2.2).

-

•

To select the value that stabilize the norm of the raise estimator (see subsection 3.1).

-

•

To select, if it exists, the value that provides values for the VIF or the CN lower or for CV higher than the established thresholds to determine the existence of worrying multicollinearity.

To finish, note that the criteria to select the variable to be raised or the raising factor can be not only one of the previous proposals but a combination of them.

5 Successive raise

Section 3 showed that may not exist the raising factor that get the enough mitigation of the multicollinearity since the VIF and the CN present a lower bound. For this reason, it can be needed to raised more than one variable.

Garcia and Ramirez (2017) described the successive raise that we summarize here with the following steps:

- Step 1:

-

Raise the vector from the regression of with the resting vectors . From this auxiliary regression, it is we constructed the raise vector of , , as where is the residual vector of the auxiliary regression. Now, it is described a new space of vectors where is replaced by , .

- Step 2:

-

Raise the vector from the regression of with the resting vectors . From this auxiliary regression, it is we constructed the raise vector of , , as where is the residual vector of the auxiliary regression. Now, it is described a new space of vectors where is replaced by , .

- Step :

-

Raise the vector from the regression of with the resting vectors . From this auxiliary regression, it is we constructed the raise vector of , , as where is the residual vector of the auxiliary regression. Now, it is described a new space of vectors where is replaced by , .

- Step :

-

Raise the vector from the residual vector, , of the regression of with the set of vectors as . Finally, it is described a new space of vectors .

Note that when all the variables are raised, the VIFs and the CN tend to 1 and then it is assured that there is a value for the vector of raised parameter, , that makes the value of the VIFs and CN lower than the established thresholds assuming that the multicollinearity has been mitigated.

6 Relation between raise and ridge regression

In García-Pérez et al. (2020) it is justified the ridge regression from a geometrical perspective and it is also formally related with the raise regression. More concretely, that paper shows that ridge estimator, , is a particular case of raising procedures shown in that paper justifying the presence of the well-known constant on the main diagonal of matrix . This is to say, there is a combination of the vector of raised parameters , that verifies .

In this context, see Appendix D, from Proposition 3 it is possible to compare estimators , , under the criteria of the root mean square error matrix and MSE.

Proposition 1.

The successive raise estimator, where , is preferred to the OLS estimator, , under the root mean square error matrix criterion for values of that verify the following expression:

Proof.

By considering and , and only replacing and , it is possible to show . It is also verified that this matrix is positive definite (see Puntanen et al. (2011)). On the other hand, remembering that the inverse of the sum of two matrices and is defined as:

| (34) |

it is possible to show that:

Given that and are positive definite commutable matrices and is positive, then their product will be a positive definite matrix. Based on the result shown in Proposition 3, it is therefore possible to conclude that satisfies the MSE admissibility condition, thus ensuring an improvement in MSE for . ∎

Proposition 2.

The ridge estimator is preferred to the successive raise estimator, where , under the criteria of the root mean square error matrix for the values of that verify the following expression:

7 Empirical examples

To illustrate the empirical application of the raise regression, we consider two data sets. The first one is used to show the estimation of the raise regression and compare it with the ridge and residualization regressions. It is also shown that the raise and residualization regressions maintains all the global characteristics of the OLS regression while, at the same time, mitigate the multicollinearity. The second example is used to illustrate the usefulness of the raise regression to mitigate the non-essential multicollinearity.

7.1 Example 1: Portland cement dataset

The regression model for these data is defined as:

| (35) |

being the heat evolved after 180 days of curing measured in calories per gram of cement, the tricalcium aluminate, the tricalcium silicate, the tetracalcium aluminoferrite and the -dicalcium silicate.

This example is originally adopted by Woods et al. (1932) and also analyzed by, among others, Kaçiranlar et al. (1999), Li and Yang (2012) and, recently, by Lukman et al. (2019) and Kibria and Lukman (2020).

Table 1 presents the main measures in relation to the diagnose of multicollinearity: the correlation matrix of the variables, the coefficients of variation, the variance inflation factors obtained from OLS and the condition number (obtained from the matrix transformed to present unit length columns333Note that Kibria and Lukman (2020) obtained a condition number approximately equal to 424 directly dividing the maximum eigenvalue of the original data (44676.206) by the minimum eigenvalue of the original data (105.419) and with out calculate the square root. Kaçiranlar et al. (1999) obtained a condition number equal to 20.58 by using the original data and calculating the square root.). All these measures indicate the presence of a troubling degree of essential multicollinearity in this model.

| Y | |||||

| Y | 1.0000000 | 0.7307175 | 0.8162526 | -0.5346707 | -0.8213050 |

| 0.7307175 | 1.0000000 | 0.2285795 | -0.8241338 | -0.2454451 | |

| 0.8162526 | 0.2285795 | 1.0000000 | -0.1392424 | -0.9729550 | |

| -0.5346707 | -0.8241338 | -0.1392424 | 1.0000000 | 0.0295370 | |

| -0.8213050 | -0.2454451 | -0.9729550 | 0.0295370 | 1.0000000 | |

| VIF | 38.49621 | 254.42317 | 46.868399 | 282.5128 | |

| CV | 0.7574338 | 0.3104718 | 0.5228758 | 0.5360508 | |

| CN | 249.5783 |

Results of the estimation by OLS are provided in the first column of Table 2. Note that only the regression coefficient associated to variable is significant at the level of confidence of 90%. In contrast, the coefficient of determination is 98.24% and the model is globally significant at the level of confidence of 99%. In fact, Kaçiranlar et al. (1999) considers that this is an example of an “anti-quirk” due to it is verified that being the simple correlation between and with . This fact is also considered as a symptom of multicollinearity.

| OLS | RIDGE () | RIDGE () | RIDGE () | ||

|---|---|---|---|---|---|

| 62.4054 (70.071) | 8.5642 | 27.9917 | |||

| 1.5511 (0.7448)* | 2.1048 | 1.9051 | 1.6757 | ||

| 0.5102 (0.7238) | 1.0651 | 0.8648 | 1.8592 | ||

| 0.1019 (0.7547) | 0.6683 | 0.4640 | -1.211 | ||

| -0.1441 (0.7091) | 0.3998 | 0.2036 | -1.8771 | ||

| 0.9824 | |||||

| 111.5*** | |||||

| MSE | 4912.09 | 2991.8 | 2171.295 | 1711.66 |

Due to the existence of multicollinearity, Table 2 presents also the estimation by ridge regression with the value of proposed by Hoerl et al. (1975) () and the value of that minimizes the MSE (). The last column presents the estimation by ridge regression with standardized data with the value of that minimizes the MSE ().

| Raised | Variable | Variable | Variable | Variable |

|---|---|---|---|---|

| 1 | 3.6781 | 1.06633 | 3.2510 | |

| 24.3091 | 1 | 18.78031 | 1.06357 | |

| 1.298236 | 3.4596 | 1 | 3.1421 | |

| 23.8586 | 1.1810 | 18.9400 | 1 | |

| 61.01328 | 15.30453 | 51.51909 | 13.65739 | |

| 0.230547 | 2.01277 | 54.8438 | 24.2248 | |

| 4050.054 | 1645.21 | 308.5229 | 211.2751 |

Table 3 shows the horizontal asymptote for VIFs and CN after raising each variable and also the value of , the and the . In relation to the selection of the variable to be raised, note that:

-

•

When variable or are raised, there is an asymptote higher than 10 for the VIFs of variables and . However, the thresholds that would be obtained for VIFs by raising variables or are in all cases less than 10.

-

•

In relation to in all cases the value is higher than one except for the case when the second variable is raised. Note that when it is verified that for all . For this reason, and taking into account the asymptotic behaviour of the VIF, the variables more appropriate to be raised will be the variables and .

-

•

The value of is lower than 20 only when variables and are raised, and for this reason these variables could be preferred to be selected.

-

•

Note that is always less than the one obtained by OLS even for the variable where due to it is verified that . The lowest MSE is obtained when variable is raised.

However, with a methodological purpose Table 4 shows the results of the raise estimation raising each variable with its :

-

•

It is also possible to check that there is not non-essential multicollinearity has been mitigated although initially it was not worrisome, since the coefficient of variation of the raised variables, CV(), has increased.

-

•

It also obtained that the estimated variances of the estimated coefficients diminishes when raise regression is applied.

-

•

Raise regression provides results in relation to the inference of the model which allows to conclude that estimated coefficient of variable is not individually significant in any case, while estimated coefficient of variable is individually significant when variables and are raised. The estimated coefficient of variable is individually significant when variable is raised. Then, the raised models presents more estimated coefficients indvidually significant than the OLS estimation.

Taking into account the values obtained for the VIFs, CN, MSE and the improvement obtained in the individual significant test, the variable should be selected to be raised. However, over again with a illustrative purpose, the variables and will be raised with two alternatives for the selection of :

-

a)

Table 5 presents the raise estimation by using the value of that get that all VIFs will be lower than 10. Note that in this case we obtain MSE lower than the one of OLS and also lower than the ones obtained from ridge regression for and and for the one presented by Kibria and Lukman (2020) in Table 10 (MSE=2170,96), who uses this same example to illustrate a new Ridge-Type Estimator. However, the CN is higher than the established thresholds.

-

b)

Table 6 presents the raise estimation raising variable and by using the first value of that get that the CN will be lower than 20. Note that in both cases, the VIFs are lower than 4. In relation to MSE, the model obtained when raising variable presents a MSE higher than the one obtained for the value of that makes the VIF lower than 10 while the model obtained when raising variable presents a MSE lower than the one obtained for the value of than makes the VIF lower than 10. The conclusions obtained from these results will be very similar to the one obtained from results presented in Table 4.

Finally, Table 7 shows the estimation of the residualization when variables and are residualized. Note that the value of the coefficient of determination is the same than in OLS and raise regression while the MSE is much lower than the one obtained from OLS, ridge or raise regression. In all cases, the values for the VIFs and the CN are lower than the established thresholds. When variable is residualized, the estimated coefficient of variable becomes individually significant for a 90% level of confidence. However, when variable is residualized, the estimated coefficients of variables and are not individually significant. Note also that the coefficient of variation (CV) is very high (from a theoretical point of view should be infinite) and, consequently, the non-essential multicollinearity is being mitigated. However, despite of these results and following García et al. (2020) and García and Salmerón (2021) it is relevant to highlight that residualization should be applied only if the residualized variable is interpretable. Thus,

-

•

If the variable is residualized, its estimated coefficient is interpreted as the part of tricalcium silicate not related to the tricalcium aluminate, the tetracalcium aluminoferrite and the -dicalcium silicate.

-

•

If the variable is residualized, its estimated coefficient is interpreted as the part -dicalcium silicate not related to the tricalcium aluminate, the tricalcium silicate and the tetracalcium aluminoferrite.

In this case, it can be a very complicated task for non-experts in the field.

| Raised | Variable 2 | Variable 3 | Variable 4 | Variable 5 | ||||

|---|---|---|---|---|---|---|---|---|

| (=0.230547) | VIF | (=2.01277) | VIF | (=54.8438) | VIF | (=24.2248) | VIF | |

| 88.8665 | 95.3277 | 71.482793 | 48.7570 | |||||

| (57.8629) | (23.6760)*** | (15.0332)*** | (4.9829)*** | |||||

| 1.2605 | 25.762 | 1.2176 | 7.514 | 1.4537 | 1.078 | 1.6901 | 3.306 | |

| (0.6052)** | (0.3290)*** | (0.1246)*** | (0.2182)*** | |||||

| 0.2416 | 176.275 | 0.1693 | 28.92 | 0.4177 | 18.856 | 0.6510 | 1.462 | |

| (0.6025) | (0.2402) | (0.197041)** | (0.0548)*** | |||||

| -0.1885 | 31.393 | -0.2401 | 8.242 | 0.001825 | 1.015 | 0.2441 | 3.211 | |

| (0.6177) | (0.3165) | (0.013515) | (0.1975) | |||||

| -0.4088 | 194.673 | -0.4773 | 32.176 | -0.2348 | 19.025 | -0.0057 | 1.442 | |

| (0.5886) | (0.2393)** | (0.1840) | (0.0281) | |||||

| 0.9824 | 0.9824 | 0.9824 | 0.9824 | |||||

| 111.5*** | 111.5*** | 111.5*** | 111.5*** | |||||

| 4050.054 | 1645.21 | 308.5229 | 211.2751 | |||||

| 206.301 | 83.897 | 52.119 | 16.97 | |||||

| CV() | 0.79361 | 0.32824 | 4.4718 | 1.0056 |

| Raised | Variable 3 | Variable 5 | ||

|---|---|---|---|---|

| () | VIF | () | VIF | |

| 102.9625 | 50.7337 | |||

| (13.2350)*** | (13.16963)*** | |||

| 1.1402 | 4.768874 | 1.67 | 4.3769 | |

| (0.2621)*** | (0.2511)*** | |||

| 0.0903 | 8.9387 | 0.6307 | 9.1570 | |

| (0.1281) | (0.1373)*** | |||

| -0.3194 | 4.8194 | 0.22355 | 4.5389 | |

| (0.2420) | (0.23486) | |||

| -0.5545 | 9.9939 | -0.02575 | 9.9928 | |

| (0.1334)*** | (0.12673) | |||

| 0.9824 | 0.9824 | |||

| 111.5*** | 111.5*** | |||

| MSE | 1820.895 | 309.8762 | ||

| CN | 46.358 | 46.395 | ||

| CV() | 0.34222 | 0.58710 |

| Raised | Variable 3 | Variable 5 | ||

|---|---|---|---|---|

| () | VIF | () | VIF | |

| 109.27585 | 49.033075 | |||

| (5.8073)*** | (5.8489)*** | |||

| 1.07626 | 3.761 | 1.687338 | 3.374 | |

| (0.2328)*** | (0.22049)*** | |||

| 0.02493 | 1.605 | 0.648247 | 1.948 | |

| (0.03538) | (0.0063325)*** | |||

| -0.38502 | 3.563 | 0.241269 | 3.295 | |

| (0.20810) | (0.2001) | |||

| -0.618428 | 1.853 | -0.008509 | 1.982 | |

| (0.05743)*** | (0.041881) | |||

| 0.9824 | 0.9824 | |||

| 111.5*** | 111.5*** | |||

| MSE | 2231.592 | 213.198 | ||

| CN | 19.9942 | 19.99037 | ||

| CV() | 0.5252 | 0.79122 |

| Residualized | Variable 3 | VIF | Variable 5 | VIF |

|---|---|---|---|---|

| 111.684 | 48.1936 | |||

| (4.6956)*** | (4.14)*** | |||

| 1.05185 | 3.678 | 1.6959 | 3.251 | |

| (0.2302)*** | (0.2164)*** | |||

| 0.5101 | 1 | 0.6569 | 1.064 | |

| (0.72379) | (0.0468)*** | |||

| -0.41 | 3.46 | 0.25 | 3.142 | |

| (0.2050)* | (0.1954) | |||

| -0.6428 | 1.181 | -0.1441 | 1 | |

| (0.04584)*** | (0.7090) | |||

| 0.9824 | 0.9824 | |||

| 111.5*** | 111.5*** | |||

| MSE | 22.66984 | 17.72962 | ||

| CN | 15.305 | 13.657 | ||

| CV() | 3.56 | 7.25 |

7.2 Example 2: Euribor data

The following regression model presents an analysis of the Euribor (100%):

| (36) |

in relation to the Harmonized Index of Consumer Prices (100%) (), the Balance of Payments to net current account () in millions of euros and the Government Deficit to net non-finacial accounts () expressed in millions of euros. It is supposed that the random disturbance is centered, homoscedastic and uncorrelated. This dataset, previously used by Salmerón et al. (2019) and Salmerón et al. (2020), is composed by 47 Eurozone observations for the period January 2002 to July 2013 (quarterly and seasonally adjusted data).

Table 8 presents the main measures in relation to the diagnose of multicollinearity: the correlation matrix of the predictors, the coefficients of variation, the VIFs obtained from OLS and the CN (obtained from the matrix transformed to present unit length columns). Note that the coefficient of variation of the variable is equal to 0.07033 which is lower than the threshold 0.1002506 provided by Salmerón et al. (2019) to consider that the variable shows such a slight variability that it is highly related to the intercept provoking worrying non-essential multicollinearity. The existence of this king o f worrying multicollinearity is also suggested by the fact that the values of VIFs are lower than 10 while the CN is higher than 30. Remember that the VIF is not able to detect the non-essential multicollinearity contrary to what happens with the CN.

| 1 | 0.23129 | -0.4685 | |

| 0.23129 | 1 | -0.07033 | |

| -0.4685 | -0.07033 | 1 | |

| VIF | 1.351 | 1.059 | 1.285 |

| CV | 0.07033 | 4.38723 | -0.556102 |

| CN | 39.35375 |

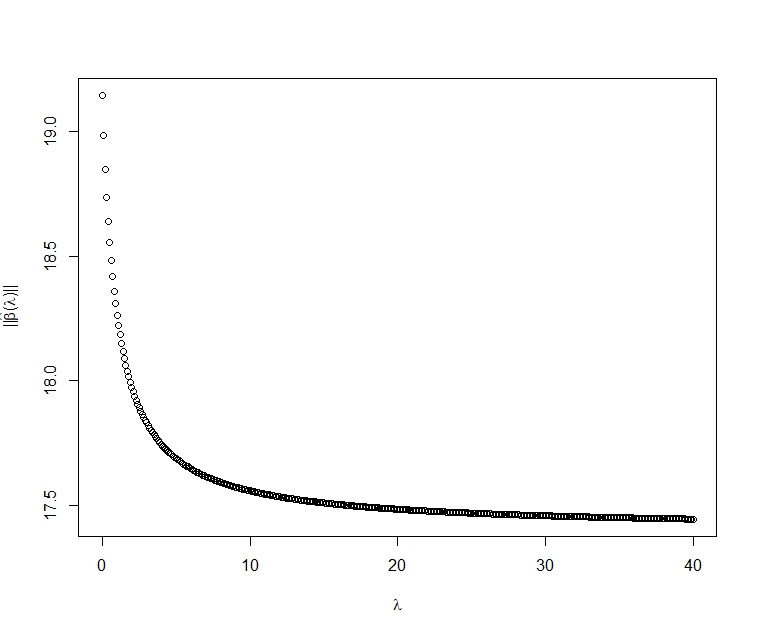

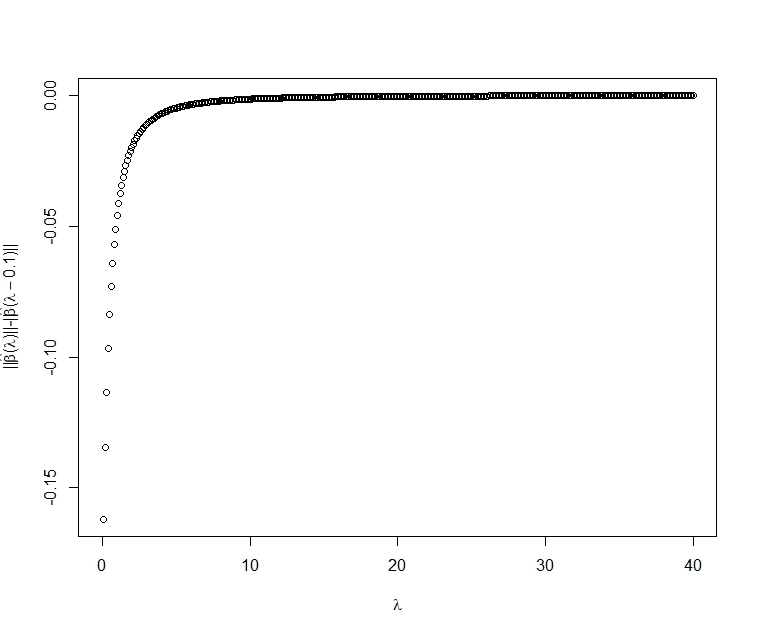

The traditional solution for the non-essential multicollinearity is to center the variable which was applied by Salmerón et al. (2019). Alternatively, it will be possible to apply the raise regression treating to minimizes the MSE and/or mitigate multicollinearity raising the variable that provoke it (in this case ). Table 9 presents the estimation by OLS (second column), the estimation raising the variable with the first value of that makes the CV higher than (third column), the first value of that provides a CN lower than 20 (fourth column). the value of that minimizes the mean square error (fifth column) and the value of that stabilizes the norm of the estimators (sixth column). Figure 1 shows the relation between and (varying between 0 and 40, with jumps of 0.1) and Figure 2 shows the difference between the norm of the estimators calculated for a given and for its immediately preceding one. That difference is lower than 0.001 from .

Note that the different models are similar in relation to individual inference and in all cases the VIFs are close to 1. In relation to MSE, when raising the variable with the value of that minimizes the MSE, the model provides a reduction of 95.7157% in the MSE in comparison with the MSE obtained by OLS. This reduction is also relevant (84.36%) when it is compared to the MSE, 0.4339, obtained by Salmerón et al. (2019) where the same model is estimated but centering variable . Note that the condition number is lower 20 under the criteria of minimising the MSE and the criteria of stabilizing the norm of the estimators. This last criteria requires a lower value for and also presents a reduction of the MSE very relevant (95.4661%).

| OLS | VIF | RAISE () | VIF | RAISE () | VIF | RAISE () | VIF | RAISE () | VIF | |

| 4.376 | ||||||||||

| (1.258)*** | ||||||||||

| 4.158 | 4.275 | 4.177 | 4.1870 | |||||||

| (0.1837)*** | (0.6509)*** | (0.1683)*** | (0.1902)*** | |||||||

| -0.002 | 1.35 | |||||||||

| (0.0126) | ||||||||||

| -0.002 | 1.146 | - 0.0010 | 1.089 | -5.38 | 1 | -0.0001563 | 1.002 | |||

| (0.013) | (0.00637) | (3.289) | (0.000956) | |||||||

| -3.647 | 1.059 | |||||||||

| (3.897 )*** | ||||||||||

| -3.647 | 1.027 | -3.655 | 1.019 | -3.661 | 1.005 | -3.6607 | 1.005 | |||

| (3.897 )*** | (-3.823)*** | (3.797)*** | (-3.797)*** | |||||||

| 1.971 | 1.284 | |||||||||

| (2.202)*** | ||||||||||

| 1.971 | 1.121 | 1.980 | 1.076 | 1.988 | 1.005 | 1.987 | 1.007 | |||

| (2.202 )*** | (2.016)*** | (1.948)*** | (1.950)*** | |||||||

| 0.8314 | 0.8314 | 0.8314 | 0.8314 | 0.8314 | ||||||

| 70.68*** | 70.68*** | 70.68*** | 70.68*** | 70.68*** | ||||||

| CN | 39.35375 | 25.471 | 19.99 | 4.2555 | 4.909 | |||||

| MSE | 1.582988 | 0.680108 | 0.4622 | 0.06782 | 0.07177 | |||||

| 19.14574 | 18.51747 | 18.27183 | 17.4464 | 17.5312 | ||||||

| CV() | 0.0703 | 0.1004 | 0.1251 | 2.3232 | 0.79991 |

8 Conclusions

Traditionally, penalized estimator (such as the ridge estimator, the Liu estimator, etc.) have been applied to estimate models with multicollinearity. These procedures exchange the mean square error by the bias and although the variance diminishes, the inference is lost and also the goodness of fit. Alternatively, the raise regression (Garcia et al. (2011) and Salmerón et al. (2017)) allows the mitigation of the problems generated by multicollinearity but without losing the inference and keeping the coefficient of determination.

This paper presents as novelty the generalization of the raise estimator for any numbers of regressors together to its estimation, goodness of fit, global characteristics and its individual inference. Anothers contributions are the development of the norm of the raised estimator, the analysis of the variance of the estimators, that the coefficient of variation increases when the raise regression is applied (and, as consequence, the raise regression is able to mitigate not only the essential multicollinearity but also the non-essential one) and complete some criteria to select the variable to be raised and the raising factor that can be applied individually or as a combination. An interesting conclusion is the relation between the raise regression with the ordinary least squares and with the residualization. Finally, the paper also present a comparison between the OLS, the raise and the ridge estimators under the criteria of MSE supporting the contribution of García-Pérez et al. (2020) who conclude that the ridge estimator is a particular case of the raising procedures.

Apart from these contributions, with the aim of having a complete vision of the technique, the paper also reviews some previous results in relation to the Mean Square Error, the Variance Inflation Factor, the Condition Number and the successive raise.

In conclusion, this paper contributes with the development of the raise regression with the goal of extend is application in many different fields where collinearity exists and ridge estimator is systematically applied without taking into consideration its lack of inference. Note that raise regression may mitigate essential and non-essential multicollinearity, maintaining the main characteristic of the original model and allowing the inference.

Acknowledgements

This work has been supported by project PP2019-EI-02 of the University of Granada, Spain.

References

- Bae et al. (2014) Bae, W. S., M. J. Kim, and C. G. Kim (2014). The general linear test in the ridge regression. Communications for Statistical Applications and Methods 21(4), 297–307.

- Belsley et al. (2005) Belsley, D. A., E. Kuh, and R. E. Welsch (2005). Regression diagnostics: Identifying influential data and sources of collinearity, Volume 571. John Wiley & Sons.

- Bingham and Larntz (1977) Bingham, C. and K. Larntz (1977). A simulation study of alternatives to ordinary least squares: Comment. Journal of the American Statistical Association 72(357), 97–102.

- Coutsourides et al. (1979) Coutsourides, E. et al. (1979). F and t tests for a general class of estimators. South African Statistical Journal 13(2), 113–119.

- De Hierro et al. (2020) De Hierro, A. R. L., C. García, and R. Salmerón (2020). Analysis of the condition number in the raise regression. Communications in Statistics-Theory and Methods, 1–16.

- Farebrother (1976) Farebrother, R. (1976). Further results on the mean square error of ridge regression. Journal of the Royal Statistical Society. Series B (Methodological), 248–250.

- García and Salmerón (2021) García, C. B. and R. Salmerón (2021). Discussion on residualization and the enlarging of the sample to address multicollinearity. Journal of Research Methods for the Behavioral and Social Sciences. In revision..

- García et al. (2020) García, C. B., R. Salmerón, C. García, and J. García (2020). Residualization: Justification, properties and application. Journal of Applied Statistics 47(11), 1990–2010.

- Garcia et al. (2011) Garcia, C. G., J. G. Pérez, and J. S. Liria (2011). The raise method. an alternative procedure to estimate the parameters in presence of collinearity. Quality & Quantity 45(2), 403–423.

- Garcia and Ramirez (2017) Garcia, J. and D. Ramirez (2017). The successive raising estimator and its relation with the ridge estimator. Communications in Statistics-Theory and Methods 46(22), 11123–11142.

- García-Pérez et al. (2020) García-Pérez, J., M. del Mar López-Martín, C. García-García, and R. Salmerón-Gómez (2020). A geometrical interpretation of collinearity: A natural way to justify ridge regression and its anomalies. International Statistical Review 88(3), 776–792.

- Goeman et al. (2018) Goeman, J., R. Meijer, and N. Chaturvedi (2018). L1 and l2 penalized regression models. Vignette R Package Penalized. URL http://cran. nedmirror. nl/web/packages/penalized/vignettes/penalized. pdf.

- Gökpınar and Ebegil (2016) Gökpınar, E. and M. Ebegil (2016). A study on tests of hypothesis based on ridge estimator. Gazi University Journal of Science 29(4), 769–781.

- Halawa and El Bassiouni (2000) Halawa, A. and M. El Bassiouni (2000). Tests of regression coefficients under ridge regression models. Journal of Statistical Computation and Simulation 65(1-4), 341–356.

- Hoerl et al. (1975) Hoerl, A. E., R. W. Kannard, and K. F. Baldwin (1975). Ridge regression: some simulations. Communications in Statistics-Theory and Methods 4(2), 105–123.

- Hoerl and Kennard (1970a) Hoerl, A. E. and R. W. Kennard (1970a). Ridge regression: applications to nonorthogonal problems. Technometrics 12(1), 69–82.

- Hoerl and Kennard (1970b) Hoerl, A. E. and R. W. Kennard (1970b). Ridge regression: Biased estimation for nonorthogonal problems. Technometrics 12(1), 55–67.

- Hoerl and W. Kennard (1990) Hoerl, A. E. and R. W. Kennard (1990). Ridge regression: degrees of freedom in the analysis of variance. Communications in Statistics-Simulation and Computation 19(4), 1485–1495.

- Kaçiranlar et al. (1999) Kaçiranlar, S., S. Sakallioğlu, F. Akdeniz, G. P. Styan, and H. J. Werner (1999). A new biased estimator in linear regression and a detailed analysis of the widely-analysed dataset on portland cement. Sankhyā: The Indian Journal of Statistics, Series B, 443–459.

- Kibria and Lukman (2020) Kibria, B. and A. F. Lukman (2020). A new ridge-type estimator for the linear regression model: Simulations and applications. Scientifica 2020.

- Lawless (1978) Lawless, J. F. (1978). Ridge and related estimation procedures: theory and practice: ridge and related estimation. Communications in Statistics-Theory and Methods 7(2), 139–164.

- Levenberg (1944) Levenberg, K. (1944). A method for the solution of certain non-linear problems in least squares. Quarterly of applied mathematics 2(2), 164–168.

- Li and Yang (2012) Li, Y. and H. Yang (2012). A new liu-type estimator in linear regression model. Statistical Papers 53(2), 427–437.

- Lukman et al. (2019) Lukman, A. F., K. Ayinde, S. Binuomote, and O. A. Clement (2019). Modified ridge-type estimator to combat multicollinearity: Application to chemical data. Journal of Chemometrics 33(5), e3125.

- Marquardt (1963) Marquardt, D. W. (1963). An algorithm for least-squares estimation of nonlinear parameters. Journal of the society for Industrial and Applied Mathematics 11(2), 431–441.

- Marquardt (1970) Marquardt, D. W. (1970). Generalized inverses, ridge regression, biased linear estimation, and nonlinear estimation. Technometrics 12(3), 591–612.

- Marquardt (1980) Marquardt, D. W. (1980). Comment: You should standardize the predictor variables in your regression models. Journal of the American Statistical Association 75(369), 87–91.

- Marquardt and Snee (1975) Marquardt, D. W. and R. D. Snee (1975). Ridge regression in practice. The American Statistician 29(1), 3–20.

- McDonald and Galarneau (1975) McDonald, G. C. and D. I. Galarneau (1975). A monte carlo evaluation of some ridge-type estimators. Journal of the American Statistical Association 70(350), 407–416.

- Monarrez et al. (2007) Monarrez, M. R. P., M. A. R. Medina, and J. J. A. Solís (2007). Regresión ridge y la distribución central t. CIENCIA ergo-sum, Revista Científica Multidisciplinaria de Prospectiva 14(2), 191–196.

- Obenchain (1977) Obenchain, R. (1977). Classical f-tests and confidence regions for ridge regression. Technometrics 19(4), 429–439.

- O’brien (2007) O’brien, R. M. (2007). A caution regarding rules of thumb for variance inflation factors. Quality & quantity 41(5), 673–690.

- Ohtani (1985) Ohtani, K. (1985). Bounds of the f-ratio incorporating the ordinary ridge regression estimator. Economics Letters 18(2-3), 161–164.

- OM (2001) OM, A. B. O. (2001). Ridge regression and inverse problems. Stockholm University, Department of Mathematics.

- Piegorsch and Casella (1989) Piegorsch, W. W. and G. Casella (1989). The early use of matrix diagonal increments in statistical problems. SIAM review 31(3), 428–434.

- Puntanen et al. (2011) Puntanen, S., G. P. Styan, and J. Isotalo (2011). Matrix tricks for linear statistical models: our personal top twenty. Springer Science & Business Media.

- Riley (1955) Riley, J. D. (1955). Solving systems of linear equations with a positive definite, symmetric, but possibly ill-conditioned matrix. Mathematical Tables and Other Aids to Computation, 96–101.

- Roldán López De Hierro et al. (2018) Roldán López De Hierro, A. F., R. Gómez Salmerón, and C. García García (2018). About the limits of raise regression to reduce condition number when three explanatory variables are involved. Rect@ 19(1), 45–62.

- Salmerón et al. (2018) Salmerón, R., C. García, and J. García (2018). Variance inflation factor and condition number in multiple linear regression. Journal of Statistical Computation and Simulation 88(12), 2365–2384.

- Salmerón et al. (2017) Salmerón, R., C. Garcia, J. Garcia, and M. d. M. Lopez (2017). The raise estimator estimation, inference, and properties. Communications in Statistics-Theory and Methods 46(13), 6446–6462.

- Salmerón et al. (2020) Salmerón, R., C. G. García, and J. García Pérez (2020). Detection of near-multicollinearity through centered and noncentered regression. Mathematics 8, 931.

- Salmerón et al. (2020) Salmerón, R., A. Rodríguez Sánchez, C. G. García, and J. García Pérez (2020). The vif and mse in raise regression. Mathematics 8(4), 605.

- Salmerón et al. (2019) Salmerón, R., A. Rodríguez-Sánchez, and C. García-García (2019). Diagnosis and quantification of the non-essential collinearity. Computational Statistics, 1–20.

- Schmidt (1976) Schmidt, P. (1976). Econometrics. Inc., New York.

- Sengupta and Sowell (2020) Sengupta, N. and F. Sowell (2020). On the asymptotic distribution of ridge regression estimators using training and test samples. Econometrics 8(4), 39.

- Singh (2011) Singh, R. (2011). Two famous conflicting claims in econometrics. Asian-African Journal of Econometrics 11(1), 185–186.

- Smith and Campbell (1980) Smith, G. and F. Campbell (1980). A critique of some ridge regression methods. Journal of the American Statistical Association 75(369), 74–81.

- Snee and Marquardt (1984) Snee, R. D. and D. W. Marquardt (1984). Comment: Collinearity diagnostics depend on the domain of prediction, the model, and the data. The American Statistician 38(2), 83–87.

- Stahlecker and Schmidt (1996) Stahlecker, P. and K. Schmidt (1996). Biased estimation and hypothesis testing in linear regression. Acta Applicandae Mathematica 43(1), 145–151.

- Stein (1981) Stein, C. M. (1981). Estimation of the mean of a multivariate normal distribution. The annals of Statistics, 1135–1151.

- Theobald (1974) Theobald, C. M. (1974). Generalizations of mean square error applied to ridge regression. Journal of the Royal Statistical Society: Series B (Methodological) 36(1), 103–106.

- Thisted (1976) Thisted, R. A. (1976). Ridge regression, minimax estimation, and empirical Bayes methods. Department of Statistics, Stanford University.

- Thisted (1980) Thisted, R. A. (1980). A critique of some ridge regression methods: Comment. Journal of the American Statistical Association 75(369), 81–86.

- Trenklar (1980) Trenklar, G. (1980). Generalized mean squared error comparisons of biased regression estimators. Communications in Statistics-Theory and Methods 9(12), 1247–1259.

- Ullah et al. (1984) Ullah, A., R. A. Carter, and V. K. Srivastava (1984). The sampling distribution of shrinkage estimators and theirf-ratios in the regression model. Journal of Econometrics 25(1-2), 109–122.

- Van Nostrand (1980) Van Nostrand, R. C. (1980). A critique of some ridge regression methods: Comment. Journal of the American Statistical Association 75(369), 92–94.

- Vanhove (2020) Vanhove, J. (2020). Collinearity isn’t a disease that needs curing.

- Vinod (1987) Vinod, H. (1987). Confidence intervals for ridge regression parameters. Time series and econometric modelling, 279–300.

- Willan and Watts (1978) Willan, A. R. and D. G. Watts (1978). Meaningful multicollinearity measures. Technometrics 20(4), 407–412.

- Woods et al. (1932) Woods, H., H. H. Steinour, and H. R. Starke (1932). Effect of composition of portland cement on heat evolved during hardening. Industrial & Engineering Chemistry 24(11), 1207–1214.

Appendix A Estimation of model (2) by OLS

Given the general linear model (2) it is obtained that:

| (41) | |||||

| (50) |

only considering that , with , and taking into account that:

where y are, respectively, the OLS estimator and the SSR of the auxiliary regression (3) being the identity matrix with adequate dimension.

On the other hand, supposing that the random disturbances are spherical, the individual inference will be given by the main diagonal of matrix , it is to say:

| (51) |

In this case, the null hypothesis is rejected (in favor of the alternative hypothesis ) if:

| (52) |

where is the estimation by OLS of the variance of the random disturbance:

where are the residuals of model (2).

At the same time, the null hypothesis is rejected (in favor of the alternative hypothesis ) if:

| (53) |

Note that the element of is where is the element of .

Finally, the residuals of the model are given by the following expression:

| (56) | |||||

| (57) |

due to being the residuals of the auxiliary regression (3) it is verified that .

Appendix B Calculation of the raise estimation

Taking into account the inversion of the partitioned matrices, it is obtained that:

where:

Then:

where it was used that for .

Appendix C Residualization

García et al. (2020) formalizes the residualization regression. Thus, parting from model (2), the following expression is obtained for the regression with orthogonal variables:

| (58) |

where , being the result of eliminating the column (variable) of matrix , , and being the residuals of the auxiliary regression (3).

On the other hand, the residuals of model (58) are given by:

| (62) | |||||

| (63) |

It can be observed, see expressions (25) and (57), that these expressions coincide with the ones of models (2) and (4). Consequently, it is also verified that .

Taking into account the expression (51), is evident that the main diagonal of matrix differs to the one associated to model (2) except for the element . In this case, the null hypothesis is rejected (in favor of the alternative hypothesis ) if:

| (64) |

Note that from (52) it is possible to establish that .

At the same time, the null hypothesis is rejected (in favor of the alternative hypothesis ) if:

| (65) |

Note that is the element of .

From the point of view of multicollinearity, the VIF of the orthogonalized variable is equal to 1 while the VIFs of the rest of variable coincide to the VIF of matrix . Analogously, the CN obtained from the matrix coincide to the one obtained from matrix .

Finally, the MSE of the residualization method is:

Appendix D Behavior of the estimators in MSE

It is known that, see Theobald (1974), given the general linear model (2), it is possible to compare two estimators with the form with by applying the criterion of the matrix of the root mean square (MtxMSE) defined by:

| (66) |

From:

| (67) |

it is known that if the matrix is definite or positive semidefinite, then estimator will be more appropriate than estimator . It is also verified that . Hence, it is possible to conclude that is better than in terms of MSE.

From the above expression and following Theorem 2.2.2 of Trenklar (1980), it is possible to obtain the following result.

Proposition 3.

Let , with , be two homogeneous linear estimators of such that is a positive definite matrix. Furthermore, let the following inequality be valid:

| (69) |

then .