The Wasserstein space of stochastic processes

Abstract.

Wasserstein distance induces a natural Riemannian structure for the probabilities on the Euclidean space. This insight of classical transport theory is fundamental for tremendous applications in various fields of pure and applied mathematics.

We believe that an appropriate probabilistic variant, the adapted Wasserstein distance , can play a similar role for the class of filtered processes, i.e. stochastic processes together with a filtration. In contrast to other topologies for stochastic processes, probabilistic operations such as the Doob-decomposition, optimal stopping and stochastic control are continuous w.r.t. . We also show that is a geodesic space, isometric to a classical Wasserstein space, and that martingales form a closed geodesically convex subspace.

Key words and phrases:

Aldous’ extended weak topology, Hoover and Keisler’s adapted distribution, Hellwig’s information topology, Pflug-Pichler’s nested distance, Vershik’s iterated Kantorovich distance, stability of stochastic optimization, geodesic space, barycenter of stochastic processes1. Overview

It is often useful to change the view from considering objects in isolation to studying the space of these objects and specifically their mutual relationship w.r.t. the ambient space. A classic instance is to switch from studying functions to considering the Lebesgue- or Sobolev-spaces of functions in functional analysis; a more contemporary example is the passing from measures to the manifold of measures based on optimal transport theory. The aim of this article is to investigate what should be the appropriate ambient space for the class of stochastic processes.

1.1. The space of laws on and its limitations

A natural starting point for this is to represent stochastic processes on the canonical probability space. Specifically, the class of real valued processes in finite discrete time is naturally represented as the set of probability measures on . Importantly, the usual weak topology on fails to capture the temporal structure of stochastic processes and is not strong enough to guarantee continuity of stochastic optimization problems or basic operations like the Doob-decomposition.

As a remedy, a number of researchers from different scientific communities have introduced topological structures on the set of stochastic processes with the common goal to adequately capture the temporal structure. We list Aldous extended weak topology [9] (stochastic analysis), Hellwig’s information topology [57, 58] (economics), Bion-Nadal and Talay’s version of the Wasserstein distance [35] (stochastic analysis, optimal control), Pflug and Pichler’s nested distance [80, 81] (stochastic optimization), Rüschendorf’s Markov constructions [89] (optimal transport), Lassalle’s causal transport problem [72] (optimal transport), and Nielsen and Sun’s chain rule transport [77] (machine learning). Remarkably, in finite discrete time, these seemingly independent approaches define the same topology on , the weak adapted topology, see [12].

A natural compatible metric111Precisely, convergence in is equivalent to convergence in the weak adapted topology plus convergence of the -th moment, see also [12]. for the weak adapted topology is the adapted Wasserstein distance

The difference to the classical Wasserstein distance comes from the fact that one considers only bicausal couplings , see Definition 2.1 below. These couplings are non-anticipative and can be viewed as a Kantorovich analogue of non-anticipative transport maps, see [34].

While the weak adapted topology / appear canonical and have recently seen a burst of applications (see [43, 82, 83, 52, 11, 3, 95, 85, 69, 76, 87, 86, 96, 13, 64] among others) we also highlight two limitations:

-

(1)

The metric space is not complete. In fact, this shortcoming also arises for other natural distances that respect the information structure of stochastic processes.

-

(2)

Following the classical theory of stochastic analysis one would like to consider processes together with a general filtration, not just the filtration generated by the process itself.

1.2. Filtered processes as the completion of

Rather conveniently, these supposed shortcomings already represent their mutual resolution: a possible interpretation of the incompleteness of is that the space is not ‘large’ enough to represent all processes one would like to consider. In our first main result we show that the extra information that can be stored in an ambient filtration is precisely what is needed to arrive at the completion of . To make this precise we need the following definition:

Definition 1.1.

A five-tuple

| (1.1) |

where is adapted to , is called a filtered (stochastic) process. We write for the class of all filtered processes and for the subclass of processes with .

Clearly, is embedded in : for set , where is the canonical process, i.e. , and for .

It is relatively straightforward to extend the concept of bicausal couplings to processes with filtrations (see Definition 2.1 for details) and accordingly the notion of adapted Wasserstein distance extends to filtered processes via

As in the case of / spaces (or similar situations), we identify two filtered processes if and denote the corresponding set of equivalence classes by . Our first main result is:

Theorem 1.2.

is a metric on and is the completion of .

We also show in Theorem 5.4 below that certain simpler classes of processes are dense in , e.g. filtered processes that can be represented on a finite state space or finite state Markov chains. This seems important in view of numerical applications.

1.3. as geodesic space

In fact, our proof of Theorem 1.2 reveals more, namely the following result on the metric structure of :

Theorem 1.3.

There exists a Polish space such that is isometric to the classical Wasserstein space .

Explicitly, is constructed by considering Wasserstein spaces of Wasserstein spaces in an iterated fashion as already considered by Vershik [91]. Theorem 1.3 allows to transfer concepts from optimal transport to the theory of stochastic processes, e.g. it allows to consider displacement interpolation and Wasserstein barycenters of filtered processes and to view as a (formal) Riemannian manifold. Specifically, using the work of Lisini [74] we obtain:

Theorem 1.4.

Assume . Then is a geodesic space and the set of martingales forms a closed, geodesically convex subspace.

Famously, McCann introduced the concept of displacement interpolation in his thesis [75], giving a new meaning to the transformation of one probability into another. In analogy, Theorem 1.4 suggests an interpolation between stochastic processes.

We emphasize that the usual Wasserstein interpolation on is not compatible with concepts one would like to consider for stochastic processes, e.g. stochastic optimization problems are not continuous along geodesics, the set of martingales is not displacement convex, etc.

We also note that the set is not -displacement convex: even if are laws of relatively regular processes, the respective geodesic does in general not lie in , see Example 5.11. This further underlines the importance of considering processes together with their filtration.

1.4. Equivalence of filtered processes

We briefly discuss the equivalence relation induced by

| (1.2) |

Intuitively, one would hope that processes with zero distance are equivalent in the sense that they have identical properties from a probabilistic perspective. In fact, based on formalizing what assertions belong to the ‘language of probability’, Hoover–Keisler [62] have made precise what it should mean that two processes have the same probabilistic properties. and are then called equivalent in adapted distribution, in signs . We will establish below that equivalence in adapted distribution can be expressed in terms of adapted Wasserstein distance:

Theorem 1.5.

Let . Then if and only if .

Informally, Theorem 1.5 asserts that the equivalence classes in collect precisely all representatives of a process that should be considered identical from a probabilist’s point of view.

Other (more familiar) notions of equivalence on are equivalence in law, in symbols , and Aldous’ notion of synonymity, in symbols . Both of these are strictly coarser than and may identify processes that have different probabilistic properties. For example, there are filtered processes with where is a martingale while is not. Similarly, we will construct examples of processes where but optimal stopping problems written on lead to different results (see Theorem 7.1).

1.5. Continuity of Doob-decomposition, optimal stopping, Snell-envelope

In line with Theorem 1.5, implies that and have the same Doob-decomposition, that optimal stopping problems of the form

| (1.3) |

where runs through all -stopping times, yield the same optimal value and have the same Snell-envelop. Moreover, we show that the above operations are continuous w.r.t. the weak adapted topology, indeed we establish:

Theorem 1.6.

The mapping that assigns to a filtered process its Doob-decomposition is Lipschitz continuous. If is bounded and continuous (resp. Lipschitz) for each , then (1.3) is continuous (resp. Lipschitz) in .

In Section 6 we collect further statements of similar flavour as Theorem 1.6. It is important to note that comparable results do not hold w.r.t. to other (coarser) topologies for filtered processes. Specifically, convergence in Aldous’ extended weak topology is strictly weaker than convergence in and is not strong enough to obtain continuity of optimal stopping problems (see Section 7). This seems remarkable, since Aldous [9, page 105] deliberates the question which framework is natural to study continuity of optimal stopping.

1.6. Canonical representatives of filtered processes

A slightly altered variant of the Polish space appearing in Theorem 1.3 also plays an important role in finding canonical representatives for the equivalence classes in : In Section 3 below we will show that there exists with Polish, such that every filtered process is represented in a canonical way via a probability on , i.e. there exists such that

In particular, all information about the process is stored in the corresponding measure , while the underlying probability space , the representing stochastic process and the respective filtration do not depend on . In this sense the situation is analogous to the canonical representation of stochastic processes via probabilities on the path space. In view of Theorem 1.5 this also implies that one can assume without loss of generality that a given filtered process is defined on a Polish probability space.

1.7. Prohorov-type result and barycenter of processes

An extremely useful property of the usual weak topology is the abundance of (pre-)compact sets based on Prohorov’s theorem. Remarkably, this carries over to ‘adapted’ topologies. This was first established by Hoover [60, Theorem 4.3], see also [11, Lemma 1.7]. In the present context this fact can be expressed as follows:

Theorem 1.7.

A set is -precompact if and only if the respective set of laws in is -precompact.

Note that by Prohorov’s theorem, -precompactness in is equivalent to tightness plus uniform -integrability, see for instance [94].

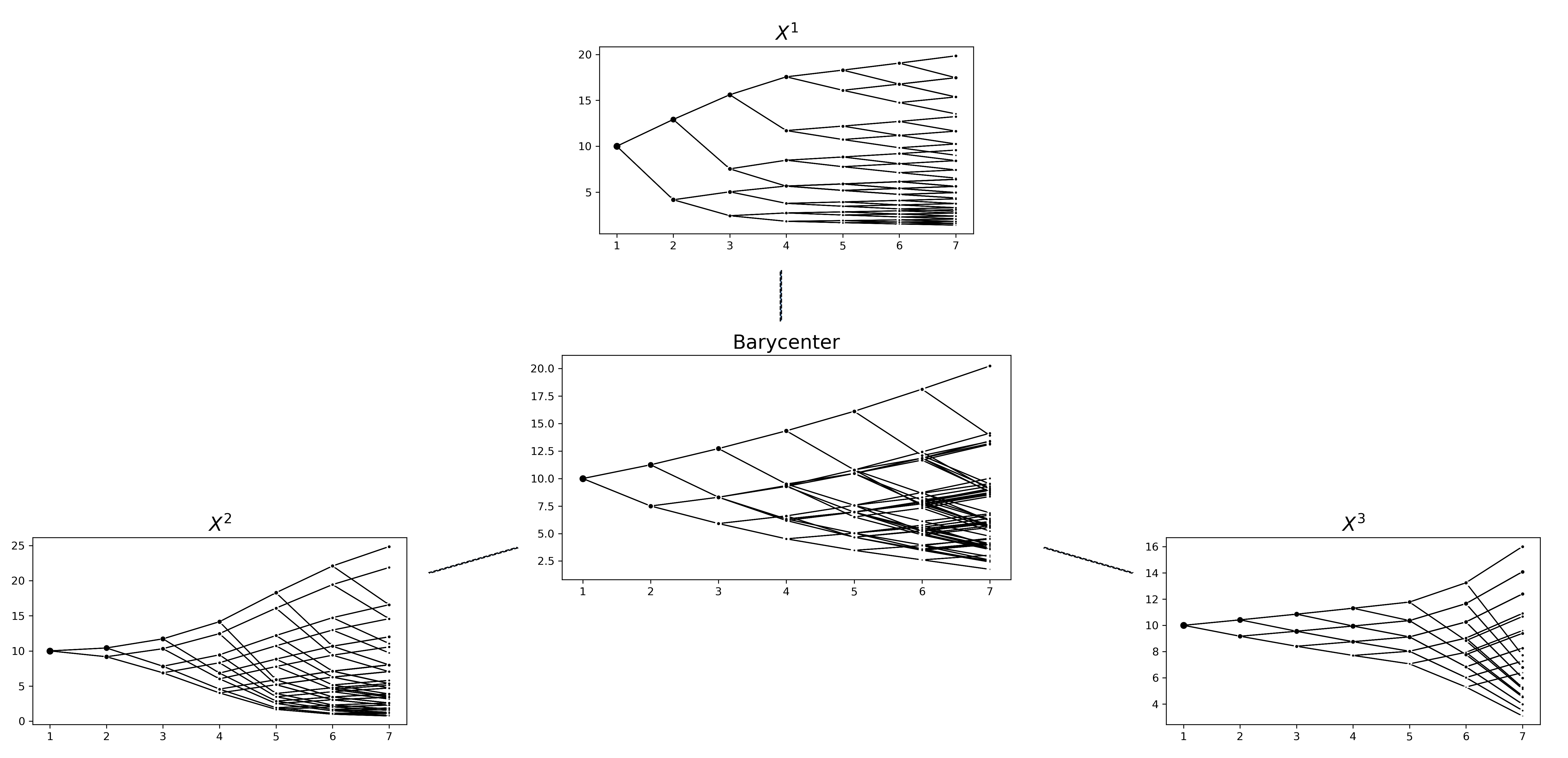

Theorem 1.7 is relevant in several proofs given below and has important consequences for the applications of our results presented in Section 6. For instance, it allows us to establish the existence of barycenters of stochastic processes: Famously, Agueh and Carlier [6] introduced the concept of barycenters w.r.t. Wasserstein distance which has striking consequences in machine learning (e.g. [88, 42]), statistics (e.g. [78, 18]) as well as in pure mathematics (e.g. [73, 68]). In Theorem 6.7 we show that for filtered processes and convex weights there exists a barycenter process i.e. a filtered process which minimizes

1.8. Applications and extensions

As already noted above, the adapted Wasserstein distance improves over the classical weak topology / Wasserstein distance in that it guarantees stability of basic operations such as the Doob-decomposition and optimal stopping. Naturally we expect similar results for other probabilistic problems with inherent time structure. In this line, we describe applications to stability of stochastic optimal control, utility maximization and pricing / hedging, robust finance in the realm of American options, conditional McKean-Vlasov control, and weak optimal transport, see Sections 6.1 - 6.8 below. In view of applications it is relevant that adapted Wasserstein distance can be efficiently computed numerically as well as estimated from given data; we comment on this in Section 6.9.

While the focus of the present article lies on stochastic processes in finite discrete time, extensions to more general cases are intriguing. In Appendix B we consider the case of infinite discrete time, i.e. the set of processes whose paths lie in (or a countable product of Polish spaces). We obtain results very similar to the finite discrete time case, mainly based on limiting arguments.222We thank an anonymous referee for pointing us to this direction. A notable difference is that the path space is not geodesic and hence is not geodesic either.

Concerning continuous time processes , it is known from stochastic analysis, that different applications require the use of different topologies / metrics on the path space. This fact appears even more noticeable when also information is taken into account. In Appendix C we briefly present adapted topologies for continuous time stochastic processes that have been used in the literature or seem sensible. We describe how needs to be altered to fit the respective choices and comment on some strengths and weaknesses of the emerging theories.

1.9. Remarks on related literature.

Imposing a ‘causality’ constraint on a transport plan between laws of processes seems to go back to the Yamada–Watanabe criterion for stochastic differential equations [99] and is used under the name ‘compatibility’ by Kurtz [71].

A systematic treatment and use of causality as an interesting property of abstract transport plans between filtered probability spaces and their associated optimal transport problems was initiated by Lassalle [72] and Acciaio, Backhoff, and Zalashko [2].

As noted above, different groups of authors have introduced similar ‘adapted’ variants of the Wasserstein distance, this includes the works of Vershik [91, 92], Rüschendorf [89], Gigli [51, Chapter 4] (see also [10, Section 12.4]), Pflug and Pichler [80], Bion-Nadal and Talay [35], and Nielsen and Sun [77]. Pflug and Pichler’s nested distance has had particular impact in multistage programming, see [81, 82, 52, 69, 86] among others.

In addition to these distances, extensions of the weak topology that account for the flow of information were introduced by Aldous in stochastic analysis [9] (based on Knight’s prediction process [70]), Hoover and Keisler in mathematical logic [62, 60] and Hellwig in economics [57]. Very recently, an approach using higher rank signatures was given by Bonner, Liu, and Oberhauser [36], in particular providing a metric for convergence in adapted distribution in the sense of Hoover–Keisler.

The idea to represent information (in the sense of filtrations) using conditional distributions originated in the theory of dynamical systems and Vershik’s program to classify filtrations whose time horizons starts at , see e.g. [92] and in particular the survey [93]. For a more probabilistic account of this line of research we refer to [47]. Independently, Pflug [79] introduced this idea in stochastic optimization and defined the space of ‘nested distributions’.

Recently, there has been significant interest in adapted / causal transport problems in discrete time or with a finite number of hierarchical levels. A goal of the present article is to provide the theoretical framework for these emerging lines of research and we briefly indicate some of these directions: In mathematical finance, the use of weak adapted topologies was initiated in the context of game options [43]. Further contributions apply adapted transport and adapted Wasserstein distances to questions of insider trading and enlargement of filtrations [2], stability of pricing / hedging and utility maximization [52, 22, 23, 11, 1, 30, 31] and interest rate uncertainty [3]. Adapted transport is used in [21] to study the sensitivity of multiperiod optimization problems and distributionally robust optimization problems. In [56] it is applied to time-dynamic matching problems [24], and in [90, 63] for the computational resolution of optimal stopping and other filtration-dependent problems. In [38] a connection of adapted transport to the Weisfeiler-Lehman distance is reveiled. Machine learning algorithms based on adapted or hierarchical structures are studied in the context of image processing [65], text processing and hierarchical domain translation [100, 46], causal graph learning [7], video prediction and generation [98, 97], and universal approximation [5]. In [39], adapted transport is used as the starting point to develop a framework for more general causal dependence structures.

1.10. Organization of the paper

In Section 2 we introduce some important concepts and in particular the notions of (bi-) causality and adapted Wasserstein distance.

In Section 3 we formally discuss the Wasserstein space of filtered processes as a preparation to establish Theorem 1.2 and Theorem 1.3 subsequently. In Subsection 3.1 we construct a canonical filtered space that supports for each equivalence class a canonical representative. Building on the foregoing subsections, we establish in Subsection 3.2 an isometric isomorphism between filtered processes, their canonical counterparts, and a classical Wasserstein space.

Section 4 links the weak adapted topology to the concept of adapted functions and the prediction process by Hoover and Keisler.

Section 5 deals with topological and geometric aspects. We prove a compactness criterion, show that is the completion of and prove that finite state Markov processes are dense in , prove that is a geodesic space for , and show that martingales form a closed, geodesically convex subset of .

In Section 6 we discuss applications and comment on numerical aspects related to .

Section 7 is concerned with an example that, among other things, shows that Aldous’ extended weak topology fails to guarantee continuity of optimal stopping problems.

Finally, in Appendix A, we discuss a notion of ‘block approximation’ of couplings, which is an auxiliary concept required to prove the results in Subsection 3.2 for probability spaces that are not necessarily Polish. In Appendix B and C we discuss extensions of the present setting to the case of stochastic processes index by infinite discrete time and continuous time, respectively.

2. Notational conventions

Throughout this article, we fix a time horizon and . For each time , let be a Polish space with a fixed compatible complete metric . If , then where is the Euclidean norm. Given a finite family of sets and , we use the following abbreviation for its product

The same convention applies to vectors. For , the projection onto the -th coordinate of is denoted by . Using this convention we are interested in stochastic processes taking values in the path space . Processes on are usually denoted by capital letters, i.e., , whereas specific elements of the path space are denoted by lower case, i.e., .

Distances: For a Polish space with fixed compatible complete metric , we write for the set of Borel probability measures on , and for the subset whose elements integrate for some (and hence all) . If is another Polish space and , , we write for the set of all couplings with marginals , that is if and its first marginal equals and its second . We equip with the topology of weak convergence and with the (-th order) Wasserstein distance , that is

This renders and Polish spaces. Note that for a bounded metric, the weak convergence topology and the one induced by coincide. Whenever clear from context, we will omit excessive subscripts and simply write and for and respectively.

Filtrations: For a filtered process , we use the convention that . It is important to note that since the processes start at time , this convention is only notational and does not imply that the initial -algebra is trivial. Frequently we consider multiple products of -algebras. To prevent notation getting out of hand, we write

for two filtered processes and . Moreover, we will often identify with ; e.g. an -measurable functions is naturally associated on with an -measurable function depending only on the second coordinate, and vice versa. In a similar manner, for a function , we continue to write for the function .

Couplings: In optimal transport couplings are the central tool for comparing probability measures. For filtered processes this role is taken by bicausal couplings, i.e. couplings which respect the information structure of the underlying filtered probability spaces.

Definition 2.1 (Causal couplings).

Let , be filtered processes. A probability on is called coupling between and if its marginals are and . We call

-

(a)

causal (or causal from to ) if, for every , conditionally on we have that and are independent,

-

(b)

anticausal (or causal from to ) if, for every , conditionally on we have that and are independent,

-

(c)

bicausal if it is both, causal and anticausal.

We write , and for the set of couplings, causal couplings, and bicausal couplings, respectively.

In case that the underlying spaces are path spaces equipped with canonical filtration / processes, these definitions correspond precisely to the classical definitions given in the literature, see [80, 81, 16, 14, 12] among others. In the context of space with more general filtrations causality and causal transport are considered in [72, 2].

The following lemma provides useful characterizations of causality which we will frequently use throughout the article.

Lemma 2.2 (Causality).

In words, (ii) says that given the past of , the past of does not provide additional information about the future of and (iii) says that given the past of , the future of does not provide additional information about the past of .

Proof of Lemma 2.2.

The adapted Wasserstein distance between filtered processes and taking values in is then defined as

When clear from context, we write instead of . Similarly, we write instead of etc.

Kernels and product measures: For two Polish spaces and , the term kernel refers to a Borel-measurable mapping . For and a kernel , we write for the measure given by . If we write for the product measure. For a measure and a Borel-measurable mapping , the push-forward of under is denoted by .

3. The Wasserstein space of stochastic processes

3.1. The canonical filtered space

In order to prove Theorem 1.2 we introduce the canonical space of filtered processes. The classical canonical space of a stochastic process is the triplet consisting of path space, Borel--algebra, and its induced law. Clearly, this triplet is adequate if one is interested solely in trajectorial properties of the process. However, the filtration is a major part of filtered processes and therefore we need to capture the information contained in its filtration in a canonical way. Thus we need to define a canonical space which is capable to carry besides the path properties also the relevant informational properties of .

As an instructional example, consider two 1-step filtered processes and taking values in . We write for the trivial -algebra, for the Borel -algebra on , and for the coordinate process on . Let , and define

Even though the laws of the paths of the two processes coincide, their probabilistic behavior is very different due to their different filtrations, specifically we have

| (3.1) |

From this perspective, the product is adequate to capture and additionally the information on we can witness at time 1 based on the filtration, that is .

This observation leads to the definition of what we baptize the canonical filtered space, the information process, and the canonical filtered process below:

Definition 3.1 (Canonical space).

Fix . We iteratively define a sequence of nested spaces. We write and recursively for

| (3.2) |

with metric . The elements of are denoted by . The canonical filtered space is given by the triplet

| (3.3) |

where is denoted by , elements of by , the Borel--algebra on by , and by . In the context of the canonical filtered space the map denotes the evaluation map

| (3.4) |

The spaces introduced in Definition 3.1 are Polish as all operations involved in their definition preserve this property. The next definition associates to a filtered process its canonical counterpart – the information process defined on and taking values in . We shall later see that the information process selects all information contained in the original filtration relevant for the process; hence its name.

Definition 3.2 (The information process).

To each , we associate its information process defined by setting

and, recursively for ,

Note that is -valued and is -valued. In particular this implies that the information process is well-defined: as consists of Polish spaces, the conditional probabilities appearing in the recursive definition of above exist.

The information processes will be an essential ingredient when we define canonical representatives of filtered processes (see Definition 3.8 below). The next lemma can be seen as a first justification of its name:

Lemma 3.3 (The information process is self-aware).

For every bounded, Borel (continuous) function and every there is a bounded, Borel (continuous) function such that

More generally, let be a Polish space. For every Borel (continuous) function and every there is a Borel (continuous) function such that

This lemma is an easy consequence of properties of the unfold operator introduced below, see Lemma 3.5. Nevertheless, to boost the reader’s intuition, we want to include a direct proof for the first statement in the notationally lighter case :

Sketch of proof for .

For there is nothing to do, as is -measurable. Let . For simplicity, we assume first that is a product for suitable and . Then we can write

where we used that is -measurable. By definition , whence

For general not necessarily of product form, a straightforward application of the monotone class theorem concludes the proof. ∎

In what follows, we are often dealing with mappings between nested spaces of probability measures with different algebraic structures. The unfold operator, introduced below, is an essential tool in reducing bookkeeping to a comprehensible level.

Definition 3.4 (Unfold).

For every , we define

| (3.5) | ||||

and call the unfold operator (at time ). For , we define to be the identity map.

Recall the definition of , see Definition 3.2. As is a random variable taking values in , the unfold operator can be applied pointwise, i.e., we may consider . The following lemma explores properties of in view of the information process :

Lemma 3.5.

For the following hold:

-

(i)

For we have

(3.6) -

(ii)

For we have

(3.7) In other words, for all bounded Borel functions we have

(3.8) -

(iii)

is Lipschitz continuous from to .

Proof.

- (i)

-

(ii)

The statements in (3.7) and (3.8) are clearly equivalent and we shall therefore only prove the latter one via a backward induction.

Since there is nothing to do for , we assume that the statement is true for . Let be the Borel function defined as

(3.9) whereby the inductive hypothesis now reads .

-

(iii)

The assertion is shown via a backward induction over .

For the unfold operator is given as the identity map, which is in particular Lipschitz continuous. Assume that the claim is true for some . By (3.6) we can write , where . This map is explicitly given by . An application of Lemma 3.6 below implies that is again Lipschitz continuous with a new constant. ∎

Lemma 3.6.

Let and be Polish spaces and let be -Lipschitz. Then the map

is -Lipschitz.

Proof.

A short computation shows that there are , and a constant such that for all ; in particular is well-defined for every .

Let and denote by the -optimal coupling between them. For every pair , let be optimal for . Using the Jankov-von Neumann theorem [67, Theorem 18.1], standard arguments show that can be chosen universally measurably. Then

defines a coupling between and . Thus we can estimate

where the last inequality holds by -Lipschitz continuity of . ∎

Proof of Lemma 3.3.

Let be bounded and Borel measurable (continuous), and . As is continuous by Lemma 3.5 (iii), we obtain continuity of

Define the map as the push-forward . Obviously, when is continuous, is also continuous as the composition of continuous functions. By Lemma 3.5 (ii), we obtain

We have thus proved the second assertion.

To obtain the first assertion, let . Define by which is well-defined since is bounded with values in a compact set, say, . Hence, we can view as a function mapping into . By the first part of the proof, we obtain

The map is continuous on and we conclude that is continuous if is. ∎

Equipped with the unfold operator we define our real object of interest:

Definition 3.7 (Canonical filtered processes).

Using the concept of information process we can associate to an arbitrary filtered process a unique element in :

Definition 3.8 (Associated canonical filtered processes).

We want to stress at this point that, as stated in (3.12), all information of is already contained in by Lemma 3.5. The relations between and become apparent in Theorem 3.10 below, and the relation of filtered processes to their canonical counterparts becomes apparent through Lemma 3.9.

Lemma 3.9.

Let , and let be their associated canonical processes. The following hold.

-

(i)

.

-

(ii)

If , then .

-

(iii)

If , then .

Proof.

To show (i), we write and first check causality of using (iii) of the characterization of causality given in Lemma 2.2. To that end, let be bounded and -measurable. From the definition of we see that -almost surely . Thus is -measurable and causality of from to follows from

To see causality of from to , we will again use Lemma 2.2, this time item (ii). Let be bounded and -measurable. Again, due to the structure of it is readily verified that -almost surely and

| (3.13) | ||||

| (3.14) |

By the self-awareness property of the information process, see Lemma 3.3, (3.13) and (3.14) we find

which completes the proof of item (i).

3.2. The isometry

Based on the preparatory work from the preceding subsection, we are able to establish Theorem 3.10. From this, we derive that naturally induces a complete metric on the factor space , and that is isometrically isomorphic to the (classical) Wasserstein space , thereby establishing Theorem 1.3.

Theorem 3.10.

Let and let be the associated canonical processes. Then

| (3.16) |

In particular, is a pseudo-metric on and the embedding is an isometric isomorphism of and .

Proof.

The first equality in (3.16) is a direct consequence of Lemma 3.9 and Theorem A.4 in the Appendix. For the convenience of the reader, we present an alternative proof of the first equality under the assumption that the probability spaces of and are Polish, thereby omitting the technical result in Theorem A.4.

To see the reverse inequality, let and write

These couplings are bicausal by Lemma 3.9 (i) and admit disintegrations and since the considered probability spaces are Polish by assumption. Consider the probability

For symmetry reasons we will only show that is causal from to . By Lemma 2.2 it suffices to show that for any bounded, -measurable we have

As is bicausal, Lemma 2.2 asserts that is -measurable. By the same reasoning, we obtain -measurability of

where . Hence, by the definition of and the tower property we get

As was arbitrary, this yields and by symmetry . Moreover, we have and conclude that .

It remains to show the second equality. Write and . By Lemma A.1, we have that

where the second infimum is taken over all kernels

| (3.17) |

Now, for every , let be a kernel as in (3.17) that is an optimal coupling (w.r.t. ) between its marginals. Their existence follows from a standard measurable selection argument. Then, for every , , and every kernel as in (3.17), we have that

| (3.18) | ||||

with equality if . In particular, for every , an iterative application of (3.18) shows that

with equality if for every . Optimizing over yields the claim. ∎

Definition 3.11 (Wasserstein space of stochastic processes).

We call the quotient space

the Wasserstein space of stochastic processes. is equipped with (which is by Theorem 3.10 well-defined on independent of the choice of representative).

Our canonical choice of a representative of is the associated canonical process . From now on, whenever we use the probability space of (the equivalence class of filtered processes) , we refer to the filtered probability space provided by if not stated otherwise.

Corollary 3.12.

The map is lower semicontinuous w.r.t. the weak adapted topology333The weak adapted topology relates to the adapted Wasserstein distance the same way the weak topology of measures relates to the Wasserstein distance: The weak adapted topology is induced by when, for each , the metric is replaced by the bounded metric . on .

4. Adapted functions and the prediction process

This section relates the adapted Wasserstein distance to the existing concepts of prediction processes and adapted functions introduced by Knight [70], Aldous [9], and Hoover and Keisler [62]. The main result of this section, Theorem 4.11 below, shows that all concepts induce the same relation on filtered processes.

Before recalling the definition of adapted functions from [61] (see also [62]), let us say that, intuitively, an adapted function is an operation that takes a filtered processes as argument and returns a random variable defined on the underlying probability space of this filtered process. Simple examples of adapted functions are and .

Definition 4.1 (Adapted functions).

We call an adapted function – we write – if it can be built using the following three operations:

-

(AF1)

If is continuous bounded, then ; we set .

-

(AF2)

If , , and , then ; we set .

-

(AF3)

If and , then ; we set .

Further define the rank of an adapted function inductively as follows: the rank of is 0; the rank of is the maximal rank of ; and the rank of is the rank of plus 1.

The set of all adapted functions of rank at most is denoted by .

Moreover, we can naturally embed into by identifying with , since for all . Consequently, we may assume without loss of generality in item (AF2) that all have the same rank.

Adapted functions were defined in [62] in a continuous time setting. The present discrete time setting permits to give the following, perhaps clearer, representation:

Lemma 4.2.

Let and . Then if and only if for every there is and an -dimensional vector consisting of elements in , and there is such that

| (4.1) |

Proof.

It turns out to be useful to keep track of the depth of an adapted function, a notion that we now introduce: Loosely speaking, for , its depth is the number of times (AF2) was applied to a base element of the form with . The depth (at rank ) of a ‘base element’ with is defined as , i.e.,

| (4.2) |

Recursively, we assign to with and , , its depth

| (4.3) |

Note that by the iterative construction of any formation , is either a base element or of the form detailed in (AF2), and its depth is well-defined by (4.2) and (4.3).

Let . We begin the induction at depth . Then has if and only if it is a base element, in which case (4.1) holds true. Now assume that and that (4.1) applies to all with . We write where and all have depth less than . By the inductive hypothesis, for every there are vectors consisting of elements in , and such that

Collecting and sorting all the terms of the vectors for gives

Finally, let be the permutation with the property

then together with satisfies (4.1). ∎

Definition 4.3 (Adapted distribution).

Two filtered processes have the same adapted distribution (of rank ) if for every adapted function (resp. ); we write (resp. ).

Remark 4.4.

In the definition of adapted functions, we started in (AF1) with the base set of continuous and bounded functions from to . It is possible to vary this base set, without changing the induced equivalence relations and , see Definition 4.3. One may replace (AF1) with any of the following choices:

-

(AF1a)

if is bounded and Borel measurable, then ;

-

(AF1b)

if is bounded and Lipschitz continuous, then ;

-

(AF1c)

if and is bounded and continuous, then .

In a similar manner, we may consider in (AF2) solely Lipschitz continuous / Borel measurable and bounded , and still preserve the equivalence relations introduced in Definition 4.3. We shall prove this further down below.

The purpose of the next example is twofold: first, to show where adapted distributions and adapted functions naturally appear, and also to familiarize the reader with the latter.

Example 4.5 (Martingales and optimal stopping).

Let .

-

(a)

If is a martingale , then so is as already observed in [9]. Indeed, for ,

is an element of .444 For demonstrative purposes, we disregard that only bounded functions are allowed in the definition of adapted functions. Indeed, this is only a technical issue and all terms are well-defined by standard approximation arguments. Its evaluation yields

that is the martingale property of .

-

(b)

Another important property preserved by is Markovianity. This also holds for the important property of being ‘plain’ defined in (5.2) below.

-

(c)

Let be nonanticipative.555That is, depends only on when . By the Snell-envelope theorem we have

where is defined by backward induction starting with and

Thus, each equals the value of an adapted function of rank , from where it follows that implies .

Closely related to adapted functions is the prediction process:

Definition 4.6 (Prediction process).

For the first order prediction processes is given by

Iteratively, the -th order prediction process is given by

Finally, the prediction process is defined as the -valued random variable

For convenience, we set the zero-th order prediction process and so that the iterative scheme of Definition 4.6 is valid for .

Lemma 4.7.

For every there is a continuous function such that

Proof.

Let be the corresponding projection, that is . Therefore, is continuous with .

It is worth pointing out that contains ‘at least as much information’ as its predecessor . In fact, we shall later see in Proposition 7.2 that for , it contains strictly more information in general.

Lemma 4.8.

Let . There is a 1-Lipschitz function such that

In particular, if are such that and have the same distribution, then and have the same distribution as well.

Proof.

For consider the isometric injections

For , since , we may apply to , and obtain for all . Moreover, admits a 1-Lipschitz extension given by

where we write . Indeed, is -Lipschitz as, for , we have by Jensen’s inequality

where is an -optimal coupling of and . We denote by the composition .

Finally, the mapping

is 1-Lipschitz and satisfies

for all . This completes the proof. ∎

Let us remark that, when , the process is a measure-valued martingale w.r.t. which is terminating at .

A version of the next lemma can be found in [62], though the proof is different due to differences in the definition of adapted functions (as multi-time stochastic processes).

Lemma 4.9.

Let and let . Then the following are equivalent:

-

(i)

;

-

(ii)

and have the same distribution.

Before proving the lemma, we want to point out that the same proof with obvious modifications also works to obtain Remark 4.4. For example, replace at every instance ‘continuous’ with ‘Borel-measurable’ for (AF1a).

Proof.

Claim: For every there is such that

| (4.5) |

For the claim is trivially true as and due to item (AF1). Assume now that the claim is true for , and let . Using Lemma 4.2, we may represent as in (4.1). Thus, it suffices to show (4.5) for where and . By the inductive hypothesis there is such that for all . Therefore

for all , where , is continuous and bounded. This shows (4.5) and thus that (ii) implies (i).

We proceed to show that (i) implies (ii). To that end, we interject two preliminary statements. Define and inductively define as the set of all functions of the form

| (4.6) |

where, for every , is a vector of functions in and (with adequate ) is continuous and bounded.

Claim: is an algebra which separates points in .

As usual, we proceed by induction. The claim follows trivially for , since . Assume now that the claim is true for . Clearly, is an algebra. To see the second part of the claim, namely that it separates points, let and be two distinct elements , that is, for some . By the inductive hypothesis is an algebra which separates points in , therefore [48, Theorem 4.5] provides with

whence, separates points in .

Claim: For there is with

| (4.7) |

Again, the assertion is trivial for as . Assume that the claim holds for , and let be represented by and as in (4.6). By definition of the prediction process we have

for all . By assumption there are vectors of adapted functions in with

Similarly as in the proof of Lemma 4.2 we collect all terms and obtain some with , which shows the claim.

Lemma 4.10.

There is a 1-Lipschitz map such that

Proof.

By Lemma 4.8 there are 1-Lipschitz maps , with .

Claim: For there is a 1-Lipschitz map with

| (4.8) |

To establish (4.8) for general , we proceed by induction. Assuming that the claim holds true for , we find by the definition of the information process, see Definition 5.9, for

where is given by

Since is 1-Lipschitz by assumption, the same holds true for . Therefore, is 1-Lipschitz and satisfies (4.8), which yields the claim.

Finally, by the previously shown claim, the map

has the desired properties. ∎

Theorem 4.11.

Let . All of the following are equivalent:

-

(i)

.

-

(ii)

.

-

(iii)

and have the same distribution.

-

(iv)

and have the same distribution.

-

(v)

and have the same distribution.

-

(vi)

and have the same distribution.

-

(vii)

.

In Proposition 7.2 we shall further prove that for every , the relation strictly refines : there are with but (and especially ). Importantly, these refinements are essential even for seemingly simple applications as we shall show in Theorem 7.1: Only the relation guarantees that two processes and have the same values for optimal stopping problems.

Proof of Theorem 4.11.

In a first step, note that (i) implies (ii); that (iii) implies (iv); and that (v) implies (vi). Further, Lemma 4.9 shows that (i) and (iii) are equivalent and that (ii) and (iv) are equivalent. Theorem 3.10 shows that (v) and (vii) are equivalent. Lemma 4.7 shows that (v) implies (iii). Finally, Lemma 4.10 shows that (iv) implies (v). This concludes the proof. ∎

5. Topological and geometric properties of

5.1. Compactness in

To develop a comprehensive understanding of a topology, it is essential to get a hold on compact sets. For the weak topology, this is bestowed on us by Prokhorov’s theorem which gives an easy to check tightness-criterion for relative compactness. Theorem 5.1 implies that, perhaps surprisingly, the very same tightness-criterion also implies relative compactness for stochastic processes in

Theorem 5.1 (Prokhorov’s theorem).

For a subset , the following are equivalent.

-

(i)

is relatively compact in .

-

(ii)

is relatively compact in .

It is worthwhile to recall that condition (ii) is equivalent to tightness plus uniform integrability (see, e.g., [94]), that is, for every and there is a compact set such that

As a consequence of the nested structure of , the following intensity operator plays an important role in the proof of Theorem 5.1: for two Polish spaces and we define via

| (5.1) |

for . The intensity map closely relates relatively compact sets of its domain and its range in the sense of the subsequent lemma.

Lemma 5.2 (c.f. Lemma 5.7 in [31]).

Let and be two Polish spaces. For are the following equivalent:

-

(i)

is relatively compact.

-

(ii)

is relatively compact.

Proof of Theorem 5.1.

As we know by Theorem 3.10 that is isometrically isomorphic to , we obtain that is relatively compact if and only if the set is relatively compact. On the other hand, note that for , , and we have by the nested definition of that for all

Applying Lemma 5.2 yields equivalence of the following statements:

-

•

is relatively compact;

-

•

is relatively compact;

Hence, by applying this argument iteratively, we find that is relatively compact if and only if is relatively compact, which we wanted to show. The final assertion is a direct consequence of the classical Prokhorov’s theorem and the characterization of Wasserstein convergence in , see [94, Definition 5.8]. ∎

5.2. Denseness of simple processes

A canonical way of embedding into is the following: we can associate to each law the processes

| (5.2) |

where denotes the coordinate process on , and call this type of process plain. The set of all plain processes is denoted by .

Proposition 5.3.

Let be an arbitrary probability space, let be a -measurable map such that , and denote by the plain process associated to ; i.e. is given by (5.2) with . Then

| (5.3) |

satisfies . In particular, if are plain and , then .

Proof.

The coupling is bicausal between and as well as and . Thus . ∎

Among others, a purpose of this subsection is to show that the space of filtered processes naturally appears as the completion of all plain processes .

We call a probability space finite if consists of finitely many elements.

Theorem 5.4.

If has no isolated points, then the set

is dense in . In particular, the plain processes are a dense subset.

This theorem follows from the next proposition.

Proposition 5.5.

Let and let . Then there is

| (5.4) |

where for every , is a function of and is a finite subset of , such that

| (5.5) |

In particular, if has no isolated points, then can be chosen Markovian.

The proof relies on the following result, which is essentially shown in [32, Lemma 4.8]. Recall here that for , the term refers to where and are plain processes, see (5.2), distributed according to and , respectively. In a similar fashion, we will use here to denote the set of all bicausal couplings between the corresponding plain processes.

Lemma 5.6.

For each , let be an increasing family of finite subsets of Polish spaces such that and let be the map which assigns each point its nearest point in (with ties broken arbitrarily but measurably). Then, for any , we have

| (5.6) |

Proof.

For every , set

By [12, Lemma 1.4], (5.6) is equivalent to

| (5.7) | |||

| (5.8) |

as , where is some arbitrary but fixed element. For convenience, we choose .

If each were compact, (5.7) would follow directly from [32, Lemma 4.8]. However, compactness in [32, Lemma 4.8] was only used to additionally obtain the rate of convergence, and the same proof shows that in the present setting (5.7) holds true. As for (5.8), note that the reverse triangle inequality shows that

for every . Thus, decreases to zero as and is bounded by due to the definition of and . Dominated convergence shows that (5.8) holds and completes the proof. ∎

Proof of Proposition 5.5.

Consider and interpret as a path space. By Corollary 5.6 there is a family of laws on with

and for every , is finitely supported.

Fix and such that . Let , be the family of maps introduced in Corollary 5.6. We write . The maps and are both -measurable and

is a finite sub--algebra of . The filtered process is given as in (5.4) with process and filtration . By virtue of Lemma 2.2 it is readily verified that the coupling is bicausal between and

whence . Similarly, the coupling is bicausal between and

thus, and . By Theorem 3.10 we conclude

5.3. Martingales

Assume for this subsection that for each .

Proposition 5.7 (Martingales).

The set of all martingales

is closed w.r.t. .

There is a multitude of ways how to prove Proposition 5.7:

-

(i)

as a consequence of the continuity of Doob-decomposition (Proposition 6.8 below),

-

(ii)

as a consequence of the continuity of optimal stopping,

-

(iii)

as a consequence of Example 4.5,

-

(iv)

by characterizing martingales as those processes for which is concentrated on a particular closed subset of ,

-

(v)

or directly by coupling arguments.

We will present the last variant.

Proof of Proposition 5.7.

Let be a sequence in converging to . Fix , let and . By Lemma 2.2 and the martingale property of we have

Thus, letting , Jensen’s inequality yields that

As was arbitrary, is dominated by which is arbitrarily small for sufficiently large. Hence, showing that is a martingale. ∎

5.4. is a geodesic space

The purpose of this section is to show Theorem 5.10, and in particular that is a geodesic space. For concise notation, we shall assume throughout that for every (but see also Remark 5.13).

Definition 5.8 (Constant speed geodesic).

A family in is said to be a constant speed geodesic connecting if

-

(a)

and ,

-

(b)

for all .

A tangible way of defining constant speed geodesics is – in analogy to the classical -displacement interpolation – by means of geodesics on the state space and optimal couplings. To that end, recall that is the canonical space defined in Definition 3.1.

Definition 5.9 (Interpolation process).

Let and let . We call the family given by

| (5.9) |

the interpolation process between and (w.r.t. the coupling ).

The following is the main result of this section.

Theorem 5.10 (Filtered processes form a geodesic space).

Let .

-

(i)

The space is a geodesic space, that is, for every there is a constant speed geodesic connecting them.

-

(ii)

A family in is a constant speed geodesic between if and only if the family

is a -constant speed geodesic666 A family in is said to be a -constant speed geodesic connecting if , , and for every . between and .

-

(iii)

If is an optimal bicausal coupling for , then the interpolation process is a constant speed geodesic between and .

In a forthcoming paper, it will be shown that not only does the interpolation process constitute a geodesic, but actually all geodesics can be described as interpolation processes, at least once one is willing to allow for external randomization, that is, extending the probability space by independent randomness.

Proof.

We start by proving (i) and (ii). As is a geodesic space, it follows from [74] that is a geodesic space, too. Moreover, the product (endowed with the -norm) of two geodesic spaces remains geodesic, hence is a geodesic space. Repeating this argument inductively shows that a geodesic space. Claim (i) and (ii) now follow from the isometry between and given in Theorem 3.10.

We now show (iii). Bicausality of and Lemma 2.2 immediately show part (a) of Definition 5.8, and it remains to deal with part (b). To that end, note that the coupling is bicausal between and . Then, for every , as , we compute

| (5.10) | ||||

where the last equality holds by optimality of . A straightforward application of the triangle inequality shows that there cannot be strict inequality in (5.10), and whence the claim follows. ∎

The next example illustrates that even in case of geodesics between plain processes (c.f. (5.2)) it is necessary to consider general filtrations (instead of the filtrations generated by the processes).

Example 5.11.

Let . We consider two processes with paths in : and are the plain process associated to the laws (on the path space )

respectively. It is then easy to verify that there exists a unique constant speed geodesic and that it is given by the interpolation process of and w.r.t. the unique -optimal coupling . This coupling sends the mass from to and the mass from to . Therefore, at time , , is not a plain process, since

or put differently, even though we know at already precisely where we will end up at , thus, is not plain.

Theorem 5.12.

For , the set (of martingales in ) forms a closed, geodesically convex subset of .

For ease of exposition, we will only check that the set of martingales is geodesically convex when restricting to geodesics given by interpolation processes. Knowing that all geodesics can be characterized this way modulo an external randomization, this assumption can in fact be made without loss of generality. Alternatively, a proof via our description of geodesic processes as geodesics on in Theorem 5.10 is possible too, but less informative, and therefore left to the ambitious reader.

Simplified proof.

By Proposition 5.7, it remains to show that is geodesically convex. To that end, let and let be a constant speed geodesic connecting them, which, as already explained, is assumed to be given as the interpolation processes w.r.t. some .

We need to show that, for given fixed , the processes is a martingale, too. To that end, let and write

where we use bicausality of in the form of Lemma 2.2, and the martingale property of both and . Hence is a martingale which completes the proof. ∎

6. Continuity w.r.t. and applications

We have argued in the introduction that the weak adapted distribution governs ‘all’ probabilistic aspects of a stochastic process. In this section we highlight this claim, and further show that several (optimization) problems involving stochastic processes continuously depend on the adapted distribution. And moreover, that quantitative estimates w.r.t. are possible. Throughout this section we assume that for every .

6.1. Optimal stopping

Fix a non-anticipative function and set

| (6.1) |

for , where denotes the set of all -stopping times taking values in . In Example 4.5 we have already seen that is well-defined on in the sense that the value of does not depend on the choice of representative.

Proposition 6.1 (Optimal stopping).

Let such that and are integrable. Then we have

In particular, the following hold.

-

(i)

If is continuous bounded for every , then is continuous on w.r.t. the weak adapted topology.

-

(ii)

If is continuous and satisfies that for every and some , then is continuous on w.r.t. .

-

(iii)

If is Lipschitz for every , then is -Lipschitz on .

In Theorem 7.1 we will construct an example showing that the whole adapted distribution is required to control optimal stopping problems. Note that the non-quantitative version of Proposition 6.1 (i.e. continuity of optimal stopping for continuous that satisfies an adequate growth condition) already follows from Example 4.5.

Proof of Proposition 6.1.

The ‘in particular’ statement follows by symmetry from the first statement, so we shall only prove the first one. Its proof is similar to [12] and is included here for the convenience of the reader. Let and be a stopping time such that . Further let and, for every , define

By causality, c.f. Lemma 2.2, we have , hence

In conclusion we obtain

which, as and were arbitrary, yields the assertion. ∎

6.2. American options and robust pricing

Working in the setup of e.g. [29], stands for the (discounted) price of a financial asset at a time and denotes the current price. One assumes that there exists a family of European derivatives, described by a (continuous and linearly bounded) family of functions which are liquidly traded in the market, meaning that the respective prices are specified from externally given data. The set of all calibrated models consists of all martingales with mean which correctly reproduce the prices given by the market, i.e. in mathematical terms

| (6.2) |

A common assumption is

| (CC) | contains all call options written on and . |

Going back to a famous observation of Breeden-Litzenberger [37], this implies the following basic fundamental fact:

Proposition 6.2.

Under assumption (CC) the set is -compact.

A direct consequence is that for a further (continuous, linearly bounded) European derivative the set of possible arbitrage free prices consists of the interval , where the endpoints are attained for ‘extremal models’. Proposition 6.2 as well as various extensions of it play a crucial role for the duality theory as well as the characterization of extremal models in robust finance, see [33, 27, 54, 40] among many others.

A particular limitation of Proposition 6.2 is that it allows only to consider derivatives with a European payoff structure, but neglects derivatives with an American exercise structure, where the buyer may choose when to exercise and the buyers price in a model equals

| (6.3) |

Apart from a few important exceptions (see [26, 59, 8]) the robust finance literature is focused on the case of European derivatives. The simple reason is that going beyond the standard European case requires an adequate topology on processes with a non trivial filtration, which was hitherto unavailable. As derivatives with American exercise structure are more common than European derivatives it is highly desirable to extend the existing theory to this case. As a consequence of our results we obtain.

Proposition 6.3.

Assume that is a family of derivatives with linearly bounded continuous payoffs and European or American exercise structures. Under assumption (CC), the set is -compact. Moreover, for a European or American derivative with continuous linearly bounded payoff , the lower/upper pricing bounds for the derivative are attained.

6.3. Utility maximization

Let be an increasing concave (utility) function, and denote by the left-continuous version of the derivative. Denote by the set of all -predictable processes that are bounded by 1, and by the discrete-time stochastic integral of w.r.t. . For and , denote by the value of the utility maximization problem with random endowment , that is,

In [11, Theorem 1.8] it is shown that depends continuously on (w.r.t. ) when restricting to plain processes (i.e. to whose filtration is generated only by their paths). In the context of utility maximization, however, it is of central importance to also understand the effect that changes of the information/filtration of have to , and the following result extends [11, Theorem 1.8] to the general setting.

Theorem 6.4.

Let be Lipschitz continuous and assume that there exists such that . Then, for every there is a constant (depending only on , and the Lipschitz constant of ) such that

for every with .

Proof.

For simplicity, we assume that and focus on (i.e. is Lipschitz); the modifications needed for the general case are minimal and follow e.g. as detailed in [11]. Let be (almost) optimal for and let be (almost) optimal for . Define for every . Clearly is bounded by 1, and by bicausality of , is -measurable (see Lemma 2.2); hence . It follows that

By concavity of and Jensen’s inequality, followed by Lipschitz continuity of ,

where is the Lipschitz constant of . It remains to note that , hence . Reversing the roles of and proves the claim. ∎

Remark 6.5.

As explained in [11, Section 3.3], in the context of optimization problems involving stochastic integrals and (semi-)martingales, it is more natural to define with a different cost function instead of , namely with where denotes the Doob-decomposition, the quadratic variation, and the first variation norm. Clearly, this modification of is also possible (and reasonable) in the present setting.

6.4. Stochastic control

Optimal stopping and utility maximization are basic stochastic control problems involving processes and we have shown in Proposition 6.1 and Theorem 6.4 that their values are continuous w.r.t. the adapted Wasserstein distance. As it happens, this is the general principle for stochastic control problems.

For example, if is convex in the second and third argument, a similar reasoning as used for the proof of Theorem 6.4 shows that under suitable continuity and growth assumptions on ,

is (locally Lipschitz) continuous w.r.t. .

We refer to [11] for a more elaborate analysis of such problems in a mathematical finance context. In particular, using the results of the present paper, the results of [11] for the stability of superhedging, risk based headging and utility indifference pricing (which are formulated only for processes endowed with their raw filtration) extend to processes with arbitrary filtrations.

6.5. Conditional McKean-Vlasov control

Denote by the set of all -adapted processes that are bounded by 1 and let be a discrete-time Brownian motion777That is, , and for every the increments are standard normal and independent of .. For consider the controlled process , defined recursively via and

where is some fixed continuous function prescribing the dynamics of . Further let be continuous and consider the McKean-Vlasov control problem in its weak formulation:

| (6.4) |

we refer to [84] for more background on problems of the type (6.4). Based on Prokhorov’s theorem for filtered processes, it is straightforward to show that a solution to (6.4) exists:

Proposition 6.6.

The infimum over all Brownian motions and controls in (6.4) is attained.

Sketch of proof.

Let be a minimizing sequence for (6.4) (in particular, ), and set . By Theorem 5.1, the set is relatively compact, hence there exists

such that (potentially after passing to a subsequence) . It is straightforward to verify that is a Brownian motion and that . Further, since each is continuous,

as . The claim now readily follows form continuity of . ∎

6.6. Weak optimal transport

Motivated by applications to functional inequalities, Gozlan et. al. [53] introduced the weak optimal transport problem, which extends classical transport to ‘non-linear’ costs . Given marginal distributions on , the task is

| (WOT) |

Weak transport preserves enough structure from the classical case to allow for a useful theory while being sufficiently general to capture many problems that lie outside the scope of transport theory, see [20] for an overview. Cornerstone results in weak optimal transport (existence of optimizers, duality, geometric characterization of optimal couplings, stability in the data) were shown in the generality of classical transport only in [17, 3, 31], relying on two-period results of the current article and the two period version of Theorem 1.7. In analogy to classical transport, the key idea is to relax (WOT) and consider

| (6.5) |

By Theorem 1.7 this is an optimization over a compact set which of course admits minimizers under the usual assumption of lower semi-continuity. Indeed (6.5) can be viewed as a classical linear optimization problem over probabilities on .

In several weak transport problems it is natural to consider not just two marginal constraints, but arbitrarily many (relaxed martingale transport [54], robust pricing of VIX-futures [55], model-independence in fixed income markets following [3], multi-marginal Skorokhod embedding [41, 28]). In view of this, we propose the -marginal weak transport problem

| (6.6) |

As above this is an optimization problem over a compact set, which corresponds to a linear optimization problem of probabilities on , susceptible to classical convex analysis.

6.7. -barycenters

The -barycenter of two stochastic processes is the minimizer of

Clearly, this minimization problem is attained by the connecting constant speed geodesic at time (which exist thanks to Theorem 5.10). More generally, one can ask whether a distribution on the stochastic processes has an -barycenter , that is, a minimizer of

| (6.7) |

Theorem 6.7.

Let . Then there exists minimizing (6.7).

Proof.

Corollary 3.12 implies that is lower semicontinuity w.r.t. the weak adapted topology. Hence, it follows that

is lower semicontinuity on w.r.t. the weak adapted topology. Since for if and only if , it suffices to show relative compactness of the sublevel set

| (6.8) |

where , in the weak adapted topology. Note that the moments of can be controlled as follows:

| (6.9) |

By Theorem 5.1, relative compactness of the set (6.8) is equivalent to tightness of the laws. Tightness of (6.8) follows from standard arguments since the -moments are uniformly bounded by (6.9) and is compact for . ∎

6.8. The Doob-decomposition

Our final example deals with continuity of the Doob-decomposition. Recall that the Doob-decomposition of a filtered process is given by

where is the unique decomposition of such that , is a martingale and is -predictable. (Of course, is a sub-martingale if and only if the process is increasing.)

Proposition 6.8.

The following chain of inequalities holds888The processes takes values in which we endow with the norm .

| (6.10) |

for all , where is a constant depending only on and .

Recall that the predictable process of the Doob-decomposition of is given by

for and . Thus, can be viewed as an adapted function of rank 1, that is and similarly . Building upon this observation, it is not hard to deduce -continuity of .

Proof of Proposition 6.8.

Fix and note that, as the filtration of a filtered process and its Doob-decomposition coincide by definition, we have that

The first inequality in (6.10) is immediate from Jensen’s inequality. The triangle inequality together with Jensen’s inequality show

| (6.11) |

By definition of and we have for

Again, Jensen’s inequality implies

| (6.12) |

for every . In conclusion, suitably combining (6.11) and (6.12) leads to the second inequality in (6.10). ∎

6.9. Numerical and statistical aspects

In view of applications, the numerical computation of the adapted Wasserstein distance is of crucial importance and has been recently studied in [87, 44, 25]. In fact, these papers consider more general adapted transport problems between stochastic processes and of the form

| (6.13) |

where is a continuous function. In order to briefly explain the methodology, suppose that the processes and are both discrete, i.e. plain and only take finitely many values. (We remark that for general processes and that are not necessarily discrete, one may replace them first by discrete approximations e.g. as in Proposition 5.5). In this case, solving (6.13) is equivalent to solving a linear program (see e.g. [80, Section 8] and [44, Section 3.4] for more details). The recursive structure of bicausal couplings allows to solve the linear program via a dynamic programming principle (DPP) involving one-step classical optimal transport problems (see [81, Chapter 2.10.3]). In the current setting, the value functions are recursively given by

for with the convention that and . Then is precisely the optimal value (6.13) and the values of can be computed efficiently e.g. via Sinkhorn’s algorithm (see [87]). Based on the DPP formulation, a fitted value iteration method is proposed in [25]. There the value function of the DPP is iteratively empirically estimated and then approximated by neural networks that minimize an empirical loss. Another recent approach builds on establishing a bicausal version of the Sinkhorn algorithm (see [44]). For comprehensive comparisons of these methods, we refer to [44] and [25]. Furthermore, in [98], a minimax reformulation is proposed where the infimum is taken over all couplings and the supremum over an adequate class of functions penalizing the causality constraint. Both families of functions are then parametrized by neural networks and trained by an adversarial algorithm. In a continuous time framework, [35] establishes a Hamilton-Jacobi-Bellman equation for the value function.

The estimation of processes w.r.t. from statistical data was studied in [13] under the assumption of bounded values and later extended in [4] (see also [83, 52]). Roughly put, while the classical empirical measure does not converge to its population counterpart in the weak adapted topology (nor do e.g. the values of the corresponding optimal stopping problems) one can construct a modified empirical measure (based on clustering ideas) which does converge in the weak adapted topology. In fact, the rate of convergence of that estimator (w.r.t. ) is similar to the (optimal) rate of convergence of the classical empirical measure (w.r.t. ).

7. An important example

Fix and recall that, by Theorem 4.11, the relation is equal to the relation , which again coincides with the relation induced by .

A natural question left open in Section 4 and Section 5 is what rank of the adapted distribution is necessary to govern probabilistic properties of stochastic processes. For instance, we have seen in Example 4.5 that the adapted distribution of rank 1 suffices for preserving the notion of being a martingale. However, we will see that rank 1 equivalence is not sufficient in general. Rather Theorem 4.11 is sharp: does not imply . In fact, we show that there exist filtered processes that are equivalent but lead to different values for an optimal stopping problem.

Theorem 7.1.

Let . There exist with and a bounded, continuous non-anticipative function such that (compare (6.1) for the definition of ).

In particular, using Proposition 6.1 and Theorem 4.11, this implies that . More generally, we will show in the following that as long as , the relation strictly refines the relation .

Proposition 7.2.

Let and let . Then there are with representatives defined on the same filtered probability space such that

-

(i)

for every ,

-

(ii)

for some .

The processes and will be constructed on a common probability space consisting of atoms, satisfy and for , and only their respective filtrations will differ.

7.1. Proof of Proposition 7.2

This section is devoted to the proof of Proposition 7.2 which will then be used to establish Theorem 7.1. In fact, we shall first concentrate on Proposition 7.2 with , and later conclude for general via a simple argument.

The construction of and is recursive, and we shall start with . Consider the probability space consisting of two elements, say , with the uniform measure, and let be the identity map, that is, . Now define the filtered processes and via

Then the following holds.

Lemma 7.3.

and satisfy the claim in Proposition 7.2 for .

Proof.

Adapted functions of rank depend only on the process itself and not on the filtration, hence for all . That is, part (i) of Proposition 7.2 is true. On the other hand, one computes

for every bounded, measurable function . Now define by

so that has rank . Then

As , this proves the second part of Proposition 7.2. ∎

Now assume that, in a -time step framework, we have constructed filtered processes and which satisfy Proposition 7.2 (where ). We shall construct new filtered processes and in an -time step framework for which the statement of the lemma remains true. At this particular instance the superscript ‘’ stands for ‘new’.

At this point, we enrich the filtered probability space of and by an independent random variable (i.e. is independent of ) in the following manner: When denotes the probability space of and , we consider the new probability space

| (7.1) |

We write for the projection onto the first coordinate. In other words, we can think of as a coin-flip which is independent of everything that was constructed so far. Further we view as a filtration on (7.1); similarly for (recall here that are the trivial -algebras by convention). Then, by slight abuse of notation, we can view and as processes defined on , namely be identifying with and filtration and similarly for . By independence of , this clearly does not affect any properties of the processes. Define the processes and on the probability space (7.1) via

for . One can check that and are indeed filtrations and that, for every -integrable random variable which is independent of , we have that

| (7.2) | ||||

for every . We spare the elementary proof hereof.

Lemma 7.4.

For and we have

| (7.3) |

In particular, .

Proof.

The proof is by induction over : for , the statement is trivially true (recalling that ).

Now assume that it is true for (with ), and let . First assume that is formed by (AF3) only. By assumption we have

| (7.4) |

Now use independence of and and (7.4) to compute

where the last three equalities are due the fact that and satisfy Proposition 7.2, that is, . The same computation is valid for , whence we have (7.3) for this particular choice of . Finally, by Lemma 4.2, this extends to all , not necessarily those formed solely by (AF3). ∎

Lemma 7.5.

For we have

| (7.5) |

Proof.

Lemma 7.6.

and satisfy the claim in Proposition 7.2 with .

Proof.

At this point we have completed the proof of Proposition 7.2 under the additional assumption that . For general , construct and for the -time step framework as above. Recursively repeating the argument detailed below (7.1), we can append trivial time steps to the processes and , and thereby obtain -time step processes with the desired properties. This proves Proposition 7.2 for arbitrary .

7.2. Proof of Theorem 7.1

As already announced, we use the processes and (and the notation specific to these processes) constructed for the proof of Proposition 7.2

The proof will be inductive, starting with . Consider the cost function ,

The dynamic programming principle for the optimal stopping problem (also called ‘Snell envelope theorem’) tells us that the optimal stopping values are

This proves the claim for .

For the case of general , recall that and are the processes obtained through the -step processes and and an independent coin-flip .

By the previous step, we assume that in a -step framework we have constructed a cost function such that . Defining the new cost function in the -step framework by

we claim that .

To that end, we once more rely on the dynamic programming principle to obtain

| (7.6) |

Similarly, additionally using that is trivial and is deterministic, we get

| (7.7) |

In order to relate the conditional stopping problems after time 2 appearing in (7.6) and (7.7), recall that we view and as -time step processes by appending a trivial initial time step; see the explanation right after (7.1). The same convention is applied here to as well.

In a first step we show the following decomposition of stopping times:

| (7.8) |

The right-hand side is clearly contained in the left-hand side. For the reverse inclusion, pick . By definition of , there are sets and such that

for every . One can then check that

define stopping times in and , respectively, and that . This shows (7.8).

We are now ready to finish the proof. Recalling that is the trivial -algebra and that for , independence of and and the decomposition of stopping times (7.8) shows that

In a similar manner

As , plugging the above equalities in (7.6) and (7.7) readily shows and thus completes the proof.

Acknowledgements: Daniel Bartl is grateful for financial support through the Austrian Science Fund (FWF) projects ESP-31N and P34743N. Mathias Beiglböck is grateful for financial support through the Austrian Science Fund (FWF) projects Y0782 and P35197.

References

- [1] B. Acciaio, J. Backhoff, and G. Pammer. Quantitative Fundamental Theorem of Asset Pricing. Sept. 2022. arXiv:2209.15037 [q-fin].

- [2] B. Acciaio, J. Backhoff-Veraguas, and A. Zalashko. Causal optimal transport and its links to enlargement of filtrations and continuous-time stochastic optimization. Stochastic Process. Appl., 130(5):2918–2953, 2020.

- [3] B. Acciaio, M. Beiglböck, and G. Pammer. Weak transport for non-convex costs and model-independence in a fixed-income market. Math. Finance, 31(4):1423–1453, 2021.

- [4] B. Acciaio and S. Hou. Convergence of adapted empirical measures on . 2022.

- [5] B. Acciaio, A. Kratsios, and G. Pammer. Designing universal causal deep learning models: The geometric (hyper) transformer. Mathematical Finance, 2023.

- [6] M. Agueh and G. Carlier. Barycenters in the Wasserstein space. SIAM J. Math. Anal., 43(2):904–924, 2011.

- [7] S. Akbari, L. Ganassali, and N. Kiyavash. Learning causal graphs via monotone triangular transport maps. arXiv preprint arXiv:2305.18210, 2023.