Information projection approach to propensity score estimation for handling selection bias under missing at random

Summary. Propensity score weighting is widely used to improve the representativeness and correct the selection bias in the voluntary sample. The propensity score is often developed using a model for the sampling probability, which can be subject to model misspecification. In this paper, we consider an alternative approach of estimating the inverse of the propensity scores using the density ratio function satisfying the self-efficiency condition. The smoothed density ratio function is obtained by the solution to the information projection onto the space satisfying the moment conditions on the balancing scores. By including the covariates for the outcome regression models only in the density ratio model, we can achieve efficient propensity score estimation. Penalized regression is used to identify important covariates. We further extend the proposed approach to the multivariate missing case. Some limited simulation studies are presented to compare with the existing methods.

Keywords: Calibration estimation; Density ratio model; Self-efficiency; Missing data

1 Introduction

In statistical analysis using sample data, the concept of representativeness is crucial. The fundamental issue is that the final sample might be subject to selection bias and might not accurately reflect the target population. A naive analysis that ignores selection bias can produce incorrect results. Another way to frame the selection bias problem is as a missing data problem. Making valid statistical inference with missing data is a fundamental problem in statistics (Little and Rubin, 2019, Kim and Shao, 2021).

The propensity score (PS) weighting approach is widely used for adjusting the selection bias in the final sample. Frequently, the propensity score is calculated using the selection probability model. In principle, regression models for binary responses, such as logistic regression, can be used to estimate the selection probability in the presence of observed auxiliary data. The target parameter can then be estimated using an inverse probability weighting estimator to provide an unbiased estimate. However, correctly specifying the propensity score model can be tricky, and we frequently lack sufficient understanding of the selection mechanism. Furthermore, the final estimation can be unstable when some propensity scores are close to zero (Ma and Wang, 2020). The bias and variance of the resulting estimator are likely to be amplified by the nature of such an ‘inverse’ fashion.

The existing methods for propensity score estimation are either based on the maximum likelihood method (Rosenbaum and Rubin, 1983, Robins et al., 1994) or calibration method (Folsom, 1991, Tan, 2010, Kott and Chang, 2010, Graham et al., 2012, Hainmueller, 2012, Imai and Ratkovic, 2014, Chan et al., 2016, Zhao, 2019). The calibration method can also be justified under an outcome model, which gives a doubly robust flavor. However, the objective function for calibration estimation is not fully agreed.

In this paper, we introduce the self-efficiency condition as a new paradigm for PS estimation. The self-efficiency condition means that the resulting PS estimator is equivalent to the prediction-based estimator using the outcome response model. Due to the equivalence, the self-efficient propensity score estimator is more efficient than existing approaches. To build a self-efficient PS estimation, we first model density ratios with information projection (Csiszár and Shields, 2004), which minimizes the Kullback-Leibler divergence measure for models with moment constraints on the balance scores. Density ratio models are widely employed to address classification and two-sample problems (Qin, 1998, Nguyen et al., 2010, Chen and Liu, 2013). To our best knowledge, however, it has not been studied in the context of correcting selection bias. Once the density ratio model has been constructed using the information projection approach, the model parameters can be estimated using the empirical likelihood technique (Qin and Lawless, 1994).

The self-efficient PS estimation is also closely related to weight smoothing. Information projection of the density ratio function combined with calibration estimation is used to accomplish weight smoothing. We give some asymptotic theories for the smoothed PS estimator utilizing the balance score function. The proposed estimator is doubly robust and locally efficient in the sense of Robins et al. (1994). By applying the weight smoothing based on the covariate in the outcome model, we can achieve the efficiency gain. In addition, a two-step estimation approach is designed to facilitate parameter estimation computation. Variance estimation of the PS estimator can be implemented using either the linearization method or bootstrap.

Furthermore, the proposed paradigm includes discussing propensity score estimation in high-dimensional covariate scenarios. When there are more auxiliary variables than we require, the PS estimator can be inefficient. Only significant covariates for the outcome model should be included in the log density ratio model for effective PS estimation. We consider penalized regression to identify important covariates. Given the observed study variable and the corresponding auxiliary variables, we can implement penalized regression methods to select important covariates and obtain an efficient PS estimator.

Finally, using the proposed framework, the PS estimation can be easily extended to handle multivariate missing data. We can partition the sample into multiple groups based on missing patterns and apply the density ratio estimation method to obtain the inverse propensity scores. By constructing a self-efficient PS estimation, we can combine information from multiple sources with different missing patterns.

The paper is organized as follows. In Section 2, the basic setup is introduced. In Section 3, the proposed method is developed using the information projection technique. In Section 4, its asymptotic properties are investigated. In Section 5, the proposed method is extended to handle high dimensional covariate cases. In Section 6, an extension to multivariate missing data setup is developed. Two limited simulation studies are presented in Section 7 to compare with other existing methods and to understand the effect of choice of calibration variables. Concluding remarks are made in Section 8.

2 Basic Setup

Suppose that the parameter of interest can be written as the unique solution to , where is the study variable that is subject to missingness, is the auxiliary variable that is always observed, and is a smooth function of with nonsingular gradient matrix . Thus, the joint density of is completely unspecified except for the moment condition . We further assume that the second moments of exist.

Suppose we have an independently and identically distributed realization of , denoted as . Since is subject to missingness, the actual dataset is , where is the sampling indicator variable defined as

We assume that the sampling mechanism is missing at random (MAR) in the sense of Rubin (1976). That is,

| (1) |

Under MAR, we are interested in finding the propensity weights such that the solution to

| (2) |

leads to consistent estimation of . Equation (2) is called the propensity score equation. One popular choice for is

| (3) |

There are two problems with the choice in (3). First, we do not know the true propensity score function . Second, the resulting estimator is not necessarily efficient. To resolve these problems, we may consider the following conditions:

| (4) |

where is the best predictor of for . Condition (4) is attractive as the solution to the PS estimating equation in (2) is equivalent to the expected estimating equation, which leverages the best predictors of the unobserved parts of the population estimating equation. We call condition (4) self-efficiency condition, as we can obtain an efficient estimator of by solving the expected estimating equation (Wang and Pepe, 2000). The term “self” is employed to emphasize that efficiency is achieved without including additional terms to the propensity score equation.

To compute the conditional expectation in (4), one could make an extra assumption on the outcome model and estimate the parameters in the model. To avoid the difficulty associated with the modeling for , we assume that

| (5) |

for some . Once condition (5) is met, the additional modeling for can be omitted. Under (5), by taking the conditional expectations on both terms in (4), we can check that the self-efficiency condition implies

| (6) |

where is a vector of basis functions in . Thus, the self-efficient propensity score method achieves the balancing property for . The balancing property is also called calibration property in survey sampling (Deville and Särndal, 1992, Fuller, 2009, Wu and Thompson, 2020).

Another implication of the self-efficiency is related to weight smoothing. Note that, under assumption (5), the self-efficiency condition in (4) implies that is a function of , which means that the final PS weights are functions of the covariates in the outcome regression model. By including the covariates in the outcome model only, we can achieve weight smoothing and efficient estimation.

Thus, under assumption (5), it makes sense to impose the self-efficiency for obtaining the propensity weights. How to uniquely determine to satisfy the self-efficiency condition is our main research problem. We address this problem by introducing the density ratio function and information projection in the next section.

3 Proposed method

3.1 Density ratio function

To introduce the density ratio function, we use to denote generic density functions. Further, let denote the conditional density of given for . Using this notation, we define the following density ratio function:

By Bayes theorem, we obtain

Assuming is known, we can express

| (7) |

and use

as the propensity score weight for unit with . So, our propensity score weighting problem reduces to density ratio function estimation problem. Note that we can easily estimate by , and .

Let be a vector of basis functions of . Condition (5) implies that, as far as estimation of is concerned, the MAR condition holds conditional on , that is,

| (8) |

According to Rosenbaum and Rubin (1983), in (8) is called the balancing score function.

Using satisfying (8), we can construct

| (9) |

where is the true density ratio function. To distinguish from the original density ratio function , we may call the smoothed density ratio function in the sense that it satisfies

| (10) |

Thus, the smoothed density ratio function is regarded as a low-dimensional projection of onto the space satisfying (10).

We can use in (9) to construct a smoothed PS estimating function of as follows:

| (11) |

Furthermore, since is a function of only, we obtain

| (12) |

where is the true density ratio function. Note that result (12) implies that

where

Therefore, we can establish the following result.

Proposition 1

Proposition 1 implies that the solution to is more efficient than the solution to . Such phenomenon has been recognized by Little and Vartivarian (2005), Beaumont (2008), Kim and Skinner (2013) and Park et al. (2019). To find a model of the smoothed density ratio function in (9), we introduce information projection in the following subsection.

3.2 Information projection

To motivate the proposed method, suppose that we have two probability distributions , with absolutely continuous with respect to . For simplicity, we also assume that are absolutely continuous with respect to Lebesgue measure , with density with support , for . The Kullback-Leibler divergence between and is defined by

Finding the density ratio function can be formulated as an optimization problem using the KL divergence. Specifically, we wish to minimize

| (15) |

with respect to satisfying some moment conditions of the variables that are available from the whole sample. Let be the given balancing score obtained from assumption (5). Because are observed throughout the sample, we can estimate from the sample. Given , to utilize the auxiliary information, we have

| (16) |

where . Thus, we wish to find the minimizer of in (15) subject to the constraint in (16). The following lemma gives the form of the solution to the optimization problem.

Lemma 1

The solution (17) is obtained using the information projection method in information geometry. Roughly speaking, constraint in (16) is a moment condition on to satisfy (9). Thus, we can use Lagrange multiplier method to obtain the solution as an exponential tilting form. Note that (17) is equivalent to assuming a model for the density ratio function. That is, our model is

| (18) |

where is the normalizing constant satisfying

By (7), the log-linear density ratio model (18) is equivalent to the logistic regression model for the sample selection probability

| (19) |

Thus, our framework provides another justification of the logistic regression model for the sample selection probability that has been considered in Folsom (1991), Kott (2006), and Tan (2020), among others. But, the parameter estimation discussed in §3.3 is different from the existing methods. Also, the covariates in the parametric model in (19) is derived from the outcome model assumption in (5). Nonetheless, including other covariates in the calibration weighting can make the resulting PS estimator robust against model misspecification (Han and Wang, 2013, Chan et al., 2014, Chen and Haziza, 2017, Yang et al., 2020).

3.3 Model parameter estimation

We now wish to estimate the parameters in the log-linear density ratio model in (18) and estimate . Note that the parameter is defined through , which can be expressed as

| (22) |

as an integral equation for , where and satisfy the constraints (20) and (21).

To estimate the parameters, we use

to find the minimizer of among satisfying the integral constraints (20), (21), and (22). The problem can be formulated as an optimization problem using the empirical likelihood (EL) method of Qin and Lawless (1994). In the EL method, a fully nonparametric density can be assumed to replace in the integral equations. That is, we maximize

subject to

| (23) |

| (24) |

| (25) |

and

| (26) |

The solution to the above optimization problem lead to and we obtain the profile empirical likelihood

| (27) |

The maximizer of can be used as the final estimator of . However, such a joint optimization of and is computationally expensive.

To introduce an alternative computation, note that the form of the smoothed propensity weights

depends on only through . Thus, we can first exclude (25) in the EL optimization to remove the dependency on in and then obtain by solving for . This two-step procedure will greatly simplify the computation.

Note that maximizing subject to (23) only gives . Imposing (24) and (26) to the unconstrained optimization does not play any role on the final solution because and are unknown. Thus, the solution to the optimization problem remains the same:

with and satisfying

| (28) |

which is a calibration equation for .

Once the model parameters in (18) are estimated, we can compute the smoothed propensity score estimating function

| (29) |

where

| (30) |

and and are computed from (28). The final estimator of is obtained by solving

The proposed propensity score estimating function in (29) satisfies the self-efficiency. To see this, without loss of generality, assume that is a scalar. Note that, for a fixed , we can write

| (31) |

where and for any . Now, since , the smoothed PS estimator in (31) is algebraically equivalent to

| (32) |

The second term in the right hand side of (32) is zero at where satisfies

Thus, we have

| (33) |

Therefore, the proposed estimator satisfies the self-efficiency condition in (4).

Equation (33) means that the final inverse propensity weights do not directly use the regression model for prediction, but it implements regression prediction indirectly. Thus, the smoothed PS estimator incorporates the outcome regression model through calibration equation in (28) and achieves the self-efficiency. On the other hand, model calibration of Wu and Sitter (2001) uses the outcome model directly in the calibration equation. Similar ideas have been considered in the context of nonparametric calibration estimation in survey sampling. For examples, Montanari and Ranalli (2005) used a single-layer Neural Network model and Breidt et al. (2005) used penalized Spline model for nonparametric calibration estimation.

Remark 1

Assumption (5) states that the basis functions do not depend on , which does not always hold. If the basis functions in (5) depends on , that is,

| (34) |

we can use the following iterative procedure.

-

1.

Given the current parameter estimate , find , for , such that (34) holds for .

-

2.

Estimate the parameter in

(35) by apply the calibration equation on .

-

3.

Use

to find the solution to

-

4.

Set and goto Step 1 until convergence.

This is essentially an extension of the EM algorithm (Dempster et al., 1977) applied to regression model. Step (a)-(b) corresponds to the E-step and Step (c) corresponds to the M-step. In the E-step, instead of using a parametric model, we use the information projection to compute the conditional expectation under assumption (5).

4 Statistical properties

We now discuss the asymptotic properties of the smoothed PS estimator which is the solution to using in (29). To formally discuss the asymptotic properties of , let be the estimating function for . By (28), we can express

| (36) |

where . Let be the true parameter value in the log-linear density ratio model in (18) so that . By the constraint in (16), we have , where the reference distribution is the conditional distribution of given . The unbiasedness of can also be derived under the selection probability model associated with (18). That is, under the selection probability model

| (37) |

we can also obtain .

Thus, as long as the sufficient conditions for are satisfied, we can establish the weak consistency of and apply the standard Taylor linearization to obtain the following theorem, where is the true value of parameter in model (18).

The regularity conditions and the proof are presented in the Supplementary Material.

Theorem 1

Assume that density ratio model (18) holds. Under the regularity conditions described in the Supplementary Material, we have

| (38) |

where , , and is the probability limit of the solution to

| (39) |

By Theorem 1, we can obtain, ignoring the smaller order terms,

| (40) |

where . Under the selection probability model (37), the first term of (40) has zero expectation. Also, if the regression outcome model satisfies

| (41) |

then we obtain and the second term of (40) has zero expectation. Thus, expression in (40) gives the doubly robust property (Bang and Robins, 2005, Tsiatis, 2007, Cao et al., 2009, Kim and Haziza, 2014) in that the resulting estimator is justified either the outcome regression model or the selection probability model is correctly specified.

Corollary 1

Remark 2 (Remark 2)

The variance term in (43) deserves a further discussion. Let be the true selection probability. We may use the true selection probability to construct a doubly robust estimator of the form

| (44) |

By Jensen’s inequality, we can obtain

| (45) | ||||

Thus, the smoothed PS estimator is more efficient than the doubly robust estimator in (44). Furthermore, if the selection probability model satisfies (37), we have equality in (45) and the smoothed PS estimator is locally optimal in the sense that it achieves the variance lower bound of Robins et al. (1994).

Remark 3 (Remark 3)

Condition (41) is a critical condition for the validity of the proposed estimator. If the space is large enough, then (41) is likely to be satisfied and result (42) will hold. However, if is too large, then we can find such that . In this case, we can construct a smoothed density ratio function using the basis functions in only. By Remark 2, it is more efficient than the smoothed PS estimator using the basis function in . Therefore, including unnecessary calibration variables in the calibration equation will increase the variance. This is consistent with the empirical findings of Brookhart et al. (2006) and Shortreed and Ertefaie (2017). We will discuss this result further in Section 5. See also the second simulation study in Section 7.2.

We now discuss variance estimation. Using (38), we obtain

| (46) |

where ,

and are the solution to

for all .

Now, the variance estimation of can be constructed from (46). Specifically, let

where are the solution to

for all . The linearization variance estimator is then written as

where , , and .

The empirical likelihood approach also provides a way to develop a likelihood ratio test for parameters in a completely analogous way to that for parametric likelihoods. Let be the profile empirical log-likelihood in (27) under constraints (23), (24) and (26). Further, define the profile empirical likelihood

| (47) |

We have the following result.

Theorem 2

Under regularity conditions in the Supplementary Material,

| (48) |

as , where is obtained from the two-step procedure and is the true parameter.

For the empirical likelihood ratio test for can also be developed similarly to Qin and Lawless (1994).

5 Dimension Reduction

We now consider the case of . In Section 4, we have seen that either lies in the linear space or is the basis for logistic regression (37) can give the root--consistency of the proposed estimator. However, as pointed out in Remark 3, including other -variables outside the outcome model into may lead to efficiency loss.

To explain the idea further, we assume that , where is an index set for a subset of . The following lemma presents an interesting result.

Lemma 2

If MAR condition in (1) holds and the reduced model for holds such that

| (49) |

for , then we can obtain the reduced MAR given . That is,

| (50) |

Note that (50) is a special case of the reduced MAR in (8) using as the balancing score function. In the spirit of Remark 3, we can see that the smoothed PS estimator using is more efficient than the PS estimator using . Therefore, it is better to apply a model selection procedure to select the important variables which satisfies (49).

To find satisfying (49), we utilize two-stage estimation strategy to complete the smoothed propensity score function:

-

1.

Step 1: Use a penalized regression method to select the basis function for the regression of on .

-

2.

Step 2: Use the basis function in Step 1 to to obtain the calibration equation in (28) and construct .

In the first stage, we adapt the penalized estimating equations (Johnson et al., 2008) to select important covariates in the outcome model. Generally speaking, we utilize an -estimator in the outcome model and we denote the corresponding score function as . For example, can be written as

| (51) |

where . The penalized estimating equations can be written as

| (52) |

where , is a continuous function and is an elementwise product between two vectors. Further, let . In M-estimation framework, usually serves as a penalization function. Various penalization functions can be used but we only consider the smoothly clipped absolute deviation function (SCAD) (Fan and Li, 2001). In particular,

| (53) |

where , is the indicator function and is constant specified as in Fan and Li (2001). Further, we let to denote the variable index set selected after SCAD procedure. Here we use a working model to select the variables. According to Johnson et al. (2008), under some regularity conditions, we have

| (54) |

which constructs the model selection consistency. After the first stage, we now obtain the important variable set .

In the second stage, we use the selected variables to compute the smoothed density ratio function. That is, use

The resulting PS estimator is then computed by

with .

Corollary 2

Suppose that the assumptions for Theorem 1 hold. Also, the additional assumptions listed in the Supplementary Material hold. If satisfies , then we obtain, with probability goes to 1,

| (55) |

where

By Corollary 2, we can safely ignore the uncertainty due to the model selection in the first step. The asymptotic results in (55) is based on the model selection consistency in (54). That is, if we define where is obtained from the first stage procedure, the linearization in (55) is conditional on . By (54), we obtain and the limiting distribution of given , denoted by , is asymptotically equivalent to . See also Theorem 1 of Yang et al. (2020) for a similar argument.

6 Multivariate missing data

We now consider the case of multivariate study variables, denoted by , and they are subject to missingness. There are possible missing patterns with study variables. Let be the realized number of different missing patterns in the sample. Thus, the sample is partitioned into disjoint subsets with the same missing patterns. The parameter of interest is defined through , where .

Let be the -th subset of the sample from this partition. We assume that consists of elements with complete response and that is nonempty. Without loss of generality, we may define if and otherwise. We wish to construct an estimating function using all available information:

where is the observed part of for . Instead of using a model for each conditional distribution, we can use the density ratio model such that

| (56) |

for . Condition (56) is the self-efficiency condition in (4).

To construct the density ratio function satisfying (56), we first find such that . Thus, using the I-projection idea in Section 3, we may assume

| (57) |

as the log-linear model for density ratio function. The model parameters in (57) can be estimated by calibration equation derived from (56) and model assumption (57):

with respect to for , where is a vector of for .

Now, the smoothed PS estimator of can be obtained by solving

| (58) |

where

is the final weights for PS estimation.

To investigate the asymptotic behavior of the solution to (58), the density ratio for missing pattern can be simplified as , for . Let the true parameter of interest be and the true parameter for density ratio be . Then we have the following theorem.

Theorem 3

Under the regularity conditions stated in the Supplemtentary Material, for multivariate missing case, the solution to (58) satisfies

where

| (59) | ||||

, and is the probability limit to the solution of

The above theorem depicts the asymptotic behavior of our proposed estimators in multivariate missing case. Its proof is presented in the Supplementary Materials.

7 Simulation Study

7.1 Simulation Study One

Two limited simulation studies are performed to check the performance of the proposed method. In the first simulation study, we compare the proposed method with other existing methods under the MAR setup with few covariates. The setup for the first simulation study employed a factorial structure with two factors. The first factor is the outcome regression (OR) model that generates the sample. The second factor is the response mechanism (RM). We generate and based on the RM first. We have two different setup for the response mechanism as follows:

-

•

RM1 (Logsitic model):

-

•

RM2(Gaussian mixture model):

Once and are generated, we generate from two different outcome models, OR1 and OR2, respectively. That is, we generate from

-

•

OR1:

-

•

OR2:

Here, .

From each of the sample, we compare four different PS estimators of :

-

1.

The proposed information projection (IP) PS estimator using the maximum entropy method in Section 3 using as the control variable for calibration. Thus, the proposed PS estimator can be written as where is of the form in (30) with

(60) -

2.

The classical PS estimator using maximum likelihood estimation (MLE) of the response probability with Bernoulli distribution with parameter .

- 3.

- 4.

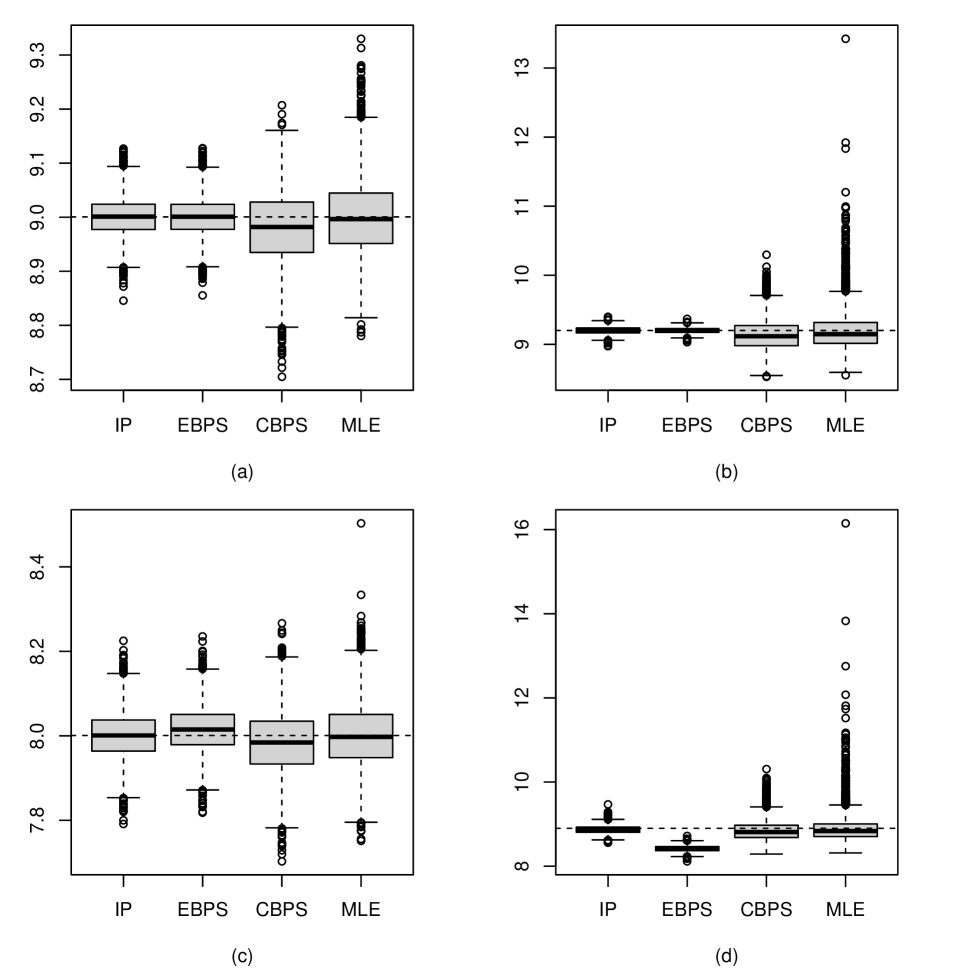

To check the performance of the four estimators, we use sample size with Monte Carlo samples. The results are presented in Figure 1, where IP is our proposed method.

When we use as the calibration variable, OR1 matches with the working outcome model and RM1 matches with the working response model. Among the four methods considered, our proposed method and EBPS method perform better than the other two methods. Entropy balancing propensity score method also shows good performances when OR1 or RM1 is true as it is doubly robust, but when both models fail (i.e. OR2RM2 setup), the performance is really poor. Our proposed method is also doubly robust and it performs reasonably well even when both models fail. Note that our proposed PS weights can be written as

Thus, the PS estimator of can be expressed as

where

Thus, the proposed PS estimator can be expressed as a special case of fractional hot deck imputation of Yang and Kim (2014), which is a robust estimation method. Other PS estimators does not allow for this interpretation.

7.2 Simulation Study Two

We performed another simulation study to understand the effect of the calibration variables for smoothed PS weighting. We first generate from multivariate normal distribution with mean and variance where

and generate from where . We also generate where , with for Scenario 1 and for Scenario 2, respectively. The parameter of interest is . The population size is . We considered three choices of the calibration variables in the proposed PS method.

-

1.

The proposed PS estimator using as the calibration variable

-

2.

The proposed PS estimator using as the calibration variable

-

3.

The proposed PS estimator using as the calibration variable

Monte Carlo samples of size are used to compute the Monte Carlo bias, Monte Carlo standard errors and the root mean squared errors of the estimators considered. The simulation result in Table 1 shows that the PS estimator using is the most efficient among the three calibration estimators considered. That is, using calibration variables in the outcome model only achieves the best efficiency. In Scenario 2, the calibration estimator using the covariates for the outcome model is more efficient than the calibration estimator using the covariates for the selection model. The simulation result is consistent with our theory in Remark 3.

Scenario 1 Scenario 2 Method BIAS SE RMSE BIAS SE RMSE a 0.00 0.063 0.063 0.00 0.072 0.072 b 0.00 0.083 0.083 -0.34 0.086 0.351 c 0.00 0.070 0.070 0.00 0.085 0.085

8 Conclusion

In handling the selection bias of the voluntary sample, the problem of estimating the inverse propensity score is recast as a problem of estimating the density ratio function. The density ratio function is defined for the balancing score function, and the propensity scores that arise can be efficient if the balancing score includes the actual mean function. The information projection technique builds a self-efficient propensity score estimating function. The variable selection technique for the outcome model can be utilized to generate efficient propensity score weights. The proposed method can be utilized as a unifying tool for merging information from multiple data sources.

There are several directions for further extensions of the proposed method. The proposed method can be extended to handle data integration problems (Chen et al., 2020) in survey sampling. Also, the proposed method is based on the assumption of missing at random. Extension to nonignorable nonresponse (Kim and Yu, 2011) can be also an interesting research direction. Instead of using Kullback-Leibler divergence, we may use Hellinger divergence (Antoine and Dovonon, 2021, Li et al., 2019) or -power divergence (Eguchi, 2021) to achieve some robustness. In addition, the proposed method can be used for causal inference, including the estimation of the average treatment effect from observational studies (Yang and Ding, 2020). Developing tools for causal inference using the proposed method will be an important extension of this research.

Acknowledgement

The authors would like to thank professors Wayne A. Fuller and Zhiqiang Tan for their constructive comments.

References

- Antoine and Dovonon (2021) Antoine, B. and P. Dovonon (2021). Robust estimation with exponentially tilted Hellinger distance. Journal of Econometrics 224, 330–344.

- Bang and Robins (2005) Bang, H. and J. M. Robins (2005). Doubly robust estimation in missing data and causal inference models. Biometrics 61, 962–973.

- Beaumont (2008) Beaumont, J.-F. (2008). A new approach to weighting and inference in sample surveys. Biometrika 95, 539–553.

- Breidt et al. (2005) Breidt, F., G. Claeskens, and J. Opsomer (2005). Model-assisted estimation for complex surveys using penalised splines. Biometrika 92(4), 831–846.

- Brookhart et al. (2006) Brookhart, M. A., S. Schneeweiss, K. J. Rothman, R. J. Glynn, J. Avorn, and T. Stürmer (2006). Variable selection for propensity score models. American Journal of Epidemiology 163, 1149–1156.

- Cao et al. (2009) Cao, W., A. A. Tsiatis, and M. Davidian (2009). Improving efficiency and robustness of the doubly robust estimator for a population mean with incomplete data. Biometrika 96, 723–734.

- Chan et al. (2014) Chan, K. C. G., S. C. P. Yam, et al. (2014). Oracle, multiple robust and multipurpose calibration in a missing response problem. Statistical Science 29, 380–396.

- Chan et al. (2016) Chan, K. C. G., S. C. P. Yam, and Z. Zhang (2016). Globally efficient non-parametric inference of average treatment effects by empirical balancing calibration weighting. Journal of the Royal Statistical Society, Series B 78, 673–700.

- Chen and Liu (2013) Chen, J. and Y. Liu (2013). Quantile and quantile-function estimations under density ratio model. Annals of Statistics 41, 1669–1692.

- Chen and Haziza (2017) Chen, S. and D. Haziza (2017). Multiply robust imputation procedures for the treatment of item nonresponse in surveys. Biometrika 104, 439–453.

- Chen et al. (2020) Chen, Y., P. Li, and C. Wu (2020). Doubly robust inference with non-probability survey samples. Journal of the American Statistical Association 115, 2011–2021.

- Csiszár and Shields (2004) Csiszár, I. and P. C. Shields (2004). Information theory and Statistics: A tutorial. Now Publishers Inc.

- Dempster et al. (1977) Dempster, A. P., N. M. Laird, and D. B. Rubin (1977). Maximum likelihood from incomplete data via the EM algorithm. Journal of the Royal Statistical Society, Series B 39, 1–37.

- Deville and Särndal (1992) Deville, J. C. and C. E. Särndal (1992). Calibration estimators in survey sampling. Journal of the American Statistical Association 87, 376–382.

- Eguchi (2021) Eguchi, S. (2021). Pythagoras theorem in information geometry and applications to generalized linear models. Handbook of Statistics 45, 15–42.

- Fan and Li (2001) Fan, J. and R. Li (2001). Variable selection via nonconcave penalized likelihood and its oracle properties. Journal of the American Statistical Association 96, 1348–1360.

- Folsom (1991) Folsom, R. E. (1991). Exponential and logistic weight adjustments for sampling and nonresponse error reduction. In Proceedings of the American Statistical Association, Social Statistics Section, Volume 197201.

- Fuller (2009) Fuller, W. A. (2009). Sampling Statistic. Wiley, Hoboken, NJ.

- Graham et al. (2012) Graham, B. S., C. C. de Xavier Pinto, and D. Egel (2012). Inverse probability tilting for moment condition models with missing data. The Review of Economic Studies 79, 1053–1079.

- Hainmueller (2012) Hainmueller, J. (2012). Entropy balancing for causal effects: A multivariate reweighting method to produce balanced samples in observational studies. Political Analysis 20, 25–46.

- Han and Wang (2013) Han, P. and L. Wang (2013). Estimation with missing data: beyond double robustness. Biometrika 100, 417–430.

- Imai and Ratkovic (2014) Imai, K. and M. Ratkovic (2014). Covariate balancing propensity score. Journal of the Royal Statistical Society, Series B 76, 243–263.

- Johnson et al. (2008) Johnson, B. A., D. Lin, and D. Zeng (2008). Penalized estimating functions and variable selection in semiparametric regression models. Journal of the American Statistical Association 103, 672–680.

- Kim and Haziza (2014) Kim, J. K. and D. Haziza (2014). Doubly robust inference with missing data in survey sampling. Statistica Sinica 24, 375–394.

- Kim and Shao (2021) Kim, J. K. and J. Shao (2021). Statistical methods for handling incomplete data (second ed.). CRC press.

- Kim and Skinner (2013) Kim, J. K. and C. J. Skinner (2013). Weighting in survey analysis under informative sampling. Biometrika 100, 358–398.

- Kim and Yu (2011) Kim, J. K. and C. L. Yu (2011). A semiparametric estimation of mean functionals with nonignorable missing data. Journal of the American Statistical Association 106, 157–165.

- Kott (2006) Kott, P. S. (2006). Using calibration weighting to adjust for nonresponse and coverage errors. Survey Methodology 32, 133.

- Kott and Chang (2010) Kott, P. S. and T. Chang (2010). Using calibration weighting to adjust for nonignorable unit nonresponse. Journal of the American Statistical Association 105, 1265–1275.

- Li et al. (2019) Li, L., A. Vidyashankar, G. Diao, and E. Ahmed (2019). Robust inference after random projections via Hellinger distance for location-scale family. Entropy 21, 348.

- Little and Rubin (2019) Little, R. J. and D. B. Rubin (2019). Statistical Analysis with Missing Data. John Wiley & Sons.

- Little and Vartivarian (2005) Little, R. J. A. and S. Vartivarian (2005). Does weighting for nonresponse increase the variance of survey means? Survey Methodology 31, 161–168.

- Ma and Wang (2020) Ma, X. and J. Wang (2020). Robust inference using inverse probability weighting. Journal of the American Statistical Association 115, 1851–1860.

- Montanari and Ranalli (2005) Montanari, G. E. and M. G. Ranalli (2005). Nonparametric model calibration estimation in survey sampling. Journal of the American Statistical Association 100, 1429–1442.

- Nguyen et al. (2010) Nguyen, X., M. J. Wainwright, and M. I. Jordan (2010). Estimating divergence functionals and the likelihood ratio by convex risk minimization. IEEE Transactions on Information Theory 56, 5847–5861.

- Park et al. (2019) Park, S., J. K. Kim, and K. Kim (2019). A note on propensity score weighting method using paradata in survey sampling. Survey Methodology 45, 451–463.

- Qin (1998) Qin, J. (1998). Inference for case-control and semiparametric two-sample density ratio models. Biometrika 85, 619–630.

- Qin and Lawless (1994) Qin, J. and J. Lawless (1994). Empirical likelihood and general estimating equations. Annals of Statistics 22, 300–325.

- Robins et al. (1994) Robins, J. M., A. Rotnitzky, and L. P. Zhao (1994). Estimation of regression coefficients when some regressors are not always observed. Journal of the American statistical Association 89(427), 846–866.

- Rosenbaum and Rubin (1983) Rosenbaum, P. R. and D. B. Rubin (1983). The central role of the propensity score in observational studies for causal effects. Biometrika 70, 41–55.

- Rubin (1976) Rubin, D. B. (1976). Inference and missing data. Biometrika 63, 581–592.

- Shortreed and Ertefaie (2017) Shortreed, S. M. and A. Ertefaie (2017). Outcome-adaptive lasso: Variable selection for causal inference. Biometrics 73, 1111–1122.

- Tan (2010) Tan, Z. (2010). Bounded, efficient and doubly robust estimation with inverse weighting. Biometrika 97, 661–682.

- Tan (2020) Tan, Z. (2020). Regularized calibrated estimation of propensity scores with model misspecification and high-dimensional data. Biometrika 107, 137–158.

- Tsiatis (2007) Tsiatis, A. (2007). Semiparametric theory and missing data. Springer Science & Business Media.

- Wang and Pepe (2000) Wang, C. Y. and M. S. Pepe (2000). Expected estimating equations to accommodate covariate measurement error. Journal of the Royal Statistical Society, Series B 62, 509–524.

- Wu and Sitter (2001) Wu, C. and R. R. Sitter (2001). A model-calibration approach to using complete auxiliary information from survey data. Journal of the American Statistical Association 96, 185–193.

- Wu and Thompson (2020) Wu, C. and M. E. Thompson (2020). Sampling Theory and Practice. Springer.

- Yang and Ding (2020) Yang, S. and P. Ding (2020). Combining multiple observational data sources to estimate causal effects. Journal of the American Statistical Association 115, 1540–1554.

- Yang et al. (2020) Yang, S., J. Kim, and R. Song (2020). Doubly robust inference when combining probability and non‐probability samples with high dimensional data. Journal of the Royal Statistical Society, Series B 82, 445–465.

- Yang and Kim (2014) Yang, S. and J. K. Kim (2014). Fractional hot deck imputation for robust inference under item nonresponse in survey sampling. Survey Methodology 40, 211–230.

- Zhao (2019) Zhao, Q. (2019). Covariate balancing propensity score by tailored loss functions. Annals of Statistics 47, 965–993.