When should you adjust inferences for multiple hypothesis testing?††thanks: D.V. and K.W. contributed equally to this work. We are grateful to Nageeb Ali, Isaiah Andrews, Tim Armstrong, Oriana Bandiera, Sylvain Chassang, Tim Christensen, Graham Elliott, Stefan Faridani, Will Fithian, Paul Glewwe, Peter Hull, Guido Imbens, Lawrence Katz, Toru Kitagawa, Pat Kline, Michael Kremer, Michal Kolesar, Ivana Komunjer, Damian Kozbur, Lihua Lei, Adam McCloskey, Konrad Menzel, Francesca Molinari, Jose Montiel-Olea, Ulrich Mueller, Mikkel Plagborg-Møller, David Ritzwoller, Joe Romano, Adam Rosen, Jonathan Roth, Andres Santos, Azeem Shaikh, Jesse Shapiro, Joel Sobel, Sandip Sukhtankar, Yixiao Sun, Aleksey Tetenov, Winnie van Dijk, Tom Vogl, Quang Vuong, Michael Wolf, and seminar and conference participants for valuable comments, and to staff at J-PAL, Sarah Kopper and Sabhya Gupta in particular, for their help accessing data. Aakash Bhalothia and Muhammad Karim provided excellent research assistance. P.N. and K.W. gratefully acknowledge funding from the UC San Diego Academic Senate. All errors and omissions are our own. Email: dviviano@fas.harvard.edu, kwuthrich@ucsd.edu, pniehaus@ucsd.edu

Abstract

Multiple hypothesis testing practices vary widely, without consensus on which are appropriate when. We provide an economic foundation for these practices. In studies of multiple treatments or sub-populations, adjustments may be appropriate depending on scale economies in the research production function, with control of classical notions of compound errors emerging in some but not all cases. Studies with multiple outcomes motivate testing using a single index, or adjusted tests of several indices when the intended audience is heterogeneous. Data on actual research costs suggest both that some adjustment is warranted and that standard procedures are overly conservative.

Keywords: Bonferroni, family-wise error rate, false discovery rate, multiple subgroups, multiple treatments, multiple outcomes, research costs, interaction effects

1 Introduction

Hypothesis testing plays a prominent role in processes of scientific communication. Typically researchers report results from more than one test, and there has recently been increasing interest in and debate over whether the testing procedures they employ should reflect this in some way—that is, whether some form of multiple hypothesis testing (MHT) adjustment should be applied. As a concrete example, consider pharmaceutical companies reporting the results of clinical trials to regulators when seeking approval to market new drugs: the U.S. regulator (the Food and Drug Administration, FDA) recently released guidelines calling for MHT adjustments on the grounds that omitting them could “increase the chance of false conclusions regarding the effects of the drug” (Food and Drug Administration, 2022). Analogous concerns arise in many other settings—including academic research.

A number of procedures for MHT adjustment have been proposed, and their statistical properties are well-understood (see e.g. Romano et al., 2010, for an overview). What is less clear is whether and when these procedures are economically desirable. That is, under what conditions does MHT adjustment lead to better decision-making from the point of view of the actor designing the communication process? The answer is far from obvious. It is certainly true, for example, that without MHT adjustments the chance of making at least one type I error increases with the number of tests. But this is analogous to the truism that the more decisions one makes the more likely one is to make at least one mistake. It is indisputable, but sheds no light on the pertinent questions, which are whether and how the rule for making individual decisions should change with the total number being made.

This paper provides a framework for analysing such questions. We focus in particular on whether and when MHT adjustments arise as a solution to incentive misalignment between a researcher and a mechanism designer. Our interest in this case reflects two primary considerations. The first is substantive: incentives are clearly an issue in real-world cases of interest (e.g. the FDA, which we will use as a running example). The instinctive concern many seem to have is that without MHT adjustments the researcher would have an undue incentive to test many hypotheses in the hopes of getting lucky. We would like to formalize and scrutinize that intuition. And the second is pragmatic: to have a theory of MHT adjustments we must have a theory that rationalizes hypothesis testing at standard levels in the first place, which (as we discuss further below) is hard to do convincingly in a non-strategic setting (e.g., Tetenov, 2012, 2016).

Specifically, we study a model of scientific communication in which a benevolent social planner chooses norms with respect to MHT adjustments, taking into account the way this shapes researchers’ incentives. The model embeds three core ideas. First, social welfare is (potentially) affected by the summary recommendations (in particular, hypothesis tests) contained in research studies. We describe the case where hypothesis rejections lead to changes in welfare relative to the status quo, but under a straightforward reinterpretation the framework can also accommodate situations in which “precise null” results affect welfare. Second, while this makes research a public good, the costs of producing it are born privately by the researcher. She decides whether or not to incur these costs and conduct a (pre-specified) experiment based at least in part on the private returns to doing so. Hypothesis testing protocols must therefore balance the twin goals of (i) motivating the production of research and (ii) producing welfare-enhancing guidance from it. Finally, we examine how to balance these objectives conservatively, selecting protocols that are maximin in the sense that they maximize welfare in the worst case with respect to the true treatment effects (reflecting for example a “do no harm” principle).

Collectively these assumptions give rise to the incentive issue we wish to study, and can also rationalize standard hypothesis-testing procedures in the single-hypothesis case, as shown in an insightful paper by Tetenov (2016). In the multiple hypothesis case, however, they do not select a uniquely optimal policy—in fact we show that no maximin protocol dominates all others. To complete the model we therefore introduce notions of local and global power to select among admissible maximin rules. We then establish conditions under which separate hypothesis tests based on threshold-crossing protocols—in particular, the -tests ubiquitous in applied work—are optimal. Such procedures emerge within our framework when multiplicity takes the form of testing multiple treatments or estimating effects within multiple sub-populations.111These forms of multiplicity are common in practice. For example, the majority of the clinical trials reviewed in Pocock et al. (2002, Table 1) tested for effects in more than one subgroup. In economics, 27 of 124 field experiments published in “top-5” journals between 2007 and 2017 feature factorial designs with more than one treatment (Muralidharan et al., 2020). We then characterize the role of multiplicity, drawing two broad conclusions.

First, it is generically optimal to adjust testing thresholds (i.e. critical values) for the number of hypotheses. A loose intuition is as follows. The worst states of the world are those in which the status quo of no treatment is best; in these states a research study has only downside, and it is desirable to keep the benefits from experimentation low enough that the researcher chooses not to experiment. If the hypothesis testing rule were invariant to the number of hypotheses being tested, then for sufficiently many hypotheses this condition would be violated: the researcher’s expected payoff from false positives alone would be high enough to warrant experimentation. Some adjustment for hypothesis count may thus be needed. We believe that this logic aligns fairly well with the lay intuition that researchers should not be allowed to test many hypotheses and then “get credit” for false discoveries.

Second (and as this suggests), the research cost function determines exactly how much adjustment is required. One can in fact pick a cost function such that no further adjustment is required, as the costs of doing research scale with the number of hypotheses tested in just such a way as to “build in” the needed correction. More generally, optimal testing protocols compensate for residual imbalances in researcher incentives with respect to the number of hypotheses, taking the researcher’s costs into account. As a result the framework can explain when common criteria emerge as appropriate solutions, and when they do not, as a function of the economic environment. When research costs are fixed, for example, it is optimal to control the average size of tests (e.g. via a Bonferroni correction), while when costs scale in exact proportion to the number of tests no MHT adjustment is required. We illustrate these ideas quantitatively in the context of our FDA example, using the formulae implied by our model along with published data on the typical cost structure of clinical trials. This yields adjusted critical values that are neither as liberal as unadjusted testing at standard levels, nor as conservative as those implied by some of the procedures in current use. Our model also helps to clarify confusion about the boundaries of MHT adjustment, and whether researchers should adjust for multiple testing across different studies. The cost-based perspective suggests that MHT adjustments may be appropriate when there are cost complementarities across studies, but not otherwise.

A broader principle suggested by these results is that welfare-optimal MHT adjustments depend on how exactly hypotheses interact. Our base model emphasizes interactions in the research cost function, which (as we discuss below) appear to be substantial in real-world settings. We also consider a series of extensions in which there is successively more scope for interactions of other kinds, through non-linearities in the researcher’s payoff and through interactions between the welfare effects of the treatments (e.g. complementary treatments). Combined with an appropriately weakened notion of optimality, these extensions yield some interesting results, including (in one case) family-wise error rate (FWER) control at the level of groups of hypotheses.

We also consider the case in which multiplicity takes the form of multiple outcomes. Separate hypothesis tests do not arise naturally in this case, at least if the outcomes all relate to a single decision (e.g. whether to approve a drug); instead it is optimal to report a single test based on an index of the outcomes. The optimal index can be constructed using classical statistical reasoning in the spirit of Anderson (2008) when the outcomes represent different measures of or proxies for the same underlying concept, or using economic weights when they capture distinct contributions to welfare (mortality and morbidity, for example). One can also extend the model to capture a scenario in the spirit of Andrews and Shapiro (2021) in which research results potentially influence multiple decisions because they are read by an audience with heterogeneous preferences over the outcomes; in this case indexing potentially (but not necessarily) combined with MHT adjustment is optimal.

We conclude with some remarks on breadth of applicability. The specific procedures that are optimal will vary depending on the details of the scientific communication process, something that is clear even within the range of possibilities we consider here. But we expect two principles to be robust. First, costs must matter in any model that justifies MHT as a way of “getting researcher incentives right.” If incentives matter, then it must be the net incentives, i.e. rewards net of costs, that matter. And second, different kinds of multiplicity may call for different solutions depending on how they map to decision-making.

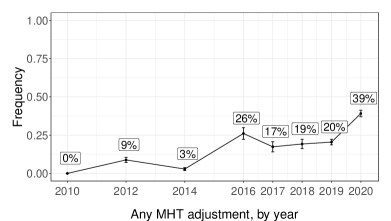

It is also natural to wonder about applicability to economic research in particular, especially given recent publishing trends. The share of experimental papers published in “top 5” journals that use some form of MHT adjustment grew rapidly from 0% in 2010 to 39% in 2020, so that there is now wide variability in whether (and how) these papers adjust (see Figure 3) and little consensus on what the norms should be. Of course, it may be uncharitable to ascribe the researcher motives we study here to academic economists, many of whom are (we believe) genuinely motivated by social impact as well as by the desire to publish well. But even if we adopt a relatively dim view of their motives, we must still account for their costs. We illustrate this point using a unique dataset on the costs of projects submitted to the Abdul Latif Jameel Poverty Action Lab (J-PAL) from 2009 to 2021, which we assembled specifically for this purpose. Costs in this dataset vary substantially, but not one-for-one, with the number of hypotheses tested. This leads once again to adjusted critical values which are neither as liberal as unadjusted testing at the standard 5% level, nor as conservative as those implied by some of the procedures in current use. Even a cynic, we conclude, should require procedures less stringent than these.

Our paper draws inspiration from other work using economic models to inform the choice of statistical procedures. The audience for research results plays a central (albeit passive) role, as in recent work on scientific communication (e.g., Andrews and Shapiro, 2021; Frankel and Kasy, 2022). More generally, the preferences and incentives of researchers drive the analysis (e.g., Chassang et al., 2012; Tetenov, 2016; Banerjee et al., 2017; Spiess, 2018; Henry and Ottaviani, 2019; Banerjee et al., 2020; Williams, 2021; McCloskey and Michaillat, 2022; Yoder, 2022). Our contributions are to adapt and apply this perspective to the analysis of multiple hypothesis testing specifically, and use our theory to interpret unique data on the costs of actual experimental evaluations.

In doing so we aim to provide some practical guidance for navigating the extensive statistical literature on MHT. This literature focuses on the design of algorithmic procedures for controlling particular notions of compound error; see Efron (2008a) and Romano et al. (2010) for overviews.222See, e.g., Holm (1979); Westfall and Young (1993); Benjamini and Hochberg (1995); Benjamini and Liu (1999); Storey (2002); Storey et al. (2004); Lehmann and Romano (2005a); Lee and Shaikh (2014); Romano and Wolf (2016); List et al. (2019, 2021) among many others. Few statistical optimality results exist (e.g., Spjotvoll, 1972; Lehmann et al., 2005; Romano et al., 2011), however, and none of the prior work studies MHT procedures as a way of addressing incentive problems. We draw on these references for inspiration, for example, for our notion of local power (see also Lehmann and Romano (2005b, Chapter 9.2)), but maximize a different (social planner’s) objective and subject to incentive compatibility constraints. We also draw on List et al. (2019)’s helpful distinction between different types of multiplicity, and show how these lead to different optimal testing procedures.

Our paper also relates to an extensive literature at the intersection between decision theory and hypothesis testing, dating back to Wald (1950) and Robbins (1951). Previous work has motivated notions of compound error control in single-agent non-strategic environments; see in particular Kline et al. (2022) for a recent example in economics based on a Bayesian interpretation of the False Discovery Rate (FDR), as well as Storey (2003), Lehmann and Romano (2005b), and Efron (2008b) for further examples.333The literature on statistical treatment choice has similarly focused for the most part on non-strategic planners’ problems. See Manski (2004) and Tetenov (2012) as well as Hirano and Porter (2009); Kitagawa and Tetenov (2018); Hirano and Porter (2020); Athey and Wager (2021) for recent contributions. We complement this literature (as well as the statistical literature discussed in the previous paragraph) by developing a model that explicitly incorporates the incentives and constraints of the researchers. Relative to the decision-theoretic approach, this has two main advantages. First, it lets us characterize when MHT adjustments are appropriate—and also when they are not—as a function of measurable features of the research and publication process. Second, it allows us to justify and discriminate between different notions of compound error (e.g. FWER and FDR) in the same framework based on these same economic fundamentals.

2 Multiple treatments and multiple subgroups

Our goal is to understand what norms with respect to MHT adjustments lead to desirable welfare outcomes. To this end, we ask what statistical procedures a benevolent social planner would choose, taking into account a representative experimental researcher’s incentives. In our running example, we can think of the researcher as a pharmaceutical company running a pre-specified clinical trial evaluating the effect of a new drug. The planner corresponds to the regulator (e.g. the FDA) who defines protocol testing standards they expect to see in studies submitted in support of an application for approval.

In our model, multiple testing issues arise whenever research informs multiple decisions. We therefore start by discussing settings with multiple treatments or different sub-populations, as here there is a clear one-to-one mapping between multiple hypothesis tests and multiple decisions. The case of multiple outcomes is more subtle and discussed in Section 3.

2.1 Model

We study optimal MHT adjustments in a game between a benevolent social planner and a researcher, which makes explicit the central role of the researcher’s incentives. A framework for studying MHT should be able to rationalize conventional (single) hypothesis testing in the first place. This is known to be a challenging problem and requires non-trivial restrictions on the research process (see e.g. Section 1 in Tetenov, 2016, for a discussion). In particular, it requires strong asymmetries to match the inherently asymmetric nature of null hypothesis testing. For example, Tetenov (2012) shows that justifying testing at conventional levels requires extreme degrees of asymmetry in a single agent model with minimax regret: statistical tests at the 5% (1%) level correspond to decision makers placing 102 (970) times more weight on type I than type II regret. In our two-player game, the asymmetry necessary for rationalizing hypothesis testing arises from the planner’s desire to prevent the implementation of treatments that may hurt (groups of) individuals (reflecting for example a “do no harm” principle), in line with our running example.

The planner prescribes and commits to a hypothesis testing protocol, restricting how the researcher can report findings. Given this protocol, the researcher decides whether or not to run an experiment with different non-exclusive treatments by comparing the private benefits of experimentation to the costs.444Our results generalize (up to rescaling) to settings where all findings are exclusive (so only one of the finding gets implemented) and every treatment reported to be effective is equally likely to be implemented. This is because the planner’s objective described below is invariant up to scale. The treatments may represent either distinct treatments (e.g. drugs or interventions) or different sub-populations to whom a treatment might be applied.

If the researcher experiments, she draws a vector of statistics and incurs a cost (or expected cost, if is unknown ex-ante). Here, , and is the parameter of interest. We generally think of the cost and number of treatments as being jointly drawn from some generic distribution of research opportunities; it will help build intuition, however, to think of them as being related via a common research cost function, so that we will henceforth write . These costs are sunk after the experiment is conducted and do not depend on .

For simplicity, we assume that research designs (defined by , , and ) arise exogenously in the main text. We show how our results extend to endogenous designs (i.e. when is chosen endogenously by the researcher) in Appendix A.3.

The researcher reports results in the form of a vector of non-exclusive findings (see Remark 2 for exclusive policies),

where if and only if treatment is found to be effective. We will refer to as a hypothesis testing protocol. We focus on settings where researchers can be required to pre-specify and report all the tests they conduct; given this we abstract from issues of -hacking and selective reporting. Pre-specification is recommended, for example, by the FDA (Food and Drug Administration, 2022).

The planner chooses the types of statistical test(s) that the researcher may employ by selecting , where is a pre-specified and exogenous class of functions. Unless otherwise specified, we do not impose any restrictions on other than pointwise measurability. Our focus will be on studying how optimal hypothesis testing protocols vary as a function of variation in the number of treatments being tested.

Welfare depends on the researcher’s findings. To define welfare, we introduce the selector function , with each entry corresponding to a different combination of findings,

| (1) |

If there are no findings (i.e., ), then the status quo prevails. For , let denote the welfare generated by combination . Given findings , the overall welfare is , where .

To derive our main results, we assume that welfare is additive.

Assumption 1 (Additive welfare).

Let for all .

Assumption 1 rules out interaction effects between treatments. This is the case, for example, when the treatments are very different so that interaction effects are unlikely, or when each treatment corresponds to treating a different sub-population, and there are no cross-group spillovers. We explicitly consider interaction effects in Section 2.5.

We will often return to the following running example (or variants of it) in which the researcher studies treatments using a linear regression model.

Example 1 (Running example).

Consider the problem of studying the effect of non-exclusive experimental treatments and on an outcome of interest based on a sample with observations. Suppose that

| (2) |

For simplicity, the baseline average outcome is normalized to zero, and and are the average treatment effects of and net of the costs of implementation. Under these assumptions, , where is the OLS estimator of , and the covariance matrix is known. This fits into our framework by setting in which case is the CDF of a distribution. A leading example of a testing protocol is separate testing based on (one-sided) -tests in which case We will show below that this testing protocol is optimal for a suitable choice of the threshold . ∎

We introduce two asymmetries in our model that are essential for justifying standard hypothesis testing (Tetenov, 2016). First, we impose asymmetry in the incentives. While the planner maximizes welfare, the researcher’s payoff does not depend on welfare but on the number of reported findings. If, instead, the incentives of the researcher and the planner were aligned, then hypothesis testing of any kind would be unnecessary.555In this case, the optimal planner strategy would be to leave unrestricted in which case the researcher would always report finding effects for the treatments associated with positive welfare effects, and only those treatments. The key assumption is that some (but not necessarily all) researchers have misaligned preferences. Our results remain unchanged as long as researchers have misaligned preferences with positive probability. See Appendix A.6. Misaligned incentives are a pertinent feature of the regulatory approval process. The pharmaceutical company’s incentives to find significant effects that support approval may not be fully aligned with the regulator’s desire to approve only products that are welfare-increasing.

Second, we assume that there is asymmetric information: the parameter is known to the researcher but unknown to the planner. In the regulatory approval process example, it is likely that pharmaceutical companies have more information about their products than the regulator. Our main results continue to hold when the researcher is imperfectly informed and has an arbitrary prior about . See Appendix A.2.

The (expected) researcher’s payoff from conducting the experiment, which we denote by , depends on the costs of doing so and on the number of findings. For now, we assume that is linear in the number of findings, which will be appropriate to our leading applications. We discuss the robustness of our results to uncertainty with respect to the functional form of in Section 2.2 and also examine threshold-crossing payoff functions in Section 2.5.

Assumption 2 (Linear researcher payoff).

The researcher’s payoff conditional on experimenting is, up-to-rescaling by ,

| (3) |

For example, in the drug-approval context, linearity of the payoff function occurs when researchers care about expected profits earned by selling the drug or device to each subpopulation for which its use is approved (so that one should interpret as the cost relative to expected profits).777As we show in Section 2.4, once we fix the level of a single one-sided test the planner only needs to know up to scale. More generally, linearity approximates settings for which researchers are rewarded in proportion to the number of statistically significant results they find.

We impose a standard tie-breaking rule.

Assumption 3 (Tie-breaking rule).

If the researcher is indifferent between experimenting or not, she makes the choice that yields the highest welfare.

The planner commits to a hypothesis testing protocol , taking into account the best response of the researcher. Welfare depends on and the parameter :888The definition of welfare below implicitly assumes that the target population is independent of the experimental sample but subject to the same data-generating process. These are standard assumptions (e.g., Manski, 2004; Kitagawa and Tetenov, 2018; Athey and Wager, 2021).

| (4) |

The second case () follows from Assumption 3.

Remark 1 (Unequal weights).

Remark 2 (Exclusive policies).

In our baseline model, we consider a setting with either multiple subpopulations or with multiple treatments that are non-exclusive. In some applications, however, the social planner might view the treatments as mutually exclusive, as for example if she anticipates that policymakers will implement at most one of them. If the researcher only reports one discovery such that , the resulting model is isomorphic to the one discussed in Section 2.5.2 with in Section 2.5.2 replaced by , subject to the constraint that . If the researcher can report multiple findings, and each treatment will only be implemented with (exogenous) probability smaller than one due to capacity constraints, our results under Assumption 2 directly apply. ∎

2.2 Maximin protocols and size control

We study the optimal choice of hypothesis testing protocols in settings where the planner’s goal is to prevent the implementation of harmful treatments, motivated for example by “do no harm” principles. Specifically, we examine testing protocols that maximize worst-case welfare, i.e. testing protocols that are maximin optimal:

We denote the set of maximin hypothesis testing protocols by . Define the null space, the set of parameters such that welfare is negative regardless of the choice of , as follows.

Definition 1 (Null space).

The null space is

The following proposition provides a characterization of maximin hypothesis testing protocols , generalizing Proposition 1 in Tetenov (2016) (discussed in Appendix C) to the case of hypotheses. It shows that our definition of the null space is directly connected to maximin optimality.

Proposition 1 (Maximin protocols).

Let Assumption 3 hold and suppose that . A testing protocol is maximin-optimal, i.e.,

| (5) |

if and only if

| (6) |

Proof.

Proposition 1 shows that maximin optimality is equivalent to two conditions. First, as in the case with hypotheses, maximin testing protocols depend on the researcher’s payoff , and deter experimentation over , where all treatments reduce welfare. Second, welfare for must be non-negative. This second condition requires that if some treatments reduce welfare, there must be other treatments that compensate them. The first condition captures a notion of size control. We show below that the second condition is non-binding for one-sided -tests in the leading case where is normally distributed.

We illustrate the definition of the null space and the characterization of maximin protocols in our running example.

Example 2 (Running example continued).

In our running example, the null space is Figure 1 provides a graphical illustration. By Proposition 1, a testing protocol is maximin only if (but not necessarily if)

| (7) |

Equation (7) shows that maxmin testing protocols impose restrictions on size control (i.e., the probability of reporting a false discovery). ∎

Notes: Graphical illustration of the null space and the alternative space . See Remark 3 for a discussion of the two orthants where the coefficients have different signs.

Which (if any) hypothesis testing protocols are maximin optimal? The answer to this question depends on the distribution of . Motivated by asymptotic approximations, we focus on the leading case where is normally distributed.

Assumption 4 (Normality).

, where is known, and for .

The variance homogeneity assumption, , holds by design if the experimental treatment arms are well-balanced. (It is required for maximin optimality in Proposition 2, but not the subsequent ones). We extend our results to settings with heterogeneous variances in Appendix B.3. We show that maximin optimality continues to hold for and holds approximately (up-to an error that depends on variance heterogeneity) for .

The next proposition shows that standard separate -tests are maximin optimal for a particular choice of critical values.

Proposition 2 (Maximin optimality of separate -tests).

Proof.

See Appendix D.2. ∎

Proposition 2 shows that separate one-sided -tests with critical values are maximin optimal. The key technical challenge in our game-theoretic framework is to show that welfare is non-negative even when parameters have different signs (Equation (6)). In Section 2.3, we show that -tests with critical values also have desirable properties when compared to other tests.

An important practical implication of Proposition 1 (and 2) is that the optimal critical value depends on the average costs of the experiment. See Section 2.4 for a further discussion.

We conclude this section by showing that any hypothesis testing protocol that is maximin optimal for a given researcher payoff function , is also maximin optimal for any other payoff function that is dominated by .

Proposition 3 (Any maximin-optimal protocol is also maximin-optimal within a larger class of researcher payoff functions).

Let the conditions in Proposition 1 hold. Then any that is maximin-optimal for a given researcher payoff function is also maximin-optimal for any researcher payoff function such that for all .

Proposition 3 demonstrates an important robustness property of our results. It is particularly useful in settings with uncertainty about the researcher’s payoff. For example, Proposition 3 guarantees that any maximin protocol derived under the linearity Assumption 2 is also maximin optimal for any weakly increasing payoff function that is bounded from above by a linear payoff function.

Remark 3 (Null space).

The definition of the null space corresponds to the global null hypothesis in the literature. It is a subset of the strong null space . We note that plays an important role in the second condition of Proposition 1 (). Since for all by definition, this condition is equivalent to assuming that welfare is positive for .∎

Remark 4 (Average size control).

When the researcher’s payoff is linear (Assumption 2), a corollary of Proposition 1 is that maximin testing protocols must control average size, . Many of the popular MHT corrections reviewed in the introduction do not directly target average size control and, thus, will generally not be optimal in our model. This explains why classical Bonferroni corrections are optimal in our model when is constant (see Section 2.4), while common refinements of Bonferroni such as Holm (1979)’s method are not. By construction, Bonferroni satisfies average size control, whereas common refinements do not. The optimality of Bonferroni (and average size control) is driven by the linearity of the experimenter’s payoff function. Bonferroni corrections may not be most powerful with nonlinear payoff functions, but are maximin optimal for all payoff functions dominated by a linear payoff function (see Proposition 3). Section 2.5 and Appendix A.4 provide optimal testing protocols for different researcher payoff functions. ∎

Remark 5 (Two-sided hypothesis testing).

The structure of the model in the main text naturally justifies one-sided hypothesis testing. In Appendix A.7, we consider a variant of our model that rationalizes two-sided hypothesis testing, and standard two-sided -tests in particular.∎

Remark 6 ( depends on ).

Our results directly apply to settings where is a function of , . For example, suppose that , but the total sample size is fixed with , for some (i.e. the units are distributed equally across treatment arms). In this case, the protocol under Proposition 2 is , where . This MHT adjustment is more stringent than when does not depend on . The reason is that experiments with more treatments have lower power per test when , which increases the likelihood of false discoveries. ∎

2.3 Most powerful testing protocols

The set of maximin testing protocols contains infinitely many elements, some of which may be very conservative. An example are -tests with critical values , which discourage experimentation for all values of . While these tests are maximin optimal (Proposition 2), they have zero power and are uniformly dominated by the testing protocol (8) with . This motivates the use of additional criteria for choosing among the many maximin testing protocols. In other words, among testing protocols that minimize the planner’s downside, how might she select those with large upside? To this end, we study the power of testing protocols, where power in our framework is measured in terms of implied welfare.

2.3.1 There is no uniformly most powerful testing protocol

We first show that no maximin testing protocol dominates all other testing protocols when . That is, there exists no maximin protocol that leads to higher welfare for all alternatives than all other maximin protocols.

Proposition 4 (No testing protocol dominates the others).

Let . Let Assumptions 1, 2, and 3 hold. Then there exists a parameter space and a distribution such that no maximin protocol (weakly) dominates all other maximin testing protocols for any cost , i.e., there exists no such that for all . Moreover, there exists such a distribution satisfying Assumption 4.

Proof.

The assumption that is not restrictive, and the result continues to hold when for a finite constant . See Appendix D.4 for details.999Proposition 4 assumes that . If the researcher will always be indifferent between experimenting or not, and we can assign probability one to each discovery without violating the researcher’s incentive compatibility constraint. ∎

In the terminology of classical hypothesis testing, Proposition 4 states that there are settings in which no uniformly most powerful tests exist whenever . This does not imply, however, that there are no maximin rules that are strictly dominated. For example, -tests with are maximin optimal (Proposition 2) but strictly dominated by protocol (8) with . The result in Proposition 4 is in stark contrast to the single-hypothesis case where uniformly most powerful tests (i.e. dominant testing protocols) exist.101010For example, under normality a uniformly most powerful test exist by classical results when interpreting power in terms of welfare effects (e.g., Van der Vaart, 2000, Chapter 15).

Proposition 4 implies that choosing a particular notion of power is unavoidable. We first consider a local notion of power, motivated by the literature on statistical testing, and then discuss a complementary notion of global power. In Appendix A.5.1, we consider two additional notions of power: an alternative local notion of power and a global notion of power inspired by the literature on weighted average power (WAP).

2.3.2 -Tests are locally most powerful

Here we analyze the local power of hypothesis testing protocols. We start by defining a suitable local alternative space.

Definition 2 (-alternatives).

For , define the local alternative space as

The set of -alternatives is the set of parameters for which, for some policy decision, welfare is strictly positive by . Note that for all .

Based on Definition 2, we introduce the following notion of local power. It is similar in spirit to the ones employed in Section 4 of Romano et al. (2011) and Chapter 9.2 of Lehmann and Romano (2005b), among others.111111The proposed notion of local power, when interpreted as a function of the sample size through the lens of classical hypothesis testing, appropriately rescales welfare to avoid trivial solutions and considers sequences of alternatives with parameters of order , where . This is motivated by the fact that any local sequence of order would not provide us with meaningful power comparisons.

Definition 3 (Locally more powerful).

A testing protocol is locally more powerful (or -more powerful) than if121212In Appendix E.2.1, we show that the expression below is uniformly bounded for all .

| (9) |

Definition 3 introduces a partial ordering of testing protocols based on their worst-case performance under -alternatives. It considers parameter values in an alternative space that contains the origin as . The rescaling by the location parameter avoids trivial solutions.131313Rescaling by the location parameter is common in local asymptotic analyses and is standard practice when making optimality statements (e.g., Athey and Wager, 2021). Under the notion of local power in Definition 3, the planner prioritizes power for detecting small treatment effects.141414Worst-case local power is consistent with the maximin framework presented here. Interestingly, the maximin solution differs from Bayesian approaches where planners might specify a prior over the parameter space. However, in Appendix A.5.1, we show that Definition 9 is a refinement of an alternative notion of power where for all , which is equivalent to imposing a point-mass prior on small positive values of the treatment effects.

We say that a maximin testing protocol is locally most powerful (or -most powerful) if it is (weakly) locally more powerful than any other maximin testing protocol . Appendix A.1 shows that locally most powerful tests are also admissible.

The next proposition states that a testing protocol is locally most powerful if and only if the rejection probability of each separate test at (the boundary of the null space) equals .

Proposition 5 (Separate size control is locally most powerful).

Proof.

Proposition 5 has three important implications. First, it shows that a testing protocol is locally most powerful and maximin if and only if it imposes size control that is separate. That is, given restrictions on the marginal probabilities of rejecting individual hypotheses, no further restrictions are placed on the joint probabilities. Second, locally most powerful maximin testing protocols are symmetric across the different hypotheses. Symmetry is natural absent additional restrictions on the relative importance of the different hypotheses. Third, Proposition 5 shows that whether and to what extent the level of these separate tests should depend on the number of hypotheses being tested—in other words, whether an adjustment for the presence of multiple hypothesis is required—depends on the structure of the research production function . See Section 2.4 for a discussion.

2.3.3 -Tests are approximately globally most powerful

In Section 2.3.2, we introduced a local notion of power and showed that separate -tests are locally most powerful. This result was derived for a fixed variance , which corresponds to a finite sample analysis. Here we show that -tests are also approximately globally most powerful as the variance converges to zero, , which can be motivated by asymptotics where the sample size in the experiment diverges, . Define the global alternative space as follows.

Definition 4 (Global alternatives).

For , the global alternative space is

Definition 4 considers an alternative hypothesis space where at least one parameter is positive and bounded away from zero.

Proposition 6 (Separate -tests are approximately globally most powerful).

Proof.

See Appendix D.6. ∎

Proposition 6 shows that separate -testing uniformly dominates any other protocol up to an error that converges to zero at a rate proportional to the standard deviation. Typically, under a fixed alternative with , is of order inverse of the sample size guaranteeing a fast (parametric) convergence rate of the approximation error.151515Note that approximate global optimality is consistent with Proposition 4, since the proof of Proposition 4 leverages local (in ) asymptotic arguments, taking in mixed orthants. Proposition 6 complements our local power result, showing that -tests have desirable global properties.

Remark 7 (Rationalizing power under ambiguity aversion).

It is interesting to interpret our analysis through the lens of the preferences of an ambiguity-averse planner, inspired by Banerjee et al. (2020). Suppose that the planner utility is given by

| (11) |

Here denotes the weight assigned to prior value .

Maximin and locally most powerful protocols correspond to the case where and prioritize the worst-case utility for in a neighborhood around zero. Maximin and approximately globally most powerful tests guarantee approximate optimality for any and :

This follows from maximin optimality of . ∎

2.4 Implication for practice and empirical illustration

Our theoretical results show that separate one-sided -tests with critical values are maximin optimal and have desirable power properties. To illustrate the practical implications of our results, we decompose (without loss of generality) the total research costs into fixed and variable components and , . Using this notation, the optimal critical value is .

Consider first a case in which the research production function exhibits no economies of scale with respect to the number of hypotheses being tested. Specifically, suppose there are no fixed costs, , and that the variable costs scale linearly in , . Then the critical value is . That is, standard inference without adjustment for MHT is optimal in this case. While it is true that the researcher obtains a higher expected reward from taking on projects that test more hypotheses, the appropriate correction for this is already “built in” to the costs of conducting research, so that no further correction is required.

Now consider the case in which the research production function exhibits strong economies of scale. Specifically, suppose there are only fixed costs and that the variable costs are zero, i.e. and . Then the critical value is . In other words, using a Bonferroni correction is optimal in this case. This correction is necessary to appropriately align the researcher’s incentives with those of the planner, as without it the researcher would have a disproportionate incentive to conduct projects with a large number of hypotheses.

Our results further allow for computing MHT adjustments while holding fixed conventions such as setting the level with a single hypothesis to . In this approach, we do not require information about the level of the cost function , but only the relative cost function . This is attractive in settings where we observe costs only up to an (unknown) proportionality constant. Specifically, Proposition 2 implies that the level of the separate -tests with multiple hypotheses, , is proportional to :

| (12) |

The MHT correction factor reflects the ratio of the average costs per test. Unless the overall costs are fixed (i.e., ), this correction factor differs from the standard Bonferroni correction factor .

We illustrate how to compute the MHT correction factor in the regulatory approval example. Using data on the costs of 31,000 clinical trials of pharmaceutical drugs conducted in the United States between 2004 and 2012, Sertkaya et al. (2016) estimate that for an average Phase 3 trial 46% of costs are fixed, with the rest varying either directly with the number of subjects enrolled or with the number of sites at which they were enrolled.161616According to Sertkaya et al. (2016, Table 2), the variable costs (i.e., the per-patient and per-site costs) are USD 10,826,880, and the total costs are USD 19,890,000, so that the fraction of fixed costs is . This suggests a cost function of the form and satisfying , where is the number of subgroups in a typical study. Using based on the tabulations in Pocock et al. (2002)171717We use the median estimate multiplied by the probability of reporting more than one subgroup. and setting , as is typical for one-sided tests (Food and Drug Administration, 2022, p.13), one can with some arithmetic obtain the relationship

| (13) |

Studies with would thus use a value of , studies with would use a value of , and so on, asymptoting to (up to rounding).181818The critical values are not particularly sensitive to . For example, if we double so that , then , , and .

Note that these values are both more conservative than unadjusted thresholds, and also less conservative than would typically be implied by, for example, procedures suggested by the FDA (since these imply as with independent tests). One could of course refine these figures with more detailed and comprehensive data on the costs and benefits of clinical trials. But the broad point is simply to illustrate that it is feasible to apply the framework using existing, publicly available data, and in doing so to generate testing protocols more nuanced than those currently used in practice.

2.5 Additional forms of interactions between treatments

So far, we have analyzed settings where treatments interact only via the research cost function. Here we briefly describe extensions to two settings with successively more scope for interaction between hypotheses in each configuration. In the first we continue to assume no economic interactions between treatments but allow for interactions in the researcher’s payoff function through threshold effects. In the second we allow for arbitrary economic interactions between treatments—for example, complementary treatments—as well as threshold payoff functions. We summarize our results here and refer to Appendix A.4 for a detailed discussion.

2.5.1 Linear welfare and threshold-crossing payoff function

We introduce interactions in the researcher’s payoff by replacing the linear payoff function in Assumption 2 with a threshold function, where studies yield a (constant) positive payoff if and only if they produce sufficiently many findings:

| (14) |

This extension is particularly relevant in the academic publishing context, if the researchers value publications and only studies with sufficiently many findings are published. This could capture capacity constraints at journals, for example.

With a threshold crossing payoff function the incremental value of a finding to the researcher depends on the number of other findings. This leads to more complicated optimal hypothesis testing protocols that depend on the joint distribution of . Therefore, we restrict attention to independent testing protocols for which with . For this class of testing protocols, we show that one-sided -tests,

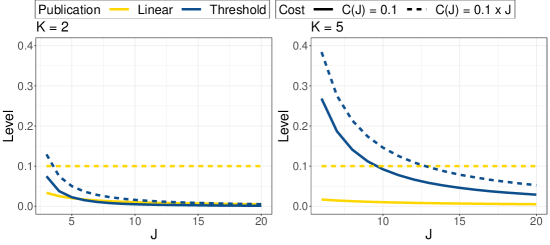

are still optimal when , where depends on , , and . When , which is equivalent to assuming a constant payoff function and constant costs in the number of discoveries, we can show that as . Thus, asymptotically, fixed-cost research production functions again rationalize Bonferroni corrections.

2.5.2 General welfare and threshold-crossing payoff function

To introduce the possibility of interactions between the treatments being studied, in addition to interactions in the cost and the payoff function, we assume that , where each component of denotes the effect of a combination of treatments. Welfare upon experimentation equals . Importantly, unlike Assumption 1, this allows for interactions in the welfare impact of multiple treatments. With , for example, complementarities can be modeled as , , and for some . As a result, we have since we are interested in all possible combinations of treatments.

We show that separate size control over each group of findings,

| (15) |

is locally most powerful. Here denotes the set of indexes that corresponds to groups of or more hypotheses, and thus groups that are sufficient for approval. Equation (15) can be interpreted as a Bonferroni correction at the level of groups of tests sufficient for approval. Any MHT procedure that satisfies Equation (15) controls the weak FWER at level at . When this implies control of the probability of a single false rejection, i.e. control of the standard weak FWER.

Finally, we show that standard -tests are not optimal when there are interaction effects. Motivated by this negative result, we then provide an example of a maximin and locally most powerful testing protocol. Under this protocol, a combination of treatments is recommended if its effect is significant and the largest among all combinations, highlighting the complexity of optimal testing protocols when there are interactions between treatments.

3 Multiple outcomes

We turn next to the more nuanced case of multiple outcomes. When a study considers multiple treatments or sub-groups it is straightforward to see that it may affect social welfare through multiple policy decisions—which of the treatments to implement, for example, or which of the sub-groups to treat. As we have seen above, this can give rise to a natural rationale for reporting multiple test results, potentially with an MHT adjustment. But it is not as clear that multiple outcomes necessitate multiple tests—let alone MHT adjustments. In fact it is common (though not universal) practice to aggregate multiple outcomes into a single index and simply report one test for effects on this index.

In this section we examine these issues using the formal apparatus introduced above. Generally speaking the answers will depend, as one might expect, on how the various outcomes relate to welfare. To make these ideas concrete we explicitly introduce the idea that research findings impact welfare by influencing the decisions of one or more policymakers, identifying welfare with the preferences of those policymakers. This allows us to examine the relationship between preferences over the various outcomes and statistical procedures for interpreting them.

Specifically, we first consider a scenario in which a study may inform a single decision by a policymaker with known preferences. In this scenario it is (we will show) indeed optimal to index the outcomes and conduct a single test; the question whether to conduct MHT adjustments thus does not arise. But of course in some applications there may be uncertainty about who will use the results or what their objectives will be, which could motivate multiple tests. For example, researchers conducting policy experiments in economics might report a test for effects on education outcomes that is relevant to education ministers, and a separate test for effects on health outcomes relevant to health ministers. In Section 3.2 we consider a scenario along these lines and examine when MHT adjustment is appropriate.

Throughout this section we assume a single treatment in order to focus attention on issues that are specific to multiple outcomes; the results can be extended to multiple treatments at the expense of additional notation.

3.1 Single policymaker

Suppose there is a (single) policymaker who, given the findings reported by the researcher, implements the treatment (possibly with some positive exogenous probability). Welfare depends on the policy effects on different outcomes . The outcomes are associated with statistics which measure the effect of the treatment on those outcomes. For example, suppose that the researcher evaluates the effect of a treatment on outcomes, , using the regression model for all . In this case, is the treatment effect of on the th outcome , the vector of statistics is , where is the OLS estimator of , and is the CDF of a distribution. We assume that the outcomes are appropriately standardized so that the treatment effects are on the same scale.

Welfare equals a weighted average of the effects on the different outcomes, where , and the weights are common knowledge. The planner chooses a hypothesis testing protocol that may depend on the number of outcomes , . Given this protocol, the researcher payoff is

The planner maximizes the welfare, which is given by

| (16) |

In the following, we show that one-sided -tests based on a weighted average of the outcome-specific statistics,

| (17) |

are maximin optimal and locally most powerful if the weights are chosen optimally. The choice of the optimal weights depends on the interpretation of the outcomes , the corresponding statistics , and the parameter space . We consider two alternative interpretations. In the first, each entry of measures impacts on distinct arguments in the policymaker’s welfare function. For example, a study might report effects of a drug on distinct endpoints, both of which matter independently to the regulator. Second, we assume that each entry of is a distinct measure of the same underlying welfare-relevant outcome. This describes settings in which there are multiple ways of measuring the same construct.191919These settings also closely related to “latent variable” models in which multiple outcomes are interpreted as proxies for some deeper, underlying construct of interest (e.g., multiple measures of “health” in medical studies). See Appendix B.6.

We start by considering a setting where each entry of measures impacts on economically distinct outcomes.

Assumption 5 (Economically distinct outcomes).

Assumption 5 encompasses two separate requirements. First, we normalize the parameter space of to .202020This normalization is not restrictive, and we could instead use any interval for . Second, we assume that there are no cross-parameter restrictions, formalizing what we mean by “economically distinct” outcomes.

The next proposition shows that with economically distinct outcomes, one-sided -tests based on the welfare-optimal index are optimal.

Proposition 7 (Economically distinct outcomes).

Proof.

See Appendix D.7. ∎

The intuition for the optimality result in Proposition 7 is that choosing as the test statistic is optimal because it guarantees that so that the test is similar at the boundary of the null space.

Unlike with multiple treatments in Section 2, the optimal critical value of the one-sided -test (18), , is decreasing in whenever (as seems most likely to hold in practice) is increasing in . This is because the researcher only tests one hypothesis, regardless of the number of outcomes she must collect to do so. Thus, if the planner wants to incentivise researchers to conduct experiments with many outcomes, she needs to lower the critical value to encourage them to do so.

The essence of Proposition 7 is that if a weighted average of the underlying parameters is what determines the welfare consequences of implementing the policy, then an analogous weighted average of the individual statistics is the appropriate test statistic. If the planner and policymaker coincide, the weights are known to and chosen by the planner. More generally, our results imply that it is important for researchers running policy experiments to elicit the optimal weights so that they can report tests of the appropriate indices.

Remark 8 (Indexing vs. classical MHT adjustments based on separate tests).

Conducting separate tests on the outcomes individually (with or without MHT adjustment) is not optimal when there is a single policymaker; this would discard valuable information about the relative magnitudes of the effects. See Appendix B.4 for a formal discussion and an example. Note that this implication of the model differs from the practice of running separate tests and then discussing significant effects. By contrast, our model suggests that—when it is clear how to do so—aggregating information before testing is optimal from a welfare perspective. ∎

Now let each element of be a distinct measure of a common underlying parameter.

Assumption 6 (Multiple measurements).

Under Assumption 6, welfare conditional on implementing the treatment is . Since welfare and the null space are invariant to the choice of the weights when all components of are equal, it is optimal to aggregate into a single statistic with variance-minimizing weights.212121This is in the spirit of “disjunction testing” in the language of Rubin (2021). The next proposition provides the formal result.

Proposition 8 (Multiple measurements).

Proof.

See Appendix D.8. ∎

Proposition 8 implies that the most powerful threshold crossing rule chooses the weights to minimize subject to an adding-up constraint.222222The above arguments show that one-sided -tests based on a weighted average of statistics are optimal. In practice, researchers often first aggregate the outcomes and then run tests based on the aggregate outcome (e.g. Anderson, 2008). For linear estimators like OLS, these two approaches are equivalent. See Appendix B.5 for a further discussion. This protocol coincides with classical notions of uniformly most powerful tests in the statistical literature on single hypothesis testing (Van der Vaart, 2000). Thus, in the case of multiple measurements, the recommendations from the economic model with incentives coincide with those based on the classical statistical approach.

3.2 Multiple policymakers

We now relax the assumption that the study’s “audience” consists of a single policymaker with known preferences, and instead consider a study that reports the results of multiple tests each relevant to a different potential audience member. Consider an audience of different policymakers. Each policymaker decides whether to implement the treatment based on its effects on .

As before, we assume that each policymaker’s welfare equals a weighted average of effects on the different outcomes: , where and is known for all . In interpreting the results of a policy experiment, for example, education ministers may care primarily about learning outcomes while health ministers care primarily about health outcomes.

The researcher reports different tests, one for each policymaker, such that the testing protocol takes the following form

where is the finding corresponding to policymaker . The protocol may depend on both the number of outcomes and the number of policymakers .

The researcher’s payoff is similar to Section 2.

| (20) |

Here is a weakly increasing function and denotes the cost of experimentation. In Equation (20), the researcher’s payoff depend on the number of findings, whereas the costs of the experiments are determined by the number of outcomes, .

The planner is aware of the different policymakers who may read and implement the study’s findings, but does not know for certain which will do so. She thus faces two sources of uncertainty, with respect to both the welfare effects of the treatment and the audience for evidence on those effects.

Suppose first that each policymaker is equally likely to implement the policy (i.e., implements the policy with probability ) so that the expected welfare is

| (21) |

It follows directly from Equation (21) that the problem of multiple testing is now isomorphic to the one discussed in Section 2, with in Section 2 replaced by here. For example, assuming that , i.e. the payoff function is linear in the number of discoveries, the threshold-crossing protocol

is maximin optimal and locally most powerful. The key difference to the results in Section 2 is that the separate -tests are based on indices that incorporate the heterogeneous policymaker weights.

As an alternative to the approach above, one could examine a worst-case approach with respect to the identity of the implementing policymaker—that is, how to maximize the planner’s payoff in the worst case with respect to both and . This model leads to very conservative hypothesis testing protocols. When the researcher’s payoff is linear, threshold crossing protocols such as -tests are not maximin optimal for any (finite) critical values. When the researcher’s payoff takes a threshold form, a hypothesis testing protocol is maximin optimal if and only if it controls the probability of at least discoveries under the null. This criterion is stronger than and implies -FWER control. We refer to Appendix A.8 for a formal analysis of the worst-case approach.

Remark 9 (FDR control).

In settings where the planner is maximin with respect to both and , it is possible to “invert” the analysis and ask what researcher incentives rationalize other popular criteria such as FDR control. Interestingly, it turns out that rationalizing the FDR requires us to assume that the researcher is malevolent in the sense that her payoff is increasing in the number of false discoveries. We interpret this result as suggesting that FDR control does not arise as a natural solution in our frequentist maximin framework. As we will discuss in Section 4.2, however, we see other cogent arguments for FDR control once one is willing to move outside such frameworks and consider decision-making from a Bayesian perspective. ∎

4 Broader applicability to scientific communication

This section provides some discussion of the scope across which the framework’s implications (summarized in decision-tree format in Figure 2) may apply. We first consider in Section 4.1 the scope for application to academic research in economics, particularly experimental program evaluation work. In Section 4.2 we then offer some more general concluding observations.

4.1 Policy evaluation experiments within economics

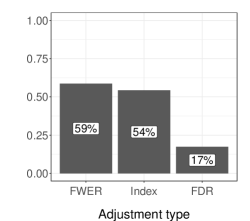

As economists we are of course particularly interested in hypothesis testing norms within economics. This is a salient issue given recent publication trends. Figure 3 illustrates these for experimental papers published in “top-5” economics journals, plotting the share that conduct at least one MHT adjustment (defined here as either control of a compound error rate or indexing) in the left-hand panel, and the distribution of adjustment types (not mutually exclusive) in the right-hand panel. A little over a decade ago not a single paper used any adjustment, while by 2020 we were drawing near to an even split between those that did and those that did not. The methods used also vary a great deal, with control of the FWER most common, followed by indexing, and then by control of the FDR. These figures suggest—consistent with our personal experiences as authors and as referees—that there is no clear consensus at the moment on whether and how authors should be asked to perform MHT adjustments.

Notes: The left-hand panel reports the share of experimental papers that conduct at least one MHT adjustment, including both indexing and control of compound error rates, by year of publication. (Note that almost all experimental studies have more than one hypothesis). The right-hand panel reports the frequency of each adjustment type, pooling across years. Adjustment types are not mutually exclusive. Authors’ calculations based on a review of publications in the American Economic Review (excluding Papers and Proceedings), Econometrica, the Journal of Political Economy, the Quarterly Journal of Economics, and the Review of Economic Studies.

Can the framework above provide helpful guidance? Its assumptions arguably correspond most closely to economics papers that report the results of experimental program evaluations. Here there are clear policy decisions that the research is explicitly designed to inform (i.e., whether or not to implement or scale the programs being evaluated). Indeed, researchers often conduct studies like these in collaboration with implementation partners, such as governments or NGOs, precisely in order to evaluate the impact of treatments the partners are considering. The paper’s findings may thus affect social welfare because, in addition to potentially being published in an academic journal, they can influence those decisions.232323In our model, the policymaker’s decision to implement treatments does not depend on whether and where the paper gets published. This captures the idea that the paper will eventually be published somewhere and that policymakers cannot easily discriminate between papers based on the academic prestige of the outlet, which is plausible in the context we consider. Pre-specification of the analysis to be conducted in a pre-analysis plan (corresponding to our assumption that researchers pre-specify their tests) is now common in this genre of work (Miguel, 2021). And it is also common for such “policy experiments” to test more than one treatment as part of the same study. For example, Banerjee et al. (2007) study the effects of both a remedial education program and a computer-assisted learning program on student test scores in India. Overall, at least 27 multiple-treatment experiments were published in top-5 journals 2007–2017.242424 Muralidharan et al. (2020) document 27 such experiments that also included interactions arms.

Given these parallels, one can think of the planner’s problem in our framework as being analogous to that facing the editorial board of an academic journal choosing editorial standards regarding the use of hypothesis testing procedures.252525We abstract from other factors that would be important for a positive description of the academic publication process, including the incentives of journal editors (e.g., maximizing the journal’s impact factor) and competition between journals. We can incorporate some of these (e.g., the role of space constraints in journals in Section 2.5). How closely the researcher’s problem maps, meanwhile, depends on the view one takes of researchers’ incentives. Publishing papers is certainly one of their objectives, and if we interpret as the publication probability (multiplied by a factor ), Assumption 2 describes a setting where the publication probability increases in the number of findings.262626Assumption 2 allows the publication prospects to depend on factors beyond the number of discoveries (e.g., novelty, quality, and unobserved preferences) as long as they are independent of , as in the model of the publication process in Brodeur et al. (2016). This interpretation is consistent with evidence that referees and researchers more generally treat rejections of the null as mattering.272727For example, using data from three different empirical literatures, Andrews and Kasy (2019) find that significant results are much more likely to be published than insignificant ones.

This may of course be too harsh a view of researcher incentives. Undoubtedly many economists undertake program evaluation work in large part because they themselves wish to improve policy decision-making. That said, economists are also undeniably motivated to publish papers, and the framework is applicable as long as the planner is concerned that some of them over-value this goal relative to social considerations (see Appendix A.6). And it may prove informative to work out what even a relatively extreme view implies for practice.

To that end, we analyze the implications of the framework for hypothesis testing quantitatively using unique data on the costs of conducting experimental evaluations. The data cover (essentially) all funding proposals for such evaluations submitted to the Abdul Latif Jameel Poverty Action Lab (J-PAL) from 2009 to 2021. J-PAL is the leading funder and facilitator of experimental economic research in low-income countries, and funds projects that are typically designed to inform policy in those countries. The characteristics of these projects thus align fairly closely with the assumptions in our framework.

The data contain both the reported total financial cost of each project (including the amount requested from sources other than J-PAL) and the number of experimental arms in the study, allowing us to examine scale economies along this dimension of multiplicity. Financial costs are not the only costs incurred, of course, but are likely to be highly correlated with other relevant ones that a researcher deciding whether to undertake a project would consider: ceteris paribus, larger budgets will tend to mean more researcher effort raising funds and managing teams of research assistants, for example.282828Because we fix and then calculate the adjustments implied for by the data on relative costs, our calculations here would be unaffected if the relevant costs include non-financial costs but these are proportional to the financial costs we observe. We focus primarily on projects in low-income countries, which are J-PAL’s main focus and make up 80% of the data, but also examine the smaller and more recent sample of projects in high-income countries (primarily the United States).

| Main sample | High income countries | |||||

| (1) | (2) | (3) | (1) | (2) | (3) | |

| log(Treatment Arms) [] | 0.180 | 0.183 | 0.215 | 0.391 | 0.259 | 0.214 |

| (0.077) | (0.064) | (0.080) | (0.128) | (0.102) | (0.098) | |

| Proposal Type FEs | No | Yes | Yes | No | Yes | Yes |

| Initiative FEs | No | No | Yes | No | No | Yes |

| -value, | 0.019 | 0.004 | 0.007 | 0.002 | 0.011 | 0.029 |

| -value, | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| Observations | 812 | 812 | 655 | 195 | 195 | 195 |

| Adjusted R2 | 0.005 | 0.352 | 0.380 | 0.026 | 0.411 | 0.400 |

Note: The dependent variable in all specifications is the (log of) the total cost of the proposed project. Proposal type fixed effects include indicators for full projects, pilot projects, and add-on funding to existing projects. Initiative fixed effects include an indicator for each J-PAL initiative that received funding applications. “High income countries” are as according to the World Bank classification. Heteroskedasticity-robust standard errors in parenthesis.

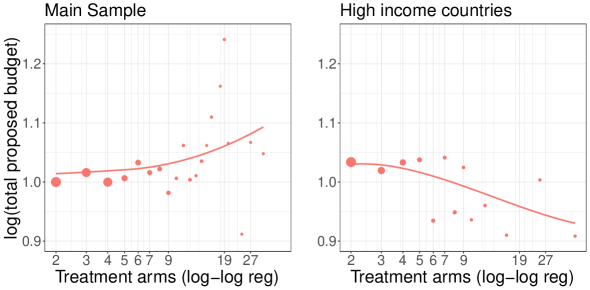

We examine the relationship between project costs and the number of experimental arms using simple regressions of log(total project cost) on log(number of experimental arms). In some specifications we also condition on fixed effects for additional project characteristics; this accounts for the fact that the joint distribution of costs and treatment arms we observe may arise from a single research cost function , as we supposed above for expositional simplicity, or from a mixture of different project-type-specific cost functions. We then report results from tests of the hypotheses that the coefficient on log-cost is zero and one, respectively. The first condition holds if costs are invariant with respect to the number of arms, in which case average size control is indicated (Proposition 5). The second holds if costs are proportionate to the number of arms, in which case no MHT adjustment is indicated.

The data reject both of these hypotheses (see Columns 1–3 of Table 1, as well as Figure 5 in the Appendix). Regardless of the specification, costs are significantly less than proportional to the number of treatments tested. But they are also not invariant to scale: projects with more arms cost significantly more, with a 100 log point increase in the number of arms raising costs by approximately 20 log points on average. Interpreted through the lens of our model, these patterns provide both a prima facie justification for applying MHT adjustment to studies of this sort, and also imply that simply controlling the average size of tests in these studies (e.g., via a Bonferroni correction) would be too conservative. Quantitatively, the appropriate level of the separate -tests for a study testing treatments would satisfy

| (22) |

If (as is a current norm) studies evaluating one treatment used a critical value of , studies of two treatments would thus use a value of , studies of three treatments would use a value of , and so on. In short, even if we take a relatively dim view of researcher motivations, the MHT adjustments implied by the framework are less conservative than those often used in practice.

Note that the appropriate adjustments may be context-specific. In the smaller sample of studies from high-income countries we see that studies with more arms cost less on average (Columns 4–6), presumably reflecting heterogeneity in project types. And there is likely similar heterogeneity underlying the low-income country data. Projects that deliver experimental manipulations through SMS and measure outcomes in administrative data, for example, likely have very different cost structures than those that involve large-scale in-person interventions and surveys of households in remote rural areas. Our anonymized data do not let us observe and draw out sharp distinctions between different projects (e.g., whether an experiment is a field or online experiment), though we do see that even simply adding fixed effects to condition on proposal type and initiative can change the coefficient on the number of treatment arms meaningfully. A planner who could observe more detailed project type information would generally wish to condition testing protocols on it.292929In some cases researchers might be able to credibly disclose the cost structure of studies in a similar class to theirs, and pre-specify test procedures based on these. If so one would expect this to lead to widespread disclosure via the unravelling effects that are standard in disclosure games.

4.2 Some generic principles

A systematic assessment of the framework’s applicability to other genres of experimental research, both inside and outside of economics, is beyond the scope of this paper. We certainly do not wish readers to take it as providing blanket prescriptions for practice across all such domains. At the same time, however, several of the principles that drive our results seem likely to generalize broadly across experimental work.

First, if MHT adjustments are a means of “getting research incentives right,” then they must depend on the costs of doing research. It must be the net incentives, i.e., rewards net of costs, that matter. This perspective is useful as it grounds optimal testing procedures in measurable quantities, as we saw above in the applications to clinical trials and policy experiments in economics. It may also help to clarify confusion about the boundaries of MHT adjustment—the concern, for example, that if it is appropriate to apply MHT adjustment to all the hypotheses tested within one study, then it seems no less appropriate to apply it to all the hypotheses tested within one researcher’s lifetime. A cost-based perspective avoids such “reductio ad absurda” by delineating clear boundaries. Two hypotheses interact for the purposes of determining testing protocols if they also interact in the research cost function. MHT adjustment might thus be inappropriate within a single paper that reports results from two separate experiments, but might be appropriate across two papers that report distinct results from the same experiment.

Second, different types of multiplicity should typically be treated differently. Multiple treatments and multiple sub-populations imply multiple decisions—which treatments should be given, and to which sub-populations? This in turn means that multiple tests are needed, and the MHT question becomes pertinent. Multiple outcomes, on the other hand, do not necessarily imply that the researcher must conduct multiple tests. They can (and often are) aggregated into summary statistics instead. This distinction aligns with our reading of the historical narrative about MHT practices in the literature: the multiple-treatment case—genetic association testing in particular—has often been cited as the leading motivation for new MHT procedures proposed (see Dudoit et al., 2003; Efron, 2008a, for reviews), while the (superficially similar) case of multiple outcomes case seems to have been grouped in with the others subsequently and less intentionally.

What of non-experimental research? Our focus has been on the experimental case, where it is reasonable to imagine requiring researchers to commit in advance to the tests they will run. Optimal protocols for observational studies would likely need to account for additional factors. Observational work is often iterative in complex ways, and issues such as -hacking may consequently loom large. (Interestingly, and in contrast to experimental work in economics, fewer than 5% of top-5 non-experimental empirical papers published in 2020 even mention multiple testing as a potential issue.) That said, the central role of the research cost function is a point of commonality across these problems.