sectioning \setkomafontdescriptionlabel \setkomafontsection \setkomafontsubsection \setkomafontsubsubsection \setkomafontparagraph \setkomafontsubparagraph \setkomafontauthor \setkomafontdate

Learning to reflect

Abstract

Stochastic optimal control problems have a long tradition in applied probability, with the questions addressed being of high relevance in a multitude of fields. Even though theoretical solutions are well understood in many scenarios, their practicability suffers from the assumption of known dynamics of the underlying stochastic process, raising the statistical challenge of developing purely data-driven strategies. For the mathematically separated classes of continuous diffusion processes and Lévy processes, we show that developing efficient strategies for related singular stochastic control problems can essentially be reduced to finding rate-optimal estimators with respect to the -norm risk of objects associated to the invariant distribution of ergodic processes which determine the theoretical solution of the control problem. From a statistical perspective, we exploit the exponential -mixing property as the common factor of both scenarios to drive the convergence analysis, indicating that relying on general stability properties of Markov processes is a sufficiently powerful and flexible approach to treat complex applications requiring statistical methods. We show moreover that in the Lévy case—even though per se jump processes are more difficult to handle both in statistics and control theory—a fully data-driven strategy with regret of significantly better order than in the diffusion case can be constructed.

Keywords: nonparametric statistics; singular control; diffusion processes; Lévy processes; overshoots; exploration vs. exploitation; reinforcement learning; -norm risk

MSC 2020: 62M05, 62G05, 93E20, 93E35, 60G10, 60G51, 60J60

1 Introduction

From a purely mathematical point of view, the field of statistics of stochastic processes is very appealing as it lives from the combination of different techniques and findings from diverse mathematical areas, in particular statistics, probability theory or functional analysis. The fundamental motivation of this branch of statistics, however, results from concrete applications. Thus, besides mathematical elegance and completeness, the developments and results in this area should always be tested in terms of their applicability.

An important area in which stochastic processes (especially of diffusion-type) are used by default to account for random impacts is stochastic control theory. Whereas the theory itself is very well developed and offers concrete decision strategies for a variety of problems, these are usually based on the assumption that the decision maker has full knowledge of the dynamics of the underlying random process. In [12], we have already presented an approach to overcome this constraint by means of nonparametric estimation methods and proposed a fully data-driven approach to solving a concrete impulse control problem. In this paper, we are expanding the view and approaching the problem from a general perspective. Basic components for the data-based solution of a large class of stochastic control problems are

-

¿¿

the control of the -norm risk for the estimation of certain (functionals of) characteristics of the random process, in particular

-

¿¿

the derivation of upper bounds on the convergence rate.

In Section 1.1, we describe the nature of the control problems and how they naturally lead to associated nonparametric estimation problems. Based on this, in Section 1.2, we briefly formulate our general statistical modelling framework.

1.1 The motivating control problems

The stochastic control problems we consider in this paper are—under the assumption that the decision maker has access to the underlying dynamics—classical, and variants are well-studied. They have in common that a decision maker controls a continuous-time process on the real line, but the controls do not change continuously over time, but are of a singular type. More precisely, it turns out that the optimal strategies call for reflecting the underlying process at certain boundaries. These optimal boundaries can be found (semi-) explicitly as optimizers of certain (deterministic) auxiliary functions, based on the dynamics of the underlying uncontrolled process. In this paper, we consider the more realistic situation that the decision maker has to estimate the underlying dynamics while controlling the process. The main key for such a statistical treatment is that, for an underlying ergodic scalar diffusion , the corresponding auxiliary function can be described explicitly in terms of the invariant density, as detailed in Section 2. For estimating the optimizer in this case, the -norm risk of invariant density estimators has to be studied. In Section 3, we then turn our attention to a control problem for underlying Lévy processes. In this case, the auxiliary function is identified as a generator functional of the ascending ladder height process belonging to a Lévy process . Again, a -norm estimation procedure for such functionals has to be found.

A data-driven solution method for the control problems therefore naturally leads to the challenging statistical problem of setting set up a framework such that the seemingly different issues of -norm estimation of the invariant density of an ergodic diffusion on the real axis and -norm estimation of ladder height generator functionals for a Lévy process can be integrated into.

1.2 Nonparametric analysis: Controlling the -norm risk of Markovian functionals

The identification of an appropriate technical framework is a crucial issue for the statistical analysis of stochastic processes. Specific model choices such as scalar diffusion processes or multivariate reversible processes with continuous trajectories permit the application of particular technical tools (e.g., associated to diffusion local time or to the symmetry of the semigroup), but generally do not provide any information about the robustness of the used statistical methods beyond the chosen framework. In contrast, exponential -mixing of general continuous-time Markov processes has been identified in [18] as a criterion which, on the one hand, is strong enough to serve as a central building block of a robust statistical analysis while, on the other hand, providing sufficient generality to allow to include an exhaustive list of Markov processes in the framework. Statistical properties of such processes can thus be studied based on fairly general results rooted in stability theory of Markov processes. We recall them at this point in order to apply them afterwards to estimation problems that are central for developing efficient data-driven stochastic control procedures.

Basic notions and results

Suppose that is a Borel right Markov process on some Borel state space with semigroup

and unique invariant distribution , i.e., for any it holds that

Denote, for , and . We say that , started in some distribution on the state space, is exponentially -mixing if there exist constants such that

Here, denotes the probability measure on , defined as the image measure of under the canonical injection . This implies that, for , we have . This demonstrates that -mixing of a Markov process describes a form of asymptotic independence of its future and its past. In case , we just write , and it can be shown that the -mixing coefficient reduces in this case to

denoting the total variation norm. The central assumption in [18] is that the stationary Markov process is exponentially -mixing, i.e., there exist constants such that

| (1.1) |

Under this condition, the following result is proved.

Proposition 1.1 (Theorem 3.2 in [18]).

Let be a countable class of bounded real-valued functions satisfying , and define

Suppose that is stationary with invariant distribution and exponentially -mixing, and let . Then, there exist and constants such that, for any ,

| (1.2) |

Here, for ,

defines a semi-distance and, for any semi-distance and , denotes the covering number of by -balls of radius .

This result covers a wide range of potential applications. For example, it can be used to find optimal upper bounds (regarding the -norm risk over bounded domains) for nonparametric estimation of the invariant density for -valued Markov processes with transition densities (cf. Sections 4 and 5 in [18]). Such results are derived from Proposition 1.1 by bounding the (pseudo-) norms and thus the associated entropy integrals for the function class related to the chosen estimation procedure. For , this can be achieved by using the analytical properties of , while bounds on the pseudo-metric are based on suitable bounds for the variance of integral functionals of . As shown in [18], for this is taken care of using the exponential -mixing property of once we assume that, additionally, an on-diagonal heat kernel estimate is in place for the densities of the Markov semigroup, i.e., there exists some constant such that

Application in the scalar setting

It will be demonstrated in the sequel that the one-dimensional case can also be treated optimally within the framework described in Proposition 1.1, thereby distinguishing between two different situations. In Section 2.1, we study kernel invariant density estimation (for scalar ergodic diffusions) which requires a careful balancing of bias and stochastic error of the estimator (in case of pointwise risk, the well-known bias–variance tradeoff) by choosing an appropriate bandwidth . In dimension , the -mixing property is not quite sufficient to guarantee variance bounds that are tight enough for proving optimal upper bounds on the convergence rates. We additionally require convergence of the semigroup densities to the invariant density at sufficient speed on compact sets, combined with a relaxation of the on-diagonal heat kernel estimate of the semigroup. In Appendix A, we demonstrate that classical assumptions on the diffusion process—as they are introduced in Section 2 to ensure existence of a stationary solution—are tight enough to match the above requirements. This is of considerable independent interest since, in contrast to the local time arguments usually employed for the statistical analysis of scalar diffusions, the techniques generalize without much effort to the multivariate diffusion case. Our framework therefore arguably closes the gap between the relatively distinct approaches to statistical estimation of scalar and multivariate diffusions (see, e.g., [16] vs. [15] or [13, 14] vs. [42, 41]). Moreover, it potentially extends results obtained exclusively for symmetric diffusions to the general case since it is not reliant on functional inequalities, which are not well-suited to the non-reversible setup, see also the discussion in [18].

Suppose that we can find an unbiased estimator of the characteristic we are interested in. In this situation, a fine analysis of the variance of Markovian functionals is not necessarily needed. This is, e.g., the case if we can express the quantity of interest as an integral wrt the stationary distribution of some stationary Markov process , since then the continuous-time mean estimator

is unbiased. If is moreover -mixing, we can make use of Proposition 1.1 based on purely analytical arguments. This will become clear in Section 3.1, where we are investigating -norm estimation of generator functionals of the ascending ladder height process belonging to a Lévy process via an unbiased mean estimator based on overshoots of . The thereby established -norm bounds will be of central importance for the procedure in Section 3.2.

1.3 Organization of the paper

In Section 2, we develop a data-driven strategy for a singular control problem associated to a scalar diffusion process. The construction and error analysis is given in Section 2.2, based on a minimax optimal estimation procedure for the stationary density under exponential -mixing assumptions, which is carried out in Section 2.1. Appendix A complements the study of Section 2.1 by demonstrating how the variance analysis of the estimator can be carried out in a self-contained fashion within the -mixing framework without having to resort to local time arguments which do not generalize to higher dimensions. In Section 3, a data driven strategy for an impulse control problem with an underlying Lévy process is constructed. The statistical foundations for the estimation strategy of Section 3.2 are presented in Section 3.1. Central aspects of overshoot convergence as main ingredient to the statistical analysis are summarized in Appendix C.

2 Data-driven singular controls for diffusions on the real line

We now introduce the singular control problem for underlying scalar diffusion processes, given as a solution of the Itō-type SDE

| (2.1) |

some measurable functions and some standard Brownian motion on some probability space One motivation for considering such problems comes from investigating optimal dividend distributions [3, 6, 10]. Another stream of literature deals with determining a policy that optimizes the expected cumulative present value of the harvesting [2, 24, 28]. In particular for the latter application, it is natural to study an ergodic formulation, as it reflects the idea of considering sustainable harvesting guidelines, which we will also use here.

Assume that for some constants is continuous, differentiable and globally Lipschitz and satisfies for all . For fixed constants and , define the set as

Note that a linear growth condition for Lipschitz drift is always satisfied, but the class specifies a global magnitude of this maximal growth in terms of the constant . Moreover, given as above and any , an immediate consequence is that there exists a strong solution of the SDE (2.1) for given initial value independent of . If we let , then defines a non-explosive Feller Markov process and thus in particular a Borel right process. Moreover, has a unique stationary distribution having invariant density

| (2.2) |

with normalizing constant . In the following, we will abbreviate and, if there is no room for confusion, also just write instead. For any , is continuously differentiable and there exists a constant (depending only on ) such that

| (2.3) |

Furthermore, for any fixed bounded set , there exists some (depending again only on ) such that

| (2.4) |

The controls used to formulate the problem are of the form for non-decreasing, right-continuous and adapted processes and . Here, and denote the cumulative upwards and downwards controls, resp. These processes can be decomposed into singular and jump part as

where and are continuous. In the following, we will mostly deal with a special class of controls for which the jump part is absent (with a possible exception at ): and are associated to the local times at certain fixed points .

We denote the set of all controls by and, for each , we define the controlled process as the solution to

where we work under the assumption that , implying in particular that the uncontrolled process has a stationary distribution .

The problem to be studied is now to determine the minimal value and the minimizer of

| (2.5) |

where is a continuous, nonnegative function with

modelling the running costs and are positive constants describing the (proportional) costs associated with applying a control. We can interpret our goal as keeping close to the target state , say, and therefore assume that has a minimum in 0. The goal in the sequel is to find a data-driven strategy for problem (2.5) when the drift of the underlying process is unknown. While parts of the following analysis are similar to the one in [12], it here turns out to be essential to control the -norm risk of estimators of the characteristics (precisely, the invariant density ) of solving (2.1).

2.1 Estimating the stationary density of ergodic diffusion processes

We first show how the underlying statistical problem for the uncontrolled process can be integrated into our general framework presented in Section 1.2. For a large class of ergodic scalar diffusion processes solving (2.1) it is known that, given continuous observations , the invariant density can be estimated with a parametric rate of convergence. For an overview, we refer to Sections 1.3.2 and 4.2 in [26]. It is however not straightforward to extend bounds on the pointwise or risk to the -norm bounds required for our application. A corresponding result is given in Corollary 13 in [1] whose proof, however, relies substantially on the use of diffusion local time. We show how this behaviour can also be deduced from mixing properties of the diffusion.

Given some fixed domain , constants and a measurable function , introduce the set

| (2.6) |

Note that for diffusions with drift it holds that is exponentially ergodic, i.e., the total variation distance between the marginal laws of and the invariant distribution decreases exponentially fast in time, and is exponentially -mixing with mixing coefficient , which is independent of . As demonstrated in Proposition A.2 and Lemma A.4, exponential ergodicity and the exponential -mixing property are satisfied for any such that the coefficients and are globally Lipschitz. Apart from the assumption on the Hölder continuity of , restricting the class to should therefore be understood as a technical device to obtain uniform control on the coefficients in the exponential -mixing bound, which is needed for the upper bound in the minimax sense provided in Theorem 2.1. In the following, we consider the supremum norm on .

Theorem 2.1 (concentration of invariant density estimators).

Fix some open and bounded set , assume that , for some , and let be a compactly supported, Lipschitz-continuous kernel function of order . Define the estimator

| (2.7) |

Then, for any ,

| (2.8) |

Proof.

Fix and , and denote , , ,

Given any , it follows from Proposition A.2 and Lemma A.3 that the associated diffusion process solving (2.1) is exponentially -mixing. Thus, we may apply Proposition 1.1 for bounding

| (2.9) |

Let as in Proposition 1.1, and denote by the local time of at the point up to time , fulfilling in particular . Using the occupation times formula and Minkowski’s integral inequality, one obtains

| (2.10) |

where the last estimate follows from Proposition 5.1 in [16] and is a constant depending only on the class . Thus,

such that for . Similarly, for any ,

Assuming that and denoting by the Lipschitz constant of , it then follows from Lemma A.6 that

Thus, Proposition 1.1 gives that (2.9) is upper-bounded by

| (2.11) |

where the last implication follows from the choice of and . The conditions on the order of the kernel function and the fact that further imply that, for any ,

In combination with the upper bound on the stochastic error stated in (LABEL:eq:stocherror), we thus obtain (2.8). ∎

For the sake of a concise presentation, we have here restricted to demonstrating how a bound for the -norm risk can be derived directly from Proposition 1.1. Main components for doing so are the verification of the mixing property and the derivation of bounds of the variance of integral functionals. Further details on these two steps are summarised in Section A. In particular, we show there how a variance bound as in (2.10) can be derived without relying on specific properties of diffusion local time.

Although assuming stationarity of the process is standard in the statistical literature, this assumption can be slightly problematic for practical purposes. In the present scenario this will become evident for our proof technique of the data-driven control strategy, where we require -norm bounds under instead of . To extend the rate result (2.8) from the stationary regime to the non-stationary case, we use the following auxiliary result, which shows that exponential convergence allows to exactly quantify the loss imposed by non-stationarity for nonparametric estimation. We focus on the case as the relevant result for our purposes.

Lemma 2.2.

Let be a topological space and an -valued exponentially ergodic Markov process, i.e., there exist a function and constants such that, for any ,

where is the invariant distribution of . Then, for any bounded , and large enough such that , it holds that

Proof.

Let

and

Then,

where for the second inequality we used reverse triangle inequality for the first two summands and the last equality is a consequence of the Markov property of and stationarity of under . Using that , exponential ergodicity of yields

as claimed. ∎

With this at hand, we obtain a non-stationary version of Theorem 2.1.

Corollary 2.3.

Given the assumptions from Theorem 2.1, it holds for any that

| (2.12) |

2.2 Application

We now turn to analyzing the singular control problem. Given the literature on related problems, it is natural to expect reflecting barrier strategies, i.e., strategies which maintain the process between two constant thresholds and and just grow at these points, to be optimal. We denote such strategies for upper and lower, resp., boundaries by and and refer to [23, §23] for an explicit characterization, which underlines the interpretation of these processes as local times at the boundaries and , resp., of the process .

2.2.1 Solution for known drift

Using classical ergodic results for one-dimensional linear diffusions, it is straightforward to show the following analytic expression for the expected costs when applying reflecting barrier strategies. We refer to [4, Proposition 2.1] for a detailed proof.

Lemma 2.4.

Let and . Then, for ,

with

where denotes the speed density and the scale function of the underlying diffusion.

For our later purposes, the main observation is that—given the volatility —the expected cost function can completely be described in terms of the invariant density of the underlying diffusion. Indeed:

Therefore, minimizers of correspond to optimizers of (2.5) in the class of reflecting barrier strategies. The next natural question is whether such minimizers are indeed optimal within the class of all admissible strategies, i.e., whether the minimal value in (2.5) is equal to

This also holds under natural assumptions as can be proven, e.g., adapting the lines of argument in [29, 11] to the two-sided case. We, however, do not go into detail here to not overburden our paper with technicalities, but restrict our attention to the class of reflecting barrier strategies in the following.

As 0 is our target state, it is furthermore natural that 0 is contained in the no-action-region which is assumed to be bounded. More precisely, we assume that there exists such that the minimizer of fulfill

In [4], a natural set of assumptions is introduced to guarantee that is characterized as the unique critical point of the function . We, however, do not need uniqueness for our purposes.

2.2.2 Construction of the estimators

We proceed by constructing estimators and for the optimal thresholds and which are based on the estimator of the invariant density (see (2.7)). To this end, we fix some , set , and write . In principle, we just use the plug-in estimator, taking however into account that (cf. (2.4))

This leads to the estimator

for the expected value of a reflection strategy with barriers , yielding

as our estimator for the optimal thresholds. Using this, we obtain that the expected costs, when using the strategy based on the estimator after having observed the uncontrolled process for time units, converge to the optimal value with rate .

Proposition 2.5.

For any , there exists such that

2.2.3 Data-driven singular controls

In most real world applications, the decision maker is faced with the problem of collecting data about the underlying dynamics and finding the optimal strategy at the same time. Here, however, a classical trade-off between exploration and exploitation occurs. On the one hand, the decision maker wants to minimize her expected costs and therefore uses singular control strategies with an optimal estimated threshold. On the other hand, using such a greedy strategy all the time, the decision maker can’t learn about the drift of the underlying process outside the estimated control interval and therefore this procedure cannot even be expected to converge.

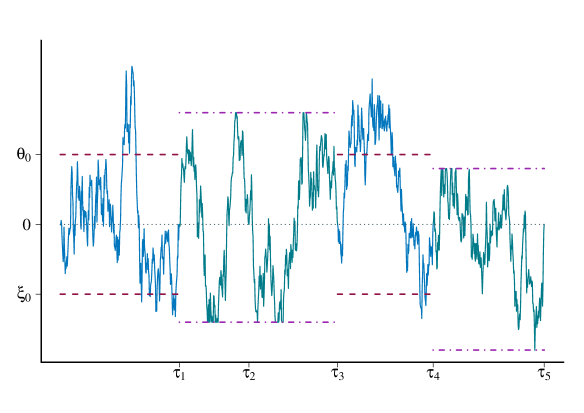

Our solution is to separate exploration and exploitation periods as follows (see Figure 2.1): At the beginning of every period except the first, the process is in the target state 0. In the exploration periods, we then let the process run uncontrolled and the period ends when the process again reaches 0 after having visited two predefined boundaries .

In the exploitation periods, we use an estimator for as defined in the previous section in order to choose suitable thresholds based on the observations. The exact specification for this estimator is given below. An exploitation period ends after the process has been reflected at both the upper and lower estimated boundary and has returned to 0. In the following, we will always set .

We combine exploration and exploitation periods using a (deterministic) sequence , where (and ) means that the -th period is of exploration-type (and exploitation-type, resp.) and denote the corresponding strategy by . By we denote the stopping times separating the periods defining . The question now is how to balance the time spent for exploration and exploitation. A suitable choice can be made by taking into account the estimation error bounds from the previous section and balancing the errors from misspecifying due to the estimation error and the losses due to the lack of control in the exploration periods. As we will see below, a suitable choice are sequences such that there exists with

| (2.13) |

Observe that for such a sequence there exists such that

| (2.14) |

Note that is a Brownian motion for the filtration generated by and the independent random variable . With respect to this filtration, the times separating the different periods are stopping times. Therefore, the process which is constructed by putting together the paths of in the exploration periods, is again a Brownian motion. As the process which is constructed by joining the paths of in the exploration periods fulfills and solves the SDE

it has the same dynamics as the uncontrolled process .

We denote the estimator for the optimal threshold from Section 2.2.2 for the uncontrolled process until time by and define where denotes the time that the controlled process has spent in the exploration periods until , and is a constant specified in the following lemma. In other words, we base the estimator for the threshold used in the exploitation periods just on the observations in the exploration periods and, in addition, just for technical reasons, ignore all observations after time .

We first observe that condition (2.13) implies that the time spent in the exploration periods until time is of order . In particular, and . More precisely:

Lemma 2.6.

Let satisfy (2.13) with corresponding data-driven strategy as specified above. Then, there exist such that

where denotes the number of exploration periods until time .

The proof, which is quite technical and based on renewal theoretic arguments, is deferred to Appendix B. The main result of this section given below shows that, by employing the strategy , we can guarantee that the expected regret per time unit vanishes with rate .

Theorem 2.7.

Let satisfy (2.13) with corresponding data-driven strategy as specified above. Then, the expected regret per time unit is of order . That is, for any , we have

Proof.

We first consider the costs in the exploration periods. Using [5, Chapter VI, Theorem 1.2], we first see that in one exploration cycle starting and ending in 0, the expected costs are

with finiteness of (arbitrary) moments of under being demonstrated in Appendix B. Hence, the expected costs per time unit in full exploration cycles are and the time spent in such cycles until is bounded by . If we consider the cumulative costs until time , we have to take into account that the last exploration cycle may be cut off at the deterministic time . Putting pieces together, we can bound the expected costs in the exploration period as follows:

where we applied Lemma 2.6 with denoting the number of exploration periods until time and is the filtration generated by the controlled process . To analyze the costs in the exploitation periods, we write for the time spent in the exploitation periods and—again using [5, Chapter VI, Theorem 1.2]—similarly get

where denotes the length of an exploitation period with maximal length (i.e., a period with reflection in ). On the event , we have that , so that by Lemma 2.6 and Proposition 2.5, we have

for certain constants , hence

for certain constants . Putting pieces together , we obtain

∎

3 Data-driven controls for Lévy processes

We now turn our attention to another class of non-continuous control problems. The first main difference is that we consider a one-sided class of problems, that is, we just consider downward controls. Second, we assume the underlying processes to have jumps. More precisely, as our driving process, we take a Lévy process , started in under , satisfying the basic assumption

-

()

is upward regular, i.e.,

and moreover .

Let us note that any Lévy process with unbounded variation (i.e., either has a non-trivial Gaussian part or ) satisfies the upward regularity assumption. For a full description of upward regularity in terms of necessary and sufficient conditions, also covering a subset of Lévy processes with bounded variation, see [27, Theorem 6.5].

Control problems with underlying jump processes are known to be much harder to analyze than their counterparts without jumps, see [32] for discussions and many examples. To formulate our problem, we fix a non-decreasing function . In contrast to the singular controls discussed in Section 2.2, we now consider controls of impulse-type. These are sequences of stopping times and -measurable random variables describing the times of the interventions and the state after exercising the control, respectively. The corresponding controlled process is given as

Here, the value at time , but with the control not having taken place yet, is denoted by

In general, for processes with jumps, this quantity may deviate from both the value at time after the control has taken place and the left limit . We can interpret as the value of a natural resource we are managing. In most examples of interest, has a sigmoidal form, so that (without interventions) the value is expected to grow fast whenever takes moderate values, while the value grows slowly whenever has either large or small values. The stopping times describe the times of intervention. From the motivating problem, it is clear that we only assume downward controls to be admissible, i.e., we assume that for all .

Our aim is to find a maximizer and the corresponding value of the expected rewards without fixed transaction costs, defined by

| (3.1) |

in the class of all admissible impulse control strategies .

We will argue in Section 3.2 below that the main tool for solving (3.1) is the ascending ladder height process. For the reader who is not familiar with this notion, we have collected the underlying concepts and main results needed in the following in Appendix C. Note that () implies almost surely. Let , , be the ascending ladder height subordinator of , where is a version of local time at the supremum and is its right-continuous inverse. Note that can be chosen to be continuous by upward regularity of , which entails that is strictly increasing and thus is a strictly increasing subordinator (or, put differently, is not compound Poisson). Moreover, for any , is an -stopping time, where denotes the usual completed natural filtration of . Motivated by the solution technique for the associated control problem, we choose a scaling of such that and hence, by Wald’s equality (cf. [33, Corollary 2.5.2]),

Let denote drift and Lévy measure of and be the domain of the extended generator of , i.e., a measurable function belongs to if the exists some measurable function such that

is a local martingale. By Itō’s formula for semimartingales applied to , see e.g. Theorem I.4.57 in [25], it follows that for such that

| (3.2) |

is well-defined that is a local martingale. For such functions we set . We will see in Section 3.2 below that the auxiliary function is the key for the solution to (3.1). More precisely, yields a maximum representation of the payoff that is needed to guarantee optimality of a threshold time, which can be derived from .

3.1 Estimating generator functionals for the ascending ladder height Lévy process

Motivated by this observation, to implement a data-driven strategy our goal is to find an estimator of for an appropriate , based on a continuously observed trajectory of up to some fixed time horizon , with good approximation properties wrt the -norm risk. Estimating is therefore of significant applied interest and, as it will turn out, establishing bounds for the sup-norm risk provides the right tool to infer estimates for the expected regret of data-driven control strategies. For our purposes, we will need to assume that is bounded, which is clearly in line with a typically sigmoidal form of .

In order to construct an estimator for , a first intuitive approach would be to assume that is absolutely continuous with Lebesgue density and reconstruct a path from the full observations to develop a nonparametric estimator of and then analyze the plug-in estimator

| (3.3) |

based on convergence rates of as . An appropriate estimator for in this scenario is given by

for , where is some bandwidth and a high-order kernel function, see [38, 39].

However, under ()—even with a full record of —local time cannot be observed in general since its construction is not purely path dependent, see [8, Chapter 4]. Hence, in our framework such ansatz is hopeless, unless is assumed to have a one sided jump structure, i.e., is either a subordinator (increasing paths), spectrally negative (only negative jumps but non-monotone paths) or spectrally positive (only positive jumps but non-monotone paths). In the subordinator case we can simply choose and hence , i.e., the problem of estimating the generator functional via the plug-in estimator reduces to estimation of the Lévy measure and drift of . When is spectrally negative, we can choose , where and is some scaling factor. Then, , where is the first passage time of the level . By exclusively negative jumps, reaches its maxima continuously, hence , where must be chosen such that

| (3.4) |

by our required scaling of local time. Thus, estimation of the generator functional in this case boils down to estimating the drift , which would require estimation of expected first passage times for different levels and solving (3.4) for with the expectation on the right hand side replaced by the constructed estimators. This is a non-trivial procedure and it is not clear how such issue should be efficiently attacked with a given dataset. For the case of spectrally positive processes, a similar issue would arise for the correct scaling of local time at the infimum.

Thus, the only direct estimation approach other than the one we introduce below, demands restricting to a subordinator. If its Lévy measure is finite (i.e., must be a compound Poisson subordinator with positive drift since we require ()), it follows from Theorem 3.1 in [39] that (ignoring the drift part) the -risk of the estimator (3.3) is of order . At the end of this section, we will argue that even in this much more restricted setting, our estimator—which can be applied for arbitrary jump structures—matches this performance.

Let us therefore now show how to go a more sophisticated route, exploiting the probabilistic structure of the generator functional by making use of stability results on overshoots of Lévy processes recently discussed in [19]. This is in general a very natural approach for statistical inference of objects related to due to its intimate connections with overshoots of , briefly described in the sequel. An overshoot of over the level is defined by

where is again the first hitting time of . If we consider the spatial levels that surpasses along its lifetime as time index, it can be shown that under () the overshoot process is a Feller Markov process.

Its role in revealing the characteristics of the ascending ladder height process stems from the simple observation that the closure of the range of almost surely is identical to the range of the running supremum process , , and hence the overshoot process of is indistinguishable from . It is shown in [19] that the unique invariant distribution of is given by

with the second equality being a consequence of our particular scaling of local time. If we assume additionally that

-

()

either, , or there exists such that ,

it follows from Proposition C.1 that, for any ,

| (3.5) |

where (as before) denotes the total variation distance. In Proposition C.1, conditions on the characteristics of the parent process implying () are given. These underline that most explicit Lévy models fall into the total variation convergence scheme provided that upward regularity is satisfied, since these usually either possess a non-trivial Gaussian component or the Lévy measure is constructed from a Lebesgue density. Finally, assuming

-

()

there is such that ,

which is true iff integrates , Proposition C.3 states that total variation convergence in (3.5) takes place at exponential rate and that is exponentially -mixing whenever the initial distribution integrates . In particular, the stationary overshoot process is exponentially -mixing, with -mixing coefficient

| (3.6) |

for some constant and arbitrary . Starting from this general setup, the fundamental observation for our purposes is that, for , we can rewrite (3.2) in terms of an integral wrt the invariant overshoot distribution .

Lemma 3.1.

For any with bounded derivative we have

Proof.

Note first that and boundedness of guarantee that both sides of the equation are well defined. Plugging in and using Fubini we obtain for ,

∎

Remark 3.2.

This formula is valid for any subordinator with finite mean.

It follows from von Neumann’s ergodic theorem that, for any and ,

It is therefore natural to consider as an estimator of , based on overshoot observations up to some spatial level , the unbiased (under ) estimator

with assumed to be known (which is not a strict assumption in light of i.i.d. increments of ). To establish convergence bounds wrt to the -norm risk, we make use of Proposition 1.1. We apply this result to the function class

to find a convergence rate of for the -norm risk

for some bounded open set . The choice of evaluating the sup-norm risk wrt is somewhat arbitrary and can be replaced by for any by spatial homogeneity of the Lévy process. We stress however that, although we make heavily use of ergodic arguments, we do not need the process to be started in the stationary overshoot distribution for our results. Similar to the proof of Corollary 2.3, the key for this is Lemma 2.2 in conjunction with exponential ergodicity of .

Proposition 3.3.

Let such that is bounded. Then there exists a constant such that

Proof.

By stationarity of under and its exponential -mixing property (3.6), which is guaranteed given our assumptions, it follows easily (see, e.g., the proof of Proposition 2.4 in [18]) for any bounded and that

for some . Hence, there exists a constant such that, independently of , for any bounded

| (3.7) |

Letting and using the fact that is Lipschitz on the bounded set thanks to , it follows with Lemma A.6 that

where denotes the Lipschitz constant of on . It therefore follows that the associated entropy integral is finite, i.e.,

and by (3.7) the same is true for the entropy integral

with a constant independent of . Since , choosing and plugging into (1.2) therefore reveals that there exists a constant such that

| (3.8) |

As in the proof of Corollary 2.3, we transfer the sup-norm risk bound from the stationary regime to the case when is started in . This can again be achieved utilizing exponential ergodicity of . Let

Then,

which is finite by boundedness of . Using exponential ergodicity of as stated in Proposition C.3 and applying Lemma 2.2 shows that for and large enough such that

Together with (3.8), this implies that

for some constant , by triangle inequality. ∎

Proposition 3.3 shows that is not only an elegant but also efficient estimator for , provided that we have an overshoot sample available up to a fixed level . However, we observe the Lévy process up to a fixed time and not up to the random first passage time . Our agenda therefore must be to build an estimator which is -measurable and whose -norm convergence properties can be inferred from Proposition 3.3. To this end, we aim to make use of the law of large numbers for Lévy processes. Recalling that almost surely for any starting distribution of , it follows that, for any ,

| (3.9) |

Define

| (3.10) |

and note that, since for any , we have

as a consequence of thanks to being an -stopping time. Therefore, for any as desired. As a key result, the following preparatory lemma shows that the two essential components involved in an upper bound of the sup-norm risk of are indeed the rate of and the speed of convergence in (3.9).

Lemma 3.4.

Let such that is bounded. Then, there exists a constant such that, for any and , we have

| (3.11) |

Proof.

Let again . Then, for , it follows by the triangle inequality and Proposition 3.3 that

where for the second inequality we used that, by our choice of , we have on . ∎

The following result complements results on tail asymptotics of the marginal for fixed of a Lévy process with bounded jumps, which can be found in Theorem 26.1 of [35], and non-asymptotic tail bounds of a Lévy process for small times , recently discussed in [21]. It is a slight digression from the remainder of this section in the sense that the assumptions ()-() are dropped in favour of bounded jumps and zero mean of . The statement is of independent interest since it gives nonasymptotic bounds on the speed of convergence of the law of large numbers for Lévy processes with bounded jumps and allows establishing optimal rates for our concrete estimation problem.

Theorem 3.5.

Suppose that is a non trivial zero mean Lévy process with bounded jumps and Lévy triplet Then, there exists and for such that for any ,

Proof.

Let be the maximal jump size of . If , is a scaled Brownian motion since and was assumed non-trivial. In this case, the result follows directly from the exponential decay of tails of Brownian motion. Suppose therefore that . We only show . The statement then follows by performing the same calculations for the dual process , which also is a zero mean Lévy process with jumps bounded in absolute value by . Since has bounded jumps and zero mean, its Laplace exponent is well-defined on and given by

Furthermore, observe that is smooth with derivative

By [35, Lemma 26.4], is invertible on with strictly increasing inverse denoted by . As in the proof of [35, Lemma 26.5] it follows from

that

Since , this yields

This implies that there exists some and such that for all ,

| (3.12) |

Moreover, it follows from [35, Lemma 26.4] that for any ,

| (3.13) |

Defining and letting be large enough so that for all , it follows from (3.12) and (3.13) that indeed

∎

With this preparation we can now investigate convergence rates of .

Theorem 3.6.

Let such that is bounded.

-

(i)

Suppose that for some . Then,

In particular, if all moments of exist, then, for any ,

-

(ii)

Suppose that has bounded jumps. Then, for large enough, it holds that

Proof.

- (i)

- (ii)

∎

Remark 3.7.

-

(i)

Since our exponential -mixing assumption requires flat tails of at and moreover , the assumption of exponential moments is quite natural in our modelling framework. When jumps are bounded, () is always satisfied. Hence, for most Lévy processes falling into our estimation regime, we can expect a convergence rate of approximately .

-

(ii)

One may wonder whether there was anything to gain, if in the definition of , we replaced by the running supremum . In practice, this would be more natural since otherwise—at least intuitively—data was wasted and moreover the estimator becomes meaningless whenever (which, as time progresses becomes increasingly unlikely). The construction of our estimator on the other hand is driven by analytical tractability. However, in terms of the convergence rate of the estimator we cannot expect to gain much by working with the running supremum. This is evident from observing that Doob’s maximal inequality for the submartingale yields that for any s.t. and ,

Let us interpret this result in detail from a nonparametric angle and, as announced at the beginning of this section, compare our estimator to the plug-in estimator given in (3.3) for the restricted setting of subordinators with strictly positive drift and absolutely continuous Lévy measure with bounded density , for which the latter can be applied.

For the subordinator case, the plug-in estimator has an -convergence rate of . As shown in Theorem 3.6, the overshoot estimator converges at rate with respect to the -norm for any given Lévy process with bounded jumps satisfying () and () and hence in particular for any subordinator with Lévy measure having bounded support (but not necessarily bounded density since infinite jump activity is allowed). It is well-known from nonparametric invariant density estimation of well-behaved scalar stochastic processes that, within a continuous observation scheme, the invariant density can be estimated with the parametric rate wrt the -norm. Estimation wrt the -norm on the other hand introduces an additional -factor, increasing the optimal rate to , as, e.g., in the previously discussed case of scalar ergodic diffusions, see Theorem 2.1.

Thus, in the current nonparametric estimation context we observe the same phenomenon that the common price to be paid is an additional log-factor for optimal estimation with respect to the -norm compared to the optimal -rate. This also indicates that in principle, our approach to find an upper bound on the convergence rate of the overshoot estimator via Proposition 3.3 and Lemma 3.4 for a time-dependent observation scheme is tight enough to establish the optimal convergence rate for more general Lévy processes with unbounded jumps. This is evident from observing that the key result for the proof of Theorem 3.5 is Lemma 26.4 from [35], which relies on a Chernoff bound for the upper tail of a Lévy process at some fixed time . However, interpreting this bound rigorously requires being able to tightly control the asymptotic behaviour of the inverse of the Laplace exponent’s derivative, which for general Lévy processes is not possible. This is why we made use of Markov’s inequality with power functions in the proof of part (i) of Theorem 3.6 instead of the generic Chernoff bound. However, for more particular classes of Lévy processes with explicit Laplace exponent, an ansatz similar to Theorem 3.5 may also provide the optimal convergence rate.

3.2 Application

We now return to the control problem described at the beginning of this section. In the following, we still assume () – () and now present the main tool for our analysis, an auxiliary function defined via

where denotes the extended generator of the ladder height process of as discussed in Section 3.1. Noting that when , Dynkin’s formula and the fact that the values of and coincide at first hitting times almost surely, imply that

this generates an intuition why this function is suitable for the analysis of problem (3.1): using the theory of regenerative processes, see [5], the value coincides with the value of the impulse strategy which shifts the process back to whenever the process is above , so that—at least intuitively— corresponds to the value of the reflection strategy in . The usefulness of this approach for ergodic impulse control problems is demonstrated in [11], where most of the following results can be found. Some further complementing analysis is carried out in [40]. The main observation is that properties of the function determine the form of the optimal solution. For our considerations, we assume the following:

-

()

The function has a unique maximum , is strictly increasing on and strictly decreasing on .

3.2.1 Solution for known processes using an auxiliary impulse control problem

In [11], different classes of functions are discussed that make () hold for all Lévy processes . The main idea for analysing the problem (3.1) is to introduce artificial fixed costs for each interaction, so that we are faced with a problem where we expect stationary impulse control strategies of -type to be optimal. By considering the solutions for , we then obtain the value and an optimal strategy for the problem without costs. More precisely, for each , we define

where the supremum is taken over all admissible impulse control strategies . By elementary arguments, it is immediately seen that is independent of the initial state . To study the dependence on the fixed costs , let us shortly review the key results on long-term average impulse control problems.

Lemma 3.8 ( [40], Theorem 4.3.6).

-

(i)

For all

-

(ii)

If , then an strategy of the form

is optimal. The values and are given as follows: is the larger of the two roots of the equation

If we denote the lower one by , then is given as the maximizer of

Under additional assumptions on the Lévy process, it turns out that which simplifies the solution of the impulse control problems, but is not needed for our purposes. We now study the dependence of on .

Theorem 3.9 ([40], Theorem 4.3.6, 5.3.3, 5.3.4, and 5.3.5.).

The previous results suggest that the reflection strategy at level is optimal in problem (3.1). However, this strategy does not directly fall into the class of impulse control strategies we consider here, but is of (strictly) singular type. In order not to overburden the paper with technicalities, we leave out the discussion of extending the strategy space here. Note however that, due to our ergodic problem formulation, extending the control space is even not needed to obtain optimizers for (3.1): the (non-stationary) threshold strategy with time dependent thresholds and (with as ) is optimal in the class of impulse strategies and converges with arbitrary speed in by choosing sufficiently small costs . Therefore, the term ‘reflection strategy’ refers to a suitably fast approximating impulse strategy in the following.

3.2.2 Data-driven singular controls

The results in Section 3.1 now directly lead to a method for estimating the optimal reflection boundary : after having observed the underlying Lévy process for time units, we define the estimator for the auxiliary function , using the estimator defined in (3.10), and then choose

| (3.16) |

where is some arbitrary bounded, open neighborhood of . The results from Section 3.1 now yield that the estimated optimizer gives the optimal value up to a regret of order when the -th moment of exists and of order when jumps of are bounded. Indeed:

Theorem 3.10.

Let be a bounded open neighborhood of . Suppose that for some . Then, it holds that

If has bounded jumps, then

4 Discussion

The statistical questions discussed in this paper have a clear motivation coming from the analysis of data-driven strategies for natural classes of stochastic control problems. For underlying diffusion processes, the solutions to ergodic singular control problems from Section 2.2 can be written in terms of the invariant density, such that the key to developing data-driven strategies consists in replacing this quantity by a sample-based analogue. From a statistical perspective, this is advantageous because rate-optimal estimation in this case (as opposed to, e.g., estimation of the drift coefficient) does not require an adaptive choice of the bandwidth. Due to the costs for reflection, the error measure to be used is the -norm risk studied in Section 2.1. This is an interesting observation as for the—from the stochastic control perspective highly related—impulse control problem investigated in [12], the risk had to be analysed. The substantially more involved issue of bounding the -norm risk of estimators is tackled by means of Proposition 1.1, exploiting mixture properties of the diffusion process. Since the focus of this paper is on the development of concrete control strategies, we have restricted the presentation in Section 2.1 to a concise proof of the required upper bound (see Theorem 2.1). Once again, we refer to Section A, where we describe a completely self-contained derivation of the convergence rate for diffusions with drift (cf. (2.6)). In particular, it does not rely on any results for diffusion local time and can also be extended in a straightforward way to higher dimensions. We have reduced our explicit statistical investigation to the one-dimensional case solely because of the intended application to the stochastic control problem. Compared to the risk, the evaluation of the -norm risk produces a well-known unavoidable logarithmic factor, which is also reflected in the expected regret per time unit (Theorem 2.7).

While the underlying diffusion processes in Section 2 were assumed to have an ergodic behaviour allowing for a statistical analysis, this is not the case for the Lévy-driven problem introduced in 3.2. By considering a space-time transformation of the Lévy process in form of the overshoot process , we obtained an ergodic Markov process fitting right into our general modeling framework, which allows to express the quantity of interest for the singular control problem, , as an integral w.r.t. its invariant distribution. Combining a simple mean estimator based on an overshoot sample with classical results on the long-time behaviour of Lévy processes then allowed us to construct an estimator whose performance depends on the tail-behaviour of and yields an almost parametric -norm estimation rate in case of light tails and the optimal nonparametric rate when jumps are bounded.

Based on this estimation procedure, we were then able to identify a data-driven singular control strategy, such that the estimated optimal reflection boundary yields an expected regret of the same order as the nonparametric estimation of the auxiliary function .

In contrast to the diffusion case, in the Lévy process framework we are not faced with an exploration vs. exploitation problem: due to the spatial homogeneity of Lévy processes, each controlled process carries the same information as the uncontrolled one (if we assume that the decision maker has access to the values ) as the decision maker can reconstruct an uncontrolled path by just undoing the controls. Therefore, the following greedy strategy can be applied without additional losses: we use the (approximate) reflection controls with time-dependent boundary

for each time point .

Finally, let us briefly outline the connection to related research fields. The exploration vs. exploitation trade-off encountered in Section 2 is also well-known from the famous multi-armed bandit problem. In this regard, it is interesting to observe that the number of boundaries to be estimated in the control problems in our context does not influence the rate of convergence. Up to the logarithmic factor coming from the -norm vs. risk discussed above, the rates of convergence indeed turn out to be the same for the two-sided problem studied here and the one-sided problem from [12]. This is in strong contrast to the related results for -armed bandit problems, see [30, 9].

From a more applied point of view, it is furthermore of interest to compare the data-driven procedure proposed here to results obtained by using established methods from (deep) reinforcement learning. These algorithms are very generally applicable, as they usually only require the presence of a Markovian decision process setting. For classical methods such as the regular Q-learning algorithm, very robust convergence results exist; however, the latter is not practicable for problems in which the state space is too large. In the stochastic control setting considered here, a very large state space cannot be avoided, and a natural approach for circumventing this obstacle is to treat the problem based on the Q-learning algorithm with function approximation. In this respect, the fusion with neural networks has proven to be particularly powerful. A mathematical theory of convergence for the resulting deep reinforcement learning procedures however is still under development. Results from recent contributions such as [22] are very interesting, but there remains a large gap between their theoretical assumptions and the Markov decision process framework that emerges for our concrete control problems. It seems practically impossible to apply their general convergence statements for deep Q-learning to our concrete setting such that one is forced to fall back on purely empirical tests of the algorithms. By way of contrast, our statistically driven method allows for a thorough theoretical analysis and yields rules that are both interpretable and explainable.

Regarding the practical implementation, we do not give a detailed numerical comparison here as this strongly depends on the exact framework, but just mention that in our scenarios both approaches learn the optimal rule reasonably well, where the statistical approach is (not surprisingly) faster and for a longer time horizon very accurate.

Acknowledgement

CS gratefully acknowledges financial support of Sapere Aude: DFF-Starting Grant 0165-00061B “Learning diffusion dynamics and strategies for optimal control”. LT was supported by Research Training Group “Statistical Modeling of Complex Systems” funded by the German Science Foundation.

Appendix A Supplementary material for Section 2.1

As announced in the main part, we will now describe the foundations of the statistical analysis of the -norm risk in the scalar diffusion setting in a more detailed manner. To be specific, consider a stationary diffusion on , with drift , Lipschitz continuous and differentiable diffusion coefficient such that for some , invariant density given in (2.2) and transition densities .

In the scalar framework, it is standard to exploit the properties of diffusion local time, and the proof of the tight variance bound in Theorem 2.1 (see (2.10)) actually relies on a corresponding result. However, this approach has the obvious drawback that it does not allow for a natural extension to higher dimensions. The following assumptions represent an alternative framework which can be adapted straightforwardly to dimension and, as will be demonstrated in the sequel, at the same time also yields optimal results in dimension .

-

(1)

For any compact set , there exists a non-negative, measurable function such that

(A.1) -

(2)

There exists a non-negative, measurable function such that, for any ,

For the sake of clarity, we restrict our presentation to the one-dimensional case as it is studied throughout the paper. As mentioned, the above framework and subsequent results admit straightforward extensions to higher dimensions. We refer to Section 2.1 in [18] for the precise definition of the assumptions in the general case.

Verifying A.1 and (2)

Let us emphasize that in the context of scalar diffusions, (2) is a rather mild condition, which can often be formulated as a heat kernel bound in the literature—that is, for some —under general conditions on the coefficients . E.g., classical results from PDE theory yield that if is bounded, transition densities for the semigroup of exist and fulfill

for some universal constants , implying the above form of with , see, e.g., equation (1.2) in [37]. In our framework, is potentially unbounded but satisfies the linear growth condition . Theorem 3.2 in [34] therefore yields that (2) is indeed satisfied in our setting. More precisely:

Lemma A.1.

There exists some constant such that, for any , we have

In particular, for any and , i.e., (2) holds.

We proceed by showing how to derive A.1 from exponential ergodicity of , which holds under the given coefficient assumptions as argued below. Before we start with the proof, let us briefly show that is a -process, i.e., that there exist a lower semicontinuous kernel and a sampling distribution on such that for the sampled kernel

This condition is quite general for specific models of ergodic Markov processes, see, e.g., the discussion in Appendix A.1 of [18]. In our model, has the -Feller property, see, e.g., [36, Theorem 19.9], and every point is reachable in finite time almost surely (cf. [26, Proposition 1.15]), i.e., for any initial distribution, , where . Hence, we can deduce from [44, Theorem 7.1] that, indeed, is a -process. Moreover, from almost sure reachability of any point, it is clear that is Harris recurrent wrt the Lebesgue measure , i.e., for any such that , we have for any , where

Proposition A.2.

is exponentially ergodic, i.e., there exist constants such that

| (A.2) |

where is a -function, which is equal to for Moreover, A.1 holds true with

Proof.

Denote by the extended generator of with domain , i.e., if there exists a measurable function such that the process

| (A.3) |

is a local martingale. By Itō’s formula, for any and

| (A.4) |

we have that satisfy (A.3). Hence, and we write for and given in (A.4). Let be a function as in the statement of the proposition. Using the definition of , it follows for that

Thus, satisfies the Lyapunov-type inequality

| (A.5) |

where . Since is trivially irreducible by ergodicity and also a -process, it follows that any compact set is petite by [44, Theorem 5.1] and, hence, is unbounded off petite sets (we refer to [20] for the latter two notions). Moreover, for any , the skeleton chain is irreducible. This follows from observing that, by the linear growth restriction on the drift , [34, Theorem 3.1] yields that, for any , has a Lebesgue density such that for any we have . Thus, is irreducible wrt to the Lebesgue measure. Existence of an irreducible skeleton chain and Harris recurrence give aperiodicity of as defined in [20] and, hence, we conclude from [20, Theorem 5.2] that (A.5) indeed implies exponential ergodicity in the sense of (A.2).

Let us now come to verifying A.1. Analogously to the proof of [16, Proposition 5.1], define, for ,

where and with is some bounded smoothing function fulfilling . Then, using , it holds that and hence . Plugging in, we obtain from (A.4) that

| (A.6) |

It follows that

| (A.7) |

Moreover, by the properties of , , and, since is invariant, we have

| (A.8) |

where the last equality is an immediate consequence of (A.6). Combining (A.2), (A.7) and (A.8), it therefore follows for any and ,

implying the assertion. ∎

Implications of A.1 and (2) on the statistical analysis

The above assumptions provide an alternative framework which is very well suited to deriving (optimal) bounds on the -norm risk of estimators. Inspection of the proof of Theorem 2.1 shows that it is based on three essential components, namely

-

(1)

the verification of the exponential -mixing property (as this allows to draw conclusions on the tail behaviour of the underlying process),

-

(2)

a tight upper bound for the variance of integral functionals (see (2.10)), and

-

(3)

upper bounds for the associated entropy integrals.

Point (1) is addressed by the following auxiliary result.

Lemma A.3 ([18], Proposition A.2).

If is an ergodic -process and there exist constants such that in (A.1) has the form , then is exponentially -mixing.

As a consequence, having already argued that is a -process, we obtain the exponential -mixing property from Proposition A.2.

Lemma A.4.

is exponentially -mixing.

We proceed by demonstrating how point (2) can be verified without resorting to the concept of diffusion local time and its specific properties. It was already mentioned in Section 1 that the -mixing property in dimension is not quite sufficient to guarantee variance bounds of the order stated in (2.10). Indeed, let be any ergodic scalar diffusion process with transition density and invariant measure , let be a bounded function with compact support of Lebesgue measure , and fix and . Referring to our application in Section 2, we require an upper bound of the form

| (A.9) |

Using the Markov property and invariance of , one obtains the representation

for

Standard heat kernel bounds of the form imply that

| (A.10) |

For bounding the second integral, the standard approach (which is known to provide tight variance bounds in dimension ) consists in exploiting mixing properties of . Hence, a natural idea is to work under the assumption that is exponentially -mixing and fulfills the mixing bound (1.1). This gives

| (A.11) |

Balancing the upper bounds (A.10) and (A.11) suggests to choose , resulting in the final estimate

This upper bound differs by a logarithmic factor from (A.9) and does not allow to prove the optimal convergence rate. By way of contrast, A.1 combined with the mild heat kernel estimates of the semigroup in (2)—which both hold in our setting by Lemma A.1 and Proposition A.2—yield results that are tight enough for proving the optimal upper bound on the convergence rate stated in Theorem 2.1.

Lemma A.5.

Fix some open and bounded set , and let be a Lipschitz-continuous kernel function with . Then, for any and , it holds

Proof.

A close inspection of the proof of Proposition 2.1 in [18] reveals that there exists some constant s.t., for any bounded with compact support satisfying and ,

Using that, for any , and the right hand side is a bounded domain, it follows that with being a constant independent of . Moreover, , giving the assertion. ∎

Note that Proposition A.2 (in combination with Lemma A.3) and Lemma A.5 address items (1) and (2), respectively, required for the analysis of the -norm risk. Finally, concerning point (3), the following lemma provides standard bounds on covering numbers on function classes related to kernel estimation procedures wrt the norms appearing in Proposition 1.1. By a slight abuse of notation, we do not distinguish notationally between the -norm on and the function space .

Lemma A.6 (Lemma C.1 in [18]).

Let be a bounded set, a Lipschitz-continuous function with Lipschitz constant , fix , and denote

If, for some ,

then there exist constants such that, for any and ,

Appendix B Proof of Lemma 2.6

Before we start with the proof, we need some preparatory remarks. The length of the first exploration period is given by

with , for and denoting the transition operators of the Markov process . We will need that . By the strong Markov property and the fact that by point recurrence of the ergodic diffusion , we obtain

and thus finiteness of the third moment of boils down to finiteness of the third moment of first hitting times of the diffusion. From [31, Section 5], see also [7], it is known that if the diffusion coefficient is bounded and there exist such that

| (B.1) |

then for all . In our setting, boundedness of is satisfied with , and we have

for some constants . Thus, for , (B.1) is fulfilled, which implies that for any and , . It is worth noting that [31] demonstrate how the existence of moments of hitting times is initimately connected to polynomial ergodicity of a diffusion and hence the existence of arbitrarily large hitting time moments can be regarded as a consequence of exponential ergodicity of under the given assumptions. In particular as desired.

We will also make use of the following simple observation.

Lemma B.1.

Let be a random variable taking values in almost surely and suppose that

is differentiable with Then, the function

is increasing.

Proof.

By the smoothness assumptions, we have

with . Since is increasing, it follows that , proving the assertion. ∎

We are now ready to carry out the proof of Lemma 2.6.

Proof of Lemma 2.6.

We start with some necessary notation. Let , , be the length of the -th exploration period for and the length of the -th exploitation period for . In particular, and is an i.i.d. family of random variables under . Define also as the length of the first exploration/exploitation periods, thus

where . Finally, denote and the number of exploration/exploitation periods starting before time , , where

Clearly, for any , and thus

By construction and the strong law of large numbers, both the left-hand and the right-hand side -a.s. converge to and hence

| (B.2) |

Let now be such that

where denotes stochastic ordering. Existence of such random variables is clear in case , and for we can take to be a cycle length when reflecting in and be a cycle length when reflecting in . Choosing and we have

Let now and be i.i.d. copies of and , resp., where by resorting to a coupling argument if needed, we may assume wlog that , -a.s. for all , (see, e.g., [43, Section 3]). Defining

it follows that

With the standard renewal theorem we have

By construction, we have

Since, by Jensen’s inequality and the above,

it follows that

which establishes the second part of the assertion. For the first part, consider the uncontrolled diffusion process and let

where

By the strong Markov property, are i.i.d. and if we denote for , then is a renewal process with increment distribution . Furthermore, we define in analogy to the controlled case above for , where and , and for . Finally, let for . Clearly,

for any , which yields

| (B.3) |

where

| (B.4) |

By the standard renewal theorem and the properties of we have

which, on account of the fact that by combining the strong law of large numbers and (B.4) we have

shows that

Consequently, an application of Fatou’s lemma provides

Thus, choosing , there exists such that for any large enough we have

which, together with Markov’s inequality and (B.3), yields

Thus, to show that it is enough to establish that

| (B.5) |

To this end, note first that for any and we have

By construction, , where

is the -algebra generated by the lengths of the first “exploration/exploitation” periods up to the -th “exploration” period of the uncontrolled process . Clearly, for any and , which shows that is a stopping time. Hence, we can use Wald’s second moment identity, see [5, Propostion A10.2], to obtain

Since by Jensen’s inequality and the renewal theorem

(B.5) will follow if we can prove that . By classical renewal arguments, cf. [5, Proposition 6.3], we have

| (B.6) |

and by construction it follows that

By Jensen’s inequality, we have , and (B.6) combined with Lemma B.1 yields (note here that for and thus we may differentiate under the integral to obtain as needed). Thus, , which shows that indeed . ∎

Appendix C A brief summary of Lévy processes and their overshoots

This section is devoted to giving a (very) brief summary of Lévy processes and their overshoots in order to keep the article reasonably self-contained. Talking about overshoots quite naturally guides us into fluctuation theory of Lévy processes, which is based on a rigorous treatment of excursions of Lévy processes from its maximum and minimum. For an extensive textbook treatment of fluctuation theory, we refer to [27] with basic properties of overshoots being discussed in Chapter 5. A general account on Lévy processes is given in the monographs [8] and [35].

We consider a Lévy process with underlying natural filtration augmented in the usual way, which is equipped with a family of probability measures such that is a Markov process. Thus, has càdlàg paths, almost surely starts in under , has stationary and independent increments under and its semigroup is given by

From the last equality, it follows that is spatially homogeneous, i.e. and one easily derives that is a Feller process, that is, if we denote by the space of continuous functions vanishing at infinity, it holds that for any and moreover strongly as .

While the Fellerian nature of Lévy processes is still fairly general from a Markovian perspective, it is the spatial homogeneity which gives rise to a quite unique and powerful theory. The fundamental starting point to the analysis of Lévy processes is the Lévy–Khintchine formula, which identifies the characteristic function of the marginals of the process and hence uniquely describes the complete process in terms of a characteristic triplet , where , and is a measure on (called Lévy measure) having no atom at and being such that . The Lévy–Khintchine formula then states that , , , with the characteristic exponent satisfying

On the level of processes, the Lévy–Khintchine representation can be translated into a partition of the process into a linear Brownian motion and an independent pure jump process characterized by , which itself decomposes into an independent compound Poisson process and a zero mean -martingale with infinitely many jumps bounded by on any finite time interval. If , it follows from the Lévy–Khintchine representation that the first moment of is finite for any and with

determining the long-time behaviour of in the sense that

-

(i)

, -a.s.;

-

(ii)

, -a.s.;

-

(iii)

, -a.s..

and

With this basic preparation on the characteristics of Lévy processes, let us now come to their fluctuation theory, with a certain emphasis on the so called Wiener–Hopf factorization. This commands a discussion of the ascending ladder height process, which dominates our analysis of data-driven solutions to impulse control problems associated to Lévy processes. This process is derived from the local time at the supremum , which is a stochastic process measuring the time that spends at its running supremum , . Its construction is based on the observation that , which can be interpreted as the process obtained from reflecting at its supremum, is a strong Markov process and hence one can define as the local time at for , which means that is an additive functional of which almost surely increases on the closure of . In case that is upward regular, i.e., for we have , can be constructed as a process with almost surely continuous paths, which entails that its right-continuous inverse , , is almost surely strictly increasing. In this case, the ascending ladder height process , defined by

is a killed subordinator, strictly increasing up to its lifetime , i.e., is equal in law to a strictly increasing Lévy process, which is sent to the cemetery state after an independent exponentially distributed random time with expectation . If , which as seen before is guaranteed if and , it follows that almost surely and hence is unkilled. Moreover, when , which is the setting that we will be working with in this paper, it holds that as well, which can be deduced from (C.2) below. It is important to note that is only characterized uniquely up to a multiplicative constant and hence the definition of depends on the chosen scaling of local time. For our purposes, it will be convenient to choose a scaling of local time such that and hence, by Wald’s equality, .

When upward regularity does not hold, will not be strictly increasing and consequently, the ascending ladder height process is a (possibly killed) compound Poisson subordinator. In any scenario, the Laplace exponent , given by

satisfies and we refer to as the drift and as the Lévy measure of .

In the same vein, we can construct the ascending ladder height process for the dual Lévy process , which corresponds to time changing by the right continuous inverse of local time at the infimum of . Therefore, is referred to as the descending ladder height process. If we denote by the Laplace exponent of , then the Wiener–Hopf factorization tells us that is fully characterized by means of the ascending and descending ladder height processes since the Lévy–Khintchine exponent of can be expressed as a factorization of the Laplace exponents of and ,

| (C.1) |

where the constant depends on the scaling of local time at the supremum and infimum. Among others, this factorization allows to express the characteristics of in terms of the characteristics of and . A particularly useful identity for understanding the ascending ladder height Lévy measure, usually referred to as Vigon’s équation amicale inversé, was demonstrated in [45]:

| (C.2) |

Here, , , denotes the potential measure of and without loss of generality, the constant in (C.1) is set to unity.

While the theoretical solution strategy of the Lévy driven impulse control problem is driven by the generator functional with denoting the generator of the ascending ladder height process , our data-driven strategy makes use of the link between and overshoots of to find an estimator , from which the optimal reflection boundary is approximated by the greedy strategy (3.16). Let us first discuss classical properties of overshoots and then make the transition to the approach undertaken in [19], whose results are fundamental for the approximation properties of our statistical procedure.

Let be a given level and consider the overshoot over , given by