disposition

Backtesting Systemic Risk Forecasts using Multi-Objective Elicitability111We are grateful to Immanuel Bomze for suggesting to consider multivariate scoring functions equipped with general orders. Furthermore, we would like to thank Timo Dimitriadis, Rüdiger Frey, Christoph Hanck, Jana Hlavinová, Kurt Hornik, Marc-Oliver Pohle, Birgit Rudloff and Johanna F. Ziegel for detailed comments and valuable discussions. Of course, all errors and and opinions expressed in this article are solely the authors’ responsibility. Yannick Hoga gratefully acknowledges support of the German Research Foundation (DFG) through grant HO 6305/2-1.

Abstract

Systemic risk measures such as CoVaR, CoES and MES are widely-used in finance, macroeconomics and by regulatory bodies. Despite their importance, we show that they fail to be elicitable and identifiable. This renders forecast comparison and validation, commonly summarised as ‘backtesting’, impossible.

The novel notion of multi-objective elicitability solves this problem. Specifically, we propose Diebold–Mariano type tests utilising two-dimensional scores equipped with the lexicographic order.

We illustrate the test decisions by an easy-to-apply traffic-light approach. We apply our traffic-light approach to DAX 30 and S&P 500 returns, and infer some recommendations for regulators.

Keywords: Backtest; (Conditional) Elicitability; Forecasting; Identifiability;

Lexicographic Order; Multi-objective Optimisation; Systemic Risk

JEL classification: C18 (Methodological Issues), C52 (Model Evaluation, Validation, and Selection), C58 (Financial Econometrics)

1 Motivation

Regulating financial institutions in isolation is often not sufficient to prevent financial crises due to the interdependent risks these institutions face. In particular, their losses commonly exhibit a pronounced comonotonic behaviour in the extreme tails: When one financial institution, or the market as a whole, is in distress, other institutions are much more prone to being at risk as well. The U.S. subprime mortgage crisis of 2008–2009, the European sovereign debt crisis of 2010–2011 and the Covid-19 crash of 2020 have forcefully demonstrated this fact and also the need to assess the systemic nature of risk. As a consequence of these crises, a huge literature on measuring systemic risk has emerged over the last decade (GK11; ChenIyengarMoallemi2013; AB16; Aea17; BE17; FeinsteinRudloffWeber2017).

Systemic risk measures are important in various contexts. First, they are important in banking regulation under the Basel framework of the BCBSBF19, where they are vital in determining which banks are among the globally systemically important banks (G-SIBs). Such G-SIBs are then subjected to higher capital requirements. Second, in finance, systemic risk measures may be used to study spillover effects in the financial system (AB16) or the build-up of asset price bubbles (BRS20). Third, they may be used to study the linkage between the financial sector and the real economy. Among others, GKP16 and BE17 show that an increase in systemic risk is predictive of future declines in real economic activity. All these examples underscore the importance of accurately measuring and predicting systemic risk.

In this paper, we revisit three influential systemic risk measures. First, we consider AB16’s (AB16) conditional value-at-risk (CoVaR) and conditional expected shortfall (CoES) as extensions of the well-known value-at-risk (VaR) and expected shortfall (ES) to the realm of systemic risk. If are the losses of interest and the losses of a reference position, () is the VaR (ES) of at level , given that is “in distress”. Here, we interpret the event that is in distress as being larger or equal than its -quantile, i.e., . Finally, we consider Aea17’s (Aea17) marginal expected shortfall, , as the conditional mean of given . Section 2 introduces the exact definitions.

Bea17 distinguish between the “source-specific approach” and the “global approach” to systemic risk measurement. The source-specific approach considers individual sources of systemic risk, such as contagion risk or liquidity crises. In contrast, global measures of systemic risk potentially incorporate all mechanisms studied in the source-specific approach. Bea17 categorize CoVaR, CoES and MES under the global approach.

In practice, forecasting systemic risk measures—such as CoVaR, CoES and MES—requires adequate models for the marginals and , and for their dependence structure. The literature has developed numerous different modelling approaches for this; see GT13 and BC19 for forecasting models for CoVaR and CoES, and BE17 and Eck18 for MES models. Due to the importance of systemic risk measures outlined above, it is vital to develop statistical quality assessments of the various models’ predictive performances. It is the main aim of this paper to provide such tools, which are referred to as ‘backtests’ in finance.

Backtests have two main goals. On the one hand, one may wish to assess the absolute quality of forecasting models, also called the calibration, akin to model validation in statistics. Following the terminology of FZG16, we call such procedures “traditional backtests”. Roughly speaking, they check how well a sequence of risk measure forecasts aligns with corresponding observations of losses. Traditional backtests rely on the identifiability of the underlying risk measure, which ensures the existence of a (possible multivariate) function that uniquely “identifies” the true report (see Definition 3.2). On the other hand, the presence of several alternative prediction models for a risk measure necessitates “comparative backtests” (FZG16) to assess their predictive accuracy relative to each other. This is akin to statistical model selection procedures. Comparative backtests exploit the elicitability of the underlying risk measure. This implies the existence of a real-valued loss (or also: scoring) function , which is minimised in expectation by the optimal forecast (see Definition 3.1).

Our contributions in this paper are the following: First, we show that , and are not identifiable and elicitable as standalone risk measures (Proposition 4.1). The practical implication of this is that neither traditional nor comparative backtests can be carried out. In particular, any regulation based solely on these systemic risk measures is pointless, because neither the adequacy of the forecasts can be determined nor can different systemic risk forecasts be sensibly compared (say to a regulatory standard model).

We provide a partial remedy for this drawback by giving joint identification functions for , , and (Theorem 4.2). These identification functions can be used for (conditional) calibration tests in the spirit of NZ17. To the best of our knowledge, this entails the first traditional backtest for these systemic risk measures apart from Banulescu-RaduETAL2019. We contrast our approach with theirs in detail in Remark 4.3. In particular, they use one-dimensional identification functions for and , which fail to be strict in contrast to our two-dimensional identification functions. For the backtest of Banulescu-RaduETAL2019, this non-strictness leads to a complete loss of power in identifying certain misspecified systemic risk forecasts (Section G in the Supplement). Theoretically, our results are akin to the fact that is not identifiable on its own, but the pair is identifiable (FZ16a).

In stark contrast to the joint elicitability of the pair , however, we show that the pairs , and the triplet fail to be elicitable (Section D). So while traditional backtests for the above pairs and the triplet may be constructed by virtue of their identifiability, classical comparative backtests exploiting elicitability are not feasible.

As a remedy to this negative result, we propose the novel concept of multi-objective elicitability, which works with multivariate scores mapping to equipped with a certain (partial) order relation . This contrasts sharply with classical -valued losses . Their prevalence to date is grounded in tradition (Gne11) and the fact that is equipped with the canonical (total) order relation , which allows for straightforward comparisons of losses. Subsection 3.2 introduces multi-objective scores and the corresponding concepts of multi-objective consistency and elicitability. The terminology stems from the field of multi-objective optimisation: According to Ehrgott2005 it is “a mathematical theory of optimization under multiple objectives”, and can be encountered in various fields of science, economics, logistics and engineering. Since this novel concept to forecast evaluation may open up the avenue to a whole field of applications and research (which is underpinned by further instances; see Example B.1), we give a concise general outline of the theory, using partial orders on or even infinite-dimensional real vector spaces.

For the systemic risk forecasts we consider here, scores mapping to equipped with the lexicographic (total) order—described in Subsection 3.3—are sufficient. In particular, the performance of different systemic risk forecasts must be ranked with regard to the lexicographic order. Specifically, Theorem 4.4 shows that , and are multi-objective elicitable, and it provides classes of strictly multi-objective consistent scores. We outline in Section 5 how these scores can be used for comparative backtests of Diebold–Mariano type. These comparative backtests are different from—in our case infeasible—“standard” comparative backtests in that they build on the newly introduced notion of multi-objective elicitability (with scores mapping to equipped with the lexicographic order) instead of the “standard” notion of elicitability (with scores mapping to equipped with the canonical order ). In particular, some systemic risk forecast is now preferable to some other forecast when the -valued score of the former is smaller (with regard to the lexicographic order) than that of the latter. Thus, financial institutions may build on this result to improve their prediction models for , and , which is crucial for an adequate assessment of the diverse risks faced by these institutions.

Since the multi-objective scores of Theorem 4.4 take values in equipped with the lexicographic order, some particularities arise for statistical hypothesis tests. While simple “two-sided” null hypotheses of equal predictive performance can be tested with a classical Wald-test, particular caution must be taken when testing for superior predictive ability. Due to the particularities of the lexicographic order, a straightforward “one-sided” composite null hypothesis would be insensitive to the systemic risk measure forecast, ignoring the primary goal of the backtesting procedure. Therefore, we suggest to use “one and a half”-sided composite null hypotheses, testing for superior predictive ability in the systemic risk component and equal performance in the auxiliary component. Section 5 provides details, including an adaptation of the Basel framework’s traffic-light approach to systemic risk backtests.

An empirical application in Section 6 demonstrates the viability of the comparative backtest. There, we consider daily log-losses of the DAX 30 with daily log-losses of the S&P 500 as a reference quantity. We compare systemic risk forecasts derived from a benchmark Gaussian copula model with those produced by a -copula model, where in both models the correlation parameter of the copula is driven by generalised autoregressive score (GAS) dynamics (CKL13). We find that the predictive performance of the -copula is superior with -values close to , which is consistent with its popularity in empirical work. One conclusion from our empirical analysis is that fairly long samples are required to validly distinguish between different forecasts, because the effective sample sizes in comparing systemic risk forecasts are (almost by definition) reduced. Thus, the one year evaluation period for (univariate) VaR and ES forecasts in the Basel framework of the BCBSBF19 is, in our view, insufficient for systemic risk forecasts.

The paper closes with a discussion and outlook (Section 7). Besides the parts already mentioned above, the Supplement provides proofs for the results of Section 3 (Section A) and further background material on multi-objective elicitability (Section B). All other proofs are relegated to Section E. Section F investigates the finite-sample properties of our comparative backtests in simulations. The R code to reproduce all numerical experiments is available online.

Throughout the paper, we indicate vectors with bold letters. We highlight the distinction between row and column vectors only when it is essential, and use the symbol ′ to indicate the transpose of a vector or matrix.

2 Formal definition of CoVaR, CoES and MES

Fix some non-atomic probability space where all random objects are defined. Using standard notation, let , , be the space of all -valued random vectors on . Furthermore, for , let be the collection of random vectors whose components possess a finite th moment. For let be its joint distribution. Then define for the collection . We overload notation and identify any with its cumulative distribution function (cdf) .

Our systemic risk measures of interest—, and —are maps from (or for MES) to . They are law-determined, meaning that their values for and coincide if . Hence, we can consider them as risk-functionals on (or ). Similarly, the popular univariate risk measure , , is a law-determined map . In the rest of the paper, we will frequently overload notation and identify these law-determined risk measures with their induced risk functionals. As such, we will use the terms ‘risk measure’ and ‘risk functional’ interchangeably.

Let be a two-dimensional random vector. Here, stands for the losses of a position of interest (with the sign convention that positive values are losses and negative values are gains) and is a univariate reference position or aggregate of a reference system, having the same sign convention. Denote by their joint distribution function and by and their marginals, respectively. Recall that for the -quantile of is the closed interval , where . Then, is the lower -quantile of , i.e., . For , is always finite. Our sign convention is such that the larger the risk measure of a position, the riskier it is deemed. Hence, we typically choose a probability level of close to 1 for , such as or .

AB16 define as the -quantile of the conditional distribution function . The conditioning event in this definition is problematic for several reasons. First, it may have probability zero (which is the case when is continuous). Second, it does not fully capture the tail-risk of . Third, since the roles of and are asymmetric by construction, one may want to consider different probability levels to specify the event of ‘being in distress’. Thus, we follow GT13 and Banulescu-RaduETAL2019 in redefining for , as

| (2.1) |

where . For , we simply have , and if we simply write .

Since is merely a quantile of the distribution , it inherits the same defects as . That is, it ignores tail risks beyond the quantile level and it fails to be coherent, particularly defying the rationale of advantageous diversification effects (Aea99; MS14). The well-known Expected Shortfall at level , , does not suffer from these defects. This motivates AB16 to introduce the conditional Expected Shortfall (CoES). As for , we modify the conditioning event and formally introduce for , , via

| (2.2) |

If is continuous, then . Again, , and we write .

Finally, we consider the marginal Expected Shortfall (MES) of Aea17, which measures the expectation of when is in distress, i.e., when is in its right tail. Specifically, we introduce for the map ,

| (2.3) |

Again, , and if is continuous. If is discontinuous, Remark C.1 proposes a novel correction term which generalises the three measures considered in this paper.

3 (Conditional) identifiability and multi-objective elicitability

We present the theory in this section in all generality to serve as a basis for future research on multi-objective scores. Therefore, we work with general functionals which do not necessarily have the interpretation of risk functionals. All proofs are in Section A.

3.1 Notation, basic definitions and results

Adopting the decision-theoretic terminology of Gne11, we denote by an action domain. This is the space of plausible forecasts, which can be finite for categorial forecasts, or for point forecasts, or a set of distributions for probabilistic forecasts. Moreover, let be an observation domain—a set where verifying observations materialise—with as a leading example. Denote by the set of all probability distributions on . Let be subclasses of . We consider a general, possibly set-valued functional with the power set of . Later on, will have the interpretation of a risk functional. Note that is the class of distributions, where our functional is defined on, and is the subclass on which will be identifiable/elicitable (see Definitions 3.1 and 3.2). For instance, for , we have and is given in Theorem 4.2 (i)/Theorem 4.4 (ii).

We adopt the selective notion of forecasts discussed in FFHR2021 where one is content with correctly specifying a single element as opposed to specifying the entire set . (If one is interested in exhaustive forecasts—i.e., in forecasts for the whole set —one can change the action domain to .) If attains singletons only, we identify the value of with its unique element. This identification allows us to treat point-valued functionals as set-valued functionals without loss of generality. We mention that the risk functionals to be considered in Section 4 are all point-valued.

A function , where is an index set, is called -integrable if for all components , , it holds that for all , . If is -integrable, we define the map , for , . A similar convention and notation is used for maps . We start with the classical definition of elicitability and consistent scoring functions, mapping to .

Definition 3.1.

An -integrable map is an -consistent scoring function for if for all , all and for all . It is a strictly -consistent scoring function for if, additionally, implies that . is elicitable on if there is a strictly -consistent scoring function for .

Definition 3.2.

An -integrable map is an -identification function for if for all and for all . It is a strict -identification function for if, additionally, for all and for all , implies that . is identifiable on if there is a strict -identification function for .

Suppose in a risk management context that corresponds to the -functional and are the observed losses. Subject to mild conditions on , is elicitable, where the ‘pinball loss’ is strictly -consistent. This allows to compare competing VaR forecasts and via their empirical average score differences . A negative (positive) sign of indicates superiority (inferiority) of over . Identifiability, on the other hand, opens the way to test for calibration by checking, e.g., if the test statistic is sufficiently close to or not. E.g., when corresponds to checking calibration amounts to checking if the empirical VaR-violation rate is roughly , which can be done in terms of . These examples demonstrate the importance of elicitability and identifiability for comparing and evaluating (risk) forecasts in practice.

Under regularity conditions, the notions of elicitability and identifiability are equivalent for point-valued functionals mapping to (SteinwartPasinETAL2014). There are also important functionals which fail to be elicitable and identifiable, most prominently the variance and expected shortfall (Gne11). In such situations, the notions of conditional elicitability and conditional identifiability can be helpful. Following the concept presented in FZ16a, we slightly adapt EKT15’s (EKT15) original definition of conditional elicitability. We also introduce the corresponding counterpart of conditional identifiability.

Definition 3.3.

Consider two functionals , , and let .

-

(i)

is conditionally elicitable with on , if is elicitable on and is elicitable on for any .

-

(ii)

is conditionally identifiable with on , if is identifiable on and is identifiable on for any .

It is easy to see that the variance is conditionally elicitable and conditionally identifiable with the mean, and that is conditionally elicitable and conditionally identifiable with on appropriate classes of distributions, respectively (EKT15). The pairs (mean, variance) and even turn out to be elicitable and identifiable (FZ16a). For identifiability, this is an instance of the following proposition, which is already stated without a proof in the discussion of FZ16a.

Proposition 3.4.

If is conditionally identifiable with on , then the pair is identifiable on .

Of course, an analogue to Proposition 3.4 for (conditional) elicitability would be desirable, and it has been stated as an open problem in the discussion of FZ16a. Unfortunately, the answer is negative: While Section C establishes the conditional elicitability of , and all with , the corresponding pairs and the triplet generally fail to be elicitable; see Section D.

3.2 Multi-objective scores, consistency and elicitability

To overcome the structural drawback of elicitability in comparison to identifiability, in particular the lack of an analogue to Proposition 3.4, we introduce the novel notion of multi-objective scoring functions and the corresponding concepts of multi-objective consistency and multi-objective elicitability. It is inspired by the fundamental observation that identification functions are generally multivariate.

To be more precise, the dimension of the identification function usually coincides with the dimension of the functional. If an identification function is often induced by the derivative of a consistent scoring function . Also, the antiderivative of an (oriented) identification function yields a consistent score, thus roughly establishing a one-to-one correspondence between the class of identification functions and the class of consistent scoring functions. For a -dimensional functional, the gradient of a consistent score is -valued and naturally induces an identification function, subject to smoothness conditions. However, not every -dimensional identification function possesses an antiderivative for . This is due to integrability conditions asserting that if it was integrable, the corresponding Hessian of the stipulated antiderivative would need to be symmetric (see also Example D.1 for an illustration). This rules out the one-to-one relation in the multivariate setting, giving rise to a gap between the class of consistent scoring functions and the one of identification functions. This gap and its consequences on estimation are discussed in detail by DFZ2020.

We sidestep this integrability constraint by introducing the concept of multivariate scoring functions. Indeed, it is this multivariate structure of identification functions which facilitates the straightforward proof of Proposition 3.4. Therefore, we mimic this multi-dimensionality for scores, letting them map to , where usually , or even more generally to some real vector space , where the index set may be finite, countable or even uncountable. In the application of the general theory developed here to the systemic risk measures, it suffices to consider -valued scores; see Theorem 4.4 in Section 4. The motivation for defining a classical score as a univariate map to (see Definition 3.1) is grounded in tradition on the one hand. On the other hand, is equipped with the canonical (total) order relation , which allows for straightforward comparisons of forecasts by checking whether the empirical average score differences satisfy or . Consistency in Definition 3.1 ultimately relies on the existence of an order.

Hence, we need to equip with a vector partial order and write . A binary relation on is a partial order if it is reflexive (, ), antisymmetric ( if and , then ), transitive ( if and , then ). Two elements are comparable if or . A total order is a partial order where all elements are comparable. A partial order on induces a strict partial order on as follows. For all it holds that if and only if and . A partial order on is a vector partial order if it is compatible with addition and positive scaling. That is, if for all and for all it holds that implies that , and implies that . (In the sequel, we always mean a vector partial order whenever we write “partial order”.) The canonical choice is the componentwise order defined for as if and only if for all . The use of a partial order on leads to two different generalisations of Definition 3.1. These are due to the fact that in a partial order implies that , but the reverse implication fails if and are not comparable.

Definition 3.5.

-

(i)

An -integrable map is a strongly multi-objective -consistent scoring function for if for all , all and all . It is a strictly strongly multi-objective -consistent scoring function for if, additionally, implies that . is strongly multi-objective-elicitable on (with respect to the order on ) if there is a strictly strongly multi-objective -consistent scoring function for .

-

(ii)

An -integrable map is a weakly multi-objective -consistent scoring function for if for all , all and all . It is a strictly weakly multi-objective -consistent scoring function for if, additionally, for all and for any it holds that if for all , then . is weakly multi-objective-elicitable on (with respect to the order on ) if there is a strictly weakly multi-objective -consistent scoring function for .

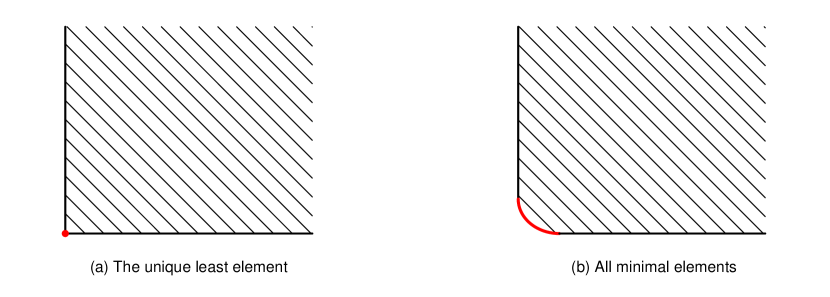

As discussed, a partial order on is sufficient to define multi-objective consistency. Using the notation for and , the definition of multi-objective consistency does not require comparability of all elements for some fixed . Weak multi-objective consistency solely implies that all elements of are minimal in . The strict version additionally ensures that all minimal elements of are in . Strong multi-objective consistency additionally means that the elements of are not only minimal in , but that they are the (unique) least element of . Due to the uniqueness of a least element, is a singleton. The strict version of strong multi-objective consistency additionally means that . See Figure 1 for an illustration of the two situations. Clearly, (strict) strong consistency implies (strict) weak consistency. If we omit the qualifiers “weak” or “strong”, we refer to the strong version.

Multi-objective consistency translates the essence of consistency as a ‘truth serum’, or being incentive compatible, to the multivariate realm. No matter what forecast an agent issues, they would be better off (or at least not worse off) in expectation when issuing a correctly specified functional value . (In the weak version, if an agent issued some , they would not be better off with some other forecast.) Strictness means that any action leads to a worse outcome in expectation than the truth . So this minimal requirement of honouring truthful forecasts is preserved.

Remark 3.6.

To the best of our knowledge, the notion of multi-objective scoring functions with the related concepts is novel to the forecast evaluation literature. However, it has some connections to the concept of forecast dominance introduced by EhmETAL2016. Let be some class of univariate (strictly) -consistent scoring functions for some functional . Adapting their definition slightly, we say that a forecast dominates relative to if for all and for all . In our terminology, we could phrase this forecast ranking in terms of a multivariate score , , where is the usual componentwise partial order. By virtue of mixture representations, EhmETAL2016 impressively demonstrate that for quantiles and expectiles, one can rephrase forecast dominance with respect to (nearly) all consistent scoring functions equivalently in terms of extremal or elementary scores . For this situation, we can easily construct a multi-objective score , mapping to the function space equipped with the componentwise order. EhmETAL2016 provide numerous instances of comparable and incomparable forecast rankings. This example provides an easy construction for a (strictly) multi-objective -consistent score, , if is elicitable.

For verifying observations , our Definition 3.5 suggests to compare two sequences of forecasts () via their average scores and . However, while using classical univariate scores always leads to a conclusive forecast ranking (ignoring questions of statistical significance for a moment), the presence of a partial order may lead to inconclusive rankings, particularly if neither of the two forecasts is correctly specified. For instance, if and (e.g., for the bivariate systemic risk scores of Theorem 4.4), then neither nor in the componentwise order on .

3.3 Multi-objective elicitability with respect to the lexicographic order

and conditional elicitability

To overcome the issue of inconclusive forecast rankings, we equip with a total order. In a total order, all elements are comparable. Hence, the notions of weak and strong multi-objective consistency / elicitability coincide and a distinction is redundant. A promising choice is the lexicographic order. For our purposes, and to ease the exposition, it suffices to consider equipped with the lexicographic order . On it holds that if or if ( and ). The lexicographic order is widely used for preference relations in microeconomics. In particular, it is well-known for the fact that it cannot be represented by a real-valued utility function (MWG1995, Chapter 3.C).

There are at least two reasons for our choice of the lexicographic order. First, as a total order, it allows for conclusive forecast rankings, which we exploit in our comparative backtests in Section 5. For instance, if as above and for the systemic risk scores, then the inconclusive ranking is resolved because . Second, the lexicographic order opens the way to the following analogue of Proposition 3.4.

Theorem 3.7.

If is conditionally elicitable with on and is a singleton for all , then the pair is multi-objective elicitable on with respect to the lexicographic order on .

Theorem 3.7 is almost a direct analogue of Proposition 3.4, with the intriguing exception that is assumed to be a singleton on in Theorem 3.7; see Remark A.1 for further details. We illustrate how the construction of Theorem 3.7 leads to strictly consistent multi-objective scores mapping to for the cases of (mean, variance) and in Subsection B.1. There, we also provide further examples of conditionally elicitable functionals failing to be elicitable in the traditional sense, but which are multi-objective elicitable with respect to . Section B.2 elaborates on how the multi-objective scores can be considered a “generalised antiderivative” of a -dimensional identification function with relaxed symmetry conditions. Section B.3 provides further details on comparing misspecified forecasts under multi-objective elicitability, and on the sensitivity of multi-objective scores with respect to increasing information sets. Finally, Section B.4 revisits a powerful necessary condition for identifiability and elicitability, namely the Convex Level Sets (CxLS) property, for multi-objective scores.

The proof of Theorem 3.7 explicitly exploits the asymmetric structure of the lexicographic order which fits well with the asymmetric notion of conditional elicitability, where the roles of and may not be changed. In particular, in the setup of Theorem 3.7, the pair is generally not multi-objective elicitable on with respect to the lexicographic order on . More generally, we suspect that under the conditions of Theorem 3.7 the lexicographic order is the only order on which renders multi-objective elicitable.

4 Structural results for CoVaR, CoES and MES

4.1 CoVaR, CoES and MES fail to be identifiable or elicitable

The following proposition shows that the three risk measures , and generally fail to be identifiable or elicitable on sufficiently rich classes of bivariate distributions . It is proven by showing that the CxLS property (which remains necessary for multi-objective scores; see Proposition B.4) is violated in each case.

Proposition 4.1.

For , , and are neither identifiable nor elicitable on any class containing all bivariate normal distributions along with their mixtures.

Proposition 4.1 casts doubt on traditional and comparative backtesting approaches for CoVaR, CoES and MES as standalone systemic risk measures. Thus, these measures should not be used for regulatory purposes on their own, because forecasts for them can neither be verified for their adequacy nor can they be sensibly compared to improve their modeling.

4.2 Joint identifiability results

Section C establishes the conditional identifiability and conditional elicitability of , , and with , respectively. This, in combination with Proposition 3.4, immediately yields the following joint identifiability results, where for and we use the notation

| (4.1) | ||||

Theorem 4.2.

Let . Consider the strict -identification function for , , .

-

(i)

On , the pair is identifiable with a strict identification function ,

(4.2) -

(ii)

On , the triplet is identifiable with a strict identification function ,

(4.3) -

(iii)

On , the pair is identifiable with a strict identification function ,

(4.4)

Following NZ17, Theorem 4.2 can readily be used to assess the absolute forecast quality via joint (Wald-type) calibration tests. These either test the null hypothesis of unconditional calibration, for all , or the more informative null of conditional calibration, for all . Here, the -algebra represents the information available to the forecaster at time . Recall that the null of conditional calibration is equivalent to for all -measurable random vectors for all . Unless is particularly simple, this approach is statistically not feasible, because a finite selection of -measurable random vectors is required in practice. Note that using only a finite collection amounts to testing a broader null than the original one of conditional calibration.

Remark 4.3.

It is worth pointing out the improvements upon the substantial work of Banulescu-RaduETAL2019, who develop—inter alia—traditional backtests of systemic risk measures. Translating their notation into ours, they propose in their equation (4) a one-dimensional identification function for the pair of the form ,

| (4.5) |

Banulescu-RaduETAL2019 point out that this an identification function since However, it fails to be strict, since, so long as , we have . Thus, the specific null of ‘correct’ unconditional calibration with from (4.5) is too broad, since it is satisfied for all with . This implies only trivial power against such alternatives for the corresponding Wald-test for calibration. This is in stark contrast to the Wald-test employing our two-dimensional identification function in (4.2), where if and only if . We refer to Section G for a simulation study illustrating the possible detrimental effects of the non-strictness of (4.5). We stress that the non-strictness is not only problematic in the uncountably many cases where , but in all cases where VaR is overpredicted and CoVaR underpredicted or the other way around. This is because by overpredicting (underpredicting) VaR and underpredicting (overpredicting) CoVaR, the different biases cancel out in the one-dimensional identification function in (4.5), thus leading to a loss of power in identifying misspecified forecasts; see Figure 9. Intuitively speaking, two moment conditions via a two-dimensional identification function are necessary to uniquely identify the two-dimensional pair . This is in line with other two-dimensional strict identification functions for two-dimensional functionals in the literature, e.g. for Value at Risk and Expected Shortfall, see FZ16a; NZ17.

4.3 Multi-objective elicitability results

Recall that , and are all elicitable. Surprisingly, their conditional counterparts , and fail to be elicitable despite being identifiable (Section D). This is due to integrability conditions, causing an extreme gap between the class of strict identification functions and the class of strictly consistent scoring functions, which turns out to be empty. Thus, comparative backtests cannot be implemented using a scalar strictly consistent scoring function. Furthermore, the conditional elicitability results of Section C can hardly be used for forecast comparisons, unless the forecasts are the same and correctly specified. However, the conditional elicitability in combination with Theorem 3.7 immediately yields the following novel joint multi-objective elicitability results with respect to the lexicographic order on . These results can readily be used for comparing systemic risk forecasts as detailed in Section 5. We again use the notation introduced in (4.1).

Theorem 4.4.

Let .

-

(i)

On , the score ,

(4.6) is strictly -consistent for , if is strictly increasing and for all , the function is -integrable.

-

(ii)

On , the pair is multi-objective elicitable with respect to . A strictly -consistent multi-objective scoring function is given by

(4.7) where is strictly increasing and is -integrable for all .

-

(iii)

On , the triplet is multi-objective elicitable with respect to . A strictly -consistent multi-objective scoring function is given by

(4.8) where is increasing, is strictly convex with subgradient , and is -integrable for all .

-

(iv)

On , the pair is multi-objective elicitable with respect to . A strictly -consistent multi-objective scoring function is given by

(4.9) where is strictly convex with subgradient and is -integrable for all .

The choice of the functions in Theorem 4.4 is inessential. It may only influence the integrability of the scoring functions on the one hand and it can control the sign of the scores on the other hand. For the remaining functions in Theorem 4.4, one could choose the standard choices, e.g., the identity for and in (4.6), (4.7) and (4.8), giving rise to the common ‘pinball loss’, or in (4.9) leading to the square loss. For further possible choices, especially for in (4.8), we refer to Subsection F.3.

Table 1 summarises the results of Section 4. For purposes of comparison, the final three rows display the properties of and . The multi-objective elicitability of the pair follows from Example B.1. Table 1 highlights the structural difference between , , on the one hand and their conditional counterparts , , and on the other hand. While elicitability in the usual sense holds for the former, it fails for the latter. This highlights the importance of the newly introduced concept of multi-objective elicitability, which allows for comparative backtests. Section 5 shows how to implement comparative backtests with the multi-objective scores of Theorem 4.4.

| Risk Measure | Identifiability | Elicitability | Multi-objective |

|---|---|---|---|

| Elicitability | |||

| ✗ | ✗ | ✗ | |

| ✗ | ✗ | ✗ | |

| ✗ | ✗ | ✗ | |

| ✓ | ✗ | ✓ | |

| ✓ | ✗ | ✓ | |

| ✓ | ✗ | ✓ | |

| ✓ | ✓ | ✓ | |

| ✗ | ✗ | ✗ | |

| ✓ | ✓ | ✓ |

5 Diebold–Mariano tests for multi-objective scores

5.1 Two-sided tests

DM95 propose to use formal hypothesis tests to account for sampling uncertainty in forecast comparisons. These so-called Diebold–Mariano (DM) tests are widely used in empirical forecast comparisons and continue to be studied in the theoretical literature. However, consistent with the extant notion of strict consistency, DM tests have hitherto relied on scalar scoring functions. Thus, here we show how to use our two-dimensional multi-objective scores from Theorem 4.4 in DM tests, with a special focus on the implications caused by the lexicographic order.

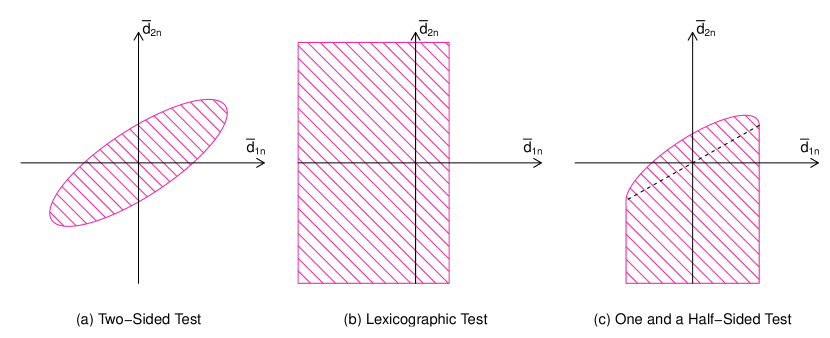

To that end, denote by one of the multi-objective scores of Theorem 4.4. Let and be the appertaining competing sequences of forecasts (e.g., if , then for ). The verifying observations are . We compare the two forecasts via the (bivariate) score differences . The two-sided null hypothesis is that both forecasts predict equally well on average, i.e., for all , where . (Along the lines of GW06, one can also test the conditional null hypothesis for all , where the -algebra contains all information available at time .) We test using the Wald-type test statistic

| (5.1) |

where is some consistent estimator of the variance-covariance matrix under the null hypothesis (i.e., in the componentwise norm, , as ). To account for possible autocorrelation in the sequence , one can use

| (5.2) |

where is a sequence of integers satisfying , and is a uniformly bounded scalar triangular array with , as , for all ; see Whi01 for detail. Under the assumption that does not exhibit autocorrelation under the null, can be set to 0 such that is simply the sample variance-covariance matrix.

Theorem 5.1.

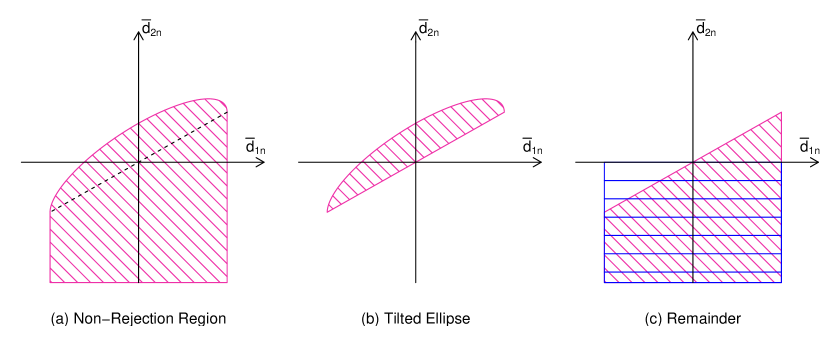

Thus, we reject at significance level , if , where is the -quantile of the -distribution. A typical non-rejection region in terms of and is sketched in Figure 3 (a), and has the well-known ellipse shape. For brevity, we leave out a formal investigation of our test under the alternative. We mention, however, that consistency of our test can be established along the lines of GW06.

5.2 One and a half-sided tests

In several contexts, it may be desirable to perform a one-sided comparative backtest to establish the superiority of risk forecasts over some benchmark forecasts . These different forecasts could stem from two different internal models of a financial institution (say, a legacy model and and extension thereof). It could also be the case that the benchmark forecasts originate from a regulatory standard model, and—in line with the conservative backtesting approach of FZG16—the financial institution has the onus of proof to show the superiority of its internal model over the standard model. In such situations, it is tempting to test the null hypothesis , which is equivalent to

| (5.3) |

Here, the goal would be to reject the null of better or, at least, equally good benchmark forecasts as evidence of the superiority of . However, as under standard conditions (see Theorem 5.1), has an asymptotic bivariate normal distribution, the probability that and vanishes for large sample sizes. Thus, testing (5.3) amounts to a test of the null , i.e., that the benchmark VaR forecasts are superior. This null can be tested via , where we reject (5.3) at significance level when . The corresponding non-rejection region is sketched in Figure 3 (b). In particular, we would reject solely based on the predictive performance of the component. In other words, once is rejected such that the internal VaR forecasts are superior, the internal forecasts are preferable in the lexicographic order irrespective of the quality of the systemic risk component. Since this would entirely ignore the motivation of the backtest, we disregard this one-sided backtesting approach.

As a compromise, we suggest to test the following ‘one and a half-sided’ null hypothesis. Since the two systemic risk forecasts only play a role for the ranking in the lexicographic order when , our suggested null hypothesis takes the form

We demonstrate below how to interpret a rejection of this null. The region in pertaining to is the lower part of the vertical axis in Figure 3 (c).

Obviously, is the union of all with , where

For each individual , this can be tested using the Wald-type test statistic , where is defined similarly as , only with replaced by . (Note that this substitution leaves unaffected.) Thus, we reject if and only if

| (5.4) |

where . The area associated with the appertaining non-rejection region is shaded in pink in Figure 3 (c). The rejection condition (5.4) is of course equivalent to where the solution follows from a simple quadratic minimisation problem. Hence,

| (5.5) |

To illustrate this graphically, note that the line defined by —indicated by the dashed line in Figure 3 (c)—passes through the extremal (negative and positive) horizontal points of the ellipse. Thus, if , (5.5) parametrizes the upper half of the tilted ellipse, and if the area below. In our numerical experiments, we use to test .

The next proposition shows that rejecting when leads to a test of level , where denotes the cdf of a -distribution.

Proposition 5.2.

Under the conditions of Theorem 5.1, rejecting if leads to an asymptotic size -test with . That is,

Remark 5.3.

For a test of with desired significance level of , one can determine the required level from using standard root-finding algorithms. E.g., if / / , then / / .

Remark 5.4.

To compare systemic risk forecasts on an equal footing, it may be desirable to compare them based on the same marginal model being used and, hence, based on the same VaR forecasts . In this case, differences in predictive ability can be attributed solely to the different dependence models; see, e.g., NZ19+ and Hog20a+. (Note that Theorem 5.1 no longer applies for identical VaR forecasts, since the limit of the covariance matrix is only positive semi-definite.) When , testing for is redundant, and and reduce to and , respectively. These hypotheses can be tested using . Under , converges to an -limit when restricting the assumptions of Theorem 5.1 to the sequence . Hence, we would reject (or ) at significance level , if (or ).

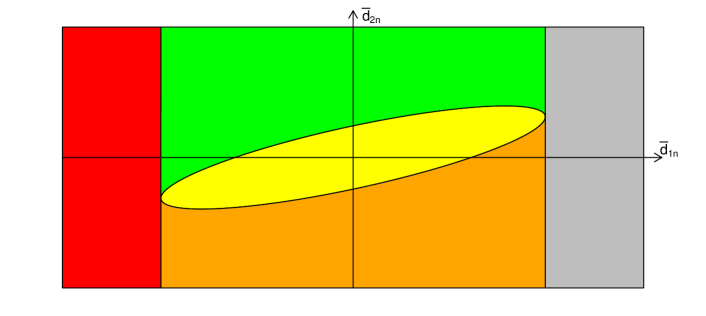

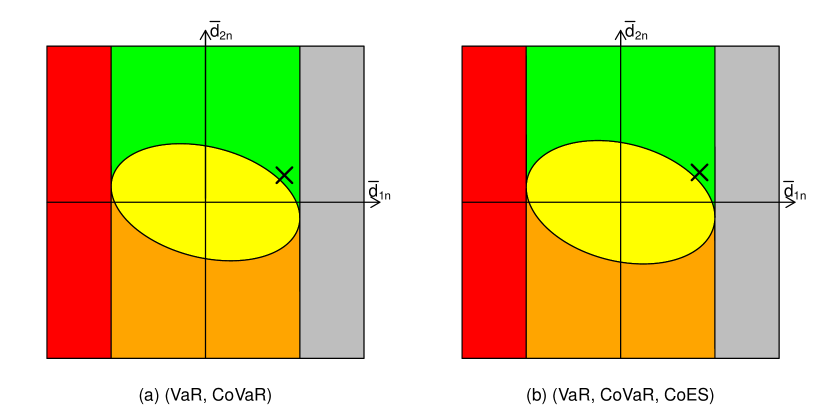

Figure 4 presents a schematic for interpreting test decisions on depending on the values of and . In a regulatory context, it extends the three-zone traffic-light classification of the BCBSBF19:

“The green zone corresponds to backtesting results that do not themselves suggest a problem with the quality or accuracy of a bank’s model. The yellow zone encompasses results that do raise questions in this regard, but where such a conclusion is not definitive. The red zone indicates a backtesting result that almost certainly indicates a problem with a bank’s risk model.”

The union of the yellow and the orange areas in Figure 4 corresponds to the non-rejection region depicted in Figure 3 (c). By symmetry, the union of the yellow and the green areas is the non-rejection region associated with the null

Thus, for in the yellow area we can neither reject nor (at significance level , respectively). This implies that there is no evidence of differences in predictive ability between the internal and the benchmark model (at level ). From a regulatory perspective, the bank’s internal model is ‘at the boundary’ of what can be deemed acceptable. Hence, we suggest heightened attention and close monitoring by the regulator, as indicated by the yellow colour.

When falls into the orange area, then—while the VaR forecasts are of comparable quality—the benchmark model provides superior systemic risk forecasts. Here, as indicated by the orange colour, a revision of the internal systemic risk forecasts is called for, while the internal marginal model is in order.

In contrast, the green area indicates superior systemic risk forecasts of the internal model, with VaR forecasts being comparably accurate. In this case, the financial institution should be allowed to use its internal model for risk forecasting purposes. The green colour indicates a pass of the backtest.

In the red region, the VaR forecasts of the internal model are deemed inferior to the benchmark predictions, whence there is no basis to compare the systemic risk forecasts. (The red region corresponds to the rejection region of the null at level . E.g., for we get and .) Here, the bank should not be allowed to use its own marginal model (the traffic light is red), but instead should be required to use the benchmark model for the marginals to ensure a fair assessment of the systemic risk forecasts. For this comparison, where the VaR forecasts are identical, one can focus solely on the systemic risk component by using ; see Remark 5.4. For the comparison via , we suggest to adopt a similar decision heuristic as in FZG16: Neither nor can be rejected when (corresponding to our yellow zone). When () such that () can be rejected, the internal systemic risk forecasts are superior (inferior), corresponding to our green (red) zone.

Similarly as for the red region, there are no grounds for meaningful systemic risk forecast comparisons in the grey area, since the internal model’s VaR forecasts are superior. (Formally, it corresponds to the rejection region of the null at level .) In this case, there is no cause for action on the end of the bank (hence the grey colour), but the regulator should rather adopt the bank’s VaR model as a basis for comparing the systemic risk forecasts. As before, the subsequent comparison of systemic risk forecasts should be carried out by using , since the VaR forecasts are identical.

Section F investigates the finite-sample properties of , , and under and in detail. Here, we only summarize the main findings. First, size is adequate already for , which is encouraging since effective sample sizes in risk forecast comparisons are small. Second, power increases markedly in . Third, comparisons for (CoVaR, CoES) are slightly more powerful than those for CoVaR alone, most likely due to the increased informational content of the CoES component. Fourth, as expected for one-sided tests, departures from and are easier to detect for the former. Fifth, it is in general easier to detect differences in predictive ability of the systemic risk component, when the VaR component is identical (instead of only comparable) across forecasts. Intuitively, the inclusion of comparable VaR forecasts dilutes the power of the test in the systemic risk component.

6 Empirical application

Consider daily log-losses on the S&P 500 and log-losses on the DAX 30 from 2000–2020, where the data are taken from www.wsj.com/market-data/quotes (ticker symbols: SPX and DX:DAX). So if denotes the stock index value at time , then (). We only keep those observations where data on both indexes are available, giving us observations. Here, for , we compare rolling-window (VaR, CoVaR, CoES) forecasts for the series , where denotes the moving window length. The choice of and amounts to considering the risk for large losses of the DAX 30, given that the world’s leading stock index—the S&P 500—is in distress. To promote flow in this section, we often refer to the simulation setup in Section F for details on the time series models and the risk forecast computation.

For short-term risk management purposes, conditional (systemic) risk measure forecasts are more informative than unconditional ones. Conditional risk measures are based on the conditional distribution of , that is, for . Here, the filtration is generated by the information available to a forecaster at time . These are usually past observations , and possibly additional exogenous information. Here, we assume , such that we forecast the conditional risk measures , , and . For notational brevity, we suppress the dependence of the risk measures on the risk levels and , which we fix at .

We consider two different methods for forecasting. The first method uses a simple GARCH(1,1) model for and and—as a dependence model for the respective innovations and —a Gaussian copula driven by GAS dynamics. That is, we assume to have Gaussian copula density with time-varying correlation parameter following GAS dynamics. Details on the precise specification are in Subsection F.1, where the same model (with in Equation (F.2)) is used in the simulations. Both the marginal and the dependence model are regularly used as benchmark models in forecast comparisons.

The second method uses the GJR–GARCH(1,1) model of GJR93. The GJR–GARCH model possesses an additional parameter that allows positive and negative shocks of equal magnitude to have a different effect on volatility. As a dependence model, we now use a -copula driven by GAS dynamics, similarly as in Equation (F.2). For both models we remain agnostic regarding the specific distribution of the and —both in the model estimation (by using the robust Gaussian quasi-maximum likelihood estimator for the GARCH-type marginal models) and the risk forecasting stage (by using their empirical cdfs and in computing the risk measures). For details on how the risk predictions are calculated, we refer to Subsection F.2.

We now compare two sequences of rolling-window predictions. For each rolling window of length , we re-fit the two models on a daily basis. This gives us forecasts from the GARCH model with Gaussian copula, and from the GJR–GARCH with -copula. We interpret the as generic benchmark forecasts, which are to be improved upon by the . In an oversight context, the may be some regulatory benchmark forecasts and the forecasts from the bank’s internal model. Or from a banking perspective, the may be forecasts issued from a trading desk’s legacy model and the are forecasts from a refined version thereof. The latter context is more realistic here, because in the regulatory framework the focus is more often on the relation of between an individual bank’s returns and the market as a whole. In any case, the methodology remains the same. We compare forecasts based on the verifying observations .

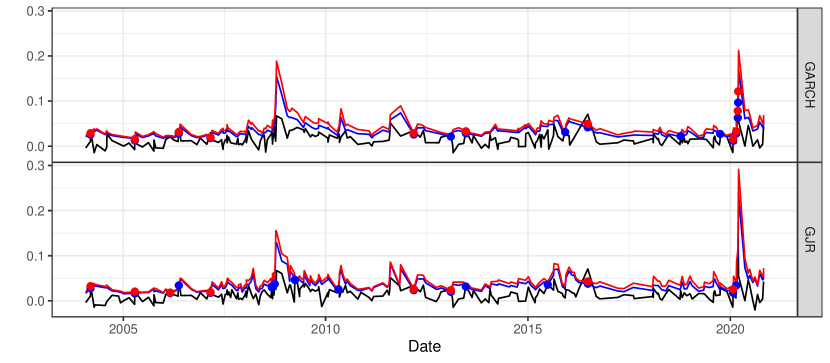

Figure 5 shows CoVaR and CoES forecasts from both models, where the top panel corresponds to the GARCH model with Gaussian copula and the bottom panel to the GJR–GARCH with -copula. Specifically, the panels show the CoVaR (blue) and CoES (red) forecasts for the DAX log-losses (black) on days where the S&P 500 exceeds its VaR forecast. Note that due to the different marginal models (and, hence, the different VaR forecasts), the black lines differ slightly in the upper and lower panel of Figure 5. By definition, the S&P 500 should only exceed its VaR forecast on 5% of all trading days, i.e., on days in our out-of-sample period. With 213 (218) VaR violations, our marginal GARCH(1,1) model (GJR–GARCH(1,1) model) is close to the ideal frequency. By definition, we expect our CoVaR forecasts to be not exceeded on 95% of these 213 days (218 days) with a VaR violation. With 15 and 16 exceedances (blue dots), which correspond to non-exceedance frequencies of 93.0% and 92.7%, the Gaussian copula and the -copula model are reasonably close to the 95%-benchmark. However, for the Gaussian copula, the CoVaR exceedances seem to cluster more, such as during the beginning of the Covid-19 pandemic in early 2020 (top panel of Figure 5). Such violation clusters are undesirable from a risk management perspective, providing some informal evidence in favour of the -copula model. We investigate this more formally in the following. Note that both panels of Figure 5 indicate marked spikes in systemic risk during the financial crisis of 2008–2009, during the European sovereign debt crisis in the first half of the 2010’s, and—most markedly—in 2020 as a consequence of the Covid-19 pandemic.

As pointed out above, we regard the GARCH model with Gaussian copula as our benchmark model. So we now want to test for (VaR, CoVaR) and (VaR, CoVaR, CoES). Due to the less clustered CoVaR exceedances and the compelling empirical evidence in favour of GJR–GARCH models (GJR93; BEK11) and GAS--copula models (CKL13; BC19), we expect the GJR–GARCH model with -copula to produce lower scores, i.e., better risk forecasts, possibly leading to a rejection of . We carry out the tests using with the scores of Equations (F.4) and (F.5) having 0-homogeneous score differences, and with from (5.2) (with ); see Supplement Subsection F.3 for details. For VaR and ES forecasts, scoring functions giving 0-homogeneous score differences are typically recommended, since they allow for ‘unit-consistent’ and powerful comparisons (NZ17). We confirm the latter in our simulations for systemic risk forecasts as well, thus justifying our choice. Let be defined as in Subsection 5.1. Indeed, computing , we find that the GJR–GARCH with -copula produces lower scores for both the (VaR, CoVaR) and the (VaR, CoVaR, CoES) forecasts. The score differences are even statistically significant at the 5%-level: The -values for the -based Wald test are 2.9% for (VaR, CoVaR) and 3.0% for (VaR, CoVaR, CoES).

Figure 6 illustrates the test decisions. Panel (a) shows the results for the (VaR, CoVaR) comparison. Both and are positive, favouring the forecasts from the GJR–GARCH model with -copula. Additionally, the pair lies above the yellow ellipse, which traces the contour of a bivariate normal distribution with probability content . This confirms the significance of the score difference at the -level; recall Remark 5.3. The results for the (VaR, CoVaR, CoES) forecasts in panel (b) are qualitatively similar. Adopting our traffic-light interpretation, the GJR–GARCH model with -copula would be deemed an adequate risk forecasting model.

Nonetheless, the borderline significance of this example shows that discriminating between (systemic) risk forecasts requires long samples for the given parameter choice of . This is as expected, because by only considering observations with one extreme component, the effective sample size is massively reduced to roughly . Indeed, for both models, the effective out-of-sample period for comparing systemic risk forecasts is reduced from a length of 4193 to just over 200. The practical implication is that one should allow for sufficiently large samples to prove the superiority of the internal model over the benchmark. Alternatively, one could adapt a slightly looser definition of distress in the reference asset , e.g., by setting . The current evaluation period for VaR forecasts specified in the Basel framework by the BCBSBF19 is one year, amounting to roughly 250 daily returns. Even for evaluating VaR and ES forecasts, the horizon of 250 days has been called into question for being too short (DLS20), and this is only magnified for systemic risk forecasts. So whatever evaluation period for systemic risk measures is eventually settled on in a regulatory context, it likely needs to be far in excess of one year.

7 Discussion and outlook

To our knowledge, this is the first paper to come up with comparative backtests for the systemic risk measures CoVaR, CoES and MES, which are crucial inputs in financial, macroeconomic and regulatory applications. Model selection procedures based on our results may enhance modelling attempts of these quantities in financial institutions. Moreover, the fact that our notion of multi-objective elicitability serves as a ‘truth serum’ implies that the regulatory framework can be improved by enticing financial institutions to accurately model systemic risk. In terms of calibration tests, we are only aware of one more paper: Banulescu-RaduETAL2019 introduce such tests, which unfortunately hinge on non-strict identification functions. This may lead to a severe loss of power under the alternative as demonstrated in Remark 4.3 and Section G. Due to the strictness of our identification functions, such a phenomenon cannot happen in our context.

The novel concept of multi-objective elicitability is likely to be fruitful also in applications beyond the proposed DM-backtests for systemic risk measures. In Subsection B.1, we provide more examples of interesting situations where conditional elicitability holds, yet classical joint elicitability fails. By virtue of Theorem 3.7, one can now construct incentive compatible elicitation mechanisms for these functionals, or can come up with -estimation procedures in a regression context.

Beyond the confines of finance, we anticipate many other interesting applications of our backtests. For instance, in economics, ABG19 and Aea21 have recently drawn attention to tail risks and their interconnections by popularizing the Growth-at-Risk, which is simply the VaR of GDP growth. This literature has led to an increase in the use of risk forecast evaluation methods in economics (e.g., BS21). Hence, the backtests developed in this paper should be relevant for future macroeconomic applications as well.

References

- Acharya et al. (2017) Acharya VV, Pedersen LH, Philippon T, Richardson M. 2017. Measuring systemic risk. The Review of Financial Studies 30: 2–47.

- Adrian et al. (2019) Adrian T, Boyarchenko N, Giannone D. 2019. Vulnerable growth. The American Economic Review 109: 1263–1289.

- Adrian and Brunnermeier (2016) Adrian T, Brunnermeier MK. 2016. CoVaR. The American Economic Review 106: 1705–1741.

- Adrian et al. (2021) Adrian T, Grinberg F, Liang N, Malik S, Yu J. 2021. The term structure of Growth-at-Risk. Forthcoming in American Economic Journal: Macroeconomics https://www.aeaweb.org/articles/pdf/doi/10.1257/mac.20180428.

- Artzner et al. (1999) Artzner P, Delbaen F, Eber JM, Heath D. 1999. Coherent measures of risk. Mathematical Finance 9: 203–228.

- Bank for International Settlements (2019) Bank for International Settlements. 2019. Basel Framework. Basel, http://www.bis.org/basel_framework/index.htm?export=pdf.

- Banulescu-Radu et al. (2021) Banulescu-Radu D, Hurlin C, Leymarie J, Scaillet O. 2021. Backtesting marginal expected shortfall and related systemic risk measures. Management Science 67: 5730–5754.

- Benoit et al. (2017) Benoit S, Colliard JE, Hurlin C, Pérignon C. 2017. Where the risks lie: A survey on systemic risk. Review of Finance 21: 109–152.

- Bernardi and Catania (2019) Bernardi M, Catania L. 2019. Switching generalized autoregressive score copula models with application to systemic risk. Journal of Applied Econometrics 34: 43–65.

- Brownlees et al. (2011) Brownlees C, Engle R, Kelly B. 2011. A practical guide to volatility forecasting through calm and storm. Journal of Risk 14: 3–22.

- Brownlees and Engle (2017) Brownlees C, Engle RF. 2017. SRISK: A conditional capital shortfall measure of systemic risk. The Review of Financial Studies 30: 48–79.

- Brownlees and Souza (2021) Brownlees C, Souza ABM. 2021. Backtesting global Growth-at-Risk. Journal of Monetary Economics 118: 312–330.

- Brunnermeier et al. (2020) Brunnermeier M, Rother S, Schnabel I. 2020. Asset price bubbles and systemic risk. The Review of Financial Studies 33: 4272–4317.

- Chen et al. (2013) Chen C, Iyengar G, Moallemi CC. 2013. An Axiomatic Approach to Systemic Risk. Management Science 59: 1373–1388.

- Creal et al. (2013) Creal D, Koopman SJ, Lucas A. 2013. Generalized autoregressive score models with applications. Journal of Applied Econometrics 28: 777–795.

- Diebold and Mariano (1995) Diebold FX, Mariano RS. 1995. Comparing predictive accuracy. Journal of Business & Economic Statistics 13: 253–263.

- Dimitriadis et al. (2020a) Dimitriadis T, Fissler T, Ziegel JF. 2020a. The Efficiency Gap. Preprint. https://arxiv.org/abs/2010.14146.

- Dimitriadis et al. (2020b) Dimitriadis T, Liu X, Schnaitmann J. 2020b. Encompassing tests for value at risk and expected shortfall multi-step forecasts based on inference on the boundary. Preprint. https://arxiv.org/abs/2009.07341.

- Eckernkemper (2018) Eckernkemper T. 2018. Modeling systemic risk: Time-varying tail dependence when forecasting marginal expected shortfall. Journal of Financial Econometrics 16: 63–117.

- Ehm et al. (2016) Ehm W, Gneiting T, Jordan A, Krüger F. 2016. Of quantiles and expectiles: consistent scoring functions, Choquet representations and forecast rankings. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 78: 505–562.

- Ehrgott (2005) Ehrgott M. 2005. Multicriteria Optimization. Berlin, Heidelberg: Springer.

- Emmer et al. (2015) Emmer S, Kratz M, Tasche D. 2015. What is the best risk measure in practice? a comparison of standard measures. Journal of Risk 18: 31–60.

- Feinstein et al. (2017) Feinstein Z, Rudloff B, Weber S. 2017. Measures of systemic risk. SIAM Journal on Financial Mathematics 8: 672–708.

- Fissler et al. (2021) Fissler T, Frongillo R, Hlavinová J, Rudloff B. 2021. Forecast evaluation of quantiles, prediction intervals, and other set-valued functionals. Electronic Journal of Statistics 15: 1034–1084.

- Fissler and Ziegel (2016) Fissler T, Ziegel JF. 2016. Higher order elicitability and Osband’s principle. The Annals of Statistics 44: 1680–1707.

- Fissler et al. (2016) Fissler T, Ziegel JF, Gneiting T. 2016. Expected shortfall is jointly elicitable with value-at-risk: Implications for backtesting. Risk Magazine : 58–61.

- Giacomini and White (2006) Giacomini R, White H. 2006. Tests of conditional predictive ability. Econometrica 74: 1545–1578.

- Giesecke and Kim (2011) Giesecke K, Kim B. 2011. Systemic risk: What defaults are telling us. Management Science 57: 1387–1405.

- Giglio et al. (2016) Giglio S, Kelly B, Pruitt S. 2016. Systemic risk and the macroeconomy: An empirical evaluation. Journal of Financial Economics 119: 457–471.

- Girardi and Tolga Ergün (2013) Girardi G, Tolga Ergün A. 2013. Systemic risk measurement: Multivariate GARCH estimation of CoVaR. Journal of Banking & Finance 37: 3169–3180.

- Glosten et al. (1993) Glosten LR, Jagannathan R, Runkle DE. 1993. On the relation between the expected value and the volatility of the nominal excess return on stocks. The Journal of Finance 48: 1779–1801.

- Gneiting (2011) Gneiting T. 2011. Making and evaluating point forecasts. Journal of the American Statistical Association 106: 746–762.

- Hoga (2021) Hoga Y. 2021. Modeling time-varying tail dependence, with application to systemic risk forecasting. Forthcoming in Journal of Financial Econometrics : 1–31.

- Mainik and Schaanning (2014) Mainik G, Schaanning E. 2014. On dependence consistency of CoVaR and some other systemic risk measures. Statistics & Risk Modeling 31: 49–77.

- Mas-Colell et al. (1995) Mas-Colell A, Whinston MD, Green JR. 1995. Microeconomic Theory. Oxford University Press.

- Nolde and Zhang (2020) Nolde N, Zhang J. 2020. Conditional extremes in asymmetric financial markets. Journal of Business & Economic Statistics 38: 201–213.

- Nolde and Ziegel (2017) Nolde N, Ziegel JF. 2017. Elicitability and backtesting: Perspectives for banking regulation. The Annals of Applied Statistics 11: 1833–1874.

- Steinwart et al. (2014) Steinwart I, Pasin C, Williamson R, Zhang S. 2014. Elicitation and Identification of Properties. JMLR Workshop Conf. Proc. 35: 1–45.

- White (2001) White H. 2001. Asymptotic Theory for Econometricians. San Diego: Academic Press, First edn.

Supplement

Appendix A Proofs for Section 3

-

Proof of Proposition 3.4::

Let be a strict -identification function for and, for any , let be a strict -identification function for . We claim that

is a strict -identification function for . Consider some and . First, assume . Then and . Second, assume and . Due to the former equality and the strictness of , it holds that . Now we can invoke the strictness of on to conclude that . ∎

-

Proof of Theorem 3.7::

Let be a strictly -consistent scoring function for . For any let be a strictly -consistent scoring function for . We claim that

(A.1) is a strictly multi-objective -consistent scoring function for with respect to . To see this, consider some with and . From the strict -consistency of it follows that

(A.2) where the inequality is strict if . If the inequality is strict, we can already conclude that Otherwise, it must be the case that . Since by assumption is a singleton, . Invoking the strict -consistency of , we obtain that

(A.3) where the inequality is strict if . If the inequality is strict, this implies that Otherwise, equality implies that . ∎

Remark A.1.

Theorem 3.7 is almost a direct analogue of Proposition 3.4, with the intriguing exception that is assumed to be a singleton on in Theorem 3.7. An inspection of the proof reveals that this is needed to show the inequality in (A.3). If at this stage of the proof one has that and , it is per se not clear (and in general also not the case) that from which the inequality in (A.3) would follow. What would be sufficient, however, to dispense with the assumption on and to still show (A.3) is the following: It is possible to choose a family of strictly -consistent scores , , for such that for all and for all we have equality for the expected scores, . In many practical examples, this can be achieved; see, e.g., Example B.1 (b).

Appendix B More background on multi-objective elicitability

B.1 Further examples of multi-objective elicitable functionals

We provide more examples of functionals that are conditionally elicitable, yet fail to be elicitable in the traditional sense. Examples (c) and (d) are concerned with -prediction intervals. In line with FFHR2021 for some random variable with distribution , this is any interval such that . Of course, each distribution has a multitude of different -prediction intervals. We consider two possible attempts of coming up with interpretable -prediction intervals.

Two univariate scores are equivalent if there exists a positive constant and a function such that . Ignoring integrability issues for a moment, it is clear that equivalence preserves (strict) consistency. If and are -integrable, so is . However, by a convenient choice of , the integrability conditions of can be milder than those of . E.g., while , , is a strictly -consistent scoring function for the mean, the equivalent score is strictly -consistent score for the mean. A straightforward generalisation is obvious for multi-objective scores of the form (A.1), i.e.,

| (B.1) |

Example B.1.

-

(a)

The variance functional is conditionally elicitable with the mean functional on . A strictly multi-objective -consistent score is given by (B.1), where and Alternatively, to achieve a strictly multi-objective -consistent score, one can consider the equivalent version , or more generally , where is strictly convex with subgradient .

-

(b)

For , is conditionally elicitable with the -quantile, , on . A strictly multi-objective -consistent score is given via (B.1), where and It is straightforward to verify that this family of scores satisfies the condition discussed in Remark A.1. Similar to (a), we can achieve strict multi-objective -consistency upon replacing by , or more generally by , where is strictly convex with subgradient .

-

(c)

Fix . Motivated by prediction intervals induced by quantiles of the form for we consider the following form of -prediction intervals. Let be elicitable on , where all are strictly increasing cdfs, and let be the right endpoint of the shortest -prediction interval whose left endpoint is given via . FFHR2021 asserts that is not elicitable, subject to smoothness conditions, but FFHR2021 yields that is conditionally elicitable with on . A strictly multi-objective -consistent scoring function is given by (B.1), where is a strictly -consistent score for and

where is strictly increasing and -integrable.

-

(d)

A different approach to constructing interpretable -prediction intervals is to specify the midpoint in terms of an elicitable functional, such as the mean or the median. Again, let and let be elicitable on and let be half of the length of the shortest -prediction interval with midpoint . FFHR2021 asserts that is not elicitable, subject to smoothness conditions, but FFHR2021 yields that is conditionally elicitable with on . A strictly multi-objective -consistent scoring function is given via (B.1), where is a strictly -consistent score for and

where is strictly increasing with being -integrable for all .

-

(e)

For , let as in (4.1). Define the right -tail of a distribution as where . Then, is conditionally elicitable with on . A strictly multi-objective -consistent score is given via (B.1), where with strictly increasing and bounded , and the second component of is given by Here, is a strictly proper scoring rule. This result follows from Gne11a; see also Theorem C.2 and HolzmannKlar2017 for related approaches.

B.2 Dimensionality considerations

Consider an elicitable functional with strictly -consistent score , where . Under sufficient smoothness conditions on the score and the expected score , first order conditions yield that the -dimensional gradient of is an -identification function for (which is not necessarily strict). Under the conditions of Theorem 3.7, first order conditions of the corresponding strictly multi-objective -consistent score (B.1) also induce an -identification function whose dimension coincides with . To illustrate this, suppose that and are univariate, such that . We have the scores . At the optimum we obtain the first order condition and . Hence, if the derivatives exist and tacitly assuming that integration and differentiation commute, constitutes a two-dimensional -identification function for . This means we can consider the two-dimensional score (B.1) as a generalised antiderivative of a -dimensional identification function where the symmetry conditions imposed by the Hessian are massively relaxed, which renders the existence of such an object possible. Thus, multi-objective scores provide a means to close the gap between identification and scoring functions for multivariate functionals.

B.3 More on multi-objective elicitability with respect to the lexicographic order

Remark B.2.

Resuming with the discussion right before Theorem 3.7, the use of the lexicographic order on allows to compare any forecasts, also misspecified ones. As for the classical univariate concept of strict consistency, strong consistency stays silent about the ranking of possibly misspecified forecasts, which is, however, the more realistic scenario (Patton2020). For univariate functionals, consistency implies order-sensitivity under mild conditions (BelliniBignozzi2015; Lambert2019): If two forecasts are both smaller or larger than the true functional value, the one closer to the true value achieves an expected score at most as large as the other forecast. For multivariate forecasts, there are various generalisations of order-sensitivity (see, e.g., LambertETAL2008; FisslerZiegel2019). For multi-objective scores similar order-sensitivity results would be desirable. We suspect that the componentwise order-sensitivity concept would be particularly promising in that regard.

Remark B.3.

On the level of the prediction space setting (GneitingRanjan2013), HolzmannEulert2014 establish that consistent scoring functions are sensitive with respect to increasing information sets. That is, when comparing two ideal forecasts based on nested information sets, the more informed forecast outperforms the less informed one on average. This is an instance of the more general calibration–resolution principle of Pohle2020, showing that minimising a consistent scoring function amounts to “jointly maximizing information content and minimizing systematic mistakes”. Using the same arguments as in HolzmannEulert2014 and Pohle2020 (basically exploiting the tower property of conditional expectations), one can establish a similar principle for multi-objective consistent scores mapping to .

B.4 The necessity of the Convex Level Sets property

Here, we revisit a powerful necessary condition for identifiability and elicitability, namely the Convex Level Sets (CxLS) property, for multi-objective scores. We use the same notation as in Section 3 of the main paper, in particular we let . Following the terminology of FFHR2021 we say that a functional , satisfies the selective CxLS property on if for all and for all such that we have satisfies the selective CxLS* property on if for all and for all such that implies that . We shall frequently omit the term “selective” and will just speak of the CxLS and the CxLS* property. Clearly, the CxLS* property implies the CxLS property. If attains singletons only on , then the two properties coincide. They then take the familiar form that implies . It is well known that the CxLS property is necessary for identifiability (which we state for the sake of completeness). Proposition 3.4 in FFHR2021 establishes that the CxLS* property is necessary for univariate elicitability. The following generalises this result to strong multi-objective elicitability.

Proposition B.4.

Consider a functional .

-

(i)

If is identifiable on , it satisfies the CxLS property on .

-

(ii)

If is strongly multi-objective elicitable on , it satisfies the CxLS* property on .

-

Proof of Proposition B.4::

For (i), let be a strict identification function. Let such that for some . For it holds that Due to the strictness of , we have .

For (ii), the proof follows along the lines of the proof of Proposition 3.4 in FFHR2021. With the same set-up as above, consider some strictly strongly multi-objective -consistent scoring function . For , the strict strong multi-objective -consistency of implies that for any we have for and for the score difference is . Hence, equals which is for and otherwise . ∎

Proposition B.4 implies that strong multi-objective elicitability shares an important feature with the usual univariate notion of elicitability. Showing that the CxLS* is violated is the standard procedure to rule out elicitability. Consequently, functionals violating the CxLS* property such as variance or ES also fail to be strongly multi-objective elicitable. This applies in particular to scoring functions mapping to , since is a total order.

On the other hand, weak multi-objective elicitability appears to be much more flexible than its strong counterpart. Indeed, the following consideration shows that the CxLS property is not necessary for weak multi-objective elicitability: Suppose we have a strictly weakly multi-objective -consistent scoring function for mapping to , where is the componentwise order. Suppose further that there are such that for all . Assume there is some and some such that and . Then, invoking the linearity of the integral, . Therefore, and the CxLS property is violated (and thus also the CxLS* property).

A further investigation of weak multi-objective elicitability therefore seems to be an interesting field. Such an investigation will be deferred to future work.

Appendix C Conditional identifiability and conditional elicitability results

Here, we show that , and are all conditionally elicitable and conditionally identifiable with , subject to mild assumptions on the corresponding class of bivariate distributions.

Remark C.1.