Università Cattaneo LIUC, Castellanza, Italy

Fluctuation phenomena, random processes, noise, and Brownian motion Entropy and other measures of information Economics; econophysics, financial markets, business and management

Inferring Multi-Period Optimal Portfolios via Detrending Moving Average Cluster Entropy

Abstract

Despite half a century of research, there is still no general agreement about the optimal approach to build a robust multi-period portfolio. We address this question by proposing the detrended cluster entropy approach to estimate the portfolio weights of high-frequency market indices. The information measure produces reliable estimates of the portfolio weights gathered from the real-world market data at varying temporal horizons. The portfolio exhibits a high level of diversity, robustness and stability as it is not affected by the drawbacks of traditional mean-variance approaches.

pacs:

05.40.-apacs:

89.70.Cfpacs:

89.65.Gh1 Introduction

Markowitz mean-variance approach [1] estimates minimum risk and maximum return for portfolio optimization models in financial decision-making processes. Variants of the original mean-variance approach have been proposed integrating financial concepts and tools such as: capital asset pricing [2], Sharpe ratio [3], excess growth rate [4] Gini-Simpson index [5]. However, contrary to the aim of diversifying, mean-variance approaches yield weights strongly concentrated on some assets, resulting in low diversity of the portfolio.

Traditional approaches have shown even more dramatic limits in multiple horizons and out-of-sample estimates, where nonstationarities and fat tails of the price return distribution come unavoidably into play [6, 7]. As high-frequency data become available, microstructure noise increasingly becomes dominant in the returns and volatility series, affecting portfolio performance by reducing signal-to-noise ratio, particularly over multiple periods. Larger sampling intervals could reduce the effect of microstructure noise but with the evident disadvantage of not making full use of the available data. Dynamic readjustment of the portfolio and sequential wealth re-allocation to selected assets in consecutive trading periods is a key requirement to gather relevant news. Regretfully, errors related to the microstructure noise and non-normality of financial series are particularly relevant when portfolio weights should be estimated at different horizons [8, 9].

Despite numerous and prominent efforts, the efficacy of quantitative methods of portfolio allocation still remains an open issue, leaving the financial community with the deceiving impression that the naive equally-weighted portfolio of assets is not yet significantly outperformed by other approaches to portfolio optimization [10, 11, 12]

Over the past decades, a growing wave of interest has been directed towards the analysis of nonlinear interactions arising in complex systems in different contexts. Complex systems exhibit remarkable features related to patterns emerging from the seemingly random structure of time series due to the interplay of long- and short-range correlated processes [13, 14, 15, 16, 17, 18, 19, 20]. Hence, entropy and other information measures have increasingly found applications in complex systems science and, in particular, in economics and finance. As a tool for quantifying dynamics, entropy has been adopted for shedding light on fundamental aspects of asset pricing models [21, 22]. As a tool for quantifying diversity, entropy has been exploited for mitigating drawbacks of traditional portfolio strategies. In this specific context, entropy is considered a convenient instrument of shrinkage and dispersion for the traditional portfolio weights distribution lacking reasonable diversity degree [23, 24, 25, 26, 27, 28, 29, 30, 31, 32, 33, 34, 35, 36, 37, 38, 39, 40].

The detrended cluster entropy approach [41, 42, 43] has been adopted to investigate several assets over a single period in [44]. An information measure of diversity, the cluster entropy index , was put forward by integrating the entropy function over the cluster dimension , with the moving average window as a parameter. It was shown that the cluster entropy index of the volatility is significantly market dependent. Hence, the construction of an efficient single-period static portfolio based on the cluster entropy index has been proposed and compared to traditional mean-variance and equally-weighted portfolios of assets.

The cluster entropy approach was extended to multiple temporal horizons showing an interesting and significant horizon dependence particularly in long-range correlated markets in [45, 46]. Artificially generated price series have been systematically analysed in terms of the cluster entropy dependence on the horizons . The cluster entropy for Fractional Brownian Motion (FBM) and Generalized AutoRegressive Conditional Heteroskedasticity (GARCH) processes proved unable to reproduce real markets dynamics. Conversely, for Autoregressive Fractionally Integrated Moving Average (ARFIMA), the cluster entropy proved able to replicate asset behaviour. Hence, results obtained by the cluster entropy approach on real-world market series are consistent with the hypothesis of financial processes deviating from i.i.d. stochastic processes, proving the ability of the detrended cluster entropy approach of capturing the important statistical features and stylized facts of the real world markets [45, 46].

In this work, building on the method proposed in [44, 45] and the systematic analysis conducted in [46], we discuss how a robust multi-period dynamic portfolio can be constructed via the cluster entropy of return and volatility of assets. The cluster entropy index will be dynamically implemented at different temporal horizons . The multi-period portfolio is estimated over five assets () and twelve consecutive monthly periods over one year ().

2 Mean-Variance Approach to Portfolio Construction

A portfolio is a vector , satisfying , representing the relative allocation of wealth in asset . Let be the return of the asset at time . The expected return of the portfolio can be written in terms of the expected return of each asset as:

| (1) |

Let indicate the standard deviation of the return of the asset , the covariance between and . The variance of the portfolio return can be written as:

| (2) |

According to the Markowitz portfolio strategy, the weights , for are chosen to minimize the variance of the return under the constraint of an expected portfolio return . The performance of the mean-variance portfolio can be maximized in terms of the Sharpe ratio defined as:

| (3) |

The maximization of the Sharpe ratio, with maximum portfolio return eq. (1) and minimum portfolio variance eq. (2), is commonly adopted in the standard portfolio theory to nominally yield the optimal weights . However, as eq. (1) and eq. (2) imply normally distributed stationary return series, the approach is flawed at its foundation. Thus, very biased portfolio weights are obtained as it could be reasonably expected with the asymmetric and heavy tailed return distributions of real-world markets. Several variants of the original theory have been thus proposed to overcome those limits. The poor accuracy and lack of diversity in the estimation of portfolio weights, with the transaction costs involved in the optimization constraints, have been soon recognized as limits of the applicability of mean-variance based models [10, 11, 12].

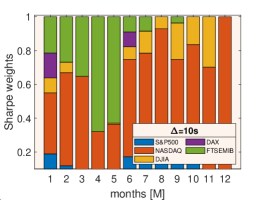

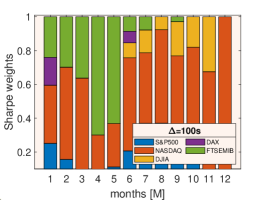

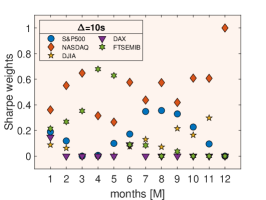

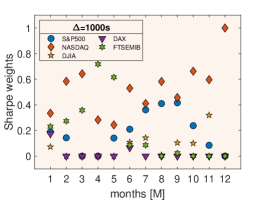

To fully appreciate the errors in the weights yielded by the traditional mean-variance approach, the Sharpe-ratio has been estimated on tick-by-tick data of the high-frequency markets described in Table 1 by using the code provided by the MATLAB Financial Toolbox.

| Ticker | Name | Country | Currency | Members | Length |

|---|---|---|---|---|---|

| NASDAQ | Nasdaq Composite | US | USD | 2570 | 6982017 |

| S&P500 | Standard & Poor 500 | US | USD | 505 | 6142443 |

| DJIA | Dow Jones Ind. Avg | US | USD | 30 | 5749145 |

| DAX | Deutscher Aktienindex | DE | Euro | 30 | 7859601 |

| FTSEMIB | Milano Indice di Borsa | UK | Euro | 40 | 11088322 |

The values of portfolio weights, which maximize the Sharpe ratio, are shown in fig. 1 and fig. 2. Raw market data are sampled to yield equally spaced series with equal lengths. Sampling intervals are indicated by . The Sharpe ratio maximization is performed on twelve multiple horizons . One can note (i) the unreasonably high variability of the weights of the same assets over consecutive periods and (ii) the biased distribution of the portfolio weights oriented towards the riskiest assets rather than a diversified portfolio, resulting in a quite scary and disappointing overall investment scenario.

3 Cluster Entropy Approach to Portfolio Construction

Among several alternatives proposed to build an effective portfolio, entropy-based tools have been recently developed, supported by the general idea that entropy itself is a measure of diversity.

Entropy-based portfolio inference is based on Shannon entropy, defined as

| (4) |

being the probability associated to a given stochastic variable relevant to the asset .

Initial attempts have introduced the portfolio weights, obtained by Markowitz based approaches, into eq. (4). Portfolio weights of risky assets, with and have the structure of a probability distribution, thus Shannon entropy can be written as:

| (5) |

One can immediately note that with equally distributed naive weights for all , reaches its maximum value . Conversely, when for the asset and for the others, .

Portfolio optimization, based on Kullback-Leibler minimum cross-entropy principle, was proposed in [25]:

| (6) |

is minimized with respect to the reference distribution . If the equally distributed probability of the weights is taken as reference, the approach provides a shrinkage of the poorly diversified weights towards the uniform distribution.

When entropy approaches are used, the portfolio is generally shrinked toward an equally weighted portfolio, which corresponds to the maximally diversified portfolio yielded by the equally distributed naive weights rule. However, the portfolios yielded by either eq. (5) or eq. (6) are still affected by the native limitation of operating with the weights estimated by the traditional approach, requiring normally and stationary distributed data. Thus, very critical performances are obtained when multiple horizons and out-of-sample estimates are considered.

The Detrending Moving Average (DMA) cluster entropy method goes beyond this limit as it does not rely on the assumption of Gaussian distributed returns. The DMA cluster entropy approach to portfolio optimization relies on the general Shannon functional eq. (4). The probability distribution function of each asset , defined as , is obtained by intersecting the asset time series with its moving average series [41, 42]. The simplest moving average is defined at each as the sum of the past observations from to , namely . However, more general detrending moving average cluster distributions can be generated with higher-order moving average polynomials as shown in [47, 48].

Consecutive intersections of the time series and their moving averages yield several sets of clusters, defined as the portion of the time series between two consecutive intersections of with . The cluster duration is equal to: where and refers to consecutive intersections of and . For each moving average window , the probability distribution function , i.e. the frequency of the cluster lengths , can be obtained by counting the number of clusters with length , . The probability distribution function results:

| (7) |

with the fractal dimension and the Hurst exponent of the series (), according to the widely accepted framework of power-law scaling of temporal correlation (see e.g. [49, 45, 46, 50]). The term in eq. (7) takes the form:

| (8) |

to account for the drop-off of the power-law behavior and the onset of the exponential decay when due to the finiteness of . When , a set of the order of clusters with lengths centered around a single value. When , that is when tends to the length of the whole sequence, only one cluster with is generated. Intermediate values of produces the broad distribution of cluster durations.

When the probability distribution eq. (7) is fed into the Shannon functional eq. (4), the entropy of the cluster lifetime distribution of the asset results:

| (9) |

where is a constant, and respectively arises from power-law and exponentially correlated cluster duration. The subscript refers to the single cluster duration and will be suppressed in the forthcoming discussion for simplicity.

The cluster entropy index of a relevant random variable, e.g. the return of a given asset , can be described as:

| (10) |

The first sum is referred to the power law regime of the cluster duration probability distribution. The second sum is referred to the linear regime of the cluster duration probability distribution, i.e. the excess entropy term with respect to the logarithmic one. The index represents the threshold value of the cluster lifetime between the regimes.

4 Results

As recalled in the Introduction, the cluster entropy and related portfolio’s weights have been estimated over a single period (i.e. a single temporal horizon of about six years) in [44]. In this work, the entropy ability to quantify dynamics and heterogeneity is exploited to estimate the weights of a multi-period portfolio. Such a construction is possible as the cluster entropy estimates involve horizon dependence. The values of the cluster entropy weights can be directly compared to the results obtained by using the traditional mean-variance approach and Sharpe ratio maximization shown in fig. 1 and fig. 2.

The construction of the multi-period portfolio is carried on by implementing the procedure on five market time series. The datasets include tick-by-tick prices from Jan. 1 to Dec. 31, 2018 downloaded from the Bloomberg terminal (further details provided in Table 1). Given the price series and the related time series of the returns , the volatility is defined as:

| (11) |

with the volatility window ranging from to and the expected returns over the window defined as:

| (12) |

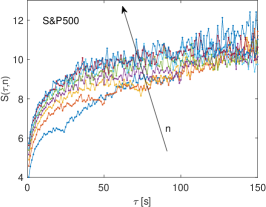

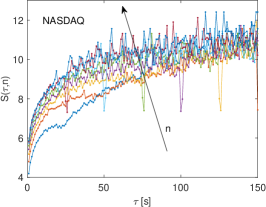

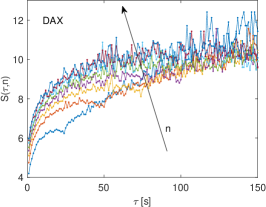

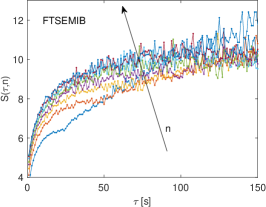

The cluster entropy of the volatility series is estimated by introducing eq. (7) into eq. (4) for different horizons (twelve monthly horizons out of one year have been considered). Results obtained on volatility series (assets described in Table 1) are plotted in fig. 3. The behaviour is consistent with the expectations provided by eq. (9): a logarithmic trend is observed at small cluster lengths , whereas a linear trend appears at larger values.

The current approach takes a different perspective compared to the traditional portfolio strategies. The cluster entropy is straightaway estimated from the financial market data with no assumption about the return distribution. To obtain the portfolio weights, the cluster entropy index of the volatility of each market is estimated by using eq. (10). Then the average index is calculated over the set of moving average values :

| (13) |

The quantity is a cumulative figure of diversity, a number suitable to quantify and compare information content in different markets. For each market and volatility windows the index estimated according to eq. (13) is normalized as follows:

| (14) |

to satisfy the condition . The quantities build the portfolio according to the probability of the riskiest assets in the case of high-risk propensity of the investor. Alternative estimates based on the cluster entropy index might be easily carried on for low-risk profiles.

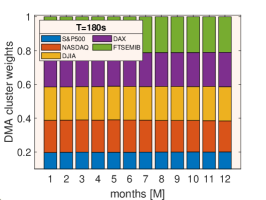

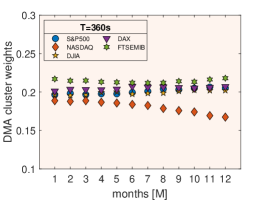

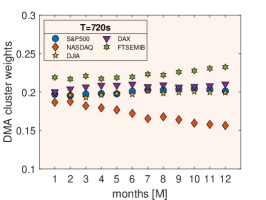

The weights are plotted in fig. 4 and fig. 5 for the five assets. At short horizons and small volatility windows , the weights take values close to as it would be expected by a uniform wealth allocation. The weights distribution, with values close to , is related to the low predictability degree of price series and associated risk (volatility) given the limited amount of data at short periods and volatility windows. As and increase, a less diversified weights distribution emerges consistently with the increased amount of information gathered along the widened temporal horizon. Further results of the portfolio weights according to cluster entropy model can be found in the Supplementary Material attached to this letter.

5 Conclusion

An innovative, dynamic and robust perspective of investment, based on the detrending moving average cluster entropy approach, is offered by a multi-period portfolio strategy that does not rely on the flawed assumptions of normal and stationary distribution of market data. The strategy is implemented on volatility of high-frequency market series (details in Table 1) over multiple consecutive horizons . The high degree of stability, diversity and reliability of the portfolio weights can be indeed appreciated by the results shown in fig. 4 and in fig. 5. A continuous set of values of portfolio weights with a smooth and sound dependence on the horizon can be observed. The entropy-based estimate of the portfolio is straightaway obtained from the stationary detrended distribution of the financial series rather than by using the unrealistic mean-variance hypothesis of Gaussian returns. At short volatility windows (e.g. in fig. 5), weights take values close to the equally distributed portfolio. These results are consistent with expected investment strategies where volatility (risk) does not give a prominent contribution. As increases, the volatility plays a relevant role in the weights estimate which deviates from the uniform distribution.

The proposed approach uses a stationary set of variables (i.e. the detrended cluster durations of the return and volatility series rather than non-stationary and not-normal variables as asset returns and volatility) [41, 42, 43, 44, 46, 45]. The basic drawbacks of the traditional mean-variance approach are thus removed at their roots. Clustering methods have demonstrated ability to obtain sound analysis of data with applications in various fields including portfolio strategies [51, 52, 53, 54, 55, 56, 57]. Our approach is based on the joint adoption of clustering and information measure. Several developments can be envisaged, as for example cluster entropy portfolio optimization based on the cross-correlation cluster distance measures and Kullback-Leibler entropy.

Acknowledgements.

P.M. acknowledges financial support from FuturICT 2.0 a FLAG-ERA Initiative within the Joint Transnational Calls 2016, Grant Number: JTC-2016-004References

- [1] Markowitz H. The Journal of Finance, 7, 1952, 77.

- [2] Evans J. L. Archer S. H.The Journal of Finance231968761.

- [3] Sharpe W. F.The Journal of Finance191964425.

- [4] Fernholz E. R. Stochastic portfolio theory (Springer) 2002 pp. 1–24.

- [5] Woerheide W. Persson D.Financial services review2199273.

- [6] Hakansson N. H.The Journal of Finance261971857.

- [7] Gressis N., Philippatos G. C. Hayya J.The Journal of Finance3119761115.

- [8] Boyd S., Busseti E., Diamond S., Kahn R. N., Nystrup P. Speth J. Foundations and Trends in Optimization320171.

- [9] Oprisor R. Kwon R.Journal of Risk and Financial Management1420213.

- [10] DeMiguel V., Garlappi L. Uppal R.The Review of Financial Studies2220091915.

- [11] Fletcher J.International Review of Financial Analysis202011375.

- [12] Frahm G. Wiechers C. A diversification measure for portfolios of risky assets in Advances in Financial Risk Management (Springer) 2013 pp. 312–330.

- [13] Raberto M., Cincotti S., Focardi S. M. Marchesi M.Physica A: Statistical Mechanics and its Applications2992001319.

- [14] Di Matteo T., Aste T. Dacorogna M. M.Physica A: Statistical Mechanics and its Applications3242003183.

- [15] Yamasaki K., Muchnik L., Havlin S., Bunde A. Stanley H. E. Proceedings of the National Academy of Sciences10220059424.

- [16] Yakovenko V. M. Rosser Jr J. B.Reviews of modern physics8120091703.

- [17] Chakraborti A., Toke I. M., Patriarca M. Abergel F. Quantitative Finance112011991.

- [18] Carbone A., Kaniadakis G. Scarfone A. M.The European Physical Journal B572007121.

- [19] Kwapien J. Drozdz S.Physics Reports5152012115.

- [20] Sornette D. Why stock markets crash: critical events in complex financial systems Vol. 49 (Princeton University Press) 2017.

- [21] Backus D., Chernov M. Zin S.The Journal of Finance69201451.

- [22] Ghosh A., Julliard C. Taylor A. P.The Review of Financial Studies302017442.

- [23] Philippatos G. C. Wilson C. J.Applied Economics41972209.

- [24] Ou J.The Journal of Risk Finance6200531.

- [25] Bera A. K. Park S. Y.Econometric Reviews272008484.

- [26] Ormos M. Zibriczky D.PLoS ONE92014e115742.

- [27] Batra L. Taneja H.Communications in Statistics-Theory and Methods20201.

- [28] Lim T. Ong C. S.The Journal of Financial Data Science2020.

- [29] Simonelli M. R.European Journal of Operational Research1632005170.

- [30] Zhou R., Cai R. Tong G.Entropy1520134909.

- [31] Zhou R., Wang X., Dong X. Zong Z.Advances in Information Sciences and Service Sciences52013833.

- [32] Meucci A. Risk and asset allocation (Springer Science & Business Media) 2009.

- [33] Meucci A. Nicolosi M.Applied Mathematics and Computation2742016495.

- [34] Kirchner U. Zunckel C.arXiv preprint arXiv:1102.47222011.

- [35] Vermorken M. A., Medda F. R. Schroder T.The Journal of Portfolio Management39201267.

- [36] Yu J.-R., Lee W.-Y. Chiou W.-J. P.Applied Mathematics and Computation241201447.

- [37] Pola G.Journal of Asset Management172016218.

- [38] Contreras J., Rodriguez Y. E. Sosa A.Energy Economics642017286.

- [39] Bekiros S., Nguyen D. K., J. L. S. Uddin G. S.European Journal of Operational Research2562017945.

- [40] Chen X., Tian Y. Zhao R.PLoS ONE122017e0183194.

- [41] Carbone A., Castelli G. Stanley H. E.Physical Review E692004026105.

- [42] Carbone A. Stanley H. E.Physica A: Statistical Mechanics and its Applications384200721.

- [43] Carbone A.Scientific Reports320132721.

- [44] Ponta L. Carbone A.Physica A: Statistical Mechanics and its Applications5102018132 .

- [45] Ponta L., Murialdo P. Carbone A.Physica A: Statistical Mechanics and its Applications2021125777.

- [46] Murialdo P., Ponta L. Carbone A.Entropy222020634.

- [47] Arianos S., Carbone A. Turk C.Physical Review E842011046113.

- [48] Carbone A. Kiyono K.Physical Review E932016063309.

- [49] Carbone A. Castelli G. Scaling properties of long-range correlated noisy signals: Appplication to financial markets SPIE’s First International Symposium on Fluctuations and Noise (International Society for Optics and Photonics) 2003 406–414.

- [50] Rak R., Drozdz S., Kwapien J. Oswiecimka P. EPL Europhysics Letters112201548001.

- [51] Duran B. S. Odell P. L. Cluster analysis: a survey (Springer Science Business Media) 100 2013.

- [52] Aghabozorgi S., Shirkhorshidi A. S. Wah T. Y.Information Systems53201516.

- [53] Iorio C., Frasso G., D’Ambrosio A. Siciliano R.Expert Systems with Applications95201888.

- [54] Puerto J., Rodriguez-Madrena M. Scozzari A.Computers & Operations Research1172020104891.

- [55] Tayali S. T.Knowledge-Based Systems2092020106454.

- [56] Tola V., Lillo F., Gallegati M. Mantegna R. N.Journal of Economic Dynamics and Control322008235.

- [57] Massahi M., Mahootchi M. Khamseh A. A.Empirical Economics20201.