A central limit theorem for the Benjamini-Hochberg false discovery proportion under a factor model ††thanks: This article will appear in Bernoulli. While there are formatting differences, the main text of this arXiv submission should be exactly the same as the version that will appear in Bernoulli.

Abstract

The Benjamini-Hochberg (BH) procedure remains widely popular despite having limited theoretical guarantees in the commonly encountered scenario of correlated test statistics. Of particular concern is the possibility that the method could exhibit bursty behavior, meaning that it might typically yield no false discoveries while occasionally yielding both a large number of false discoveries and a false discovery proportion (FDP) that far exceeds its own well controlled mean. In this paper, we investigate which test statistic correlation structures lead to bursty behavior and which ones lead to well controlled FDPs. To this end, we develop a central limit theorem for the FDP in a multiple testing setup where the test statistic correlations can be either short-range or long-range as well as either weak or strong. The theorem and our simulations from a data-driven factor model suggest that the BH procedure exhibits severe burstiness when the test statistics have many strong, long-range correlations, but does not otherwise.

keywords:

[class=MSC2020] Primary 62J15 ; secondary 60F17keywords:

\kwd@sepEmpirical cumulative distribution function ; functional central limit theorem ; functional delta method ; multiple hypothesis testing ; Simes linecondition

,\safe@setrefAthanksADepartment of Statistics, Stanford University, Stanford, CA, USA . \safe@setrefe1@; \safe@setrefe2@

1 Introduction

The Benjamini-Hochberg (BH) procedure is a widely used method for balancing Type I and Type II errors when testing many hypotheses simultaneously. The procedure is designed to control the False Discovery Rate (FDR), which is the expected value of the proportion of discoveries that are false (FDP), below a user specified threshold (Benjamini and Hochberg (1995)). The procedure was originally shown to guarantee FDR control when the test statistics are assumed to be independent, an assumption unlikely to hold in most application settings. The BH procedure was later proven in Benjamini and Yekutieli (2001) to control the FDR when there are dependent test statistics satisfying the Positive Regression Dependency (PRDS) property. While PRDS is quite restrictive (for example, it does not hold for two-sided hypothesis tests when the test statistics are correlated or when there are negatively correlated test statistics (Fithian and Lei (2020))), under more general conditions simulation studies have found BH to conservatively control the FDR (Farcomeni (2006), Kim and van de Wiel (2008)).

While FDR control is important, the motivation for this paper is our concern that FDR control alone can give investigators who use BH false confidence in a low prevalence of false discoveries among their rejected hypothesis. This can happen if the distribution of the FDP has both a wide right tail and a mean that is still below the user specified threshold. As an example, it would be worrisome in the plausible scenario that an investigator is led to believe that roughly 10 percent of their discoveries are false, when in fact, a majority of them are false. To address such concerns, a number of multiple testing procedures have been proposed to control the tail probability that the FDP exceeds a user specified threshold (Korn et al. (2004), Romano and Shaikh (2006), Romano and Wolf (2007)). Efron (2007) also raised concerns about high variability of FDP due to correlations of the test statistics and proposed an empirical Bayes approach for estimating a dispersion parameter of the test statistics and controlling FDR conditionally on the dispersion parameter. Despite the promise of these methods, the BH procedure remains overwhelmingly popular and the default method of choice for investigators with multiple testing problems. It is therefore important to determine under which conditions are we assured that the distribution of the FDP will be well concentrated about its mean, the FDR, and under which conditions there is a risk that the distribution of the FDP has a wide right tail. Throughout this text we will refer to the former scenario with low variability of the FDP about its mean as the non-bursty regime, and the alarming, latter scenario where occasionally the FDP is much larger than expected as the bursty regime.

While previous simulations in the literature can be used to identify some settings where the BH procedure will exhibit burstiness (see for example, Figure 5 of Friguet, Kloareg and Causeur (2009) or Figure 1 of Delattre and Roquain (2015)), the aim of this paper is to gain a theoretical understanding of when burstiness is a concern for BH. We identify dependency structures among test statistics that in conjunction with certain proportions of nonnulls make BH prone to delivering bursts of false discoveries. We find other settings where such bursts must be rare. Our results are asymptotic and hold in a two-group mixture model previously studied by Genovese and Wasserman (2004), Delattre and Roquain (2016) and Izmirlian (2020). In that model, independent variables define which hypotheses are nonnull, the null -values have the distribution and the nonnull -values have some other distribution in common.

The BH procedure and the asymptotic distribution of the FDP is well studied for the setting where the test statistics are independent. Finner and Roters (2001); Finner and Roters (2002) study properties of the number of false discoveries under independence both when there are no nonnulls and when the nonnull -values are always . The limiting distribution of the FDP was studied by Genovese and Wasserman (2004) under independence of the test statistics; however, their asymptotic FDP results are derived for the “plug-in" method (Benjamini and Hochberg (2000)) rather than the standard BH procedure. To our knowledge, a CLT for the FDP of the BH procedure itself was first explicitly stated in Neuvial (2008), which uses a functional delta method argument. Izmirlian (2020), using a CLT for a randomly stopped process, provides a simpler proof of a CLT for the FDP and corrects an error in Neuvial’s asymptotic variance formula. These works show that in the two group mixture model with Bernoulli parameter and with hypotheses to test, when using the BH procedure at FDR control level , converges as to a centered Gaussian with variance that depends on , , and the common nonnull -value distribution.

There are fewer results on the limiting distribution of the FDP for dependent test statistics. Farcomeni (2007) derives a CLT for the FDP of the plug-in procedure when the -values are stationary and satisfy some mixing conditions but for brevity omits explicitly stated FDP CLTs for the standard BH procedure. Using the proof methodology of Neuvial (2008), Delattre and Roquain (2011) derive a CLT for the FDP of the BH procedure for one sided testing, when the test statistics follow an equicorrelated Gaussian model, with correlation parameter as the number of tests . Delattre and Roquain (2016) extend this result to settings where the Gaussian test statistics follow arbitrary dependence structures but the average pairwise correlation of the test statistics, and the average 2nd and 4th powers of the pairwise correlations of the test statistics satisfy some constraints.

In Delattre and Roquain (2016), CLTs for the FDP are derived under two distinct regimes. In their first regime, the average pairwise correlation among test statistics is strictly greater than for tests. Under this regime, the FDP is not -consistent for the product of the FDR control parameter with the limiting proportion of nulls, and the FDP only converges to a Gaussian with scale factors much smaller than . Their other regime considered has an average correlation among test statistics that is at most . For this regime Delattre and Roquain (2016) derive a CLT for the FDP with scaling, but they require a restrictive assumption which they call “vanishing-second order", precluding settings where there are short-range correlations of constant order. Examples of test statistic correlation matrices to which Delattre and Roquain (2016) will not apply include tridiagonal Toeplitz correlation matrices as well as block correlation matrices of constant block size, both of which are simple models of interest for studying multiple testing under dependence.

With the aim of identifying dependency structures for which the investigator should be concerned about bursty behavior of the BH procedure, in this paper, we introduce a model that allows for a combination of long-range and potentially strong dependence among the test statistics via a factor model, along with additional strongly-mixing noise that has rapidly decaying long-range dependence. The model also allows for the proportion of nonnulls among the hypothesis tests to vary as a function of . Under some regularity conditions on the factor model and on the noise with rapidly decaying long-range dependence, we prove a CLT for the FDP under more general conditions than prior CLTs. We also establish a CLT for the False Positive Ratio (FPR), which is the proportion of false discoveries among all tests conducted. The new CLTs hold conditionally on the realized latent variable of the factor model. Applying these new results, we make the following contributions to the literature of asymptotic results for the BH procedure:

-

1.

CLTs of the FDP for simple models, with short-range and constant-order dependency structures, that were not covered by the results of Delattre and Roquain (2016). Examples include block correlation structures with fixed block size and banded correlation structures. These results allow for non-stationary test statistics, so they cannot be inferred from theorems in Farcomeni (2007) either.

- 2.

-

3.

CLTs for the FPR rather than just the FDP because the FDP limiting behavior is unilluminating when it converges in probability to 1.

-

4.

CLTs where the expected proportion of nonnulls varies as the number of test statistics grows, allowing for a sparse allocation of nonnulls.

-

5.

A discussion of the dependency regimes under which the investigator should be concerned about BH having bursty behavior, such as the setting where the number of nonnulls is , and the dependency structure contains a factor model component.

To qualify point 2 above, we note that Delattre and Roquain (2016) include some CLTs for the FDP under long-range dependency that our theorems do not. Ours all have a scaling. They include some with a slower than scaling. For instance, they get such a CLT under an equicorrelated Gaussian model with correlation but . To clarify point 5 above, we characterize what causes alarming burstiness of the BH FDP when the test statistics are dependent, which to our knowledge has not been analyzed theoretically before. A separate issue is the pathologically low power of BH when the FDR control level is below a critical threshold (Chi, 2007). This issue was studied in greater generality by Zhang, Fan and Yu (2011) using the framework of Storey, Taylor and Siegmund (2004).

The proof of our main theorem builds upon the proof structure seen in Neuvial (2008) and Delattre and Roquain (2016). As is done in those works, we derive a functional CLT (FCLT) for the empirical cumulative distribution functions (ECDFs) of the null and nonnull -values, compute the Hadamard derivative of the FDP written as a functional of the two ECDFs, and apply the functional delta method to obtain a CLT for the FDP. While the proofs of previous FDP CLTs in the literature require establishing an FCLT for the -value ECDFs defined on , in Section 2.3.4, we define a focal interval , and our proof demonstrates that merely an FCLT for the ECDFs restricted to is needed. Our use of a focal interval allows us to obtain a CLT for the FDP in new settings where the null and nonnull -value ECDFs are poorly behaved asymptotically in either or . To obtain an FCLT when restricting our attention to , we use an FCLT from Andrews and Pollard (1994) for bounded function classes. The regularity conditions in Andrews and Pollard (1994) are conducive to obtaining an FCLT of the -value ECDFs in settings where the test statistics follow block or banded correlation structures (see point 1 above). Therefore, in addition to the contributions enumerated above, our use of a focal interval and our use of an FCLT from Andrews and Pollard (1994) are contributions to proof methodology for BH asymptotics.

Our results suggest that approaches which estimate and remove the factor model components from the test statistics prior to applying BH can alleviate burstiness issues. A number of such approaches for estimating and removing factor model components in multiple testing settings have been proposed and have shown promise in simulations (Friguet, Kloareg and Causeur, 2009; Sun, Zhang and Owen, 2012; Fan, Han and Gu, 2012; Wang et al., 2017; Fan et al., 2019). Our CLT for the BH method itself can be a useful step towards deriving CLTs for methods that first estimate and remove factor model components and subsequently apply BH.

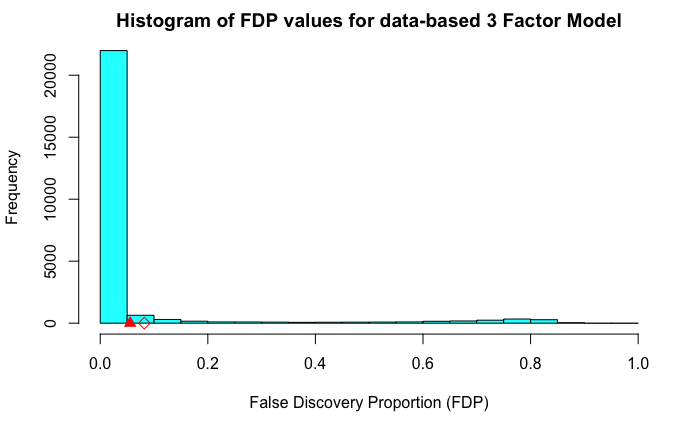

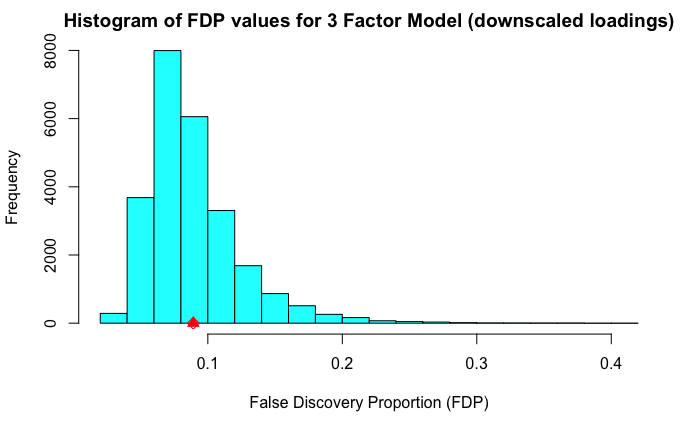

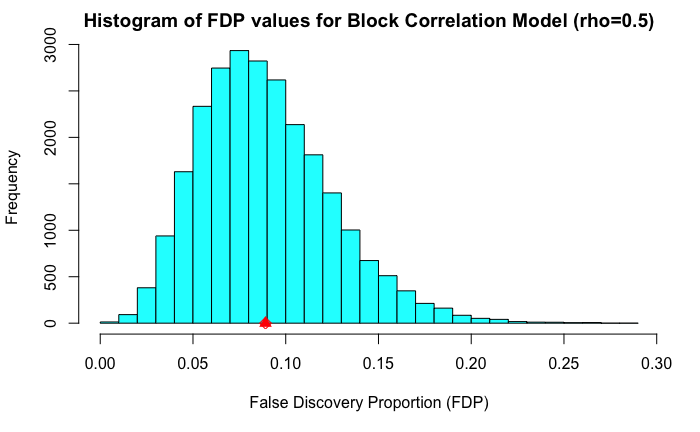

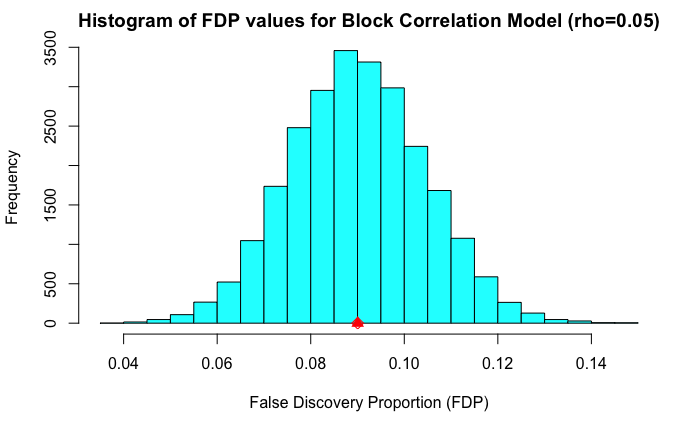

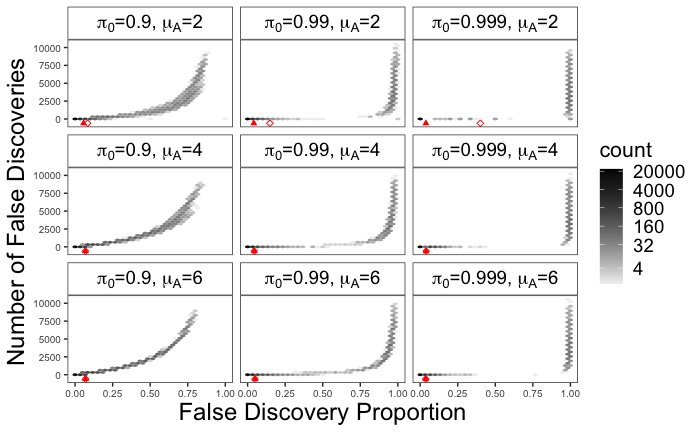

Figure 1 shows simulations of the FDP under some models that we study in this paper. In each case, there are Monte Carlo simulations. The BH procedure is used with on test statistics that are for null hypotheses and for alternative hypotheses. Each hypothesis is independently null with probability and nonnull otherwise. The models differ in the correlation among test statistics. For the first histogram, test statistics were sampled with correlations based on a -factor model fit to some Duchenne Muscular Dystrophy data described in Section 6. The second histogram is for the same correlation matrix after dividing the off-diagonal entries by . Next are two block correlation models with blocks of size and within-block correlations of or . To keep one of the blocks had only test statistics in it. In all four settings the FDR is seen to be controlled below , as desired. The positive False Discovery Rate (pFDR), defined as the expected value of the FDP conditional on there being at least one rejection, does not exceed in these simulations either. Of the four histograms, the one with data-driven correlations shows a long tailed distribution for FDP that we consider extremely bursty, the two with synthetic block correlations show FDPs that are typically quite close to the target FDR of , and the one with downscaled data-driven correlations is intermediate.

The organization of this paper is as follows. In Section 2, we describe our multiple testing setup and our model to account for both long-range correlations and short-range correlations among the test statistics. We also introduce our notation, definitions and the conditions under which our results hold. In Section 3, we state our most general CLTs for the FDP and FPR of the BH procedure. These hold conditionally on the common latent factors in our model. The proofs of these theorems are provided in the supplemental material. In Section 4, we exploit these theorems to obtain FDP CLTs (that are not conditional on a latent factor) for settings where the long-range dependence is rapidly decaying and no factor model component is needed to account for long-range dependencies. In Section 5, we exploit these theorems to obtain FDP and FPR CLTs conditional on the latent factor that give insight into the burstiness of the BH procedure, and we show that the burstiness of the BH procedure is particularly alarming when the test statistics follow a factor model and the number of nonnulls is sparse (for example, if the number of nonnulls is where is the number of hypotheses tested). In Section 6, we describe the Duchenne Muscular Dystrophy dataset and the 3-factor model that was fit to it, and we show simulations based on the fitted factor model. In Section 7, we discuss these results and their implications for multiple testing.

2 Setup and definitions

In this section we introduce our notation for the two-group mixture model. Our version relies on a factor analysis model that we also introduce. We also review the BH procedure and state our regularity conditions in this section.

2.1 Two-group mixture model with factors

Our setting has hypothesis tests indexed by and our asymptotics let . In a two-group mixture model, the marginal distribution of each of the -values is a mixture of a common null distribution and a common nonnull distribution, both of which do not depend on . For , let be an indicator variable with if and only if hypothesis of is nonnull. We take for .

Our two-group mixture model is thus based on a sequence of nonnull probabilities, and letting will let us model sparsity of nonnull hypotheses. For instance, with , the number of nonnulls has constant expectation and has an asymptotic Poisson distribution.

To focus on dependency among tests it is convenient to assume Gaussian test statistics for . In our two-group mixture model, the test statistics where the null holds have mean zero and the ones where the alternative hypothesis holds have common mean . We assume that where is multivariate Gaussian, and we induce dependence among our -values by introducing correlations among the . We briefly remark that the common nonnull mean assumption is not necessary for our theoretical results to hold, but is made for cleaner exposition, as our primary interest is in investigating how the dependency between the test statistics can drive bursty behavior.

We study two kinds of dependence operating simultaneously. One is an -mixing dependence that decays rapidly as the distance between hypothesis indices increases. This model captures some of the dependence one expects from hypotheses corresponding to a linearly ordered variable such as the position of a single nucleotide polymorphism (SNP) along the genome.

The other form of dependence we include is a factor model. Uses of factor models in multiple hypothesis testing include Friguet, Kloareg and Causeur (2009), Lucas, Kung and Chi (2010), Sun, Zhang and Owen (2012) and Gerard and Stephens (2020). A factor model can capture the dependency structure commonly seen among the test statistics in multiple testing problems involving gene expression data because it can capture important aspects of the correlation matrix of gene expression measurements. For example, Owen (2005) gives conditions where the correlation matrix for test statistics measuring association of a single phenotype with expression levels of genes is actually equal to the correlation matrix of the sampled gene measurements.

We construct the -factor model for the array as follows. We assume that the number of factors remains fixed as , as is assumed in Fan et al. (2019), among others. We let be the latent factor, which we suppose is only drawn once and does not change as . We let be a triangular array of fixed ‘loading’ vectors in . The factor model component of is . For our -mixing model with possibly strong short-range correlations but rapidly diminishing long-range correlations, we let be a sequence of covariance matrices and for each , we let independently of . To combine both dependency structures, we let , giving our correlation structure for the array .

We suppose that all of the test statistics have the same variance and without loss of generality, we take this common variance to be one. We do not assume the factor model to have a perfect fit, and assume instead that where for all . Because , these assumptions give along with the two kinds of dependency discussed above.

We let and denote the probability density function (PDF) and the cumulative distribution function (CDF), respectively, of and we let be the complementary CDF. Then our -values for one-sided hypothesis tests are

| (1) |

for , and so for the true null hypotheses. Fixing , throughout the text we will let , , , and denote the rejection threshold, the number of false discoveries, the FDP, and the FPR respectively when applying the Benjamini-Hochberg procedure at level to the -values . The formulas for these quantities are given explicitly in the next subsection, where we review the BH procedure. In our main theorems, we state CLTs for the quantities and conditionally on the value of the latent factor .

2.2 The BH procedure

In this subsection, we describe how the BH procedure is conducted at level on tests with -values . First take the sorted -values and set . The number of rejected hypothesis will be given by

| (2) |

The BH procedure rejects the hypotheses that correspond to the smallest -values: that is it will reject all hypothesis for which . As noted in Neuvial (2008), can equivalently be defined as the largest at which the empirical CDF (ECDF) of the -values is at least as large as . We leverage this equivalence in our theorem proofs.

2.3 Definitions and conditions

Here we present some definitions as well as regularity conditions sufficient for our conditional CLTs to hold. All of the definitions, conditions and formulas in this subsection are conditional on a fixed value of the latent factor .

2.3.1 Variance and mixing conditions on

Recall from our setup that for all , , allowing us to define for convenience. It is also helpful to introduce the following condition, which forces the variance of all terms to be bounded away from zero.

Condition 1.

.

Note about Condition 1:. recalling that in our model, this condition provides a uniform bound for all .

To describe the mixing condition on , for , define . Now let be the -field generated by the variables for and be the -field generated by the variables for . For integers our -mixing parameters are defined by

| (4) |

Condition 2.

There exists an even integer and such that both

Notes about Condition 2:. Throughout the text we will let , be such numbers. Note that it is possible that this condition can be loosened to allow to be rational, but then we need to trust a claim in Andrews and Pollard (1994) that their Theorem 2.2 would still hold for not an even integer.

Condition 2 will hold when the correlation between and is a rapidly decaying function of . If this correlation is always zero for each (making the error sequences -dependent for each ), Condition 2 will hold. In the following remark, we argue that Condition 2 will typically hold when is modelled by a stationary ARMA process or by a stationary GARCH process (a definition of these processes can be found in Paolella (2019), for example).

Remark 1.

Suppose that the standardized errors just depend on and not on . If can be modelled by a stationary ARMA model with absolutely continuous errors with respect to Lebesgue measure on , then Condition 2 will hold. To see this, note that by Theorem 1 in Mokkadem (1988), such a stationary ARMA process will be geometrically completely regular and hence the -mixing coefficients of will be for some . By independence of the and since , this implies that will hold for that same , further implying that Condition 2 will hold. By similar reasoning, if is modeled by a stationary GARCH process, Theorem 8 in Lindner (2009) implies that under certain conditions on the GARCH process errors, Condition 2 will hold.

2.3.2 Definitions of some subdistributions of -values and their condition

For any positive integer , define , and then write

Our subsequent definitions use for quantities based on the null hypotheses and for quantities from the nonnull hypotheses. For and let

We call and the empirical subdistribution functions of the null and nonnull -values respectively. These empirical subdistribution functions sum to the ECDF of the -values. Let be the monotone increasing bijection given by

We aggregate in the following subdistribution functions

and then let

| (5) |

Condition 3 ensures that these quantities are well defined.

Condition 3.

For all and , exists.

2.3.3 Defining the asymptotic ECDF and the Simes point

Now define via

| (6) |

for . Note that is the ECDF of the -values and is the limiting expected ECDF of the -values. Throughout the text we will refer to as the asymptotic ECDF because under most dependency structures, we expect to be the point-wise limit in probability of .

The rejection threshold for the BH procedure at level is the largest point such that the ECDF of the -values evaluated at lies above the line through the origin of slope , called the Simes line. It is reasonable to expect the limiting -value rejection threshold for the BH procedure at level to be the largest at which intersects the Simes line. We use the term Simes point to describe the largest point where the asymptotic ECDF intersects the Simes line. More precisely, the Simes point is

| (7) |

interpreting the supremum of the empty set to be zero. The Simes point satisfies . The upper limit follows from . Both and depend on the specific realization of latent factor on which we condition.

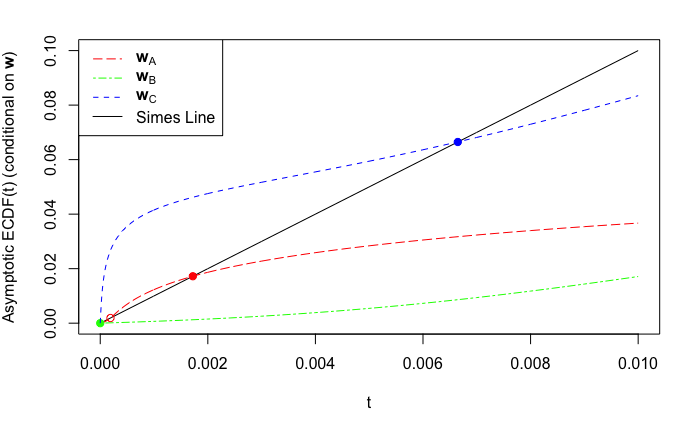

Figure 2 illustrates the Simes points. The setting has , and . The horizontal axis has putative -values over the range . The Simes line is . There are hypotheses corresponding to genes in the GDS 3027 Duchenne Muscular Dystrophy data described in Section 6. For three draws we show the asymptotic ECDF curves. One of them crosses the Simes line twice and the Simes point is the last crossing. One crosses it only once and one has Simes point because the Simes line is never crossed.

We will need continuity of on under Conditions 1 and 3. We do not know whether must be continuous at or , but our results do not depend on that.

-

Proof.

It is sufficient to show that is Lipschitz continuous on whenever . For any such , observe that for and integers

Now and then using Condition 1 it follows that for any ,

Since , for any . This argument holds for any and , and so for any and integer and ,

Taking the limit as of the left side of the above inequality, which exists by Condition 3, we get for all and for both . Thus, is Lipschitz continuous on for which implies is Lipschitz continuous on . ∎

2.3.4 Defining a focal interval for our processes

We are going to work with an interval of positive length for which the Simes point is the unique element with . First we need a technical condition to rule out some pathological behavior. Under this condition there will exist such an interval .

Condition 4.

The Simes point is positive, is the largest point where actually crosses the Simes line, and is not an accumulation point for points of intersection of and the Simes line. That is,

-

(i)

,

-

(ii)

, and

-

(iii)

is not an accumulation point of .

Note about Condition 4:. For many factor model choices, Condition 4 will hold with some probability in depending on the specific realization of . This is due to the dependence of and on the specific realization of the latent factor on which we condition. For example, see Figure 2.

Proposition 2.2.

-

(i)

, and

-

(ii)

the Simes point is the unique solving .

-

Proof.

Pick any and suppose that Conditions 1, 3, and 4 hold. By Condition 4,

Now because for all . Also, by continuity of (see Proposition 2.1). Hence, because but , there exists a sequence such that for all , and . Since does not have an accumulation point at and since is continuous, there is a sufficiently large with for all . We choose and then property (i) holds by our definition of . Also, because . Turning to property (ii), for all by the the choice of and , while for all , by the definition of . ∎

2.3.5 Defining our stochastic process and its Gaussian process limit

Our stochastic processes of interest are two jointly distributed random càdlàg functions on . We will show convergence to a pair of Gaussian processes with continuous sample paths on . The expressions and are both awkward, while denotes functions on a square region. Therefore, we use the symbol to denote and study random elements in and . Explicitly, is the collection of all pairs of real valued continuous functions on while is the collection of all pairs of real valued càdlàg functions on . We study the following processes in :

| (8) | ||||

We are ultimately interested in a functional central limit theorem (FCLT) for the joint process , so we must find the limiting joint covariance kernel of this pair of processes. To describe this limiting covariance kernel, we introduce some convenient definitions and notation.

For convenience, throughout the text we will define to be the sequence of correlation matrices corresponding to and, as before, for each define . Note that and that each has unit variance. For any and , define

| (9) |

Given a bivariate Gaussian with unit variance and correlation , the above quantity is the covariance between the indicator that the first coordinate of this bivariate Gaussian exceeds its quantile and the indicator that the second coordinate of this bivariate Gaussian exceeds its quantile.

Now for any and and define

It is convenient to break up the expression of into two terms. Define

and define

In the following proposition we show that .

Proposition 2.3.

For any and and

-

Proof.

For define

For , , and are all independent, so

When , and , so that

Since the above expressions hold for any ,

Now define

| (10) |

By the simplified formula for , the above limit exists by Condition 3 if we further impose Condition 5 below.

Condition 5.

For any and ,

both exist.

It is easy to see that the function defined above gives a joint covariance kernel that is symmetric and positive semidefinite because it is the limit of symmetric and positive semidefinite joint covariance kernels .

2.3.6 Regularity conditions on , , and

Before introducing the main theorems, we introduce another two conditions that will be used in their proof.

Condition 6.

Both and are differentiable at .

The final condition is needed to derive a FCLT from a FCLT. We would like to hold the subdistribution functions and constant as changes but this does not hold in all cases of interest. Instead we assume that they approach limits and at a fast rate.

Condition 7.

For , .

Notes about Condition 7:. As with all of the other conditions in Section 2.3, Condition 7 merely needs to hold for the fixed value of the latent factor on which we condition. In addition, a version of Theorem 3.1 below will still hold if we loosen Condition 7 to say that there exist Gaussian processes and on that are independent from the noise such that for both ,

This looser condition can be useful to study asymptotic behavior of the BH procedure in settings where the nonnull effect sizes are not constant and instead are assumed to come from some prior distribution. However, if we use this looser condition, the resulting theorem statement will be messier.

3 Statement of the theorems

Theorem 3.1.

-

Proof.

See the supplemental material for a proof of this theorem. ∎

The proof is quite long but to summarize we first derive an FCLT for the joint process by proving finite dimensional distribution convergence using a CLT from Neumann (2013) and then extend to an FCLT by using a result from Andrews and Pollard (1994). We then define to be a particular function satisfying with probability converging to as . Then we argue that is Hadamard differentiable at tangentially to and compute the Hadamard derivative by mimicking the approach in Neuvial (2008). To complete the proof of the CLT given in (11), we tie these results together with the functional delta method in Chapter 20.2 of van der Vaart (1998). Using the same proof technique we obtain the following conditional CLT for the ratio .

Theorem 3.2.

-

Proof.

See the supplemental material for a proof of this theorem. ∎

It is often the case that for a particular factor and noise model, Conditions 1–\totalcondition will not hold for all values of the latent factor . Condition 4 will often be violated when drawing . We do not expect a positive probability that will be an accumulation point of , nor do we expect a positive probability that , but we do expect a positive probability that . Therefore, in the next theorem we describe the asymptotic behavior of the BH procedure, conditional on when .

Theorem 3.3.

-

Proof.

See the supplemental material for a proof of this theorem. ∎

Remark 2.

Theorem 3.3 will still hold if we loosen the mixing Condition 2 and simply require that the error array has summable -mixing coefficients. This is because the proof of Proposition S.2.1 in the supplemental material (Kluger and Owen, 2023) does not require Condition 2 to hold and merely requires that the error array has summable -mixing coefficients.

Remark 3.

When and , it is not guaranteed that . For example, in the scenario where for all , the errors are independent and , one can show that and , yet . As another example, Gontscharuk and Finner (2013) provide a scenario where , but asymptotically the false discovery rate exceeds the FDR control parameter , implying that cannot possibly converge to zero in probability in their scenario.

In the above theorems, the limiting of behavior of BH depends on a latent factor which in practice is unobserved. Estimation of the unobserved latent factor is out of scope for this paper but for estimators of the latent factor and properties of these estimators we point the reader to Fan, Han and Gu (2012), Azriel and Schwartzman (2015), Sun, Zhang and Owen (2012), Wang et al. (2017) and Fan et al. (2019). In the next section we focus on results for the case where the correlations are short-range and there is no factor model or latent factor to consider.

4 Corollaries when there is no factor model component

The simplest applications of Theorems 3.1 and 3.2 are to settings where there is no factor model component. That is , or equivalently for . Then the test statistics are where for a correlation matrix . Next suppose, as is usual in the two-group mixture model that for all . Finally, we will assume that the errors satisfy mixing Condition 2, which can hold, for example, if the errors are -dependent (see Remark 1 for other examples where Condition 2 is met).

Many of the \totalcondition conditions in our theorems hold trivially in this setting. Most trivially, making Condition 1 hold. The mixing Condition 2 holds by assumption. Also in this setting, because and for each , Conditions 3 and 7 on the subdistributions can be seen to hold.

To check that Condition 4 ruling out pathologies about holds note that . A simple calculation shows that and

implying that is strictly concave on and that as . By strict concavity of , and since both and the Simes line intersect the origin, contains at most one point. It remains to show existence of a point with . Since as and , there must be an such that . Also , so the continuous function must cross at some unique . By continuity of and uniqueness this unique is the Simes point defined in (7) and further Condition 4 will be satisfied. Because and because and are differentiable on , Condition 6 also holds.

The only remaining condition to check is Condition 5 on convergence of the covariance kernels. Let be any open interval containing and . Since for , does not vary with or , the first limit in Condition 5 always holds. Since for each , and , Condition 5 holds whenever

| (18) |

exists for all with defined at (9). We summarize this along with an application of Theorem 3.1 in Corollary 4.1.

Corollary 4.1.

In the setting of Section 2.1, suppose further that:

-

i)

the factor loadings are all zero and

-

ii)

the probability of nonnull hypotheses does not depend on .

Let be the unique satisfying and let be any open interval containing both and . If the are such that mixing Condition 2 holds and the correlations among the are such that defined at (18) exists for all , then

| (19) |

where .

-

Proof.

As discussed before the statement of the corollary, Conditions 1–\totalcondition hold in this setting. Noting that in this setting and there is no dependency on the latent factor , the result holds by Theorem 3.1. ∎

We note that this corollary will hold even if and the requirement that was included for a cleaner proof of Theorem 3.1.

We also note that if the correlations between the test statistics are known, or even if only the first few moments of the test statistic pairwise correlations are known, the quantity can be computed efficiently using the first few terms in a Hermite polynomial expansion, as seen in Theorem 2 of Schwartzman and Lin (2011). Below, we specialize Corollary 4.1 to settings with block diagonal correlations and with Toeplitz correlations. In these settings, Condition 2 will hold and will have an easily-expressed formula.

Corollary 4.2 (Block diagonal correlations).

-

Proof.

This follows from a direct application of Corollary 4.1. ∎

The corollary as written requires to be a multiple of , but it extends easily to through an arbitrary sequence of . One can let the “last" block be smaller than the others if necessary.

Another simple correlation structure we can consider has banded Toeplitz correlation matrices for .

Corollary 4.3 (Toeplitz correlation).

-

Proof.

This follows from a direct application of Corollary 4.1. ∎

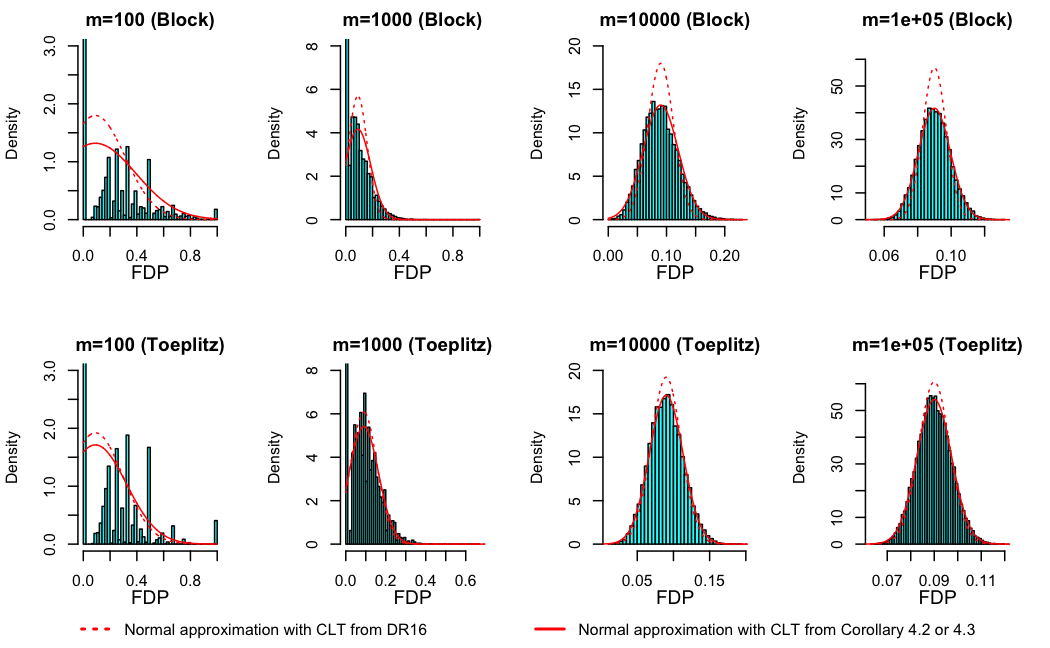

We check the CLTs provided by Corollaries 4.2 and 4.3 via simulation in Figure 3. We compare the normal approximation given by these CLTs to the normal approximation given by Corollary 4.2 in Delattre and Roquain (2016). We simulate block and banded correlation structures that do not satisfy the sufficient conditions in their Corollary 4.2.

For each correlation structure and each , we ran Monte Carlo simulations with , , and . The block correlation matrices we considered had block size , and within block correlations . The banded Toeplitz correlation matrix had with above and below the diagonal and two rows above and below the diagonal. Our normal approximation fits very well for the larger values of . For large the normal approximation from Delattre and Roquain (2016) appears to accurately estimate the mean but not the variance of the FDP. From this we believe that something in their sufficient conditions must also have been necessary.

5 Burstiness in a factor model

The results in the previous section are CLTs that do not require conditioning on the latent factor as they assumed no long-range correlations modeled via a factor model. The CLTs are messier when factor model components are introduced, so we present two examples for factor model settings where the formulas for the asymptotic distribution of the FDP have some simplifications.

5.1 -factor model for long-range equicorrelated Gaussian noise

Suppose that for each , for a fixed , but we now have a one dimensional latent factor; that is . For simplicity, we consider the simplest factor model structure: an equicorrelated Gaussian model. In particular, we let where for all . We will also allow for errors with shorter range correlations to be added to the model by supposing that where is a correlation matrix with blocks of size and off diagonal within-block correlations of . We assume that the blocks are of equal size, except the last one if does not divide . In this model the test statistics are and the correlation structure of the errors (not related to the indicators of whether the hypotheses are true) follows a matrix where

In such a setting it is easy to show that all of our conditions, except possibly Condition 4 will hold. Condition 4 ruling out pathologies involving will hold depending on the value of drawn from . Some may give though we do not expect a positive probability that will be an accumulation point of .

Corollary 5.1.

In the multiple hypothesis testing setting of Section 5.1, condition on and for let with for . If is such that satisfies Condition 4 that the Simes point is positive with no pathologies, then

where and

- Proof.

Remark 4.

In the setting of Corollary 5.1, if is small, then perhaps the test statistic correlations can be modeled with a factor model with a bit more than factors but asymptotically such an approach would require adding infinitely many factors in the model. In our setup, the equicorrelations are long-range and persist as and hence they are modeled with a factor model whereas the additional noise with correlation blocks of size involves short-range correlations and are therefore not modeled as a factor.

In this subsection, we have demonstrated that Theorems 3.1 and 3.2 can be used to provide further insight into asymptotics of the BH procedure in the setting of Gaussian test statistics with constant pairwise correlation. In such a setting, Finner, Dickhaus and Roters (2007) find the limiting expected values of both the FDP and the FPR as functions of a one-dimensional latent factor. We have extended their results by deriving the limiting distribution of the FDP as a function of a one-dimensional latent factor (the limiting distribution of the FPR can similarly be derived from Theorem 3.2). We also considered a more general setting than the equicorrelated Gaussian model in order to exhibit that Theorems 3.1 and 3.2 can handle settings with both short and long-range correlations simultaneously.

5.2 Setting where number of nonnulls is

Here we consider sparse nonnulls with . It can be shown with a Chernoff bound for the binomial that in this case the number of nonnulls is . Also suppose that under the model for test statistics of Section 2.1, Conditions 1-\totalcondition hold. Then it will follow that and moreover . If this is the case, then we will have , , and .

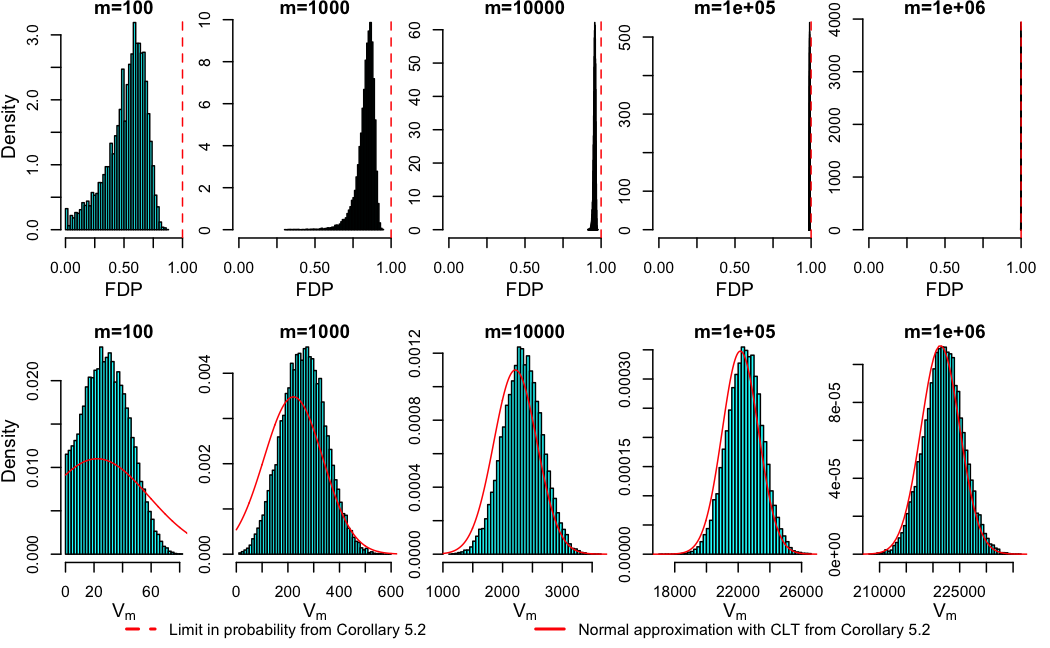

Corollary 5.2.

Suppose that we are in the multiple testing setting of Section 2.1 and that . If, conditionally on a specific value of the latent factor , Conditions 1-\totalcondition hold, then

and

where

The corollary indicates that severe bursts can occur; can converge to a positive number even while the proportion of hypotheses that are nonnull converges to 0.

We check the result of Corollary 5.2 via simulation in Figure 4. We simulate from the 1-factor model described in Section 5.1, except now the proportion of nonnulls is not fixed in . Instead we set . For each , we conditioned on and ran Monte Carlo simulations with , , , , and . For these choices of parameters, the conditions of Corollary 5.2 are met.

6 Data driven factor model example

We fit a 3-factor model to the GDS 3027 Duchenne Muscular Dystrophy (DMD) data, which can be found on the Gene Expression Omnibus. This data set was analyzed in Kotelnikova et al. (2012) and Wang et al. (2022) and had genes and subjects. Of these subjects 23 had DMD and 14 did not. We centered the data for each gene and stored it in a matrix . To fit a homoskedastic factor model, we looked at the plot of the singular values of and chose to work with the largest three of them for illustrative purposes. We then computed , the singular value decomposition-based rank approximation to , and estimated the homoskedastic noise, as the standard deviation of the entries in . We let be the matrix whose columns consist of the first 3 right singular vectors of scaled by their corresponding singular values. We subsequently treat and as fixed quantities and then assume the following factor model under the global null: , where the entries of and are IID standard Gaussians. Under the alternative we suppose that for each nonnull gene, the values of for that gene are shifted by a fixed constant for DMD subjects and a different fixed constant, maintaining centering of the columns of , for the control subjects.

Since the dataset is from a case-control study, to compute the test statistics we condition on DMD status and assume that the stochasticity in our observations comes from the random matrices and . The unstandardized test statistics are simply the difference-in-means between the DMD group and the control group for each gene and this unstandardized test statistics vector has covariance matrix proportional to . The standardized test statistics are given by dividing each entry of by the squareroot of the corresponding diagonal entry of . The vector of test statistics then satisfy where is a vector of constant means (which are zero for the null genes), is a matrix of factor loadings similar to but with appropriately rescaled rows, and is heteroskedastic, independent, and centered Gaussian noise. Assuming that each standardized nonnull test statistic has the same mean , that we conduct one-sided testing, and that the nonnulls are determined by IID draws, using the test statistics we are in the multiple hypothesis testing setting of Section 2.1.

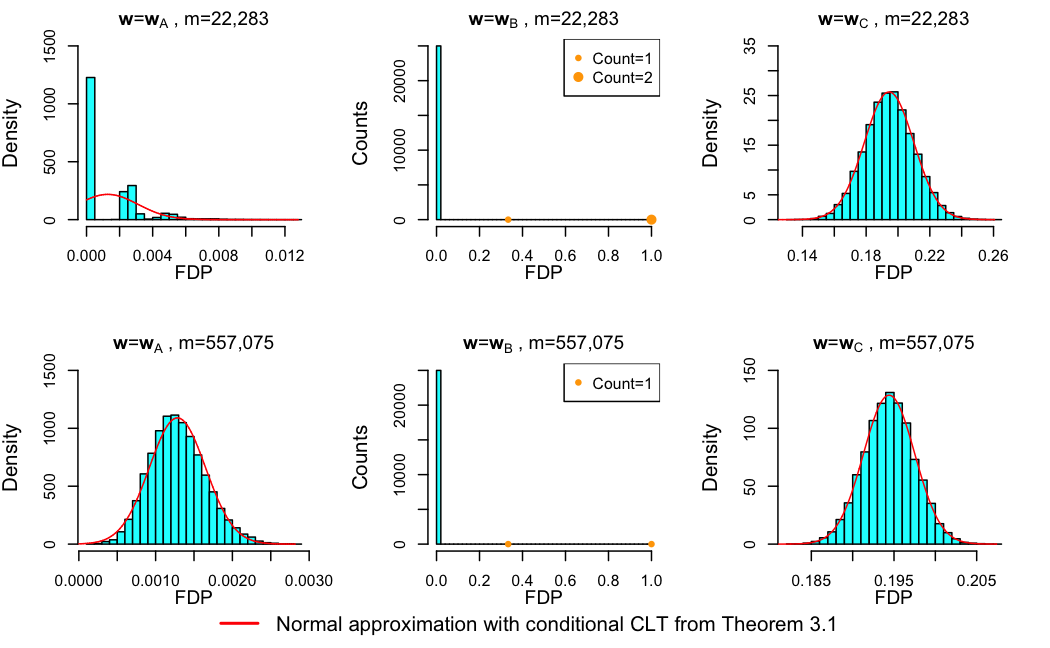

Figure 2 in Section 2 shows the asymptotic ECDF of the -values for three specific realizations of the latent factor in the data-driven 3-factor model and multiple testing setting described above, with , , and . Figure 5 shows histograms of the FDP based on Monte Carlo simulations for the same data-driven 3-factor model, multiple testing setup, factor outcomes, and parameters as Figure 2.

In the top panel of Figure 5, as is the case in the original 3-factor model fit to the GDS 3027 dataset. In the bottom panel, to increase the number of tests and check asymptotic behavior, we copy each row of factor loadings in the original factor model times to get a distribution of the FDP when tests are conducted. That is much larger than we would need for gene expression and approaches the range we would encounter for SNPs. In case A, the CLT is reasonable for the larger but not the smaller sample size. The CLT fits well for both sample sizes for case C. In case B, the sufficient conditions for the conditional CLT do not hold and Theorem 3.3 holds instead.

This simulation shows some bursty behavior for BH as follows. Cases A and C are both covered by the conditional CLT and there we see that even in cases covered by the conditional CLT, the FDP can vary greatly, being nearly Gaussian with means varying by nearly 100-fold. When cases like case B arise there is no conditional CLT, and by Theorem 3.3, the BH rejection threshold converges to in probability. In case B, we observe a very heavy tail to the FDP distribution, although fewer than 1 out of every Monte Carlo simulations yields a nonzero FDP, and no simulation yields more than 1 false discovery. In conclusion, the simulations are consistent with the results of Theorems 3.1 and 3.3.

A large FDP tail is not necessarily indicative of alarming bursty behavior for BH, as the FDP can be equal to in scenarios where there is only one false discovery. Looking at the FDP simultaneously with the number of false discoveries gives a clearer sense of whether the bursty behavior is alarming. In Figure 6, we run Monte Carlo simulations using the previously described data-driven 3-factor model. In contrast to Figure 5, we do not condition on specific realizations of the latent factor and we also plot the joint distribution of the FDP and the number of false discoveries rather than the marginal distribution of the FDP. In the simulations, we set the FDR control parameter and repeat the simulations for the nonnull effect size and for Bernoulli mixture null parameter .

Remark 5.

Controlling pFDR using Storey’s -value is another popular multiple testing approach that is heralded for avoiding floods of false positives (Storey and Tibshirani (2003)). Our simulations show that when the nonnull effect sizes are small and the number of nonnulls is sparse the pFDR will be high, implying that controlling the pFDR would mitigate the issue of burstiness in such cases. When there are many nonnulls or when the nonnull effect sizes are large, the pFDR is nearly equal to the FDR (due to few simulations with no discoveries), implying that controlling the pFDR would not mitigate burstiness in such cases.

Remark 6.

For the data-driven 3-factor model with , the distribution of is largely driven by the realization of the latent factor . This can be seen in the top panel of Figure 5, and we further quantified this by running Monte Carlo simulations from the model for each of different randomly generated latent factor vectors. The variance of the FDP between groups with different latent factors was approximately times larger than the average variance within each latent factor vector group.

7 Discussion

Here we discuss the conclusions that can be drawn from our theorems and simulations about when BH exhibits alarming burstiness and when BH is safe from burstiness concerns. We end with a discussion of the relevance and feasibility of factor model-based corrections for addressing burstiness concerns.

Burstiness occurs when there are many strong, long-range correlations between the test statistics. When we model the long-range correlations via a factor model, this phenomenon can be explained by Theorem 3.1. By Theorem 3.1, the asymptotic limit of is , a quantity that can vary drastically for different realizations of . The variation in is greater when the long-range correlations are stronger (or equivalently, when the factor model loading vectors have larger magnitude). Therefore, the FDP has high variability when there are many strong, long-range correlations between the test statistics. Meanwhile, by Theorem 3.2, there could be a flood of false discoveries, making the bursts severe. Our simulations from the 3-factor model fit to the DMD dataset indicate a wide right tail of the FDP distribution as well as severe bursts (see the top-left panel of Figure 1 and Figure 6). Notably, we find that sparsity of the number of nonnulls exacerbates burstiness issues. This can be explained by Corollary 5.2 and is observed in Figures 4 and 6.

Conversely, our theorems and simulations indicate that there are many settings where the test statistics are correlated, but the BH procedure is free of burstiness concerns. When there are no long-range correlations, no factor model is needed to model the correlations, so the variance of the FDP will decrease rapidly as the number of tests increases, even when the short-range correlations are strong. For example, in the setting of Corollary 4.1, converges to a quantity less than the desired FDR control and has variance of order , even with strong short-range correlations. The simulations in the bottom of Figure 1 and all the panels of Figure 3 involve strong short-range correlations and still demonstrate this desirable behavior (the desirable behavior is not seen in the panels of Figure 3 where is small because, in that case, the “short-range" correlations are actually long-range relative to the number of tests). Even when there are long-range correlations but the long-range correlations are weak, modeled by a factor model with loading vectors of small magnitude, the BH procedure will not exhibit worrisome bursts. With loading vectors with small magnitude, the terms will not be sensitive to the realized value of , and in turn and will also not be so sensitive to the realized value of . Therefore, when the loading vectors have small magnitude, the asymptotic limit of given in Theorem 3.1 will not oscillate much as varies. Indeed, in Figure 1, when the long-range correlations are all reduced by a factor of 10 (as we move from the top-left panel to the top-right panel), alarming burstiness is no longer observed.

These results suggest that estimating the correlation structure with a factor model can be useful for identifying whether or not burstiness is a concern in particular applications. The results further suggest that methods which estimate and remove the factor model components from the test statistics prior to applying BH (e.g. methods that estimate and , subtract from each test statistic, and subsequently apply BH) can alleviate burstiness issues. A number of such approaches for estimating and removing factor model components in multiple testing settings have been proposed and have shown promise in simulations (Friguet, Kloareg and Causeur, 2009; Sun, Zhang and Owen, 2012; Fan, Han and Gu, 2012; Wang et al., 2017; Fan et al., 2019).

While a full discussion of these recent methods is out of scope for this paper, we briefly note that there are two major challenges with estimation and removal of factor model components in a multiple testing setting. First, it is possible that removing the factor model components from the test statistics might remove some of the important signal that one is trying to detect with hypothesis testing. For example, this can happen if a large collection of genes is associated with one of the leading factors, yet at the same time, that collection of genes is also associated with the outcome variable. To avoid such issues, methods which remove the factor model components often rely upon an assumption that the number of nonnulls is sparse. Second, estimating the underlying factor model for a dataset is statistically challenging. It is difficult to estimate the latent factors and the factor loadings well without a large number of samples, and even choosing the number of latent factors is a difficult task. For a comparison of methods for estimating the number of latent factors, see Owen and Wang (2016).

Acknowledgments

The authors wish to thank Will Fithian, Kevin Guo, Grant Izmirlian, Lihua Lei, Kenneth Tay, Marius Tirlea, Jingshu Wang, and anonymous reviewers for helpful comments and discussions. The authors also thank Kevin Guo for a proof sketch on how to remove a condition from an earlier version of this paper and Jingshu Wang for sharing the DMD data. Finally, the authors would like to thank two anonymous referees, an Associate Editor and the Editor for their constructive comments that helped improve the quality of this paper.

Funding

DMK was supported by a Stanford Graduate Fellowship and a Stanford Graduate Interdisciplinary Fellowship. ABO was supported by the National Science Foundation under grants IIS-1837931 and DMS-2152780.

References

- Andrews and Pollard (1994) Andrews, D. W. K. and Pollard, D. (1994). An Introduction to Functional Central Limit Theorems for Dependent Stochastic Processes. Int. Stat. Rev. 62 119–132.

- Azriel and Schwartzman (2015) Azriel, D. and Schwartzman, A. (2015). The Empirical Distribution of a Large Number of Correlated Normal Variables. J. Amer. Statist. Assoc. 110 1217–1228.

- Benjamini and Hochberg (1995) Benjamini, Y. and Hochberg, Y. (1995). Controlling the False Discovery Rate: A Practical and Powerful Approach to Multiple Testing. J. R. Stat. Soc. Ser. B. Stat. Methodol. 57 289–300.

- Benjamini and Hochberg (2000) Benjamini, Y. and Hochberg, Y. (2000). On the Adaptive Control of the False Discovery Rate in Multiple Testing With Independent Statistics. J. Behav. Educ. Statist. 25 60–83.

- Benjamini and Yekutieli (2001) Benjamini, Y. and Yekutieli, D. (2001). The control of the False Discovery Rate in Multiple Testing Under Dependency. Ann. Statist. 29 1165–1188.

- Chi (2007) Chi, Z. (2007). On the performance of FDR control: Constraints and a partial solution. Ann. Statist. 35 1409 – 1431.

- Delattre and Roquain (2011) Delattre, S. and Roquain, E. (2011). On the false discovery proportion convergence under Gaussian equi-correlation. Statist. Probab. Lett. 81 111–115.

- Delattre and Roquain (2015) Delattre, S. and Roquain, E. (2015). New procedures controlling the false discovery proportion via Romano–Wolf’s heuristic. Ann. Statist. 43 1141 – 1177.

- Delattre and Roquain (2016) Delattre, S. and Roquain, E. (2016). On empirical distribution function of high-dimensional Gaussian vector components with an application to multiple testing. Bernoulli 22 302–324.

- Dudley (1999) Dudley, R. M. (1999). Uniform Central Limit Theorems. Cambridge Studies in Advanced Mathematics 1, 1–22. Cambridge University Press.

- Efron (2007) Efron, B. (2007). Correlation and Large-Scale Simultaneous Significance Testing. J. Amer. Statist. Assoc. 102 93-103.

- Fan, Han and Gu (2012) Fan, J., Han, X. and Gu, W. (2012). Estimating False Discovery Proportion Under Arbitrary Covariance Dependence. J. Amer. Statist. Assoc. 107 1019-1035.

- Fan et al. (2019) Fan, J., Ke, Y., Sun, Q. and Zhou, W.-X. (2019). FarmTest: Factor-Adjusted Robust Multiple Testing With Approximate False Discovery Control. J. Amer. Statist. Assoc. 114 1880-1893.

- Farcomeni (2006) Farcomeni, A. (2006). More powerful control of the false discovery rate under dependence. Stat. Methods Appl. 15 43–73.

- Farcomeni (2007) Farcomeni, A. (2007). Some Results on the Control of the False Discovery Rate under Dependence. Scand. J. Stat. 34 275–297.

- Finner, Dickhaus and Roters (2007) Finner, H., Dickhaus, T. and Roters, M. (2007). Dependency and false discovery rate: Asymptotics. Ann. Statist. 35 1432 – 1455.

- Finner and Roters (2001) Finner, H. and Roters, M. (2001). On the False Discovery Rate and Expected Type I Errors. Biom. J. 43 985-1005.

- Finner and Roters (2002) Finner, H. and Roters, M. (2002). Multiple hypotheses testing and expected number of type I. errors. Ann. Statist. 30 220 – 238.

- Fithian and Lei (2020) Fithian, W. and Lei, L. (2020). Conditional calibration for false discovery rate control under dependence.

- Friguet, Kloareg and Causeur (2009) Friguet, C., Kloareg, M. and Causeur, D. (2009). A factor model approach to multiple testing under dependence. J. Amer. Statist. Assoc. 104 1406-1415.

- Genovese and Wasserman (2004) Genovese, C. and Wasserman, L. (2004). A Stochastic Process Approach to False Discovery Control. Ann. Statist. 32 1035–1061.

- Gerard and Stephens (2020) Gerard, D. and Stephens, M. (2020). Empirical Bayes shrinkage and false discovery rate estimation, allowing for unwanted variation. Biostatistics 21 15–32.

- Gontscharuk and Finner (2013) Gontscharuk, V. and Finner, H. (2013). Asymptotic FDR control under weak dependence: A counterexample. Statist. Probab. Lett. 83 1888-1893.

- Hall and Heyde (1980) Hall, P. and Heyde, C. C. (1980). Martingale Limit Theory and Its Application. Probability and Mathematical Statistics: A Series of Monographs and Textbooks 269-283. Academic Press.

- Izmirlian (2020) Izmirlian, G. (2020). Strong consistency and asymptotic normality for quantities related to the Benjamini–Hochberg false discovery rate procedure. Statist. Probab. Lett. 160.

- Kim and van de Wiel (2008) Kim, K. I. and van de Wiel, M. A. (2008). Effects of dependence in high-dimensional multiple testing problems. BMC Bioinformatics 9 114.

- Kluger and Owen (2023) Kluger, D. M. and Owen, A. B. (2023). Supplement to “A central limit theorem for the Benjamini-Hochberg false discovery proportion under a factor model”.

- Korn et al. (2004) Korn, E. L., Troendle, J. F., McShane, L. M. and Simon, R. (2004). Controlling the number of false discoveries: application to high-dimensional genomic data. J. Statist. Plann. Inference 124 379-398.

- Kotelnikova et al. (2012) Kotelnikova, E., Shkrob, M. A., Pyatnitskiy, M. A., Ferlini, A. and Daraselia, N. (2012). Novel Approach to Meta-Analysis of Microarray Datasets Reveals Muscle Remodeling-related Drug Targets and Biomarkers in Duchenne Muscular Dystrophy. PLoS Comput. Biol. 8 1-10.

- Lindner (2009) Lindner, A. M. (2009). Stationarity, Mixing, Distributional Properties and Moments of GARCH(p, q)–Processes In Handbook of Financial Time Series 43–69. Springer Berlin Heidelberg, Berlin, Heidelberg.

- Lucas, Kung and Chi (2010) Lucas, J. E., Kung, H. N. and Chi, J. T. A. (2010). Latent factor analysis to discover pathway-associated putative segmental aneuploidies in human cancers. PLoS Comput. Biol. 6 e100920:1–15.

- Mokkadem (1988) Mokkadem, A. (1988). Mixing properties of ARMA processes. Stochastic Process. Appl. 29 309-315.

- Neumann (2013) Neumann, M. H. (2013). A central limit theorem for triangular arrays of weakly dependent random variables, with applications in statistics. ESAIM Probab. Stat. 17 120-134.

- Neuvial (2008) Neuvial, P. (2008). Asymptotic properties of false discovery rate controlling procedures under independence. Electron. J. Stat. 2 1065–1110.

- Owen (2005) Owen, A. B. (2005). Variance of the number of false discoveries. J. R. Stat. Soc. Ser. B. Stat. Methodol. 67 411–426.

- Owen and Wang (2016) Owen, A. B. and Wang, J. (2016). Bi-Cross-Validation for Factor Analysis. Statist. Sci. 31 119 – 139.

- Paolella (2019) Paolella, M. S. (2019). Linear Models and Time-Series Analysis: Regression, ANOVA, ARMA and GARCH. Wiley series in probability and statistics. John Wiley & Sons, Hoboken, NJ.

- Pollard (1990) Pollard, D. (1990). Empirical Processes: Theory and Applications. NSF-CBMS Regional Conference Series in Probability and Statistics 2 i–86.

- Romano and Shaikh (2006) Romano, J. P. and Shaikh, A. M. (2006). On stepdown control of the false discovery proportion. Institute of Mathematical Statistics Lecture Notes - Monograph Series 49 33-50.

- Romano and Wolf (2007) Romano, J. P. and Wolf, M. (2007). Control of Generalized Error Rates in Multiple Testing. Ann. Statist. 35 1378-1408.

- Schwartzman and Lin (2011) Schwartzman, A. and Lin, X. (2011). The effect of correlation in false discovery rate estimation. Biometrika 98 199-214.

- Storey, Taylor and Siegmund (2004) Storey, J. D., Taylor, J. E. and Siegmund, D. (2004). Strong Control, Conservative Point Estimation and Simultaneous Conservative Consistency of False Discovery Rates: A Unified Approach. J. R. Stat. Soc. Ser. B. Stat. Methodol. 66 187–205.

- Storey and Tibshirani (2003) Storey, J. D. and Tibshirani, R. (2003). Statistical significance for genomewide studies. Proc. Natl. Acad. Sci. USA 100 9440-9445.

- Sun, Zhang and Owen (2012) Sun, Y., Zhang, N. R. and Owen, A. B. (2012). Multiple hypothesis testing adjusted for latent variables, with an application to the AGEMAP gene expression data. Ann. Appl. Stat. 6 1664–1688.

- van der Vaart (1998) van der Vaart, A. W. (1998). Asymptotic Statistics. Cambridge University Press, New York, NY.

- Wang et al. (2017) Wang, J., Zhao, Q., Hastie, T. and Owen, A. B. (2017). Confounder adjustment in multiple hypothesis testing. Ann. Statist. 45 1863.

- Wang et al. (2022) Wang, J., Gui, L., Su, W. J., Sabatti, C. and Owen, A. B. (2022). Detecting multiple replicating signals using adaptive filtering procedures. Ann. Statist. 50 1890 – 1909.

- Zhang, Fan and Yu (2011) Zhang, C., Fan, J. and Yu, T. (2011). Multiple testing via FDRL for large-scale imaging data. Ann. Statist. 39 613 – 642.

Supplementary Material

Proofs of Theorems 3.1,

3.2, and 3.3

A supplement with the proofs of Theorems 3.1, 3.2, and 3.3 can be found below. The first section of the supplement restates definitions and theorems from the probability literature that we use in our proofs. The second section of the supplement provides proofs of Theorems 3.1, 3.2, and 3.3. The third section of the supplement exhibits Hadamard derivative calculations that are used in our proofs of Theorems 3.1 and 3.2.

S.1 Background needed to prove Theorems 3.1, 3.2 and 3.3

This section contains results and definitions that we draw upon in order to prove our theorems. They come from Neumann (2013), Hall and Heyde (1980), Andrews and Pollard (1994) and van der Vaart (1998).

S.1.1 Theorems for proving converges in f.d.d.

Neumann (2013) gives a CLT for triangular arrays of dependent random variables. Neumann’s CLT in conjunction with the Cramér Wold device, will later be used to establish f.d.d. convergence of our empirical process from (8) to a joint Gaussian process. Below, we restate results from Theorem 2.1 in Neumann (2013) with notation convenient for us.

Theorem S.1.1.

(Neumann’s CLT) Let be a triangular array of centered random variables with . Further suppose that both

| (S1) |

| (S2) |

Furthermore, suppose there exists a summable sequence of real numbers such that for any and any satisfying , the following two covariance upper bounds both hold for any measurable function with :

-

(i)

, and

-

(ii)

.

Then .

To check the covariance upper bound conditions in Neumann’s CLT, it will be helpful to use Theorem A.5 in Hall and Heyde (1980). Below, we restate Theorem A.5 in Hall and Heyde (1980) with notation convenient for us.

Theorem S.1.2.

Suppose that and are random variables which are -measurable and -measurable, respectively, and that almost surely both and . Then

| (S3) |

S.1.2 Results and definitions from Andrews and Pollard (1994)

In order to obtain an FCLT from f.d.d. convergence we will need to introduce some definitions and results from Andrews and Pollard (1994). Andrews and Pollard (1994) use a chaining argument to provide an FCLT for bounded function classes. Their FCLT does not require independence.

We first introduce some definitions from their paper. Let be a triangular array of -valued random elements of a measurable space. Define to be the sequence of -mixing coefficients for this array. We use to denote a collection of bounded functions from to .

Definition S.1.1.

The seminorm function for the array of -valued random variables is the function that maps any real valued function on , to a real number via the following equation

| (S4) |

This can be used to define a seminorm on a collection of functions on .

Before stating their FCLT we also restate Definition 2.1 of Andrews and Pollard (1994) which gives the bracketing number.

Definition S.1.2.

Let be a function class and be the seminorm function for an array of random variables , as in Definition S.1.1. For the bracketing number is the smallest natural number for which there exists functions and functions with for all such that for each , there exists a such that . Here, means that for all , and we will use this shorthand notation in the proof of Theorem S.2.1.

To relate the function class to an empirical process we introduce the following operator .

Definition S.1.3.

Let be a class of real valued functions whose domain contains the support of each individual entry in the array . For any and any , define

| (S5) |

This operator maps individual functions in to centered and renormalized random variables. It defines an empirical process indexed by the elements of . We are now ready to restate the FCLT given in Corollary 2.3 of Andrews and Pollard (1994).

Theorem S.1.3.

Let be a strongly mixing triangular array whose -mixing coefficients satisfy

| (S6) |

for some even integer and some . Let be the seminorm function for the array as given in Definition S.1.1, and let be a uniformly bounded class of real-valued functions whose bracketing numbers (Definition S.1.2) satisfy

| (S7) |

for the same and . Finally, let be the operator from Definition S.1.3. If for all and , converges to a multivariate Gaussian distribution as , then converges in distribution to a Gaussian process indexed by with -continuous sample paths.

We will now clarify what -continuous sample paths and “convergence in distribution" in the above theorem mean. We start by clarifying what -continuity of sample paths for a Gaussian process means.

Definition S.1.4.

Let be a function class, let be a seminorm, and let be a Gaussian process indexed by , defined on the probability space . Note that for each , is a real valued random variable with a univariate normal distribution, and for a fixed , is a specific realization of that random variable. Fixing , we say that has a -continuous sample path at if for all , there exists an such that holds for any with . We say has -continuous sample paths, if for every and , has a -continuous sample path at .

For a fixed , the process is not guaranteed to be Borel measurable. Chapter 9 of Pollard (1990) raises caution about measurability issues of such empirical process and page 9 of Dudley (1999) provides an example showing that the empirical process of IID random variables is not guaranteed to be measurable with respect to the -norm topology. To skirt around these measurability issues, we will use a modified notion of convergence provided in Definition 9.1 of Pollard (1990). Introducing the modified notion of convergence allows us to use the FCLT from Andrews and Pollard (1994) (reproduced in Theorem S.1.3) and ultimately allows us to extend upon the results of Delattre and Roquain (2016), which use a different FCLT.

We reproduce the modified definition of convergence in distribution below. Some readers might prefer to skip this definition and to instead treat everything as measurable so that the outer expectation and the expectation are the same and so that the standard notion of convergence in distribution is interchangeable with the modified definition.

Definition S.1.5.

Let be a sequence of functions from a probability space into a metric space (not necessarily Borel measurable), and let be a Borel measurable map from into . For any bounded real valued function , is not necessarily well defined, so we define to be an operator that gives the outer expectation of a real valued function on . In particular, if is a real valued function on , then

We say that converges in distribution to , if for every bounded, uniformly continuous, real valued function on , .

Throughout the text we will use the operator in the statements such as to denote convergence in distribution in the sense of Definition S.1.5.

S.1.3 Results and definitions from van der Vaart (1998)

In the proof of Theorems 3.1 and 3.2, we will rely on some definitions and theorems from van der Vaart (1998). Most notably, we need to introduce the notion of Hadamard differentiability and the functional delta method from van der Vaart (1998). The functional delta method is defined for an alternate definition of convergence in distribution, provided in Chapter 18.2 of van der Vaart (1998), which turns out to be equivalent to Pollard’s (1990) notion of convergence in distribution in Definition S.1.5. We reproduce the alternate definition of convergence in distribution provided in Chapter 18.2 of van der Vaart (1998) below.

Definition S.1.6.

Let be a sequence of random elements and be a Borel-measurable random variable. converges in distribution to in the sense of Chapter 18.2 in van der Vaart (1998), if for all bounded, continuous functions , where denotes outer expectation.

Remark S.1.1.

-

Proof.

Definition S.1.5 states that converges in distribution to if and only if for all bounded, uniformly continuous functions , . Definition S.1.6 states that converges in distribution to if and only if for all bounded, continuous functions (which need not be uniformly continuous). Clearly, if convergence in distribution holds in the sense of Definition S.1.6, it will hold in the sense of Definition S.1.5. To show the converse note that if for all bounded, uniformly continuous functions , then for all bounded, Lipschitz functions , but by the Portmanteau Lemma (Lemma 18.9 in van der Vaart (1998)) this is equivalent to for all bounded, continuous functions . The notions of convergence of distribution in Definitions S.1.5 and S.1.6 are therefore equivalent. ∎

In our proofs of Theorems 3.1 and 3.2, it will also be helpful to introduce the alternate definition for convergence in probability of non-measurable real valued functions from a probability space, seen in Chapter 18.2 of van der Vaart (1998), and to derive Slutsky’s lemma for our alternate notions of convergence in distribution and convergence in probability.

Below, we reproduce the alternate notion of convergence in probability seen in Chapter 18.2 of van der Vaart (1998).

Definition S.1.7.

If is a sequence of functions from a probability space into a metric space , we say that converges in probability to if for all , . Here, denotes outer probability measure since neither nor needs to be Borel-measurable. Throughout the text, we will use the operator to denote convergence in probability in the sense of this definition.

We will need to use Slutsky’s lemma for our alternate definitions of convergence in probability and convergence in distribution, which we state and prove below by directly applying Theorems 18.10(v) and 18.11(i) from Chapter 18.2 of van der Vaart (1998).

Lemma S.1.1 (Slutsky’s lemma).

If and for some constant , then .

- Proof.

Since our proofs of Theorems 3.1 and 3.2 rely heavily on the concept of Hadamard differentiability and on the functional delta method, we reproduce the definition of Hadamard differentiability as well as the functional delta method from Chapter 20.2 of van der Vaart (1998) below.

Definition S.1.8 (Hadamard differentiability).

Let , be normed spaces, let be a map defined on a subset , and consider an element . Further, let be a different subset of . We say that is Hadamard differentiable at tangentially to the subset if there exists a continuous, linear map such that for any and collection of elements of satisfying both and ,

This map , if it exists, is said to be the Hadamard derivative of the function at tangentially to the subset .

Theorem S.1.4 (Functional Delta Method).

Let and be normed linear spaces and let be Hadamard differentiable at tangentially to with Hadamard derivative at tangentially to given by the linear map . Let be a sequence of maps from our probability space to such that for some sequence of numbers and a valued random variable . Then .

-

Proof.

See Theorem 20.8 in van der Vaart (1998). ∎

S.2 Proof of Theorems 3.1, 3.2, and 3.3

In this section, we will assume the setting of Theorem 3.1. Further, to simplify notation and analysis, we will fix the realization of the latent factor , so that all probabilities, expectations and outer expectations assume a fixed and are taken with respect to the probability measure and -algebra generated by .

S.2.1 Helpful results for proving Theorems 3.1 and 3.2

In this subsection, we develop results to prove Theorems 3.1, 3.2 and 3.3. We start with a helpful lemma.

Lemma S.2.1.

Under the conditions of Theorem 3.1, there is a constant such that for and

| (S8) |

-

Proof.

For any and , note that the derivative of with respect to satisfies

by the argument used in the proof of Proposition 2.1. Since does not depend on , or , this completes the proof. ∎

We now define the joint Gaussian process on to which converges in distribution and start by proving f.d.d. convergence.

Definition S.2.1.

We define be a joint Gaussian process on with mean zero and joint covariance kernel .

We note that is well defined because is a symmetric and positive semidefinite joint covariance kernel.

Proposition S.2.1.

Under the conditions of Theorem 3.1, .

-

Proof.

Fix any and fix any and . Define to be the covariance matrix given by for . To show f.d.d. convergence we must show that . By the Cramér-Wold device, it suffices to show that for any .

Now fix any . To show , we will use Neumann’s CLT (Theorem S.1.1). For define,

Clearly for all . Note that which implies that and, therefore, . Therefore, to apply Theorem S.1.1 to the triangular array , we must check (S1), (S2), as well as the existence of a summable satisfying the desired properties.

To check (S1) note that because ,

where the last equality holds by (10) under Condition 5 and by our definition of . Therefore, letting , (S1) holds. It is easy to see that (S2) holds because for all and , , where does not depend on or .

Now for each define , where is defined in Equation (4). By Condition 2, and therefore is a summable sequence of real numbers. Fix any and any satisfying . Further, fix any measurable function such that and we will show that covariance inequalities (i) and (ii) from Theorem S.1.1 hold. To prove covariance inequality (i), let and . Clearly, both and almost surely. Now recalling the -algebras defined in Section 2.3.1 note that is -measurable and is -measurable. Thus by Theorem S.1.2,

where the second inequality uses Equation (4) and the third inequality uses nonnegativity of and the definition of . Therefore, covariance inequality (i) of Theorem S.1.1 holds. To show covariance inequality (ii) holds, we use the same argument except we let and . Note that both and almost surely and that again is -measurable while is -measurable. Therefore, by Theorem S.1.2 and the definitions of and ,

We have thus shown that with the summable sequence , covariance inequality (i) and (ii) of Theorem S.1.1 hold for any fixed , any satisfying , and any such that . Thus by applying Neumann’s CLT (Theorem S.1.1),

∎

Now that we have established we can derive an FCLT for by applying a result from Andrews and Pollard (1994), which is based on a chaining argument. The FCLT uses a slightly modified definition of weak convergence which can be applied to a sequence of non-Borel measurable -valued random variables (see Definition S.1.5 or equivalently Definition S.1.6.)

Theorem S.2.1.

Under the conditions of Theorem 3.1, , where is a joint Gaussian process with mean zero and joint covariance kernel , and almost surely.

-

Proof.

The proof is lengthy and so we split it into a sequences of steps as follows:

- 1)

-

2)

upper bounding the bracketing number ,

-

3)

checking the FCLT conditions,

-

4)

applying the FCLT,

-

5)

defining limiting processes and , and finally

-

6)

verifying that .

Defining the relevant function class, , and seminorm, .. First, for each recall that has unit variance. Let be an expansion of our triangular array where . Because and are deterministic and is bounded away from 1 by Condition 1, the arrays and have the same -mixing coefficients. These coefficients satisfy Condition 2. Now define , and define via

For , note that .

The function class we will use includes the various restrictions of to a fixed and while , , and vary:

| (S9) |

Letting be the seminorm function for the array given by Definition S.1.1, observe that for and a simple computation gives

| (S10) |

where the inequality follows from Lemma S.2.1.