The American put with finite-time maturity

and stochastic interest rate

Abstract.

In this paper we study pricing of American put options on a non dividend-paying stock in the Black and Scholes market with a stochastic interest rate and finite-time maturity. We prove that the option value is a function of the initial time, interest rate and stock price. By means of Itô calculus we rigorously derive the option value’s early exercise premium formula and the associated hedging portfolio. We prove the existence of an optimal exercise boundary splitting the state space into continuation and stopping region. The boundary has a parametrisation as a jointly continuous function of time and stock price, and it is the unique solution to an integral equation which we compute numerically. Our results hold for a large class of interest rate models including CIR and Vasicek models. We show a numerical study of the option price and the optimal exercise boundary for Vasicek model.

Key words and phrases:

American put option, stochastic interest rate, free boundary problems, integral equation1. Introduction

Pricing of American options is a classical problem in mathematical finance which has attracted continuous attention since the initial work of McKean Jr, (1965). Its study has also become a benchmark for methodological developments of optimal stopping theory and the associated free boundary problems. In this paper we contribute to this strand of research by studying the American put option on a Black and Scholes market with a stochastic interest rate and finite-time maturity. The stock price and the interest rate are driven by (possibly) correlated Brownian motions and we make minimal assumptions about the dynamics of the interest rate under the pricing measure: the coefficients are time independent and Lipschitz continuous. CIR model, which does not satisfy these conditions, is also included in our analysis.

It is well known (Bensoussan,, 1984; Karatzas,, 1988) that the American put option price is given by the value function of a related optimal stopping problem. In our model, this optimal stopping problem is 3-dimensional with 2-dimensional diffusive dynamics (stock price and interest rate) and time. The stopping set, i.e., the set of points in which it is optimal to exercise the option, is separated from the continuation set, where it is optimal to hold (or sell) the option, by a single surface called the stopping boundary. The value function is a classical solution to a PDE in the interior of the continuation set, i.e., it is twice continuously differentiable in and once continuously differentiable in , whereas it coincides with the put payoff in the stopping set.

One of our technical contributions is to establish by means of probabilistic methods that the value function is globally once continuously differentiable in all variables. Then, the continuity of the gradient of the value function permits the application of a generalisation of Itô’s formula (due to Cai and De Angelis, (2021)) and a rigorous derivation of a hedging portfolio. The hedging portfolio invests in three instruments: the money market (savings) account, the zero-coupon bond with maturity equal to the maturity of the option and the stock. We show that the usual Delta hedging strategy is optimal: the positions in the bond and the stock are given by relevant partial derivatives of the value function. As a further consequence of the generalised Itô’s formula we also derive the decomposition of the American option price as the sum of the price of a European put option with the same maturity and the same exercise price, and an early exercise premium. This is known in the literature as the early exercise premium formula, which corresponds to Doob’s decomposition of supermartingales into a martingale and a non-increasing process (applied here to the Snell envelope of the optimal stopping problem).

Our second contribution concerns the continuity properties of the stopping boundary in our model, which have not been established in the literature. We are able to demonstrate that the stopping boundary, when parametrised as a function of , is continuous. Apart from being of interest in its own right, this enables a characterisation of the stopping boundary as the unique continuous solution of an integral equation arising from the early exercise premium decomposition. When a stopping boundary is known, efficient numerical methods are at disposal for computation of the option price. One can use Monte Carlo methods based on the early exercise decomposition or classical PDE methods for Cauchy problems (in contrast to the original problem with a free boundary).

American option pricing with stochastic interest rates has already attracted a lot of attention in the literature, mainly focusing on approximations and numerical methods. Lattice (tree) based methods are employed by Appolloni et al., (2015) to price options in Black and Scholes model with CIR interest rate dynamics and by Battauz and Rotondi, (2019) in a model with Vasicek interest rates. Geske and Johnson, (1984)’s approximation of discretely exercised American options prices is adapted by Ho et al., (1997) and Chung, (2000) to a class of stochastic interest rate models that lead to log-normally distributed bond prices. An alternative approximation is provided by Menkveld and Vorst, (2000). A framework for option pricing with Heath, Jarrow, Morton’s bond market model (Heath et al.,, 1992) is developed by Amin and Jarrow, (1992) with a binomial-tree-based implementation of pricing of foreign exchange options performed in Amin and Bodurtha Jr, (1995).

Detemple and Tian, (2002) study the pricing of American options in a general diffusive model with a -dimensional Brownian motion. They formulate assumptions under which there is a single exercise surface but without proving its continuity. In a Black and Scholes market model with Vasicek interest rates they show that this exercise boundary solves an integral equation of the same form as in this paper. The uniqueness of solutions to this integral equation is not discussed and their numerical method for computing the solution is different to ours.

Hedging underlies the success of mathematical finance in derivatives markets. A rigorous theory that links hedging of American options with solutions of optimal stopping problems was initiated by Bensoussan, (1984) using PDE methods and extended by Karatzas, (1988) to more general models and payoffs thanks to the martingale theory of optimal stopping. A hedging strategy for an American option consists of an investment portfolio and a non-decreasing cumulative consumption process which increases only when the state-time process is in the stopping set. In the Black and Scholes model with constant interest rate the classical Delta hedge is known to replicate the option (Karatzas and Shreve, 1998b, , Thm. 7.9, Ch. 2). This paper seems to be the first to rigorously derive the hedging strategy for American put options on a market with a stochastic interest rate. This is accomplished thanks to the -regularity of the value function that we are able to prove and which did not appear in previous works.

A characterisation of an optimal stopping boundary as solution to a (system of) integral equations has been known since the earliest works (see Van Moerbeke, (1976)). In more recent works Kim, (1990); Jacka, (1991); Carr et al., (1992); Myneni, (1992), the stopping boundary for the classical Black and Scholes market with constant interest rate is shown to be the unique solution to an uncountable system of integral equations arising from the early exercise premium decomposition of the option price. A break-through came with the work of Peskir, (2005) where he shows that the stopping boundary is the unique continuous solution of a single integral equation. His key observation is that the integral equation only needs to be satisfied for stock prices at the boundary while earlier results required that it does so for all stock prices at and below the boundary. Peskir, (2005)’s integral equation opens doors to side-stepping the computation of the value function in the process of determining the optimal exercise strategy; see numerical methods designed in Little et al., (2000); Kim et al., (2013). Our paper extends Peskir, (2005)’s results to the market with a stochastic interest rate and the optimal boundary being a two-dimensional surface. It is also the continuity of the boundary that allows us to establish the uniqueness of solutions to the integral equation. A closely related paper that furthermore motivated our numerical approach is Detemple et al., (2018) where the authors solve an integral equation for Black and Scholes market with stochastic volatility.

The regularity of the value function in one-dimensional optimal stopping problems is often phrased as smooth-fit and plays a major role in determining explicit solutions. In a Black and Scholes model with constant interest rate, smooth-fit for American options with finite-time maturity is understood as continuous differentiability of the value function with respect to the stock price, for each fixed value of the time variable (see Jacka, (1991) and subsequent works). That is a ‘directional’ derivative and continuity is only considered with respect to one variable. Sobolev space regularity is studied in Jaillet et al., (1990) for American options on multiple assets and deterministic, time-dependent discount rate under the assumption of uniform ellipticity of the associated second order differential operator. By Sobolev embedding it is possible to determine continuous differentiability of the value function with respect to the initial values of all the assets but not with respect to time. Continuous differentiability with respect to time and stock price for the value of the American put with finite-time maturity and constant interest rate is obtained in De Angelis and Peskir, (2020) along with other complementary findings about continuous differentiability of the value function for a large class of optimal stopping problems. In this paper, we refine the arguments from De Angelis and Peskir, (2020) and remove global integrability conditions that may not hold in our set-up.

The early exercise premium formula for American options was studied in great generality, in non-Markovian problems beyond the setting of the American put option by Rutkowski, (1994) with methods from martingale theory. The nature of the methods employed in Rutkowski, (1994) to derive his main results is such that the emphasis is removed from the optimal boundary, which in fact only appears in specific examples (see Sec. 3 of that paper) as a time-dependent function. Here instead we derive the early exercise premium formula starting from the analysis of the optimal boundary (and its regularity) as a function of time and one stochastic factor from our two-factor model.

Some of the ideas in this paper find wider applicability in optimal stopping theory. The generalisation of Itô’s formula that we use to find the hedging portfolio has natural applications to other optimal stopping problems as discussed extensively in Section 3 of Cai and De Angelis, (2021). Localisation of the arguments from De Angelis and Peskir, (2020) to prove continuous differentiability of the value function does not rely much on the specific structure of our problem and suggests a general recipe to address the issue. Finally, our ideas for the continuity of the optimal stopping surface have been expanded upon to cover more general settings in Cai et al., (2021).

The paper is structured as follows. Section 2 introduces the market model, main assumptions and notation. The main contributions are discussed in Section 3 while their proofs are delayed until after Section 4. A numerical study with interest rates following Vasicek model is presented in Section 4 along with a sensitivity analysis. Monotonicity and Lipschitz continuity of the value function is proved in Section 5. Existence of the stopping surface and its regularity (in the sense of diffusions) are shown in Section 6. In Section 7 we prove that the value function is continuously differentiable on the whole domain. Auxiliary estimates needed for admissibility of the hedging strategy are provided in Section 9. Three appendices contain further details.

2. Problem formulation

Let be a complete probability space carrying two correlated Brownian motions and with for all and a fixed (here is the expectation under ). We denote by the filtration generated by augmented with the -null sets. On this probability space we consider a financial market with one risky asset and a bond. The asset and the risk-free (short) rate take values, respectively, in intervals and , and follow the dynamics

| (2.1) | ||||

| (2.2) |

with specified below. The probability measure is a risk neutral measure for this market. We denote by a fixed finite trading horizon.

Throughout the paper we assume and (with possibly unbounded). The right boundary is unattainable in a finite time (it is a natural or entrance-not-exit boundary). The left boundary is either unattainable or reflecting. It will become clear later that the exact behaviour of the interest rate process at this boundary is irrelevant for the majority of results and their proofs. For the dynamics of the interest rate our benchmark example is the CIR model, but, with a relatively small additional effort, our results cover other stochastic interest rate models, e.g., Vasicek model. Therefore, we make the following standing assumption:

Assumption 2.1.

The coefficients and in (2.2) meet one of the conditions below:

-

(i)

(CIR model) For we have and .

-

(ii)

and are globally Lipschitz and continuously differentiable on bounded subsets of with for all , and . For any compact set , and any for some and , there is (depending on , and ) such that

(2.3)

The assumption that cannot be relaxed without trivialising the pricing problem. A strictly positive lower boundary could, however, be of interest. For the clarity of presentation, it is omitted but it can be studied with similar methods as those developed in this paper.

The above assumptions are sufficient to guarantee that (2.2) admits a unique strong solution defined on . In the case of CIR model, we also have which implies that the spot rate is non-negative (but not necessarily strictly positive), see e.g. (Jeanblanc et al.,, 2009, Sec. 6.3.1), so the left boundary is reflecting (also non-attainable if ). Hence, the bound (2.3) is satisfied with the constant . The linear growth of and in (2.2) guarantees that for each there is only depending on and , such that (Krylov,, 1980, Ch. 2, Sec. 5, Thm. 9)

| (2.4) |

Under Assumption 2.1, the solution of (2.1) may be expressed as

| (2.5) |

so that depends on both initial values and . On the contrary, the dynamics of the interest rate does not depend on the initial asset value. The coupling between the processes and stems from formula (2.5) and the correlation between the Brownian motions. To keep track of the dependence of the processes on their initial values, in what follows we often use the notation for the process started at and . Also we may sometimes use the notation , , and .

According to the classical theory (Karatzas and Shreve, 1998b, , Ch. 2, Thm. 5.8) the rational price of an American put option with maturity time , strike price , written on the asset and evaluated at time is given by

where the essential supremum is over -stopping times in and the function denotes the positive part. In our Markovian set-up, for a Borel-measurable function (see (Shiryaev,, 2008, Ch. 3)). Using that the process is time-homogeneous and strong Markov, we can express as

| (2.6) |

where and are, respectively, the values of the spot rate and of the asset at time . The above is an optimal stopping problem with Markovian structure and a 3-dimensional state space.

Since the process

| (2.7) |

is non-negative and continuous, and thanks to the integrability condition (2.3), we can rely on standard optimal stopping theory (see, e.g., Appendix D in Karatzas and Shreve, 1998b ) to conclude that the smallest optimal stopping time for (2.6) is -a.s. given by

| (2.8) |

where we note that since . Clearly depends on the initial value of the 3-dimensional state process .

The form (2.8) of gives rise to the so-called continuation set and its complement, the stopping set , that is

| (2.9) | ||||

| (2.10) |

Upon observing the spot rate and the asset value, at each time the option holder must decide whether to hold the option or to exercise it. She should wait (possibly trading the option on the market) if since the option value is strictly larger than the payoff of immediate exercise. On the contrary, if the option should be immediately exercised. Notice that

Remark 2.2.

Setting

(i.e., is the discounted option value process), we have that (Karatzas and Shreve, 1998b, , Appendix D)

| (2.11) | is a right-continuous -supermartingale, | |||

| (2.12) |

We will soon show (Proposition 5.1) that is a continuous function, so that is a continuous process.

Notation. We set

| (2.13) |

and denote by the boundary of in , i.e., .

For future frequent use we denote by the infinitesimal generator of , which, for any reads

| (2.14) |

where , and , , denote, respectively, the first and second order partial derivatives of .

3. Main results

In this section we provide the main results of the paper. In Sections 3.1 and 3.2, under the sole Assumption 2.1, we establish continuous differentiability of the value function (jointly in all variables), along with its monotonicity in and convexity in . We also prove the existence and monotonicity of an optimal exercise boundary and present two possible parametrisations of it. Then, in Sections 3.3—3.6, under a mild additional assumption on and (Assumption 3.6) we derive continuity of the optimal exercise boundary (as a function of two variables) and an integral equation that uniquely determines it (also under Assumption 3.8). Finally, we obtain the early exercise premium formula for the option price and the hedging portfolio that replicates the option’s payoff at all times.

3.1. Optimal stopping boundary

In the classical Black-Scholes model with constant interest rate, the stopping set is determined by a boundary: it is optimal to exercise the option the first time when the stock price drops below this boundary. A similar characterisation of the stopping region can be derived in our model with the difference that the stopping boundary is a surface. To this end, we research monotonicity properties of the value function.

Proposition 3.1.

The value function is finite for all and it satisfies the following conditions:

-

(i)

is non increasing for all ,

-

(ii)

is non increasing for all ,

-

(iii)

is convex and non increasing for all .

Proof.

See Section 5. ∎

The monotonicity in and and the convexity in is the same as in the classical Black-Scholes model and the proof is very similar. The dependence on has financial explanation: larger interest rate implies stronger discounting of future cashflows and, hence, lower present value.

Remark 3.2.

In the case (perpetual option) the discounted payoff process (2.7) is still uniformly integrable and continuous. This implies that, letting denote the value of the perpetual option, the stopping time

is optimal by standard theory and (2.11)–(2.12) continue to hold in this setting (see, e.g., (Shiryaev,, 2008, Ch. 3, Thm. 3)). In particular, it can be shown that is non-increasing and is convex and non-increasing.

From the general optimal stopping theory we expect that the value function be continuous. Indeed, this fact is proved from first principles in our Proposition 5.1 in Section 5 (without relying on the form of the stopping set). The continuity of means that the continuation set is open and the stopping set is closed. In view of the monotonicity properties established in Proposition 3.1, we can show that there is a surface splitting and .

In models with constant interest rate, an optimal boundary is often defined as function of time which provides a threshold for the process . A parametrisation of the stopping surface as a function of time and interest rate is also available in our setting. For the sake of mathematical tractability we prefer to work with the parametrisation in terms of time and stock price. Due to technical reasons that will become clearer in Section 6, we are able to prove the continuity of jointly in both variables , but not the joint continuity of in . However, is more convenient for numerical computations in Section 4 as it admits values in a bounded interval . The connection between and is established in Proposition 3.4.

Proposition 3.3.

There exists a function on such that

| (3.1) | ||||

| (3.2) |

The function has following properties:

-

(i)

For any , the mapping is right-continuous and non-increasing and the mapping is left-continuous and non-decreasing.

-

(ii)

for .

-

(iii)

for ; when the risk-free rate is non-negative (i.e., ), we have for .

Proof.

See Section 6. ∎

Notice that (ii) and (iii) above imply that it is never optimal to exercise the option out of the money or if the interest rate is negative. This is in line with classical financial wisdom.

The following proposition whose simple proof is omitted gives details of the reparametrisation of the stopping boundary as a function of time and interest rate.

Proposition 3.4.

Define

The mappings and are right-continuous and non-decreasing for any . For any we have when , and when . Furthermore,

3.2. Smoothness of the value function

It is well-known that satisfies (in the classical sense)

| (3.3) | ||||

where is the generator of defined in (2.14). Hence, standard arguments assert that is in . Classical optimal stopping theory identifies the boundary of the set by imposing the so-called smooth-fit condition. In the American put problem with constant interest rate this corresponds to proving that is continuous for each fixed, with denoting the value function associated to the option price. In our setting we prove a stronger result and show continuous differentiability of across the stopping boundary , i.e., the global continuity of the gradient of (as a function of all variables) in . We use ideas similar to those in De Angelis and Peskir, (2020) but we must refine arguments therein and use estimates with ‘local’ nature since we are not able to directly check their assumptions. In particular, global differentiability of the flow and related integrability conditions (see Eqs. (4.4)–(4.7) and Theorem 10 in De Angelis and Peskir, (2020)) are not easily verifiable when, for example, the interest rate follows the CIR dynamics.

Theorem 3.5.

We have .

Proof.

See Section 7. ∎

It is worth noticing that the proof of the above result combines a number of steps that may be of independent interest. In particular, we prove local Lipschitz continuity of (Proposition 5.1) and the regularity of the stopping boundary in the sense of diffusions. The latter gives the continuity of optimal stopping times as functions of the initial state, which plays a crucial role in the proof of the theorem.

3.3. Continuity of the stopping boundary and Dynkin’s formula

Preliminary right/left-continuity properties of the stopping boundary illustrated above follow from its monotonicity and the closedness of the stopping set (see Proposition 3.3). However, thanks to the regularity of the value function , we can also prove joint continuity of the stopping boundary in both variables. For this we require local Hölder continuity of the derivatives of the coefficients in the dynamics of the short rate .

Assumption 3.6.

The functions and in (2.2) have first and second order derivatives, respectively, Hölder continuous on any compact subset of .

Note that this assumption is satisfied by CIR model. It strengthens Assumption 2.1(ii) by requiring that the derivatives are not only locally continuous but also locally Hölder continuous. This technical requirement is satisfied by many popular short rate models. The joint continuity of optimal stopping boundaries depending on multiple variables has not been proved with probabilistic techniques before, so the next result is of independent mathematical interest.

Proposition 3.7.

Under Assumption 3.6, the function is continuous.

Proof.

See Section 8. ∎

Summarising, we have , and the optimal stopping boundary is continuous. This is not sufficient to apply the change of variable formula developed in Peskir, (2007) which is often used in optimal stopping literature to establish Itô’s formula for the value function. Indeed, since Peskir, (2007) deals with functions that are not necessarily , it requires that be a semi-martingale, so that the local time on the stopping boundary is well-defined. While we were unable to prove it for our optimal boundary, we can instead take advantage of the continuous differentiability of our value function and use a generalisation of Itô’s formula from Cai and De Angelis, (2021) which only requires the monotonicity of the boundary. Notice that, interestingly, we need not control the second order spatial derivatives near in order to apply results from Cai and De Angelis, (2021). We do however need to ensure that both boundary points of the set are non-attainable, because we have not proven that the derivatives , and , understood as the limit as , are well-defined.

Assumption 3.8.

The lower boundary point is non-attainable by the process . In particular, under Assumptions 2.1-(i) we require .

Proposition 3.9.

Under Assumption 3.8, for any and any stopping time , the value function satisfies the following Dynkin’s formula:

| (3.4) |

Proof.

See Section 8. ∎

In the proof of the above proposition, we show that the discounted value function satisfies for any stopping time

| (3.5) | ||||

This representation will play a fundamental role in deriving a hedging strategy for the American put option in Section 3.6.

3.4. Early exercise premium

Inserting in (3.4), we obtain a decomposition of the American option price into a sum of the European option price and an early exercise premium (see Rutkowski, (1994) for a derivation of this formula only using general martingale theory):

| (3.7) |

where

| (3.8) | ||||

The last equality follows from by construction of as the generalised inverse of . By Remark 3.10 the early exercise premium also reads

3.5. Integral equation for the stopping boundary

Proposition 3.9 provides a characterisation of the optimal stopping boundary . Indeed, for any such that , inserting and in (3.4) yields an integral equation for :

| (3.9) |

The condition that is necessary as can take values and which do not belong do the state space , and the interest rate process may not be started from there. Notice also that when so the left-hand side of (3.9) can be replaced by . In line with well-known results for American options with constant interest rate (Peskir,, 2005), it also turns out that is the unique solution of the integral equation.

Proposition 3.11.

The integral equation (3.9) has an analogue for the function from Proposition 3.4. Indeed, for , taking and in Proposition 3.9 and using we see that solves the integral equation:

| (3.10) | ||||

where we use which follows from by construction of as the generalised inverse of . This parametrisation of the integral equation extends the one obtained in the classical American put problem with constant interest rate to our two-factor set-up. Once again we can prove uniqueness of the solution to the integral equation but without requiring continuity of , which is a non-standard result for this type of equations.

Corollary 3.12.

Under the assumptions of Proposition 3.11, the function is the unique function such that:

-

(1)

and are right-continuous and non-decreasing,

-

(2)

the generalised left-continuous inverse is continuous in , non-decreasing in and non-increasing in ,

-

(3)

satisfies (3.10) with ( therein replaced by ) for all such that and .

Notice that for follows immediately from .

Integral equations (3.9) and (3.10) offer a method to compute the optimal stopping boundary without using the value function . We will demonstrate it in Section 4 where we design a numerical method for solving such integral equations. Knowing the stopping boundary , the decomposition (3.7) can be employed to obtain an efficient numerical estimate of the option value. This offers an alternative to numerical solution of the variational inequality for the value function , and, subsequently, extraction of the optimal exercise boundary.

3.6. Hedging portfolio

Thanks to the change of variable formula (3.5) we are also able to rigorously construct a hedging portfolio that (super)replicates the option payoff at all times. This is based on the classical delta-hedging ideas in the Black and Scholes model but its rigorous mathematical derivation requires smoothness of the option price function which was not previously established in the literature.

Consider a market comprising three instruments: the money market account , the risky stock with the dynamics (2.1), and a zero-coupon bond with maturity . We will construct a hedging portfolio for the American option on this market. We remark that the zero-coupon bond can be replaced by any other financial instrument whose dynamics depends on the Brownian motion driving the interest rate, see Karatzas, (1988).

The risk-neutral price of the zero-coupon bond at time is given by

| (3.11) |

By standard arguments based on pathwise continuity of the flow , one can easily show that is continuous on . Then, under Assumption 2.1, the classical PDE theory (Friedman,, 1964, Thm. 9, Ch. 4, Sec. 3) guarantees that is the unique classical solution of the boundary value problem

where and is an arbitrary bounded interval. In particular, by arbitrariness of we have and

Then, using Itô’s formula, the discounted bond price dynamics reads

| (3.12) |

Denote by the holdings in the stock, the bond and the money account, respectively. Let be a non-decreasing continuous process starting from modelling consumption. The value of a self-financing portfolio starting at time from is

| (3.13) |

The portfolio is admissible if all integrals above are semimartingales. Taking the money-market account as a numeráire, we obtain from equations (3.13) and

| (3.14) |

that the dynamics of the discounted portfolio value reads

| (3.15) |

This means that a self-financing portfolio is uniquely determined by the processes and .

Comparing (3.15) with (3.5), a candidate for the hedging strategy is given by

| (3.16) |

We can indeed prove that such portfolio strategy is admissible and replicates the option’s payoff.

Proposition 3.13.

Under Assumption 3.8 the portfolio is admissible and replicates the payoff of the American put option.

Proof.

See Section 9. ∎

4. Numerical analysis

In the numerical analysis, we assume that the interest rate follows Vasicek model. In particular, this means that and

| (4.1) |

whose explicit solution is given by

| (4.2) |

We first derive a numerical method for computing the optimal stopping boundary using the integral equation from (3.10). Once the boundary is obtained, we use it to also compute the value function via (3.7). Section 4.2 contains an analysis of the effect of parameters on the stopping boundary and the value function.

4.1. Computational approach

With an abuse of notation, we denote by the time- price of a zero-coupon bond with maturity (c.f. (3.11)); the dependence on the initial state is indicated in the subscript of the expectation operator. By Proposition 3.4 we have for , i.e., it is never optimal to stop for negative values of the interest rate. To compute for , recall the integral equation (3.10): for such that , we have

| (4.3) |

where and are stated in (3.8). With the last parameter of , we emphasise the dependence on the function :

In the numerical scheme below, we evaluate for consecutive approximations of .

In Appendix D, we derive the following formulas for and using well-known properties of the joint law of :

| (4.4) | ||||

| (4.5) |

where is the cumulative distribution function of the standard normal distribution. An explicit formula for is given by (D.3) and the other auxiliary quantities used above are stated in (D.1).

Equation (4.3) defines the boundary as a fixed point of a non-linear mapping. To compute it, we follow an iterative scheme motivated by Detemple et al., (2018). We fix and discretise the variables as follows:

We specify an initial approximation of the boundary:

For each , we compute the boundary at points by solving the algebraic equation:

| (4.6) |

The right-hand side, which is difficult to compute, is independent of , while the left-hand side is known in an explicit form. We stop iterations when, for a pre-determined ,

The numerical evaluation of requires that the boundary be known for all points in the state space while we compute it only on the grid . We, therefore, use Matlab interpolation function with the Modified Akima cubic Hermite polynomials (‘makima’) interpolation method. Integrals are computed using Matlab functions employing standard quadrature methods.

It should be remarked that the stopping boundary may have a singularity (jump) at , which corresponds to a horizontal part of the parametrisation of the stopping surface: a jump occurs when . Furthermore, satisfies for and for , see Proposition 3.4. This hints at a potential numerical difficulty around , particularly for times close to maturity.

4.2. Sensitivity analysis

Unless stated otherwise, numerical results are presented for the parameter values

| (4.7) |

and the convergence criterion with . The magnitude of and is based on empirical findings reported in the literature, c.f. (Hull,, 2009, Chapter 31) and Fergusson and Platen, (2015). Although main currencies have recently enjoyed much lower interest rates, our choice of means that the effects of random interest rate and its parameters on the market dynamics and optimal stopping boundary are more pronounced and graphs more transparent.

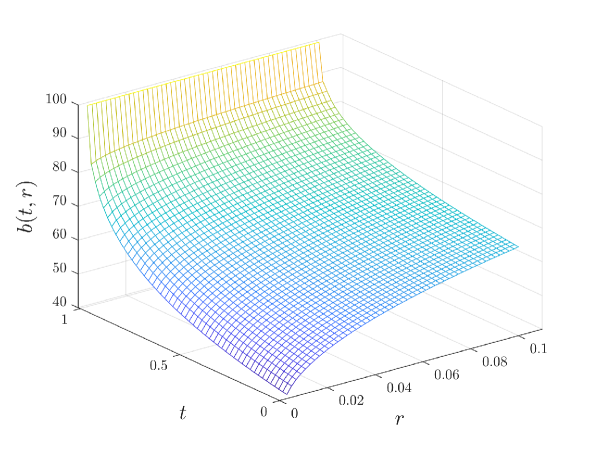

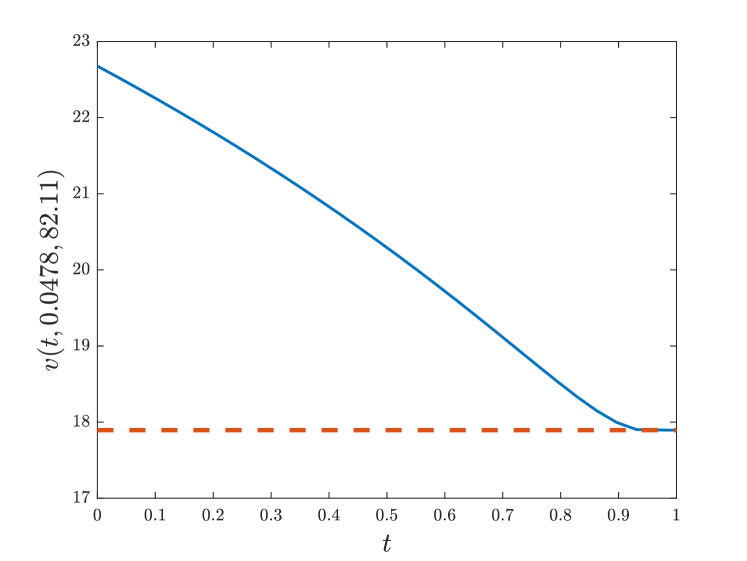

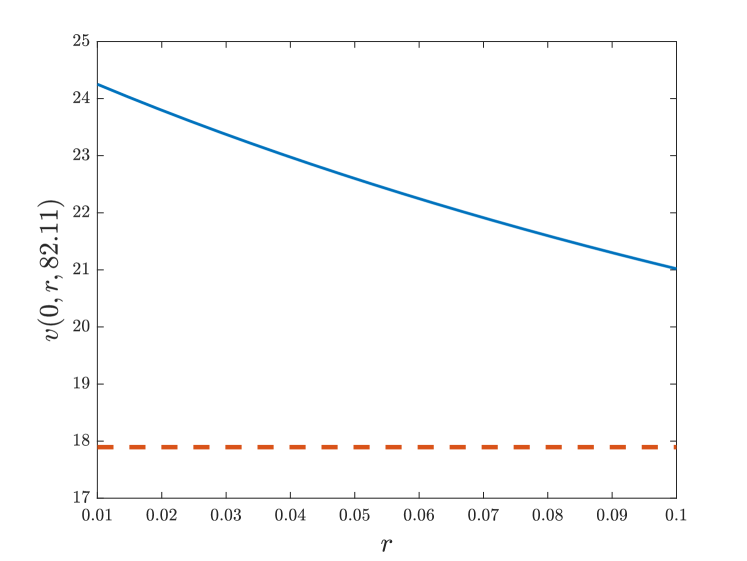

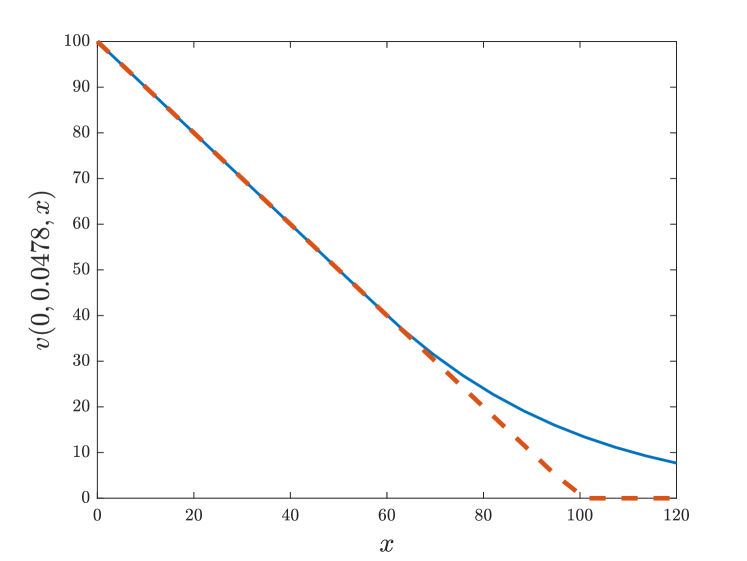

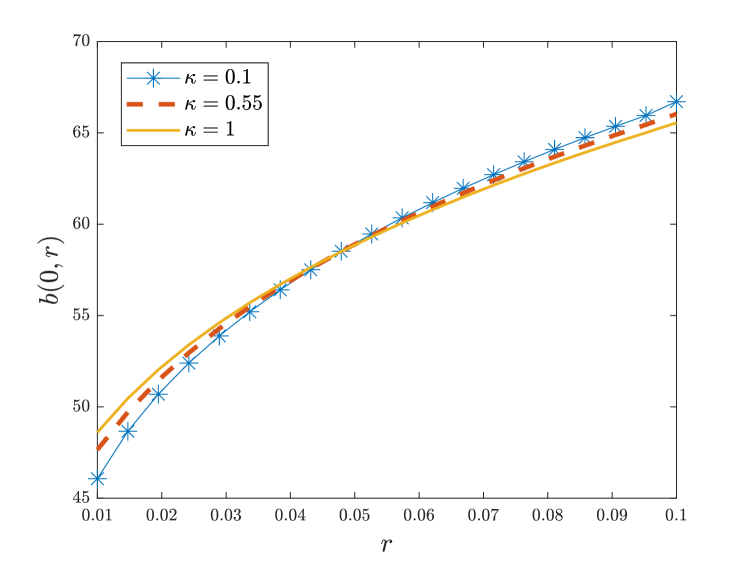

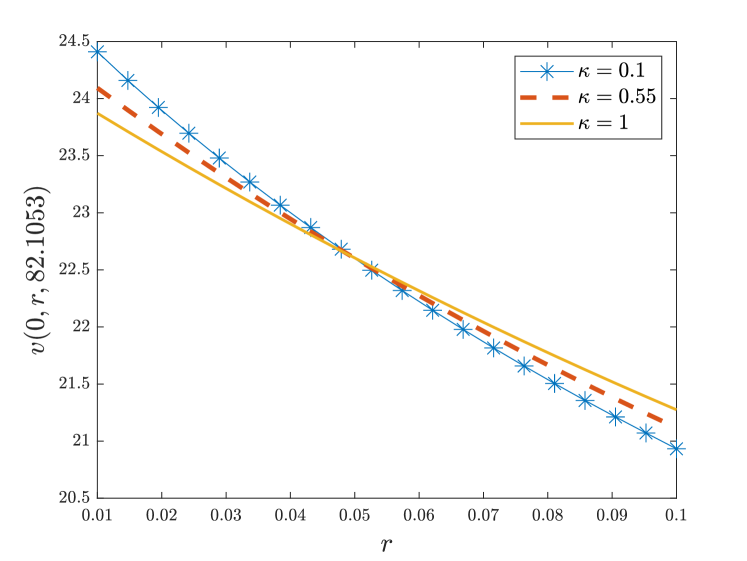

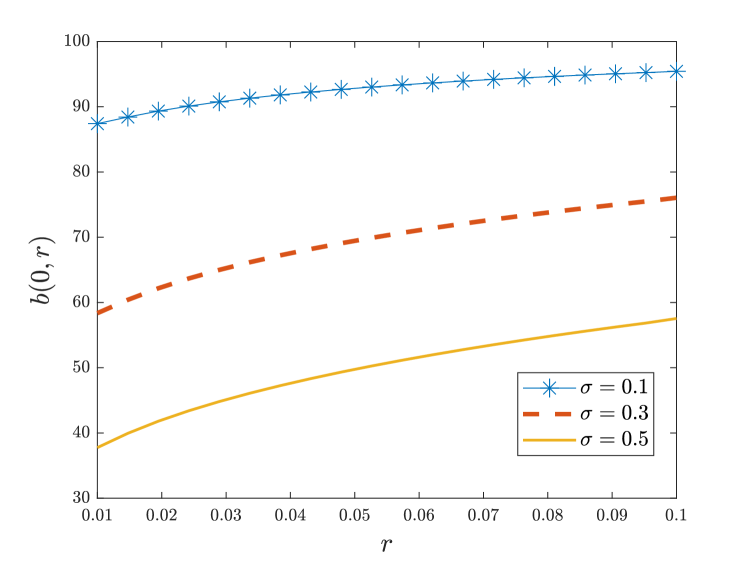

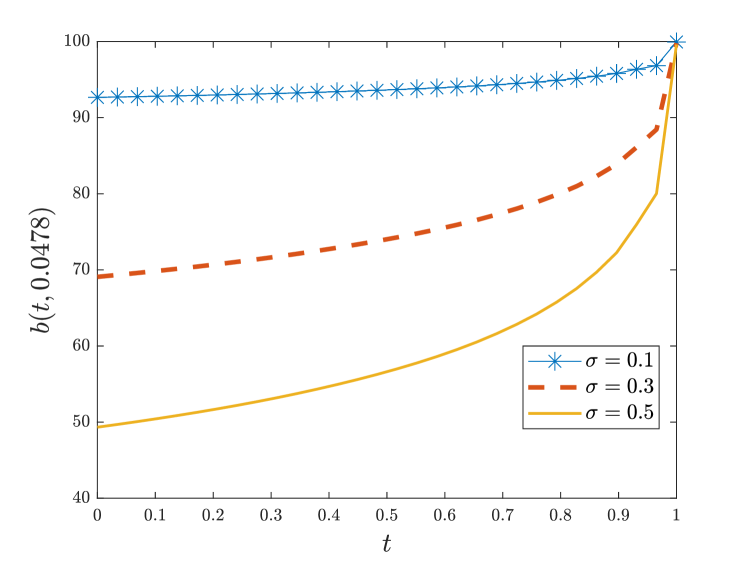

Figure 1 plots the stopping boundary using parameters (4.7). The optimal stopping boundary increases as tends to the maturity and as the interest rate grows (c.f. Proposition 3.4). This behaviour is consistent with the one of the optimal exercise boundary for the American put option in the Black-Scholes model with a constant interest rate (Peskir,, 2005). Figure 2 illustrates the value function via sections in directions of , and rooted at the point , which illustrates the findings of Proposition 3.1. In Panel (2(a)), the value decreases to the value of the immediate exercise as the option is purchased deep in the money.

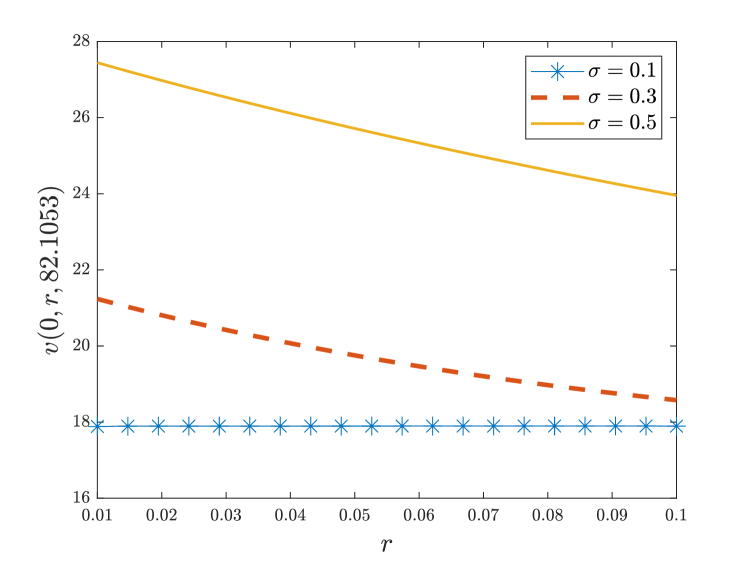

Effects of the interest rate. The option price is significantly affected by the initial interest rate (Panel (2(b))) because the maturity of the option is long (1 year). The effect depends on the mean-reversion coefficient and it increases when the mean reversion parameter decreases. Indeed, this tendency is clearly visible in Figure 3. A large mean-reversion speed () means that the interest rate is quickly pulled towards , diminishing the effect of the initial value. Taking expectation on both sides of (4.2) gives that the expected interest rate at the maturity is

which, for , means . On the contrary, we obtain for and so the effect of the initial interest rate on the stopping boundary (Figure 3(a)) and the value function (Figure 3(b)) is more pronounced. The optimal strategy for prescribes to be more patient compared to larger values of when the interest rate is near and act faster when the interest rate is close to . Indeed, with a slow mean-reversion the interest rate stays close to the current value for longer, so the observed behaviour of the stopping boundary and the of value function is akin to that observed by a model with a constant interest rate (Broadie and Detemple,, 1996; Peskir,, 2005).

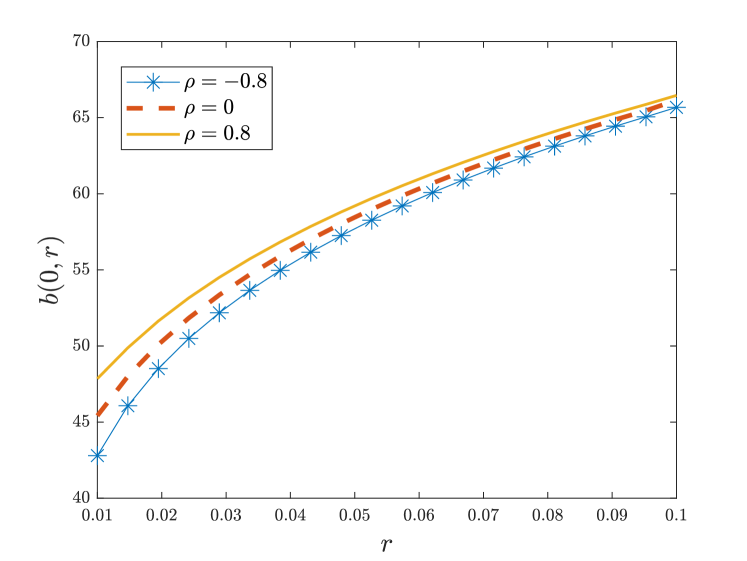

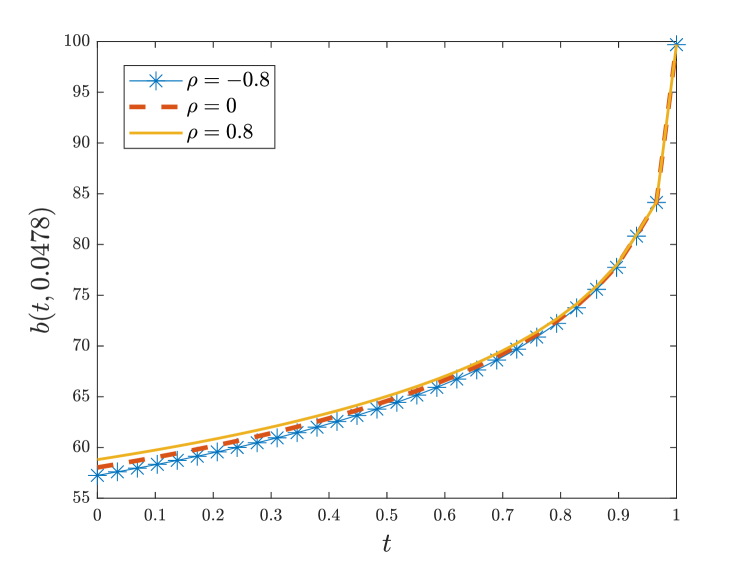

Effects of the correlation coefficient. The sensitivity of the stopping boundary with respect to the correlation coefficient between Brownian motions driving the stock price and the interest rate is displayed in Figure 4; the value function behaves accordingly and it is not displayed. High positive correlation implies that the interest rate and the stock price tend to move together. The increase in the interest rate pushes the stock price up and vice versa, resulting in a more unstable environment and an earlier optimal stopping. On the contrary, a strong negative correlation sees the stock price and the interest rate dampening the effect of each other’s moves: an increase in the stock price brings a drop in the interest rate, therefore, making longer waiting (lower stopping boundary) more desirable due to effect on the drift of the stock price as well as on the discount factor. Naturally, this effect diminishes the closer one gets to the maturity of the option, see Figure 4(b).

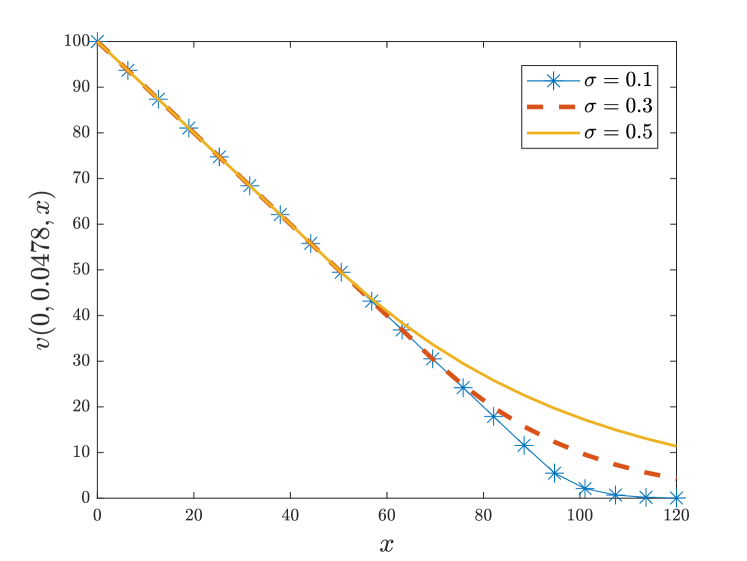

Effects of the volatility of stock and interest rate. The effect of the diffusion coefficient of the spot rate on the stopping boundary and on the value function is negligible. We compared results for , the range of values observed in empirical literature mentioned above. We noticed variations in the value function of less than and in the stopping boundary of less than .

In line with the financial intuition, the value of American Put option is increasing in , see Figure 5(c) and 5(d). When , the optimal stopping boundary is close to the exercise price (Figure 5(a)), so the option is immediately exercised for the initial stock price presented on Panel (c), hence the flat graph. For other values of , the exercise boundary is below the initial stock price and the effect of the interest rate is clearly visible. The structure of results in Figure 5 is, as expected, in line with the findings for the American Put option in the Black-Scholes model with constant interest rate (Broadie and Detemple,, 1996; Peskir,, 2005).

The remaining sections of the paper contain technical details and proofs.

5. Monotonicity and Lipschitz continuity of the option value

In this section we establish some initial regularity properties of the option value. We start with key monotonicity results and then prove Lipschitz continuity of the value function.

Proof of Proposition 3.1.

Finiteness of follows by (2.3) and boundedness of the put payoff. Monotonicity in is also a trivial consequence of the fact that the discounted put payoff is independent of time. For we argue as follows: since is increasing -a.s. for all (by uniqueness of the trajectories) we get, for any

where we took the discounting inside the positive part and used (2.5).

Finally, monotonicity in is a simple consequence of monotonicity of (2.5) with respect to and the fact that is decreasing. Convexity also follows by standard arguments: fix , take and in and denote . By the convexity of the put payoff, using that and that , it is not hard to verify that . ∎

Proposition 5.1.

(Lipschitz continuity). For any compact there exists a constant such that

| (5.1) |

for all and in .

Proof of Proposition 5.1.

We look separately at Lipschitz continuity in the three variables. Arguments for and are quite standard while the main argument for the Lipschitz continuity in goes back to (Jaillet et al.,, 1990, Thm. 3.6). However, in our framework the interest rate is random and the coefficients of the underlying process are state dependent, which results in some additional difficulties.

Continuity in . Fix and take in . Let and note that it is admissible for . Using Proposition 3.1(iii), the explicit expression for in (2.5) and the Lipschitz property of the put payoff, we get

where in the last equality we used Doob’s optional sampling theorem.

Continuity in . Fix and take in such that . Denote, for simplicity, and and notice that for all -a.s. Set . From Proposition 3.1(ii) and simple estimates we obtain

| (5.2) | ||||

To complete the proof we consider separately cases (i) and (ii) in Assumption 2.1. Let us start with : using that for , and the explicit form of the SDE in the CIR model, we get

where we have used the integral equation for and that .

If Assumption 2.1(ii) holds instead, we apply Hölder inequality:

| (5.3) | ||||

where is the constant from (2.3) which depends on . To conclude it is sufficient to use moment estimates for SDEs (Krylov,, 1980, Ch. 2, Sec. 5, Thm. 9) which guarantee that

| (5.4) |

for some only depending on and the coefficients in (2.2).

Continuity in . For , define and for . The couple is a strong solution to (see, e.g., (Bass,, 1998, Ch. 1, Prop. 8.6))

where . Using these processes, we can rewrite (2.6) as

| (5.5) |

where for any -stopping time in the random variable is an -stopping time. Since the process is identical in law to , with a slight abuse of notation we can identify with the unique strong solution of

| (5.6) | ||||

| (5.7) |

and take stopping times in (5.5) with respect to the filtration generated by . In what follows we denote by an optimal stopping time for (5.5).

Fix now and set , . Let and for denote also

so that . We remark that is also admissible for the problem in (5.5) and the underlying dynamics (5.6)–(5.7) with , because it is an -stopping time in . Indeed the advantage of (5.5) with (5.6)–(5.7) is that the class of admissible stopping times no longer depends on the initial time .

Recalling Proposition 3.1(i) and using Lipschitz continuity of we have

| (5.8) | ||||

Let us consider the second term on the right hand side of (5.8). By the fundamental theorem of calculus and the explicit formula for

| (5.9) |

For , define a measure by . Then is a Brownian motion under and

where we applied Hölder inequality and used that . Inserting the above estimate into (5.9) gives

| (5.10) |

Next we address the first term on the right hand side of (5.8). This is performed separately in cases (i) and (ii) of Assumption 2.1. We start by considering case (ii), i.e., and in (5.7) are Lipschitz continuous. Fundamental theorem of calculus and Hölder inequality give

| (5.11) | ||||

where, using (2.3),

Thanks to (2.4), , so it remains to estimate the last term of (5.11). By (Krylov,, 1980, Ch. 2, Sec. 5, Thm. 9) there is a constant depending only on and the Lipschitz constant for and in (5.7) such that

where for the second inequality we used that . Notice that by (2.4) and the linear growth of and

Inserting the above estimates into (5.11) we conclude that there is a constant such that for any

This and (5.10) feed into (5.8) so that

| (5.12) |

for a suitable that depends on .

Finally, we must estimate the first term on the right hand side of (5.8) under the assumption that follows the CIR dynamics (Assumption 2.1(i)). Let for and . The dynamics for reads

| (5.13) |

Since for , and , comparison results for SDEs (Karatzas and Shreve, 1998a, , Prop. 5.2.18) imply

| (5.14) |

Using the integral version of (5.13) and the martingale property of the stochastic integral, we obtain

Due to (5.14), the last term is non-positive, so

| (5.15) |

where

6. Properties of the free boundary

This section is devoted to establishing the existence of an optimal stopping boundary (free boundary) and some of its main properties. In particular we show the so-called ‘regularity’ of the stopping boundary in the sense of diffusion theory which, together with the monotonicity, is instrumental in our proof of global regularity of the value function .

Proof of Proposition 3.3.

The payoff does not depend on and is non-increasing in by Proposition 3.1. Therefore, if then for for any . This allows us to represent the stopping region via (3.1) with

| (6.1) |

with the convention that . It is convenient to prove (ii) first.

(ii) Fix . If we show that for some , then . This means that and . Recall that is the correlation coefficient between the Brownian motions and driving the SDEs for and , respectively. Then we can write for some other Brownian motion independent of . Letting be the filtration generated by , using the explicit form of the dynamics of we have

| (6.2) | ||||

where

and the final equality above holds by the independence of from and the fact that is -measurable. Since , then for any and we conclude that .

(i) By the monotonicity of in , we have for any , hence is non-increasing in .

Fix and let be optimal for . Then, using that and recalling (2.5), we obtain

Therefore, if then , which implies that is non-decreasing in .

Fix arbitrary , let as , then as , where the limit exists by the monotonicity of . Since , then also by the closedness of , hence which implies . Taking , a similar argument yields .

(iii) Under the CIR model, the positivity follows by the definition of . Only under Assumption 2.1 (ii) a proof is required. Assume that there exists such that . Let and . Define a stopping time

By the monotonicity of , we have . Hence, is sub-optimal and

| (6.3) |

where the last inequality follows from the optional sampling theorem and the fact that . Since and for , we obtain

which, in conjunction with (6.3), leads to a contradiction.

Finally, we show that for any if . Assume for some . By the monotonicity of and the openness of there is such that

where . Fix and . Take an arbitrary . Let

By construction , so -a.s. By the martingale property of the value function we obtain

| (6.4) | ||||

A contradiction is obtained by taking the limit , since is independent of and strictly smaller than since . ∎

An important consequence of Proposition 3.4 is that for

We immediately see that enjoys the so-called cone property (Karatzas and Shreve, 1998a, , Def. 4.2.18). Indeed, for any , there is an orthant with vertex in (hence a cone with aperture ) that satisfies . This will be used to establish regularity of the boundary in the sense of diffusions, which, has important consequences for the smoothness of our value function , as we shall see below.

To this end, we introduce the hitting time to , denoted , and the entry time to the interior of , denoted . That is, for we set -a.s.

| (6.5) | ||||

Both and are stopping times with respect to the filtration . We will often write and to indicate the starting point of the process.

Proposition 6.1 (Regularity of the boundary).

For , we have

| (6.6) |

The proof can be found in Appendix B. It rests on Gaussian bounds for the transition density of a diffusion and ideas from the proof of well-known analogous results for multi-dimensional Brownian motion, see e.g. (Karatzas and Shreve, 1998a, , Thm. 4.2.19). It is also worth recalling that is the boundary of in , so that it excludes .

7. Continuous differentiability of the option value

We start by establishing the following continuity properties of processes and .

Lemma 7.1.

Let be a sequence converging to as . Then

| (7.1) | ||||

| (7.2) |

Proof of Lemma 7.1.

Assume first that is a monotone sequence. Define . Then for a.e. , is continuous and converges to monotonically as for all . Hence the convergence is uniform on thanks to Dini’s theorem and (7.1) holds.

Lemma 7.2.

Let be a sequence in converging to as . Then

Proof of Lemma 7.2.

The proof relies on known facts from the theory of Markov processes, which we summarise in Appendix A for the reader’s convenience, combined with Proposition 6.1. Proposition 6.1 and Lemma 7.1 imply that Assumptions A.1 and A.2 are satisfied for . It is also immediate to see that -a.s. with defined in (A.1).

Next we provide gradient estimates based on probabilistic arguments.

Proposition 7.3.

Let be a compact set with non-empty interior. There is such that for any we have

| (7.3) | ||||

| (7.4) |

where .

Remark 7.4.

Later on we obtain also a bound on the derivative of the value function with respect to the interest rate. We present it separately in (7.19) because, due to the square root appearing in the diffusion coefficient of the CIR dynamics, we need to use local approximations of the stochastic dynamics of . That procedure does not lead to a neat expression as in (7.3) and (7.4).

Proof of Proposition 7.3.

Fix . Recall that . If then (7.3) follows easily from and . Assume and notice that , -a.s. We split the proof into two parts.

(Proof of (7.3)) For all sufficiently small we have . From now on, consider such . To simplify notation let . Using that is admissible and sub-optimal for we get

Dividing the above expression by and taking limits as we get

| (7.5) |

For the reverse inequality we use that is admissible and sub-optimal for :

where in the last inequality we used that , . Divide the above expression by and take limits as :

| (7.6) |

(Proof of (7.4)) The upper bound follows from the monotonicity of in (Proposition 3.1). For all sufficiently small we have and . From now on, consider such . Denote . Thanks to the choice of , the stopping time is admissible for . Using the (super)martingale property of (see (2.11)–(2.12)) we get

| (7.7) | ||||

where the equality follows from on since is non-decreasing (Proposition 3.4). Let . Fix a sufficiently small so that this set is contained in and set equal to the Lipschitz constant for on (c.f. Proposition 5.1). Since , we have for any . Using the Lipschitz continuity of , we bound (7) from below by

Dividing by and taking the limit completes the proof of (7.4). ∎

We are now ready to prove that the value function is globally continuously differentiable on .

Proof of Theorem 3.5.

It suffices to show that the value function has continuous partial derivatives across the stopping boundary, that is

| (7.8) | |||

| (7.9) |

for any sequence in converging to as . Fix such a sequence and denote .

Convergence of . Note that (Proposition 3.3) and (the final equality can be shown by arguments as in (6)). From Proposition 7.3 we therefore have

From Lemma 7.2, we obtain -a.s. We know from that . Lemma 7.1 and the continuity of trajectories of imply the convergence as . An application of the dominated convergence theorem completes the proof of (7.9).

Convergence of . Let be a closed ball centered on and contained in . With no loss of generality (by discarding a finite number of initial elements of the sequence) we assume that for all . Let

and notice, in particular, that . The boundary is regular for and by the same reasoning as in the proof of Proposition 6.1. Repeating arguments from the proof of Lemma 7.2 shows that , -a.s. Fix . Since , there exists such that . From inequality (7.4), we get

| (7.10) | ||||

Using that is bounded by some constant for every , we have

| (7.11) |

Lemma 7.2 guarantees that -a.s., so the first term converges to as by the dominated convergence theorem. Fatou’s lemma gives a bound for the second term:

where we used that and the convergence of the stopping times. We obtain the convergence of in (7.8) by sending .

Convergence of . Consider a sequence converging to . Since is the boundary of in , without loss of generality we can assume that

Denote , where and .

We know that on (Proposition 3.1). We will now develop a lower bound for on , which will allow us to show that as . Let be compact and such that . Denote for some . For we define

By the monotonicity of and the explicit expression (2.5) for we have, for all ,

from which it is not hard to verify that , -a.s., for all , where

Take . There is such that for all . Denote by the optimal stopping time for . For any , we apply the (super)martingale properties of the value function (2.11)-(2.12) with the stopping time :

| (7.12) | ||||

where for the final inequality we used that , -a.s. Recalling that and is non-negative we have

| (7.13) | ||||

where the second inequality comes from the local Lipschitz property of the value function ( is the constant from Proposition 5.1), and the function is bounded from above by a constant depending on , due to Assumption 2.1-(ii).

We shall now use the differentiability of the diffusion flow with respect to the parameter in the sense of (Krylov,, 1980, Ch. 2, Sec. 8, Thm. 6). Apart from other assumptions, this requires that the coefficients be globally Lipschitz. As we only consider in a compact set , we construct a two dimensional diffusion whose coefficients coincide with the coefficients of on , are globally Lipschitz, continuously differentiable and with a polynomial growth. The process is indistinguishable from on , i.e., on the set where it is of interest for the estimation of and , so for the sake of readability we will write in the estimates below (we use an analogous construction in Appendix B, where full details are available).

By (Krylov,, 1980, Ch. 2, Sec. 8, Thm. 6), there is a measurable in process , depending on , such that for any

| (7.14) |

where and .

Fix for some . Recalling that and using Hölder inequality yields

| (7.15) | ||||

where we used the estimate (2.3) in the last inequality and (7.14) to obtain the convergence.

To bound the last term on the right hand side of (7.13), we observe that

We then apply Hölder inequality and the second limit in (7.14):

| (7.16) | ||||

By the explicit formula (2.5), we have , where , and

We proceed similarly as in (7.16) to obtain

| (7.17) | ||||

Similar arguments as above enable us to derive a lower bound for :

| (7.18) | ||||

where in the first inequality we used the Lipschitz property of for any .

Combining (7.15)–(7.18) gives a lower bound for on :

| (7.19) | ||||

By (Krylov,, 1980, Ch. 2, Sec. 8, Thm. 8) and standard diffusion estimates (Krylov,, 1980, Ch. 2, Sec. 5, Cor. 10) the norms of and above are bounded uniformly for (recall that ). Now take in (7.19). Since -a.s. and -a.s. by Lemma 7.2, the dominated convergence theorem gives that the first two terms of (7.19) tend to zero as due to and the last term converges to zero because

and the mapping is continuous in the norm , see (Krylov,, 1980, Ch. 2, Sec. 8, Thm. 6). This concludes the proof. ∎

8. Continuity of the stopping boundary and the integral equation

Proof of Proposition 3.7.

Since on , it remains to prove the continuity at . It is known from Proposition 3.3 that is non-increasing and right-continuous at , and is non-decreasing and left-continuous at .

We first show that is right continuous at . It is obvious for since for . We proceed with an argument for . Assume, by contradiction, that , so there exist such that . Let for some and . From the monotonicity of , we have and . Let be a function defined on and satisfying

| (8.1) | ||||

Thanks to (Friedman,, 1964, Theorem 10, p. 72) we know that is on with Hölder continuous derivatives. Since the coefficients of (2.14) have Hölder continuous first derivatives, there is a unique classical solution of the above PDE (which is of elliptic type) and (Friedman,, 1964, Theorems 19 and 20, p. 87). From (3.3), the function satisfies (8.1), so, by uniqueness, on and by Theorem 3.5.

We differentiate the PDE in (8.1) with respect to and obtain

| (8.2) |

where

Let be a function with compact support on such that and for define

Multiply (8.2) by and integrate over :

Intergration by parts gives

| (8.3) | ||||

where and are adjoint operators to and , respectively. The expression above involves only and its first derivatives, which are continuous by Theorem 3.5. We take the limit in (8.3) and notice that , and . Thus,

where we also use that . Since is continuous on and , we have on for any sufficiently small . Using additionally that is , we perform the following integration

where we have used Fubini’s theorem in the first equality, in the second equality, in the third equality, and the integration by parts in the last equality. As the above inequality holds for an arbitrary smooth function with a compact support in , we must have almost everywhere on . This contradicts that is a non-increasing function (see Proposition 3.1), hence is continuous.

We turn our attention to the left-continuity of at (the right-continuity has already been established in Proposition 3.3). Assume, by contradiction, that the left-continuity fails at . Since is non-increasing, there exist such that . By the continuity of at and the monotonicity of , there is such that . Hence, for any sequence , we have

so that

Consider a PDE

| (8.4) | ||||

where denotes the parabolic boundary of . By (Friedman,, 1964, Theorem 6, p. 65), Equation (8.4) admits a unique classical solution , which coincides with on . This also implies that by Theorem 3.5.

Let be a function with compact support in and be a function with compact support in such that . Fixing from the sequence , we multiply (8.4) by and integrate over :

Integration by parts gives

| (8.5) |

where is the adjoint operator for . When , the first integral vanishes since and on . By the dominated convergence theorem, (8.5) reads

where we integrate by parts and use that on for the second equality. We obtain a contradiction because the last integral is strictly negative.

Having established the continuity in and separately, the monotonicity of allows us to conclude the continuity of at (see, e.g., Kruse and Deely, (1969)). ∎

Proof of Proposition 3.9.

Let be an increasing sequence of compact subsets of such that and define for large enough so that . We apply a version of Itô formula from (Cai and De Angelis,, 2021, Theorem 2.1), which we state in Appendix C for the reader’s convenience. We delay the verification of the assumptions required until the end of the proof. Using that

| (8.6) | |||||

we obtain that the dynamics of the discounted value function on is given by

| (8.7) | ||||

Taking expectations and applying the optional sampling theorem we arrive at

| (8.8) |

Using (2.3) and (2.4), Hölder inequality implies

The majorant for the second term of (8.8) follows from Assumption 2.1 (details can be found in the proof of (9.1) in Lemma 9.1). The dominated convergence theorem proves (3.4), since upon recalling that the boundary of is assumed non-attainable by the process .

It remains to verify assumptions of (Cai and De Angelis,, 2021, Theorem 2.1) as stated in Appendix C. Identifying and , we have,

By Assumption 2.1, is Lipschitz for on every compact set in . Indeed, it can be directly verified for the CIR process. In case (ii) of Assumption 2.1 we use Lipschitz continuity of . The marginal distribution of the process has density with respect to the Lebesgue measure (see Remark B.1, which makes use of Assumption 3.8), so , -a.s. for any . Setting , this verifies the first assumption in the theorem in Appendix C. For the second assumption, using (8.6), we have

Since and the function is continuous (see Assumption 2.1), is continuous and bounded on . We finally have that the third assumption in the theorem holds by Proposition 3.3. ∎

Proof of Proposition 3.11.

The proof follows ideas originally developed in Peskir, (2005). Assume there exists another continuous function that satisfies conditions (1) and (2) in the statement of this proposition. Define a function

It is not difficult to prove that is continuous by the continuity of and of the flow . By the Markov property of , one can also check that

is a continuous -martingale. Hence, for any and any stopping time , the optional sampling theorem yields

| (8.9) |

which is analogous to the formula for in (3.4).

For an easier exposition of the arguments of proof we proceed in steps. In the first four steps we show the equality for all such that . Then, in the final step we use monotonicity and continuity of and to extend the equality to all .

Step 1. We first show that for any such that . Fix such that (the claim for follows by the continuity of ). Define a stopping time

By the continuity of and , and the fact that and are unattainable by , we have on . By assumption and, consequently, since . In combination with (8.9), this yields

| (8.10) |

where we use that on . Applying Tanaka’s formula to and taking expectation, we get

where is the local time of the process at . The local time is null until since , recalling that when . Compare the right-hand side of the above expression to (8.10) to conclude that .

Step 2. The next step is to show that for . Since we have already proved when , we take such that . Define a stopping time

Since on , we obtain from (8.9)

where the first equality is by and the final inequality holds by the definition of .

Step 3. Now we show that for any such that (it is immediate for as ). Arguing by contradiction, assume that there exists such that . Let , and define

Since , on , and , the above two equations imply that

As the function is non-negative, on and we conclude that

| (8.11) |

The dynamics of is non-degenerate on , so the density of has a full support (on ) for (this can be inferred by classical Gaussian bounds as those we use in (B.4) in Appendix). Hence, by the continuity of and , for a sufficiently small ,

Paired with the continuity of trajectories of , it contradicts (8.11).

Step 4. Next, we prove at all points such that . Arguing by contradiction, assume for some such that . Let and define

where in the first expression we used that on . Since for , we have by step 1. Then recalling that and comparing the two equations above give us

This is a contradiction since by the continuity of and there is a random variable such that

Step 5. Here we show that on . Let be a sequence such that and with (respectively , if ; note that , so if ). Since for all ’s, by the four steps above, by continuity we also get (respectively , if ). Then, by the monotonicity of both and we get for all (respectively ). This implies, in particular, that

which concludes the proof. ∎

9. Hedging strategy

We start this section with an auxiliary lemma whose assertions are used to show admissibility of the hedging strategy. Estimate (9.1) is also used in the proof of Proposition 3.9.

Lemma 9.1.

For any compact set , and , we have

| (9.1) | ||||

| (9.2) | ||||

| (9.3) |

Proof.

From (2.6) we obtain an upper bound for the function :

| (9.4) |

Using this bound, we have -a.s.

where in the second equality we employ the Markov property of . By Doob’s maximal inequality applied to the martingale , we conclude

where is the constant from (2.3). This proves (i).

We now address (9.2). We have

where we use in the last inequality, which follows from (7.3). From here, (9.2) is immediate.

It remains to prove (9.3). First we consider the case of Assumption 2.1(ii). From (5.2), (5.3) and (5.4), we deduce

| (9.5) |

for some constant depending only on and the coefficients of (2.2) (notice in particular that the expected value in the right-hand side above comes from the constant in (5.3)). Hence

where the last inequality is by the same argument as in the proof of (9.1). We take expectation of both sides and apply Hölder inequality with ( is defined in Assumption 2.1) and

where the second inequality follows from Jensen’s inequality and is the constant from (2.3). Let be the Lipschitz constant for . Then, using triangle inequality for norms,

where the last inequality follows from (2.4) and . Combining the above estimates proves (9.3).

Proof of Proposition 3.13.

Acknowledgment: C. Cai gratefully acknowledges support by China Scholarship Council. T. De Angelis gratefully acknowledges support by EPSRC grant EP/R021201/1.

Appendices

Appendix A Convergence of stopping times

In this appendix we provide a self-contained exposition around the continuity of hitting/entry times to certain domains in . Similar results can be found in many textbooks, e.g., (Dynkin,, 1965, p. 32-40), (Blumenthal and Getoor,, 1968, Chapter 1).

Throughout this section, denotes a subset of that is closed in , i.e., . Introduce the hitting time to , denoted , and the entry time to the interior of , denoted . That is, for , we set -a.s.

| (A.1) | ||||

The above definition differs from (6.5) since guaranteeing that . Both and are stopping times with respect to the augmentation of the filtration generated by the Brownian motions . It is immediate to see that

| (A.2) |

We will often write and to indicate the starting point of the process.

Denote by the complement of in : (which is an open set). When we write we mean the boundary of in . We have two assumptions

Assumption A.1 (Regularity).

For , we have

Assumption A.2.

For any sequence converging to as , it holds that

| (A.3) |

Note that Assumption A.1 necessitates that . It also enables establishing a connection between and .

Lemma A.3.

Under Assumption A.1, for all .

Proof.

The equality is trivial for . Take in its complement, i.e., in . Since (A.2) holds, we only need to show that . Let us argue by contradiction and assume that . There exists such that . Denoting by the shift operator, by the strong Markov property we get

where the last equality follows by observing that , -a.s. and Assumption A.1. ∎

Lemma A.4.

Let as . Under Assumption A.2, it holds -a.s.

Proof.

For simplicity, we denote and . For -a.e. we have by (A.3)

| (A.4) |

Fix in the set of -full measure for which the above holds. If then the result is obvious because . Assume . Take any such that . By the continuity of paths and the openness of , there is such that . From (A.4) and the openness of , for all sufficiently large , so . As the above argument holds for any and for a.e. , we obtain the claim. ∎

Proof.

For we denote by their Euclidean distance and by . Denote and . To simplify notation we also set

Fix in a set of full -measure on which trajectories of are continuous and the limit (A.3) holds. If then (A.5) holds trivially. Otherwise, we must have by Assumption (A.1), so since is open. For , define

Using the triangle inequality we get for all . Thanks to Assumption A.2, for all and all sufficiently large , so for all and all sufficiently large . This gives

Using the continuity of and the fact that , we have . As this holds for a.e. , the proof of (A.5) is complete. ∎

Proposition A.6.

Let be a sequence converging to as . Then

| (A.6) | ||||

Appendix B Proof of Proposition 6.1

Fix and define , where we also recall that . Since is non-increasing, it is immediate to see that . Recalling the notation introduced in (A.1), set

We have , -a.s., and by the continuity of the process . From now on we omit in the notation the dependence on since the initial point is fixed throughout the proof.

Take a compact ball centred at . Let denote the matrix of the diffusion coefficient for (2.1)–(2.2), i.e.

Since the correlation coefficient , there is such that

| (B.1) |

where denotes the scalar product in and the corresponding norm.

Define a new process with the dynamics defined on

| (B.2) | ||||

| (B.3) |

such that the coefficients coincide with the coefficients of (2.1)-(2.2) on , are Lipschitz continuous on and satisfy the uniform ellipticity condition (B.1) with on . Denoting and , by the uniqueness of solutions for SDEs we get indistinguishable stopped paths:

The uniform ellipticity condition (B.1) on implies that the process admits a transition density which satisfies the following Gaussian bound (see, e.g., Aronson, (1967); Fabes and Stroock, (1989)): there exists and such that

| (B.4) |

Let be a closed cone with vertex and non-empty interior contained in . Put . Denote by the entry time of to and by the entry time of to . The next estimate relies on analogous results for multi-dimensional Brownian motion (Karatzas and Shreve, 1998a, , Thm. 4.2.9); in particular the second inequality below follows from (B.4):

We change variables to and and use that this transformation maps into to obtain

| (B.5) |

For any , since we have

where the last inequality is by (B.5). As , we have and , which implies that . By the Blumenthal law (Karatzas and Shreve, 1998a, , Thm. 2.7.17) we obtain . Recalling that , and , we conclude .

Remark B.1.

It is worth noticing that the arguments above show the existence of the transition density of the process for any compact set such that . This implies that for each also the law of is absolutely continuous with respect to the Lebesgue measure on , when the boundary of is unattainable by . Indeed, let be such that , with denoting the Lebesgue measure on . Let be a compact set such that . Then by the same construction as above

| (B.6) | ||||

where the final equality uses that the transition law of is absolutely continuous with respect to . Now, letting , using that and are not attainable by and and are not attainable by , we can make arbitrarily small, which proves the claim.

Appendix C Generalisation of Itô’s formula

Here we state a particular case of (Cai and De Angelis,, 2021, Theorem 2.1) using notations appropriate for our set-up. We set . Let be a two-dimensional standard Brownian motion and denote the unique strong solution of

Let and denote for some function . Here . Then the theorem reads as follows:

Theorem C.1.

Assume the following:

-

(1)

The coefficients are locally Lipschitz and for a.e. ;

-

(2)

A function is such that with . Moreover, for any compact subset the function

is bounded for . That is, there exists such that

-

(3)

The mappings and are monotonic.

Then, we have the change of variable formula:

Appendix D Derivation of (4.4)-(4.5)

We start by introducing the following notation (we suppress dependence on and for the sake of simplicity):

| (D.1) | ||||

Lemma D.1.

For a measurable bounded function and , the function

has an explicit representation

| (D.2) |

where

We defer the proof until the end of this section and apply the above lemma to derive formulae for , and . Taking in (D.2), we have

| (D.3) |

This also implies that

Insert this and (D.3) into (D.2) and let

This transforms the integral in (D.2) into an integral of two independent Gaussian variables

| (D.4) |

Proof of Lemma D.1.

The proof follows the lines of similar computations in the literature, see Baxter and Rennie, (1996) and Detemple and Tian, (2002). Using the explicit expression of in (4.2) and stochastic Fubini’s theorem (Protter,, 2005, Theorem IV.64), we compute

| (D.5) | ||||

Define implicitly by

Then is a Brownian motion that is independent of . Using the explicit expression of and (D.5), we write as

| (D.6) | ||||

Define a new measure by the Radon-Nikodym density

The process given by

is a Brownian motion under . We write the explicit formula (D.5) for in terms of :

Denoting by the expectation under , we obtain from (D.6)

| (D.7) |

where

For each fixed , the random vector is multivariate Gaussian under with zero mean, and variance and covariance given by

Hence, we have an explicit integral representation of (D.7)

| (D.8) | ||||

A change of variable yields (D.2). ∎

Acknowledgements

C. Cai gratefully acknowledges support by China Scholarship Council. T. De Angelis gratefully acknowledges support by EPSRC Grant EP/R021201/1. All authors would like to thank Sheng Wang for drawing our attention to gaps in the proofs of Propositions 3.3 and 3.11.

References

- Amin and Bodurtha Jr, (1995) Amin, K. I. and Bodurtha Jr, J. N. (1995). Discrete-time valuation of American options with stochastic interest rates. The Review of Financial Studies, 8(1):193–234.

- Amin and Jarrow, (1992) Amin, K. I. and Jarrow, R. A. (1992). Pricing options on risky assets in a stochastic interest rate economy. Mathematical Finance, 2(4):217–237.

- Appolloni et al., (2015) Appolloni, E., Caramellino, L., and Zanette, A. (2015). A robust tree method for pricing American options with the Cox–Ingersoll–Ross interest rate model. IMA Journal of Management Mathematics, 26(4):377–401.

- Aronson, (1967) Aronson, D. G. (1967). Bounds for the fundamental solution of a parabolic equation. Bulletin of the American Mathematical Society, 73(6):890–896.

- Bass, (1998) Bass, R. F. (1998). Diffusions and elliptic operators. Springer Science & Business Media.

- Battauz and Rotondi, (2019) Battauz, A. and Rotondi, F. (2019). American options and stochastic interest rates. Working Paper.

- Baxter and Rennie, (1996) Baxter, M. and Rennie, A. (1996). Financial calculus: an introduction to derivative pricing. Cambridge University Press.

- Bensoussan, (1984) Bensoussan, A. (1984). On the theory of option pricing. Acta Applicandae Mathematica, 2(2):139–158.

- Blumenthal and Getoor, (1968) Blumenthal, R. and Getoor, R. (1968). Markov Processes and Potential Theory. Academic Press, New York.

- Broadie and Detemple, (1996) Broadie, M. and Detemple, J. (1996). American option valuation: New bounds, approximations, and a comparison of existing methods. The Review of Financial Studies, 9(4):1211–1250.

- Cai and De Angelis, (2021) Cai, C. and De Angelis, T. (2021). A change of variable formula with applications to multi-dimensional optimal stopping problems. arXiv:2104.05835.

- Cai et al., (2021) Cai, C., De Angelis, T., and Palczewski, J. (2021). On the continuity of optimal stopping surfaces for jump-diffusions. Preprint.

- Carr et al., (1992) Carr, P., Jarrow, R., and Myneni, R. (1992). Alternative characterizations of American put options. Mathematical Finance, 2(2):87–106.

- Chung, (2000) Chung, S.-L. (2000). American option valuation under stochastic interest rates. Review of Derivatives Research, 3(3):283–307.

- De Angelis and Peskir, (2020) De Angelis, T. and Peskir, G. (2020). Global regularity of the value function in optimal stopping problems. Annals of Applied Probability, 30(3):1007–1031.

- Detemple et al., (2018) Detemple, J., Kitapbayev, Y., and Zhang, L. (2018). American option pricing under stochastic volatility models via Picard iterations. Working paper.

- Detemple and Tian, (2002) Detemple, J. and Tian, W. (2002). The valuation of American options for a class of diffusion processes. Management Science, 48(7):917–937.

- Dynkin, (1965) Dynkin, E. (1965). Markov Processes, volume 2. Academic Press, New York.

- Fabes and Stroock, (1989) Fabes, E. and Stroock, D. (1989). A new proof of Moser’s parabolic Harnack inequality using the old ideas of Nash. In Analysis and Continuum Mechanics, pages 459–470. Springer.

- Fergusson and Platen, (2015) Fergusson, K. and Platen, E. (2015). Application of maximum likelihood estimation to stochastic short rate models. Annals of Financial Economics, 10(02):1550009.

- Friedman, (1964) Friedman, A. (1964). Partial Differential Equations of Parabolic Type. Prentice-Hall.

- Geske and Johnson, (1984) Geske, R. and Johnson, H. E. (1984). The American put option valued analytically. The Journal of Finance, 39(5):1511–1524.

- Heath et al., (1992) Heath, D., Jarrow, R., and Morton, A. (1992). Bond pricing and the term structure of interest rates: A new methodology for contingent claims valuation. Econometrica, pages 77–105.

- Ho et al., (1997) Ho, T. S., Stapleton, R. C., and Subrahmanyam, M. G. (1997). The valuation of American options with stochastic interest rates: A generalization of the Geske-Johnson technique. The Journal of Finance, 52(2):827–840.

- Hull, (2009) Hull, J. (2009). Options, futures and other derivatives. Upper Saddle River, NJ: Prentice Hall.

- Jacka, (1991) Jacka, S. (1991). Optimal stopping and the American put. Mathematical Finance, 1(2):1–14.

- Jaillet et al., (1990) Jaillet, P., Lamberton, D., and Lapeyre, B. (1990). Variational inequalities and the pricing of American options. Acta Applicandae Mathematica, 21(3):263–289.

- Jeanblanc et al., (2009) Jeanblanc, M., Yor, M., and Chesney, M. (2009). Mathematical methods for financial markets. Springer Science & Business Media.

- Karatzas, (1988) Karatzas, I. (1988). On the pricing of American options. Applied Mathematics & Optimization, 17:37–60.

- (30) Karatzas, I. and Shreve, S. E. (1998a). Brownian Motion and Stochastic Calculus. Springer.

- (31) Karatzas, I. and Shreve, S. E. (1998b). Methods of mathematical finance, volume 39. Springer.

- Kim, (1990) Kim, I. J. (1990). The analytic valuation of American options. The Review of Financial Studies, 3(4):547–572.

- Kim et al., (2013) Kim, I. J., Jang, B.-G., and Kim, K. T. (2013). A simple iterative method for the valuation of American options. Quantitative Finance, 13(6):885–895.

- Kruse and Deely, (1969) Kruse, R. and Deely, J. (1969). Joint continuity of monotonic functions. The American Mathematical Monthly, 76(1):74–76.

- Krylov, (1980) Krylov, N. (1980). Controlled Diffusion Processes. Springer.

- Little et al., (2000) Little, T., Pant, V., and Hou, C. (2000). A new integral representation of the early exercise boundary for American put options. Journal of Computational Finance, 3:73–96.

- McKean Jr, (1965) McKean Jr, H. P. (1965). A free boundary problem for the heat equation arising from a problem of mathermatical economics. Industrial Management Review, 6:32–39.