A robust specification test in linear panel data models

Abstract

The presence of outlying observations may adversely affect statistical testing procedures that result in unstable test statistics and unreliable inferences depending on the distortion in parameter estimates. In spite of the fact that the adverse effects of outliers in panel data models, there are only a few robust testing procedures available for model specification. In this paper, a new weighted likelihood based robust specification test is proposed to determine the appropriate approach in panel data including individual-specific components. The proposed test has been shown to have the same asymptotic distribution as that of most commonly used Hausman’s specification test under null hypothesis of random effects specification. The finite sample properties of the robust testing procedure are illustrated by means of Monte Carlo simulations and an economic-growth data from the member countries of the Organisation for Economic Co-operation and Development. Our records reveal that the robust specification test exhibit improved performance in terms of size and power of the test in the presence of contamination.

Keywords: Panel data; Model specification; Hausman test; Robust estimation; Least squares.

1 Introduction

The attraction of panel data relies on the use of individual-specific components in the models such that these models allow to focus particularly on explaining within variations over time and control over individual heterogeneity as noted in Beyaztas and Bandyopadhyay (2020). The most commonly used statistical approaches that include individual-specific components are the fixed effects and random effects models (also called error component models, cf. Bălă and Prada (2018) and Zhang (2010)). The individual-specific heterogeneity is explained by the differences in the error variance components in random effects model while this heterogeneity is assumed to be fixed and reflected using time-invariant intercept terms in the fixed effects model. As pointed out by Mundlak (1978), the major difference between the fixed effects and random effects specifications is that a limited form of endogeneity may occur in fixed effects model, namely, the individual-specific effects are permitted to be correlated with the regressors whereas such correlation is not allowed to be in random effects model (cf. Cameron and Trivedi (2009)).

The inclusion of the individual-specific components in panel data regression models requires a critical decision on how to treat individual- specific effects relying on an assumption on whether or not regressors are correlated with the unobserved effects. As noted in Baltagi (2005), this assumption is important when the individual-specific effects are included in the error component models as a part of the disturbance since those effects may be unobservable and correlated with the columns of explanatory variables. In this case, the strict exogeneity assumption pertaining to random effects model is violated. This results in obtaining biased and inconsistent estimates of the parameters when the least squares (OLS) and generalized least squares (GLS) methods are used (cf. Hausman and Taylor (1981)). To overcome this issue, one way is to use fixed effects transformation for the mean centered data by eliminating the individual-specific effects. At this stage, the fixed effects estimator yields unbiased and consistent estimates of the regression parameters in fixed effects models. However, using this transformation has two shortcomings: () it wipes out all time-invariant variables, thus, the fixed-effects estimator is incapable of estimating the coefficients corresponding to these variables, () under some conditions, the fixed effects estimator may be inefficient since it only exploits the variation within each cross sectional unit (cf. Hausman and Taylor (1981)). If the accuracy and precision of some well-known panel data estimators are investigated for random effects specification, the GLS method provides a prominent estimator with more efficient estimates and high explanatory power of the model compared to the fixed effects method although both estimators are consistent. As a consequence, all indicate that any failure to account for those individual-specific effects may lead us to unreliable results with poorly fitted models, using biased and/or inefficient estimates of the parameters when making statistical inferences in linear panel data regression models. Thus, the panel specification testing has become an important issue in typical fields of applied economics and econometrics such as growth models, international trade, purchasing power parity tests, environmental economics when choosing an appropriate approach between fixed effects and random effects specifications (cf. Herwartz and Neumann (2007)).

A core task in panel specification testing is to check the assumption against correlation between individual-specific effects and the explanatory variables when determining the appropriate approach between two principle approaches, i.e., fixed effects and random effects estimators (also called within and GLS estimators, respectively). Therefore, it is crucial to have a method in testing this assumption (cf. Wooldridge (2002)). In static linear panel data models, a testing procedure based on the difference between the random effects and fixed effects estimates has been proposed by Hausman (1978) for the orthogonality assumption of the individual effects and explanatory variables.

The Hausman’s specification test has become a prominent procedure for the purposes of model selection and the evaluation of parameter estimates, depending on the trade-off between accuracy and precision of fixed effects and random effects estimators, especially in most applications of economics and econometrics since the 1980s (see Jirata et al. (2016)). A similar test with the Hausman’s specification test, using limited information technique, has been proposed by Spencer and Berk (1981) for testing the misspecification in a single equation of a simultaneous system equation. Additionally, alternative expressions yielding numerically identical results with the Hausman test have been developed by Hausman and Taylor (1981) based on the following paired differences: () within and between estimators, () random effects and between estimators. Indeed, the numerical identicality of Hausman’s test and Hausman and Taylor (1981)’s tests can be demonstrated by the well-known results of Maddala (1971) as noted in Arellano (1993). Following this study, some extended methods using those expressions have been developed by Metcalf (1996) and Frondel and Vance (2010) for the purposes of constructing novel specification testing. Metcalf (1996) proposes an extension of the specification test suggested by Hausman and Taylor (1981) by utilizing the different sets of instrumental variables depending on the sample size in the context of panel data models including endogeneity. A variant of Hausman specification test, which allows to investigate for the equality of all coefficients in considered two models and that of individual variables, has been developed by Frondel and Vance (2010) using numerically identical procedure of Hausman and Taylor (1981). Several procedures have been proposed considering the robustness against departures from the assumptions on the errors; see, for instance, Arellano (1993), Ahn and Low (1996) and Chen et al. (2018). An alternative variable addition test to the Hausman’s test, as a Wald test in an extended regression model, has been suggested by Arellano (1993) by using robust variance-covariance matrix of White (1984), and the proposed test statistics are robust to the presence of heteroskedasticity and serial correlation. Ahn and Low (1996) have derived a reformulation of the Hausman test based on a Generalized Method of Moment (GMM) approach and they propose an alternative GMM statistic, which is equal to the Wald test developed by Arellano (1993), by including the extended set of moment restrictions. The authors show that their proposed test has similar performance with the Hausman’s test in determining the endogenous regressors but it exhibits improved performance with better power compared to the Hausman’s test when detecting nonstationary coefficients. Also, two Hausman type test statistics, which are robust against the correlation between the covariates and the effects and based on the comparison of the variance estimators of idiosyncratic error at different robust levels, have been established by Chen et al. (2018) in the presence of individual and time effects for the panel data regression models.

Recently, some bootstrap approaches have been proposed in the context of specification testing in panel data. A bootstrap method which utilizes a feature of wild bootstrap to deal with heteroskedasticity of disturbances and inhomogeneity of serial correlation has been proposed by Herwartz and Neumann (2007) in generating the critical values for Hausman statistic when testing the null hypothesis of Hausman’s test. Also, Bole and Rebec (2013) propose to use bootstrap method to improve the performance of Hausman testing in static panel data models and they demonstrate that the asymptotic convergence of both Hausman test statistic and its bootstrapped version using Edgeworth expansion. Moreover, a robust regression based Hausman specification test for unbalanced panel data with the inclusion of endogenous regressors has been built by Joshi and Wooldridge (2017) using the comparison between random effects two stage least squares (RE2SLS) and fixed effects two stage least squares (FE2SLS) estimators.

Most of the attention has been paid to robust estimation although the researches on the robustness of testing procedures dates back to 1931 as noted in Agostinelli and Markatou (2001). However, the advantages of using robust test procedure are two-fold: (a) level of the test remains stable due to any departures from the null hypothesis (robustness of validity) and (b) power of the test maintains to be good against the departures from the alternative hypothesis ( robustness of efficiency) as pointed out by Agostinelli and Markatou (2001). To the best of our knowledge, the literature considering the robustness of specification tests especially in the presence of outliers remains quite limited within the framework of static linear panel data models.

This paper aims to study the effects of outliers on the Hausman specification test results in static panel data models. We propose to build a robust version of Hausman specification test using weighted likelihood based fixed effects estimator proposed by Beyaztas and Bandyopadhyay (2020) that are robust against the various types of outliers and asymptotically consistent with the corresponding least squares based estimator. It is shown that the new specification test based on the distance between conventional random effects and weighted fixed effects estimators of Beyaztas and Bandyopadhyay (2020) is asymptotically equivalent to the Hausman specification test under the null hypothesis. Also, we investigate the size and power of the proposed test in the presence of random and clustered vertical outliers when testing the orthogonality of regressors and individual effects. Monte Carlo experiments demonstrate that the proposed testing procedure yield better power compared to traditional one when the data include outlying observations.

The rest of the paper is organized as follows. Section 2 presents a detailed information on the linear panel data models, OLS and weighted likelihood based estimation methods. In Section 3, we describe our specification testing procedure which uses weighted likelihood based fixed effects estimator, followed by a discussion on large sample properties of the Hausman’s specification test and proposed test in Section 4. An extensive Monte Carlo simulation is performed to investigate the finite sample properties of the proposed testing procedure, and the results are compared with traditional Hausman test in Section 5. To illustrate the applicability of the methodology, we apply our proposed test and traditional one to the economic-growth data obtained from the member countries of the Organisation for Economic Co-operation and Development (OECD) in Section 6. Section 7 concludes the work with some remarks.

2 Linear Panel Data Models and Estimation

A linear panel data regression model is given by

| (2.1) |

where the subscript represents an individual observed at time , is a vector of the regression parameters, and ’s denote the dependent variable and the -dimensional vectors of independent variables, respectively and ’s denote the compound error terms. A one-way error component model for the error terms can be written as

| (2.2) |

where ’s represent the unobservable individual-specific effects and ’s denote the independent and identically distributed (iid) error terms with , and for , respectively. The panel data regression model can be represented in a vector form as follows

| (2.3) |

where is an vector obtained by stacking observations for individual , is . Also, Equation 2.2 can be expressed as

| (2.4) |

where obtained by stacking observations for , is a matrix of individual dummies with and being an identity matrix of dimension and a vector of ones, respectively and denotes the kronecker product. The matrix of individual dummies may be included for the estimation of ’s in fixed effects panel data models.

In fixed-effects models, individual-specific effects ’s, belonging to each cross-sectional unit, are assumed to be fixed and included as time-invariant intercept terms. Those time-invariant characteristics of individuals are allowed to be correlated with the explanatory variables by including dummy variables for different intercepts, allowing a limited form of endogeneity in fixed-effects panel data regression models (cf. Cameron and Trivedi (2009)).

The following representation of the model can be obtained by substituting the Equation 2.4 into the Equation 2.3 as

| (2.5) |

and the estimates of and are obtained by the OLS method. The least squares dummy variable (LSDV) estimators can be obtained from the model given in Equation 2.5. However, since the parameter of interest to estimate is , by multiplying the system by the within-groups operator , the transformed model is obtained as

where denotes a matrix, which results in obtaining the deviations from individual means, and represents a matrix providing the averages of observations over time for each individual. In fact, this turns into a regression model of with the elements on with for the kth explanatory variable where and respectively, denote the time averages of and for the -th cross-sectional unit, so that the individual-specific effects have been eliminated. Then, by employing OLS method on the transformed model, the fixed effects estimator of can be obtained as

with . The within-group transformed model for the mean centered data can be expressed in a regression form as follows

where , and obtained using the time averages of , and for each-cross sectional unit: , and . Then, the fixed effects estimator can be reobtained as

with

The variation from observation to observation in each cross-sectional unit, i.e., within variation is exploited in fixed-effects approach (cf. Bălă and Prada (2018) and Kennedy (2003)). Hence, if the variation within each cross-sectional unit is small or does not exist, the parameters of the fixed-effects models cannot be correctly estimated as noted in Cameron and Trivedi (2009). Both between variation, i.e., the variation in observations from an individual unit to another individual unit, and within variation over time are taken into account by the random-effects models. Also, when the number of individuals randomly drawn from a population is significantly large, the fixed-effects model may result in a large loss of degrees of freedom and the fixed effects estimators of ’s may become biased and inconsistent due to the increasing number of those parameters (cf. Baltagi (2005) and Greene (2003)). In this case, the random-effects specification is an appropriate choice for modelling panel data as noted in Baltagi (2005).

The individual heterogeneity is treated as the differences in the error variance components and thus, a part of disturbance terms comprises the individual-specific effects ’s in random-effects models. If s are assumed to be random then, under an additional assumption of with and , the random-effects model can be explained as in Equation 2.1.

In order to estimate the regression coefficients in random-effects models, GLS is an appropriate method to deal with serial correlation in the compound error terms ’s (Wooldridge (2002)). The GLS estimator (or random effects estimator) is expressed as

where represents the variance-covariance matrix of compound error terms defined as

where with and being identity matrices of dimension and , respectively (cf. Hausman (1978), Wooldridge (2002) and Beyaztas and Bandyopadhyay (2020)).

To express the GLS method in a regression form, the quasi-demeaning transformation of the variables is required to ensure homoscedasticity of the variance-covariance matrix as noted in Hausman (1978), Croissant and Millo (2008), Jirata et al. (2016) and Beyaztas and Bandyopadhyay (2020). The time-averages of the variables weighted by are subtracted from the original variables, i.e., , and , in obtaining the transformed version of the random effects model defined as follows

Then, by performing OLS method on this model, the random effects estimator can be reobtained as

with .

The fixed effects and random effects estimators provide consistent estimates under random effects specification. However, random effects estimator yields more efficient results than those of fixed effects estimator. This superiority of random effects estimators stems from using both within and between variations as noted in Beyaztas and Bandyopadhyay (2020). However, the random effects estimator produces biased estimates under fixed effects specification while the fixed effects estimator is consistent. At this point, Hausman’s specification test utilizes this trade-off between bias and efficiency of those two estimators when choosing an appropriate approach between fixed effects and random effects specifications.

Consistency in parameter estimation relies on a number of quite restrictive conditions which are not ensured in general when the OLS-based estimation techniques such as fixed effects and random effects estimators are used. Thus, the presence of outliers and aberrant observations may fairly distort the parameter estimates used in parametric and nonparametric testing procedures (cf. Zimmerman (1994) and Osborne and Overbay (2004)). The motivation of this study is to establish a robust version of the Hausman specification test in the presence of data contamination. To this end, we propose to use weighted likelihood based fixed effects estimator of Beyaztas and Bandyopadhyay (2020) in constructing robust Hausman test statistic, which has stable test size under null hypothesis and good power properties under alternative hypothesis.

Before describing the robust Hausman test procedure, the main concepts utilized in obtaining the weighted likelihood based estimators proposed by Beyaztas and Bandyopadhyay (2020) are presented below.

Suppose that is a random sample of vector with density function under random effects specification and is an matrix of explanatory variables with as defined previously. The joint probability density of disturbance terms is given by

where represents the variance-covariance matrix of dimension . The log-likelihood function, assuming that and terms follow normal distribution, is obtained as follows

where denotes the log-likelihood contribution for each cross-sectional unit (cf. Beyaztas and Bandyopadhyay (2020)). The maximum likelihood (ML) estimator of is the solution of usual score functions, and , defined as

where and represent the error terms and density function, respectively.

A weight function developed by Markatou et al. (1997) and Markatou et al. (1998) is expressed relying on the distribution of a chosen model for the theoretical error terms , with density , and the empirical distribution function of the observed residuals , as noted in Agostinelli and Markatou (1998). The Pearson residual used in construction of the weight function is explained in the following form

where and denote respectively a kernel density estimator based on and a model density smoothed for , and also, represents the normal kernel density with bandwidth parameter as in the study of Beyaztas and Bandyopadhyay (2020). The smoothing parameter for normal model is selected using where denotes a constant used in specifying the level downweighting factor as suggested by Markatou et al. (1998). Then, the weighted likelihood estimators of the parameter vector and error scale are the solutions of the set of weighted likelihood estimating equations (WLEEs) as follows

where denotes the weight function, in which denotes the positive part and represents a Residual Adjustment Function (RAF) (cf. Lindsay (1994)). The function that we use is Hellinger-distance based RAF to obtain the weights as in Beyaztas and Bandyopadhyay (2020). When , the weights s take the value of one, and this results in obtaining the unweighted estimates of the parameters, e.g., ML estimates (cf. Agostinelli (2002), Agostinelli and Markatou (2001) and Beyaztas and Bandyopadhyay (2020)).

The main idea behind the weighted likelihood methodology is based on using weighted score equations instead of usual score equations in estimating the parameters. The weights that distinguish ML method to weighted likelihood are calculated using a function of Pearson residuals defined above. The weight function can be considered as a concordance measure between the assumed model of the error terms and estimated model of the observed residuals, and it takes a value ranging from to . If the data set do not have any contaminated data points under the correctly specified model, the value assigned by the weight function is approximately for the Pearson residuals near to since this is an indication of the concordance between the assumed and estimated models. When the data include outlying points that are inconsistent with the assumed model, the weight function may produce small weights relying on the degree of discordance between and for those outliers which result in large Pearson residuals (cf. Markatou et al. (1997) and Beyaztas and Bandyopadhyay (2020)). Hence, the linear panel data estimators based on WLEE proposed by Beyaztas and Bandyopadhyay (2020) are robust against outliers and data contamination. The weighted likelihood based estimators are defined as in Beyaztas and Bandyopadhyay (2020), and those estimators can also be expressed as in the context of likelihood.

In the following Section 3, we provide a detailed description on Hausman specification test and introduce our proposal that is a robust version of Hausman specification test based on the weighted likelihood methodology.

3 Testing Specification

A critical consideration to distinguish between random effects and fixed effects specification depends on the existence or absence of a correlation between individual effects and the explanatory variables thus, testing this orthogonality assumption is a crucial issue as noted in Wooldridge (2002) and Baltagi (2005). A general form of the specification test, which also implies testing the orthogonality assumption, has been proposed by Hausman (1978) (cf. Holly (1982)).

Hausman’s specification test is subject to a Wald testing approach by comparing the fixed effects and random effects estimates. The fixed effects and random effects estimators, which are consistent under the null hypothesis of no correlation between individual effects and regressors, are compared in constructing the standard Hausman specification test (cf. Baltagi (2005) and Amini et al. (2012)). Under the null hypothesis of no misspecification, namely, random effects specification, the GLS method provides an asymptotically efficient estimator whereas the fixed effects estimator is not efficient even if it is consistent and unbiased (cf. Hausman (1978)). However, under the alternative hypothesis that the fixed effects specification is appropriate, the random effects estimator is inconsistent and biased because of the omitted variables while the violation of the orthogonality assumption has no effect on the fixed effects estimator as emphasized by Maddala (1971), Mundlak (1978), Hausman (1978) and Ait-Sahalia and Xiu (2019).

The Hausman test statistic is established based on a quadratic form obtained by the difference of a consistent estimator under the alternative hypothesis with an efficient estimator under the null hypothesis as noted in Holly (1982) and it is defined as

where and . Under the null hypothesis, the test statistic is asymptotically central distributed with degrees of freedom, in which is the dimension of parameter vector .

The main idea behind the test is based on the fact that both fixed effects and random effects estimators are consistent under the null hypothesis of orthogonality but random effects estimator is inconsistent under the alternative hypothesis . Thus, both estimators require to produce quitely similar estimates under and . Then, those estimates are compared utilizing Wald statistic in this testing procedure. In summary, to employ this testing procedure, two estimators and two model specifications are required to be considered as noted in Spencer and Berk (1981). One of those two estimators must be consistent and asymptotically efficient under null hypothesis but it is not consistent if the null hypothesis is not true. On the other hand, the other estimator must be consistent regardless of whether the null hypothesis is true or false but it is inefficient (asymptotically) under the null hypothesis. In this case, the estimated difference between those two estimates, a statistic naturally occuring in computing Hausman test, converges to zero when the null hypothesis is true while its probability limit is different from zero under the alternative hypothesis (cf. Hausman (1978), Spencer and Berk (1981) and Baltagi (2005)). At the end, this results in a simple test of the null hypothesis relying on the distribution of the estimated differences as noted in Spencer and Berk (1981).

In this study, we propose to use the difference between random effects and weighted likelihood based fixed effects estimators to construct weighted version of the Hausman’s specification test that is robust in the presence of outliers and asymptotically equivalent to the corresponding test.

Let denotes the weighted likelihood based fixed effects estimator (cf. Beyaztas and Bandyopadhyay (2020)). In obtaining , we use within group transformation to eliminate the individual effects. Then, the weighted squared function of the residuals defined on the mean centered data, , is attempted to be minimized as . Under some mild conditions, Beyaztas and Bandyopadhyay (2020) demonstrated that asymptotic equivalence of the weighted likelihood based estimators and corresponding OLS based estimators for random effects and fixed effects specifications as follows

using the fact that . Then, based on a sample of observations , by considering two estimators and that are both consistent and asymptotically normally distributed, with achieving the asymptotic Cramer-Rao bound, a robust weighted version of the Hausman’s specification test is constructed as

where . Under the null of , the asymptotic covariance between and is equal to zero, i.e. , since the weighted likelihood based estimators have the same limiting distributions with their traditional counterparts. Note that when the difference between weighted likelihood based estimators (i.e. ) is used in constructing robust Hausman test, this may results in obtaining distorted estimate of the difference under alternative hypothesis since the unbiasedness property of the weighted likelihood based random effects estimator is not affected by the choices of random effects and fixed effects specifications. This also contrasts with the main idea underlying the Hausman test. Thus, we only consider the weighted likelihood based fixed effects estimator to obtain robust version of the Hausman test.

4 Asymptotic Properties

In this section, we discuss the asymptotic distribution and local power properties of the weighted likelihood based Hausman test.

Arellano (1993) has obtained the Hausman test of correlated effects as a Wald test by using an augmented regression expressed as

where , and (cf. Baltagi (2005)). In this case, the Hausman alternative hypothesis can be defined as , and the Hausman’s test statistic is equivalent to a Wald statistic used to test whether (cf. Baltagi (2005)). In other words, the coefficient , which implies that the degree of correlation between the individual effects and regressors, is local to zero for fixed . Also, Holly (1982) has derived the Hausman’s specification test using the maximum likelihood method. The author has demonstrated that the asymptotic power properties of the Wald test, the Lagrange Multiplier test and the Likelihood ratio test are the same with the maximum likelihood version of the Hausman’s test under a sequence of local alternatives as noted in Honda (1987).

To start with, we consider the local asymptotic approach as in Holly (1982). Let us consider a sample of size from a parametric family of distributions with a log-likelihood based on a vector of parameters of primary interest and a vector of nuisance parameters . The null and alternative hypotheses can be expressed in a general form as follows, respectively.

-

•

-

•

where is a vector of parameters under a sequence of local alternative hypotheses which have the form of where as noted in Honda (1987), and represents a vector of parameters as defined earlier. Holly (1982) has derived the distribution of the test statistic for these sequences of alternative hypotheses when . The distribution under the null of is obtained for (cf. Holly (1982)).

Let and , respectively, denote a combined vector of the parameters and the “true vector parameter”. By using the following definitions of Holly (1982) and Honda (1987),

the constrained and unconstrained maximum likelihood estimators of are obtained as the solutions of and , respectively, as follows

where and denote the compact subsets of and . Then, and are respectively obtained from the solutions of and for large sample size .

Holly (1982) and Honda (1987) have derived the following likelihood equations about the parameter vector

where denote a information matrix partitioned into four submatrices , , and of dimensions , , , and , respectively, and represents the convergence in probability of the difference between two sides of the equation. We assume that the information matrix is positive definite as in Honda (1987).

Based on the above, the Hausman’s test statistic can be expressed in following form as in Holly (1982), Honda (1987) and Hausman and Taylor (1981)

| (4.6) |

where the sign represents the generalized inverse of the matrix and .

When the some regularity conditions hold, Holly (1982) and Hausman and Taylor (1981) have demonstrated that the Hausman’s test statistic has an asymptotic non-central distribution with degrees of freedom equal to the rank of under local alternatives , and the non-centrality parameter is defined as

where . Also, and are assumed to be non-singular matrices (cf. Honda (1987)).

Honda (1987) showed that the Hausman’s test statistic given in Equation 4.6, which have the same asymptotic properties with the Wald test and Lagrange Multiplier test, has distribution with degrees of freedom under the condition when the Moore-Penrose inverse is used as the generalized inverse in constructing the Hausman’s statistic.

Remark 1.

Under the conditions A1.-A7. in Beyaztas and Bandyopadhyay (2020), based on asymptotic equivalence of the weighted likelihood based fixed effects estimator and its conventional counterpart, the weighted likelihood based Hausman test statistic asymptotically follows a central distribution with degrees of freedom under the null hypothesis . The asymptotic distribution under local alternatives is a non-central distribution with a noncentrality parameter in Equation 4 and same degrees of freedom when the condition holds. (cf. Agostinelli and Markatou (2001) and Beyaztas and Bandyopadhyay (2020))

5 Numerical Results

In this section we present the results obtained from an extensive simulation study to investigate the performances of the proposed and conventional test procedures. The following simulations are conducted to explore the test sizes and power properties of the proposed WLEE based Hausman specification test under different sample sizes and different types of outliers. All calculations have been carried out using R 3.6.0. on an IntelCore i7 6700HQ 2.6 GHz PC. (The codes can be obtained from the author upon request.)

In our experiments, the data under the null hypothesis are generated from the following random effects model to study the level of the tests

where , and . The vector of parameters set equal to .

To examine the power properties of the robust and conventional Hausman specification tests under the alternative hypothesis, the individual-specific effects in the above data generating process are generated depending on the regressors through as follows

where .

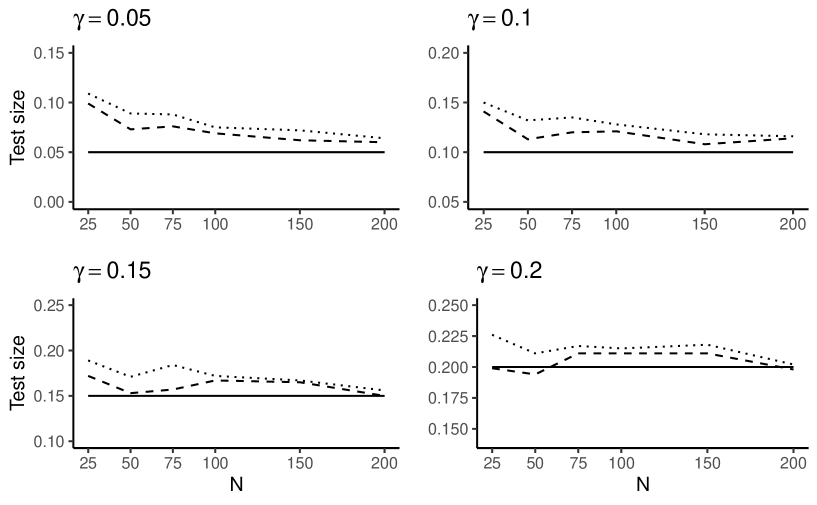

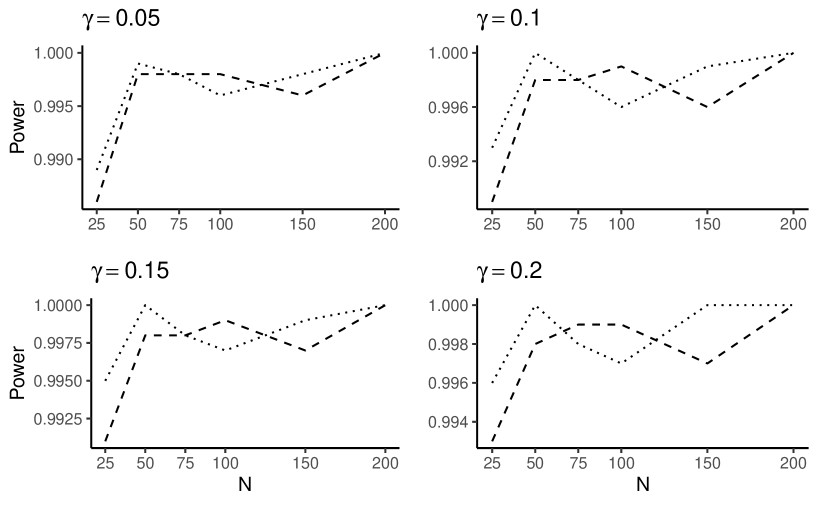

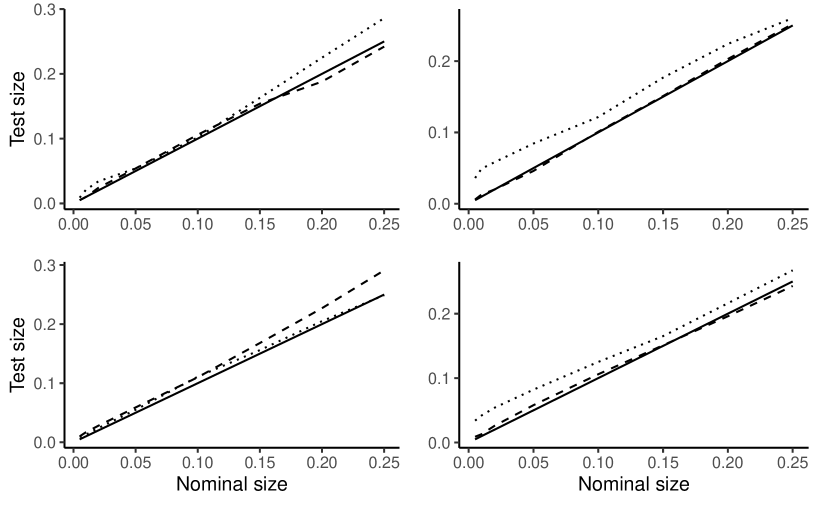

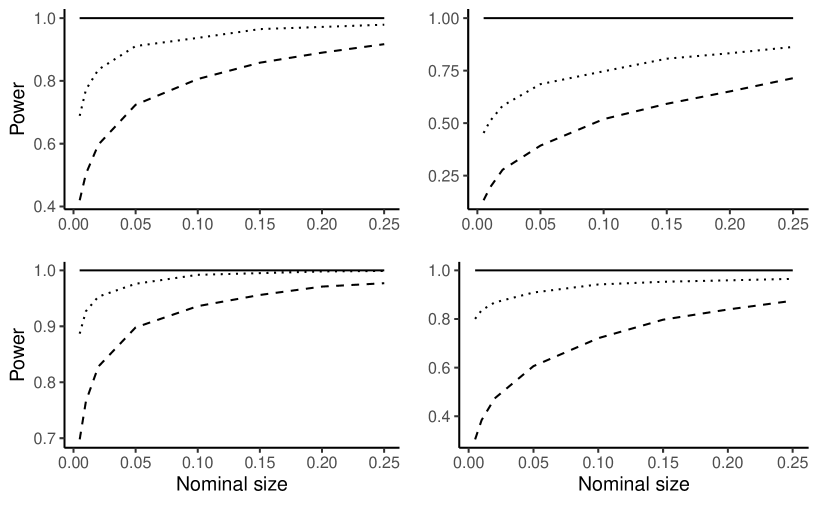

Throughout the experiments, the number of Monte Carlo replications is set at . To compare the performances of Hausman specification test and the proposed weighted likelihood based specification test, we calculate the percentage of rejections based on generated samples under null hypothesis. Figure 1 illustrates the empirical test sizes of conventional and robust test procedures at different values of nominal sizes for the increasing number of cross-sectional units by keeping time period fixed at . The empirical sizes of both tests has a tendency to exceed their nominal sizes especially when the cross-sectional dimension is small. Although under the null hypothesis, the weighted likelihood based specification test has a greater percentage of rejections than that of its conventional counterpart, both tests produce quite similar empirical sizes as increases. Note that the differences between empirical sizes of two procedures converges to zero when at a faster rate compared to since the weighted likelihood based specification test is a root- consistent procedure. Thus, we only consider the short micro panels in our simulation experiments. We also calculate the percentage of rejections for the datasets generated under alternative hypothesis to compare the Hausman test with its weighted likelihood version in terms of their power. Figure 2 present the power of both testing procedures when the number of time periods is fixed at . It is clear that both procedures exhibit quite similar power performances and their power values are very close to one. It can further be seen that the power of both tests increases with the increasing sample size, in general.

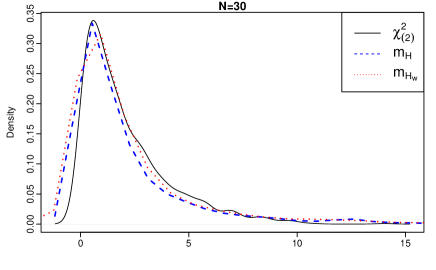

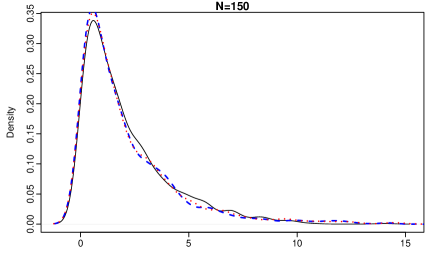

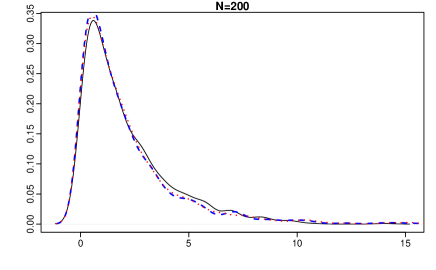

Moreover, in Figure 3, we plot the densities of Hausman test statistic and its weighted version based on simulated samples under null hypothesis, and we generate data from a chi-square distribution with two degrees of freedom with non-centrality parameter to compare the distributions of testing procedures with the asymptotic distribution. In this figure, the lines representing the distributions of those test statistics overlap as increases since the proposed weighted likelihood based test is asymptotically consistent with the original Hausman specification test.

The main objective is to develop a robust testing procedure, which is asymptotically equivalent to the corresponding test, in the sense of preserving size and power in the presence of contaminated datasets. Thus, to investigate the robustness performances of the proposed testing procedure, Monte Carlo experiments are carried out under two contamination schemes and two levels of contamination. Throughout the simulations, we choose the panel size consisting of a total of observations with cross-sectional size and time period . Two percentages of contamination considered are 5% and 10% by setting the number of outliers as and . To generate contaminated datasets, outliers are inserted into the data by random and concentrated contamination (cf. Bramati and Croux (2007)). In case of random contamination, the outlying data points are randomly allocated over all observations while at least a half of observations within cross-sectional units are replaced by the outliers to obtain concentrated contamination (cf. Bramati and Croux (2007) and Beyaztas and Bandyopadhyay (2020)). In our contamination schemes, random vertical outliers () are generated by replacing randomly selected original values of the response variable with the observations from an Uniform distribution . To create concentrated vertical outliers (), the observations from an Uniform distribution are substituted in the randomly selected blocks of the original values of response variable. Figure 4 displays the empirical test sizes of conventional and the proposed tests under random and concentrated contamination for different values of nominal sizes . Under the null hypothesis, the percentages of rejections obtained for both testing procedures are very close to the nominal sizes when the data are contaminated by random and concentrated vertical outliers at 5% contamination. However, the proposed test has a slight tendency to overestimate its nominal size at 10% contamination under both types of contamination since there is a trade-off between test size and power, and a large test size is an indicator of gaining power of the test. Furthermore, Figure 5 indicate the power performances of those testing procedures in the presence of random and concentrated vertical outliers. For all considered type and level of contamination, the weighted likelihood based specification test exhibit improved performances over the traditional one in terms of power.

6 Case Study

In this section, we use an economic growth data to illustrate the supremacy of the proposed weighted likelihood based specification test over the traditional testing procedure. The dataset, an annual sample of 30 OECD countries running over the period 2010 to 2019 (), are obtained from OECD databases. For these data, the following panel data regression model is constructed based on the conventional neoclassical one-sector aggregate production function (cf. Kasperowicz (2014))

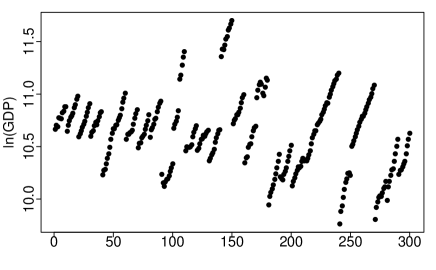

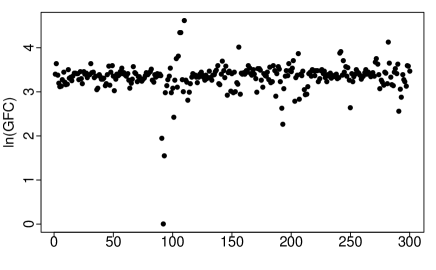

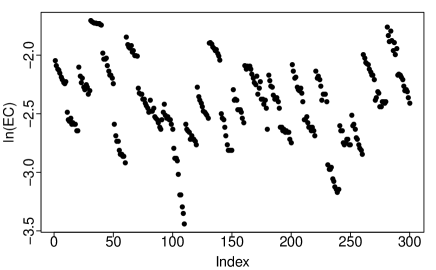

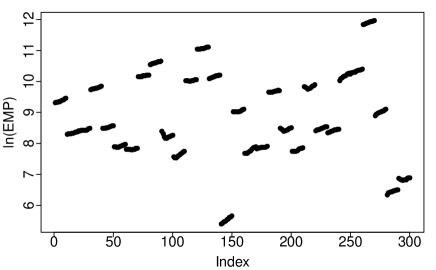

where denote the gross domestic product per capita as a response variable, , and , respectively, represent the gross fixed capital (also called investment), total energy consumption and total employment rate as explanatory variables. Kasperowicz (2014) demonstrates the positive relation between economic growth and energy consumption based on the data collected for 12 European countries over 13 years and the details on this model can be found in Kasperowicz (2014). Figure 6 presents the scatter plots of the log-transformed versions of the , , and variables. It is evident from the scatterplots that all the log-tranformed variables include outliers and those outliers seems to have a clustered structure particularly in , and .

The Hausman test and weighted likelihood based specification procedure are applied to the data and the estimated test statistics of both testing procedures are reported in Table 1. In this table, the result of Hausman specification test (with ) indicates that the orthogonality hypothesis of the individual-specific effects and the explanatory variables is not rejected at the significance level and the random-effects specification is adequate. On the other hand, the calculated of the proposed weighted likelihood based specification test suggests that the fixed-effects specification is appropriate. Next, we calculate the residual sum of squares () and the coefficient of determination under fixed effects and random effects specifications to choose appropriate approach between fixed effects and random effects specifications. As shown in Table 1, the calculated value under fixed effects model is considerably less than that of random effects model and is almost twice as much . Also, higher value is obtained when the fixed effects specification is chosen. All the results indicate that the fixed effects are present in the panel regression model, and the weighted likelihood based specification test produce more reliable and stable results than those of standard Hausman test in the presence of outliers.

| 6.6635 | 10.0374 | 0.6269 | 1.1962 | 0.8416 | 0.7208 |

| (0.0834) | (0.0182) |

7 Conclusions

The presence of individual and clustered outliers in panel data may affect the stability and power properties of the testing procedures used in model specification. The literature considering the robustness of testing procedures is available in the context of time series and regression models. However, the amount of works on the robustness of specification testing in panel data models is quite limited. Thus, in this paper, an asymptotically valid, robust specification test procedure has been proposed in linear panel data models. The proposed specification test uses the difference between conventional random effects estimator and the weighted likelihood based fixed effects estimator proposed by Beyaztas and Bandyopadhyay (2020) in construction of the test statistic. The stability of the level of the proposed test and its power properties are examined via extensive simulation studies and an economic growth data, and the results obtained from the proposed testing procedure are compared with the results of Hausman’s specification test. Also, the asymptotic properties of the proposed procedure are investigated based on the properties of the weighted likelihood based estimators. Our records demonstrate that the proposed test has asymptotically same distribution as that of Hausman’s test under the null hypothesis and performs well when the outliers are not presented in the data. However, the proposed specification test exhibits improved performances over the conventional specification test in terms of power of the tests when the data include random and clustered outliers. The prominent result produced by the proposed testing procedure is that it is powerful in detecting the potential correlation between the individual effects and regressors in the presence of contaminated data.

References

- (1)

- Agostinelli (2002) Agostinelli, C. (2002), ‘Robust stepwise regression’, Journal of Applied Statistics 29(6), 825–840.

- Agostinelli and Markatou (1998) Agostinelli, C. and Markatou, M. (1998), ‘A one-step robust estimator for regression based on the weighted likelihood reweighting scheme’, Statistics & Probability Letters 37(4), 341–350.

- Agostinelli and Markatou (2001) Agostinelli, C. and Markatou, M. (2001), ‘Test of hypotheses based on the weighted likelihood methodology’, Statistica Sinica 11(2), 499–514.

- Ahn and Low (1996) Ahn, S. C. and Low, S. (1996), ‘A reformulation of the hausman test for regression models with pooled cross-section-time-series data’, Journal of Econometrics 71(1-2), 309–319.

- Ait-Sahalia and Xiu (2019) Ait-Sahalia, Y. and Xiu, D. (2019), ‘A hausman test for the presence of market microstructure noise in high frequency data’, Journal of Econometrics 211(1), 176–205.

- Amini et al. (2012) Amini, S., Delgado, M. S., Henderson, D. J. and Parmeter, C. F. (2012), Fixed vs random: The hausman test four decades later, in B. H. Baltagi, H. R. Carter, W. K. Newey and H. L. White, eds, ‘Advances in Econometrics’, Vol. 29, Emerald Group Publishing Limited, Bingley, pp. 497–513.

- Arellano (1993) Arellano, M. (1993), ‘On the testing of correlated effects with panel data’, Journal of Econometrics 59(1-2), 87–97.

- Baltagi (2005) Baltagi, B. H. (2005), Econometric Analysis of Panel Data, John Wiley and Sons, Chichester.

- Beyaztas and Bandyopadhyay (2020) Beyaztas, B. H. and Bandyopadhyay, S. (2020), ‘Robust estimation for linear panel data models’, Statistics in Medicine 39(29), 4421–4438.

- Bole and Rebec (2013) Bole, V. and Rebec, P. (2013), ‘Bootstrapping the hausman test in panel data models’, Communications in Statistics-Simulation and Computation 42(3), 650–670.

- Bramati and Croux (2007) Bramati, M. C. and Croux, C. P. (2007), ‘Robust estimators for the fixed effects panel data model’, Econometric Journal 10(3), 521–540.

- Bălă and Prada (2018) Bălă, R. M. and Prada, E. M. (2018), ‘Migration and private consumption in europe: a panel data analysis’, Procedia Economics and Finance 10, 141–149.

- Cameron and Trivedi (2009) Cameron, A. C. and Trivedi, P. K. (2009), Microeconometrics Using Stata, Stata Press, Texas.

- Chen et al. (2018) Chen, J., Yue, R. and Wu, J. (2018), ‘Hausman-type tests for individual and time effects in the panel regression model with incomplete data’, Journal of the Korean Statistical Society 47(3), 347–363.

- Croissant and Millo (2008) Croissant, Y. and Millo, G. (2008), ‘Panel data econometrics in r: The plm package’, Journal of Statistical Software 27(2), 1–43.

- Frondel and Vance (2010) Frondel, M. and Vance, C. (2010), ‘Fixed, random, or something in between? a variant of hausman’s specification test for panel data estimators’, Economics Letters 107(3), 327–329.

- Greene (2003) Greene, W. H. (2003), Econometric Analysis, Prentice Hall, New Jersey.

- Hausman (1978) Hausman, J. A. (1978), ‘Specification tests in econometrics’, Econometrica 46(6), 1251–1271.

- Hausman and Taylor (1981) Hausman, J. A. and Taylor, W. E. (1981), ‘Panel data and unobservable individual effects’, Econometrica 49(6), 1377–1398.

- Herwartz and Neumann (2007) Herwartz, H. and Neumann, M. H. (2007), ‘A robust bootstrap approach to the hausman test in stationary panel data models’, Economics working paper 2007-29 .

- Holly (1982) Holly, A. (1982), ‘A remark on hausman’s specification test’, Econometrica 50(3), 749–759.

- Honda (1987) Honda, Y. (1987), ‘On hausman’s specification test’, The Economic Studies Quarterly 38(2), 172–183.

- Jirata et al. (2016) Jirata, M. T., Cheruiyot, C. and Romanus, O. (2016), Estimation of Panel Data Models with Individual Effects, LAP LAMBERT Academic Publishing.

- Joshi and Wooldridge (2017) Joshi, R. and Wooldridge, J. M. (2017), Specification tests in unbalanced panels with endogeneity.

- Kasperowicz (2014) Kasperowicz, R. (2014), ‘Economic growth and energy consumption in 12 european countries: a panel data approach’, Journal of International Studies 7(3), 112–122.

- Kennedy (2003) Kennedy, P. (2003), A Guide to Econometrics, The MIT Press, Cambridge.

- Lindsay (1994) Lindsay, B. (1994), ‘Efficiency versus robustness: The case for minimum hellinger distance and related methods’, Annals of Statistics 22(2), 1018–1114.

- Maddala (1971) Maddala, G. S. (1971), ‘The use of variance components models in pooling cross section and time series data’, Econometrica 39(2), 341–358.

- Markatou et al. (1997) Markatou, M., Basu, A. and Lindsay, B. (1997), ‘Weighted likelihood estimating equations: The discrete case with applications to logistic regression’, Journal of Statistical Planning and Inference 57(2), 215–232.

- Markatou et al. (1998) Markatou, M., Basu, A. and Lindsay, B. (1998), ‘Weighted likelihood estimating equations with a bootstrap root search’, Journal of the American Statistical Association 93(442), 740–750.

- Metcalf (1996) Metcalf, G. E. (1996), ‘Specification testing in panel data with instrumental variables’, Journal of Econometrics 71(1-2), 291–307.

- Mundlak (1978) Mundlak, Y. (1978), ‘On the pooling of time series and cross section data’, Econometrica 46(1), 69–85.

- Osborne and Overbay (2004) Osborne, J. W. and Overbay, A. (2004), ‘The power of outliers (and why researchers should always check for them)’, Practical Assessment, Research and Evaluation 9(6), 1–12.

- Spencer and Berk (1981) Spencer, D. E. and Berk, K. N. (1981), ‘A limited information specification test’, Econometrica 49(4), 1079–1085.

- White (1984) White, H. (1984), Asymptotic Theory for Econometricians, Academic Press, Orlando, FL.

- Wooldridge (2002) Wooldridge, J. M. (2002), Econometric Analysis of Cross Section and Panel Data, The MIT Press, Cambridge.

- Zhang (2010) Zhang, L. (2010), The use of panel data models in higher education policy studies, in J. Smart, ed., ‘Higher Education: Handbook of Theory and Research’, Emerald Group Publishing Limited, Dordrecht.

- Zimmerman (1994) Zimmerman, D. W. (1994), ‘A note on the influence of outliers on parametric and nonparametric tests’, The Journal of General Psychology 121(4), 391–401.